pt indosat tbk 9m 2013 results · 2015-11-12 · indosat ir - new template v23 1220.pptx 26 indosat...

TRANSCRIPT

1 Indosat IR - New Template v23 1220.pptx

1

PT Indosat Tbk 9M 2013 Results

2 Indosat IR - New Template v23 1220.pptx 2 Indosat IR - New Template v23 1220.pptx

2 Indosat Presentation 9M 2013

2

Agenda

Financial and Operational Results

Management Focus

Supplemental Information

3 Indosat IR - New Template v23 1220.pptx

3

Financial and Operational Highlights

4 Indosat IR - New Template v23 1220.pptx 4 Indosat IR - New Template v23 1220.pptx

4 Indosat Presentation 9M 2013

4

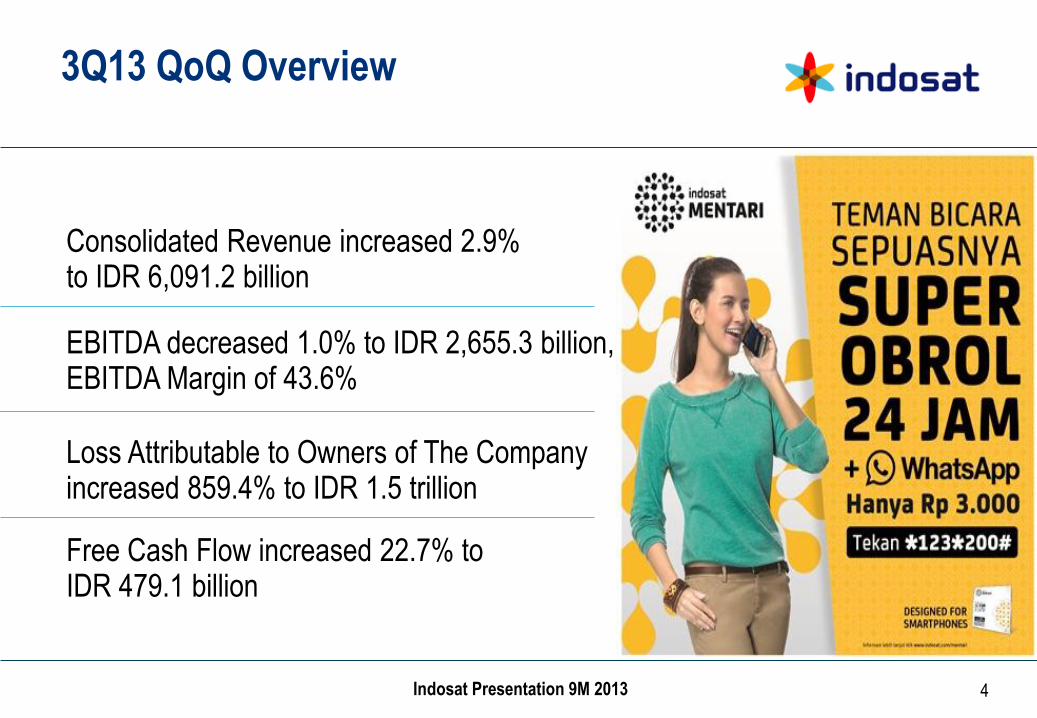

3Q13 QoQ Overview

Consolidated Revenue increased 2.9% to IDR 6,091.2 billion

EBITDA decreased 1.0% to IDR 2,655.3 billion, EBITDA Margin of 43.6%

Loss Attributable to Owners of The Company increased 859.4% to IDR 1.5 trillion

Free Cash Flow increased 22.7% to IDR 479.1 billion

5 Indosat IR - New Template v23 1220.pptx 5 Indosat IR - New Template v23 1220.pptx

5 Indosat Presentation 9M 2013

5

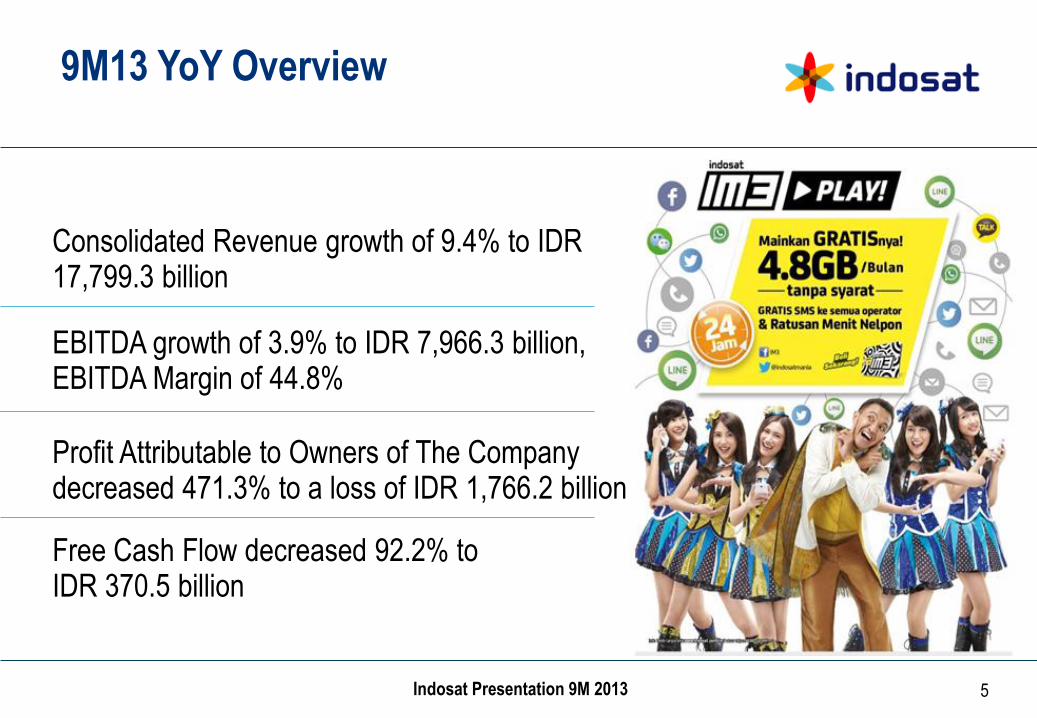

9M13 YoY Overview

Consolidated Revenue growth of 9.4% to IDR 17,799.3 billion

EBITDA growth of 3.9% to IDR 7,966.3 billion, EBITDA Margin of 44.8%

Profit Attributable to Owners of The Company decreased 471.3% to a loss of IDR 1,766.2 billion

Free Cash Flow decreased 92.2% to IDR 370.5 billion

6 Indosat IR - New Template v23 1220.pptx 6 Indosat IR - New Template v23 1220.pptx

6 Indosat Presentation 9M 2013

6

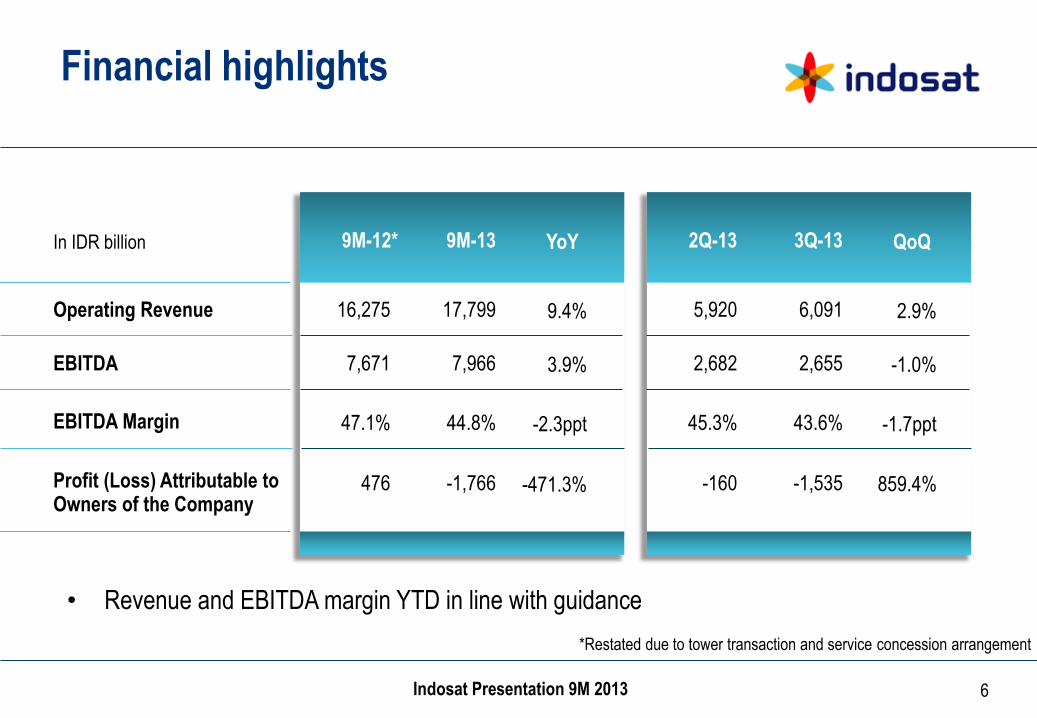

Financial highlights

16,275 Operating Revenue

EBITDA

EBITDA Margin

Profit (Loss) Attributable to Owners of the Company

17,799

9M-12* 9M-13 YoY

9.4%

7,671 7,966 3.9%

47.1% 44.8% -2.3ppt

476 -1,766 -471.3%

5,920 6,091

2Q-13 3Q-13 QoQ

2.9%

2,682 2,655 -1.0%

45.3% 43.6% -1.7ppt

-160 -1,535 859.4%

In IDR billion

• Revenue and EBITDA margin YTD in line with guidance

*Restated due to tower transaction and service concession arrangement

7 Indosat IR - New Template v23 1220.pptx 7 Indosat IR - New Template v23 1220.pptx

7 Indosat Presentation 9M 2013

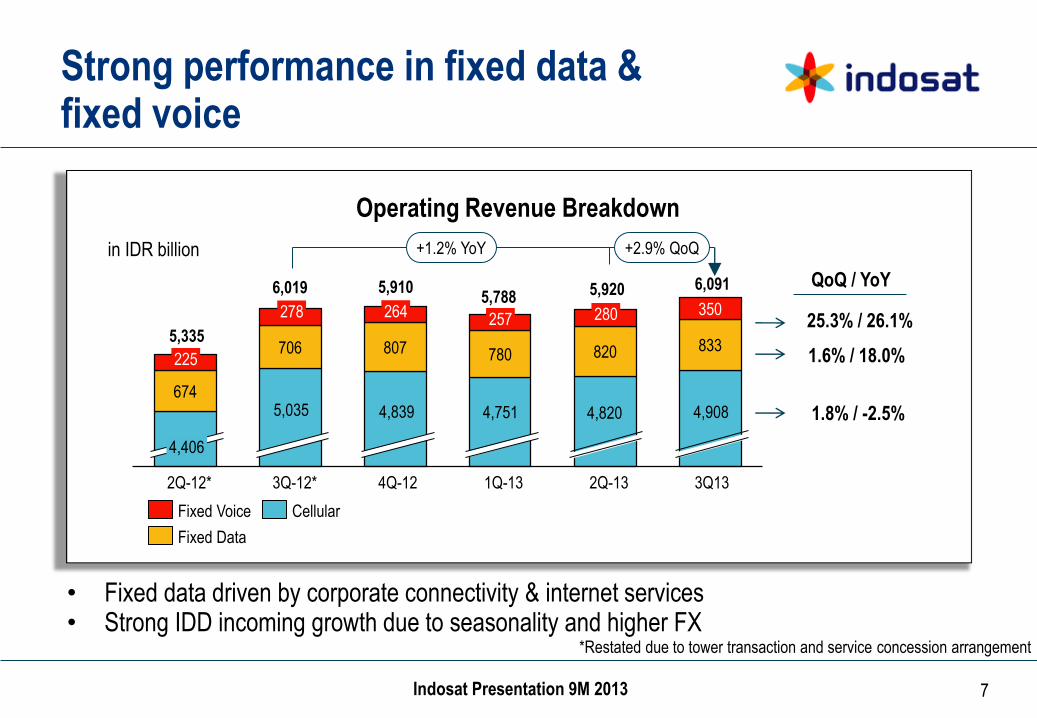

674

706 807 780 820 833

350

7

Strong performance in fixed data & fixed voice

Operating Revenue Breakdown

in IDR billion

2Q-13

+2.9% QoQ +1.2% YoY

3Q13

6,091 5,920

1Q-13 4Q-12 3Q-12* 2Q-12*

Cellular

Fixed Data

Fixed Voice

25.3% / 26.1%

1.6% / 18.0%

1.8% / -2.5%

• Fixed data driven by corporate connectivity & internet services • Strong IDD incoming growth due to seasonality and higher FX

QoQ / YoY

5,335

6,019 5,910 5,788

280 257 264

4,751 4,839

4,406

5,035 4,908 4,820

225

278

*Restated due to tower transaction and service concession arrangement

8 Indosat IR - New Template v23 1220.pptx 8 Indosat IR - New Template v23 1220.pptx

8 Indosat Presentation 9M 2013

8

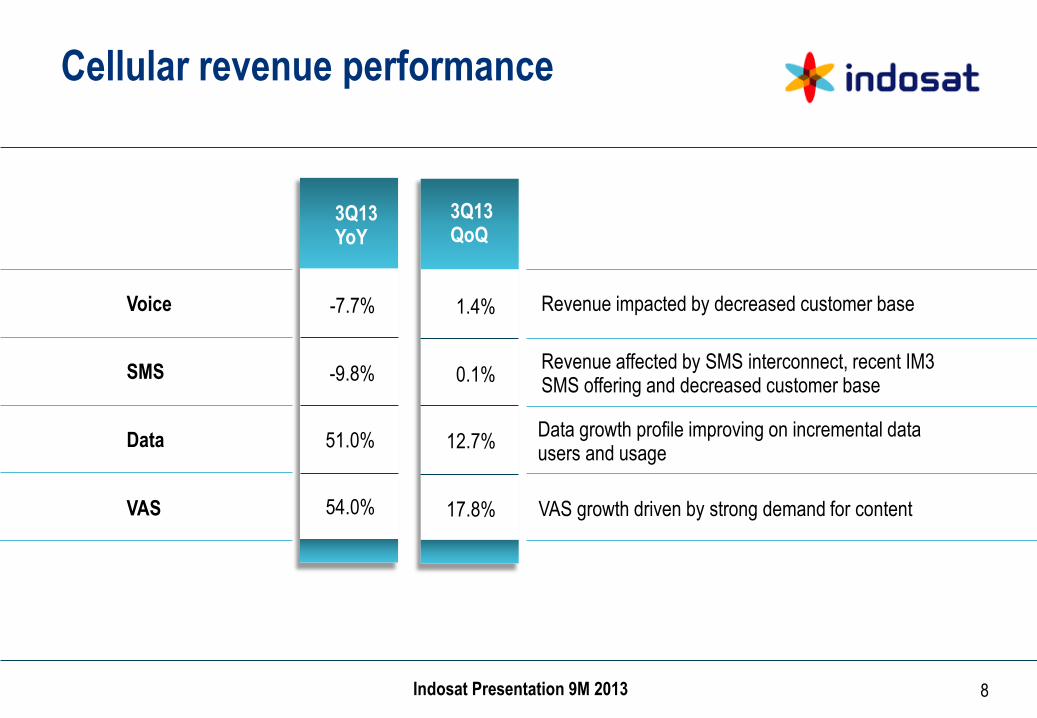

Cellular revenue performance

Voice

SMS

Data

VAS

-7.7%

3Q13 YoY

-9.8%

51.0%

54.0%

1.4%

3Q13 QoQ

0.1%

12.7%

17.8%

Revenue impacted by decreased customer base

Revenue affected by SMS interconnect, recent IM3 SMS offering and decreased customer base

Data growth profile improving on incremental data users and usage

VAS growth driven by strong demand for content

9 Indosat IR - New Template v23 1220.pptx 9 Indosat IR - New Template v23 1220.pptx

9 Indosat Presentation 9M 2013

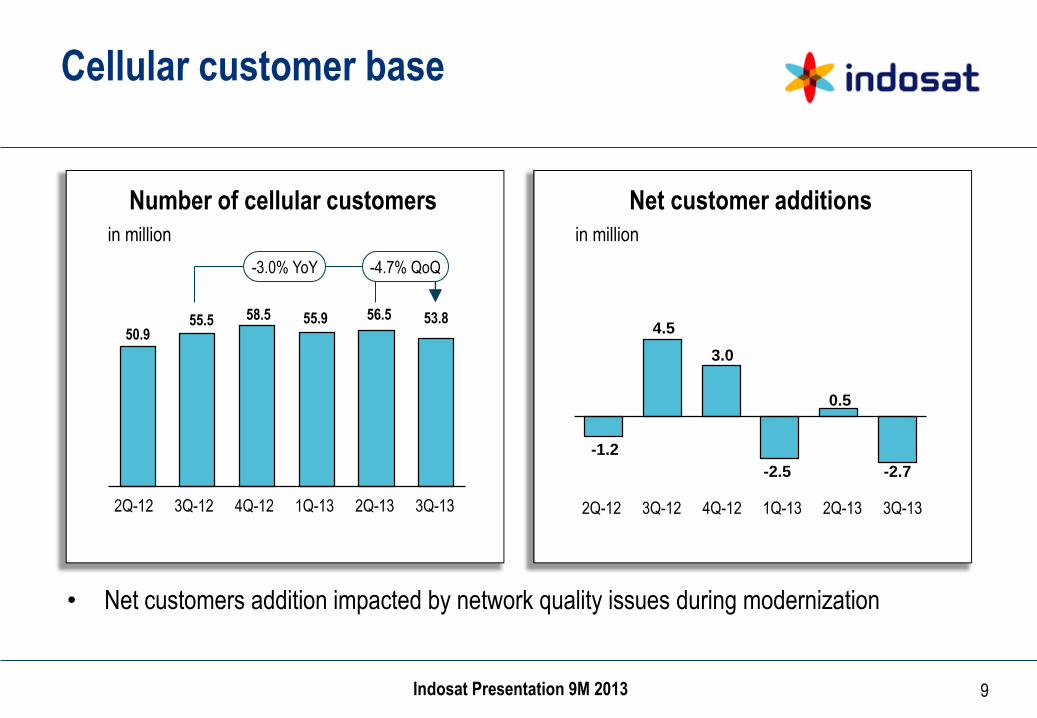

50.9 55.5 58.5 55.9 56.5 53.8

9

Cellular customer base

3Q-13

-3.0% YoY -4.7% QoQ

2Q-13 1Q-13 4Q-12 3Q-12 2Q-12

Number of cellular customers

in million

3Q-13 2Q-12 2Q-13 1Q-13 4Q-12 3Q-12

Net customer additions

in million

• Net customers addition impacted by network quality issues during modernization

-1.2

4.5

3.0

-2.5

0.5

-2.7

10 Indosat IR - New Template v23 1220.pptx 10 Indosat IR - New Template v23 1220.pptx

10 Indosat Presentation 9M 2013

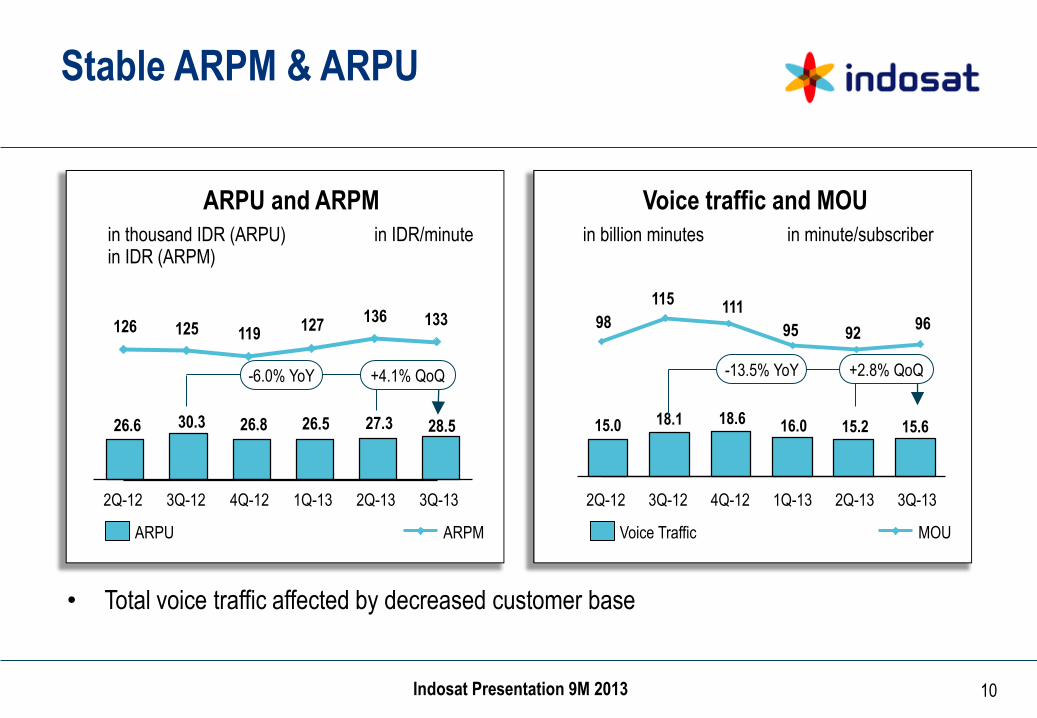

98

115 111

95 92 96 126 125 119

127 136 133

15.0 18.1 18.6 16.0 15.2 15.6

10

Stable ARPM & ARPU

Voice traffic and MOU

-13.5% YoY

3Q-13

+2.8% QoQ

2Q-13 1Q-13 4Q-12 3Q-12 2Q-12

Voice Traffic

in billion minutes in minute/subscriber

MOU

• Total voice traffic affected by decreased customer base

ARPU and ARPM

26.6 30.3 26.8 26.5 27.3 28.5

2Q-13 1Q-13 4Q-12 3Q-12 2Q-12

+4.1% QoQ -6.0% YoY

3Q-13

ARPU

in thousand IDR (ARPU) in IDR (ARPM)

ARPM

in IDR/minute

11 Indosat IR - New Template v23 1220.pptx 11 Indosat IR - New Template v23 1220.pptx

11 Indosat Presentation 9M 2013

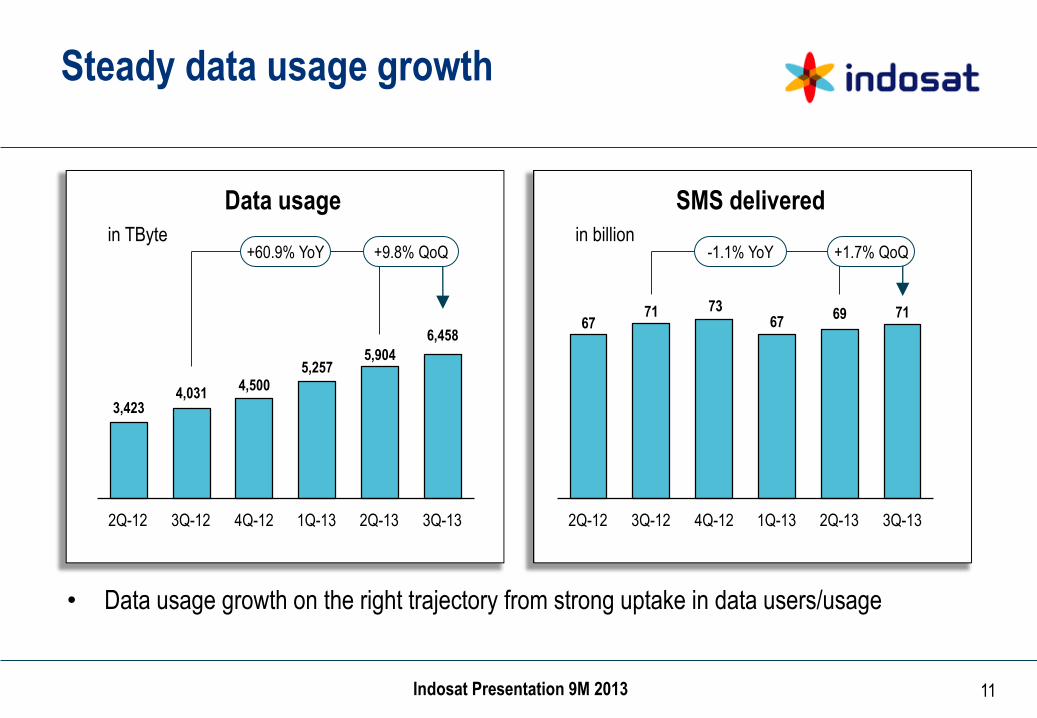

67 71 73

67 69 71

3,423 4,031

4,500 5,257

5,904

6,458

11

Steady data usage growth

Data usage

in TByte +9.8% QoQ +60.9% YoY

3Q-13 2Q-13 1Q-13 4Q-12 3Q-12 2Q-12

SMS delivered

in billion -1.1% YoY

3Q-13 2Q-13

+1.7% QoQ

1Q-13 4Q-12 3Q-12 2Q-12

• Data usage growth on the right trajectory from strong uptake in data users/usage

12 Indosat IR - New Template v23 1220.pptx 12 Indosat IR - New Template v23 1220.pptx

12 Indosat Presentation 9M 2013

12

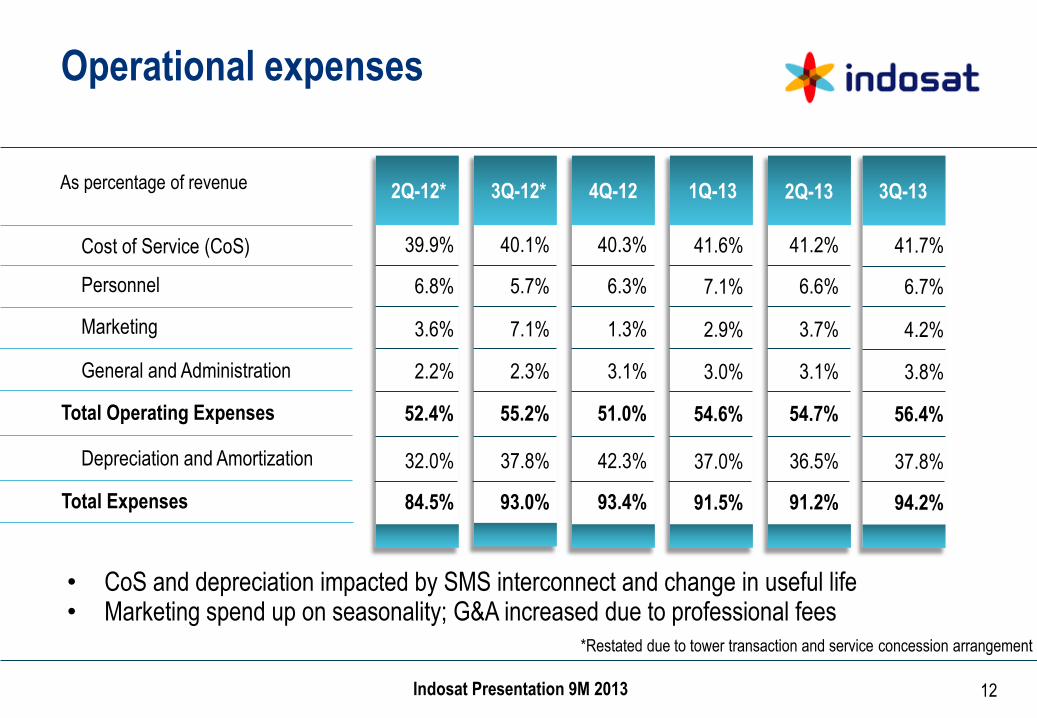

Operational expenses

Cost of Service (CoS)

Depreciation and Amortization

Personnel

Marketing

As percentage of revenue

General and Administration

Total Expenses

2Q-12* 3Q-12*

39.9%

4Q-12

32.0%

6.8%

3.6%

2.2%

84.5%

40.1%

1Q-13

37.8%

5.7%

7.1%

2.3%

93.0%

• CoS and depreciation impacted by SMS interconnect and change in useful life • Marketing spend up on seasonality; G&A increased due to professional fees

40.3%

42.3%

6.3%

1.3%

3.1%

93.4%

Total Operating Expenses 52.4% 55.2% 51.0%

3Q-13

41.2%

36.5%

6.6%

3.7%

3.1%

91.2%

54.7%

*Restated due to tower transaction and service concession arrangement

2Q-13

41.6%

37.0%

7.1%

2.9%

3.0%

91.5%

54.6%

41.7%

37.8%

6.7%

4.2%

3.8%

94.2%

56.4%

13 Indosat IR - New Template v23 1220.pptx 13 Indosat IR - New Template v23 1220.pptx

13 Indosat Presentation 9M 2013

2,537 2,824 2,893

2,629 2,682 2,655

13

EBITDA performance

EBITDA and EBITDA margin

-1.0% QoQ -6.0% YoY

3Q-13 2Q-13 1Q-13 4Q-12 3Q-12* 2Q-12*

EBITDA

in IDR billion

45.4% 49.0%

46.9% 47.6%

EBITDA Margin

• 3Q EBITDA (YoY) impacted by softer revenue growth

• YTD EBITDA margin in line with guidance

45.3% 43.6%

*Restated due to tower transaction and service concession arrangement

14 Indosat IR - New Template v23 1220.pptx 14 Indosat IR - New Template v23 1220.pptx

14 Indosat Presentation 9M 2013

Normalized net profit bridge

1,047

476

-1,766

-1,766

674

1,608

832

14

Normalized net profit*

Net profit

-471.3% YoY -54.6% YoY

9M-13 9M-12** 9M-11**

in IDR billion in IDR billion 9M13

• Net profit affected by substantial FX loss and change in network equipment useful life

Normalized Net– FX Loss Change in

Useful Life

Reported

* Net profit is Profit Attribution to Owners of the Company ** Restated due to tower transaction and service concession arrangement

15 Indosat IR - New Template v23 1220.pptx 15 Indosat IR - New Template v23 1220.pptx

15 Indosat Presentation 9M 2013

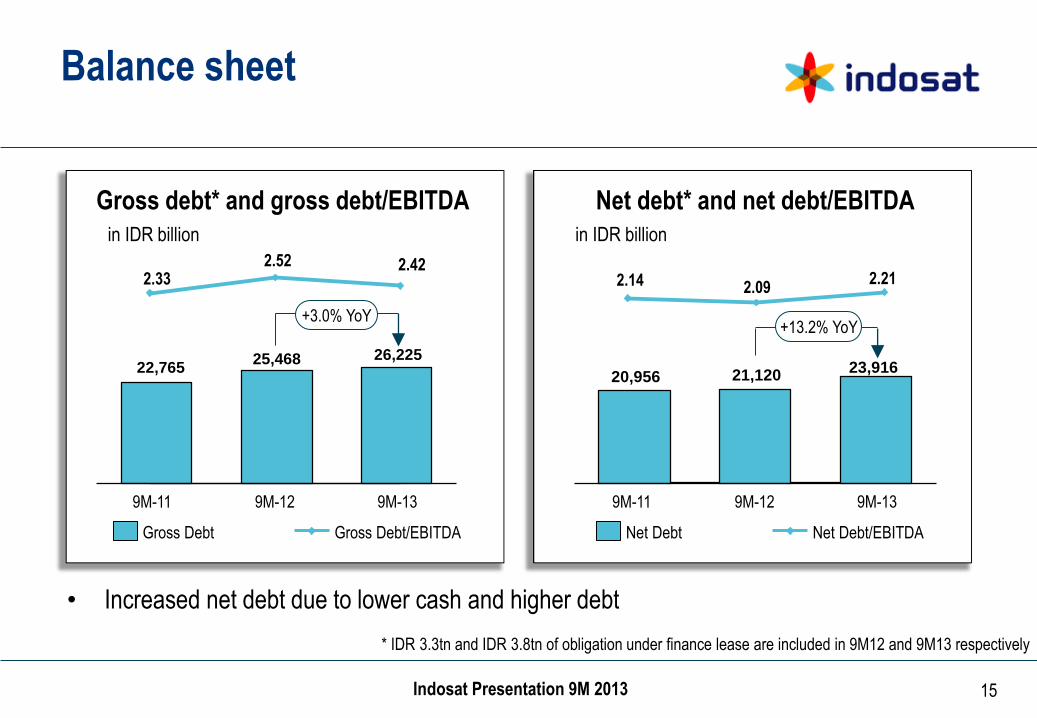

2.33 2.52 2.42

22,765 25,468 26,225

2.14 2.09 2.21

20,956 21,120 23,916

15

Balance sheet

Gross debt* and gross debt/EBITDA Net debt* and net debt/EBITDA

9M-12 9M-11 9M-13

+3.0% YoY

Gross Debt

in IDR billion

Gross Debt/EBITDA

9M-13 9M-11 9M-12

+13.2% YoY

Net Debt Net Debt/EBITDA

in IDR billion

• Increased net debt due to lower cash and higher debt

* IDR 3.3tn and IDR 3.8tn of obligation under finance lease are included in 9M12 and 9M13 respectively

16 Indosat IR - New Template v23 1220.pptx 16 Indosat IR - New Template v23 1220.pptx

16 Indosat Presentation 9M 2013

1,731 1,334 1,332

2,612 2,750 2,516

32.5

22.2 22.4

45.1 46.5 41.3

16

Free Cash Flow

Free cash flow

in IDR billion

1,137

3,528

-447 -499

390 479

3Q-13 2Q-13 1Q-13 4Q-12 3Q-12* 2Q-12*

Capex and Capex/Revenue

3Q-13 2Q-13 1Q-12 4Q-12 3Q-12 2Q-12

Capex

in IDR billion

Capex/Revenue

• Network modernization driving higher cash capex

*Restated due to tower transaction and service concession arrangement

17 Indosat IR - New Template v23 1220.pptx 17 Indosat IR - New Template v23 1220.pptx

17 Indosat Presentation 9M 2013

774

661 622 624

404 346

17

Network roll-out

Number of BTS

16,898 17,211 17,334 17,452 17,668 18,214

4,141 4,431 4,596 4,645 4,781 4,993

+3.4% QoQ +7.2% YoY

3Q-13

21,930

2Q-13

21,642

1Q-13

21,039

4Q-12 3Q-12 2Q-12

2G 3G

Cellular Revenue per BTS

In IDR million

9M 2013 9M 2012

XL

Indosat

Telkomsel

• Network modernization program mainly focusing on existing footprint in key market areas • Successfully launched 3G 900/2100 HSDPA+ in South Bali

22,097 22,449 23,207

18 Indosat IR - New Template v23 1220.pptx 18 Indosat IR - New Template v23 1220.pptx

18 Indosat Presentation 9M 2013

18

Q3 in summary

19 Indosat IR - New Template v23 1220.pptx

19

Management Focus and Key updates

20 Indosat IR - New Template v23 1220.pptx 20 Indosat IR - New Template v23 1220.pptx

20 Indosat Presentation 9M 2013

20

Near term management focus

Execute well on network modernization and improve network quality

Drive strong uptake and usage of our data services

Improve cost efficiencies to enable investments in growth

Transform culture with focus on quick wins

21 Indosat IR - New Template v23 1220.pptx 21 Indosat IR - New Template v23 1220.pptx

21 Indosat Presentation 9M 2013

21

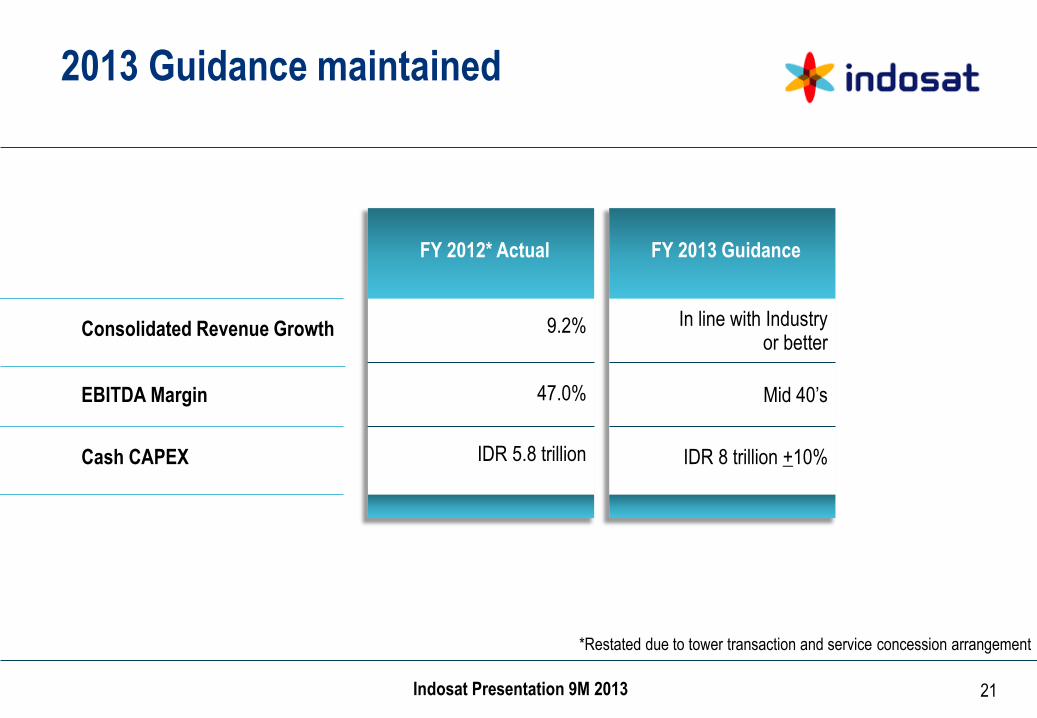

2013 Guidance maintained

FY 2012* Actual FY 2013 Guidance

Consolidated Revenue Growth 9.2% In line with Industry or better

EBITDA Margin 47.0% Mid 40’s

Cash CAPEX IDR 5.8 trillion IDR 8 trillion +10%

*Restated due to tower transaction and service concession arrangement

22 Indosat IR - New Template v23 1220.pptx 22 Indosat IR - New Template v23 1220.pptx

22 Indosat Presentation 9M 2013

22

Thank You

Any further questions?

Upcoming events FY 2013 Results

Indosat Investor Relations Jl. Medan Merdeka Barat No. 21 Jakarta - 10110 Tel: +62 21 30442615 [email protected]

23 Indosat IR - New Template v23 1220.pptx 23 Indosat IR - New Template v23 1220.pptx

23 Indosat Presentation 9M 2013

23

Disclaimer

• PT Indosat Tbk cautions investors that certain statements contained in this document state management's intentions, hopes, beliefs, expectations, or predictions of the future are forward-looking statements

• Management wishes to caution the reader that forward-looking statements are not historical facts and are only estimates or predictions. Actual results may differ materially from those projected as a result of risks and uncertainties including, but not limited to:

• Our ability to manage domestic and international growth and maintain a high level of customer service

• Future sales growth

• Market acceptance of our product and service offerings

• Our ability to secure adequate financing or equity capital to fund our operations

• Network expansion

• Performance of our network and equipment

• Our ability to enter into strategic alliances or transactions

• Cooperation of incumbent local exchange carriers in provisioning lines and interconnecting our equipment

• Regulatory approval processes

• Changes in technology

• Price competition

• Other market conditions and associated risks

• The company undertakes no obligation to update publicly any forward-looking statements, whether as a result of future events, new information, or otherwise

24 Indosat IR - New Template v23 1220.pptx

24

25 Indosat IR - New Template v23 1220.pptx

25

Supplemental Information

26 Indosat IR - New Template v23 1220.pptx 26 Indosat IR - New Template v23 1220.pptx

26 Indosat Presentation 9M 2013

26

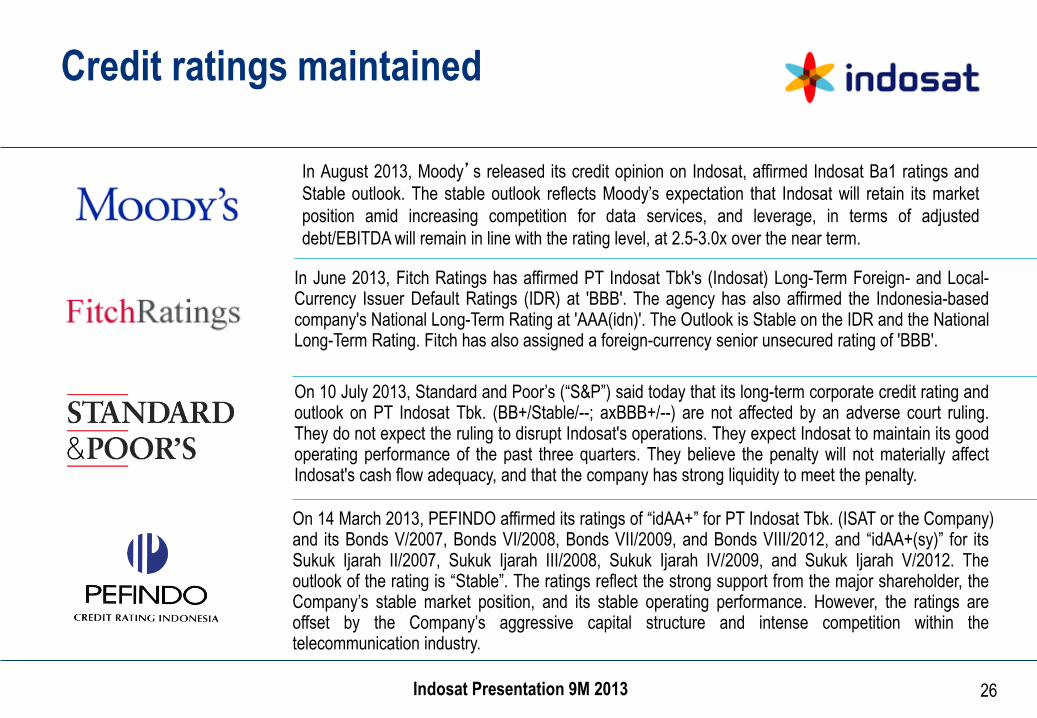

Credit ratings maintained

In June 2013, Fitch Ratings has affirmed PT Indosat Tbk's (Indosat) Long-Term Foreign- and Local-Currency Issuer Default Ratings (IDR) at 'BBB'. The agency has also affirmed the Indonesia-based company's National Long-Term Rating at 'AAA(idn)'. The Outlook is Stable on the IDR and the National Long-Term Rating. Fitch has also assigned a foreign-currency senior unsecured rating of 'BBB'.

On 10 July 2013, Standard and Poor’s (“S&P”) said today that its long-term corporate credit rating and outlook on PT Indosat Tbk. (BB+/Stable/--; axBBB+/--) are not affected by an adverse court ruling. They do not expect the ruling to disrupt Indosat's operations. They expect Indosat to maintain its good operating performance of the past three quarters. They believe the penalty will not materially affect Indosat's cash flow adequacy, and that the company has strong liquidity to meet the penalty.

On 14 March 2013, PEFINDO affirmed its ratings of “idAA+” for PT Indosat Tbk. (ISAT or the Company) and its Bonds V/2007, Bonds VI/2008, Bonds VII/2009, and Bonds VIII/2012, and “idAA+(sy)” for its Sukuk Ijarah II/2007, Sukuk Ijarah III/2008, Sukuk Ijarah IV/2009, and Sukuk Ijarah V/2012. The outlook of the rating is “Stable”. The ratings reflect the strong support from the major shareholder, the Company’s stable market position, and its stable operating performance. However, the ratings are offset by the Company’s aggressive capital structure and intense competition within the telecommunication industry.

In August 2013, Moody’s released its credit opinion on Indosat, affirmed Indosat Ba1 ratings and

Stable outlook. The stable outlook reflects Moody’s expectation that Indosat will retain its market

position amid increasing competition for data services, and leverage, in terms of adjusted

debt/EBITDA will remain in line with the rating level, at 2.5-3.0x over the near term.

27 Indosat IR - New Template v23 1220.pptx 27 Indosat IR - New Template v23 1220.pptx

27 Indosat Presentation 9M 2013

27

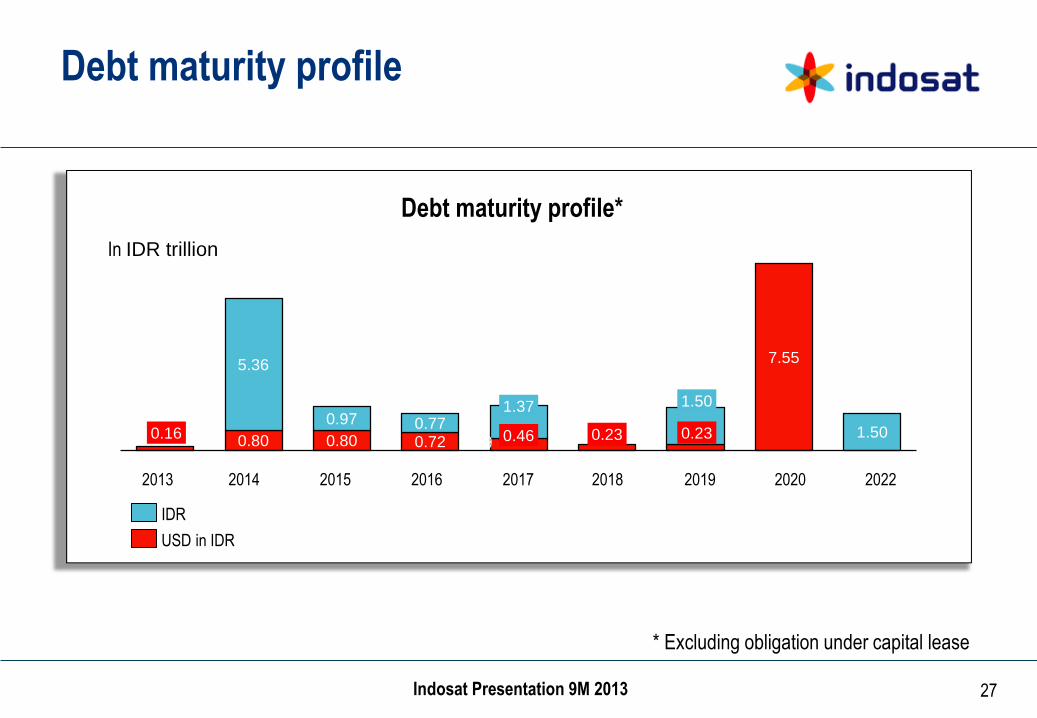

Debt maturity profile

Debt maturity profile*

In IDR trillion

0.16 0.80 0.80 0.72 0.46 0.23 0.23

7.55 5.36

0.97 0.77 1.37 1.50

1.50

2019 2018 2017 2013 2020 2022 2016

0.59

2015 2014

IDR

USD in IDR

* Excluding obligation under capital lease

28 Indosat IR - New Template v23 1220.pptx 28 Indosat IR - New Template v23 1220.pptx

28 Indosat Presentation 9M 2013

28

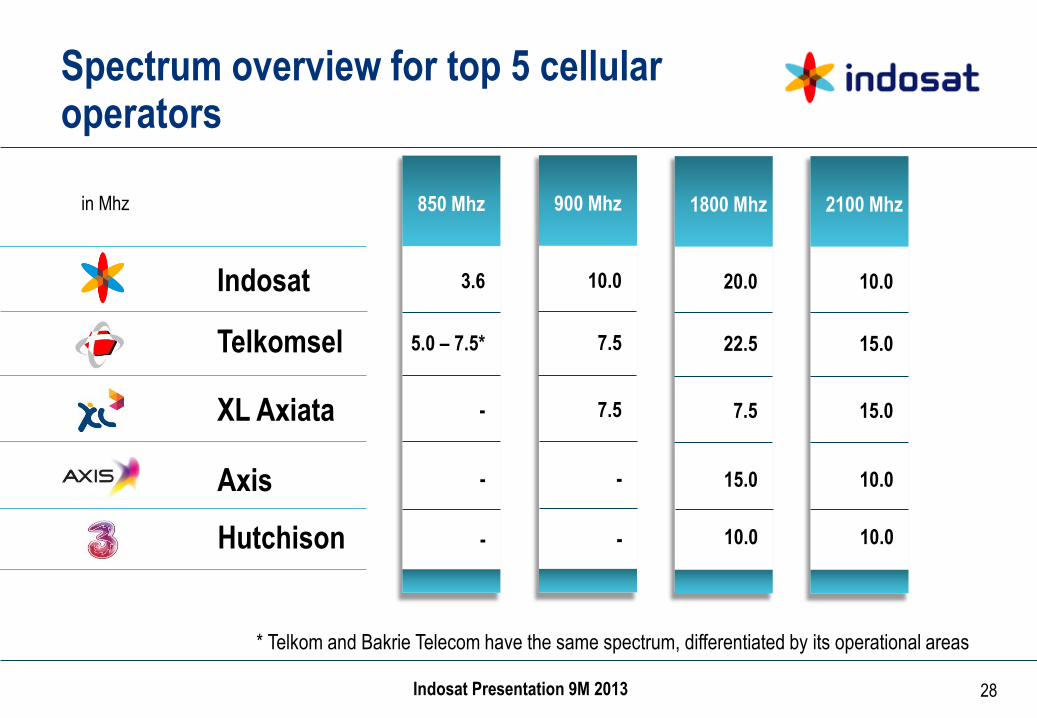

Spectrum overview for top 5 cellular operators

10.0

900 Mhz

7.5

7.5

Indosat

Telkomsel

XL Axiata

20.0

1800 Mhz

22.5

7.5

10.0

2100 Mhz

15.0

15.0

in Mhz

- 15.0 10.0 Axis

Hutchison - 10.0 10.0

3.6

850 Mhz

5.0 – 7.5*

-

-

-

* Telkom and Bakrie Telecom have the same spectrum, differentiated by its operational areas