1h 2018 results - assets.indosatooredoo.com · smartfren 2 x 11.0 - 30.0 . pt indosat tbk. –1h...

TRANSCRIPT

1H 2018 Results

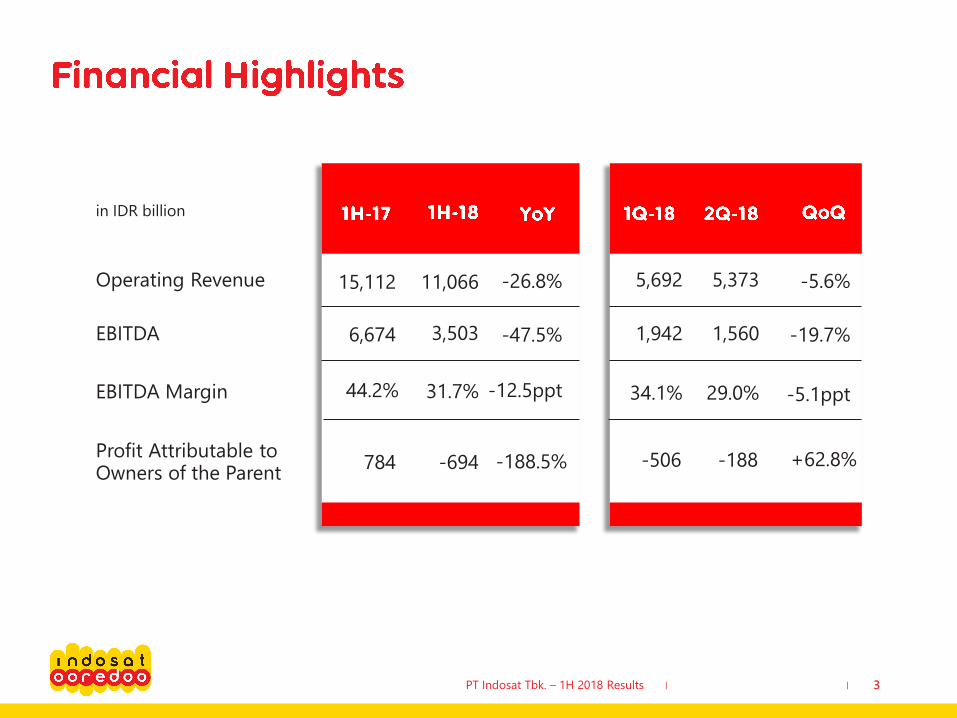

| |PT Indosat Tbk. – 1H 2018 Results 3

Operating Revenue

EBITDA

EBITDA Margin

Profit Attributable to Owners of the Parent

11,066 -26.8%

3,503 -47.5%

44.2% -12.5ppt

-694 -188.5%

5,373 -5.6%

1,560 -19.7%

29.0% -5.1ppt

-188 +62.8%

in IDR billion

15,112

6,674

31.7%

784

5,692

1,942

34.1%

-506

| |PT Indosat Tbk. – 1H 2018 Results 4

1,060

1,0851,375

1,043 967

234

217 220

232 178

in IDR billion

-5.6% QoQ-31.3% YoY

CellularFixed DataFixed Voice

-23.3% | -23.8%

-7.3% | -8.8%

-4.3% | -35.2%

QoQ | YoY

2Q-17 3Q-17 4Q-17 1Q-18

6,529

7,823

7,453

6,1514,228

7,360

5,692

2Q-18

5,765

5,373

4,417

| |PT Indosat Tbk. – 1H 2018 Results 5

Voice

SMS

Data

VAS

-33.4%

-57.1%

-12.6%

-3.7%

-7.9%

-20.4%

-5.0%

-2.3%

Shifting business model from push marketingstrategy to customer’s demand driven Go-To-Market Strategy

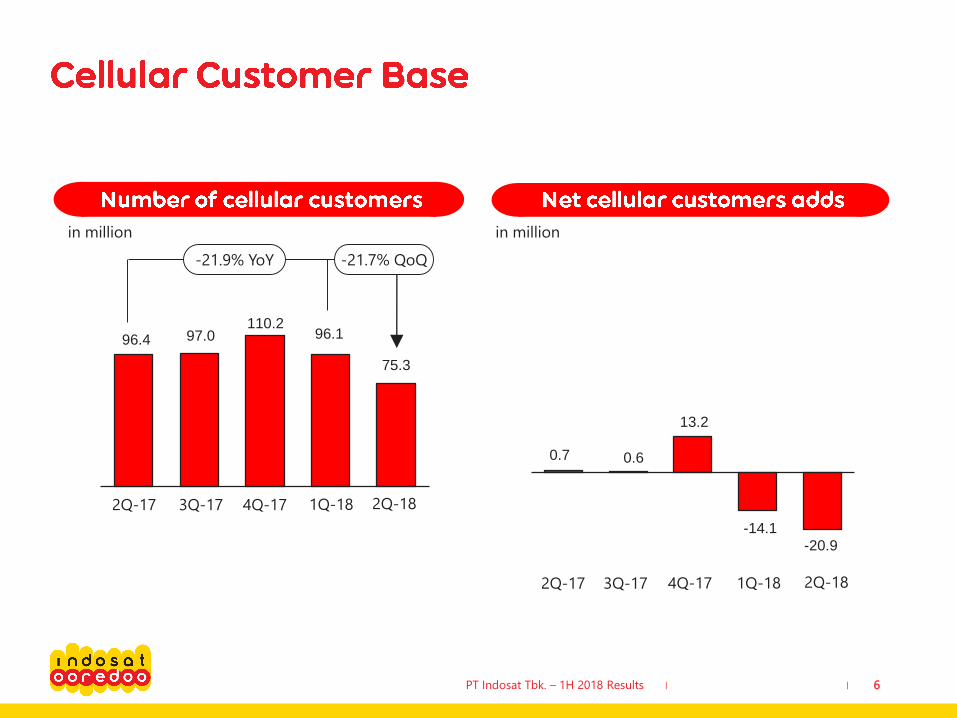

| |PT Indosat Tbk. – 1H 2018 Results 6

96.4 97.0110.2

96.1

75.3

-21.9% YoY -21.7% QoQ

in million in million

0.7 0.6

13.2

-14.1-20.9

2Q-17

2Q-17

3Q-17

3Q-17

4Q-17

4Q-17

1Q-18

1Q-18

2Q-18

2Q-18

| |

5347

3729

35

PT Indosat Tbk. – 1H 2018 Results 7

131144 149 150 155

-45.8% YoY -9.7% QoQ

Voice Traffic

in billion minutes (Voice Traffic)

in minute/subscriber (MOU)

MOU

22.5 20.6 17.612.4 15.9

+28.0% QoQ-29.3% YoY

ARPU

in thousand IDR (ARPU)

ARPM

in IDR (ARPM)

2Q-17 2Q-173Q-17 3Q-174Q-17 4Q-171Q-18 1Q-182Q-18

15.6 12.4 11.6 9.4 8.5

2Q-18

| |PT Indosat Tbk. – 1H 2018 Results 8

246,862

293,225333,263

368,232

449,105

in TByte

+22.0% QoQ+81.9% YoY

2Q-17 3Q-17 4Q-17 1Q-18 4Q-17

59%63% 66%

70% 72%

+2.0% QoQ+13.0% YoY

2Q-17 3Q-17 1Q-182Q-18 2Q-18

| |PT Indosat Tbk. – 1H 2018 Results 9

Cost of Service (CoS)

Depreciation and Amortization

Personnel

Marketing

as percentage of revenue

General and Administration

Total Expenses

Total Operating Expenses

45.8%

29.9%

4.0%

4.6%

6.7%

91.1%

61.2%

53.1%

37.6%

10.7%

5.5%

1.7%

108.5%

71.0%

7.2%

4.2%

3.2%

39.6%

28.2%

82.5%

54.3%

7.6%

4.7%

3.2%

41.2%

29.8%

86.4%

56.6%

50.2%

36.5%

10.3%

3.1%

2.2%

102.4%

65.9%

| |PT Indosat Tbk. – 1H 2018 Results 10

3,574 3,2322,856

1,9421,560

-19.7% QoQ-56.3% YoY

EBITDA

in IDR billion

EBITDA Margin

4Q-17

43.4%

2Q-17

38.8%

3Q-17

45.7%

428

784

-694

-188.5% YoY+83.2% YoY

1H-181H-171H-16

in IDR billion

34.1%

1Q-18

29.0%

2Q-18

| |PT Indosat Tbk. – 1H 2018 Results 11

1.74

1.42

2.01

21,083 19,226 19,290

1.55

1.25

1.87

18,83016,821 17,971

1H-171H-16 1H-18

+0.3% YoY

Gross Debt

in IDR billion

Gross Debt/EBITDA

1H-181H-16 1H-17

Net Debt Net Debt/EBITDA

in IDR billion

+6.8% YoY

| |

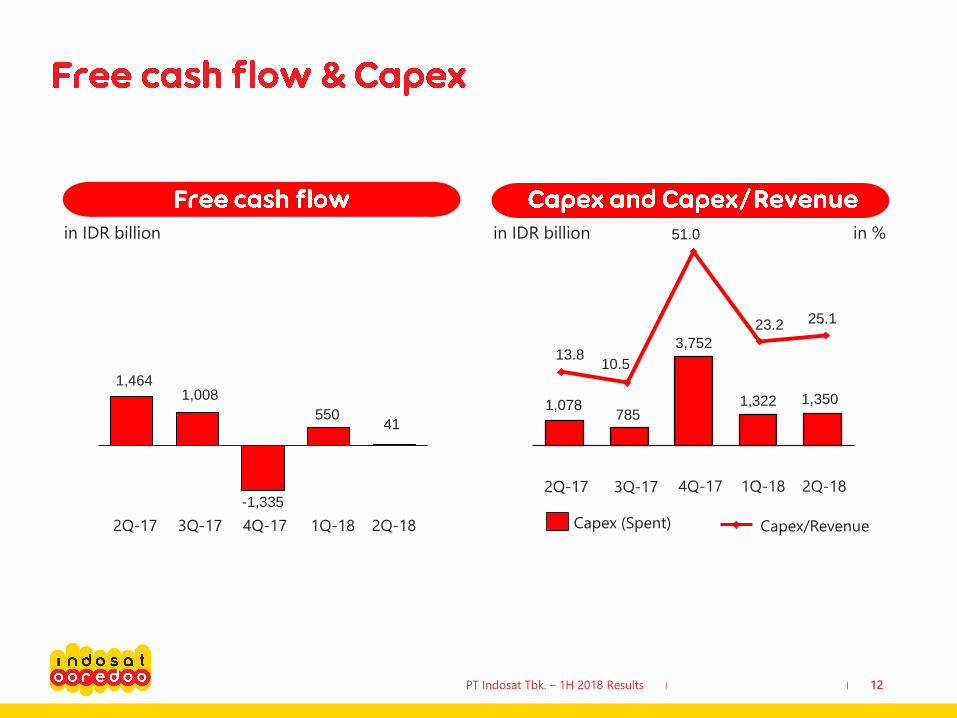

13.8 10.5

51.0

23.2 25.1

PT Indosat Tbk. – 1H 2018 Results 12

in IDR billion

1,4641,008

-1,335

55041

Capex (Spent)

in IDR billion

Capex/Revenue

4Q-17

2Q-17

in %

3Q-17

2Q-17

4Q-17

3Q-17 1Q-18

1Q-18 2Q-18

1,078785

3,752

1,322 1,350

2Q-18

| |PT Indosat Tbk. – 1H 2018 Results 13

• 4G coverage has reached 239 cities in Indonesia, 34 cities addition during 1H 2018.

24,235 24,225 23,999 24,294 24,427

29,255 29,912 30,179 31,062 31,880

5,533 6,110 7,179 9,019 10,066

+3.1% QoQ+12.5% YoY

2G3G

59,023

4Q-17

4G

2Q-17 3Q-17

60,247 61,357

1Q-18

64,375More than 80% of total sites have

been modernized since 2013 and

READY for 4.5G and beyond

technology deployment

2Q-18

66,373

| |PT Indosat Tbk. – 1H 2018 Results 15

Consolidated Revenue Growth Below market

EBITDA Margin High 30’s

CAPEX ~ IDR 8 trillion(Spent)

-26.8%

31.7%

IDR 2.7 trillion(Spent)

| |PT Indosat Tbk. – 1H 2018 Results 18

On September 16, 2014, the South Jakarta Attorney Office (“Kejaksaan

Negeri Jakarta Selatan”), without preliminary notification, executed the

Supreme Court’s Decision on Mr. Indar Atmanto. The execution was

done based on a quotation of the Supreme Court’s Decision, which

states, among others, that (i) Mr. Indar Atmanto is found guilty and

sentenced to eight years imprisonment and charged with penalty of

Rp300,000,000,- (if the penalty is not paid, Mr. Indar Atmanto would

serve an additional six months imprisonment), and (ii) IM2 pay the

losses sustained by the State amounting to Rp1,358,343,346,674,-.

Subsequently, on January 16, 2015, Mr.Indar Atmanto and/or his lawyer

or IM2 received the document on the Supreme Court’s decision

regarding the litigation case. As of the issuance date of the

consolidated financial statements, Mr. Indar Atmanto and IM2 plan to

conduct further legal act by submitting a reconsideration request

peninjauan kembali (”PK”).

On March 16, 2015, Mr. Indar Atmanto’s submission of Judicial Review

[Peninjauan Kembali (”PK”)] was officially registered at the Corruption

Court under No. 08/AKTA.PID.SUS/PK/TPK/2015/PN.Jkt.Pst.

On November 4, 2015, the Supreme Court’s official website announced

that the Judicial Review filed by Mr. Indar Atmanto was rejected based

on Supreme Court’s decision dated October 20, 2015. However, no

detailed information regarding the exact content of such Supreme

Court’s decision was available. As of the issuance date of the interim

consolidated financial statements, the official copy of such Supreme

Court’s decision hasn’t been received.

| |PT Indosat Tbk. – 1H 2018 Results 19

On December 8, 2017, S&P Global Ratings raised its long-term corporate credit rating on

Indonesia-based telecommunications operator PT Indosat Tbk. (Indosat) to 'BBB-' from

'BB+'. The outlook is stable. The upgrade reflects their expectation that Indosat will

maintain its solid cash flow adequacy and reduce debt over the next 12-24 months. The

company's steady cash flows, moderate capital spending, and prudent financial policies

should support the improvement. We anticipate that Indosat's ratio of funds from

operations (FFO) to debt will remain above 40% until 2019.

On 13 March 2018, PEFINDO has affirmed its “idAAA” ratings for PT Indosat Tbk (ISAT) and

its Shelf Registration Bond II Year 2017-2019, Shelf Registration Bond I Year 2014-2016, and

Bond VIII Year 2012. PEFINDO has also affirmed its “idAAA(sy)” ratings for ISAT’s Shelf

Registration Sukuk Ijarah II Year 2017-2019, Shelf Registration Sukuk Ijarah I Year 2014-

2016, and Sukuk Ijarah V Year 2012. The outlook for the corporate rating is “stable”.

On 12 May 2017, Moody's Investors Service has has upgraded to Baa3 from Ba1 the

issuer rating of Indosat Tbk. (P.T.) (Indosat Ooredoo). The outlook for the rating is stable.

At the same time, Moody's has withdrawn the company's Ba1 Corporate Family Rating.

The rating upgrade reflects the continued strengthening of Indosat Ooredoo's operational

metrics as well as the ongoing stabilization of its financial profile, including lower leverage

levels.

On 25 February 2018, Fitch Ratings has affirmed Indonesian telecom operator

PT Indosat Tbk's (Indosat Ooredoo) Long-Term Foreign-and Local-

Currency Issuer Default Rating (IDR) at ‘BBB+’ simultaneously affirmed the foreign-

currency senior unsecured rating at 'BBB+‘. Fitch Ratings has also affirmed Indosat

Ooredoo’s National LongTerm Rating at 'AAA(idn)'. The Outlook is Stable.

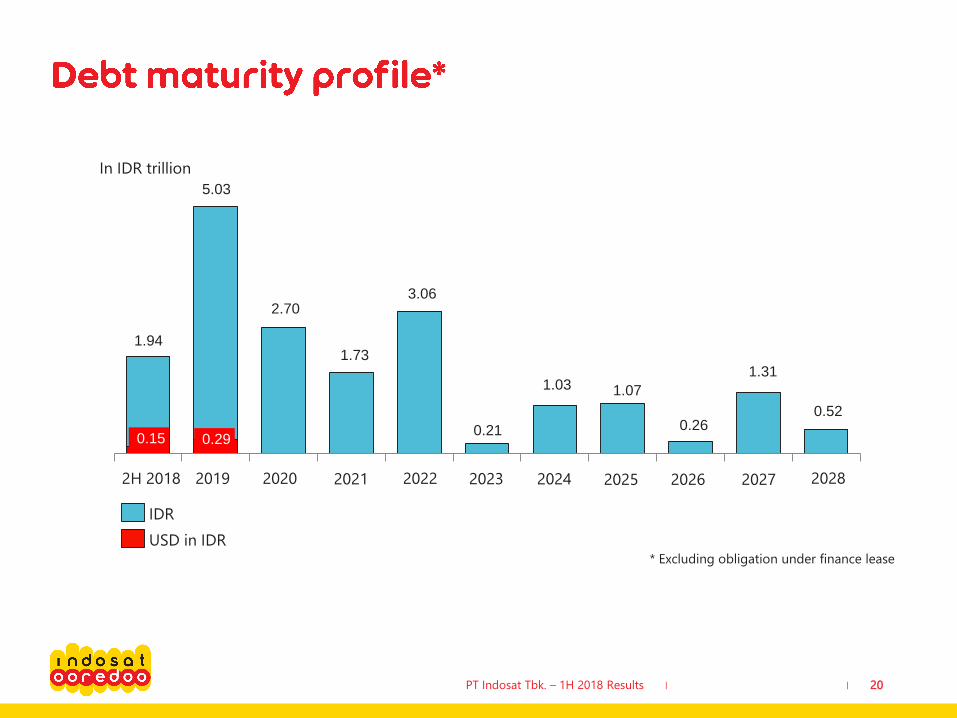

| |PT Indosat Tbk. – 1H 2018 Results 20

0.15 0.29

1.94

5.03

2.70

1.73

3.06

0.21

1.03 1.07

0.26

1.31

0.52

In IDR trillion

20202019 20222H 2018

IDR

USD in IDR

2021 20242023 2025 2026

* Excluding obligation under finance lease

2027 2028

| |PT Indosat Tbk. – 1H 2018 Results 21

Number of BTS

2 x 12.5

2 x 15

2 x 7.5

Indosat

Telkomsel

XL Axiata

2 x 20.0

2 x 22.5

2 x 22.5

2 x 15.0

2 x 15.0

2 x 15.0

in Mhz

Hutchison - 2 x 10.0 2 x 15.0

15.0*

45.0

-

-

* Indosat/IM2: West Java exclude Bogor, Depok & Bekasi

2020 2020 2019, 2026,2028

2019Valid until

Smartfren 2 x 11.0 30.0 - -

| |PT Indosat Tbk. – 1H 2018 Results 22

• PT Indosat Tbk ( “Indosat” or “Company” ) cautions investors that certain statements contained in this document state its management's intentions, hopes, beliefs, expectations, or predictions of the future are forward-looking statements

• The Company wishes to caution the reader that forward-looking statements are not historical facts and are only estimates or predictions. Actual results may differ materially from those projected as a result of risks and uncertainties including, but not limited to:

• The Company’s ability to manage domestic and international growth and maintain a high level of customer service

• Future sales growth

• Market acceptance of the Company’s product and service offerings

• The Company’s ability to secure adequate financing or equity capital to fund our operations

• Network expansion

• Performance of the Company’s network and equipment

• The Company’s ability to enter into strategic alliances or transactions

• Cooperation of incumbent local exchange carriers in provisioning lines and interconnecting our equipment

• Regulatory approval processes

• Changes in technology

• Price competition

• Other market conditions and associated risks

• The company undertakes no obligation to update publicly any forward-looking statements, whether as a result of future events, new information, or otherwise