ptt public company limited -...

TRANSCRIPT

CORPORATES

CREDIT OPINION11 December 2017

Update

RATINGS

PTT Public Company LimitedDomicile Thailand

Long Term Rating Baa1

Type LT Issuer Rating - FgnCurr

Outlook Stable

Please see the ratings section at the end of this reportfor more information. The ratings and outlook shownreflect information as of the publication date.

Contacts

Rachel Chua [email protected]

Laura Acres +65.6398.8335MD-Corporate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

PTT Public Company LimitedUpdate to credit opinion

Summary

PTT Public Company Limited’s (PTT) Baa1 issuer rating primarily reflects the company'sstandalone credit quality as captured in its baa2 Baseline Credit Assessment (BCA).

The baa2 BCA reflects the company's (1) strategically important position as Thailand'snational integrated oil and gas company, with a natural monopoly in gas transmission anddistribution; (2) significant upstream production and control over around 60% of Thailand'stotal refining capacity; (3) strong and resilient credit metrics through periods of sustained lowoil prices; and (4) strong liquidity profile, with a large cash balance.

At the same time, PTT's BCA remains constrained by its declining hydrocarbon reserves,which translate into higher capital investment and acquisition risk, lower upstream margins,as well as inherent exposure to the cyclical nature of oil prices and refining/petrochemicalmargins.

The Baa1 issuer rating also incorporates our expectation of a high likelihood of extraordinarysupport from the Government of Thailand (Baa1 stable), which results in a one-notch uplift.

Our support assessment reflects (1) the Thai Ministry of Finance’s explicit intention tomaintain state ownership; (2) PTT’s status as a majority-owned state enterprise; (3) theclose supervision and alignment of the company's corporate policy with the government’senergy policy; and (4) its national importance for gas distribution and, ultimately, to thecountry's power generation sector, as well as its responsibility to prevent any fuel shortagesin Thailand.

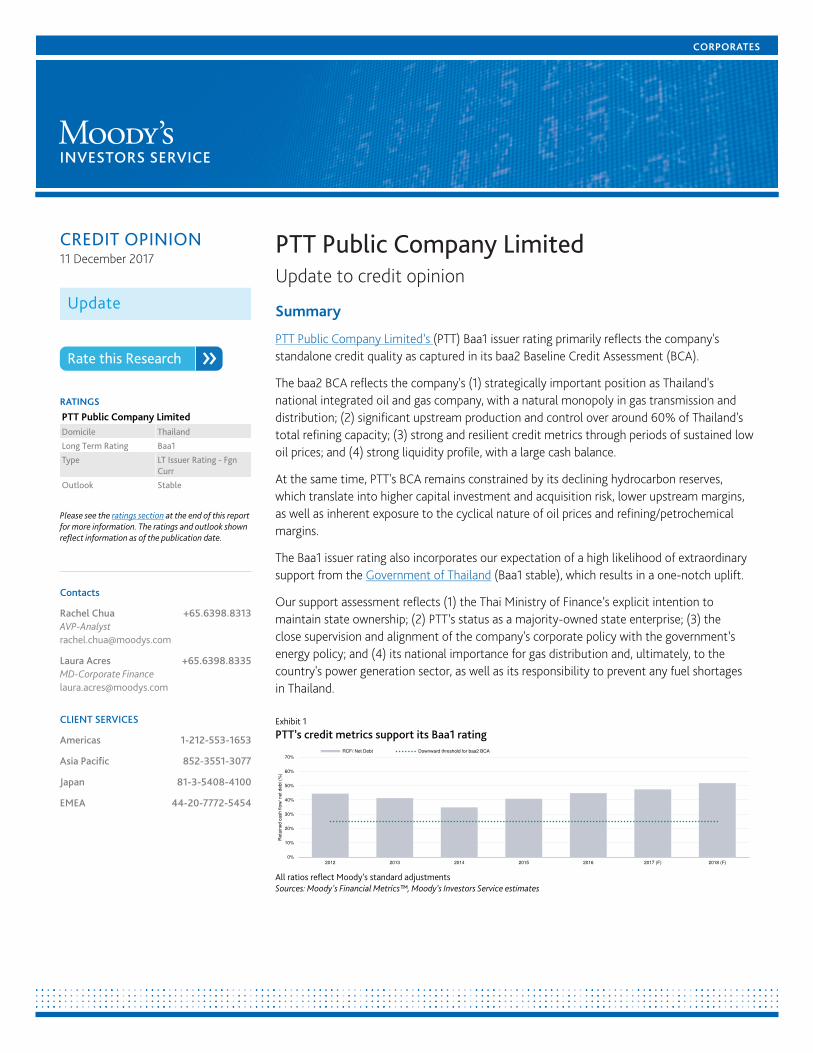

Exhibit 1

PTT’s credit metrics support its Baa1 rating

0%

10%

20%

30%

40%

50%

60%

70%

2012 2013 2014 2015 2016 2017 (F) 2018 (F)

Re

tain

ed

ca

sh

flo

w/

ne

t d

eb

t (%

)

RCF/ Net Debt Downward threshold for baa2 BCA

All ratios reflect Moody’s standard adjustmentsSources: Moody's Financial Metrics™, Moody’s Investors Service estimates

MOODY'S INVESTORS SERVICE CORPORATES

Credit strengths

» Natural monopoly status in Thailand’s gas transmission and distribution sector, which drives stable returns

» Resilient credit metrics as a result of its integrated business model

» Expected support from the Thai government

» Strong liquidity profile, with a large cash balance

Credit challenges

» Lower upstream earnings and margins due to low oil prices

» Ongoing reserve replacement challenge, which drives capital investment and acquisition risk

Rating outlookThe stable rating outlook is in line with the outlook on Thailand’s sovereign rating and reflects our expectation that PTT will maintain aprudent financial profile as it pursues growth.

Factors that could lead to an upgradeWe will upgrade PTT’s Baa1 issuer rating only if we upgrade the Government of Thailand’s Baa1 sovereign rating.

Near-term upward rating pressure on PTT’s BCA is limited, given its lower upstream margins, declining hydrocarbon reserves andexpansion plans.

Nonetheless, PTT’s BCA can improve to baa1 if the company lowers its debt leverage through (1) PTT Exploration & Production's(PTTEP; Baa1 stable) successful project developments, which would in turn lead to growth in reserves and production; (2) strengtheningits cash flows from the natural gas business; or (3) significant growth in contributions from its other downstream businesses.

An improvement in PTT’s BCA will not automatically lead to an upgrade of its issuer rating.

Factors that could lead to a downgradePTT's Baa1 issuer rating will be downgraded if (1) Thailand's sovereign rating is lowered; (2) the company's BCA deteriorates below baa3;or (3) government ownership is reduced to below 51%, or government control is reduced by some other means, which would require areassessment of the level of support incorporated into its rating.

We would lower PTT's BCA to baa3 if the oil price environment deteriorates significantly, such that oil prices fall and stay below $35per barrel for a prolonged period. Negative pressure on the BCA could also develop if the company undertakes large debt-fundedacquisitions, resulting in weaker credit metrics and higher execution risk.

Credit metrics indicative of a deterioration of its BCA include retained cash flow (RCF)/net debt below 25% and EBITDA/interest below5x. A lowering of the BCA to baa3 will not automatically result in a downgrade of PTT's issuer rating.

This publication does not announce a credit rating action. For any credit ratings referenced in this publication, please see the ratings tab on the issuer/entity page onwww.moodys.com for the most updated credit rating action information and rating history.

2 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

Key indicators

Exhibit 2

USD Millions Dec-12 Dec-13 Dec-14 Dec-15 Dec-16

LTM

Sep-17

12- 18 months

forward view

EBIT / Avg. Book Capitalization 15.1% 12.9% 10.3% 9.3% 10.2% 12.8% 10% - 12%

EBIT / Interest Expense 8.6x 7.5x 4.8x 4.6x 5.5x 7.0x 6.0x - 7.0x

RCF / Net Debt 44% 41% 35% 41% 45% 46% 40% - 50%

Debt / Book Capitalization 38% 37% 42% 41% 38% 36% 35% - 40%

Average Daily Production (MBOE / Day) 312 329 359 373 368 348 360 - 370

Total Proved Reserves (MBOE) 901,000 846,000 777,000 738,000 695,000 695,000 695,000

Crude Distillation Capacity (mbbls/day) 440 440 440 635 635 635 635.0

Downstream EBIT/Total Throughput Barrels ($/bbl) $0.2 $0.2 $0.7 $7.4 $9.2 $9.4 $8 - $9

All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations.Source: Moody's Financial Metrics™, Moody's Investors Service estimates

ProfilePTT is an integrated oil, gas and petrochemical company based in Thailand. Its main operations include transmission and distributionof natural gas, and upstream exploration and production through its 65%-owned subsidiary PTT Exploration & Production. PTTholds interests in three out of six oil refineries in Thailand, which, together with its six gas separation plants, support the company'spetrochemical business. The company is also directly engaged in oil marketing and international trading.

Exhibit 3

PTT's reported EBITDA contribution from its key business segmentsFor the nine months ended 30 September 2017

Exploration and Production31%

Refining and Petrochemical35%

Gas and oil marketing32%

Others2%

Source: Company data

In the 12 months ended 30 September 2017, the company reported consolidated revenue of THB1.9 trillion ($58 billion). Thecompany's largest shareholder is the Thai Ministry of Finance, which owns 51.1% of its total share capital, while the government-invested Vayupak Mutual Funds owns a further 13.1%.

Detailed credit considerationsStable returns from gas transmission and distributionPTT's natural gas business provides a stable source of cash flow. The company owns and operates all six gas separation plants inThailand, with total capacity of 6.7 metric tons per year (MTPA), and substantially all of the country's gas pipeline network which is over4,000km. This network links commercial gas fields to gas separation plants, domestic power producers and other industry users.

In the first nine months of 2017, PTT's gas business accounted for 15% of its revenue and 26% of EBITDA. The natural gas sales volumefor the same period averaged 4,730 million standard cubic feet per day (mmscfd), down from 4,782 mmscfd in the same period a yearago owing to lower demand from power producer customers.

3 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

Power producers and gas separation plants accounted for around 79% of PTT’s total gas sales in the first nine months of 2017. Outputfrom the gas separation plants, which are owned by PTT, are then sold to petrochemical plants. These gas sales are subject to agovernment-prescribed tariff structure that comprises (1) the average price PTT pays to gas suppliers (including PTTEP), (2) a supplymargin of 1.75% for most of its customers, and (3) a pipeline tariff of THB21.9 per million British thermal units (mmbtu) to coveroperating costs and a permitted return.

Moreover, there is a low degree of volume risk for PTT because the take-or-pay gas contracts it has entered into with offtakers andsuppliers are essentially back-to-back and typically span 25-30 years. These long-term contracts partially mitigate PTT’s exposure tothe cyclical nature of the oil and gas sector.

Resilient credit metrics as a result of its integrated business modelAs Thailand’s national oil company, PTT had proved oil and gas reserves of 695 million barrels of oil equivalent (mmboe) as of year-end2016. It is the largest shareholder of three refineries in Thailand, accounting for around 60% of the country’s total refining capacity. Italso had a market share of about 40% in the domestic oil marketing business as of 30 September 2017.

PTT’s credit profile remained resilient in 2016 even as oil prices declined materially. Given its integrated operations, the lower upstreamearnings was more than offset by the healthy earnings generated in its mid- and downstream businesses. In 2016, following significantcost-cutting initiatives across the group, PTT reported a 9% year-on-year EBITDA growth (Exhibit 4). It also had a stronger RCF/netdebt of 44.8% in 2016 compared with 40.9% in 2015.

Exhibit 4

PTT's reported EBITDA grew in 2016 despite lower oil prices

0

50

100

150

200

250

300

350

2014 2015 2016 9M2017

Re

po

rte

d E

BIT

DA

(T

HB

bill

ions)

Exploration and Production Refining and Petrochemical Gas and oil marketing Others

Source: Company data

Over the next 12-18 months, we expect PTT’s EBITDA to be largely supported by (1) the completion of its liquefied natural gas (LNG)terminal expansion to 10MTPA from 7MTPA, (2) increased gas volumes in its natural gas pipelines, (3) stable upstream earnings, and (4)healthy refining and petrochemical earnings from full-year contributions of its upgraded plants.

We also expect the company to benefit from firm refining margins and stable per-barrel oil prices in the $50s. As such, we project thecompany's RCF/net debt will remain healthy at around 45%-50% over the next 12-18 months. As of 30 September 2017, its RCF/netdebt was 46.1%.

Lower upstream earnings and margins due to low oil pricesPTT's upstream earnings contribution has declined since 2015 given the lower oil price environment. In 2016, its reported EBITDA inthe exploration and production segment fell 38.5% compared to 2014. This demonstrates the upstream segment's exposure to the oilprice cyclicality.

Nonetheless, we note that PTT's focus on natural gas sales provides a buffer against volatility in its oil sales which is exposed moredirectly to oil price fluctuations. Its natural gas sales agreements have built-in mechanisms where the selling prices and minimumvolumes are pre-determined and adjustment periods of 3-12 months are specific. Its upstream sales volume comprises 70% of naturalgas while oil and condensate make up the remaining 30%.

4 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

This stability distinguishes PTT's upstream business from other global peers. In 2015, when crude oil prices fell 46%, PTT's averageoil and gas selling price only fell around 30%. In addition, with the company's gas volume projected to increase to 74% of its totalproduction in 2019 from 69% in 2016, we expect its cash flow to be increasingly stable from the larger gas sales contribution.

PTT's upstream business also benefits from low labor costs and its well-established infrastructure and production facilities. In thefirst nine months of 2017, the company reported unit production cost of $28.4 per barrel of oil equivalent (boe), of which cash costsaccounted for $13.3 per boe compared with $15.8 per boe in 2015.

Even in a low oil price environment, it has maintained an upstream EBITDA margin of 70%-75% over the last few years. We expectupstream margins to remain within this range in the coming 12-18 months even as the company ramps up exploration activities toreplace its depleting proved reserves.

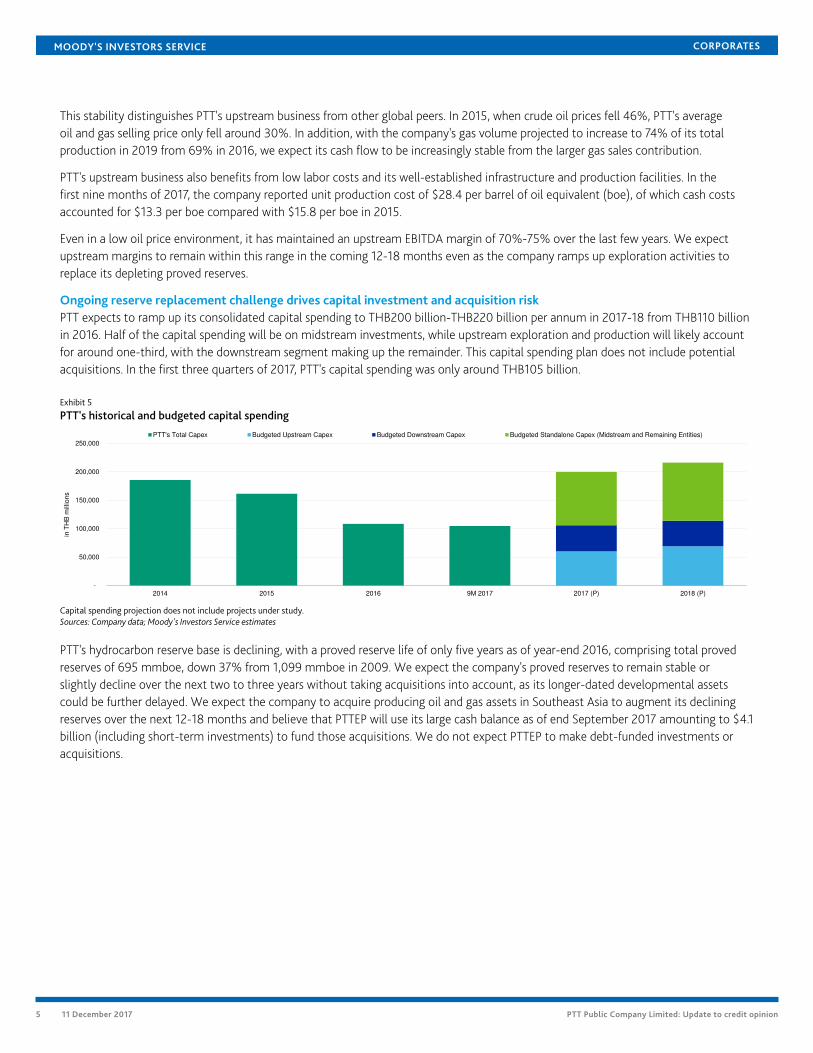

Ongoing reserve replacement challenge drives capital investment and acquisition riskPTT expects to ramp up its consolidated capital spending to THB200 billion-THB220 billion per annum in 2017-18 from THB110 billionin 2016. Half of the capital spending will be on midstream investments, while upstream exploration and production will likely accountfor around one-third, with the downstream segment making up the remainder. This capital spending plan does not include potentialacquisitions. In the first three quarters of 2017, PTT's capital spending was only around THB105 billion.

Exhibit 5

PTT's historical and budgeted capital spending

-

50,000

100,000

150,000

200,000

250,000

2014 2015 2016 9M 2017 2017 (P) 2018 (P)

in T

HB

mill

ion

s

PTT's Total Capex Budgeted Upstream Capex Budgeted Downstream Capex Budgeted Standalone Capex (Midstream and Remaining Entities)

Capital spending projection does not include projects under study.Sources: Company data; Moody's Investors Service estimates

PTT's hydrocarbon reserve base is declining, with a proved reserve life of only five years as of year-end 2016, comprising total provedreserves of 695 mmboe, down 37% from 1,099 mmboe in 2009. We expect the company's proved reserves to remain stable orslightly decline over the next two to three years without taking acquisitions into account, as its longer-dated developmental assetscould be further delayed. We expect the company to acquire producing oil and gas assets in Southeast Asia to augment its decliningreserves over the next 12-18 months and believe that PTTEP will use its large cash balance as of end September 2017 amounting to $4.1billion (including short-term investments) to fund those acquisitions. We do not expect PTTEP to make debt-funded investments oracquisitions.

5 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

Exhibit 6

PTT's proved oil and gas reserves are declining

-

200

400

600

800

1,000

1,200

2009 2010 2011 2012 2013 2014 2015 2016

Millio

n b

arr

els

of oil e

qu

iva

len

t (M

MB

OE

)

Domestic Overseas

Source: Company data

PTTEP also expects its reserves and production to increase organically from a number of key projects, including Mozambique RovumaOffshore Area 1, an asset of Cove Energy Plc that it acquired in August 2012; the Ubon oil field in the Gulf of Thailand; a field inSouthwest Vietnam; and Hassi Bir Rekaiz in Algeria. Accordingly, these projects will add considerable diversity to the company'soperating profile but will not materially boost the life of its reserves.

PTTEP has announced that it will participate in the upcoming bidding for the concessions of the Bongkot gas field, which will expire in2023. The auctions are scheduled to begin at the end of 2017, after the terms of reference and associated laws are finalized, while thewinning bids are likely to be announced in July 2018. At present, PTTEP holds a 44.4% stake in Bongkot, the largest natural gas field inthe Gulf of Thailand.

Support from the Thai governmentPTT's Baa1 issuer rating incorporates our assessment of a high likelihood of extraordinary support from the Thai government under ourjoint default analysis for government-related issuers. Our support assessment is based on the following:

» The government’s ability to provide support:

– The government’s ability to provide support is based on its Baa1 rating.

» The government’s willingness to provide support:

– Government ownership and control: The government owns 51.1% of PTT and a further 13.1% through the government-invested Vayupak Mutual Funds. As the major shareholder, the government has the ability to substantially influence thecomposition of the board. All major strategic and investment plans by PTT must also be proposed to and reviewed by thecabinet.

– Economic importance: PTT plays a critical role in the country's energy sector because it owns and operates more than60% of the country's total refining capacity. The company also has a monopoly in gas transmission and distribution withinthe country, as well as a 40% market share of Thailand's oil marketing stations. On the upstream segment, we estimatePTT's domestic production accounts for around 20%-25% of the country's total upstream oil and gas volumes.

– Reputational risk: Given the extent of government control over PTT, any default by PTT will have reputational implicationsfor the government and cause disruptions in the capital markets in Thailand, where the government and government-owned companies are the largest borrowers.

– Track record of providing support:

› PTT has loans amounting to THB1 billion that are guaranteed by the Ministry of Finance.

6 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

Liquidity analysisPTT has a strong liquidity profile. It had consolidated cash and cash equivalents of THB195 billion and short-term investments ofTHB182 billion as of 30 September 2017 compared with THB107 billion of debt maturing over the next 12 months.

On a stand-alone basis, the company's liquidity remains strong, with cash and short-term investments totaling THB119 billion versusTHB42 billion of short-term maturities.

In November 2017, PTT completed an early redemption of $500 million of bonds using cash on hand, which further reduced its totaloutstanding borrowings. The company generally operates with sufficient cash on hand to service maturing debt, buffer its workingcapital requirements and extend credit to group entities when appropriate.

We believe the company has limited flexibility to reduce dividend payments. While the payout ratio is set at a minimum of 25%, it hasvaried widely from 54% in 2014 to almost 150% in 2015. As such, under our base-case scenario, we project dividends paid in 2017 and2018 to remain largely in line with the THB45 billion paid in 2016.

Other considerationsPTT conducts its downstream refining and petrochemical operations primarily through its associates. Nonetheless, since 2015, PTT hasfully consolidated the financial statements of its key associates — 49%-owned Thai Oil Public Company Limited (Baa1 stable), 49%-owned PTT Global Chemical Public Company Ltd (Baa2 stable) and 39%-owned IRPC Public Company Ltd (Ba1 stable) — to complywith Thai accounting standards because it is deemed to have control over these entities. PTT plans to list its oil and retail businesses in2018 while maintaining an ownership of 45%-50%. We expect the financials of these businesses to remain fully consolidated as well.

PTT's senior unsecured bond ratings are not affected by structural subordination, reflecting the company's own cash flow generationfrom its natural gas and oil marketing businesses. The likely support from the Thai sovereign in case of need also mitigates thestructural subordination risk.

In addition, its upstream subsidiary PTTEP will also see its credit metrics remaining supportive of its Baa1 rating with retained cash flow/adjusted debt above 45% and EBITDA interest cover above 10x over the next 12-18 months.

7 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

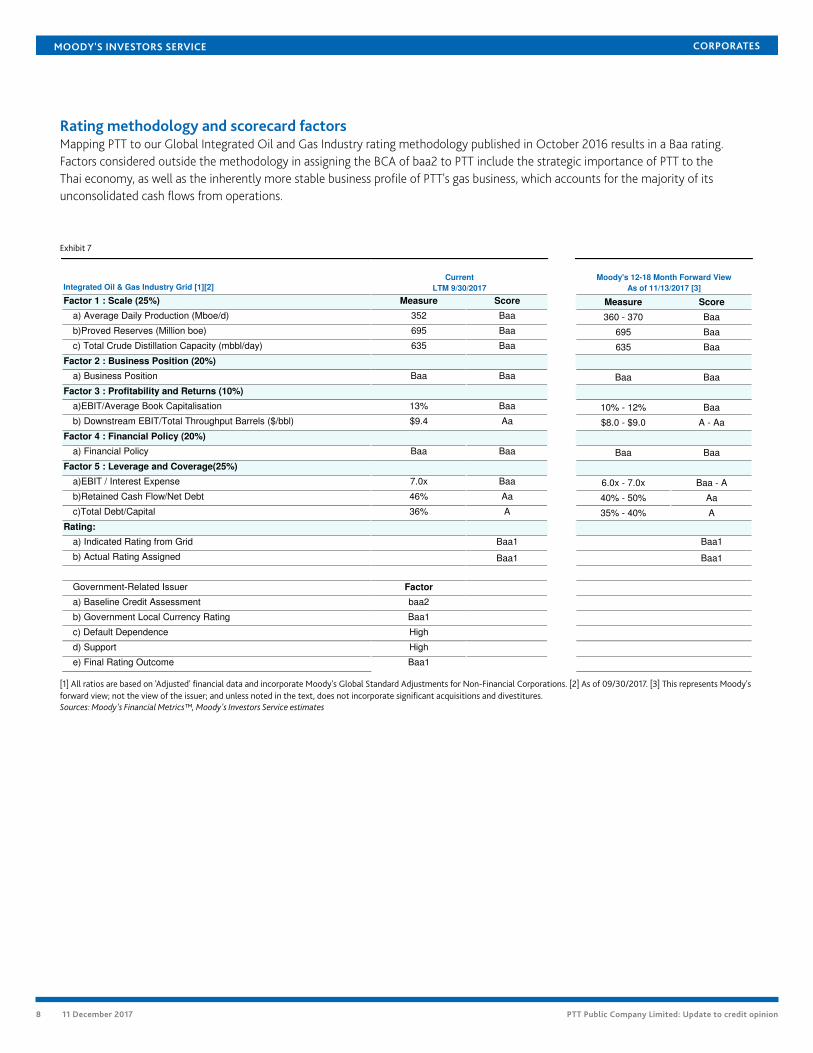

Rating methodology and scorecard factorsMapping PTT to our Global Integrated Oil and Gas Industry rating methodology published in October 2016 results in a Baa rating.Factors considered outside the methodology in assigning the BCA of baa2 to PTT include the strategic importance of PTT to theThai economy, as well as the inherently more stable business profile of PTT's gas business, which accounts for the majority of itsunconsolidated cash flows from operations.

Exhibit 7

Integrated Oil & Gas Industry Grid [1][2]

Factor 1 : Scale (25%) Measure Score Measure Score

a) Average Daily Production (Mboe/d) 352 Baa 360 - 370 Baa

b)Proved Reserves (Million boe) 695 Baa 695 Baa

c) Total Crude Distillation Capacity (mbbl/day) 635 Baa 635 Baa

Factor 2 : Business Position (20%)

a) Business Position Baa Baa Baa Baa

Factor 3 : Profitability and Returns (10%)

a)EBIT/Average Book Capitalisation 13% Baa 10% - 12% Baa

b) Downstream EBIT/Total Throughput Barrels ($/bbl) $9.4 Aa $8.0 - $9.0 A - Aa

Factor 4 : Financial Policy (20%)

a) Financial Policy Baa Baa Baa Baa

Factor 5 : Leverage and Coverage(25%)

a)EBIT / Interest Expense 7.0x Baa 6.0x - 7.0x Baa - A

b)Retained Cash Flow/Net Debt 46% Aa 40% - 50% Aa

c)Total Debt/Capital 36% A 35% - 40% A

Rating:

a) Indicated Rating from Grid Baa1 Baa1

b) Actual Rating Assigned Baa1 Baa1

Government-Related Issuer Factor

a) Baseline Credit Assessment baa2

b) Government Local Currency Rating Baa1

c) Default Dependence High

d) Support High

e) Final Rating Outcome Baa1

Current

LTM 9/30/2017

Moody's 12-18 Month Forward View

As of 11/13/2017 [3]

[1] All ratios are based on 'Adjusted' financial data and incorporate Moody's Global Standard Adjustments for Non-Financial Corporations. [2] As of 09/30/2017. [3] This represents Moody'sforward view; not the view of the issuer; and unless noted in the text, does not incorporate significant acquisitions and divestitures.Sources: Moody's Financial Metrics™, Moody's Investors Service estimates

8 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

Appendix

Exhibit 8

PTT's adjusted debt breakdown

(in US Millions)

FYE

Dec-12

FYE

Dec-13

FYE

Dec-14

FYE

Dec-15

FYE

Dec-16

LTM Ending

Sep-17

As Reported Debt 14,880.1 14,781.8 22,152.3 18,321.8 17,141.6 17,315.4

Pensions 190.3 247.4 524.4 522.1 588.4 631.9

Operating Leases 274.4 269.2 299.2 324.2 304.8 327.3

Hybrid Securities 162.9 151.6 1,130.3 1,033.4 1,038.5 1,147.5

Non-Standard Adjustments 36.2 31.4 47.7 748.7 736.3 751.2

Moody's-Adjusted Debt 15,543.8 15,481.5 24,154.0 20,950.2 19,809.7 20,173.3

All figures are calculated using Moody’s standard adjustments.Source: Moody’s Financial Metrics™

Exhibit 9

PTT's adjusted EBITDA breakdown

(in US Millions)

FYE

Dec-12

FYE

Dec-13

FYE

Dec-14

FYE

Dec-15

FYE

Dec-16

LTM Ending

Sep-17

As Reported EBITDA 8,360.7 8,479.3 9,868.7 8,868.7 8,871.9 10,357.5

Pensions 6.8 9.4 75.5 15.4 49.3 51.8

Operating Leases 45.0 48.0 101.0 113.7 103.1 105.4

Unusual 91.1 -7.3 -338.9 217.9 11.5 -194.0

Non-Standard Adjustments -518.2 -344.6 -26.5 124.9 55.1 69.1

Moody's-Adjusted EBITDA 7,985.4 8,184.9 9,679.8 9,340.6 9,090.8 10,389.7

All figures are calculated using Moody’s standard adjustments.Source: Moody’s Financial Metrics™

9 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

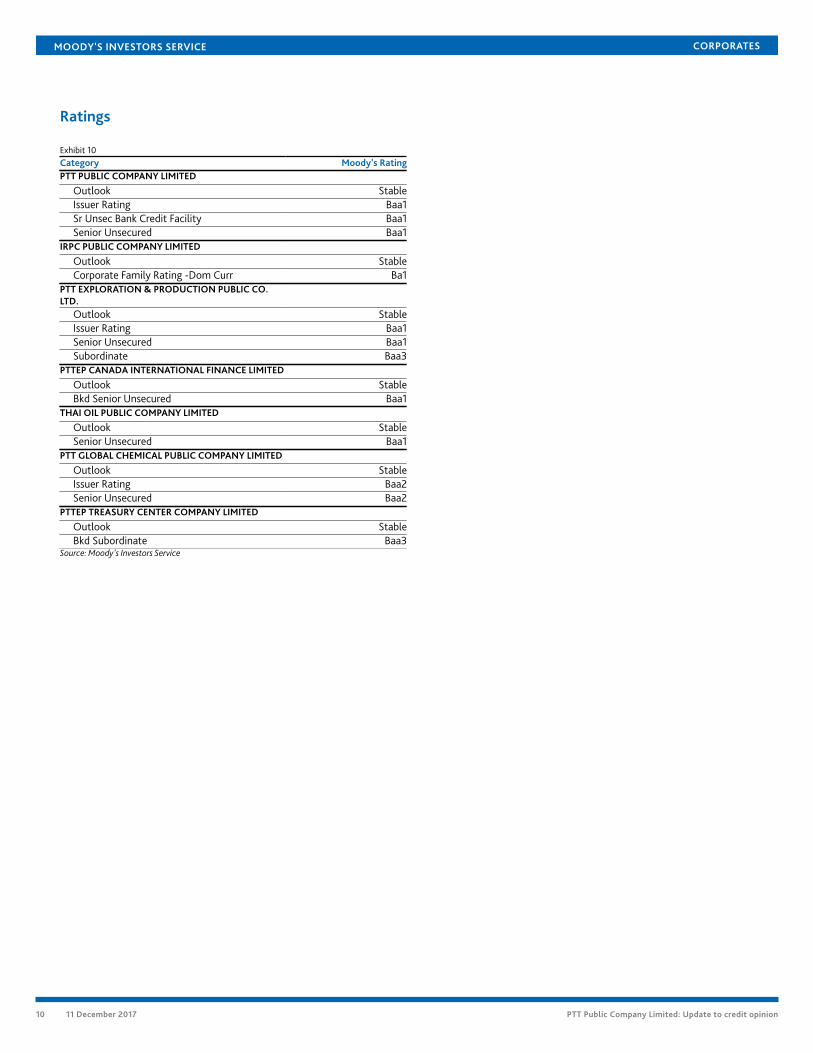

Ratings

Exhibit 10Category Moody's RatingPTT PUBLIC COMPANY LIMITED

Outlook StableIssuer Rating Baa1Sr Unsec Bank Credit Facility Baa1Senior Unsecured Baa1

IRPC PUBLIC COMPANY LIMITED

Outlook StableCorporate Family Rating -Dom Curr Ba1

PTT EXPLORATION & PRODUCTION PUBLIC CO.LTD.

Outlook StableIssuer Rating Baa1Senior Unsecured Baa1Subordinate Baa3

PTTEP CANADA INTERNATIONAL FINANCE LIMITED

Outlook StableBkd Senior Unsecured Baa1

THAI OIL PUBLIC COMPANY LIMITED

Outlook StableSenior Unsecured Baa1

PTT GLOBAL CHEMICAL PUBLIC COMPANY LIMITED

Outlook StableIssuer Rating Baa2Senior Unsecured Baa2

PTTEP TREASURY CENTER COMPANY LIMITED

Outlook StableBkd Subordinate Baa3

Source: Moody's Investors Service

10 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

© 2017 Moody’s Corporation, Moody’s Investors Service, Inc., Moody’s Analytics, Inc. and/or their licensors and affiliates (collectively, “MOODY’S”). All rights reserved.

CREDIT RATINGS ISSUED BY MOODY'S INVESTORS SERVICE, INC. AND ITS RATINGS AFFILIATES (“MIS”) ARE MOODY’S CURRENT OPINIONS OF THE RELATIVE FUTURE CREDITRISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES, AND MOODY’S PUBLICATIONS MAY INCLUDE MOODY’S CURRENT OPINIONS OF THERELATIVE FUTURE CREDIT RISK OF ENTITIES, CREDIT COMMITMENTS, OR DEBT OR DEBT-LIKE SECURITIES. MOODY’S DEFINES CREDIT RISK AS THE RISK THAT AN ENTITYMAY NOT MEET ITS CONTRACTUAL, FINANCIAL OBLIGATIONS AS THEY COME DUE AND ANY ESTIMATED FINANCIAL LOSS IN THE EVENT OF DEFAULT. CREDIT RATINGSDO NOT ADDRESS ANY OTHER RISK, INCLUDING BUT NOT LIMITED TO: LIQUIDITY RISK, MARKET VALUE RISK, OR PRICE VOLATILITY. CREDIT RATINGS AND MOODY’SOPINIONS INCLUDED IN MOODY’S PUBLICATIONS ARE NOT STATEMENTS OF CURRENT OR HISTORICAL FACT. MOODY’S PUBLICATIONS MAY ALSO INCLUDE QUANTITATIVEMODEL-BASED ESTIMATES OF CREDIT RISK AND RELATED OPINIONS OR COMMENTARY PUBLISHED BY MOODY’S ANALYTICS, INC. CREDIT RATINGS AND MOODY’SPUBLICATIONS DO NOT CONSTITUTE OR PROVIDE INVESTMENT OR FINANCIAL ADVICE, AND CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT AND DO NOTPROVIDE RECOMMENDATIONS TO PURCHASE, SELL, OR HOLD PARTICULAR SECURITIES. NEITHER CREDIT RATINGS NOR MOODY’S PUBLICATIONS COMMENT ON THESUITABILITY OF AN INVESTMENT FOR ANY PARTICULAR INVESTOR. MOODY’S ISSUES ITS CREDIT RATINGS AND PUBLISHES MOODY’S PUBLICATIONS WITH THE EXPECTATIONAND UNDERSTANDING THAT EACH INVESTOR WILL, WITH DUE CARE, MAKE ITS OWN STUDY AND EVALUATION OF EACH SECURITY THAT IS UNDER CONSIDERATION FORPURCHASE, HOLDING, OR SALE.

MOODY’S CREDIT RATINGS AND MOODY’S PUBLICATIONS ARE NOT INTENDED FOR USE BY RETAIL INVESTORS AND IT WOULD BE RECKLESS AND INAPPROPRIATE FORRETAIL INVESTORS TO USE MOODY’S CREDIT RATINGS OR MOODY’S PUBLICATIONS WHEN MAKING AN INVESTMENT DECISION. IF IN DOUBT YOU SHOULD CONTACTYOUR FINANCIAL OR OTHER PROFESSIONAL ADVISER. ALL INFORMATION CONTAINED HEREIN IS PROTECTED BY LAW, INCLUDING BUT NOT LIMITED TO, COPYRIGHT LAW,AND NONE OF SUCH INFORMATION MAY BE COPIED OR OTHERWISE REPRODUCED, REPACKAGED, FURTHER TRANSMITTED, TRANSFERRED, DISSEMINATED, REDISTRIBUTEDOR RESOLD, OR STORED FOR SUBSEQUENT USE FOR ANY SUCH PURPOSE, IN WHOLE OR IN PART, IN ANY FORM OR MANNER OR BY ANY MEANS WHATSOEVER, BY ANYPERSON WITHOUT MOODY’S PRIOR WRITTEN CONSENT.

All information contained herein is obtained by MOODY’S from sources believed by it to be accurate and reliable. Because of the possibility of human or mechanical error as wellas other factors, however, all information contained herein is provided “AS IS” without warranty of any kind. MOODY'S adopts all necessary measures so that the information ituses in assigning a credit rating is of sufficient quality and from sources MOODY'S considers to be reliable including, when appropriate, independent third-party sources. However,MOODY’S is not an auditor and cannot in every instance independently verify or validate information received in the rating process or in preparing the Moody’s publications.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability to any person or entity for anyindirect, special, consequential, or incidental losses or damages whatsoever arising from or in connection with the information contained herein or the use of or inability to use anysuch information, even if MOODY’S or any of its directors, officers, employees, agents, representatives, licensors or suppliers is advised in advance of the possibility of such losses ordamages, including but not limited to: (a) any loss of present or prospective profits or (b) any loss or damage arising where the relevant financial instrument is not the subject of aparticular credit rating assigned by MOODY’S.

To the extent permitted by law, MOODY’S and its directors, officers, employees, agents, representatives, licensors and suppliers disclaim liability for any direct or compensatorylosses or damages caused to any person or entity, including but not limited to by any negligence (but excluding fraud, willful misconduct or any other type of liability that, for theavoidance of doubt, by law cannot be excluded) on the part of, or any contingency within or beyond the control of, MOODY’S or any of its directors, officers, employees, agents,representatives, licensors or suppliers, arising from or in connection with the information contained herein or the use of or inability to use any such information.

NO WARRANTY, EXPRESS OR IMPLIED, AS TO THE ACCURACY, TIMELINESS, COMPLETENESS, MERCHANTABILITY OR FITNESS FOR ANY PARTICULAR PURPOSE OF ANY SUCHRATING OR OTHER OPINION OR INFORMATION IS GIVEN OR MADE BY MOODY’S IN ANY FORM OR MANNER WHATSOEVER.

Moody’s Investors Service, Inc., a wholly-owned credit rating agency subsidiary of Moody’s Corporation (“MCO”), hereby discloses that most issuers of debt securities (includingcorporate and municipal bonds, debentures, notes and commercial paper) and preferred stock rated by Moody’s Investors Service, Inc. have, prior to assignment of any rating,agreed to pay to Moody’s Investors Service, Inc. for appraisal and rating services rendered by it fees ranging from $1,500 to approximately $2,500,000. MCO and MIS also maintainpolicies and procedures to address the independence of MIS’s ratings and rating processes. Information regarding certain affiliations that may exist between directors of MCO andrated entities, and between entities who hold ratings from MIS and have also publicly reported to the SEC an ownership interest in MCO of more than 5%, is posted annually atwww.moodys.com under the heading “Investor Relations — Corporate Governance — Director and Shareholder Affiliation Policy.”

Additional terms for Australia only: Any publication into Australia of this document is pursuant to the Australian Financial Services License of MOODY’S affiliate, Moody’s InvestorsService Pty Limited ABN 61 003 399 657AFSL 336969 and/or Moody’s Analytics Australia Pty Ltd ABN 94 105 136 972 AFSL 383569 (as applicable). This document is intendedto be provided only to “wholesale clients” within the meaning of section 761G of the Corporations Act 2001. By continuing to access this document from within Australia, yourepresent to MOODY’S that you are, or are accessing the document as a representative of, a “wholesale client” and that neither you nor the entity you represent will directly orindirectly disseminate this document or its contents to “retail clients” within the meaning of section 761G of the Corporations Act 2001. MOODY’S credit rating is an opinion asto the creditworthiness of a debt obligation of the issuer, not on the equity securities of the issuer or any form of security that is available to retail investors. It would be recklessand inappropriate for retail investors to use MOODY’S credit ratings or publications when making an investment decision. If in doubt you should contact your financial or otherprofessional adviser.

Additional terms for Japan only: Moody's Japan K.K. (“MJKK”) is a wholly-owned credit rating agency subsidiary of Moody's Group Japan G.K., which is wholly-owned by Moody’sOverseas Holdings Inc., a wholly-owned subsidiary of MCO. Moody’s SF Japan K.K. (“MSFJ”) is a wholly-owned credit rating agency subsidiary of MJKK. MSFJ is not a NationallyRecognized Statistical Rating Organization (“NRSRO”). Therefore, credit ratings assigned by MSFJ are Non-NRSRO Credit Ratings. Non-NRSRO Credit Ratings are assigned by anentity that is not a NRSRO and, consequently, the rated obligation will not qualify for certain types of treatment under U.S. laws. MJKK and MSFJ are credit rating agencies registeredwith the Japan Financial Services Agency and their registration numbers are FSA Commissioner (Ratings) No. 2 and 3 respectively.

MJKK or MSFJ (as applicable) hereby disclose that most issuers of debt securities (including corporate and municipal bonds, debentures, notes and commercial paper) and preferredstock rated by MJKK or MSFJ (as applicable) have, prior to assignment of any rating, agreed to pay to MJKK or MSFJ (as applicable) for appraisal and rating services rendered by it feesranging from JPY200,000 to approximately JPY350,000,000.

MJKK and MSFJ also maintain policies and procedures to address Japanese regulatory requirements.

REPORT NUMBER 1100238

11 11 December 2017 PTT Public Company Limited: Update to credit opinion

MOODY'S INVESTORS SERVICE CORPORATES

Contacts

Rachel Chua [email protected]

Laura Acres +65.6398.8335MD-Corporate [email protected]

CLIENT SERVICES

Americas 1-212-553-1653

Asia Pacific 852-3551-3077

Japan 81-3-5408-4100

EMEA 44-20-7772-5454

12 11 December 2017 PTT Public Company Limited: Update to credit opinion