publication 3372 tigta semiannual report

TRANSCRIPT

TreasuryInspector General

for TaxAdministration

“Taxes are what we pay for a civilized society”

– Oliver Wendell Holmes

Semiannual Report to the Congress

October 1, 1998 – March 31, 1999

First Edition

…the 105th Congress created a statutory Inspector General,specifically for oversight of the Internal Revenue Service

…Section 1103 of Public Law 105-206, The InternalRevenue Service Restructuring and Reform Act of 1998,enacted July 22, 1998…

“The Treasury Inspector General for Tax Administrationshall exercise all duties and responsibilities of an InspectorGeneral of an establishment with respect to the Departmentof the Treasury and the Secretary of the Treasury on allmatters relating to the Internal Revenue Service. TheTreasury Inspector General for Tax Administration shallhave sole authority under this Act to conduct an audit orinvestigation of the Internal Revenue Service OversightBoard and the Chief Counsel for the Internal RevenueService.”

April 30, 1999

MEMORANDUM FOR SECRETARY RUBIN

FROM: Lawrence W. RogersActing Treasury Inspector General for Tax Administration

SUBJECT: Treasury Inspector General for Tax Administration Semiannual

Report to the Congress

It was an honor to serve as the Treasury Department's Transition team leader, and recently asActing Treasury Inspector General, to establish the new Office of the Inspector General for TaxAdministration (TIGTA). I want to acknowledge the highly dedicated and professional people ofthe former Internal Revenue Service (IRS) Office of Chief Inspector. Since the InspectionService was created in 1952, they have served with honor and distinction in their contributions tothe IRS, the Department and the taxpayers. They also demonstrated that same commitment anddedication to duty during the recent transition to the newest statutory Office of InspectorGeneral.

I also would like to thank Nancy Killefer, Assistant Secretary for Management and ChiefFinancial Officer, and Charles O. Rossotti, Commissioner of the IRS, for their assistance andstewardship in completing the transition to begin business as the Office of Treasury InspectorGeneral for Tax Administration on January 18, 1999.

The executives, managers and staff of the TIGTA faced great challenges in making vast changesin independence, organization, procedures, and restructuring in a short time. A significantamount of senior management and staff were diverted from their usual work conducting auditsand investigations to implementing the legislative requirements of the IRS Restructuring andReform Act of 1998. The result was the newest and third largest Inspector General in the FederalGovernment.

I am pleased and proud to provide our first Semiannual Report for you to transmit to theCongress. This report includes the accomplishments of the TIGTA since January 18, and the IRSInspection Service from October 1, 1998, through January 17, 1999.

I can report that the entire staff of the TIGTA looks forward to working with you and theDepartmental Officials to insure the highest degree of independence while working closely withthe IRS as we watch over the nation’s tax administration system.

Attachment

Semiannual Report to the Congress

March 31, 1999

Office of The Treasury Inspector Generalfor Tax Administration

Table of Contents

General Information Page 1

Office of Audit Page 9

Office of Investigations Page 23

National Integrity Program Page 31

Statistical Reports - Audit• Questioned Costs• Funds Put to Better Use• Additional Quantifiable Impacts on Tax Administration

Appendix I

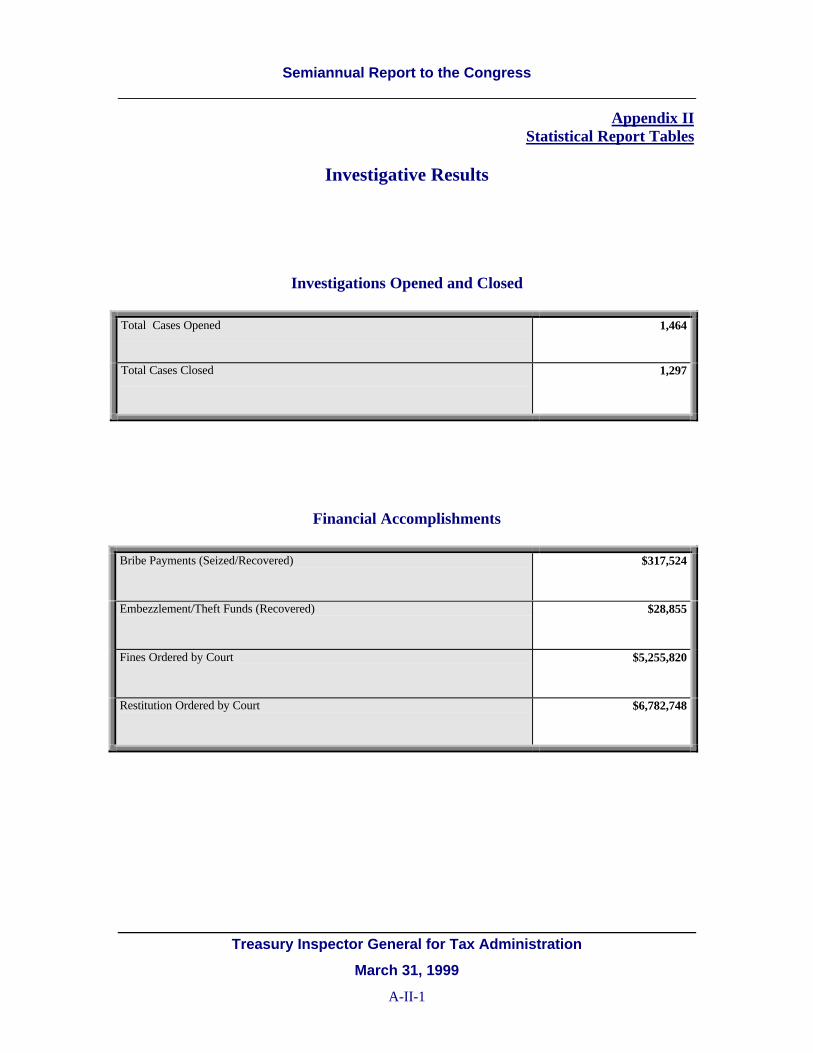

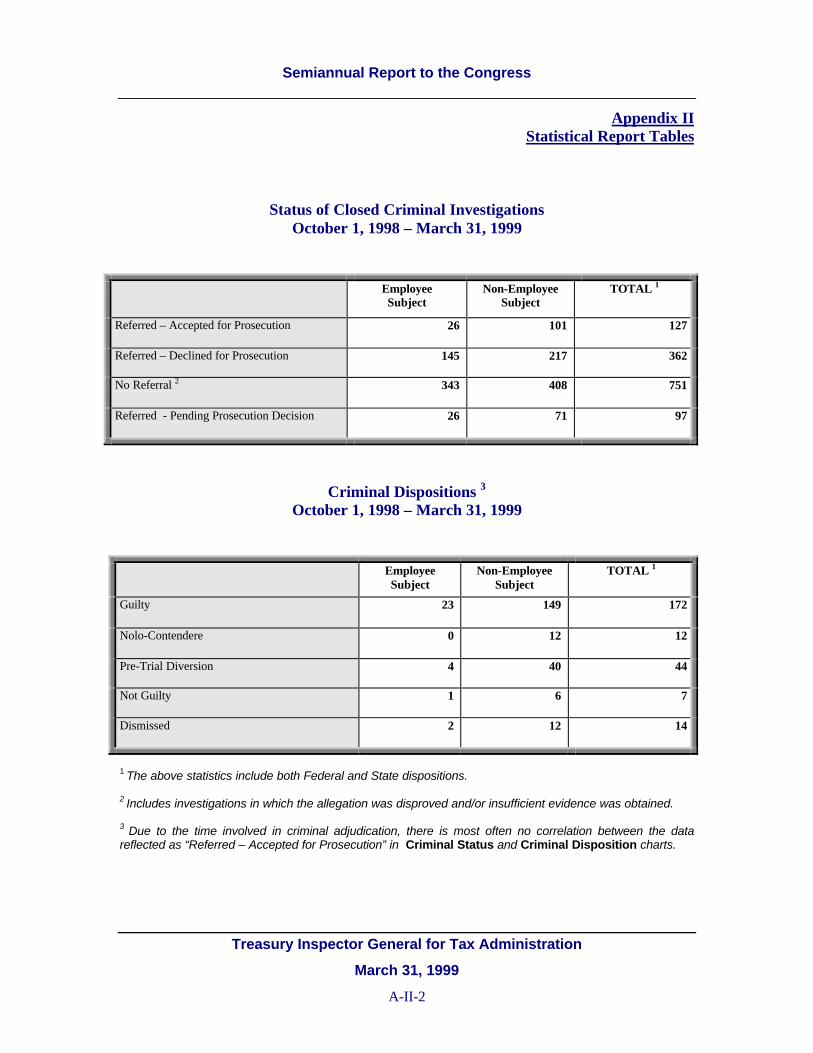

Statistical Reports - Investigations• Investigations

q Opened/Closedq Financial Accomplishmentsq Status of Closed Criminal Investigationsq Criminal Dispositions

• Complaints/Allegations Received –q TIGTAq IRSq Administrative Status and Dispositions

Appendix II

Statistical Reports - Other• Unimplemented Corrective Actions• Access to Information• Prior Reporting Period – No Management Response• Revised Management Decisions• Disputed Audit Recommendations• Review of Legislation and Regulations

Appendix III

Audit Report Listing – October 1, 1998 through March 31, 1999 Appendix IV

RRA98 Section 1203 Standards Appendix V

RRA98/IRC/Other Mandated TIGTA Reporting Requirements Appendix VI

Organizational Chart Appendix VII

Acronyms Appendix VIII

Report Cross-Reference - IG Act/RRA98/Other ReportingRequirements

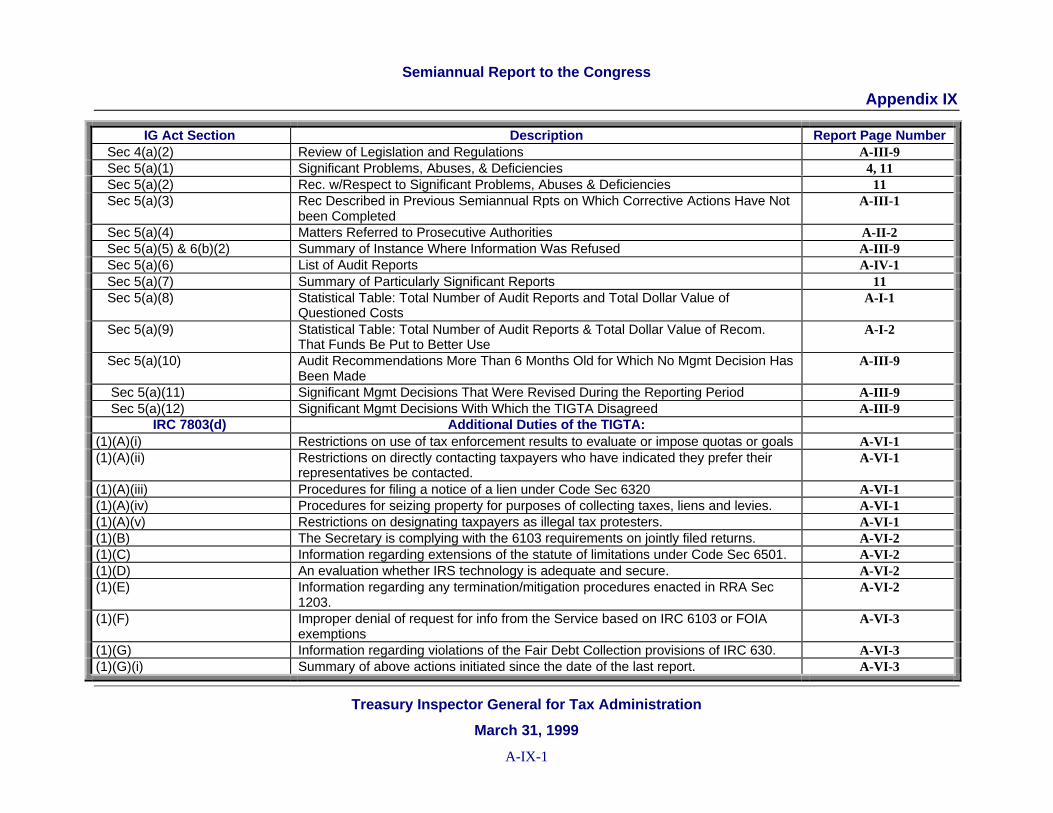

Appendix IX

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

Senate Finance Committee ConductedHearings of IRS Activities

Office of The Treasury Inspector Generalfor Tax Administration

Recent Legislation Createdthe Newest Statutory InspectorGeneral

In July 1998, the Congress passed the InternalRevenue Service Restructuring and ReformAct of 1998 (RRA98), and created the neweststatutory Office ofInspector General, theTreasury InspectorGeneral for Tax Admin-istration (TIGTA).

This latest amendmentto the Inspector General(IG) Act of 1978 addedthe TIGTA to executeall duties and respon-sibilities of an InspectorGeneral with respect tothe Department and the Secretary of theTreasury on all matters relating to the InternalRevenue Service (IRS), including those of theIRS Oversight Board and the IRS Office ofChief Counsel.

This change in the IG Act, effectiveJanuary 18, 1999, transferred to TIGTA, allthe powers and responsibilities of the formerIRS Office of Chief Inspector, except forconducting background checks of andproviding physical security to IRS employees.

Treasury Order 115-01, dated January 14,1999, delineates the specifics of theauthorities granted to the TIGTA by law andthose delegated by the Secretary of theTreasury. Treasury Directive 27-14, datedJanuary 15, 1999, describes the organizationand functions of the TIGTA. A TIGTAorganizational chart is appended to this report.

Information About The TreasuryInspector General for TaxAdministration

The TIGTA is organizationally placed withinthe Department of the Treasury, but isindependent of the Department and all other

offices andagencies withinthe Department.

Under super-vision of theTIGTA are aDeputy, threeAssistant Inspect-ors General(Audit, Investi-gations, and

ManagementServices), an Office of Counsel and animmediate staff.

The TIGTA provides leadership andcoordination and recommends policy foractivities designed to:

• promote economy, efficiency,and effectiveness in theadministration of the internalrevenue laws; and,

• prevent and detect fraud andabuse in the programs andoperations of the IRS andrelated entities.

The TIGTA is responsible for:

• conducting and supervisingindependent and objectiveaudits and investigationsrelating to IRS programs andoperations;

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

2

• protecting the IRS againstexternal attempts to corruptor threaten its employees;

• reviewing and makingrecommendations regardingexisting and proposedlegislation and regulationsrelating to the programs andoperations of the IRS;

• recommending actions toresolve fraud and otherserious problems, abusesand deficiencies in theprograms and operations ofthe IRS; and,

• informing the Secretary andthe Congress of theseproblems and the progressmade in resolving them.

As of March 27, 1999 (pay period endeddate), the TIGTA staff totaled 980 as follows:

Audit 393

Investigations 455

InformationTechnology

90

Other 42

Authorities

The Treasury Inspector General for TaxAdministration (TIGTA) has all theauthorities granted under the InspectorGeneral Act of 1978. In addition, the TIGTAhas access to tax information in theperformance of its responsibilities and theauthority to report criminal violations directlyto the Department of Justice. The TIGTA andthe Commissioner of IRS have establishedpolicies and procedures delineatingresponsibilities to investigate offenses underthe internal revenue laws.

The TIGTA provides a program ofcomprehensive Audit and Investigativeservices of IRS operations and activities. Thisincludes a national integrity programemphasizing deterrence and detectionapproaches to assist IRS in ensuring thehighest degree of integrity and ethics in itsworkforce.

Resources from the TIGTA Offices of Audit,Investigations and Information Technologyare jointly utilized to:

• inform IRS executives andmanagers of the importance ofestablished internal controls bothto protect Government assets andrevenue from fraud and to protectIRS employees from temptations;

• proactively identify additionalviolators of fraud based onprofiles of existing crimes;

• identify for investigation,suspicious instances of computerbrowsing through comparisonsagainst established computerizedpatterns; and,

• report to the Secretary of theTreasury, the IRS Commissioner,and the IRS Oversight Board,internal control weaknesses thatresulted in fraud, along withrecommendations to correct thedeficiencies.

In addition to these duties and responsibilities,the RRA98 amended the IG Act of 1978, 5USC, Appendix 3, Section 8D to give TIGTAstatutory authority to carry firearms andenforce the provisions of Title 26, USCSection 7608(b)(2). These functions includethe law enforcement authority to execute andserve search warrants, serve subpoenas, andmake arrests.

The TIGTA also has responsibility forinvestigating allegations of misconduct on allIRS employees, including the IRS Chief

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

3

Counsel and the IRS Oversight Board.Previously, these responsibilities were splitbetween the IRS Inspection Service and theTreasury Inspector General, generally basedon the grade level of the employees.

Information About Our Clients,Taxpayers and the InternalRevenue Service

The Internal Revenue Service (IRS) collectsover $1.7 trillion annually, or approximately95 percent of the budget needed to fund thenation's government. This is no smallachievement, since it requires the processingof over 200 million returns, issuing over80 million refunds, distributing over 1 billionforms and publications, and servicing over110 million taxpayers.

As of March 27, 1999 (pay period endeddate), IRS employed 116,391 permanent andtemporary employees as follows:

Description Number

Support Services 7,320Submission Processing 28,606Customer Service 29,302Taxpayer Advocate 615Criminal Investigations 4,455Examination 20,652Research/Statistics ofIncome

831

Information Systems 7,195Collections 10,134Legal Services 2,615Appeals 2,161Employee Plans/ExemptOrganizations 2,015International 490

Total 116,391

TIRS must continually strive to achieve thesetasks while maintaining the highest level ofintegrity and assuring taxpayer privacy. TheIRS must enforce tax laws to ensure that allparts of the taxpaying public pay the properamount of tax.

In addition to these daily challenges, the IRSentered Fiscal Year (FY) 1999 facing some ofthe most extensive and complex legislationsince the Tax Reform Act of 1986. TheTaxpayer Relief Act of 1997 imposednumerous tax law changes and will requireextensive reprogramming of systems, changesto forms and instructions, and training for IRSemployees.

When fully implemented, the IRSRestructuring and Reform Act of 1998(RRA98) will result in enhanced taxpayerprotection and rights and organizationalchanges intended to achieve a more efficientand responsive IRS.

RRA98 was passed, due in part tocongressional hearings which focused on themisuse of enforcement statistics and abusivetreatment of taxpayers. Several taxpayerstestified to unfair and unreasonable treatmentby IRS employees. The new legislation alsomandates a change in the basic way the IRSdoes business.

Commissioner Rossotti describes the changesas serving taxpayers better by building a newIRS. In the months since passage of RRA98,the Commissioner has been moving to makemajor changes to modernize the IRS. Theconcept for modernizing the Internal RevenueService is much more than changing theorganization structure. It is a completechange in how the IRS does business. TheIRS must shift its focus from internaloperations to the taxpayer's point of view.

It is important to recognize the unparalleledenormity of what the IRS will undergo as aresult of this legislation. The five majorefforts involved in implementing the conceptare to:

During congressional hearings, severaltaxpayers testified to unfair andunreasonable treatment by IRS employees.

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

4

• reorganize around the needs of itscustomers, the taxpayers;

• improve business practices fromcustomer education to filingassistance to collection;

• establish clear responsibilities andmanagement roles for each divisionwith accountability for meeting theneeds of that group of taxpayers;

• establish necessary measures fororganizational performance thatbalances business results, customersatisfaction, and employeesatisfaction and productivity; and,

• replace outdated computer systemswith new systems that will supportthe new mission and goals.

Further complicating IRS' tax administrationduties is the upcoming century date changeand how it will affect IRS computer systems.Like the rest of private industry andgovernment, IRS is preparing its systems forthe Year 2000 (Y2K).

Every aspect of tax administration could beaffected by the century date change since allIRS functions rely to some degree onautomated computer processes.

To assist the IRS in meeting these challenges,as well as many other crucial taxadministration initiatives, TIGTA hasdeveloped comprehensive Audit andInvestigation programs for FY 1999.

The TIGTA Audit Program

The Assistant Inspector General for Auditheads the TIGTA Office of Audit and hasestablished a comprehensive method ofstrategic evaluation of IRS programs,activities and functions to expend TIGTA’sAudit function resources in the areas ofhighest vulnerability to the nation’s taxsystem.

The Office of Audit promotes the soundadministration of the nation's tax laws byconducting a number of comprehensive,independent performance and financial auditsof IRS programs, operations, and activities to:

• assess efficiency, economy,effectiveness and programaccomplishments;

• ensure compliance with applicablelaws and regulations; and,

• prevent, detect, and deter fraud, waste,and abuse.

In a January 20, 1999, letter, the Office ofAudit advised the Chairman, Subcommitteeon Oversight of the House of RepresentativesCommittee on Ways and Means, of the mostserious management issues facing IRS.

The TIGTA reported that the greatestcollective risks to tax administration are the1999 and 2000 income tax filing seasons dueto several convergent factors. During thatperiod, the IRS must address the year 2000date change challenge, major changes in thetax law, and replacement of majorcomponents of the tax processing system.

In addition, the IRS will face the challenge ofthe consolidation of the mainframe computeroperations of its 10 current processing servicecenters nationwide (methodologies that beganin 1961) into two computing centers. Themost significant management issues facingthe IRS include:

• processing returns andimplementing tax law changesduring the tax filing season;

The TIGTA recently advised the HouseWays and Means Committee on the mostsignificant tax administrationvulnerabilities.

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

5

• progressing in its Year 2000compliance efforts;

• implementing the IRSRestructuring and Reform Actof 1998 -

q Taxpayer Protection andRights

q Information TechnologyInvestment Management

q Quality Telephone andWalk-In CustomerService

• minimizing tax filing fraudand protecting the revenue;

• implementing the Govern-ment Performance and ResultsAct;

• selecting and controlling taxreturns for examination; and,

• managing its finances.

The Office of Audit's program supportsinitiatives involving information technologyprograms, Year 2000 conversion plans,financial reviews, tax filing season activities,Government Performance and Results Act(GPRA) implementation, taxpayer protectionand rights, and other critical IRS activities.

Details of these and other program activitiescan be found in the Office of Audit section ofthis report (begins on page 9).

The TIGTA Investigation Program

The Assistant Inspector General forInvestigations heads the TIGTA Office ofInvestigations and conducts investigations andprobes to provide IRS and Treasurymanagement with independent investigativeproducts that:

• protect IRS employees againstexternal attempts to corrupt orthreaten its employees;

• promote the efficient and effectiveadministration of the tax laws;and,

• detect and deter fraud and abusein IRS programs and operations.

The Office of Investigations is committed toensuring that complaints or allegations ofcriminal misconduct and seriousadministrative wrongdoing are independentlyand objectively investigated.

Investigations that result in administrativeviolations are referred to IRS managementofficials for appropriate action. Investigationsinvolving apparent criminal offenses arepresented to U.S. Attorney offices forprosecutive merit and determination.

The Office of Investigations programactivities are designed to protect the integrityof the IRS. The Office of Investigationsdischarges this responsibility throughproactive and reactive investigative programs.

The investigative program activities aredesigned to protect the integrity of the IRSand to protect IRS employees againstexternal attempts to corrupt or threaten themwhen carrying out their responsibilities.

In addition, the Office of Investigations iscommitted to providing the highest priority interms of the responsiveness in investigatingthreats and assaults against IRS employees.

The Office of Investigations has placedincreased emphasis on investigatingallegations of serious administrativemisconduct involving IRS employees.Section 1203 of RRA98 established amandatory penalty of removal for IRS

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

6

employees who commit certain acts oromissions in the performance of theemployee’s official duties. Included in the listof standards are falsifying or destroyingdocuments to conceal mistakes; willful failureto obtain required approvals authorizingseizure of taxpayer assets, making falsestatements under oath, etc. For a complete listof the Section 1203 violations, seeAppendix V.

The Office of Investigations reviewsallegations of taxpayer abuse received byTIGTA and makes a determination whetherthere is sufficient information to warrant theinitiation of an investigation. To ensure thatdiscipline relative to violations of the new lawis consistent at all levels within the IRS, anIRS Review Board was established to reviewall cases where there has been a determinationthat a violation of Section 1203 has occurred.

In addition, the Office of Investigationsinvestigates other prohibited activitiesspecified in RRA98 and the IG Act, includingthose relating to the use of enforcementstatistics for performance evaluations and thesetting of performance goals by IRSmanagement officials.

Details of these and other TIGTAinvestigative program activities are located inthe Office of Investigations section of thisreport (begins on page 23).

The TIGTA National IntegrityProgram

The TIGTA National Integrity Program ismanaged by the Office of Investigations, withsupport from the Office of Audit andTIGTA’s Office of Information Technology.

The National Integrity Program wasestablished in 1994, to aggressively detectwrongdoing within the IRS. Established onthe premise that a proactive approach wouldidentify areas of fraud that would otherwisego undetected, the first segment of the

National Integrity Program involves sharingwith IRS executives and managers identifiedareas of weak internal controls and theresulting employee fraud that occurred.

One goal is to foster an understanding of theimportance of established internal controlsystems, both to protect the Government fromlosses, and employees from temptations.

The second segment of the proactive NationalIntegrity Program involves two avenues:

• evaluating actual instances ofcriminal activity, developing acomputer "profile" of theimproper transactions, andmatching that profile againstmassive volumes of otheraccount transactions toidentify other violators; and,

• matching predefined scenariosof computer browsingactivities against the IRS'millions of audit trailtransactions recorded on itsIntegrated Data RetrievalSystem and other computerdatabases.

These national integrity projects wereincluded in Computer Matching Actagreements approved by the TreasuryDepartment's Data Integrity Board andannounced in the Federal Register.

Proactive detection focuses on profilingknown crimes and computer browsingpatterns and using computer applicationsto identify additional indicators of similarviolations.

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

7

In addition, internal control weaknesses thatpermitted the employee fraud to goundetected are reported to IRS executivemanagement with recommendations forcorrective actions.

Details of these and other program activitiescan be found in the National IntegrityProgram section of this report (begins onpage 31).

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

9

Treasury Inspector General for Tax AdministrationOffice of Audit

INTRODUCTION

The Assistant InspectorGeneral for Audit(AIGA) is under thegeneral supervision ofthe TIGTA. The AIGAoversees the Office ofAudit and is respon-sible for the develop-ment and execution ofthe nationwide auditprogram for InternalRevenue Service (IRS)activities and opera-tions, including theactivities of the IRS’ Oversight Board andOffice of Chief Counsel.

The mission of the Office of Audit is topromote the sound administration of thenation’s tax laws by conductingcomprehensive, independent performance andfinancial audits of IRS programs andoperations to:

• assess efficiency, economy,effectiveness and programaccomplishments;

• ensure compliance with appli-cable laws and regulations; and,

• prevent, detect, and deter fraud,waste and abuse.

Audit recommendations are made to:

• improve tax administrationservices;

• strengthen controls over IRSprograms and operations; and,

• timely report on program andoperational deficiencies.

In addition, the Officeof Audit works withthe Office of Investi-gations, as appropriate,in response to allega-tions of misconduct,fraudulent activities,waste, and abuse.

The Office of Auditalso participates withthe Office of Investi-gations in the TIGTANational Integrity

Program. (See the National Integrity Programsection of this report for information on jointaudit and investigations efforts involvingproactive integrity projects.)

AUDIT PLANNING

To accomplish its mission, the Office of Auditdeveloped and published an annual audit plan,which describes the audit focus and directionfor FY 1999. The FY 1999 plan includes bothmandatory audits required by Federal statuteor regulation and discretionary audit workapproved by the AIGA.

Mandatory Audit Coverage

Mandatory audit coverage includesinformation technology, taxpayer protectionand rights, contracting and the GovernmentPerformance and Results Act (GPRA). SeeAppendix VI for a listing of mandatory auditrequirements and TIGTA’s status of work onthese audits.

Additionally, the Office of Audit is planningto implement a multi-year audit approach toreviewing IRS’ implementation of GPRA.This Act is intended to improve the quality

TIGTA Annual Audit PlanAnd Audit Reports

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

10

and delivery of government services. The Actalso holds federal agencies accountable forprogram results by emphasizing goal setting,customer satisfaction, and resultsmeasurement.

For FY 1999, the Office of Audit plans toperform high level assessments in the areas ofIRS’ strategic planning process, GPRAcommunication and training process, andperformance measure validity (customersatisfaction, employee satisfaction, andbusiness results). The results of theseassessments will be used to determine thenumber of individual audits needed tothoroughly evaluate IRS’ implementation ofGPRA.

The Office of Audit is also responsible forconducting reviews on the financialoperations of the IRS. In FY 1999, the Officeof Audit staff will perform audit tests insupport of the audit of IRS financialstatements. This assignment is part of atraining effort with the General AccountingOffice (GAO), which has exercised itsauthority to conduct the audit and opine onthe IRS financial statements for FY 1999.Involvement will better position the Office ofAudit to eventually assume responsibilityfrom GAO for auditing the IRS financialstatements. In addition, at the request of theDepartment’s Assistant Secretary forManagement/Chief Financial Officer, theOffice of Audit is separately assessing thedesign of and monitoring progress on the IRSaction plan that is addressing IRS’ long-standing problems with financialmanagement.

Discretionary Audit Coverage

Discretionary audit work is dependent on theresources remaining after staff has beenassigned to accomplish the mandatory auditrequirements. The Office of Audit’s planneddiscretionary work was identified through acomprehensive, high-level risk assessment

process, which was designed to prioritizeworkload by focusing on the areas of greatestrisk to IRS.

Each year, the Office of Audit solicits inputand suggestions for audit coverage from theCommissioner and IRS executives. Thosesuggestions are then incorporated into theaudit plan development process. In the future,audit requests also may originate from theCongress and the IRS Oversight Board.

This process applies risk factors to key auditareas in IRS, and documents and summarizesresults to aid the Office of Audit managementin selecting areas for coverage. Risk factorsare the criteria used to identify the relativesignificance of, and the likelihood that,conditions or events may occur that adverselyaffect the organization. Some of the factorsused in evaluating the risks associated withIRS' auditable areas include: impact of newprograms; tax law changes; adequacy andeffectiveness of internal controls; prior auditfindings; and, stakeholder concerns.

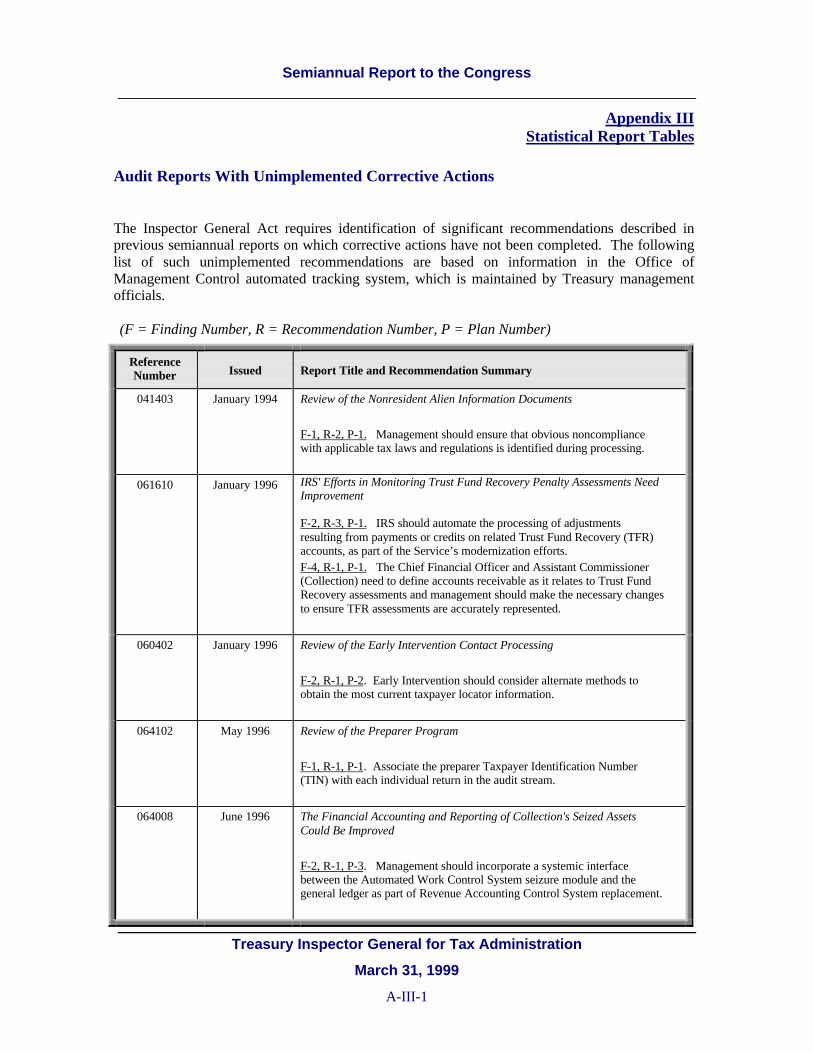

Follow-up on Audit Reports withUnimplemented Corrective Actions

Due to the large number of previously issuedaudit reports with unimplemented correctiveactions (See Appendix III), we are developinga strategic approach in our Fiscal Year 2000audit plan to review the status of each of theserecommendations to determine if:

• the time frame for implemen-tation of the corrective actionseems reasonable;

• the pending corrective actionitem should be closed due tochanging conditions that havemitigated the need foradditional action; or,

• a follow-up audit is warrantedto assess the status of IRS’implementation of thecorrective action.

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

11

SIGNIFICANT AUDIT RESULTS

During this reporting period, the Office ofAudit initiated the majority of its in-processaudits after formulating an annual audit planwhich was based largely on the recentlydeveloped risk assessment process. Themajority of those final audit reports will beissued in the remaining six months ofFY 1999.

The Office of Audit also lost the availabilityof some of its senior management and stafffrom time normally expended on managingand conducting audits, to activity involvingthe legislative requirements of RRA98,including planning and preparation for thenew TIGTA mandated annual reviews and theIRS’ preparations for implementing the manyprovisions of RRA98.

With the remaining direct staff resourcesavailable, the Office of Audit issued 27 auditreports covering topics such as Year 2000Conversion, Filing Season Readiness, andInformation Technology.

Audit resources were focused in the areashaving the most significant and inherent risksto IRS. The results of the most significantreviews are discussed in the followingsections.

Year 2000 (Y2K) ComplianceProgress

The Y2K century date change (CDC) is oneof the most critical problems facing businessand government data processingorganizations. The Y2K problem is extremelycritical for IRS, because the CDC could affectevery aspect of tax administration. Virtuallyall IRS functions, to some degree, rely onautomated computer processes.

To maximize system-processing capabilitiesand to preserve data storage space, many datefields in IRS’ system programs andapplications have been limited to a two-digitrepresentation (i.e., 98 for 1998).

IRS estimates the cost for Y2K changes willbe approximately $850 million through FY1999. These costs include updating andtesting over 80 mainframe computers (Tier Icomputers), 75,000 computer applicationprograms, 1,400 minicomputers (Tier IIcomputers), and 100,000 desktop computers(Tier III computers), as well as datacommunications networks comprising morethan 50,000 individual product components.

IRS management estimates 50 million lines ofprogramming code need to be reviewed forpossible changes. If mission critical code isnot Y2K compliant, IRS systems may not run,causing the processing of tax returns to slowdown or stop.

As a result, taxpayers may not receive timelyrefunds or notices, and account adjustmentsmay not be processed. As the Year 2000approaches, it is imperative that all major tax-processing systems be Y2K compliant toavoid processing shutdowns.

The Office of Audit has conducted severalreviews to assess IRS efforts for ensuring thatall IRS systems (Tier I, II, and III) andprograms are Y2K compliant, includingproject management, inventory and tracking,and software and hardware issues.

December 1999 Su Mo Tu We Th Fr Sa

1 2 3 45 6 7 8 9 10 1112 13 14 15 16 17 1819 20 21 22 23 24 25

26 27 28 29 30 31

January 2000Su Mo Tu We Th Fr Sa 1 2 3 4 5 6 7 8 9 10 11 12 13 14 1516 17 18 19 20 21 2223 24 25 26 27 28 2930 31

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

12

In-process reviews include:

• Preparation of Tier II Systems(minicomputer) for CDC;

• Management Controls forOversight of IRS CDC;

• Y2K Conversion Efforts – TierIII (desktop computers);

• Y2K End-to-End SystemsIntegration Test II and III;

• Effectiveness of Y2K TestingEfforts; and,

• Y2K External Trading PartnerIssues – Phase II.

Highlighted final audit reports include:

Follow-Up Review of CorrectiveActions Resulting from Audit’sPhase III Code Review(Report No. 090102)

TIGTA auditors conducted an on-line reviewof IRS’ Y2K conversion and testing todetermine the effectiveness of efforts inconverting those application components thatcomprise the bulk of the tax processingsystems. (Report No. 083605). As the Y2Ksituation is extremely critical, this follow-upaudit was completed in October 1998 todetermine if the corrective actions, identifiedin the June review, were completed.

During the follow-up review, the Office ofAudit analyzed 32 corrective actions that wereidentified in the previous report, andidentified three significant areas warrantingadditional attention.

The original audit identified 42 componentswhere the date field was defined as acharacter rather than as a numeric field. IRSwas advised that greater adherence and

clarification were needed to IRSprogramming standards to avoid any risk thatthis programming error could affect futureIRS processing.

At the time of the October 1998 follow-upreview, the CDC Project Office had notimplemented a change in IRS’ programmingstandards.

The Office of Audit's report noted twoadditional areas requiring further IRS action.Specifically, the CDC Project Office should:

• coordinate the development andissuance of documentedprocedures for recompiling allIRS programs after the relatedsystem macros are modified; and,

• develop a more aggressiveschedule for ensuring thedevelopment of test deliverablesfor all commercial-off-the-shelf(COTS) products.

The Office of Audit recommended that theCDC Project Office review the originalrecommendations and coordinate thedevelopment and issuance of all documentedprocedures for recompiling all IRS programsafter related system macros are modified.

Also, the testing and certification of all COTSproducts should be made a priority because ofthe potential impact these products could haveon the comprehensive testing effort currentlyunderway.

IRS management agreed with therecommendations and has completed thecorrective action on all reported audit issues.One action included hiring an outsideconsultant to review 100 percent of theprogramming code questioned.

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

13

Evaluation of the Service’s Effortsto Implement Year 2000Compliance for External TradingPartners(Report No. 091303)

In 1996, IRS established the CDC ProjectOffice with an objective to ensure that allsystems are Y2K compliant. This requiresclose coordination with many ExternalTrading Partners (ETPs)—organizations thatexchange data with IRS—including state,local, and foreign governments; banks; andother Federal agencies. The CDC ProjectOffice has encountered delays in completingseveral ETP activities.

The Office of Audit evaluated IRS’ efforts toimplement Y2K compliance of the externaldata exchanges. The Office of Audit reportedthe CDC Project Office has madeconsiderable progress in completing aninventory of external data exchanges andcommunicating IRS’ Y2K format changeswith ETPs.

The Office of Audit recommended that IRSmanagement continue its efforts to ensure thatIRS systems meet Y2K compliant standardsand that discrepancies in the inventory ofexternally exchanged data files and dataexchanges are corrected.

IRS management was responsive to thefindings during this on-line review and hasinitiated corrective action.

Review of Phase 4 Year 2000Conversion and Testing(Report No. 090403)

Based on prior audit recommendations(Report No. 083605), IRS initiated actions toimprove its Y2K certification efforts andimprove the accuracy of its ApplicationsProgram Registry (APR) data. The APRcontains inventory data on the phase, numberand status of Y2K programs by linking thestandardized project name and phase with

IRS’ Integrated Network and OperationsManagement System (INOMS). INOMStracks Automated Data Processing equipmentused throughout IRS.

IRS also is working toward being classified asa Capability Maturity Model Level 2organization to institutionalize effectivemanagement processes for software projects,which will allow for repetition of successfulpractices developed on earlier projects.

The Office of Audit reported that IRS needsto continue with its efforts to improve theaccuracy of the APR, ensure developers andtesters document test activities and givegreater consideration to how Y2Kprogramming changes will affect hardwarecapacity and system performance.

In addition, the Office of Audit noted theCDC Project Office has not establishedcontrols to verify the accuracy of Y2Kcompliance certifications. Since thesecertifications are not validated, the CDCProject Office is unable to fully assess the riskthat exists for programs that are not Y2Kcompliant. IRS management agreed with thefindings and has initiated corrective action.

Review of the Service’s Year 2000Non-Information TechnologyProject(Report No. 090503)

Although Y2K conversion efforts primarilyfocus on information systems, there arenumerous facility systems and personalproperty items that use microchips, software,firmware, or other mechanisms for controllingtime and date logic that could be impacted bythe CDC. These systems comprise the Non-Information Technology (Non-IT)environment.

The Office of Audit reported that IRS hasinitiated steps to prepare its Non-ITenvironment for Y2K. However, a significantamount of work must still be completed to

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

14

ensure Non-IT equipment becomes Y2Kcompliant. In addition, the CDC ProjectOffice needs to enhance its programmanagement efforts to better direct andcoordinate Non-IT conversion activities.

The Office of Audit recommended that theCDC Project Office define and document therequirements for all phases of IRS’ Non-ITconversion process; require supportingfunctions to provide detailed work breakdownschedules; and, determine whether the processused to certify investigative equipment wasappropriate.

Also, IRS’ Office of Management andFinance, in conjunction with the functionalarea chiefs, should ensure all IRS occupiedbuildings are prioritized for conversion. IRSmanagement agreed with the findings and hasinitiated corrective action.

Review of the Service’s Efforts toPrepare Its Tier II Infrastructure forthe Year 2000(Report No. 091206)

This report included the results of the Officeof Audit's review of IRS’ efforts to prepare itsTier II (minicomputer) infrastructure for theCDC.

Although the majority of IRS’ tax processingoccurs at the Tier I (mainframe computer)level, there is a significant amount ofprocessing at the minicomputer level. As aresult, some minicomputer systems feed datato the mainframe computer systems.

The report recommended that IRS betterfocus, manage, and control its CDC effort toassure business continuity. Criticalimprovements are needed for: planning andcoordination of the conversion effort;inventory management; and, contingencyplanning. In addition, IRS managementneeds to ensure consistency between Y2Kneeds and the INOMS instructions to improve

the accuracy and completeness of theinventory.

The Office of Audit identified that theplatform inventory is complete, but nearlyhalf of the 837 platforms reviewed wererecorded inaccurately. The COTS softwareinventory also was incomplete and inaccurate.Approximately 28 percent of the 411 productswere not recorded on INOMS, and 22 percentwere recorded with the incorrect version.

During the audit, IRS management addressedthe issues that the Office of Audit presented.However, the final report was issued withoutIRS management’s response to all reportedissues.

Subsequent to the issuance of the final report,IRS management provided a response and hasinitiated corrective action on all reported auditissues.

Review of the Internal RevenueService’s Effectiveness in theMonitoring and Reporting of Year2000 Funds(Report No. 092204)

The CDC Project Office established a BudgetOffice to obtain, distribute and manage Y2Kappropriated funds. The Budget Office isresponsible for managing InformationSystems (IS) and non-IS funds for the CDCproject and to track budgetary information forthe CDC Project Office, IRS executives, andother internal and external stakeholders.

The Budget Office also is responsible formonitoring and reporting the availability anduse of congressionally mandated funds;unobligated funds transferred from expiredIRS accounts; and, supplemental full timeequivalents (FTEs) from within IRS'operational budget.

IRS has been effective in accounting for itsY2K funds. However, more attention isneeded in the identification of decreasedfunding requirements and the recording of

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

15

Y2K payroll expenditures. While the BudgetOffice uses a working budget report andbiweekly budget meetings for monitoring andassessing additional budget needs, IRSmanagement must become more proactive inidentifying unused funds.

In addition, IRS needs to ensure that completeand accurate information is recorded andreported for Information Systems’ FTEsexpended on Y2K efforts. Further, timecharges to the Y2K Project Cost AccountingSubsystem (PCAS) codes are not complete,accurate, or properly classified.

The Office of Audit recommended that IRSimprove its monitoring procedures ofavailable funds and ensure that appropriatePCAS codes are used and that time chargesare accurately and completely reported. IRSagreed with the findings and has initiatedcorrective action.

Review of the Internal RevenueService’s Year 2000 Efforts toInventory Telecommunications andCommercial Off-the-Shelf Products(Report No. 092402)

The CDC Project Office has the responsibilityfor controlling IRS’ Y2K effort to inventory,convert, upgrade, or replace computer-relatedequipment and software so that all automateddata processing functions continueuninterrupted into Y2K.

The Office of Audit review was conducted toprovide a preliminary assessment of theadequacy of IRS efforts in two areas: theinventory of telecommunications equipment;and, the inventory of system software andCOTS products. Technical expertise for thisreview was acquired under contract.

The review by the Office of Audit indicatedthat CDC still has significant work toaccomplish to complete thetelecommunications inventory and to

reexamine the completeness of the COTSproduct inventory.

To minimize risks associated with inaccurateor incomplete inventories, the Office of Auditrecommended that CDC Project Officemanagement improve its guidance on howthese products are to be reported in theinventory and to re-examine the completenessof its COTS inventory. In addition, anindependent verification of the INOMSinventory of COTS products should beconducted for all Tier I (mainframe) computersystems. IRS management agreed with therecommendations and initiated appropriatecorrective actions.

Review of the Internal RevenueService’s Year 2000 ContingencyPlanning Efforts(Report No. 092705)

The Y2K problem is complicated by the size,complexity, and interdependencies of the IRS’computer systems. The consequences ofsystem failures and the absolute deadlinemake it a critical task for an organization aslarge and as reliant on computers as the IRS.Because of the enormity of the task, there isrisk that all systems will not be converted intime.

The Office of Audit’s review of IRS’contingency plans indicated that IRS has notdevoted sufficient emphasis to Y2Kcontingency planning. The database used fortracking the conversion process wasinaccurate and has not improved. Theunreliable data hinders IRS management’sability to monitor conversion progress andprepare contingency plans for systems at riskof not meeting the conversion deadlines.Even when the data did identify systems atrisk, IRS management did not follow its ownprocesses and did not ensure that contingencyplans were timely developed. In addition,IRS had not properly coordinated the Y2K

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

16

contingency planning efforts with its overallcontingency planning efforts for disasters andother types of failures.

The Office of Audit recommended thefollowing corrective actions:

• review Y2K inventory files on arecurring basis;

• establish validity checks;• establish procedures to identify

and monitor components andsystems that have not completedthe Y2K milestones;

• establish procedures to identify“at risk” systems during thecertification process;

• adhere to the formal ContingencyRequest Memorandum process;

• assign responsibility for the IRS’overall contingency managementstrategy; and,

• consider monitoring the status ofcontingency planning as part ofthe Y2K report.

The Office of Audit did not agree that IRSmanagement’s response adequately addressedthe problems and corrective actions andincluded “auditor comments” in the finalreport transmittal to the Commissioner.

Filing Season Readiness

IRS’ 1999 and 2000 filing seasons will beimpacted by numerous organizational andlegislative changes. Legislation enacted in1997 and 1998 in the Taxpayer Relief Act,Balanced Budget Act, and RRA98 is the mostextensive and complicated legislation IRS hasfaced since the Tax Reform Act of 1986.

The 1999 and 2000 filing seasons will befurther complicated by ongoing efforts tomeet Y2K deadlines, consolidate IRSmainframe processing to two sites, and

implement National Performance Reviewrecommendations.

In light of these changes, the Office of Auditconducted reviews to assess IRS’ ability totimely and effectively process returns, issuerefunds, and answer taxpayer questions.

In-process reviews include:

• Information Systems’ QualityAssurance Over Key Tax Lawsfor 1999 Filing Season;

• Walk-In Assistance On-Line -1999 Filing Season;

• Toll-Free Services During the1999 Filing Season;

• Early Implementation of TaxLaws – 1999 Filing Season;

• 1999 Filing Season Readiness –Individual Master File;

• Taxpayer Assistance on Key TaxLaws – 1999 Filing Season; and,

• Implementation of LegislativeProvisions – Year 2000 FilingSeason, Individual MasterFile/Non-Individual Master File.

Highlighted final audit reports include:

Executive Compilation andInterpretation of the 1998 FilingSeason(Report No. 091903)

The Office of Audit evaluated the 1998 filingseason in terms of the progress IRS wasmaking to become a “customer focused”organization based on the IRSCommissioner’s concept for modernizing IRSand on IRS' Customer Service Task Forcereport, “Reinventing Service at the IRS.”

Success of the 1998 filing season wasdetermined by how IRS prepared for and met

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

17

the needs of taxpayers in the areas of:processing tax returns (both paper andelectronic individual tax returns); issuingtimely refunds; providing customer assistanceat walk-in sites; and, through the expansion oftoll-free telephone service.

The review showed that IRS had a successful1998 filing season. This success includedsignificant increases in the number of returnsfiled electronically, implementation of anumber of tax law changes, and significantimprovements in customer service through theexpansion of toll-free telephone service andthe introduction of Saturday walk-in service.In addition, IRS was able to process returnsaccurately and issue refunds timely.

The number of electronic returns filed farsurpassed the 1998 goals, which can beattributed to the extensive efforts by IRS toencourage taxpayers to file electronically.

These accomplishments proved to besignificant in meeting taxpayer needs andimproving customer service to meet the IRSCommissioner’s goal of providing first-rateservice to taxpayers. However, the auditresults indicated that improvements can bemade in electronic filing, simplification ofreturn filing, improving customer service andin meeting the challenges for the 1999 filingseason.

The RRA98 goal of 80 percent of tax returnsto be electronically filed by the year 2007poses a difficult challenge and will requireelimination of barriers, such as the additionalcosts to electronically file and therequirements to mail in signature documentsand Form W-2 statements.

In response to the Office of Audit’s report,IRS agreed to explore: the possibility ofproviding a simpler tax form for millions oftaxpayers; raising the dollar tolerance oninterest and dividends for submitting aseparate schedule; and, establishing ataxpayer profile database. The IRS respondedthat unless it gets Congressional approval, it

could not implement the Office of Audit’srecommendation to use “whole dollars only”for all tax return entries to reduce processingerrors and taxpayer burden. The Office ofAudit added an "auditor comment" to the final

report recommending IRS seek the legislativeapproval necessary for the change.

Although IRS is taking several actions nextfiling season to enhance electronic filing, IRSmanagement did not agree that the Office ofAudit’s recommendation to encourageincreased Telefile usage would provide astrong incentive for more taxpayers to use theSystem.

Also, the Commissioner did not agree that theIRS should implement a structured process toquickly identify and react during the filingseason to taxpayer and IRS processingproblems. The Office of Audit remainsconcerned that IRS does not have an adequateprocess to quickly identify and react toprocessing problems during the filing season.

Information Technology

Modernization of IRS’ computer systems andsecurity of taxpayer information have beenmajor concerns over the past several years.Prior efforts to modernize antiquated taxsystems fell short of what is required toprepare IRS for the next century.

RRA98 requires TIGTA to evaluate theadequacy and security of IRS technology onan ongoing basis.

Reviews performed in this area focused onassessing IRS’ progress in implementing itsmodernization initiatives, includingprocurement practices to supportmodernization efforts, and evaluatingInformation Systems’ success in meeting thebusiness needs of operational functions.

In-process reviews include:

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

18

• Integrated Submission andRemittance Processing (ISRP)System – Phase III;

• Readiness for Service CenterMainframe Consolidation;

• Telecommunications Costs andCapacities for MainframeConsolidation;

• Office of Systems Standards andEvaluation;

• Operational Security Controls;

• Logical Access and SecurityControls; and,

• Telecommunications Security ofIRS Computer Systems.

Highlighted final audit reports include:

Review of the IntegratedSubmission and RemittanceProcessing (ISRP) System SoftwareDevelopment and Pilot Activities(Report No. 090903)

The Integrated Submission and RemittanceProcessing (ISRP) System will replace IRS’primary data input systems for processingpaper tax returns and remittance processing—the Distributed Input System and theRemittance Processing System. Thisreplacement is critical because IRS' existingcomputer systems are 13 and 20 years old,respectively, and neither is capable ofprocessing dates beyond the year 1999.

The ISRP systems development project is oneof four critical Information Systems’ projectsmonitored monthly by the Commissioner’sYear 2000 Executive Steering Committee.This review focused on IRS' mission-criticalneed for Y2K compliant systems to processtaxpayers’ paper tax returns.

In January 1998, the Office of Audit issued areport on the Initial System DevelopmentActivities of the ISRP System (Report No.082204). This report identified IRS’aggressive rollout schedule, the absence ofcontingency plans, and increaseddevelopment risks for the ResidualRemittance Processing System (RRPS)functionality.

The primary objective of this review was todetermine if the decisions and activitiesregarding the design, development, andinstallation of the ISRP pilot systems werecomplete and reliable.

The Office of Audit reported mixed results onthe pilot system, and risks remain forsuccessful implementation of a nationwideproduction system. Specifically, the RRPSdemonstrated inconsistent reliability as aproduction system, and neither ISRPsubsystem conclusively demonstratedanticipated productivity gains.

There are additional system design, projectscheduling and resource allocation risks,which management must continue to monitorand address to ensure successful nationwideimplementation before January 1, 2000.

The Office of Audit findings andrecommendations were presented to IRSmanagement during the progress of this on-line review. Any recommendations that werenot immediately addressed by IRSmanagement during the review weresubsequently resolved or acknowledged byIRS management during pilot operations.

Management Oversight Should BeStrengthened to ImproveAdministration of the TreasuryInformation Processing SupportService (TIPSS) Contract(Report No. 090205)

The Treasury Information Processing SupportServices (TIPSS) contract consists of multiple

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

19

contracts to support IRS’ tax systemmodernization efforts.

While TIPSS is assisting IRS in acquiringinformation technology services, there isminimum incentive for the contractor tocontrol costs because TIPSS is a cost-plus-fixed-fee contract. Therefore, it is imperativethat the contract be effectively administered toallow the Service to monitor and evaluate thecontractor’s progress.

The Office of Audit reported that not allcontrols were effective to ensure serviceswere received in accordance with contractprovisions.

In particular the auditors noted that:

• 84 percent of contractor taskorders were issued withoutdefining the contractor’s cost,which may lessen the contractor’smotivation to perform the taskorder as efficiently as possible;

• contractor performance is notbeing timely evaluated eachquarter by the Contracting OfficerTechnical Representatives; and,

• contractors were invoicing IRS forsignificantly fewer hours thanwere originally contracted forunder a term contract.

Under a term contract there is an opportunityto renegotiate the contract when it appears thefull number of hours will not be needed.

However, the report noted that foreight completed term-type task orders, thecontractors invoiced IRS for fewer hours thancontracted. This process allowedapproximately $490,000 in fixed feesassociated with the original contract costs toremain obligated to the contract.Approximately $3,517,000 had not beendeobligated on 28 task orders that had beencompleted for over one year.

Management agreed with the findings and hasinitiated corrective action.

Evaluation of the Service’s Effortsto Acquire a new Federally FundedResearch and Development Center(FFRDC) Contractor(Report No. 091502)

IRS has undertaken a complete redesign andmodernization of its computer-basedinformation processing system. To assist withthe modernization efforts, IRS is soliciting aprime systems integration (PRIME) contractorand another Federally Funded Research andDevelopment Center (FFRDC) contractor tomanage the overall modernization efforts. Byestablishing a FFRDC, IRS can obtaintechnical assistance without anyorganizational conflicts of interest, either realor apparent.

The PRIME contract and the new FFRDCcontract will be used in conjunction withseveral other contracts to implement theplanned modernization. The PRIMEcontractor will implement the modernizationblueprint, and the new FFRDC contractor willvalidate the approach of the PRIMEcontractor to ensure it is consistent with themodernization blueprint.

The report noted that although IRS issoliciting contractors to assist with itsmodernization efforts, additional emphasis isneeded to define the interrelated roles of thevarious contractors to ensure all contractorsremain free from potential conflicts ofinterest. To do so, IRS needs to clearly definethe responsibilities of all contractors involvedin the modernization efforts.

In addition, procurement personnel need totake action to ensure the FFRDC will be freefrom organizational conflicts of interest.

Management agreed with the findings and hasinitiated corrective action.

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

20

Taxpayer Protection and Rights

RRA98 will result in enhanced taxpayerprotection and rights, as well asorganizational changes intended to achieve amore efficient and responsive IRS.

In-process reviews include:

• Impact of Examination Quality onTaxpayer Rights and Burden; and,

• Protecting the Privacy of TaxAccount Disclosures.

Highlighted final audit reports include:

Review of Taxpayer Requests forDisclosure of Tax Information(Report No. 090804)

In FY 1997, IRS received over 1.1 millionrequests for tax return information from thepublic. Requests were made for photocopiesof tax returns or for transcripts of tax returninformation.

Beginning in October 1994, IRS offered toprovide taxpayers with transcripts of returninformation free of charge as an alternative toproviding photocopies of returns at a cost tothe taxpayer of $14. However, providingtranscripts of return information has madeIRS extremely vulnerable to unauthorizeddisclosure of tax return information.

The Office of Audit recommended that IRSimplement the following corrective actions:

• processing controls need to beimproved;

• requirements for the release of taxreturn transcripts needstrengthening; and,

• written requests from taxpayersneed to be properly maintained.

Management agreed with the findings and hasinitiated corrective actions.

IRS Employee Outside EmploymentRequests(Report No. 091804)

The Office of Audit presented control issuesthat were identified during separate integrityreviews in two regions.

Not all employee requests for permission toengage in employment outside the IRS wereproperly received, approved, and/ormonitored by IRS management as required toprevent conflicts of interest between the IRSemployees’ official duties and their outsideemployment. Also, abuses of outsideemployment authorizations were not detected.

The Office of Audit identified one IRSemployee who was preparing tax returns forcompensation and referred 56 other IRSemployees to the Office of Investigations aspossible browsers of tax records for eithertheir outside employers or their spouses’employers. Based on these referrals, twoemployees resigned, and IRS managementremoved one employee and took otherdisciplinary action on other employees.

To improve the internal control weaknesses,the Office of Audit recommended that:

• national guidelines be updated andclarified;

• a one-time resubmission of alloutside employment requests bemade to enable a national clean-up of Labor Relations’ andmanagers’ records;

• employees be reminded thatunauthorized research of the taxrecords of their outsideemployers, or the tax records oftheir spouses’ employers, willsubject them to disciplinaryaction; and,

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

21

• the Totally Automated PersonnelSystem and Outside EmploymentSystem be implemented in eachLabor Relations office that hasthese systems.

Management agreed with therecommendations and has initiated correctiveactions.

Follow Up Review of Parent andDependent Duplicate ExemptionClaims(Report No. 091000)

The Office of Audit issued an audit report in1996 (Report No. 063502) advising IRSmanagement that action was needed to reversethe continuous and costly problem ofduplicate use of Social Security Numbers(SSNs).

IRS management agreed with the auditors’recommendations to minimize both taxpayerburden and the impact on IRS’ resources, andto segment the condition for control andaggressive management. As a result, IRSmanagement placed the Duplicate DependentsProject in its FY 1996 Research Plan.

Since the date this issue was reported, IRSmanagement efforts have shown somepositive results in identifying potentialsolutions for the duplicate SSN problem.However, the initial results are not complete,and IRS management intends to continuetesting.

One test IRS management conducted wascorrespondence examinations on a nationwidesample of repeat taxpayers (those in both theTax Year 1995 and 1994 duplicate SSNpopulations). These examinations resulted inapproximately $3.2 million in adjustments totaxpayers’ accounts.

IRS management agreed with the factspresented in this follow-up report.

Review of Special Projects in theNew Jersey District CollectionDivision(Report No. 093307)

In FY 1998, the Office of Audit performedtwo audits in the New Jersey CollectionDivision that focused on the use of Collectionperformance measures, statistics, and the useof seizure authority. The Office of Auditconcluded that the focus on collectionproductivity, from a national perspective, hadcreated an overall climate that potentially setsthe stage for miscommunications toemployees and managers at all levels of theorganization.

The reports also indicated that the New JerseyDistrict’s strong focus on achievingorganization productivity goals created anatmosphere that impacted front-line collectionoperations in a manner that placed taxpayers’rights at risk. Facts identified in the LiquorLicense Project contributed to this conclusion.

Based on the results of the two audits, theOffice of Audit conducted this review ofspecial projects in the Collection Division.The objective was to determine whetherprojects were established based on soundevidence and support, controlled to ensurethat project objectives were achieved, andmonitored to ensure that taxpayers’ rightswere protected.

IRS has a legitimate need to assist taxpayersin voluntarily meeting their tax obligations bytailoring efforts to the needs of market groups,as well as developing methods to enforcepayment when other alternatives areunsuccessful.

The Office of Audit reported that specialprojects were used to help the New JerseyDistrict Collection Division achieve statisticalgoals, while resulting in mistreatment oftaxpayers. During the audit, the ActingDistrict Director suspended activity on allCollection Division special projects. All

Semiannual Report to the Congress

Treasury Inspector General for Tax Administration

March 31, 1999

22

special projects have now been closed and theTIGTA Office of Investigations is conductinginquiries into some of the report findings.

To strengthen the use of special projects in amanner consistent with both sound taxadministration and concern for taxpayers, theOffice of Audit recommended that the DistrictDirector approve all levy and seizure actionson special project cases. The Office of Auditalso recommended that Collectionmanagement certify that all legal andprocedural requirements are met prior toseizure or levy.

IRS management also should ensure thatenforcement actions taken on special projectcases:

• are consistent with enforcementactions taken on non-projectcases;

• have a sound basis for initiation;and,

• are properly reauthorized whenthere are changes in objectives,scope, or project duration.

Finally, special projects should be adequatelydocumented, and District Counsel shouldreview and approve all locally developednotices used on special projects.

IRS management agreed with the findings andhas initiated corrective action.

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

23

Investigation Badges 1952 - 1999

Treasury Inspector General for Tax AdministrationOffice of Investigations

INTRODUCTION

The TIGTA Officeof Investigations isresponsible for thedevelopment andexecution of thenationwide investi-gative programsrelating to oversightof activities of theInternal RevenueService (IRS) and itsoperations.

The Office of Investigations is responsible forprotecting the integrity of the IRS and forprotecting employees of the IRS and relatedentities against external attempts to corrupt orthreaten them when carrying out theirresponsibilities. This includes investigatingallegations of criminal wrongdoing andserious administrative misconduct by IRSemployees.

Other areas of responsibility include:

• administering programs to protectIRS employees from violence;

• operating a national complaintscenter, including a hotline, toreceive and process allegations offraud, waste or abuse; and

• providing forensic examination ofdocumentary evidence.

INVESTIGATIVE ACTIVITIES

The Office ofInvestigations focuseson investigating alle-gations of seriousadministrative or crim-inal misconduct whichmay involve IRSemployees, such asbribery, financialfraud, false statements,computer violations,

disclosure of tax information, and abuse oftaxpayer rights. During this reporting period,the Office completed 438 employeemisconduct investigations.

The Office of Investigations also investigatesindividuals who attempt to interfere with orcorrupt the administration of the federalincome tax system, to include investigationsof bribery, assault, threat, theft, andembezzlement. During this six-monthreporting period the Office of Investigationscompleted 859 investigations involving thesetypes of allegations.

TIGTA special agents routinely conductintegrity awareness presentations for IRSemployees and various professionalorganizations. These presentations aredesigned to heighten awareness of integrityand to provide a deterrent effect against fraudand abuse involving IRS programs andoperations. During this six-month period theOffice of Investigations conducted 409presentations for 13,241 individuals.

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

24

Taxpayer Rights and Protection

The IRS Restructuring and Reform Act of1998 (RRA98) created new and importanttaxpayer rights and protections and alsoprovided for mandatory termination ofemployment for certain acts or omissions byIRS employees. During this reporting periodall IRS employees received mandatorytraining on the RRA98, Section 1203, conductprovisions.

There were no terminations under Section1203 during this reporting period. SeeAppendix V for a summary of Section 1203standards. During this six-month reportingperiod, TIGTA did not investigate anyallegations of unauthorized requests by theIRS Oversight Board for return informationand/or contacts relating to specific taxpayers.

Between July 22, 1998 (the enactment date ofRRA98) and March 31, 1999, TIGTAinitiated 47 investigations relating to alleged“1203” violations. Of these, 32 are currentlyongoing, and 15 have been closed andreferred to the IRS for administrativeadjudication.

In addition, TIGTA received 238 informationitems that TIGTA provided to IRS managersfor actions as they deemed appropriate. Theseinformation items are complaints orallegations where TIGTA determined that aninvestigation was not warranted.

To receive complaints of wrongdoing by IRSemployees, TIGTA also has established a toll-free telephone number and has published thistelephone number in IRS Publication 1 (YourRights as a Taxpayer) which is provided totaxpayers who are likely to have directcontact with IRS employees. TIGTA alsoestablished a national complaint center toreceive and process allegations of fraud,waste, abuse and other forms of wrongdoing.

Threats and Assaults

The Office of Investigations is committed toproviding the highest priority in terms ofresponsiveness and investigative emphasis tothreats and assaults against IRS employees.To further ensure the safety of IRS employeesand prevent violent situations from occurring,the Office of Investigations has developed anemployee protection program to identifyindividuals who may pose a threat to thesafety of IRS employees. During this six-month period, the Office of Investigationscompleted 353 threat and assaultinvestigations.

Bribery

Bribery of IRS employees is a major concernfor the IRS. As a result of frequent contactsIRS employees have with taxpayers, theirpositions and responsibilities make thempotential targets for bribery attempts. Thesuccess of TIGTA’s bribery program isdependent upon quality referrals and thecooperation of IRS employees. To enhanceboth of these aspects, TIGTA special agentstake every opportunity to develop solidrelationships with employees. In addition,TIGTA special agents frequently providebribery awareness presentations to theseemployees. During this six-month reportingperiod, the Office of Investigations completed43 bribery investigations. Examples arelocated in the Significant Criminal andAdministrative Investigations section of thisreport.

Forensic and Technical Services

Criminal investigations often depend upon theforensic analysis of evidence. Fingerprint and

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

25

handwriting technology, photography, andchemical analysis are just a few of thelaboratory tools that assist TIGTA specialagents in identifying subjects.

The TIGTA Forensic Science Laboratory(FSL) supports field investigations throughtimely processing of documentary, physical,and chemical evidence. As the FSL movestoward accreditation and expanded service tofield agents, additional personnel are beinghired. During this six-month period, the FSLreceived 79 case submissions, issued 63reports of laboratory examination, andevaluated over 2,400 items of physicalevidence.

During this reporting period the FSLevaluated the broad array of physical evidenceencountered by TIGTA special agents. Someexamples of the more significant laboratoryexaminations conducted during this reportingperiod include:

• handwriting and latent printexaminations of stolen remittancechecks, totaling $35,718, resultedin eliminating suspicion of asuspect;

• handwriting examinations oncollection closing documentstotaling over $222,000, resulted inan IRS revenue officer beingidentified as the author of eight ofthe nine signatures, despite hisdenials to the contrary;

• preserving and significantlyimproving readability of facsimilecopies related to an IRS contractfraud investigation; and,

• handwriting examinations ofletters sent to a news publisherdescribing threats to kill IRSagents and Federal judges. Asuspect was identified as theauthor of these letters.

TIGTA also conducts forensic computeranalysis of seized computers for evidentiarypurposes. Computer technology has rapidlybecome a tool for criminal activity, used infrauds against businesses, financialinstitutions and the IRS.

The Technical Services Section providesexpertise to TIGTA special agents in the useof technical and electronic investigativeequipment, including on-site assistance duringinvestigations.

SIGNIFICANT CRIMINALAND ADMINISTRATIVEINVESTIGATIONS

The following are brief synopses of some ofthe significant investigations conducted byTIGTA special agents during this reportingperiod.

Assault/Threat Investigations

Three Individuals Involved InThreats To Kill High LevelGovernment Officials, Including IRSEmployees

On July 1, 1998, as part of a multi-agencytask force, TIGTA special agents participatedin the arrest of three individuals who weremembers of a separatist group and chargedthem with terrorism and use of weapons ofmass destruction. During a jury trial, twosubjects were found guilty; the third subjectwas found not guilty. On February 5, 1999,the guilty subjects were each sentenced to 24years imprisonment and 5 years-supervisedrelease.

The individuals had sent threatening e-mail tothe President, the IRS Commissioner, andother high level Government officials. The e-mail stated that IRS employees and their

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

26

families were targeted for destruction throughthe use of non-traceable, personal deliverysystems, which would inject bacteria and/orviruses for the purpose of killing and causinggreat suffering.

One of the subjects, an alleged chemist,purchased the materials needed to make thedevice and talked about making or obtainingbotulism, HIV, anthrax, or rabies to be usedas the infectious disease/toxin in the deliverydevice.

Individual Threatens to UseExplosive Devices on IRS Building

An individual entered a plea of guilty topossession of an explosive device, which wasto be used to burn an IRS District office.TIGTA special agents acted as members of atask force in the investigation of the suspect,who was allegedly a member of a militiagroup. The subject told an informant that theyshould burn the local IRS District office.Based upon the threat against IRS propertyand the potential for the loss of life, the taskforce acted quickly to effect the arrest of thesuspect.

Bribery Investigations

Two Co-Conspirators Enter a Pleaof Guilty in Bribery Case

After attending a TIGTA Bribery AwarenessPresentation, an IRS revenue agent reported abribe overture by a taxpayer purported to beinvolved in an illegal drug trafficking ring.During a subsequent meeting, the taxpayergave the revenue agent $1,000 to eliminate a$70,000 tax liability. Subsequently, six othermembers of the drug ring also offered bribesto the revenue agent.

On November 5, 1998, TIGTA special agentsarrested all seven subjects. Two of thesubjects entered a plea of guilty to the

charges. Trials are pending for the other fivesubjects.

Former IRS Employee Found Guiltyof Accepting Bribes

On December 21, 1998, a former IRSemployee was found guilty of acceptingbribes from a taxpayer. The taxpayer wasalso found guilty and sentenced on August 26,1998, for his guilty plea to bribery andconspiracy. In a separate civil settlementagreement entered into between the IRS andthe taxpayer, it was agreed that more than$5 million in taxes and penalties would bepaid to the IRS by the convicted taxpayer.

When confronted by TIGTA special agents,an IRS employee confessed that he received atotal of $150,000 and ten automobiles from ataxpayer, whose corporations’ assets totaledover $225 million. The total value of thebribe, including the automobiles, amounted toapproximately $175,000. In addition, whilethe IRS employee was cooperating withTIGTA special agents, the taxpayer offeredhim another $150,000 to fraudulently disposeof other IRS audits involving several of hisrelated companies.

The revenue agent subsequently cooperatedwith the TIGTA special agents and admittedto accepting an additional $67,500 in bribesand numerous gifts during his 30-year careerwith the IRS. He also provided informationrelative to corruption within the IRS districtby identifying other revenue agents andmanagers who were involved in corruptdealings during this time frame.

Two Former IRS EmployeesSentenced for Preparing and FilingFraudulent Tax Returns

On January 20, 1999, two former IRSemployees were found guilty of bribery andconspiracy. One of the employees wassentenced to 21 months incarceration, threeyears probation, and ordered to pay $279,313

Semiannual Report to the Congress

Treasury Inspector General for Tax AdministrationMarch 31, 1999

27

in restitution. The second employee receivedone-year incarceration, three years probationand ordered to pay $72,785 in restitution.

The TIGTA investigations determined that thetwo employees conspired with numerousindividuals to prepare and file fraudulentFederal income tax returns and IRS auditreports in a scheme to generate fraudulent taxrefunds or to eliminate existing tax liabilities.Also, the employees took steps to prevent thefraudulent tax returns from being audited.Both employees often demanded and receivedbribes of up to one-half of each fraudulentrefund. The potential loss to the governmentin this scheme was estimated at $500,000.

Taxpayer Sentenced for Bribing anIRS Employee

On October 30, 1998, a taxpayer, whoadmitted paying an IRS employee inexchange for having fraudulent refundsgenerated to him by the IRS employee, wassentenced to four months incarceration, fourmonths home detention and three yearssupervised probation. The taxpayer was alsoordered to make restitution to the IRS in theamount of $16,887. This investigation wasthe result of a joint TIGTAAudit/Investigations Integrity Project, whichwas referred to the Office of Investigationsfor investigation.

IRS Employee Pleads Guilty toBribery and Preparing a FalseReport

On November 30, 1998, an IRS employeeentered a plea of guilty to bribery andpreparing a false report. The employee alsoresigned from his IRS position. TIGTAinitiated the investigation after an attorneyreported that an IRS employee had offered toreduce his tax liability by $100,000 for a$25,000 fee.

During a meeting between the IRS employeeand the attorney, the IRS employee gave the

attorney a “revised” audit report that indicatedhe and his wife owed $161,000 in taxes,interest, and penalties for 1995 and 1996, areduction of around $105,000.

In a second meeting, the attorney met with theIRS employee and gave him an envelope thatcontained the “revised” audit report signed byhim and his wife, a check for the amountshown on the audit report, and $15,000 cash.TIGTA special agents arrested the IRSemployee at the end of the meeting.

Disclosure/Improper ComputerAccess Investigations

IRS Employee Sentenced forBribery and UnauthorizedDisclosure of Tax Information

On January 25, 1999, the first IRS employeeindicted for violating the Taxpayer BrowsingProtection Act was convicted of bribery,unauthorized disclosure of tax returninformation and unauthorized inspection oftax returns. The employee was sentenced toimprisonment and supervised probation.

The investigation resulted from informationreceived by TIGTA from an agentinvestigating an ongoing fraud schemeinvolving an individual who was using theidentities of others to obtain fraudulent loansand credit cards. An informant revealed thatthe subject had obtained this information froman IRS employee. The subject subsequentlyentered into a plea agreement with the U.S.Attorney’s office and offered to cooperatewith TIGTA regarding the IRS employee’sinvolvement in the scheme.