purpose of the meeting

TRANSCRIPT

______________________________ The staff prepares Board meeting handouts to facilitate the audience’s understanding of the issues to be addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive due process and deliberations.

Accounting for Financial Instruments

Equity Method Investments

February 24, 2010

PURPOSE OF THE MEETING 1. At the August 19, 2009 Board meeting, the Board decided that all financial

instruments as defined in the Master Glossary of the FASB Accounting Standards

Codification™, with certain limited exceptions, should be included in the scope of

the project on accounting for financial instruments. As a result of this decision,

nonconsolidated equity investments currently accounted for under the equity

method would be measured at fair value with changes recognized in earnings.

However, the Board decided to separately consider whether investments in equity

securities that are accounted for under the equity method of accounting should be

included in the scope of the accounting for financial instruments project.

2. The purpose of today’s Board meeting is to discuss guidance for identifying which

nonconsolidated equity investments should be accounted for under the equity

method of accounting versus when those investments that should be within the

scope of the project on accounting for financial instruments.

ACCOUNTING APPROACHES 3. The staff proposes the following approaches for identifying when nonconsolidated

equity investments would be accounted for under the equity method of accounting:

a. Approach A: An investor would apply the equity method of accounting only

if the investor has significant influence over the investee and the investment

is considered related to the investor’s consolidated businesses. All other

investments would be within the scope of the project on accounting for

financial instruments and, accordingly, measured at fair value.

b. Approach B: An investor would apply the equity method of accounting only

if the investor must approve some or all of the decisions related to the

investee’s ordinary course of business that have a significant effect on the

investee’s financial performance. All other nonconsolidated equity method

investments would be measured at fair value.

c. Approach C: An investor would record investments that are currently

accounted for under the equity method at fair value if the investor’s intention

at the time of its investment is to generate an investment return (that is,

obtain dividends, capital appreciation of the investee, or both) and the entity

has an exit strategy to realize such amounts. All other nonconsolidated

equity method investments would continue to be accounted for using the

equity method.

d. Approach D: The equity method of accounting would be eliminated for

nonconsolidated equity investments. Accordingly, all such investments

would be within the scope of the accounting for financial instruments project

and measured at fair value.

e. Approach E: An investor in equity securities that qualify for equity method

accounting would continue to apply the equity method of accounting as it

exists today. However, the investor also would be required to disclose the

fair value of the investment on the face of the balance sheet and the change

in the fair value of the investment on the face of its income statement.

Question 1

Which one of these alternatives does the Board support?

FAIR VALUE OPTION

4. Currently, Topic 825, Financial Instruments, of the Codification permits an entity

to make an irrevocable election to measure most financial instruments at fair

value with changes in fair value recognized through earnings. Accordingly,

nonconsolidated equity investments that the investor has the ability to exercise

significant influence over may be accounted for under either the equity method in

accordance with Topic 323, Equity Method and Joint Ventures for Investments, or

at the election of the investor at fair value.

5. If the Board decides on approach A, B, C, or E in Question 1, then the Board must

decide if it should continue to be permit the fair value option for equity method

investments. If the Board decides on approach D above, then this section is not

relevant.

6. Based on discussions with the large accounting firms and a review of SEC filings

after the effective date of Topic 825, financial statement preparers infrequently

elect the fair value option for equity method investments. Entities that elected

the fair value option believe that fair value (a) provides a more objective

measurement of the value of their investment compared to the equity method of

accounting, (b) reflects economic events in earnings on a timely basis and

mitigates volatility in earnings from using different measurement attributes, and

(c) simplifies the accounting for publicly traded equity securities that are

accounted for under the equity method of accounting.

7. The staff has identified two alternatives for the Board

a. Alternative A— Permit the election of the fair value option for equity

method investments.

b. Alternative B— Prohibit the election of the fair value option for equity

method investments.

Question 2

Does the Board support Alternative A or Alternative B?

______________________________ The staff prepares Board meeting handouts to facilitate the audience’s understanding of the issues to be addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive due process and deliberations.

Accounting for Financial Instruments: Scope of the Proposed Accounting Standards Update

February 24, 2010

INTRODUCTION 1. The purpose of this meeting is to provide the Board with an overview of the

outreach that the staff has performed as it relates to the breadth of entities to be

included within the scope of the proposed Accounting Standards Update and for the

Board to decide which entities, if any, should be excluded from certain aspects of

the proposed Update.

OUTREACH 2. The staff held a series of calls to discuss the implications of the tentative model on

accounting for financial instruments on small and/or nonpublic financial

institutions. The staff provided a detailed summary of the outreach to the Board

before this Board meeting. The main issues described in the outreach summary

relates to a number of different aspects of the model, including the following:

a. Loans—operational burden related to measuring loans at fair value for smaller banking institutions that originate and hold the loans

b. Deposits—uncertainty and potential implementation issues surrounding application of the method for core deposit remeasurement

c. Issued debt—burden of remeasuring an entity’s issued debt at fair value if changes in the price of an entity’s credit are not realizable by the entity.

3. The staff also obtained input on constituents about whether there should be a

potential exemption from certain aspects of the Board’s tentative classification,

measurement, and impairment model and the guidance that the entities subject to

such an exemption should follow.

Page 2 of 4

ENTITIES WITHIN THE SCOPE OF THE PROPOSED UPDATE 4. The staff is presenting the following alternatives for the Board’s consideration.

These alternatives are to identify entities that would be excluded from certain

aspects of the proposed Update.

a. Alternative 1: All entities would be included in the scope except for entities whose asset size at the beginning of the fiscal year is below a defined quantitative amount.

(1) Alternative 1A: An exemption for entities with less than $500 million in consolidated total assets

(2) Alternative 1B: An exemption for entities with less than $1 billion in consolidated total assets.

b. Alternative 2: A scope exception for private entities with all public entities included within the scope of the proposed Update.

(1) Alternative 2A: An exemption for private entities with less than $500 million in consolidated total assets

(2) Alternative 2B: An exemption for private entities with less than $1 billion in consolidated total assets.

c. Alternative 3: A scope exception based on the financial sophistication of the entity

d. Alternative 4: An exemption based on the filing status of the entity

e. Alternative 5: No scope exemption.

Question 1

Does the Board support one of the above alternatives?

Page 3 of 4

MODEL APPLIED TO EXEMPTED ENTITIES 5. This section is only applicable if the Board decides in Question 1 above to exempt

specific entities from the scope of the classification and measurement guidance in

the proposed Update. This section is not relevant if the Board decides against

excluding any entities from the scope of the project. Under any of these

alternatives, entities would still be required to follow the impairment and hedging

guidance in the proposed Update.

a. Model 1—Originated fair value through other comprehensive income instruments measured at cost: Model 1 would propose that all entities subject to the scope exception apply the model, excluding any instrument that is eligible to be recorded at fair value through other comprehensive income that is issued or originated by the entity would be measured at amortized cost.

b. Model 2—Retain two classification and measurement categories: Model 2 would propose retaining two classification and measurement categories, but would change the second category from fair value through other comprehensive income to amortized cost.

c. Model 3—Retain current U.S. GAAP: Model 3 would propose that all entities subject to the scope exception continue to apply U.S. GAAP as they do today.

Additionally, the Board could develop a new model or combine any of these models with required disclosures.

Question 2

Should the model applied to exempted entities be one of the alternatives identified above or another alternative?

Page 4 of 4

OPTION TO APPLY THE EXEMPTION 6. Additionally, if the Board decides to allow certain entities to be exempt from

certain aspects of the model, the Board must also decide whether the exception is

mandatory or optional. Entities may elect to apply the model for a variety of

reasons, including known future growth and comparability with peers, among

others.

a. Alternative 1—Exemption is required: All entities subject to the exemption would be required to apply the model that the Board decides upon in Question 2.

b. Model 2—Exemption is optional: Entities would have the option to be exempt from the model. This decision would be required to be made at the beginning of the reporting period. Once an entity decides to follow the full fair value measurement approach in the Update, the entity would be prohibited from the exemption in the future.

Questions 3

Should the exemption be optional or mandatory?

Board Meeting Handout

______________________________ The staff prepares Board meeting handouts to facilitate the audience’s understanding of the issues to be addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive due process and deliberations.

Accounting for Financial Instruments: Classification and measurement of financial liabilities

February 24, 2010

PURPOSE OF THE MEETING

1. The purpose of this meeting is to discuss whether and, if so, how to address changes

in own credit risk of financial liabilities measured at fair value.

2. The Board’s tentative decisions made to date in the project on accounting for

financial instruments would require all financial liabilities to be recognized at fair

value with certain exceptions. All financial liabilities would subsequently be

measured at fair value with all changes in fair value recognized in net income unless

both of the following conditions are met:

a. The entity’s business strategy is to hold the financial liability with principal amounts for payment(s) of contractual cash flows rather than to settle the financial liability with a third party.

b. The financial liability is not a hybrid instrument that is required to be bifurcated under FASB Accounting Standards Codification™ Subtopic 815-15 on embedded derivatives (originally issued as FASB Statement No. 133, Accounting for Derivative Instruments and Hedging Activities).

If the above conditions are met, certain changes in fair value may be recognized in

other comprehensive income.

3. Certain types of an entity’s own debt may be measured at amortized cost if the

conditions for recognizing certain changes in fair value in other comprehensive

income have been met and measuring the financial liability at fair value would

create or exacerbate an accounting mismatch.

Page 2

ISSUE 1: LIABILITIES THAT MEET THE CRITERIA FOR MEASUREMENT AT FAIR VALUE THROUGH OTHER COMPREHENSIVE INCOME

4. The staff has identified two broad alternatives for the Board’s consideration to

address changes in own credit for financial liabilities with principal payments that

are held for payment of contractual cash flows that do not contain embedded

derivative features that require bifurcation under Subtopic 815-15 (referred to as

Category C instruments at the February 10, 2010 joint Board meeting).

a. Alternative 1—Amortize cost with limited exception. Under Alternative 1, an entity would be permitted to measure financial liabilities with principal payments that are held for payment of contractual cash flows that do not contain embedded derivative features that require bifurcation under Subtopic 815-15 (excluding core deposits) at amortized cost unless the financial liability is contractually linked to assets that are measured at fair value (for example, a securitization that does not meet the requirements for derecognition).

b. Alternative 2—Isolate effects of changes in own credit. There are at least two variants of this alternative:

(1) Present the total fair value change in other comprehensive income with separate presentation or disclosure of the change in own credit risk.

(2) Use an “adjusted” fair value measurement attribute that reflects no changes in own credit risk (the “frozen credit spread” method).

5. Under the “frozen credit spread” method, the liability would initially be measured at

fair value and subsequently remeasured at a current value that ignores changes in

the issuer’s own credit risk. Changes in the adjusted fair value measurement would

be recognized in other comprehensive income.

6. Under either variant of this alternative it will be necessary to address how changes

in the issuer’s own credit risk should be calculated, including whether and how to

differentiate between the price of credit and the credit standing of the issuing entity.

7. Although not listed as a separate alternative, the Board also could confirm its

tentative decision to measure these instruments at fair value with all changes

recognized in other comprehensive income.

Page 3

Staff Recommendation 8. Some staff members recommend Alternative 1. Other staff members recommend

that the Board confirm its previous decision to require financial liabilities in this

category to be measured at fair value with subsequent changes in fair value

recognized in other comprehensive income.

Question 1

How does the Board want to measure financial liabilities with principal payments that are held for payment of contractual cash flows that do not contain embedded derivative features that require bifurcation under Subtopic 815-15?

ISSUE 2: LIABILITIES HELD FOR PAYMENT OF CONTRACTUAL CASH FLOWS THAT CONTAIN EMBEDDED DERIVATIVES THAT REQUIRE BIFURCATION UNDER SUBTOPIC 815-15 9. This issue relates to financial liabilities referred to as Category B instruments at the

February 10, 2010 joint Board meeting. This category includes financial liabilities

with principal payments held for contractual cash flows that contain embedded

derivatives that require bifurcation under Subtopic 815-15. The Board was

previously presented with alternatives to consider in measuring financial liabilities

in this category at the February 10 joint meeting.

Staff Recommendation 10. If the Board decides to expand the use of amortized cost for Category C instruments

in Issue 1, the staff recommends that the Board consider bifurcation of instruments

in Category B. However, if the Board decides that Category C instruments should

be measured at fair value through other comprehensive income, the staff

recommends that the Board confirm its tentative decision that liabilities in this

category be measured at fair value with changes in fair value recognized in net

income.

Question 2

How does the Board want to measure financial liabilities with principal payments that are held for payment of contractual cash flows that contain embedded derivative features that require bifurcation under Subtopic 815-15?

Board Meeting Handout Disclosures about Credit Quality and the Allowance for Credit Losses

February 24, 2010

The staff prepares Board meeting handouts to facilitate the audience's understanding of the issues to be addressed at the Board meeting. This material is presented for discussion purposes only; it is not intended to reflect the views of the FASB or its staff. Official positions of the FASB are determined only after extensive due process and deliberations.

PURPOSE OF THIS MEETING 1. The purpose of this meeting is for the Board to redeliberate issues related to the

proposed Statement, Disclosures about the Credit Quality of Financing Receivables

and the Allowance for Credit Losses. Appendix A provides a summary of the

disclosures included in the proposed Statement and the staff’s recommended

modifications to those proposed disclosures, if any.

OPTIONS FOR THE BOARD’S CONSIDERATION 2. The staff is presenting the following topics for the Board’s consideration:

a. Definitions of portfolio segment and class of financing receivable (Questions 1 and 2)

b. Rollforward of the allowance for credit losses (Questions 3 and 4)

c. Rollforward of the carrying amount of financing receivables (Questions 5–7)

d. Disclosures about the credit quality of financing receivables (Questions 8–11)

e. Modifications of financing receivables (Question 12)

f. Fair value disclosures (Question 13)

g. Scope—Financing receivables:

(1) Financing receivables measured at fair value or lower of cost or fair value (Question 14)

(2) Leases (Question 15)

(3) Promises to give (Question 16)

(4) Accounts receivable (Question 17)

(5) Unfunded lending commitments (Question 18).

h. Scope—all creditors (Question 19)

Page 2 of 21

i. Purchased credit impaired loans (Question 20)

j. Loss contingency disclosure clarification (Question 21)

k. Interim and annual reporting periods (Question 22)

l. Effective date and transition (Question 23)

m. Other recent guidance.

Definitions of Portfolio Segment and Class of Financing Receivable

Staff Recommendation 3. The staff is split on whether the requirement to disaggregate financing receivables

based on impairment methodology should be retained or removed from the

definition of portfolio segment. The portfolio segment definition is utilized in the

disclosures required by paragraphs 11(c) and 11(d) of the proposed Statement,

namely the activity in the allowance for credit losses disclosure and the activity in

the carrying amount of financing receivables.

4. Some staff members believe that requiring charge-offs by impairment methodology

is not meaningful because more charge-offs and recoveries would be reported in the

“individually evaluated” section even though the related financing receivable may

have been reported in the “collectively impaired” section from origination almost

until the time of charge-off. They further note that investors were ambivalent about

the proposed disaggregation based on impairment methodology. Additionally, there

is concern that the proposed disclosures may become outdated based on

developments in the project on accounting for financial instruments.

5. Another staff member believes that the originally proposed disaggregation provides

decision-useful information to users. This split is critical in allowing an investor to

effectively break down the allowance between the allowance related to impaired

loans determined in accordance with Subtopic 310-40, Troubled Debt

Restructurings by Creditors, and the allowance for those loans evaluated

collectively under Topic 450, Contingencies. Furthermore, management separately

calculates and determines impairment in accordance with the respective accounting

standards and there is no increased burden or costs on management. This staff

member also believes that this split will be more critical with the tentative decisions

Page 3 of 21

made to date in the project on accounting for financial instruments. That project

proposes allowing management to analyze loans for impairment on either a pool or

individual basis. Therefore, this split will provide the investor with a better

understanding from a qualitative perspective about how management is analyzing

the portfolio.

6. The staff recommends the following modification to the definition of class of

financing receivable:

a. Class of financing receivable:

(1) The staff recommends retaining the provision in paragraph 6(a) of the proposed Statement, which would require segregation of class on the basis of the initial measurement attribute. The staff notes that based on tentative decisions made to date in the project on accounting for financial instruments, there will be only one measurement attribute for financing receivables, namely, fair value through other comprehensive income (assuming that fair value loans are not within the scope). Therefore, this disaggregation would no longer be relevant. Under current U.S. generally accepted accounting principles, there are four different measurement attributes of loans: amortized cost (originated and held), present value of future cash flows (purchased loans with credit deterioration), lower of cost or market (mortgage loans originated and held-for-sale), and fair value.

(2) The staff recommends retaining the provision in paragraph 6(b) of the proposed Statement, which would require management to disaggregate class of financing receivable to the level that management utilizes when assessing and monitoring risk and performance of the portfolio. The provision includes a list of factors that should be retained. The staff recommends adding additional language that would remind management that the determination of class is based on management judgment.

Page 4 of 21

Questions 1 and 2

Does the Board believe that the definition of portfolio segment should be modified to remove the requirement to further disaggregate financing receivables based on impairment methodology?

Does the Board agree with the staff’s recommendations to retain the definition of class of financing receivable as proposed, emphasizing that judgment will be required to apply that definition?

Rollforward of the Allowance for Credit Losses

Staff Recommendation 7. The staff recommends no modification to the proposed requirement to disaggregate

the rollforward of the allowance for credit losses by portfolio segment. The staff

notes that most comment letter respondents and investors support this proposed

requirement.

Questions 3 and 4

Does the Board agree with the staff’s recommendation to retain the proposed requirement to provide a rollforward schedule of the total allowance for credit losses by portfolio segment and in the aggregate?

Does the Board want to retain the proposed requirement to further disaggregate the rollforward schedule of the allowance for credit losses by portfolio segment based on impairment methodology (Topic 450 versus Subtopic 310-40)?

Partially Charged-Off Loans 8. Based on recent discussions with financial statement users, a Board member

suggested adding the following disclosure requirement:

Provide qualitative and quantitative information about partial charge-offs of financing receivables by portfolio segment to enable users to better understand how partial charge-offs affect the allowance for credit losses. This information may include amounts charged off, the remaining outstanding balance of partially charged-off receivables, and the number of financing receivables that have been partially charged-off.

Page 5 of 21

9. Users believe that this additional information will assist in better understanding

allowance coverage ratios. While the proposed disclosures about impaired

financing receivables (paragraph 14 of the proposed Statement) likely would apply

to partially charged-off receivables, users believe that without additional

information those disclosures would not enable them to understand how partial

write-downs affect allowance coverage ratios.

Question 4a

Does the Board want to add a disclosure requirement that would require a creditor to provide qualitative and quantitative information about partial charge-offs of financing receivables by portfolio segment to enable users to better understand how partial charge-offs affect the allowance for credit losses?

Rollforward of the Carrying Amount of Financing Receivables

Staff Recommendation 10. The staff recommends removing the requirement to provide a rollforward schedule

of the carrying amount of financing receivables from the final Accounting

Standards Update. The staff believes that the information required to comply with

the proposed disaggregated disclosure is not readily available and will not provide

meaningful information to financial statement users about the credit quality of

financing receivables and the allowance for credit losses.

11. The staff recommends that the final Update require an entity to disclose the carrying

amount of the finance receivable balance as of the end of each reporting period for

each disaggregated portfolio segment. The staff notes that the end-of-period

balance is necessary to compute allowance for credit loss ratios by portfolio

segment.

12. The staff recommends that an entity be required to disclose separately purchases of

financing receivables and sales of financing receivables during a reporting period

by portfolio segment. The staff believes that this information is readily available

and is responsive to recent input obtained from users of financial statements.

Page 6 of 21

Questions 5–7

Does the Board agree with the staff’s recommendation to remove the requirement to provide a rollforward schedule of the carrying amount of financing receivables by portfolio segment?

Does the Board agree with the staff’s recommendation to require an entity to disclose the carrying amount of financing receivables as of the end of each reporting period by portfolio segment?

Does the Board agree with the staff’s recommendation to require an entity to disclose separately, by portfolio segment, purchases of financing receivables during a reporting period and sales of financing receivables during a reporting period?

Disclosures about the Credit Quality of Financing Receivables

Staff Recommendation 13. The staff recommends that the credit quality disclosures in the proposed Statement

be modified to clarify that the proposed disclosures should be based on how and to

what extent management monitors the credit quality of its portfolios on an ongoing

manner. The staff believes that the proposed disclosures in paragraph 13(b) of the

proposed Statement are consistent with the recommended disclosures included in

the Shipley & Fisher II working group reports.1

14. The staff recommends that a creditor be required to provide the proposed

disclosures in paragraph 13(b) of the proposed Statement for its entire portfolio

rather than limiting the proposed disclosures to only those assets that are neither

past due nor impaired. The staff believes this suggested change will provide users

with a better understanding of the credit quality of each portfolio. The staff also

However, the staff notes that those

working groups believe that the recommended disclosures should be voluntary

disclosures.

1 Two working groups issued final reports in 2001 encouraging financial entities to improve their credit quality disclosures. The Federal Reserve Board, with the support of the Securities and Exchange Commission and the Office of the Comptroller of the Currency, established the Working Group on Public Disclosure in 2000 to develop options for improving the public disclosure of financial information by banking and securities organizations. Several international organizations, including the Basel Committee on Banking Supervision and the International Organisation of Securities Commissions, sponsored the Multidisciplinary Working Group on Enhanced Disclosure from 1999–2001.

Page 7 of 21

recommends removing the requirement to link internal risk ratings to standard

external ratings to address banking regulators’ objections.

15. The staff recommends that the proposed disclosures in paragraphs 13(d) and 13(e)

of the proposed Statement be modified to apply to all financing receivables with the

exception of financing receivables deemed impaired under Subtopic 310-40. The

staff believes that the impairment disclosures that apply to financing receivables

deemed impaired under Subtopic 310-40 provide users with more relevant

information. This modification addresses the concern that the proposed Statement

would expand the guidance in Subtopic 310-40 beyond its current scope.

16. The staff recommends that the proposed credit quality disclosures continue to be

provided by class.

17. The staff recommends that the proposed disclosures be amended as follows:

A creditor shall disclose information that enables users of its financial statements to assess the quantitative and qualitative risks arising from the credit quality of its financing receivables. To meet that objective, a creditor shall disclose all of the following by class of financing receivable:

a. Management’s policy for determining past due or delinquency status (that is, whether past due status is based on how recently payments have been received or by contractual terms).

b.

i. For financing receivables at amortized cost that are neither past due as determined by management’s policy nor impaired as defined by Statement 114, qQuantitative and qualitative information about the credit quality of financing receivables at the end of the reporting period, including a description of the credit quality indicator and the carrying amount of the financing receivables by credit quality indicator.

To the extent that a creditor updates credit quality indicators on an ongoing basis,

When internal ratings are disclosed, a creditor shall provide qualitative discussion on how the ratings relate to loss likelihoods. A creditor shall make it clear which financing receivables are included. To the extent that the following credit quality indicators are used by creditors, either of the following additional disclosure requirements applies:

Page 8 of 21

1. Internal risk ratings- If a regulated creditor discloses a class of financing receivables on the basis of internal risk ratings, then the creditor shall provide an explanation of how its internal risk ratings compare with the federal regulatory ratings of pass, special mention, substandard, doubtful, and loss. Those ratings are defined in the Uniform Agreement on the Classification of Assets and Appraisal of Securities Held by Banks and Thrifts issued by the Office of the Comptroller of the Currency, the Federal Deposit Insurance Corporation, the Board of Governors of the Federal Reserve System, and the Office of the Thrift Supervision.

2. Consumer credit risk scores- If a creditor discloses a class of financing receivables on the basis of consumer credit risk scores, then the creditor shall update the consumer credit risk scores on an annual basis and disclose the date or range of dates that the scores were last updated.

c. For financing receivables carried at a measurement other than amortized cost (fair value, the lower of cost or market, or present value of amounts to be received) that are neither past due as determined by management’s policy nor impaired as defined by Statement 114, quantitative information about the credit quality at the end of the reporting period shall be disclosed separately by measurement attribute.

d. For financing receivables that are past due as determined by management’s policy, but not impaired, an analysis of the age of the carrying amount of financing receivables at the end of the reporting period.

e. The carrying amount at the end of the reporting period of financing receivables past due 90 days or more, but not impaired, for which interest is still accruing in the financial statements.

Exclude any financing receivables deemed to be impaired under Subtopic 310-40.

f. The total of financing receivables disclosed in items (b), (c), and (d) above reconciled to the allowance for credit losses for collectively impaired financing receivables by portfolio segment.

Exclude any financing receivables deemed to be impaired under Subtopic 310-40.

Page 9 of 21

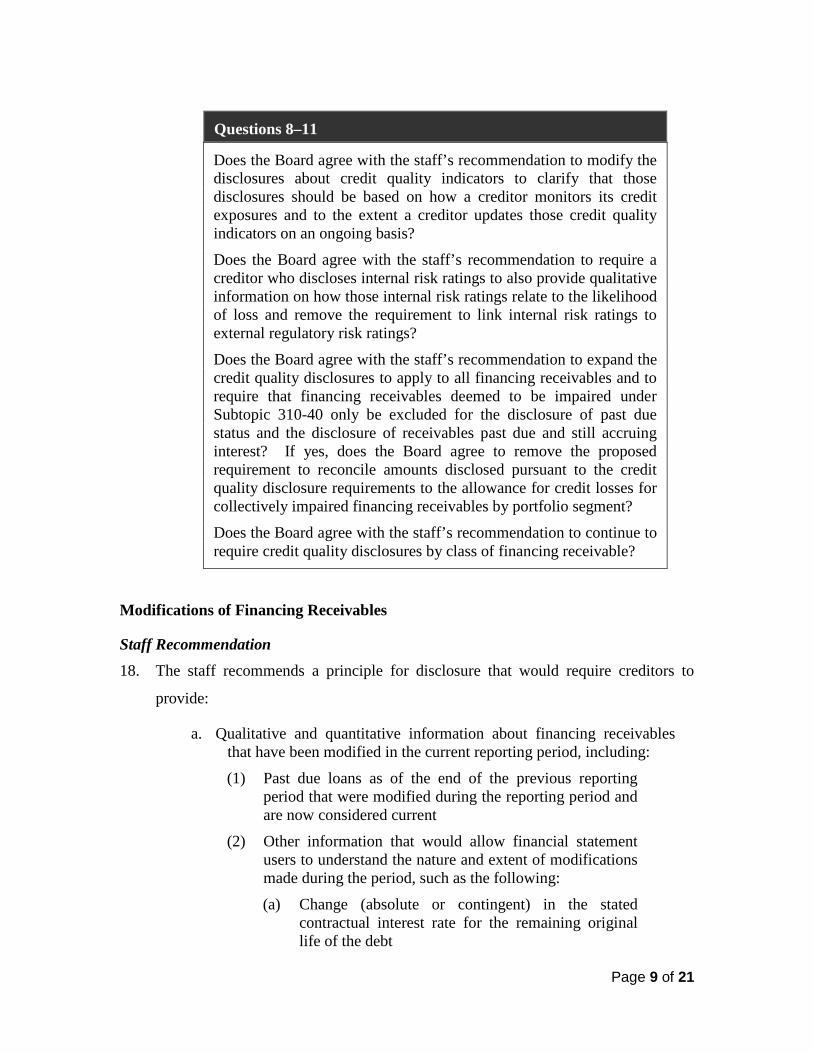

Questions 8–11

Does the Board agree with the staff’s recommendation to modify the disclosures about credit quality indicators to clarify that those disclosures should be based on how a creditor monitors its credit exposures and to the extent a creditor updates those credit quality indicators on an ongoing basis?

Does the Board agree with the staff’s recommendation to require a creditor who discloses internal risk ratings to also provide qualitative information on how those internal risk ratings relate to the likelihood of loss and remove the requirement to link internal risk ratings to external regulatory risk ratings?

Does the Board agree with the staff’s recommendation to expand the credit quality disclosures to apply to all financing receivables and to require that financing receivables deemed to be impaired under Subtopic 310-40 only be excluded for the disclosure of past due status and the disclosure of receivables past due and still accruing interest? If yes, does the Board agree to remove the proposed requirement to reconcile amounts disclosed pursuant to the credit quality disclosure requirements to the allowance for credit losses for collectively impaired financing receivables by portfolio segment?

Does the Board agree with the staff’s recommendation to continue to require credit quality disclosures by class of financing receivable?

Modifications of Financing Receivables

Staff Recommendation 18. The staff recommends a principle for disclosure that would require creditors to

provide:

a. Qualitative and quantitative information about financing receivables that have been modified in the current reporting period, including:

(1) Past due loans as of the end of the previous reporting period that were modified during the reporting period and are now considered current

(2) Other information that would allow financial statement users to understand the nature and extent of modifications made during the period, such as the following:

(a) Change (absolute or contingent) in the stated contractual interest rate for the remaining original life of the debt

Page 10 of 21

(b) Change in the maturity date or dates with no compensation or at a stated interest rate lower than the current prevailing market rate for new debt with similar risks and term

(c) Change (absolute or contingent) in the face amount or maturity amount of the debt as stated in the instrument or other agreement

(d) Change (absolute or contingent) in accrued interest.

Question 12

Does the Board agree with the staff’s recommendation?

Fair Value Disclosures

Staff Recommendation 19. The staff recommends that the requirement to disclose fair value information by

portfolio segment be removed from the final Update. The staff believes that most

creditors currently do not have processes in place to measure fair values for their

financing receivables by portfolio segment. Considering the overlap with current

existing fair value disclosures, the staff believes that it would be more appropriate

to address further disaggregation of fair value information in the project on

accounting for financial instruments.

Question 13

Does the Board agree with the staff’s recommendation to remove the requirement to disclose fair value information of loans by portfolio segment?

Scope—Financing Receivables

Financing Receivables Measured at Fair Value or Lower of Cost or Fair Value

Staff Recommendation 20. The staff recommends that the Board explicitly exclude financing receivables

measured at fair value directly through earnings or at lower of cost or fair value

from the scope of the final Update.

Page 11 of 21

Question 14

Does the Board agree with the staff’s recommendation to explicitly exclude financing receivables measured at fair value directly through earnings or at lower of cost or fair value from the scope of the final Update?

Leases

Staff Recommendation 21. The staff recommends that finance leases, including leveraged leases, be included in

the scope of the final Update. The proposed disclosures will provide information

based on how a creditor evaluates the credit risk of its financing receivables and the

adequacy of its allowance for credit losses. Those disclosures are not intended to

change how management monitors its credit risk or allowance for credit losses.

Therefore, the benefits derived from providing the additional disclosures will

outweigh the cost of providing those additional disclosures.

Question 15

Does the Board agree with the staff’s recommendation to include finance leases, including leveraged leases, in the scope of the final Update?

Promises to Give

Staff Recommendation 22. The staff recommends that the Board explicitly exclude unconditional promises to

give, regardless of their term, from the scope of the final Update.

Question 16

Does the Board agree with the staff’s recommendation to explicitly exclude unconditional promises to give, regardless of their term, from the scope of the final Update?

Page 12 of 21

Accounts Receivable

Staff Recommendation 23. The staff recommends that the Board continue to exclude accounts receivable with

contractual maturities of one year or less that arose from the sale of goods or

services, except for credit card receivables, from the definition of financing

receivables in the final Update.

Question 17

Does the Board agree with the staff’s recommendation to exclude accounts receivable with contractual maturities of one year or less that arose from the sale of goods or services, except for credit card receivables, from the definition of financing receivables in the final Update?

Unfunded Lending Commitments

Staff Recommendation 24. The staff recommends that the Board continue to exclude unfunded lending-related

commitments from the scope of the final Update.

Question 18

Does the Board agree with the staff recommendation to exclude unfunded lending-related commitments from the scope of the final Update?

Scope—All Creditors

Staff Recommendation 25. The staff recommends that the Board specify that the disclosure guidance in the

final Update is optional for an entity that meets all of the following criteria:

a. The entity is a nonpublic entity.

b. The entity’s total assets are less than $100 million on the date of the financial statements.

The criteria would be applied to the most recent period presented in comparative

financial statements to determine applicability of this option.

Page 13 of 21

26. If disclosures are not required in the current period, the disclosures for previous

periods may be omitted if financial statements for those periods are presented for

comparative purposes. If disclosures are required in the current period, disclosures

that have not been reported previously need not be included in financial statements

that are presented for comparative purposes.

Question 19

Does the Board agree with the staff’s recommendation to make the disclosure guidance in the final Update optional for an entity that is (a) a nonpublic entity and (b) has less than $100 million total assets?

Purchased Credit Impaired Loans

Staff Recommendation 27. The staff recommends excluding disclosures applicable only to purchased credit

impaired loans from this project. The staff believes that additional disclosures

applicable only to purchased credit impaired loans should be exposed for public

comment. The staff recommends that the Board add a short-term project to its

agenda to enhance disclosures about purchased credit impaired loans. If the Board

agrees with the additional disclosures applicable only to purchased credit impaired

loans, the staff could proceed with issuing a proposed Update for public comment.

Question 20

Does the Board agree with the staff’s recommendation to exclude disclosures applicable only to purchased credit impaired loans from this project?

Page 14 of 21

Loss Contingency Disclosure Clarification

Staff Recommendation 28. The staff recommends that the Board specify that the disclosures in paragraphs 450-

20-50-3 through 50-5 (originally issued as paragraph 10 of FASB Statement No. 5,

Accounting for Contingencies) are not required for the allowance for loan losses

based on the fact that the estimations are normal, recurring, and inherent to

estimations. The staff also notes that the disclosures proposed by this project are

sufficiently detailed enough to provide additional insight into both the credit quality

of an entity’s financing receivable portfolio as well as the allowance for loan losses.

Question 21

Does the Board agree with the staff’s recommendation?

Interim and Annual Reporting Periods

Staff Recommendation 29. The staff recommends that the final Update should be effective for both interim and

annual periods.

Question 22

Does the Board agree with the staff’s recommendation that the final Update should be effective for both interim and annual periods?

Effective Date and Transition

Staff Recommendation 30. The staff recommends that the final Update should be effective for interim and

annual reporting periods ending after December 15, 2010, because a delayed

effective date would provide creditors with sufficient time to implement the final

Update. Additionally, the final Update should not require disclosures for earlier

periods presented for comparative periods at initial adoption. Also, in periods after

Page 15 of 21

initial adoption, the final Update should require comparative disclosures only for

periods ending after initial adoption.

Question 23

Does the Board agree with the staff’s recommendation that the final Update should be effective for interim and annual reporting periods ending after December 15, 2010, with a prospective transition?

Page 16 of 21

Appendix A—Summary of the Staff’s Recommendations This appendix is intended to provide a summary of the major points in the proposed Statement to be redeliberated and the related staff’s recommendations.

(This version of the appendix has been re-ordered to follow the sequence of questions in the Board memo.)

Exposure Draft Staff Recommendation Definition of portfolio segment and class of financing receivable

A portfolio segment is the level at which a creditor develops and documents a systematic methodology to determine its allowance for credit losses (for example, by type of financing receivable, industry, and risk rates). Portfolio segments are additionally disaggregated by individual and collective evaluation for impairment. (Topic 450 versus Subtopic 310-30)

The staff is split regarding the requirement to disaggregate the disclosures by portfolio segment based on impairment methodology. View A would require an entity only to disaggregate allowance balances and corresponding receivables balances as of the end of the reporting period. View B would retain the requirement to disaggregate all components within the allowance rollforward by impairment methodology. View C would remove the requirement to disaggregate information based on impairment methodology.

A class of financing receivable is a level of information that enables users of financial statements to understand the nature and extent of exposure to credit risk arising from financing receivables held at the date of the financial statements. A creditor’s principle determination of class is based on both of the following:

• Classes must segregate financing receivables on the basis of the initial measurement attribute (amortized cost, fair value, lower of cost or fair value, and present value of amounts to be received).

• Classes then must be disaggregated to the level that management utilizes when assessing and monitoring risk and performance of the portfolio.

Retain the provision that would require segregation of class based on measurement attribute. Retain the provision that would require management to disaggregate class of financing receivable when assessing and monitoring risk and performance of the portfolio, including the list of factors to consider. Add additional language that would remind management that the determination of class is based on management judgment.

Page 17 of 21

Disclosures

Allowance for Credit Losses: information that enables users to understand (a) risk characteristics of portfolio segments, (b) factors and methodologies used in estimating the allowance for each portfolio segment, and (c) the activity in both the receivables and the allowance for each portfolio segment:

• Description by portfolio segment of the accounting policies and methodology used to estimate the allowance for credit losses

• Description by portfolio segment of management’s policy for charging off uncollectible financing receivables

• Activity in the total allowance for credit losses (rollforward of allowance) by portfolio segment and in total, presented both for receivables individually evaluated for impairment (as determined by Subtopic 310-30) and for receivables collectively evaluated for impairment (as determined Topic 450).

• Activity in the financing receivables related to the allowance for credit losses (rollforward of financing receivables) by portfolio segment and in total, presented both for receivables individually evaluated for impairment and for receivables collectively evaluated for impairment.

Retain the requirement to disaggregate the rollforward of the allowance for credit losses by portfolio segment. As noted above, the staff has split views on whether the activity in the allowance for credit losses should be disaggregated based on impairment methodology. Remove from the final Update the requirement to provide a rollforward schedule of financing receivables. Instead, require an entity to disclose the carrying amount of the financing receivable balance as of the end of each reporting period by disaggregated portfolio segment, and require an entity to separately disclose purchases and sales of financing receivables during a reporting period by portfolio segment.

Page 18 of 21

Credit Quality Information: Information that enables users to assess the quantitative and qualitative risks arising from the credit quality of its financing receivables:

• Management’s policy for determining past due or delinquency status

• For financing receivables carried at amortized cost that are neither past due nor impaired, quantitative and qualitative information about the credit quality of those financing receivables by credit quality indicator:

o If a creditor uses internal risk ratings, the creditor shall provide an explanation of how its internal risk ratings compare with federal regulatory ratings

o If a creditor uses consumer credit scores, the creditor shall update those scores on an annual basis and disclose the date they were last updated.

• For financing receivables carried at a measurement other than amortized cost that are neither past due nor impaired, quantitative information about the credit quality

• For financing receivables that are past due but not impaired, an analysis of age of the carrying amount of financing receivables

Modify the credit quality disclosures from the proposed Statement to clarify that the proposed disclosures should be based on how and to what extent management monitors the credit quality of its portfolios in an ongoing manner. Require a creditor to disclose credit quality indicators for its entire portfolio that are monitored on an ongoing basis rather than limiting those disclosures to only those assets that are neither past due nor impaired (i.e., performing assets). Remove the requirement to link internal risk ratings to standard external ratings. Modify the past due disclosures to apply to all financing receivables unless a creditor individually evaluates its financing receivables for impairment. Retain the proposal that credit quality disclosures be provided by class. Add a principle for disclosure that would require creditors to provide :

• Qualitative and quantitative information about financing receivables that have been modified in the current reporting period, including:

o Past due loans as of the previous reporting period-end that were modified during the reporting period and are now considered current

o Other information that would allow financial statement users to understand the nature and extent of modifications made during the period,

Page 19 of 21

• The carrying amount of

financing receivables that are past due but not impaired for which interest is still accruing

• The carrying amount of financing receivables that are considered current but have been modified in the current year after being past due

• The following three items: o (a) the total amount of

financing receivables measured at amortized cost that are neither past due nor impaired;

o (b) the total amount of financing receivables measured at other than amortized cost that are neither past due nor impaired; and

o (c) the total amount of financing receivables that are past due but not impaired

Reconciled to the allowance for credit losses for collectively impaired financing receivables by portfolio segment.

such as change in the stated contractual interest rate, change in the maturity date or dates with no compensation, change in the face amount or maturity amount of the debt, or change in accrued interest.

Remove the requirement to reconcile each of the following:

• The total amount of financing receivables measured at amortized cost that are neither past due nor impaired;

• The total amount of financing receivables measured at other than amortized cost that are neither past due nor impaired; and

• The total amount of financing receivables that are past due but not impaired

to the allowance for credit losses for collectively impaired financing receivables by portfolio segment.

Fair Value: information by portfolio segment that enables users of financial statements to assess the fair value of loans at the end of the reporting period:

• The fair value of loans by portfolio segment

• The method(s) and significant assumptions used to estimate fair value.

Remove this requirement from the final Update.

Scope Definition of financing receivable: loans defined as a contractual right to receive money on demand or on fixed or determinable dates that is

Leases: Continue to include finance leases in the scope of the final Update.

Page 20 of 21

recognized as an asset in the creditor’s statement of financial position, whether originated or acquired

Includes: • Accounts receivable with

terms exceeding one year • Notes receivable • Receivables relating to

lessors’ rights to payments from leases other than operating leases.

Excludes: • Accounts receivable with

maturities of less than one year that arose from the sale of goods or services, except for credit card receivables

• Debt securities as defined by Topic 320

• Unconditional promises to give that are not assets of not for profit entities and that are due in one year or less

• Acquired beneficial interests or the transferor’s beneficial interests in the transferred financial assets within the scope of Topic 325.

Finance receivables measured at fair value through earnings or at lower of cost or market: Exclude from the scope of the final Update. Unfunded lending commitments: Continue to exclude unfunded lending-related commitments from the scope of the final Update. Trade receivables: Continue to exclude trade receivables with maturities of less than one year from the scope of the final Update. Promises to give: Exclude all unconditional promises to give from the scope of the final Update.

Scope Entities: applies to all public and nonpublic entities

Modify the scope and provide an option for entities that are nonpublic and have total assets less than $100 million.

Other Items Purchased credit-impaired loans Do not require disclosures applicable only

to purchased credit impaired loans. Rather, expose any specialized disclosures in a dedicated short-term project.

Loss contingency disclosure clarification

Clarify that the requirement to disclose the possible loss or range of loss does not apply to recurring loss contingencies arising from a creditor’s normal estimation of its allowance for loan losses.

Page 21 of 21

Scope

Reporting period: applies to both interim and annual reporting periods

Retain this aspect of the proposed Statement.

Effective Date Effective Date: Effective for interim and annual reporting periods ending after December 15, 2009. Comparative disclosures are encouraged but not required for periods before initial adoption.

Modify the effective date to be for interim and annual reporting periods ending after December 15, 2010