q1-21 presentation

TRANSCRIPT

Q1-21 Presentation

2

Presenters

Convene | Q1-21 Presentation

Agenda• Introduction to Convene

• FY21 Status

• Growth and strategic initiatives

• Financials

• Summary

4

v

~12% annual growth in number of transactions 2016-2019

~10% annual revenue growth 2020-2023

Significant potential in new markets

2020 EBITDA of NOKm ~200

Established in 7 industry verticals

~900,000 mobile payment transactions in 2020

~80% market share in GP vertical in Norway

~14 million transactions annually

2020 revenue of NOKm ~425

Convene Group

v

Convene | Q1-21 Presentation

5

Our specialized solutions for payment processing are designed to meet the unique needs of healthcare

industries

Payment equipment

Transaction administration

Revenue cycle management Financing

Mobile and online payment Integration

Terminals accepting chip, card, cash, and invoice printing

Direct payment through

automated link sent to mobile or accessed via

platform

Direct integration with EHR-systems for efficient work-

flows

End-to-end administration

of payment services

Efficient and ethical

collection of outstanding

claims

Provision of financing-as-a-service without balance sheet

risk

Convene technology platform

Convene | Q1-21 Presentation

6

A clear and differentiated value proposition for our clients

xxx

Reduced administrative costs and need for back-office staff,

eliminating human errors

Increased time for revenue generating activities

Increased revenue through automated collection and financing services

Optimized consumer experience and customer service

Secure ethical and humane debt collection

Agile and scalable platform capable of adapting to changes in customer needs

Convene | Q1-21 Presentation

7

Financing-as-a-Service

First terminal sold

2010

20%

100%2021

Melin Collection established

20132010

Melin Medical is established

Company history and key milestones

Expansion into new verticals

2019

Mobile payment

introduced

2019

100%

Continued expansion

through acquisitions

2018

2020

“Just-walk-home”

initiative

New markets and

acquisitions

2017

Rebranding

2020

Convene | Q1-21 Presentation

8

FaaS is the next catalyst for growth

(1) Revenue from Gordion is categorized as Other

(2) ARR = rental-based + transaction-based revenue

Other Rental-based revenue Transaction-based revenue

Growth phase I:Equipment roll-out

Growth phase II:Revenue Cycle Management

Growth phase III:Financing-as-a-service

ARR 2 :

Key growth de-nominator

# Units # billable transactions # total transactions

82%

2010

0%

14%

0%

2014

0%

79%

2012 2013

9%

61%24%

9%

2011

9%

26%65%

78%

24%

76%

2%

3%

13%

0%21%

2%

20%

78%

20212015

16%

15%

84%

2017

78%

12%

13%

10%

2018 20222019

8%

81%

2020

78%

2016 2023

11%

76

0%0 2

24

126151

188

247

357

400424

NewProductlaunch

NewProductlaunch

NewProductlaunch

- 85% 91% 100% 100% 97% 98% 98% 88% 87% 92% 91%

M&A

M&A

Convene | Q1-21 Presentation

Agenda• Introduction to Convene

• FY21 Status

• Growth and strategic initiatives

• Financials

• Summary

10

Status Q1-21DEVELOPMENT DURING Q1-21

0.0k

0.5k

1.0k

1.5k

2.0k

2.5k

3.0k

3.5k

4.0k

Q3

16

Q1

17

Q3

17

Q1

18

Q3

18

Q1

19

Q3

19

Q1

20

Q3

20

Q1

21

Solutions in operation by industry

Prm. care Sec. care Vet. care Fitness

Churn rate in % Q1 2021 Q4 2020 Q3 2020 Q2 2020

Quarterly churn rate in % 2.0% 1.8% 1.4% 1.6%

Convene | Q1-21 Presentation

• Strong results during the quarter, driven by solid underlying top line development

• Continued growth in online consultations and roll out of mobile payment solution. The change in patient behaviour was initially driven by the pandemic, but we expect a lasting change compared to pre Covid levels.

• Stable development in number of installed solutions in the core health markets, still churn within Fitness.

• Status strategic growth projects:

o Dental Market: Pilot phase for Opus Dental integration. New integration with Anita systems.

o Leap / Faas: Substantial progress with testing and securing functionality of the platform

o Sweden: Slower progress than expected, partly related to Covid. Working diligently with partners resolve this.

11

Covid 19 update

Convene | Q1-21 Presentation

• Operations are well adapted to Covid-19 environment

• Majority of organization is still working from home

• Driver for roll out of mobile payment solutions and online consultations

• Gordion: Furlough level in 2021 is 20%

• Stable business and operations during Covid-19

• Gradual ease of restrictions and re-opening of the society

• Fitness centers local close-down during Q1. Most cities, including Oslo, have reopened fitness centers in the end of May

Agenda• Introduction to Convene

• FY21 Status

• Growth and strategic initiatives

• Financials

• Summary

13

Convene is a market leader in Norway

Market share per vertical Norway (%) 2021 (1)

(1) Market share of other competitors unknown.

20%

0%

10%

30%

40%

90%

70%

100%

60%

50%

80%

Specialists

67%

GPs

3%

61%

29%

78%

Vets

17%

93%

3%

Fitness

80%

22%

Dentists

4%

39%

Other / No solution

# of clinics with EHRs

~1,700 ~1,900 ~1,200 ~1,500~1,700

Svea

Microlog

PayEx

HelseRespons

Convene

Convene | Q1-21 Presentation

Market development during Q1

• Underlying good results during Covid-19 in our Norwegian markets.

• Stable development in number of installed solutions in our core health markets, still churn within Fitness.

• Delivered COVID patient check-lists to Unilabs Norway on terminal.

14

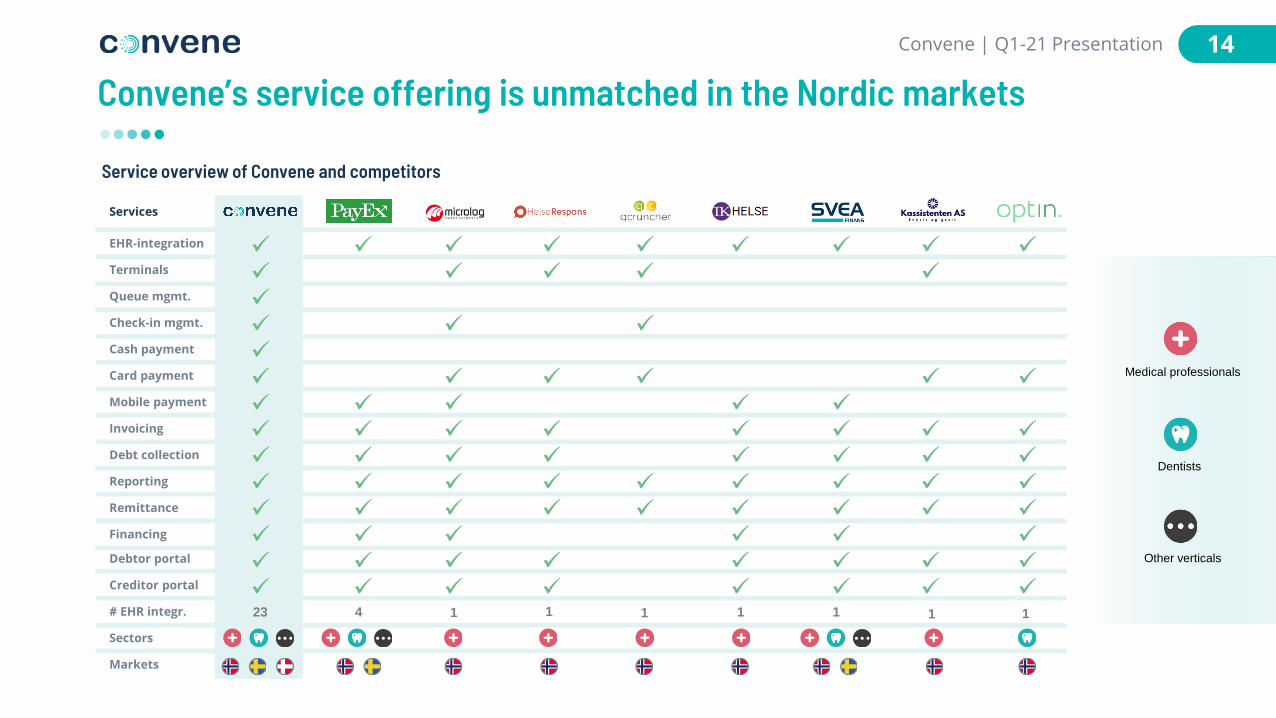

Convene’s service offering is unmatched in the Nordic markets

23

Service overview of Convene and competitors

EHR-integration

Terminals

Queue mgmt.

Check-in mgmt.

Cash payment

Card payment

Mobile payment

Invoicing

Debt collection

Reporting

Remittance

Financing

Debtor portal

Creditor portal

# EHR integr.

Sectors

Markets

Services

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

✓

11 1 1 1 14 1

Medical professionals

Dentists

Other verticals

Convene | Q1-21 Presentation

15

v

v

The Scandinavian dentist market Installed and sold solutions in the Norwegian dentist market

Market dynamics

0

100

200

300

400

500

600

700

201920162014 2015 2017 2018 2020

Clinics

Market share

Market players

Average payment

~2,200

29%

NOK 850-30,000

~2,500

1%

SEK 800-30,000

~1,300

n.a

DKK 300-30,000

Norway Sweden Denmark

• 6,000 dental clinics across Scandinavia • Major EHR provider is Opus Dental with a market share of

~95% in Norway and ~45% in Sweden.• High fees and limited acceptance for credit card payments• A large share of the population in all countries visit the

dentist annually• Most dental care covered by patients in Norway and

Sweden (exception underaged patients). 40% of the cost covered for all consumers in Denmark

• High fees favor the potential for consumer financing

Status Convene

• Opus Dental: o Existing integration for invoicing solutionso Pilot phase for terminal integration

• Anita Systems: o New EHR-system integration in Norway

• Substantial future potential driven by FaaS / patient financing project together with BraBank

v

v

Convene | Q1-21 Presentation

Q1 2021

Well positioned to increase market share in the dentist market

16

Sweden Convene | Q1-21 Presentation

Status Convene

GPs and Specialists• Integration with CGM J4 (Gothenburg), Metodika and Webdoc.

• Major potential in Stockholm and Skåne regions for GPs

o Integration agreements in place with CGM for TakeCare (Stockholm) and PMO (Skåne) since 2017/2018.

o Payment API in TakeCare has been finalized (feature not released to production)

o Approval from regions needed to get access to the healthcare platforms and implement new solutions and features (incl. payment solutions). This is delayed, partly due to Covid

o Working together with our partners to resolve this

o Region has a clear ambition and strategy for digitalization and automation of healthcare services

• Backlog of signed contracts: ~100 GP and specialists (waiting for integration)

Dental market• Integration agreement in place with Opus Dental.

o Roll out in Swedish market planned after successful launch in Norway (some development needed to amend integration to the Swedish market)

• Backlog of signed contracts: ~50 dentist clinics (waiting for integration)

Market

650 GPs and specialists and 2.500 dentist clinics

In general, fewer but larger clinics compared to Norway

Regions (län) are the decision maker and owner of EHR systems (not the clinics as in Norway)

Convene are established in GP, Hospital and Specialist, Dentist, Physiotherapist and Chiropractors.

17

ConvenePay

With ConvenePay you can easily pay for the service directly from your mobile phone, tablet or PC.

• Stable and high invoice share over time.

• Installed on private COVID test-clinics.

• Mobile payment transactions five months into the fiscal year are already on 2020 level.

FAST. SIMPLE. FLEXIBLE.

850 +Companies

1.750.000 +Transactions

Convene | Q1-21 Presentation

0

50,000

100,000

150,000

200,000

250,000

MOBILE PAYMENT TRANSACTIONS 2020 2021

18

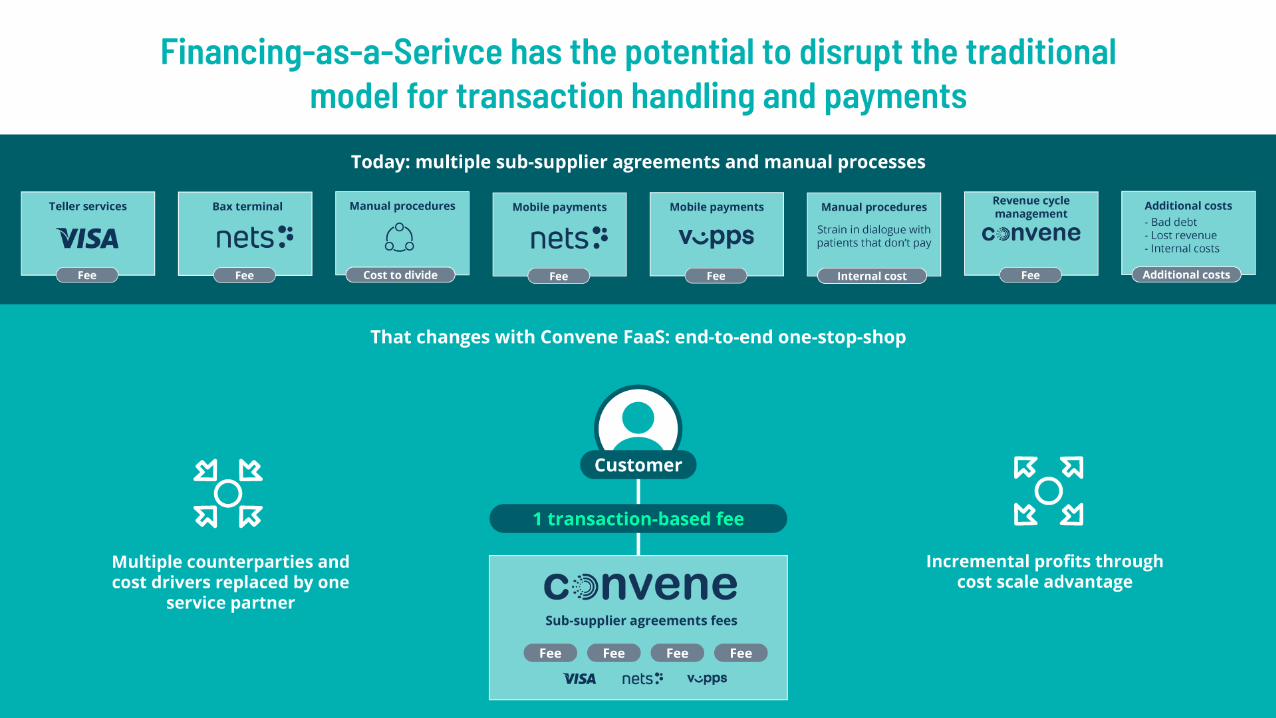

When expanding the service offering to include Financing-as-a-Service, Convene will introduce a fee

model generating revenue from all transactions

Convene | Q1-21 Presentation

BUSINESS PLAN INITIATIVES

20%

“Pay later” consumers

“Instant pay” consumers

Traditional transactions split: Instant vs. late payers Revenue share target of transactions going forward

100%~14 million

transactions

80%

19Convene | Q1-21 Presentation

20

0 50 100 150 200 250 300 350

Clear value proposition for service providers

With FaaS, service providers are guaranteed instant settlement at a lower total cost

Current resolution rate after invoice issuance

20

5%

30%

25%

0%

70%

15%

10%

20%

35%

40%

45%

50%

55%

60%

65%

75%

80%

85%

90%

95%

Resolution rate (%)

Days from invoice issuance

Instant settlement of all claims

No loss on outstanding claims

Guaranteed financing for service consumers

Only one, full-service counter party

Convene | Q1-21 Presentation

24% of outstanding invoice claims are paid within 10 days, 63% are paid within 1 month.

5% of all invoice claims are never paid

21

Faas Status

Convene | Q1-21 Presentation

• Substantial progress with project. Pilot period has stared.

• Platform is live on production environment and is currently undergoing testing and functional evaluation.

• We are handling transactions and producing invoices on weekly basis, and working with securing the moneyflow through the platform between all parties.

• Alignment and training of internal organization is in place and dedicated resources from the internal organization has been dedicated to the new platform.

• The next phase is to onboard a larger set of customers.

Agenda• Introduction to Convene

• FY21 Status

• Growth and strategic initiatives

• Financials

• Summary

23

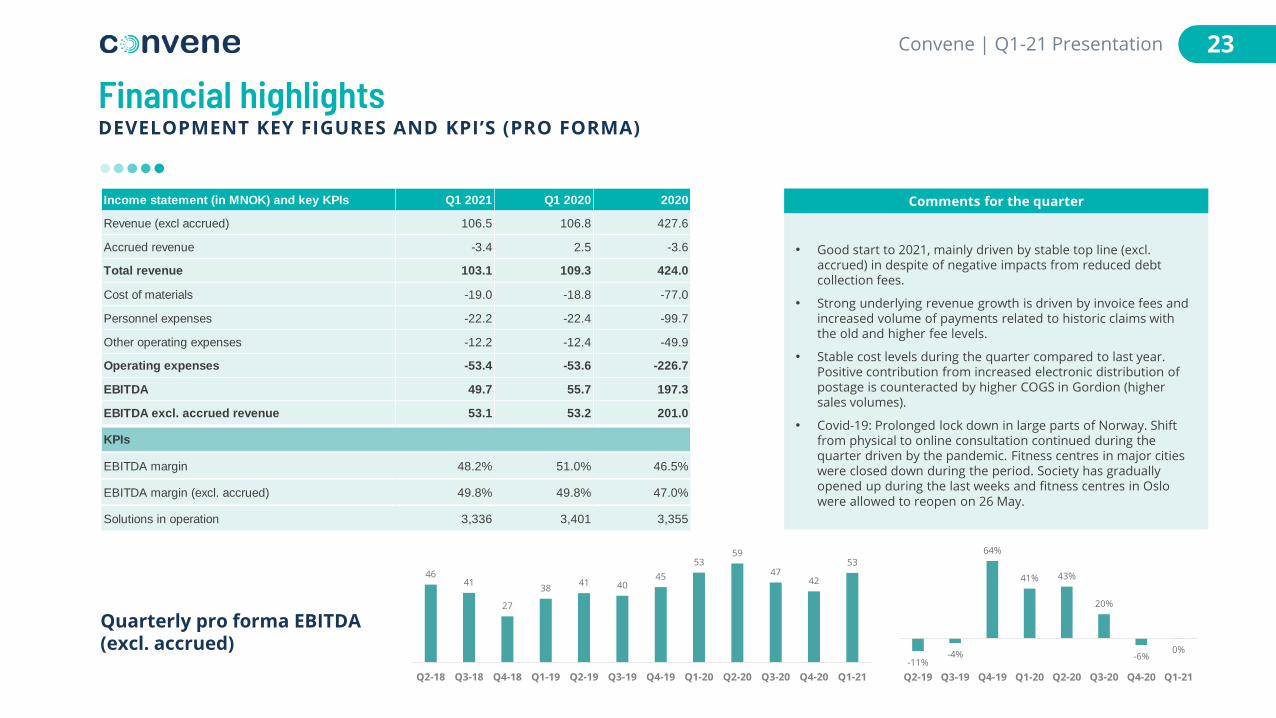

Financial highlightsDEVELOPMENT KEY FIGURES AND KPI’S (PRO FORMA)

• Good start to 2021, mainly driven by stable top line (excl. accrued) in despite of negative impacts from reduced debt collection fees.

• Strong underlying revenue growth is driven by invoice fees and increased volume of payments related to historic claims with the old and higher fee levels.

• Stable cost levels during the quarter compared to last year. Positive contribution from increased electronic distribution of postage is counteracted by higher COGS in Gordion (higher sales volumes).

• Covid-19: Prolonged lock down in large parts of Norway. Shift from physical to online consultation continued during the quarter driven by the pandemic. Fitness centres in major cities were closed down during the period. Society has gradually opened up during the last weeks and fitness centres in Oslo were allowed to reopen on 26 May.

Comments for the quarter

Quarterly pro forma EBITDA(excl. accrued)

Convene | Q1-21 Presentation

Income statement (in MNOK) and key KPIs Q1 2021 Q1 2020 2020

Revenue (excl accrued) 106.5 106.8 427.6

Accrued revenue -3.4 2.5 -3.6

Total revenue 103.1 109.3 424.0

Cost of materials -19.0 -18.8 -77.0

Personnel expenses -22.2 -22.4 -99.7

Other operating expenses -12.2 -12.4 -49.9

Operating expenses -53.4 -53.6 -226.7

EBITDA 49.7 55.7 197.3

EBITDA excl. accrued revenue 53.1 53.2 201.0

KPIs

EBITDA margin 48.2% 51.0% 46.5%

EBITDA margin (excl. accrued) 49.8% 49.8% 47.0%

Solutions in operation 3,336 3,401 3,355

4641

27

3841 40

45

5359

4742

53

Q2-18 Q3-18 Q4-18 Q1-19 Q2-19 Q3-19 Q4-19 Q1-20 Q2-20 Q3-20 Q4-20 Q1-21

-11%-4%

64%

41% 43%

20%

-6%0%

Q2-19 Q3-19 Q4-19 Q1-20 Q2-20 Q3-20 Q4-20 Q1-21

24

Top line developmentDEVELOPMENT REVENUES PER SEGMENT (AS REPORTED)

• Invoice fee: Price increase with 17% in in the end of June 20. In addition, positive contribution from an increase in online consultations and accelerated role out of mobile pay solutions.

• Final reminder fees: 50% reduction in fee levels.

• Debt collection fees: Reduction is related to reduced fee levels. Higher than expected revenue related to historic claims with the old and higher fee levels.

• Gordion: Solid first quarter as we see increased activity levels in several markets. Car parking was especially strong in the first quarter.

Comments

Convene | Q1-21 Presentation

NOK million Q1 2021 Q1 2020 delta 2020

Revenue from terminals 11 10 0 42

Revenue from invoicing 40 32 8 121

Revenue from reminder fees 4 7 -3 28

Revenue from debt collection 30 37 -8 155

Revenue from legal claims 3 3 0 12

Other revenue 10 9 0 34

Gordion 9 7 2 36

Total revenue (excl. accrued) 107 107 -0 428

Accrued revenue -3 8 -11 -4

Total revenue 103 115 -11 424

Growth year-over-year (excl. accrued revenue) -0.3% 6.0% n/a 7.1%

Growth year-over-year (reported figures) -10.0% 14.3% n/a 4.9%

25

Cash FlowCASH FLOW Q1-21 (AS REPORTED)

NOK thousands Q1 2021 Q1 2020 2020

Profit/loss before income taxes -14,447 -7,752 -71,075

Income tax payable -3,791 -815 -815

Depreciation and amortization 35,490 34,293 138,698

Interest expense lease liabilities 367 395 1,575

Changes in accounts receivable and payable -5,264 -6,084 -2,891

Change in accruals, other short-term assets and

liabilities12,143 -5,006 12,759

Net cash flow from operating activities 24,498 15,031 78,249

Payments non-current assets -10,826 -13,662 -46,371

Proceeds from disposal of non-current assets – – 175

Net cash flow from investment activities -10,826 -13,662 -46,196

Proceeds from borrowings – – –

Repayment of lease liabilities -2,801 -2,597 -11,529

Net cash flow from financing activities -2,801 -2,597 -11,529

Net change in cash and cash equivalents 10,871 -1,228 20,524

Opening cash balance 65,348 44,824 44,824

Closing cash balance 76,220 43,596 65,348

Convene | Q1-21 Presentation

26

2020-2021 EBITDA bridge2020-2021E PRO FORMA EBITDA, EXCL. ACCRUED IN MNOK

2020 EBITDA Reduction in debt and legal collection fees

Growth inSweden

Provision model and

administration fee

Invoice Fee FaaS Organic growth and

other

2021E EBITDAFTE reduction debt collection

201

-85

150 -180

Mobile PayChange in

copayment structure

-85

-10

-85

Convene | Q1-21 Presentation

Agenda• Introduction to Convene

• FY21 Status

• Growth and strategic initiatives

• Financials

• Summary

28

Summary

Convene | Q1-21 Presentation

• Strong results during the quarter

• Continued growth in online consultations and roll out of mobile payment solutions.

• Stable development in number of installed solutions in the core health markets.

• Good progress on Dental project and FaaS, slower progress then expected in Sweden.