q1 fy’18...2 mtpa steel coal mines cement road solutions lgs 17. capacity in deail iron making...

TRANSCRIPT

Q1 FY’18

Industry Update &

Key Performance Highlights

8th August, 2017

DISCLAIMERThis presentation may contain certain forward looking statements concerning JSPL’s futurebusiness prospects and business profitability, which are subject to a number of risks anduncertainties and the actual results could materially differ from those in such forward lookingstatements.

The risks and uncertainties relating to these statements include, but are not limited to, risks anduncertainties regarding fluctuations in earnings, our ability to manage growth, competition(both domestic and international), economic growth in India and the target countries forexports, ability to attract and retain highly skilled professionals, time and cost over runs oncontracts, our ability to manage our international operations, government policies and actionswith respect to investments, fiscal deficits, regulations, etc., interest and other fiscal costsgenerally prevailing in the economy. Past performance may not be indicative of futureperformance. We do not undertake to update our forward-looking statements.

This presentation is not intended, and does not, constitute or form part of any offer, invitation orthe solicitation of an offer to purchase, otherwise acquire, subscribe for, sell or otherwisedispose of, any securities in JSPL or any of it’s subsidiary undertakings or any other invitation orinducement to engage in investment activities, neither shall this presentation nor the fact of it’sdistribution form the basis of, or be relied on in connection with, any contract or investmentdecision. Few numbers in this presentation are purely indicative & provisional and could changelater.

2

OUTLOOK

Q1 FY’18

INDUSTRYDEVELOPMENTS

BRIEF BACKGROUND OPERATIONALPERFORMANCE

PRESENTATION OUTLINE

3

Global Steel Market Trend

10

11 11

7

6

8

67

Au

g-1

5

Sep

-15

Oct

-15

No

v-1

5

Dec

-15

Jan

-16

Feb

-16

Mar

-16

Ap

r-1

6

May

-16

Jun

-16

Jul-

16

Au

g-1

6

Sep

-16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

> Chinese Export down by 38% from peak level Fig in Mt

1.30%

9%

2.50%

6%

0.50%0%

1.20%

6.10%

3%

World CIS MENA ASEAN EU 28 China Japan India USA

> CY 2017 steel demand outlook revised upward

Y-o-Y

> Global Steel Prices stabilized due to

Upward demand and Firming Raw

material prices

> Chinese Exports down by 38%

> Chinese Capacity cut led to

lower pressure on Chinese Export

-Total 90.63 Mt steel capacity

closed during CY ‘16

> 2017 & 2018 World Finished Steel

Demand Revised Upward

38%

Source: WSA/Morgan Stanley 4

Source: WSA 5

799

808

105.1

104.8

89

96

1615

1629

0.8 % 800

836

4.5 %

401

420

4.6 %

52

52

0.5 %

47

49

World Crude Steel Production firmed up led by higher output from major producers

CY ‘15

No #1 China

No #2 Japan

No #3 India

CY ‘16

0.3%

7.4 %

6 Month CY ‘16 6 Month CY ‘17

5.3 %

World

1.2 %

6

Steel industry’s contribution to

National GDP

Nearly 2%

Steel Industry’s contribution to

Index of Industrial Production (IIP)

6.68%

Employment by the steel industry

Over 7lakh direct

Current Market value of the Indian

Steel Industry

$75 bn

Total Investment

expected till 2025-

2030

$187 Bn

India’s per capita steel consumption is expected to increase to 158 Kg in 2031 from current 61 Kg

> Indian steel industry continues to capitalize on its competencies to invest further.

Domestic Steel Industry continues to grow and play major role in Nation Building

116144

300

FY '16 FY '20e FY '31 (GoI Vision)

Crude Steel Capacity Projection

81.5

230

FY '16 FY '31e

Finished Steel Consumption

In Million MT (Mt)

Source: WSA

Source: JPC 7

Q1 FY ‘18 : Other Highlights

> Crude Production of Primary Producers grew by 6.4%, while the crude production of Other Producers grew by 0.1% only.

> Finished Steel Demand : o Over all Steel consumption of finished steel grew by 4.6%o Finished Carbon Steel Consumption grew by 5.7%, While Finished Alloy Steel Consumption

Decreased by 5.7%

Indian Steel Scenario : Q1 FY ’18 Major Highlights

(Qty : Mt) FY ‘17 Q1 FY ‘18

Domestic Steel Industry Qtychange

Qtychange

(y-o-y) (y-o-y)

Crude Steel Production 97.4 8.50% 24.56 3.5%

Finished Steel (Non Alloy+Alloy)

Import 7.23 -38% 1.71 -7%

Export 8.25 102% 2.04 66%

Real Consumption (Demand) 83.65 2.60% 21.0 4.6%

OUTLOOK

Q1 FY’18

INDUSTRYDEVELOPMENTS

BRIEF BACKGROUND OPERATIONALPERFORMANCE

PRESENTATION OUTLINE

8

INDUSTRY UPDATESTEEL SECTOR

9

Source: Steel Mint 10

Finished steel price trend

475485

500

445 440

470

505515

03

/Ap

r/1

7

10

/Ap

r/1

7

17

/Ap

r/1

7

24

/Ap

r/1

7

01

/May

/17

08

/May

/17

15

/May

/17

22

/May

/17

29

/May

/17

05

/Ju

n/1

7

12

/Ju

n/1

7

19

/Ju

n/1

7

26

/Ju

n/1

7

03

/Ju

l/1

7

10

/Ju

l/1

7

17

/Ju

l/1

7

24

/Ju

l/1

7

31

/Ju

l/1

7

07

/Au

g/1

7

International Flat Steel Prices ($/MT- FOB China)

Plate FOB China

445

453

450

483

03

/Ap

r/1

7

10

/Ap

r/1

7

17

/Ap

r/1

7

24

/Ap

r/1

7

01

/May

/17

08

/May

/17

15

/May

/17

22

/May

/17

29

/May

/17

05

/Ju

n/1

7

12

/Ju

n/1

7

19

/Ju

n/1

7

26

/Ju

n/1

7

03

/Ju

l/1

7

10

/Ju

l/1

7

17

/Ju

l/1

7

24

/Ju

l/1

7

31

/Ju

l/1

7

07

/Au

g/1

7

International Long Steel Prices ($/MT- FOB China)

Rebar FOB China Wire Rod FOB China

Source: Platts 11

707067

63

5557

6161

6769

7981

9188

9493

8383

7978

103103102

94

858384

80

85

88

101102

114110

114117

110110

104105

28

Ju

ly '1

7

28

Ju

ly '1

7

17

Ju

ly '1

7

30

Ju

ne

'17

15

Ju

ne

'17

31

May

'17

15

May

'17

5 M

ay '1

7

28

Ap

ril '

17

13

Ap

ril '

17

4 A

pri

l '1

7

29

Mar

'17

20

Mar

'17

7 M

ar '1

7

28

Feb

'17

14

Feb

'17

1 F

eb '1

7

26

Jan

'17

10

Jan

'17

3 J

an '1

7

Iron Ore CNF China Pellets (65%) CFR China

Lowest price

International Iron Ore & Pellet Prices remains volatile (CFR China - $/MT)

Peak price

Source: Platts, Argus 12

International Coal : Price Trend

International Coal Prices trend

(From April ‘17 till 7th August’17:)

> Prime Hard Coking Coal: down by $81/MT (FOB Australia)

> Semi Hard Coking Coal : down by $62/MT (FOB Australia)

> Steam Coal RB1 Coal : down by $7/MT (FOB S. Africa)

97 93 96

232

302

262

186164 158

260

171

146166

179

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

No

v-

16

Dec

-16

Jan

-17

Feb

-17

Mar

-1

7

Ap

r-1

7

May

-1

7

Jun

-17

Jul-

17

Lat

est

Prime Hard Coking Coal ($/MT FOB Australia)

81.4 82 88

210

269

234

168150 150

222

160

135149

160

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Lat

est

Semi Hard Coking Coal ($/MT FOB Australia)

52.76 52

64

83

91

8386

83

79 77

72

7882

84

Jan

-16

Ap

r-1

6

Jul-

16

Oct

-16

No

v-1

6

Dec

-16

Jan

-17

Feb

-17

Mar

-17

Ap

r-1

7

May

-17

Jun

-17

Jul-

17

Lat

est

Steam Coal RB1 ($/MT FOB S Africa)

INDUSTRY UPDATEPOWER SECTOR

13

Source: CEA 14

148161

174200

224245

272298

327 330

Mar'09 Mar'10 Mar'11 Mar'12 Mar'13 Mar'14 Mar'15 Mar'16 Mar'17 June'17

220.5

6.8

44.658.3

330.2

Thermal Nuclear Hydro Renewables Total

Installed Capacity (GW) in India

3.4 GW addition in Q1 FY18

Thermal67%

Nuclear2%

Hydro14%

Renewables17%

Wind 32.5

Solar 13.1

Bio Mass 8.2 Small Hydro 4.4

Renewables (GW) Portfolio

Installed Capacity Portfolio

Installed Capacity in India (June 2017)

Installed Capacity (GW) Growth

37

8095 96

307

37

7995 95

305

0.5%0.7%

0.1%

1.5%

0.7%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

0

50

100

150

200

250

300

ER & NE SR WR NR All IndiaRequirement Availability Deficit

Demand-Supply Scenario

Power Demand-Supply Position Q1 FY18 (BUs)

65

123146 153

488

64

122146 151

483

1.2%

0.8%0.4%

1.8%

1.0%

-1.0%

-0.5%

0.0%

0.5%

1.0%

1.5%

2.0%

0

50

100

150

200

250

ER & NE SR WR NR All India

Requirement Availability Deficit

Peak Demand & Peak Met in Q1 FY18 (GW)

All India power demand increased by 4.2% Y-o-Y in Q1 FY18 while supply improved by 4.3% Y-o-Y in Q1 FY18

All India demand-supply gap was 2.25 billion Units in Q1 FY18 and peak deficit during Q1 FY18 was 5 GW.

Source: CEA 15

OUTLOOK

Q1’FY18

INDUSTRYDEVELOPMENTS

BRIEF BACKGROUND

PRESENTATION OUTLINE

OPERATIONALPERFORMANCE

16

Steel PowerMines & Minerals

Global Ventures

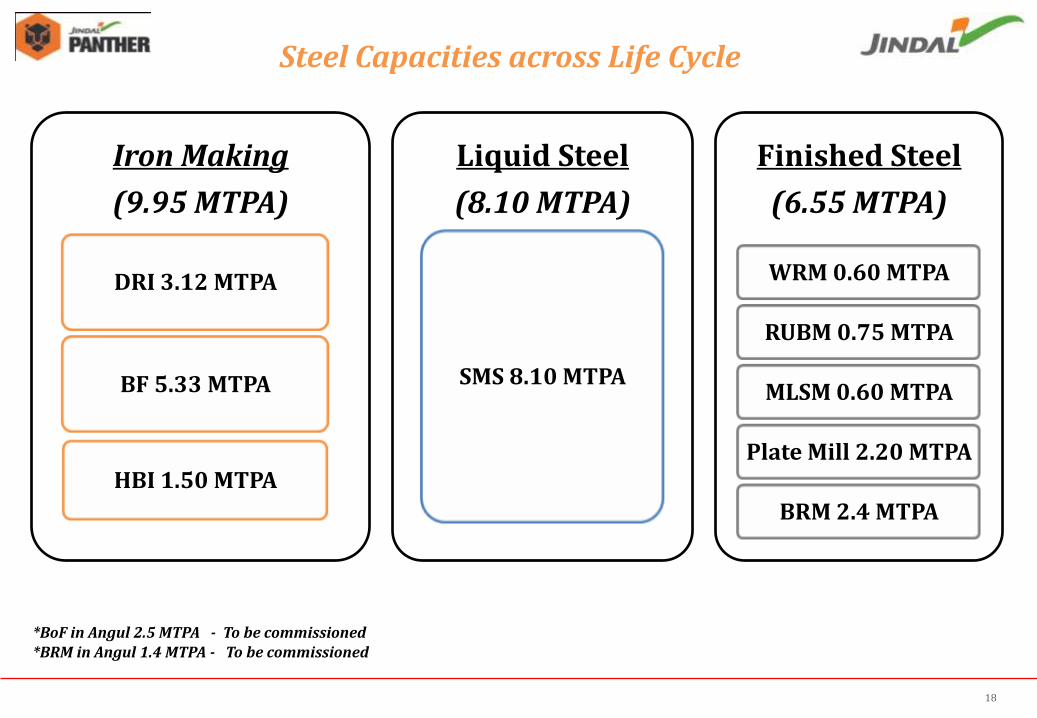

Current Capacities – Domestic & Global

Business Segments

*Domestic**1000 MW Divestment announced

Construction Material &

Solution

6.1 MTPA Steel* 3.11 MTPA*

Iron ore IPP – 3400MW**CPP – 1634 MW

2 MTPA SteelCoal Mines

CementRoad solutions

LGS

17

Capacity in deail

Iron Making

(9.95 MTPA)

BF 5.33 MTPA

DRI 3.12 MTPA

HBI 1.50 MTPA

Liquid Steel

(8.10 MTPA)

SMS 8.10 MTPA

Finished Steel

(6.55 MTPA)

WRM 0.60 MTPA

RUBM 0.75 MTPA

MLSM 0.60 MTPA

Plate Mill 2.20 MTPA

BRM 2.4 MTPA

Steel Capacities across Life Cycle

*BoF in Angul 2.5 MTPA - To be commissioned*BRM in Angul 1.4 MTPA - To be commissioned

18

Capacity in deail

Raigarh(Chhattisgarh)

SMS 3.6MTPA

BF 2.125 MTPA

DRI 1.32 MTPA

Plate Mill 1.00 MTPA

RUBM 0.75 MTPA

MLSM 0.60 MTPA

CPP 824 MW

Angul

(Odisha)

SMS 2.5 MTPA

*SMS 2.5 MTPA

DRI 1.8 MTPA

BF 3.2 MTPA

CGP 225,000 Nm3/Hr

Plate Mill 1.2 MTPA

*BRM 1.4 MTPA

CPP 810 MW

Barbil

(Odisha)

Pellet Plant

9 MTPA

Patratu (Jharkhand)

WRM 0.60

MTPA

BRM 1.0 MTPA

Oman

SMS 2.0 MTPA

HBI 1.5 MTPA

BRM 1.4 MTPA

JPL

Tamnar 3400 MW

Mining

Iron Ore 3.11

MTPA

Coal Overseas

6.60 MTPA

Detailed plant wise capacities

Power Hot Metal Liquid Steel Finished Steel

*To be commissioned

19

Standalone Q1 FY 18 –Snapshot of Key Financials (Figures in Rs. Crores)

Particulars Q1FY18 Q1FY17 Q4FY17 %YoY %QoQ

Total Revenue 3,832 3,562 4,554 +8% -16%

EBITDA 750 659 928 +14% -19%

EBITDA % 20% 19% 20%

Depreciation 481 489 489 -2% -2%

Finance Cost 532 601 529 -11% +1%

Profit/(Loss) Before Tax (263) (431) (81) +39% -224%

Profit/(Loss) After Tax (178) (277) (116) +36% -53%

Cash Profit 218 58 408 +276% -47%

20

Angul

Tamnar

RaigarhCaptive power projects (within JSPL)

ProjectCapacity

(MW)Fuel Configuration Status

DCPP, Raigarh 540 Coal 4x135 MW Operational

JSPL, Raigarh 284Coal & waste heat

2x25 MW & 40 MW(Waste heat)

2x55 MW 3x25 MW

Operational

Angul, Odisha 810 Coal 6 x135 MW Operational

Independent Power Projects (IPP)

ProjectCapacity

(MW)Fuel Configuration Status

Tamnar 1* 1,000 Coal 4x250 MW Operational

Tamnar 2 2,400 Coal 4x600 MW Operational

IPP CPP

One of the largest thermal portfolios in India

JSPL - Power Capacities

*Divestment announced 21

96.43% subsidiary of JSPL

JINDAL POWER LIMITED

EUP -I1000MW (4 X 250)

EUP -II1200MW (2 X 600)

EUP -III1200MW (2 X 600)

22

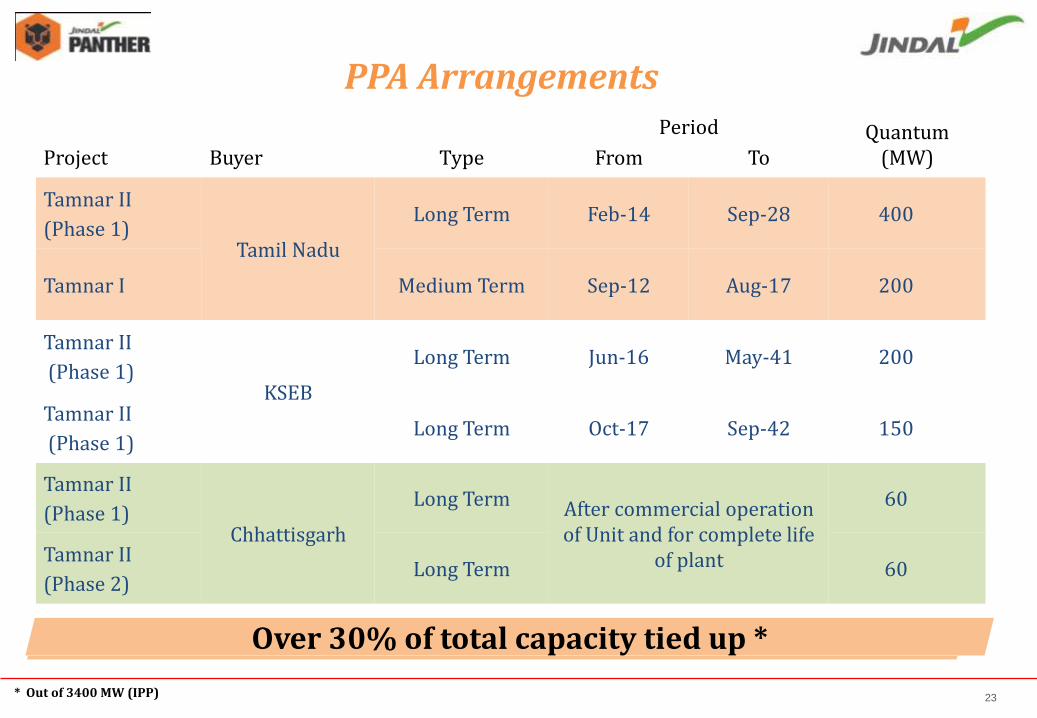

Project Buyer Type

Period Quantum (MW)From To

Tamnar II

(Phase 1)Tamil Nadu

Long Term Feb-14 Sep-28 400

Tamnar I Medium Term Sep-12 Aug-17 200

Tamnar II

(Phase 1)KSEB

Long Term Jun-16 May-41 200

Tamnar II

(Phase 1)Long Term Oct-17 Sep-42 150

Tamnar II

(Phase 1)Chhattisgarh

Long Term After commercial operation of Unit and for complete life

of plant

60

Tamnar II

(Phase 2)Long Term 60

PPA Arrangements

Over 30% of total capacity tied up *

* Out of 3400 MW (IPP) 23

Tamnar-I, 1,000 MW (EUP I)

In the interim, coal sourced through – market purchase and e-auction

Bilateral/short term/merchant

TNEB – 200 MW

258km transmission line from plant to national grid

Tamnar-II - 1,200 MW (EUP II)

Long term linkage from Mahanadi Coal Limited (MCL) and South Eastern Coalfields Limited (SECL)

TNEB – 400MW

CSEB – 60MW

KSEB – 200MW

KSEB – 150MW

Open access available

Tamnar-II - 1,200 MW (EUP III)

Market purchase and e-auction

CSEB – 60MW

Open access to be finalised against PPAs

FSA

PPA

Evacuation

Raw materials, transmission & PPAs in place for achieving higher PLF

Key Contractual Arrangements for JPL

24

JPL Q1 FY18 – Snapshot of Key Financials (Figures in Rs. Crores)

Particulars Q1FY18 Q1FY17 Q4FY17 %YoY %QoQ

Net Sales 1,079 668 863 +62% +25%

EBITDA 468 182 382 +157% +23%

EBITDA % 43% 27% 44%

Depreciation + Amortization 373 322 376 +16% -1%

Interest 227 176 235 +29% -3%

Profit/(Loss) Before Tax (62) (217) (134) +71% +54%

Profit/(Loss) After Tax (32) (217) (84) +85% +62%

Cash Profit 310 104 241 +198% +29%

Generation (MU) 3,186 2,171 2,336 +47% +36%

25

Developing a 3 MTPA coal

mine in Mozambique’s coal-

rich Moatize region

Mozambique, Africa

JSPL’s Kiepersol Colliery produces Anthracite

coal, sold domestically and internationally.

South Africa, Africa Acquired 60.3% stake in

Wollongong Coal

Australia

1.5 MT HBI , 2 MT SMS Plant &

1.4MTPA Rebar Mill – an

Integrated Steel Plant

Shadeed, Oman

Summary of International Operations

26

Oman

Holding structure for global operations

Jindal Steel & Power Ltd

Listed Operating Entity in India

Australia

Coking Coal

South Africa

Anthracite Coal

Mozambique

Thermal/ Coking Coal

Jindal Steel & Power (Mauritius) Ltd

Holding company for overseas business

2 MTPA Steel plant

27

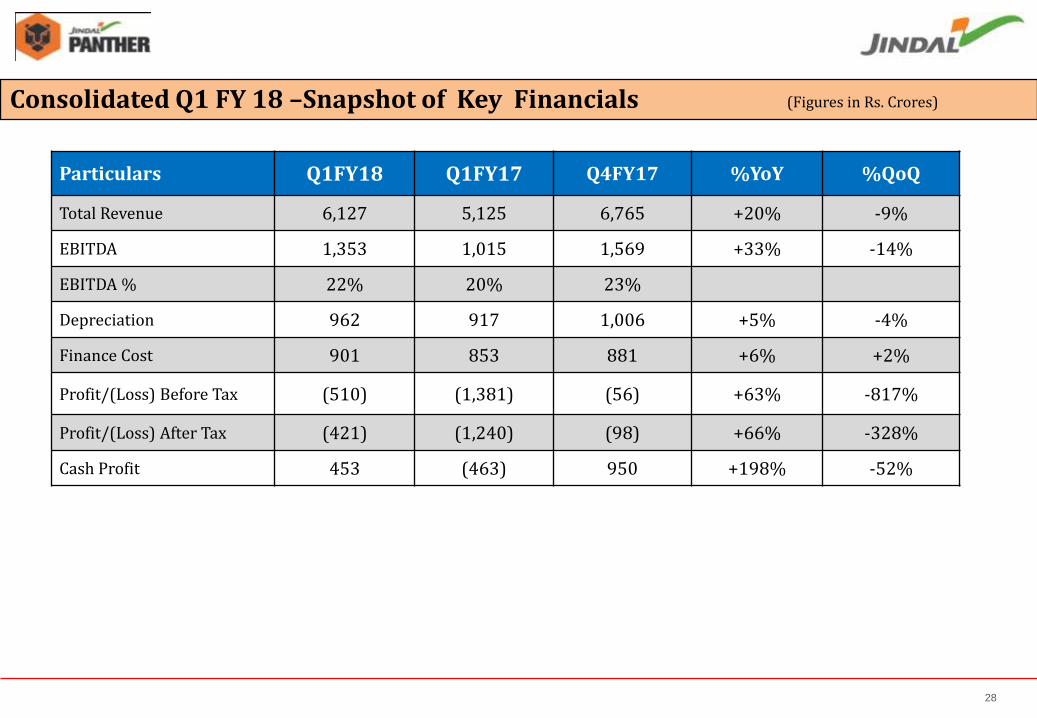

Consolidated Q1 FY 18 –Snapshot of Key Financials

Particulars Q1FY18 Q1FY17 Q4FY17 %YoY %QoQ

Total Revenue 6,127 5,125 6,765 +20% -9%

EBITDA 1,353 1,015 1,569 +33% -14%

EBITDA % 22% 20% 23%

Depreciation 962 917 1,006 +5% -4%

Finance Cost 901 853 881 +6% +2%

Profit/(Loss) Before Tax (510) (1,381) (56) +63% -817%

Profit/(Loss) After Tax (421) (1,240) (98) +66% -328%

Cash Profit 453 (463) 950 +198% -52%

(Figures in Rs. Crores)

28

OUTLOOK

Q1 FY’18

INDUSTRYDEVELOPMENTS

BRIEF BACKGROUND

PRESENTATION OUTLINE

OPERATIONALPERFORMANCE

29

Performance highlights

India’s largest Blast Furnace commissioned at Angul.

JSPL’s Standalone EBITDA increased by 14% Y-o-Y for Q1FY18

JSPL’s Consolidated Steel Production for Q1FY18 was 1.26 Million Tonne up 6% YoY (1.19 Million Tonne in Q1FY17)

JSPL’s Consolidated EBITDA increased by 33% Y-o-Y for Q1FY18

Oman records highest ever quarterly rebar production and sales in 1QFY18

JPL increased its EBITDA by 157% Y-o-Y and 23% Q-o-Q in Q1FY18

30

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18

0.84 0.88 0.840.91 0.90

0.35 0.28 0.31

0.39 0.36

Jindal Shadeed JSPL

1.301.19 1.16 1.15

Consolidated Steel Production

(Figures in Million Tonnes)

1.26

Consolidated Steel Sales

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

Q1FY17 Q2FY17 Q3FY17 Q4FY17 Q1FY18

0.78 0.81 0.84 0.920.81

0.33 0.27 0.32

0.390.34

Jindal Shadeed JSPL

1.311.11 1.08 1.16 1.15

31

Key Customers & Adding…

32

India’s largest Blast Furnace

33

For any information please contact: -

Mr. Nishant Baranwal – Head, Investor RelationsTel : +91 11-41462198Mobile:+91 8800690255Email: - [email protected]

Ms. Shweta Bagaria – Assistant Manager, Investor RelationsTel: +91-124-6612073Mobile: +91 95995 53717Email: [email protected]

34

THANK YOU

35