q3fy13 quarterly result review banking - nirmalbang.com quarterly result review- banking.pdfemail:...

TRANSCRIPT

Q3FY13 Quarterly Result Review

BANKING

Aniket Bharadia - Research Associate | Tel: 022 3926 8034

Email: [email protected]

Silky Jain - Research Analyst | Tel: 022 3926 8178

Email: [email protected]

1 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Q3FY13 Quarterly Results Review

The overall banking result for Q3FY13 was broadly on expected lines. The highlights of the overall banking results are:

Flattish growth in Net interest income

Decline in bond yields supported growth in non interest income. However core fee income continued to disappoint with lower growth in loan book

Loan book witnessed moderate growth reflecting cautious approach adopted by most of the banks

Provisions continued to remain higher impacting bottom line performance

Additions to NPA continued to remain elevated though the pace has gradually subsided as compared to Q1 and Q2FY13.

Private Banks continued to impress with an all round show whereas PSU banks once again had to bear the brunt of stressed assets.

HDFC Bank, Yes Bank, Indusind Bank, ING Vysya and J&K Bank continued to demonstrate healthy performance across all parameters amongst the private sector banks.

Within PSU Banks space; Banks like PNB and Union Bank of India surprised positively with improvement in performance on the asset quality front.

In the last quarter we had witnessed a significant rally in the banking stocks driven by improved sentiments on the overall economic situation and initiatives taken from the government of India to revive the economy. Amidst the rally, the PSU banks were the forerunners and we saw an up move of nearly 25%-30% in the stocks prior to the results. However, the rally was not sustainable as there was no major improvement in the results. This quarter was no exception to the fact that the private banks once again outpaced the PSU banks in terms of performance on all fronts, be it asset quality, business growth, core performance or profitability.

Going forward, after taking cues from various interactions with Management post results; declining interest rate cycle and improving macro economic conditions, we believe that the asset quality woes for the banking sector on a whole seems to be peaking out. Although we do not expect an immediate recovery in the performance of the banks, we believe that from Q1FY14E onwards the signs of improvement will be visible albeit on a gradual basis. We have to accept the fact that slippages will continue to remain a part and parcel of the PSU banks but better recovery efforts are likely to help them in bringing down the NPAs from the current levels.

We continue to prefer Private Banks as compared to Public Sector Banks in terms of core income growth and asset quality. Based on our analysis of the Q3FY13 results we have shortlisted some stocks which have demonstrated better performance than the other banks and based on that can outperform the overall performance of the banking sector.

Private Banks Public Sector Banks

ICICI Bank Union Bank of India Axis Bank HDFC Bank ING Vysya Bank

Punjab National Bank Oriental Bank of Commerce Dena Bank

Indusind Bank Syndicate Bank Yes Bank J&K Bank DCB

2 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

We have analyzed the Q3FY13 results of the banks based on the different parameters. The overall macro environment has seen some changes which could be a positive sign for the banking industry; once the environment improves further, the banks which are fundamentally stronger would be amongst the ones which will face a faster recovery as compared to the other banks. We have evaluated the banks on the following parameters:

Net Interest Margins Most of the banks saw improvement in NIMs on QoQ basis with decline in cost of funds as banks aggressively shed off their high cost bulk deposits. Increasing CD ratio and interest income on recoveries also supported improvement in NIMs on QoQ basis.

Among PSU banks BOB, Allahabad Bank, Andhra Bank, Corporation Bank and among private banks ICICI, Indusind, ING Vysya, DCB, J&K, Yes Bank reported sequential improvement in margins.

Going forward, we believe that the NIMs would be impacted as most of the banks have reduced their base rates and the deposit rates still remain at a comparatively higher level. Moreover most of the banks have to resort to priority sector lending which will also have an impact on the NIMs.

Source: Company data, Nirmal Bang Research

Loan growth: Source: Company data, Nirmal Bang Research

Loan Growth Advances continued to witness moderation. Most of the banks shifted the focus on the retail and SME loans and avoided corporate loans due to ongoing economic concerns. Overall industry advances grew by 15.2% in Q3FY13 (as on 28

th December 2012) as compared to 16.01% growth in Q3FY12 with the

maximum growth coming in the last fortnight of the Q3FY13.

DCB, Dena Bank, CUB, Indusind, Kotak Bank, HDFC Bank and Karur Vysya were among the few which outpaced the others showing growth way above the Industry average. However, Canara Bank, IDBI Bank of Baroda displayed poor show on advance growth front.

Sequentially most of the bank’s loan book increased. Vijaya bank (10.4%) showed an impressive double digit growth, where as Bank of India (7.7%), Union Bank of India (7.5%), Allahabad Bank (8.4%), Federal Bank (8.8%), Indusind Bank (7.6%) and Dena Bank (7.1%) also reported good growth. Going forward we expect the demand in advances would continue backed by the demand for working capital at the end of the fiscal year and Q4 being seasonally strong quarter for the banks.

3.0%2.7%

2.1%

2.8%

3.3%

2.3%

3.5%

3.1%

2.3%

3.0%

3.5%

2.5%

ICICI bank BOB IDBI Al lahabad

bank

Indusind IOB

Improvement in NIMs (QoQ)

Q2FY13 Q3FY13

3.2%3.6%

4.7%4.2%

3.3%

2.7%

3.1%3.5%

4.6%4.1%

3.3%

2.6%

Compression In NIMs (QoQ)

Q2FY13 Q3FY13

3 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Source: Company data, Nirmal Bang Research Deposit growth continued to remain lukewarm with growth being much lower than the advances growth. Overall industry deposits grew by 11.14% leading to a sharp increase in the Credit/ Deposit ratio (CD ratio).

Kotak Mahindra bank, City Union bank, DCB, Indusind, Dena bank and HDFC Bank reported good growth in deposits. Whereas PNB, Canara Bank, Federal Bank, IDBI continued to witness pressure in deposit growth.

CASA growth CASA ratio of the banks witnessed a flattish growth. The noteworthy point was that there was not a significant decline in the CASA ratio as compared to Q2FY13 levels. Industry CA is still under pressure but some banks have shown a growth in it while SA continued to witness traction. Yes Bank (75%), UCO Bank (49.4%), Indusind Bank (36.2%) witnessed YoY growth as compared to others. Sequentially UCO bank (23.7%) and Yes Bank (14.5%) are the only banks which witnessed improvement in CASA growth.

Going forward increasing competition from private sector banks for sourcing CASA deposits is likely to keep CASA growth under check.

32%

22%20% 20% 19%

17%16% 16%

15% 15% 14% 14% 13% 13%12%

10%

0.3%

Advance Growth YoY (PSU Bank)

39%

32% 31%

26% 24% 23% 22% 21% 20% 19% 18% 18% 16%

Advance Growth YoY (Pvt Bank)

46%

37%34% 32% 32% 32% 31% 31% 31% 30% 28%

26% 26% 25% 24% 22% 21%

CASA Ratio (PSU Bank)

45%41% 40% 39%

32%29% 29% 29%

26%

21% 20% 18% 17%

CASA Ratio (Pvt Bank)

Source: Company data, Nirmal Bang Research

4 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Non-interest income Most of the banks reported a muted growth in the core fee income reflecting slower loan growth. However, treasury income provided some support. The growth in treasury income was driven by fall in bond yields. Banks like Federal Bank, Canara Bank and IDBI bank also witnessed a one-time gain on sale of stake in the CARE IPO. Banks like HDFC Bank, Indusind Bank and YES Bank continued to witness strong growth in non interest income. Cost to income ratio Operating expenses of most of the PSU banks were on the higher side with provision on wage negotiation. However, private banks witnessed an improvement in the cost to income ratio driven by cost efficiencies. IDBI, IOB, Kotak Mahindra, Canara Bank and DCB showed some improvement in their Cost to Income ratio on QoQ basis where as Indian Bank, Bank of Baroda and Allahabad bank’s cost to income ratio deteriorated QoQ. Going forward we expect cost to income ratio to remain on the higher side for most of the PSU banks given the revision in wages.

Source: Company data, Nirmal Bang Research

Asset Quality: Deteriorating asset quality continued to haunt the PSU banks. A few banks saw further deterioration in their Gross NPA levels. Private banks continued to maintain their edge in terms of asset quality and gross NPA remained broadly stable. Banks like Indian Bank, UCO bank, United Bank, BOB, Andhra Bank, IOB, IDBI and SBI witnessed deterioration in asset quality. Bank of India, PNB, Union Bank, ICICI bank, Syndicate, ING Vysya and Vijaya bank reported improvement in their Gross NPAs.

The pace of increase in Gross NPA declined from the last quarter as the banks focused more on recoveries and up gradations. Recoveries and up gradations picked up pace in the last quarter (slightly better than Q1 and Q2FY13) as compared to the last two quarters which provided some cushion to the declining asset quality of the banks.

Going ahead, private banks will continue to outperform clearly reflecting better risk management and lower exposure to stressed sector. Nevertheless, we believe that even the PSU banks have witnessed bulk of the pain and now the road to recovery from current situation will be driven by support from improving macro economic conditions, declining interest rates, focus on recoveries and up gradations.

39.0%

51.3%

69.6%

50.0%

71.9%

32.0%

46.3%

65.3%

46.5%

68.5%

IDBI IOB Kotak Mah Can Bank DCB

Improvement in C/I ratio (QoQ)

Q2FY13 Q3FY13

38.9% 35.4%

45.7%40.0%

34.3%39.9%

45.9%39%

48.5%42.7%

36.5%41.7%

Indian Bank BOB Al lahabad

bank

City Union

Bank

J&K Dena

Deterioration in C/I ratio (QoQ)

Q2FY13 Q3FY13

5 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Source: Company data, Nirmal Bang Research

Provision coverage ratio remained stable for most of the banks. Private banks maintained their PCR over 75% showing that they were well equipped against the deteriorating asset quality whereas on the other hand PSU banks are still struggling to enhance the provision coverage ratio. ING Vysya Bank continued to maintain the best PCR in the industry. PNB and UBI witnessed an improvement in the coverage ratio.

Provisions increased for most of the PSU banks as they had to provide for increase in provision norms from 2% to 2.75% on restructured book. Higher provisions impacted the bottom line performance of the PSU banks. Going forward, we expect provisions to continue to remain on the higher side as under the draft RBI guidelines on provisioning for standard restructured accounts, banks are required to increase the provision requirement from 2.75% to 3.75% by FY14E and 5% by FY15. Any incremental restructuring in FY14 will have to be provided at 5%. Source: Company data, Nirmal Bang Research

Though the slippages declined marginally on sequential basis for the PSU Banks, it continued to remain at an elevated level. BOB, UCO Bank, Federal bank, Andhra Bank, OBC and IDBI saw further corrosion in their slippage ratios where as Allahabad bank, Bank of India, IOB, Canara bank, J&K Bank and SBI witnessed some improvement. Going ahead we believe that the pace of slippage will moderate with most of the banks focusing on recovery drive abating the asset quality pressure.

83%

71% 71% 69% 66% 64% 64% 61% 61% 61% 61% 59% 58% 56% 52% 49%41%

Provision Coverage Ratio ( PSU Bank )

97% 94%88%

81% 80% 80% 78% 75% 75% 70% 70% 67%59%

Provision Coverage Ratio ( Pvt Bank )

3.4%3.7% 3.5%

2.5%1.9%3.1%

3.4% 3.3%

2.3%1.8%

Bank of India Union Bank of India

ICICI Syndicate Ing Vysya

Improvement in Gross NPAs (QoQ)

Q2FY13 Q3FY13

2.06%

4.88%

3.88%

1.98%

3.87% 3.65%

5.15%

3.18%

5.53%

4.42%

2.41%

4.13%3.80%

5.30%

Indian Bank UCO bank United BOB IOB DCB SBI

Deterioration in Gross NPAs (QoQ)

Q2FY13 Q3FY13

6 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Restructured Book The proportion of restructured loan as compared to total advances continued to be significantly high in case of PSU banks. Central Bank, Andhra bank, Allahabad bank, Indian bank, PNB and IOB continued to have higher restructured book amongst PSUs where as J&K, Federal bank and South Indian Bank had higher proportion of restructured loan amongst Private banks.

However, a few banks have maintained a healthy asset quality with minimal restructured book. Kotak, DCB, Indusind, HDFC bank, Yes bank and SBI maintained low restructured book percentage to total advances. Change in regulation on restructured loan classification led to decline in restructured book for SBI and BoI.

We believe that chunk of restructuring has already taken place in 9MFY13 and Q4FY13 would probably witness the peak of restructuring as any restructuring done from Q1FY13 would attract higher provisions which will impact the bottom line performance of the banks.

Management of various PSU banks have indicated that the pipeline for restructuring looks bottoming out and with the revised guidelines of RBI on restructured book, the restructured book will stand reduced with satisfactory performance of the accounts for over two years which will make them upgraded to standard assets. We believe that improving macro economic situation and declining interest scenario would lead to a reduction in the quantum of restructured book as assets get reclassified and upgraded. Source: Company data, Nirmal Bang Research

Source: Company data, Nirmal Bang Research

5.5% 5.5%

4.6%

3.3%2.7%

2.4%

1.5% 1.3%

0.4% 0.3% 0.3% 0.2% 0.05%

Rest Book % of Total Advances

14.3%

11.5%10.8% 10.7% 10.2% 9.9% 9.5% 9.3%

8.5%7.6% 7.2% 6.9% 6.6% 6.5% 6.1% 5.6%

3.4%

Rest Book % of Total Advances

6.1%

4.2%4.8%

3.7%

1.1%0.5%

3.3% 1.7% 2.8% 3.2% 0.80% 0.2%

Al lahabad

bank

Bank of India IOB SBI J&K Ing Vysya

Improvement in Slippage Ratio (QoQ)

Q2FY13 Q3FY13

1.9%

2.9%

1.6%

2.2%

1.5%

2.5%

4.30%

2.2%2.6%

1.7%

BOB United Bank Federal bank OBC IDBI

Deterioration in Slippage Ratio (QoQ)

Q2FY13 Q3FY13

Source: Company data, Nirmal Bang Research

7 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Bank NIMs NII YoY growth

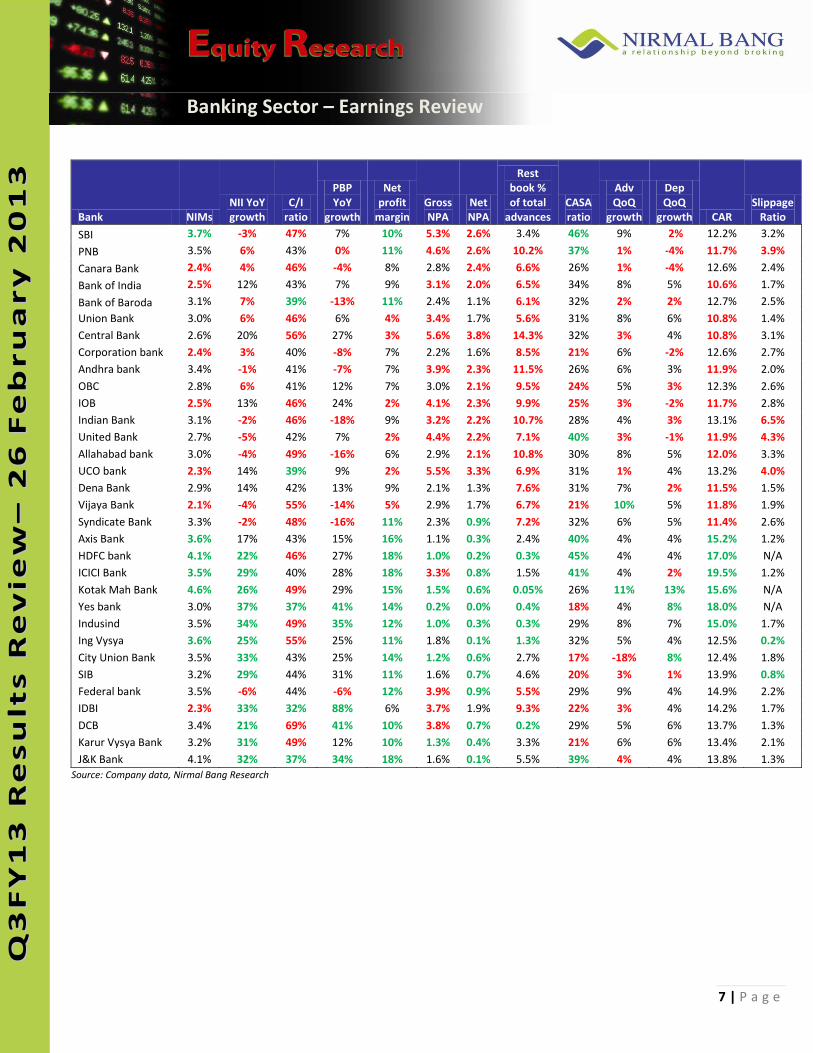

C/I ratio

PBP YoY

growth

Net profit

margin Gross NPA

Net NPA

Rest book % of total

advances CASA ratio

Adv QoQ

growth

Dep QoQ

growth CAR Slippage

Ratio

SBI 3.7% -3% 47% 7% 10% 5.3% 2.6% 3.4% 46% 9% 2% 12.2% 3.2%

PNB 3.5% 6% 43% 0% 11% 4.6% 2.6% 10.2% 37% 1% -4% 11.7% 3.9%

Canara Bank 2.4% 4% 46% -4% 8% 2.8% 2.4% 6.6% 26% 1% -4% 12.6% 2.4%

Bank of India 2.5% 12% 43% 7% 9% 3.1% 2.0% 6.5% 34% 8% 5% 10.6% 1.7%

Bank of Baroda 3.1% 7% 39% -13% 11% 2.4% 1.1% 6.1% 32% 2% 2% 12.7% 2.5%

Union Bank 3.0% 6% 46% 6% 4% 3.4% 1.7% 5.6% 31% 8% 6% 10.8% 1.4%

Central Bank 2.6% 20% 56% 27% 3% 5.6% 3.8% 14.3% 32% 3% 4% 10.8% 3.1%

Corporation bank 2.4% 3% 40% -8% 7% 2.2% 1.6% 8.5% 21% 6% -2% 12.6% 2.7%

Andhra bank 3.4% -1% 41% -7% 7% 3.9% 2.3% 11.5% 26% 6% 3% 11.9% 2.0%

OBC 2.8% 6% 41% 12% 7% 3.0% 2.1% 9.5% 24% 5% 3% 12.3% 2.6%

IOB 2.5% 13% 46% 24% 2% 4.1% 2.3% 9.9% 25% 3% -2% 11.7% 2.8%

Indian Bank 3.1% -2% 46% -18% 9% 3.2% 2.2% 10.7% 28% 4% 3% 13.1% 6.5%

United Bank 2.7% -5% 42% 7% 2% 4.4% 2.2% 7.1% 40% 3% -1% 11.9% 4.3%

Allahabad bank 3.0% -4% 49% -16% 6% 2.9% 2.1% 10.8% 30% 8% 5% 12.0% 3.3%

UCO bank 2.3% 14% 39% 9% 2% 5.5% 3.3% 6.9% 31% 1% 4% 13.2% 4.0%

Dena Bank 2.9% 14% 42% 13% 9% 2.1% 1.3% 7.6% 31% 7% 2% 11.5% 1.5%

Vijaya Bank 2.1% -4% 55% -14% 5% 2.9% 1.7% 6.7% 21% 10% 5% 11.8% 1.9%

Syndicate Bank 3.3% -2% 48% -16% 11% 2.3% 0.9% 7.2% 32% 6% 5% 11.4% 2.6%

Axis Bank 3.6% 17% 43% 15% 16% 1.1% 0.3% 2.4% 40% 4% 4% 15.2% 1.2%

HDFC bank 4.1% 22% 46% 27% 18% 1.0% 0.2% 0.3% 45% 4% 4% 17.0% N/A

ICICI Bank 3.5% 29% 40% 28% 18% 3.3% 0.8% 1.5% 41% 4% 2% 19.5% 1.2%

Kotak Mah Bank 4.6% 26% 49% 29% 15% 1.5% 0.6% 0.05% 26% 11% 13% 15.6% N/A

Yes bank 3.0% 37% 37% 41% 14% 0.2% 0.0% 0.4% 18% 4% 8% 18.0% N/A

Indusind 3.5% 34% 49% 35% 12% 1.0% 0.3% 0.3% 29% 8% 7% 15.0% 1.7%

Ing Vysya 3.6% 25% 55% 25% 11% 1.8% 0.1% 1.3% 32% 5% 4% 12.5% 0.2%

City Union Bank 3.5% 33% 43% 25% 14% 1.2% 0.6% 2.7% 17% -18% 8% 12.4% 1.8%

SIB 3.2% 29% 44% 31% 11% 1.6% 0.7% 4.6% 20% 3% 1% 13.9% 0.8%

Federal bank 3.5% -6% 44% -6% 12% 3.9% 0.9% 5.5% 29% 9% 4% 14.9% 2.2%

IDBI 2.3% 33% 32% 88% 6% 3.7% 1.9% 9.3% 22% 3% 4% 14.2% 1.7%

DCB 3.4% 21% 69% 41% 10% 3.8% 0.7% 0.2% 29% 5% 6% 13.7% 1.3%

Karur Vysya Bank 3.2% 31% 49% 12% 10% 1.3% 0.4% 3.3% 21% 6% 6% 13.4% 2.1%

J&K Bank 4.1% 32% 37% 34% 18% 1.6% 0.1% 5.5% 39% 4% 4% 13.8% 1.3%

Source: Company data, Nirmal Bang Research

8 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

Going forward: What needs to be watched out for While the asset quality for banks still remains a concern, the efforts undertaken by the banks in recovery and up-gradation will play a critical role in containment of deterioration in asset quality. Q4 is seasonally strong quarter for the bank and we may see some extravagant increase in banks operating performance driven by cyclicity impact. Apart from that we do not foresee a significant improvement in Q4FY13 earnings growth as the business environment continues to remain challenging coupled with the asset quality challenges.

The initiatives taken by the government of India in order to revive the economy will have a long term positive impact on the overall sector. We believe that positives of rate cut and revival of economy would play a crucial role in performance of the banking sector as a whole.

Based on our various parameters and current valuations we believe that the following stocks can outperform the overall banking sector. We have retained most of the stocks of our last review performance as they have been delivering consistent performance over the period. In this review we have added Union Bank of India (improving performance in the last 2 quarters); HDFC Bank (consistent performer) and PNB (positive surprise) in our list.

Stock Picks Source: Company data, Nirmal Bang Research

Bank CMP P/E Adj. P/BV Adj. P/BV * Slippage

Ratio CAR RoE (%)

ICICI Bank 1,071 13.72 1.92 1.94 1.2% 19.5% 11.9%

Axis Bank 1,391 10.70 2.23 2.28 1.2% 15.2% 18.4%

HDFC Bank 656 20.89 4.45 4.47 N/A 17.0% 17.8%

Ing Vysya Bank 541 12.77 1.87 1.89 0.2% 12.5% 12.8%

Indusind Bank 424 20.71 4.25 4.27 1.7% 15.0% 18.3%

Yes bank 469 12.25 2.96 2.98 N/A 18.0% 21.3%

J&K Bank 1,288 5.40 1.36 1.45 1.3% 13.8% 22.0%

DCB 42 9.85 1.33 1.33 1.3% 13.7% 10.1%

Union Bank of India 220 12.03 1.29 1.50 1.4% 10.8% 14.8%

PNB 835 5.42 1.26 1.59 3.9% 11.7% 16.8%

Dena 98 4.15 0.82 1.00 1.5% 11.5% 18.9%

Syndicate Bank 123 3.64 0.89 1.08 2.6% 11.4% 18.2%

OBC 278 6.21 0.78 0.95 2.6% 12.3% 9.9%

*Considering 15% of outstanding restructured book to slip into NPAs

9 | P a g e

II nn ii

tt ii aa

tt ii nn

gg

CC oo

vv ee

rraa

gg ee

Banking Sector – Earnings Review

QQ33

FFYY

1133

RRee

ssuu

ll ttss

RRee

vvii ee

ww––

2266

FFee

bbrruu

aarryy

2200

1133

NOTES

Disclaimer:

This Document has been prepared by Nirmal Bang Research (A Division of Nirmal Bang Securities PVT LTD). The information, analysis and

estimates contained herein are based on Nirmal Bang Research assessment and have been obtained from sources believed to be reliable. This

document is meant for the use of the intended recipient only. This document, at best, represents Nirmal Bang Research opinion and is meant

for general information only. Nirmal Bang Research, its directors, officers or employees shall not in anyway be responsible for the contents

stated herein. Nirmal Bang Research expressly disclaims any and all liabilities that may arise from information, errors or omissions in this

connection. This document is not to be considered as an offer to sell or a solicitation to buy any securities. Nirmal Bang Research, its affiliates

and their employees may from time to time hold positions in securities referred to herein. Nirmal Bang Research or its affiliates may from

time to time solicit from or perform investment banking or other services for any company mentioned in this document.

Nirmal Bang Research (Division of Nirmal Bang Securities PVT LTD)

B-2, 301/302, Marathon Innova, Opp. Peninsula Corporate Park

Off. Ganpatrao Kadam Marg Lower Parel (W), Mumbai-400013 Board No. : 91 22 3926 8000/8001

Fax. : 022 3926 8010