quarterly fixed income and currency … · quarterly fixed income and currency review and outlook...

TRANSCRIPT

FOR PROFESSIONAL CLIENTS ONLY. NOT TO BE REPRODUCED WITHOUT PRIOR WRITTEN APPROVAL.PLEASE REFER TO ALL RISK DISCLOSURES AT THE BACK OF THIS DOCUMENT.

QUARTERLY FIXED INCOME AND CURRENCY REVIEW AND OUTLOOKJULY 2018

UK GOVERNMENT BONDS // 5Harvey Bradley, Portfolio Manager, Fixed Income• Markets pricing in an August rate hike

• Inflation reaches one-year low

• Bank of England forecasts 0.4% GDP growth in Q2

EUROPEAN GOVERNMENT BONDS // 6Gareth Colesmith, Senior Portfolio Manager, European Fixed Income• Italy’s sovereign bonds still at risk from new government’s spending plans

• European Central Bank in little rush to raise deposit rate from negative territory

• Central bank asset purchases to wind down this year

US GOVERNMENT BONDS // 7Isobel Lee, Head of Global Fixed Income Bonds• Tax cuts and increased federal spending are underpinning the growth outlook

• We continue to expect gradual rate hikes through 2018 and beyond

• Longer-maturity bond yields have moved to fair value for now

GLOBAL INVESTMENT GRADE CREDIT // 8Peter Bentley, Head of UK and Global Credit• Credit spreads continue their choppy run

• Political risk remains a concern, but markets will benefit from low supply over summer

• Given valuations, adding risk at these levels does not look attractive

US INVESTMENT GRADE CREDIT // 10Jesse Fogarty, Senior Portfolio Manager• Credit spreads widen for second quarter running

• Trade tensions deepen, raising risk of trade war

• Valuations still look tight overall, tactically market should be supported over summer

SUMMARY

EMERGING MARKET DEBT // 11Colm McDonagh, Head of Emerging Market Fixed Income• Technical factors have driven the recent sell-off

• Emerging market fundamentals remain sound

• Indiscriminate selling has created opportunities for less constrained investors

SECURED LOANS // 13Ranbir Singh Lakhpuri, Senior Portfolio Manager, Secured Finance• Technical backdrop remains strong, even with elevated issuance levels

• Strong demand for asset class likely to remain

• Investors’ ability to push back on documentation growing

HIGH YIELD // 14Uli Gerhard, Senior Portfolio Manager, High Yield• High yield debt markets remained volatile due to political uncertainty and outflows

• Default rates expected to remain low given broadly positive economic growth outlook

• Emerging market corporates face a range of risks

ASSET-BACKED SECURITIES // 15Shaheer Guirguis, Head of Secured Finance• Asset-backed securities (ABS) markets remained steady through volatile period for risk assets

• Recent weakness driven by increased supply rather than fundamentals

• ABS markets still offer compelling strategic value given fundamental credit quality and security

CURRENCIES // 16Paul Lambert, Head of Currency• Economic growth outperforming relative to other countries, and rising trade tensions, boosted

the US dollar (USD)

• Emerging market currencies weakened across the board

• USD strength likely to persist for now

The key risk continues to be the evolution of Brexit

negotiations, as well as the profile of UK inflation

HARVEY BRADLEY

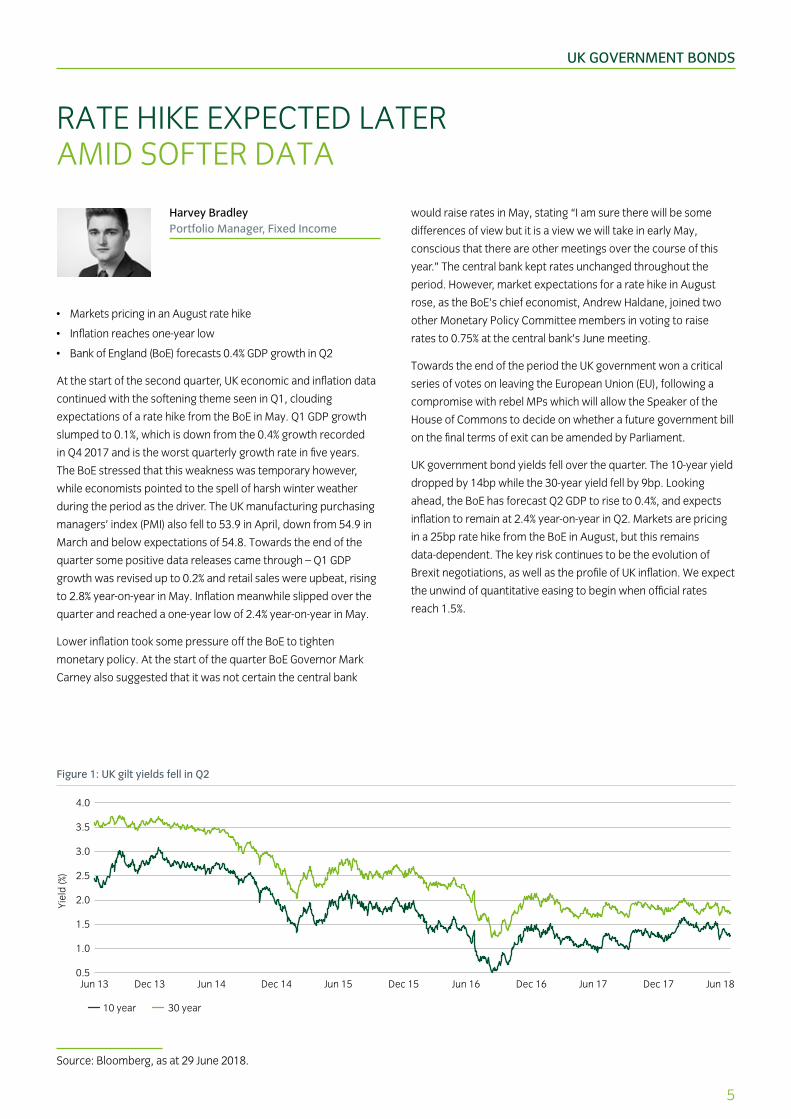

Figure 1: UK gilt yields fell in Q2

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.030-year yield

10-year yield

Jun 18Dec 17Jun 17Dec 16Jun 16Dec 15Jun 15Dec 14Jun 14Dec 13Jun 13

10 year 30 year

Yiel

d (%

)

Source: Bloomberg, as at 29 June 2018.

5

UK GOVERNMENT BONDS

RATE HIKE EXPECTED LATER AMID SOFTER DATA

Harvey Bradley Portfolio Manager, Fixed Income

• Markets pricing in an August rate hike

• Inflation reaches one-year low

• Bank of England (BoE) forecasts 0.4% GDP growth in Q2

At the start of the second quarter, UK economic and inflation data

continued with the softening theme seen in Q1, clouding

expectations of a rate hike from the BoE in May. Q1 GDP growth

slumped to 0.1%, which is down from the 0.4% growth recorded

in Q4 2017 and is the worst quarterly growth rate in five years.

The BoE stressed that this weakness was temporary however,

while economists pointed to the spell of harsh winter weather

during the period as the driver. The UK manufacturing purchasing

managers’ index (PMI) also fell to 53.9 in April, down from 54.9 in

March and below expectations of 54.8. Towards the end of the

quarter some positive data releases came through – Q1 GDP

growth was revised up to 0.2% and retail sales were upbeat, rising

to 2.8% year-on-year in May. Inflation meanwhile slipped over the

quarter and reached a one-year low of 2.4% year-on-year in May.

Lower inflation took some pressure off the BoE to tighten

monetary policy. At the start of the quarter BoE Governor Mark

Carney also suggested that it was not certain the central bank

would raise rates in May, stating “I am sure there will be some

differences of view but it is a view we will take in early May,

conscious that there are other meetings over the course of this

year.” The central bank kept rates unchanged throughout the

period. However, market expectations for a rate hike in August

rose, as the BoE’s chief economist, Andrew Haldane, joined two

other Monetary Policy Committee members in voting to raise

rates to 0.75% at the central bank’s June meeting.

Towards the end of the period the UK government won a critical

series of votes on leaving the European Union (EU), following a

compromise with rebel MPs which will allow the Speaker of the

House of Commons to decide on whether a future government bill

on the final terms of exit can be amended by Parliament.

UK government bond yields fell over the quarter. The 10-year yield

dropped by 14bp while the 30-year yield fell by 9bp. Looking

ahead, the BoE has forecast Q2 GDP to rise to 0.4%, and expects

inflation to remain at 2.4% year-on-year in Q2. Markets are pricing

in a 25bp rate hike from the BoE in August, but this remains

data-dependent. The key risk continues to be the evolution of

Brexit negotiations, as well as the profile of UK inflation. We expect

the unwind of quantitative easing to begin when official rates

reach 1.5%.

6

EUROPEAN GOVERNMENT BONDS

POLITICS DOMINATES

Gareth Colesmith Senior Portfolio Manager, European Fixed Income

• Italy’s sovereign bonds still at risk from new government’s

spending plans

• European Central Bank (ECB) in little rush to raise deposit rate

from negative territory

• Central bank asset purchases to wind down this year

The growing political discord between centrist and anti-

establishment political movements continued to be a major theme

in Europe over the second quarter.

Following weeks of negotiation after Italy’s general election, the

Five Star Movement and Lega Nord agreed a coalition to govern.

The coalition’s policy proposals included plans for an €80bn fiscal

expansion worth around 5% of GDP, including cuts in income and

corporate taxes and a minimum citizens’ income. No clues were

offered on how the programme would be funded, however. Earlier

leaked proposals – including a request for up to €250bn of Italian

debt held by the ECB to be written off and to explore mechanisms

for leaving the euro (EUR) – were rescinded from the final

proposals. From the markets’ perspective, a less significant change

of government occurred in Spain, where Prime Minister Mariano

Rajoy suffered a no-confidence vote and was replaced by the

Socialist opposition (and pro-EU) leader Pedro Sánchez.

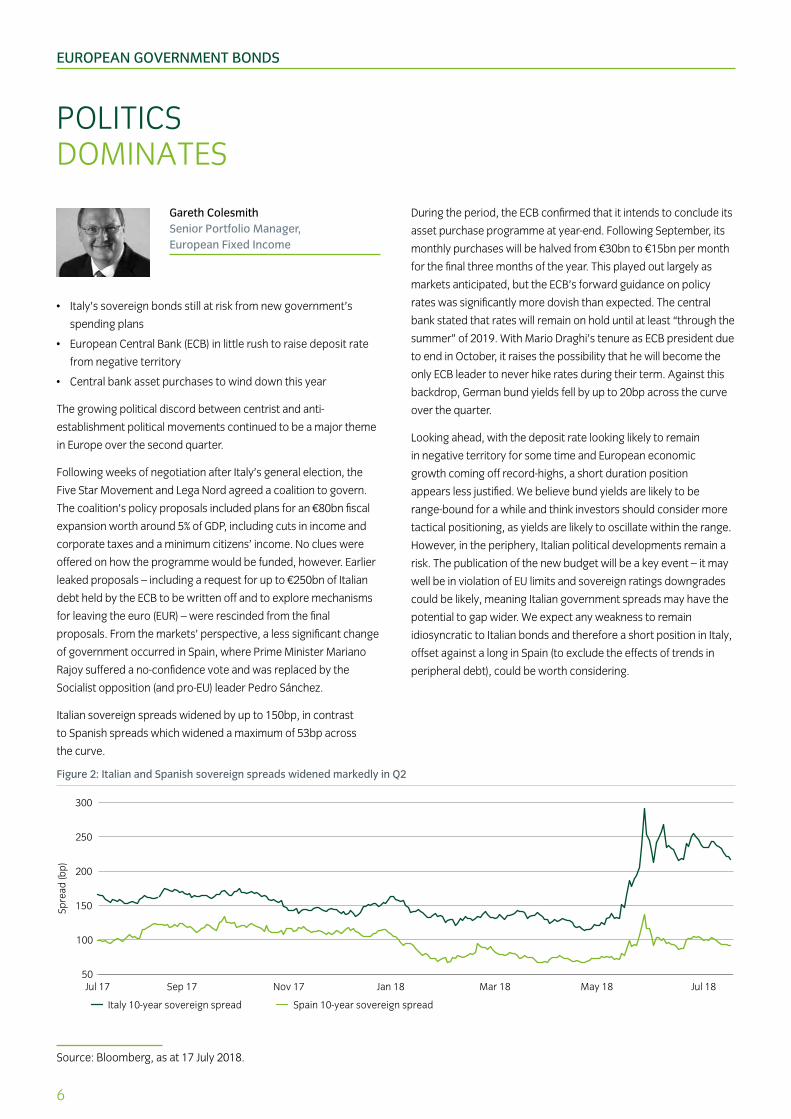

Italian sovereign spreads widened by up to 150bp, in contrast

to Spanish spreads which widened a maximum of 53bp across

the curve.

During the period, the ECB confirmed that it intends to conclude its

asset purchase programme at year-end. Following September, its

monthly purchases will be halved from €30bn to €15bn per month

for the final three months of the year. This played out largely as

markets anticipated, but the ECB’s forward guidance on policy

rates was significantly more dovish than expected. The central

bank stated that rates will remain on hold until at least “through the

summer” of 2019. With Mario Draghi’s tenure as ECB president due

to end in October, it raises the possibility that he will become the

only ECB leader to never hike rates during their term. Against this

backdrop, German bund yields fell by up to 20bp across the curve

over the quarter.

Looking ahead, with the deposit rate looking likely to remain

in negative territory for some time and European economic

growth coming off record-highs, a short duration position

appears less justified. We believe bund yields are likely to be

range-bound for a while and think investors should consider more

tactical positioning, as yields are likely to oscillate within the range.

However, in the periphery, Italian political developments remain a

risk. The publication of the new budget will be a key event – it may

well be in violation of EU limits and sovereign ratings downgrades

could be likely, meaning Italian government spreads may have the

potential to gap wider. We expect any weakness to remain

idiosyncratic to Italian bonds and therefore a short position in Italy,

offset against a long in Spain (to exclude the effects of trends in

peripheral debt), could be worth considering.

Figure 2: Italian and Spanish sovereign spreads widened markedly in Q2

Spre

ad (b

p)

Spain 10-year sovereign spreadItaly 10-year sovereign spread

50

100

150

200

250

300

Spain 10-year spreadItaly 10-year sovereign spread

Jul 18May 18Mar 18Jan 18Nov 17Sep 17Jul 17

Source: Bloomberg, as at 17 July 2018.

US GOVERNMENT BONDS

TAX REFORMS AND FEDERAL SPENDING UNDERPIN A SOLID GROWTH OUTLOOK

Isobel Lee Head of Global Fixed Income Bonds

• Tax cuts and increased federal spending are underpinning the

growth outlook

• We continue to expect gradual rate hikes through 2018

and beyond

• Longer-maturity bond yields have moved to fair value for now

The US Treasury curve shifted upwards and flattened, with shorter

maturities impacted to the largest degree, following a 25bp hike in

the federal funds rate in June. Federal Reserve (Fed) Chairman

Jerome Powell stated that the economy had strengthened

“significantly” since the global financial crisis and was now

approaching a “normal” level that no longer requires the Fed to

encourage economic activity. The Federal Open Market Committee

also changed its forecasts to reflect two further interest rate hikes

in 2018 (to take the total to four).

Economic growth slowed in the first quarter, but reaccelerated in

the second quarter with all segments of domestic demand showing

robust growth. Tensions around international trade escalated as

President Trump pressed ahead with plans to impose a 25% tariff on

$50bn of Chinese imports and allowed the exemption on key allies

for steel and aluminium tariffs to expire on 1 June. The G7 summit,

held in Quebec on 12 June, appeared to deepen divisions. Although

creating some volatility in markets, there appears to be little impact

on growth as yet, with business sentiment still at elevated levels.

The tax-reform policies implemented at the end of 2017, combined

with an agreement to increase federal spending, continues to

underpin a solid economic outlook. Inflationary pressures were

depressed through 2017, but more recent data suggests a modest

acceleration. We believe headline inflation is likely to remain above

2% in 2018 and could reach a peak of 3% if oil prices remain

elevated. The combination of strong growth and loose fiscal policy

means that we expect the Fed to continue to gradually tighten

policy until signs of economic slowdown become apparent or

financial conditions tighten significantly.

Yields on 10-year US Treasuries have been unable to move above

3% on a sustained basis, partially a result of strong demand from

US pension funds who are buying bonds to match long-term

liabilities. One consequence of the tax-reform plan is that

corporates are rushing to make pension fund contributions before

a drop in corporate tax rates later in the year reduces the tax

benefit. A surprise acceleration in inflation, possibly buoyed by

higher trade tariffs, could be a risk for bond markets, especially

if it were to come at a point when pension fund demand was

dissipating and Treasury supply increasing. In the short term,

however, the upward move in yields over the year has reduced the

overvaluation in bond markets, moving them closer to fair value –

meaning that we believe a significant duration underweight is no

longer appropriate.

Figure 3: US yield curve has flattened

Yiel

d (%

)

30 June 2018 31 March 2018 30 June 2017

0.5

1.0

1.5

2.0

2.5

3.0June 30, 2017

March 31, 2018

June 30, 2018

30Y10Y7Y5Y3Y2Y1Y6M3M1M

Maturity

Source: Bloomberg, as at 30 June 2018.

7

8

GLOBAL INVESTMENT GRADE CREDIT

NOT YET TIMETO ADD RISK

Peter Bentley Head of UK and Global Credit

• Credit spreads continue their choppy run

• Political risk remains a concern, but markets will benefit from

low supply over summer

• Given valuations, adding risk at these levels does not look

attractive

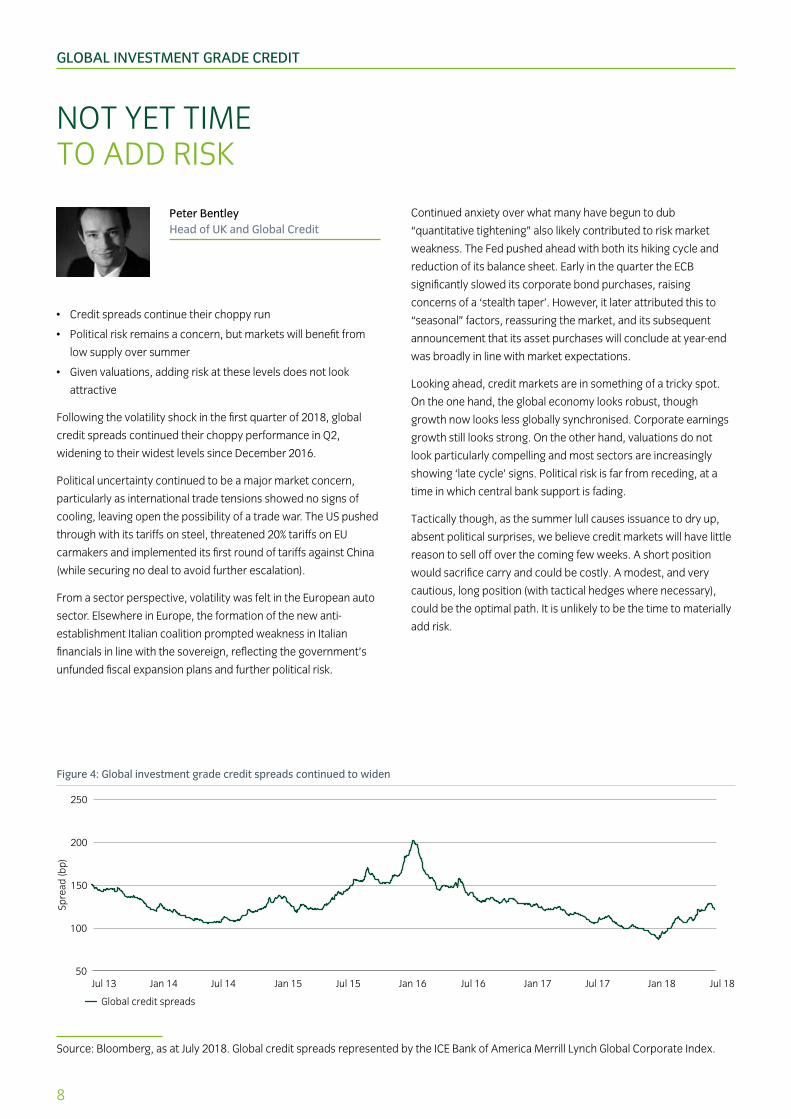

Following the volatility shock in the first quarter of 2018, global

credit spreads continued their choppy performance in Q2,

widening to their widest levels since December 2016.

Political uncertainty continued to be a major market concern,

particularly as international trade tensions showed no signs of

cooling, leaving open the possibility of a trade war. The US pushed

through with its tariffs on steel, threatened 20% tariffs on EU

carmakers and implemented its first round of tariffs against China

(while securing no deal to avoid further escalation).

From a sector perspective, volatility was felt in the European auto

sector. Elsewhere in Europe, the formation of the new anti-

establishment Italian coalition prompted weakness in Italian

financials in line with the sovereign, reflecting the government’s

unfunded fiscal expansion plans and further political risk.

Continued anxiety over what many have begun to dub

“quantitative tightening” also likely contributed to risk market

weakness. The Fed pushed ahead with both its hiking cycle and

reduction of its balance sheet. Early in the quarter the ECB

significantly slowed its corporate bond purchases, raising

concerns of a ‘stealth taper’. However, it later attributed this to

“seasonal” factors, reassuring the market, and its subsequent

announcement that its asset purchases will conclude at year-end

was broadly in line with market expectations.

Looking ahead, credit markets are in something of a tricky spot.

On the one hand, the global economy looks robust, though

growth now looks less globally synchronised. Corporate earnings

growth still looks strong. On the other hand, valuations do not

look particularly compelling and most sectors are increasingly

showing ‘late cycle’ signs. Political risk is far from receding, at a

time in which central bank support is fading.

Tactically though, as the summer lull causes issuance to dry up,

absent political surprises, we believe credit markets will have little

reason to sell off over the coming few weeks. A short position

would sacrifice carry and could be costly. A modest, and very

cautious, long position (with tactical hedges where necessary),

could be the optimal path. It is unlikely to be the time to materially

add risk.

Figure 4: Global investment grade credit spreads continued to widen

50

100

150

200

250 Global credit spreads (RHS, bp)

Jul 18Jan 18Jul 17Jan 17Jul 16Jan 16Jul 15Jan 15Jul 14Jan 14Jul 13

Global credit spreads

Spre

ad (b

p)

Source: Bloomberg, as at July 2018. Global credit spreads represented by the ICE Bank of America Merrill Lynch Global Corporate Index.

We believe credit markets will have

little reason to sell off over the coming

few weeksPETER BENTLEY

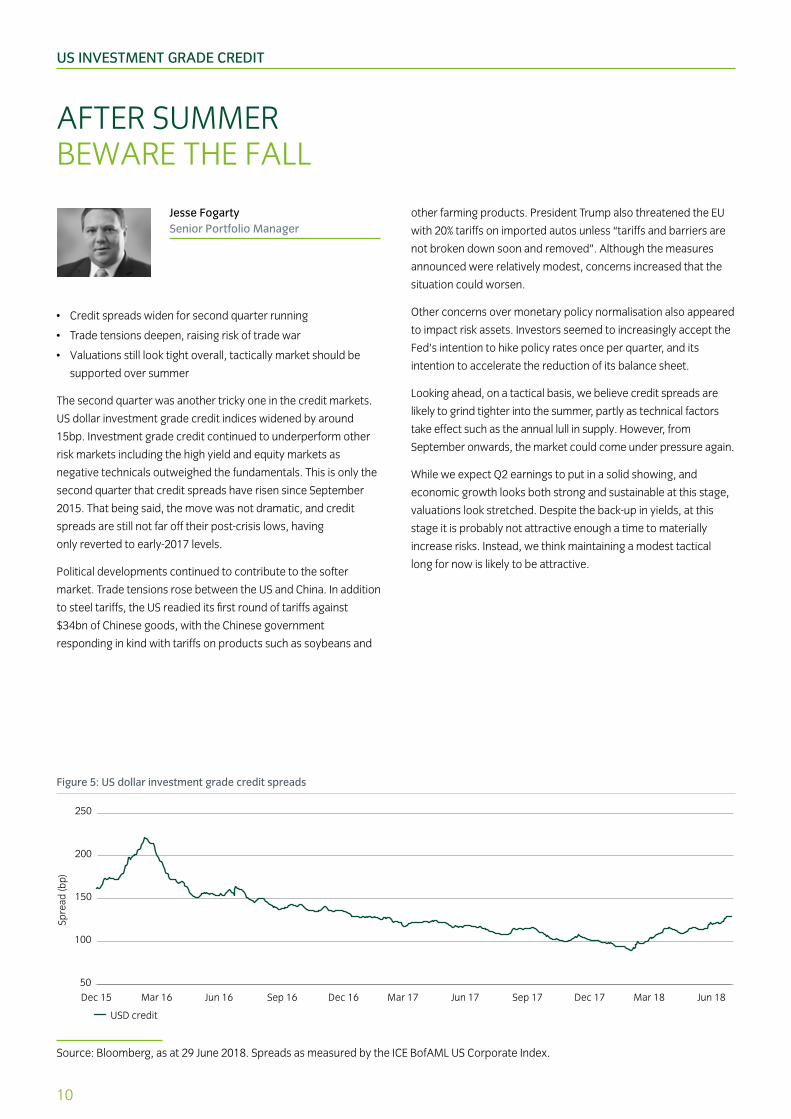

Figure 5: US dollar investment grade credit spreads

50

100

150

200

250

Jun 18Mar 18Dec 17Sep 17Jun 17Mar 17Dec 16Sep 16Jun 16Mar 16Dec 15

USD credit

Spre

ad (b

p)

Source: Bloomberg, as at 29 June 2018. Spreads as measured by the ICE BofAML US Corporate Index.

US INVESTMENT GRADE CREDIT

AFTER SUMMER BEWARE THE FALL

Jesse Fogarty Senior Portfolio Manager

• Credit spreads widen for second quarter running

• Trade tensions deepen, raising risk of trade war

• Valuations still look tight overall, tactically market should be

supported over summer

The second quarter was another tricky one in the credit markets.

US dollar investment grade credit indices widened by around

15bp. Investment grade credit continued to underperform other

risk markets including the high yield and equity markets as

negative technicals outweighed the fundamentals. This is only the

second quarter that credit spreads have risen since September

2015. That being said, the move was not dramatic, and credit

spreads are still not far off their post-crisis lows, having

only reverted to early-2017 levels.

Political developments continued to contribute to the softer

market. Trade tensions rose between the US and China. In addition

to steel tariffs, the US readied its first round of tariffs against

$34bn of Chinese goods, with the Chinese government

responding in kind with tariffs on products such as soybeans and

other farming products. President Trump also threatened the EU

with 20% tariffs on imported autos unless “tariffs and barriers are

not broken down soon and removed”. Although the measures

announced were relatively modest, concerns increased that the

situation could worsen.

Other concerns over monetary policy normalisation also appeared

to impact risk assets. Investors seemed to increasingly accept the

Fed’s intention to hike policy rates once per quarter, and its

intention to accelerate the reduction of its balance sheet.

Looking ahead, on a tactical basis, we believe credit spreads are

likely to grind tighter into the summer, partly as technical factors

take effect such as the annual lull in supply. However, from

September onwards, the market could come under pressure again.

While we expect Q2 earnings to put in a solid showing, and

economic growth looks both strong and sustainable at this stage,

valuations look stretched. Despite the back-up in yields, at this

stage it is probably not attractive enough a time to materially

increase risks. Instead, we think maintaining a modest tactical

long for now is likely to be attractive.

10

EMERGING MARKET DEBT

A TECHNICALLY DRIVEN SELL-OFF

Colm McDonagh Head of Emerging Market Fixed Income

• Technical factors have driven the recent sell-off

• Emerging market fundamentals remain sound

• Indiscriminate selling has created opportunities for less

constrained investors

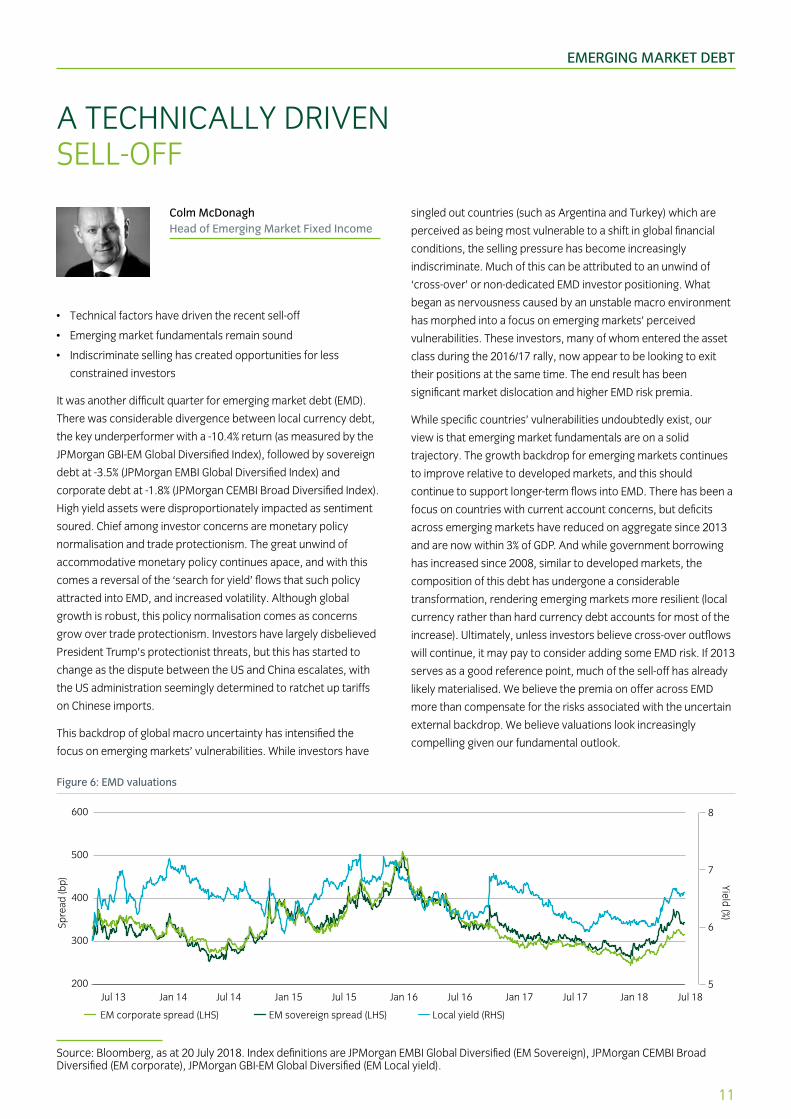

It was another difficult quarter for emerging market debt (EMD).

There was considerable divergence between local currency debt,

the key underperformer with a -10.4% return (as measured by the

JPMorgan GBI-EM Global Diversified Index), followed by sovereign

debt at -3.5% (JPMorgan EMBI Global Diversified Index) and

corporate debt at -1.8% (JPMorgan CEMBI Broad Diversified Index).

High yield assets were disproportionately impacted as sentiment

soured. Chief among investor concerns are monetary policy

normalisation and trade protectionism. The great unwind of

accommodative monetary policy continues apace, and with this

comes a reversal of the ‘search for yield’ flows that such policy

attracted into EMD, and increased volatility. Although global

growth is robust, this policy normalisation comes as concerns

grow over trade protectionism. Investors have largely disbelieved

President Trump’s protectionist threats, but this has started to

change as the dispute between the US and China escalates, with

the US administration seemingly determined to ratchet up tariffs

on Chinese imports.

This backdrop of global macro uncertainty has intensified the

focus on emerging markets’ vulnerabilities. While investors have

singled out countries (such as Argentina and Turkey) which are

perceived as being most vulnerable to a shift in global financial

conditions, the selling pressure has become increasingly

indiscriminate. Much of this can be attributed to an unwind of

‘cross-over’ or non-dedicated EMD investor positioning. What

began as nervousness caused by an unstable macro environment

has morphed into a focus on emerging markets’ perceived

vulnerabilities. These investors, many of whom entered the asset

class during the 2016/17 rally, now appear to be looking to exit

their positions at the same time. The end result has been

significant market dislocation and higher EMD risk premia.

While specific countries’ vulnerabilities undoubtedly exist, our

view is that emerging market fundamentals are on a solid

trajectory. The growth backdrop for emerging markets continues

to improve relative to developed markets, and this should

continue to support longer-term flows into EMD. There has been a

focus on countries with current account concerns, but deficits

across emerging markets have reduced on aggregate since 2013

and are now within 3% of GDP. And while government borrowing

has increased since 2008, similar to developed markets, the

composition of this debt has undergone a considerable

transformation, rendering emerging markets more resilient (local

currency rather than hard currency debt accounts for most of the

increase). Ultimately, unless investors believe cross-over outflows

will continue, it may pay to consider adding some EMD risk. If 2013

serves as a good reference point, much of the sell-off has already

likely materialised. We believe the premia on offer across EMD

more than compensate for the risks associated with the uncertain

external backdrop. We believe valuations look increasingly

compelling given our fundamental outlook.

Figure 6: EMD valuations

200

300

400

500

600 M corporate spread

M sovereign spread

Jul 18Jan 18Jul 17Jan 17Jul 16Jan 16Jul 15Jan 15Jul 14Jan 14Jul 13

EM corporate spread (LHS) EM sovereign spread (LHS) Local yield (RHS)

Spre

ad (b

p)

5

6

7

8

Local yield

Yield (%)

Source: Bloomberg, as at 20 July 2018. Index definitions are JPMorgan EMBI Global Diversified (EM Sovereign), JPMorgan CEMBI Broad Diversified (EM corporate), JPMorgan GBI-EM Global Diversified (EM Local yield).

11

We expect returns to be primarily driven by income through the remainder of 2018

RANBIR SINGH LAKHPURI

13

SECURED LOANS

INVESTORS PUSH BACK AS SUPPLY RISES

Ranbir Singh Lakhpuri Senior Portfolio Manager, Secured Finance

• Technical backdrop remains strong, even with elevated

issuance levels

• Strong demand for asset class likely to remain

• Investors’ ability to push back on documentation growing

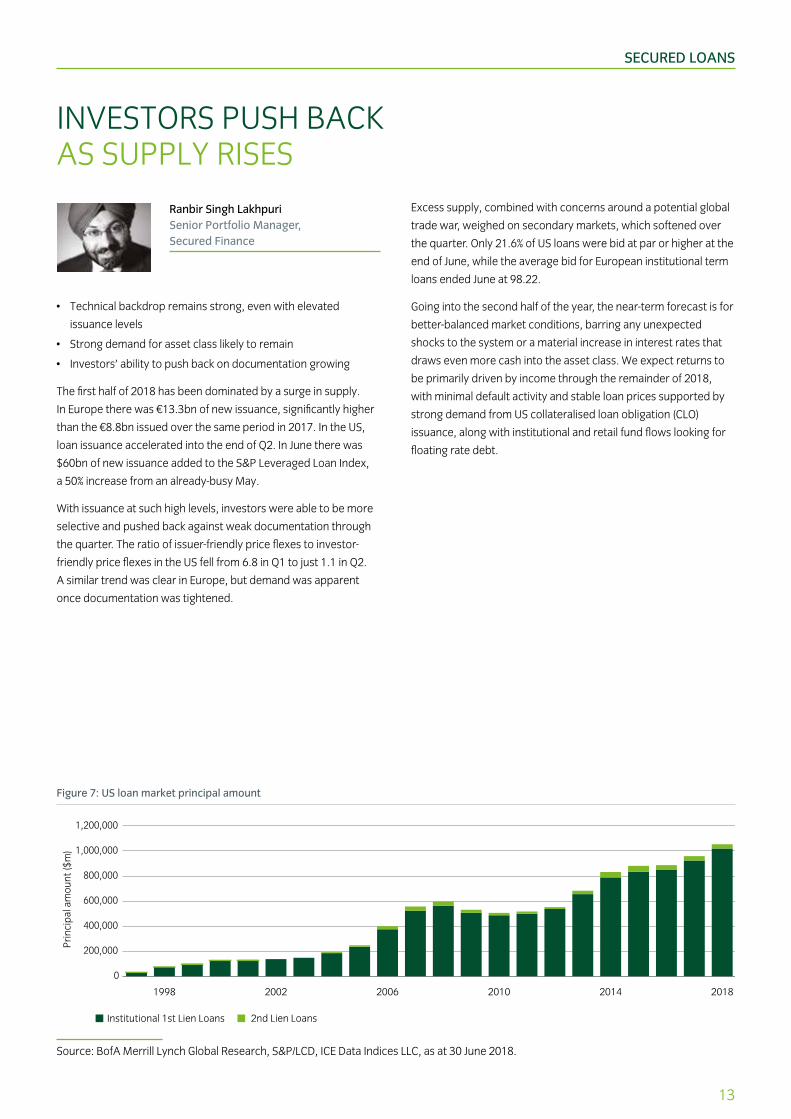

The first half of 2018 has been dominated by a surge in supply.

In Europe there was €13.3bn of new issuance, significantly higher

than the €8.8bn issued over the same period in 2017. In the US,

loan issuance accelerated into the end of Q2. In June there was

$60bn of new issuance added to the S&P Leveraged Loan Index,

a 50% increase from an already-busy May.

With issuance at such high levels, investors were able to be more

selective and pushed back against weak documentation through

the quarter. The ratio of issuer-friendly price flexes to investor-

friendly price flexes in the US fell from 6.8 in Q1 to just 1.1 in Q2.

A similar trend was clear in Europe, but demand was apparent

once documentation was tightened.

Excess supply, combined with concerns around a potential global

trade war, weighed on secondary markets, which softened over

the quarter. Only 21.6% of US loans were bid at par or higher at the

end of June, while the average bid for European institutional term

loans ended June at 98.22.

Going into the second half of the year, the near-term forecast is for

better-balanced market conditions, barring any unexpected

shocks to the system or a material increase in interest rates that

draws even more cash into the asset class. We expect returns to

be primarily driven by income through the remainder of 2018,

with minimal default activity and stable loan prices supported by

strong demand from US collateralised loan obligation (CLO)

issuance, along with institutional and retail fund flows looking for

floating rate debt.

Figure 7: US loan market principal amount

0

200,000

400,000

600,000

800,000

1,000,000

1,200,0002nd Lien Loans

Inst'l 1st Lien Loans

201820142010200620021998

Prin

cipa

l am

ount

($m

)

n Institutional 1st Lien Loans n 2nd Lien Loans

Source: BofA Merrill Lynch Global Research, S&P/LCD, ICE Data Indices LLC, as at 30 June 2018.

14

HIGH YIELD

HIGH YIELD MARKET VOLATILE BUT GROWTH REMAINS SUPPORTIVE

Uli Gerhard Senior Portfolio Manager, High Yield

• High yield debt markets remained volatile due to political

uncertainty and outflows

• Default rates expected to remain low given broadly positive

economic growth outlook

• Emerging market corporates face a range of risks

High yield debt experienced increased volatility over the quarter,

with six deals pulled in the European market. Sentiment was

affected by concerns over the Italian political situation, as well as

weakness in emerging markets, though economic data continued

to be broadly positive. Over the three months, the US high yield

market generated a small positive return, while European high

yield recorded a loss.

The economic environment, translating into positive earnings

momentum, continues to be positive for the asset class. While

investment grade funds have recently pulled back from investing

in high yield, they have done so in a relatively orderly fashion.

There are heightened credit concerns in some sectors (particularly

in the US), but defaults continue to run at low levels, supported by

the stable macroeconomic backdrop and solid capital markets.

We expect growth in the US and Europe to be enough to support

earnings momentum through the rest of this year and 2019,

keeping defaults low. However, the rate of growth in Europe has

moderately slowed and the direction of the Italian economy is of

concern. Moreover, some of the tariffs announced by the Trump

administration are set to come into effect soon, and we await the

effect on credit and clarity on what happens next.

With regard to technical factors, US and European investors

continued to sell shorter-dated paper, given rising redemptions

and higher interest rates. Year-to-date fund flows have been

negative, but we do not foresee a significant increase in supply

over the next few months. We do not expect European interest

rates to move significantly higher this year – this expectation was

reinforced by the comments from ECB President Draghi, who

stated rates were unlikely to increase before late 2019. This

benign backdrop should help to underpin demand from

investment grade accounts. However, given the risk of short-term

volatility, we continue to remain vigilant.

Risks we are alert to include heightened volatility and the

evaporation of liquidity in some emerging market corporates. We

expect comments from the Trump administration regarding

companies and sectors outside the US to result in periods of

extreme volatility. There are a variety of country-specific risks that

we are alert to: in Mexico the ongoing threat of NAFTA dissolution,

in Brazil, we will stay cautious into the October election; and we

are also keeping an eye on the Chinese yuan, and the Chinese

government’s decision to push liquidity into the domestic system

to support growth.

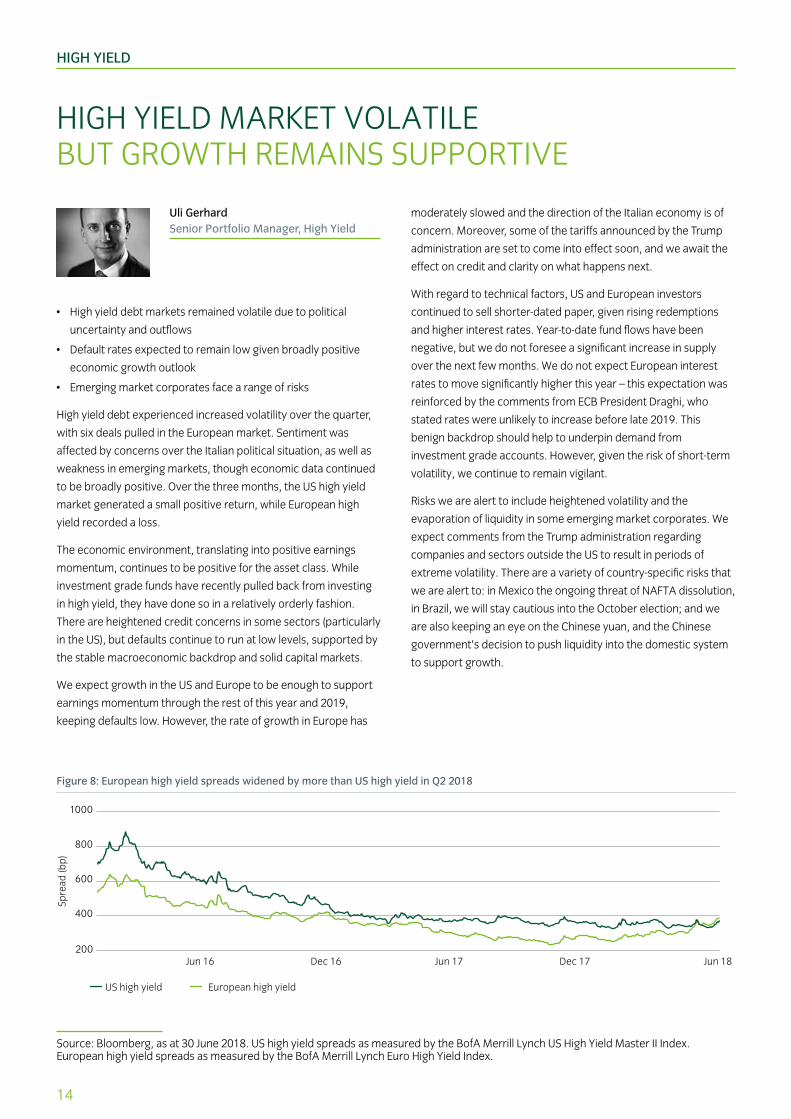

Figure 8: European high yield spreads widened by more than US high yield in Q2 2018

US high yield

European high yield

200

400

600

800

1000HE00

H0A0

Jun 18Dec 17Jun 17Dec 16Jun 16

Spre

ad (b

p)

Source: Bloomberg, as at 30 June 2018. US high yield spreads as measured by the BofA Merrill Lynch US High Yield Master II Index. European high yield spreads as measured by the BofA Merrill Lynch Euro High Yield Index.

15

ASSET-BACKED SECURITIES

FUNDAMENTALS REMAIN STRONG AS SUPPLY INCREASES

Shaheer Guirguis Head of Secured Finance

• Asset-backed securities (ABS) markets remained steady

through a volatile period for risk assets

• Recent weakness driven by increased supply rather than

fundamentals

• ABS markets still offer compelling strategic value given

fundamental credit quality and security

ABS markets remained relatively steady through a volatile quarter

for risk assets, with European ABS and US structured credit

markets moving largely in line with each other, though there were

pockets of volatility and some weakness late in the period. Early in

the quarter, investor sentiment broadly improved as trade-war

rhetoric appeared to fade and economic data showed signs of

stabilising, and risk assets performed well. However, in May,

sentiment turned as tariff disputes began to escalate and

uncertainty grew over the US-North Korean relationship. The

Italian election result had a sharp impact on risk assets. Markets

settled somewhat later in the quarter, but concerns continued to

rise over the impact of tariffs. Through this uncertainty and

volatility, ABS markets were relatively stable, though some areas

were affected by wider news.

The European ABS market began the quarter generating carry-

style returns, with relative performance within the market driven

by technical factors – the UK non-conforming market

outperformed as the available float shrank, while CLOs

underperformed in the wake of heavy issuance. The market

remained relatively steady in May, even as risk assets came under

heavy pressure due to escalating uncertainty. In response to

Italian political developments, lower-rated Italian commercial

mortgage backed-securities suffered, as did BB/BBB-rated CLOs,

but technical support – including continued ECB activity – helped

other segments of the market to remain steady. Late in the

quarter, the market weakened somewhat as lower-beta sectors,

like UK AAA-rated RMBS, suffered as supply surged; while spreads

in higher-beta sectors, such as CLOs, widened due to both supply

and weaker demand. Overall, we would note that issuance in

European ABS markets rose over the quarter. We believe this

reflects issuers seeking to wean themselves from the ECB asset

purchase programme.

The US structured credit market, as noted above, broadly moved

in line with the European ABS market. Early in the quarter, most

sectors recorded carry-style returns, and continued to remain

relatively steady through the wider market volatility in May.

However, there was some June weakness in higher-beta sectors

such as the credit risk transfer and CLO markets. Over the quarter,

supply picked up in sectors such as commercial real estate CLOs,

and from emerging sectors like mortgage insurance.

Recent weakness in the European ABS market, and US structured

credit market, has been driven by supply rather than any changes

in fundamentals. In Europe, markets have been re-pricing as ECB

asset purchases wind down, and it is not yet clear if the ECB will

reinvest maturing debt in the ABS market after the programme

ends. We have modestly reduced risk in our ABS portfolios, but

continue to believe ABS markets offer compelling strategic value

given the fundamental credit quality and security of the assets.

Figure 9: ABS spreads versus Libor were broadly stable – until late in Q2

Italian RMBS Snr UK RMBS AA GBP 5 Yr EURO CLO AA 7-8yCMBS Snr Euro

European EUR Autos Snr UK Non-Conforming RMBS Snr GBP

0

50

100

150

200

250CMBS Snr Euro

UK Non-Conforming RMBS Snr GBP

European EUR Autos Snr

EURO CLO AA 7-8y

UK RMBS AA GBP 5 Yr

Italian RMBS Snr

Jun 18Dec 17Jun 17Dec 16Jun 16

Spre

ad (b

p)

Source: JP Morgan as at 29 June 2018.

16

CURRENCIES

US ECONOMIC OUTPERFORMANCE DRIVES UP THE DOLLAR

Paul Lambert Head of Currency

• Economic growth outperforming relative to other countries,

and rising trade tensions, boosted the US dollar (USD)

• Emerging market currencies weakened across the board

• USD strength likely to persist for now

The USD reversed its weakening trend in the second quarter, rising

by 2.3% on a trade-weighted basis. The currency was supported by

the ongoing economic growth outlook in the US as well as the

growing divergence in policy between the Fed and other central

banks. In June, the Fed raised rates by 25bp, and raised its median

rate projections for 2018 and 2019. The USD also gained on the

back of rising trade tensions during the period, particularly versus

growth-sensitive commodity and emerging market currencies.

Emerging market currencies were weaker across the board. At the

beginning of the quarter, the Russian rouble (RUB) was among the

weakest performers, as the imposition of tough sanctions by the

US on Russia led investors to cut widely held long positions in the

currency. The Turkish lira also weakened notably, but recovered

somewhat in May as the combination of 300bp of emergency rate

hikes and a simplification of the Turkish central bank’s monetary

policy framework succeeded in stabilising the currency – it ended

the quarter down 13.9%. The Chinese renminbi meanwhile fell by

5.2%, as the US announced it would be imposing tariffs on a

growing range of Chinese imports.

A dovish ECB policy statement and weak data drove the EUR down

by 5.2% over Q2. Politics also weighed on the EUR in May, as

struggles to form a government in Italy led to a widening in

peripheral spreads.

US cyclical outperformance is supporting the USD, particularly

versus other major currencies. At the same time trade tensions are

leading to USD strength versus growth-sensitive currencies that

will suffer the most if global trade is disrupted. In our view this

combination can persist for now. Looking ahead, however, we are

mindful that the cyclical US outperformance is stretched relative to

history, and we are alert to any signs that relative growth rates are

starting to converge which would be negative for the USD. Any

improvement in relations between the US and its trading partners,

especially China, could also see a turnaround in USD sentiment.

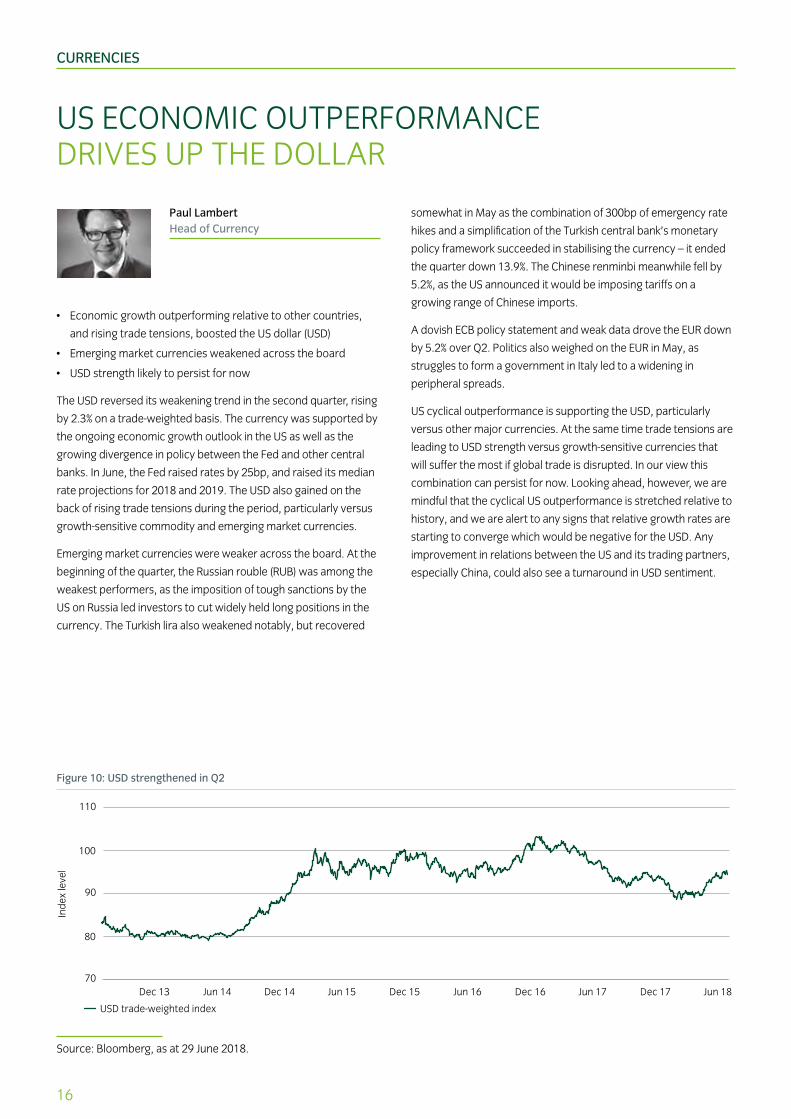

Figure 10: USD strengthened in Q2

70

80

90

100

110

Jun 18Dec 17Jun 17Dec 16Jun 16Dec 15Jun 15Dec 14Jun 14Dec 13

Inde

x le

vel

USD trade-weighted index

Source: Bloomberg, as at 29 June 2018.

CREDIT

HIGHYIELD

BANK LOANS

SECUREDFINANCE

CREDITANALYSIS

RESPONSIBLEINVESTMENT

GLOBALCREDIT

GLOBALRATES

MONEYMARKETS

EUROPEANCREDIT

INFLATIONLINKED

US FIXEDINCOME

EMD

CURRENCY

TRADING

IMPLEMENTATIONAND OPERATIONS

PRODUCTSPECIALISTS

Adrian Grey

CIO ACTIVE MANAGEMENT Head of Fixed Income

This document is a financial promotion and is not investment advice. Unless otherwise attributed the views and opinions expressed are those of Insight Investment at the time of publication and are subject to change. This document may not be used for the purposes of an offer or solicitation to anyone in any jurisdiction in which such offer or solicitation is not authorised or to any person to whom it is unlawful to make such offer or solicitation. Insight does not provide tax or legal advice to its clients and all investors are strongly urged to seek professional advice regarding any potential strategy or investment. Issued by Insight Investment Management (Global) Limited. Registered office 160 Queen Victoria Street, London EC4V 4LA. Registered in England and Wales. Registered number 00827982. Authorised and regulated by the Financial Conduct Authority. FCA Firm reference number 119308.© 2017 Insight Investment. All rights reserved.

FIND OUT MORE

Institutional Business Development [email protected] +44 20 7321 1552

European Business Development [email protected] +49 69 12014 2650 +44 20 7321 1928

Consultant Relationship Management [email protected] +44 20 7321 1023

Client Relationship Management [email protected] +44 20 7321 1499

@InsightInvestIM

company/insight-investment

www.insightinvestment.com

14094-06-18

IMPORTANT INFORMATION

RISK DISCLOSURESPast performance is not indicative of future results. Investment in any strategy involves a risk of loss which may partly be due to exchange rate fluctuations.

The performance results shown, whether net or gross of investment management fees, reflect the reinvestment of dividends and/or income and other earnings. Any gross of fees performance does not include fees and charges and these can have a material detrimental effect on the performance of an investment.

Any target performance aims are not a guarantee, may not be achieved and a capital loss may occur. Strategies which have a higher performance aim generally take more risk to achieve this and so have a greater potential for the returns to be significantly different than expected.

Portfolio holdings are subject to change, for information only and are not investment recommendations.

ASSOCIATED INVESTMENT RISKSFixed income

Where the portfolio holds over 35% of its net asset value in securities of one governmental issuer, the value of the portfolio may be profoundly affected if one or more of these issuers fails to meet its obligations or suffers a ratings downgrade.

A credit default swap (CDS) provides a measure of protection against defaults of debt issuers but there is no assurance their use will be effective or will have the desired result.

The issuer of a debt security may not pay income or repay capital to the bondholder when due.

Derivatives may be used to generate returns as well as to reduce costs and/or the overall risk of the portfolio. Using derivatives can involve a higher level of risk. A small movement in the price of an underlying investment may result in a disproportionately large movement in the price of the derivative investment.

Investments in emerging markets can be less liquid and riskier than more developed markets and difficulties in accounting, dealing, settlement and custody may arise.

Investments in bonds are affected by interest rates and inflation trends which may affect the value of the portfolio.

Where high yield instruments are held, their low credit rating indicates a greater risk of default, which would affect the value of the portfolio.

The investment manager may invest in instruments which can be difficult to sell when markets are stressed.

Where leverage is used as part of the management of the portfolio through the use of swaps and other derivative instruments, this can increase the overall volatility. While leverage presents opportunities for increasing total returns, it has the effect of potentially increasing losses as well. Any event that adversely affects the value of an investment would be magnified to the extent that leverage is employed by the portfolio. Any losses would therefore be greater than if leverage were not employed.

DONT FORGET TO INSERT CONTACT DETAILS

AND DISCLAIMER ON PREVIOUS PAGE