questionnaire analysis - world banksiteresources.worldbank.org/.../resources/analysisv23.docx ·...

TRANSCRIPT

Questionnaire AnalysisSecond draft

Nyenode Business Universiteit

September 2010

Questionnaire Analysis 2010

Sample SelectionThe respondents of this research were classified into the following sectors: business services sector; manufacturing/production related industry; Transport, logistics and communications; Agriculture, hunting or forestry; Trading and repairing of consumers goods; public administration services, government services, and obligatory social security services; construction industry; financial institutions; environmental services, culture, recreation and other services; education services; winning of natural resources; health and welfare services; production, distribution, and trading in electricity, natural gas, steam, and water; renting and trading of real estate and movable properties; catering industry; and fisheries. Despite classifying and including industries in broad and inclusive categories there were, nevertheless, some responses that didn’t fit into this classification. Hence they are treated as “other sectors”.

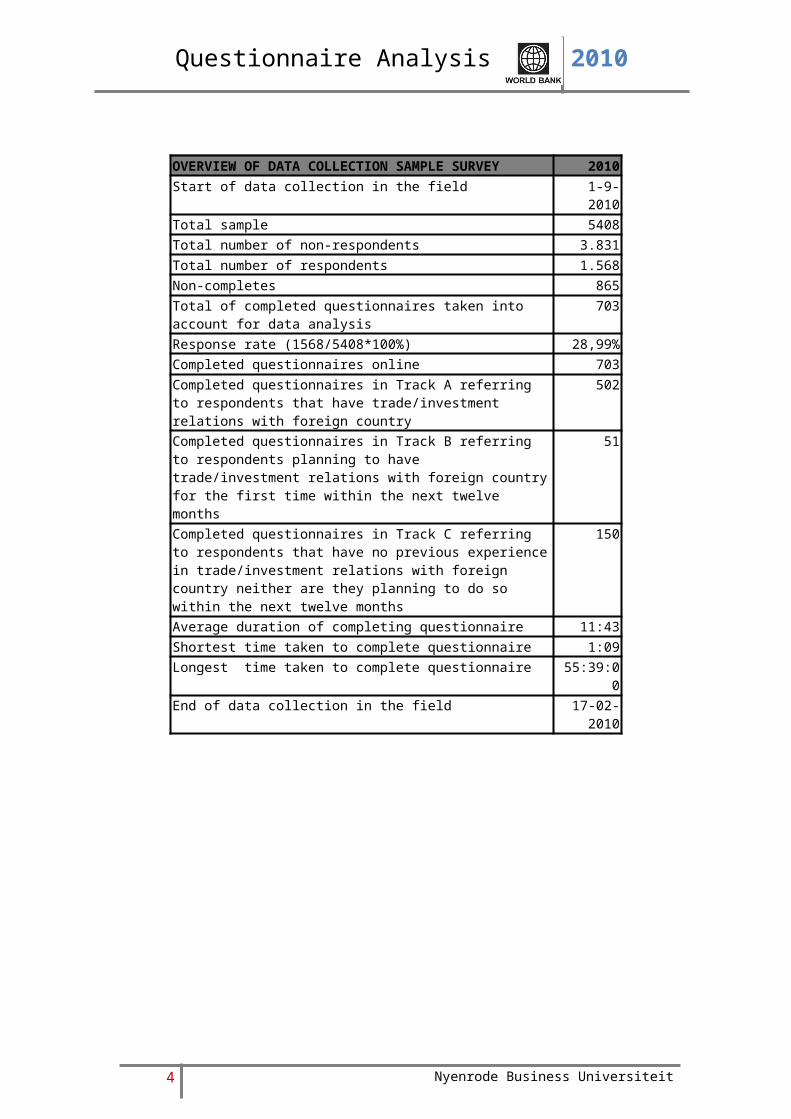

Data CollectionAfter identifying the key sectors that are crucial for the research, a data base was acquired which included foreign and Dutch service and production firms operating from the Netherlands per September 2009. An online questionnaire was designed to capture the objectives of this research. This questionnaire was then tested and discussed with the World Bank and targeted firms. Based on these consultations amendments were incorporated. The questionnaire in its final form consisted of 27 questions capturing the following issues on firm level: company details, gender information of firms’ employees at the domestic location, foreign trade and investment relations, offshoring activities, information about employees employed at foreign locations and other information regarding foreign locations (Appendix #). Based on their response to first question (S1), respondents are divided into one of three categories: those with previous experience in foreign trade/investments (Track A), those planning to have foreign trade/investment relations within the next 12 months (Track B), and those neither having foreign trade/investment experience nor having plans to do so within the next 12 months (Track C) –. An invitation letter specifying the purpose of the research including a link to an online questionnaire was sent per e-mail to the research population represented in our database consisting of 5.408 firms with an emphasis on compliance to strict data secrecy. Appropriate reminders per e-mail and timely follow up per telephone resulted in 1568 companies accepting the invitation to participate in the research while the rest either declined or did not respond. Among these 1.568 companies, 865 respondents did not complete the questionnaire and hence their responses were not considered for the analysis represented in the underlying report. The response rate, defined as the percentage of the invitations versus the number of completed questionnaires, was 28.99% (1568/5408*100%) as depicted in table below.

2 Nyenrode Business Universiteit

Questionnaire Analysis 2010

OVERVIEW OF DATA COLLECTION SAMPLE SURVEY 2010Start of data collection in the field 1-9-2010Total sample 5408Total number of non-respondents 3.831Total number of respondents 1.568Non-completes 865Total of completed questionnaires taken into account for data analysis 703

Response rate (1568/5408*100%) 28,99%Completed questionnaires online 703Completed questionnaires in Track A referring to respondents that have trade/investment relations with foreign country

502

Completed questionnaires in Track B referring to respondents planning to have trade/investment relations with foreign country for the first time within the next twelve months

51

Completed questionnaires in Track C referring to respondents that have no previous experience in trade/investment relations with foreign country neither are they planning to do so within the next twelve months

150

Average duration of completing questionnaire 11:43Shortest time taken to complete questionnaire 1:09Longest time taken to complete questionnaire 55:39:00End of data collection in the field 17-02-2010

3 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Above figure provides an overview of the industry sectors that participated in this research. The majority of respondents (31.58%) belong to the business services sector; followed by respondents in manufacturing/production related industry (18.78%); Transport, logistics and communications (9.53%); Agriculture, hunting or forestry and Trading and repairing of consumers goods (both 7.82%).

4 Nyenrode Business Universiteit

Questionnaire Analysis 2010

The responses are segregated for the organizations’ foreign trade/investment relations with MENA region and the rest of the world. It shows that 1.65% of the respondents engaged in providing business services have relatively high percentage of trade/investment relationship with the MENA region. This is followed by 1.10% of respondents in industry, 0.86% in trading and repairing of consumer goods, and 0.78% in transport, logistics, and communication.

5 Nyenrode Business Universiteit

Agriculture, hunting or forestry

Winning of natural resources

Industry

Production, distribution andtrade in electricity, natural

gas, steam and water

Construction industry

Trading and repairingof consumer goods

Catering industry

Transport, logisticsand communications

Financial institutions

Renting and trading in realestate and movable property

Public administration services,government services andobligatory social security

Education

Business services

Health and welfare services

Environmental services, culture,recreation and other services

Other industries

0 5 10 15 20 25 30

Industrial classification - MENA vs Rest of the World

Trade / investment relations with rest of the worldTrade / investment relations in MENA

Percentage of responses

Indu

stry

Questionnaire Analysis 2010

Agriculture, hunting or forestry

Winning of natural resources

Industry

Production, distribution andtrade in electricity, natural

gas, steam and water

Construction industry

Trading and repairingof consumer goods

Catering industry

Transport, logisticsand communications

Financial institutions

Renting and trading in realestate and movable property

Public administration services,government services andobligatory social security

Education

Business services

Health and welfare services

Environmental services, culture,recreation and other services

Other industries

0 20 40 60 80 100

Comparision of foreign trade/investment relations between MENA and rest of the world per industry

Trade / investment relations in MENA Trade / investment relations with rest of the world

Percentage of responses

Indu

stry

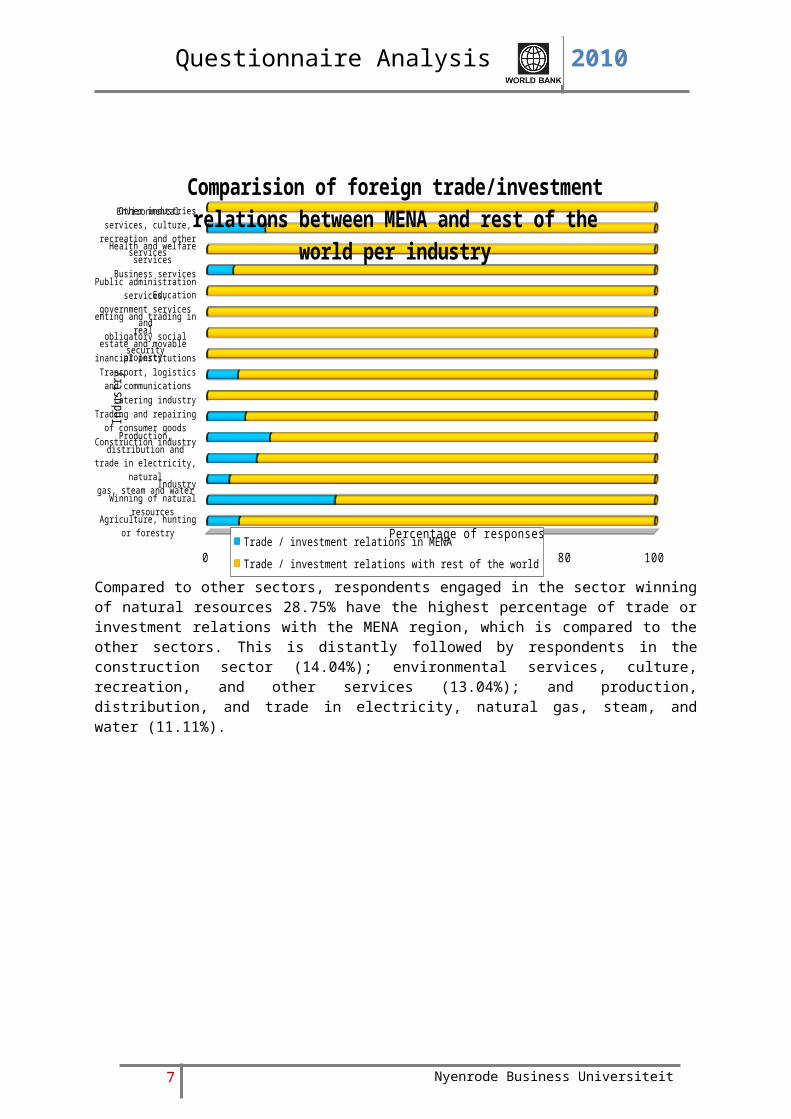

Compared to other sectors, respondents engaged in the sector winning of natural resources 28.75% have the highest percentage of trade or investment relations with the MENA region, which is compared to the other sectors. This is distantly followed by respondents in the construction sector (14.04%); environmental services, culture, recreation, and other services (13.04%); and production, distribution, and trade in electricity, natural gas, steam, and water (11.11%).

6 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Trade / investmentrelations in MENA

Trade / investment rela-tions

with rest of the world

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Comparison between type of industries that have foreign trade/investment relations with MENA and

rest of the world

Agriculture, hunting or forestry Winning of natural resources IndustryProduction, distribution andtrade in electricity, naturalgas, steam and water

Construction industry Trading and repairingof consumer goods

Catering industry Transport, logisticsand communications

Financial institutions

Renting and trading in realestate and movable property

Public administration services,government services andobligatory social security

Education

Business services Health and welfare services Environmental services, culture,recreation and other services

Other industries

Percentage of responses

Regio

n

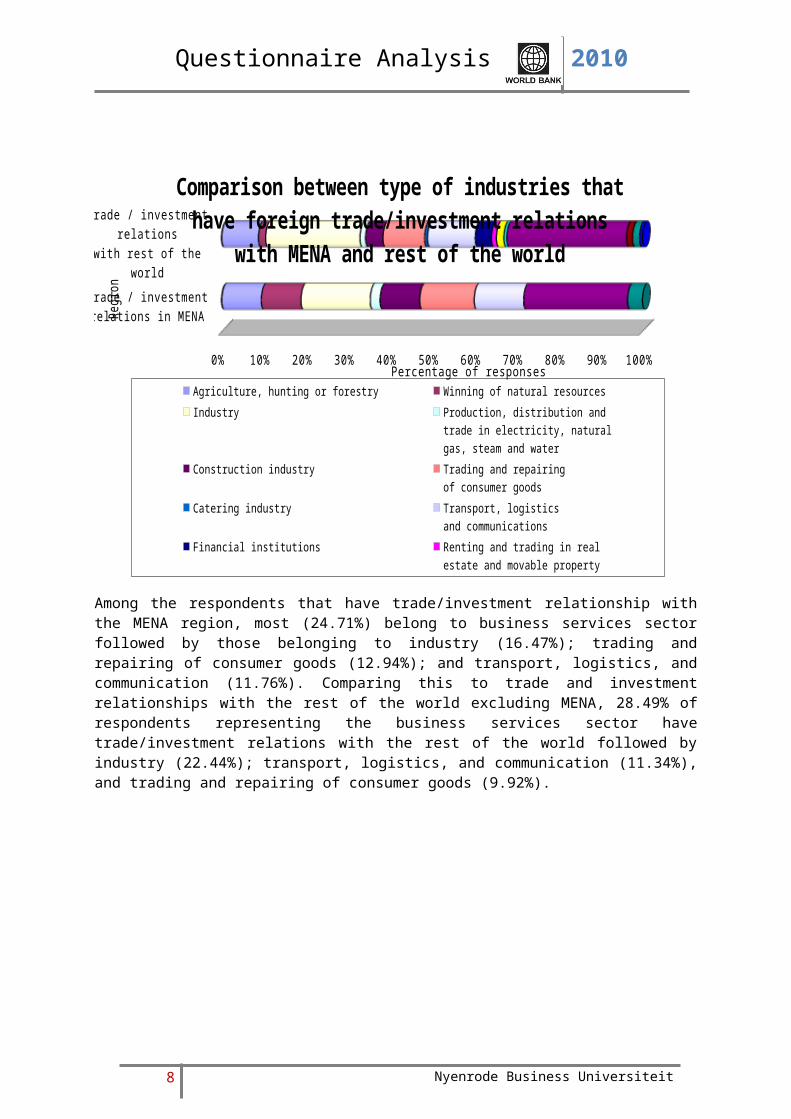

Among the respondents that have trade/investment relationship with the MENA region, most (24.71%) belong to business services sector followed by those belonging to industry (16.47%); trading and repairing of consumer goods (12.94%); and transport, logistics, and communication (11.76%). Comparing this to trade and investment relationships with the rest of the world excluding MENA, 28.49% of respondents representing the business services sector have trade/investment relations with the rest of the world followed by industry (22.44%); transport, logistics, and communication (11.34%), and trading and repairing of consumer goods (9.92%).

7 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Further, nearly half of the respondents (48.08%) indicated that they are not part of an enterprise, while 24.89% indicated that the organization they are representing is a subsidiary. Further, 14.65% of the respondents represented headquarters of a multinational group of enterprise and 12.38% represented headquarters of domestic group of enterprises, as indicated in figure above.

8 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Yes, it is the parent of anall-resident group of enterprises

Yes, it is the parent of amultinational group of en-

terprises

Yes, it is a subsidiary

No, it is not part of an enterprise group

0 5 10 15 20 25 30 35 40

Type of organization - MENA vs rest of the world

Rest of the worldMENA Region

Percentage of responses

Type

of o

rgan

izat

ion

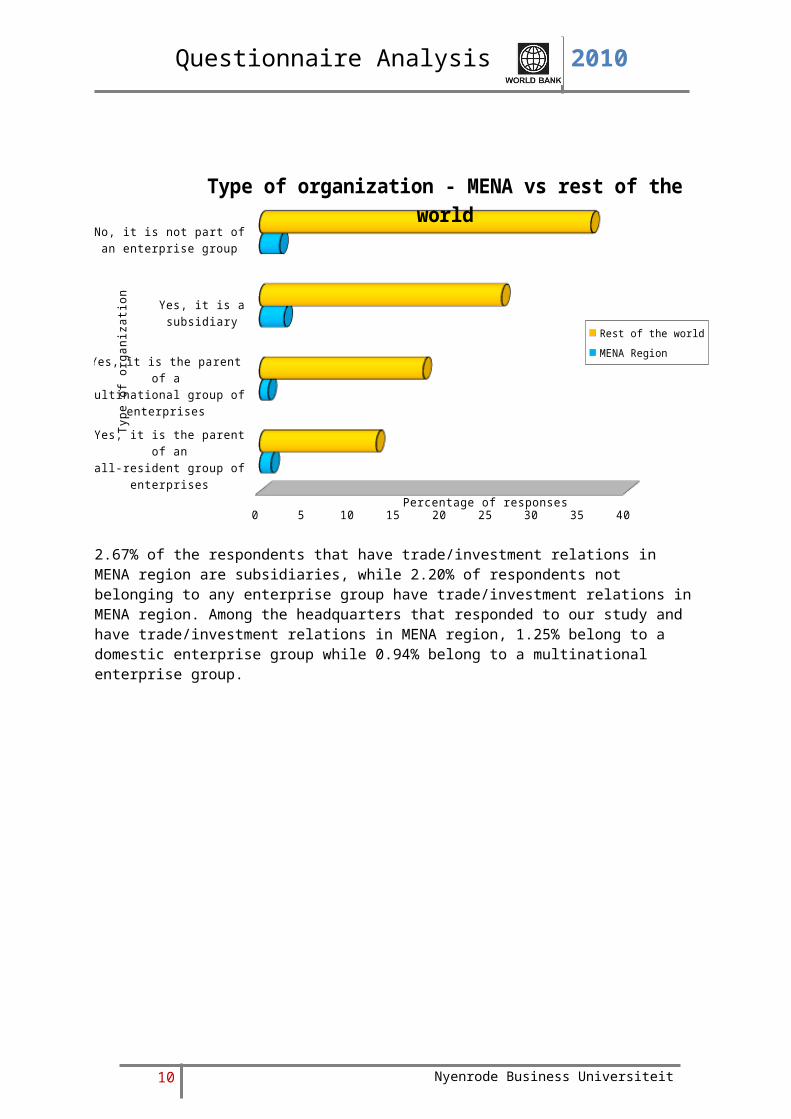

2.67% of the respondents that have trade/investment relations in MENA region are subsidiaries, while 2.20% of respondents not belonging to any enterprise group have trade/investment relations in MENA region. Among the headquarters that responded to our study and have trade/investment relations in MENA region, 1.25% belong to a domestic enterprise group while 0.94% belong to a multinational enterprise group.

9 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Yes, it is the parent of anall-resident group of enterprises

Yes, it is the parent of amultinational group of en-

terprises

Yes, it is a subsidiary

No, it is not part of an enterprise group

0 20 40 60 80 100 120

Preferred region for foreign trade/investment per type of organization

MENA Region Rest of the world

Percentage of responses

Type

of o

rgan

izat

ion

9.19% of the subsidiaries have trade/investment relation in the MENA region followed by Dutch domestic enterprise group (8.99%); non-enterprise group (5.74%) and then multinational enterprise group (5.02%).

10 Nyenrode Business Universiteit

Questionnaire Analysis 2010

MENA Region

Rest of the world

0 20 40 60 80 100

Type of organization per region

Yes, it is the parent of anall-resident group of enterprisesYes, it is the parent of amultinational group of enterprisesYes, it is a subsidiaryNo, it is not part of an enterprise group

Percentage of responses

Reg

ion

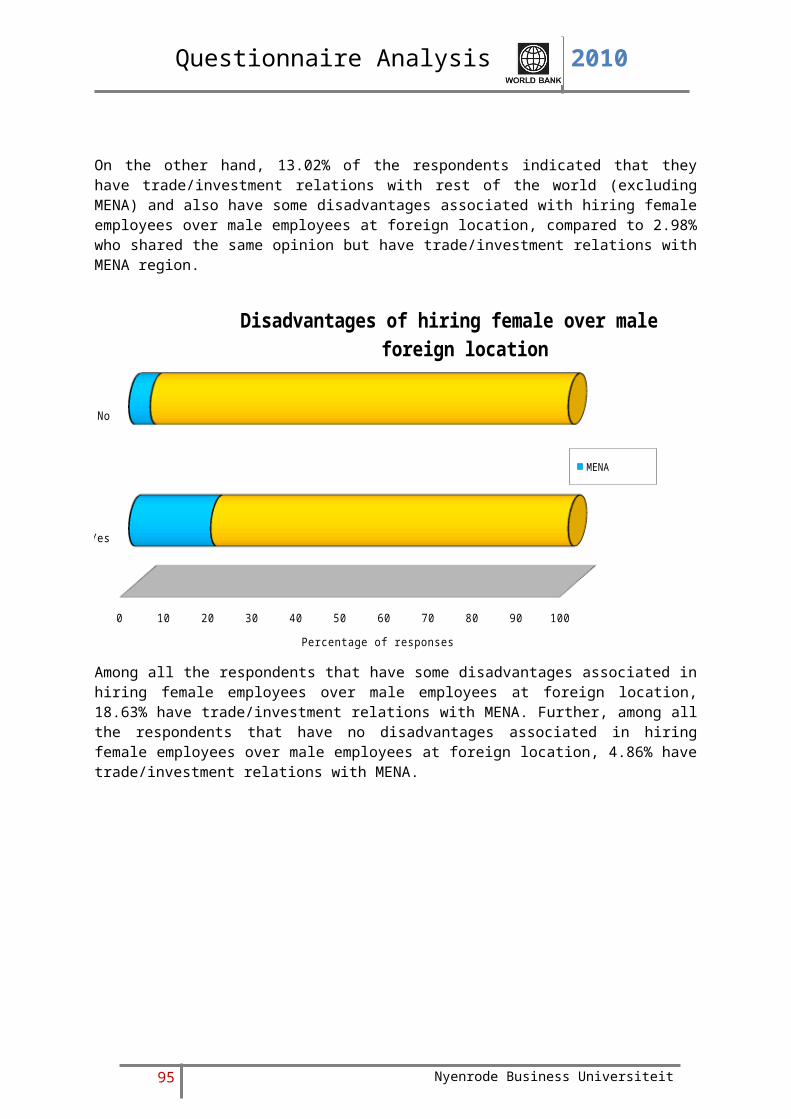

Of all the respondents that have trade/investment relations with the MENA region, 37.78% are subsidiaries of an enterprise groups, followed by those that are a non-enterprise groups (31.11%); headquarters of domestic enterprise groups (17.78%) and headquarters of multinational enterprise groups (13.33%).

These figures change while dealing with trade/investment relations with rest of the world. In this category, non-enterprise group respondents ranked highest with 38.82% having indicated to have trade/investment relations with the rest of the world (excluding the MENA region), followed by respondents that are subsidiaries of an enterprise groups (28.35%); respondents that are headquarters of multinational enterprise groups (19.16%); and respondents that are headquarters of a domestic enterprise group (13.67%).

11 Nyenrode Business Universiteit

Questionnaire Analysis 2010

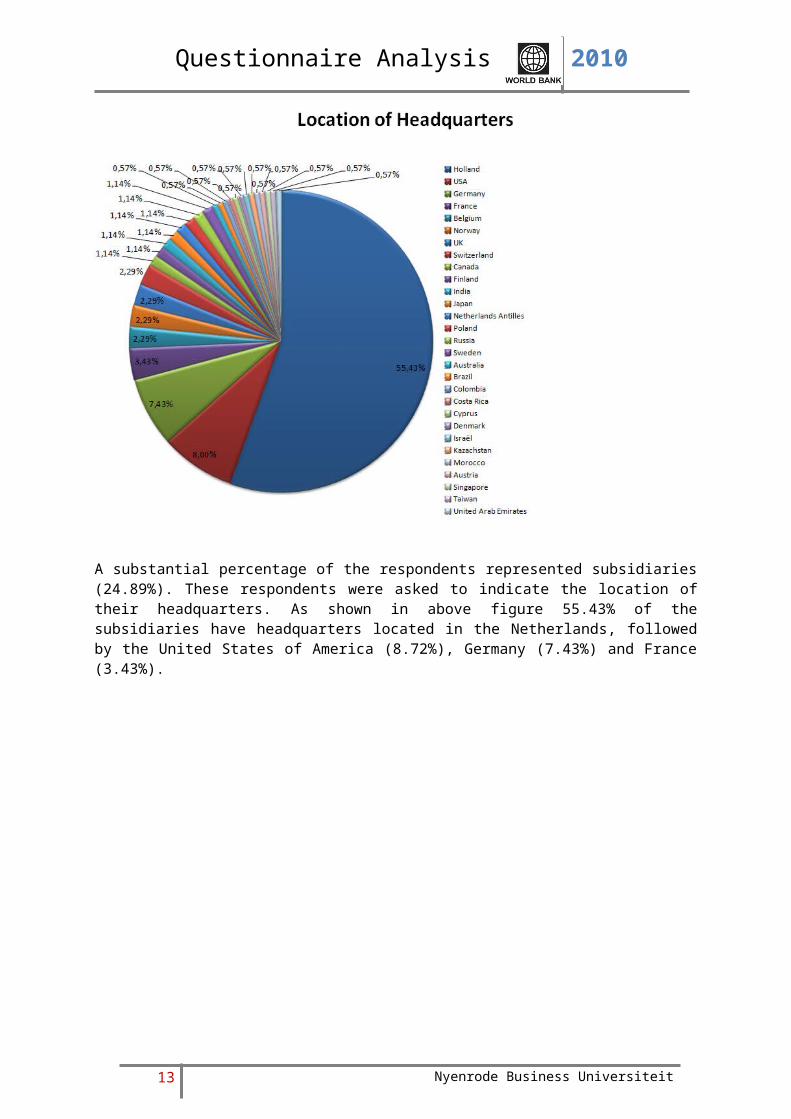

A substantial percentage of the respondents represented subsidiaries (24.89%). These respondents were asked to indicate the location of their headquarters. As shown in above figure 55.43% of the subsidiaries have headquarters located in the Netherlands, followed by the United States of America (8.72%), Germany (7.43%) and France (3.43%).

12 Nyenrode Business Universiteit

Questionnaire Analysis 2010

1%

99%

Comparison of location of headquarters - MENA vs Rest of the world

MENA Rest of the world

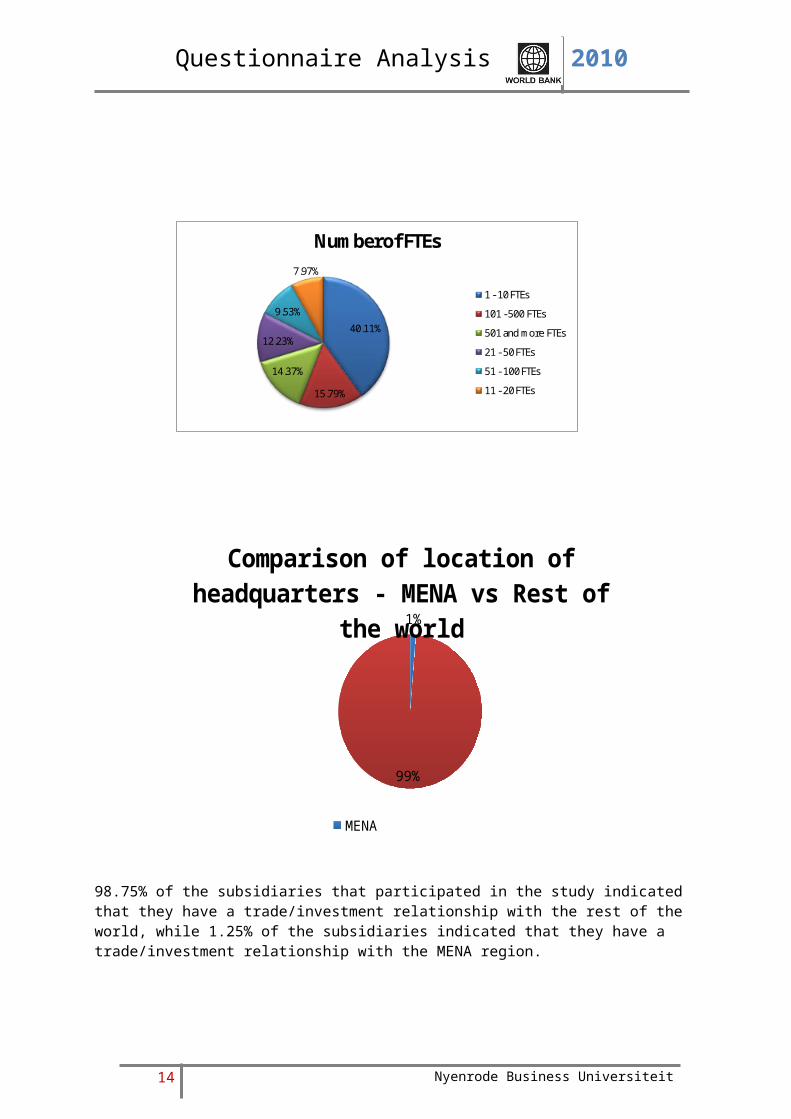

98.75% of the subsidiaries that participated in the study indicated that they have a trade/investment relationship with the rest of the world, while 1.25% of the subsidiaries indicated that they have a trade/investment relationship with the MENA region.

13 Nyenrode Business Universiteit

40.11%

15.79%

14.37%

12.23%

9.53%

7.97%

Number of FTEs

1 - 10 FTEs

101 - 500 FTEs

501 and more FTEs

21 - 50 FTEs

51 - 100 FTEs

11 - 20 FTEs

Questionnaire Analysis 2010

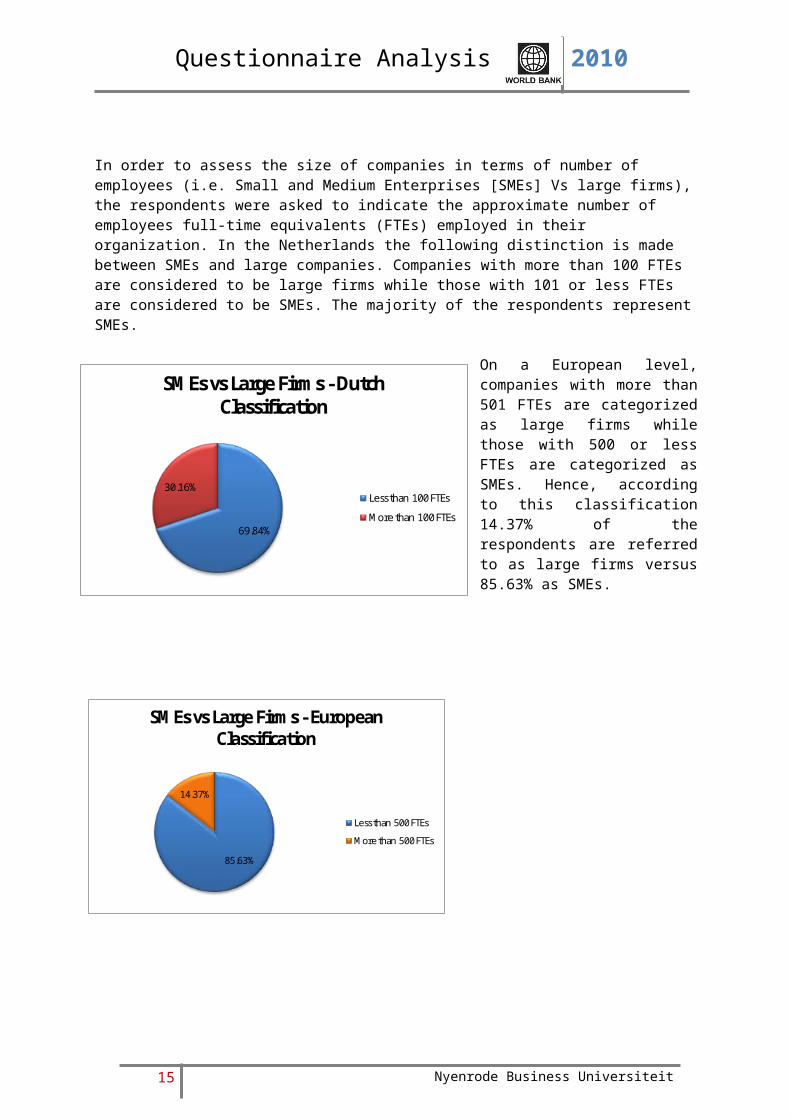

In order to assess the size of companies in terms of number of employees (i.e. Small and Medium Enterprises [SMEs] Vs large firms), the respondents were asked to indicate the approximate number of employees full-time equivalents (FTEs) employed in their organization. In the Netherlands the following distinction is made between SMEs and large companies. Companies with more than 100 FTEs are considered to be large firms while those with 101 or less FTEs are considered to be SMEs. The majority of the respondents represent SMEs.

On a European level, companies with more than 501 FTEs are categorized as large firms while those with 500 or less FTEs are categorized as SMEs. Hence, according to this classification 14.37% of the respondents are referred to as large firms versus 85.63% as SMEs.

14 Nyenrode Business Universiteit

85.63%

14.37%

SMEs vs Large Firms - European Classification

Less than 500 FTEs

More than 500 FTEs

69.84%

30.16%

SMEs vs Large Firms - Dutch Classification

Less than 100 FTEs

More than 100 FTEs

Questionnaire Analysis 2010

1-10

11-20

21-50

51-100

101-500

501 and more

0 5 10 15 20 25 30 35

Comparison of FTEs - MENA vs Rest of the world

Rest of the WorldMENA

Percentage of responses

Num

ber o

f FTE

s

15 Nyenrode Business Universiteit

Questionnaire Analysis 2010

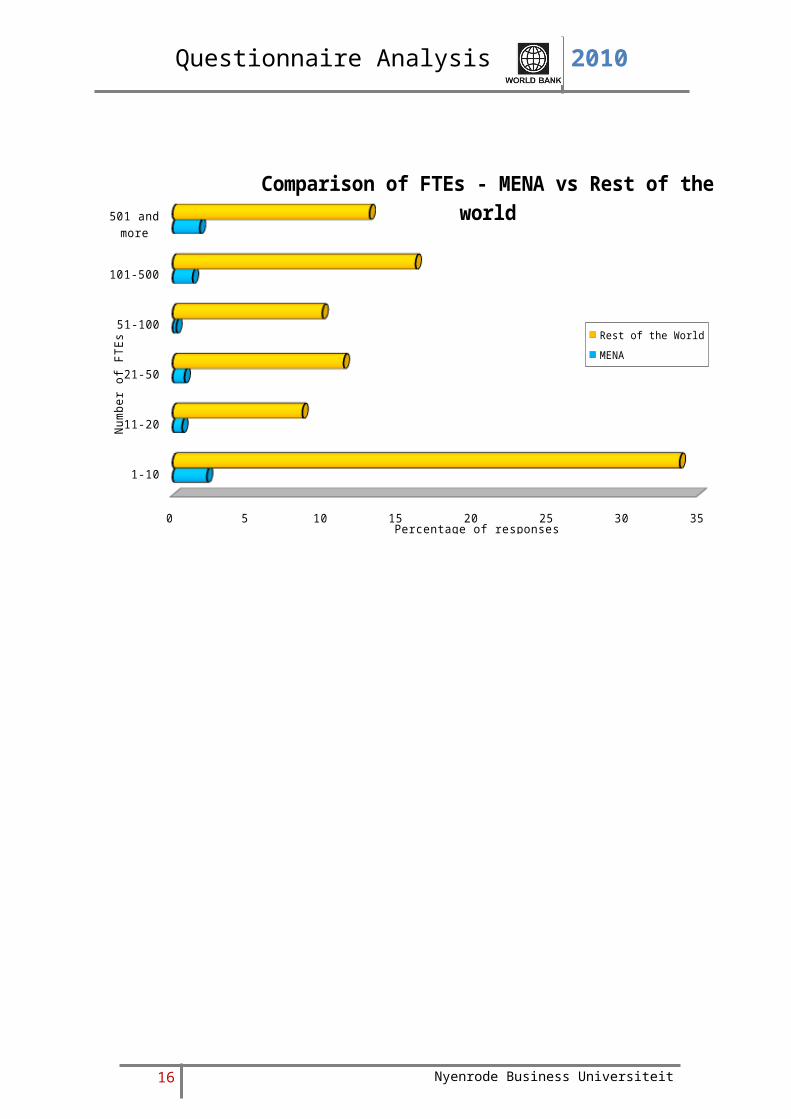

Of those respondents having a trade/investment relationship with the MENA region, 3.92% employ less than 100 FTEs, 1.33% employ between 100 and 500 FTEs and 1.8% employ more than 500 FTEs in the Netherlands.Of those respondents having a trade/investment relationship with countries the rest of the world, 63.69% employ less than 100 FTEs, 16.16% employ between 100 and 500 FTEs, and 13.10% employ more than 500 FTEs in the Netherlands.

1-10

11-20

21-50

51-100

101-500

501 and more

0 20 40 60 80 100

Preferred region for foreign trade/investment per number of FTEs

MENARest of the World

Percentage of responses

Num

ber o

f FTE

s

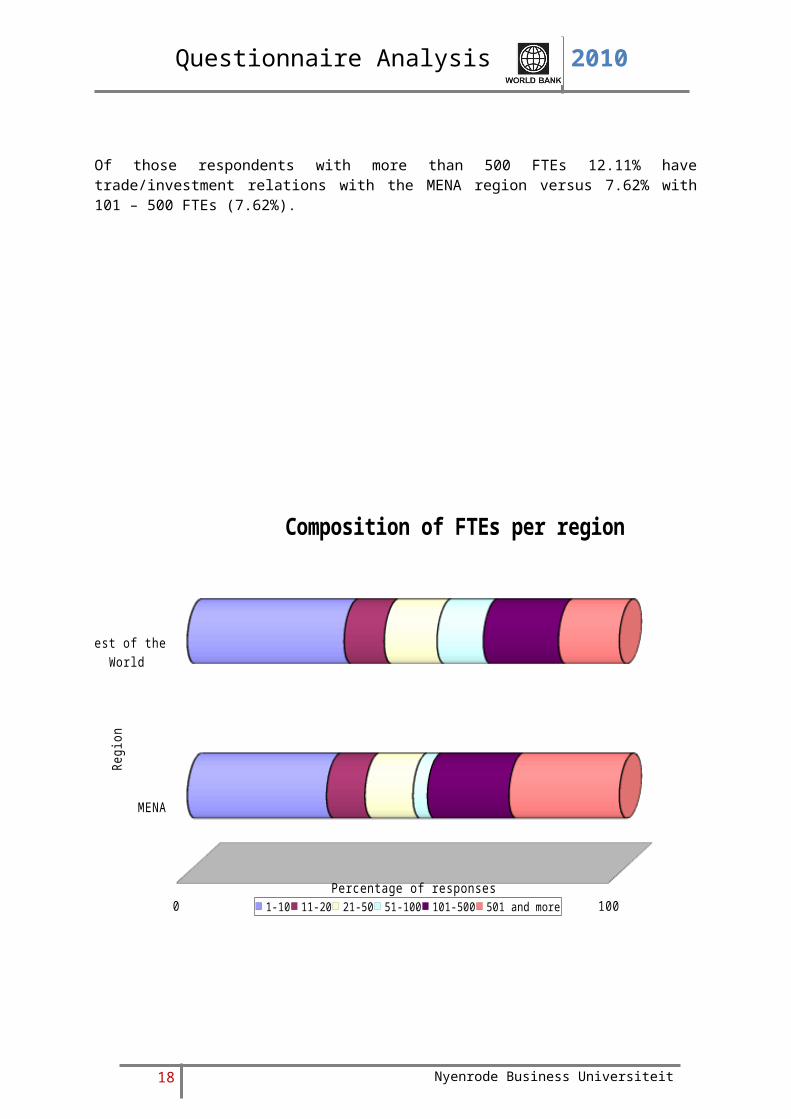

Of those respondents with more than 500 FTEs 12.11% have trade/investment relations with the MENA region versus 7.62% with 101 – 500 FTEs (7.62%).

16 Nyenrode Business Universiteit

Questionnaire Analysis 2010

MENA

Rest of the World

0 20 40 60 80 100

Composition of FTEs per region

1-10 11-20 21-50 51-100 101-500 501 and more

Percentage of responses

Regio

n

Among all the respondents that have trade/investment relations with MENA region, 32.22% have 1 -10 FTEs followed by 25.56% that have more than 500 FTEs and 18.89% that have 100 to 500 FTEs. For respondents with trade/investment relations with the rest of the world, 36.29% of the respondents have 1 – 10 FTEs followed by 17.38% that have 100 – 500 FTEs and 14.09% that have more than 500 FTEs.

17 Nyenrode Business Universiteit

Questionnaire Analysis 2010

The next part of the questionnaire focus is on gender issues. To begin with, we assessed the number of female employees as a percentage of total employees employed by the respondents on the domestic market.

We categorized five proportional brackets classified as following: 0% of total employees are female, 1–24% of total employees are female, 25–49% of total employees are female, 50–74% of total employees are female, and 75–100% of the total employees are female and asked the respondents to choose the option most resembling their organization. In response to this question, 44.95% of the respondents indicated to have 1–24% of female employees within their organization, followed by 19.20% of the respondents having 25–49% of female employees in their organization. 17.07% of the respondents claim to have no female employees in their organization at all as indicated in above figure.

18 Nyenrode Business Universiteit

17.07%

44.95%19.20%

9.96%

8.82%

Percentage of female employees employed on the domestic market

0 %

1 – 24%

25 – 49%

50 – 74%

75 – 100%

Questionnaire Analysis 2010

0 %

1 – 24%

25 – 49%

50 – 74%

75 – 100%

0 5 10 15 20 25 30 35 40 45 50

Comparison of medium to highly educated female employees - MENA vs Rest of the world

Rest of the worldMENA

Percentage of responses

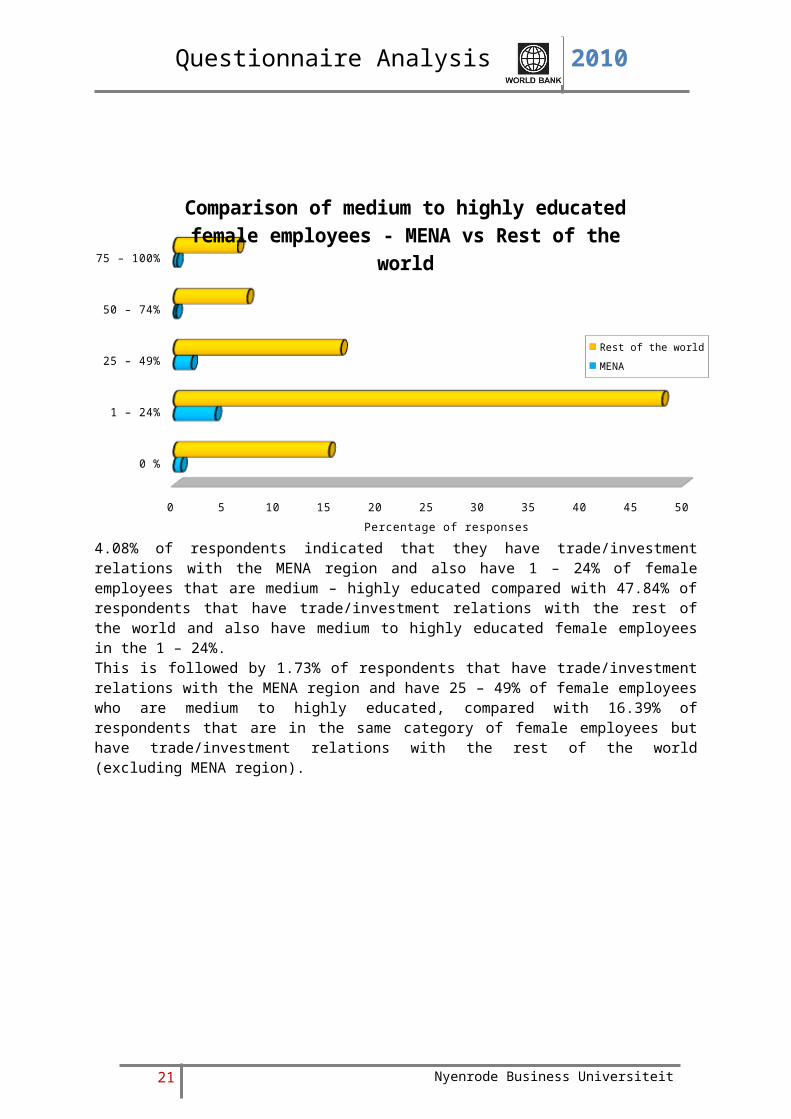

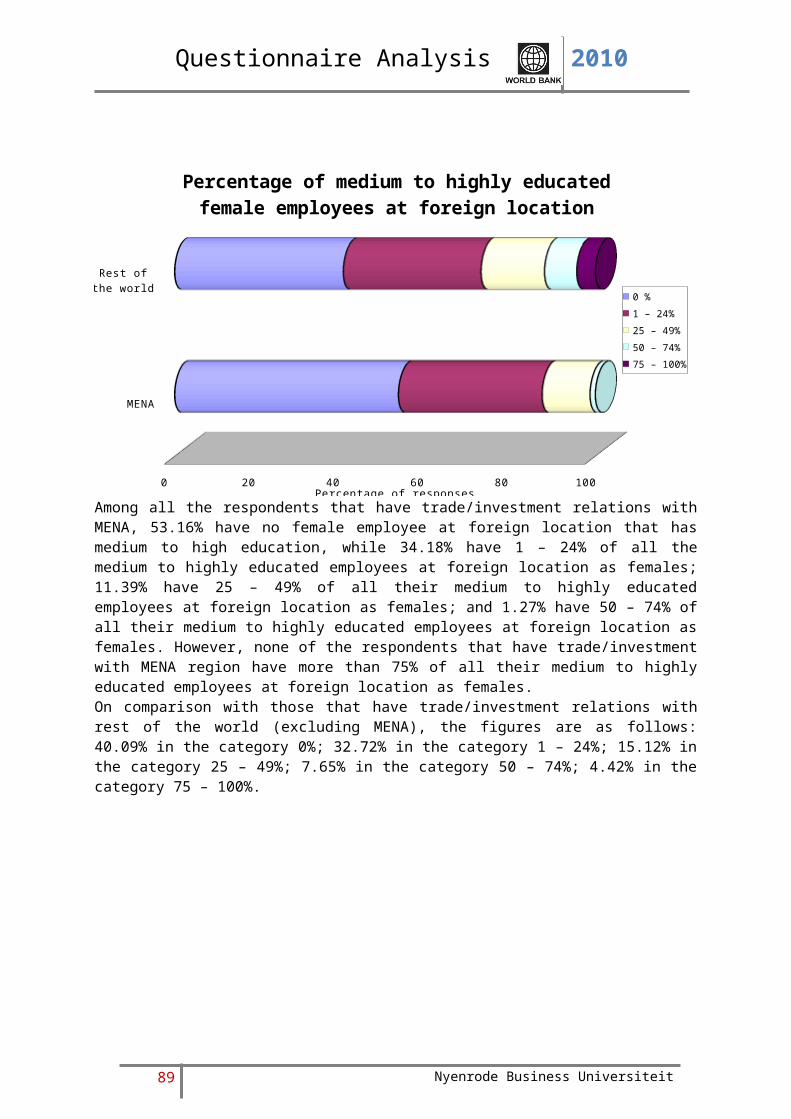

4.08% of respondents indicated that they have trade/investment relations with the MENA region and also have 1 – 24% of female employees that are medium – highly educated compared with 47.84% of respondents that have trade/investment relations with the rest of the world and also have medium to highly educated female employees in the 1 – 24%.This is followed by 1.73% of respondents that have trade/investment relations with the MENA region and have 25 – 49% of female employees who are medium to highly educated, compared with 16.39% of respondents that are in the same category of female employees but have trade/investment relations with the rest of the world (excluding MENA region).

19 Nyenrode Business Universiteit

Questionnaire Analysis 2010

0 %

1 – 24%

25 – 49%

50 – 74%

75 – 100%

0 20 40 60 80 100

Preferred region for foreign trade/investment per category female employees

MENA Rest of the world

Percentage of responses

9.52% of respondents that belong to 25 – 49% bracket have trade/investment relations with the MENA region followed by 7.85% of those in the 1 – 24% bracket and 4.76% in the 75 – 100% bracket.

20 Nyenrode Business Universiteit

Questionnaire Analysis 2010

MENA

Rest of the world

0 20 40 60 80 100

Composition of medium to highly educated employees in organizations per region

0 %

1 – 24%

25 – 49%

50 – 74%

75 – 100%

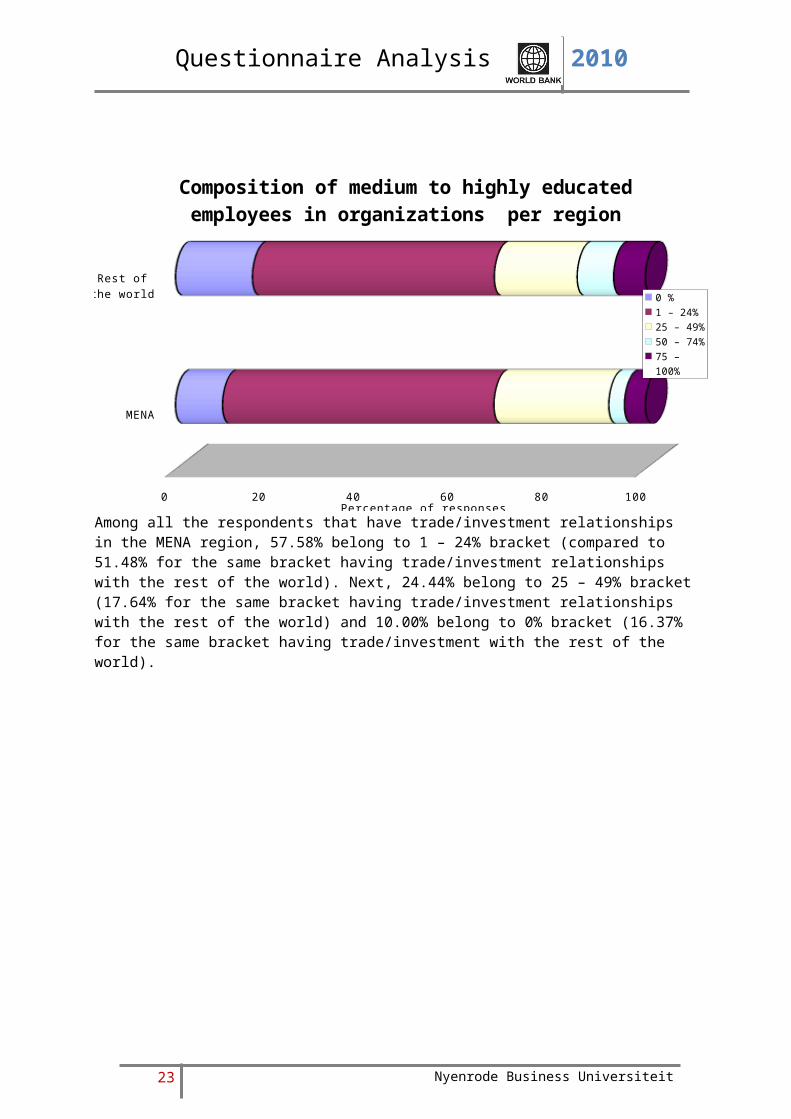

Percentage of responsesAmong all the respondents that have trade/investment relationships in the MENA region, 57.58% belong to 1 – 24% bracket (compared to 51.48% for the same bracket having trade/investment relationships with the rest of the world). Next, 24.44% belong to 25 – 49% bracket (17.64% for the same bracket having trade/investment relationships with the rest of the world) and 10.00% belong to 0% bracket (16.37% for the same bracket having trade/investment with the rest of the world).

21 Nyenrode Business Universiteit

Questionnaire Analysis 2010

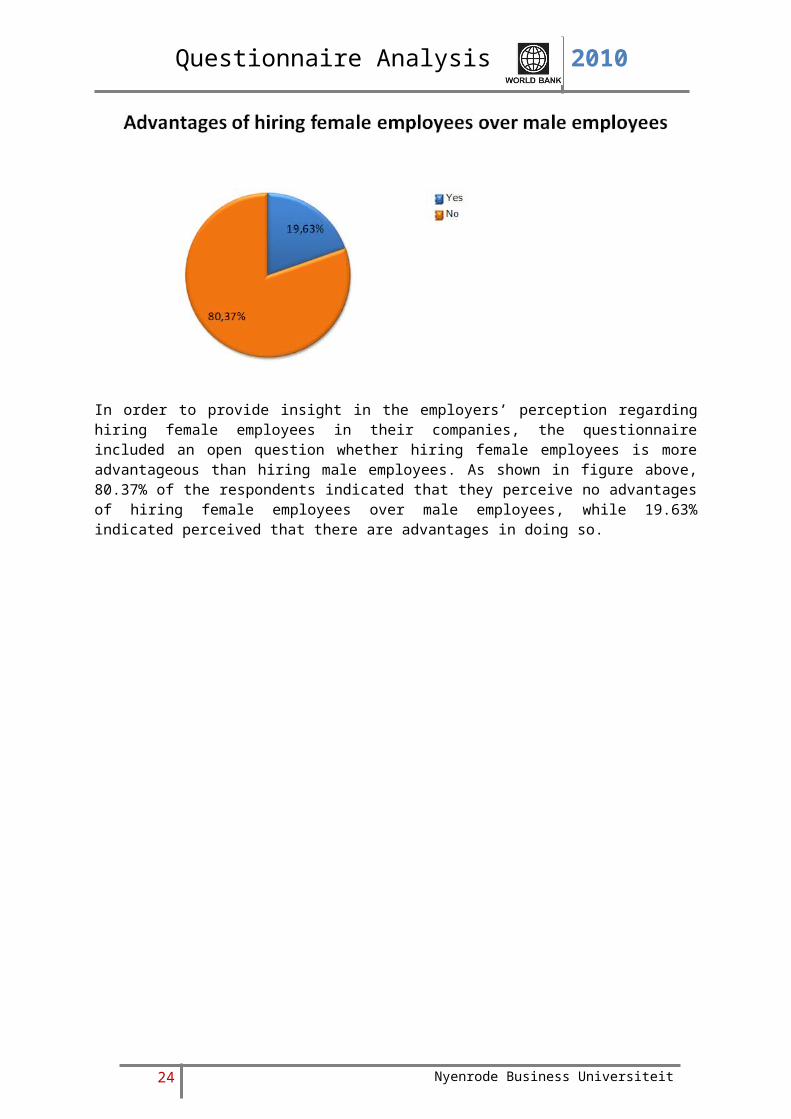

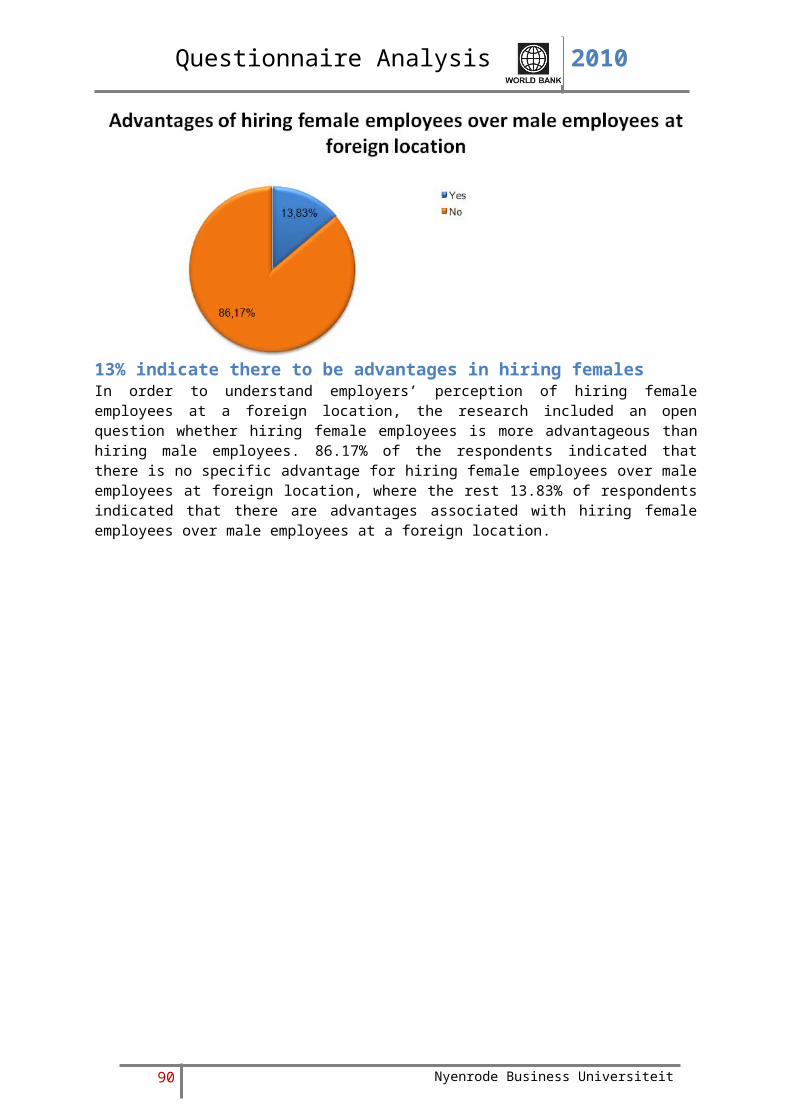

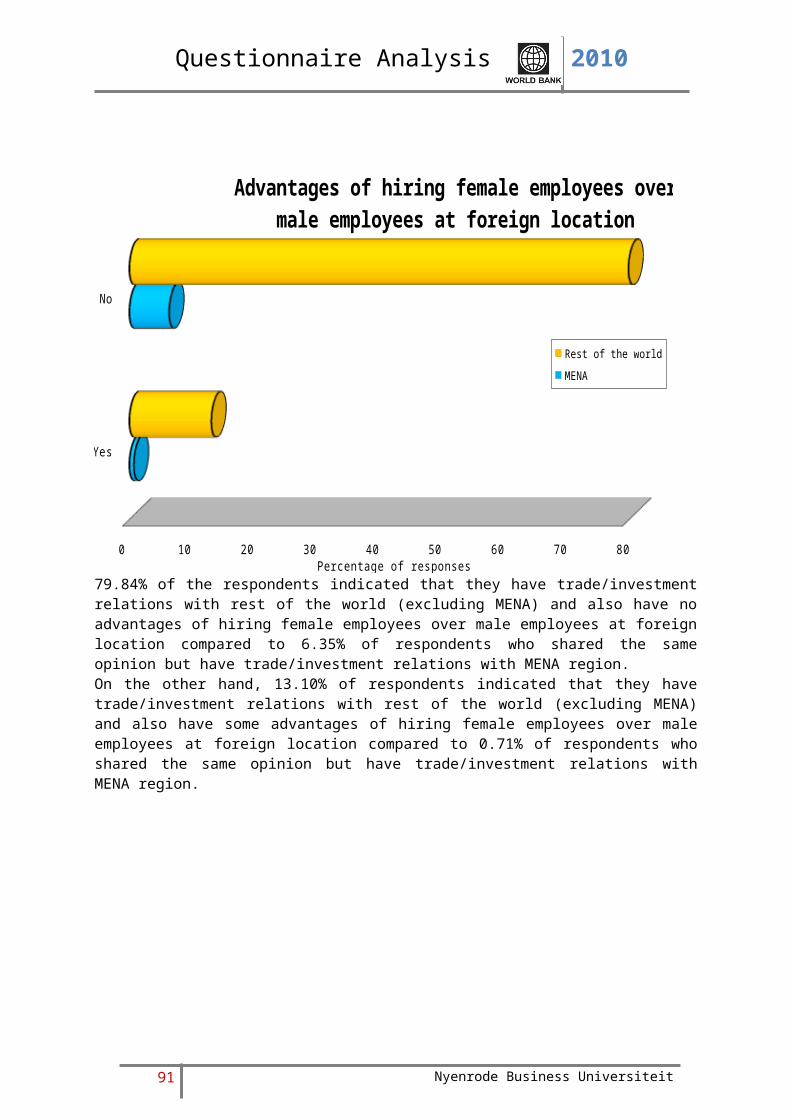

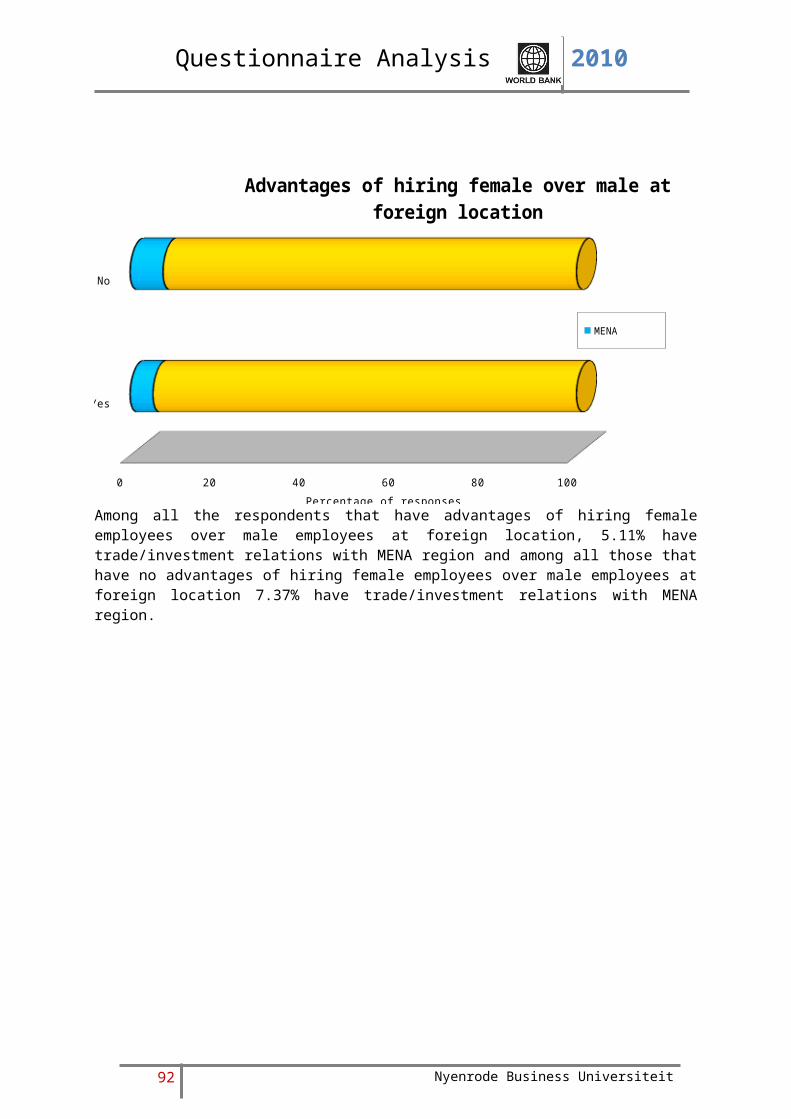

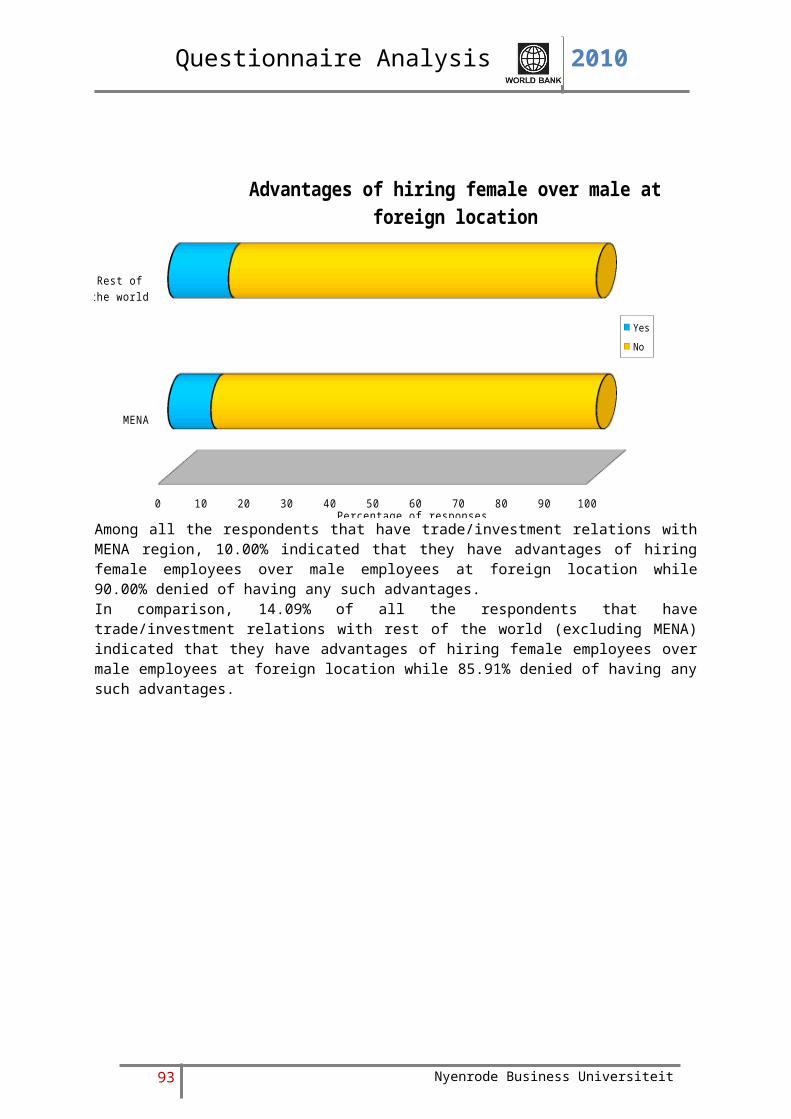

In order to provide insight in the employers’ perception regarding hiring female employees in their companies, the questionnaire included an open question whether hiring female employees is more advantageous than hiring male employees. As shown in figure above, 80.37% of the respondents indicated that they perceive no advantages of hiring female employees over male employees, while 19.63% indicated perceived that there are advantages in doing so.

22 Nyenrode Business Universiteit

Questionnaire Analysis 2010

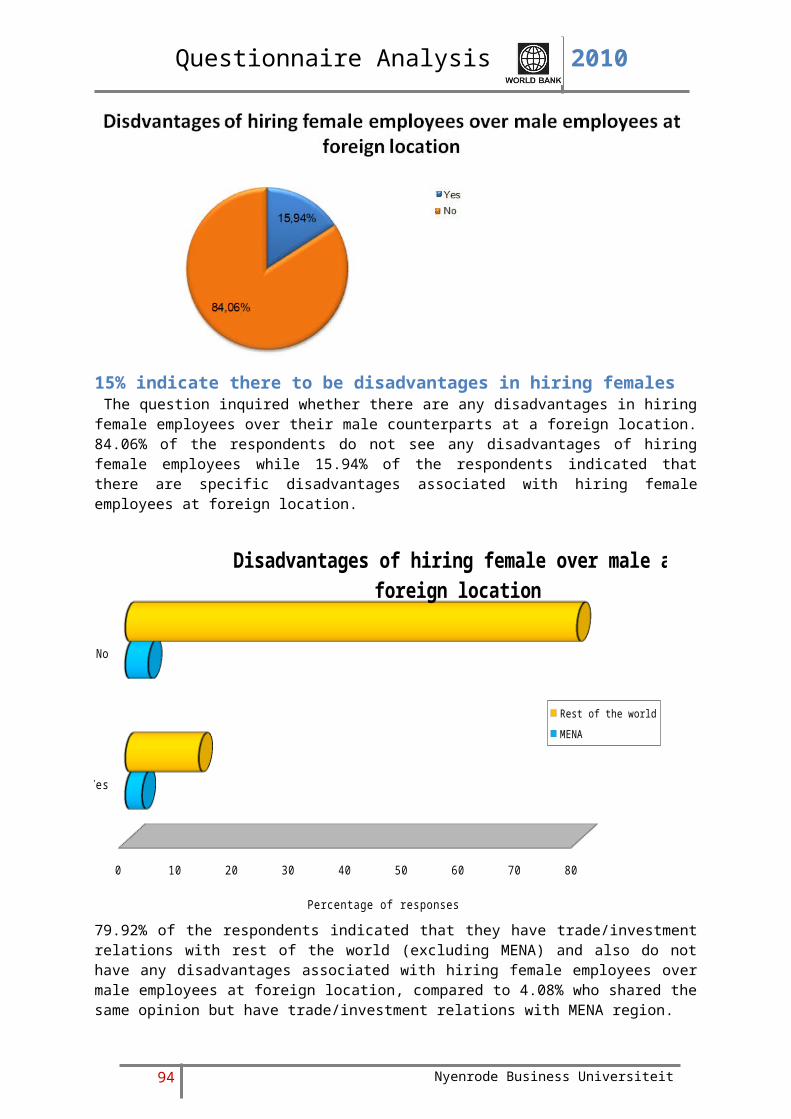

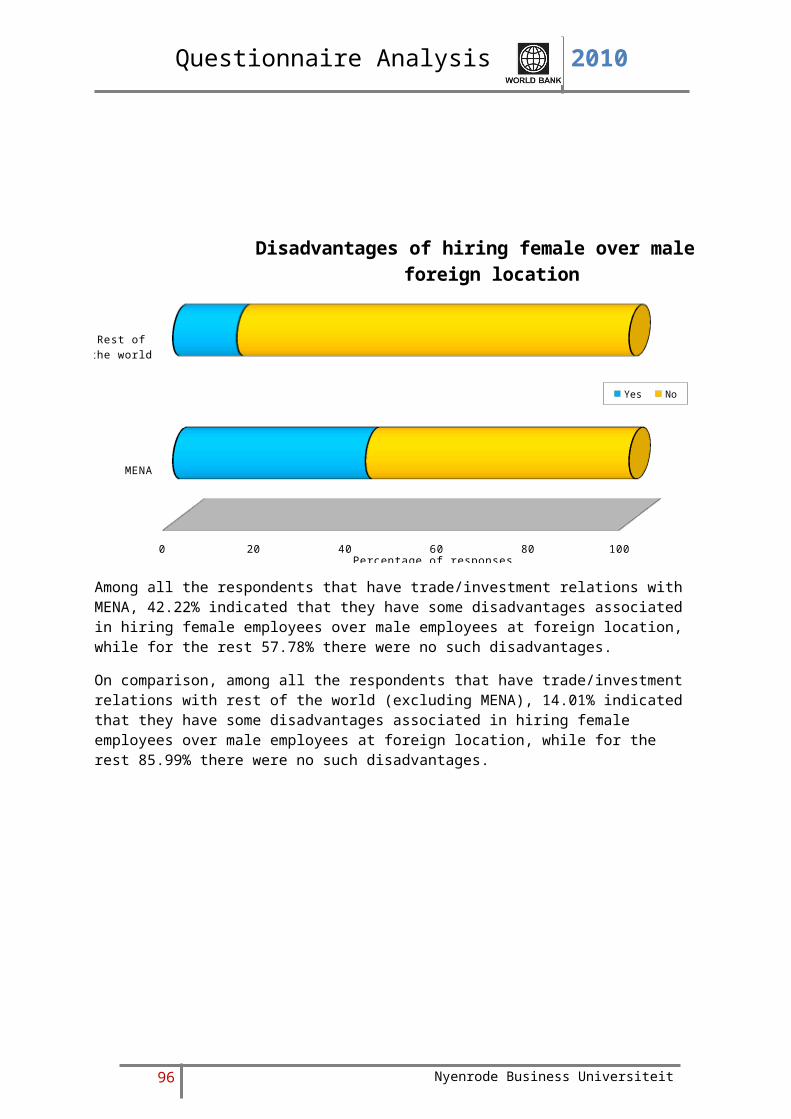

The next question inquired whether employers perceive disadvantages for hiring female employees over their male counterparts. As shown in figure above, 80.94% of the respondents indicated that they do not perceive any disadvantages of hiring female employees, while 19.06% of the respondents indicated that they do perceive disadvantages associated with hiring female employees over male employees.

23 Nyenrode Business Universiteit

Questionnaire Analysis 2010

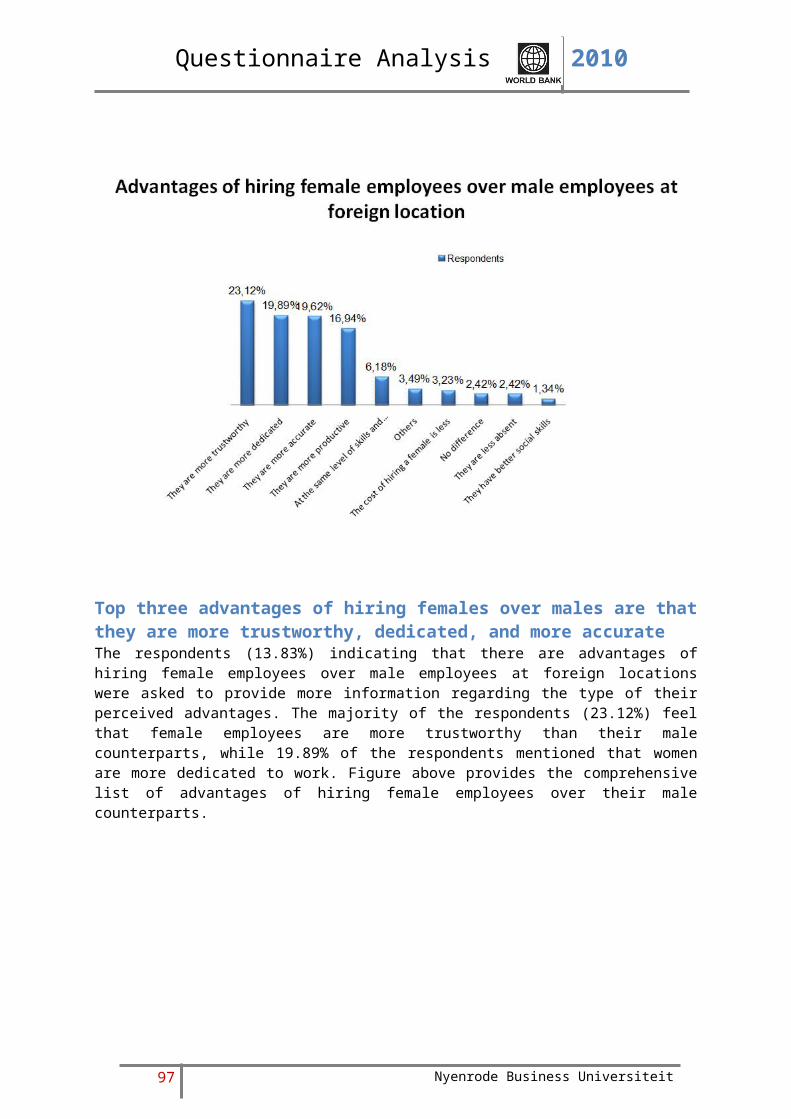

19.63% of the respondents, who indicated that there are advantages of hiring female employees, were asked to choose from one of the seven advantages of hiring women. If none of these options

were suitable for them, they could key-in their response by selecting an option “Other advantages” option and describe them. Based on these answers, the following new categories of advantages were created: They are better able to multitask; they have better social skills; they create better balance/gender diversity. A separate new category was created: No difference. After a final analysis of all answer options, it is found that 25.74% mentioned that women are more accurate than men followed by 20.68% who indicated that women are more dedicated than men. Above figure indicates the top ten advantages associated with hiring female employees.

24 Nyenrode Business Universiteit

Questionnaire Analysis 2010

They are more productive

They are more trustworthy

They are less absent

They are more accurate

They are more dedicated

At the same level of skills and education,

females have a higher level of training

The cost of hiring a female is less

They are better able to multi-task

They have better social skills

They create betterbalance/gender diversity

Meaningless

No difference

Others

0 5 10 15 20 25

Comparison of advantages of hiring female em-ployees over male employees in the Netherlands -

MENA vs Rest of the world

Foreign trade / investment relations with rest of the world Foreign trade / investment relations with MENA

Percentage of responsesAdva

ntag

es o

f hiri

ng fe

mal

e em

ploy

ees

in th

e N

ethe

r-

land

s

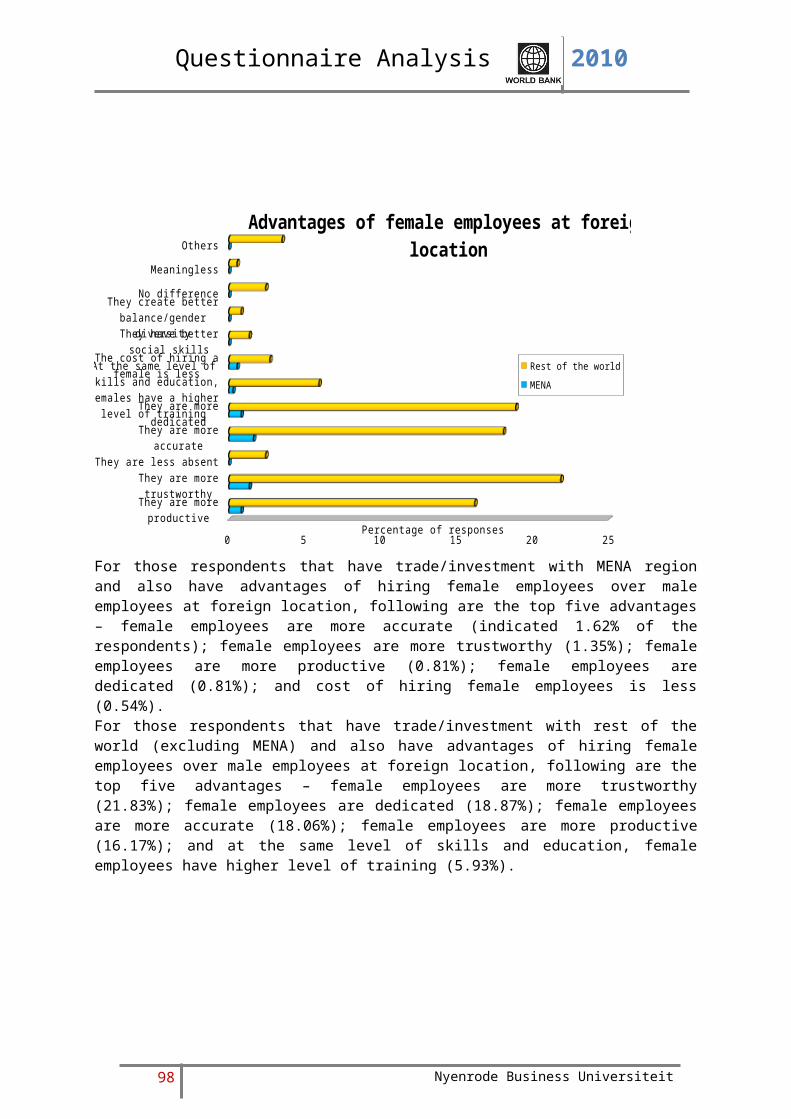

Female employees are more accurate (indicated by 23.59% of respondents), female employees are more dedicated (17.16%), female employees are more trustworthy (11.53%), at the same level of skills and education female employees have higher level of training (9.12%), and female employees are more productive (8.85%) are the top five advantages of hiring female employees over male employees in the Netherlands as reported by respondents that have trade/investment relations with rest of the world (excluding MENA).For those respondents that have trade/investment relations with MENA the top five advantages are as follows: female employees are more accurate (2.41%), female employees are more productive (1.34%), female employees are more dedicated (1.61%), female employees are more trust worthy (1.07%), and at the same level of skills and education female employees have higher level of training (1.07%).

25 Nyenrode Business Universiteit

Questionnaire Analysis 2010

They are more productive

They are more trustworthy

They are less absent

They are more accurate

They are more dedicated

At the same level of skills and education,

females have a higher level of training

The cost of hiring a female is less

They are better able to multi-task

They have better social skills

They create betterbalance/gender diversity

Meaningless

No difference

Others

0 20 40 60 80 100

Foreign trade/investment relations per type of advantage of hiring female employees in the

Netherlands

Foreign trade / investment relations with MENA Foreign trade / investment relations with rest of the world

Percentage of responses

Adva

ntag

es o

f hiri

ng fe

mal

e em

ploy

ees

in th

e N

ethe

r-

land

s

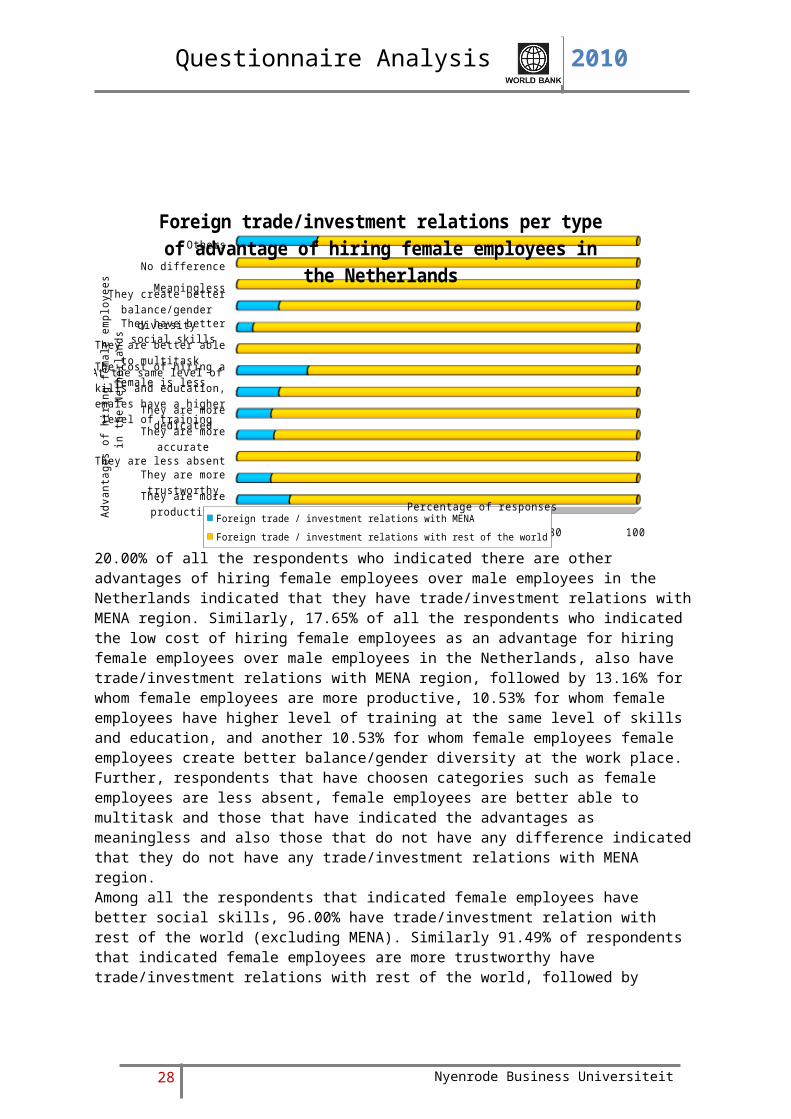

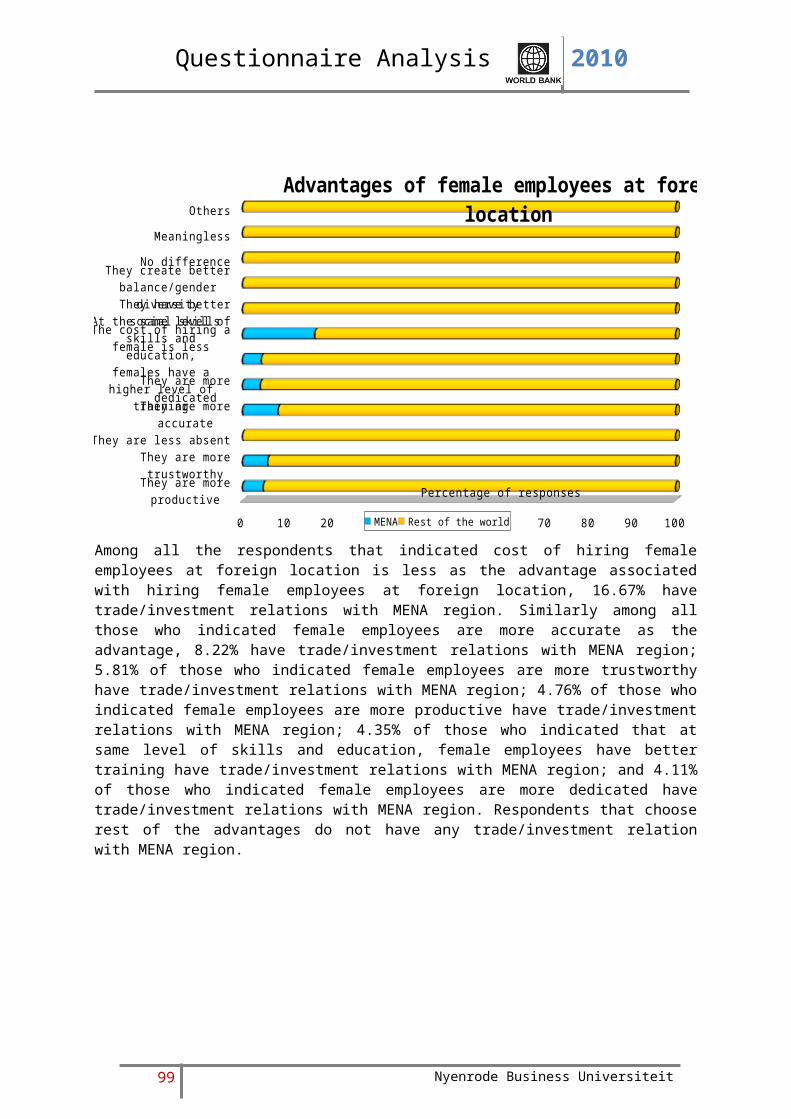

20.00% of all the respondents who indicated there are other advantages of hiring female employees over male employees in the Netherlands indicated that they have trade/investment relations with MENA region. Similarly, 17.65% of all the respondents who indicated the low cost of hiring female employees as an advantage for hiring female employees over male employees in the Netherlands, also have trade/investment relations with MENA region, followed by 13.16% for whom female employees are more productive, 10.53% for whom female employees have higher level of training at the same level of skills and education, and another 10.53% for whom female employees female employees create better balance/gender diversity at the work place. Further, respondents that have choosen categories such as female employees are less absent, female employees are better able to multitask and those that have indicated the advantages as meaningless and also those that do not have any difference indicated that they do not have any trade/investment relations with MENA region.Among all the respondents that indicated female employees have better social skills, 96.00% have trade/investment relation with rest of the world (excluding MENA). Similarly 91.49% of respondents that indicated female employees are more trustworthy have trade/investment relations with rest of the world, followed by 91.43% for whom female employees are more dedicated, and 90.72% for whom female employees are more accurate.

26 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Foreign trade / investment rela-

tions with MENA

Foreign trade / investment rela-tions with rest of the world

0 20 40 60 80 100

Advantages of hiring female employees overmale employees in the Netherlands

They are more productive They are more trustworthy They are less absent

They are more accurate They are more dedicated At the same level of skills and education, females have a higher level of training

The cost of hiring a female is less They are better able to multitask They have better social skills

They create betterbalance/gender diversity

Meaningless No difference

Others

Percentage of responses

Among all the respondents that have trade/investment relations with MENA, 25.00% indicated female employees are more accurate, 16.67% indicated female employees are more dedicated, 13.89% indicated female employees are more productive, 11.11% indicated female employees are more trustworthy, and another 11.11% indicated that at the same level of skills and education, female employees have higher level of training.Among all the respondents that have trade/investment relations with rest of the world (excluding MENA), 26.11% indicated female employees are more accurate, 18.99% indicated female employees are more dedicated, 12.76% indicated female employees are more trustworthy, and another 10.09% indicated that at the same level of skills and education, female employees have higher level of training, and 9.79% indicated female employees are more productive.The pattern of advantages of hiring female employees in the Netherlands chosen by those that have trade/investment with MENA and the rest of the world broadly matches with each other.

27 Nyenrode Business Universiteit

Questionnaire Analysis 2010

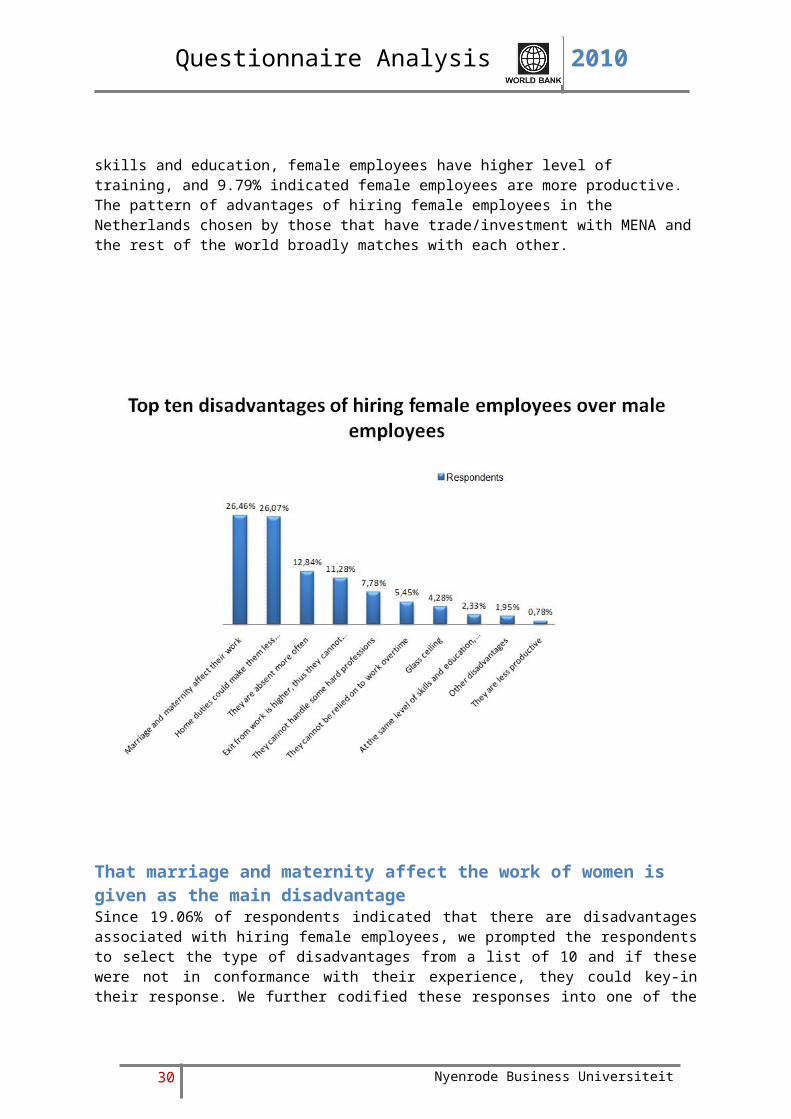

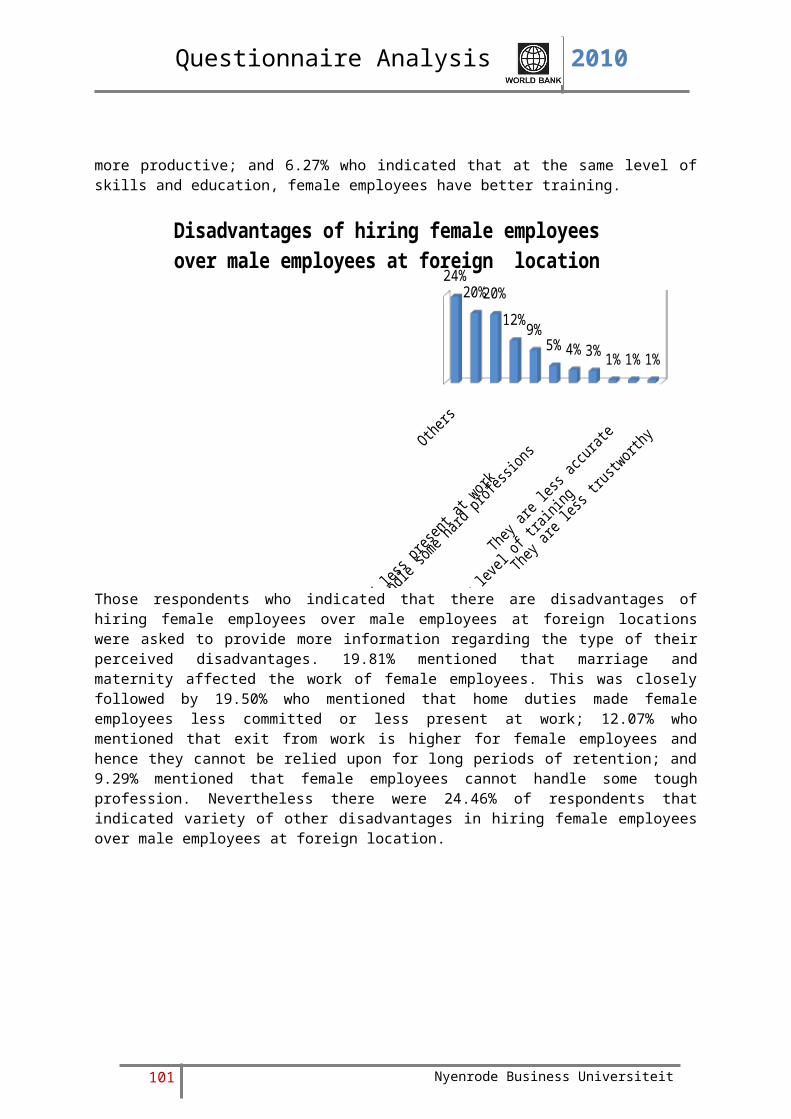

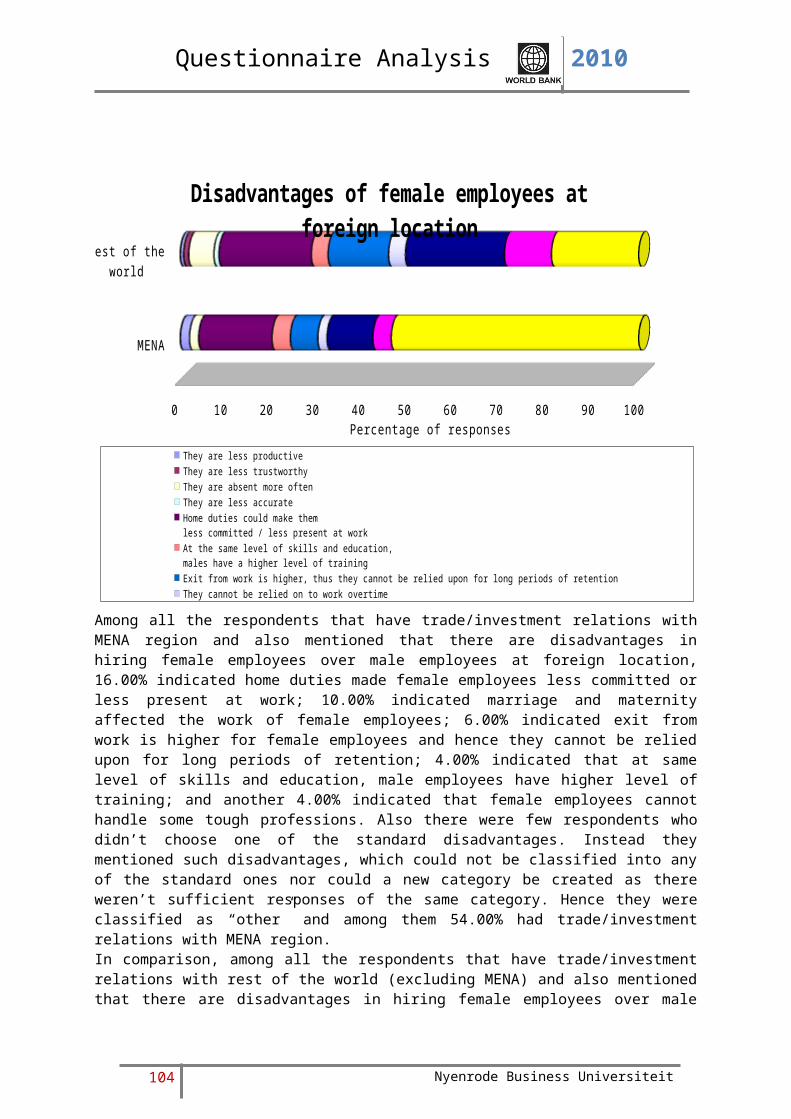

That marriage and maternity affect the work of women is given as the main disadvantageSince 19.06% of respondents indicated that there are disadvantages associated with hiring female employees, we prompted the respondents to select the type of disadvantages from a list of 10 and if these were not in conformance with their experience, they could key-in their response. We further codified these responses into one of the listed categories. There were few responses that did not seem to fit the standard classification. Hence the new category “Glass ceiling” was created to accommodate these responses.As indicated in the figure above, respondent’s assigned marriage and maternity as the top disadvantage associated with women followed by their commitments towards their personal obligations. Above figure provides a detailed listing of top 10 disadvantages associated with women.

28 Nyenrode Business Universiteit

Questionnaire Analysis 2010

They are less productive

They are absent more often

They are less accurate

Home duties couldmake them less committed /

less present at work

At the same level ofskills and education, males

have a higher level of training

Exit from work is higher,thus they cannot be relied

upon for long periods of reten-tion

They cannot be relied on to work overtime

Marriage and maternity affect their work

They cannot handle some hard professions

Glass ceiling

No disadvantages

Others

0 5 10 15 20 25 30

Disadvantages of females employees over male employees in the Netherlands

Foreign trade/investment relationship with rest of the world Foreign trade/investment relationship with MENA

Percentage of responses

Dis

adva

ntag

es

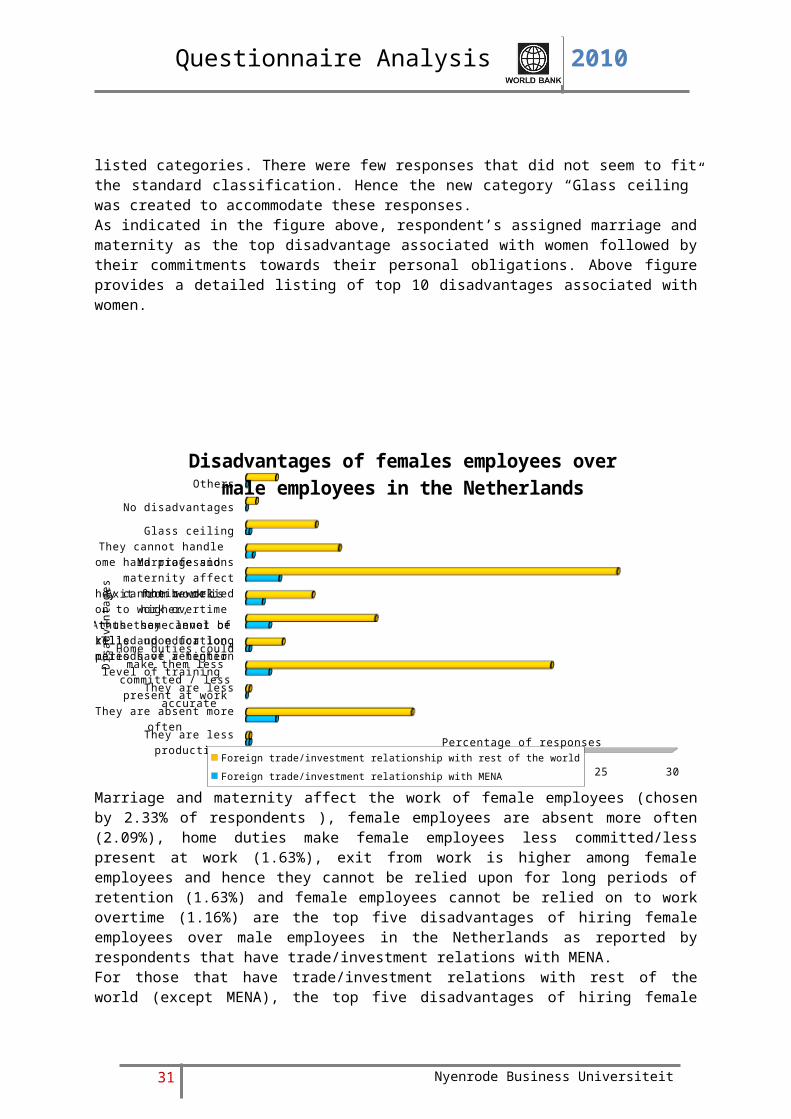

Marriage and maternity affect the work of female employees (chosen by 2.33% of respondents ), female employees are absent more often (2.09%), home duties make female employees less committed/less present at work (1.63%), exit from work is higher among female employees and hence they cannot be relied upon for long periods of retention (1.63%) and female employees cannot be relied on to work overtime (1.16%) are the top five disadvantages of hiring female employees over male employees in the Netherlands as reported by respondents that have trade/investment relations with MENA.For those that have trade/investment relations with rest of the world (except MENA), the top five disadvantages of hiring female employees over male employees are: Marriage and maternity affect the work of female employees (26.05%), home duties make female employees less committed/less present at work (21.40%), female employees are absent more often (11.63%), exit from work is higher among female employees and hence they cannot be relied upon for long periods of retention (9.07%), and female employees cannot handle some hard professions (6.51%).

29 Nyenrode Business Universiteit

Questionnaire Analysis 2010

They are less productive

They are absent more often

They are less accurate

Home duties couldmake them less committed /

less present at work

At the same level ofskills and education, males

have a higher level of training

Exit from work is higher,thus they cannot be relied

upon for long periods of re-tention

They cannot be relied on to work overtime

Marriage and maternity affect their work

They cannot handle some hard professions

Glass ceiling

No disadvantages

Others

0 20 40 60 80 100

Disadvantages of female employees over males employees in the Netherlands

Foreign trade/investment relationship with MENA Foreign trade/investment relationship with rest of the world

Percentage of responses

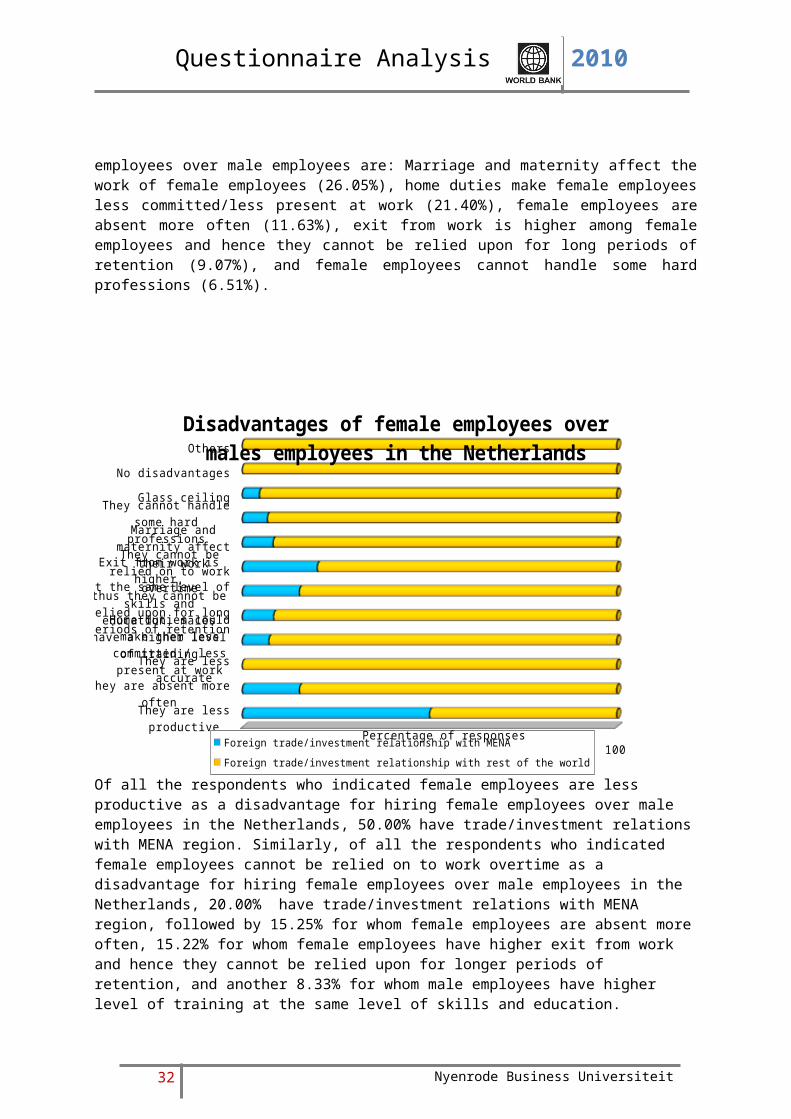

Of all the respondents who indicated female employees are less productive as a disadvantage for hiring female employees over male employees in the Netherlands, 50.00% have trade/investment relations with MENA region. Similarly, of all the respondents who indicated female employees cannot be relied on to work overtime as a disadvantage for hiring female employees over male employees in the Netherlands, 20.00% have trade/investment relations with MENA region, followed by 15.25% for whom female employees are absent more often, 15.22% for whom female employees have higher exit from work and hence they cannot be relied upon for longer periods of retention, and another 8.33% for whom male employees have higher level of training at the same level of skills and education. Further, respondents that have choosen categories such as female employees are less accurate, female employees have no disadvantages and other reasons indicated that they do not have any trade/investment relations with MENA region.Among all the respondents that indicated female employees have glass ceiling, 95.45% have trade/investment relation with rest of the world (excluding MENA). Similarly 93.33% of respondents that indicated female employees cannot handle some hard professions have trade/investment relations with rest of the world, followed by 92.93% for whom home duties could make female employees less committed/less present at work, and 91.80% for whom marriage and maternity could affect the work of female employees.

30 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Among all the respondents that have trade/investment relations with MENA, 23.26% indicated marriage and maternity affects the work of female employees, 20.93%% indicated female employees are absent more often, 16.28% indicated home duties made female employees less committed/less present at work, 16.28% indicated female employees have higher exit from work and hence they cannot be relied upon for long periods of retention, and another 11.63% indicated that at female employees cannot be relied on to work overtime.Among all the respondents that have trade/investment relations with rest of the world (excluding MENA), 28.94% indicated marriage and maternity affects the work of female employees, 23.77% indicated home duties made female employees less committed/less present at work, 12.92% indicated female employees are absent more often, 10.08% indicated female employees have higher exit from work and hence they cannot be relied upon for long periods of retention, and 7.24% indicated female employees cannot handle some hard profession.The pattern of disadvantages of hiring female employees in the Netherlands chosen by those that have trade/investment with MENA and the rest of the world broadly matches with each other.

31 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Largest portion of almost 55% are male owned, private companies This question aims to shed some light on the ownership of respondents’ organization based on gender. Above figure shows 54.62% of the organizations who participated in the research to be private companies owned by men versus 7.40% that are private companies owned by women; 23.19% are publicly traded companies with male CEOs versus 3.84% that are publicly traded companies with female CEOs. Thus, majority of the organizations that participated in the research are owned or operated by men. Therefore, we can infer that the majority of opinions about women employees are by employers who are men. Another 10.95% of the organizations are private companies that are equally owned by men and women.

32 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Private company, male owned

Private company, female owned

Private company, joint owned by male and female

(50/50)

Publicly traded company, male CEO

Publicly traded company, female CEO

0 10 20 30 40 50 60

Foreign trade/investment relations based on type and ownership of organizations

Foreign trade/investment in rest of the world

Foreign trade/investment in MENA

Percentage of responses

Tyoe

and

own

ersh

ip o

f org

aniz

ation

s

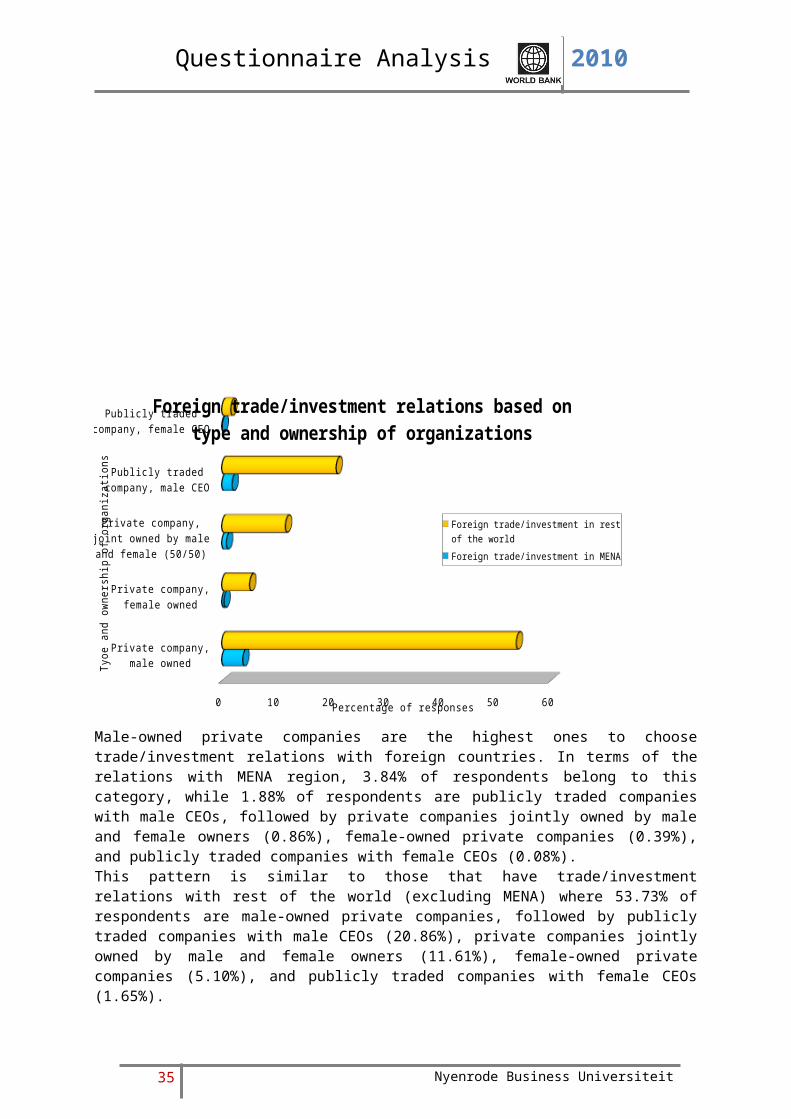

Male-owned private companies are the highest ones to choose trade/investment relations with foreign countries. In terms of the relations with MENA region, 3.84% of respondents belong to this category, while 1.88% of respondents are publicly traded companies with male CEOs, followed by private companies jointly owned by male and female owners (0.86%), female-owned private companies (0.39%), and publicly traded companies with female CEOs (0.08%).This pattern is similar to those that have trade/investment relations with rest of the world (excluding MENA) where 53.73% of respondents are male-owned private companies, followed by publicly traded companies with male CEOs (20.86%), private companies jointly owned by male and female owners (11.61%), female-owned private companies (5.10%), and publicly traded companies with female CEOs (1.65%).

33 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Private company, male owned

Private company, female owned

Private company, joint owned by male and female (50/50)

Publicly traded company, male CEO

Publicly traded company, female CEO

0 20 40 60 80 100 120

Foreign trade/investment relations based on type and ownership of organizations

Foreign trade/investment in MENA Foreign trade/investment in rest of the world

Percentage of responses

Type

and

ow

ners

hip

of o

rgan

izat

ions

Among all the male-owned private companies, 6.68% have trade/investment relations with MENA region against 93.32% that have trade/investment with rest of the world (excluding MENA). Similarly, the figures are 7.14% against 92.86% for female-owned private companies; 6.92% against 93.08% for private companies jointly owned by male and female executives, 8.28% against 91.72% for publicly traded companies with male CEOs, and 4.55% against 95.55% for publicly traded companies with female CEOs. Clearly, publicly traded companies with male CEOs are leading traders/investors in MENA region followed by female owned private companies, private companies jointly owned by male and female executives, male-owned private companies and lastly publicly traded companies with female CEOs.

34 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Foreign trade/invest-

ment in MENA

Foreign trade/invest-ment in rest of the world

0 20 40 60 80 100

Foreign trade/investment relations based on type and ownership of organizations

Private company, male owned Private company, female ownedPrivate company, joint owned by male and female (50/50) Publicly traded company, male CEOPublicly traded company, female CEO

Percentage of responses

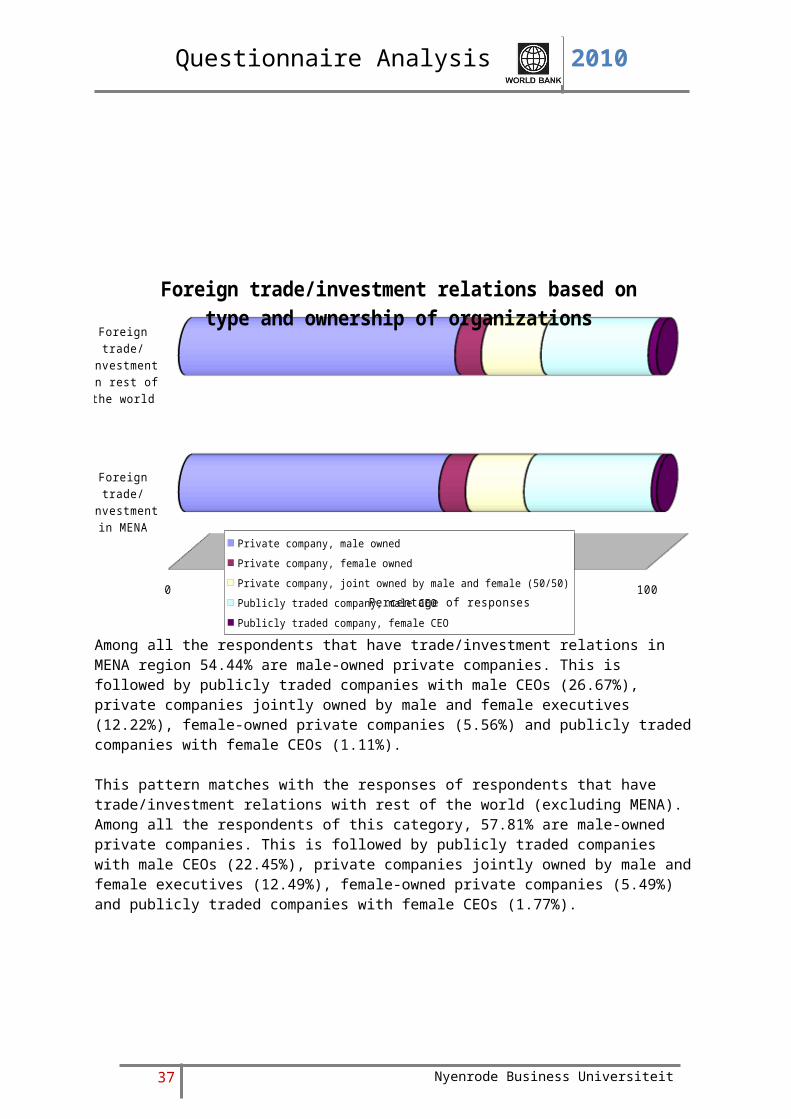

Among all the respondents that have trade/investment relations in MENA region 54.44% are male-owned private companies. This is followed by publicly traded companies with male CEOs (26.67%), private companies jointly owned by male and female executives (12.22%), female-owned private companies (5.56%) and publicly traded companies with female CEOs (1.11%).

This pattern matches with the responses of respondents that have trade/investment relations with rest of the world (excluding MENA). Among all the respondents of this category, 57.81% are male-owned private companies. This is followed by publicly traded companies with male CEOs (22.45%), private companies jointly owned by male and female executives (12.49%), female-owned private companies (5.49%) and publicly traded companies with female CEOs (1.77%).

35 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Almost half of the respondents have no female members in their management team or board of directors at all.Furthermore, figure above shows that 49.08% of the organizations that participated in the research do not have any female employees in their management team and/or board of directors while 50.92% have female employees in their management team and board of directors. Among those who have female employees in their management team and board of directors, 1–24% of the management team and/or board of directors are female in 29.30% of the organizations; 25–49% in 9.53% of the organizations; 50–74% in 6.40% of the organizations; and 75–100% of the management team and board of directors are female in 5.69% of the organizations.

36 Nyenrode Business Universiteit

Questionnaire Analysis 2010

0 %

1 – 24%

25 – 49%

50 – 74%

75 – 100%

0 5 10 15 20 25 30 35 40 45 50

Foreign trade/investment relations based on share of females in management and board of directors

Foreign trade/investment relations with rest of the world

Foreign trade/investment relations with MENA

Percentage of responses

Shar

e pf

fem

ales

in th

e m

anag

emen

t and

boa

rd o

f di

-re

ctor

s

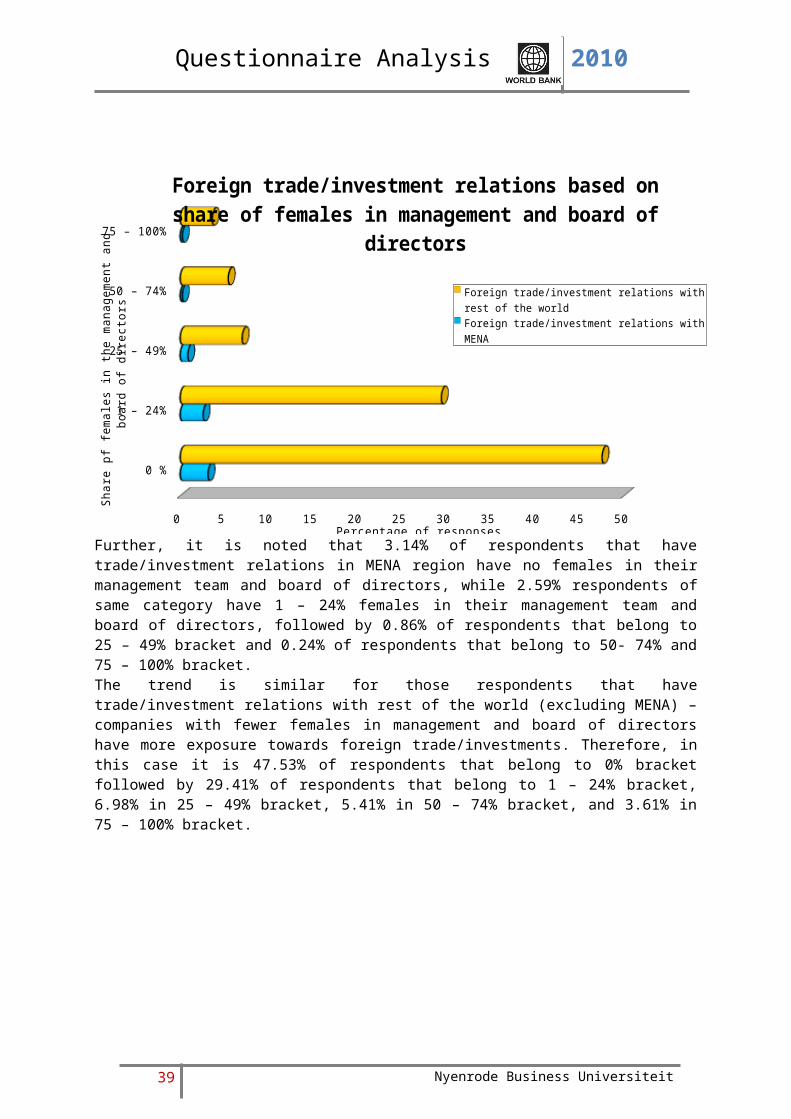

Further, it is noted that 3.14% of respondents that have trade/investment relations in MENA region have no females in their management team and board of directors, while 2.59% respondents of same category have 1 – 24% females in their management team and board of directors, followed by 0.86% of respondents that belong to 25 – 49% bracket and 0.24% of respondents that belong to 50- 74% and 75 – 100% bracket.The trend is similar for those respondents that have trade/investment relations with rest of the world (excluding MENA) – companies with fewer females in management and board of directors have more exposure towards foreign trade/investments. Therefore, in this case it is 47.53% of respondents that belong to 0% bracket followed by 29.41% of respondents that belong to 1 – 24% bracket, 6.98% in 25 – 49% bracket, 5.41% in 50 – 74% bracket, and 3.61% in 75 – 100% bracket.

37 Nyenrode Business Universiteit

Questionnaire Analysis 2010

0 %

1 – 24%

25 – 49%

50 – 74%

75 – 100%

0 20 40 60 80 100 120

Foreign trade/investment relations based on share of females in management and board of directors

Foreign trade/investment relations with MENA Foreign trade/investment relations with rest of the world

Percentage of responsesShar

e of

fem

ales

in th

e m

anag

emen

t and

boa

rd o

f di

-re

ctio

rs

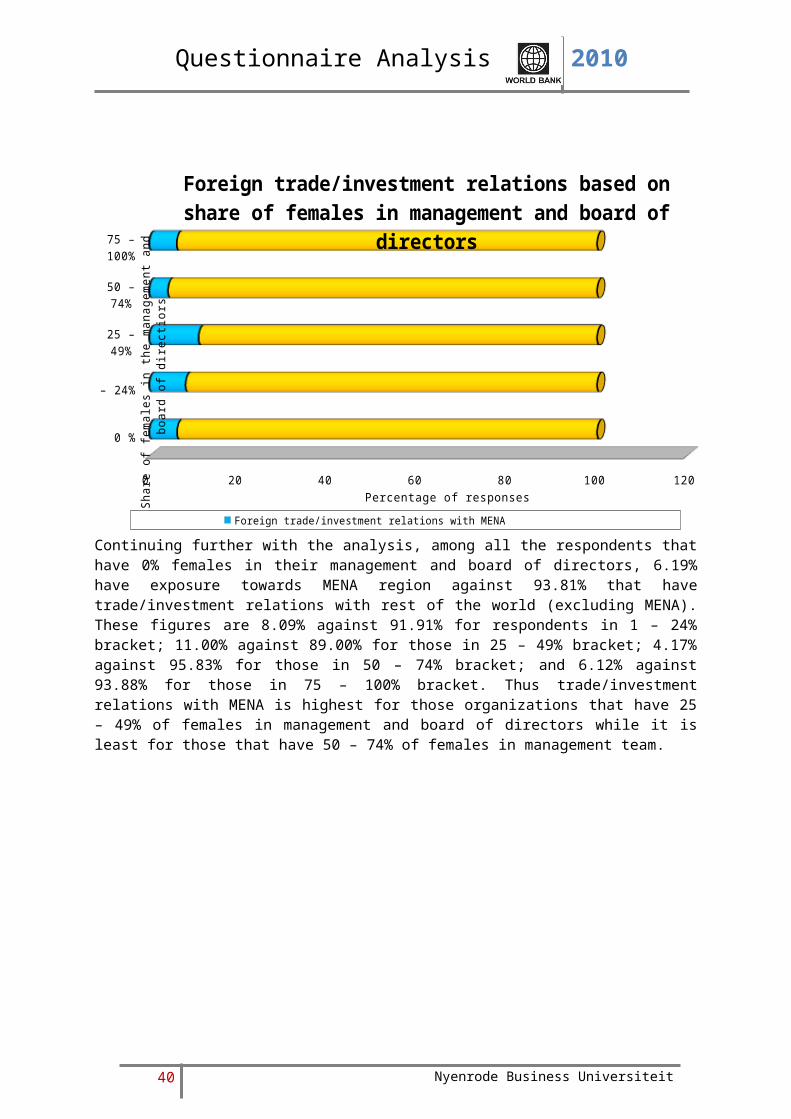

Continuing further with the analysis, among all the respondents that have 0% females in their management and board of directors, 6.19% have exposure towards MENA region against 93.81% that have trade/investment relations with rest of the world (excluding MENA). These figures are 8.09% against 91.91% for respondents in 1 – 24% bracket; 11.00% against 89.00% for those in 25 – 49% bracket; 4.17% against 95.83% for those in 50 – 74% bracket; and 6.12% against 93.88% for those in 75 – 100% bracket. Thus trade/investment relations with MENA is highest for those organizations that have 25 – 49% of females in management and board of directors while it is least for those that have 50 – 74% of females in management team.

38 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Foreign trade/investment rela-tions with MENA

Foreign trade/in-vestment rela-

tions with rest of the world

0 10 20 30 40 50 60 70 80 90 100

Foreign trade/investment relations based on share of females in management and board of directors

0 %1 – 24%25 – 49%50 – 74%75 – 100%

Percentage of responses

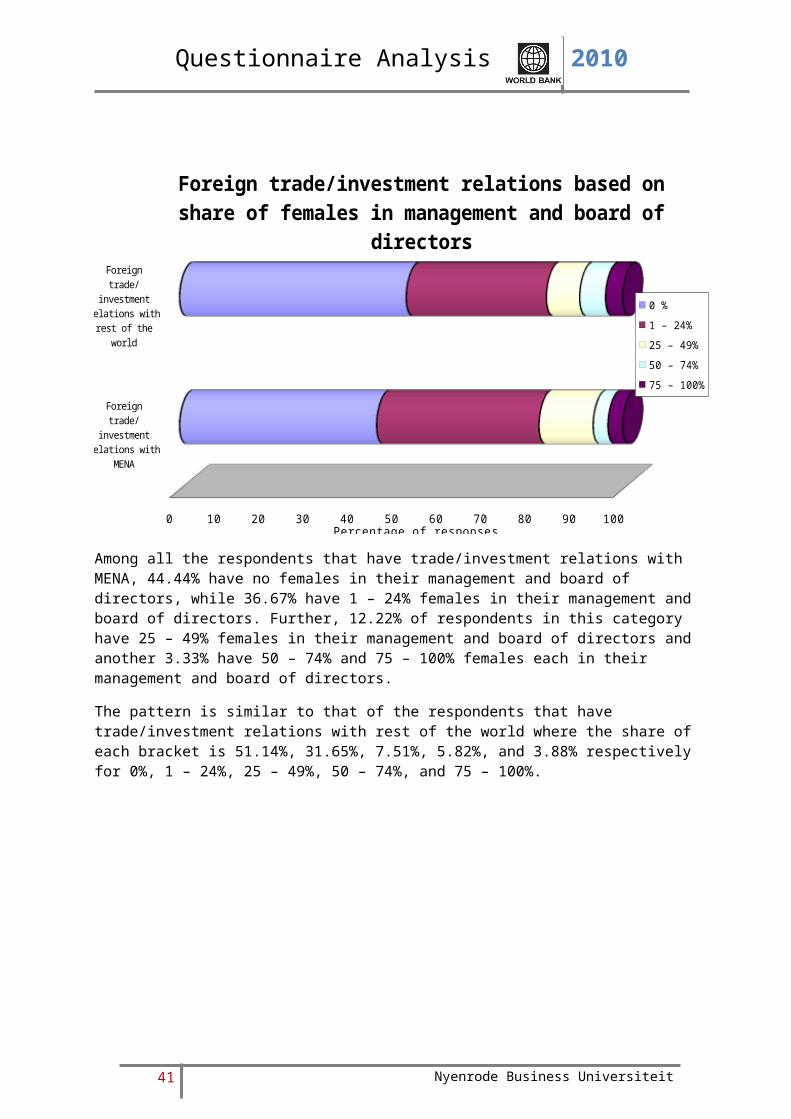

Among all the respondents that have trade/investment relations with MENA, 44.44% have no females in their management and board of directors, while 36.67% have 1 – 24% females in their management and board of directors. Further, 12.22% of respondents in this category have 25 – 49% females in their management and board of directors and another 3.33% have 50 – 74% and 75 – 100% females each in their management and board of directors.

The pattern is similar to that of the respondents that have trade/investment relations with rest of the world where the share of each bracket is 51.14%, 31.65%, 7.51%, 5.82%, and 3.88% respectively for 0%, 1 – 24%, 25 – 49%, 50 – 74%, and 75 – 100%.

39 Nyenrode Business Universiteit

Questionnaire Analysis 2010

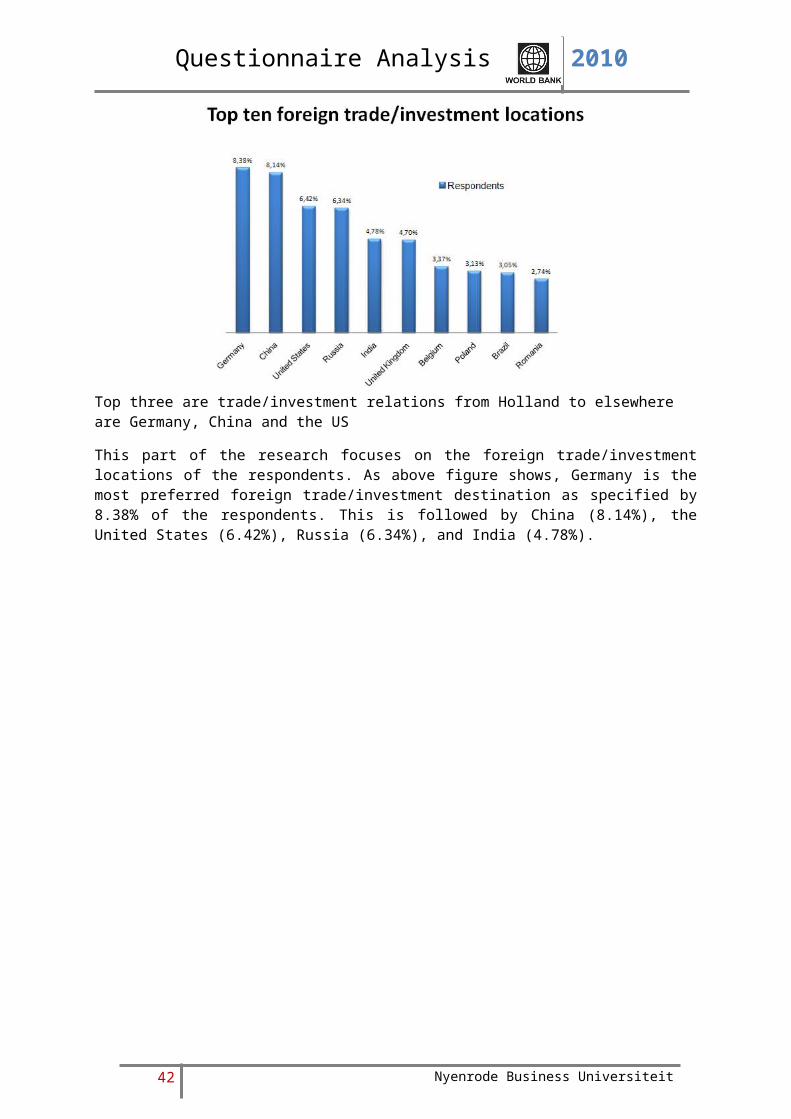

Top three are trade/investment relations from Holland to elsewhere are Germany, China and the US

This part of the research focuses on the foreign trade/investment locations of the respondents. As above figure shows, Germany is the most preferred foreign trade/investment destination as specified by 8.38% of the respondents. This is followed by China (8.14%), the United States (6.42%), Russia (6.34%), and India (4.78%).

40 Nyenrode Business Universiteit

Questionnaire Analysis 2010

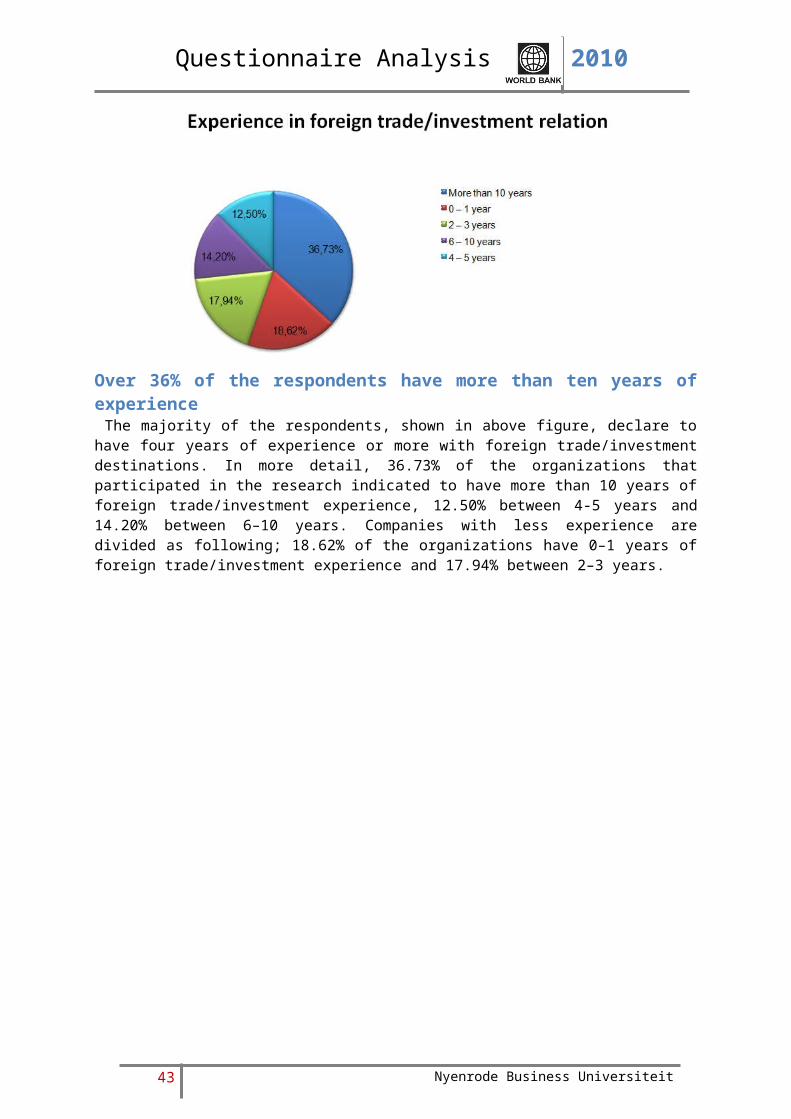

Over 36% of the respondents have more than ten years of experience The majority of the respondents, shown in above figure, declare to have four years of experience or more with foreign trade/investment destinations. In more detail, 36.73% of the organizations that participated in the research indicated to have more than 10 years of foreign trade/investment experience, 12.50% between 4-5 years and 14.20% between 6–10 years. Companies with less experience are divided as following; 18.62% of the organizations have 0–1 years of foreign trade/investment experience and 17.94% between 2–3 years.

41 Nyenrode Business Universiteit

Questionnaire Analysis 2010

0 – 1 year

2 – 3 years

4 – 5 years

6 – 10 years

More than 10 years

0 5 10 15 20 25 30 35 40

No. of years of foreign trade/investment relations with MENA and rest of the world

Foreign trade/relations with rest of the worldForeign trade/relations with MENA

Percentage of responses

No. o

f yea

rs o

f for

eign

trade

/inve

stm

ent r

elatio

ns

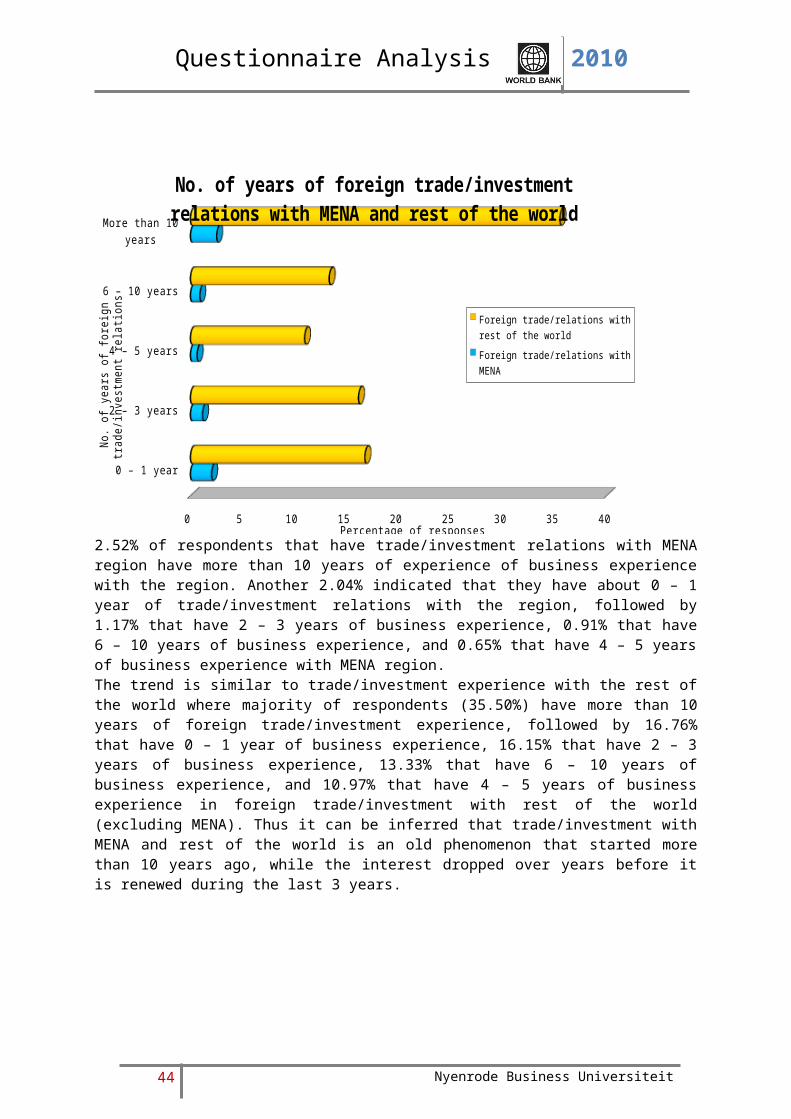

2.52% of respondents that have trade/investment relations with MENA region have more than 10 years of experience of business experience with the region. Another 2.04% indicated that they have about 0 – 1 year of trade/investment relations with the region, followed by 1.17% that have 2 – 3 years of business experience, 0.91% that have 6 – 10 years of business experience, and 0.65% that have 4 – 5 years of business experience with MENA region.The trend is similar to trade/investment experience with the rest of the world where majority of respondents (35.50%) have more than 10 years of foreign trade/investment experience, followed by 16.76% that have 0 – 1 year of business experience, 16.15% that have 2 – 3 years of business experience, 13.33% that have 6 – 10 years of business experience, and 10.97% that have 4 – 5 years of business experience in foreign trade/investment with rest of the world (excluding MENA). Thus it can be inferred that trade/investment with MENA and rest of the world is an old phenomenon that started more than 10 years ago, while the interest dropped over years before it is renewed during the last 3 years.

42 Nyenrode Business Universiteit

Questionnaire Analysis 2010

0 – 1 year

2 – 3 years

4 – 5 years

6 – 10 years

More than 10 years

0 20 40 60 80 100

No. of years of foreign trade/investment relations with MENA and rest of the world

Foreign trade/relations with MENA Foreign trade/relations with rest of the world

Percentage of responsesNo.

of y

ears

of e

xper

ienc

e in

fore

ign

trade

/inve

stm

ent

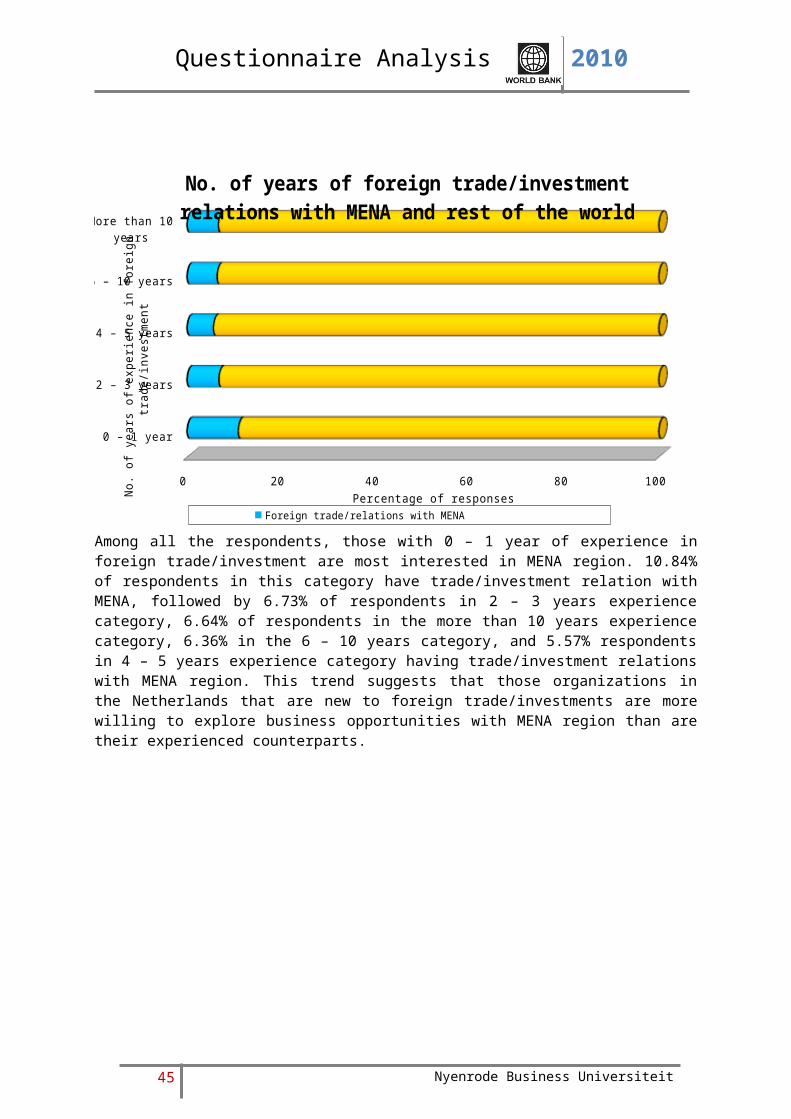

Among all the respondents, those with 0 – 1 year of experience in foreign trade/investment are most interested in MENA region. 10.84% of respondents in this category have trade/investment relation with MENA, followed by 6.73% of respondents in 2 – 3 years experience category, 6.64% of respondents in the more than 10 years experience category, 6.36% in the 6 – 10 years category, and 5.57% respondents in 4 – 5 years experience category having trade/investment relations with MENA region. This trend suggests that those organizations in the Netherlands that are new to foreign trade/investments are more willing to explore business opportunities with MENA region than are their experienced counterparts.

43 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Foreign trade/rela-tions with

MENA

Foreign trade/rela-

tions with rest of the world

0 10 20 30 40 50 60 70 80 90 100

No. of years of foreign trade/investment relations with MENA and rest of the world

0 – 1 year2 – 3 years4 – 5 years6 – 10 yearsMore than 10 years

Percentage of responsesAmong all the respondents that have trade/investment relations with MENA, majority have more than 10 years of experience in the region similar to the trend of the rest of the world. Thus, 34.67% of respondents that have trade/investment relations with MENA have more than 10 years of experience in the region against 38.29% of the respondents that have trade/investment relations with rest of the world (excluding MENA) have more than 10 years of foreign trade/investment relations. These figures are 28.00% for MENA against 18.08% for rest of the world in the 0 – 1 year experience category, 16.00% for MENA against 17.42% for rest of the world in the 2 – 3 years experience category, 12.44% for MENA against 14.38% for rest of the world in the 6- 10 years experience category, and 8.89% for MENA against 11.83 for rest of the world in the category 4 – 5 years experience in foreign trade/investments.

44 Nyenrode Business Universiteit

Questionnaire Analysis 2010

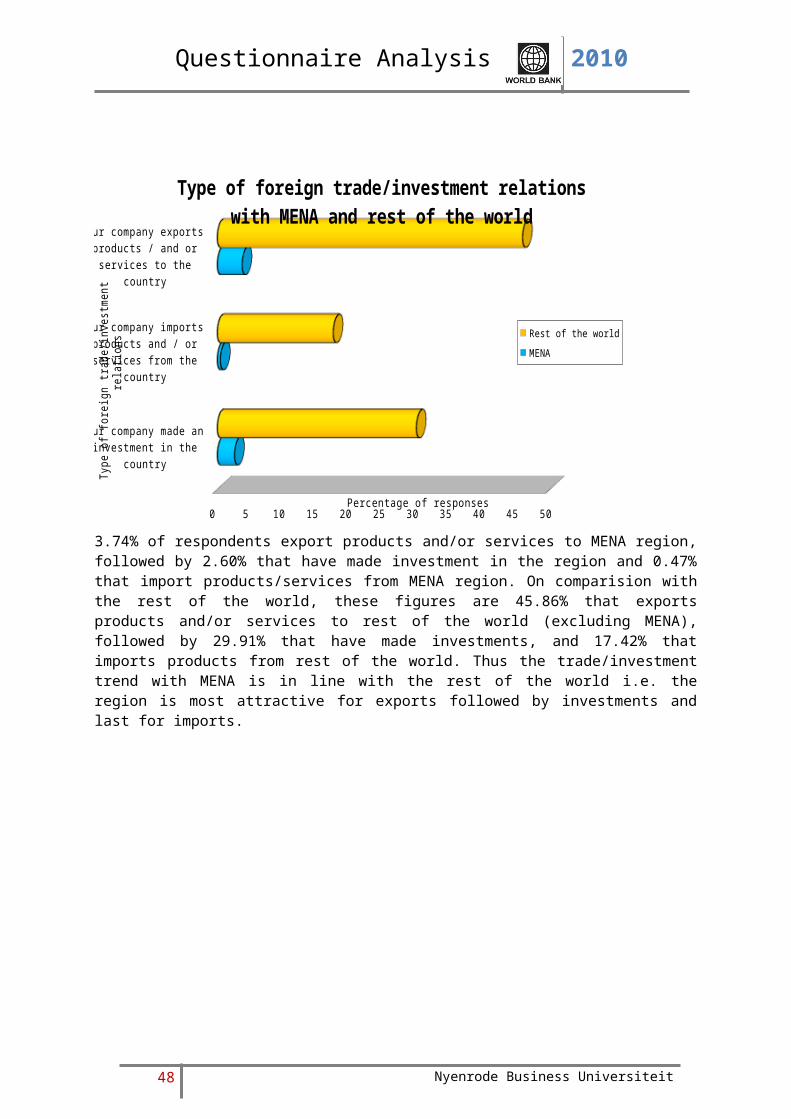

The majority of the respondents export products and or services Since a considerable number of organizations indicated to have sufficient experience in foreign trade/investments, we further probed the type of experience that these organizations possess/are planning to explore with regards to foreign trade/investment. The responses were categorized into 3 categories – our company exports products and/or services to the country, our company made an investment in the country and our company imports products and/or services from the country. The figure above clearly shows that the majority of organizations (46.10%) have exported/or are planning to export their products/services to a foreign location; 34.02% of the organizations indicated that they have invested/or are planning to invest in a foreign location; lastly 19.88% of the respondents indicated that they import/or are planning to import products/services from foreign locations.

45 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Our company made an investment in the country

Our company imports products and / or services

from the country

Our company exports products / and or services

to the country

0 5 10 15 20 25 30 35 40 45 50

Type of foreign trade/investment relations with MENA and rest of the world

Rest of the worldMENA

Percentage of responses

Type

of f

oreig

n tra

de/in

vest

men

t rela

tions

3.74% of respondents export products and/or services to MENA region, followed by 2.60% that have made investment in the region and 0.47% that import products/services from MENA region. On comparision with the rest of the world, these figures are 45.86% that exports products and/or services to rest of the world (excluding MENA), followed by 29.91% that have made investments, and 17.42% that imports products from rest of the world. Thus the trade/investment trend with MENA is in line with the rest of the world i.e. the region is most attractive for exports followed by investments and last for imports.

46 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Our company made an investment in the country

Our company imports products and / or services

from the country

Our company exports products / and or services

to the country

0 10 20 30 40 50 60 70 80 90 100

Type of foreign trade/investment relations with MENA and rest of the world

MENA Rest of the world

Percentage of responses

Type

of f

oreig

n tra

de/in

vest

men

t rela

tions

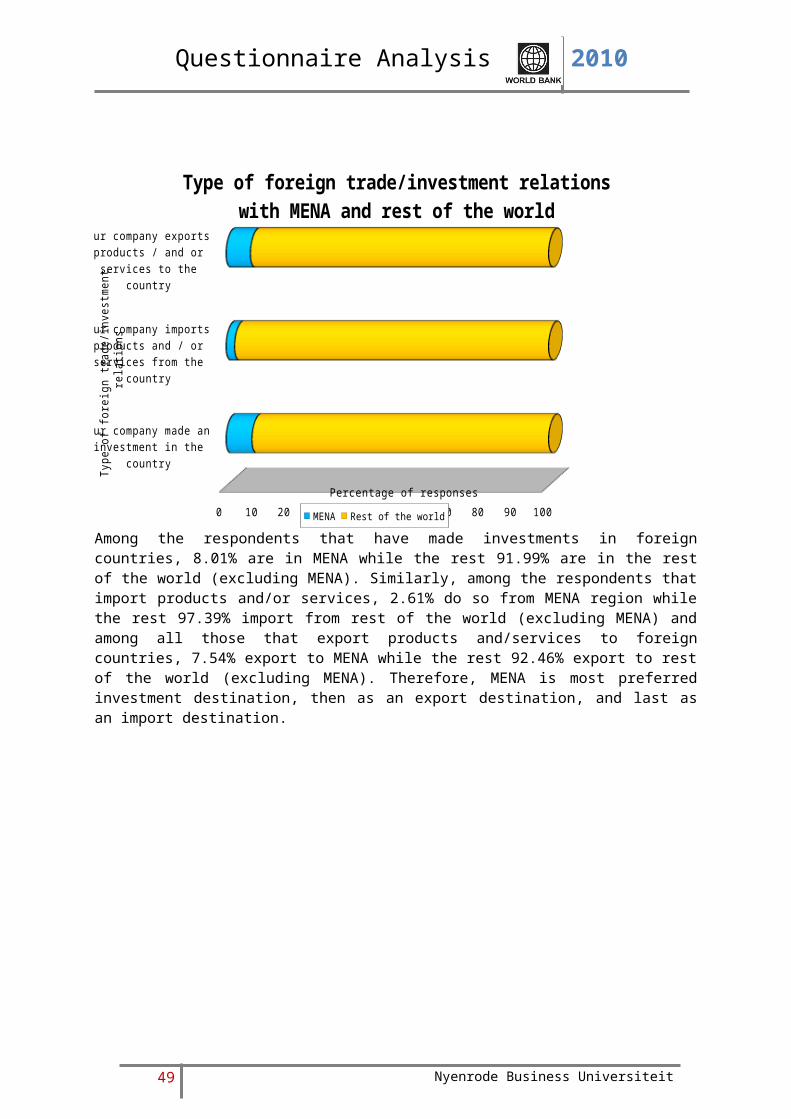

Among the respondents that have made investments in foreign countries, 8.01% are in MENA while the rest 91.99% are in the rest of the world (excluding MENA). Similarly, among the respondents that import products and/or services, 2.61% do so from MENA region while the rest 97.39% import from rest of the world (excluding MENA) and among all those that export products and/services to foreign countries, 7.54% export to MENA while the rest 92.46% export to rest of the world (excluding MENA). Therefore, MENA is most preferred investment destination, then as an export destination, and last as an import destination.

47 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Foreign trade/invest-

ment relations with MENA

Foreign trade/invest-

ment relations with rest of the world

0 10 20 30 40 50 60 70 80 90 100

Type of foreign trade/investment relations with MENA and rest of the world

Our company made an investmentOur company imports products and / or servicesOur company exports products / and or services

Percentage of responses

Among all the respondents that have trade/investment relations with MENA region, 54.90% are engaged in exporting to the region followed by 38.24% of those that have invested in the region, and 6.86% of those that import from the region. This trend is similar to that of the rest of the world where 49.21% of respondents are engaged in exporting their products and/or services, followed by 32.09% that have made foreign investments, and 18.70% that import products and/or services in to the Netherlands.

48 Nyenrode Business Universiteit

Questionnaire Analysis 2010

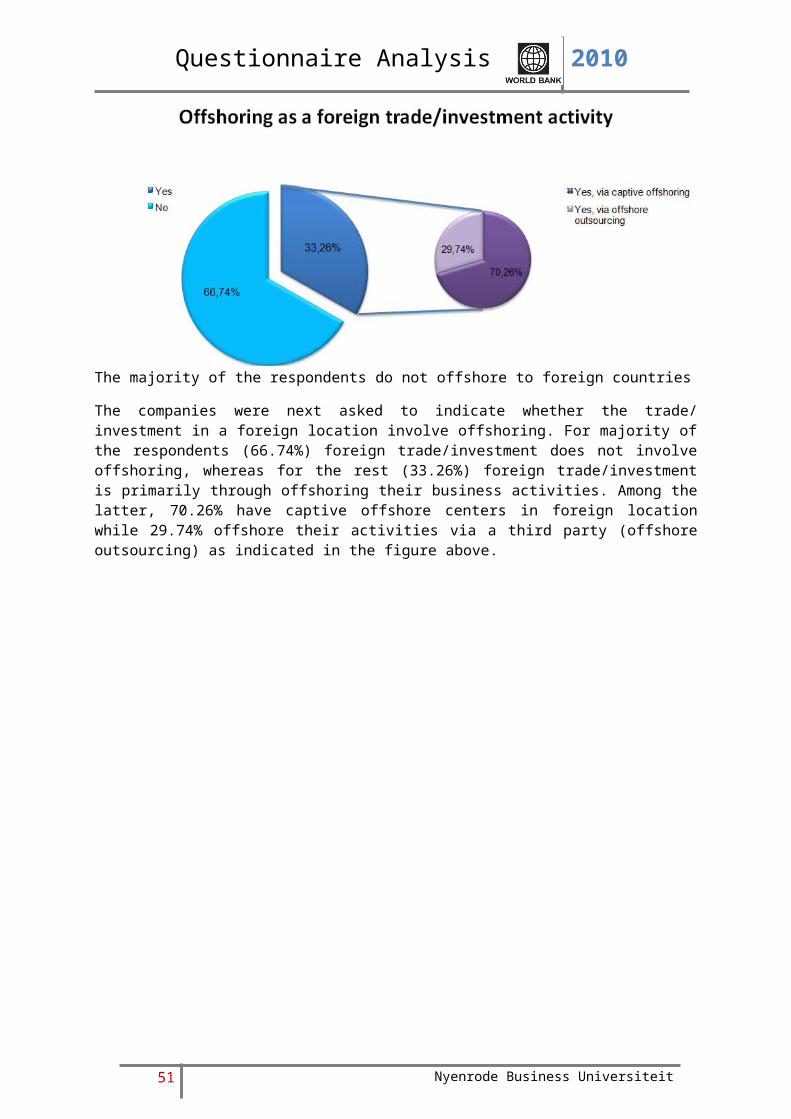

The majority of the respondents do not offshore to foreign countries

The companies were next asked to indicate whether the trade/ investment in a foreign location involve offshoring. For majority of the respondents (66.74%) foreign trade/investment does not involve offshoring, whereas for the rest (33.26%) foreign trade/investment is primarily through offshoring their business activities. Among the latter, 70.26% have captive offshore centers in foreign location while 29.74% offshore their activities via a third party (offshore outsourcing) as indicated in the figure above.

49 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Yes, via captive offshoring

Yes, via offshore outsourcing

No

0 10 20 30 40 50 60 70

Offshoring as foreign trade/investment relations

Rest of the worldMENA

Percentage of responses

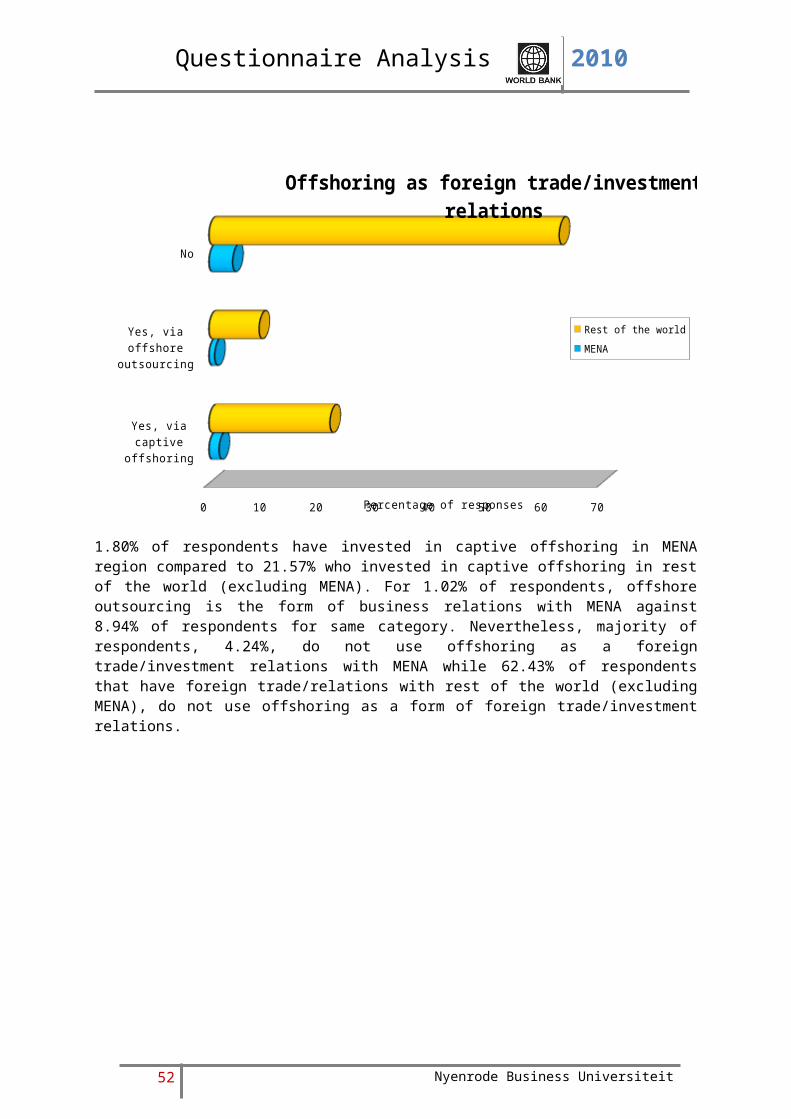

1.80% of respondents have invested in captive offshoring in MENA region compared to 21.57% who invested in captive offshoring in rest of the world (excluding MENA). For 1.02% of respondents, offshore outsourcing is the form of business relations with MENA against 8.94% of respondents for same category. Nevertheless, majority of respondents, 4.24%, do not use offshoring as a foreign trade/investment relations with MENA while 62.43% of respondents that have foreign trade/relations with rest of the world (excluding MENA), do not use offshoring as a form of foreign trade/investment relations.

50 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Yes, via captive offshoring

Yes, via offshore outsourcing

No

0 10 20 30 40 50 60 70 80 90 100

Offshoring as foreign trade/investment relations

MENARest of the world

Percentage of responses

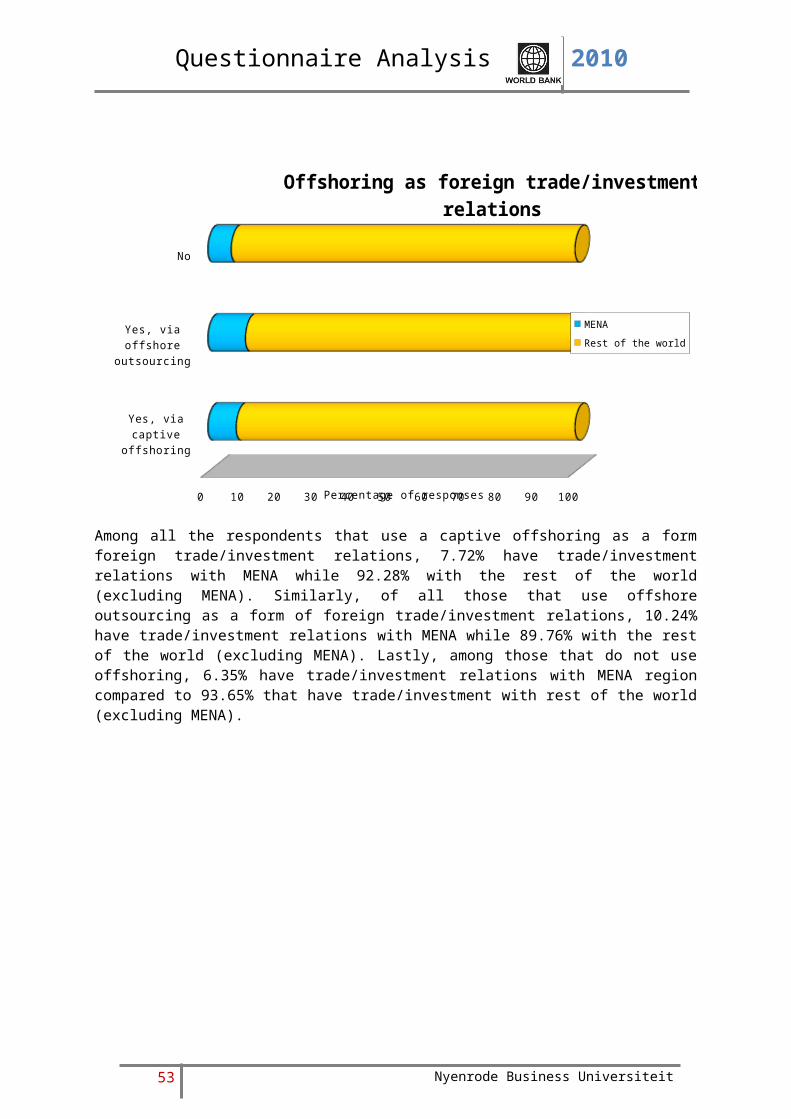

Among all the respondents that use a captive offshoring as a form foreign trade/investment relations, 7.72% have trade/investment relations with MENA while 92.28% with the rest of the world (excluding MENA). Similarly, of all those that use offshore outsourcing as a form of foreign trade/investment relations, 10.24% have trade/investment relations with MENA while 89.76% with the rest of the world (excluding MENA). Lastly, among those that do not use offshoring, 6.35% have trade/investment relations with MENA region compared to 93.65% that have trade/investment with rest of the world (excluding MENA).

51 Nyenrode Business Universiteit

Questionnaire Analysis 2010

MENA

Rest of the world

0 10 20 30 40 50 60 70 80 90 100

Offshoring as foreign trade/investment relations

Yes, via captive offshoringYes, via offshore outsourc-ingNo

Percentage of responses

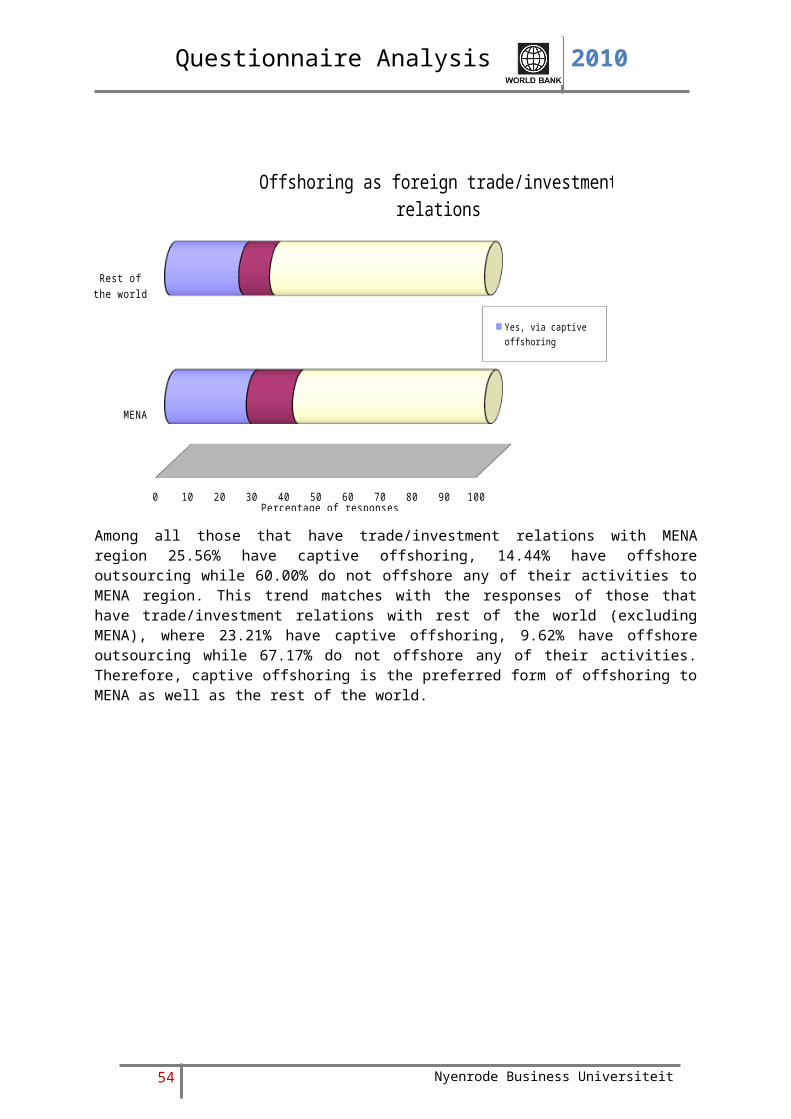

Among all those that have trade/investment relations with MENA region 25.56% have captive offshoring, 14.44% have offshore outsourcing while 60.00% do not offshore any of their activities to MENA region. This trend matches with the responses of those that have trade/investment relations with rest of the world (excluding MENA), where 23.21% have captive offshoring, 9.62% have offshore outsourcing while 67.17% do not offshore any of their activities. Therefore, captive offshoring is the preferred form of offshoring to MENA as well as the rest of the world.

52 Nyenrode Business Universiteit

Questionnaire Analysis 2010

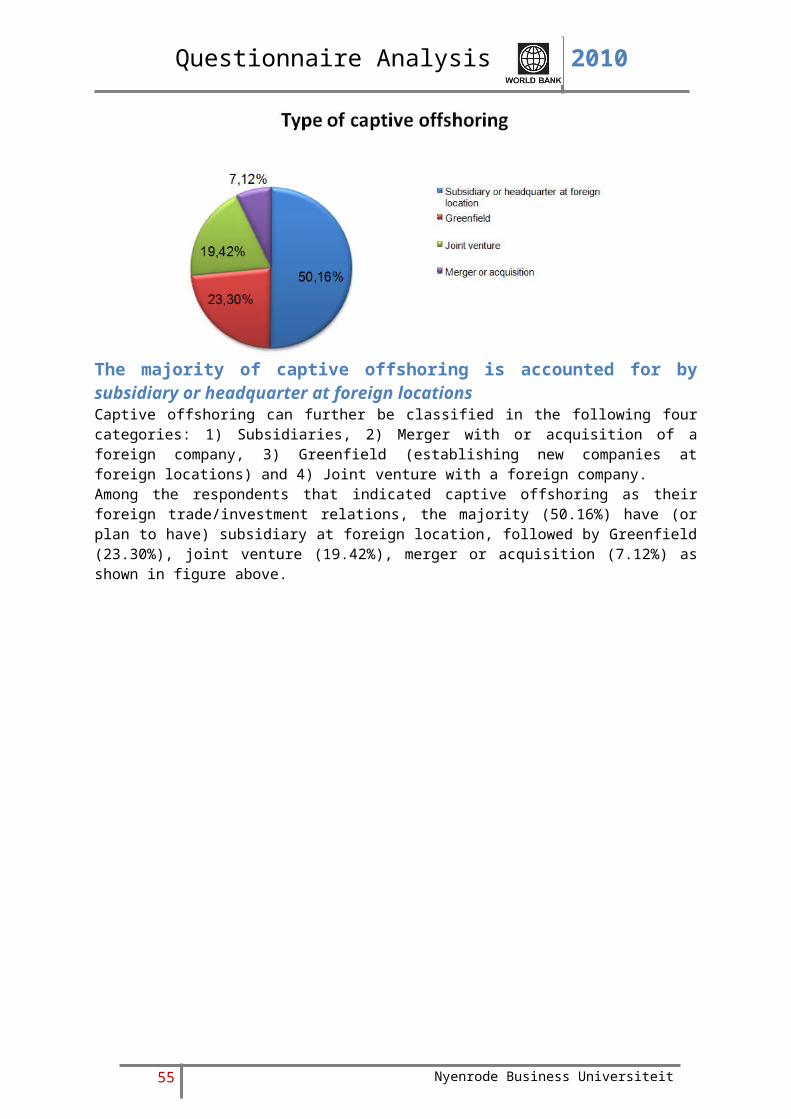

The majority of captive offshoring is accounted for by subsidiary or headquarter at foreign locations Captive offshoring can further be classified in the following four categories: 1) Subsidiaries, 2) Merger with or acquisition of a foreign company, 3) Greenfield (establishing new companies at foreign locations) and 4) Joint venture with a foreign company.Among the respondents that indicated captive offshoring as their foreign trade/investment relations, the majority (50.16%) have (or plan to have) subsidiary at foreign location, followed by Greenfield (23.30%), joint venture (19.42%), merger or acquisition (7.12%) as shown in figure above.

53 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Subsidiary or headquar-ter at foreign location

Merger or acquisition

Greenfield

Joint venture

0 5 10 15 20 25 30 35 40 45 50

Type of captive offshoring as foreign trade/in-vestment relations

Rest of the worldMENA

Percentage of responses

Having a subsidiary or headquarter at foreign location is preferred type of captive offshoring by most respondents (48.48%) that have foreign trade/investment relations (excluding MENA). However, majority those that have trade/investment relations with MENA region (4.55%) prefer to have a joint venture in the region. While Greenfield investment is the next most preferred (22.08%) type of captive offshoring for respondents that have foreign trade/investment (excluding MENA), having a subsidiary or headquarter in MENA region is the next most preferred (1.95%) type captive offshoring for respondents that have trade/investment relations with MENA region. 14.94% of those that have foreign trade/investment (excluding MENA) also have joint venture form of captive offshoring, followed by 7.14% of respondents have merger or acquisition form of captive offshoring. On the other hand, among those that have trade/investment relations with MENA, 0.97% of respondents also have Greenfield investments while none are involved in mergers and acquisitions.

54 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Subsidiary or headquar-ter at foreign location

Merger or acquisition

Greenfield

Joint venture

0 10 20 30 40 50 60 70 80 90 100

Type of captive offshoring as foreign trade/in-vestment relations

MENARest of the world

Percentage of responses

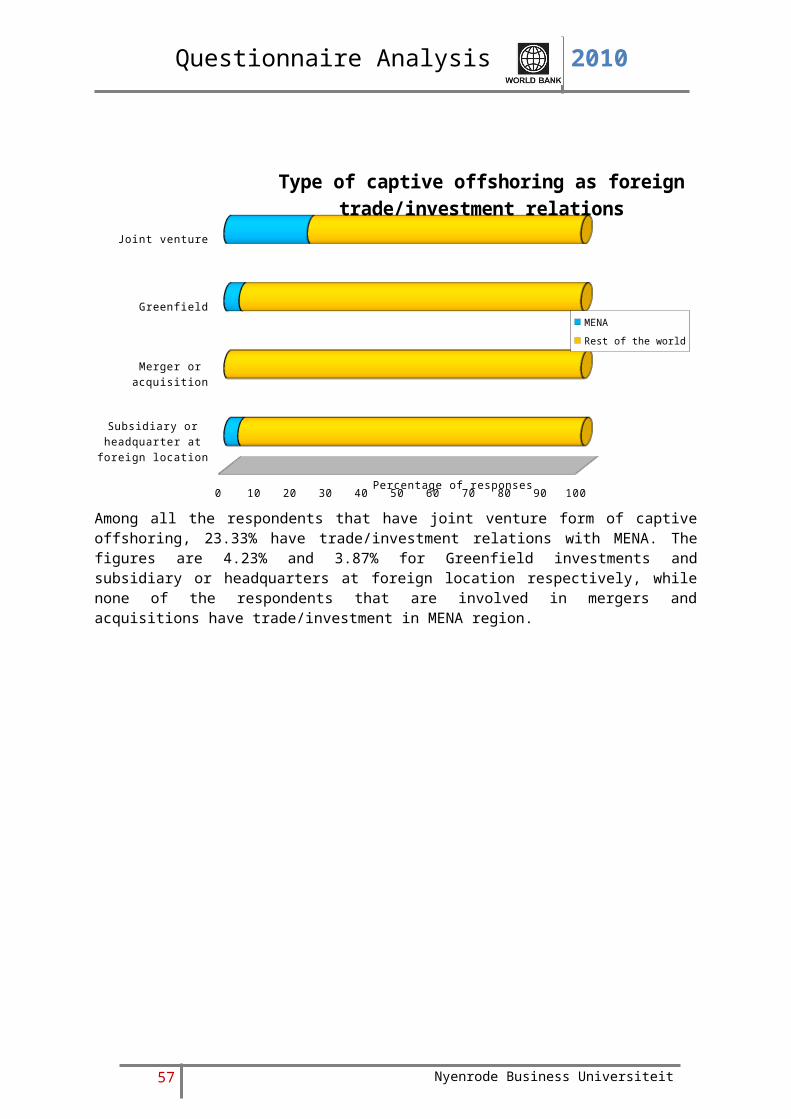

Among all the respondents that have joint venture form of captive offshoring, 23.33% have trade/investment relations with MENA. The figures are 4.23% and 3.87% for Greenfield investments and subsidiary or headquarters at foreign location respectively, while none of the respondents that are involved in mergers and acquisitions have trade/investment in MENA region.

55 Nyenrode Business Universiteit

Questionnaire Analysis 2010

MENA

Rest of the world

0 20 40 60 80 100

Type of captive offshoring as foreign trade/in-vestment relations

Subsidiary or headquarter at foreign location

Merger or acquisition

Greenfield

Joint venture

Percentage of responses

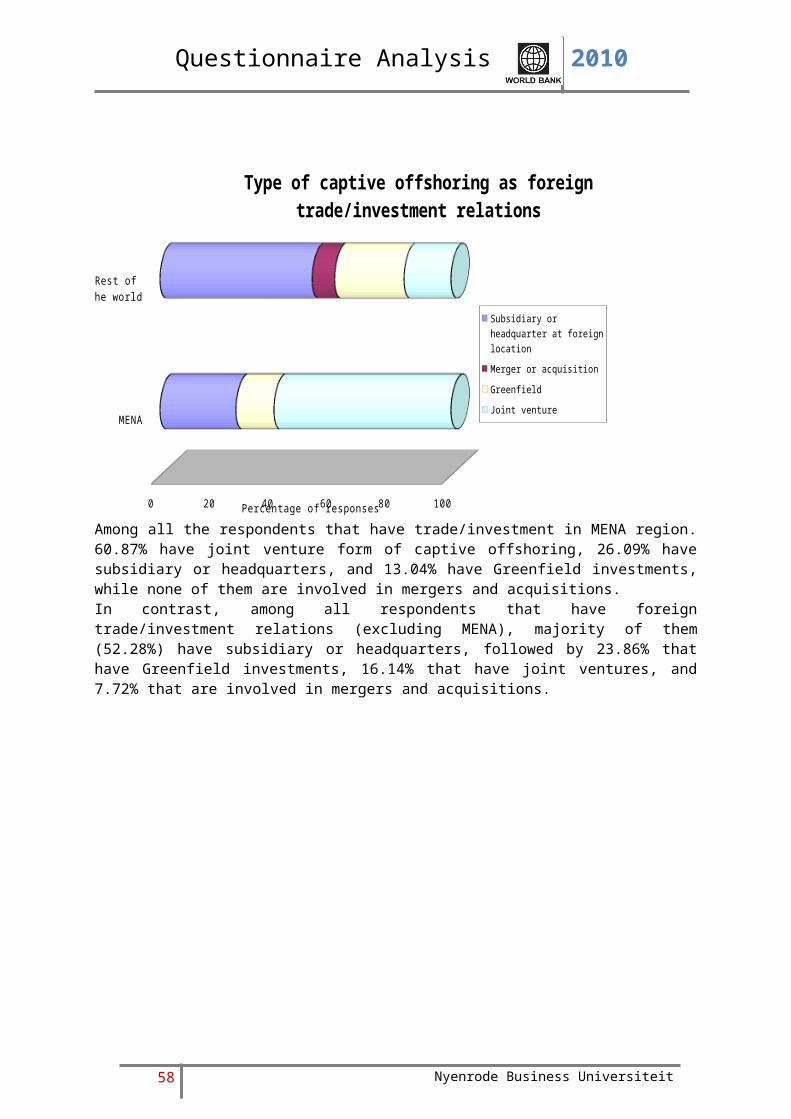

Among all the respondents that have trade/investment in MENA region. 60.87% have joint venture form of captive offshoring, 26.09% have subsidiary or headquarters, and 13.04% have Greenfield investments, while none of them are involved in mergers and acquisitions.In contrast, among all respondents that have foreign trade/investment relations (excluding MENA), majority of them (52.28%) have subsidiary or headquarters, followed by 23.86% that have Greenfield investments, 16.14% that have joint ventures, and 7.72% that are involved in mergers and acquisitions.

56 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Top three locations are the Netherlands, USA and India From the companies that indicated to offshore activities to foreign countries via a third party (9.89%, as described in figure above), 12.03% of the respondents have their third party headquartered in the Netherlands, followed by the USA (8.27%), India (6.77%), Russia (6.02%) and Germany and China both 5.26%.

57 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Top three activities that are being relocated to foreign locations are Sales, Production and Marketing As shown in figure above, the majority of relocated activities are related to sales (18.47%). 15.63% of the respondents indicated that they relocated production activities, followed by 12.79% of the respondents referring to marketing activities as being relocated. Above figure provides an overview of type of activities that are relocated from the Netherlands to foreign locations.

58 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Technology & Applicationdevelopment

IT-infrastructure

Financial & Administrative services

Research & Development

Distribution & Logistics

After sales service

Engineering

Management functions

Marketing

Sales

Production

Business services

Others

0 2 4 6 8 10 12 14 16 18

Activities relocated to foreign locations

Rest of the worldMENA

Percentage of responses

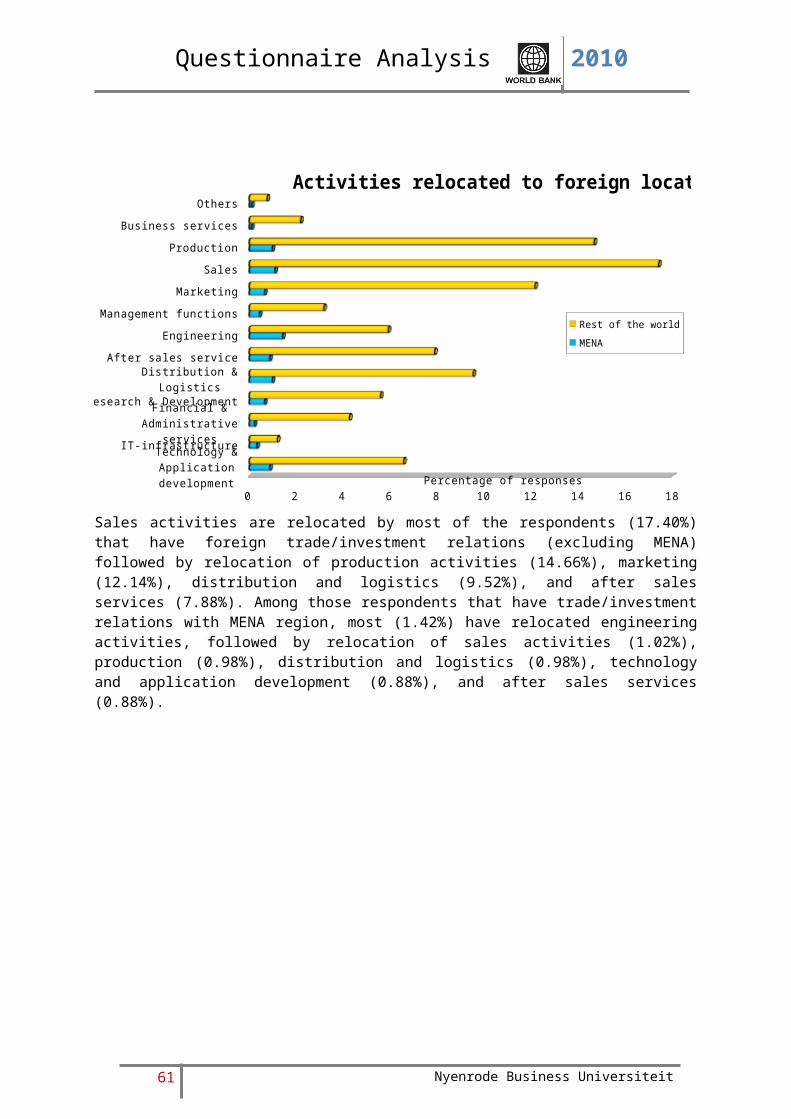

Sales activities are relocated by most of the respondents (17.40%) that have foreign trade/investment relations (excluding MENA) followed by relocation of production activities (14.66%), marketing (12.14%), distribution and logistics (9.52%), and after sales services (7.88%). Among those respondents that have trade/investment relations with MENA region, most (1.42%) have relocated engineering activities, followed by relocation of sales activities (1.02%), production (0.98%), distribution and logistics (0.98%), technology and application development (0.88%), and after sales services (0.88%).

59 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Technology & Applicationdevelopment

IT-infrastructure

Financial & Administrative services

Research & Development

Distribution & Logistics

After sales service

Engineering

Management functions

Marketing

Sales

Production

Business services

Others

0 20 40 60 80 100 120

Activities relocated to foreign locations

MENA Rest of the world

Percentage of responses

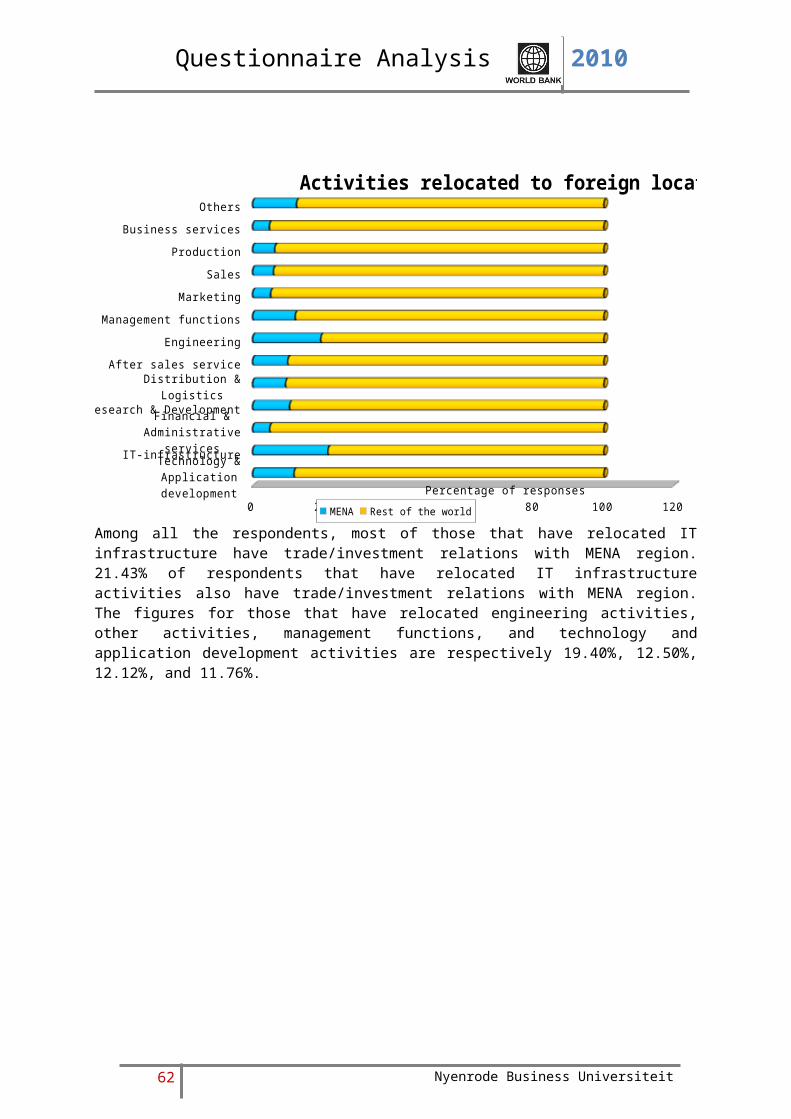

Among all the respondents, most of those that have relocated IT infrastructure have trade/investment relations with MENA region. 21.43% of respondents that have relocated IT infrastructure activities also have trade/investment relations with MENA region. The figures for those that have relocated engineering activities, other activities, management functions, and technology and application development activities are respectively 19.40%, 12.50%, 12.12%, and 11.76%.

60 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Technology & Applicationdevelopment

After sales service

Distribution & Logistics

Production

Sales

Engineering

0 2 4 6 8 10 12 14 16 18

Top 5 activities relocated by respondents having trade/investment relations with MENA

Percentage of response

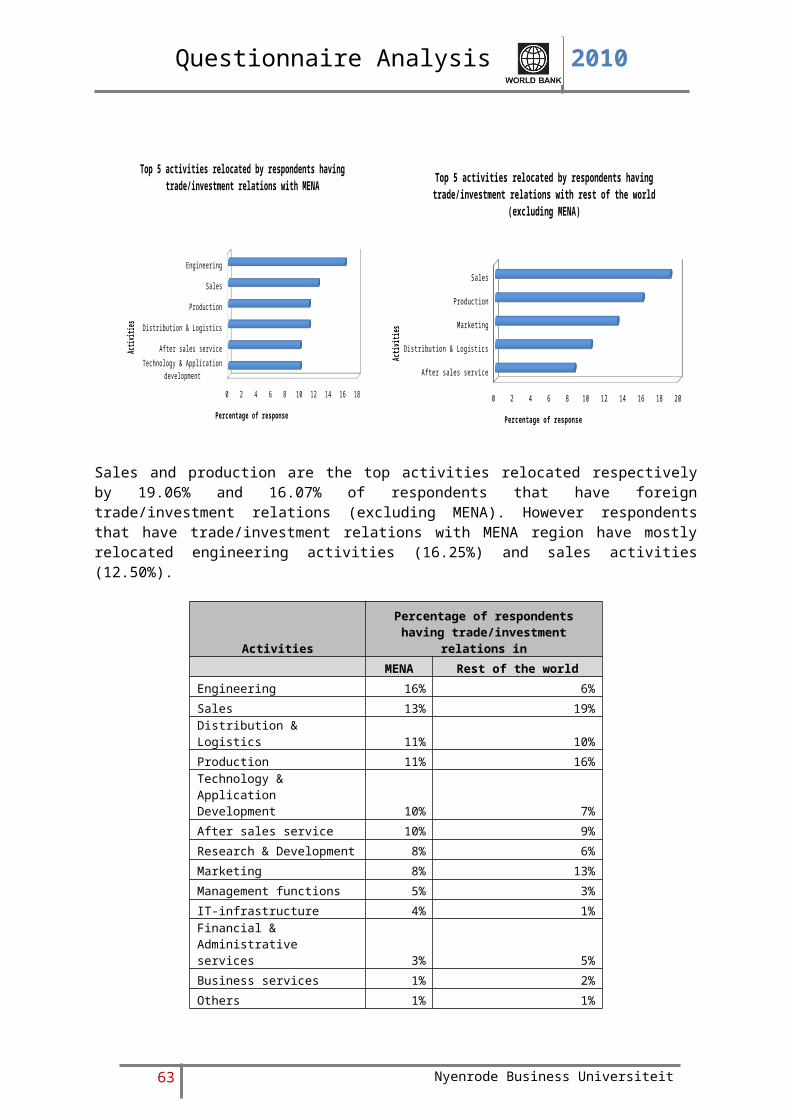

Activi

ties

Sales and production are the top activities relocated respectively by 19.06% and 16.07% of respondents that have foreign trade/investment relations (excluding MENA). However respondents that have trade/investment relations with MENA region have mostly relocated engineering activities (16.25%) and sales activities (12.50%).

ActivitiesPercentage of respondents

having trade/investment relations inMENA Rest of the world

Engineering 16% 6%

Sales 13% 19%

Distribution & Logistics 11% 10%

Production 11% 16%Technology & Application Development 10% 7%

After sales service 10% 9%

Research & Development 8% 6%

Marketing 8% 13%

Management functions 5% 3%

IT-infrastructure 4% 1%Financial & Administrativeservices 3% 5%

Business services 1% 2%

Others 1% 1%

Total 100% 100%

61 Nyenrode Business Universiteit

After sales service

Distribution & Logistics

Marketing

Production

Sales

0 2 4 6 8 10 12 14 16 18 20

Top 5 activities relocated by respondents having trade/investment relations with rest of the world (excluding MENA)

Percentage of responseAc

tivitie

s

Questionnaire Analysis 2010

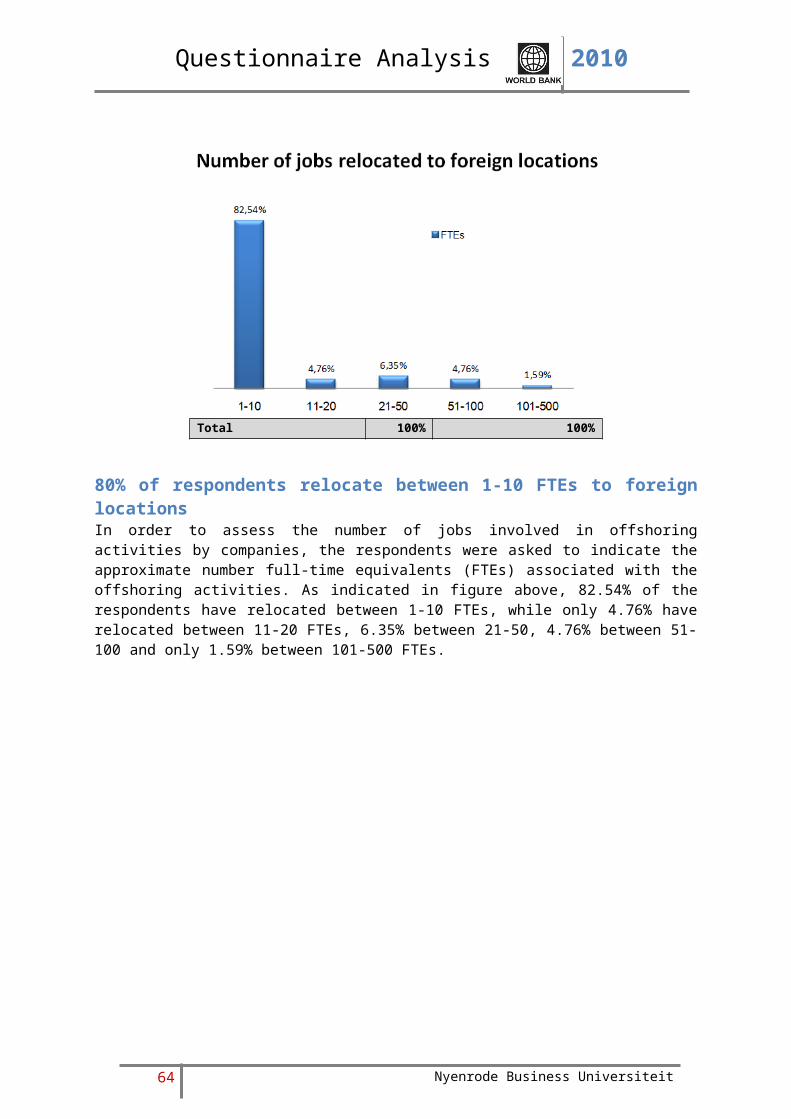

80% of respondents relocate between 1-10 FTEs to foreign locationsIn order to assess the number of jobs involved in offshoring activities by companies, the respondents were asked to indicate the approximate number full-time equivalents (FTEs) associated with the offshoring activities. As indicated in figure above, 82.54% of the respondents have relocated between 1-10 FTEs, while only 4.76% have relocated between 11-20 FTEs, 6.35% between 21-50, 4.76% between 51-100 and only 1.59% between 101-500 FTEs.

62 Nyenrode Business Universiteit

Questionnaire Analysis 2010

1-10

11-20

21-50

51-100

101-500

501 o...

0 10 20 30 40 50 60 70 80

Number of FTEs relocated from The Netherlands to foreign locations

Trade/investment relations with rest of the worldTrade/investment relations with MENA

Percentage of responses

Num

ber

of F

TE

s re

loca

ted

from

the

Net

herla

nds

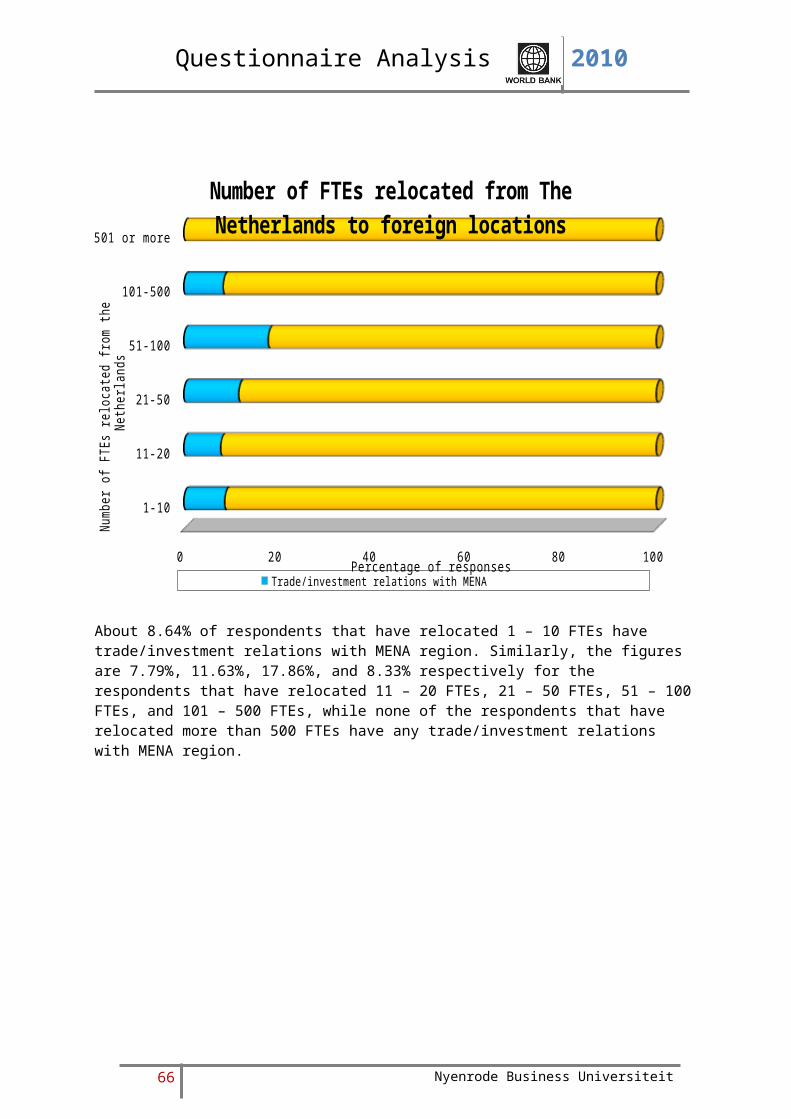

Most of the respondents that have trade/investment relations with MENA region (7.09%) have relocated 1 – 10 FTEs from the Netherlands followed by 0.65% that have relocated 11 – 20 FTEs, 0.55% that have relocated 21 – 50 FTEs and 51 – 100 FTEs each, and 0.11% that have relocated 101 – 500 FTEs. However, none of the respondents that have trade/investment relations with MENA region have relocated more than 500 FTEs.This pattern is similar to that of respondents that have foreign trade/investment (excluding MENA), where majority of respondents (74.92%) have relocated 1 – 10 FTEs, followed by 7.74% that have relocated 11 – 20 FTEs, 4.14% that have relocated 21 – 50 FTEs, 2.51% that have relocated 51 – 100 FTEs, 1.20% that have relocated 101 – 500 FTEs and 0.55% that have relocated more than 500 FTEs.

63 Nyenrode Business Universiteit

Questionnaire Analysis 2010

1-10

11-20

21-50

51-100

101-500

501 or more

0 20 40 60 80 100

Number of FTEs relocated from The Netherlands to foreign locations

Trade/investment relations with MENA Trade/investment relations with rest of the worldPercentage of responses

Numb

er o

f FTE

s re

locat

ed fr

om th

e Ne

ther

lands

About 8.64% of respondents that have relocated 1 – 10 FTEs have trade/investment relations with MENA region. Similarly, the figures are 7.79%, 11.63%, 17.86%, and 8.33% respectively for the respondents that have relocated 11 – 20 FTEs, 21 – 50 FTEs, 51 – 100 FTEs, and 101 – 500 FTEs, while none of the respondents that have relocated more than 500 FTEs have any trade/investment relations with MENA region.

64 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Trade/in-vestment re-lations with

MENA

Trade/invest-ment relations with rest of the

world

0 10 20 30 40 50 60 70 80 90 100

Number of FTEs relocated from The Netherlands to foreign locations

1-10 11-20 21-50 51-100 101-500 501 or more

Percentage of responses

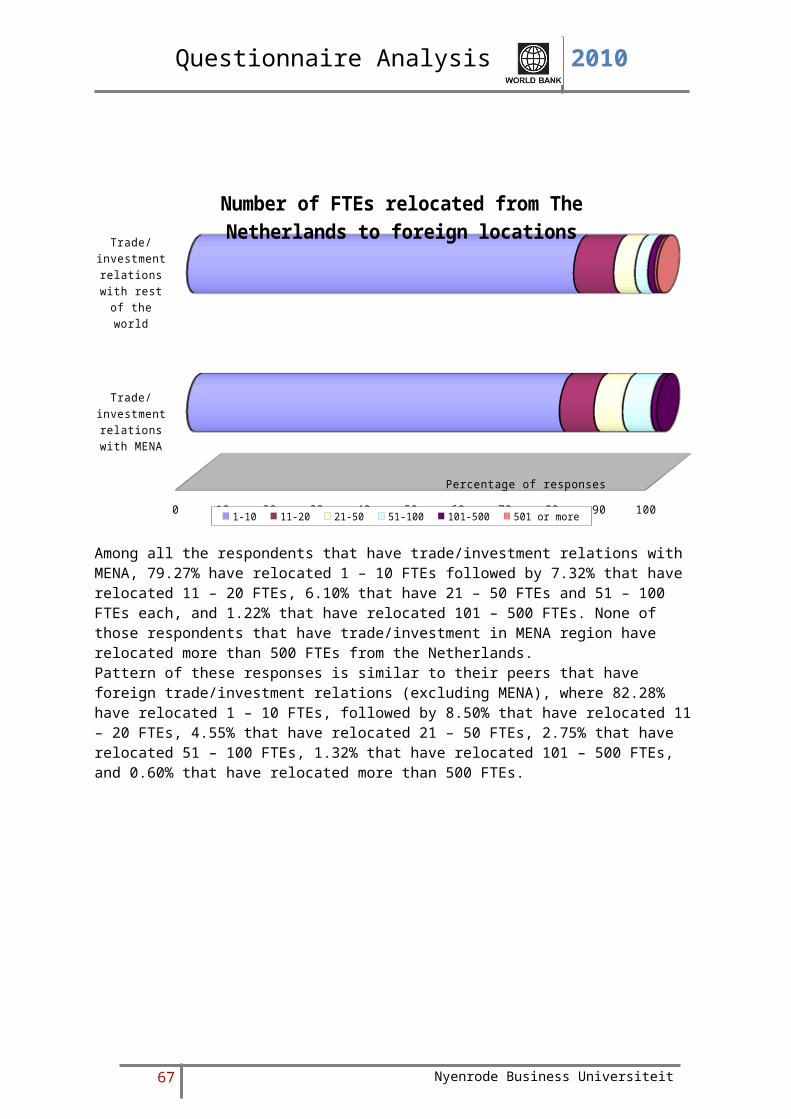

Among all the respondents that have trade/investment relations with MENA, 79.27% have relocated 1 – 10 FTEs followed by 7.32% that have relocated 11 – 20 FTEs, 6.10% that have 21 – 50 FTEs and 51 – 100 FTEs each, and 1.22% that have relocated 101 – 500 FTEs. None of those respondents that have trade/investment in MENA region have relocated more than 500 FTEs from the Netherlands.Pattern of these responses is similar to their peers that have foreign trade/investment relations (excluding MENA), where 82.28% have relocated 1 – 10 FTEs, followed by 8.50% that have relocated 11 – 20 FTEs, 4.55% that have relocated 21 – 50 FTEs, 2.75% that have relocated 51 – 100 FTEs, 1.32% that have relocated 101 – 500 FTEs, and 0.60% that have relocated more than 500 FTEs.

65 Nyenrode Business Universiteit

Questionnaire Analysis 2010

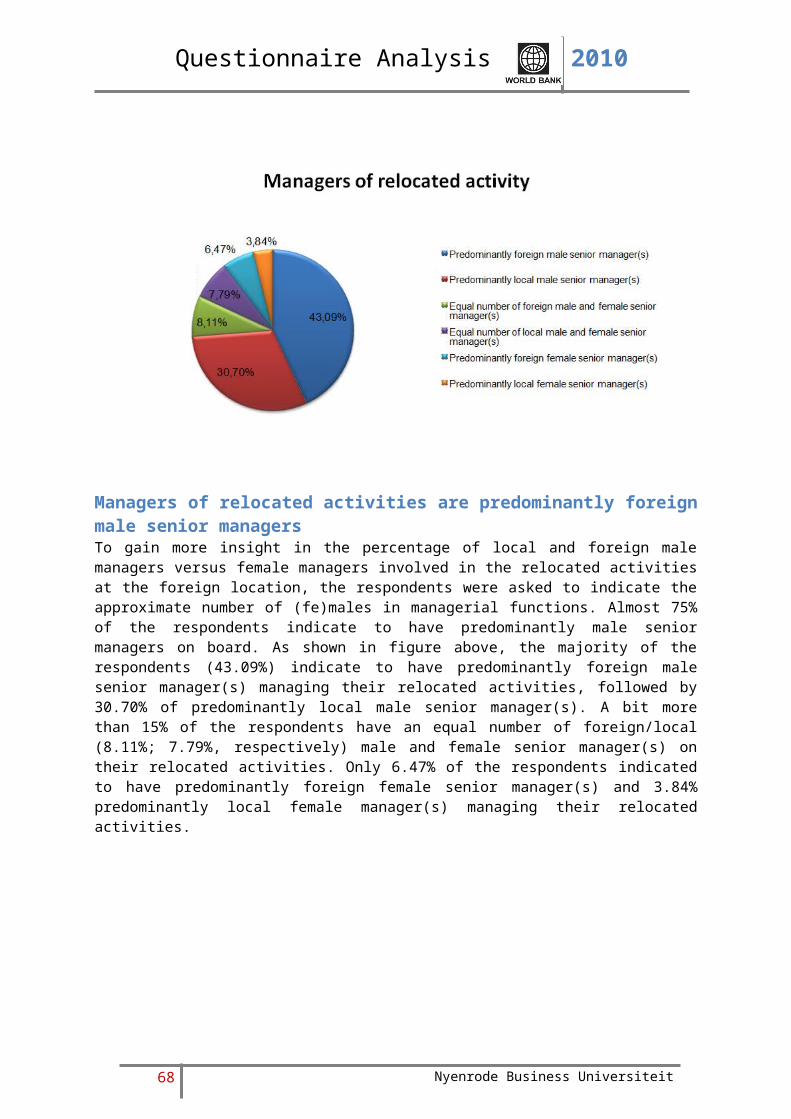

Managers of relocated activities are predominantly foreign male senior managers To gain more insight in the percentage of local and foreign male managers versus female managers involved in the relocated activities at the foreign location, the respondents were asked to indicate the approximate number of (fe)males in managerial functions. Almost 75% of the respondents indicate to have predominantly male senior managers on board. As shown in figure above, the majority of the respondents (43.09%) indicate to have predominantly foreign male senior manager(s) managing their relocated activities, followed by 30.70% of predominantly local male senior manager(s). A bit more than 15% of the respondents have an equal number of foreign/local (8.11%; 7.79%, respectively) male and female senior manager(s) on their relocated activities. Only 6.47% of the respondents indicated to have predominantly foreign female senior manager(s) and 3.84% predominantly local female manager(s) managing their relocated activities.

66 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Predominantly foreign male senior manager(s)

Predominantly foreign female senior manager(s)

Equal number of foreign male and female senior

manager(s)

Predominantly local male senior manager(s)

Predominantly local female senior manager(s)

Equal number of local male and female senior man-

ager(s)

0 5 10 15 20 25 30 35 40

Managers of relocated activity

Trade/investment relations with rest of the worldTrade/investment relations with MENA

Percentage of responses

About 5.27% of respondents have trade/investment relations with MENA and also have predominantly foreign male senior managers managing their relocated activities. Another 2.41% of respondents that have trade/investment relations with MENA region indicated that they have predominantly local male senior managers managing their relocated activities. The figures for other categories are respectively 0.44%, 0.44% and 0.22% for equal number of foreign male and female senior managers, equal number of local male and female senior managers, and predominantly foreign female senior managers managing their relocated activities. None of the respondents that have trade/investment relations with MENA have predominantly local female senior managers managing the relocated activities.The trend is similar for respondents that have foreign trade/investment relations (excluding MENA). Their figures are 37.87%, 28.43%, 7.68%, 7.35%, 6.26%, and 3.62% respectively for predominantly foreign male senior managers, predominantly local male senior managers, equal number of foreign male and female senior managers, equal number of local male and female senior managers, predominantly foreign female senior managers, and predominantly local female senior managers.Therefore, foreign male senior managers are the most preferred while local female senior managers are the least preferred to manage relocated activities.

67 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Predominantly foreign male senior manager(s)

Predominantly foreign female senior manager(s)

Equal number of foreign male and female senior

manager(s)

Predominantly local male senior manager(s)

Predominantly local female senior manager(s)

Equal number of local male and female senior man-

ager(s)

0 20 40 60 80 100

Managers of relocated activity

Trade/investment relations with MENA Trade/investment relations with rest of the world

Percentage of responses

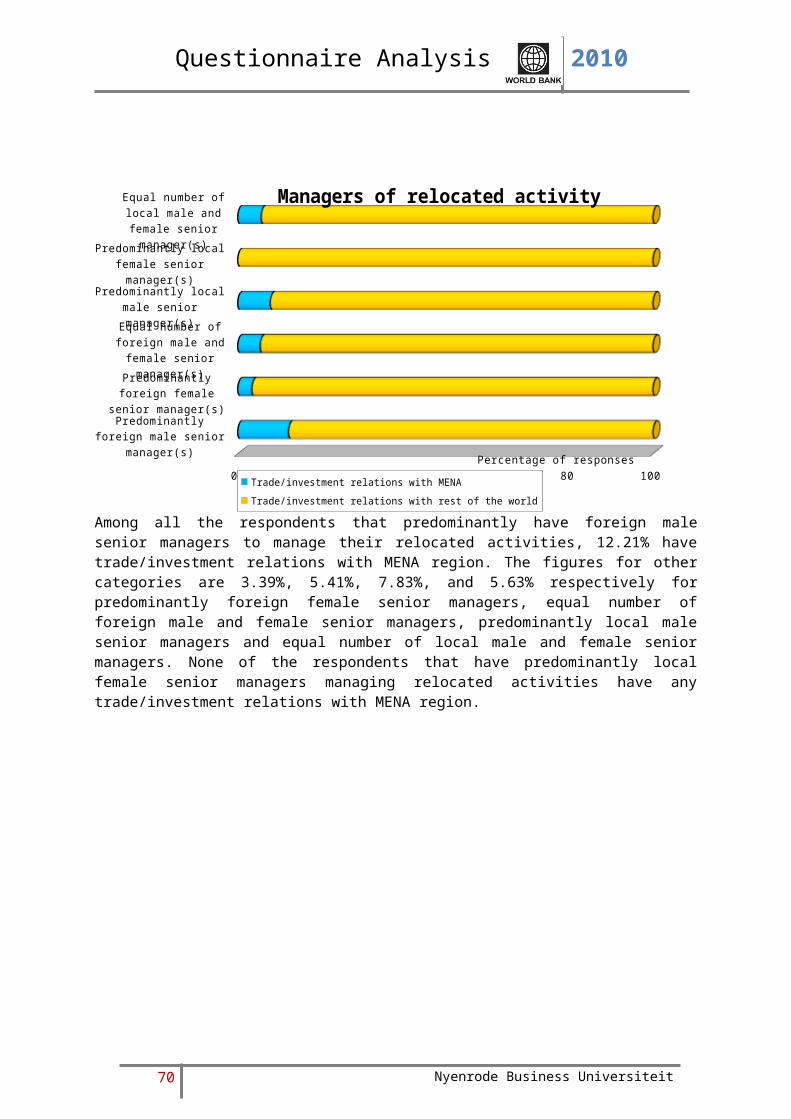

Among all the respondents that predominantly have foreign male senior managers to manage their relocated activities, 12.21% have trade/investment relations with MENA region. The figures for other categories are 3.39%, 5.41%, 7.83%, and 5.63% respectively for predominantly foreign female senior managers, equal number of foreign male and female senior managers, predominantly local male senior managers and equal number of local male and female senior managers. None of the respondents that have predominantly local female senior managers managing relocated activities have any trade/investment relations with MENA region.

68 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Trade/investment relations with

MENA

Trade/investment relations with rest

of the world

0 10 20 30 40 50 60 70 80 90 100

Managers of relocated activity

Predominantly foreign male senior manager(s) Predominantly foreign female senior manager(s)

Equal number of foreign male and female senior manager(s) Predominantly local male senior manager(s)

Predominantly local female senior manager(s) Equal number of local male and female senior manager(s)

Percentage of responses

Among all the respondents that have trade/investment relations with MENA region, 60.00% have indicated that their relocated activities are predominantly managed by foreign male senior manager compared to 41.52% of their peers who have foreign trade/investment relations (excluding MENA). Similarly, for relocated activities predominantly managed by foreign female senior manager the figures are 2.50% against 6.86% for MENA and rest of the world respectively; for relocated activities managed by equal number of foreign male and female senior managers it is 5.00% against 8.42% for MENA and the rest of the world respectively; for relocated activities predominantly managed by local male senior managers it is 27.50% against 31.17% for MENA and rest of the world respectively; for relocated activities predominantly managed by local female senior managers it is 0.00% against 3.97% for MENA and rest of the world respectively; and for equal number of local male and female senior managers it is 5.00% against 8.06% for MENA and rest of the world respectively.

69 Nyenrode Business Universiteit

Questionnaire Analysis 2010

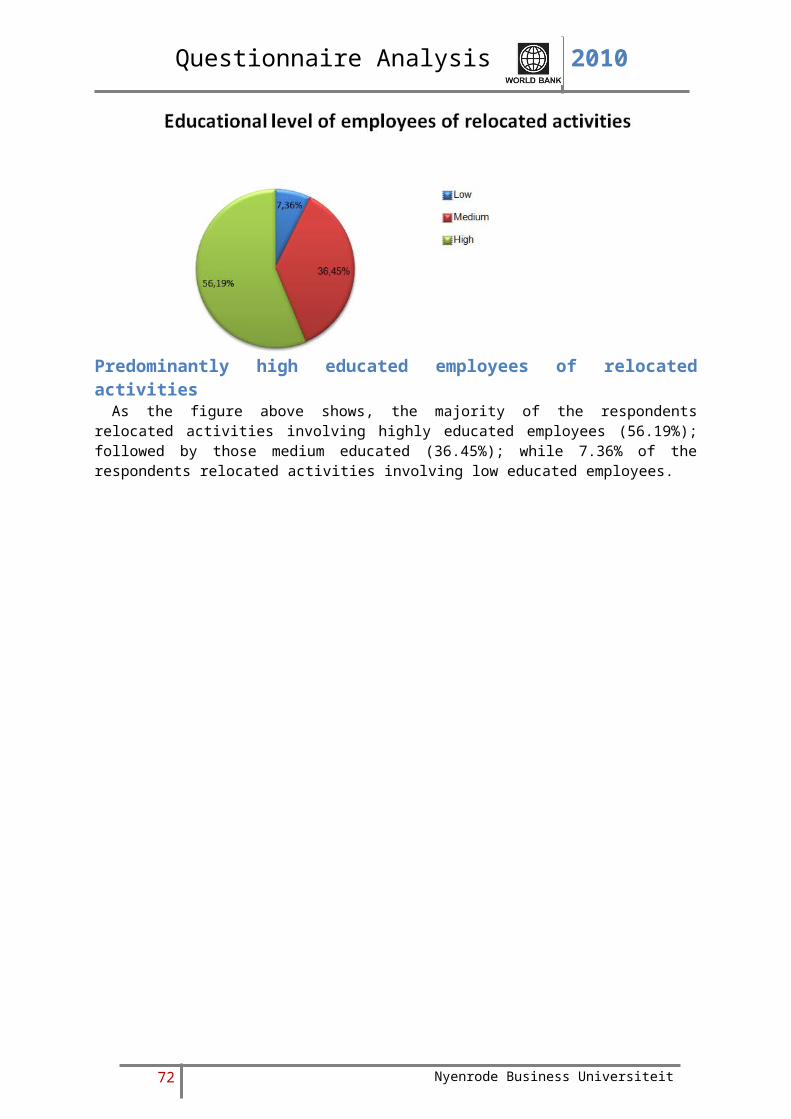

Predominantly high educated employees of relocated activities As the figure above shows, the majority of the respondents relocated activities involving highly educated employees (56.19%); followed by those medium educated (36.45%); while 7.36% of the respondents relocated activities involving low educated employees.

70 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Low

Medium

High

0 10 20 30 40 50 60

Education level of employees involved in relocated activities

Rest of the worldMENA

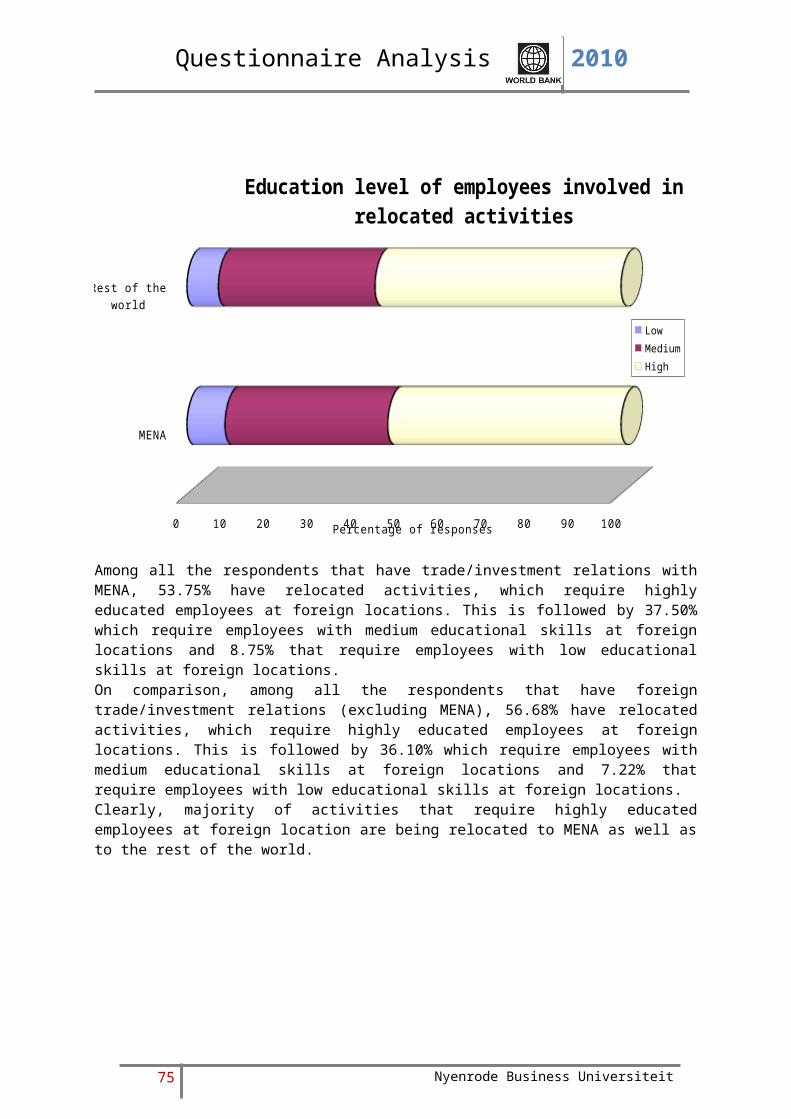

Percentage of responses For about 51.70% of respondents that have foreign trade/investment relations (excluding MENA) and have relocated their activities from the Netherlands, the relocated activities require highly educated employees at foreign location, where as this number is 4.72% for similar category of respondents that have trade/investment relations with MENA. Further, for 32.93% of respondents that have foreign trade/investment relations (excluding MENA) and have relocated their activities from the Netherlands, the relocated activities require employees with medium education skills at foreign location compared to 3.29% for similar category of respondents that have trade/investment relations with MENA. Lastly about 6.59% of respondents that have foreign trade/investment relations (excluding MENA) have relocated activities that require employees with low educational skills at foreign location compared to 0.77% of respondents of similar category but have trade/investment relations with rest of the world.

71 Nyenrode Business Universiteit

Questionnaire Analysis 2010

Low

Medium

High

0 20 40 60 80 100

Education level of employees involved in relocated activities

MENARest of the world

Percentage of responses

Among all the respondents that have relocated activities that require highly educated employees at foreign location, 8.37% have trade/investment relations with MENA. Similarly among all the respondents that have relocated activities that require employees with medium educational skills at foreign location, 9.09% have trade/investment relations with MENA, while the figure is 10.45% for those in the category that requires employees with low educational skills at foreign location.

72 Nyenrode Business Universiteit

Questionnaire Analysis 2010

MENA

Rest of the world

0 10 20 30 40 50 60 70 80 90 100

Education level of employees involved in relocated activities

LowMediumHigh

Percentage of responses