r x working capital and the financing decision xworking capital and the financing decision...

TRANSCRIPT

C H

A P

T E

R

S I X

Working Capital andthe Financing Decision

McGraw-Hill Ryerson ©McGraw-Hill Ryerson Limited 2000

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-1aThe nature of asset growth

A. Stage I: Limited or no Growth

Dollars Temporary current assets

Capital assets

Time period

PPT 6-1

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-1bThe nature of asset growth

B. Stage II: GrowthDollars

Temporary current assets

Capital assets

Time period

Permanentcurrent assets

PPT 6-1

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-1bThe nature of asset growth

B. Stage II: GrowthDollars

Temporary current assets

Capital assets

Time period

Permanentcurrent assets

PPT 6-1

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-2aSales and earnings for McGraw-Hill Ryerson, 1990-1998

0

5000

10000

15000

20000

25000

30000

35000

3rd 90

3rd 91

3rd 92

3rd 93

3rd 94

3rd 95

3rd 96

3rd 97

3rd 98

$ th

ousa

nds

Quarterly salesSources: www.sedar.com www.mcgrawhill.ca Symbol: MHR

PPT 6-2

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-2bSales and earnings for McGraw-Hill Ryerson, 1990-1998

-5000

-4000

-3000

-2000

-1000

0

1000

2000

3000

4000

5000

3rd 9

0

3rd 9

1

3rd 9

2

3rd 9

3

3rd 9

4

3rd 9

5

3rd 9

6

3rd 9

7

3rd 9

8

$ th

ousa

nds

Quarterly earnings

PPT 6-2

Sources: www.sedar.com www.mcgrawhill.ca Symbol: MHR

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

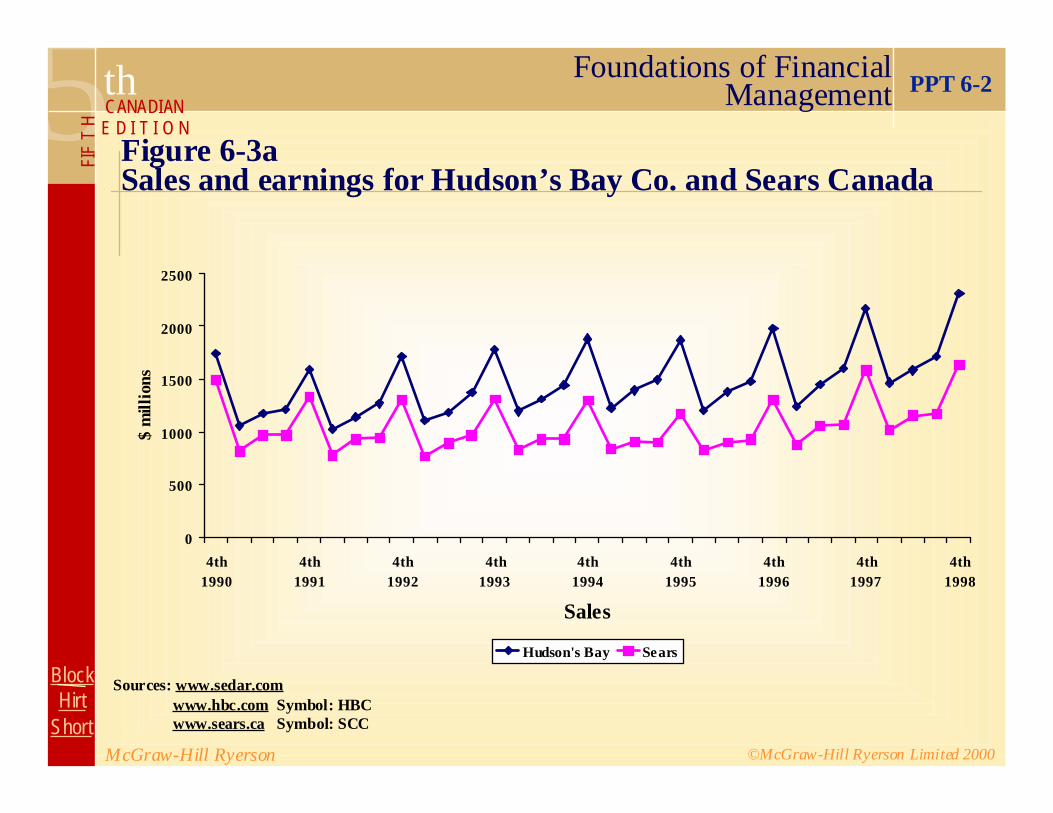

Figure 6-3aSales and earnings for Hudson’s Bay Co. and Sears Canada

0

500

1000

1500

2000

2500

4th1990

4th1991

4th1992

4th1993

4th1994

4th1995

4th1996

4th1997

4th1998

Sales

$ m

illio

ns

Hudson's Bay Sears

PPT 6-2

Sources: www.sedar.com www.hbc.com Symbol: HBC www.sears.ca Symbol: SCC

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-3bSales and earnings for Hudson’s Bay Co. and Sears Canada

-100000

-50000

0

50000

100000

150000

200000

4th199 0

4th199 1

4th199 2

4th199 3

4th199 4

4th199 5

4th199 6

4th199 7

4th199 8

Earnings

$ th

ousa

nds

Hudson's Bay SearsSources: www.sedar.com www.hbc.com Symbol: HBC www.sears.ca Symbol: SCC

PPT 6-2

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Accounts receivable0-30 days31-60 days61-90 days91-120 days

Accounts receivable0-30 days31-60 days61-90 days91-120 days

Materials and serviceSuppliers: accts. payableLabor: wages payableOther: expenses

Materials and serviceSuppliers: accts. payableLabor: wages payableOther: expenses

InventoryFinished GoodsGoods in processRaw materials

InventoryFinished GoodsGoods in processRaw materials

SalesGeographical areaProduct or divisionCustomer type

SalesGeographical areaProduct or divisionCustomer type

CustomersCustomers

Short-term lendersChartered banksNon-bank lendersForeign banks and lenders

Short-term lendersChartered banksNon-bank lendersForeign banks and lenders

Government taxesFederal income taxesProvincial taxesOther taxes

Government taxesFederal income taxesProvincial taxesOther taxes

CashCashMarketable securitiesMarketable securities

Interest and dividends

PPT 6-3

Expanded cash flow cycle

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

1st Quarter 2nd Quarter 3rd Quarter 4th Quarter

October …. 300 January ….. 0 April ….1,000 July ……. 2,000

November ..150 February …. 0 May …..2,000 August ….1,000

December ... 50 March ….. 600 June …..2,000 September ..500

Total sales of 9,600 units at $3,000 each = $28,800,000 in sales.

PPT 6-4

Table 6-1Yawakuzi sales forecast (in units)

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

InventoryProduction (at cost of

Beginning (level Ending $2,000inventory + production) – Sales = inventory per unit)

PPT 6-5

Table 6-2Yawakuzi’s production schedule and inventory

October 800 800 300 1,300 $2,600,000November 1,300 800 150 1,950 3,900,000December 1,950 800 50 2,700 5,400,000January 2,700 800 0 3,500 7,000,000

February 3,500 800 0 4,300 8,600,000March 4,300 800 600 4,500 9,000,000April 4,500 800 1,000 4,300 8,600,000May 4,300 800 2,000 3,100 6,200,000

June 3,100 800 2,000 1,900 3,800,000July 1,900 800 2,000 700 1,400,000August 700 800 1,000 500 1,000,000September 500 800 500 800 1,600,000

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Table 6-3aSales forecast, cash receipts and payments, and cash budget

Oct Nov Dec Jan Feb Mar Apr May June July Aug Sept

Sales (units) 300 150 50 – – 600 1,000 2,000 2,000 2,000 1,000 500

Sales $0.9 $0.45 $0.15 – – $1.8 $3.0 $6.0 $6.0 $6.0 $3.0 $1.5(unit price, $3,000)

Sales Forecast ($ millions)

50% cash .45 $.225 $.075 – – $0.9 $1.5 $3.0 $3.0 $3.0 $1.5 $.7550% cash fromprior month’s sales .75* 0.450 0.225 0.075 – – 0. 9 1.5 3.0 3.0 3.0 1.50

Total cashreceipts $1.20 0.675 $0.300 $0.075 – $0.9 $2.4 $4.5 $6.0 $6.0 $4.5 $2.25

*Assumes September sales of $1.5 million.

Cash Receipts Schedule ($ millions)

PPT 6-6

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Constant productionof 800 units/month(cost $2,000 per unit) $1.6 $1.6 $1.6 $1.6 $1.6 $1.6 $1.6 $1.6 $1.6 $1.6 $1.6 $1.6Overhead .4 .4 .4 .4 .4 .4 .4 .4 .4 .4 .4 .4Dividends & interest – – – – – – – – – – 1.0 –Taxes .3 – – .3 – – .3 – – .3 – –Total cashpayments $2.3 $2.0 $2.0 $2.3 $2.0 $2.0 $2.3 $2.0 $2.0 $2.3 $3.0 $2.0

Cash flow $(1.1) $(1.325) $(1.7) $(2.225) $(2.0) $(1.1) $.1 $2.5 $4.0 $3.7 $1.5 $.25Beginning cash .25† .25 .25 .25 .25 .25 .25 .25 .25 .25 1.1 2.60Cumulativecash balance $(.85) $(1.075) $(1.45) $(1.975) $(1.75) $(.85) $.35 $2.75 $4.25 $3.95 $2.6 $2.85Monthly loanor (repayment) 1.1 1.325 1.7 2.225 2.0 1.1 (0.1) (2.5) (4.0) (2.85) – –Cumulative loan 1.1 2.425 4.125 6.350 8.35 9.45 9.35 6.85 2.85 – – –Ending cash balance .25 .25 .25 .25 .25 .25 .25 .25 .25 1.1 2.6 2.85

Oct Nov Dec Jan Feb Mar Apr May June July Aug Sept

Cash Payments Schedule ($ millions)

Cash Budget ($ millions; required minimum balance is $0.25 million)

PPT 6-6

Table 6-3bSales forecast, cash receipts and payments, and cash budget

†Assumes cash balance of $.25 million at the beginning of October and that this is the desired minimum cash balance.

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Table 6-4Total current assets, first year ($ millions)

Accounts Total CurrentCash Receivable Inventory Assets

October $0.25 $0.450 $2.6 $3.30November 0.25 0.225 3.9 4.375December 0.25 0.075 5.4 5.725

January 0.25 0.00 7.0 7.25February 0.25 0.00 8.6 8.85March 0.25 0.90 9.0 10.15

April 0.25 1.50 8.6 10.35May 0.25 3.00 6.2 9.45June 0.25 3.00 3.8 7.05

July 1.10 3.00 1.4 5.50August 2.60 1.50 1.0 5.10September 2.85 0.75 1.6 5.20

PPT 6-7

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Cash flow $0.25 $(1.1) $(1.325) $(1.7) $(2.225 $(2.0) $(1.1) $0.1 $2.5 $4.0 $3.7 $1.5 $0.25Beginningcash 2.60 2.85 1.75 0.425 0.25 0.25 0.25 0.25 0.25 0.25 0.25 3.7 5.2Cumulative 2.85 1.75 0.425 (1.275) (1.975) (1.75) (0.85) 0.35 2.75 4.25 3.95 5.2 5.45cash balance

Monthly loanor (repayment) – – 1.525 2.225 2.0 1.1 (0.1) (2.5) (4.0) (0.25) – –Cumulative loan – – 1.525 3.750 5.75 6.85 6.75 4.25 0.25 –. – –Ending cashbalance $2.85 $1.75 $0.425 $0.25 $0.25 $0.25 $0.25 $0.25 $0.25 $0.25 $3.70 $5.2 $5.45

Sept Oct Nov Dec Jan Feb Mar Apr May June July Aug Sept

Second YearEnd of

First Year

PPT 6-8

Table 6-5aCash budget and assets for second year with no growth in sales($ millions)

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Sept Oct Nov Dec Jan Feb Mar Apr May June July Aug Sept

Second YearEnd of

First Year

Ending cashbalance $2.85 $1.75 $0.425 $0.25 $0.25 $0.25 $0.25 $0.25 $0.25 $0.25 $3.70 $5.2 $5.45Accountsreceivable 0.75 0.45 0.225 0.075 –. –. 0.95 1.50 3.0 3.0 3.0 1.5 0.75Inventory 1.6 2.6 3.9 5.4 7.0 8.6 9.0 8.6 6.2 3.8 1.4 1.0 1.60Total cur-rent assets $5.2 $4.8 $4.55 $5.725 $7.25 $8.85 $10.15 $10.35 $9.45$7.05 $8.1 $7.7 $7.80

Total Current Assets

PPT 6-8

Table 6-5bCash budget and assets for second year with no growth in sales($ millions)

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-6The nature of asset growth (Yawakuzi)

11

10

9

8

7

6

5

4

3

2

1

O N D J F M A M J J A S O N D J F M A M J J A S

InventoryCash

Cash

Accountsreceivable

Inventory

Totalcurrentassets

Accountsreceivable

Inventory

$ millions

PPT 6-9

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-7Matching long-term and short-term needs

Dollars

Temporary current assets

Capital assets

Time period

Permanentcurrent assets

Short-termfinancing

Long-termfinancing

(debt & equity)

PPT 6-10

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-8Using long-term financing for part of short-term needs

Dollars

Temporary current assets

Capital assets

Time period

Permanentcurrent assets

PPT 6-11

Short-termfinancing

Long-termfinancing

(debt & equity)

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Dollars

Temporary current assets

Capital assets

Time period

Permanentcurrent assets

PPT 6-11

Short-termfinancing

Long-termfinancing

(debt & equity)

Figure 6-9Using short-term financing for part of long-term needs

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-11A. Flat yield curve, March 1999

4.00

5.00

6.00

7.00

8.00

9.00

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16

Years

Per

cent

PPT 6-12

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-11(2)A. Normal yield curve, July 1993

PPT 6-12

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-11(3)C. Inverted yield curve, December 1989

PPT 6-12

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Figure 6-12Long-term and short-term interest rates

PPT 6-13

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Plan A Plan B Part 1. Current assets

Temporary . . . . . . . $250,000 $250,000Permanent . . . . . . . 250,000 250,000 Total current assets . . . 500,000 500,000

Short-term financing (6%). . 500,000 150,000Long-term financing (10%) . 0 350,000

$500,000 $500,000Part 2. Capital assets

Plant and equipment . . . . $100,000 $100,000Long-term financing (10%) . $100,000 $100,000

Part 3. Total financing (summary of parts 1 & 2)Short-term (6%) . . . . . $500,000 $150,000Long-term (10% . . . . . 100,000 450,000

$600,000 $600,000

Table 6-7Alternative financing plans

EDWARDS CORPORATION

PPT 6-14

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Plan A

Table 6-8Impact of financing plans on earnings

Earnings before interest and taxes $200,000Interest (short-term), 6% ×××× $500,000 – 30,000Interest (long-term), 10% ×××× $100,000 – 10,000

Earnings before taxes 160,000Taxes (50%) 80,000

Earnings aftertaxes $ 80,000

Earnings before interest and taxes $200,000Interest (short-term), 6% ×××× $150,000 – 9,000Interest (long-term), 10% ×××× $450,000 – 45,000

Earnings before taxes 146,000Taxes (50%) 73,000

Earnings aftertaxes $ 73,000

Plan B

PPT 6-14

EDWARDS CORPORATION

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

1. Normal Expected higher return Probability of Expectedconditions under Plan A normal conditions outcome

$7,000 ×××× .80 = ++++ $5,600

2. Tight Expected lower return Probability ofmoney under Plan A tight money

($15,000) ×××× .20 = (3,000)

Expected value of return for Plan A versus Plan B = +$2,600

Table 6-9Expected returns under different economic conditions

EDWARDS CORPORATION

PPT 6-15

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

1. Normal Expected higher return Probability of Expectedconditions under Plan A normal conditions outcome

$7,000 ×××× .80 = ++++$5,600

2. Tight Expected lower return Probability ofmoney under Plan A tight money

($50,000) ×××× .20 = (10,000)

Expected value of return for Plan A versus Plan B = ($4,400)

PPT 6-15

EDWARDS CORPORATION

Table 6-10Expected returns for high-risk firm

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Asset Liquidity

Financing Plan Low Liquidity High Liquidity

1 2Short-term High Profit Moderate profit

High risk Moderate risk

3 4Long-term Moderate profit Low profit

Moderate risk Low risk

PPT 6-16

Table 6-11Current asset liquidity and asset financing plan

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Chapter 6 - Outline LT 6-1

• What is Working Capital Management?

• Hedged Approach to Financing

• Short-Term vs. Long-Term Financing

• Term Structure of Interest Rates

• Working Capital Financing Plans

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Working Capital Management LT 6-2

• Working Capital Management is financing and controllingthe current assets of a firm

• Sales growth often leads to a buildup in inventory andaccounts receivable. Firm may require additional externalfinancing

• Crucial to short-term success or failure of a business

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Hedged Approach to Financing

• Match liquidity (life) of your assets to the maturity (term) of yourfinancing

• Means your assets will be generating cash when your liabilities comedue

Balanced FinancingTemporary (seasonal) build-up in inventory and accounts receivable

– finance with trade credit, short-term bank loans, short-term notespayable

Permanent (minimum) levels of inventory, receivables +

Property and equipment, long-term investments

– finance with long-term loans, leases, bonds, capital stock, retainedearnings

LT 6-3

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Short-Term vs. Long-Term Financing LT 6-4

Short-term financing is less expensive but riskier

– lower interest rates

– short-term rates are volatile

– risk of default if sales slow down

– risk that bank may not extend / renew loans

Long-term financing is more expensive but less risky

– usually higher interest rates,

– you may pay interest on funds you don’t always need

– you have capital at all times

Firm must decide the appropriate “mix”

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Term Structure of Interest Rates LT 6-5

• The Term Structure of Interest Rates is also known as theYield Curve

• A graph showing the interest rate for Government ofCanada securities with different maturity dates

• Normally, long-term rates are higher than short-term rates

th5

©McGraw-Hill Ryerson Limited 2000

Foundations of FinancialManagement CANADIAN

E D I T I O N

FIF

T H

McGraw-Hill Ryerson

BlockHirt

Short

Working Capital Financing Plans LT 6-6

A moderate (balanced) firm:

– S/T financing and high liquidity OR

– L/T financing and low liquidity

An aggressive (risky) firm:

– S/T financing and low liquidity

A conservative (safe or cautious) firm:

– L/T financing and high liquidity

Appropriate strategy is determined based on company’stolerance for risk