raise much deeper concerns short yrd. leaked internal emails

TRANSCRIPT

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 1/38

Moxreports .com focuses on reverse engineering the tactics and strategies used by hedge fundsand insiders in the capital markets.

CURRENT STATUS: I am still �ne tuning this upgraded site. Comments and suggestions are welcome [email protected] (HTTPS://MOXREPORTS.COM/20190617-2/)

(/)

SUBSCRIBE(HTTPS://MOXREPORTS.COM/SUBSCRIBE/)

Short YRD. Leaked Internal EmailsRaise Much Deeper Concerns(https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/) JANUARY 31, 2017 | RP

Summary

Shares of YRD have been shunned by traditional China smart money. Outside ownership is dominated bya few US “quant funds” who perform little fundamental research.Existing concerns have weighed on the stock including fraud, an explosion of guaranteed subprime creditexposure and new illegal activities in China.To entice lenders, YRD guarantees deep subprime loans. But YRD’s risk reserve is deeply undercapitalized while deep subprime exposure now exceeds 80%.An unnamed fund affiliated with Chairman quickly dumped nearly all of its YRD shares following the newPRC guidance which made such guarantees illegal.Recently leaked internal emails show that YRD’s Chairman is forcing parent company employees tomake undisclosed USD purchases or be fired.

This article is the opinion of the author. Nothing herein comprises a recommendation to buy or sell anysecurity. The author is short YRD. The author may choose to transact in securities of one or morecompanies mentioned within this article within the next 72 hours. The author has relied upon publiclyavailable information gathered from sources, which are believed to be reliable and has included links tovarious sources of information within this article. However, while the author believes these sources to bereliable, the author provides no guarantee either expressly or implied.Company OverviewName: Yirendai (NYSE:YRD (http://seekingalpha.com/symbol/YRD))

Industry: China P2P lending / finance portal

Market cap: $1.3 billion

Share price: $20

52 week low: $3.35

Options: Liquid calls and puts

Short Thesis:

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 2/38

– Deep subprime overexposure

– Surge in loan fraud

– Undisclosed illegal activities risk in China

– Stock price irregularities / trading activity in the US ADR’s

– Predatory related party transactions benefiting parent company over US investors

PART A: INDUSTRY PREVIEW – P2P IN CHINA IS COMING UNRAVELED (YOU SHOULD HAVEKNOWN BETTER)

In just the last few days, US investors have begun to find out what Chinese investors have known allalong. This information comes from two articles last week in the Wall Street Journal and the Englishlanguage South China Morning Post over the past few days.

As I will show, the problems facing China’s P2P lending space are transparently awful. Investing in thisspace defies commons sense. But as I will show later, the problems specific to YRD are actually evenworsethan the generic problems of the industry as a whole.

Just from a macro common sense perspective it is safe to say this: anyone dumb enough tobe LONG on stocks with heavy exposure to China’s domestic credit markets should probably not bemanaging money. Evidence of China’s “default storm (https://www.bloomberg.com/news/articles/2017-01-19/china-default-storm-brewing-as-record-junk-debt-due-poses-risks)” is said to already beexacerbating a “recent spate of fraud (https://www.bloomberg.com/news/articles/2017-01-25/expect-more-forgeries-fakes-in-china-debt-market-amid-bond-rout?utm_content=buffer692db&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer)” in thecredit markets “amid a rout (http://www.bloomberg.com/news/articles/2016-12-23/china-inc-struggling-to-sell-bonds-poses-quandary-for-economy) that has analysts predicting a record number of defaults(https://www.bloomberg.com/news/articles/2017-01-25/expect-more-forgeries-fakes-in-china-debt-market-amid-bond-rout?utm_content=buffer692db&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer) in2017″. Just look to Bloomberg, the WSJ, the New York Times, or any English language financial newsjournal covering China.

For the most part, larger US investors (and effectively ALL Chinese investors) have shunned YRDsADRs. In terms of outside investors, only a few smaller “quant funds” continue to hold positions. Theseinvestors make their investment decisions based on “factor models” which focus on key headline metricsand NOT based on underlying fundamental research into the company.

The P2P lending space in China is something akin to a Ponzi scheme which is rife with fraud. Thisis NOT an overstatement.

This is why China investors have shunned the space and why Chinese securities regulators have madeP2P IPOs so difficult to achieve in China. The regulators in China seek to protect Chinese investors. Soinstead, these P2P players from China are simply choosing to IPO in the US where various smallerinvestors can be lured into the stock.

YRD initially intended (https://www.bloomberg.com/news/articles/2015-04-15/china-peer-to-peer-lender-yirendai-said-to-plan-300-million-ipo) to raise $300 million in its NYSE IPO. A few months later, the IPOwas only able to raise $75 million at $10. And then, even that tiny IPO traded down(http://www.reuters.com/article/us-yirendai-ipo-idUSKBN0U11X420151218) as much as 16.5% on theday of the IPO.

Seemingly nobody wanted to buy YRD at any price. Within months, the stock traded down to as low as$3.35 in 2016. In the IPO and the aftermarket, YRD has been unable to sustain any substantialinvestment from any major institutions and certainly no smart China money has shown any interest

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 3/38

whatsoever in owning the stock.

During 2016, YRD continued to report loan growth which was downright explosive. (But so did everyother P2P player in China’s rapidly booming P2P space). Accordingly, the headline metrics for YRDlooked temptingly good. YRD appeared to present a low P/E ratio, strong revenue growth, huge returnon equity, etc. This began to attract a number of US quant funds (shown below) to take numerous smallpositions based on their “factor models”.

Here’s where it gets interesting.

At the time of the lows, YRD stock was also supported by undisclosed buying by an unnamed fundaffiliated with YRD Chairman Ning Tang. (Even as no major institutions and certainly no major Chinainvestorshave shown any willingness to own the stock at any price.) The purchases by this unnamedFund would not be disclosed until 6 months later, and in fact the purchases themselves would not evenbe disclosed until well AFTER the Fund had already dumped its shares.

As a result of the quant momentum buying and the purchases by the undisclosed Fund, at one point,shares of YRD had risen by more than 10x from those lows. But they have now begun to falter, Sharesof YRD are now down by around 50% from those highs reached a few months ago, even as loan growthcontinues to soar and presumably YRD’s apparent “profits” continue to get “better and better”. Over thepast few weeks, the share price can’t seem to catch a bid from anywhere. Notably, the unnamed Fundhas already dumped nearly ALL of its shares at higher prices.

However, to keep this in perspective, even at $20 the shares are still up dramatically from the $3 lows in2016.

As I will show below, China’s securities regulators have deliberately made it much tougher for P2Pplayers to IPO in China. They are seeking to protect Chinese investors. As a result, these P2P playerssimply turn to the US capital markets to raise money via IPOs.

Just last week, it was revealed by the English language South China Morning Post(http://www.scmp.com/business/banking-finance/article/2064717/chinese-peer-peer-lender-ppdaicom-planning-us-ipo-likely?utm_content=buffer4c283&utm_medium=social&utm_source=twitter.com&utm_campaign=buffer) thatChinese P2P lender Ppdai.com would also choose to come public in the US. Like YRD, Ppdai’sexpectations are ambitious and it hopes to raise $200 million from US investors. Additional players in theChina P2P space such as Dianrong and China Rapid Finance are also expected to tap the capitalmarkets.

Ahead of the Ppdai IPO, the SCMP article quite clearly comes across as a warning to USinvestors who might be tempted to invest in a Chinese P2P. The SCMP makes clear what Chineseinvestors have known all along. Here are a few quotes from SCMP, which again came out just last week:

– In China, “P2P lending…has been mired in a slew of scandals amid runaway investment and fraudsince late 2015.”

– “Beijing will heighten requirements for P2P players…The intention of the heightened regulation ispartly to shut down some firms that purport to be P2P lenders.”

– “dozens of unscrupulous players raised funds from depositors and then channeled the loans tocorporate clients such as property developers.”

– “In 2015, Beijing-based Ezubao was found to have defrauded more than 1 million investors of about100 billion yuan.”

The SCMP article came out last Monday. By Friday, we had a separate article from the Wall StreetJournal which should serve to further warn US investors about the P2P space in China.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 4/38

A Default in China Spreads Anxiety Among Investors (http://www.wsj.com/articles/a-default-in-china-spreads-anxiety-among-investors-1485513181)

The firm highlighted by the WSJ is Cosun, a Chinese phone maker. Unlike the loans facilitated by YRD(which are effectively consumer to consumer), this was a corporate that had raised the money via P2P.

And the firm that facilitated the loans was Ant Financial, which is owned by giant Alibaba Group(NYSE:BABA (http://seekingalpha.com/symbol/BABA)). In other words, we are NOT talking about asmall time player here. The problems in China’s P2P space have infected every corner of that market.

According to the WSJ, the investment process here is effectively the same as the process used by YRDand every other China P2P player.

A large number of small Chinese retail investors (in this case it was around 13,000 investors) log on withtheir smart phones and opt to make small investments in some sort of P2P loan product. There is noresearchand no due diligence. They just click on their smart phone and then “poof” they haveinvested in something which is supposed to provide some attractive level of returns. Their money istransferred out of their bank account immediately and automatically.

As shown by the WSJ, the default

illustrates a rising risk in China, where hundreds of millions of people seeking higher returns on their savings haveused their mobile phones to buy risky, unregulated investments.

Again, the P2P in this case was backed by China’s Alibaba, perhaps the largest and most prestigiousname in Chinese ADR’s. YRD is certainly in a far lower league than Ant and Alibaba. At its lows lastyear, YRD was worth just $200 million.

And (just like we will see with YRD), the Cosun case looks like it demonstrates a clear example ofoutright fraud being the culprit. Notably, both Chinese and US investors have been victimized.

From the WSJ:

Other businesses owned by Cosun’s founder have faced accusations from U.S. and Hong Kong securitiesregulators that they engaged in dubious accounting. Three of his companies got delisted from stock markets inthe U.S. and Hong Kong. He appears to have never responded to any of the claims.

It sounds like investors should have known better. But with no research being conducted during theirquick smart phone process, this is what happens.

THE POINT:

The point of this so far: Investing in China’s P2P space is just downright dumb. You have alreadybeen explicitly warned by the SCMP and the WSJ. Chinese equity investors and regulators haveknown this all along. This is why the P2P players are dumping these ADR’s on US investors.

As we will see, the specifics as they apply to YRD are even worse.

PART B: SUMMARY OF YRD SPECIFICALLY

I have spent much of my adult life living, working and traveling in China. I studied Chinese at PekingUniversity, which the Chinese often refer to as the “Harvard of China”. When in China, I spend most ofmy time in Beijing and I have often invested long and short in US listed Chinese stocks following mycareer as an investment banker in Hong Kong and New York.

There are certainly a few interesting US listed Chinese ADR picks. But as I’m going to show today,Chinese P2P lender Yirendai is actually a compelling short.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 5/38

The last two problematic Chinese ADR’s I exposed fell by 50-90%.

Additional Chinese stocks I have exposed were subsequently delisted or became the subject of SECinvestigations.

To fully understand the depth of the problems at YRD, there are a wide variety of points to be made.Some are very severe and urgent. Some are more along the level of just disturbing trends which aresharply worsening over time. For the sake of completeness, I am going to address all of these pointsand let the reader figure out which ones mean the most to them according to their own perspective.

PLEASE NOTE:

TO UNDERSTAND HOW EACH OF THESE PIECES FIT TOGETHER, IT IS IMPORTANT TO READTHIS ENTIRE ARTICLE. THE POINTS I MAKE ARE DELIBERATELY PRESENTED IN ORDER OFINCREASING SEVERITY.

At the end of this article, I will show an internal email from YRD’s Chairman Ning Tang to his employeesat YRD parent Credit Ease which were posted on a site in China. According to those postings,effectively he is requiring employees to contribute their own personal money (required to be made in USdollars) into a fund which is buying “undisclosed” US equities (presumably shares of YRD). The orderfrom Ning Tang is mandatory and he makes it clear that anyone who doesn’t personally buy into this isthreatened with immediate dismissal. Yeah, it’s that bad.

I will also show how an undisclosed and unnamed “affiliated fund” of Ning Tang was aggressively buyingshares of YRD at the lows last year, but then dumped effectively all of its shares right as newregulations loan guarantees (such as those by YRD) are in fact illegal. That fund dumped at prices wellabove current levels.

As a preview, here are the points which will be elaborated and substantiated below:

None of the usual China “smart money” (i.e. funds like Sequoia, Matrix, etc. ) are willing to invest anythingin YRD. YRD’s Chairman still owns a large indirect stake in YRD, but other members ofYRD management refuse to own any shares whatsoever. As I will show below, the reasons for this willbecome blatantly obvious.Outside holders are primarily US based low fee quant funds who have made their investment selectionsbased on superficial analysis of basic equity metrics such as stated “EPS growth”, stated “book value”and stated “gross profitability”.These metrics, which appear to be positive on the surface, are only made possible by virtue of YRDproviding a credit guarantee (which has recently been deemed illegal in China). Investors are clearly notpricing in the now extreme subprime credit risk. They have also not appreciated what will happen toYRD’s metrics when the now-illegal credit guaranteedisappears (which it is about to).US listed YRD was actually spun out of parent company Credit Ease. Credit Ease originates fully 67% ofYRD’s loans and takes a flat cut out as an origination fee. Credit Ease therefore receives substantialincome with zero risk. By virtue of the guarantee, US investors in YRD bear all of the risk associated withthe loans. It is a massive related party transaction which benefits the parent company over USshareholders.YRD maintains the loans for the P2P investors. Because YRD guarantees the loans, Chinese retailinvestors (P2P lenders) accept a very low rate of return and YRD enjoys very high income (in the shortterm) while loan growth continues to be strong (in the short term).YRD (the entity sold to US investors) is actually a dumping ground for deep subprime loans for parentCredit Ease. As a result, YRD has dramatically altered its business model. YRD has gone from makingmostly prime “A Grade” loans in 2013 to almost exclusivelymaking deep subprime “D Grade”loans with APRs up to 40%. Default rates for C and D loans are already soaring by far more thanexpected. But (even more troubling) even the “prime” “Grade A” charge off rates haveskyrocketed from 2% to 9%.Given the level of distress in “A Grade” loans, we can assume the “D Grade” loans are going to beexponentially worse. And deep subprime “D Grade” loans now compriseover 80% of new loans !In reporting “delinquent loans”, YRD cherry picks the 15-89 day past due metric which it cites as just1.9%. But this is largely irrelevant since the defaults tend to occur after 89 days, as we can see.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 6/38

Defaults beyond 90 days can be seen to be clearly much higher. (YRD’s highlighted metrics cantherefore be filed under #AlternativeFacts)YRD pretends to have its own sophisticated credit scoring system. But the reality is that there is nonational FICO system in China. YRD approves loans to deep subprime “D Grade” credits within just 10minutes with minimal credit checks in an application process completed on a smart phone. YRDallows borrowers to “self declare” their use of proceeds.In the past two quarters, YRD was forced to disclose the impact of significant “organized loan fraud”affecting already approved borrowers totaling over RMB81 million. After their initial discovery, thesefraud amounts were larger than originally assumed and YRD was forced to write off 100% of the amountsin question.In addition, the only “risk reserve fund” established to back these loans is deeply undercapitalized.But it gets better. These loan guarantees made by YRD for P2P loans have been made illegal undernew regulations in China. Despite the new ruling, YRD continues to offer guarantees, simply because itmust. I do NOT expect to see YRD get hit by any massive penalties in China in connection with illegalloan guarantees. Instead, YRD will simply be forced to stop offering the guarantee.But without such a guarantee, YRD will be forced to give investors a dramatically higherpayout, crushing its heretofore attractive “metrics” of both profitability AND growth. The US based quantguys who own YRD ADRs clearly haven’t figured this out. (…yet.)The new regulations also prohibit ties to asset management activities. Yet YRD is clearly tied to assetmanagement firm Toumi. In fact, I will reveal leaked internal emails below which show that YRD’sChairman is forcing employees of YRD’s parent to personally invest their own money, SPECIFICALLY INUS DOLLARS into the Toumi asset management platform be for the purpose of driving money into someunnamed US dollar stock. Employees who don’t comply and contribute their personal money to thisinvestment scheme will be fired ! (Note that the only US dollar stock connected to the Chairman happensto be YRD).Prior to the compulsory Toumi investment, I will also show how an unnamed fundaffiliated withChairman Ning Tang was aggressively making undisclosed purchases of YRD ADRs last year, pushingup the share price when it was struggling. The fund then immediately began dumping effectively all of itsshares of YRD just as the government announcement about illegal loan guarantees came out. Nodisclosure of the purchases was made until after the shares had already been dumped.

PART C: BACKGROUND

Following my exposé (http://seekingalpha.com/article/3109346-airmedia-doubles-on-misleading-investment-transaction) of Chinese advertising company Air Media (NASDAQ:AMCN(http://seekingalpha.com/symbol/AMCN)) that stock ended up falling by around 50%. Air Media hadtouted that it was being bought up by an outside 3rd party, causing the stock to more than double. Thesuckers were largely US investors who didn’t do their research in Chinese.

But once I posted the Chinese language documents online (along with English translations), we couldsee that the transaction was just a sham. The stock returned to its pre-hype lows.

But that one was pretty easy.

Other China trades were actually a lot more interesting.

In the past I had highlighted (http://seekingalpha.com/article/2062403-sungy-mobile-set-to-burn-u-s-investors) a US listed Chinese ADR called Sungy Mobile (NASDAQ:GOMO(http://seekingalpha.com/symbol/GOMO)), which then fell by as much as 90%.

Sungy came public (http://www.nasdaq.com/markets/ipos/company/sungy-mobile-ltd-918355-73782) ata price of $11.22. It then quickly soared to around $30, giving it a market cap of well over $1 billion. Theunderwriter on Sungy’s IPO was Credit Suisse, who continued to tout the stock with a $34 target. Thecompany lacked much by way of current financial results, but CS was predicting transformative growthwhich would presumably justify the lofty valuation.

When I first raised the alarm on Sungy, the stock was still sitting at around $28. I illustrated clearly thatSungy’s underlying “product” was not in any way commercially viable. The “product” consisted of variousapp downloads for one’s phone such as ways to customize the background wallpaper. Yes, it was really

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 7/38

that bad. Sungy also had document reader app, which primarily competed with free offerings fromsoftware providers. Again, it was a pretty much nonsense of a product and it seemed hard to believethat anyone would fall for it. But there were a few buyers of the stock following the IPO. Ongoing supportfrom the sell side and macro bullishness towards China elevated the stock price to irrational levels. Inhindsight, it was obvious. (But then again, it is always obvious in hindsight….)

Following my article, Sungy began a rapid and steady downward trajectory, quickly hitting $12. Theimplosion picked up speed when each new deeply disappointing quarter showed that failure wasinevitable.

The decline picked up even more speed and soon Sungy was down to $2-3. At this time, Sungymanagement simply took the company private, buying back all of the shares at around $5. It was quite anice scam. Sell the shares to US investors at $11.22 and then buy them all back a $5 a little while later,keeping all of the cash and the remains of the businesses.

As we can see, Sungy isn’t the only Chinese company to foist a bad businesses upon unsuspecting USinvestors.

PART D: OVERVIEW ON YRD’S P2P LENDING ACTIVITIES

Yirendai (“YRD”) is a Chinese P2P lender, analogous to Lending Club (NYSE:LC(http://seekingalpha.com/symbol/LC)) in the US.

Like YRD, Lending Club initially saw its day in the sun as investors flocked to the novel idea of P2Plending. But then a series of shady activities by management (originating undisclosed loans toemployees to boost volume) along with revelations of very bad risk management sent the stock down byaround 80% from $25.00 to around $5.00.

This is exactly what we will see with YRD. Keep in mind that loan volume has continued to growstrongly at Lending Club, just like it has at YRD. But apparently originating more and more bad loansis not something that ultimately supports a strong share price.

It did not take long for Lending Club to fall by 80%.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 8/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858591700498307_origin.png)

Like Lending Club, YRD simply acts as a middle man. YRD connects willing retail investors (lenders) inChina to willing borrowers in China. The lenders make loans to the borrowers via YRD’s platform andYRD sits in the middle and collects a spread.

In China, the growth of P2P lending continues at a torrid pace as small loan investors (lenders) continueto seek decent returns on small amounts of cash while consumers have shown they will continue topay APR’s of up to 40% to take on loans which are becoming well beyond their financial means. Inmany cases, these the purpose of these loans is just to pay for consumer luxuries like cosmetic surgeryor expensive vacations.

Along with the boom in P2P in China, there are a number of emerging concerns about the industry.

Keep in mind that such easy credit was not available in China during the global credit implosion of 2008-2009. Much of the reason that China stayed strong and stable following that US led crisis was thatChinese consumers had very little debt and lots of cash.

This arrival of unchecked easy credit in China is a new phenomenon which has largely beenushered in by P2P lending.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 9/38

In August of 2016, Guo Guangchang, Chairman of Fosun International, told Bloomberg News thatChina’s peer-to-peer lending industry is “basically a scam(https://www.bloomberg.com/news/articles/2016-08-31/china-s-p2p-industry-is-basically-a-scam-billionaire-guo-says),” arguing that players in the multi-billion dollar sector, troubled by collapses andfrauds, lack the ability to price risk.”

In December 2015, the country’s biggest Ponzi scheme(https://www.bloomberg.com/news/articles/2016-08-31/china-s-p2p-industry-is-basically-a-scam-billionaire-guo-says) was exposed after Internet lender Ezubo allegedly defrauded more than 900,000people out of the equivalent of $7.6 billion. China has 1,778 “problematic” online lenders, according tothe banking regulator.”

And the stories continue to get more bizarre. Even last month (December 2016), Chinese regulatorscontinued to raise concerns about other P2P abuses such as lenders requiring young girls tosend naked “selfies (http://www.ibtimes.co.uk/naked-selfies-women-used-collateral-online-loans-china-1595188)” of themselves in order to receive P2P loans. Once they obtained the naked photos, thelenders then extorted the young women, threatening to publish the photos online.

The picture that quickly emerges of China’s P2P industry is one of a financial “wild west” which lackssufficient regulations, controls and protections. In the absence of appropriate regulations, some P2Plenders have shown explosive growth via the use of deeply reckless practices.

(Think back to 2007 in the US when anyone involved in the mortgage industry was making a fortune bysigning up volumes of new borrowers who clearly had zero ability to repay what they were borrowing.)

And now the situation in China P2P is actually changing, both from the industry side and from the side ofthe capital markets.

On the capital markets side, we can see from October 2016 that P2P players who want to go public arenow less able to do so in China. They are being forced to sell their shares into foreign markets ratherthan to Chinese investors:

Due to regulators issuing stricter rules on online lending in October, A-shares are no longer considered favorablefor P2P IPOs, likely driving P2P companies to list overseas.

In other words, because China’s regulators have determined that P2P companies are not suitablefor Chinese investors, these companies are simply turning around and selling shares to USinvestors.

Keep in mind that over the past few years, many US listed Chinese companies actually took theircompanies private, LEAVING the US capital markets to get a much higher valuation by listing in China.But for the problematic companies that can’t list in China, deep pocketed US investors remain as aviable alternative. Valuation is simply not relevant. Completing the IPO at any price is all that matters.

As we will see, this is one clear reason why we see none of the usual “China Smart Money” involved inYRD. It also likely explains why we do not see any ownership by YRD management outside of founderNing Tang’s legacy position.

This will be illustrated more clearly below.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 10/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-1485859244059639_origin.png)

PART E: WHO DOES OWN SHARES OF YRD ? WHO DOESN’T OWN SHARES OF YRD ?

Both of the questions above are equally important.

First, let’s look at insiders.

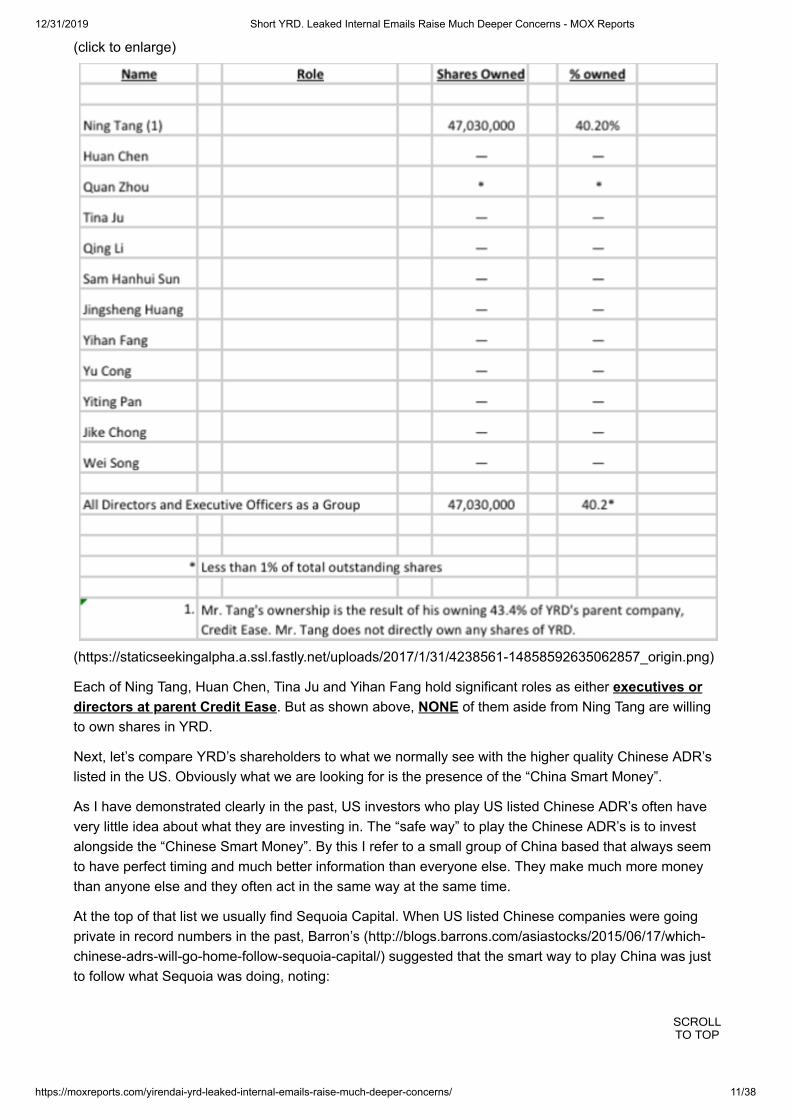

From YRD’s 20F, filed in April 2016. We can see founder and Chairman Ning Tang owns 40.2% of YRD.This stake is owned indirectly because the shares are actually owned by Credit Ease, which is YRD’sparent company. Ning Tang is founder, Chairman and CEO of Credit Ease and via that ownership, heindirectly owns the shares of YRD. Ning Tang does not directly own any shares of YRD.

As described in a section below, Tang’s ownership then increased and decreased slightly as an“affiliated Fund” bought shares and then later sold them.

As we can see, from the 20F (http://www.secinfo.com/d12TC3.w2u6g.htm#1stPage) filed in 2016, noother member of management is willing to own shares in YRD.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 11/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858592635062857_origin.png)

Each of Ning Tang, Huan Chen, Tina Ju and Yihan Fang hold significant roles as either executives ordirectors at parent Credit Ease. But as shown above, NONE of them aside from Ning Tang are willingto own shares in YRD.

Next, let’s compare YRD’s shareholders to what we normally see with the higher quality Chinese ADR’slisted in the US. Obviously what we are looking for is the presence of the “China Smart Money”.

As I have demonstrated clearly in the past, US investors who play US listed Chinese ADR’s often havevery little idea about what they are investing in. The “safe way” to play the Chinese ADR’s is to investalongside the “Chinese Smart Money”. By this I refer to a small group of China based that always seemto have perfect timing and much better information than everyone else. They make much more moneythan anyone else and they often act in the same way at the same time.

At the top of that list we usually find Sequoia Capital. When US listed Chinese companies were goingprivate in record numbers in the past, Barron’s (http://blogs.barrons.com/asiastocks/2015/06/17/which-chinese-adrs-will-go-home-follow-sequoia-capital/) suggested that the smart way to play China was justto follow what Sequoia was doing, noting:

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 12/38

The venture capital owns 16.1% of cosmetics e-commerce Jumei (NYSE:JMEI(http://seekingalpha.com/symbol/JMEI)), 14.6% of wealth management service provider Noah Wealth(NYSE:NOAH (http://seekingalpha.com/symbol/NOAH)), 10.7% of China’s Craigslist 500.com (NYSE:WBAI(http://seekingalpha.com/symbol/WBAI)), 7.5% of online travel agent Tuniu (NASDAQ:TOUR(http://seekingalpha.com/symbol/TOUR)), 4.9% of mobile social media (mostly for dating) Momo(NASDAQ:MOMO (http://seekingalpha.com/symbol/MOMO)) and 4.2% of Ski-mobi (NASDAQ:MOBI(http://seekingalpha.com/symbol/MOBI)), a mobile app organizer.

The other “usual suspects” in China, such as Matrix, IDG, Shunwei and CITIC are also present in manyof the most notable Chinese ADR’s.

So what do we see in YRD ?

Here is the most recent list of top outside investors in YRD.

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858593766097114_origin.png)

Here are the things that should stick out to you.

#1 – Precisely none of the usual “China Smart Money” have any interest in owning YRD. That’s a badsign for YRD. Ordinarily one would expect to see several of the top China funds invested in such a USlisted China ADR.

#2 – There are no funds whatsoever that have taken any substantial portion of YRD (i.e. absolutely nooutside 5% holders)

#3 – No fund listed has a significant portion of their fund invested in YRD

#4 – The few funds that do hold positions in YRD are clearly “quant funds”

Items #1-#3 above speak for themselves. No one in China or outside of China has been attracted tomake any significant investment in YRD in meaningful size.

But item #4 (the involvement of quant funds) requires a closer look.

The list above shows that the largest investors in YRD includes: AJO, Numeric Investors, Acadian andNepsis. As can be seen from each of their websites, these are clearly “quant funds”.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 13/38

For example, on its website, AJO notes that:

Because the market is complex, opportunities are best exploited with a systematic, quantitative approach. We usemodern investment technology and academic research to complement the wisdom of classical investment thinkingand analysis.

AJO manages (http://www.secinfo.com/dutpf.w1d.htm#1stPage) around $24 billion andtypically chargesfees (http://www.ajopartners.com/pricing/)of just 30-60 basis points.

My point (as I see it) is that quant funds tend to be diversified investors which charge low fees.As a result, they cannot afford to do deep research on each of the names they invest in. This iswhy they have no idea about the problems that I am unveiling today.

Here we can see the various “factors” that have likely led this type of quant fund to invest in somethinglike YRD. The following comes from AJOs website.

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858595176208372_origin.png)

Looking at the “factors” above, it now becomes clear why a presumably smart quant fund like AJO wouldinvest in something as awful as YRD.

Yes, YRD shows strong revenue growth with a strong emerging “trend” (on the surface).

Yes, YRD appears to have strong insider ownership (on the surface).

Yes, YRD appears to show strong profitability (on the surface).

Etc. Etc. Etc.

The reality is that if a bunch of smart guys at a fund like AJO consistently pick the right factors, then overtime they will likely have better than average returns across their large and well diversified portfolio. Butonce in while they are going to have individual positions (such as YRD) that get obliterated because

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 14/38

investing blindly in the superficial numbers will often not reveal deeper underlying problems that arefound through in-depth research on a single name.

PART F: SO HERE’S WHERE QUANT INVESTING GOES WRONG

(Note that YRD deliberately cherry picks the 15-89 day delinquency rate as a proxy for bad loans. YRDdiscloses this metric at just 1.9%. I view this as an example of #AlternativeFacts. The data from thissection below are taken directly from other disclosures by YRD. Even a cursory analysis of thedisclosure shows that the situation with its subprime loans is quickly imploding from quarter to quarter.But as I see it, the low fee quant investors simply do not have the incentive structure in place to meritconducting this type of analysis.)

YRD has switched from making “prime” loans to almost exclusively making very deep“subprime” loans.

When YRD first began making loans in 2013, it was making fully 100% of them to “A Grade” loans. Thiscreated several difficult constraints for the company.

First, the size of the pool of total borrowers who are “A Grade” is much smaller than the overall marketof lower credit borrowers.

Second, “A Grade” borrowers don’t really have the need to borrow small amounts of money fordiscretionary purchases (after all, that’s why they are “A Grade” borrowers….). So their demand forloans is quite small.

Third, “A Grade” borrowers have plenty of other credit optionsavailable to them, such that one canonly charge them a much lower rate of interest at up to 17% at best. But keep in mind that much of that17% goes to the actual end investor (the lender on the YRD platform). YRD keeps only a portion of thisas a fee. For “A credit loans”, the fee to YRD amounts to just 5.6%.

As a result of these issues, YRD was initially only able to generate a small volume of loans and was onlyable generate a very low level of return. In fact, because of the low 5.6% fee level, YRD disclosed that:

Grade A loans have an average transaction fee rate of 5.6%,which is lower than the average transaction fee ratesfor our other grades of loans, any failure to achieve a low default rate for our Grade A loans will diminish ourprofit margin and may even cause us to incur losses. Historically, Grade A loans have been unprofitable.

Clearly there was only one solution: Switch to subprime lending

YRD continues to disclose (http://www.secinfo.com/d12TC3.w2u6g.htm#ke3o) that it only lends to“prime” borrowers. But this is quite provably not the case. The overwhelming majority of new loans arebeing made to borrowers with “D Grade” credits and where APR’s run as high as 39.5%. This is quiteobviously deep into subprime territory; there is nothing remotely “prime” about a short term loan with a39.5% APR.

Starting in 2013, YRD was making 100% of its loans to “A Grade” borrowers. But by 2015, more than80% of these borrowers were now “D Grade” credits.

The reason is obvious. “D Grade” borrowers pay up to 39.5% APR on their loans. This allows YRD tokeep a much higher spread of 28.2% on these loans. In other words, YRD makes around 5x as muchon “D Grade” loans as it does on “A Grade” loans. It also helps that the total demand for “D Grade” ismultiples higher than the tiny demand for “A Grade”.

The result is that with subprime YRD switched into a massively larger targetmarket whose profitability is 5x higher.

And then YRD went even further:

YRDimplemented (http://www.secinfo.com/d12TC3.w2u6g.htm#ke3o):

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 15/38

· accelerated approvals (…bad)

· for subprime borrowers (…even worse)

· with even fewer credit checks (…catastrophic)

YRD disclosed:

FastTrack Loan Products

FastTrack loans are a new, fast expanding product that is currently only available through our mobile applications.These loans can be as large as RMB100,000 (US$15,437).

In 2014 and 2015, the average FastTrack loan amounts were RMB36,328 and RMB39,458 (US$6,091.3),respectively.

To apply for a FastTrack loan, a borrower completes an online application providing their PRC identity cardinformation, e-commerce account information, mobile phone number and a credit card statement as well as thedesired loan amount and duration. This product offers near instantaneous credit approval, allowing qualifiedborrowers to receive an initial decision in as fast as ten minutes.

Fast track is important because it means the following (in contrast to traditional P2P loans):

No verification of incomeNo verification of bank statementsRelies only on ecommerce statements and credit card statementsApproval in as fast as 10 minutes via smartphone

But how to entice lenders to lend to such visibly weak credits ?

Clearly lending to a Fast Track “D Grade” credit is a much different proposition that lending to an “AGrade” borrower. As a result, many investors on YRD’s platform would likely be unwilling to lend at all.Those that are willing to lend would demand a much higher rate of return.

YRD came up with a simple solution: provide a guarantee to investors that they will get their interestand principal repaid.

Even in years past, P2P lenders in China were not really supposed to be providing guarantees tolenders. As a result, YRD discloses to US shareholders that it does not provide guarantees on interestor principal. But in the past, it hadn’t really been codified into law during the nascent phase of P2Pdevelopment.

Yet in the lending contract which it provides to lenders in China, we can see quite clearly that aguarantee is explicitly part of the lending contract. (See specifically clause 2.4(https://www.yirendai.com/entry/agreement/2195.html)).

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858596292495756_origin.png)SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 16/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858596471408548_origin.png)

The existence of an explicit guarantee should also be 100% obviousjust by looking at the rates thatYRD offers to lenders. This part requires no translation as the meaning is universal in any language.

From the following table, we can see that the rate lenders receive is identical regardless of whether theloan is being made to an “A Grade” credit or to a “D Grade” credit. The only variability shown in the ratesis due to differences in maturity of the loan, where longer dated loans bear a slightly higher rate ofinterest (regardless of credit quality).

The following table comes from page 57 of the 20F.

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-148585969491551_origin.png)SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 17/38

The only reason that investors are willing to accept the same rate of return regardless of credit quality isthat the loan is guaranteed. Duh !This is basic finance 101 which should be obvious to any undergradbusiness major.

The table below shows the explosion of loans and apparent short term revenues and profits thatoccurred once YRD switched from prime “A Grade” loans to deep subprime “D Grade” loanswith guarantees.

FY 2013 FY 2015 IncreaseYRD LoanVolume

$42.7 million $1.5 billion 35x

YRD Revenue $3.1 million $209 million 67xYRD Net Income ($8.3 million) loss $43.8 millionAnd in fact, the explosion in deep subprime loans has continued even through Q3 2016. More than 80%of loans continue to be made to “Grade D” borrowers.

But here are the two critical problems with providing loan guarantees

Problem #1 – Loan defaults are soaring and the “risk reserve fund” is deeply under capitalized

The actual amount of the risk reserve fund is not exactly clear because YRD has made contradictorydisclosures in recent earnings calls.

On the Q3 call, YRD noted that:

As of September 30, 2016, the outstanding balance of liabilities from risk reserves fund guarantee is at 7.6% of theremaining principal of performing loans covered by risk reserve fund, up from 7.2% in Q2 2016

But this doesn’t match what was said on the Q2 call:

As of June 30, 2016, the outstanding balance of liabilities from risk reserve fund guarantee is at 6.7% of remainingprincipal of performing loans, up from 6.5% in Q1 2016.

The fact that these numbers are changing (for the worse) after the fact is obviously problematic. But theprecise number isn’t what’s important. What matters is that the number is apparently around 7%, whichis far too low given the soaring rate of “charge off’s”.

Anyone who actually cares can see that “charge offs” are accelerating at a much faster rate – EVENAMONG “PRIME” LOANS WHICH ARE DEEMED TO BE “A CREDITS” !

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 18/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858597478608444_origin.png)

If we look at loans by age, “A Grade” loans which are around 3 years old are now being charged off at arate of 9%. And that is for the highest credit loans on the book !

It is unquestionable that we are going to see much higher loan charge off rates for deep subprime“Grade D” loans which now comprise more than 80% of all new loans.

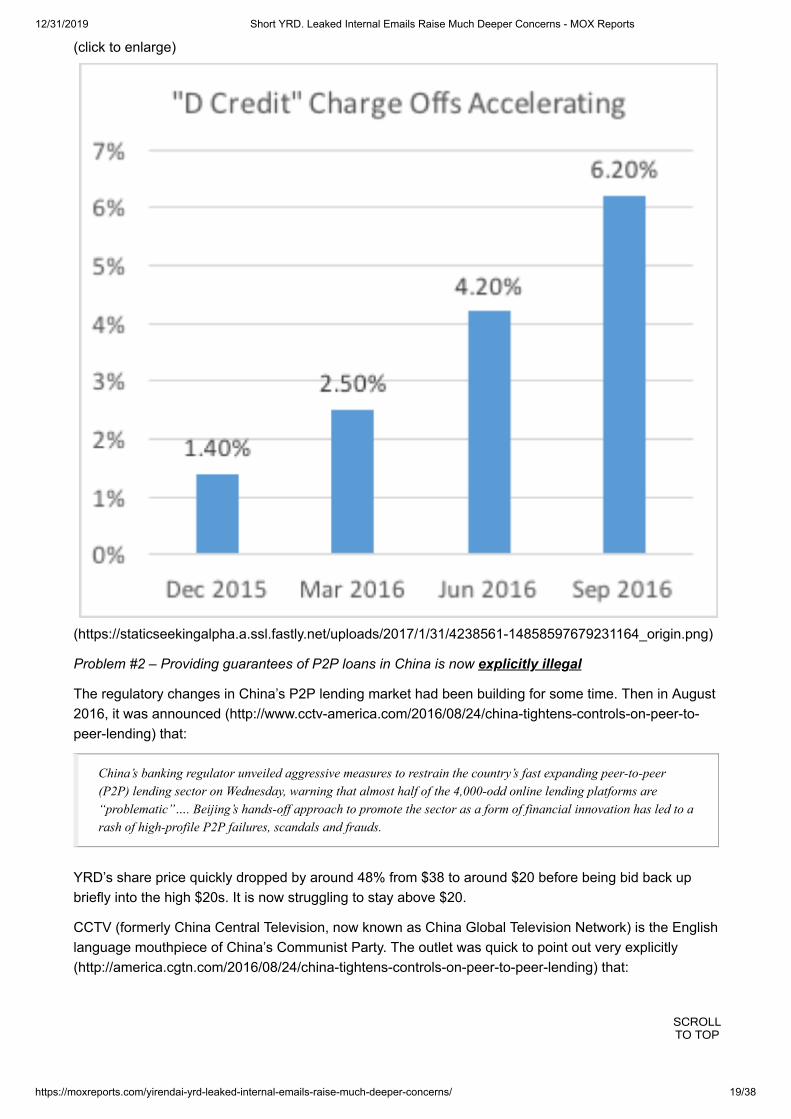

“D Grade” loans are a much newer product so there is far less historical data. We can see the charge offrates accelerating dramatically over the period of just several months.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 19/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858597679231164_origin.png)

Problem #2 – Providing guarantees of P2P loans in China is now explicitly illegal

The regulatory changes in China’s P2P lending market had been building for some time. Then in August2016, it was announced (http://www.cctv-america.com/2016/08/24/china-tightens-controls-on-peer-to-peer-lending) that:

China’s banking regulator unveiled aggressive measures to restrain the country’s fast expanding peer-to-peer(P2P) lending sector on Wednesday, warning that almost half of the 4,000-odd online lending platforms are“problematic”…. Beijing’s hands-off approach to promote the sector as a form of financial innovation has led to arash of high-profile P2P failures, scandals and frauds.

YRD’s share price quickly dropped by around 48% from $38 to around $20 before being bid back upbriefly into the high $20s. It is now struggling to stay above $20.

CCTV (formerly China Central Television, now known as China Global Television Network) is the Englishlanguage mouthpiece of China’s Communist Party. The outlet was quick to point out very explicitly(http://america.cgtn.com/2016/08/24/china-tightens-controls-on-peer-to-peer-lending) that:

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 20/38

The regulations also ban P2P firms from providing guarantees for investment principal or returns, a commonmarketing practice to lure funds from unsophisticated retail investors.

“Investors must understand they need to bear the risks for their investments, no matter big or small,” said Li fromthe CBRC.

These are not deposits. So we are telling P2P investors: P2P is risky, investments need to be cautious.

So it could not be any more explicit. P2P firms are “banned” from providing guarantees for investmentprincipal or returns (interest).

YRD management was quick to assure its US investors via English language news media(http://www.bidnessetc.com/72634-yirendai-stock-back-greener-pastures-again/) that it was fullycompliant with the new rules and that so called “risk reserve funds” were allowed.

Again. #AlternativeFacts.

As we have already seen, YRD is providing explicit guarantees. This is visible in its Chinese languagecontracts with lenders. It is also 100% observable via the uniformity in returns provided to investorsacross vastly different credit grades.

So to be clear: YRD is explicitly providing guarantees, which is illegal in China. Period.

Ok, so now the question becomes “so what”.

I do NOT expect that the regulators are going to swoop in and shut down YRD.

Instead, the problem is that YRD will soon be forced to stop providing those guarantees. Period. Endof Story.

In my view, when that happens, there will be two consequences which will immediately shatter the factormodels of the few “Quant” investors who currently own YRD’s ADRs.

The first consequence is that new loan volume is going to shrivel up immensely. There is a hugedemand to lend money to what is perceived as “risk free” borrowers. Anyone with a bit of extra cash onhand can sign up on the platform and start generating income with virtually no (perceived) worry ofrepayment. These loan investors are rightfully treating these guaranteed investments as “deposits“.And this is exactly what the government has warned against.

As soon as the paradigm shifts to one of lending money to deep subprime “D Grade” borrowers whowere Fast Track approved in just 10 minutes so that they could get some plastic surgery that they can’tafford anyways…well…I expect the collective desire to lend huge sums of money will shrink by at least80%. That much should be quite obvious.

Of the potential investors who do choose to participate in such a market, they will obviously (andrightfully) require dramatically higher returns which will close in on the 39.5% that YRD can currentlycharge such subprime borrowers.

As a result, I expect that the 28% “spread” that YRD enjoys is also going to largely evaporate.

In fact, with lenders demanding to get compensated for the risk, we are likely to see YRD’s realizablespread fall to around the same levels that we saw for its realizable spread on “A Grade” loans. This justmakes common sense. YRD was getting lenders to make “A Grade” loans to “A Grade” borrowers, suchthat the pricing was quite efficient. There was a clear limit to the spread that could be charged withoutdriving borrowers and/ or lenders to more efficiently priced platforms. Once we see YRD facilitating “DGrade” loans to “D Grade” borrowers, the same market efficiency issue will come into play.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 21/38

And as we saw above, YRD already disclosed that the spread it makes on “A Grade” loans is notenough to be profitable. YRD actually loses moneyon “A Grade” loans when accounting for admin andmarketing costs.

Here is how to wrap your head around the new paradigm shift:

In the past and up until now, YRD has been providing an undercapitalized and illegal guarantee tolenders so that it could pay them artificially low (i.e. perceived as nearly “risk free”) interest rates whenthey lent out their money. But the borrowers of this money then paid full market (i.e. “risky”) rates ofinterest. YRD sat in the middle and collected the enormous “vig”.

Because the rate that lenders required was always fixed at very low levels, the obvious choice for YRDwas to lend to whoever it could extract the highest rates from. Obviously this means lending to the worstcredits possible.

On paper (and in the models of US quant investors), this all works fine in the short run. It looks as if thecompany is minting ever increasing amount of profits. Loan volumes are soaring and net income issoaring even more. And that is all great. But only in the short run.

In reality. this is no different that if my grandma in Boca Raton began selling hurricane insurance out ofher basement to as many people as possible. Sure, she is bringing in a fortune in premiums in the shortterm. But she is selling insurance that she is unable to cover as soon as an “event” occurs. Theseeconomics are similar to what we see with YRD. And just as with P2P loan guarantees in China, this iswhy it would be illegal for my grandma in Boca to provide such a service.

PART G: YRD IS A SUBPRIME DUMPING GROUND FOR PARENT COMPANY CREDIT EASE

The reality as I see it is that YRD has largely been set up as a dumping ground for terrible subprimepaper, foisting the future losses on oblivious US investors who are relying on superficial factor models.

IMPORTANT:

After reading below, it will quickly become clear why the “China Smart Money” won’t touch YRD.

It will also become clear why YRD and other P2P players are listing in the US rather than China.

It will also become clear why YRD management refuses to own shares in YRD itself.

YRD’s parent is Credit Ease, which is engaged in a variety of micro finance, inclusive finance and wealthmanagement activities.

It turns out that most of YRD’s business is in reality a giant related party transaction with parentCredit Ease.

Credit Ease “originates” around 2/3 of the loans that go to YRD.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 22/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858598222216804_origin.png)

Credit Ease charges a 6% fee off the top for originating, which was recently increased from 5%.

Keep in mind that Chairman Ning Tang doesn’t need to care so much about what happens to US listedYRD because he is actually the largest shareholder of Credit Ease and that’s where the real money is.

YRD discloses that:

Our agreements with CreditEase may be less favorable to us than similar agreements negotiated betweenunaffiliated third parties.

The slice going to Credit Ease is by far the most attractive part of the business model. Credit Ease takesits 6% cut on a huge volume of low quality loans, with zero risk, and then walks away. Regardless ofwhat happens in the future (defaults etc.), Credit Ease makes a fortune. Clearly Credit Ease is stronglyincentivized to maximize total loan volume without any consideration for credit quality. And this isexactly what YRD is doing.

US listed YRD is the middle man between these borrowers and lenders. And US listed YRD is also theone guaranteeing the exploding volume of loans being made to the lowest rung of subprime borrowers.Again, these are “D Grade” borrowers who are paying up to 40% APR. With Fast Track approvals, wecan see that there are minimal verification requirements, including some which simply use the “honorsystem” for borrower disclosures.

P2P platforms (including) YRD typically prohibit borrowers from taking out more than one simultaneousloan. But there is no way for any of the P2P lenders to check and see if borrowers are taking out multipleloans from multiple different P2P lenders at the same time. So YRD relies on the “honor system“.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 23/38

When granting loan approvals, the “use of proceeds” is also taken into consideration. For example,borrowing to make lasting improvements to one’s home would be given higher preference than, say,getting plastic surgery. But YRD has no way to verify use of proceeds, so it again simply relies on the“honor system“.

In both Q2 and Q3, there were several muted references to the massive spike in loan fraud that hadhit YRD, notably in the Fast Track segment.

On the Q2 conference call, CFO Denis Cong noted that

Recently, in early July, during our regular credit underwriting process, we have discovered potential credit cardstatement fraud behavior from certain group of applicants for certain type of our online fast-track loans. Westopped offering this product and conducted immediate investigation. After thorough study and analysis, includingsystematic data checks and in person offline investigation works, we have preliminary concluded that there is likelyan organized fraud incident that impacted on a group of approved borrowersmainly in early July with totalcontract loan volume of RMB72 million.”

In the follow up Q&A, Cong admitted that the company was writing down the full amount of this loss dueto fraud.

And then by the time Q3 rolled around, we learned that YRD had actually underestimated the amountof the fraud. In Q3, YRD disclosed (http://www.secinfo.com/d12TC3.w43m8.d.htm#1stPage) that theamount had now increased to over RMB81 million, roughly 15%.

In fact, I expect to see further escalation of loan fraud once we see Q4 as a result of YRD’s increasinguse of Fast Track approvals to give easy credit with minimal credit checks within just 10 minutes.

PART H: Additional illegal activities at YRD

The illegal activities in this Part are not a dominant part of the equation in terms of YRD’s financialpicture.

But I see them as necessary to understanding the bigger picture as we segue into the next section onpotential trading irregularities in YRD ADR’s

In a report from global law firm Linklaters(http://www.linklaters.com/Insights/AsiaNews/LinkstoChina/Pages/P2P-lending-Chinaenters-into-regulated-era.aspx) from August 2016, the firm made clear that under the newly released regulationsfrom China’s CBRC, there P2P players were specifically prohibited from engaging in 13 categories ofactivities, including:

“Creating Asset Pools”“Providing Guarantees” for borrowersSelling “Wealth Management” products

From the sections above, it should already be clear that YRD is providing explicit guarantees. This isbeyond any doubt. (regardless of what #AlternativeFacts YRD chooses to state).

According to media interviews (http://www.bidnessetc.com/72634-yirendai-stock-back-greener-pastures-again/) in English:

Mr. Cong assured that CreditEase and Yirendai were “in full compliance” with the new requirements, and that thetwo companies were in “close discussions” with CBRC ahead of yesterday’s announcement.

(Note, in the Part below, we’re going to look at that quote again in the context of the TIMING of the salesby an affiliated Fund.)

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 24/38

But from what I see, YRD is also clearly “Creating Asset Pools” via its creation of a trust(http://www.secinfo.com/d12TC3.w2u6g.htm#1stPage) which invests in the loans that it facilitates. Thistrust was established in 2015 in an attempt to expand to institutional investors. The structure isconvoluted: The trust invests in loans made through the YRD platform using funds from its sole investor,which is also the beneficiary. The name of the beneficiary is Zhe Hao Shanghai Asset ManagementCompany, which happens to be an affiliate of Credit Ease. In April 2016, Zhe Hao then transferredbeneficiary rights to a CICC “Special Purpose Vehicle” which intends to list on the Shenzhen Exchangeand issue asset backed securities. In other words…. YRD is “Creating Asset Pools”.

In addition, YRD can also be directly linked to asset management firm Toumi.

Here is a screenshot of the website for iToumi.com. I have added a few translations in red. There shouldbe no doubt that this is a Chinese asset management platform. We can also see the name Credit Ease,so that should not be in doubt either.

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858599094062972_origin.png)

But a closer look reveals that iToumi.com is actually being administered by Yirendai (“YRD”), not byCredit Ease.

Here is a snapshot of the WhoIs lookup for the iToumi.com website as it was shown a few months ago.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 25/38

Obviously engaging in illegal activities is not a good thing in general. But in these two cases, thecreation of trusts and the wealth management activities are not really such a big deal by themselves.

Instead, it is their links to the other activities below that are cause for much greater concern forme.

PART I: TRADING IN YRD SHARES BY AN UNDISCLOSED “AFFILIATED” FUND OF NING TANG

Following the IPO of YRD in December 2015 and then through 2016, there were issued a series ofopaque and contradictory 13D’s which describe various purchases and sales of YRD shares by anunnamed “Fund” which is “affiliated” with YRD Chairman Ning Tang.

In the initial 13D (http://www.secinfo.com/d14D5a.mCXGk.htm#1stPage), it was noted that

A fund affiliated with Mr. Ning Tang (the “Fund”) purchased 1,500,000 ADSs offered in the IPO at the initialpublic offering price for a total price of US$15,000,000 and on the same terms as the other ADSs being offered inthe IPO. The funds used to purchase the 1,500,000 ADSs were invested by third-party investors. Mr. Ning Tangdisclaims beneficial ownership of all of the ADSs purchased by the Fund except to the extent of his pecuniaryinterest therein.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 26/38

OK. Fine. So Ning Tang “disclaims beneficial ownership” of the shares AND he notes that the fundswere even provided by third party investors.

But then the 13D contradicts itself later in the filing, noting that:

After the purchase made by the Fund in the Company’s IPO, Mr. Ning Tang’s beneficial ownership in theCompany increased to 46,430,000 Shares, representing approximately 39.7% of the total issued and outstandingShares…The 46,430,000 Shares beneficially owned by Mr.Ning Tang (http://www.secinfo.com/$/SEC/Name.asp?S=ning+tang) comprise (NYSE:I (http://seekingalpha.com/symbol/I)) 43,430,000 Shares beneficially owned by Mr.Tang through his indirect holding of 43.4% of the total outstanding shares of CreditEase on an as-converted basisand CreditEase’s holding of 100,000,000 Shares in the Company, and (ii) 3,000,000 Shares represented by1,500,000 ADSs owned by the Fund.

So in fact, the shares being purchased by “the unnamed Fund” are actually beneficially owned by NingTang.

Here is why that becomes important.

First, there were more purchases of YRD being used to support the stock when it was hitting new lowsin March of 2016. Yet there was no disclosure of these purchases until 6 months later.

Those disclosures quickly become problematic.

Only in September (http://www.secinfo.com/d12TC3.w3Xm6.htm#1stPage) did we see disclosure(http://www.secinfo.com/d12TC3.w3Xm6.htm#1stPage) from YRD that in March (6 months earlier), NingTang’s unnamed “Fund” purchased an additional 300,000 ADS’s on the open market. This would havebeen done at around prices of $10 or even below.

These purchases were made between March 22nd and March 29th.

But by the time that filing came out in September, Tang’s fund had already begun dumping thoseshares, again without timely disclosure.

Between August 22nd and September 7th, Tang’s Fund sold all 300,000 of those shares acquired inMarch, as well as an additional 300,000 shares.

So we didn’t even know about the purchases until well AFTER the shares had already been dumped(along with hundreds of thousands more shares).

Then in a subsequent 13D from two weeks later in September revealed that the fund continued to dumpa further million shares.

By this time, the Fund had now dumped around 90% of its holdings.

What is important to note here is that the Fund acquired its shares when the stock was hitting new lowsand the buying served to prop up the share price in March.

But then the Fund quickly began dumping around 90% of its shares within a few weeks – within 24hours of the new regulations being announced in China which outlaw the loan guarantees being used byYRD. Not surprisingly, the share price quickly took a significant dive.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 27/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858599769653656_origin.png)

In the graph above, you can tell exactly when the announcement occurred in August, because that iswhat sent YRD plunging from its all time high near $40. You can also see that that is exactly when theFund began liquating 90% of its shares of YRD.

SINCE THAT PEAK, SHARES OF YRD HAVE NOW ALREADY FALLEN BY 50% !

Again, Chairman Ning Tang has disclaimed his beneficial ownership of these shares, but from the 13Dswe can see that this is clearly not the case.

Perhaps of greatest importance is the fact that the Fund was began dumping 90% of its shares of YRDvirtually simultaneouswith the public statements by the CEO and CFO which assured US investorsthat YRD had no issues with the new regulations which made its loan guarantees illegal in China.

The selling began just days BEFORE the public announcement of the new regulations. So let’s look atthe quote from the interview with CFO Cong one more time.

Mr. Cong assured that CreditEase and Yirendai were “in full compliance” with the new requirements, and that thetwo companies were in “close discussions” with CBRC ahead of yesterday’s announcement.

PART J: Chairman Ning Tang “orders” employees to buy undisclosed US equities or be FIRED !

Imagine for a moment if there were a company which operated in the US, which employed US citizens.The company then sends out an order to all of the US employees, telling them that they must converttheir own personal US dollars into Chinese RMB and then contribute their RMB into an investmentvehicle controlled by the Chairman of the company. That vehicle would then take US employees’ moneyand buy some “unnamed” stock that only trades in China.

Sounds ludicrous right ?

Read on because according to posted leaked emails, this is exactly what YRD’s parent companyappears to be doing with its Chines employees as it forces them to buy some “unnamed” US dollarstock. (The only US dollar equity that I can find tied to YRD’s chairman happens to be YRD.)

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 28/38

A few weeks ago, a financial news portal in China began publishing leaked internal emails betweenmanagement and employees at Credit Ease. Credit Ease is YRD’s parent company and both entities arecontrolled by YRD Chairman Ning Tang.

What we find is an emailed employee complaint to Chairman Ning Tang as well as the emailed responsefrom Chairman Tang to that employee.

The site posting the leaked emails is known as “Financial Gossip Girl” ( 金融八卦女)。Its web address issimply the Chinese Pinyin for that name (jinrongbaguanv.com (http://m.jinrongbaguanv.com/)), whichnow redirects you to download their App directly.

The content on Financial Gossip Girl is also available on Weibo (http://weibo.com/jinrongbaguanv)(http://weibo.com/jinrongbaguanv%29).

Financial Gossip Girl is a crowd sourced portal covering the financial services industry in China. Thegroup currently employs a group of 10 editors with professional finance backgrounds, all of whomremain anonymous.

Much of the information on the site appears to be sourced from employees in some of China’s largestfinancial firms. It was first established as a website in 2011 by a group of finance professionals in China.So the site has now been around for 6 years.

In 2016, Financial Gossip Girl was featured in an article in Harper’s Bazaar China (http://m.v4.cc/News-1580856.html) which gives more detail on the group. Other scattered reviews of the site can be found onChinese financial sites.

The group has stated that the purpose of the App is to eventually become a full social networking site forfinance professional, arguably similar to LinkedIn, but with the twist that users can post detailedinformation on their employers.

In the US, where financial services are much more heavily regulated than in China, we clearly do nothave such a site covering the financial industry. But in the pharma industry we have something quitesimilar in the US.

The analogy I use is that of Café Pharma (cafepharma.com (http://cafepharma.com/)) , which is awebsite where pharma employees in the US can log on and share very detailed information about whatgoes on inside. I use Café Pharma often when researching US based pharma companies and it is oftenexceptionally informative about what really goes on behind the scenes at Big Pharma in the US.

(For those who are interested in following Financial Gossip Girl in China, it is the App that delivers themost news in the easiest to use form. It can be downloaded from Apple’s AppStore. While I am in Asia,the updates come in throughout the day. But in the US, you can expect multiple updates to yoursmartphone every day during the wee hours of the morning, which gets a bit annoying.)

Here is a complete pdf file (https://moxreports.com/wp-content/uploads/2017/01/%E5%AE%9C%E4%BF%A1%E5%BC%BA%E5%88%B6%E5%91%98%E5%Bthe email posting to and from various Credit Ease employees.

(Note: I have spent enough time in China that I am more than comfortable enough reading theseChinese documents. But for the sake of objectivity I hired a professional Chinese translation firm in LosAngeles that specializes in servicing Fortune 500 firms in legal disputes that involve Chinese.)

The title of the posting was as follows:

宜信强制员工买500美元的产品,不买就被辞退!还要附带50美元手续费

The translation of this reads:

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 29/38

Credit Ease forces employees to buy USD500 of “product” or be fired ! Also must pay a USD 50 service fee.

The “product” here is the asset management “product” being offered by Toumi, the asset managementfirm listed above (which YRD isn’t even supposed to be involved with under the new Chineseregulations).

The reason that Chinese employees (who are paid in Chinese RMB) are being forced to come up withUSD to invest is that this “product” of Toumi is one in which the company buys US listed equities.

References in the email below to “RA” refer to Toumi’s “Robo Advisor” which takes the employees USDcontributions and then selects the investments for them. The employees do not select their owninvestments.

Given that Ning Tang is only connected to one US listed stock, there is only one logical choice for whichUS listed equity he would be forcing his employees to buy under threat of being fired. For me, the onlysensible conclusion is YRD.

This view is further bolstered by the information above which shows that an unnamed “Fund” affiliatedwith Ning Tang was buying up shares of YRD during the course of 2016, and then dumping those sharesof YRD as soon the company ran into public regulatory problems.

But with the current Toumi purchases, the benefit to Ning Tang and his Fund would be that the money atrisk here is coming from thousands of low level Credit Ease employees. It is no longer his money or themoney of his affiliated Fund.

The employees are employed in two different Finance groups. There is Group #1 and Group #2. Bothare required to make USD investments into the USD investment “product”.

The first disclosed email shows the following:

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858600406166255_origin.png)

The translation of this reads:

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 30/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858600556291668_origin.png)

It is important to note that the deadlines for making contributionsinto the asset management“product” come before employees are paid their year end bonuses. So even if an employeedoesn’t think he will be fired, he knows that his full year bonus will be in jeopardy.

Following this mass email to finance department employees, one employee wrote directly toChairman Ning Tang. That email is shown here (name redacted, finance department #1).

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858600887156975_origin.png)

He makes a clear reference to commands from Ning Tang that those who don’t contribute to theUSD investment “product” should not come to work on Monday.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 31/38

(click to enlarge)

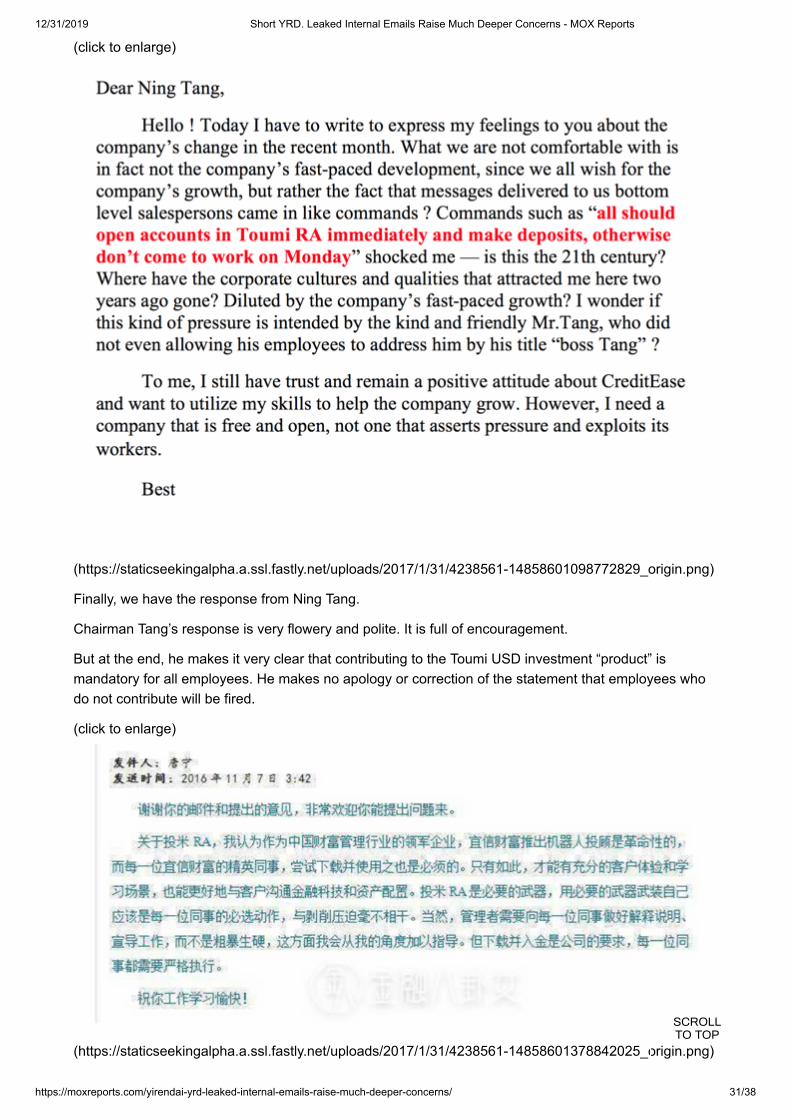

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858601098772829_origin.png)

Finally, we have the response from Ning Tang.

Chairman Tang’s response is very flowery and polite. It is full of encouragement.

But at the end, he makes it very clear that contributing to the Toumi USD investment “product” ismandatory for all employees. He makes no apology or correction of the statement that employees whodo not contribute will be fired.

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858601378842025_origin.png)

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 32/38

(click to enlarge)

(https://staticseekingalpha.a.ssl.fastly.net/uploads/2017/1/31/4238561-14858601552658138_origin.png)

The language, the source and the level of detail above cause me to believe that the exchange above isauthentic. I did send an email to Credit Ease asking about this issue but I have not yet received aresponse.

PART K: CONCLUSION

Without even looking at YRD specifically, investors should know that investing in ANY of China’s P2Pplayers is just downright dumb. The industry has exploded in size due to poor oversight and regulationwhich is already resulting in massive and widespread fraud and defaults.

This is why China’s securities regulators have sought to protect Chinese investors from P2P IPO’s andforced the P2P players to simply IPO in the US.

It is also why precisely NONE of the traditional “smart money” in China, which is present in mostChinese ADR’s, has been willing to invest in YRD AT ANY PRICE. Outside US investment in YRDconsists primarily of “quant funds” who plug YRD’s attractive headline metrics into their “factor models”. Ibelieve that they simply don’t know what they own. Likewise, YRD management also wisely refuses toown shares of YRD.

When YRD began making loans in 2013, precisely 100% of these loans were to prime “A Grade”credits. But as we saw, YRD could not generate substantial volumes of loans in this market. And in fact,YRD could not even generate a profit from these “A Grade” loans.

So instead, YRD quickly transitioned to deep subprime “D Grade” loans where borrowers pay up to40% APRs for short term loans. Such deep subprime loans quickly comprised more than 80% of newloans being made by YRD.

SCROLLTO TOP

12/31/2019 Short YRD. Leaked Internal Emails Raise Much Deeper Concerns - MOX Reports

https://moxreports.com/yirendai-yrd-leaked-internal-emails-raise-much-deeper-concerns/ 33/38

To turbo charge growth even further, YRD introduced “Fast Track” loans where these deep subprimeborrowers could get approved for a loan within just 10 minutes with minimal credit checks ordisclosure and with the entire process being conducted by smart phone. Much of the borrowerdisclosure simply relies upon “the honor system”.

The result was 100% predictable: loan volume exploded exponentially as these deep subprimeborrowers lined up to borrow money for such discretionary luxuries as plastic surgery and expensivevacations. In the short term, YRD appears to be reaping substantial profits from charging fees on suchloans.

The problem is that no one in their right mind wants to lend to this type of borrower. As a result, to enticeChinese retail to lend, YRD offers a guarantee of interest and principle. This guarantee is shownexplicitly on the loan contract shown to lenders on YRD’s web page. It is also readily apparent byobserving that lenders receive the same rate of interest regardless of whether their loans are beingmade to “A Grade” credits or to “D Grade” credits. The rate of interest received by lenders is quiteclearly being determined by the guarantee from YRD and NOT by the underlying credit of the borrower.

But in 2016, Chinese regulators made clear that such guarantees were illegal.