rb timespread (cts/gal) aug/sep 2.07 -0.14 ice gasoil ... · -187 kb/d versus may and a very sharp...

TRANSCRIPT

The contents of this document is for informational purposes only and is not an offer to sell or a solicitation to buy any futures contract, option, security, or derivative including foreign exchange. Trading entails significant risks and may not be appropriate for all investors

© 2006 Petromatrix GmbH. Receiving this report is commercially and legally restricted to direct, subscribing, clients of Petromatrix. Contact: [email protected]

1

DAILY MARKET REPORT 11-JULY 18

Latest

c.o.b.

Daily

Change

Daily

Change %

WTI ($/bbl) Aug 74.11 0.26 0.35%

Brent ($/bbl) Sep 78.86 0.79 1.01%

RBOB ($/gal) Aug 2.1603 0.0118 0.55%

NY ULSD ($/gal) Aug 2.2218 0.0261 1.19%

Natgas US ($/mmbtu) Aug 2.7880 -0.0400 -1.41%

Heat Crack vs WTI ($/bbl) Aug 19.21 0.84

RBOB Crack vs WTI ($/bbl) Aug 16.62 0.24

321 Crack vs WTI ($/bbl) Aug 17.48 0.44

Heat Crack vs Brent ($/bbl) Sep 14.69 0.31

RBOB Crack vs Brent ($/bbl) Sep 11.00 -0.24

321 Crack vs Brent ($/bbl) Sep 12.23 -0.06

Brent/WTI ($/bbl) Sep -6.30 -0.21

WTI Timespread ($/bbl) Aug/Sep 1.55 -0.32

Brent Timespread ($/bbl) Sep/Oct 0.24 0.02

RB Timespread (cts/gal) Aug/Sep 2.07 -0.14

NY ULSD Timespread (cts/gal) Aug/Sep -0.55 0.01

ICE Gasoil Timespread ($/MT) Jul/Aug -0.25 0.00

Gold 1,255.40 -4.20 -0.33%

GSCI 2,793.85 0.81 0.03%

S&P 500 2,793.84 9.67 0.35%

Amex Oil Index 1,546.37 9.76 0.64%

Dollar Index 94.16 0.08 0.09%

VIX 12.64 -0.05 -0.39%

The contents of this document is for informational purposes only and is not an offer to sell or a solicitation to buy any futures contract, option, security, or derivative including foreign exchange. Trading entails significant risks and may not be appropriate for all investors

© 2006 Petromatrix GmbH. Receiving this report is commercially and legally restricted to direct, subscribing, clients of Petromatrix. Contact: [email protected]

2

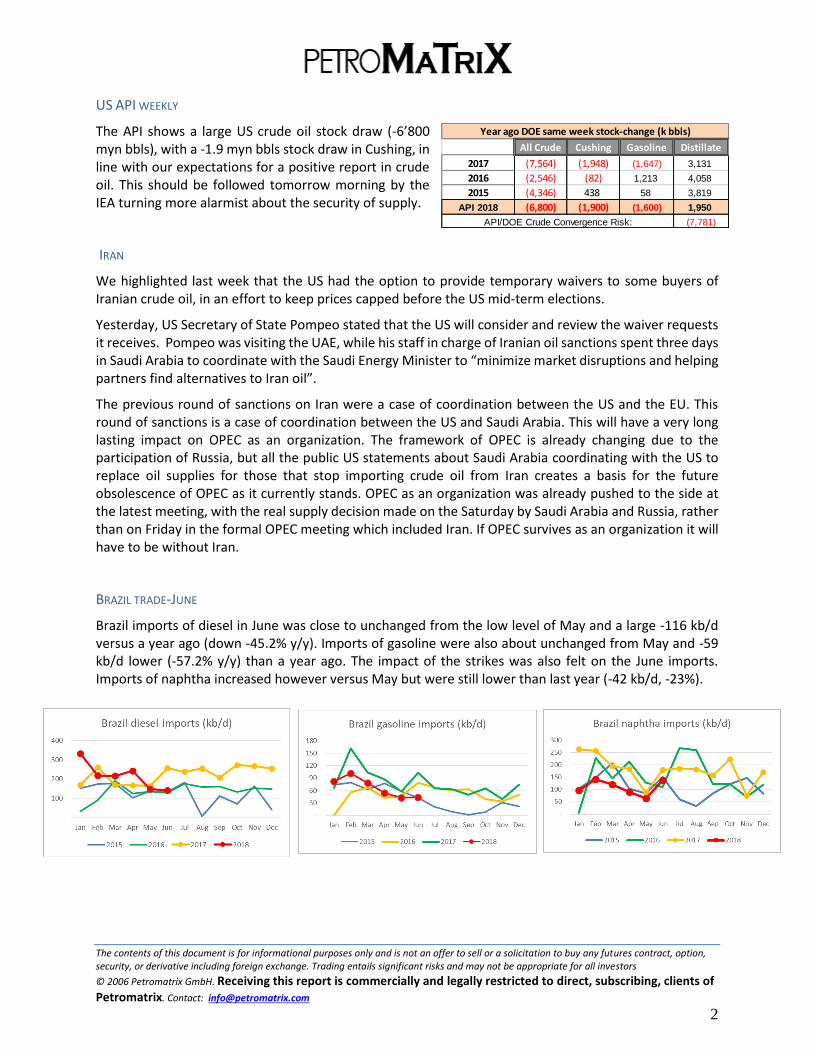

US API WEEKLY

The API shows a large US crude oil stock draw (-6’800 myn bbls), with a -1.9 myn bbls stock draw in Cushing, in line with our expectations for a positive report in crude oil. This should be followed tomorrow morning by the IEA turning more alarmist about the security of supply.

IRAN

We highlighted last week that the US had the option to provide temporary waivers to some buyers of Iranian crude oil, in an effort to keep prices capped before the US mid-term elections.

Yesterday, US Secretary of State Pompeo stated that the US will consider and review the waiver requests it receives. Pompeo was visiting the UAE, while his staff in charge of Iranian oil sanctions spent three days in Saudi Arabia to coordinate with the Saudi Energy Minister to “minimize market disruptions and helping partners find alternatives to Iran oil”.

The previous round of sanctions on Iran were a case of coordination between the US and the EU. This round of sanctions is a case of coordination between the US and Saudi Arabia. This will have a very long lasting impact on OPEC as an organization. The framework of OPEC is already changing due to the participation of Russia, but all the public US statements about Saudi Arabia coordinating with the US to replace oil supplies for those that stop importing crude oil from Iran creates a basis for the future obsolescence of OPEC as it currently stands. OPEC as an organization was already pushed to the side at the latest meeting, with the real supply decision made on the Saturday by Saudi Arabia and Russia, rather than on Friday in the formal OPEC meeting which included Iran. If OPEC survives as an organization it will have to be without Iran.

BRAZIL TRADE-JUNE

Brazil imports of diesel in June was close to unchanged from the low level of May and a large -116 kb/d versus a year ago (down -45.2% y/y). Imports of gasoline were also about unchanged from May and -59 kb/d lower (-57.2% y/y) than a year ago. The impact of the strikes was also felt on the June imports. Imports of naphtha increased however versus May but were still lower than last year (-42 kb/d, -23%).

All Crude Cushing Gasoline Distillate

2017 (7,564) (1,948) (1,647) 3,131

2016 (2,546) (82) 1,213 4,058

2015 (4,346) 438 58 3,819

API 2018 (6,800) (1,900) (1,600) 1,950

(7,781)

Year ago DOE same week stock-change (k bbls)

API/DOE Crude Convergence Risk:

The contents of this document is for informational purposes only and is not an offer to sell or a solicitation to buy any futures contract, option, security, or derivative including foreign exchange. Trading entails significant risks and may not be appropriate for all investors

© 2006 Petromatrix GmbH. Receiving this report is commercially and legally restricted to direct, subscribing, clients of Petromatrix. Contact: [email protected]

3

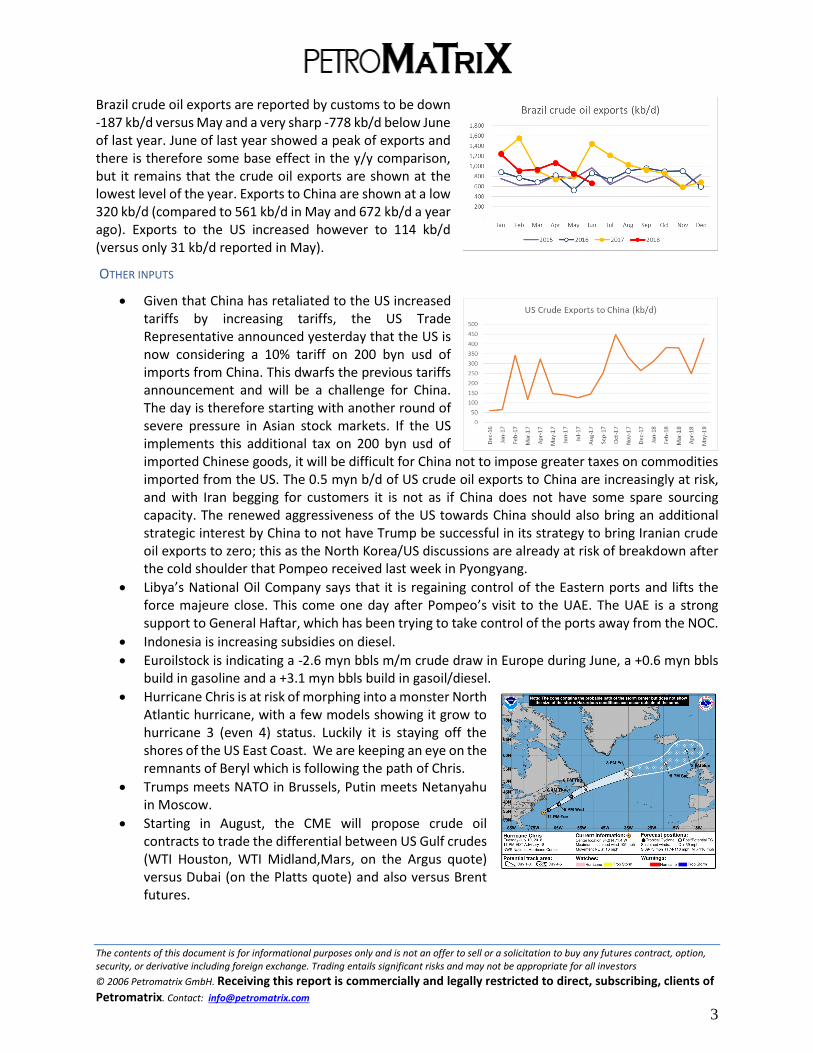

Brazil crude oil exports are reported by customs to be down -187 kb/d versus May and a very sharp -778 kb/d below June of last year. June of last year showed a peak of exports and there is therefore some base effect in the y/y comparison, but it remains that the crude oil exports are shown at the lowest level of the year. Exports to China are shown at a low 320 kb/d (compared to 561 kb/d in May and 672 kb/d a year ago). Exports to the US increased however to 114 kb/d (versus only 31 kb/d reported in May).

OTHER INPUTS

Given that China has retaliated to the US increased tariffs by increasing tariffs, the US Trade Representative announced yesterday that the US is now considering a 10% tariff on 200 byn usd of imports from China. This dwarfs the previous tariffs announcement and will be a challenge for China. The day is therefore starting with another round of severe pressure in Asian stock markets. If the US implements this additional tax on 200 byn usd of imported Chinese goods, it will be difficult for China not to impose greater taxes on commodities imported from the US. The 0.5 myn b/d of US crude oil exports to China are increasingly at risk, and with Iran begging for customers it is not as if China does not have some spare sourcing capacity. The renewed aggressiveness of the US towards China should also bring an additional strategic interest by China to not have Trump be successful in its strategy to bring Iranian crude oil exports to zero; this as the North Korea/US discussions are already at risk of breakdown after the cold shoulder that Pompeo received last week in Pyongyang.

Libya’s National Oil Company says that it is regaining control of the Eastern ports and lifts the force majeure close. This come one day after Pompeo’s visit to the UAE. The UAE is a strong support to General Haftar, which has been trying to take control of the ports away from the NOC.

Indonesia is increasing subsidies on diesel.

Euroilstock is indicating a -2.6 myn bbls m/m crude draw in Europe during June, a +0.6 myn bbls build in gasoline and a +3.1 myn bbls build in gasoil/diesel.

Hurricane Chris is at risk of morphing into a monster North Atlantic hurricane, with a few models showing it grow to hurricane 3 (even 4) status. Luckily it is staying off the shores of the US East Coast. We are keeping an eye on the remnants of Beryl which is following the path of Chris.

Trumps meets NATO in Brussels, Putin meets Netanyahu in Moscow.

Starting in August, the CME will propose crude oil contracts to trade the differential between US Gulf crudes (WTI Houston, WTI Midland,Mars, on the Argus quote) versus Dubai (on the Platts quote) and also versus Brent futures.

The contents of this document is for informational purposes only and is not an offer to sell or a solicitation to buy any futures contract, option, security, or derivative including foreign exchange. Trading entails significant risks and may not be appropriate for all investors

© 2006 Petromatrix GmbH. Receiving this report is commercially and legally restricted to direct, subscribing, clients of Petromatrix. Contact: [email protected]

4

OIL PRICE OUTLOOK

Brent found some support in the European hours, fed by news of the small workers strike in Norway. WTI did not managed however to find enough power for a test of 75.00 $/bbl as the front WTI month continues to suffer from a steep reduction on the front backwardation. The US session brought WTI back to 74.00 $/bbl for the close. WTI has closed about unchanged both Monday and Tuesday: it is currently parked just below 75.00 $/bbl in order to attack that level on the release of the DOE weekly report, but that trade might start to be a bit too visible and we are not sure if such a planned break could hold given that there are almost no more speculative shorts in WTI. That expected trade received also some overnight complications, first with the announcement of the next tariff plan by the US and second with headlines that Libya’s NOC is regaining administrative control of the exports in the eastern ports.

A supportive DOE weekly report and a potential supportive IEA report tomorrow are expected and should be already partly priced-in. The US 200 byn usd tariff proposal and the lifting of force majeure in Libya were overnight surprises that were not priced-in. It is now more probable that some speculative length will look for profit-taking on any rally led by the upcoming oil reports.

The S&P500 was supported and was getting ready for a test of the resistance of 2’800 but it now has to digest a global equity retracement after the US tariffs announcement.

In WTI we trace a first resistance at 74.50 $/bbl and the big test at 75.00 $/bbl (recent high at 75.27 $/bbl). First support at 73.50 $/bbl, followed by a strong line at 73.00 $/bbl and by 72.20 $/bbl.

In Brent we trace a first resistance at 79.00 $/bbl and by 80.00 $/bbl. First support at 77.50 $/bbl followed by 77.00 $/bbl and by 76.60 $/bbl (20-day mavg).