recap of fy04 -...

TRANSCRIPT

©2008 ModusLink Global Solutions. All Rights Reserved

Investor Presentation

October, 2008

SEC Safe Harbor Statement

2

This presentation contains forward-looking statements which address a variety of subjects including, for example, the expected growth of markets in which ModusLink Global Solutions and ModusLink operate, expected industry expansion, expected growth in annual revenue, expected reduction in SG&A, expected improvement in gross margins and operating income, the further execution of ModusLink’s strategic business plan, the development and implementation of business strategies in our target markets and through our venture capital business, and the assessment of the companies within the venture capital portfolio. The following important factors and uncertainties, among others, could cause actual results to differ materially from those described in these forward-looking statements: ModusLink Global Solutions' success, including its ability to improve its cash position, expand its operations and revenues, reduce its costs, improve its gross margins and sustain profitability, depends on its ability to execute on its business strategy and the continued and increased demand for and market acceptance of its products and services; ModusLink Global Solutions' management may face strain on managerial and operational resources as they try to oversee the expanded operations; ModusLink Global Solutions may not be able to expand its operations in accordance with its business strategy; ModusLink Global Solutions' cash balances may not be sufficient to allow ModusLink Global Solutions to meet all of its business and investment goals; Potential acquisitions and investments may not be available at all or on favorable terms; ModusLink Global Solutions may experience difficulties integrating technologies, operations and personnel in accordance with its business strategy; ModusLink Global Solutions sells to its clients on a purchase order basis, rather than pursuant to contracts with minimum purchase requirements and therefore revenue and financial results are subject to demand variability; ModusLink Global Solutions derives a significant portion of its revenue from a small number of customers and the loss of any of those customers could significantly damage ModusLink Global Solutions' financial condition and results of operations; risks inherent in conducting international business the mergers and acquisitions and IPO markets are inherently unpredictable and liquidity events for companies in the venture capital portfolio may not occur; and increased competition and technological changes in the markets in which ModusLink Global Solutions competes. This presentation contains certain non-GAAP financial measures. A reconciliation of the non-GAAP financial measures to the most directly comparable GAAP measures is included herein. This presentation includes estimates which may not be indicative of future results. For a detailed discussion of cautionary statements that may affect ModusLink Global Solutions' future results of operations and financial results, please refer to ModusLink Global Solutions' filings with the Securities and Exchange Commission, including ModusLink Global Solutions' most recent Annual Report on Form 10-K and Quarterly Report on Form 10-Q. Forward-looking statements represent management's current expectations and are inherently uncertain. We do not undertake any obligation to update forward-looking statements made by us.

Investor Highlights

$1.1B revenue company moving from a transformational phase to a growth phaseFocusing operations in the high growth Business Process Outsourcing (BPO) market Strong and growing customer base: • More than 70% of revenues from Fortune 500 companies

Strong balance sheet: • No Debt; Cash of $162M; NOL’s of $2.0B

Seasoned management team

3

What is our story?

4

Changed name to ModusLink Global

Solutions, Inc.Network of Companies & Venture Capital

Multiple Operating Businesses

Search Portals Infrastructure

Interactive Mkt. Prof. Services

Venture CapitalSupply Chain

Acquired Open Channel Solutions and PTS

Electronics

Acquired Modus Media

Focused Operating Company

Supply Chain BPO

Venture Capital

1995 2000 2005 20102008

What is Business Process Outsourcing (BPO)?

The outsourcing of non-core business functions:

5

ModusLink Focus

Finance and Accounting

Sales and Marketing

Logistics and

DistributionCustomer Services

Procurement

Training

Human Resources

Core Company

ModusLink Supply Chain BPO Processes

6

Plan Source Make Deliver Return

Supply Chain Optimization Consulting Global Inventory Planning

Supply Base ManagementInbound Logistics

Content/ Materials ManagementOptimized Product Configuration

Outbound LogisticsDirect to Retail/ ConsumereBusinessWireless ActivationEntitlement Management

Returns ManagementAsset Recovery and RepairWarranty and RecallFinancial Management Services

What solutions do we provide?Four examples of our many supply chain solutions are:

Computing Software Communications Storage Consumer Electronics

Factory Feed X X X

After-Market Services X X X X X

Optimized Configuration/ Postponement X X X

E-Business X X X X X

7

Target Markets

How do we compete against the ODM’s and CM’s?

ODMs + CM’s

8

Strengths:

• Long run production

• Low cost manufacturing geographies

• Procurement leverage

• Product design capabilities

ModusLink coordinates multi-vendor requirements across the entire supply chain

Make

Weaknesses:

• Product & package complexity

• Far away from consumer markets

• Changes in demand drive packaging rework

• Clients prefer multiple key suppliers

SourcePlan Deliver Return

Why is BPO Important for the Supply Chain?

Shorter product lifecycles

Higher cost/shrinking margins

Product customization

Longer supply chains

Geographically diverse suppliers

Global inventory pools

9

What is the Size and Growth of the BPO Market?

10

Business Process Outsourcing Spending 2006 – 2011 ($Billions)

Source: IDC – Sept 2007

10% CAGR

0.2%0.4% 0.4%

0.7%0.9%

1.4%1.7%

4.6%

Globalware Shin Shin MentorMedia

ATC Zomax Arvato RRDonnelley

ModusLink

How Big is our Addressable Market?

11

ODM / Contract Manufacturers

10%

Source: Dataquest, Company Estimates

In-House providers &

other 77%

Outsourced Supply Chain

13%

The Supply Chain BPO Market is a $25 Billion and can be broken out into three distinct sectors – the Outsourced Supply Chain sector comprises 13% of the total market:

What value do we provide?

Geographic expertise linked with global executionManage flow of goods across multiple suppliers and manufacturersSupport multiple product configurations with minimum investment in inventoryFlexible operational footprint that can change with market conditionsAn extension of Client OperationsStandard and customized solutions that meet customer needs

12

ModusLink delivers on the key drivers for outsourcing Supply Chain processes, specifically we provide:

ModusLink Supply Chain Footprint

13

Waltham, MA HQRaleigh, NCNashville, TNLindon, UTBloomington, INIndianapolis, INOntario, CAMiami, FLMonterrey, MexicoGuadalajara, Mexico

Apeldoorn, NetherlandsOrléans, FranceAngers, FranceKildare, IrelandBrno, Czech RepublicBudapest, Hungary

Atsugi, JapanShanghai, ChinaPudong, ChinaKunshan, ChinaSongjiang, China Taipei, TaiwanShenzhen, ChinaFutian, ChinaPenang, MalaysiaSingapore

Footprint Focus: Low Cost Supply and Major Markets for Consumption

Computing

Software

Storage

16 Core Solutionssuch as:

Factory Feed

After‐Market Services

OPC/Postponement

E‐Business

Global Standardization

Continuous Improvement

Facility Optimization

What is our Strategy?

14

Focus on Target Markets

Expand Client Relationships

through Innovative Solutions

Invest to Drive Operational Efficiencies

Focus on Target

Markets

Expand Client

Relationships through

Innovative Solutions

Invest to Drive

Operational Efficiencies

Communications

Consumer Electronics

Financial Review

15

Financial Highlights

Positioned for revenue growth in fiscal 2009 and beyond

Steadily improving gross margin

Investing to support future profitability

Maintaining a strong balance sheet providing foundation for growth strategy

16

Transitioning to a Growth Phase

$600

$700

$800

$900

$1,000

$1,100

$1,200

$1,300

FY06 FY07 FY08 FY09 Guidance**

Rev

enue

(in

$M)

GAAP Rev. Adj. Rev.*

17

Revenue Trend

* Adjusted for two previously announced discontinued programs.See appendix for reconciliation to closest GAAP measure.

** Midpoint of latest (9/29/2008) guidance revenue range.

Revenue Growth Drivers:

1) Increased Penetration of Existing Customers

2) New customers

3) New Solutions

4) Acquisitions

Improving Gross Margins

6%

8%

10%

12%

14%

16%

FY06 FY07 FY08

Full Year

18

Gross Margin as a % of Revenue Trend

Gross Profit Drivers:

1) Reduce Low Margin Programs

2) Improve mix to higher profit solutions

3) Increase sales to new verticals

4) Lean Sigma Focus

5) ERPTarget Operating Model

Making investments to drive future cost savings

0%

2%

4%

6%

8%

10%

12%

FY06 FY07 FY08

Full Year

19

SG&A as a % of Revenue

SG&A Investments:

1) Sales & Marketing

2) Global Footprint Restructuring

3) ERP/IT

4) Shared Services Consolidation

* SG&A excludes non-cash goodwill impairment charge of $14M in FY08.

Target Operating Model

Balance Sheet and Other Highlights

($ in millions) FY06 FY07 FY08

Cash Balance 228.8$ 282.4$ 162.1$ Outstanding Debt (24.8) (24.8) -

Net Cash Position 204.0 257.6 162.1

@Ventures Investment (6.8) (11.2) (4.6) @Ventures Proceeds 36.5 35.0 19.1

Net Cash from @Ventures 29.7 23.8 14.5

Net Operating Loss Carryforwards 2,000.0 2,000.0 2,000.0

20

In 2008 we strengthened our Balance Sheet:

•$53M for Acquisitions•$35M Stock Repurchase•$25M Debt Repayment

Venture capital investments have returned net cash of $68M over

past three years

US‐generated income can be offset for a long period

Year-End

@Ventures V

Established in 199570 internet, software and IT company investmentsMost recent fund formed in 2004Up to $50 million capital• Approximately $30 million

invested to dateClean technology focus: • Alternative energy• Energy efficiency• Water purification & management

21

Leverage deep experiencewith emerging technology

companies to foster development and

encourage liquidity events

Profile of Management TeamExecutive Title Yrs. Exp. Experience

Joe Lawler Chairman, President and CEO 30 RR Donnelley, Gander Mountain, Fingerhut

Companies, CML Group, Gillette

Steve Crane Chief Financial Officer 28 Interactive Data Corp.,Pepsi Cola Int’l, Chase Manhattan Bank

Matt Dattilo Chief Information Officer 23 PerkinElmer, General ElectricPeter Gray General Counsel 15 Hale and DorrJim Herb SVP, Human Resources 36 RR Donnelley

Mark Kelly President, Aftermarket Services 21 Modus Media, RR Donnelley

Bill McLennan President, Global Operations 26 Onyx Capital Ventures, RR Donnelley, FMC

Corporation, Paction Corporation

David Riley EVP, Corporate Development 14 Towermarc Corporation, Ernst & Young

Scott Smith President, Sales and Marketing, ModusLink

25IBM, Lenovo Group

Peter Mills Managing Director 31@ Ventures, US Display Consortium, Sematech, Softrend, BPI, Digital Equipment, Ford

22

Investor Highlights

$1.1B revenue company moving from a transformational phase to a growth phaseFocusing operations in the high growth Business Process Outsourcing (BPO) market Strong and growing customer base: • More than 70% of revenues from Fortune 500 companies

Strong balance sheet: • No Debt; Cash of $162M; NOL’s of $2.0B

Seasoned management team

23

24

Thank You

25

Appendix

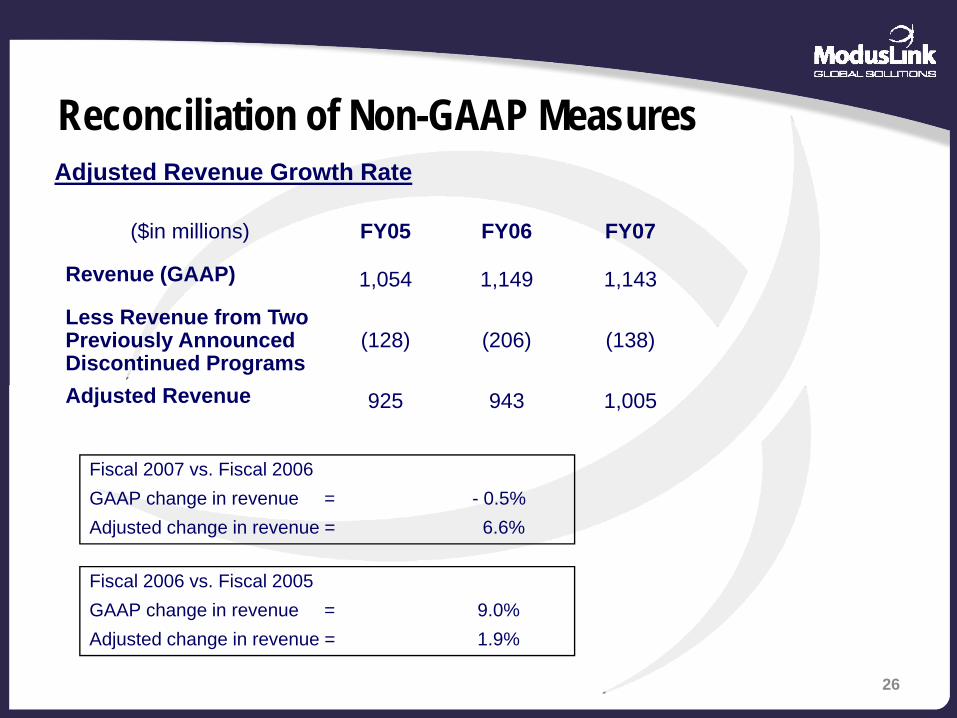

Reconciliation of Non-GAAP Measures

($in millions) FY05 FY06 FY07

Revenue (GAAP) 1,054 1,149 1,143

Less Revenue from Two Previously Announced Discontinued Programs

(128) (206) (138)

Adjusted Revenue 925 943 1,005

26

Adjusted Revenue Growth Rate

Fiscal 2007 vs. Fiscal 2006GAAP change in revenue = - 0.5%Adjusted change in revenue = 6.6%

Fiscal 2006 vs. Fiscal 2005GAAP change in revenue = 9.0%Adjusted change in revenue = 1.9%