recent developments in the energy model times … · power & heat cogeneration plants thermal,...

TRANSCRIPT

RECENT DEVELOPMENTS IN THE ENERGY MODEL TIMES-CANADA:

FOCUS ON THE UNCONVENTIONAL GAS PRODUCTION UNTIL 2050

Energy and Environment (E2G) Team

GERAD Research Center

Montreal, QC, Canada

ETSAP Workshop, November 9th , 2011

TIMES-Canada

Base year: 2007Horizon: 2050 (energy) Horizon: 2100 (climate)

Regions: 13 provinces and territories

Time slices- 4 seasons: Spring, Summer, Fall, Winter- 3 day periods: Day, Night, Peak

Start Mid End Length

1 2007 2007 2007 1

2 2008 2008 2009 2

3 2010 2010 2011 2

4 2012 2012 2013 2

5 2014 2015 2017 4

6 2018 2020 2022 5

7 2023 2025 2027 5

8 2028 2030 2032 5

9 2033 2040 2047 15

10 2048 2050 2052 5

Power & Heat

Cogeneration PlantsThermal, Nuclear

Renewables, Biomass International ExportsCrude oil, RPP, Biomass

Gas, Coal, H2, LNG

Domestic Trades-Pipelines

-Transmission

IND (8) - Tons

Iron & Steel, Cement

Chemicals, Copper

Demand for

Energy Service

End-Use

Technologies

Production / Conversion

Technologies

Primary

Energy

Primary Energy Final Energy Useful Energy

DM 2050Oil prices (3)

Elasticities

DM 2100Growth (2)

Elasticities

COM (7) - PJ/m2

Heating, Cooling

Lighting, Appliances

RSD (20) - PJ/unit

Heating, Cooling

Lighting, Appliances

TRA (16) - Pkm/Tkm

Road: short/long dist.

Rail, Marine, Air

AGR (1) - PJ

IND ProductionFurnaces, Boilers

Machinery

COM ServicesFurnaces, AC,

Fluorescents, Etc.

RSD DwellingsHeat Pumps, Lamps

Freezers, Ranges

TRA VehiclesCars, trucks, buses

Trains, Ships, Planes

-TrucksAGR Process

Refineries

Hydrogen Plants

Biomass PlantsSolid: pellet, wood

Liquid: biofuels

Gaseous: biogas

Coke Plants

Renewable PotentialsHydro, Wave, Tidal

Wind, Solar, Geo

Ocean Thermal & Salinity

Biomass PotentialsCrops: Starch, Oilseeds

Greasy residues

Lignocellulosic sources

Dedicated crops

Waste, Biogas, Algae

Fossil Fuel ReservesConventional & Oil sands

Crude oil, Gas, Coal

Uranium & Lithium

Reserves

ScenariosEnergy policies

Climate policies

International ImportsCrude oil, RPP, Biomass

Gas, Coal, H2

GHG Emissions

Combustion, Process

CCS

LNG Regasification

CAC Emissions

Extraction Oil, Gas, Coal

LNG Liquefaction

LNG Imports

CCS

Carbon sequestration

EOR, Aquifers, Afforestation

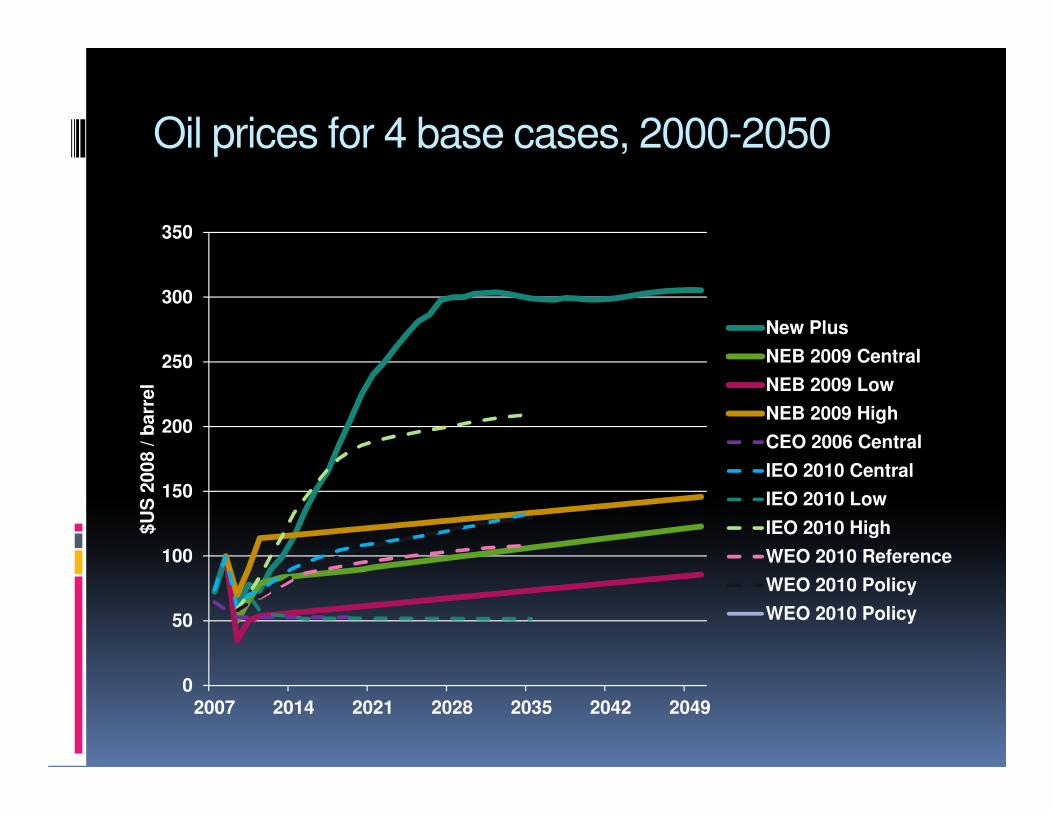

Oil prices for 4 base cases, 2000-2050

0

50

100

150

200

250

300

350

2007 2014 2021 2028 2035 2042 2049

$U

S 2

008 / b

arr

el

New Plus

NEB 2009 Central

NEB 2009 Low

NEB 2009 High

CEO 2006 Central

IEO 2010 Central

IEO 2010 Low

IEO 2010 High

WEO 2010 Reference

WEO 2010 Policy

WEO 2010 Policy

Final energy consumption up to 2050

0

2000

4000

6000

8000

10000

12000

2007 2014 2021 2028 2035 2042 2049

PJ

Renewable

Oil

Gas

Electricity

Coal

Biomass

Final energy consumption in 2050

0

2000

4000

6000

8000

10000

12000

14000

2007 2050 Low 2050 Central 2050 High 2050 Plus 2050 Base -Central - 35%

PJ

Renewable

Oil

Gas

Electricity

Coal

Biomass

Fuel consumption in transport up to 2050

0

500

1000

1500

2000

2500

3000

3500

4000

2007 2014 2021 2028 2035 2042 2049

PJ

Natural gas and NGL

Heavy Fuel Oil

Gasoline

Electricity

Diesel

Biofuels

Aviation fuels

0

500

1000

1500

2000

2500

3000

3500

2007 2014 2021 2028 2035 2042 2049

PJ

Natural gas and NGL

Heavy Fuel Oil

Gasoline

Electricity

Diesel

Biofuels

Aviation fuels

Base central

Base central – 35% GHG in 2050

CARBON CAPTURE AND SEQUESTRATION (CCS) MODULE

SKEORSTD

ELC

Thermal Power plantsPost-combustion capture

ECOA*zo, EGAS*zo

ELFO*zo, EHFO*zo

Thermal Power plants-Pre-combustion capture

ECOA*ze, EGAS*ze

ELFO*ze, EHFO*ze

GASNAT

ELCCO2NELCCH4NELCN2ON

ELCSCO2NCO2 captureSCAPCHPELC

SINKCO2N

OILCRD

Sink – Oil fields onshoreMINSINKOILONS

Sink – Gas fields onshoreMINSINKGASONS

Sink – Oil fields offshoreMINSINKOILOFF

Sink – Gas fields offshoreMINSINKGASOFF

Sink – Deep saline aquifersMINSINKAQUIFE

Sink – CBM recovery < 1000 mMINSINKCBMLOW

Sink – CBM recovery > 1000 mMINSINKCBMHIG

Sink – Enhanced oil recovery MINSINKEORSTD

CCS– Oil fields onshoreSINKOILONS

CCS– Gas fields onshoreSINKGASONS

CCS– Oil fields offshoreSINKOILOFF

CCS– Gas fields offshoreSINKGASOFF

CCS– Deep saline aquifersSINKAQUIFE

CCS– CBM recovery < 1000 mSINKCBMLOW

CCS– CBM recovery > 1000 mSINKCBMHIG

CCS – Enhanced oil recovery SINKEORSTD

Sink potential Sequestration

GASNAT

SKEOILONS

SKEGASONS

SKEOILOFF

SKEGASOFF

SKECBMLOW

SKECBMHIG

SKEAQUIFE

ELC

ELC

ELC

ELC

ELC

ELC

ELC

ELC

Sink potential in the WEST region

0

500

1000

1500

2000

2500

3000

3500

AB BC MB SK

To

ns

Depl oil fields.Onshore.

Depl oil fields.Offshore.

Depl gas fields.Onshore.

Depl gas fields.Offshore.

Enhanced oil recovery.

Enhanced CBM recovery <1000 m.

Enhanced CBM recovery >1000 m.

Deep saline aquifers.

CCS: preliminary results

Base case: Investments in a pulverized coal power plant with CCS for enhanced oil recovery in the WESTConstraint: Investments in renewable electricity to reduce GHG emissions

-

200

400

600

800

1,000

1,200

1,400

1,600

1,800

AB BC SK NB NS

M t

on

nes Lignite

Subbituminous

Bituminous

Anthracite

Coal reserves Need to review - Investment growth in renewable power- Coal trade between provinces

0

20

40

60

80

100

12020

07

20

09

20

11

20

13

20

15

20

17

20

19

20

21

20

23

20

25

20

27

20

29

20

31

20

33

20

35

20

37

20

39

20

41

20

43

20

45

20

47

20

49

To

ns

Base - Central Base - Central -35% reduction

LIQUEFIED NATURAL GAS (LNG) MODULE

QC RabaskaSLNGGASQC30

New Large TerminalSLNGGASLAR15

New Small TerminalSLNGGASSMA15

Import AlgeriaIMPGASLNGALG

Import NigeriaIMPGASLNGNIG

Import ROWIMPGASLNGROW

Import TrinidadIMPGASLNGTRI

Import RussiaIMPGASLNGRUS

Import QatarIMPGASLNGQAT

Import NorwayIMPGASLNGNOR

NS Maple LNGSLNGGASNS15

NB CanaportSLNGGASNB09

QC Grande-AnseSLNGGASQC13

QC Gros CacounaSLNGGASQC14

BC Kitimat LNGSLNGLIQBC15

New Offshore TerminalSLNGLIQOFF20

New Standard TerminalSLNGLIQSTD15

Export BajaEXPGASLNGBAJ

Export ChinaEXPGASLNGCHI

Export ROWEXPGASLNGROW

Export TaipeiEXPGASLNGTAI

Export KoreaEXPGASLNGSKO

Export MexicoEXPGASLNGMEX

Export JapanEXPGASLNGJAP

GASLNG

Regasification

Terminals

PIPGAS

Liquefaction

Terminals

GASLNG

RES of

Natural Gas

LNG import costs between 2007-2010

0.00

0.20

0.40

0.60

0.80

1.00

1.20

1.40

Alg

eri

a

Nig

eri

a

No

rwa

y

Ru

ss

ia

Qa

tar

Tri

nid

ad

& T

ob

ag

o

Ba

ja C

ali

forn

ia

We

st

Me

xic

o

Ja

pa

n

So

uth

Ko

rea

Ta

pe

i

Ch

ina

-Ho

ng

Ko

ng

East West

$/G

J

LNG imports: preliminary results

0

100

200

300

400

500

600

700

800

900

200

7

200

9

201

1

201

3

201

5

201

7

201

9

202

1

202

3

202

5

202

7

202

9

203

1

203

3

203

5

203

7

203

9

204

1

204

3

204

5

204

7

204

9

PJ

Low

Central

High

Plus

Central - 35%

UNCONVENTIONAL GAS MODULE

Coal Bed Methane -

Located ReservesMINRSVCBM1,2,3

Tight Gas -

Located ReservesMINRSVTIG1,2,3

Tight Gas

Additional ReservesMINRSVTIG7,8,9

Shale Gas -

Additional ReservesMINRSVSHA7,8,9

Shale Gas -

Additional Reserves MINRSVSHA1,2,3

Coal Bed Methane -

Additional Reserves MINRSVCBM7,8,9

RSVCBM

Coal Bed Methane -

ProductionSPRIRSVCBM1

RSVSHA

Shale Gas -

ProductionSPRIRSVSHA1

RSVTIG

Tight Gas -

ProductionSPRIRSVTIG1

Coal Bed Methane -

Production AddSPRIRSVCBM2

Shale Gas -

Production AddSPRIRSVSHA2

Tight Gas -

ProductionSPRIRSVTIG2

Na

tura

l Ga

s P

ipe

lin

e

S

PIP

GA

S

GASNAT

PIPGAS

OILNGL

Cumulative gas reserves

-

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

Natural Gas Shale Gas Tight Gas CBM

PJ

NORTH

EAST

CENT

WEST

-

500,000

1,000,000

1,500,000

2,000,000

2,500,000

3,000,000

3,500,000

WEST CENT EAST NORTH

PJ

CBM

Tight Gas

Shale Gas

Natural Gas

Gas extraction and production costs

-

1

2

3

4

5

6

7

8

9

10

WEST CENT EAST WEST CENT EAST WEST WEST EAST

Natural gas Shale Gas TightGas

CBM

$/G

J

Extraction Production

Gas extraction and production costs: Ranges

0.00

1.00

2.00

3.00

4.00

5.00

6.00

7.00

8.00

9.00

10.00

Shale Gas Tight Gas CBM Shale Gas Tight Gas CBM

Exploration Production

$/G

J

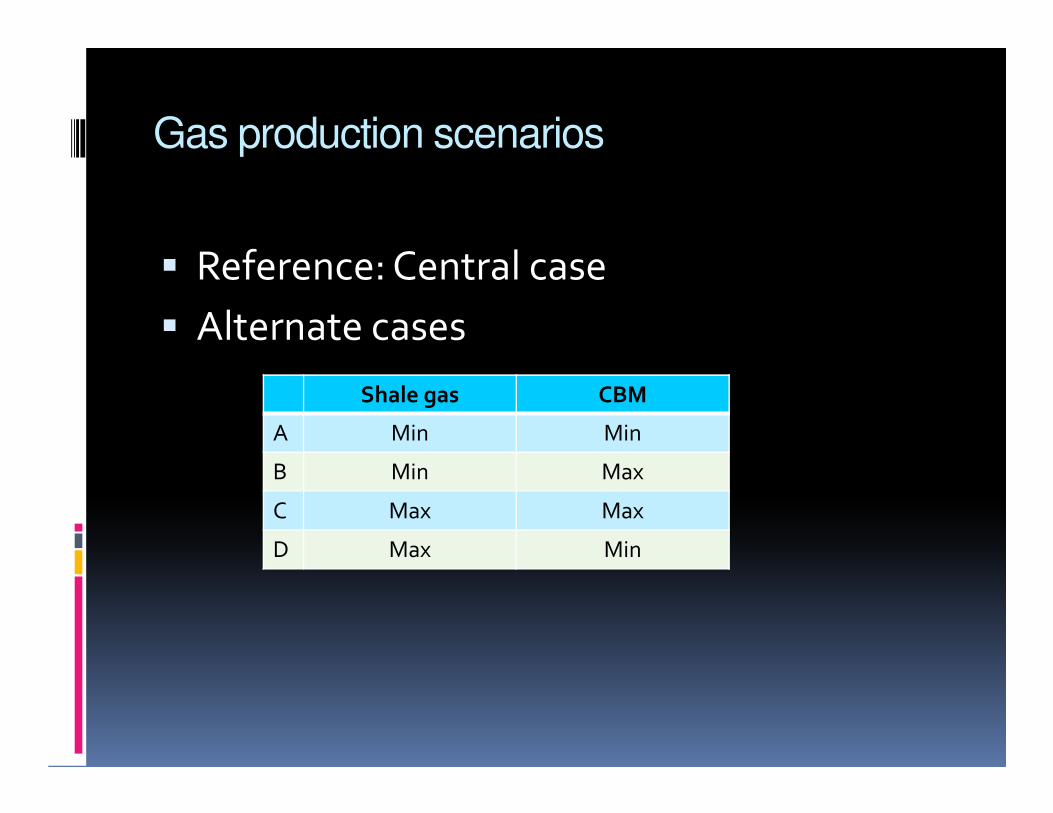

Gas production scenarios

� Reference: Central case

� Alternate cases

Shale gas CBM

A Min Min

B Min Max

C Max Max

D Max Min

Gas production : preliminary results

0

1000

2000

3000

4000

5000

6000

7000

8000

90002007

2009

2011

2013

2015

2017

2019

2021

2023

2025

2027

2029

2031

2033

2035

2037

2039

2041

2043

2045

2047

2049

PJ

NGLs

CBM

Tight Gas

Shale Gas

Natural Gas

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2007 2050 Base- Central

2050MaxMax

2050MaxMin

2050MaxMin

2050MaxMin

2050 Base- Central -

25%

PJ

NGLs

CBM

Tight Gas

Shale Gas

Natural Gas

Gas production : preliminary results

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

2007 2014 2021 2028 2035 2042 2049

PJ

NGLs

CBM

Tight Gas

Shale Gas

Natural Gas

0

1000

2000

3000

4000

5000

6000

7000

8000

9000

10000

2007 2050 Low 2050 Central 2050 High 2050 Plus 2050 Base -Central - 35%

PJ

Conventional Natural Gas Unconventional Natural Gas NGLs LNG Imports

Work in progress

Model developments

� Demand projections up to the 2100 horizon (IPCC scenarios)

� Process GHG emissions and CAC emissions

� CCS in industries

� Energy corridors and coupling with the TIAM world model

Sensitivity analysis

� Renewable power versus CCS

� Unconventional oil and gas production

� LNG imports

� Biomass potential and conversion (next generation)

� Hydrogen production

Thank you from the team

Students

Yuri Alcocer

Camille Fertel

Erik Frenette

Hichem Garbouj

Mathilde Marcy

Yosra Neji

Noushin Reisi

Researchers

• Kathleen Vaillancourt

• Olivier Bahn

• Amit Kanudia

• Maryse Labriet

• Richard Loulou

• Jean-Philippe Waaub

Research project funded by the NSERC of CanadaResearch project funded by the MDEIE of Quebec (link with REACCESS 7th FP-EU)Partners: Resources Natural Canada, Environment Canada, Hydro-Quebec