regional industry focus oil and gas · medco, bcp, sci, ezion, bumi armada, and pantech sell umwog,...

TRANSCRIPT

www.dbsvickers.com

ed-JS / sa- YM , PY

Darkest before dawn

Narrowing supply-demand gap to drive oil price recovery but pace hampered by high inventory levels worldwide

Tipping points for oil services players: oil prices above US$60/bbl; reversal in oil majors’ capex trend

Meanwhile, we see opportunities to accumulate stocks with diversified operations with a competitive edge: Medco, BCP, SCI, Ezion, Bumi Armada, and Pantech

Sell UMWOG, Elnusa on high valuations, avoid Ezra, Nam Cheong, PACRA as balance sheet stress builds up

Oil prices clearly off the bottom now. We raised our oil price forecasts for 2016 and 2017 by US$10 per barrel (bbl) to US$45-50/bbl and US$50-55/bbl respectively as well as our long term oil price by US$5/bbl to US$60-65/bbl. This comes on the back of earlier-than-expected narrowing of the supply-demand gap. We expect the convergence of oil supply-demand trends to gather momentum towards the second half of 2017 and see upside risks stemming from possibility of heightened tensions in the Middle East, production cuts and change in OPEC’s stance.

Inflexion points to watch, bankruptcies on the rise. Increasing bankruptcies and M&A activities are some of the signals of a bottoming in the cycle for oil services companies. While we have yet to see a clear pattern of escalating M&A transactions, we believe there will be more consolidation opportunities in the next 6-12 months as distress builds up in the sector and bankruptcies soar. However, we highlight that any sustained recovery in the industry must originate from the source of cash flows into the ecosystem – in other words the oil majors’ capital expenditures (capex), which will in turn be driven by firmer oil prices. Capex trends could likely start to rise again by the middle of 2017.

Sector trading at steep discount to book, except Thai

upstream plays. Bargain hunt good names. E&P companies are direct winners of any oil price recovery but prospects are probably priced in with the oil price rebound to the US$40 levels. We like diversified oil refiner Bangchak Petroleum [BCP; BUY; TP Bt39], which is a laggard in this space. Singapore rigbuilders possess competitive advantages over their global peers in terms of cost efficiency and R&D focus; We continue to favour SCI [BUY; TP S$3.10] for stability as well as potential re-rating in the marine sector. In Malaysia, we like Pantech [BUY; RM0.64] as the best proxy to ride RAPID; and see value emerging for Bumi Armada [BUY; RM0.85]. In Indonesia, we have upgraded Medco [MEDC; BUY; TP Rp2,000] supported by higher oil prices, operational efficiencies and prudent capital allocation.

Meanwhile, we see more downside for UMW Oil & Gas [UMWOG; FV; TP RM0.80] and Elnusa [FV; TP Rp420], with their rich valuations and high earnings risks. We would also avoid Singapore Offshore Support Vessel (OSV) names like Ezra, Nam Cheong and Pacific Radiance which could be facing near term balance sheet distress.

STI : 2,851.74

Analyst HO Pei Hwa +65 6682 3714; [email protected] Suvro SARKAR +65 6682 3720; [email protected] Chaipat THANAWATTANO +66 2657 7827; [email protected] William SIMADIPUTRA +62 2130 034 939 [email protected] TAN Jianyuan +603 2604 3919; [email protected] Singapore Research Team +65 6327 2288; [email protected]

STOCKS

Source: DBS Bank, DBS Vickers, AllianceDBS., Bloomberg Finance L.P.

DBS Group Research . Equity 6 Sep 2016

Regional Industry Focus

Oil and Gas

Refer to important disclosures at the end of this report

Price Mkt Cap Target Price PB (x) ROE (%)

LCY US$m LCYS$ FY16 FY16 Rating

SINGAPORE S$ S$ Keppel Corporation 5.27 7,050 5.25 0.8 8.5 HOLD Sembcorp Marine 1.28 1,971 1.20 1.0 6.5 FV Sembcorp Industries 2.71 3,569 3.10 0.7 7.3 BUY Yangzijiang 0.77 2,157 1.00 0.6 8.3 BUY Cosco Corporation 0.28 454 0.30 0.9 -18.5 HOLD Ezion Holdings 0.25 381 0.58 0.3 5.4 BUY Ezra Holdings 0.04 90.7 0.06 0.2 -67.7 FV Mermaid Maritime 0.09 95.6 0.09 0.3 3.7 HOLD Nam Cheong Ltd 0.05 71.1 0.04 0.2 -6.1 FV Pacific Radiance 0.15 77.1 0.11 0.2 -10.5 FV PACC Offshore 0.31 413 0.33 0.4 -2.0 HOLD Vard Holdings Ltd 0.14 120 0.18 0.3 -3.3 HOLD Triyards Holdings 0.26 60.8 0.50 0.8 8.5 NR MALAYSIA RM RM Bumi Armada 0.76 1,087 0.85 0.6 2.3 BUY Coastal Contracts 1.48 193 1.65 0.5 8.1 HOLD Dayang Enterprise 1.00 215 0.88 0.8 2.2 FV Dialog Group Bhd 1.53 1,984 1.70 3.6 14.3 HOLD Malaysia Marine & 1.02 401 0.98 0.6 2.5 FV SapuraKencana 1.55 2,280 1.16 0.1 7.0 FV UMW Oil & Gas 0.91 483 0.80 0.8 1.2 FV Deleum Bhd 1.08 106 1.02 0.7 -9.0 HOLD Pantech Group 0.54 81.6 0.64 1.4 8.9 BUY THAILAND Bt Bt Bangchak Petroleum 32.75 1,298 39.00 1.2 16.8 BUY IRPC PCL 4.80 2,824 5.20 1.2 11.41 HOLD PTT 333 27,382 370 1.3 12.1 BUY PTT E&P 79.50 9,086 86.00 0.8 3.5 HOLD PTT Global Chemical 60.25 7,736 70.00 1.1 9.46 BUY Thai Oil PCL 69.50 4,082 65.00 1.4 15.4 HOLD INDONESIA Rp Rp Elnusa 494 274 420 0.2 -19.2 FV Medco Energi 1,495 377 2,000 0.4 -0.3 BUY Logindo 120 23.4 132 1.2 16.0 FV Wintermar Offshore 244 74.6 239 0.5 2.9 HOLD

Regional Industry Focus

Oil and Gas

Page 2

Analysts

HO Pei Hwa +65 6682 3714

[email protected] Suvro SARKAR +65 6682 3720

Chaipat THANAWATTANO +66 2657 7827

[email protected] William SIMADIPUTRA +62 2130 034 939 [email protected]

TAN Jianyuan +603 2604 3919 [email protected] Singapore Research Team +65 6327 2288

Table of Contents Investment Summary 3 Inflexion points: what we want to see before calling a bottom 4 Oil Prices: Supply-demand gap narrowing 9 E&P and Refineries: Winners and losers of oil price rebound 15 Rigbuilders: is it time to turn positive? 17 Oilfield Services: where are we in the sector cycle? 24 Key oil producers in the region 26

Indonesia: Slow energy reform 26

Malaysia: RAPID commitment intact 29

Valuation 31 Company Guides 35

Ezion Holdings 36

Sembcorp Industries 44

Sembcorp Marine 51

Bumi Armada 58

Pantech Group 64

Bangchak Petroleum 71

Elnusa 77

Medco Energi Internasional 84

Page 2

Regional Industry Focus

Oil and Gas

Page 3

INVESTMENT SUMMARY Adjusting our near term oil price expectations. Given the narrowing gap between supply and demand, we now expect oil prices to average between US$45-50/bbl in the second half of 2016 (2H16), a notch higher than YTD average of US$42.55/bbl. In 2017, we expect a further recovery in oil prices to an average of US$50-55/bbl, as convergence of oil supply-demand trends gather momentum in the second half of 2017 (2H17). We believe oil prices will likely move upwards at a faster trajectory towards the end of this decade. Our longer term oil price forecast is currently around US$60-65/bbl, but we reckon there is more upside risk in the longer term than downside risk, in view of the recent massive cuts in capex and marginal cost of oil production. Inflexion points: what we want to see before calling a bottom. Any recovery in the industry must originate from the source of cash flows into the ecosystem – in other words oil prices and oil majors’ capex. Higher cash flows from these ‘top of the waterfall’ sources will then filter down to service players and shipyards through the value chain. Key Inflexion points:

#1: M&A activity leading to industry consolidation. M&A and industry consolidation typically occur at the bottom of the cycle. We think the next 6-12 months will present more consolidation opportunities as more O&G companies are increasingly in distress, creating attractive buyout opportunities

#2: Oil majors increasing capex spend. Oil majors must increase capex budgets, otherwise oilfield equipment services and asset owners will continue to suffer. As oil prices move towards US$60/bbl, we believe oil majors may consider revising up future capex estimates by mid-2017.

#3: Accelerating fleet retirement to scrap older vessels and rigs. For asset owners in particular rig and OSV players, the acceleration of fleet retirement is required to drive market equilibrium in a market which is flooded with oversupply of offshore support vessels.

#4: Higher vessel utilisation and day rates. Rig utilisation typically lagged oil prices by 7-24 months. The lag effect this time could be closer to the two year mark, similar to the 2008 period. This implies a potential recovery for the service asset players only in late-2017 or early-2018.

E&P companies are direct winners but largely priced in;

selective BUYs on laggards. Higher oil prices would directly benefit exploration and production (E&P) companies. However, we believe this has been largely priced in until we see another leg of oil price uplift. The refiners could benefit from near term inventory gains but margin contraction can be expected in the longer term as oil prices creep up. Our top

pick in this segment is BCP (BUY; TP: Bt39) for its undemanding valuation and laggard share price performance. Rigbuilders – a long and harsh winter. While Keppel Corp (Keppel) and Sembcorp Marine (SMM) are trading near AFC valuations, there remains uncertainties revolving the extent of damage from Brazil and potential customer default. In addition, rig orders – the key earnings driver for shipyards, are unlikely to return in the next 1-2 years amidst an unprecedented supply glut. A turnaround for rig orders to return requires the acceleration of rig retirement, cancellations of speculative build and higher oil prices. OSV owners struggling for survival. Many OSV owners are already operating below breakeven levels and it might take 12-24 months before meaningful recovery in utilisation and day rates kick in. As such, the cost competitiveness and balance sheet strength of the OSV players are extremely vital at this stage.

Diversified names are safer picks. Companies have adopted two action plans to combat the weak outlook: Firstly, stepping up their cost-cutting measures and initiatives, and secondly, diversifying beyond the oil & gas sector. SCI (BUY; TP: S$3.10) remains our preferred pick among the large cap O&M plays. SCI offers stability through its utility business and potential re-rating of O&G sector through 61% owned SMM. SCI’s utilities business is valued at an undemanding 0.7x P/B and 8x FY16F PE vs historical mean PE of 11x. Ezion (BUY; TP: S$0.58) has trumpeted its plans to enter the Chinese offshore windfarm market, having forged strategic partnerships with Chinese state-owned power provider, China Huadian and its subsidiary Sinotrans, to facilitate the entry in to the alternative energy business. Malaysia: Commitment on RAPID project intact. While Petronas is cutting capex by RM15–20bn in 2016, and RM50bn over the next four years, its commitment to develop RAPID remains unchanged and we expect a few more petrochemical and tank terminal contracts to roll out for the remainder of 2016. Pantech (BUY; TP: RM0.64) is an ideal proxy to RAPID's ongoing expansion in Pengerang. In large cap space, we continue to like Bumi Armada (BUY; TP: RM0.85) for its undemanding valuation at 2SD below mean, and earnings visibility backed by long-term FPSO contracts. Indonesia: Slow energy reform. Indonesia’s Special Task Force for Upstream Oil and Gas Business (SKK Migas) has admitted that the integration between itself and BP Migas, which has only been 20 months old, will take more time to extract synergies. We also do not see any meaningful incentives from the government in the short term to boost the fortunes of this industry amid the current challenging situation. We have upgraded MEDC (BUY; TP: Rp2,000) to BUY on better crude oil ASP and its new strategy to pursue continuous operational efficiencies and prudent capital allocation.

Page 3

Regional Industry Focus

Oil and Gas

Page 4

Key inflexion points to watch for a recovery As the wave of corporate defaults builds, investor confidence in the sector has waned. For the oil service sector, we believe a recovery is only likely in late-2017 or early-2018, as rebalancing drives oil prices closer to US$60/bbl towards end 2017, incentivising a revival in capex. Amidst the doom and gloom, we highlight several inflexion points that would signal a recovery.

Searching for the tipping point: In this section, we list some of the criteria that we consider are indicators of a bottom at the various stages of the value chain, aligning to companies under our coverage. We note that any recovery in the industry must originate from the source of cash flows into the ecosystem – in other words, the oil price and oil majors’ capex. Higher cash flows from these ‘top of the waterfall’ sources will then filter down to service players and shipyards through the value chain.

Oil & Gas industry recovery and inflexion point waterfall

Source: DBS Bank

Inflexion point #1: Industry consolidation via M&A needs to gather momentum to signal a bottom. M&A and industry consolidation typically occur at the bottom of the cycle, before a gradual improvement in industry fundamentals, driven by a rationalisation of capacity and derived cost synergies. Thus, one of the signals of a cycle bottom is increasing M&A activity. However, we have yet to see a clear pattern of escalating M&A volumes emerging, as seen in the chart below0, where we track the number and size of oil & gas M&A deals over US$100m in value (excluding PE buyouts).

Industry consolidation has been slow, as the industry has just entered into the stage of debt restructuring/bankruptcies while the volatility of oil prices may have caused potential acquirers to throw caution to the wind. The next 6-12 months will present more consolidation opportunities we expect distressed O&G companies to be on the rise, creating attractive buyout opportunities. Oil prices have generally been trending steadily up year-to-date, which should give acquiring managers that marginal boost in confidence.

Cas

h fl

ow d

irect

ion

Oil majors (IOCs and NOCs)

Stage of value chain

Rig owners

OSV owners

Other service players(e.g. ship chandlers)

Subsea vessel owners

Shipyards

Equipment players

Inflextion points

• Shell• ExxonMobil• BP

• Petronas• Pertamina• Saudi Aramco

• Seadrill• Rowan• Ensco

• POSH• PACRA• Ezra

• Ezra• Mermaid Maritime• Technip

• Sinwa Limited• Keppel Corp• Sembcorp Marine• Vard• Nam Cheong

• KTL Global• Nordic Group

Higher capex budgets

Higher utilisation/dayrates

Retirement of older fleet

For shipyards: increase in conversion or newbuilding

contracts

Oil prices >US$60/bbl

M&A/Consolidation to accelerate a recovery

• Bumi Armada• Logindo• Wintermar

Page 4

Regional Industry Focus

Oil and Gas

Page 5

No clear pattern to M&A activity yet

Source: Bloomberg Finance L.P, as of 15 June 2016

Inflexion point #2: Oil majors must increase capex budgets, otherwise service asset owners will continue to suffer. We examined the latest capex budget plans of eight of the largest International Oil Companies (IOCs) to see if the recent rebound in oil prices had loosened their purse strings. The answer was no. There are two salient points to note here: i) Despite oil prices having recovered to close to US$50/bbl from the US$30-40/bbl seen in 1Q16, capex budgets for 2016 have been trimmed even further over the last few months. Shell announced the largest cut on its capex budget for 2016 of 12%, while ConocoPhillips, Total and ExxonMobil announced smaller amounts of less than 5% each.

In aggregate, this means 2016 capex was cut by a further 5%, or US$7bn, over the last few months.

ii) 2017 and 2018 capex budgets are lower than 2016. We estimate that 2017 capex budgets are 10% lower than 2016’s quantum based on the latest disclosures by the IOCs, while 2018 capex looks to be flat y-o-y.

However, given that we are expecting oil prices to average between US$50-55/bbl in 2017, and that capex plans for 2017/18 are likely flexible rather than cast in stone, we think that a bottom in 2017 is possible before a recovery in 2018, in terms of capex spend at least. As oil prices move towards US$60/bbl, we believe oil majors may consider revising up future capex estimates by mid-2017. In the meantime, service players should continue to face pressure on utilisation and dayrates, as many of these players that added assets to their fleets in the boom years will still be fighting over a smaller pie during the trough years of 2016/17. Oil major Eni, in its latest 2016-2019 strategy presentation, made this explicit: it said that “it plans to reduce its total rig fleet by 33% (from 109 to 73) from 2014 to 2017, while the average dayrate on these rigs should be 51% lower in 2017 compared to 2014, at US$4.5m/day.” It plans to renegotiate 1,600 service contracts in 2016; which is bad news for rig owners and by association, OSV owners.

Capex in 2016 expected to be down 21% vs. 2015, and down 37% vs. 2014 in aggregate

Source: Companies

05

101520253035404550

2014 Actual 2015 Actual 2016 target as of Feb'16 2016 target as of Apr/May/Jun'16 2017 2018

-34% -35%

-40%

-26%-67%

-29%

-40%

-34%

*Assuming Shell and BG had merged as of 1 Jan 2014*ENI: using the average of 37bn capex over its 4-year programme (2016-2019)

(in US$bn)

0

5

10

15

20

25

30

35

40

45

50

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16

Value (US$m) No. of deals >US$100m

Skewed by US$53bn Shell-BG megadeal Skewed by US$33bn

Energy-Transfer-Williams megadeal

Total Deal Value (US$m) No. of Deals

Page 5

Regional Industry Focus

Oil and Gas

Page 6

Source: Companies, DBS Bank estimates Inflexion point #3: Higher rig utilisation and day rates are needed, but these may only materialise in 2018. We look at the last two oil price crashes of comparable magnitude to the current downturn, namely the 1997-1998 crash caused by the Asian Financial Crisis (AFC), and the 2008 crash following the onset of the Global Financial Crisis (GFC). During the 1997-1998 period, rig utilisation lagged oil prices by seven months in terms of bottoming out, while in the 2008 period, rig utilisation took two years longer than oil prices to bottom out. A large influx of newbuild rigs over the latter period – a supply-side pressure that was not present during the AFC period – prolonged the lag effect. Another key factor to consider is how soon oil prices hit US$60/bbl again, which is the approximate level needed to incentivise greater exploration and development activity from oil majors. Piecing the information together, given that global rig orderbook levels remain elevated in 2016 and that we are predicting average oil prices of US$60/bbl only from 2018 and beyond, we think the lag effect this time could be closer to the two year mark, similar to the 2008 period. This implies a potential recovery for the service asset players only in late-2017/early-2018 at best. Brent price vs. jackup rig utilisation (AFC – 1997-1998)

Source: Bloomberg Finance L.P., IHS Petrodata

Brent price vs. jackup rig utilisation (GFC – 2008)

Source: Bloomberg Finance L.P., IHS Petrodata

Offshore rig utilisation – waiting for the bottom

Source: IHS Petrodata

(in US$ bn) 2014 Actual 2015 Actual 2016 target as

of Feb'16 2016 target as of Apr/May/Jun'16 2017 2018

Chevron 40.3 34 25-28 25-28 17-22 17-22 Shell + BG* 44.4 35.5 33 29 25-30 25-30 BP 22.9 18.7 18 17 15-17 - ConocoPhillips 17.1 10.1 6.4 5.7 - - TOTAL 26.0 23 19 <19 17-19 17-19 ExxonMobil 38.5 31.1 23.2 23.2 22 - Statoil (NOK bn) 19.6 14.7 13 13 - - ENI 15.3 11.0 9.3 9.3 9.3 9.3

Total (US$ bn) 207.0 165.2 137.0 130.8

0.00

5.00

10.00

15.00

20.00

25.00

30.00

35.00

50556065707580859095

100

Jan

1997

Apr

199

7

Jul 1

997

Oct

199

7

Jan

1998

Apr

199

8

Jul 1

998

Oct

199

8

Jan

1999

Apr

199

9

Jul 1

999

Oct

199

9

Jan

2000

Apr

200

0

Jul 2

000

Oct

200

0

Jan

2001

Jackup utilisation (%, LHS) Brent Price

7-month lag for bottoming out of utilisation rates

0.00

20.00

40.00

60.00

80.00

100.00

120.00

140.00

160.00

50

55

60

65

70

75

80

85

90

95

Jul 2

008

Oct

200

8

Jan

2009

Apr

200

9

Jul 2

009

Oct

200

9

Jan

2010

Apr

201

0

Jul 2

010

Oct

201

0

Jan

2011

Apr

201

1

Jul 2

011

Oct

201

1

Jan

2012

Apr

201

2

Jul 2

012

Jackup utilisation (%, LHS) Brent Price

2-year lag for bottoming out of utilisation rates

0

20

40

60

80

100

120

50%55%60%65%70%75%80%85%90%95%

100%

Jan

2014

Mar

201

4

Ma y

201

4

Jul 2

014

Sep

2014

Nov

201

4

Jan

2015

Mar

201

5

May

201

5

Jul 2

015

Sep

2015

Nov

201

5

Jan

2016

Mar

201

6

Ma y

201

6

Jackup Semisub Drillship Brent (US$/bbl)

Oil pr ice trough in Jan '16

~2 year lagunt il rig

re covery?

Page 6

Regional Industry Focus

Oil and Gas

Page 7

Inflexion point #4: For OSV owners, accelerating fleet retirements of older vessels needed to reduce severe oversupply situation. But these have been few and far between due to low steel prices and cost of scrappage. OSV utilisation rates have fallen to about 50% while day rates have also plunged by at least 40% since the onset of the oil price collapse; many OSV owners are operating below breakeven levels. The anaemic operating environment has been a function of lower demand – from reduced exploration and development activity from oil majors – and oversupply resulting from overinvestment in OSVs during the heydays from 2011 to mid-2014. While the demand-side factors cannot be controlled from the perspective of OSV owners, supply-side factors can be managed especially if the industry acts collectively. In our view, retirement of vessels sends a stronger signal of waning supply-side pressures than stacking, since warm stacked vessels can be brought back to the market fairly quickly, while cold stacked vessels can also be put back to work in the event of attractive contracts. However, we note that retirement of vessels has been minimal since 2014: a total of 78 AHTS and PSVs have been retired since the beginning of 2014 (all of these were at least 30 years old), which is paltry compared to the 1,400+ vessels that are stacked at the moment. We think this has been motivated by i) low scrap values for vessels; and ii) a general reluctance to let go of assets at the bottom of the cycle as vessel owners retain some hope of better times ahead. What could help catalyse retirements? While it is difficult to predict the extent of future retirements, we think two factors will help drive an acceleration in the numbers: Firstly, as the OSV market languishes, older vessels – which account for the lion’s share of stacked vessels – are finding it harder to compete with younger vessels offering competitive day rates; clients are increasingly asking for vessels <15 years of age. Thus, diminished work prospects should drive these vessels to the scrapyard. Secondly, consolidation will help push older vessels out of the market either via a concerted effort by the larger players to retire their older vessels, or via a marginalisation of smaller players with old vessels, such as Swissco. Cumulative number of AHTS and PSVs retired since 2014

Source: Clarksons

AHTS fleet status as of mid-June 2016

Source: Clarksons PSV fleet status as of mid-June 2016

Source: Clarksons Global OSV owner ROEs at all-time lows as the OSV oversupply situation has worsened over the last 1-2 years. As SGX-listed OSV owners generally do not have an operating history long enough since listing to track performance through past crises, we have aggregated the earnings of the global players i.e. Tidewater, SEACOR and Gulfmark Offshore. We have compared earnings to various other key metrics in an attempt to glean some insights. We note the following:

i) For OSV owners, this downturn is the worst in at least three decades. During past periods of crisis, OSV owners’ pre-tax ROE was generally in the positive range. This time, it has trended in increasingly negative territory for about 1.5 years. This agrees with our channel checks as OSV owners we have met are generally in agreement that this crisis is the most severe in a long while.

ii) OSV owners’ profits generally take between 6-9 quarters to reach a trough but have not always rebounded as strongly as rig fundamentals (due to rising OSV-to-rig ratios).

0

1

2

3

4

5

6

7

8

0

10

20

30

40

50

60

70

80

90

AHTS PSV No. of retirements (monthly, RHS)

0 200 400 600 800 1000 1200

Orderbook

0-5

6-10

11-15

16-20

20-25

>26

Stacked In Service Under Construction Retired since Beg-2014

Working fleet count: 2,280Stacked fleet count: 722Retired since Jan 2014: 72

Orderbook as a % of working fleet: 8.2%

0 200 400 600 800 1000

Orderbook

0-5

6-10

11-15

16-20

20-25

>26

Stacked In Service Under Construction Retired since Beg-2014

Working fleet count: 1,774Stacked fleet count: 737Retired since Jan 2014: 24

Orderbook as a % of working fleet: 12.5%

Page 7

Regional Industry Focus

Oil and Gas

Page 8

iii) While the orderbook-to-fleet ratio (of Anchor Handling Tug Supply (AHTSs) and Platform Supply Vessel (PSVs) in aggregate) has eased to ~8% currently, deliveries of newbuild OSVs over the last few years have depressed profitability even while oil prices were at the US$100/bbl levels. OSV-to-rig ratios are at an all time high of 6.6x (as at June 2016). Thus, unless there is a mass exodus of old vessels to the scrapyard, even in a recovery scenario we may not see a strong recovery in ROEs.

Going back to basics, the value of a company is the present value of its future cash flows. ROEs have been depressed since 2008 due to oversupply and this pressure will persist unless owners retire their old vessels to reduce the supply and/or demand surges alongside an oil price spike. Thus, even a modest oil price recovery past the US$60/bbl mark may not be enough to support a case for investment in OSV companies – the supply-side must be addressed in tandem.

OSV-to-rig ratio (PSVs + AHTS) at an all-time high

Source: Clarksons, ODS Petrodata

AHTS-to-rig ratio versus AHTS orderbook-to-fleet ratio

Source: Clarksons, ODS Petrodata PSV-to-rig ratio versus PSV orderbook-to-fleet ratio

Source: Clarksons, ODS Petrodata

Global OSV owner profits in the wake of oil price crises: 6 – 9 quarters’ time from oil price trough to earnings trough

Source: Companies, Clarksons, ODS Petrodata

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

3.00

3.50

4.00

4.50

5.00

5.50

6.00

6.50

7.00

1996

-Jan

1997

-Feb

1998

-Mar

1999

-Apr

2000

-Ma y

2001

-Jun

2002

-Jul

2003

-Aug

2004

-Sep

2005

-Oct

2006

-Nov

2007

-Dec

2009

-Jan

2010

-Feb

2011

-Mar

2012

-Apr

2013

-May

2014

-Jun

2015

-Jul

Orderbook to fleet ratio (%) - RHS OSV-to-rig ratio (x) - LHS

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

20

40

60

80

100

120

Jun

1989

Feb

1990

Oct

199

0Ju

n 19

91Fe

b 19

92O

ct 1

992

Jun

1993

Feb

1994

Oct

199

4Ju

n 19

95Fe

b 19

96O

ct 1

996

Jun

1997

Feb

1998

Oct

199

8Ju

n 19

99Fe

b 20

00O

ct 2

000

Jun

2001

Feb

2002

Oct

200

2Ju

n 20

03Fe

b 20

04O

ct 2

004

Jun

2005

Feb

2006

Oct

200

6Ju

n 20

07Fe

b 20

08O

ct 2

008

Jun

2009

Feb

2010

Oct

201

0Ju

n 20

11Fe

b 20

12O

ct 2

012

Jun

2013

Feb

2014

Oct

201

4Ju

n 20

15Fe

b 20

16

Oil Crises OSV orderbook to fleet ratio (%)

Brent (US$/bbl) - LHS Jackup rig utilisation (%, LHS)

OSV owners agg. ex-impairment pre-tax ROE - RHS

6 quarters

9quarters

9quarters

No. of quarters = time from oil price trough to OSV earnings trough

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

35.0%

40.0%

2.002.202.402.602.803.003.203.403.603.80

1996

-Jan

1997

-Feb

1998

-Mar

1999

-Apr

2000

-May

2001

-Jun

2002

-Jul

2003

-Aug

2004

-Sep

2005

-Oct

2006

-Nov

2007

-Dec

2009

-Jan

2010

-Feb

2011

-Mar

2012

-Apr

2013

-May

2014

-Jun

2015

-Jul

AHTS orderbook to fleet ratio (%) - RHS

AHTS-to-rig ratio (x) - LHS

0.0%

5.0%

10.0%

15.0%

20.0%

25.0%

30.0%

1.00

1.50

2.00

2.50

3.00

3.50

1996

-Jan

1997

-Feb

1998

-Mar

1999

-Apr

2000

-Ma y

2001

-Jun

2002

-Jul

2003

-Au g

2004

-Sep

2005

-Oct

2006

-Nov

2007

-Dec

2009

-Jan

2010

-Feb

2011

-Mar

2012

-Apr

2013

-Ma y

2014

-Jun

2015

-Jul

PSV orderbook to fleet ratio (%) - RHS PSV-to-rig ratio (x) - LHS

Page 8

Regional Industry Focus

Oil and Gas

Page 9

Oil Prices: Supply-demand gap narrowing We believe oil market is set on recovery path and expect oil prices to average US$45-50/bbl in 2016; US$50-55/bbl in 2017; and US$60-65/bbl in the longer term. Overall sentiment on oil market has turned more upbeat since May 2016, driven by rebalancing with supply outages in Canada and Nigeria as well as better-than-expected demand for petroleum products from India and China. YTD-2016, Brent crude oil price has averaged around US$42.55/bbl. While prices are currently pulling back from the recent highs of US$52/bbl, with the USD appreciation and gradual resumption of supplies from Canada, we believe oil price is unlikely to test the previous lows seen earlier this year as US shale production seems to have been adequately tempered by the fall in oil prices. However, upside will be capped by overflowing inventory levels worldwide. Adjusting our near term oil price expectations. Given the narrowing gap between supply and demand, we have raised our oil price forecasts. We now expect oil prices to average between US$45-50/bbl in 2H16. In the near term, oil prices are likely to remain below the recent highs of c.US$50/bbl as production outages from Canada, Nigeria, and Libya are gradually restored, putting supply back to the market. The Brexit worries has also pushed USD index higher and the USD strength will also continue to weigh on oil prices for the rest of this year. OPEC’s refusal to vary its production stance and the fast rising supplies from Iran will offset the decline in shale production in 2016 and will continue to delay the rebalancing of the market.

In 2017, we expect a further recovery in oil prices to an average of US$50-55/bbl, driven by the convergence of oil supply-demand trends, which should gather momentum during 2H17. Upside risks could stem from the possibility of heightened tensions in the Middle East, leading to supply chain disruptions. More bullish longer term forecasts. We expect oil prices to move upwards at a faster trajectory towards the end of this decade. Firstly, of course, we consider the fact that more than US$370bn worth of capex for 2016 and 2017 had been cut by upstream developers – according to industry consultant Wood Mackenzie – and further cuts to 2020 will mean that close to 3mbpd (million barrels per day) of supply that was supposed to come onstream by 2020 will now only flow after that. This will help the supply demand equation as we approach 2020. Also, the need to develop oil production in more expensive areas – and the cost of the most expensive last barrel needed to meet demand – should continue to support oil prices. On the cautious side, we note that technological advances have rendered extraction of oil (read: shale oil) more flexible to demand changes with shorter lead time to production, and the global focus on climate change will limit the future exploitation of fossil fuels to an extent. Our longer term oil price forecast is currently around US$60-65/bbl, but we reckon there is more upside risk in the longer term than downside risk.

Oil price trends

Source: Bloomberg Finance L.P., DBS Bank

0

20

40

60

80

100

120

140

Brent WTI

Brent hit a high of US$115/bbl on 19-Jun-14 before collapsing

Brent rallied to US$52/bbl level in May 2016, but seems to have run out steam thereafter

DBS forecast for Brent:2H-2016 average – US$45-50/bbl2017 average – US$50-55/bbl

Long-term price – US$60-65/bbl

Page 9

Regional Industry Focus

Oil and Gas

Page 10

Supply demand curve has narrowed earlier than expected owing to the supply chain disruptions in various parts of the world in 2Q16, which are yet to be fully resolved, as well as slightly better than expected demand growth, especially from China and India in 2016. Global oil inventory build-up is thus likely to slow from 1.8-2.0mmbpd in 2015 to 0.8-1.0mmbpd in 2H16, and reach more balanced levels probably by the middle of 2017. We thus believe that the period of growing inventory looks to be behind us, and it is likely that sustained inventory drawdowns could happen from 2H17 onwards, lending support to slowly recovering oil prices. Global oil production and consumption trend and

forecasts

Source: US Energy Information Administration (EIA), DBS Bank Production outage was the main reason for the recent rise in oil price above US$50/bbl. Supply outages from Canada, Nigeria and Ghana amounting to almost 1.5mmbpd in May 2016 wiped out almost the entire supply-demand gap and along with signals of a production slowdown from the US, leading to a sharp rally in oil prices during the month. Raging forest fires in Canada cut about 1mmbpd of production or 25% of Canada’s production at the peak (0.8mmbpd on average in May 2016). The wildfires have now been contained and production should gradually come back to the market. Over in Nigeria, militant attacks on pipeline infrastructure have affected production severely in 2016. While Nigeria’s outages decreased in June, they still remained high at 0.6mmbpd, according to EIA estimates. While exports from Shell’s Bonny terminal are resuming, another 0.3mmbpd of the disrupted volume remains under force majuere. These unplanned outages have led to an earlier than expected narrowing of the supply-demand curve but the situation may not be sustainable, not with the existing inventory overhang and OPEC production still at record levels. Meanwhile, US production has been falling, as expected. EIA estimates that crude oil production in the US in May 2016 averaged 8.7mmbpd, which is more than 0.2mmbpd below the April 2016 level, and approximately 1mmbpd below the peak 9.7mmbpd level reached in April 2015. Even though

productivity levels have been continuously improving, it is not enough to offset the sharp fall in rig count in the US – down more than 75% from the high of 1929 rigs in November 2014 to 462 working rigs currently. Overall, average US production is expected to decline by 0.6mmbpd y-o-y in 2016 and 0.2mmbpd in 2017. US – monthly production levels Source: EIA, DBS Bank But don’t discount a rebound. As we highlighted in the previous paragraph, productivity gains across the seven main shale oil producing areas in the US has been relentless, as drillers have applied new, innovative technologies to increase output and reduce drilling time. As a result, weighted average productivity per rig in the seven major shale oil producing regions in the US has surged 68% since Oct 2014, when rig counts began their steep decline. This is not a new phenomenon. Tight oil has boasted steady productivity gains since 2007, as evident from the chart below. These productivity gains had offset the decline in drilling rigs in the early stages of this crisis but expiry of hedges, capex reductions and rising balance sheet stress since 2H15 have limited the extent to which productivity gains can make an impact. US weighted average productivity per rig in 7 major shale

regions

Source: EIA, DBS Bank

80.00

82.00

84.00

86.00

88.00

90.00

92.00

94.00

96.00

98.00

100.00

1Q10

3Q10

1Q11

3Q11

1Q12

3Q12

1Q13

3Q13

1Q14

3Q14

1Q15

3Q15

1Q16

3Q16

1Q17

3Q17

World production (mmbpd) World consumption (mmbpd)

7.0

7.5

8.0

8.5

9.0

9.5

10.0

Jan-

2014

Mar

-201

4

Ma y

-201

4

Jul-2

014

Sep-

2014

Nov

-201

4

Jan-

2015

Mar

-201

5

May

-201

5

Jul-2

015

Sep-

2015

Nov

-201

5

Jan-

2016

Mar

-201

6

mmbpd

0

100

200

300

400

500

600

Jan-

07

Jul-0

7

Jan-

08

Jul-0

8

Jan-

09

Jul-0

9

Jan-

10

Jul-1

0

Jan-

11

Jul-1

1

Jan-

12

Jul-1

2

Jan-

13

Jul-1

3

Jan-

14

Jul-1

4

Jan-

15

Jul-1

5

Jan-

16

boepd per rig

Page 10

Regional Industry Focus

Oil and Gas

Page 11

However, what this means is that shale oil can make a faster than ever comeback if oil prices move closer to desirable levels (US$50-60/bbl) and rig counts improve. Indeed, rig counts in the US have gone up in 7 of the last 8 weeks in response to the recent oil price rally seen in May-June 2016. OPEC again fails to reach consensus on output. OPEC members have failed to agree on setting a curb on production levels during their regular semi-annual meeting held in Vienna last week. This is not surprising given Iran’s refusal to participate in a production freeze, and the recovery of oil prices to more reasonable US$50/bbl levels, which may lead OPEC members to think that their market share strategy is paying off. During the meeting, the only decision taken was to appoint Nigerian delegate Mohammed Barkindo as OPEC’s new secretary general, replacing Abdullah al-Badri of Libya. The much vaunted production “freeze” did not work out. Officials from the two of the world’s largest oil producing countries – Saudi Arabia and Russia – along with other OPEC members had met in Doha earlier in April 2016 to formalise a deal to freeze production, but were not able to reach a conclusion. Recently, the Russian Energy Minister indicated that possible coordination with OPEC can be ruled out after the failure earlier in the year. November OPEC meeting unlikely to be any different. When OPEC members meet again in November, it will mark an entire year without an official production target. It seems OPEC has largely disowned its role of swing producer and is happy to let the market balance itself. OPEC production remains above 30mmbpd in recent months. OPEC production has breached the 32mmbpd mark consistently since 2H15, much higher than the target of 30mmbpd set by member nations earlier. Iraq and Saudi Arabia led the initial increase but Iran has taken up the mantle in 2016, following the removal of Western-imposed sanctions earlier this year. Iran is expected to ramp up production by up to 1mmbpd over the next two years. In addition, it has around 42mmbbls of floating oil storage. OPEC production trends

Source: Bloomberg Finance L.P., DBS Bank

Iranian supply ramp up YTD in 2016 faster than expected. Iran – fresh off the lifting of sanctions in early 2016 – continues to push hard to regain lost market share. Iran has already ramped up output to 3.6mmbpd by May 2016, up 0.8mmbpd since the beginning of the year. According to International Energy Agency (IEA) estimates, Iranian exports of crude oil in April were just under 2mmbpd, nearly double the volume at the start of the year. Exports rose to 2.1mmbpd in May, nearly touching pre-sanctions levels. Provisional loading schedules for June indicate that recent levels are being maintained with crude shipments of more than 2mmbpd. Before sanctions were tightened in mid-2012, Iran's crude oil exports totalled about 2.2 mmbpd, and that level should be reached by 2017. Iran crude oil supplies

Source: Bloomberg Finance L.P., DBS Bank

Demand growth in 2016 has exceeded expectations so far. The EIA expects oil consumption to grow by 1.4mmbpd in 2016 and 1.5mmbpd in 2016. This is slightly higher than previous demand forecasts, largely due to demand trends emanating from India and China in the first half of the year. Overall, Asia-Pacific (ex-Japan) is expected to contribute more than 1.0mmbpd of incremental demand over the next couple of years. Among developed economies, growth from US and South Korea is expected to more than offset demand declines in Japan and Europe. Downside risks will stem from the Brexit situation, as it is unclear how this will affect economic growth in the UK and Europe, going forward. India takes the lead in 2016. India is expected to lead oil demand growth in 2016/17 with about 0.4mmbpd of incremental demand p.a., driven by increased demand from the transportation and petrochemical sectors. Globally, India’s GDP growth is one of the bright spots, with expectations of 7.4-7.5% growth over the next two years. The March-June quarter of 2016 (1QFY16-17) saw oil demand growing at 7.8%, the fastest clip for any first quarter in a decade. Diesel consumption was up 4.7% while petrol consumption was up 10% y-o-y during the quarter. As it stands, India is forecast to overtake Japan as the third-largest oil user this year and the International Energy Agency (IEA) estimates that India will be

2.5

2.7

2.9

3.1

3.3

3.5

3.7

Jan-

14

Mar

-14

May

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

Ma y

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

Ma y

-16

mmbpd

25

26

27

28

29

30

31

32

33

Jan-

14

Mar

-14

Ma y

-14

Jul-1

4

Sep-

14

Nov

-14

Jan-

15

Mar

-15

Ma y

-15

Jul-1

5

Sep-

15

Nov

-15

Jan-

16

Mar

-16

Ma y

-16

mmbpd

Page 11

Regional Industry Focus

Oil and Gas

Page 12

fastest growing crude customer in the world through 2040, adding 6.0mmbbls of demand, compared to China’s 4.8mmbbls. Increasing income levels for the middle class and the government’s focus on infrastructure building are the key drivers behind this additional demand. India oil consumption trends and forecast

Source: EIA, DBS Bank India’s domestic automobile sales is a key driver

Source: Society of Indian Automobile Manufacturers, DBS Bank Importance of China may be diminishing but in no way fading. China has been the key driver of oil demand for the last decade and more, responsible for close to 50% of all incremental demand from 2005-15. China now accounts for more than 12% of global oil consumption – compared to 8% in 2005 – as oil consumption grew at 5.2% CAGR over the last decade, compared to 1.2% CAGR globally. However, as the manufacturing-based economy transitions to a service-based one, slowdown in industrial activity will have a negative impact on oil demand, and hence, China is expected to lag behind its historical growth rate in future.

China oil consumption trends

Source: EIA, DBS Bank But that does not mean Chinese demand is fading. Chinese oil demand still continues to grow, unlike demand for other commodities like coking coal, iron ore and copper which are mostly used for industrial activities. It is still expected to grow at around 0.4mmbpd in 2016/17, higher than the previous estimate of 0.3mmbpd. Demand is still growing from sectors like petrochemicals and transport, which will increasingly take the bigger sections of the pie. China oil consumption by sector (2015)

Source: IEA, DBS Bank Boost from strategic reserves may be short lived though. We believe the strength in Chinese oil demand since 2015 and even in 1H16 may be partly driven by the government’s strategy of filling up strategic reserves taking advantage of the low oil prices. The Chinese government rarely releases any numbers on strategic reserves, but press reports indicate that the goal is to build up reserves of around 500mmbbls by 2020. It is unclear how much capacity has been built till now, but it announced that strategic reserves had almost doubled within a year to close to 200mmbbls at end-2015. By the end of 2016, reserves could be filled up to current capacity levels, which would not leave much upside on the table. Thus, we expect oil demand from China in 2017 to slow down a notch from 2016 levels.

7%

8%

9%

10%

11%

12%

13%

6,000

7,000

8,000

9,000

10,000

11,000

12,000

05 06 07 08 09 10 11 12 13 14 15

China Petroleum Consumption (mbpd)

% global consumption from China

CAGR 5.2%

Petrochem19%

Road Transport

22%

Aviation5%

Industrial Use29%

Others25%

0500

1,0001,5002,0002,5003,0003,5004,0004,5005,000

05 06 07 08 09 10 11 12 13 14 15 16F 17F

India Petroleum Consumption (mbpd)

-

5

10

15

20

25

2010-11 2011-12 2012-13 2013-14 2014-15 2015-16

million units

Passenger Vehicles Commercial VehiclesThree Wheelers Two Wheelers

CAGR 5.7%

Page 12

Regional Industry Focus

Oil and Gas

Page 13

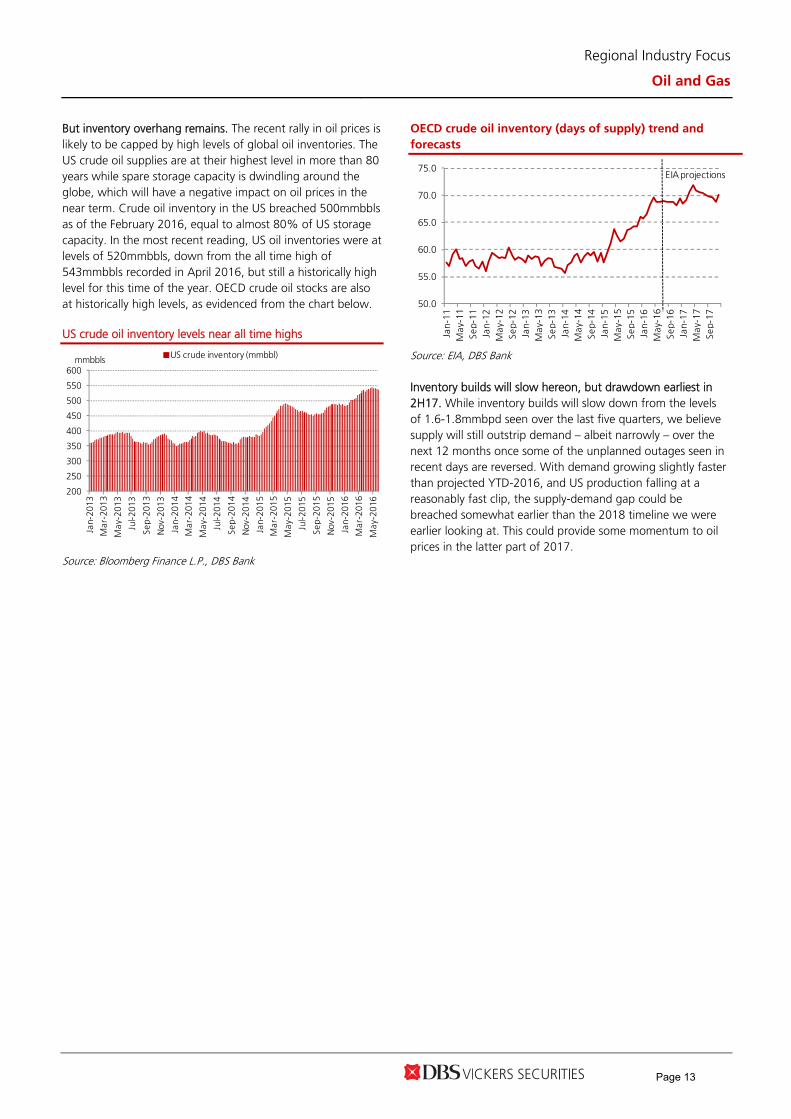

But inventory overhang remains. The recent rally in oil prices is likely to be capped by high levels of global oil inventories. The US crude oil supplies are at their highest level in more than 80 years while spare storage capacity is dwindling around the globe, which will have a negative impact on oil prices in the near term. Crude oil inventory in the US breached 500mmbbls as of the February 2016, equal to almost 80% of US storage capacity. In the most recent reading, US oil inventories were at levels of 520mmbbls, down from the all time high of 543mmbbls recorded in April 2016, but still a historically high level for this time of the year. OECD crude oil stocks are also at historically high levels, as evidenced from the chart below. US crude oil inventory levels near all time highs

Source: Bloomberg Finance L.P., DBS Bank

OECD crude oil inventory (days of supply) trend and

forecasts

Source: EIA, DBS Bank Inventory builds will slow hereon, but drawdown earliest in 2H17. While inventory builds will slow down from the levels of 1.6-1.8mmbpd seen over the last five quarters, we believe supply will still outstrip demand – albeit narrowly – over the next 12 months once some of the unplanned outages seen in recent days are reversed. With demand growing slightly faster than projected YTD-2016, and US production falling at a reasonably fast clip, the supply-demand gap could be breached somewhat earlier than the 2018 timeline we were earlier looking at. This could provide some momentum to oil prices in the latter part of 2017.

50.0

55.0

60.0

65.0

70.0

75.0

Jan-

11M

ay-1

1Se

p-11

Jan-

12M

ay-1

2Se

p-12

Jan-

13M

ay-1

3Se

p-13

Jan-

14M

ay-1

4Se

p-14

Jan-

15M

ay-1

5Se

p-15

Jan-

16M

ay-1

6Se

p-16

Jan-

17M

ay-1

7Se

p-17

EIA projections

200

250

300

350

400

450

500

550

600

Jan-

2013

Mar

-201

3

Ma y

-201

3

Jul-2

013

Sep-

2013

Nov

-201

3

Jan-

2014

Mar

-201

4

Ma y

-201

4

Jul-2

014

Sep-

2014

Nov

-201

4

Jan-

2015

Mar

-201

5

May

-201

5

Jul-2

015

Sep-

2015

Nov

-201

5

Jan-

2016

Mar

-201

6

Ma y

-201

6mmbbls US crude inventory (mmbbl)

Page 13

Regional Industry Focus

Oil and Gas

Page 14

Summary of the impact of the key structural issues so far

Key Issues What has happened since our last report Impact

OPEC Response No curb on production; official production target remains discarded as seen during the last two general meetings; not a good sign as far as supply is concerned. Production has consistently been above 32mmbpd since 2H15, higher than the earlier 30mmbpd cap set by member nations. Earlier talks of a production “freeze” led by Saudi and Russia have completely fallen through.

Profile of US shale production

Shale oil production in the US has been declining gradually since April 2015. Overall US production expected to decline by 0.6mmbbls in 2016 and 0.2mmbls in 2017. The sharp and continuous decline in number of shale rigs has only recently come to a halt, but the trend will need to be closely monitored.

However, increased productivity per well, lower costs and relatively short lead time of bringing unfinished wells into production means that shale production is flexible and can adjust to oil price movements faster than conventional oil. This can cap eventual oil price recovery.

Inventory buildup US crude inventories continue to be near record levels. Overall OECD inventory levels also continue to rise and spare storage capacity is dwindling across the globe. This will thus continue to exert pressure on oil prices in the near future. While inventory drawdowns are expected to start around 2H17, it could take up to three years to reach historical normalised levels. Thus, a sharp recovery in oil price beyond 2017 seems unlikely.

Structural changes in global oil demand

Lower oil prices have not resulted in any significant pickup in demand in the developed world. Climate change concerns, move towards cleaner emissions also weigh on incremental fossil fuel use. A balance in demand-supply could only be achieved in the later part of 2017 and beyond, based on current estimates.

Role of China and India in oil demand

China is still expected to add close to 0.4mmbpd incremental oil demand in 2015/16, but will likely lose the biggest incremental oil consumer tag to India. The ongoing transition to a service-based economy will have repercussions on oil demand but opportunistic additions to strategic reserves continue to support Chinese oil imports in 2016. India is meanwhile emerging as the leader for oil demand, and demand from both countries has been better than expected YTD in 2016.

US dollar strength The US dollar index has been climbing since Brexit concerns have led to a flight from the GBP and Euro currencies. Expectations of US rates are also rising, and hence the corresponding strength in US dollar could be further negatives for oil price.

Geopolitical issues Disruptions to oil supply chain in Nigeria and Libya have already led to significant unplanned outages in 2Q16. Further escalation of tensions in these areas, as well as in the Middle East could lead to higher oil prices.

Response from global oil majors

Capex budgets have already been cut substantially since the oil price collapsed. Oil majors have reduced capex by 35% on average when comparing 2016 budgets with 2014. Wood Mackenzie estimates that close to US$1trillion of global upstream investment will have been cut from 2015-2020. This should help oil prices rise faster towards the end of the decade.

Source: DBS Bank

Page 14

Regional Industry Focus

Oil and Gas

Page 15

E&P and Refineries: Winners and losers of oil price rebound

E&P companies are direct winners but this is largely priced in. Oil price recovery would directly benefit E&P companies, especially those with a higher portion of liquid products (crude oil and condensate) as there is usually a time lag for natural gas price adjustments, based on the long-term pricing formula. For instance, with liquid products accounting for only 30% of its total volume, PTTEP’s average selling price (ASP) has declined by 46% during 2014-1Q16 while Dubai oil price weakened 71% in the same period. Hence, the benefits from rising oil prices could be lower than those with a higher portion of liquid products, whose selling prices are directly linked to crude oil prices. For PTTEP, it normally takes 6-12 months for natural gas selling prices to reflect oil price changes. The benefits of higher oil prices could be diluted by higher operating cost, as cost negotiations with service companies would be more difficult. PTTEP’s average selling price vs. Dubai crude oil price

0

20

40

60

80

100

120

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16

PTTEP's average selling price Dubai oil priceUS$/BOE, US$/bbl

Source: PTTEP, Bloomberg Finance L.P., DBS Bank Risk of asset impairments is likely to ease. E&P companies could also benefit from lower risk of impairment charges that they faced during the oil price downtrend from mid-2014 to late-2015. Note that PTTEP booked impairment charges of US$2.4bn in 2014-15, mainly for its high-cost overseas assets, accounting for c.10% of its total assets. Nonetheless, these impairment charges would not be reversed when oil prices rise but will be recognised as higher revenue from higher selling prices. The correlation between oil prices and share prices of companies in the E&P sector has declined recently from >90% to 85%±, as the market has turned more bullish on them, which could be driven by higher oil prices. We believe current share prices have largely priced in the positive impact on earnings prospects. The upside to share price should be limited in the near term until there is a demand-supply rebalancing that takes place in 2H16, as demand growth would signal a more bullish trend.

High correlation between oil and PTTEP’s share price

0

20

40

60

80

100

120

140

0

20

40

60

80

100

120

140

160

180

200

Jan-12 Jan-13 Jan-14 Jan-15 Jan-16

PTTEP share price Brent oil price (RHS)

Bt/share US$/bbl

Source: Bloomberg Finance L.P., DBS Bank Lower gross refining margin could be offset by stock gains. Oil refiners could benefit from higher oil prices in the near term, mainly from inventory gains as crude oil prices have increased by nearly US$10/bbl from the end of 1Q16. We estimate that these companies could book stock gains of c.US$3/bbl in 2Q16. This would offset lower gross refining margins (GRM) during the quarter of US$2.7/bbl, based on Singapore GRM of Hydrocracking Unit over Dubai crude oil. Nonetheless, higher crude oil prices mean lower margins for oil refiners due to higher processing cost, mainly for fuel used in refinery, and losses in the process. This accounts for 3-6% of total crude intake, depending on the integration of the process. The wider spread for light-heavy crude oil would also increase the processing cost of oil refiners, as most Asian oil refiners still require lighter crude to achieve higher yield of light to middle distillates products (gasoline, diesel and jet fuel). As light crude oil supply enters the market at a slower pace on the back of a decline in US shale oil production, the spread of light and heavy crude oil has widened from an average US$1.2/bbl in 2015 to US$3.4/bbl in 1H16. Light-heavy crude spread

-1

0

1

2

3

4

5

6

Jan-13 Jun-13 Nov-13 Apr-14 Sep-14 Feb-15 Jul-15 Dec-15 May-16

US$/bbl

Source: Energy Policy and Planning Office, DBS Bank

Page 15

Regional Industry Focus

Oil and Gas

Page 16

Impact of lower oil prices on Thailand E&P companies and refineries

Segment/ company

Impact

Earnings sensitivity to

+US$1 change in oil

price

Share price correlation to oil price (6-month)

E&P

PTTEP PTTEP’s earnings would be bolstered by higher oil prices, as 30% of its total sales volume is liquid products (crude oil and condensate), whose prices are linked to Dubai crude oil price (+37% YTD). Assuming a decline of gas price from US$6.09/mmbtu in 1Q16 to c.US$5.9/mmbtu in 2Q16, we estimate its average selling price to increase by 7% q-o-q to US$37.4/BOE. The pricing formula of its gas product is 30% linked to fuel oil price, with a time lag of 6-12 months (which varies for each producing field). The next major price adjustment in Oct 16 is for its key operating assets, i.e. Bongkot and Arthit gas fields. With a higher average Brent oil price assumption of US$45-55/bbl for 2016-18F vs US$35-45/bbl previously, we have revised up our earnings estimates for 2016/17/18F by 80%/73%/58%. We assume that the company’s efforts to reduce operating cost when oil prices are low could sustain its low operating cost, hence the impact of higher oil prices on profitability could be substantial. Our 12-month TP was raised to Bt86/share to reflect this positive development for oil prices, based on DCF valuation with a long-term Brent oil price assumption of US$60/bbl. We upgrade our rating from FULLY VALUED to HOLD.

+5% to +8% 89%

Integrated

PTT PTT could also benefit from 67%-owned PTTEP’s higher earnings performance. Despite increasing oil prices, we estimate that profit contribution from PTTEP could remain low at only c.11-12% of PTT’s net profit in 2016-18F, compared with 35% prior to the recent decline of oil prices from 2H14 to Jan 16. The gas business would continue to play a vital role in bolstering PTT’s profitability during the next three years, partly supported by the liberalisation of domestic fuel prices, mainly LPG and NGV. We have revised up our 2016-187F earnings forecast of PTT by 9%-11% to factor in higher oil price assumptions. Our TP is also raised from Bt320 to Bt370/share, based on sum-of-parts. Our TP implies an undemanding valuation at only 11.4x P/E in 2017F, which represents its 5-year average PE multiple. Maintain BUY.

+0.6% to +0.9% 94%

Refinery

BCP BCP would benefit from stock gains, like its peers but among the oil refiners in Thailand, BCP would be less vulnerable to changes in oil price than its peers, thanks to more stable income from the oil marketing and renewable power businesses. Higher oil prices could be positive for its E&P business and reduce the downside risk from impairment charges. We believe that BCP would benefit from stock gains at a higher magnitude than its peers due to its low-cost inventory, given the planned shutdown during 1Q16. We maintain our earnings forecast for 2016-18F as higher oil prices would have a marginal impact on its operating cost. We also maintain our TP of Bt39/share, based on sum-of-parts, and BUY rating. It is our preferred play for Thailand’s oil refining sector in view of its attractive valuation and dividend yield.

-0.6% -16%

IRPC We estimate that IRPC’s earnings could be affected by higher crude oil prices, especially for light crude oil as the company has to import lighter crude oil to feed to its refinery in order to gain feedstock for its petrochemical complex. The wider spread between light and heavy crude would reduce its cost competitiveness, compared with peers. In addition, higher naphtha prices could hurt its petrochemical product spread. Nonetheless, this could be offset by the operation start-up of its fuel-oil upgrading unit under the Upstream Project For Hygiene And Value Added Products (UHV) project. The upgraded unit would reduce fuel oil output to only 8% of total capacity and enable the company to utilise its oil refinery and petrochemical complex more efficiently. The new facility will increase IRPC’s flexibility in selecting more types of crude oil, including heavy crude, without hurting its product spread and operating margin. We maintain our HOLD rating. As we roll over our valuation, based on 1.3x P/BV, to mid-2017, our TP rises to Bt5.3/share.

-1.6% to -2% 75%

PTTGC Apart from stock gains from higher oil prices, we believe PTTGC should also benefit from higher petrochemical product prices, which normally track oil prices. We also expect the company’s inventory gains in 2Q16 to outperform its peers, given the low-cost crude oil inventory that it acquired ahead of the planned shutdown. Operations-wise, the impact on PTTGC’s earnings should be less severe than TOP because of lower earnings contribution from the refinery business at c.20% of total EBITDA, vs. 73% from the petrochemical business. We think that higher oil prices should favour gas crackers whose feedstock is more competitive than naphtha crackers. We maintain our earnings forecasts for 2016-18F as well as our TP of Bt70, based on 1.3x P/BV. Maintain BUY.

+1% to +1.2% 85%

TOP TOP’s earnings could benefit from rising crude oil prices due to inventory gains in absolute terms. This could provide upside to our earnings forecasts if the higher oil prices are sustained throughout this year. Excluding this impact, we estimate that every US$1 increase in oil prices will erode TOP’s earnings by 1.6-2.6% in 2016-18F, given that its operating unit cost could increase by US$0.03/bbl for every US$1/bbl increase in oil prices. Nonetheless, we estimate that higher oil prices and a wider spread between light and heavy crude oil would affect TOP in the medium term, due to higher fuel costs for its refinery and petrochemical complex. Note that light crude accounts for at least 60% of its total crude intake. We upgrade our rating from FULLY VALUED to HOLD, as we roll over our valuation, based from its average P/BV multiple of 1.3x, to mid-2017 – thus resulting in a higher TP of Bt63/share. We think that the near-term positive impact of higher oil prices on its earnings should be largely priced in.

-1.6% to -2.6% 8%

Source: DBS Bank

Page 16

Regional Industry Focus

Oil and Gas

Page 17

Rigbuilders – is it time to turn positive? NOT YET. While stocks are trading near AFC valuations, there remain uncertainties revolving the extent of damage from Brazil and potential customer default. In addition, rig orders – the key earnings driver for shipyards, are unlikely to return in the next 1-2 years amidst an unprecedented supply glut. A turnaround for rig orders to return requires the acceleration of rig retirement, cancellations of speculative build and higher oil prices.

Valuations near AFC levels

Trading below -2SD. In this downturn, Keppel and SMM’s valuations have been hammered to 2SD below mean valuations, at 0.8x and 1.3x respectively, back to the levels similar to late 1990s post AFC. What’s in the price? Current price levels have probably reflected the bankruptcy of Sete Brasil, a long rigbuilding winter, i.e. low rig orders amid prolonged low oil prices and rig glut, deferments, and cancellations in isolated cases.

Keppel’s PB vs ROE

Source: Bloomberg Finance L.P., DBS Bank

-10%

-5%

0%

5%

10%

15%

20%

25%

30%

35%

0

1

2

3

4

5

6

P/B 1-year forward ROE (%)

(x)

Global financial crisis

Re cession in EU and US

Asian finanical crisis, OPEC excess production

OECD recession

1991 Gulf War, re versal of oil price

spike

Current crisis

Page 17

Regional Industry Focus

Oil and Gas

Page 18

SMM’s PB vs ROE

Source: Bloomberg Finance L.P., DBS Bank Concerns

Are provisions adequate? We estimate that a discount of up to 35% of contract values has been factored in SMM’s S$280m provision for non-Sete projects, which seems sufficient at this point. Keppel could be under pressure to recognise initial provisions for the non-Sete projects, and this could be up to S$200m based on our back-of-the-envelope calculation.

For Sete projects, we believe the milestone payments at ~35% of total contract value, offers a good buffer for the seven units at the advanced stages, thus preventing Sete’s stakeholders from cancelling. Cancellations risks are higher for the six units that are at the <20% completion stage. Singapore rigbuilders hold the view that the provisions made are sufficient to cover the liability to vendors at this point. While the assumptions behind the provisions are not disclosed, in case of cancellations, we believe some flexibility, in terms of equipment delivery and payment etc, could be granted in times like these, out of long-term business relationships.

Provisions made by Singapore rigbuilders

Company Impairment/provisions in 4Q15

Methodology More to come

Shipyards Keppel Corp S$230m for Sete Brasil

projects Net realisable value of rigs under construction, after assessing the construction progress, payments received, payments to vendors and market value of rigs.

Further provisions possible on Sete Brasil rigs; In addition, Keppel has yet to make any provisions for non-Sete projects, which we estimate could be up to US$200m for some of the riskier projects from Grupo R, Fecon and Clearwater.

Sembcorp Marine

S$329m for Sete Brasil projects; and S$280m for non-Sete rigs

Net realisable value of rigs under construction, after assessing the construction progress, payments received, payments to vendors and market value of rigs.

Further provisions possible on Sete Brasil rigs; We believe SMM has made adequate provisions for non-Sete units that are at risk.

Source: Company, DBS Bank

-20%

-10%

0%

10%

20%

30%

40%

50%

0

1

2

3

4

5

6

7

1990

1991

1992

1993

1994

1995

1996

1997

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

2016

P/B 1-year forward ROE

(x)

Global financial cr isis

Recession in EU and US

Asian finanical crisis,OPEC excess production

OECD recession

1991 Gulf War, re versal of oil price

spike

Current crisis

Page 18

Regional Industry Focus

Oil and Gas

Page 19

Keppel’s outstanding rig orderbook

Date announced

Type of rig / vessel Contract Value, (S$ m)

Orignal Delivery

Rescheduling Customer Comment

SEMI-SUBMERSIBLEs 4-Jun-13 DSS 38M semisubmersible rig 720.0 4Q16 SOCAR

20-Aug-13 KFELS SSAU5000NG accommodation semi 355.6 4Q15 2016 Floatel 22-Dec-11 DSS 38E semisubmersible rig 1,043.6 4Q15 Deferred Sete Brasil

Sete Brasil filed for chapter 11. Keppel has made S$230m provision in 4Q15

7-Aug-12 DSS 38E semisubmersible rig 1,030.0 4Q16 Deferred Sete Brasil

7-Aug-12 DSS 38E semisubmersible rig 1,030.0 3Q17 Deferred Sete Brasil

7-Aug-12 DSS 38E semisubmersible rig 1,030.0 2Q18 Deferred Sete Brasil

7-Aug-12 DSS 38E semisubmersible rig 1,030.0 4Q18 Deferred Sete Brasil

7-Aug-12 DSS 38E semisubmersible rig 1,030.0 3Q19 Deferred Sete Brasil

Actual Provision 230

JACK-Ups 21-Nov-13 KFELS Super A class 330.5 2Q16 2Q18 Ensco PLC One of the largest international drillers

28-Mar-13 KFELS B Class jackup rig 254.7 3Q15 2Q17 Grupo R Pending charter contract from Pemex

28-Mar-13 KFELS B Class jackup rig 254.7 4Q15 2Q17 Grupo R 15-Jul-13 KFELS B Class jackup rig 260.0 4Q15 2Q17 Grupo R 2-Aug-13 KFELS B Class jackup rig 261.6 4Q15 2Q17 Parden Small Mexican player 1-Oct-13 KFELS B Class jackup rig 276.3 4Q15 2016 Clearwater Clearwater Capital

concluded sale of the unit to Arabian Drilling Company in May-2014

1-Oct-13 KFELS B Class jackup rig 276.3 1Q16 3Q17 Clearwater 3-Mar-14 KFELS N class plus 633.9 1Q17 4Q17 TS Offshore Backed by an

international operator (COSL) which was Keppel's customer

13-Feb-14 KFELS B class 274.3 3Q16 2Q17 Fecon International New entrant, established by experienced PE fund (intrepreneur A.P. Dobrov) and an operator that is an existing customer of Keppel

13-Feb-14 KFELS B class 274.3 4Q16 3Q17 Fecon International 13-Feb-14 KFELS B class 274.3 4Q16 4Q17 Fecon International

7-Nov-13 KFELS Super B class

273.5 1Q16 1Q20 Transocean

One of the largest international drillers

7-Nov-13 KFELS Super B class 273.5 2Q16 2Q20 Transocean 7-Nov-13 KFELS Super B class 273.5 4Q16 3Q20 Transocean 7-Nov-13 KFELS Super B class 273.5 1Q17 4Q20 Transocean 7-Nov-13 KFELS Super B class 273.5 3Q17 1Q21 Transocean 31-Oct-14 KFELS Super B class 306.8 4Q16 1Q17 BOT Lease Co., Ltd Backed by Japanese

bank

Est. provision 213

Land Rig 29-Dec-14 Land drilling rig 132.3 mid-2016 CDC

Source: Company, DBS Bank

Page 19

Regional Industry Focus

Oil and Gas

Page 20

SMM’s outstanding rig orderbook

Date announced

Type of rig / vessel(s) Value, Est (S$ m)

Original Delivery

Rescheduling Customer Comment

Drillship 6-Feb-12 Drillship - Jurong Espadon design 983.0 2Q15 Deferred Sete Brasil

Sete Brasil filed for chapter 11. SMM made provision of S$329m in 4Q15

8-Aug-12 Drillship - Jurong Espadon design 1,008.0 4Q16 Deferred Sete Brasil

8-Aug-12 Drillship - Jurong Espadon design 1,008.0 3Q17 Deferred Sete Brasil

8-Aug-12 Drillship - Jurong Espadon design 1,008.0 2Q18 Deferred Sete Brasil

8-Aug-12 Drillship - Jurong Espadon design 1,008.0 4Q18 Deferred Sete Brasil

8-Aug-12 Drillship - Jurong Espadon design 1,008.0 2Q19 Deferred Sete Brasil

29-Nov-12 Drillship - Jurong Espadon design 991.9 3Q16 Deferred Sete Brasil

27-Feb-14 Drillship - Jurong Espadon III design 684.1 2Q17 1Q20 Transocean Reputable client; Market could have recovered then

27-Feb-14 Drillship - Jurong Espadon III design 684.1 1Q18 3Q20 Transocean Reputable client; Market could have recovered then

Provision made in 4Q15 329

Semi-submersible 3-Apr-12 Harsh-environment ultra-deepwater

semi-submersible rig 712.8 1Q2015 1Q17 Seadrill 35% discount to contract

value; buffered by 20% downpayment. Est provision of S$100m

12-Sep-13 Semi-submersible Well Intervention Rig 438.1 mid-2016 Helix 15-Jul-15 Semi-submersible crane vessel 1,292.0 4Q18 Heerema New orders in 2015; delivery

date still far away

Est. provision 100

1,307.8 Jackup 28-Feb-13 Baker Marine Pacific Class 400 jackup rig 257.9 2Q 2015 Technically

accepted in 1Q16

Perisai

Est. provision of S$130m

31-Dec-13 Baker Marine Pacific Class 400 jack up 268.0 3Q2016 Deferred Perisai 18-Mar-13 Baker Marine Pacific Class 400 jackup rig 260.6 End 1Q

2015 Technically accepted in

1Q16

Oro Negro

1-Jul-13 Baker Marine Pacific Class 400 jackup rig 260.6 Jul-15 4Q16 Oro Negro 1-Jul-13 Baker Marine Pacific Class 400 jackup rig 260.6 3Q2015 4Q16 Oro Negro 26-Feb-14 Baker Marine Pacific Class 400 jackup rig 270.9 4Q15 Terminated Marco Polo Est.provision = apporx. 20% of

value or S$50m. 3-Nov-14 Baker Marine Pacific Class 400 jackup rig 306.8 Jan-2017 BOT Lease Backed by Japanese bank

Est. provision 180

Source: Company, DBS Bank

Page 20

Regional Industry Focus

Oil and Gas

Page 21

Catalysts

We await better clarity before turning more positive on the rigbuilding sector. Traditionally, the leading indicators are oil prices and order flows. Oil price recovery. It is widely anticipated that oil prices below US$60/bbl will do little to help to spur demand for newbuild rigs considering the current low utilisation rate of <60% and orderbook-to-fleet ratio of 15-20%. Nevertheless, it could help to reduce deferment and cancellation risks and drive recovery of the sector.

Will history repeat itself? We believe the 1997-2000 period during the AFC is the best historical reference point for comparison. Oil prices were hovering at low levels at US$30-50/bbl (inflationary-adjusted) till mid-2000s, having collapsed >60% from peak. Rigbuilders were churning high single to low teen EBIT margins and ROEs, similar to current results. During 1998-2000, Keppel traded at 0.7-1.0x PB while SMM at 1.1-1.3x on average, before rising to 1.5-1.8x PB during 2003-2004 alongside the strong recovery in oil prices.

Historical trend of oil prices vs rigbuilders’ performance (1997-2004)

1997 1998 1999 2000 2001 2002 2003 2004 OIL PRICE Brent Crude Oil Price (US$/bbl) Average 19.3 13.3 18.0 28.5 24.9 25.0 28.5 38.0 High 24.8 16.6 26.1 34.6 29.9 30.2 34.1 51.6 Low 16.5 9.6 10.1 21.3 17.7 18.4 23.3 28.8

Inflationary Adj Brent Crude Oil Price (US$/bbl)* 2015=100 Average 28.5 19.4 25.7 39.3 33.3 33.0 36.7 47.7 High 36.6 24.1 37.1 47.6 40.0 39.7 43.9 64.7 Low 24.4 14.0 14.3 29.3 23.7 24.3 30.0 36.2 CPI 67.7 68.8 70.3 72.7 74.7 75.9 77.6 79.7

Keppel Corp P/Bv (x) Average 1.3 0.7 1.0 0.8 0.9 1.1 1.3 1.8 High 1.8 1.0 1.3 0.9 1.0 1.2 1.5 2.1 Low 0.9 0.9 0.8 0.7 0.7 0.8 1.0 1.6 ROE (%) 5.0% -6.8% 6.3% 6.0% 12.5% 13.5% 14.2% 15.5% O&M EBIT margins (%) 11.4% 12.9% 10.1% O&M EBIT growth rate (%) 135% 142% -13% 31% EBIT margins (%) 14% -6% 16% 11% 10.6% 8.4% 8.5% 10.3% EBIT growth rate (%) -8% nm nm 8% -38% -26% 9% -19%

Sembcorp Marine P/Bv (x) Average 1.2 1.3 1.3 1.1 1.3 1.4 1.5 1.5 High 1.6 1.4 1.5 1.3 1.5 1.7 1.7 2.0 Low 1.1 0.2 1.1 1.0 1.0 1.2 1.3 1.3 ROE (%) 6.5% 8.9% 9.5% 9.3% 9.1% 9.9% 8.4% 9.9% O&M EBIT margins (%) 8.2% 8.1% 9.9% 10.4% 9.7% 8.9% 7.0% 6.8% O&M EBIT growth rate (%)

62% 40% 21% -22% 5% 8% -17% 25%

Source: Companies, Bloomberg Finance L.P., DBS Bank

Page 21

Regional Industry Focus

Oil and Gas

Page 22

Historical trend of oil prices vs rigbuilders’ performance (2005-present)

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016E OIL PRICE Brent Crude Oil Price (US$/bbl) Average 55.3 66.1 72.7 98.5 62.7 80.3 110.9 111.7 108.7 99.4 53.6 45.0 High 67.7 78.3 95.8 146.1 79.7 94.8 126.7 126.2 118.9 115.1 67.8 52.5 Low 40.5 57.9 51.7 36.6 39.6 69.6 93.3 89.2 97.7 57.3 36.1 27.9

Inflationary Adj Brent Crude Oil Price (US$/bbl)* 2015=100 Average 67.1 77.7 83.1 108.5 69.2 87.3 116.9 115.3 110.6 99.6 53.6 44.3 High 82.2 92.1 109.5 160.8 88.0 103.0 133.5 130.3 121.0 115.2 67.8 51.7 Low 49.2 68.0 59.1 40.3 43.7 75.6 98.3 92.1 99.4 57.4 36.1 27.4 CPI 82.4 85.1 87.5 90.8 90.5 92.0 94.9 96.9 98.3 99.9 100.0 101.6

Keppel Corp P/Bv (x) Average 2.5 2.8 3.9 2.7 1.9 2.3 2.5 2.2 2.1 1.9 1.3 0.9 High 2.9 3.4 4.8 3.7 2.3 2.7 2.9 2.5 2.3 2.1 1.6 1.1 Low 2.1 2.5 3.0 1.2 1.3 2.0 2.0 2.0 1.9 1.5 1.1 0.8 ROE (%) 16.7% 19.1% 24.0% 22.4% 30.7% 24.4% 27.6% 26.4% 19.5% 18.8% 14.2% 9.6% EBIT margins (%)

8.2% 10.6% 10.1% 10.5% 12.3% 17.0% 28.0% 18.8% 17.2% 17.9% 14.7% 16.7%

EBIT growth rate (%)

14% 72% 31% 18% 22% 3% 81% -7% -19% 11% -36% -20%

Sembcorp Marine P/Bv (x) Average 3.3 4.0 4.6 4.4 3.7 4.1 4.1 4.3 3.7 3.0 1.9 1.3 High 4.4 4.7 6.4 6.0 4.8 4.6 5.1 4.7 4.1 3.4 2.3 1.5 Low 2.0 3.5 3.5 1.9 2.1 3.5 3.1 3.4 3.5 2.2 1.2 1.2 ROE (%) 11.9% 19.8% 16.0% 28.7% 43.7% 38.4% 30.0% 22.2% 21.7% 19.9% -10.6% 8.7% O&M EBIT margins (%)

5.9% 6.4% 7.7% 9.9% 15.1% 20.7% 18.6% 12.5% 11.4% 12.1% -3.0% 11.6%

O&M EBIT growth rate (%)

34% 83% 53% 44% 72% 9% -22% -25% 14% 12% -121% nm