ren ren company ipo analysis

DESCRIPTION

RenRen (RENN) IPO & Company Analysis Indepth report on the RenRen China Internet Social Network company & its IPO. TABLE OF CONTENTS Foreword 3 Executive Summary 4 IPO Details 5 Renren User Base & Internet Demographics in China 5 Financials 8 Sources of Revenue 10 Plans for Proceeds from IPO 11 Early Investors 11 Risk Factors 12 Management 13 Current Competition in China 14 Comparison to Facebook 22 Recent IPO Analysis 23 Investment Strategy for Renren 26TRANSCRIPT

PRESENTS

COMPANY IPO ANALYSIS

May 4, 2011

By Kenny Hong, CFA

2

TABLE OF CONTENTS

Foreword 3

Executive Summary 4

IPO Details 5

Renren User Base & Internet Demographics in China 5

Financials 8

Sources of Revenue 10

Plans for Proceeds from IPO 11

Early Investors 11

Risk Factors 12

Management 13

Current Competition in China 14

Comparison to Facebook 22

Recent IPO Analysis 23

Investment Strategy for Renren 26

3

FOREWORD

“China Internet IPO”, “Social Network“, and “Facebook” are the hottest buzz words of 2011.

Renren includes all 3 of those elements and will be one of the first social network websites

going IPO with Linkedin, Facebook, and Kaixin001 following after. Renren is a China Internet

Social Network company designed to look like the Facebook of China and is going IPO on

Wednesday, May 3, 2011. China has 457 million Internet users at the end of 2010 and is

estimated to grow to over 700 million by 2014. Renren has 114 million registered users. The

wave of hot IPOs has evolved from US Tech. firms in the 1990s to the US Internet IPOs in the

2000s to the China Internet IPOs in the 2005-2010 to the Global Social Media + China Internet

Social Media in 2011. As an early adopter and user of various Internet Social Networks, I have

experience the evolution of sites such as Friendster, Myspace, Facebook, Linkedin, and now the

China Websites and Social Networks such as Renren as I am currently based in Shanghai, China.

The recent China Internet IPOs from Dec. 2010 such as Dang Dang (Dang), Yokou (Yoku), and

Qihoo (QIHU) have been successful for institutional investors, 45% to 366% return from IPO

price to May 3rd

while the return for investors after the open IPO price has been mixed from -

5% to 121%. More data are provided in the following report. The information from this

research report has been taken from the Renren prospectus and various reputable sources in

English and Chinese as well. We hope this report will better help you in your investment

decision, business decision, or academic interests by providing you with an overview of Renren

as a company and the social network in China as well.

Kenny Hong, CFA

Vice President, Investment Advisory

4

EXECUTIVE SUMMARY

▪ Price per share: $12-14 (increase from previous $9-11)

▪ 114 million registered users (February 2011)

o Aggregate 2.9 billion photos, 249 million blogs, 20.8 billion comments/reviews

▪ 58.2% of Chinese internet users below the age of 30

▪ Users in China spent 7.8% of their online time on social networking sites compared to

13.9% globally and 11.6% in the United States (April 2010)

▪ YoY revenue growth was 239% from 2008-2009

▪ YoY revenue growth declined to 64% in 2009-2010

▪ Company has no debt and over $136M in cash on balance sheet

▪ Revenue breakdown

▪ Renren potentially has large upside from increasing its product offerings and

monetization its services

▪ Risk factors include intellectual property, user base, innovation, technology, reputation,

and regulation

▪ Management has strong engineering, tech start-up and consulting backgrounds

▪ Competitors include Kaixin001, Weibo, Pengyou, and Facebook

5

IPO DETAILS

▪ RenRen expected IPO date: May 4, 2011.

▪ RenRen ticker symbol: NYSE:RENN

▪ Price per share: $12-14 (increase from previous $9-11)

o Raising up to $743.1 million

o 15.93% to 18.59% of the company will be floating

▪ Shares offered

o ADSs by Renren: 42,898,711

o ADSs by current shareholders: 10,201,289

o Total ADSs offered: 53,100,000

o ADSs to Class A ratio: 3ADSs to 1 Class A share

▪ Private Placements

o Third-party investors affiliated with Alibaba Group, China Media Capital, and

CITTIC Securities to purchase an aggregate USD 10 million worth of Class A

shares at IPO price with respect to the ADSs to Class A ratio

RENREN USER BASE & INTERNET DEMOGRAPHICS IN CHINA ▪ Renren User Base

○ 114 million registered users (February 2011)

○ 31 million active users

o Aggregate 2.9 billion photos, 249 million blogs, 20.8 billion comments/reviews

33 million

83 million

110 million

117 million as of

March 2011

0

20

40

60

80

100

120

140

December 1, 2008 December 1, 2009 December 1, 2010

Axi

s T

itle

Cumulative total activated users (in

millions)

6

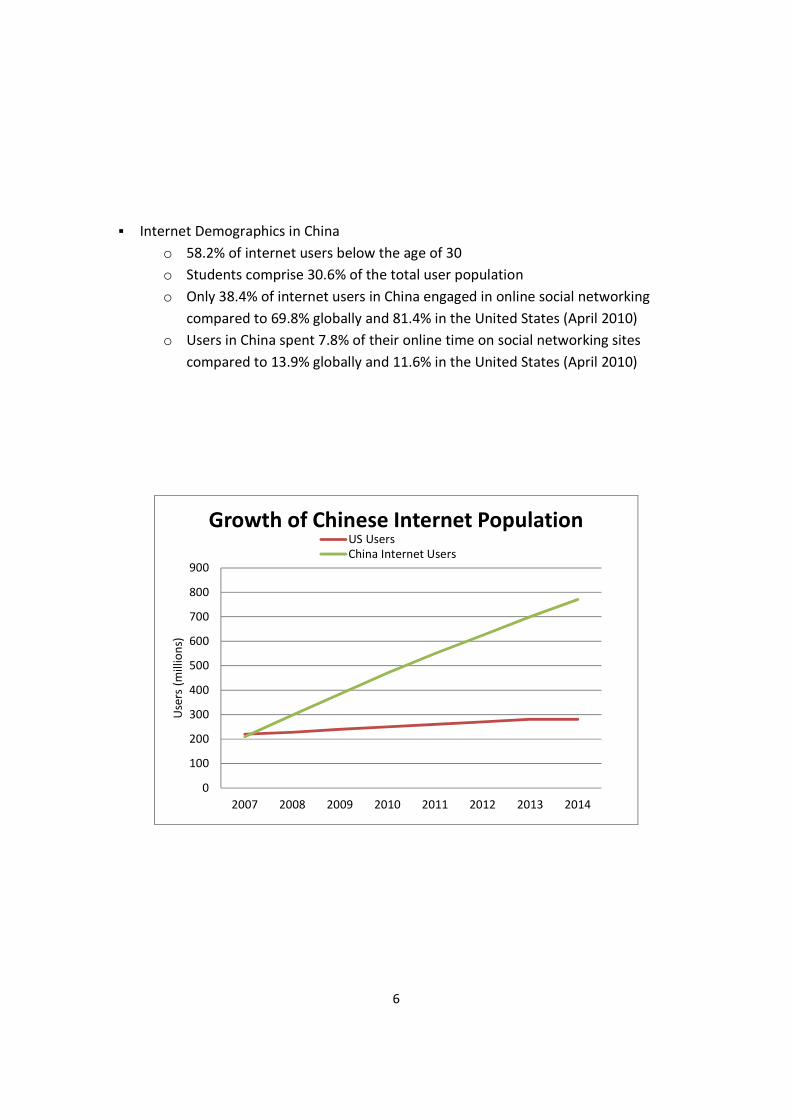

▪ Internet Demographics in China

o 58.2% of internet users below the age of 30

o Students comprise 30.6% of the total user population

o Only 38.4% of internet users in China engaged in online social networking

compared to 69.8% globally and 81.4% in the United States (April 2010)

o Users in China spent 7.8% of their online time on social networking sites

compared to 13.9% globally and 11.6% in the United States (April 2010)

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014

Use

rs (

mill

ion

s)

Growth of Chinese Internet PopulationUS Users

China Internet Users

7

Number of End Users in China by Media Interface

0

100

200

300

400

500

600

700

800

900

2007 2008 2009 2010 2011 2012 2013 2014

Axi

s T

itle

RenRen's Potential Growth

China

Internet

Users

8

Share of Advertising Spending by Medium in China

2009 2012E

FINANCIALS ▪ YoY revenue growth was 239% from 2008-2009

▪ YoY revenue growth declined to just 64% in 2009-2010

▪ Revenue forecast for the coming years maintains a growth rate between 50-60%

▪ Loss from operations in 2008 and 2009 but moved to positive numbers in 2010

▪ Majority of loss recorded in the past 2 years has been caused by change in fair value of

warrants issued to investors

▪ Company has no debt and over $136M in cash on balance sheet

$13.8

$46.7

$76.5

$122.5

$183.7

$0.0

$50.0

$100.0

$150.0

$200.0

2008 2009 2010 2011(E) 2012(E)

Renren Revenue & Growth ($USD

Mln)

2008

2009

2010

2011(E)

2012(E)

9

▪ Revenue multiplier is common method used to determine relative price of a company

▪ Renren is nearly twice as expensive as Facebook

Renren Facebook

Value $5.1 Bln $70 Bln

2010 Revenue $77 Mln $2.0 Bln

2010 Revenue Multiple 67.1x 35.0

▪ Renren average revenue per user of $0.65

▪ Facebook averages $4.00 per user

▪ Potentially Renren has large upside from increasing its product offerings and

monetization its services

Renren Facebook

Revenue $77 Mln $2.0 Bln

Number of Users 117 Mln 500 Mln

Revenue per User $0.65 $4.00

▪ No plans to pay any cash dividends in the foreseeable future

▪ Will retain future earnings to operate and expand our business

2008 2009 2010

Net Revenue $13.8 $46.7 $76.5

Gain from Opeations ($8.0) ($2.7) $7.6

Net Income $49.3 ($70.1) ($64.2)

($100.0)

($75.0)

($50.0)

($25.0)

$0.0

$25.0

$50.0

$75.0

$100.0

in m

illi

on

s o

f U

S$

RenRen Revenue & Net Income 08-10

Net Revenue

Gain from Opeations

Net Income

10

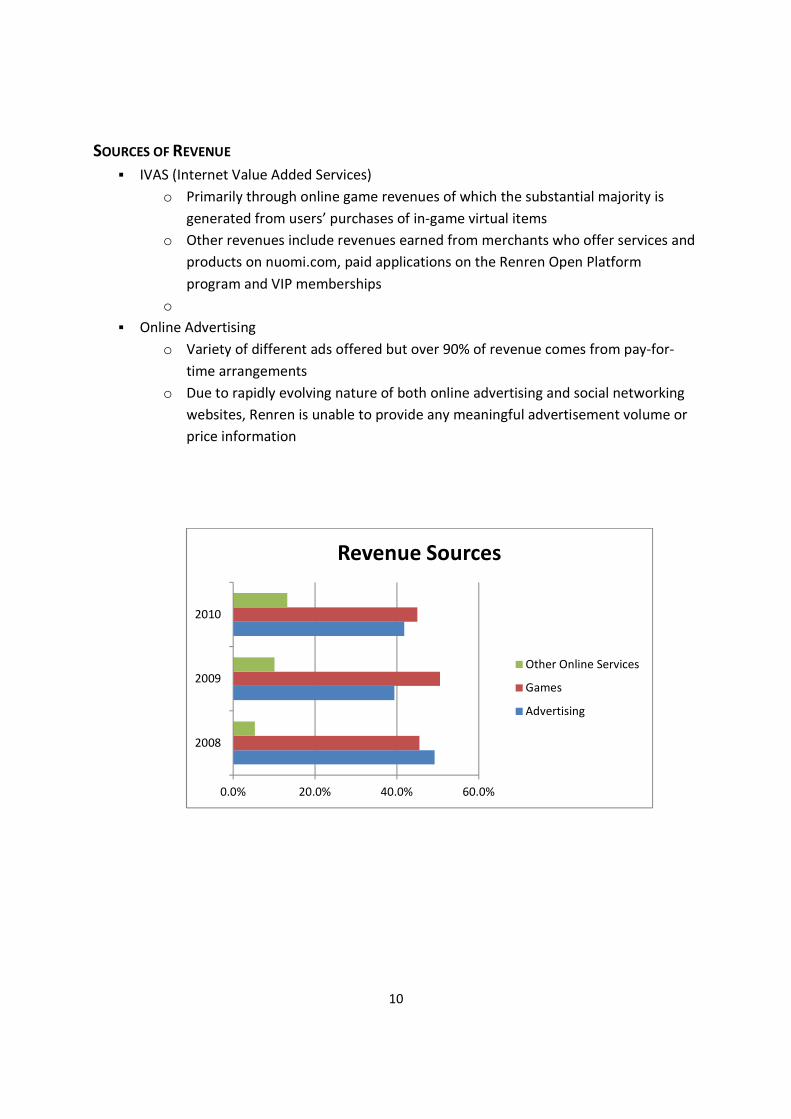

SOURCES OF REVENUE

▪ IVAS (Internet Value Added Services)

o Primarily through online game revenues of which the substantial majority is

generated from users’ purchases of in-game virtual items

o Other revenues include revenues earned from merchants who offer services and

products on nuomi.com, paid applications on the Renren Open Platform

program and VIP memberships

o

▪ Online Advertising

o Variety of different ads offered but over 90% of revenue comes from pay-for-

time arrangements

o Due to rapidly evolving nature of both online advertising and social networking

websites, Renren is unable to provide any meaningful advertisement volume or

price information

0.0% 20.0% 40.0% 60.0%

2008

2009

2010

Revenue Sources

Other Online Services

Games

Advertising

11

PLANS FOR PROCEEDS FROM IPO

▪ Renren plans on using the proceeds of the IPO in three manners

o $180M for investing in technology and research and development activities

o $180M for expanding sales and marketing activities

o Remainder of the proceeds will be used for general corporate purposes including

acquisitions and investments

EARLY INVESTORS

▪ Investors - Series D

o Softbank Corporation

� April 2008 purchased 35% for $430 million

� Aggregate of 10,071,763 series D preferred shares at USD 9.93 per share

� Has warrants to purchase 30,215,288 series D preferred shares

o Joho Capital and SBI Investment Company

� April 2008 purchased 3,133,438 series D preferred shares for USD 30

million

▪ Investors - Ordinary Shares

o Joseph Chan

� Economic ownership 22.8%

� Voting power 55.9%

▪ Underwriters of offering

o Morgan Stanley, Deutsche Bank, Credit Suisse, Bank of America Merrill Lynch,

Jefferies, Pacific Crest, and Oppenheimer

12

RISK FACTORS

� User Base, Innovation, Technology, and Reputation

o Maintain and increase user base

o Maintain innovative services and applications

o Expand into new services, new demographics, whilst keeping up with technology

o New fast-growing company in uncertain industry with heavy reliance on

advertising and third-party services

o Spammers, malicious content, collection of personal data may affect reputation,

removal of content due to PRC regulations

� Intellectual Property

o Conflict with US companies that already have patents such as Facebook

o Copying other companies or being copied

▪ Regulation

o PRC censorship issues and business license

o Conforming to US GAAP

� Transparent and reliable financial information

o Leasehold interests may be faulty

Renren’s most imminent risk factors are lawsuits and competition, due to the saturation of the

Chinese social networking market. Renren will have to maintain a competitive advantage while

minimizing problems arising from intellectual property, regulatory or other issues.

After their IPO in the US, Renren may be under closer scrutiny by investors, who require reliable

and transparent financial information. Renren must also avoid using content that is

0.0% 10.0% 20.0% 30.0% 40.0% 50.0% 60.0% 70.0% 80.0% 90.0% 100.0%

CEO Joseph Chan

SB Pan Pacific

Pre-IPO and Private Placement Investor…

Public Investors Holding Class A Shares

CEO Joseph ChanSB Pan Pacific

Pre-IPO and Private

Placement Investor

Holding Class A

Ordinary Shares

Public Investors

Holding Class A Shares

Ownership 22.8%34.2%29.6%13.4%

Voting Power 55.9%33.5%7.3%3.3%

Ownership and Voting Rights

13

questionably similar to competitors (e.g. Facebook), while expanding into new markets. Privacy

and anti-spam anti-malware will also become an issue.

MANAGEMENT

▪ Strong engineering, tech start-up and consulting backgrounds

▪ Previously worked at Google, Yahoo, Alibaba, and other tech companies

▪ Chairman & CEO: Joseph Chen, 41

o Founder of ChinaRen.com (first-gen SNS), SVP of Sohu.com

o MIT Masters in Engineering and Stanford MBA

▪ Director: Katsumasa Niki, 43

o Group manager of Softbank Corp Finance Department, director of several

Softbank subsidiaries

o Kobe University Bachelor of Economics and Chuo Grad School MBA

▪ Director: Matthew Nimetz, 71

o COO of General Atlantic (venture capital firm), corporate and international

attorney for over 30 years

o Harvard Law School and Oxford University Rhodes Scholar

▪ COO: James Jian Liu, 38

o Founder and CEO of UUMe.com, BCG China management consultant

o Shanghai Jiao Tong BS Computer Science and Stanford MBA

▪ CFO: Hui Huang, 38

o CFO of Cathay Industrial Biotech from 2003-2007, Associate in Goldman Sachs

Asia Principal Investments, BCG Associate

o Wharton MBA

▪ Chief Marketing Officer: Alvin Chiang, 40

o VP of Alibaba, VP Sales of NetEase, Yahoo

▪ SVP Games: Chuan He, 31

o Ph.D. in Computer Science from Tsinghua

▪ VP of Nuomi.com: Derek Boyang Shen, 37

o Google Head of China Development, Strategic Partner Development, Engineer

o UCLA Masters in Computer Science

14

CURRENT COMPETITION IN CHINA

April 14th

, 2010, China’s Top 4 in Comparison

15

� RenRen

○ Design and business model are copied from Facebook.

○ Users: The majority of users are students, although RenRen strives to retain those

users after graduation. In the fall of 2009, it launched a massive advertising

campaign—both traditional and digital—urging Chinese to reconnect with old

friends and classmates. The emphasis is on connecting with real-life friends online,

just as on Facebook. As RenRen grows, it is encroaching on the turf of its rivals: teens

(Qzone), white-collars (Kaixin001), and lower-tier cities (51.com).

○ User Interface: The user interface is nearly identical to Facebook (though it has not

copied Facebook’s latest redesign). It has a few unique features, such as a

“footprint” of who last visited your page and recently added game mechanics or

‘funware’ so that users can reach ‘higher levels’ for interacting on the site. It also

allows custom skins, though the majority of users stay with the basic theme.

○ Platform: The application programming interface is open to 3rd parties, but revenue

share is a capped at 56%. It boasts about 250 applications (almost all games) and is

China’s most popular open platform. Foreign game developers are just starting to

test the approval process, with FooMojo, RockYou, and PopCap leading the way.

Access for foreign developers is certain to be a hot topic at the upcoming 2010 China

Social Games Summit.

○ Games: RenRen has the most and best games, in large part due to its open platform.

But RenRen also develops games in-house, leading to concerns that RenRen will

favor its own games over those of outside developers. Other networks often copy

the most popular games on RenRen.

○ Financing: Softbank purchased 35% of RenRen for $430 million, valuing the company

at $1.2 billion. The company intends to hold an initial public offering as soon as

2011.

○ RenRen’s parent company is Oak Pacific Interactive, which also owns Mop, a smaller

Chinese social network, forum, and humor site.

○ Revenues: Annual revenue was over 100 million RMB ($15 million) in 2009,

according to one source from the company. The primary revenue channel is

advertising (brands, games, and e-commerce).

○ Analysis: RenRen is the most popular, most open, and best-financed social network

in China. Its management team is also the smartest and fastest-moving. It is actively

developing advertising, gaming, and e-commerce revenues. Its user growth is

impressive, in large part due to its aggressive marketing campaigns. The August 2009

name switch from Xiaonei (inside-campus) to RenRen (people’s web) signaled its

ambition to become China’s dominant popular social network. By comparison,

China’s other social networks are asleep at the wheel.

16

� KaiXin

o While RenRen was still concentrated on students, the upstart Kaixin001 was able to

attract white-collar workers (in large part via spam).

o Its social games got entire offices addicted to parking cars, stealing crops, and other

top games. Its white-collar workers are the richest and most monetizable

demographic of social network users. Kaixin001’s critical battle is ensuring that the

next generation of students “graduates” to its site upon entering the workforce,

rather than remaining with RenRen.

o Users: White-collar workers who can secretly farm crops and check friends’ photos

from their office desk. Its users spend twice as much time on site, as compared to

users on the other social networks.

o User Interface: The interface is clean and very simple—Kaixin001 is a pared-down

version of Facebook. It eases first-time users into social network: the most popular

applications, like the popular “Buying a House,” even comes pre-installed.

Advertising is minimal.

o Platform: Kainxin001 is a closed platform, although insiders say that it will

eventually open up. It has about 50 applications, the majority of which are games.

o Games: Kaixin001 launched the social games craze in China and its users are game-

crazy. But its games now lag behind RenRen in quantity and quality, because it’s

attempting to develop everything in-house. For instance, it took Kaixin001’s

developers 6 months (an eternity in social game years) to copy a popular restaurant

game on RenRen. That will damage Kaixin001 as it aims to attract new users and

retain and monetize its existing users.

o Financing: Kaixin001 has received a total of $23 million through two funding rounds.

Investors include Sina, Qiming Ventures, and Northern Light Venture Capital.

o Revenues: Kaixin001 has reached monthly revenues of 7 million RMB ($1 million),

but is not yet profitable. Advertisers at ad:tech Beijing told BloggerInsight that

Kaixin001 is the hottest site.

o Analysis: Kaixin001 has seen rapid growth and has captured a desirable

demographic of white-collar workers (appealing to advertisers), who spend tons of

time on the site. But its management team is far more conservative and slow-

moving than RenRen. It’s far behind in terms of its advertising and monetization

channels. Its site design has changed little and its application programming interface

remains closed. If Kaixin001 fails to innovate or at least keep up with the curve, it

will lose out. Students will stick with RenRen rather than “graduate” to Kaixin001.

17

� QZone

○ Qzone draws traffic from QQ Messenger, which boasts 523 million active users and

is also owned by Tencent. Qzone targets teens, rural, and casual users and claims a

whopping 388 million active users, a highly suspect number. Tencent’s internet

services, QQ Messenger, QQ Show, QQ Games, QQ Pet, and Qzone, do connect a

huge number of Chinese people. But the classification of Qzone as a social network

is questionable. It has tons of dormant, skeleton profiles that are pulled from QQ

Messenger. In that regard, it’s similar to MSN Spaces, which also has a ton of

“users,” but low value and retention rates. Qzone users often use nicknames or

aliases rather than real-life names. Given Tencent’s awesome advantages and

synergies in social networks, Tencent’s forays into “real-identity” social networking

should be seen as a squandered opportunity.

○ Users: Teens and rural users. Qzone is attempting to funnel its older users towards

its other social network, Xiaoyou (classmates), with limited success. It already failed

with an earlier attempt called QQ Campus.

○ User Interface: Qzone is a lousy website: it’s ugly, unintuitive, and buggy. The site is

very basic (for a social network), but not in a user-friendly way (like Kaixin001).

○ Platform: Qzone is a closed platform, though it is experimenting with licensing. It

has about 50 applications (mainly games). Benjamin Joffe, Tencent expert and CEO

of internet market research firm +8*, comments: “Applications are all copies or

licenses or bought from social gaming companies, generally with terrible revenue

share or poor valuation. Why? Because Tencent is a closed network and because

they can. Problem is: operating social games is not the same as instant messaging or

massive multi-player online games and there is a learning curve – even for Tencent.”

○ Games: Although Qzone should have a natural advantage (Tencent also owns QQ

Games), the games, like much else on the site, are of low quality. Qzone develops in-

house copies of popular games, but it lags way behind and prohibits users from

adding games without paying at certain times. Perhaps Qzone’s comparatively

young and rural users are so naïve that they pay Qzone when they can play the

same—or better—games for free on the other networks. But it’s doubtful that this is

a successful business strategy in the long run.

○ Financing: Tencent, Qzone’s parent company, is massively profitable and can

employ incredible resources should it so desire.

○ Revenues: No public figures are released. There is a lack of advertising and quality

games, so virtually all revenues must come from Qzone “Yellow Diamond”

memberships. It is difficult to estimate that revenue stream, but it’s hard to imagine

that too many Chinese users will stay loyal to Qzone in the long-run if they continue

to offer lousy services.

○ Analysis: Tencent with Qzone is like Microsoft with Windows Vista: a near-

monopolist (in instant messaging) that can thrive despite a terrible product and lack

of vision. Tencent is still massively profitable: 2009 revenues were $1.8 billion, about

18

three times Facebook’s estimated revenues. It’s unclear how much of that is

attributable to the Qzone social network though. Benjamin Joffe comments,

“Tencent is definitely not the best in terms of products or innovation – similar to

Zynga in that sense – but their ability to deliver a “good enough” mass market

service and integrating it within their ecosystem is impressive.” It holds the teen

demographic, but poor site design and management have cost it ground against its

competitors. Qzone is shut out of the market for older students and white-collar

workers, and RenRen is now encroaching on its core demographic of teens. Qzone

could still turn things around though, as its parent company Tencent is an 800-

pound gorilla in the Chinese internet.

� 51.Com

○ 51.com was an early favorite with significant backing, but is now struggling. Growth

has slowed and it has the lowest traffic rankings of the top four. In early January, the

site was briefly blocked for “objectionable” content, so management is trying to

clean itself of lewd users and content (it’s rumored to be a platform for the world’s

oldest profession). Its Chief Strategy Officer recently resigned, citing illness. 51.com

is a borderline mass-market contender at best. Urban and educated demographics

have all turned to its competitors. It’s now in the precarious position of defending its

core user base in lower tier cities.

○ Users: Users from lower tier cities.

○ User Interface: 51.com is a simple social network. It’s far more functional than

elegant. Several popular applications are pre-installed and the skins are

customizable.

○ Platform: 51.com offers an open platform. It has attracted about 50 applications

(mostly games). It is expected to offer more favorable revenue share terms than

RenRen.

○ Games: The games on 51.com are decent, though not as numerous or high-quality

as on RenRen. 51.com also develops its own games in-house: it’s investing $15

million in a gaming portal, in an attempt to reduce its reliance on advertising and

value-added services. It will also soon connect into the gaming platform from Giant

Interactive, one of its investors.

○ Financing: Giant Interactive, a publicly-listed Chinese massive multiplayer online

gaming company, invested $51 million for a 25% stake. Earlier backers include

venture capital firms Sequoia Capital, SIG, Redpoint Ventures, and Intel Capital. In

early 2007 there was premature talk of an IPO in 2010, but nothing has been heard

since.

○ Revenues: 51.com claims to have turned a profit in 2009, with advertising revenues

of about 200 million RMB ($29 million). Its open platform generated roughly 12

million RMB ($1.8 million) in revenues.

○ Analysis: 51.com was likely doomed to the mass-market by its rural roots. Its lower

tier cities approach initially allowed for quick user growth, but the site now has a

low-brow reputation and is scorned by more sophisticated netizens. RenRen’s

19

approach of starting with the elite students at China’s top universities, BeiDa and

Tsinghua, and then spreading outward (copied from Facebook), appears to have

been far more successful. Second tier social networks worldwide are falling to

Facebook. Will China’s more “sophisticated” networks push into 51.com’s territory?

BloggerInsight is inclined to think so. 51.com’s stagnation in user growth relative to

other networks is not a good sign; spreading outward from elite users has been

successful for social networks worldwide and for RenRen in China too. There are

certainly differing opinions though. Beijing-based internet guru Kaiser Kuo told

BloggerInsight, “I wouldn’t write them off at all: They’ve got a real hold in sub-

secondary cities and with their tie-up to a major game company (Giant Interactive),

they’ve got plenty of cash, and as far as I know, loads of traffic. It’s also been

cleaned up quite a bit within the last year, from what I’ve heard.” 51.com may or

may not hold its ground in lower tier cities. But one thing’s for certain: 51.com

stands little chance in China’s top-tier cities.

Current China’s Top 6 Social Networking Sites in Comparison

Renren Kaixin001 QQ Community 51. com Pengyou Weibo

URL www.renren.com

www.kaixin001.c

om

www.qq.com

www.51.com

www.pengyou.c

om

www.sina.com.c

n

Type Real-name SNS Real-name SNS Nickname SNS Real-name

SNS

Real-name

SNS

Microblog

Registered

Users 170 million

iResearch

iUserTracker)

95 million

(iResearch

iUserTracker)

481 million

(Tencent claims

these as

“actives” under

an extremely

broad,

undefined

definition)

1/8 million 131 million

(Tencent claims

these as

“actives” under

an extremely

broad,

undefined

definition)

120 million

Active

Users 95 million 40 million 190 million 40 million 80 million 65 million

User

Demograp

hics

Students,

white-collars

White-collars Teens Lesser-tier

cities, rural

users

Students,

white collars

White-collars

Alexa #15 #28 #2 #72 #26 #3

20

Rank

Traffic (for

China)

Alexa

Rank

Traffic

(globally)

#90 #155 #10 #419 #179 #13

Alexa

Rank

Pageviews

/User

(average

3months)

10.03 16.96 9.06 11.79 4.74 10.08

China

Rank #10 #19 #2 #127 #27 #3

Reports from Renren regarding its user base and market share

21

Top left: At the end of 2010, Renren held 36% market share in real-name China SNS

(excludes Qzone), leading its next closest competitor, Tencent Pengyou by 13.5%, and far

ahead of Kaixin001.

Top right: Renren also claims the highest user loyalty, meaning 70% of users are unlikely

to shut down their Renren accounts to join another SNS service.

Bottom: Future user usage frequency, 60% of users stated that they will spend same of

time in Renren as they are now, 15.9% vote they will spend more time, 20.2% vote for less

time, and 3.7% unsure.

*Note that these pictures are data from CNNIC: According to CNNIC’s latest Chinese SNS

users’ report, Renren has dominated the whole SNS market with its 39% market share and most

stable user foundation (user loyalty as high as 69.6%). However, the report has excluded Qzone

which may have a bigger market share and higher user loyalty when combined with Tencent

Pengyou.

▪ Kaixin001 and Weibo (Sina)

o Sued Renren for unfair competition

� Renren released Kaixin.com a copy of Kaixin001

o Weibo growing at 10 million users per month while Renren is only growing at 2

million users per month

o Kaixin001 planning to issue IPO one month after Renren

� Pengyou (Tencent)

○ Tencent’s latest entry into the real-name social networking space has many

users. However, whether the social graph is strong is still uncertain.

22

COMPARISON TO FACEBOOK

▪ Revenue multiplier is common method used to determine relative price of a company

▪ Renren is nearly twice as expensive as Facebook

Renren Facebook

Value $5.1 Bln $70 Bln

2010 Revenue $77 Mln $2.0 Bln

2010 Revenue Multiple 67.1x 35.0

▪ Renren average revenue per user of $0.65

▪ Facebook averages $4.00 per user

▪ Potentially Renren has large upside from increasing its product offerings and

monetization its services

Renren Facebook

Revenue $77 Mln $2.0 Bln

Number of Users 117 Mln 500 Mln

23

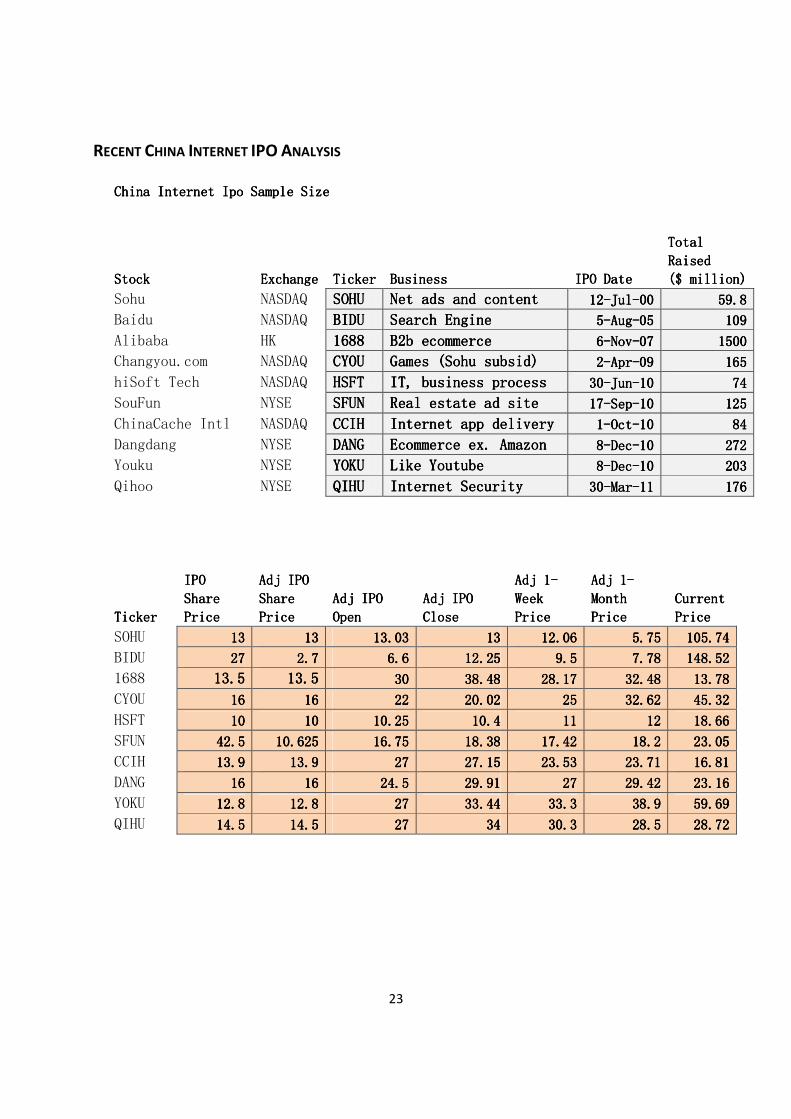

RECENT CHINA INTERNET IPO ANALYSIS

China Internet Ipo Sample SizeChina Internet Ipo Sample SizeChina Internet Ipo Sample SizeChina Internet Ipo Sample Size

StockStockStockStock ExchangeExchangeExchangeExchange TickerTickerTickerTicker BusinessBusinessBusinessBusiness IPO DateIPO DateIPO DateIPO Date

Total Total Total Total

RaisedRaisedRaisedRaised

($ million)($ million)($ million)($ million)

Sohu NASDAQ SOHUSOHUSOHUSOHU Net ads and contentNet ads and contentNet ads and contentNet ads and content 12121212----JulJulJulJul----00000000 59.859.859.859.8

Baidu NASDAQ BIDUBIDUBIDUBIDU Search EngineSearch EngineSearch EngineSearch Engine 5555----AugAugAugAug----05050505 109109109109

Alibaba HK 1688168816881688 B2b ecommerceB2b ecommerceB2b ecommerceB2b ecommerce 6666----NovNovNovNov----07070707 1500150015001500

Changyou.com NASDAQ CYOUCYOUCYOUCYOU Games (Sohu subsid)Games (Sohu subsid)Games (Sohu subsid)Games (Sohu subsid) 2222----AprAprAprApr----09090909 165165165165

hiSoft Tech NASDAQ HSFTHSFTHSFTHSFT IT, IT, IT, IT, business processbusiness processbusiness processbusiness process 30303030----JunJunJunJun----10101010 74747474

SouFun NYSE SFUNSFUNSFUNSFUN Real estate ad siteReal estate ad siteReal estate ad siteReal estate ad site 17171717----SepSepSepSep----10101010 125125125125

ChinaCache Intl NASDAQ CCIHCCIHCCIHCCIH Internet app deliveryInternet app deliveryInternet app deliveryInternet app delivery 1111----OctOctOctOct----10101010 84848484

Dangdang NYSE DANGDANGDANGDANG Ecommerce ex. AmazonEcommerce ex. AmazonEcommerce ex. AmazonEcommerce ex. Amazon 8888----DecDecDecDec----10101010 272272272272

Youku NYSE YOKUYOKUYOKUYOKU Like YoutubeLike YoutubeLike YoutubeLike Youtube 8888----DecDecDecDec----10101010 203203203203

Qihoo NYSE QIHUQIHUQIHUQIHU Internet SecurityInternet SecurityInternet SecurityInternet Security 30303030----MarMarMarMar----11111111 176176176176

TickerTickerTickerTicker

IPO IPO IPO IPO

ShareShareShareShare

PricePricePricePrice

Adj IPO Adj IPO Adj IPO Adj IPO

Share Share Share Share

PricePricePricePrice

Adj IPOAdj IPOAdj IPOAdj IPO

OpenOpenOpenOpen

Adj IPOAdj IPOAdj IPOAdj IPO

CloseCloseCloseClose

Adj 1Adj 1Adj 1Adj 1----

WeekWeekWeekWeek

PricePricePricePrice

Adj 1Adj 1Adj 1Adj 1----

MonthMonthMonthMonth

PricePricePricePrice

CurrentCurrentCurrentCurrent

PricePricePricePrice

SOHU 13131313 13131313 13.0313.0313.0313.03 13131313 12.0612.0612.0612.06 5.755.755.755.75 105.74105.74105.74105.74

BIDU 27272727 2.72.72.72.7 6.66.66.66.6 12.2512.2512.2512.25 9.59.59.59.5 7.787.787.787.78 148.52148.52148.52148.52

1688 13.513.513.513.5 13.513.513.513.5 30303030 38.4838.4838.4838.48 28.1728.1728.1728.17 32.4832.4832.4832.48 13.7813.7813.7813.78

CYOU 16161616 16161616 22222222 20.0220.0220.0220.02 25252525 32.6232.6232.6232.62 45.3245.3245.3245.32

HSFT 10101010 10101010 10.2510.2510.2510.25 10.410.410.410.4 11111111 12121212 18.6618.6618.6618.66

SFUN 42.542.542.542.5 10.62510.62510.62510.625 16.7516.7516.7516.75 18.3818.3818.3818.38 17.4217.4217.4217.42 18.218.218.218.2 23.0523.0523.0523.05

CCIH 13.913.913.913.9 13.913.913.913.9 27272727 27.1527.1527.1527.15 23.5323.5323.5323.53 23.7123.7123.7123.71 16.8116.8116.8116.81

DANG 16161616 16161616 24.524.524.524.5 29.9129.9129.9129.91 27272727 29.4229.4229.4229.42 23.1623.1623.1623.16

YOKU 12.812.812.812.8 12.812.812.812.8 27272727 33.4433.4433.4433.44 33.333.333.333.3 38.938.938.938.9 59.6959.6959.6959.69

QIHU 14.514.514.514.5 14.514.514.514.5 27272727 34343434 30.330.330.330.3 28.528.528.528.5 28.7228.7228.7228.72

24

Using IPO Offering PriceUsing IPO Offering PriceUsing IPO Offering PriceUsing IPO Offering Price

TickerTickerTickerTicker

Open vs Open vs Open vs Open vs

IPOIPOIPOIPO

OfferingOfferingOfferingOffering

First First First First

Day IPO Day IPO Day IPO Day IPO

PricePricePricePrice

ReturnReturnReturnReturn

1111----WeekWeekWeekWeek

ReturnReturnReturnReturn

1111----MonthMonthMonthMonth

ReturnReturnReturnReturn

TotalTotalTotalTotal

ReturnReturnReturnReturn

SOHU 0.23%0.23%0.23%0.23% 0.00%0.00%0.00%0.00% ----7.23%7.23%7.23%7.23% ----55.77%55.77%55.77%55.77% 713.38%713.38%713.38%713.38%

BIDU 144.44%144.44%144.44%144.44% 353.70%353.70%353.70%353.70% 251.85%251.85%251.85%251.85% 188.15%188.15%188.15%188.15% 5400.74%5400.74%5400.74%5400.74%

1688 122.22%122.22%122.22%122.22% 185.04%185.04%185.04%185.04% 108.67%108.67%108.67%108.67% 140.59%140.59%140.59%140.59% 2.07%2.07%2.07%2.07%

CYOU 37.50%37.50%37.50%37.50% 25.13%25.13%25.13%25.13% 56.25%56.25%56.25%56.25% 103.88%103.88%103.88%103.88% 183.25%183.25%183.25%183.25%

HSFT 2.50%2.50%2.50%2.50% 4.00%4.00%4.00%4.00% 10.00%10.00%10.00%10.00% 20.00%20.00%20.00%20.00% 86.60%86.60%86.60%86.60%

SFUN 57.65%57.65%57.65%57.65% 72.99%72.99%72.99%72.99% 63.95%63.95%63.95%63.95% 71.29%71.29%71.29%71.29% 116.94%116.94%116.94%116.94%

CCIH 94.24%94.24%94.24%94.24% 95.32%95.32%95.32%95.32% 69.28%69.28%69.28%69.28% 70.58%70.58%70.58%70.58% 20.94%20.94%20.94%20.94%

DANG 53.13%53.13%53.13%53.13% 86.94%86.94%86.94%86.94% 68.75%68.75%68.75%68.75% 83.88%83.88%83.88%83.88% 44.75%44.75%44.75%44.75%

YOKU 110.94%110.94%110.94%110.94% 161.25%161.25%161.25%161.25% 160.16%160.16%160.16%160.16% 203.91%203.91%203.91%203.91% 366.33%366.33%366.33%366.33%

QIHU 86.21%86.21%86.21%86.21% 134.48%134.48%134.48%134.48% 108.97%108.97%108.97%108.97% 96.55%96.55%96.55%96.55% 98.07%98.07%98.07%98.07%

70.91% 111.88% 89.06% 92.30% 703.31%

Using First Day Adj OpenUsing First Day Adj OpenUsing First Day Adj OpenUsing First Day Adj Open

TickerTickerTickerTicker

First First First First

DayDayDayDay

ReturnReturnReturnReturn

1111----WeekWeekWeekWeek

ReturnReturnReturnReturn

1111----MonthMonthMonthMonth

ReturnReturnReturnReturn

TotalTotalTotalTotal

ReturnReturnReturnReturn

SOHU ----0.23%0.23%0.23%0.23% ----7.44%7.44%7.44%7.44% ----55.87%55.87%55.87%55.87% 711.51%711.51%711.51%711.51%

BIDU 85.61%85.61%85.61%85.61% 43.94%43.94%43.94%43.94% 17.88%17.88%17.88%17.88% 2150.30%2150.30%2150.30%2150.30%

1688 28.27%28.27%28.27%28.27% ----6.10%6.10%6.10%6.10% 8.27%8.27%8.27%8.27% ----54.07%54.07%54.07%54.07%

CYOU ----9.00%9.00%9.00%9.00% 13.64%13.64%13.64%13.64% 48.27%48.27%48.27%48.27% 106.00%106.00%106.00%106.00%

HSFT 1.46%1.46%1.46%1.46% 7.32%7.32%7.32%7.32% 17.07%17.07%17.07%17.07% 82.05%82.05%82.05%82.05%

SFUN 9.73%9.73%9.73%9.73% 4.00%4.00%4.00%4.00% 8.66%8.66%8.66%8.66% 37.61%37.61%37.61%37.61%

CCIH 0.56%0.56%0.56%0.56% ----12.85%12.85%12.85%12.85% ----12.19%12.19%12.19%12.19% ----37.74%37.74%37.74%37.74%

DANG 22.08%22.08%22.08%22.08% 10.20%10.20%10.20%10.20% 20.08%20.08%20.08%20.08% ----5.47%5.47%5.47%5.47%

YOKU 23.85%23.85%23.85%23.85% 23.33%23.33%23.33%23.33% 44.07%44.07%44.07%44.07% 121.07%121.07%121.07%121.07%

QIHU 25.93%25.93%25.93%25.93% 12.22%12.22%12.22%12.22% 5.56%5.56%5.56%5.56% 6.37%6.37%6.37%6.37%

18.83% 8.83% 10.18% 311.76%

25

Using Using Using Using First Day Adj CloseFirst Day Adj CloseFirst Day Adj CloseFirst Day Adj Close

TickerTickerTickerTicker

1111----WeekWeekWeekWeek

ReturnReturnReturnReturn

1111----MonthMonthMonthMonth

ReturnReturnReturnReturn

TotalTotalTotalTotal

ReturnReturnReturnReturn

SOHU -7.23% -55.77% 713.38%

BIDU -22.45% -36.49% 1112.41%

1688 -26.79% -15.59% -64.19%

CYOU 24.88% 62.94% 126.37%

HSFT 5.77% 15.38% 79.42%

SFUN -5.22% -0.98% 25.41%

CCIH -13.33% -12.67% -38.08%

DANG -9.73% -1.64% -22.57%

YOKU -0.42% 16.33% 78.50%

QIHU -10.88% -16.18% -15.53%

Average: -6.54% -4.47% 199.51%

0

20

40

60

80

100

120

140

160

Adj IPO

Share Price

Adj IPO

Open

Adj IPO

Close

Adj 1-Week

Price

Adj 1-Month

Price

Current

Price

Pri

ce (

$/s

ha

re)

Day (Graph Not Scaled to Time Period)

China Tech IPO Price Trends

Sohu

Baidu

Alibaba

Changyou.com

hiSoft Tech

SouFun

ChinaCache Intl

Dangdang

Youku

Qihoo

26

INVESTMENT STRATEGY FOR RENREN

SPECULATIVE

HIGH VOLATILITY

ESTIMATE OPEN $14 TO $20

ESTIMATE 1ST

DAY CLOSE $16 TO $28

ENTRY PRICE: $14 TO $18

AVOID 1ST DAY ENTRY PRICE OF ABOVE $20 (HIGH RISK)

1 YEAR PRICE TARGET $30

Even though RenRen will be an overvalued stock from the start, the hype and exuberance will

drive investors and traders to speculate and drive up the price on this stock. From our IPO

analysis of China Internet IPOs, the 1st

day opening vs. IPO Offering price has ranged from

0.23% Sohu to 144% Baidu. Since the Renren’s IPO price will be between $12 to $14 dollars and

the current hype, The IPO price of Renren could estimate to open from $14 to $20. Since the

investment bankers on the deal already raised the IPO price from $9 to $11. That has already

increased the price by about 30%. If you do plan to invest in Renren, you should enter a limit

order versus a market order to prevent panic buying at a very high price. It’s possible for the

stock to hit an intraday high of as high as $28 on the 1st day and drop back to there. It would be

a very unlikely event for the stock to drop below the IPO price since the current market liquidity

is very strong, and it’s in the investment bankers’ interest to have a very strong IPO for the 1st

of a list of social network IPO. Please be aware that the 1st

day price volatility could be very

high. You should have a plan on what price you are willing to purchase and be disciplined.

Research report by:

Kenny Hong, CFA

Vice President, Investment Advisory

Shanghai mobile: +(86) 151-2111-5396

Analyst Research Contribution by (Alphabetize by first name)

Gabriel Wong

Jay Patel

Kelly Lai

Stephanie Miao

27

General: Additional information is available upon request. Information has been obtained from

sources believed to be reliable but CT Business Solutions Ltd. or its affiliates and/or subsidiaries

do not warrant its completeness or accuracy except with respect to any disclosures relative to

and/or its affiliates and the analyst’s involvement with the issuer that is the subject of the

research. All pricing is as of the close of market for the securities discussed, unless otherwise

stated. Opinions and estimates constitute our judgment as of the date of this material and are

subject to change without notice. Past performance is not indicative of future results. This

material is not intended as an offer or solicitation for the purchase or sale of any financial

instrument. The opinions and recommendations herein do not take into account individual client

circumstances, objectives, or needs and are not intended as recommendations of particular

securities, financial instruments or strategies to particular clients. The recipient of this report

must make its own independent decisions regarding any securities or financial instruments

mentioned herein. CT Business Solutions Ltd. distributes in the U.S. research published by non-

U.S. affiliates and accepts responsibility for its contents. Periodic updates may be provided on

companies/industries based on company specific developments or announcements, market

conditions or any other publicly available information. Clients should contact analysts and

execute transactions through a subsidiary or affiliate in their home jurisdiction unless governing

law permits otherwise.

Copyright 2011 CT Business Solutions Ltd. All rights reserved. This report or any portion hereof may not be reprinted,

sold or redistributed without the written consent of CT Business Solutions Ltd.#$J&