repair after the earthquakes

DESCRIPTION

Presentation for South Brighton and Southshore 1st May 2013TRANSCRIPT

Presentation prepared for residents of Southshore and South Brighton

on 1 May 2013This presentation is purely my personal assessment of the situation some TC3 residents are facing.

As of 1st May 2013.

Council has been asked to confirm the understanding that is stated in this presentation.They have refused to neither confirm or correct what is stated here.

Christchurch City Councils response: Rebuild & Repair requirements have already been made publicly available via MBIE’s, Councils,

& CERA’s, websites; & by way of Public presentations and trade shows.

This presentation is not a Christchurch City Council or CERA document.

It is my hope that Council confirms that my understanding of the situation is incorrect and states how they are going to protect the residents and the building stock in Christchurch.

Hugo KristinssonMember of:

South Brighton Resident’s Association

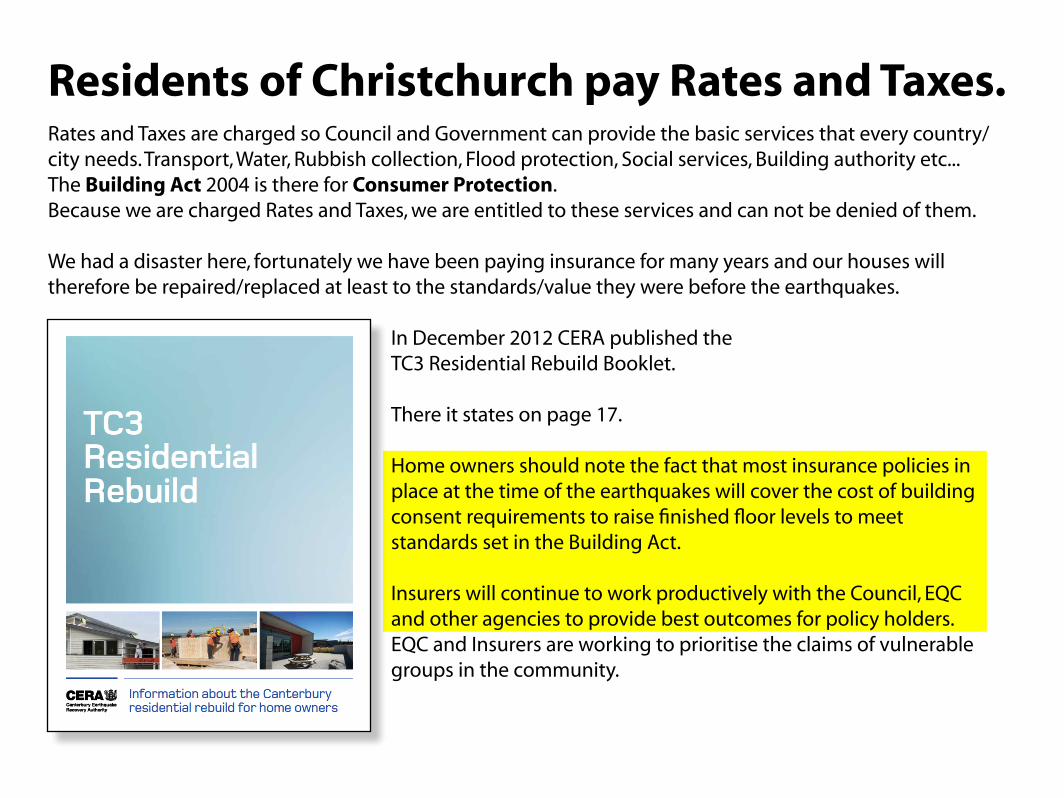

Residents of Christchurch pay Rates and Taxes. Rates and Taxes are charged so Council and Government can provide the basic services that every country/city needs. Transport, Water, Rubbish collection, Flood protection, Social services, Building authority etc...The Building Act 2004 is there for Consumer Protection.Because we are charged Rates and Taxes, we are entitled to these services and can not be denied of them.

We had a disaster here, fortunately we have been paying insurance for many years and our houses will therefore be repaired/replaced at least to the standards/value they were before the earthquakes.

In December 2012 CERA published the TC3 Residential Rebuild Booklet.

There it states on page 17.

Home owners should note the fact that most insurance policies in place at the time of the earthquakes will cover the cost of building consent requirements to raise finished floor levels to meetstandards set in the Building Act.

Insurers will continue to work productively with the Council, EQC and other agencies to provide best outcomes for policy holders.EQC and Insurers are working to prioritise the claims of vulnerable groups in the community.

What is being proposed here?Before the Earthquakes we had our properties and they were of a good value.

Houses built 1970 and later were required to have floor levels at 11.5mThis is an example of one of those buildings as they are most common here.

Type B house timber floor withPerimeter footing

Ground water 80cm

September 2010

Land Levels 11,2m

Floor Levels 11,5m

EarthquakesThe land shook.

Land where groundwater is high, liquefied.The land subsided.

Houses tilted and some sunk.Some cracked.

These houses will be repaired or rebuilt by Insurance companies or the Project Management Office = Fletchers EQR

Type B house timber floor withPerimeter footing

Ground water 20cm

May 2013

Land Levels 10,6m 49% of piles need replacements

Floor Levels 10,9m Land Subsidence 60cm

Un-consentedBuilding Consent NO Geotech Drilling NO

Groundwater Checked NO Land strength Checked NO

Structural Engineers report NOLand remediation NO

Building inspection NOCheck for Hazard notices NO

Liability if failure OWNER

Type B house

Ground water 20cm

May 2015

Land Levels 10,6m

49% of piles replaced

Floor Levels 10,9m

No Land remediation

Type B house

Ground water 100cm

Land Levels 11,4m

RibRaft FoundationFloor Levels 11,8m

Land remediationSuface structure

Building Act 2004, repairCouncil consented plans YES

Geotech Drilling YESGroundwater Checked YES Land strength Checked YES

Structural Engineers report YESSurface Structure required YES

Consented Foundations according to land conditions YESProgressive building inspection on all important issues YES

Councils liability as per leaky house syndrome YESCouncil confirmed no Hazard notices YES

Liability if failure COUNCIL

Changes on the Horizon Ecan has published a new approach to managing

Canterbury’s Floodplains in February 2013

Over the last 20 years there has been an increased realisation worldwide that full reliance on structural measures, such as stop- banks, to prevent flood damages is unrealistic and not cost effec-

tive. The emphasis now is to find a balance between measures that keep floodwaters away from people and those that keep

people away from floodwaters. Flood Protection & Drainage Bylaw 2013 are being updated and

Council states acceptable inundation will be 40cm.

Type B house

Ground water 20cm

May 2016

Land Levels 10,6m

49% of piles replaced

Floor Levels 10,9m

No Land remediation

Type B house

Ground water 100cm

Land Levels 11,4m

RibRaft FoundationFloor Levels 11,8m

Land remediationSuface structure

CCC Acceptable inundation 40cm

A D D W A T E R

Un-consented Repair As repairs were unconsented the owner has all the liability.After one or two flood events insurance companies will refuse flood insurance.Council can at any stage issue a Hazard notice reducing the value of the property.EQC can deny liability in case of further events.Subject to a Hazard Notice

2026

Type B house

Worst case scenario

Type B house

F U T U R E E V E N T SIf we have future events here, land subsidence, earthquakes or flooding.

A consented repair will have full insurance cover. Covered by EQC and Insurance Company.A property that has a Hazard notice is unlikely to have any insurance cover.

A property repaired on a weak land can be refused cover for subsidence.After repeated flooding insurance companies can refuse insurance cover.

Your bank can forfeit your mortgage.

Water will always find its way through sand. If land subsides close to water, groundwater rises and land bearing capacity decreases.

Higher groundwater increases risk of Liquefaction.

No insuranceOwners loss

EQC and insurance company liable

She’ll be right!I do not think so.

Plan for the worst Hope for the best

Is it fair to say that the Building Act 2004 is for Consumer Protection for all New Zealand residents except the residents of Christchurch?

For your own protection consider these issues before accepting any repair proposal.Ask for a written statement from your current insurance company that they will continue to provide ongoing insurance for subsidence and flooding after the repair.

Ask for a statement from your bank that your property is a valid mortgage security after the proposed repairs.

Council consented and inspected repairs. Considering the cost of a building consent is only around $5-7000 and that is your right as a tax payer. I recommend a Building Consent for any major repair.

333