report for the 2nd quarter 2018 - euroland

TRANSCRIPT

Report for the 2nd quarter 2018

Norwegian Finans Holding ASA

Letter from the CEO

Current quarter

Bank Norwegian is operating in a benign environment. The Nordic region is still experiencing robust

GDP development and favorable employment on an overall level combined with low interest rates.

Regulatory focus on the financial industry has increased lately to ensure sustainable development in

household economies. Bank Norwegian has successfully adapted its historically solid credit vetting and

prudent provision policy to accommodate updated regulations and guidelines.

Second quarter results reflect the favorable backdrop where record high profits of MNOK 484 are

combined with robust growth both in terms of loans and customers. Customer engagement continues

to increase as shown from the app where app logins exceeded 40,000 customers daily and 1 million

monthly. The app was revamped in June to improve sales and interactive communication with our 1.4

million customers.

During the quarter, the mutually beneficial partnership with Norwegian Air Shuttle ASA was extended

by a 10-year agreement. Our focus is still on the attractive Nordic region, with an option to explore

new markets. We launched additional third-party insurance products in addition to the current offering

of products comprising more than 100,000 active policies. Insurance is an area that has not yet been

developed to its full potential and will be further explored.

Two-tier strategy

In addition to favorable macro conditions, we expect continued growth in our core products due to

the strong awareness of- and trust in Bank Norwegian’s brand in all markets. Further, IFRS 9

implementation and improved risk selection tools such as proprietary scorecards throughout our

footprint will optimize pricing and strengthen the competitive position.

Bank Norwegian’s cost-efficient operation and fully digitalized customer journey combined with a

focused selection of own products on the balance sheet enables us to be highly competitive and is

widely considered to be the future model of banking. Going forward we will leverage our customer

insight, trust and engagement to enter lucrative niche markets and provide access to industry-leading

services from third parties in addition to our own products. Bank Norwegian will explore

the attractiveness of account information agent (AISP) and payment agent (PISP) positions in

connection with the implementation of PSD2 regulation by Nordic banks to ensure rapid

implementation of chosen commercial positions.

Bærum, August 14, 2018

-----------------------------------------

Tine Wollebekk, CEO

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

1

Norwegian Finans Holding ASA Report for the 2nd quarter 2018

Norwegian Finans Holding ASA (NFH) owns 100% of the shares in Bank Norwegian AS. The company does not engage in any other operations. The ownership of Norwegian Finans Holding ASA is divided between institutional and private investors in Norway and abroad, of which Norwegian Air Shuttle ASA is the largest owner with a stake of 16.4% at the end of the 2nd quarter 2018. Norwegian Finans Holding ASA is listed on the Oslo Stock Exchange with the ticker code NOFI.

Bank Norwegian started its operations in November 2007 and offers consumer loans, credit cards and deposit accounts to retail customers distributed through the Internet in the Nordic market. Bank Norwegian offers, in cooperation with the airline Norwegian, a combined credit card and reward card. The bank started operations in Sweden in May 2013. In December 2015 the bank launched operations in Denmark and Finland, where it initially offered consumer loans and deposit accounts. Credit cards were launched in June 2016.

Bank Norwegian is a digital bank that offers simple and competitive products to the retail market. The strategy is based on leading digital solutions, synergies with the airline Norwegian, attractive terms for our customers, cost-effective operations and effective risk selection.

At the end of the 2nd quarter 2018 the NFH Group had a customer base of 1,392,600 customers, which can be broken down into 1,018,300 credit card customers, 187,400 loan customers and 186,900 deposit customers.

Profit and loss as of June 30, 2018 The NFH Group’s comprehensive income amounted to MNOK 893.4 as of June 30, 2018, compared with MNOK 728.4 for the same period in 2017. Net interest income totalled MNOK 2,120.3, net other operating income amounted to MNOK 134.4, while total operating expenses were MNOK 619.9. Provisions for loan losses were MNOK 443.6.

Profit and loss for the 2nd quarter 2018 The NFH Group’s comprehensive income amounted to MNOK 482.8 compared with MNOK 410.6 in the 1st quarter 2018. Annual return on equity in the 2nd quarter was 33.4%, while return on assets was 4.2%.

Net interest income amounted to MNOK 1,091.8, an increase of MNOK 63.3 from the 1st quarter. The increase is mainly explained by loan growth. The net interest margin was 9.4%, compared with 9.5% in the 1st quarter.

Net other operating income amounted to MNOK 94.1 compared with MNOK 40.4 in the 1st quarter. Net commission income increased with MNOK 19.1 to MNOK 73.0 due to network and insurance incentive in addition to increased credit card usage. Net gain on securities and currency amounted to MNOK 21.1, compared with a net loss of MNOK 13.5 in the 1st quarter. The change is due to a gain on currency, compared with a loss in the 1st quarter.

Total operating expenses amounted to MNOK 307.4 compared with MNOK 312.6 in the 1st quarter. Personnel expenses decreased with MNOK 4.1 due to accrual effects. The MNOK 2.1 decrease in administrative expenses is explained by lower spending on digital marketing expenses and non-recurring items in the 1st quarter. Depreciation increased with MNOK 0.2. Other operating expenses increased with MNOK 0.8.

The NFH Group’s write-downs on loans were MNOK 234.7, an increase of MNOK 25.8 from the 1st quarter. Write-downs in the 2nd quarter equalled 2.6% of average gross loans, compared with 2.4% in the 1st quarter. Gross delinquent loans were MNOK 3,785, compared with MNOK 3,160 at the end of the 1st quarter. Delinquent loans accounted for 10.3% of gross loans, compared with 9.0% at the end of the 1st quarter. Gross non-performing loans accounted for 8.1% of gross loans, compared with 7.1% as of 31.3.2018. The level of non-performing loans is developing as expected considering the unseasoned portfolios in Denmark and Finland, and the portfolios in Norway and Sweden are increasing from a low base following the sale of non-performing loan portfolios in 2017.

Balance sheet as of June 30, 2018 Total assets increased with MNOK 2,179 in the quarter and amounted to MNOK 47,551.

Net loans to customers increased MNOK 1,621 and amounted to MNOK 35,435. The loan growth is comparable to the previous quarter, adjusted for currency changes. Consumer loans amounted to MNOK 26,465 and credit card loans amounted to MNOK 10,421.

Customer deposits increased MNOK 1,917 and amounted to MNOK 37,706 at the end of the quarter.

Liquid assets increased MNOK 582 and amounted to MNOK 11,779, equivalent to 24.8% of total assets.

The general meeting in Bank Norwegian AS resolved to distribute a group contribution of MNOK 247.5 in the 2nd quarter to Norwegian Finans Holding ASA.

Total equity amounted to MNOK 6,655, compared with MNOK 6,174 as of 31.3.2018. The total capital ratio was 21.1%, the core capital ratio was 19.6% and the common equity tier 1 ratio was 17.7% as of 30.6.2018.

There has been a limited review of the accounts as of 30.6.2018, and the full result is added to retained earnings.

Outlook for the remaining of the year The economic trends in the Nordic markets where the NFH Group operates are positive. The Norwegian economy shows increasing growth and falling unemployment rate. The Swedish economy is showing a high economic growth. The Danish and Finnish economies show moderate growth and an improved labor market.

The interest rate levels in the countries where the NFH Group is represented are expected to remain low, although higher interest rates are expected going forward. The NFH

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

2

Group is still expected to benefit from the interest rate level through low funding costs.

The earnings growth is expected to continue through strong loan growth, stable margins, cost control and good credit quality, even though the Nordic market for unsecured credit is impacted by increased competition. Increased competition may lead to higher customer acquisition cost, margin pressure or lower growth. Increased run-off in line with a growing portfolio may affect future loan growth.

The NFH Group has a broad Nordic platform and loan volumes are growing faster outside of Norway. The NFH Group has therefore a diversified risk in relation to the individual markets.

A high deposit to loans ratio and good access to the securities market are expected to maintain the NFH Group’s strong liquidity position.

The investment portfolio has provided a satisfactory return. The portfolio's low risk mandate will remain.

The credit quality of the loan portfolio in Norway shows a stable development and the levels of write-downs are

expected to remain stable going forward.

After the sale of non-performing loan portfolios in Norway and Sweden, the delinquency is expected to gradually increase to a normalized level. The Danish and Finnish loan portfolios show a stable development. Relatively high write-downs in Denmark and Finland are still expected for a period going forward.

Common equity tier 1 ratio was 17.7% at the reporting date and exceeds the current minimum common equity tier 1 ratio requirement of 15.5% with a wide margin. The NFH Group aims to maintain a good margin to the minimum capital adequacy requirements.

The current capital base and internal generation of capital are considered sufficient to ensure the NFH Group's growth ambitions.

As previously announced, July 4th, Norwegian Finans Holding ASA does not expect to pay dividends based on interim financial accounts in 2018. Any dividend based on interim financial accounts must await legal clarification and regulatory dialog.

Bærum, August 14, 2018 Board of directors of Norwegian Finans Holding ASA

_________________ Bjørn Østbø

Chairman of the Board

_________________ John Høsteland Board Member

____________________ Anita Aarnæs

Board Member

_________________ Christine Rødsæther

Board Member

____________________ Gunn Ingemundsen

Board Member

____________________ Rolv-Erik Spilling Board Member

____________________ Tine Wollebekk

CEO

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

3

Profit and loss account

Norwegian Finans Holding Group

Amounts in NOK 1000 Note Q2 2018 Q2 2017 YTD 2018 YTD 2017 2017

Interest income, amortised cost 1,222,548 992,282 2,369,547 1,904,990 4,077,561

Other interest income 23,863 24,177 48,069 45,518 95,122

Interest expenses 154,602 124,215 297,268 232,561 502,211

Net interest income 10 1,091,808 892,245 2,120,348 1,717,947 3,670,472

Commission and bank services income 11 143,359 93,728 263,198 174,620 399,998

Commission and bank services expenses 11 70,387 50,118 136,379 92,267 211,091

Net change in value on securities and currency 12 21,089 4,612 7,613 10,127 7,458

Net other operating income 94,061 48,222 134,432 92,480 196,365

Total income 1,185,869 940,467 2,254,780 1,810,427 3,866,837

Personnel expenses 17,373 16,351 38,858 35,745 74,957

General administrative expenses 13 264,770 215,419 531,664 431,398 906,286

Ordinary depreciation 12,150 10,861 24,072 22,236 44,477

Other operating expenses 14 13,082 10,835 25,350 22,423 45,484

Total operating expenses before losses 307,374 253,466 619,944 511,803 1,071,204

Provision for loan losses 3, 5, 6 234,707 155,193 443,609 332,417 672,388

Profit before tax 643,788 531,808 1,191,227 966,207 2,123,245

Tax charge 160,967 132,779 297,794 241,387 526,194

Profit after tax 482,822 399,029 893,433 724,820 1,597,050

Earnings per share (kroner) 2.59 2.19 4.79 3.97 8.60

Diluted earning per share (kroner) 2.59 2.19 4.79 3.97 8.60

Comprehensive incomeNorwegian Finans Holding Group

Amounts in NOK 1000 Q2 2018 Q2 2017 YTD 2018 YTD 2017 2017

Profit on ordinary activities after tax 482,822 399,029 893,433 724,820 1,597,050

Change in fair value for assets available for sale - 937 - 3,629 8,176

Tax - -7 - -27 -61

Other comprehensive income - 930 - 3,602 8,115

Comprehensive income for the period 482,822 399,959 893,433 728,421 1,605,165

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

4

Balance sheetNorwegian Finans Holding Group

Amounts in NOK 1000 Note 30.6.18 30.6.17 31.12.17

Assets

Cash and deposits with the central bank 9, 16 65,975 61,981 65,976

Loans and deposits with credit institutions 9, 16 2,323,345 1,394,852 1,260,947

Loans to customers 4, 7, 16 35,434,748 28,868,053 32,451,553

Certificates and bonds 15 9,389,792 8,185,779 8,859,834

Financial derivatives 15 43,768 946 1,935

Shares and other securities 15, 18 37,476 443 443

Assets available for sale 15, 18 - 28,374 32,922

Intangible assets 114,923 117,965 114,678

Deferred tax asset 11,157 8,318 15,904

Fixed assets 810 1,094 1,000

Receivables 19 128,630 131,124 194,800

Total assets 47,550,624 38,798,929 42,999,992

Liabilities and equity

Loans from credit institutions 85,450 - -

Deposits from customers 16 37,705,983 30,922,923 33,682,275

Debt securities issued 16, 17 1,808,003 2,040,622 2,242,423

Financial derivatives 15 2,494 3,999 52,246

Tax payable 543,078 239,822 525,886

Other liabilities 20 91,355 163,695 158,711

Accrued expenses 21 184,321 101,988 150,216

Subordinated loan 16, 17 474,622 474,721 474,614

Total liabilities 40,895,306 33,947,770 37,286,371

Share capital 186,689 186,619 186,689

Share premium 971,182 966,570 971,182

Paid, not registered capital 5,819 4,683 -

Tier 1 capital 635,000 635,000 635,000

Retained earnings and other reserves 4,856,628 3,058,288 3,920,750

Total equity 22 6,655,318 4,851,159 5,713,621

Total liabilities and equity 47,550,624 38,798,929 42,999,992

_________________

Tine Wollebekk

CEO

Board MemberBoard Member Board Member

Rolv-Erik Spilling

_________________ _________________ _________________

Christine Rødsæther Gunn Ingemundsen

Board Member

Bærum, 14 August, 2018

Board of directors of Norwegian Finans Holding ASA

John Høsteland

_________________ _________________ _________________

Bjørn Østbø Anita Aarnæs

Chairman of the Board Board Member

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

5

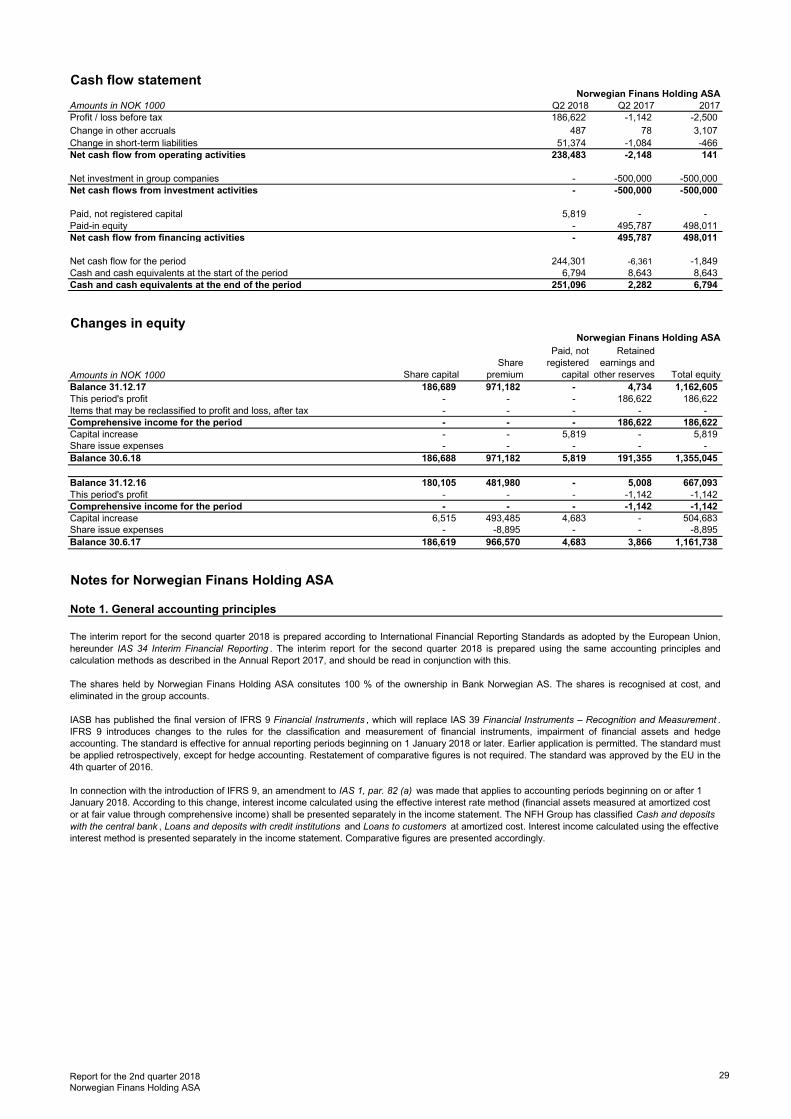

Cash flow statementNorwegian Finans Holding Group

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Profit / loss after tax 893,433 728,421 1,605,165

Unrealized gains or losses on currency 102,244 10,445 47,565

Depreciations and amortizations 24,072 22,236 44,477

Provision for loan losses 443,609 332,417 672,388

Change in loans to customers -3,372,237 -4,685,149 -8,602,143

Change in deposits from customers 4,023,708 6,499,150 9,258,502

Change in certificates and bonds -529,958 -3,721,577 -4,395,632

Change in assets available for sale, before tax - 3,629 8,176

Change in receivables, deferred tax asset and financial derivatives 31,311 -32,752 -105,003

Change in loans from credit institutions 85,450 - -

Change in shares and other securities -4,112 - -

Change in tax payable, accrued expenses and other liabilities -65,810 -34,810 342,744

Net cash flow from operating activities 1,631,710 -877,990 -1,123,760

Payment for acquisition of intangible assets -24,127 -20,950 -55,381

Payment for acquisition of tangible assets - -1,050 -1,050

Net cash flow from investment activities -24,127 -22,000 -56,431

Paid-in share capital and share premium - 495,787 495,787

Paid, not registered capital 5,819 - -

Issued debt securities - 500,000 1,299,320

Repayment of debt securities -434,413 -283,351 -880,870

Issued subordinated loan - 199,806 199,699

Issued Tier 1 capital - 299,250 299,250

Paid interest Tier 1 capital -14,347 -7,576 -21,858

Net cash flow from financing activities -442,942 1,203,916 1,391,328

Currency effect on cash and cash equivalents -102,244 -10,445 -47,565

Net cash flow for the period 1,062,398 293,482 163,571

Cash and cash equivalents at the start of the period 1,326,922 1,163,351 1,163,351

Cash and cash equivalents at the end of the period 2,389,320 1,456,833 1,326,922

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

6

Changes in equityNorwegian Finans Holding Group

Amounts in NOK 1000

Balance 31.12.17 186,689 971,182 - 635,000 3,920,750 5,713,621

This period's profit - - - - 893,433 893,433

Items that may be reclassified to profit and loss, after tax - - - - - -

Comprehensive income for the period - - - - 893,433 893,433

Paid interest Tier 1 capital - - - - -14,347 -14,347

Capital increase - - 5,819 - - 5,819

Other changes - - - - 2,226 2,226

Change in write-downs under IFRS 9 - - - - 54,567 54,567

Balance 30.6.18 186,689 971,182 5,819 635,000 4,856,629 6,655,318

Amounts in NOK 1000

Balance 31.12.16 180,105 481,980 - 335,000 2,338,191 3,335,276

This period's profit - - - - 724,820 724,820

Items that may be reclassified to profit and loss, after tax - - - - 3,602 3,602

Comprehensive income for the period - - - - 728,421 728,421

Paid interest Tier 1 capital - - - - -7,575 -7,575

Capital increase 6,515 493,485 4,683 - - 504,682

Share issue expenses - -8,895 - - - -8,895

Issued Tier 1 capital - - - 300,000 -750 299,250

Balance 30.6.17 186,619 966,570 4,683 635,000 3,058,288 4,851,159

Share

capital

Share

premium

Tier 1

capital

Retained

earnings and

other reserves

Total

equity

Paid, not

registered

capital

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

7

IASB has published the final version of IFRS 9 Financial Instruments , which replaced IAS 39 Financial Instruments – Recognition and Measurement .

IFRS 9 introduced changes to the rules for the classification and measurement of financial instruments, impairment of financial assets and hedge

accounting. The standard is effective for annual reporting periods beginning on 1 January 2018 or later. Earlier application is permitted. The standard

must be applied retrospectively, except for hedge accounting. Restatement of comparative figures is not required. The standard was approved by the EU

in the 4th quarter of 2016.

The rules for classification and measurement of financial assets under IFRS 9 are more principle-based than the rules under IAS 39. Under IFRS 9,

financial assets are assessed based on the entity’s business model and the asset’s cash flows. The NFH Group has made an assessment of the balance

sheet with regards to classification and measurement of financial assets. The NFH Group has reclassified Assets available for sale to Shares and other

securities . The classification and measurement of the NFH Group’s financial liabilities have not been affected by the transition to IFRS 9.

Assets available for sale , which consist of the NFH Group’s ownership interest in Visa Norge FLI, was under IAS 39 classified at fair value through other

comprehensive income (with reclassification). The asset was held for sale, and will after the implementation of IFRS 9 be classified at fair value through

profit and loss. For further details, see note 3.

IFRS 9 requires write-downs on loans to be calculated using different assumptions about future development of credit losses. The NFH Group has made

calculations of losses under IFRS 9 based on a base, upper and lower scenario. The calculations at 31.12.17 show a reduction of write-downs of NOK 55

million after tax compared to write-downs under IAS 39. The decreased in write-downs has been booked as a change in equity as per 1.1.2018, and

increased Loans to customers .

In connection with the introduction of IFRS 9, an amendment to IAS 1, par. 82 (a) was made that applies to accounting periods beginning on or after

January 1, 2018. According to this change, interest income calculated using the effective interest rate method (financial assets measured at amortized

cost or at fair value through comprehensive income) shall be presented separately in the income statement. The NFH Group has classified Cash and

deposits with the central bank , Loans and deposits with credit institutions and Loans to customers at amortized cost. Interest income calculated using the

effective interest method is presented separately in the income statement. Comparative figures are presented accordingly.

Norwegian Finans Holding ASA has received a group contribution of 247,5 million from its subsidiary Bank Norwegian AS in the second quarter.

Notes

Note 1. General accounting principles

The interim report for the second quarter 2018 is prepared according to International Financial Reporting Standards as adopted by the European Union,

hereunder IAS 34 Interim Financial Reporting . The interim report for the second quarter 2018 is prepared according to the Norwegian Ministry of

Finance's regulations on annual accounts, Section 1-6, on the use of IFRS.

IFRS 9 - Financial Instruments

Accounting standards which have been implemented in 2018

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

8

Note 2. Segments

Profit and loss account Q2 2018 YTD

Amounts in NOK 1000 Norway Sweden Denmark Total

Net interest income 1,026,904 363,658 228,890 500,892 4 2,120,348

Net other operating income 85,865 40,569 11,533 -3,238 -296 134,432

Total income 1,112,769 404,227 240,423 497,654 -292 2,254,780

Total operating expenses before losses 271,579 143,322 77,814 125,576 1,653 619,944

Provision for loan losses 113,233 69,064 95,766 165,546 - 443,609

Profit before tax 727,957 191,840 66,844 206,532 -1,945 1,191,227

Tax charge 181,989 47,960 16,711 51,633 -499 297,794

Profit after tax 545,967 143,880 50,133 154,899 -1,446 893,433

Other comprehensive income - - - - - -

Comprehensive income for the period 545,967 143,880 50,133 154,899 -1,446 893,433

Balance sheet 30.6.18Amounts in NOK 1000 Norway Sweden Denmark Total

Loans to customers 17,854,487 5,705,343 3,524,529 8,350,356 - 35,434,716

Other assets 6,880,984 2,120,460 954,403 1,902,449 257,612 12,115,908

Total assets 24,735,471 7,825,804 4,478,932 10,252,806 257,612 47,550,624

Deposits from customers 18,897,900 5,975,535 3,466,248 9,366,268 - 37,705,951

Other liabilities and equity 5,837,571 1,850,269 1,012,683 886,538 257,612 9,844,673

Total liabilities and equity 24,735,471 7,825,804 4,478,932 10,252,806 257,612 47,550,624

Profit and loss account Q2 2017 YTDAmounts in NOK 1000 Norway Sweden Denmark Total

Net interest income 953,850 321,670 134,878 307,508 41 1,717,947

Net other operating income 62,580 28,937 230 922 -188 92,480

Total income 1,016,430 350,606 135,108 308,430 -147 1,810,427

Total operating expenses before losses 252,282 111,428 68,850 77,645 1,596 511,803

Provision for loan losses 128,084 59,869 66,844 77,621 - 332,417

Profit before tax 636,063 179,309 -586 153,164 -1,743 966,207

Tax charge 159,021 44,827 -145 38,285 -601 241,387

Profit after tax 477,042 134,482 -441 114,879 -1,142 724,820

Other comprehensive income 3,602 - - - - 3,602

Comprehensive income for the period 480,644 134,482 -441 114,879 -1,142 728,421

Balance sheet 30.6.17Amounts in NOK 1000 Norway Sweden Denmark Total

Loans to customers 15,678,158 5,223,041 2,448,201 5,518,653 - 28,868,053

Other assets 7,827,478 867,892 1,010,810 217,065 7,631 9,930,876

Total assets 23,505,637 6,090,933 3,459,011 5,735,717 7,631 38,798,929

Deposits from customers 17,374,054 5,601,487 3,349,468 4,597,914 - 30,922,923

Other liabilities and equity 6,131,583 489,446 109,543 1,137,803 7,631 7,876,006

Total liabilities and equity 23,505,637 6,090,933 3,459,011 5,735,717 7,631 38,798,929

Profit and loss account 2017Amounts in NOK 1000 Norway Sweden Denmark Total

Net interest income 1,947,738 662,788 320,989 738,913 45 3,670,472

Net other operating income 128,393 60,055 3,864 4,414 -362 196,365

Total income 2,076,131 722,843 324,853 743,327 -317 3,866,837

Total operating expenses before losses 508,491 248,391 136,989 174,317 3,016 1,071,204

Provision for loan losses 192,354 147,436 151,982 180,617 - 672,388

Profit before tax 1,375,286 327,017 35,882 388,393 -3,333 2,123,245

Tax charge 336,358 84,575 7,532 98,531 -801 526,194

Profit after tax 1,038,928 242,442 28,350 289,862 -2,532 1,597,050

Other comprehensive income 8,115 - - - - 8,115

Comprehensive income for the period 1,047,043 242,442 28,350 289,862 -2,532 1,605,165

Balance 31.12.17Amounts in NOK 1000 Norway Sweden Denmark Total

Loans to customers 16,561,731 5,718,448 3,121,962 7,049,412 - 32,451,553

Other assets 6,462,719 1,937,559 926,098 1,210,522 11,541 10,548,439

Total assets 23,024,450 7,656,007 4,048,060 8,259,934 11,541 42,999,992

Deposits from customers 17,909,401 5,875,474 3,313,982 6,583,384 - 33,682,241

Other liabilities and equity 5,115,048 1,780,534 734,078 1,676,550 11,541 9,317,751

Total liabilities and equity 23,024,450 7,656,008 4,048,060 8,259,934 11,541 42,999,992

Finland

Finland

The profit and loss and balance sheet presentation for segments are based on internal financial reporting as it is reported to the groups management. The

figures are based on the NFH Group's governance model and accounting principles.

Finland

Finland

Finland

Finland

Other

Other

Other

Other

Other

Other

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

9

Change in balance sheet items

Financial assets Category Category

Cash and deposits with sentral banks Amortised cost 65,976 Amortised cost 65,976

Loans and deposits with credit institutions Amortised cost 1,260,947 Amortised cost 1,260,947

Loans to customers Amortised cost 32,451,553 Amortised cost 32,524,311

Certificates and bonds Fair value 8,859,834 Fair value 8,859,834

Financial derivatives Fair value 1,935 Fair value 1,935

Shares and other securities Fair value 443 Fair value 33,365

Assets available for sale* Fair value** 32,922 Fair value -

* Will be reclassified to Shares and other securites under IFRS 9.

** Fair value through other comprehensive income.

The tables below show the reclassification of balance sheet items and new expected credit loss.

Loans to customers

Balance 31.12.17 32,451,553 - - -

Change in expected credit loss - - 72,758 -

Balance 1.1.18 - - - 32,524,311

ECL IAS 39 IFRS 9

Balance 31.12.17 1,140,152 - - -

Change in expected credit loss - - -72,758 -

Balance 1.1.18 - - - 1,067,394

Shares and other securities IAS 39 IFRS 9

Balance 31.12.17 443 - - -

Reclassification - 32,922 - -

Balance 1.1.18 - - - 33,365

Assets available for sale IAS 39 IFRS 9

Balance 31.12.17 32,922 - - -

Reclassification - -32,922 - -

Balance 1.1.18 - - - -

IAS 39 IFRS 9

IFRS 9 IAS 39

Book value

31.12.17

Book value

1.1.18

New model

for expected

credit loss

Reclass-

ification

Reclass-

ification

Reclass-

ification

New model

for expected

credit loss

New model

for expected

credit loss

Note 3. IFRS 9

New model

for expected

credit loss

Reclass-

ification

Note 3.1. Change in balance sheet items

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

10

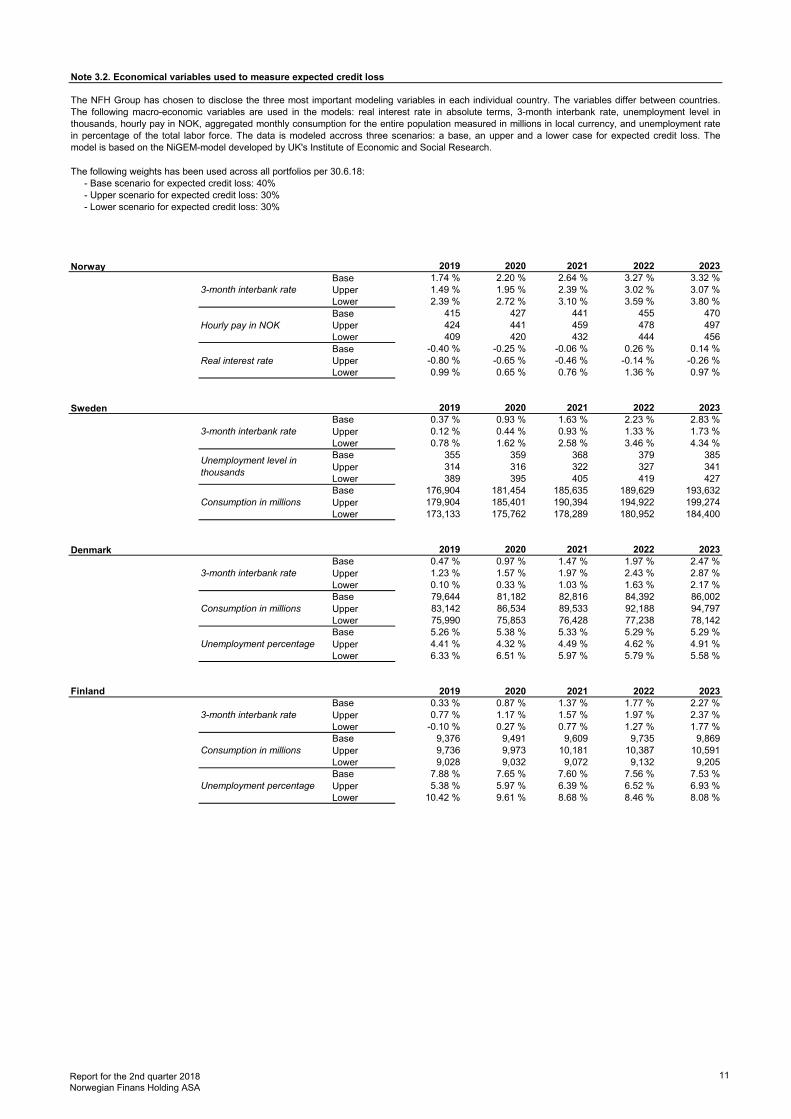

The following weights has been used across all portfolios per 30.6.18:

- Base scenario for expected credit loss: 40%

- Upper scenario for expected credit loss: 30%

- Lower scenario for expected credit loss: 30%

Norway 2019 2020 2021 2022 2023

Base 1.74 % 2.20 % 2.64 % 3.27 % 3.32 %

3-month interbank rate Upper 1.49 % 1.95 % 2.39 % 3.02 % 3.07 %

Lower 2.39 % 2.72 % 3.10 % 3.59 % 3.80 %

Base 415 427 441 455 470

Hourly pay in NOK Upper 424 441 459 478 497

Lower 409 420 432 444 456

Base -0.40 % -0.25 % -0.06 % 0.26 % 0.14 %

Real interest rate Upper -0.80 % -0.65 % -0.46 % -0.14 % -0.26 %

Lower 0.99 % 0.65 % 0.76 % 1.36 % 0.97 %

Sweden 2019 2020 2021 2022 2023

Base 0.37 % 0.93 % 1.63 % 2.23 % 2.83 %

3-month interbank rate Upper 0.12 % 0.44 % 0.93 % 1.33 % 1.73 %

Lower 0.78 % 1.62 % 2.58 % 3.46 % 4.34 %

Base 355 359 368 379 385

Upper 314 316 322 327 341

Lower 389 395 405 419 427

Base 176,904 181,454 185,635 189,629 193,632

Consumption in millions Upper 179,904 185,401 190,394 194,922 199,274

Lower 173,133 175,762 178,289 180,952 184,400

Denmark 2019 2020 2021 2022 2023

Base 0.47 % 0.97 % 1.47 % 1.97 % 2.47 %

3-month interbank rate Upper 1.23 % 1.57 % 1.97 % 2.43 % 2.87 %

Lower 0.10 % 0.33 % 1.03 % 1.63 % 2.17 %

Base 79,644 81,182 82,816 84,392 86,002

Consumption in millions Upper 83,142 86,534 89,533 92,188 94,797

Lower 75,990 75,853 76,428 77,238 78,142

Base 5.26 % 5.38 % 5.33 % 5.29 % 5.29 %

Unemployment percentage Upper 4.41 % 4.32 % 4.49 % 4.62 % 4.91 %

Lower 6.33 % 6.51 % 5.97 % 5.79 % 5.58 %

Finland 2019 2020 2021 2022 2023

Base 0.33 % 0.87 % 1.37 % 1.77 % 2.27 %

3-month interbank rate Upper 0.77 % 1.17 % 1.57 % 1.97 % 2.37 %

Lower -0.10 % 0.27 % 0.77 % 1.27 % 1.77 %

Base 9,376 9,491 9,609 9,735 9,869

Consumption in millions Upper 9,736 9,973 10,181 10,387 10,591

Lower 9,028 9,032 9,072 9,132 9,205

Base 7.88 % 7.65 % 7.60 % 7.56 % 7.53 %

Unemployment percentage Upper 5.38 % 5.97 % 6.39 % 6.52 % 6.93 %

Lower 10.42 % 9.61 % 8.68 % 8.46 % 8.08 %

Note 3.2. Economical variables used to measure expected credit loss

The NFH Group has chosen to disclose the three most important modeling variables in each individual country. The variables differ between countries.

The following macro-economic variables are used in the models: real interest rate in absolute terms, 3-month interbank rate, unemployment level in

thousands, hourly pay in NOK, aggregated monthly consumption for the entire population measured in millions in local currency, and unemployment rate

in percentage of the total labor force. The data is modeled accross three scenarios: a base, an upper and a lower case for expected credit loss. The

model is based on the NiGEM-model developed by UK's Institute of Economic and Social Research.

Unemployment level in

thousands

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

11

Norway

<=5% 700 % <=2% 900 %

>5%, 10%] 30 % >2% 0 %

>10% 20 %

Sweden

<=20% 30 % <=2% 900 %

>20% 10 % >2%, 5%] 40 %

>5% 0 %

Denmark

<=20% 300 % <=50% 80 %

>20%, 40%] 100 % >50% 0 %

>40% 20 %

Finland

<=20% 200 % <=30% 200 %

>20%, 40%] 100 % >30% 30 %

>40% 40 %

Note 3.3. Significant increase in credit risk

Probability of default (PD) is an experience-based probability that a commitment is in breach for more than 90 days in the next twelve months. The tables

below show the different trigger levels that need to be in place for a commitment to be classified in Stage 2 due to a significant increase in credit risk. A

significant increase in credit risk is assessed on the basis of several criteria, including late payment beyond 30 days after maturity. The most important

factor for the assessment is a comparison between the original probability of default and the probability of default at the reporting date. Each product has

its own threshold values when one considers an increase to be significant. Products with absolute low application PDs therefore lead to high trigger

requirements, as they are relative and come from a low level.

Original

PD

Instalment

loans

Original

PD

Instalment

loans

Original

PD

Credit card

loans

Original

PD

Credit card

loans

Original

PD

Instalment

loans

Original

PD

Credit card

loans

Original

PD

Instalment

loans

Original

PD

Credit card

loans

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

12

Amounts in NOK 1000 Gross loans Stage 1 Stage 2 Stage 3 Other changes Total

Instalment loans Norway 12,191,971 44,208 33,180 275,253 - 11,839,330

Credit card loans Norway 6,100,898 7,002 6,441 72,265 - 6,015,189

Instalment loans Sweden 3,933,187 45,377 61,695 109,289 - 3,716,825

Credit card loans Sweden 2,054,545 9,134 21,131 35,763 - 1,988,518

Instalment loans Denmark 3,204,290 57,345 24,846 182,255 - 2,939,843

Credit card loans Denmark 667,682 13,067 11,179 58,751 - 584,686

Instalment loans Finland 7,147,493 35,155 64,284 181,010 - 6,867,043

Credit card loans Finland 1,586,060 8,272 24,342 13,064 - 1,540,382

Additional provision Finland* - - - - 57,069 -57,069

Total 36,886,125 219,560 247,097 927,650 57,069 35,434,748

Instalment loans Norway

Loan loss allowance Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 44,135 33,445 235,717 313,297

Transfers :

Transfers between Stage 1 and Stage 2 -3,060 14,019 - 10,959

Transfers between Stage 1 and Stage 3 -128 - 120 -8

Transfers between Stage 2 and Stage 1 1,957 -5,820 - -3,863

Transfers between Stage 2 and Stage 3 - -10,991 29,909 18,918

Transfers between Stage 3 and Stage 2 - 935 -7,994 -7,060

Transfers between Stage 3 and Stage 1 10 - -650 -640

New financial assets issued or purchased 3,853 1,553 - 5,406

Financial assets derecognized in the period, including down payments -2,559 38 18,151 15,631

Loan loss allowance as at 30.6.18 44,208 33,180 275,253 352,641

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 9,511,647 1,325,287 1,113,643 11,950,577

Transfers :

Transfers between Stage 1 and Stage 2 -581,878 583,685 - 1,807

Transfers between Stage 1 and Stage 3 -21,469 - 21,790 321

Transfers between Stage 2 and Stage 1 366,112 -380,643 - -14,532

Transfers between Stage 2 and Stage 3 - -216,781 217,109 327

Transfers between Stage 3 and Stage 2 - 37,056 -46,784 -9,728

Transfers between Stage 3 and Stage 1 1,937 - -2,938 -1,001

New financial assets issued or purchased 770,428 42,443 - 812,871

Financial assets derecognized in the period, including down payments -435,108 -78,743 -34,822 -548,672

Gross loans to customers as at 30.6.18 9,611,669 1,312,304 1,267,997 12,191,971

12 months

expected

credit loss

Note 4. Loans to customers by customer groups

Loan loss allowance

*The NFH Group is working with implementation of an internal model as Finland, as a temporary solution, is using a standardized model. Working with the

new model in Q2 has created an expectation that the standardized model is believed to underestimate expected credit losses. The additional provision is

not attributed to any product or step. Therefore, provisions for credit losses in Finland includes a management override of MNOK 57 in the second

quarter.

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

Note 5. Change in loan loss allowance

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

13

Credit card loans Norway

Loan loss allowance

Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 6,560 6,479 58,767 71,806

Transfers :

Transfers between Stage 1 and Stage 2 -303 3,280 - 2,976

Transfers between Stage 1 and Stage 3 -18 - 124 106

Transfers between Stage 2 and Stage 1 300 -2,452 - -2,152

Transfers between Stage 2 and Stage 3 - -943 6,696 5,753

Transfers between Stage 3 and Stage 2 - 101 -2,358 -2,257

Transfers between Stage 3 and Stage 1 4 - -594 -589

New financial assets issued or purchased 458 279 - 737

Financial assets derecognized in the period, including down payments 0 -301 9,630 9,329

Loan loss allowance as at 30.6.18 7,002 6,441 72,265 85,709

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 4,758,826 531,865 322,610 5,613,301

Transfers :

Transfers between Stage 1 and Stage 2 -238,599 276,697 - 38,098

Transfers between Stage 1 and Stage 3 -11,416 - 11,649 233

Transfers between Stage 2 and Stage 1 193,021 -219,353 - -26,332

Transfers between Stage 2 and Stage 3 - -78,044 78,128 83

Transfers between Stage 3 and Stage 2 - 8,944 -19,895 -10,951

Transfers between Stage 3 and Stage 1 1,137 - -5,990 -4,853

New financial assets issued or purchased 179,824 16,891 - 196,716

Financial assets derecognized in the period, including down payments 310,547 -13,909 -2,035 294,603

Gross loans to customers as at 30.6.18 5,193,340 523,091 384,467 6,100,898

12 months

expected

credit loss

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

14

Instalment loans Sweden

Loan loss allowance Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 37,500 90,069 91,554 219,123

Transfers :

Transfers between Stage 1 and Stage 2 -5,813 11,030 - 5,217

Transfers between Stage 1 and Stage 3 -270 - - -270

Transfers between Stage 2 and Stage 1 6,002 -12,148 - -6,145

Transfers between Stage 2 and Stage 3 - -8,890 18,498 9,608

Transfers between Stage 3 and Stage 2 - 2,106 -8,027 -5,921

Transfers between Stage 3 and Stage 1 63 - -415 -353

New financial assets issued or purchased 6,735 972 - 7,707

Financial assets derecognized in the period, including down payments -3,992 -6,199 7,680 -2,511

Other adjustments 5,152 -15,245 0 -10,093

Loan loss allowance as at 30.6.18 45,377 61,695 109,289 216,361

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 1,658,112 1,809,166 423,303 3,890,581

Transfers :

Transfers between Stage 1 and Stage 2 -233,219 222,918 - -10,300

Transfers between Stage 1 and Stage 3 -9,477 - 9,687 211

Transfers between Stage 2 and Stage 1 263,960 -269,865 - -5,904

Transfers between Stage 2 and Stage 3 - -117,778 117,097 -681

Transfers between Stage 3 and Stage 2 - 38,990 -44,761 -5,771

Transfers between Stage 3 and Stage 1 2,749 - -3,414 -665

New financial assets issued or purchased 316,463 18,992 - 335,455

Financial assets derecognized in the period, including down payments -142,719 -118,148 -16,528 -277,395

Other adjustments 264,437 -257,369 587 7,655

Gross loans to customers as at 30.6.18 2,120,307 1,326,908 485,972 3,933,187

Other adjustments include the effects of a correction to the macro model unique to instalment loans in Sweden

12 months

expected

credit loss

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

15

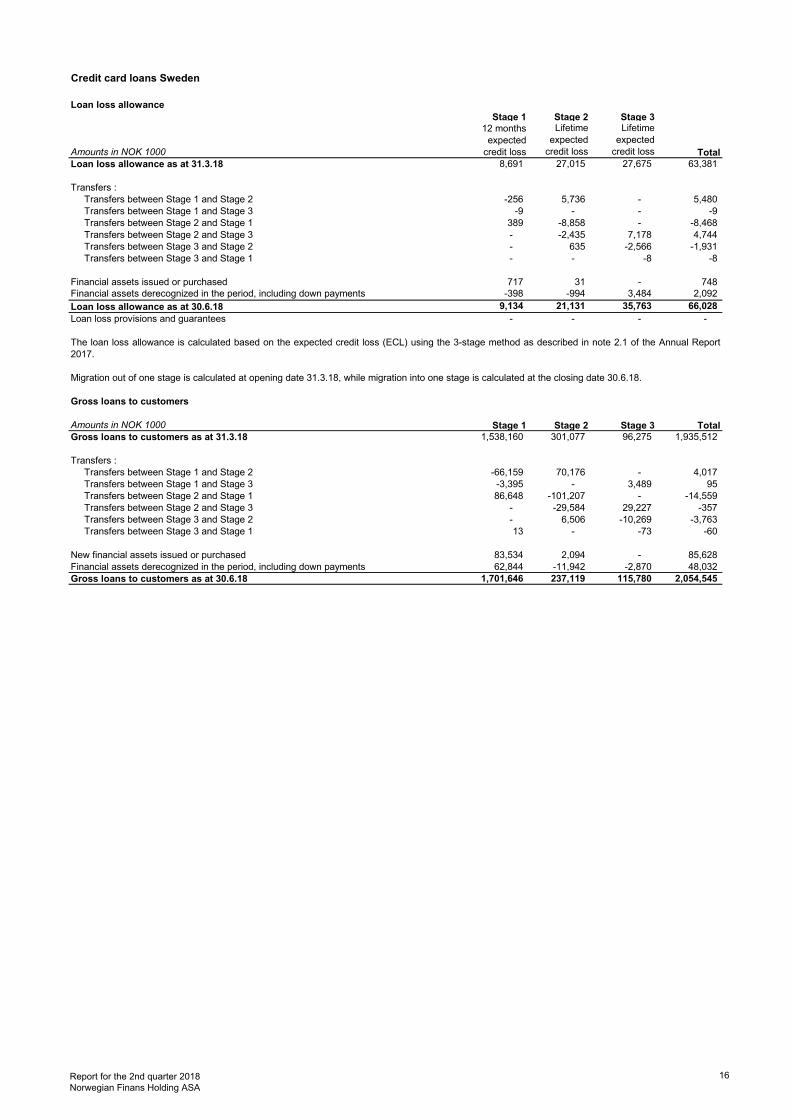

Credit card loans Sweden

Loan loss allowance

Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 8,691 27,015 27,675 63,381

Transfers :

Transfers between Stage 1 and Stage 2 -256 5,736 - 5,480

Transfers between Stage 1 and Stage 3 -9 - - -9

Transfers between Stage 2 and Stage 1 389 -8,858 - -8,468

Transfers between Stage 2 and Stage 3 - -2,435 7,178 4,744

Transfers between Stage 3 and Stage 2 - 635 -2,566 -1,931

Transfers between Stage 3 and Stage 1 - - -8 -8

Financial assets issued or purchased 717 31 - 748

Financial assets derecognized in the period, including down payments -398 -994 3,484 2,092

Loan loss allowance as at 30.6.18 9,134 21,131 35,763 66,028

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 1,538,160 301,077 96,275 1,935,512

Transfers :

Transfers between Stage 1 and Stage 2 -66,159 70,176 - 4,017

Transfers between Stage 1 and Stage 3 -3,395 - 3,489 95

Transfers between Stage 2 and Stage 1 86,648 -101,207 - -14,559

Transfers between Stage 2 and Stage 3 - -29,584 29,227 -357

Transfers between Stage 3 and Stage 2 - 6,506 -10,269 -3,763

Transfers between Stage 3 and Stage 1 13 - -73 -60

New financial assets issued or purchased 83,534 2,094 - 85,628

Financial assets derecognized in the period, including down payments 62,844 -11,942 -2,870 48,032

Gross loans to customers as at 30.6.18 1,701,646 237,119 115,780 2,054,545

Lifetime

expected

credit loss

12 months

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

Lifetime

expected

credit loss

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

16

Instalment loans Denmark

Loan loss allowance Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 54,306 34,388 136,947 225,640

Transfers :

Transfers between Stage 1 and Stage 2 -3,082 14,860 - 11,778

Transfers between Stage 1 and Stage 3 -689 - 9,874 9,185

Transfers between Stage 2 and Stage 1 1,435 -5,671 - -4,237

Transfers between Stage 2 and Stage 3 - -19,054 43,269 24,214

Transfers between Stage 3 and Stage 2 - 443 -2,778 -2,335

Transfers between Stage 3 and Stage 1 30 - -302 -272

New financial assets issued or purchased 5,101 967 - 6,068

Financial assets derecognized in the period, including down payments 245 -1,087 -4,754 -5,596

Loan loss allowance as at 30.6.18 57,345 24,846 182,255 264,446

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 2,520,494 188,305 256,786 2,965,585

Transfers :

Transfers between Stage 1 and Stage 2 -86,578 89,055 - 2,477

Transfers between Stage 1 and Stage 3 -17,620 - 18,255 635

Transfers between Stage 2 and Stage 1 41,803 -42,884 - -1,081

Transfers between Stage 2 and Stage 3 - -80,382 79,709 -673

Transfers between Stage 3 and Stage 2 - 3,653 -5,413 -1,759

Transfers between Stage 3 and Stage 1 314 - -597 -283

New financial assets issued or purchased 212,511 5,456 - 217,967

Financial assets derecognized in the period, including down payments 38,482 -8,496 -8,564 21,423

Gross loans to customers as at 30.6.18 2,709,406 154,707 340,177 3,204,290

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

12 months

expected

credit loss

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

17

Credit card loans Denmark

Loan loss allowance

Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 14,197 11,427 53,777 79,401

Transfers :

Transfers between Stage 1 and Stage 2 -222 2,653 - 2,431

Transfers between Stage 1 and Stage 3 -43 - 1,607 1,564

Transfers between Stage 2 and Stage 1 98 -1,333 - -1,235

Transfers between Stage 2 and Stage 3 - -2,812 6,473 3,661

Transfers between Stage 3 and Stage 2 - 980 -1,797 -817

Transfers between Stage 3 and Stage 1 - - - -

New financial assets issued or purchased 6,134 214 - 6,349

Financial assets derecognized in the period, including down payments -7,097 50 -1,309 -8,357

Loan loss allowance as at 30.6.18 13,067 11,179 58,751 82,996

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 463,465 55,098 132,317 650,880

Transfers :

Transfers between Stage 1 and Stage 2 -22,532 24,519 - 1,987

Transfers between Stage 1 and Stage 3 -3,640 - 3,816 176

Transfers between Stage 2 and Stage 1 12,918 -14,253 - -1,334

Transfers between Stage 2 and Stage 3 - -16,218 16,166 -51

Transfers between Stage 3 and Stage 2 - 1,864 -4,416 -2,552

Transfers between Stage 3 and Stage 1 - - - -

-

New financial assets issued or purchased 12,806 485 - 13,291

Financial assets derecognized in the period, including down payments 12,333 -4,326 -2,723 5,285

Gross loans to customers as at 30.6.18 475,350 47,171 145,161 667,682

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

12 months

expected

credit loss

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

18

Instalment loans Finland

Loan loss allowance Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 34,427 56,757 138,972 230,155

Transfers :

Transfers between Stage 1 and Stage 2 -4,580 31,676 - 27,096

Transfers between Stage 1 and Stage 3 -85 - 372 287

Transfers between Stage 2 and Stage 1 1,536 -8,768 - -7,232

Transfers between Stage 2 and Stage 3 - -18,838 49,432 30,594

Transfers between Stage 3 and Stage 2 - 1,843 -4,085 -2,243

Transfers between Stage 3 and Stage 1 3 - -141 -138

New financial assets issued or purchased 3,949 1,286 - 5,236

Financial assets derecognized in the period, including down payments -95 328 -3,539 -3,306

Loan loss allowance as at 30.6.18 35,155 64,284 181,010 280,449

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 4,990,345 957,628 690,933 6,638,906

Transfers :

Transfers between Stage 1 and Stage 2 -531,095 539,514 - 8,419

Transfers between Stage 1 and Stage 3 -1,698 - 1,739 41

Transfers between Stage 2 and Stage 1 184,037 -192,166 - -8,129

Transfers between Stage 2 and Stage 3 - -233,657 234,422 764

Transfers between Stage 3 and Stage 2 - 18,155 -21,912 -3,757

Transfers between Stage 3 and Stage 1 472 - -543 -71

New financial assets issued or purchased 593,514 27,683 - 621,197

Financial assets derecognized in the period, including down payments -60,676 -33,622 -15,579 -109,877

Gross loans to customers as at 30.6.18 5,174,900 1,083,534 889,059 7,147,493

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

12 months

expected

credit loss

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

19

Credit card loans Finland

Loan loss allowance

Stage 1 Stage 2 Stage 3

Amounts in NOK 1000 Total

Loan loss allowance as at 31.3.18 7,571 22,879 10,212 40,663

Transfers :

Transfers between Stage 1 and Stage 2 -1,268 6,851 - 5,582

Transfers between Stage 1 and Stage 3 -4 - 9 6

Transfers between Stage 2 and Stage 1 440 -3,297 - -2,857

Transfers between Stage 2 and Stage 3 - -1,758 3,762 2,004

Transfers between Stage 3 and Stage 2 - 49 -405 -356

Transfers between Stage 3 and Stage 1 2 - -29 -27

New financial assets issued or purchased 1,581 527 - 2,109

Financial assets derecognized in the period, including down payments -51 -909 -486 -1,446

Loan loss allowance as at 30.6.18 8,272 24,342 13,064 45,678

Loan loss provisions and guarantees - - - -

Migration out of one stage is calculated at opening date 31.3.18, while migration into one stage is calculated at the closing date 30.6.18.

Gross loans to customers

Amounts in NOK 1000 Stage 1 Stage 2 Stage 3 Total

Gross loans to customers as at 31.3.18 744,485 516,481 123,796 1,384,763

Transfers :

Transfers between Stage 1 and Stage 2 -135,874 163,195 - 27,321

Transfers between Stage 1 and Stage 3 -184 - 185 1

Transfers between Stage 2 and Stage 1 52,662 -53,622 - -960

Transfers between Stage 2 and Stage 3 - -40,323 40,004 -319

Transfers between Stage 3 and Stage 2 - 3,351 -5,015 -1,664

Transfers between Stage 3 and Stage 1 117 - -444 -327

New financial assets issued or purchased 68,757 9,116 - 77,873

Financial assets derecognized in the period 116,312 -14,420 -2,520 99,373

Gross loans to customers as at 30.6.18 846,275 583,779 156,006 1,586,060

Lifetime

expected

credit loss

Lifetime

expected

credit loss

The loan loss allowance is calculated based on the expected credit loss (ECL) using the 3-stage method as described in note 2.1 of the Annual Report

2017.

12 months

expected

credit loss

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

20

Note 6. Loan loss provisions and guarantees

The NFH Group has no guarantees as of 30.6.18.

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Realized losses in the period 16,404 5,873 16,325

Individual write-downs on loans including gains/losses from sale of NPL portfolios - 81,229 172,838

Write-downs - lifetime expected credit loss (stage 3) 334,150 - -

Net individual write-downs on loans 350,554 87,101 189,163

The period's change in write-downs on groups of loans including gains/losses from sale of NPL portfolios - 245,316 483,226

Write-downs - 12 months expected credit loss (stage 1) 20,657 - -

Write-downs - lifetime expected credit loss (stage 2) 15,083 - -

Other changes 57,315

Write-downs on loans 443,609 332,417 672,388

Note 7. Loans to customers by geographical region

Gross loans by geographical regions

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Østlandet 9,577,526 8,510,425 8,905,323

Sørlandet 796,735 708,019 749,306

Vestlandet 4,578,488 4,063,685 4,265,918

Trøndelag 1,332,205 1,177,651 1,237,676

Nord-Norge 1,938,657 1,745,978 1,820,883

Not classified 69,259 45,729 59,785

Total Norway 18,292,869 16,251,486 17,038,890

Götaland 2,467,565 2,200,335 2,429,467

Svealand 2,893,067 2,575,446 2,863,260

Norrland 562,122 520,669 567,585

Not classified 64,978 17,919 38,614

Total Sweden 5,987,732 5,314,369 5,898,925

Hovedstaden 1,413,028 948,054 1,227,797

Midtjylland 635,177 420,600 546,088

Nordjylland 285,402 185,754 243,884

Sjælland 805,260 543,299 699,903

Syddanmark 729,888 482,504 625,437

Not classified 3,217 1,445 2,428

Total Denmark 3,871,972 2,581,657 3,345,537

Södra Finland 5,991,834 3,906,503 5,011,778

Västra Finland 959,343 609,600 788,531

Östra Finland 685,635 439,607 566,822

Mellersta Finland 662,740 444,899 561,740

Norra Finland 376,012 249,325 320,244

Not classified 57,989 19,399 59,237

Total Finland 8,733,553 5,669,334 7,308,352

Gross loans to customers 36,886,125 29,816,846 33,591,704

Note 8. Liquidity risk

The Liquidity Coverage Ratio (LCR) is defined as the NHF Group's liquid assets relative to net liquidity output 30 days forward in time in any given stress

situation. At 30.6.18 the liquidity reserve (LCR) on total level for the NHF Group was 225% (compared to 169% per 30.6.17). The NHF Group has

significant positions in Norwegian, Swedish and Danish kroner in addition to Euro. At 30.6.18 the LCR was 345% in Norwegian kroner (compared to 235%

per 30.6.2017), 128% in Swedish kroner (compared to 51% per 30.6.2017), 189% Danish kroner (compared to 114% per 30.6.2017) and 151% in Euro

(compared to 0% per 30.6.2017). The legal requirement for liquidity reserve at total level and for significant currencies is 100% at 30.6.18, except for

Norwegian kroner where the legal requirement is 50%.

The liquidity risk is the risk that the NHF Group is not capable of covering all its financial obligations as they fall due. The liquidity risk is evaluated as low

at the time of this report, since a large portion of the NHF Group's assets consists of easily transferable securities. The asset side is financed by core

deposits from the retail market, debt securities and subordinated capital. The NHF Group manages its liquidity position by short-term cash flow forecasts

and liquidity due date summaries.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

21

Note 9. Loans and deposits with credit institutions and central banks

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Loans and deposits with credit institutions and central banks without agreed maturity or notice period 2,389,320 1,456,833 1,326,922

Loans and deposits with credit institutions and central banks 2,389,320 1,456,833 1,326,922

Specification of currencies

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

NOK 1,160,027 612,004 542,600

SEK 600,409 389,994 444,840

DKK 276,786 261,536 197,700

EUR 352,097 193,298 141,782

Loans and deposits with credit institutions and central banks 2,389,320 1,456,833 1,326,922

Average interest rate 0.20 % 0.44 % 0.22 %

Note 10. Net interest income

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Interest income from cash and deposits with the central bank 169 149 304

Interest income from loans to and deposits with credit institutions 1,503 1,302 2,705

Interest income from instalment loans 1,761,130 1,460,959 3,102,438

Interest income from overdraft accounts - 79 79

Interest income from credit card loans 605,407 439,855 967,465

Interest income from sales financing 1,338 2,647 4,571

Interest income, amortised cost 2,369,547 1,904,990 4,077,561

Interest and other income from certificates and bonds 46,248 43,672 91,939

Other interest and other interest related income 1,821 1,846 3,183

Other interest income 48,069 45,518 95,122

Interest expense from deposits from credit institutions 479 30 135

Interest expense from deposits from customers 259,023 200,227 433,959

Interest expense on debt securities issued 15,318 17,619 34,346

Interest expense on subordinated loan 9,903 5,889 15,530

Other interest and other interest related expenses 12,545 8,796 18,241

Interest expenses 297,268 232,561 502,211

Net interest income 2,120,348 1,717,947 3,670,472

Note 11. Net other operating income

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Payment services 169,048 109,857 264,887

Insurance services 67,889 42,304 87,522

Other fees and commission and bank services income 26,262 22,459 47,589

Total commission and bank services income 263,198 174,620 399,998

Payment services 68,727 47,586 110,223

Insurance services 54,200 34,365 78,620

Other fees and commission and bank services expense 13,452 10,316 22,249

Total commission and bank services expenses 136,379 92,267 211,092

Note 12. Net gains on financial instruments

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Net gains on certificates and bonds -17,794 -946 -17,251

Net gains on FX-forwards 212,515 62,961 -140,821

Net currency effects -191,220 -51,888 165,530

Net gains on shares and other securities 4,112 - -

Total 7,613 10,127 7,458

Note 13. General administrative expenses

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Sales and marketing 430,824 341,548 730,783

IT operations 37,418 48,286 81,940

External services fees 43,328 22,437 51,995

Other administrative expenses 20,094 19,127 41,568

Total 531,664 431,398 906,286

Average interest rate is calculated as interest amount in percentage of average volume for the current period.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

22

Note 14. Other operating expenses

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Credit information 16,879 14,096 28,190

Auditor 982 1,070 2,364

Rental of premises 1,161 1,110 2,309

Insurance 267 262 517

Machinery, fixtures and transport vehicles 364 193 528

Other operating expenses 5,697 5,693 11,576

Total 25,350 22,423 45,484

Note 15. Financial instruments at fair value

Level 2 Valuation based on observable market data

Level 3 Valuation based on observable market data

Financial instruments at fair value

Amounts in NOK 1000 Level 1 Level 2 Level 3 Total

Certificates and bonds - 9,389,792 - 9,389,792

Financial derivatives - 43,768 - 43,768

Shares and other securities - - 37,476 37,476

Total financial assets at fair value - 9,433,560 37,476 9,471,037

Financial derivatives - 2,494 - 2,494

Total financial liabilities at fair value - 2,494 - 2,494

Amounts in NOK 1000 Level 1 Level 2 Level 3 Total

Certificates and bonds - 8,185,779 - 8,185,779

Financial derivatives - 946 - 946

Shares and other securities - - 443 443

Financial assets available for sale - - 28,374 28,374

Total financial assets at fair value - 8,186,726 28,817 8,215,543

Financial derivatives - 3,999 - 3,999

Total financial liabilities at fair value - 3,999 - 3,999

Amounts in NOK 1000 Level 1 Level 2 Level 3 Total

Certificates and bonds - 8,859,834 - 8,859,834

Financial derivatives - 1,935 - 1,935

Shares and other securities - - 443 443

Financial assets available for sale - - 32,922 32,922

Total financial assets at fair value - 8,861,770 33,365 8,895,135

Financial derivatives - 52,246 - 52,246

Total financial liabilities at fair value - 52,246 - 52,246

Change in instruments classified at level 3

Amounts in NOK 1000 Total

Value 31.12.17 443 32,922 33,365

Additions - - -

Disposals - - -

Settlement - - -

Reclassification IFRS 9 32,922 -32,922 -

Net gain / loss on financial instruments 4,112 - 4,112

Value 30.6.18 37,476 - 37,476

Q2 2018

Financial

assets

available

for sale

Shares

and other

securities

Financial instruments in level 1 are determined based on quoted prices in active markets for identical financial instruments available on the balance sheet

date.

Q2 2018

Q2 2017

2017

Financial instruments in level 2 are determined based on inputs other than quoted prices, but where prices are observable either directly or indirectly.

These include quoted prices in markets that are not active.

Level 1 Valuation based on quoted prices in an active market

Financial instruments at fair value is measured at different levels.

When valuation can not be determined in level 1 or 2, valuation methods based on non-observable market data are used.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

23

Amounts in NOK 1000 Total

Value 31.12.17 443 24,745 25,188

Additions - - -

Disposals - - -

Settlement - - -

Reclassification IFRS 9 - - -

Net gain / loss on financial instruments - 3,629 3,629

Value 30.6.18 443 28,374 28,817

Ownership in Visa Norge FLI

Note 16. Fair value of financial instruments at amortized cost

Loans and deposits with central banks and credit institutions and deposits from customers

Loans to customers

Debt securities issued and subordinated loan

Fair value of financial instruments at amortized cost

Amounts in NOK 1000 Book value Fair value Book value Fair value Book value Fair value

Cash and deposits with the central bank 65,975 65,975 61,981 61,981 65,976 65,976

Loans and deposits with credit institutions 2,323,345 2,323,345 1,394,852 1,394,852 1,260,947 1,260,947

Loans to customers 35,434,748 35,434,748 28,868,053 28,868,053 32,451,553 32,451,553

Total financial assets 37,824,067 37,824,067 30,324,885 30,324,885 33,778,475 33,778,475

Deposits from customers 37,705,983 37,705,983 30,922,923 30,922,923 33,682,275 33,682,275

Debt securities issued 1,808,003 1,916,771 2,040,622 2,042,374 2,242,423 2,301,855

Subordinated loan 474,622 477,888 474,721 474,721 474,614 478,360

Total financial liabilities 39,988,608 40,100,642 33,438,266 33,440,018 36,399,313 36,462,490

Financial instruments at amortized cost are valued at originally determined cash flows, adjusted for any impairment losses. Amortized cost will not always

give values that match the market's assessment of the same instruments. This may be due to different perceptions of market conditions, risk and return

requirements.

Fair value is estimated to conform with amortized cost.

Loans to customers are exposed to market competition. This means that the potential added value of the loan portfolio will not be maintained over time.

Further, provisions for loan losses are provided for on an ongoing basis. The fair value of loans to customers is therefore considered to conform to the

amortized cost.

The fair value of debt securities issued and subordinated loan are based on observable market data where available.

Shares in BankID Norge AS

Ownership in Visa Norge FLI is considered to be a financial asset and is classified as Share and other securities . The fair value of the asset is estimated

at NOK 37,0 million as of 30.6.18. The calculation is based on input from Visa Norge.

Q2 2017

Financial

assets

available

for sale

Shares

and other

securities

Q2 2018 Q2 2017 2017

Bank Norwegian AS was at 12.8.14 issued 280 shares in BankID Norge AS based on the bank's share of participation in the BankID association. Value of

shares are estimated at the going rate at the time granted.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

24

Note 17. Debt securities issued and subordinated loan

Debt securities issued

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Bonds, nominal value 1,804,950 2,036,000 2,239,800

Value adjustments and currency effects -933 -93 -1,580

Accrued interest 3,986 4,715 4,203

Total debt securities issued 1,808,003 2,040,622 2,242,423

Change in debt securities issued

Amounts in NOK 1000 Issued

Bonds, nominal value 1,804,950 - -390,000 -44,850 2,239,800

Value adjustments and currency effects -933 - - -647 -1,580

Accrued interest 3,986 - - 217 4,203

Total debt securities issued 1,808,003 - -390,000 -45,280 2,242,423

Amounts in NOK 1000 Issued

Bonds, nominal value 2,036,000 500,000 -284,000 - 1,820,000

Value adjustments and currency effects -93 - - -352 259

Accrued interest 4,715 - - 1,001 3,714

Total debt securities issued 2,040,622 500,000 -284,000 649 1,823,973

Change in subordinated loan

Amounts in NOK 1000 Issued

Subordinated loan, nominal value 475,000 - - - 475,000

Value adjustments -1,237 - - -25 -1,212

Accrued interest 859 - - 33 826

Total subordinated loan 474,622 - - 8 474,614

Amounts in NOK 1000 Issued

Subordinated loan, nominal value 475,000 200,000 - - 275,000

Value adjustments -1,287 - - -706 -581

Accrued interest 1,008 - - 512 496

Total subordinated loan 474,721 200,000 - -194 274,915

Note 18. Financial Assets available for sale

Note 19. Receivables

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Distribution commissions 92,787 91,660 92,866

Prepaid expenses 21,437 16,575 4,800

Net collateral issued* - - 84,700

Other receivables 14,406 22,889 12,434

Total 128,630 131,124 194,800

Note 20. Other liabilities

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Payables to suppliers 6,327 39,454 6,545

Value added tax 7,778 8,909 8,412

Social security tax 6,270 3,981 2,467

Tax withholdings 4,253 5,996 2,335

Unsettled items related to certificates and bonds 52,943 103,108 138,135

Other liabilities 13,784 2,247 816

Total 91,355 163,695 158,711

Other

changes and

currency

effects

Overdue /

redeemed

The NFH Group is a member of Visa Norge FLI ("Visa Norge"), being a shareholder of Visa Europe Ltd. On 2 November 2015, an agreement between

Visa Europe Ltd. and Visa Inc. was announced where Visa Inc. acquires all shares in Visa Europe Ltd. This transaction consists of a cash consideration,

convertible preference shares and a deferred cash consideration paid three years after completion of the transaction. The process was finalized in June

2016 and the NFH Group has in this connection received its share of the cash consideration based on the NFH Group's stake in Visa Norge. In 2018, the

NFH Group has reclassified Assets available for sale in accordance with IFRS 9 and changes in fair value are recognized through profit or loss.

Balance

31.12.17

Balance

31.12.17

Balance

31.12.16

Other

changes and

currency

effects

Other

changes and

currency

effects

Balance

30.6.17

Overdue /

redeemed

Balance

30.6.18

Other

changes and

currency

effects

* The NFH Group has not issued any collateral as at 30.6.18. The NHF Group has received NOK 85.45 million in collateral from DNB which is classified

as Loans from credit institutions.

Balance

30.6.18

Overdue /

redeemed

Balance

30.6.17

Overdue /

redeemed

Balance

31.12.16

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

25

Note 21. Accrued expenses

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Accrued not due expenses 173,661 91,996 132,331

Bonus 7,700 7,250 12,131

Holiday pay 2,400 2,142 4,566

Board remuneration 128 558 1,146

Accrued fees 431 41 41

Total 184,321 101,988 150,216

Note 22. Capital adequacy

Total capital

Amounts in NOK 1000 Q2 2018 Q2 2017 2017

Share capital 186,752 191,301 186,689

+ Share premium 976,938 966,570 971,182

+ Other reserves 4,856,628 3,058,288 3,920,750

- Deferred tax assets, intangible assets and additional valuation adjustment 135,553 126,283 139,529

Common equity Tier 1 5,884,765 4,089,876 4,939,091

+ Additional Tier 1 capital 635,000 635,000 635,000

Tier 1 capital 6,519,765 4,724,876 5,574,091

+ Tier 2 capital 474,622 474,721 474,614

Total capital 6,994,387 5,199,597 6,048,706

Calculation basis

Credit risk

Covered bonds 204,209 164,988 232,981

+ Institutions 1,266,638 1,048,001 907,574

+ Loans to customers 23,737,598 20,431,418 22,472,413

+ Defaulted loans and other commitments 3,995,221 1,788,143 2,719,400

Operational risk 4,022,891 2,608,276 2,608,276

Total calculation basis 33,226,556 26,040,827 28,940,644

Common equity Tier 1 % 17.71 % 15.71 % 17.07 %

Tier 1 capital % 19.62 % 18.14 % 19.26 %

Total capital % 21.05 % 19.97 % 20.90 %

Note 24. Related parties

Note 25. Subsequent events

Norwegian Finans Holding ASA (org. number 991 281 924) owns 100% of Bank Norwegian AS (org. number 991 455 671).

There is no awareness of other events after the date of the balance sheet that may be of material significance to the accounts.

The NFH Group is sharing premises with Norwegian Air Shuttle ASA. A temporary lease agreement has been signed for Snarøyveien 36, Fornebu. The

temporary lease agreement expires 28 October 2019. A lease agreement for the same address has been established with Akastor and Norwegian

Property respectively, which expires in October 2021 with an option to extend the lease agreement for two additional years. The annual rent totals NOK

2.5 million.

Note 23. Lease agreements

Bank Norwegian AS and Norwegian Air Shuttle ASA have since October 2007 had an agreement regarding the bank's use of the brand name Norwegian,

IP-rights, and co-operation regarding the loyalty program and credit cards. Based on the bank's expansion into Sweden, Denmark and Finland, new

agreements has been renegotiated. All accrued rights remain. The agreements was renegotiated in the second quarter 2018.

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

26

Quarterly figures

Profit and loss account

Norwegian Finans Holding Group

Amounts in NOK 1000 Q2 2018 Q1 2018 Q4 2017 Q3 2017 Q2 2017

Interest income, amortised cost 1,222,548 1,147,000 1,128,109 1,044,461 992,283

Other interest income 23,863 24,206 24,272 25,331 24,177

Interest expenses 154,602 142,666 137,510 132,140 124,215

Net interest income 1,091,808 1,028,540 1,014,872 937,653 892,245

Commission and bank services income 143,359 119,839 120,963 104,415 93,728

Commission and bank services expenses 70,387 65,992 63,574 55,250 50,118

Net change in value on securities and currency 21,089 -13,476 -3,355 685 4,612

Net other operating income 94,061 40,371 54,034 49,850 48,222

Total income 1,185,869 1,068,911 1,068,906 987,503 940,467

Personnel expenses 17,373 21,485 20,501 18,711 16,351

General administrative expenses 264,770 266,894 245,239 229,649 215,419

Ordinary depreciation 12,150 11,922 11,837 10,403 10,861

Other operating expenses 13,082 12,268 12,053 11,008 10,835

Total operating expenses before losses 307,374 312,570 289,630 269,771 253,466

Provision for loan losses 234,707 208,903 199,109 140,862 155,193

Profit before tax 643,788 547,439 580,168 576,870 531,808

Tax charge 160,967 136,827 140,383 144,424 132,779

Profit after tax 482,822 410,611 439,785 432,446 399,029

Comprehensive incomeNorwegian Finans Holding Group

Amounts in NOK 1000 Q2 2018 Q1 2018 Q4 2017 Q3 2017 Q2 2017

Profit on ordinary activities after tax 482,822 410,611 439,785 432,446 399,029

Change in fair value for assets available for sale - - 3,081 1,466 937

Tax - - -23 -11 -7

Other comprehensive income - - 3,058 1,455 930

Comprehensive income for the period 482,822 410,611 442,843 433,901 399,959

Balance sheetNorwegian Finans Holding Group

Amounts in NOK 1000 30.6.18 31.3.18 31.12.17 30.9.17 30.6.17

Assets

Cash and deposits with the central bank 65,975 65,982 65,976 61,979 61,981

Loans and deposits with credit institutions 2,323,345 1,838,548 1,260,947 1,769,465 1,394,852

Loans to customers 35,434,748 33,813,701 32,451,553 30,135,429 28,868,053

Certificates and bonds 9,389,792 9,292,364 8,859,834 8,365,022 8,185,779

Financial derivatives 43,768 49,364 1,935 3,304 946

Shares and other securities 37,476 33,104 443 443 443

Assets available for sale - - 32,922 29,841 28,374

Intangible assets 114,923 115,836 114,678 115,579 117,965

Deferred tax asset 11,157 18,333 15,904 8,425 8,318

Fixed assets 810 904 1,000 1,071 1,094

Receivables 128,630 143,533 194,800 123,584 131,124

Total assets 47,550,624 45,371,669 42,999,992 40,614,141 38,798,929

Liabilities and equity

Loans from credit institutions 85,450 99,200 - - -

Deposits from customers 37,705,983 35,789,003 33,682,275 31,988,426 30,922,923

Debt securities issued 1,808,003 1,934,592 2,242,423 2,040,270 2,040,622

Financial derivatives 2,494 11,264 52,246 11,265 3,999

Tax payable 543,078 391,742 525,886 382,070 239,822

Other liabilities 91,355 342,312 158,711 285,142 163,695

Accrued expenses 184,321 154,835 150,216 154,636 101,988

Subordinated loan 474,622 474,677 474,614 474,536 474,721

Total liabilities 40,895,306 39,197,625 37,286,371 35,336,346 33,947,770

Share capital 186,689 186,689 186,689 186,689 186,619

Share premium 971,182 971,182 971,182 971,182 966,570

Paid, not registered capital 5,819 - - - -

Tier 1 capital 635,000 635,000 635,000 635,000 639,683

Retained earnings and other reserves 4,856,628 4,381,173 3,920,750 3,484,925 3,058,288

Total equity 6,655,318 6,174,044 5,713,621 5,277,796 4,851,159

Total liabilities and equity 47,550,624 45,371,669 42,999,992 40,614,141 38,798,929

Report for the 2nd quarter 2018 Norwegian Finans Holding ASA

27

Profit and loss accountNorwegian Finans Holding ASA

Amounts in NOK 1000 Q2 2018 Q2 2017 YTD 2018 YTD 2017 2017

Interest income, amortised cost 3 1 4 41 45

Net interest income 3 1 4 41 45

Commission and bank services expenses 214 83 296 188 362

Other income 247,500 - 247,500 - -

Net other operating income 247,286 -83 247,204 -188 -362

Total income 247,289 -83 247,208 -147 -317

Personnel expenses 315 91 559 408 1,004

Other operating expenses 689 705 1,094 1,188 2,012

Total operating expenses before losses 1,004 796 1,653 1,596 3,016

Provision for loan losses - - - -

Profit before tax 246,285 -879 245,555 -1,743 -3,333

Tax charge 59,115 -393 58,933 -601 -833

Profit after tax 187,171 -485 186,622 -1,142 -2,500

Comprehensive incomeNorwegian Finans Holding ASA

Amounts in NOK 1000 Q2 2018 Q2 2017 YTD 2018 YTD 2017 2017

Profit on ordinary activities after tax 187,171 -485 186,622 -1,142 -2,500

Comprehensive income for the period 187,171 -485 186,622 -1,142 -2,500

Balance sheetNorwegian Finans Holding ASA

Amounts in NOK 1000 30.6.18 30.6.17 31.12.17

Assets

Loans and deposits with credit institutions 251,096 2,282 6,794

Ownership interests in group companies 1,150,000 1,150,000 1,150,000

Deferred tax asset - 4,547 7,003

Receivables 6,516 5,485 -

Total assets 1,407,612 1,162,313 1,163,797

Liabilities and equity

Tax payable 51,930 - -

Other liabilities 65 - 22

Accrued expenses 572 575 1,171

Total liabilities 52,567 575 1,193

Share capital 186,689 186,619 186,689

Share premium 971,182 966,570 971,182

Paid, not registered capital 5,819 4,683 -

Retained earnings and other reserves 191,356 3,867 4,734

Total equity 1,355,046 1,161,738 1,162,605

Total liabilities and equity 1,407,613 1,162,313 1,163,797

Gunn Ingemundsen

Board Member Board Member

_________________

Board Member

Tine Wollebekk

CEO

Bærum, 14 August, 2018

John Høsteland