report of the chief financial officer - new cross hospital · report of the chief financial officer...

TRANSCRIPT

Report of the Chief Financial Officer

Summary Finance Report – February 2016

(Month 11)

Contents Page

Summary Tables 3 - 6

Income and Expenditure Account 7

Financial Targets and Rating 8

Risks 9

Pay Analysis 10 - 11

Patient Income Analysis 12 - 15

CIP 16

Statement of Financial Position 17

Cash Flow Statement 18

Summary Overview

Previously the Trust Board agreed an “adjusted” year end deficit of £0.3m. Subsequent to the plan

resubmission the Trust agreed to a TDA request for a £2.5m capital to revenue transfer, resulting in the

Trust having a further adjusted surplus target of £2.2m surplus. Following discussion at Finance &

Performance Committee; Audit Committee and with the agreement of the Trust Board the Trust notified

the NHS Trust Development Agency that it would not be able to meet the “stretch” target and is

predicting to be £2m below the stretch plan with a deficit of £2.4m (before capital to revenue transfer)

At Month 11 the Trust has a net deficit of (£4.37m), after TDA technical adjustments. In Month 11 the

position is (£3.23m) adverse to the stretch forecast. Both the original plan and the stretch forecast are

detailed on page 7.

For consistency with previous months reporting this report will continue to highlight variances to the

“stretch” target.

Contents & Summary Overview

2

Net Surplus

Other Income (excluding CRN income)

In Month 11 the Trust reported an in-month deficit of (£343k), against an in month

surplus plan of £877k, an adverse variance of (£1,219k) against the adjusted

stretch plan in month.

The Trusts Income and Expenditure position as at Month 11 is a deficit of

(£4,369k), after TDA technical adjustments, which is (£3,233k) adverse to the

stretch plan.

The Trust’s operating position (Earnings before interest, taxation, depreciation and

amortisation – EBITDA) is (£3,725k) below plan. The detail can be found on page

7.

At Month 11, patient contract income is showing a year to date deficit of

(£3.01m), with an in-month adverse variance of (£560k). The detailed reasons

for the variance in month are shown on page 12.

The key areas of underperformance in month are: Emergency Services (£259k),

Critical Care (£86k), Obstetrics (£43k) and General Surgery (£33k).

The key areas of underperformance year to date are: Emergency Services

(£1,230k), Clinical Haematology/Oncology (£1,156k), Cardiothoracic (£622k)

and Community (£321k).

Other Income has under-recovered by (£1.79m) year-to-date with an under-

recovery of (£34k) in Month 11 against the TDA plan. The year to date under-

recovery is due to the under-performance of Income on Directorate budgets.

3

Summary Tables

Patient Contract Income

Non Pay

Pay costs are underspent year to date by £2.24m against the stretch plan. In month pay

budgets are £0.2m overspent against the Month 11 stretch plan.

Substantive pay, agency and bank usage have marginally reduced in Month 11

whereas locum expenditure has increased since Month 10 (see page 10 for more

information).

Against the new financial target Division 1 has a favourable pay variance of £1.43m to

date due to continued vacancies.

Division 2 is underspent by £773k to date against the new financial target, due to

continued vacancies across the Division.

Non Pay is overspent year to date by (£787k) against the stretch target.

Division 1 is overspent by (£995k) to date across a number of Directorates. This is due

mainly to increased Maternity Pathway charges from other providers and additional

MRI scanner hire. There are also overspends on consumables relating to increased

activity.

Division 2 is £10k underspent at Month 11, while Estates and Facilities is (£77k)

overspent year to date due to non-recurrent expenditure incurred throughout the year.

Drugs was overspent by (£266k) in month, with a cumulative overspend of (£379k)

against the stretch target.

Division 1 is (£395k) adverse to the revised plan year to date. This relates to activity

related costs in Ophthalmology.

Division 2 is underspent by £105k against the revised plan, this is mainly within

Rheumatology.

4

Summary Expenditure Tables Pay

Drugs

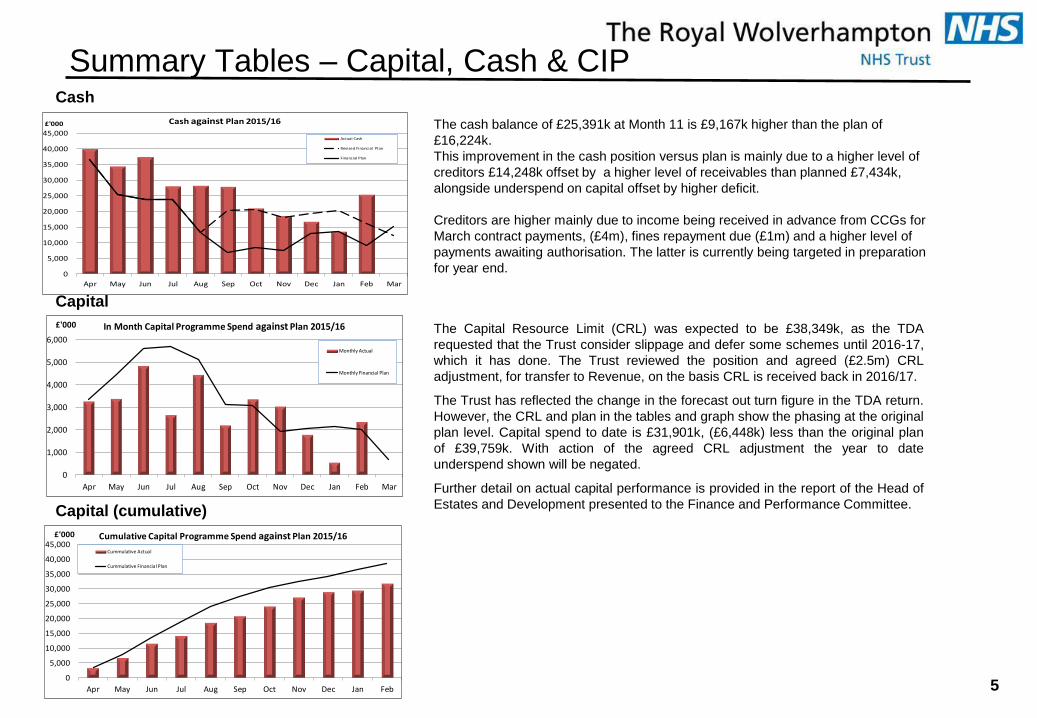

Summary Tables – Capital, Cash & CIP Cash

Capital (cumulative)

5

Capital

The Capital Resource Limit (CRL) was expected to be £38,349k, as the TDA

requested that the Trust consider slippage and defer some schemes until 2016-17,

which it has done. The Trust reviewed the position and agreed (£2.5m) CRL

adjustment, for transfer to Revenue, on the basis CRL is received back in 2016/17.

The Trust has reflected the change in the forecast out turn figure in the TDA return.

However, the CRL and plan in the tables and graph show the phasing at the original

plan level. Capital spend to date is £31,901k, (£6,448k) less than the original plan

of £39,759k. With action of the agreed CRL adjustment the year to date

underspend shown will be negated.

Further detail on actual capital performance is provided in the report of the Head of

Estates and Development presented to the Finance and Performance Committee.

The cash balance of £25,391k at Month 11 is £9,167k higher than the plan of

£16,224k.

This improvement in the cash position versus plan is mainly due to a higher level of

creditors £14,248k offset by a higher level of receivables than planned £7,434k,

alongside underspend on capital offset by higher deficit.

Creditors are higher mainly due to income being received in advance from CCGs for

March contract payments, (£4m), fines repayment due (£1m) and a higher level of

payments awaiting authorisation. The latter is currently being targeted in preparation

for year end.

0

1,000

2,000

3,000

4,000

5,000

6,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

£'000 In Month Capital Programme Spend against Plan 2015/16

Monthly Actual

Monthly Financial Plan

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb

£'000 Cumulative Capital Programme Spend against Plan 2015/16

Cummulative Actual

Cummulative Financial Plan

0

5,000

10,000

15,000

20,000

25,000

30,000

35,000

40,000

45,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

£'000 Cash against Plan 2015/16

Actual Cash

Revised Financial Plan

Financial Plan

Summary Tables – Capital, Cash & CIP

CIP

6

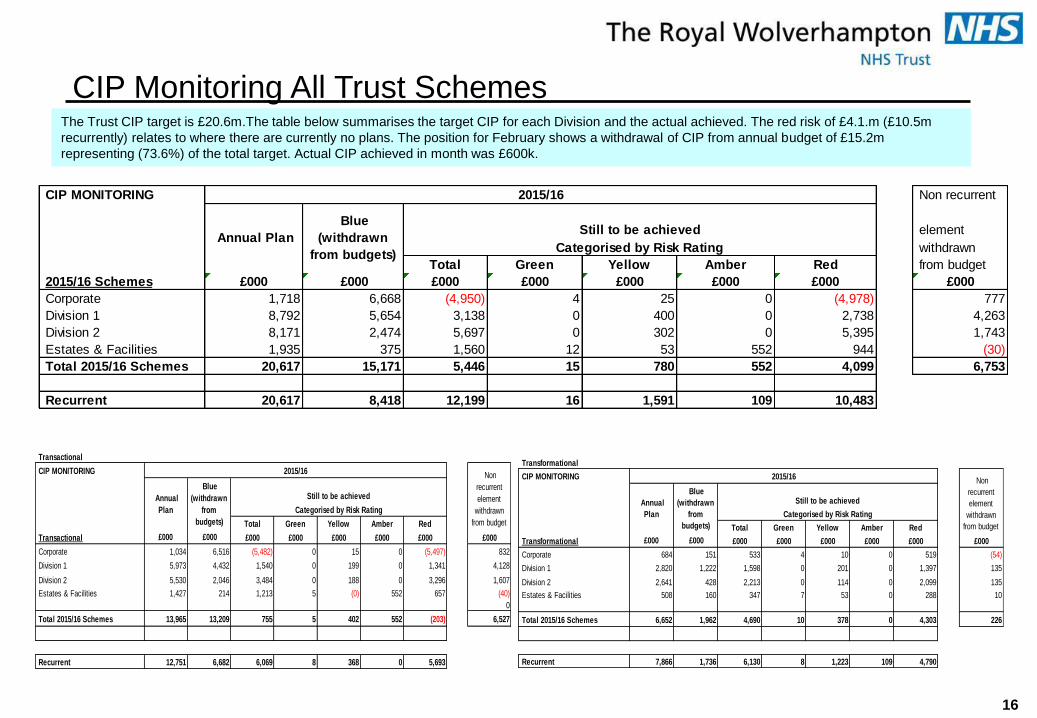

CIP Cumulative

The original Trust CIP target for 2015/16 is £20.6m.

At Month 11 a total of £15.2m (Annual Budget) has been removed from budgets,

against the annual target of £20.6m. This represents 73.6% of the total target.

The recurrent CIP achieved to Month 11 is £8.41m, which represents 40.8% of the

annual target.

The in-month target was £2.89m, with actual achievement in month of £1.34m, a

shortfall in month of (£1.56m).

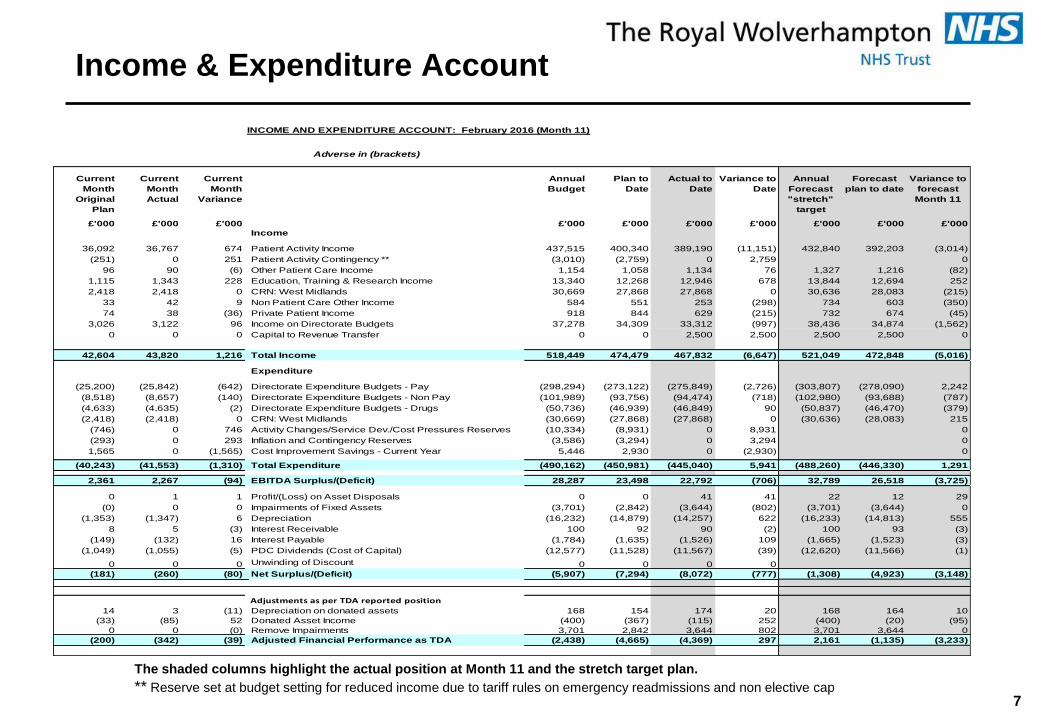

Income & Expenditure Account

7

The shaded columns highlight the actual position at Month 11 and the stretch target plan.

** Reserve set at budget setting for reduced income due to tariff rules on emergency readmissions and non elective cap

INCOME AND EXPENDITURE ACCOUNT: February 2016 (Month 11)

Adverse in (brackets)

£'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000 £'000

Income

36,092 36,767 674 Patient Activity Income 437,515 400,340 389,190 (11,151) 432,840 392,203 (3,014)

(251) 0 251 Patient Activity Contingency ** (3,010) (2,759) 0 2,759 0

96 90 (6) Other Patient Care Income 1,154 1,058 1,134 76 1,327 1,216 (82)

1,115 1,343 228 Education, Training & Research Income 13,340 12,268 12,946 678 13,844 12,694 252

2,418 2,418 0 CRN: West Midlands 30,669 27,868 27,868 0 30,636 28,083 (215)

33 42 9 Non Patient Care Other Income 584 551 253 (298) 734 603 (350)

74 38 (36) Private Patient Income 918 844 629 (215) 732 674 (45)

3,026 3,122 96 Income on Directorate Budgets 37,278 34,309 33,312 (997) 38,436 34,874 (1,562)

0 0 0 Capital to Revenue Transfer 0 0 2,500 2,500 2,500 2,500 0

42,604 43,820 1,216 Total Income 518,449 474,479 467,832 (6,647) 521,049 472,848 (5,016)

Expenditure

(25,200) (25,842) (642) Directorate Expenditure Budgets - Pay (298,294) (273,122) (275,849) (2,726) (303,807) (278,090) 2,242

(8,518) (8,657) (140) Directorate Expenditure Budgets - Non Pay (101,989) (93,756) (94,474) (718) (102,980) (93,688) (787)

(4,633) (4,635) (2) Directorate Expenditure Budgets - Drugs (50,736) (46,939) (46,849) 90 (50,837) (46,470) (379)

(2,418) (2,418) 0 CRN: West Midlands (30,669) (27,868) (27,868) 0 (30,636) (28,083) 215

(746) 0 746 Activity Changes/Service Dev./Cost Pressures Reserves (10,334) (8,931) 0 8,931 0

(293) 0 293 Inflation and Contingency Reserves (3,586) (3,294) 0 3,294 0

1,565 0 (1,565) Cost Improvement Savings - Current Year 5,446 2,930 0 (2,930) 0

(40,243) (41,553) (1,310) Total Expenditure (490,162) (450,981) (445,040) 5,941 (488,260) (446,330) 1,291

2,361 2,267 (94) EBITDA Surplus/(Deficit) 28,287 23,498 22,792 (706) 32,789 26,518 (3,725)

0 1 1 Profit/(Loss) on Asset Disposals 0 0 41 41 22 12 29

(0) 0 0 Impairments of Fixed Assets (3,701) (2,842) (3,644) (802) (3,701) (3,644) 0

(1,353) (1,347) 6 Depreciation (16,232) (14,879) (14,257) 622 (16,233) (14,813) 555

8 5 (3) Interest Receivable 100 92 90 (2) 100 93 (3)

(149) (132) 16 Interest Payable (1,784) (1,635) (1,526) 109 (1,665) (1,523) (3)

(1,049) (1,055) (5) PDC Dividends (Cost of Capital) (12,577) (11,528) (11,567) (39) (12,620) (11,566) (1)

0 0 0 Unwinding of Discount 0 0 0 0

(181) (260) (80) Net Surplus/(Deficit) (5,907) (7,294) (8,072) (777) (1,308) (4,923) (3,148)

Adjustments as per TDA reported position

14 3 (11) Depreciation on donated assets 168 154 174 20 168 164 10

(33) (85) 52 Donated Asset Income (400) (367) (115) 252 (400) (20) (95)

0 0 (0) Remove Impairments 3,701 2,842 3,644 802 3,701 3,644 0

(200) (342) (39) Adjusted Financial Performance as TDA (2,438) (4,665) (4,369) 297 2,161 (1,135) (3,233)

Plan to

Date

Annual

Budget

Current

Month

Original

Plan

Current

Month

Actual

Current

Month

Variance

Variance to

forecast

Month 11

Actual to

Date

Variance to

Date

Annual

Forecast

"stretch"

target

Forecast

plan to date

TDA

8

Financial Targets and Rating

Note: The ratings have been updated to reflect the revised Monitor ‘Financial Sustainability Risk Rating released in August, which include ratings for I&E margin and

performance against financial plan. All ratings have a maximum score of 4.

Note: The Financial Efficiency ratings detailed above have been calculated based upon the financial plan following adjustment for the capital to revenue transfer. The capital to

revenue transfer has been reflected in both the financial plan and the reported actual figures for Month 11.

Performance against Financial Targets Target Performance RAG

I & E Target Month 11 -£4,923k -£8,072k

Performance against TDA target Month 11 -£1,135k -£4,369k

CIP Target Month 11 YTD £17,315k £13,831k

CRL (Year end) £40,824k £38,349k

EFL (Year end) £34,181k £31,681k

Capital Cost Absorption Rate (Year end) 3.50% 3.50%

Financial Efficiency Rating

Ratio KPIs Rating Rating Rating

I&E Margin 0.5 % 3 (0.3) % 2 (1.0) % 2

Variance in I&E margin 0.0 % 4 0.0 % 3 (0.7) % 3

Financial Efficiency Rating 3.5 2.5 2.5

Continuity of Service Rating

Ratio Rating Plan To Date Rating Acutal To Date Rating Definitions/ notes

Liquidity Ratio(days) (12) days 2 (15) days 1 (13) days 2

Capital Servicing

Capacity (Times)1.9 Times 3 2.0 Times 3 1.7 Times 2

Overall Continuity of Service Rating 2.5 2.0 2.0

Overall Financial Sustainability Risk Rating 3.0 2.0 3.0

=Net Surplus/(Deficit)/Total Income

Cash plus trade debtors less trade creditors plus expressed as days of current year operating expenses.

.

Annual Plan

The number of times the debt can be met by the surplus. = EBITDA+interest receivable/ Total Monthly

debt payments.

Average of all four ratios. If any KPI equals 1, maximum overall rating of 2

Annual Plan Actual to Date Definitions/ notesPlan to Date

=Difference in I&E margin from plan/Total Income

TDA

TDA Plan

£'000

YTD

Actual

£'000

YTD

Variance

£'000

Income 472,941 467,922 (5,019)

Expenditure (474,076) (472,290) 1,785

Net Surplus (1,135) (4,369) (3,233)

Note: Income in the table above includes Interest Receivable,

and Expenditure includes Interest Payable and PDC Dividend.Please note: EFL and CRL above remain at original plan level as per the TDA return.

Formal adjustment to the Limits Report have now been received to reflect the Capital to

Revenue transfer and it is expected that they will be included in the Month 12 return.

Risks

9

The level of financial risk and mitigations have been assessed. The main risks relate to CIP and contractual issues for which actions are being taken

to mitigate against.

RiskLikelihood of

risk

Potential

consequence

rating

RiskCurrent Risk

£000's

Risk after

Mitigation

£000's

Mitigating Action

Cost Improvement

Programme 2015/16Likely Major B4 4,099 3,000

The current forecast for CIP is an under

achievement in 2015/16 of £4.1m. Further non-

recurrent savings have been taken in month. The

recurrent risk is £10.4m

Contract income issues-

Fines, Readmissions,

Emergency Threshold

Likely Major B4 4,823 3,919

Discussions are on-going with Commissioners in

order to secure the return of funds. Staffordshire

CCG's have confirmed that they will not be

reinvesting any emergency threshold funds /

readmissions with RWT as the funds have been

invested within Staffordshire. Walsall CCG will be

returning fines and readmissions but not

emergency threshold. Meetings are continuing in

order to pursue further funding, including

Specialised Services in relation to the Cannock

transfer of activity.

Cash Rare Major E4 2,000 0

Further to Finance action taken, the Trust should

now achieve its 2015/16 EFL. However, there

remains a considerable level of outstanding

invoiced and accrued debt, in particular NHS,

where settlement is still being actively pursued.

Risk Rating

Likelihood Rating 1. Insignificant 2. Minor 3. Moderate 4. Major 5. Catastrophic

A - Almost Certain

B - Likely

C - Possible

D - Unlikely

E - Rare

Potential Consequence Rating

Agency

In Month 11, there are 7,361 WTE’s in post, against a forecast plan of 7,375 WTE.

Since Month 10 WTE’s have reduced by 35 WTE.

Division 2 is over-established in Month 11, with WTE’s of 54 above budgeted levels,

whilst Divisions 1 and Estates and Facilities divisions continue to hold a level of

vacancies. Division 1 has 191 WTE vacant posts at Month 11.

Note: The September forecast reduction is due to the need to correct the year to date to reflect

the revised forecast.

In Month 11 agency expenditure of £1.33m was incurred, a reduction of £19k since

Month 10 and an increase of £375k since the same period in 2014/15.

The main areas of expenditure in Month 11 are: Emergency Services Group (£385k),

Oncology & Heam Group (£179k), Rehab & Amb Group (£131k) and Critical care

(£85k).

The key movements between Months 10 and 11 have been within Oncology & Heam

Group reporting a £60k increase in Month 11 and Orthopaedics, reporting a £32k

increase. The Emergency Services Group agency expenditure has reduced by £75k in

Month 11 and Critical Care expenditure has reduced by £21k in month.

The Trust continues to monitor and manage agency expenditure, with the aim to

reduce costs. All Trusts have been given a nurse agency spend cap, as a percentage

of total nursing spend. For RWT this is 3%, and nurse agency spend is 0.5%, well

within the target.

In Month 11 Locum expenditure was £203k, an increase of £27k from the Month 10

expenditure level. The Month 11 expenditure is in line with the expenditure in the

same period of 2014/15.

Locum expenditure mainly occurred in Medical Services Group (£32k), Emergency

Services Group (£24k), Oncology & Haematology (£20k) and General surgery (£17k).

Critical Care and Children’s Services have both seen increases in locum usage in

Month 11.

10

Pay Analysis WTE

Locum

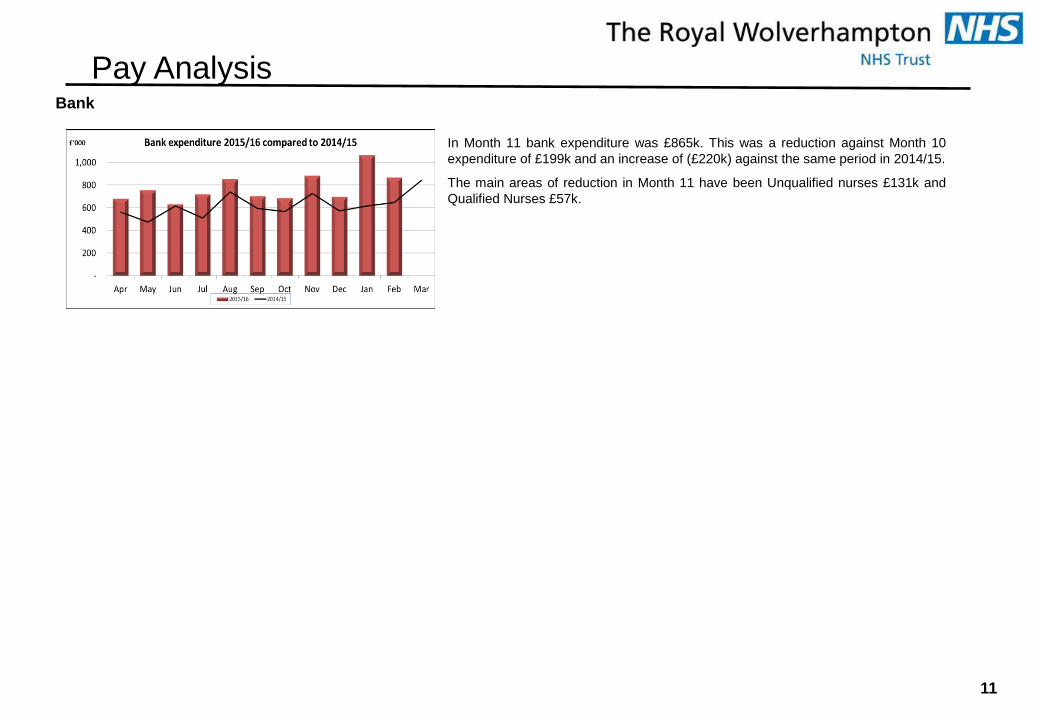

In Month 11 bank expenditure was £865k. This was a reduction against Month 10

expenditure of £199k and an increase of (£220k) against the same period in 2014/15.

The main areas of reduction in Month 11 have been Unqualified nurses £131k and

Qualified Nurses £57k.

11

Pay Analysis Bank

Patient Care Income - Variance

12

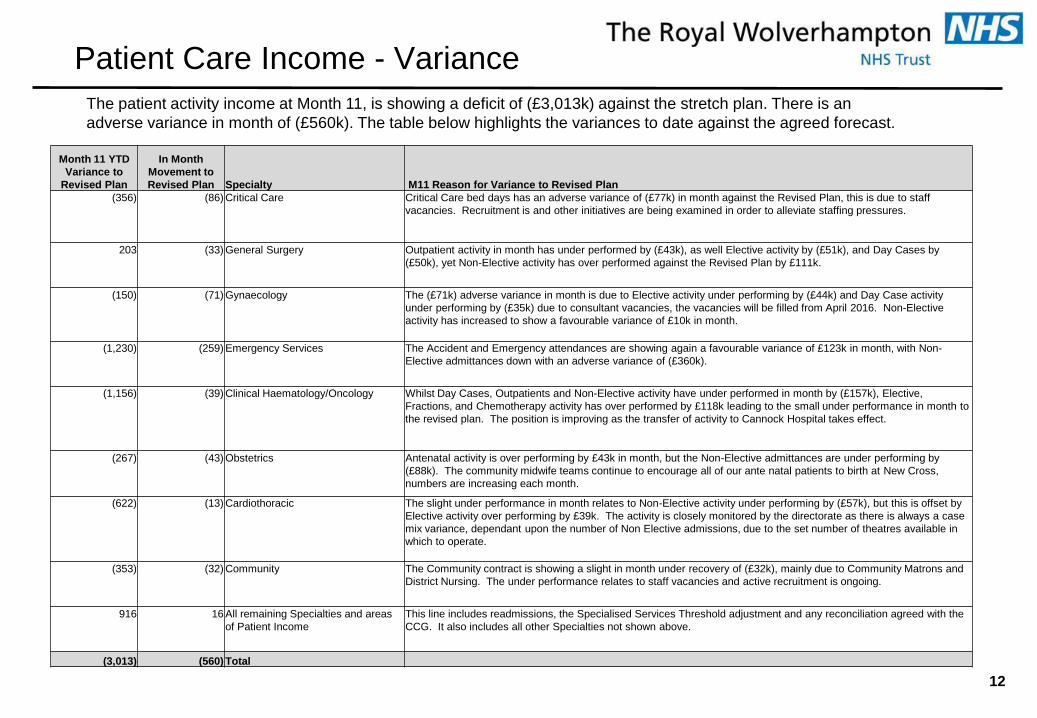

The patient activity income at Month 11, is showing a deficit of (£3,013k) against the stretch plan. There is an

adverse variance in month of (£560k). The table below highlights the variances to date against the agreed forecast.

Month 11 YTD

Variance to

Revised Plan

In Month

Movement to

Revised Plan Specialty M11 Reason for Variance to Revised Plan

(356) (86) Critical Care Critical Care bed days has an adverse variance of (£77k) in month against the Revised Plan, this is due to staff

vacancies. Recruitment is and other initiatives are being examined in order to alleviate staffing pressures.

203 (33) General Surgery Outpatient activity in month has under performed by (£43k), as well Elective activity by (£51k), and Day Cases by

(£50k), yet Non-Elective activity has over performed against the Revised Plan by £111k.

(150) (71) Gynaecology The (£71k) adverse variance in month is due to Elective activity under performing by (£44k) and Day Case activity

under performing by (£35k) due to consultant vacancies, the vacancies will be filled from April 2016. Non-Elective

activity has increased to show a favourable variance of £10k in month.

(1,230) (259) Emergency Services The Accident and Emergency attendances are showing again a favourable variance of £123k in month, with Non-

Elective admittances down with an adverse variance of (£360k).

(1,156) (39) Clinical Haematology/Oncology Whilst Day Cases, Outpatients and Non-Elective activity have under performed in month by (£157k), Elective,

Fractions, and Chemotherapy activity has over performed by £118k leading to the small under performance in month to

the revised plan. The position is improving as the transfer of activity to Cannock Hospital takes effect.

(267) (43) Obstetrics Antenatal activity is over performing by £43k in month, but the Non-Elective admittances are under performing by

(£88k). The community midwife teams continue to encourage all of our ante natal patients to birth at New Cross,

numbers are increasing each month.

(622) (13) Cardiothoracic The slight under performance in month relates to Non-Elective activity under performing by (£57k), but this is offset by

Elective activity over performing by £39k. The activity is closely monitored by the directorate as there is always a case

mix variance, dependant upon the number of Non Elective admissions, due to the set number of theatres available in

which to operate.

(353) (32) Community The Community contract is showing a slight in month under recovery of (£32k), mainly due to Community Matrons and

District Nursing. The under performance relates to staff vacancies and active recruitment is ongoing.

916 16 All remaining Specialties and areas

of Patient Income

This line includes readmissions, the Specialised Services Threshold adjustment and any reconciliation agreed with the

CCG. It also includes all other Specialties not shown above.

(3,013) (560) Total

Patient Care Activity Performance

13

3,000

3,500

4,000

4,500

5,000

5,500

6,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Elective Monthly Activity ( Spells )

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

Revised Activity Plan

3,000

3,200

3,400

3,600

3,800

4,000

4,200

4,400

4,600

4,800

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Non-Elective Monthly Activity (Spells)

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

Revised Activity Plan

6,000

7,000

8,000

9,000

10,000

11,000

12,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

A&E Monthly Activity

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

revised Plan

8,000

9,000

10,000

11,000

12,000

13,000

14,000

15,000

16,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Outpatient FirstMonthly Activity

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

Revised Plan

20,000

25,000

30,000

35,000

40,000

45,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Outpatient Follow up Monthly Activity

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

Revised Plan

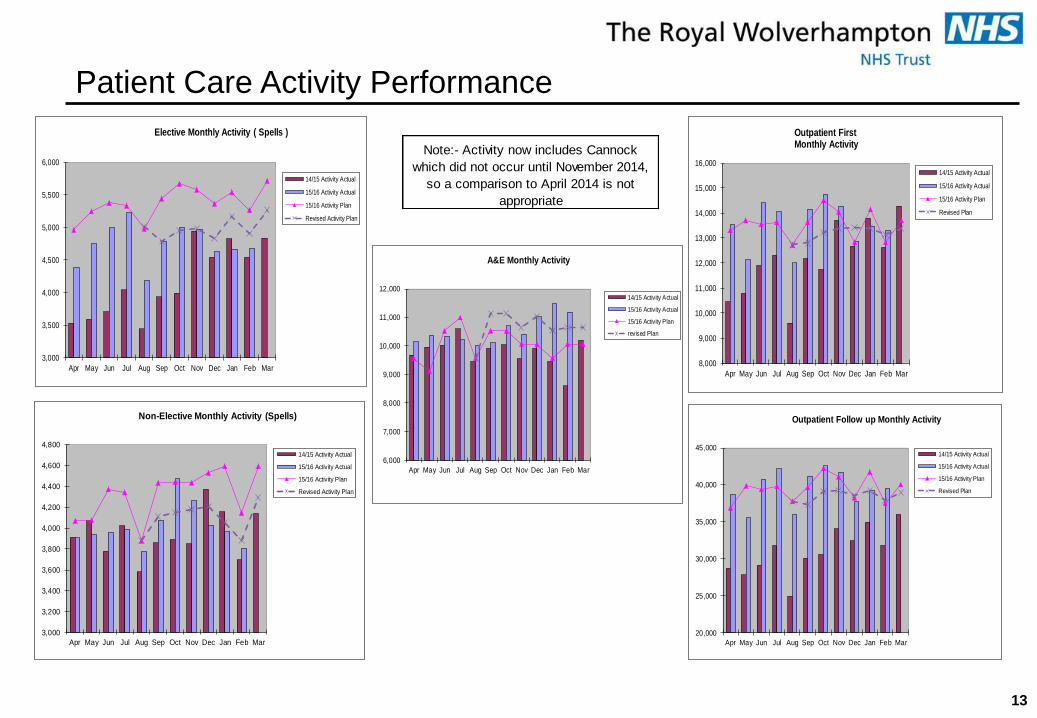

Note:- Activity now includes Cannock

which did not occur until November 2014,

so a comparison to April 2014 is not

appropriate

Community Performance against CCG Activity Plan

14

0

100

200

300

400

500

600

700

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Community Outpatients Monthly Activity

14/15 Activity Actual

15/16 Activity Actual

15/16 TOTAL Activity Plan

Outpatients includes:

- Community Paeds

- Care of the Elderly OPs- Falls Assessment

- Spasticity

38,000

43,000

48,000

53,000

58,000

63,000

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Community Contacts Monthly Activity

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

Contacts includes:

- District Nursing

- Allied Health Professionals- Walk-in Centre

- CICT Rehab- Stroke co-ordinators- Contraception &

Sexual Health- INR

1,100

1,300

1,500

1,700

1,900

2,100

2,300

2,500

2,700

2,900

Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar

Community Occupied Bed Days Monthly Activity (OBD's)

14/15 Activity Actual

15/16 Activity Actual

15/16 Activity Plan

OBDs includes:

- Care of the Elderly

- Neuro-rehabilition

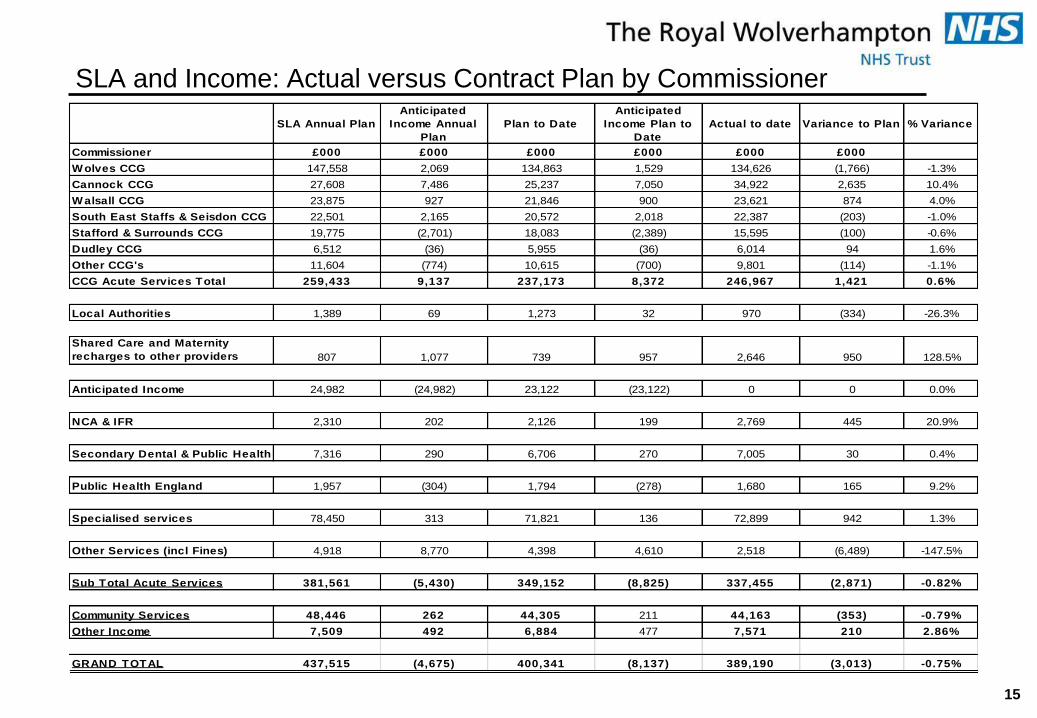

SLA and Income: Actual versus Contract Plan by Commissioner

15

SLA Annual Plan

Anticipated

Income Annual

Plan

Plan to Date

Anticipated

Income Plan to

Date

Actual to date Variance to Plan % Variance

Commissioner £000 £000 £000 £000 £000 £000

W olves CCG 147,558 2,069 134,863 1,529 134,626 (1,766) -1.3%

Cannock CCG 27,608 7,486 25,237 7,050 34,922 2,635 10.4%

W alsall CCG 23,875 927 21,846 900 23,621 874 4.0%

South East Staffs & Seisdon CCG 22,501 2,165 20,572 2,018 22,387 (203) -1.0%

Stafford & Surrounds CCG 19,775 (2,701) 18,083 (2,389) 15,595 (100) -0.6%

Dudley CCG 6,512 (36) 5,955 (36) 6,014 94 1.6%

Other CCG's 11,604 (774) 10,615 (700) 9,801 (114) -1.1%

CCG Acute Services Total 259,433 9,137 237,173 8,372 246,967 1,421 0.6%

Local Authorities 1,389 69 1,273 32 970 (334) -26.3%

Shared Care and Maternity

recharges to other providers 807 1,077 739 957 2,646 950 128.5%

Anticipated Income 24,982 (24,982) 23,122 (23,122) 0 0 0.0%

NCA & IFR 2,310 202 2,126 199 2,769 445 20.9%

Secondary Dental & Public Health 7,316 290 6,706 270 7,005 30 0.4%

Public Health England 1,957 (304) 1,794 (278) 1,680 165 9.2%

Specialised services 78,450 313 71,821 136 72,899 942 1.3%

Other Services (incl Fines) 4,918 8,770 4,398 4,610 2,518 (6,489) -147.5%

Sub Total Acute Services 381,561 (5,430) 349,152 (8,825) 337,455 (2,871) -0.82%

Community Services 48,446 262 44,305 211 44,163 (353) -0.79%

Other Income 7,509 492 6,884 477 7,571 210 2.86%

GRAND TOTAL 437,515 (4,675) 400,341 (8,137) 389,190 (3,013) -0.75%

CIP Monitoring All Trust Schemes The Trust CIP target is £20.6m.The table below summarises the target CIP for each Division and the actual achieved. The red risk of £4.1.m (£10.5m

recurrently) relates to where there are currently no plans. The position for February shows a withdrawal of CIP from annual budget of £15.2m

representing (73.6%) of the total target. Actual CIP achieved in month was £600k.

16

CIP MONITORING Non recurrent

element

withdrawn

Total Green Yellow Amber Red from budget

2015/16 Schemes £000 £000 £000 £000 £000 £000 £000 £000

Corporate 1,718 6,668 (4,950) 4 25 0 (4,978) 777

Division 1 8,792 5,654 3,138 0 400 0 2,738 4,263

Division 2 8,171 2,474 5,697 0 302 0 5,395 1,743

Estates & Facilities 1,935 375 1,560 12 53 552 944 (30)

Total 2015/16 Schemes 20,617 15,171 5,446 15 780 552 4,099 6,753

Recurrent 20,617 8,418 12,199 16 1,591 109 10,483

2015/16

Annual Plan

Blue

(withdrawn

from budgets)

Still to be achieved

Categorised by Risk Rating

Transactional

CIP MONITORING

Total Green Yellow Amber Red

Transactional £000 £000 £000 £000 £000 £000 £000 £000

Corporate 1,034 6,516 (5,482) 0 15 0 (5,497) 832

Division 1 5,973 4,432 1,540 0 199 0 1,341 4,128

Division 2 5,530 2,046 3,484 0 188 0 3,296 1,607

Estates & Facilities 1,427 214 1,213 5 (0) 552 657 (40)

Unallocated 0 0 0 0 0 0 0 0

Total 2015/16 Schemes 13,965 13,209 755 5 402 552 (203) 6,527

Recurrent 12,751 6,682 6,069 8 368 0 5,693

2015/16 Non

recurrent

element

withdrawn

from budget

Annual

Plan

Blue

(withdrawn

from

budgets)

Still to be achieved

Categorised by Risk Rating

Transformational

CIP MONITORING

Total Green Yellow Amber Red

Transformational £000 £000 £000 £000 £000 £000 £000 £000

Corporate 684 151 533 4 10 0 519 (54)

Division 1 2,820 1,222 1,598 0 201 0 1,397 135

Division 2 2,641 428 2,213 0 114 0 2,099 135

Estates & Facilities 508 160 347 7 53 0 288 10

Unallocated 0 0 0 0 0 0 0

Total 2015/16 Schemes 6,652 1,962 4,690 10 378 0 4,303 226

Recurrent 7,866 1,736 6,130 8 1,223 109 4,790

Non

recurrent

element

withdrawn

from budget

2015/16

Annual

Plan

Blue

(withdrawn

from

budgets)

Still to be achieved

Categorised by Risk Rating

Statement of Financial Position

17

The Public Sector Payment Policy sets out a target for payment of 95%, in value and volume, to be paid within 30 days of receipt. The Trust's performance against this target is:

M11 Cumulative

- Value 66% 88%- Volume 78% 89%

M10 Cumulative

- Value 89% 90%- Volume 85% 90%

The Trust's performance on volume continues to be affected by the volume of pharmacy invoices associated with the take on of Cannock Hospital. We have previously reported that escalated action is currently taking place to resolve the problem

Calculated Debtor Days for the year to date are:-

M11 Actual M11 Plan M10 ActualTotal 12.29 13.91 12.91Being:-NHS 12.78 15.23 14.14Non NHS 9.26 5.39 4.98

The lower level of NHS debtor days this month is primarily due to significant invoices being raised last period to the DoH & TDA in respect of MSFT which have now cleared. Non NHS days are higher due to a large year to date invoice relating to Social Sevices salary recharge. This invoice has been settled in March.

THE ROYAL WOLVERHAMPTON NHS TRUST

2015/16 Balance Sheet as at 28th February 2016

Feb 2016 Feb 2016 Jan 2016 Movement March 2015

Plan Actual Actual in Month Actual

£000 £000 £000 £000 £000

NON CURRENT ASSETS

Property,Plant and Equipment - Tangible Assets 403,560 398,725 396,429 2,296 382,971

Intangible Assets 676 472 490 (18) 676

Trade and Other Receivables Non Current 1,517 1,517 1,517 0 1,710

TOTAL NON CURRENT ASSETS 405,753 400,714 398,436 2,278 385,357

CURRENT ASSETS

Inventories 5,642 5,544 6,118 (574) 6,291

Trade and Other Receivables 23,228 30,662 30,538 124 19,783

Other Current Assets 0 0 0 0 0

Cash and cash equivalents 16,224 25,391 13,605 11,786 41,598

TOTAL CURRENT ASSETS 45,094 61,597 50,261 11,336 67,672

Non Current Assets Held for Sale 800 800 800 0 800

TOTAL ASSETS 451,647 463,111 449,497 13,614 453,829

CURRENT LIABLILITES

Trade & Other Payables (53,043) (67,291) (54,381) (12,910) (52,498)

Liabilities arising from PFIs / Finance Leases (1,849) (1,885) (1,885) 0 (1,885)

Provisions for Liabilities and Charges (4,830) (4,515) (4,609) 94 (5,821)

TOTAL CURRENT LIABILITIES (59,722) (73,691) (60,875) (12,816) (60,204)

NET CURRENT ASSETS / (LIABILITIES) (14,628) (12,094) (10,614) (1,480) 7,468

TOTAL ASSETS LESS CURRENT LIABILITIES 391,925 389,420 388,622 798 393,625

NON CURRENT LIABILITIES

Other Liabilities (4,837) (5,516) (4,476) (1,040) (5,943)

Provision for Liabilities and Charges (648) (648) (629) (19) (648)

TOTAL NON CURRENT LIABILITIES (5,485) (6,164) (5,105) (1,059) (6,591)

TOTAL ASSETS EMPLOYED 386,440 383,256 383,517 (261) 387,034

FINANCED BY TAXPAYERS EQUITY

Public Dividend Capital 232,043 229,543 229,543 0 225,252

Retained Earnings 21,165 21,580 21,774 (194) 26,568

Revaluation Reserve 133,042 131,943 132,009 (66) 133,042

Donated Asset Reserve 0 0 0 0 1,982

Government Grant Reserve 0 0 0 0 0

Other Reserves 190 190 190 0 190

TOTAL TAXPAYERS EQUITY 386,440 383,256 383,516 (260) 387,034

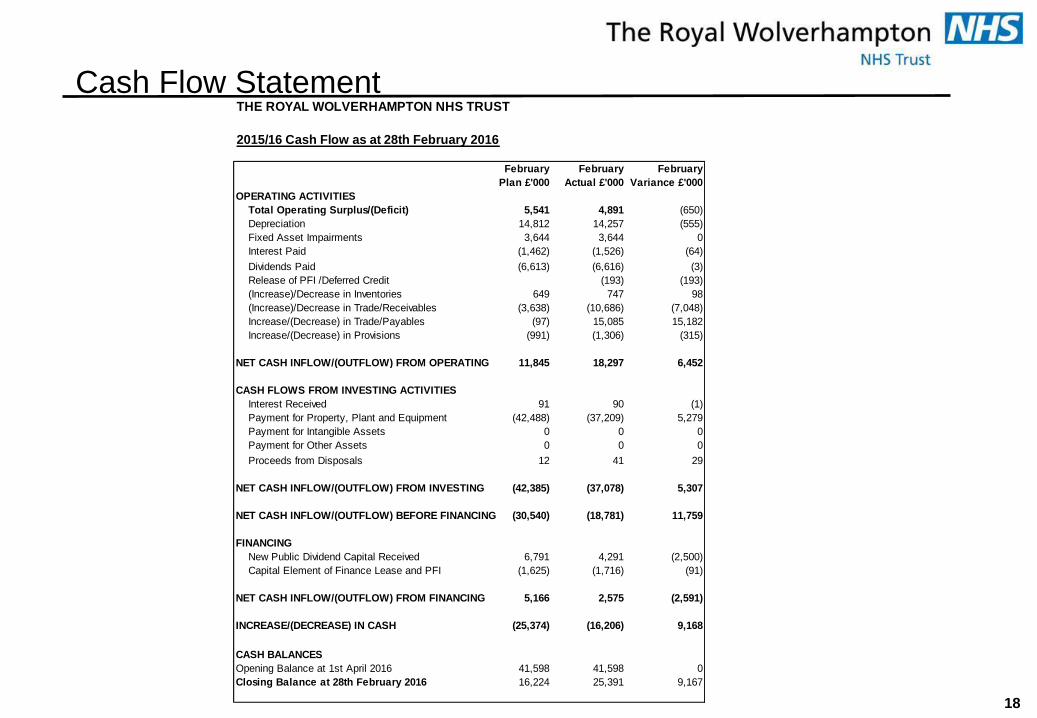

Cash Flow Statement

18

THE ROYAL WOLVERHAMPTON NHS TRUST

2015/16 Cash Flow as at 28th February 2016

February February February

Plan £'000 Actual £'000 Variance £'000

OPERATING ACTIVITIES

Total Operating Surplus/(Deficit) 5,541 4,891 (650)

Depreciation 14,812 14,257 (555)

Fixed Asset Impairments 3,644 3,644 0

Interest Paid (1,462) (1,526) (64)

Dividends Paid (6,613) (6,616) (3)

Release of PFI /Deferred Credit (193) (193)

(Increase)/Decrease in Inventories 649 747 98

(Increase)/Decrease in Trade/Receivables (3,638) (10,686) (7,048)

Increase/(Decrease) in Trade/Payables (97) 15,085 15,182

Increase/(Decrease) in Provisions (991) (1,306) (315)

11,845 18,297 6,452

CASH FLOWS FROM INVESTING ACTIVITIES

Interest Received 91 90 (1)

Payment for Property, Plant and Equipment (42,488) (37,209) 5,279

Payment for Intangible Assets 0 0 0

Payment for Other Assets 0 0 0

Proceeds from Disposals 12 41 29

(42,385) (37,078) 5,307

(30,540) (18,781) 11,759

FINANCING

New Public Dividend Capital Received 6,791 4,291 (2,500)

Capital Element of Finance Lease and PFI (1,625) (1,716) (91)

5,166 2,575 (2,591)

(25,374) (16,206) 9,168

CASH BALANCES

Opening Balance at 1st April 2016 41,598 41,598 0

Closing Balance at 28th February 2016 16,224 25,391 9,167

NET CASH INFLOW/(OUTFLOW) FROM OPERATING

NET CASH INFLOW/(OUTFLOW) FROM FINANCING

INCREASE/(DECREASE) IN CASH

NET CASH INFLOW/(OUTFLOW) FROM INVESTING

NET CASH INFLOW/(OUTFLOW) BEFORE FINANCING