report to investors-final-high_res(1).pdf

TRANSCRIPT

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 1/7

1

Report to Investors

Q3, 2013

Quick Look

! 2013 revenues now projected at $9 million

! On track to exceed 2013 EBITDA goal of $450,000

! Lease financing ended, ironically benefiting the business

! Series B capital raise delayed to show we can manage lease end

! Convertible Note was oversubscribed, raising a quick $250,000

! Marketing and Sales pipeline strong with 60% market share! Installation capacity is solid, at 2 completed installations/day

! First non-residential sales ready for installation

! Growth opportunities advancing well

! September was our 6th consecutive profitable month

! Q3 actuals exceeded budgets across the board

! Q3 and Year-To-Date are profitable

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 2/7

2

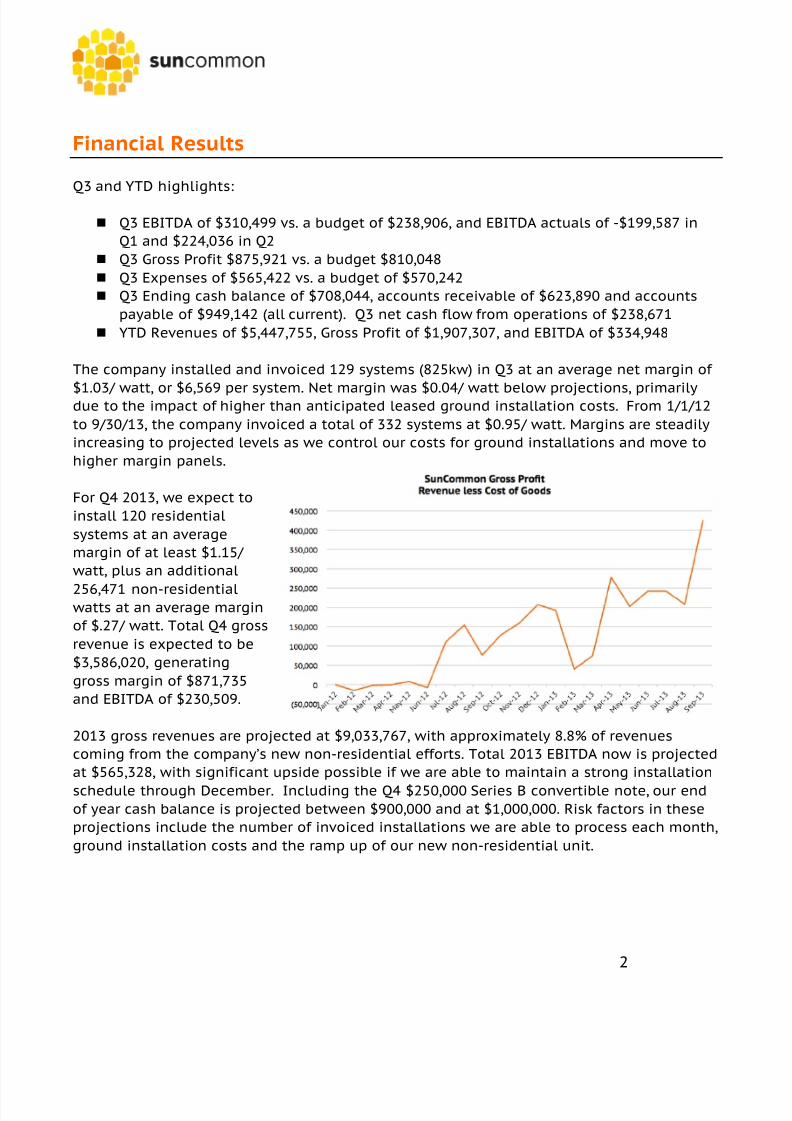

Financial Results

Q3 and YTD highlights:

! Q3 EBITDA of $310,499 vs. a budget of $238,906, and EBITDA actuals of -$199,587 in

Q1 and $224,036 in Q2

! Q3 Gross Profit $875,921 vs. a budget $810,048

! Q3 Expenses of $565,422 vs. a budget of $570,242

! Q3 Ending cash balance of $708,044, accounts receivable of $623,890 and accounts

payable of $949,142 (all current). Q3 net cash flow from operations of $238,671

! YTD Revenues of $5,447,755, Gross Profit of $1,907,307, and EBITDA of $334,948

The company installed and invoiced 129 systems (825kw) in Q3 at an average net margin of

$1.03/ watt, or $6,569 per system. Net margin was $0.04/ watt below projections, primarilydue to the impact of higher than anticipated leased ground installation costs. From 1/1/12

to 9/30/13, the company invoiced a total of 332 systems at $0.95/ watt. Margins are steadily

increasing to projected levels as we control our costs for ground installations and move to

higher margin panels.

For Q4 2013, we expect to

install 120 residential

systems at an average

margin of at least $1.15/

watt, plus an additional

256,471 non-residentialwatts at an average margin

of $.27/ watt. Total Q4 gross

revenue is expected to be

$3,586,020, generating

gross margin of $871,735

and EBITDA of $230,509.

2013 gross revenues are projected at $9,033,767, with approximately 8.8% of revenues

coming from the company’s new non-residential efforts. Total 2013 EBITDA now is projected

at $565,328, with significant upside possible if we are able to maintain a strong installation

schedule through December. Including the Q4 $250,000 Series B convertible note, our endof year cash balance is projected between $900,000 and at $1,000,000. Risk factors in these

projections include the number of invoiced installations we are able to process each month,

ground installation costs and the ramp up of our new non-residential unit.

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 3/7

3

Business News

Consumer financing. SunCommonbrought to Vermont the first-ever

residential roof-top solar lease, and

used this point of difference to enter

and then dominate the market. Yetthe challenges of sole-source

procurement caused us in 2012 to

diversify our supplier base and

consumer financing as well. During2013 Q3, SunPower increased its

lease financing costs out reach forour customers. We were initially concerned that, without our previous bread-and-

butter financing, volume would erode. Our sales team met and quickly focused onwhat customers are attracted to: install with no upfront cost and a low monthly

payment, agnostic on the particulars of the financing. So we pivoted away from

lease financing and toward the very attractive unsecured solar loan program we

designed with the New England Federal Credit Union. Not only did we maintainvolume, but by increasing our ratio of of LG panels, our margins rose dramatically.

Ironically, while it initially seemed threatening, the end of the lease has benefitted

our business. And we’re adding additional unsecured and secured loan options

through other providers to ensure steady financing availability.

Ground-mount installer comfort. With >50% of

roofs unsuitable to host solar, we wisely

expanded our offering to ground-mountedsystems. But our initial installation vendor

was incapable of accommodating our demand

and innovative fixed-pricing. We lost money

and terminated that partnership. Thesuccessor vendor, Headwaters Construction

through its solar subsidiary SolSource, hasperformed well. Our volume is solid, and we’ve

worked through the hangover of low-marginleased ground-mounts such that ground-mount installs now deliver margins

comparable to roof installs.

Net metering caps. Vermont state law requires utilities allow their customers toinstall renewable energy projects like solar up to 4% of the utility’s peak capacity.

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 4/7

4

In Q3, 4 of the state’s 20 utilities hit that cap and halted further such installations.

Green Mountain Power, with 70% of the state’s electricity customers, is both below

its net metering cap and hugely supportive of solar and SunCommon – so our

efforts are focused there without a hit to volume. And we are part of a solidcoalition of allies in government, utilities, business, environmental organizations

and our extensive customer base to expand net metering statewide in the

Legislature come January – with excellent prospects.

Pipeline remains solid. Our

innovative approach to

marketing and salescontinues to generate a

robust pipeline, as the Q3

financials show. Wemaintain a conservativerevenue recognition policy,

booking only those projects

actually invoiced. Yet we

know that revenue willensue from signed

contracts once we

complete the permitting, financing, equipment procurement and installation. At the

end of Q3, this “sold but not invoiced” backlog totaled almost $2 million in expectedfuture revenue.

Non-Residential begins. Reflecting our close relationship, SunCommon was selected

by the state’s largest electric utility, Green Mountain Power (GMP) to build the solar

on its landmark Energy Innovation Center at its statewide operations center in

Rutland. The installation began

in Q3. And Duxbury’s Crossett

Brook Middle School engaged

SunCommon to build its solar

system, which make it Vermont’smost solar school when

construction is complete in Q4.Both contribute to our bottom

line, and will generate solid

visibility for our community-

oriented business. More projectsare in the pipeline.

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 5/7

5

Looking Ahead

Geographical expansion. With dominant marketshare where we’re operating, SunCommon will

expand geographically to do more of what we’veshown we can do. Next Q1, we anticipate

expanding operations to Orange, Windsor and

Rutland Counties – where already we have 500

homeowners waiting in our database who haveasked us to help them go solar – before we even

launch there. It’s GMP territory, and that utility’s

leadership is eager for us to join them in Rutland

especially to help them make it the Solar Capital ofthe Northeast.

Community Solar. Vermont is one of few states that allow multiple customers to

benefit from a single solar array. And permitting here is quick and easy for solarsystems up to 150kW, enough for 25 homes. Our marketing and sales process

already has surfaced thousands of Vermonters who wanted to go solar, but whose

sites were unsuitable. And our salespeople are in 50 additional homes every week,

some fraction of which are not viable sites but would jump at buying their powerfrom one of our Solar Orchards at the farm down the road. We believe this is the

next big thing in solar and have spent this year perfecting the financial model(through a national accounting firm known for renewable energy finance),

identifying the first sites and designing the installation kit. We anticipate buildingthe first 2 of these in Q1, then stamping out 1 every other week. This will contribute

to our mission of knocking down the barriers that had made solar inaccessible and

helping that many more Vermonter be part of the climate change solution. And it

will furtherboost our

revenues.

SunCommon

retained thenational

accounting firm

CohnReznick

because of itsdeep

experience

structuring

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 6/7

6

solar project finance, so our model is the vetted industry standard. To finance

these projects, SunCommon will follow accepted practice by raising capital pools

comprised of debt, sponsor equity and income tax equity. We have solid prospects

for the debt and sponsor equity, and are beginning the search for tax equity toround out the necessary financing.

Capital raise. While we delayed the Series B to prove that SunCommon couldcontinue to thrive without the lease, we wanted to maintain momentum on these

growth opportunities. So we offered a Convertible Note to generate capital and

keep on track. The $250,000 ceiling was oversubscribed and quickly filled. We are

using that to complete the structuring of the Community Solar program and beginon geographical expansion. With that quarter million dollar head start, we are

finalizing the Series B prospectus and expect to present that to investors soon with

an expected close early in Q1 2014.

Conclusion

! When we started, there were 1,500 solar systems in Vermont built over the

prior decade. In SunCommon’s 18 months, we’ve sold an additional 600.

! Our marketing and sales pipeline is strong, installations are robust.

! The end of SunPower’s lease was managed well, turning what seemed like a

risk into a benefit as we ironically improved margins.! The Convertible Note capital raise was oversubscribed, showing confidence by

investors in our business.

! That allowed us to maintain momentum preparing for the exciting growthopportunities before us.

! SunCommon is profitable, with projections to exceed our profit goal for the

year.

! This appears to be working.

We continue to appreciate our beloved investors, whose early support made

possible this innovative enterprise and the success we have together achieved.

Duane, James and the entire SunCommon crew

8/14/2019 Report to Investors-FINAL-high_res(1).pdf

http://slidepdf.com/reader/full/report-to-investors-final-highres1pdf 7/7

In the Press