republic of mozambique - african development bank · republic of mozambique rural finance...

TRANSCRIPT

SCCD: N.G.

AFRICAN DEVELOPMENT FUND Language: English Original: English

REPUBLIC OF MOZAMBIQUE

RURAL FINANCE INTERMEDIATION SUPPORT PROJECT

APPRAISAL REPORT

AGRICULTURAL AND RURAL DEVELOPMENT DEPARTMENT ONAR NORTH, EASTCENTRAL AND SOUTH REGIONS OCTOBER 2003

TABLE OF CONTENTS

Page Programme Information Sheet , Currency and Measures, List of Tables, List of Annexes , (i-viii) List of Abbreviations, Basic Data Sheet, Logical Framework Matrix, Executive Summary 1. ORIGIN AND HISTORY OF THE PROGRAMME 1 2. THE AGRICULTURAL AND RURAL DEVELOPMENT 2 2.1 Salient Features 2 2.2 Poverty and Food Security 2 2.3 Land Tenure 3 2.4 Policies and Strategies 3 3. FINANCIAL SECTOR 4 3.1 Salient Features 5 3.2. Policies and regulatory Framework 5 3.3. Savings and Mobilisation Outreach 6 3.4 Rural Finance Sub-Sector 6 3.5. Gender and Rural Finance 10 3.6. Health and HIV/ AIDS 10 3.7. Potential Demand and Constraints of Rural Finance 11 3.8. Interventions of Major Donor 13 4. THE PROGRAMME AND ADF PROJECT 14 4.1 Programme Concept and Rationale 14 4.2 Programme Area and Beneficiaries 16 4.3 Strategic Context 16 4.4 Sector and Programme Objective 17 4.5 Programme Components and Description 17 4.6 Programme Costs 20

The ADF Project 21

4.7 Objectives of the ADF Project 21 4.8 Description of ADF Project 21 4.9 Rural Finance Market and Interest Rates 24 4.10 Environnemental Impact 25 4.11 ADF Project Costs 25 4.12 Sources of Finance and Expenditure Schedule 27 5. PROJECT IMPLEMENTATION 27 5.1 Executing Agency 27 5.2 Institutional Arrangements 28 5.3 Supervision and Implementation Schedule 29 5.4 Monitoring and Evaluation 30 5.5 Procurement Arrangements 31 5.6 Disbursement Arrangements 32 5.7 Financial Reporting and Auditing 33 5.8 Aid Co-ordination 33

TABLE OF CONTENTS (cont’d)

Page 6. PROJECT SUSTAINABILITY AND RISKS 34 6.1 Recurrent Costs 34 6.2 Sustainability 34 6.3 Risks and Mitigating Measures 35 7. PROJECT BENEFITS 35 7.1 Financial Analysis 35 7.2 Benefits Analysis 35 7.3 Social Impact Analysis 36 8 CONCLUSIONS AND RECOMMENDATIONS 37 8.1 Conclusions 37 8.2 Recommendation and Conditions for Loan Approval 37 8.3 Recommendations and Conditions for Grant Approval 38 This report was prepared by M. W. Karuri, Principal Financial Analyst, ONAR.1 (Team Leader), S. Pitamber, Gender Specialist, ONAR, J. Coompson, Senior Agricultural Economist, ONAR.1, B. Sambe, Micro-finance Expert, OCMU following their mission to Mozambique in August 2003. Enquiries should be directed to the authors or Mr A. D. Beileh, Manager, ONAR.1 (ext. 3747)

i

AFRICAN DEVELOPMENT FUND TEMPORARY RELOCATION AGENCY (TRA)

ANGLE DES TROIS RUES, AVENUE DU GHANA,

RUE PIERRE DE COUBERTIN, RUE HEIDI NOURA BP. 323, 1002 TUNIS BELVEDERE

TUNISIA TEL: (216) 71 333 511 FAX: (216) 71 10 34 35

EMAIL: [email protected]

PROJECT INFORMATION SHEET The information given hereunder is intended to provide some guidance to prospective suppliers, contractors and consultants and to all persons interested in the procurement of goods and services for Project approval by the Board of Directors of the Bank Group. More detailed information and guidance should be obtained from the Executing Agency of the Borrower. 1. Country: REPUBLIC OF MOZAMBIQUE 2 Project Title: Rural Finance Intermediation Support Project

(RUFISP) 3. Location: Nation-wide 4. Borrower: Republic of Mozambique 5. Executing Agency: Ministry of Planning and Finance (MPF) C.P 272 – Maputo-Mozambique Tel: 258-1-315040 Fax: 258-1-310493/315070 Email: [email protected] 6. Project Description: The Project will Comprise of four major components: A) Capacity Building and Institutional Development; B) Support to Outreach Expansion; C) Line of Credit; and D) Programme Management.

7. Total ADF Project Cost: i) Foreign Cost : UA 11.11 million (61%) ii) Local Cost : UA 07.53million Total : UA 18.64 million 8. Sources of Finance:: i) ADF Loan : UA 11.52 million ii) ADF Grant : UA 3.84 million iii) Fin. Institutions : UA 0.63 million iv) GoM : UA 2.65 million

Total UA 18.64 million 9. Date of Approval : November 2003 11. Estimated Starting Date : June 2004 for 6 years

12. Procurement of Goods : National Shopping 13. Consultancy Services: TA and Consultancy Services for Capacity Building and

Institutional support activities and studies; Service Providers/NGO to promote the Rural Finance Associations (RFAs) will be procured in accordance with the “Bank Group’s Rules of Procedure for Use of Consultants” through competition on the basis of a shortlist.

ii

CURRENCY EQUIVALENTS UA 1.00 = 29, 894 Metical (MZM)

USD 1.00 = 24,100 Metical (MZM)

WEIGHTS AND MEASURES 1 kilogram (kg) = 2.204 pounds (lb) 1 000 kg = 1 metric tonne (t) 1 kilometre (km) = 0.62 miles (mi) 1 metre (m) = 1.09 yards (yd) 1 square metre (m2) = 10.76 square feet (ft2) 1 acre (ac) = 0.405 ha 1 hectare (ha) = 2.47 acres

Fiscal Year

1 January to 31 December

LIST OF TABLES Table 1 Donor Support to Rural Microfinance sub-sector

Table 4.1 Summary of Programme Cost Estimates by Components Table 4.2 Sources of Programme Financing Table 4.3 Summary of Project Cost by Components Table 4.4 Summary of ADF Project Cost by Category of Expenditure Table 4.5 Sources of ADF Project Finance Table 4.6 Sources of Finance for the ADF Grant Table 5.1 Expenditure Schedule for the Project Table 5.2 Expenditure Schedule by Sources of Finance Table 5.3 Summary of Procurement Arrangements for ADF Project

Table 7 Summary of Financial Analysis of Sample Rural Enterprises

LIST OF ANNEXES

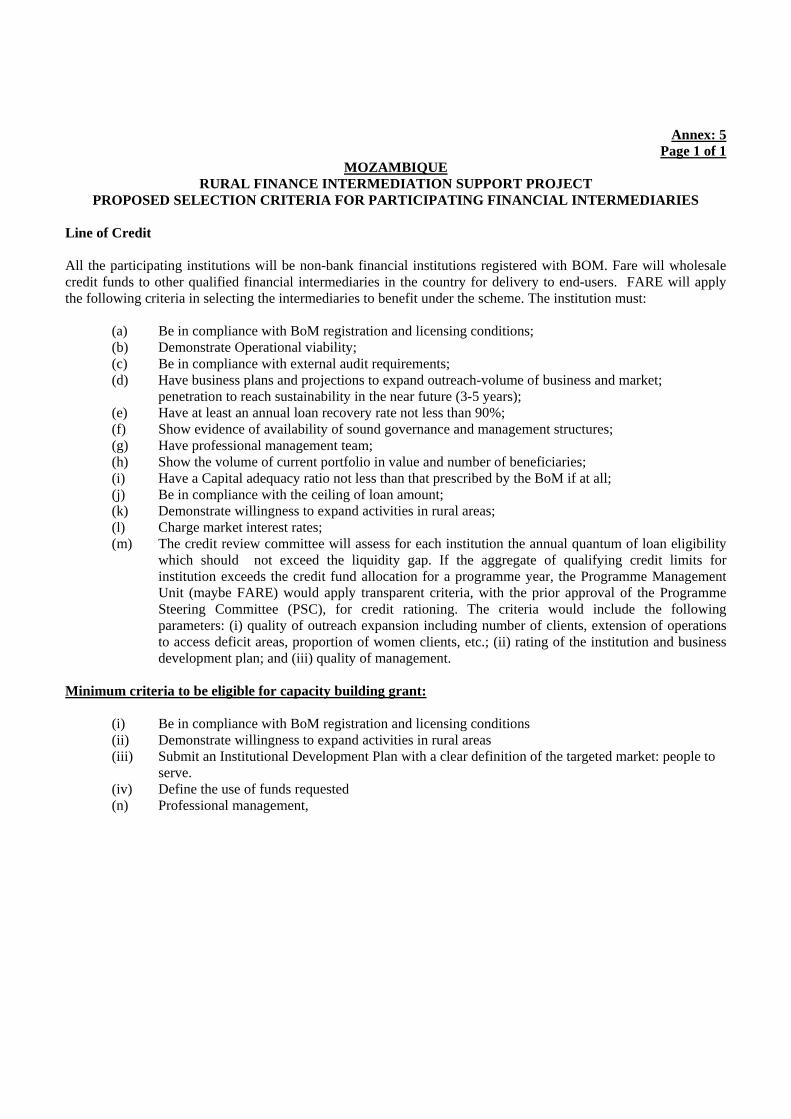

1. Map Mozambique showing Programme/Project Area 2. Brief Analysis of Key Financial Intermediaries 3. Fundo de Apoio a Reabilitacao da Economia (FARE) 4. Selection Criteria for Support to Outreach Expansion Activities 5. Selection criteria for Financial Intermediaries 6. Organisation Chart of the Programme/Project Implementation 7. Indicative ADF Project Implementation Plan 8. ADF Grant Matrix 9. Indicative List of Goods and Services 10. Bank Group Operation in Mozambique

iii

ACRONYMS AND ABBREVIATIONS ADB ADF AWPB BIM BoM CLUSA COSOP DNDR FAO FARE FFA FFHA FFPI GAPI GDP IFAD INDER MADER MBCI MFI MIC MMF MoP MPF NGO NORAD PARPA PCR PMT PROAGRI PRSP RUSP RUFISP SBAFP SME SIDA/ASD SOCREMO UNOPS USAID

African Development Bank African Development Fund Annual Work Plan and Budget Banco Internacional de Mocambique International Bank of Mozambique Bank of Mozambique Cooperative League of the United States of America Country Strategic Opportunities Paper Direcçao Nacional do Desenvolvimento (Rural National Directorate for Rural Development) Food and Agriculture Organisation of the United Nations Fundo de Apoio à Reabilitação da Economia Fundo de Fomento Agrário Fundo de Fomento da Hidráulica Agrícola Fundo de Fomento de Pequena Industria Development Fund for Small-Scale Industry Sociedade de Gastao e Financiamento para a Promocao de Pequenas Projectos de Investimentos sarl Gross Domestic Product International Fund for Agricultural Development National Institute for Rural Development Ministério de Agricultura e Desenvolvimento Rural Ministry of Agriculture and Rural Development Mocambique Banco Commercial e de Investimentos Mozambique Commercial Investment Bank Micro-finance institution Ministério da Industria e Comércio Ministry of Industry and Commerce Mozambican Microfinance Facility Ministério das Pescas Ministry of Fisheries Ministério do Plan e Finanças Ministry of Planning and Finance Non-governmental organization Norwegian Development Agency Plan for Reduction of Absolute Poverty Poupanca a Credito Rotativo rotating savings and credit Programme Management Team Agricultural Sector Public Expenditure Programme Poverty Reduction Strategy Paper Rural Finance Support Project Rural Finance Intermediation Support Project Sofala Bank Artisanal Fisheries Project Small and medium enterprise Swedish International Development Cooperation Agency Sociedade de Gastao e Financiamento para a Promocao de Pequenas Projectos de Investimentos Management and Financial Group for Promotion of Small Investment Projects United Nations Office for Project Services United States Agency for International Development

iv

v

MOZAMBIQUE: RURAL FINANCE SUPPORT PROGRAMME AND ADF PROJECT LOGFRAME MATRIX

Hierarchy of Objectives Verifiable Indicators Means of Verification Assumptions/Risks

Sector Goal: Contribute to poverty reduction.

1.1 Rural Poverty incidence and severity reduced from 70% to 50% by PY2010;

1.2 Improved household incomes;

• National income statistics; • Household income surveys; • Poverty assessment surveys

PROGRAMME/PROJECT OBJECTIVE

Programme Objectives: to improve access of rural households to financial services on a sustainable basis. ADF Project Objective: to improve access of rural households to financial services on a sustainable basis.

1.1 At least 1.6 million rural households accessing rural financial services by PY8:

1.2 120 additional RFAs established by PY6; 1.3 900 additional ASCAs established by PY8;

• Project Records; • Baseline surveys; • Impact studies; • Mid-term Review

• GoM implements programme as it is; • Rural communities are responsive to assistance

to organize them into financially viable groups/associations;

• Business climate is sufficiently dynamic to support viable financial service institutions;

• Policy and regulatory framework conducive to the development of different types of rural financial intermediaries.

1. Outreach of rural financial services expanded;

1.1 120 new RFAs established by end of PY6, 1.2 RFA membership increased from 9,000 to 27,000 by

PY 6; 1.3 MFI outreach rises from current 40,000 to over

100,000 by PY 6; 1.4 4 unions of (30 RFAs) each established by PY 6; 1.5 900 ASCAs established by PY 8 1.6 ASCAR membership rises from 4000 to over 24,000

by PY 8 1.4 Credit delivery and outreach enhanced

• Supervision Missions • Project Quarterly Progress Reports; • Reports of the contracted service providers • Mid-term Review • Impact assessment reports

• Financial Intermediaries willing to participate in the Programme;

• Continued favorable macro-economic conditions for rural and microfinance development;

• Rural communities willing to participate fully in the Programme;

• Financial intermediaries support the Programme

3. Policy and Regulatory Framework for rural finance improved;

3.1 A Rural Finance Policy Support Unit in MPF established by PY 1;

3.2 Strategic framework established and operational by PY 2;

3.3 Rural Policy Framework adopted by PY. 2 3.4 Operations Manual for MFI supervision developed

and operationalised 3.5 Self-regulatory framework for MFIs established; 3.6 65 Policy Dialogue sessions held; 3.7 29 national and regional exchange visits conducted; 3.8 8 rural finance forums held; 1.7 20 awareness building workshops

• Supervision Missions • Project Quarterly Progress Reports; • Reports of the contracted service providers • Mid-term Review • Impact assessment reports

•

viHierarchy of Objectives Verifiable Indicators Means of Verification Assumptions/Risks

PROGRAMME/PROJECT OUTPUTS

4. Line of Credit and Matching Fund Established and Operational;

4.1 Over 400,000 smallholder farmers on out grower scheme receive credit through financial intermediaries by PY8;

4.2 Over 27,000 RFAs Members receive credit by PY6; 4.3 Over 20,000 ASCAs members receive credit by PY

8;

• Supervision Missions • Project Quarterly Progress Reports; • Reports of the contracted service providers • Mid-term Review • Impact assessment reports

5. Programme/Project Management Unit Established and operating smoothly;

Establish Programme Management Unit as a precondition for loan and grant effectiveness

• Supervision Missions • Project Quarterly Progress Reports; • Reports of the contracted service providers • Mid-term Review • Impact assessment reports

Hierarchy of Objectives Verifiable Indicators Means of Verification Assumptions/Risks

PROGRAMME AND ADF PROJECT ACTIVITIES

1. Capacity Building and Institutional Development; i) Establish the Rural Finance Policy

Unit in MPF; ii) Develop a strategic Framework for

Rural Finance; iii) Develop regulatory framework for

Rural Finance; iv) Conduct Policy Dialogue; v) Training staff of MPF, FARE, MFIs

& BoM; vi) Provide Technical Assistance to

MPF, FARE and BoM; vii) Establish the MFIs Association; viii) Promote RFAs formation; ix) Promote formation of ASCAs x) Recruit Service Providers; xi) Procure vehicles & office equip; xii) Provide technical training for staff; xiii) Conduct exchange and study tours; xiv) Pay Salaries & O & M costs

Programme Cost by Component: (in Millions) i) Policy, Legislative and :UA 02.93 Institutional Support ii) Innov. and Outreach Facility :UA 11.15 iii) Support for Community-based :UA 09.00 Financial Institutions, iv) Programme Management: :UA 04.36 v) Contigencies :UA 01.71 Total : UA 29.15

• Loan Agreement; • Disbursement Records\ • Supervision Missions and Reports; • Project Accounts; • Audited Accounts for the Project; • Mid-term Review

• Continued favorable macro-economic conditions for rural and microfinance development;

• Rural communities willing to participate fully in the Programme;

2. Support to Outreach Expansion: i) Develop new products and approaches

to rural finance; ii) Disseminate new approaches to rural

finance; iii) Provide matching funds for the

Outreach expansion activities;

Programme Financing (in millions): ADF Loan : UA 11.52 ADF Grant : UA 03.84 IFAD : UA 06.66 Norwegian Fund : UA 02.63 MFIs : UA 00.90 GoM : UA 03.60

viiHierarchy of Objectives Verifiable Indicators Means of Verification Assumptions/Risks

Total : UA 29.15 3. Line of Credit

i) Provide credits to RFAs, ASCAs and other rural financial Intermediaries;

ADF Project Costs (in millions): i) Capacity Building & Instit. Dev.UA : 5.72 ii) Outreach Expansion UA: 3.00 iii) Line of Credit UA: 8.10 iv) Programme Management UA : 0.73 v) Contigencies UA : 1.10 Total UA : 18.64

4. Programme Management Unit: i) Procure vehicles; ii) Procure office equipment; iii) Conduct inception workshops; iv) Conduct mid-term review; v) Conduct studies; vi) Conduct thematic surveys; vii) Recruit local and foreign technical

support; viii) Conduct training of staff; ix) evaluate line of credit proposals; x) Conduct impact assessment

reviews and studies; xi) Conduct study on Gender in rural

finance; xii) Provide TA for the PMU

ADF Project Financing (in millions): ADF Loan UA 11.52 ADF Grant UA 03.84 Fin. Institu. UA 00.63 GoM UA 02.65 Total UA 18.64

Activities in Bold are not co-financed by ADF

viii

EXECUTIVE SUMMARY 1. Programme and ADF Project Background:

The lack of rural financial services in Mozambique is recognised as a major constraint to the commercialisation and the development of agricultural production, small-medium scale enterprises, improved market linkages, and more broadly, to the development of the rural economy. Although, there have been some scattered and at times important initiatives in the rural finance arena, these have been sporadic, and often concentrated on individual Microfinance intermediaries, or credit activities within individual agricultural, fisheries or marketing projects. These initiatives have not been developed within a comprehensible planning and policy framework. Consequently, little or no momentum has been built, initiatives have remained limited in scope, little local capacity has been created, and the institutions involved have rarely been able to attain financial viability and sustainable operations. The Proposed Rural Finance Support Programme and within it the ADF funded Rural Finance Intermediation Support Project is an outcome of a diagnostic study commissioned by the Government in July 2001, and undertaken by IFAD. 2. Purpose of ADF Loan: The ADF loan of UA 11.52 million and Grant of UA3.84 million, equivalent to 82.4% of the total project cost, will be used to finance 100% of foreign cost exchange (UA11.00 million) and 56% of local cost of (UA 4.25 million). 3. Sector Goal and ADF Project Objectives: The Sector Goal is to contribute to poverty reduction by improving the livelihoods of rural households. The ADF Project Objective is to improve the access of rural households to sustainable rural financial services. 4. Brief Description of the ADF-Project Outputs: The ADF Project will support activities under four major components: (A) Capacity Building and Institutional Development; (B) Support to Outreach Expansion (C) Line of Credit; and (D) Project Management. 5. ADF-Project Cost: The total ADF project cost is estimated at UA 18.64 million of which (11.11 million (60%) will be in foreign currency and UA 7.53 million (40%) will be in local currency. 6. Sources of Finance: The Project will be financed by the African Development Fund, the Participating Financial Institutions and the Government of Mozambique. The ADF Grant of UA 3.84 million will finance the Capacity Building and Institutional Development component, while the Loan of UA 11.52 million will finance the Line of Credit and Matching Fund. A matrix of the measurable indicators of the activities funded by the grant is attached as annex 8. 7. ADF-Project Implementation: The Project will be implemented over a six-year period. The Ministry of Planning and Finance (MPF) will be the executing agency. The day-to-day management and coordination will be under a Programme Management Unit to be established within the Fundo de Apoio à Reabilitação da Economia (FARE). FARE was established by the Government under Decree 20/92 in 1992, within the Ministry of Finance as a vehicle for implementing Government programs for economic rehabilitation and poverty alleviation in most deprived communities. 8. Conclusions: The Programme and the ADF Project are consistent with the Bank Group overall strategy and Vision for the promotion of rural and micro finance systems. It is also within the national strategies and policy direction of the GoM of extending affordable and sustainable financial services to rural areas to support economic growth and poverty reduction.

1

1. ORIGIN AND HISTORY OF THE PROGRAMME 1.1 Mozambique is ranked as one of the world’s poorest countries, 170 out of 173 countries on the Human Development Index (UNDP 2002). Some 70% of the population is estimated to live below the poverty line, in a country, rich in under-exploited resources. 80% of the 18.3 million population is found in rural areas. The country’s Plan for Reduction of Absolute Poverty (PARPA) states that the Government shall promote rural development to guarantee the needs of the majority of the population, and the social and economic progress of the country. The agricultural sector, including forestry and fishing is the major source of employment and income generation to the vast majority of the rural population. The lack of rural financial services is recognised as a major constraint to the commercialisation and the development of agricultural production, small-medium scale enterprises, improved market linkages, and more broadly, to the development of the rural economy. 1.2 In July 2002, the Government of Mozambique (GoM) requested IFAD to undertake an inventory study to review rural finance policies, activities and institutions, assess past and present donor/NGO interventions, and analyse challenges and constraints facing the rural finance sub-sector. The study was to assess the experiences of financial intermediaries and other institutions active in the sub-sector, the potential demand for financial services, and the capacity of these institutions to respond to the demand. The study and subsequent stakeholder consultations, highly recommended that in order to move forward, the Government had to take the lead, in providing a conducive policy and regulatory environment within which the rural finance system could be developed. The study also recommended that new opportunities and mechanisms to promote the development and expansion of rural finance be explored. 1.3 IFAD was requested to formulate a programme along the lines recommended by the study, and the mission to formulate a “Rural Finance Support Programme” (RUFSP) was undertaken in September 2002. An official request for the Bank to co-finance the Programme with IFAD and NORAD was received on 29th April 2003. Consequently, Bank Group missions to prepare and appraise the ADF funding within the Programme, under the title of “Rural Finance Intermediation Support Project” (RUFISP) were undertaken in May and August 2003, respectively. During the missions and the subsequent CSP-preparation and dialogue missions, the GoM has reiterated its desire and commitment in supporting the development of a sustainable and affordable rural finance system. The Rural Finance Intermediation Support Project encompasses the activities of the Programme to be funded by ADF. 1.4 The proposed Programme is an outcome of extensive stakeholders consultations conducted by the IFAD conception and formulation missions, through a series of workshops. Subsequent consultations were held by Bank Group missions during the preparation and appraisal of the ADF-Project, with the concerned ministries, departments and agencies of the GoM, the banking sector, micro-finance operators (MFIs), Non-governmental organisation (NGOs), farmers and traders associations, credit unions/associations, as well as, various donor representatives in Mozambique. The ADF Project follows the Operational Guidelines for the Rural Financial Sub-sector approved by the ADF Board of Directors, in 2002. The intervention is in line with the Bank Group Strategy for support to agricultural and rural development and the Vision Statement, which emphasises the expansion of the scope of the Bank’s development assistance in rural finance beyond the traditional lines of credit associated with directed credit, to programmes which reinforce best practice financial intermediation, and which promote poverty reduction.

2

2. AGRICULTURE AND RURAL DEVELOPMENT 2.1 Salient Features 2.1.1 Mozambique has one of the best natural agricultural production potentials in Africa. The agricultural sector, including fishing and forestry, remains the mainstay of the Mozambican economy although its importance has declined in recent years mainly due to natural calamities and increased dynamism of other sectors. The sector’s contribution to GDP fell from 30.2 percent in 1998 to 23.5 percent in 2002. It is estimated that it generates about 80 percent of the country's export earnings, and provides employment to 78 percent of the economically active population. Of the country’s total land area of 78.6 million ha, about 46 percent (36 million ha) is considered suitable for cultivation. However, only about 10 percent of this arable land is currently cultivated. Smallholders comprise some 3 to 3.5 million households that cultivate on average 1.8 ha each and account for 95% of the cultivated area, while commercial farms account for the rest. Use of aagricultural input by smallholders is almost exclusively for cotton and tobacco production (under the direction of commercial companies), or vegetable and fruit production in the “Green Zones” surrounding the larger urban areas. 2.1.2 The policy environment within the agricultural sector has substantially improved since the Government embarked on its structural adjustment programme. In addition to divesting state farm holdings and distributing state farmland to smallholders and private enterprises, all agricultural commodity prices were decontrolled and marketing of agricultural commodities was liberalized by 1995. The liberalized environment in the crop farming, livestock rearing and forestry sub-sectors has significantly increased the opportunities for profitable activity in these areas. However, the smallholder farmer cooperatives need to be assisted with inputs, training, micro-credit facilities, and marketing infrastructure for them to fully exploit the opportunities created by the liberalized environment. The lack of credit has contributed to the inability of rural households to adopt improved production technologies, diversify their income base and to better cope with external shocks such as droughts, floods and illness. 2.2 Poverty and Food Security 2.2.1 Poverty in Mozambique is extensive, with about 70% of the total 18 million population, and 62% of the urban residents living in absolute poverty. While poverty is widespread throughout the country, it is more severe in rural areas, where almost 71% of people live in poverty. Poverty analysis shows that the main determinants of poverty in Mozambique, are: (i) slow growth of the economy until the beginning of the 1990s; (ii) low levels of education of working age household members, particularly women; (iii) high dependency rates in households; (iv) low productivity in the family agriculture sector; (v) lack of employment opportunities within and outside of the agricultural sector; and (vi) poor infrastructure, especially in rural areas related to agriculture. Moreover, since the vast majority of people are employed in agriculture, poverty in Mozambique is exacerbated by several factors mainly: the isolation and poor market integration of rural households, inadequate financing, the weak coverage of basic services, training, inadequate inputs and appropriate technology, as well as the continuous threat of natural disasters such as drought and floods. Due to this, a large number of the population depend on remittances from migrant workers, and other agriculture related products such as firewood and charcoal production, petty trade and occasional off-farm employment. 2.2.2 The first major poverty reduction policy called the Strategy for Poverty Reduction in Mozambique was drafted in 1995. A major weakness of the strategy was that it did not propose specific actions in terms of target groups, goals, and mechanisms for coordination and collaboration of the different social actors in the fight against poverty. In response, the country’s Council of Ministers

3

approved in 1999 the Action Guidelines for the Eradication of Absolute Poverty, from which evolved the Plan for Reduction of Absolute Poverty (PARPA) as a means of operationalizing the Guidelines. PARPA, which constitutes Mozambique’s PRSP, has become a key government-planning instrument. It provides a medium and long-term planning tool for promoting a focus on poverty reduction in the allocation of public resources and is the policy framework within which the other initiatives are addressed. Basically, the PARPA reflects the objectives contemplated in the different national and sectoral strategic plans. It aims to reduce absolute poverty from 70% in 1997 to less than 50% by 2010. 2.2.3 The Government’s Food Security Strategy was approved by the Council of Ministers in December 1998. The Strategy envisages the implementation of policy measures that ensures greater stability in family resources through (i) increased output, (ii) diversification of subsistence crops, (iii) expansion and diversification of income generation opportunities through agricultural and non-agricultural activities, and (iv) better knowledge of food production and conservation technologies. The Strategy emphasize the importance of economic growth and the development of human capital as fundamental pillars in the process. It specifically mentions the need to: (i) create a marketing network able to provide the necessary productive inputs and to guarantee that agricultural surpluses are bought; (ii) create a rural financial system capable of supporting production activities and marketing by small and medium farmers and traders; (iii) promote access to capital by small and medium traders in order to stimulate marketing and competition; and (iv) promote nutrition education on healthy eating habits, as the core activities aimed at ensuring food security. 2.3 Land Tenure

Under the country’s land tenure system, ownership of all land is vested in the State. However, to protect the ownership rights of the family sub-sector, the Government passed the Land Law in 1996, asserting the customary tenure system and requiring that outsiders who wish to obtain land use rights must negotiate with the customary occupants and their communities. Land tenure patterns are broadly similar throughout the country, although customary practices in the different localities may differ. Land is accessed through inheritance, traditional village authorities, government programmes and by borrowing it. Secure land access documents are rare and costly to obtain, although the Land Law (Lei de Terra - Lei 19/97) recognizes traditional and squatter rights to land. The constitution also makes it obligatory to consult local communities when processing land titles. Land for smallholder needs is not a constraint in most areas. Many areas of the country are lightly populated, while two out of the 10 provinces (Nampula and Zambezia) contain 40% of the population. Generally, Mozambique has abundant land though land pressure is becoming an issue in some areas along the coast, in peri-urban areas and along major transport corridors. Women’s rights to land are guaranteed under the constitution and inheritance is recognized with no gender distinction, with the constitution in this regard taking precedence over customary norms. However, in practice, female rights are often unrecognised under customary law. The constitutional legal protection is insufficient, and there is need for it to be accompanied by regulatory enforcement mechanism. The Law equally calls for community participation in the conservation of natural resources, the resolution of conflicts over and the identification of the limits to the land they occupy. 2.4 Policies and Strategies 2.4.1 The Government with the assistance of the donor community is currently in the process of formulating its Rural Development Strategy (RDS). The underlying philosophy of the process is to ensure (i) wide participation of all stakeholder - public and private – that will be impacted by the RDS; and (ii) full government ownership throughout the process. It is expected that the strategy would be ready by December 2004. The strategy is expected to provide an umbrella for all sectoral development

4

programmes and strategies in the rural areas. The strategy recognizes that the reliance on markets and prices to allocate most types of goods and services leads to more efficient outcomes than the use of Government’s regulations and enforcement agencies. This move towards a market-based economy has allowed the Government to focus more sharply on more essential roles in the development process such as: (i) the establishment of an enabling policy environment to promote production and efficiency; (ii) the provision, directly or through contracting, of public goods (research, extension, infrastructure, social. 2.4.2 The main tenets of the Government’s strategy for the development of the rural sector is based on private sector development and ensuring the conservation of the country’s natural resource base. The principal vehicle for the implementation of the Government’s strategy for the development of the agricultural sector, the dominant sector in the rural economy, is embodied in the National Programme for Agrarian Development (PROAGRI) initiative. This multi-donor agricultural investment programme, aims to: (i) raise the productive capacity and productivity of agriculture, forestry and animal husbandry in the family sector using labour-intensive technologies, and sustainable management of natural resources; (ii) guarantee rights of access to land and reduce the bureaucracy associated with land registration; (iii) promote the marketing of agricultural and livestock products, and facilitate the marketing of surpluses and access to markets (for factors of production as well as credit); and (iv) reduce the vulnerability of households and chronic food insecurity. PROAGRI is approaching the end of Phase 1. MADER is currently in the process of defining the programme for a second phase that is scheduled to start in 2005. The first phase concentrated primarily on reorganization, rationalization and capacity building of MADER. A second phase is under formulation to run from 2005-2010. The scope is still being discussed but it is thought likely to principally focus on agricultural production enhancing investments. 3. FINANCIAL SECTOR 3.1 Salient Features

Currently, the financial system consists of banking and non-banking intermediaries, including: 10 commercial banks, 1 investment bank, 1 microfinance bank, 3 leasing companies, 3 credit cooperatives, 2 venture capital companies, 16 microfinance institutions, 1 Bulk Purchase Management Company, 5 insurance companies, a Social Insurance Fund, 6 Government Development Funds and 30 exchange bureaus. The Bank of Mozambique (BoM), which is the Central Bank was established in May 1975, and has the responsibility of setting the supervisory and regulatory framework for delivery of financial services. Its main function is to preserve the national currency value, orientate the credit policy, discipline-banking activities, and act as a Government counsellor in financial maters. The financial system is dominated by commercial banks. While the number of commercial banks has increased in recent years, the volume of their business is still small. In June 2001, the total deposits in the banking system were approximately USD 850 million, representing 22% of GDP. The Banking sector is highly concentrated, with the market leader, Banco Internacional de Mocambique (BIM), accounting for 44% of total banking assets and 40% of total branches. Ccommercial banks operate almost solely in the larger urban centers, with most of their activities concentrated around Maputo. Rural areas are characterised by lack of financial services, which would typically be provided by commercial banks.

5

3.1 Policies and Regulatory Framework 3.1.1 The financial system in Mozambique is regulated by the banking law No.15/1999 which defines the types of institutions that are allowed to conduct financial sector operations and the requirements for registration under each institutional category, as well as the supervisory role of BoM. Under the 1992 reforms of the financial sector, the BoM’s three main functions (central bank, money issuing bank and commercial bank) were separated, with BoM keeping only its central bank and money issuing functions. This created an opening for the entrance of new private, public and non-governmental operators in the financial sector, while at the same time reinforcing BoM’s mandate and ability to regulate and supervise financial sector operations. As a policy incentive to promote the establishment of financial services in rural areas, under Banking Decree 47/1998, credit institutions operating in areas out of Maputo are allowed a reduced equity capital requirement of MZM 25 billion (approximately USD 1 million) instead of the usual USD3.00 million. There is no clear evidence yet of any impact derived from this incentive. 3.1.2 The financial institutions registered under decree 47/98 and amendment 1/GGBM/1999, include the micro-finance institutions. These institutions are not allowed by law to mobilise savings/collect deposits, although they do provide credit to their clients. This does not contribute to the promotion of savings, which is a basic condition for development, and also reduces the potential viability of these institutions. While these institutions report semi-annually to the Supervision Department of BoM, their operations are not yet supervised by it. Recognizing this constraint, a group comprising MADER, the Mozambican Microfinance Facility (MMF) and some MFIs has elaborated a draft of a ‘Microbank Bill’ that was presented to BoM management in May 2002. According to this draft, the minimum capital requirement for deposit-taking MFIs would become approximately USD 0.5 million and registered MFIs would be able to operate savings accounts, collect cheques but not operate current accounts. It is also expected that under the proposed new Banking Law, which provides a framework for rationalizing the existing decrees and the strengthening the mandate of BoM to supervise the financial sector, the question of provision of rural financial services will be revisited. The BoM has recently established a Task Force under the Supervision Department to focus on micro and rural finance, which is an indication of increased interest by the bank in the development of these issues. 3.1.3 Currently, the Government does not have a focal point for the development of rural finance. In 1999, the GoM mandated the National Institute for Rural Development (INDER), a multi-sectoral rural development organisation, to act as a focal point. INDER has since been closed as an independent institution and its functions, including rural finance and microfinance market development, became a part of the National Directorate of Rural Development (DNDR) of MADER. During its two years as focal point for the development of rural finance, DNDR has focused solely on the microfinance sector. Its programmes for microfinance development, include the MicroStart and Upstream projects funded by UNDP, CIDA, the Bank Group (AMINA-Project) and others. As DNDR focus is on microfinance development, this leaves a gap in the policy development for rural finance. Since rural finance issues cut across various sectors, there is need to identify a neutral institution, which can coordinate its development across all sectors. The BoM prefers to focus on regulatory and supervisory tasks and avoids any lead role or even active participation in the promotion of the rural finance. The Ministry of Planning and Finance which has oversight over all government ministries and agencies, has been found the most ideal to direct the development of rural finance policies and strategy.

6

3.3 Savings Mobilisation and Outreach 3.3.1 Savings: Savings mobilisation from the public by Mozambican financial intermediaries is poorly developed in the urban, peri-urban and particularly in the rural areas. The range of savings instruments available in commercial banks is restricted to a small segment of the population and almost totally absent in rural areas. The minimum capital required to open a savings account in a commercial bank is MZM 5 million, or USD 208, which is a very high figure in a country with a per capita GDP of USD 250 and a minimum monthly wage of US 25. Consequently, most people have no dealings with banks, neither as borrowers or savers. Only 1.8 million Mozambican had a bank account at the end of 2002 (or 10% of total population). Financial institutions registered under decree 47/98 and amendment 1/GGBM/1999, including micro-finance institutions are still not allowed by law to mobilise savings/collect deposits. The low level of savings in Mozambique (4% of GDP) acts as a brake on the development of the economy (and source of continued dependency on external development assistance). Raising the rate of domestic resource mobilisation is a one of the major economic challenges facing the country and will be addressed within the Proposed Programme. There is need to review policies which affect as experience from the northern part of Mozambique clearly indicate that even poor households are willing to hold savings deposits if given the opportunity, positive incentives and high quality services accessible to the villages. Furthermore, the demand for financial services in rural areas will grow, if, through regular savings, small consumption and production loans can be obtained. 3.3.2 Credit: Commercial banks operate almost solely in the larger urban centers, with most of their activities concentrated around Maputo. Commercial banks are not inclined to service low-income business or households. Due to the high lending interest rates charged on loans in local currency in Mozambique, a high proportion of credit in banking portfolios is in foreign currency (49% of outstanding loans). Although commercial banks in Mozambique are extremely liquid, their share of total loans to total deposits in the sector has been at a very low level, fluctuating between 50% and 52%. The active domestic borrowing by the Government has provided an easy outlet for the banks for short investments at high interest rates and practically no risk. Consequently, banks have invested less in their portfolios and the overall availability of bank credit in the country has been very limited. Further, even when the inflation has declined to single digit figures, the interest rates on bank loans have remained high. In May 2003, the average cost of mobilising funds in the commercial bank sector was estimated to be 7%-10%, while the lending rates fluctuated between 30% and 42%. 3.3.3 At the end of 2001, loans to agriculture were only 17% of the total commercial banks’ portfolio, having declined from 22% in 1999. The particular feature is that, all loans to the rural sectors were to large-scale producers, large traders and processors. Of the agricultural loans, some 80% were allocated to the large companies in the cotton, sisal and sugar industries. Thus, while lending to sectors outside commerce is in general very limited in Mozambique, loans to rural areas are few and in practice always target large corporate borrowers. 3.4 Rural Finance Sub-sector 3.3.4 Overview: Whilst progress has been made in liberalizing and transforming the Mozambican financial sector, substantial deficiencies still remain as the financial system does little to address the needs of the poor, and their financing needs remain largely unmet. The privatisation of the banking industry and increased foreign ownership, has instead, resulted in a decrease in the number of rural agencies and branches from 290 in 1997 to 201 in 2002. The geographical location of bank branches has also changed, as new ones have tended to be established in urban areas while the ones closed were mostly those in rural areas. The outreach of existing financial services in rural areas is therefore very

7

limited in terms of product diversity and in reaching low-income households. The microfinance industry, while showing impressive growth in recent years, is still small and almost totally urban in its orientation. To fill the vacuum created by the absence of the commercial banks, attempts have been made to expand basic financial services to rural areas through government development funds and specialised credit institutions. While some progress has been achieved through these arrangements, the volume of operations has generally been small and the sustainability of activities has depended on continuous donor support.

Rural Finance Institutions 3.4.1 The key institutions providing financial services or with the potential to provide financial services to rural households are: Commercial Banks; MFIs; Registered Special Credit Institutions; State Owned Development Funds (Fundos); Credit Cooperatives; Non-Financial Rural Credit Service Providers; Community-based Financial Institutions. These institutions are supported at the policy level by the Bank of Mozambique; and the Ministry of Planning and Finance. A brief review of each of this category of institutions, strengths and weaknesses is given below. 3.4.2 Commercial Banks: The core issue concerning commercial banks in the design of any rural finance support programme is that they have very little linkages with the rural economy, in general, and with small and medium-scale agriculture, in particular. No rural district in Mozambique has commercial banking facilities. Of the 227 commercial bank branches, 103 are in Maputo city and nearly all the rest are in provincial capitals. 3.4.3 Microfinance Institutions: Given the preference by formal banking system to concentrate their efforts on a limited (mainly urban and corporate) clientele, MFIs have a potentially important role of serving the majority of the population, particularly in rural areas, with financial services. The microfinance sector in Mozambique consists of some 50 organizations providing credit services as their main activity of which 29 are registered with the BoM. Most of the credit institutions are NGO-based associations and the larger ones are often linked to and supported by a foreign parent organisation. The sector includes also seven (7) small institutions registered as Credit Co-operatives, four of which are functional and serve a predominantly urban clientele. Because of the size and type of their operations, also two formal sector operators, Novobanco and SOCREMO are sometimes considered as part of the microfinance sector. The microfinance activities in the country are currently very small. While the client numbers have more than doubled in the past two years, the whole sector still serves only some 40 000 clients. The total portfolio of the microfinance sector is also very low, approximately USD 4 million. The microfinance industry, while showing impressive growth in recent years, is small and almost totally urban in its orientation. Factors adversely affecting the viability of MFI operations in rural areas include: the high operational costs associated with long distances, poor infrastructure, often low population densities, high cost and lack of skilled personnel and the limited level of monetization in rural areas. Their lack of experience with agriculture and other rural based systems further complicates the problem. There is need to build the capacity and provide necessary incentives to MFIs to extend financial services to rural areas. 3.4.4 Registered Special Credit Institution: In the absence of commercial banks or mature MFIs operating in rural areas, donors have promoted special credit institutions as the option for providing credit to rural areas. These institutions operate under a no deposit taking licence and a minimum required capital of approximately USD 1 million. Most are dependent on donor funding but have plans to organise themselves as more independent financial operators. The four dominant development credit institutions are: (i) Sociedade de Gastao e Financiamento para a Promocao de Pequenas Projectos de Investimentos, SARL (GAPI), (ii) Asociation Monzabiquan para o’Desenvol Vimento Rural

8

(AMODER), (iii) Fundo de Fomento a Pequana Industria (FFPI), and (iv) Sociedade de Crédito de Moçambique, SARL (SOCREMO). Two of them, GAPI and SOCREMO, are registered as credit institutions (minimum share capital USD 1 million), AMODER is an association with a basic microfinance license and FFPI is a state-owned development fund which is in the process of being registered as a formal credit institution. As these institutions are expected to play a key role in the delivery of financial services to rural households under the Programme, they have been analysed in more detail in annex: 2. 3.4.5 While the Special Credit Institutions provide a rare link to the rural population, their coverage and operations still remains small. Due to the current regulations, none of them operates a formal savings facility for their customers, which is a serious obstacle for effective financial intermediation and sustainability. Furthermore, as they have often been the only channels to reach the rural communities with credit, donors have heavily supported their operations and outreach. Although their human resources and institutional capacity to respond to the donors and client demands for fast growth have been limited, there is a positive sign that serious efforts are currently being made to streamline their operations and to prepare appropriate strategic plans for their balanced growth. 3.4.6 The State Owned Development Funds (Fundos): Populary known as Fundos, these are typically Mozambican instruments to support economic development. Fundos operating in Mozambique include: i) Fundo de Fomento Agrário (FFA), ii) Fundo de Fomento da Hidráulica Agrícola (FFHA), iii) Gabinete de Promoção de Emprego (GPE), iv) Gabinete de Promoção de Pequenas Empresas (GPPE), v) Fundo de Apoio à Reabilitação da Economia (FARE) and vi) Fundo Fomento Pesqueiro (FFP). The Fundos have been engaged in various kinds of development activities in their respective sectors, including wholesaling and retailing credit operations. In recent years, most of the Fundos have received very limited funding, coming mostly from government (mainly ministry reflows from levies and taxes collected) and some from donor sources. The technical and financial capacity of the fundos in credit management has been limited, which has adversely affected credit assessment and recovery. The most serious handicap for effective credit operations by the fundos is related to their image as government development institutions. The perception by recipients of loans managed by these institutions as Government grants, has had adverse effect on loan recovery. This is because they often offer from the same ‘window’ various types of grant-based extension and promotion services, as well as loans. The Government has initiated a study into the operations of the existing Fundos, which has recommended that they should not in future engage in retailing of credit. The most important of these is FARE, which was established in 1992 by the Ministry of Planning and Finance to channel funds raised from the privatisation of public institutions to rural based small and medium enterprises. FARE has been designated by the Government to manage the proposed Programme. More detailed analysis of FARE is given in annex 3. 3.4.7 Credit Cooperatives: These are member-based institutions with a minimum capital of USD 8,000 and the right to collect savings only from their members. The current credit cooperatives include i) Tchuma (a microcredit cooperative), ii) the Caixa Comunitária dos Micro-empresários de Ulongué iii) Cooperativa de Crédito para o Desenvolvimento Rural, iv) Cooperativa de Poupança e Crédito(CPC) all falling under the General Union of Cooperatives (UGC). UGC was formed by the agricultural co-operative of Maputo in the 80’s as a service co-operative and support structure. More details of UGC are given in annex 2 of the report. The UGC has implemented credit components within Bank funded projects in the past including the Family Income Enhancement Project. UGC is a viable intermediary for channelling rural support under the proposed Programme.

9

3.4.8 Non-Financial Rural Credit Service Providers: An important feature of Mozambican rural landscape is the presence of large commercial outgrowing/agro-processing operations mainly in the cotton and cashew nut. These are run by local enterprises often affiliated with international companies and in a number of cases in joint ventures with government. They are by far the biggest providers of agricultural credit, through the agricultural inputs that they make available to the outgrowers on a credit basis. Some 400,000 smallholder families work on these schemes, representing about 12% of the rural population. Usually the outgrower companies link loans to the obligation of selling the produce to them as a guarantee. Examples include cotton ginneries and tobacco processors. There is no reliable data on the amounts of in-kind credit these companies annually give to their outgrowers. Farmers receive credits in kind ranging between MZM 1.5 –2.0 million per acre on the tobacco and cashew outgrower schemes. Assuming an average of one acre each and an average of MZM 1.75 million (UA72) each, this would amount to approximately UA 29.00 million in a single season. It is understood that most of the funds of the large foreign-controlled agricultural companies come from abroad, as credit from the local banking sector tends to be costly. As a pilot initiative, the development finance company GAPI has entered into an arrangement with Agrimo one of the larger agricultural companies, to provide seasonal loans to its outgrowers. The potential of linking the outgrower schemes with local financial intermediaries is high. Sales by large and medium traders of materials on credit to customers and smaller traders is also another type of credit transaction made by non-financial service providers in rural areas. 3.4.9 Informal Community-based Financial Institutions and other Sources of Credit: Due to the limited outreach of the formal financial intermediaries especially in rural areas, the majority of the Mozambican population has to resort to traditional informal systems for their savings and credit requirements. The most common sources of credit are friends, neighbours and relatives. The most common type of informal savings and credit arrangement in Mozambique is the xitique. These are simple rotating savings and credit groups in which all members contribute on a daily, weekly or monthly basis and one member traditionally receives the whole collected amount. These groups are easy to operate, as there is little financial management involved. As savings are collected and the ‘loans’ issued in the same meeting, transaction costs are low in amount and time. 3.4.10 These informal community based savings and credit systems, have provided the inspiration and basis for a number of NGO-supported savings and credit initiatives. The most important of these are the CARE-supported Poupanças e Crédito Rotativo (PCRs) and the Insitut de Recherche et d’application des methodes de Develloppement (IRAM) supported Caixa Comunitária de Crédito e Poupança (CCCPs) commonly known as community-based Rural Finance Associations (RFAs). Both started operations at about the same time, in 1997/8 and both have developed sound models for creation of savings systems at the community level, linked to the provision of credit. These are self-managed and self-sustaining operations with simple management procedures and suited to rural communities. They focus on low-income communities and have high involvement of women as a key target group. The approach is particularly adapted to even remotest rural communities. 3.4.11 Total RFA membership in December 2002 was 9 500 members, of which 6 000 were active members of 55 RFAs. The associations are registered as legal bodies under the Law 49/98 regulating associations. The associations have the capacity to manage the deposit and credit activity of members. RFAs have up to 500 members-with an average of 92 members in Cabo Delgado (given that most associations are young) and 250 in Maputo. The strengths of this methodology is that it relies on local management, decreasing the need for long-term external assistance. Evidence suggests that this methodology has a much lower turnover of clients than experienced in MFIs. Little to no fraud occurs in the RFAs, as association members are less likely to steal from fellow community members. RFAs are formally structured, they have elected management and fiscal committees and are registered as

10

legal bodies. They have been established through NGO assistance, which provides management and auditing assistance during their establishment. It has also been found that the promotion of RFAs in densely populated regions is easier than in scarcely populated ones. Development of such associations in more dispersed areas may require smaller groups. 3.4.12 RFA members receive credit by organising themselves in small solidarity groups of five members, with all members of the group receiving loans at the same time. Loans are for trade and agriculture and start as small as MZM 500.000 (USD 20) and interest ranges from 3% to 4.5% per month. Repayment rates are high and good RFAs manage to attain financial self-sufficiency within two years. The goal is to join the individual community associations into unions (15-20 RFAs per union), which may be registered as a cooperative in the future. The strengths of this approach is that it is based totally on local management. Subsidies for technical support are gradually phased out so that the RFAs are progressively paying the full cost. Loan sizes are small and thus accessible by most smallholders and available for highly demanded activities. While not formally promoting savings, the loan guarantee that the RFAs require from its members develops the savings culture. The RFAs are currently in Maputo, Gaza and Cabo Delgado Provinces. The fact that the approach is fully tested and has already been adopted successfully in various rural environments in Mozambique would facilitate its implementation under the Programme and extension to new areas. It is expected that the RFAs will organise themselves into unions comprising of 20-30 RFAs each. The Bank of Mozambique is working on a plan to establish an Umbrella Apex body for RFAs unions, within the next two years. 3.5 Gender and Rural Finance Women in Mozambique constitute a little over 50% of the population. Over 95% of women work in mainly rural subsistence agriculture compared to 66% of men. About 70% of the women are illiterate as compared to 40% of the men. Overall, it is estimated that in Mozambique MFIs have successfully reached about 60% women clients. However, there is a clear regional difference in involvement of women in entrepreneurial activities. Women in the South are considered generally to be more active in income generation and trading activities as opposed to the women of the North who are still constrained in engaging in entrepreneurial activities. It is estimated that in the North, MFIs outreach to women clients is only 14%. Furthermore, rural women engage in informal sector activities and have very little access to formal credit, skills or business training. The National Directorate for Women’s Affairs (NDWA) under the Ministry of Women and Social Action Coordination Affairs has the overall mandate of gender mainstreaming in the country and of coordinating between the different line ministries as well as the provincial and district level gender officers. 3.6 Health and HIV/AIDS

It is currently estimated that the coverage rate of health service stands at around 50% in the country. The most important causes of morbidity and mortality continue to be the transmittable diseases such as malaria, parasites, tuberculosis, acute respiratory infections, and diarrhea etc. The HIV/AIDS pandemic, (which is a risk factor for economic growth and national survival in the long term), is rapidly expanding and constitutes an enormous challenge to a health system already overburdened. In 2001 the estimated number of adults living with HIV/AIDS in the country was about 13%, of which women account for 62%, and children account for about 7%. Moreover an estimated 420,000 children are currently living as orphans (lost mother or father or both to AIDS). In Maputo the HIV prevalence among antenatal clinic attendees increased from less than 1% in 1988 to 13.2% in 2000. Overall, the Primary Health Care strategy identifies some of the high health-risk groups as: those

11

women of childbearing age, children, the population of rural areas, and those who live in absolute poverty. The supply of clean drinking water and sanitation is also a basic factor in improving the health and quality of life of the population. 3.7 Potential Demand and Constraints of Rural Finance 3.7.1 Potential Demand: Most of the demand in the rural areas tends to be latent in an underdeveloped environment, with low level of monetisation and very limited access to financial services. As most financial intermediaries have none or very limited operations in rural areas, it is not easy to estimate the demand for rural finance services in monetary terms. It is however, necessary to understand the nature of the demand and the types of services demanded, and likely to be demanded as development of rural areas progresses. It should also be noted that demand for financial services in rural areas is multi-facetted in nature, and to support rural development through economic growth, there will be a need for a wide range and mix of financial services to be provided, of which, credit is only one element of the mix. Effective demand for credit depends on the prices and conditions of supply for the different market segments. Three main types of loans can be distinguished in the case of Mozambique according to their utilisation: (i) consumption credit to finance basic needs in terms of food products and social expenses (school fees, marriages, health care, etc.) that is usually short-term, from 2-3 months to a maximum of 6-8 months; (ii) credit for working capital that is also short-term (6-8 months up to a maximum of 12 months) needed each year to finance agricultural activities (fertilisers, pesticides, and labour for land preparation, planting, weeding and harvesting) and for other economic activities including agro-processing and trading; and (iii) credit for investment, needed for capital equipment for an economic activity that is by nature reimbursed over some years, depending on the type of activity and the overall amount of investment. To mitigate the needs of rural households holistically the rural finance system will have to provide a mix of these credit requirements for the rural population. 3.7.2 The potential demand for financial services among the 3.5 million smallholder households, is enormous, particularly if the target is to move them towards higher levels of production technology, higher crop yields, and diversification to off farm income generating activities. There is a large incentive for credit funds amongst the 400,000-smallholder families, representing about 12% of the rural population, who receive credit in kind from agro-processing/exporting companies as part of contract farming agreements in Mozambique. The potential demand from fisher folks for access to investment is high, whether it be for purchasing or repairing boats or acquiring fishing gear. Artisanal fisheries in Mozambique involves some 11,000 vessels and a great diversity of fishing gear employing more than 90 000 people directly, excluding those involved in processing and trading. The involvement of private sector and communities in the development of small and medium scale forest industry, through microfinance, does constitute an opportunity for employment in both rural and urban poverty alleviation. To-date, like smallholder farmers, few fishers have access to credit and other financial services to allow them to improve the return to their effort and thus improve their incomes. As marketing opportunities increase through the development of infrastructure and market networks, the viability of investments in technology and advanced inputs improves and the bankable demand for smallholder farmers and small-scale fishing loans will increase. 3.7.3 Reports indicate that there has been a dramatic increase in the number of activities in the markets and street vendors in and around the provincial capitals, peri-urban areas and rural towns. Trade is probably the most dynamic and rapidly growing economic activity in rural Mozambique. A large number of Mozambicans rely on income generated from micro entrepreneurial activities in the informal sector for their livelihoods. Of the total workforce in urban and peri-urban areas, about 90% are employed in the informal sector, half of whom are women. With small amounts of working capital

12

(between 2.5-10 million MZM, or USD 100-400, but in some cases even less, the traders circulate funds and goods as fast as possible with very short buy-sell cycles. Because of the small loan amounts required, their inability to provide collateral and the informal nature of their businesses, these operators have no access to credit, neither from commercial banks nor from other financial intermediaries serving rural areas. 3.7.4 Studies conducted by FAO have found that small-scale farmers, lacking storage and financial capacity, are forced to sell much of their produce at the beginning of the marketing season when prices are lowest. Consequently, farmers are unable to maximise profits from their crop production. A feasibility study undertaken by FAO (1999), includes a proposal requiring external financing of USD 1 million to benefit 300 associations and 50 000 people over a three-year period. GAPI or AMODER have both been experimenting with inventory credit systems. Initial results show success and there is potential of expanding this scheme once the issues of warehousing have been overcome. 3.7.5 Based on the projected growth of the MFIs, they are expected to reach 60,000 clients by end of 2006. In addition, the Programme will service a total of 17,500 members from the over 900 ASCA’s to be promoted and 24,000 members from the total of 175 RFAs. Assuming average loan size per borrower of US$150 within an average duration of a year, the total need for credit to service the 101,500 clients will be about US$15,225,000. Estimate of the resource gap has also been made by a number of Special Registered Credit Institutions visited by the mission including: (i) UGC which has projected a resource gap of US$2,700,000 over a 5 years-period to service its networks of poultry cooperatives comprising 39,000 clients; (ii) FFPI is seeking a credit line of US$2,200,000 to provide credit to micro, small and medium enterprises in Mozambique over a period of 5 years. (iii) GAPI is expecting an increase of its loan portfolio by 40% representing an amount of US$1,600,000 to add to its current loan fund of US$4,200,000. The estimated resource requirement for the three institutions over the next five years is estimated at US$6,500,000. A conservative estimate of resource gap of UA 17.51 million (USD 21.73 million) can be established over the next six year period. This however, does not include the additional borrowing requirements of the 400,000 households working with outgrower schemes explained in section 3.4.11. The demand for credit from these households is expected to grow as local financial intermediaries link with the schemes. 3.7.6 Constraints: The lack of reliable rural financial services has contributed greatly to the inability of rural households to adopt improved production technologies, diversify their income base, and better cope with external shocks brought about by drought, floods and /or illness. Some gender-specific constraints, that influence the demand for financial services, include: (i) the very low levels of female literacy in much of the country; (ii) lack of access to assets and employment opportunities; (iii) lack of time and mobility linked to women's specific responsibility for reproductive labour and family welfare; and (iv) lack of access to information and business experience. Rural communities are also constrained by their little understanding of the markets, how they operate, and how to operate effectively in a free-market environment. Besides, apart from the large urban-based large-scale farmers and traders the rest have little access to investment and other financial services. 3.7.7 The lack of basic and essential social services and infrastructure does not attract financial service providers into rural areas. The banking system considers most rural households to be high risk due to their limited asset base, and lack of collateral, which they can pledge for formal credit. Due to poor infrastructure base, businesses and the private sector in rural areas generally face limited competition, low sales volumes/poor economies of scale, high transport and power costs, and lack of access to capital, all of which has resulted in economic inefficiencies, high prices, and a general lack of dynamism in the sector. The situation in rural areas is gradually changing however as the road network is expanded and access improved through other interventions funded by the GoM and the donor

13

community. The on-going Integrated Sector Investment Programme for the road sector focuses on the rehabilitation of the existing road networks that had been damaged by the war. The objective is to facilitate agricultural expansion and ease access to markets for produce as well as for inputs. Organized marketing activities have now penetrated to more distant areas and district services are being strengthened through government’s decentralization initiatives. These demonstrated constraints make a case for the need to establish targeted, innovative rural financial support system which will ensure an effective, efficient and sustainable delivery of financial services specific to the needs of the rural poor. To effectively mitigate these constraints, there will be need for concerted effort from the Government to create a conducive environment for the growth and development of rural financial service and for development partners to come up with appropriate interventions. 3.8 Interventions of Major Donors 3.8.1 In the past five years, a number of donor initiatives have supported the development of financial services in Mozambique. Table 1 below shows the size and purpose of the various donor supported interventions.

Table 1: Donor Support to Rural Microfinance sub-sector Funding Institution Amount of

Assistance Purpose

1 USAID USD25 million Emergency assistance in 1999 to support flood-affected companies in industrial, livestock, agricultural and fisheries sectors. The re-flows will be used for development of rural finance in Mozambique

2 Italian Government USD2.1 million Support rehabilitation of fisher folk affected by 1990 floods in Sofala, inhambane and Gaza Provinces

3 World Bank, NORAD EU and DFID

USD40 million Support to small and medium enterprises through TA, capacity building and line of credit

4 USAID Reflows from No. 1 above

To establish the Center for Promotion of Rural Finance

5 CIDA USD 300,000 Capacity support to MFIs through the Mozambique Micro-finance Facility (MMF). MMF will act as a launch pad for the proposed Micro finance Association.

6 ADF Amina -Project and UNDP

USD1.5 million Microstart Project: To support capacity building and resources for on-lending to MFIs.

7 ADF Amina -Project and others

USD550,000 Upstream Project: To support policy framework and dialogue for micro-finance development.

8 EU Euro2.0 million Support to AMODER & GAPI to promote rural financial intermediation

9 Irish Cooperation USD1.0 million Support to AMODER & GAPI to promote rural financial intermediation

10 German Aid -GTZ USD600,000 Support to SOCREMO 11 KfW i) EUR 3.00

million (planned) ii) EUR 3.00 million

i) EUR 500,000 for equity support to SOCREMO and EUR 2.5 million to GAPI for on-lending capital ii) KfW has supported through the Bank of Mozambique the IRAM-Project which has established the initial 55 RFAs model. In the second phase, of this project KfW is supporting the establishment of the RFA Unions and the Apex Structure.

3.8.2 The Bank Group commenced its lending operations in Mozambique in 1977. As at 30 June 2003, the Bank Group had funded a total of 63 operations (see annex 10). This included 45 projects, 11 studies, 2 emergency relief operations and 5 policy-based operations. Total cumulative commitments, net of cancellations, amounted to UA 812.71 million, comprising UA 714.46 million from ADF resources (89% of total), UA 91.36 million from ADB resources (11.2%), and UA 6.89 million from NTF resources (0.9%). The agricultural sector has been the major recipient of Bank Group funds, with 31.4% of net total commitments. To support Micro finance development the Bank Group has through

14

the former AMINA Project supported two-intervention sin Mozambique. The Microstart Programme, which has been co-financed with UNDP, and the Upstream Project, co-financed with UNDP and Australia Government. Under Microstart, three MFIs are currently supported and two of these (SOCREMO and Tchuma) are considered as potential partners under the proposed Programme. The Upstream Project mainly targets policy makers to influence microfinance policy development. The Bank in 2000 has also approved an Artisal Fisheries Development Project, which aims to support artisanal fisheries development and marketing systems. 3.8.3 A major factor, which has affected the implementation of Bank Group funded projects in Mozambique, has been the weak institutional capacity within the civil service to manage and monitor project implementation and adherence to procedures. This problem is worsened by the large number of disjointed projects and lack of harmony between donor procedures, which has overstretched the human resource requirements for project implementation. Institutional Capacity building and harmonisation of operational procedures would contribute towards the improvement of the Bank Group’s portfolio in Mozambique. The Country Strategy Paper highly recommends that institutional capacity needs should be assessed at appraisal in order incorporate capacity building measures in all future interventions. The Bank should also intensify technical support to project executing agencies through increased number of missions and more frequent seminars on Bank Group procedures. 4. THE PROGRAMME AND ADF-PROJECT The following sections 4.1 to 4.6 provide an overview of the overall Rural Finance Support Programme, followed by sections 4.7 to 4.14, which gives the detailed description, and costing of the ADF funded Rural Finance Intermediation Support Project, within the Programme. 4.1 Programme Concept and Rationale 4.1.1 The almost total absence of financial services in rural areas typified by the inability of farmers, traders and rural enterprises to get access to credit and find a safe place to deposit savings in Mozambique, calls for new ideas, different approaches and innovative institutional solutions to the problem. Past donor support has been sporadic and often concentrated on individual financial institutions and/or the financing of credit activities within stand-alone agricultural, fisheries or marketing projects. These initiatives were not developed within a comprehensive planning and strategic policy framework, which limited their impact on the poor and overall economic development. Having recognised the weakness in these past initiatives, the GoM has through a stakeholders participatory process decided to provide the framework, which would create an enabling environment, which will foster the growth of the rural finance subsector, in order to facilitate the emergence of rural house holds from poverty. This includes developing a sound legal and policy framework conducive to the growth of MFIs, community based organisation and other rural finance intermediaries. In this regard, the Rural Finance Support Programme and within it the ADF funded Rural Finance Intermediation Support Project will contribute to definition and development of an appropriate rural finance strategy for Mozambique. Unlike past interventions, the proposed Programme will support the establishment of a rural intermediation mechanism that promotes both savings and credit, in addition to the development of the appropriate rural finance infrastructure. 4.1.2 The Rural Finance Support Programme is a holistic intervention that will bring the key players together and commit the necessary resources to foster the development of rural finance through: (i) a public/private sector partnership by working with different practitioners including credit associations, commercial banks, MFIs, NGOs and other players involved in the sector; (ii) making the policy/legislative framework more effective in promoting rural finance; (iii) soliciting, piloting and

15