research project on investing in consumer brands and companies

TRANSCRIPT

Challenging conventional wisdom about

consumer product investing

Summary

2

• Venture capitalists traditionally cite a handful of reasons they prefer to

invest in technology over consumer companies; however, many of these

reasons are not fully supported by the facts

• Consumer companies making branded products or services have

fundamentally more attractive business models than companies that focus

on retail aggregation alone

• Apparel and accessories is an attractive vertical for early-stage investment

because of high and growing brand values and compelling financial profiles

• Consumer electronics is a challenging vertical for early-stage investing

because of low barriers to competition and difficulty of reaching end-users

DRAFT

Contents

• Introduction

• Retail aggregators vs. product makers

• Apparel and accessories

• Consumer electronics

3

DRAFT

US venture investment is heavily skewed towards technology with

consumer accounting for 5-10% of dollars invested…

SOURCE: PWC, NVCA MoneyTree Report 2014, CapIQ as of 4/8/15 based on Russell 3000 Index

15%

31%26%

55%

44%

19%

6%

14%

6%9%

17%

6%

16%

6%

25%

19%

17%

14%

11%

4%16%

6%

18%

20%

10%

8% 8%

16%

4%

13%6%

4% 4% 8%

19%

5%4%

18%

7%3% 6%

4%

4%

1%

3%4%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Perc

ent

of U

S V

en

ture

In

ve

stm

en

t

28.5

2000

1%

1995

4.0

3%

US Stock Market

2%

2%

7.4

2014

7.7

2013

2%2%

1%

3%

2%

2007

5.0

2%

3%

1%

Financials Services

Other

Software, ITSemiconductors, Electronics,Instrumentation, Networking

Computers, PeripheralsTelecomIndustrial/Energy

Media

Consumer

Healthcare

Venture Capital Dollars InvestedUS Stock Market

Value

4

DRAFT

Many of the largest companies in the world are non-tech

SOURCE: Capital IQ 4/8/15 5

Rank Company Name Primary Sector Primary Industry Market Cap

1 Apple Inc. (NasdaqGS:AAPL) Information Technology Technology Hardw are, Storage and Peripherals 731,588

2 Google Inc. (NasdaqGS:GOOGL) Information Technology Internet Softw are and Services 371,090

3 Berkshire Hathaw ay Inc. (NYSE:BRK.A) Financials Multi-Sector Holdings 353,030

4 Exxon Mobil Corporation (NYSE:XOM) Energy Integrated Oil and Gas 352,606

5 Microsoft Corporation (NasdaqGS:MSFT) Information Technology Systems Softw are 339,801

6 Johnson & Johnson (NYSE:JNJ) Healthcare Pharmaceuticals 278,501

7 Wells Fargo & Company (NYSE:WFC) Financials Diversif ied Banks 277,862

8 Wal-Mart Stores Inc. (NYSE:WMT) Consumer Staples Hypermarkets and Super Centers 261,408

9 General Electric Company (NYSE:GE) Industrials Industrial Conglomerates 251,788

10 Facebook, Inc. (NasdaqGS:FB) Information Technology Internet Softw are and Services 230,289

11 JPMorgan Chase & Co. (NYSE:JPM) Financials Diversif ied Banks 226,759

12 The Procter & Gamble Company (NYSE:PG) Consumer Staples Household Products 223,521

13 Pfizer Inc. (NYSE:PFE) Healthcare Pharmaceuticals 212,701

14 Verizon Communications Inc. (NYSE:VZ) Telecommunication Services Integrated Telecommunication Services 204,155

15 Chevron Corporation (NYSE:CVX) Energy Integrated Oil and Gas 200,540

16 Oracle Corporation (NYSE:ORCL) Information Technology Systems Softw are 188,264

17 The Walt Disney Company (NYSE:DIS) Consumer Discretionary Movies and Entertainment 180,766

18 The Coca-Cola Company (NYSE:KO) Consumer Staples Soft Drinks 178,628

19 Amazon.com Inc. (NasdaqGS:AMZN) Consumer Discretionary Internet Retail 177,023

20 AT&T, Inc. (NYSE:T) Telecommunication Services Integrated Telecommunication Services 169,459

21 Bank of America Corporation (NYSE:BAC) Financials Diversif ied Banks 164,223

22 Visa Inc. (NYSE:V) Information Technology Data Processing and Outsourced Services 163,296

23 Merck & Co. Inc. (NYSE:MRK) Healthcare Pharmaceuticals 162,203

24 International Business Machines Corporation (NYSE:IBM)Information Technology IT Consulting and Other Services 159,976

25 Citigroup Inc. (NYSE:C) Financials Diversif ied Banks 159,110

DRAFT

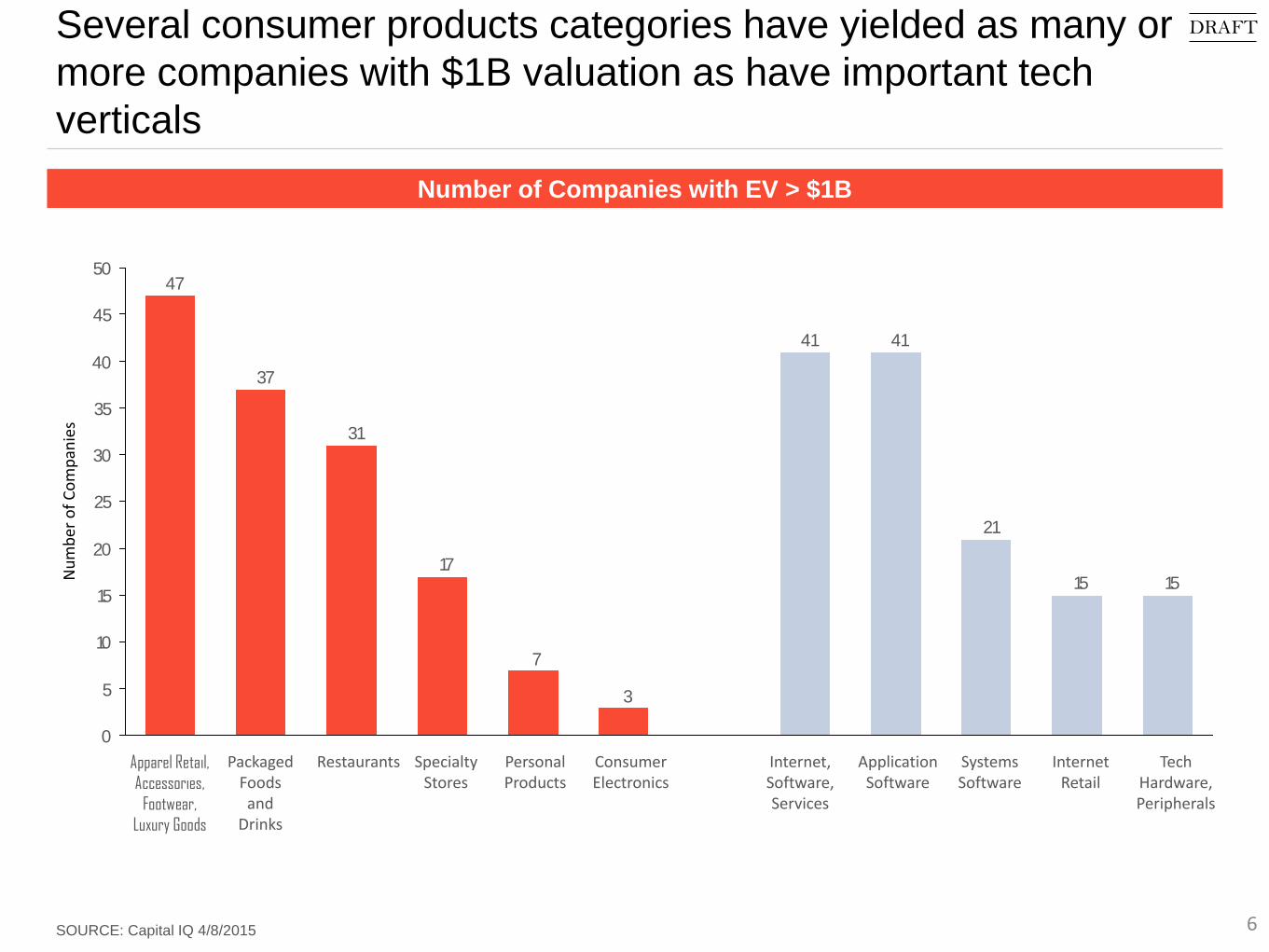

Several consumer products categories have yielded as many or

more companies with $1B valuation as have important tech

verticals

SOURCE: Capital IQ 4/8/2015

1515

21

4141

3

7

17

31

37

47

0

5

10

15

20

25

30

35

40

45

50

Internet, Software, Services

Nu

mb

er o

f C

om

pan

ies

Apparel Retail,

Accessories,

Footwear,

Luxury Goods

Packaged Foods and

Drinks

Tech Hardware, Peripherals

Systems Software

Application Software

Internet Retail

Specialty Stores

Restaurants Consumer Electronics

Personal Products

Number of Companies with EV > $1B

6

DRAFT

While some consumer companies trade at high multiples,

technology companies trade even higher

SOURCE: Capital IQ 4/8/15

7.4x8.1x8.4x

9.0x

27.2x

13.0x

15.3x16.1x

17.6x

22.0x

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

EV/L

TM R

even

ue

High Multiple Consumer Products

Companies

High Multiple Consumer Technology

Companies

7

DRAFT

Several consumer companies have scaled to $1 billion in

sales as quickly as technology’s greatest success stories

SOURCE: Forbes, CapitalIQ, FastCompany, Stanford GSB, Company Websites

10

10

10

10

9

9

8

8

8

7

6

6

5

5

5

5

4

3

2

Years to reach $1B in sales

Consumer

IT, Software, Internet

8

DRAFT

While leading tech darlings do generate high gross margins,

consumer brands hold their own and often have higher total

margin

SOURCE: Capital IQ 4/8/15

51%

55%

57%

59%

60%

61%

61%

65%

73%

79%

21%

21%

33%

28%

21%

24%

30%

19%

31%

43%

27%

29%

45%

62%

66%

68%

70%

72%

83%

87%

9%

20%

-3%

26%

18%

20%

37%

5%

40%

2%

Gross Margin EBIT Margin

9

DRAFT

Today’s consumer product IPO class has built larger businesses

per $ of VC investment than their technology counterparts …

SOURCE: Capital IQ, Pitchbook

2.2x2.3x

3.2x3.4x

4.3x

0.3x

0.7x

1.0x

1.5x1.5x

2.0x

2.8x

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

LTM

R

evenue/C

apit

al

10

Annual LTM Revenue at time of IPO / Pre-IPO Capital Raised

DRAFT

0

10

20

30

40

50

60

70

80

90

100

110

120

130

0 20 40 60 80 100 120 140 160 180 200 220 240 260 280 300 320

Eventbrite

Annu

al R

even

ue (

$ m

illio

ns)

Total Capital Raised

($ millions)

… and private ventures support a similar story to today’s IPO

class …

SOURCE: CB Insights, PrivCo April 8th, 2015, Fast Company, Inc.com

Consumer, Retail IT, Internet

Less capital, more

revenue

More capital, less

revenue

11

DRAFT

… but due to high public valuations, technology IPO class has

created more value per $ of VC investment

SOURCE: Capital IQ 5/15/15, Pitchbook

2.9x

6.5x

12.9x13.4x

20.5x

4.6x

10.9x11.3x

25.9x

28.9x30.0x

0

5

10

15

20

25

30

EV/C

apit

al

Growth

Rate

(%)

31 58 20 11 20 52 67 59 73 72 74

12

IPO Enterprise Value / Pre-IPO Capital Raised

DRAFT

Global market size of consumer categories is often multiples

larger than popular technology verticals

SOURCE: Businessoffashion.com, Statista, Forbes, Markets and Markets, Tech Crunch

208796121131

280317

1,2001,240

2,1002,140

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

2,200

Dolla

rs (B

)

Enterprise

Software

Apparel SaaSCyber

Security

Marketing

Software

Internet

Advertising

Cloud

Services

Consumer

Electronics

BeverageRestaurantsPackaged

Food

13

DRAFT

Consumer product companies can reach very high market

shares, comparable to those of leading IT firms

SOURCE: Forbes, Statista

30%

48%

68%

33%

42%45%

60%

67%

0%

10%

20%

30%

40%

50%

60%

70%

Mar

ketS

hare

US Athletic

Footwear

Global Toothpaste US Soft drinks US Out-of-

home Coffee

Global Search US Smartphones Global Cloud

Computing

US Fitness

Trackers

14

DRAFT

Contents

• Introduction

• Retail aggregators vs. product makers

• Apparel and accessories

• Consumer electronics

15

DRAFT

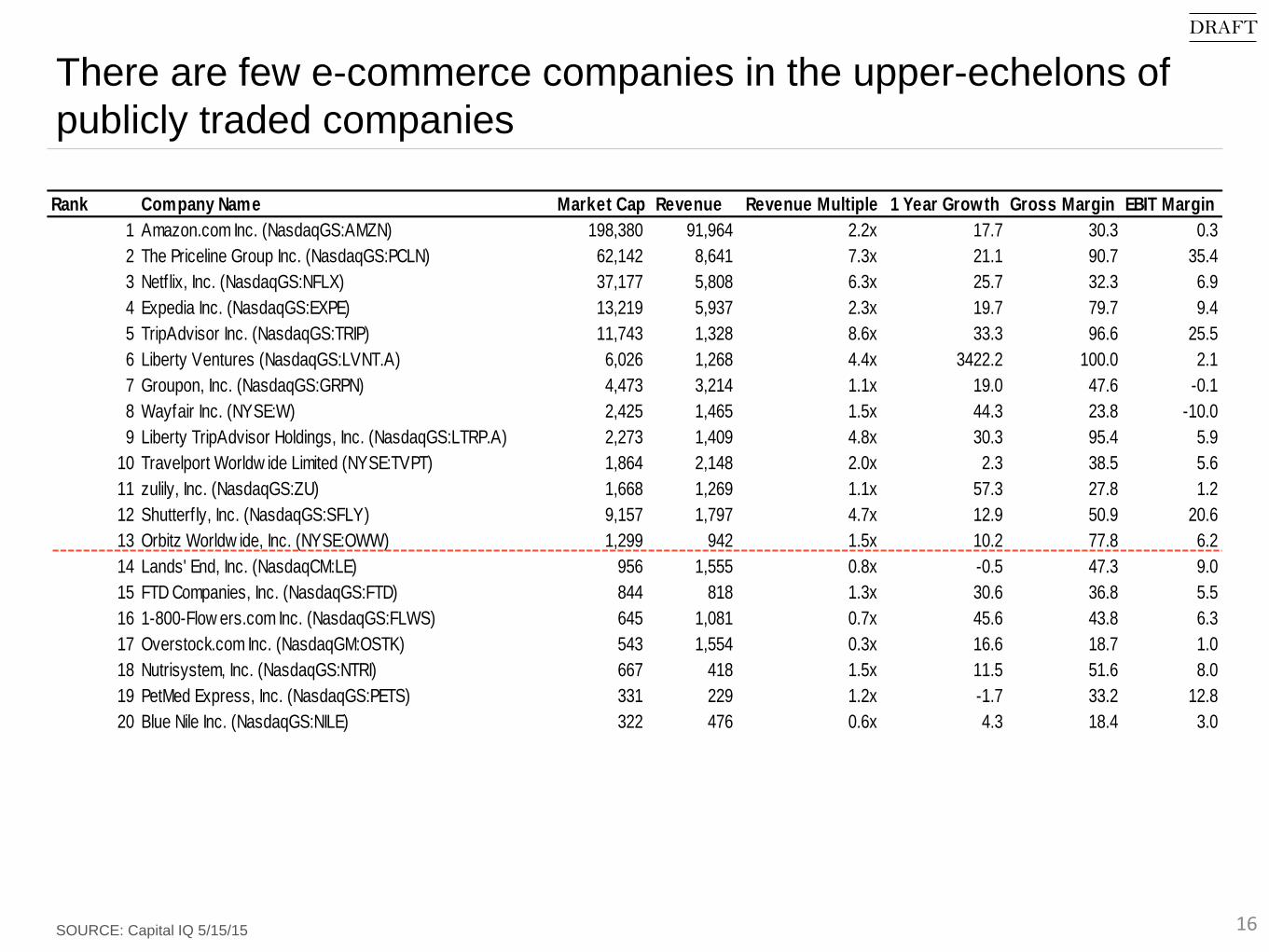

There are few e-commerce companies in the upper-echelons of

publicly traded companies

SOURCE: Capital IQ 5/15/15 16

Rank Company Name Market Cap Revenue Revenue Multiple 1 Year Growth Gross Margin EBIT Margin

1 Amazon.com Inc. (NasdaqGS:AMZN) 198,380 91,964 2.2x 17.7 30.3 0.3

2 The Priceline Group Inc. (NasdaqGS:PCLN) 62,142 8,641 7.3x 21.1 90.7 35.4

3 Netflix, Inc. (NasdaqGS:NFLX) 37,177 5,808 6.3x 25.7 32.3 6.9

4 Expedia Inc. (NasdaqGS:EXPE) 13,219 5,937 2.3x 19.7 79.7 9.4

5 TripAdvisor Inc. (NasdaqGS:TRIP) 11,743 1,328 8.6x 33.3 96.6 25.5

6 Liberty Ventures (NasdaqGS:LVNT.A) 6,026 1,268 4.4x 3422.2 100.0 2.1

7 Groupon, Inc. (NasdaqGS:GRPN) 4,473 3,214 1.1x 19.0 47.6 -0.1

8 Wayfair Inc. (NYSE:W) 2,425 1,465 1.5x 44.3 23.8 -10.0

9 Liberty TripAdvisor Holdings, Inc. (NasdaqGS:LTRP.A) 2,273 1,409 4.8x 30.3 95.4 5.9

10 Travelport Worldw ide Limited (NYSE:TVPT) 1,864 2,148 2.0x 2.3 38.5 5.6

11 zulily, Inc. (NasdaqGS:ZU) 1,668 1,269 1.1x 57.3 27.8 1.2

12 Shutterf ly, Inc. (NasdaqGS:SFLY) 9,157 1,797 4.7x 12.9 50.9 20.6

13 Orbitz Worldw ide, Inc. (NYSE:OWW) 1,299 942 1.5x 10.2 77.8 6.2

14 Lands' End, Inc. (NasdaqCM:LE) 956 1,555 0.8x -0.5 47.3 9.0

15 FTD Companies, Inc. (NasdaqGS:FTD) 844 818 1.3x 30.6 36.8 5.5

16 1-800-Flow ers.com Inc. (NasdaqGS:FLWS) 645 1,081 0.7x 45.6 43.8 6.3

17 Overstock.com Inc. (NasdaqGM:OSTK) 543 1,554 0.3x 16.6 18.7 1.0

18 Nutrisystem, Inc. (NasdaqGS:NTRI) 667 418 1.5x 11.5 51.6 8.0

19 PetMed Express, Inc. (NasdaqGS:PETS) 331 229 1.2x -1.7 33.2 12.8

20 Blue Nile Inc. (NasdaqGS:NILE) 322 476 0.6x 4.3 18.4 3.0

DRAFT

Only a handful of publicly traded e-commerce companies have

returned >5x over the last 10 years (or since IPO)

SOURCE: Capital IQ 5/15/15 17

0x

5x

10x

15x

20x

25x

30x

35x

40x

45x

50x

55x

60x

Tota

l Ret

urn

to S

hare

hold

ers

EXPE

AMZN

Year 0 Year 10

LTRP.A

W

GRPN

SFLYLVNT.A

TRIP OWWZU EBAY

NTRI

OSTK

FLWS

PETSFTD

LE NILETVPT

DRAFT

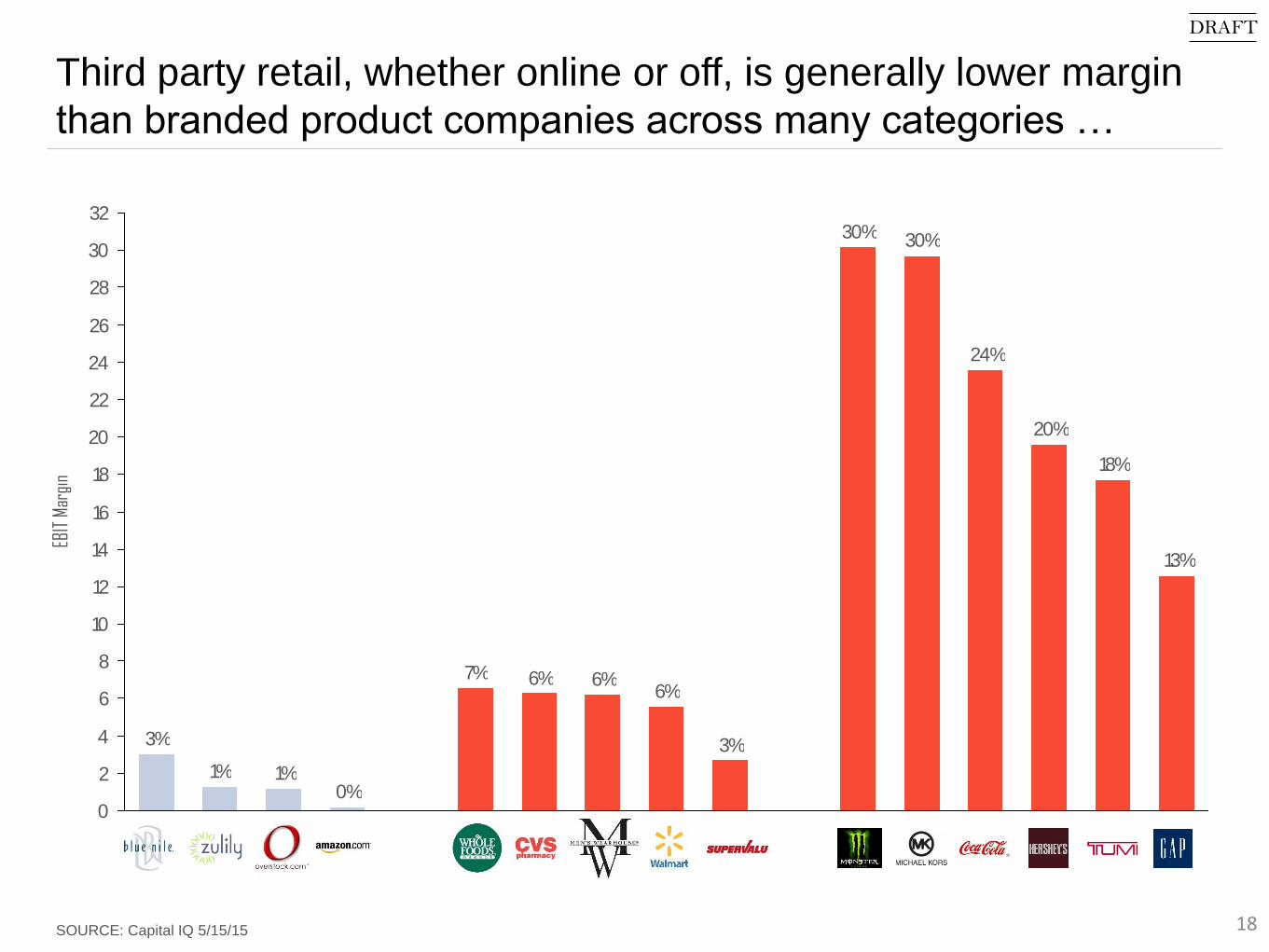

Third party retail, whether online or off, is generally lower margin

than branded product companies across many categories …

SOURCE: Capital IQ 5/15/15 18

13%

18%

20%

24%

30%30%

3%

6%6%6%7%

0%1%1%

3%

0

2

4

6

8

10

12

14

16

18

20

22

24

26

28

30

32

EBIT

Mar

gin

DRAFT

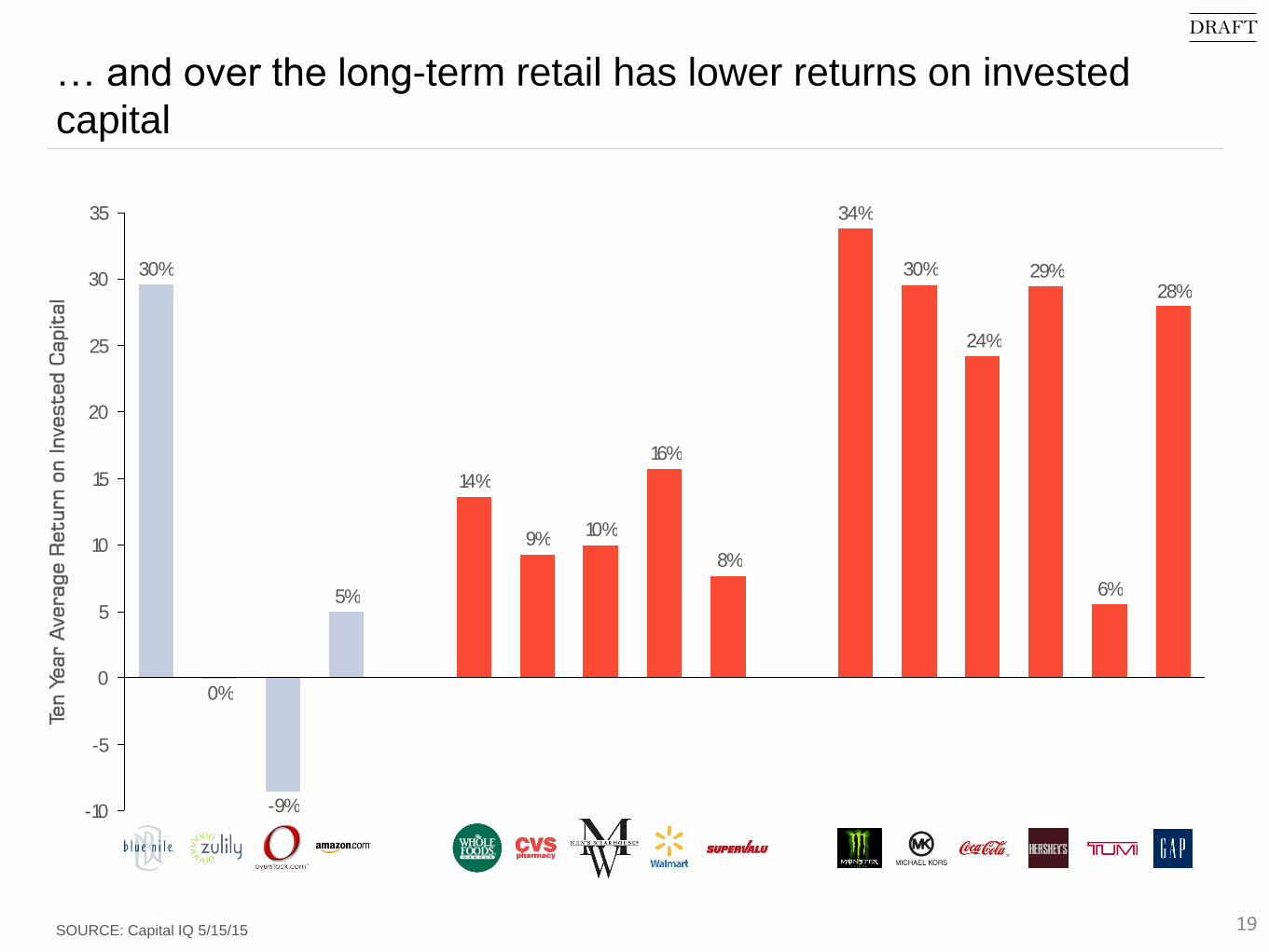

… and over the long-term retail has lower returns on invested

capital

SOURCE: Capital IQ 5/15/15 19

28%

6%

29%

24%

30%

34%

8%

16%

10%9%

14%

5%

-9%

0%

30%

-10

-5

0

5

10

15

20

25

30

35

Ten Year A

verage R

eturn on Invested C

apit

al

DRAFT

Due to lower margins, retail generally trades at lower revenue

multiples than branded products

SOURCE: Capital IQ 5/15/15 20

1.0x

2.4x

3.1x

4.4x

2.7x

0.9x

0.3x

0.6x

1.4x

0.9x 1.0x

2.2x

0.3x

1.1x

0.6x

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

Enterpris

e Valu

e/LTM

R

evenue

DRAFT

Two strategies for success in competitive retail spaces

SOURCE: Forbes 21

Aggregate Fragmented Supplier Base in Niche

MarketScale

• When supplier base is highly fragmented

retailer creates value by consolidating buying

process

• Fragmented supplier base means that retailer

brand value can exceed that of suppliers,

enabling greater value capture

• Scale allows retailers to compete on price and

convenience

• Price: Retailers with large buying volumes

and more brand recognition than suppliers

can negotiate best prices

• Convenience: Larger scale enables more

efficient and timely distribution

• Amazon market share in e-commerce is as

large as the next 12 players combined

DRAFT

Contents

• Introduction

• Retail aggregators vs. product makers

• Apparel and accessories

• Consumer electronics

22

DRAFT

Apparel and accessories industry has both positives and

negatives

SOURCE: Consumer investor interviews 23

What to Like What Not to Like

• Attractive gross margins and operating

profitability

• Relatively capital-light business models

• Ability to attract debt financing can raise

returns to equity investors

• Share of branded product is on a upward

trend with growing “value” of apparel and

luxury brands

• Clear model for growth through expanding

distribution outlets

• Retailer power and “broken wholesale

channel” limits brand margin

• “Faddy” trends makes product success

hard to predict and shortens product

lifecycle

• Finite exit environment (i.e., limited

strategic interest in acquisitions)

• Fashion is usually not a “winner take all”

market

• Low frequency of purchase for most

categories means revenue is not highly

recurring

DRAFT

Apparel and accessories then and now

SOURCE: Consumer investor interviews 24

Examples

Direct-to-consumer selling leads to greater value capture by brands

E-commerce drives increased reach with less time and money

Digital marketing builds stronger customer relationships, yields

better customer insight in design, and enables customization with

price premium

Barriers to entry arguably falling due to e-commerce and more

fragmented retail channel

Outsourcing costs have increased with rising wages in China and

other manufacturing hubs

DRAFT

There are 40 publicly traded apparel and accessories companies

with >$1B in market cap (1/2)

SOURCE: Capital IQ 5/15/15 25

Rank Company Name Market Cap Revenue Revenue Multiple 1 Year Growth Gross Margin EBIT Margin

1 Nike, Inc. (NYSE:NKE) 90,256 30,247 2.8x 11.7 45.8 13.6

2 V.F. Corporation (NYSE:VFC) 30,284 12,339 2.6x 6.5 48.7 14.8

3 L Brands, Inc. (NYSE:LB) 25,801 11,454 2.5x 6.3 47.0 17.1

4 Under Armour, Inc. (NYSE:UA) 16,773 3,248 5.3x 29.8 48.9 11.1

5 The Gap, Inc. (NYSE:GPS) 16,323 16,435 1.0x 1.8 38.3 12.6

6 Hanesbrands Inc. (NYSE:HBI) 12,576 5,474 2.7x 15.4 37.5 14.2

7 Michael Kors Holdings Limited (NYSE:KORS) 12,250 4,208 2.7x 40.7 61.0 29.7

8 Ralph Lauren Corporation (NYSE:RL) 11,622 7,620 1.4x 2.3 57.5 13.8

9 Tiffany & Co. (NYSE:TIF) 11,185 4,250 2.7x 5.4 59.7 21.0

10 Signet Jew elers Limited (NYSE:SIG) 10,694 5,954 2.0x 35.5 38.5 10.7

11 Coach, Inc. (NYSE:COH) 10,350 4,324 2.1x -11.6 69.7 18.9

12 Lululemon Athletica Inc. (NasdaqGS:LULU) 9,157 1,797 4.7x 12.9 50.9 20.6

13 PVH Corp. (NYSE:PVH) 8,672 8,241 1.4x 0.7 52.5 8.6

14 Skechers USA Inc. (NYSE:SKX) 5,271 2,607 1.9x 33.7 45.0 9.6

15 Urban Outfitters Inc. (NasdaqGS:URBN) 5,215 3,323 1.5x 7.7 42.5 11.0

16 Carter's, Inc. (NYSE:CRI) 5,210 2,927 1.9x 8.4 41.2 12.4

17 Columbia Sportsw ear Company (NasdaqGS:COLM) 4,048 2,155 1.7x 22.4 45.8 9.8

18 Fossil Group, Inc. (NasdaqGS:FOSL) 3,780 3,458 1.2x 3.1 56.6 15.7

19 Kate Spade & Company (NYSE:KATE) 3,509 1,170 3.2x 34.4 60.3 4.9

20 American Eagle Outfitters, Inc. (NYSE:AEO) 3,123 3,283 0.8x -0.7 43.9 6.5

DRAFT

There are 40 publicly traded apparel and accessories companies

with >$1B in market cap (2/2)

SOURCE: Capital IQ 5/15/15 26

Rank Company Name Market Cap Revenue Revenue Multiple 1 Year Growth Gross Margin EBIT Margin

21 DSW Inc. (NYSE:DSW) 3,117 2,496 1.2x 5.4 38.0 9.9

22 Wolverine World Wide Inc. (NYSE:WWW) 3,110 2,765 1.4x 3.4 39.5 9.7

23 G-III Apparel Group, Ltd. (NasdaqGS:GIII) 2,563 2,117 1.2x 23.2 35.8 7.8

24 Deckers Outdoor Corp. (NYSE:DECK) 2,498 1,588 1.4x 10.9 47.7 13.0

25 Steven Madden, Ltd. (NasdaqGS:SHOO) 2,478 1,354 1.8x 1.1 34.9 12.1

26 Chico's FAS Inc. (NYSE:CHS) 2,437 2,675 0.8x 3.4 53.3 6.1

27 The Buckle, Inc. (NYSE:BKE) 2,155 1,153 1.7x 2.2 50.1 22.3

28 Five Below , Inc. (NasdaqGS:FIVE) 1,866 680 2.7x 27.0 35.0 11.3

29 Genesco Inc. (NYSE:GCO) 1,643 2,860 0.5x 8.9 49.0 5.9

30 Guess? Inc. (NYSE:GES) 1,536 2,418 0.4x -5.9 35.9 6.2

31 Abercrombie & Fitch Co. (NYSE:ANF) 1,490 3,744 0.4x -9.1 61.8 4.9

32 Express Inc. (NYSE:EXPR) 1,447 2,165 0.6x -2.4 41.2 6.8

33 The Children's Place, Inc. (NasdaqGS:PLCE) 1,399 1,756 0.7x 0.2 35.7 5.4

34 Brow n Shoe Co. Inc. (NYSE:BWS) 1,349 2,572 0.6x 2.3 40.4 5.1

35 Tumi Holdings, Inc. (NYSE:TUMI) 1,302 529 2.4x 11.8 58.2 16.9

36 Iconix Brand Group, Inc. (NasdaqGS:ICON) 1,285 390 7.3x -3.7 100.0 48.6

37 Oxford Industries Inc. (NYSE:OXM) 1,258 998 1.4x 8.8 55.1 8.4

38 Crocs, Inc. (NasdaqGS:CROX) 1,216 1,148 1.1x -3.8 49.3 1.8

39 The Cato Corporation (NYSE:CATO) 1,079 987 0.8x 7.3 39.1 9.2

DRAFT

The shift from unbranded to branded means a continued

opportunity for new brands to gain share

SOURCE: Euromonitor 27

… yet many categories are still largely

unbranded

DRAFT

Percent of S

ale

s B

randed

Branded M

arket S

hare

The share of brands is rising …

Apparel and luxury has the fastest growing brand “value”

NOTE: Size of bubble represents $ value of brand growth

SOURCE: Millward Brown BrandZ Top 100 Most Valuable Global Brands 2014 28

Apparel brand values are increasing

at a rapid clip, due to branded

products gaining share

Apple and Google are by far the

world’s most valuable brands

DRAFT

Value capture opportunity from brands going direct-to-consumer

is significant

SOURCE: Goldman Sachs 29

Notional P&L of a retail, wholesale and e-commerce sale

Wholesale sale

Retail sale

Brand.come-commerce sale

Value to brand

Value to brand

Value to brand

Cost of goods sold

Cost of goods sold

Cost of goods sold

Operating costs of brand

Operating costs of brand

Operating costs of brand

Retail mark up

Store costs

DRAFT

Movement to e-commerce and downstream integration both lead

to more value capture by brand…

SOURCE: Goldman Sachs, L2 30

P&L is more attractive with e-commerce distribution and especially with brand-

owned digital channel……more room to move to

brand-owned channel

39

61 70

0

50

10

60

80

20

30

100

90

40

Aggregator.com

Perc

ent o

f e-c

omm

erce

sal

es

Brand.com

DRAFT

…yet in many categories, majority of sales are still through

wholesale…

SOURCE: Euromonitor 31

32

61

75

4549

95

60

6

4

5

3

62

37

24

5146

37

4

0

10

20

30

40

50

60

70

80

90

100

Perc

ent

of

Sale

s

Eyewear Sporting GoodsFootwear

1

Bags & LuggageWatches

1

2

JewelleryClothing

Brand.com WholesaleOwned Retail

DRAFT

… and the rise of e-commerce is mostly eating into wholesale

distribution

SOURCE: Euromonitor 32

Retail E-commerce Wholesale

E-commerce is growing

at the expense of

wholesale, while owned

retail continues to

grow

Perc

ent o

f Sal

esDRAFT

E-commerce also lowers working capital (i.e., inventory)

requirements, leading to greater capital efficiency

SOURCE: Goldman Sachs, Company Data (Samsonite, Nike, Kors, Prada, Tiffany, Coach, ASOS, YOOX) 33

Net Working Capital Days

DRAFT

… while transaction-less stores allow the benefits of owned-retail

with e-commerce inventory characteristics

SOURCE: Pando Daily, Inc.com 34

• Consumers often want to physically touch

and try on apparel items before purchase,

necessitating brands to go beyond e-

commerce

• Use of retail location as “show-room” with

transaction still via brand.com enables:

• Minimal square footage

• E-commerce inventory profile

• Closer interaction with customer

Bonobos sales per square

foot is “the highest we know

about in men’s clothing…it’s

in the four figures” – Andy

Dunn

Warby Parker Showroom in

NYC grossed $2.5 million with

600 square feet $4,200 sales

per sq. foot, on par with Tiffany

Bonobos Guide Shop

Warby Parker Showroom

DRAFT

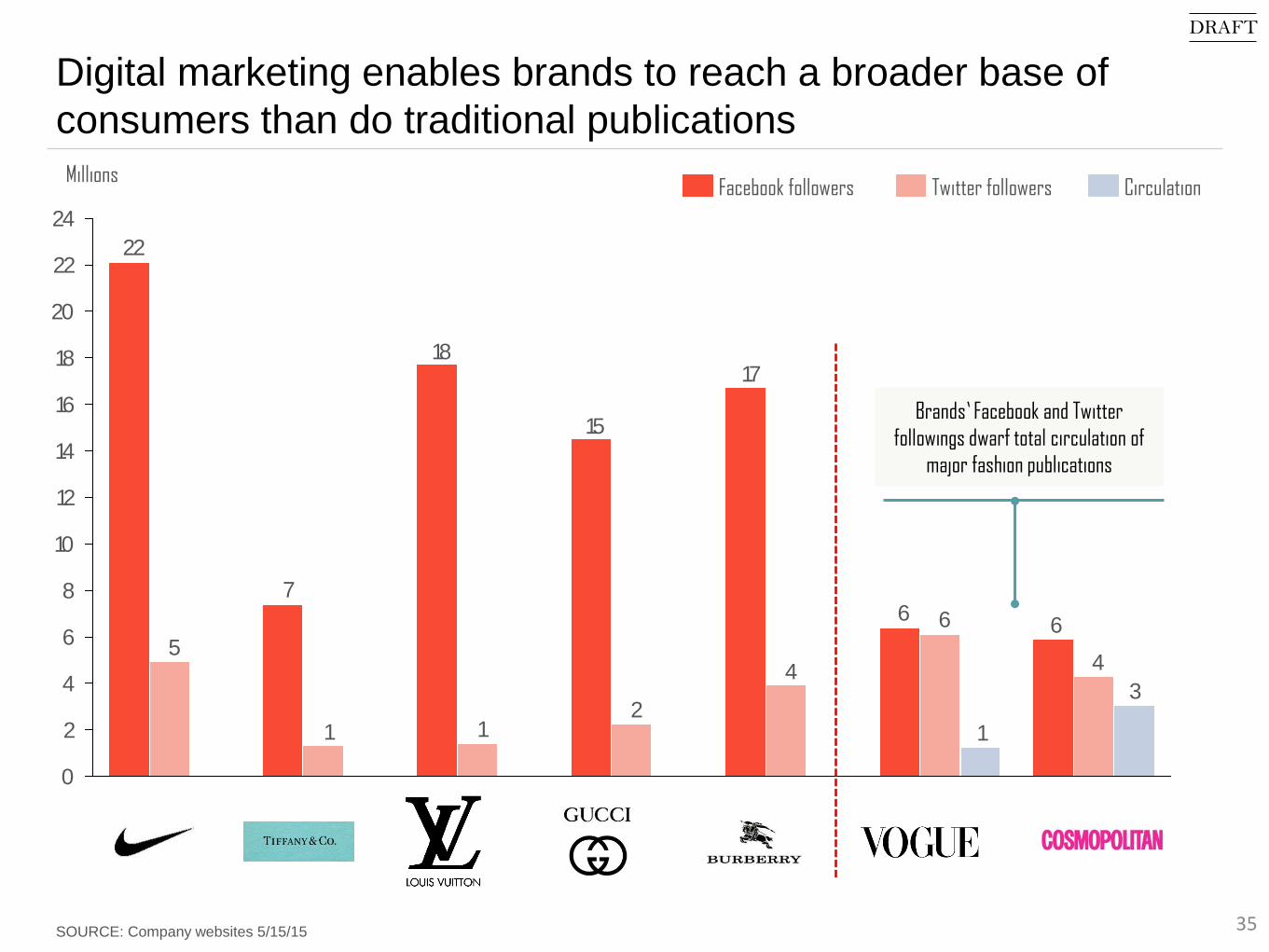

Digital marketing enables brands to reach a broader base of

consumers than do traditional publications

SOURCE: Company websites 5/15/15 35

66

17

15

18

7

22

4

6

4

211

5

3

1

0

2

4

6

8

10

12

14

16

18

20

22

24

MillionsFacebook followers Twitter followers Circulation

Brands’ Facebook and Twitter

followings dwarf total circulation of

major fashion publications

DRAFT

Rising manufacturing wages is increasing the cost of outsourced

garment production

SOURCE: American Progress, WTO 36

55

80

100

90

70

60

50

0

10

20

40

30

Shar

e of

Glo

bal C

loth

ing

Expo

rts

(201

2)

38

4

48

Bangladesh

Germany

All others

China

Italy

DRAFT

Apparel investors identify several criteria of successful early-

stage companies

SOURCE: Consumer investor interviews 37

Independent

Distribution

• Distribution not solely dependent on wholesale model and especially not on department store

• Owned retail is better than wholesale, but has significant upfront costs

Earned Media• Ability to get free PR is essential to growing brand awareness at reasonable cost

Demographic• Product should speak to a clear target demographic

• Demographic should be attractive in terms of underlying size, growth, and purchasing power

Brand• Company should have clear brand image associated with certain values

Merchandising• Trend/fads change quickly in fashion. A success 1 season does not translate into a viable

brand

• Mgmt. team should have demonstrated ability to “merchandise,” an ability to anticipate fashion trends

DRAFT

Case study: Crocs demonstrates “fad” based nature of

apparel and impact of higher margins from owned retail

SOURCE: Google Finance May 2015 38

Tops sales estimates and

operating margin hits 30%

“investors have wondered whether

Crocs can maintain its momentum, or

if the brand is a fad ready to fizzle” -

Forbes

“Strong expectations for sales during the

holiday season (mirrored by other shoe

brands including Nike)” - Reuters

Earnings miss on lower sales growth and

lower margin (caused by mixed shift

away from owned retail to third party)

DRAFT

Case study: Lululemon’s rise and fall demonstrates vulnerability to

competition and maintaining image, even with strong brand loyalty

SOURCE: Google Finance May 2015 39

Lululemon expects profit

and sales in the current

quarter to top earlier

forecasts after holiday

shoppers flocked to its

shops

Company recalls 17% of

Yoga pants due to see-

through issue

“Lululemon Stock Squeezed

15% On CEO's Decision To

Step Down” - Forbes

Same store sales decline

for first time since 2009,

driven by new yoga

segment competition and

quality image issues

“Stock rises on Strong

Guidance: Turnaround

Gaining Momentum” –

Fool.com

DRAFT

Contents

• Introduction

• Retail aggregators vs. product makers

• Apparel and accessories

• Consumer electronics

40

DRAFT

Consumer electronics industry has both positives and negatives

SOURCE: Consumer investor interviews 41

What to Like What Not to Like

• Potential to exhibit exponential growth

• High switching costs

• Retailer power and “broken wholesale channel” limits producer

margin

• Low frequency of purchase for most categories means revenue is

not highly recurring

• Low barriers leads to competition that drives down

prices/margins quickly and/or requires large investment in

innovation

• Longer time and more money required (vs. software) to get

product to market, due to both product development and

distribution challenges

DRAFT

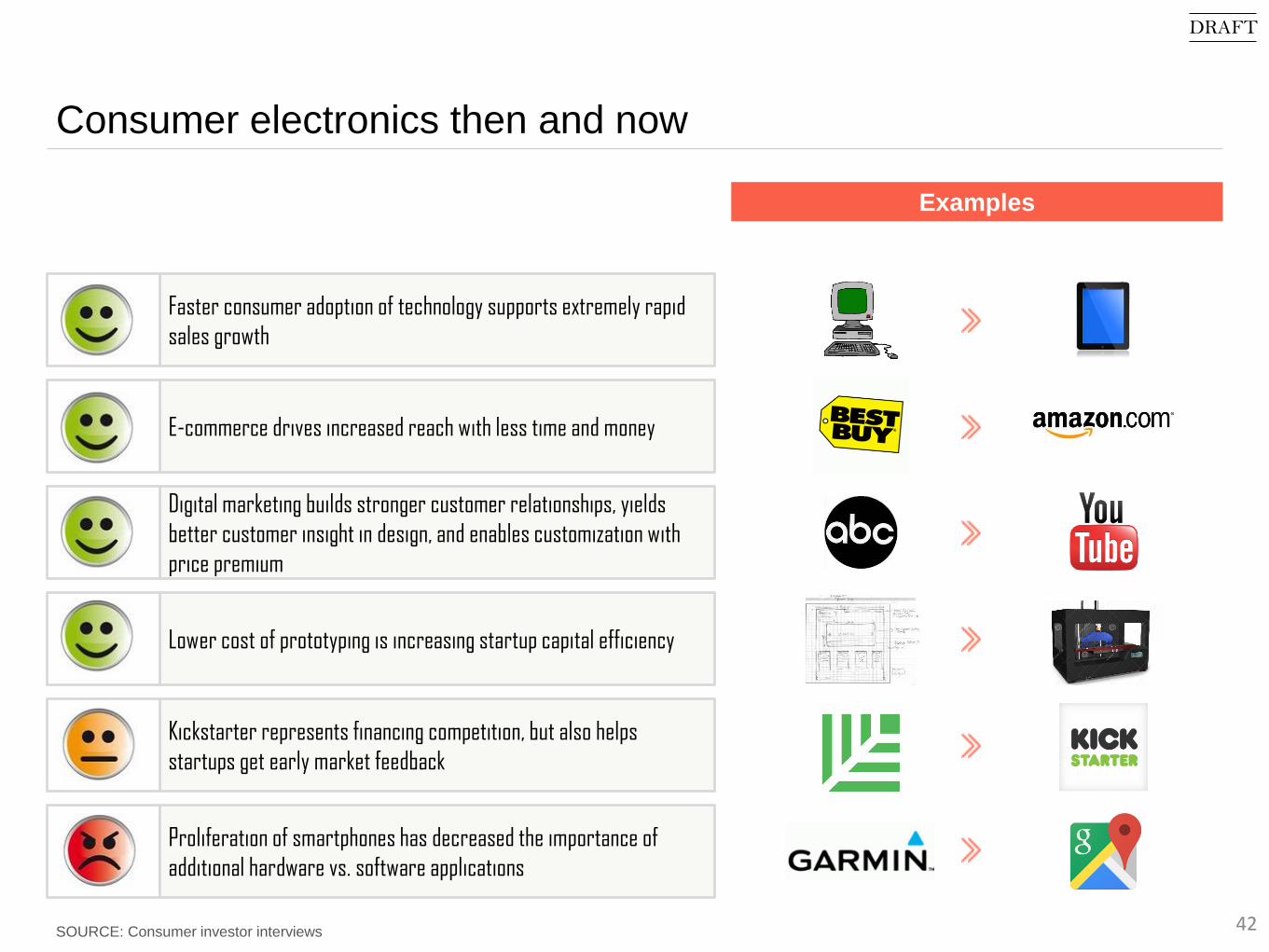

Consumer electronics then and now

SOURCE: Consumer investor interviews 42

Examples

Faster consumer adoption of technology supports extremely rapid

sales growth

E-commerce drives increased reach with less time and money

Digital marketing builds stronger customer relationships, yields

better customer insight in design, and enables customization with

price premium

Lower cost of prototyping is increasing startup capital efficiency

Kickstarter represents financing competition, but also helps

startups get early market feedback

Proliferation of smartphones has decreased the importance of

additional hardware vs. software applications

DRAFT

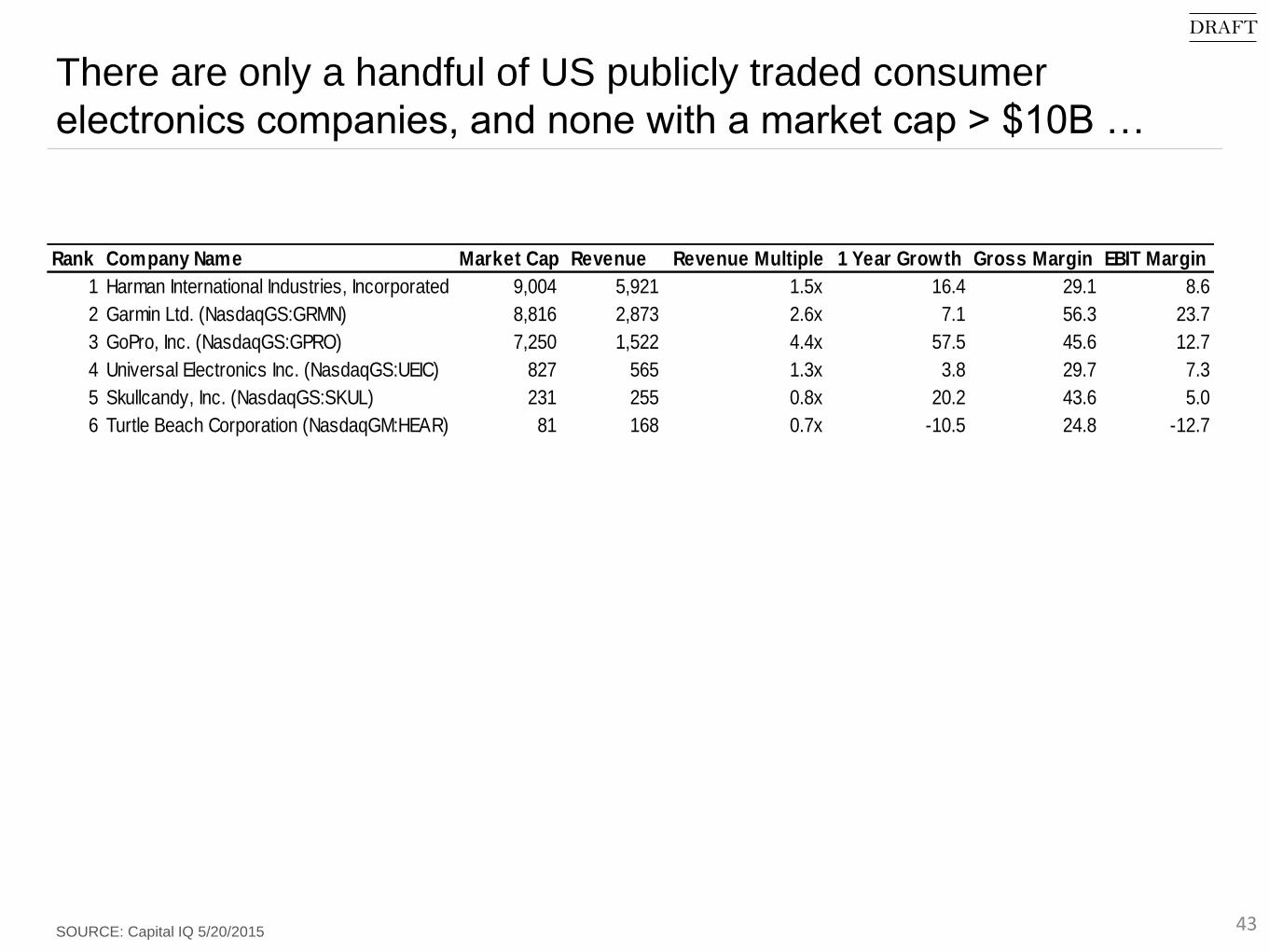

There are only a handful of US publicly traded consumer

electronics companies, and none with a market cap > $10B …

SOURCE: Capital IQ 5/20/2015 43

Rank Company Name Market Cap Revenue Revenue Multiple 1 Year Growth Gross Margin EBIT Margin

1 Harman International Industries, Incorporated (NYSE:HAR)9,004 5,921 1.5x 16.4 29.1 8.6

2 Garmin Ltd. (NasdaqGS:GRMN) 8,816 2,873 2.6x 7.1 56.3 23.7

3 GoPro, Inc. (NasdaqGS:GPRO) 7,250 1,522 4.4x 57.5 45.6 12.7

4 Universal Electronics Inc. (NasdaqGS:UEIC) 827 565 1.3x 3.8 29.7 7.3

5 Skullcandy, Inc. (NasdaqGS:SKUL) 231 255 0.8x 20.2 43.6 5.0

6 Turtle Beach Corporation (NasdaqGM:HEAR) 81 168 0.7x -10.5 24.8 -12.7

DRAFT

Yet, venture investment in consumer electronics and hardware

has been increasing …

SOURCE: VentureWire 44

DRAFT

Speed of consumer adoption of hardware products has increased

tremendously

SOURCE: The Atlantic 45

DRAFT

3D printing is one of the innovations lowering the cost of

prototypes

SOURCE: Gartner 46

0

50,000

1,00,000

1,50,000

2014A2012A 2013A 2015P

Un

its

So

ld

Number of 3D Printers Sold for <$100K

DRAFT

The falling prices of television sets demonstrates the

competitiveness of consumer electronics industries

SOURCE: BusinessInsider 47

DRAFT

Many hardware categories have been disrupted by software

applications utilizing the smartphone as a hardware platform

48

Smartphones empowered with mapping applications (i.e., Google Maps) eliminated the need for separate navigation consoles like Garmin

The proliferation of high-power cameras installed in iPhones and other smartphones resulted in the death of Flip Video

While Kindle continues to be a successful publishing and software business, the original e-reader business has lost traction due to smartphones and tablets

Calculators pre-installed in all smartphones has reduced the purchases of mid-range calculators

DRAFT

Garmin rise and fall demonstrates disruption by software

applications utilizing the smartphone as a hardware platform (1/2)

SOURCE: Google Finance May 2015 49

June 29, 2007:

Introduction of

iPhone

DRAFT

Garmin rise and fall demonstrates disruption by software

applications utilizing the smartphone as a hardware platform (2/2)

SOURCE: CapitalIQ 5/15/201550

2,871

2,6322,7162,759

2,690

2,946

3,494

3,180

1,774

1,028

763

573465

369346233

24%

22%22%

27%29%

31%33%

40%38%

36%37%

36%

0

500

1,000

1,500

2,000

2,500

3,000

3,500

0%

5%

10%

15%

20%

25%

30%

35%

40%

EBIT M

arginA

nn

ual

Sal

es

($ M

)

2012 2013 20142010

24%

2011

20%

25%

20092007 20082002 2005 20062004

36%

200320011999 2000

Sales

EBIT Margin

June 29, 2007: Introduction of

iPhone

DRAFT

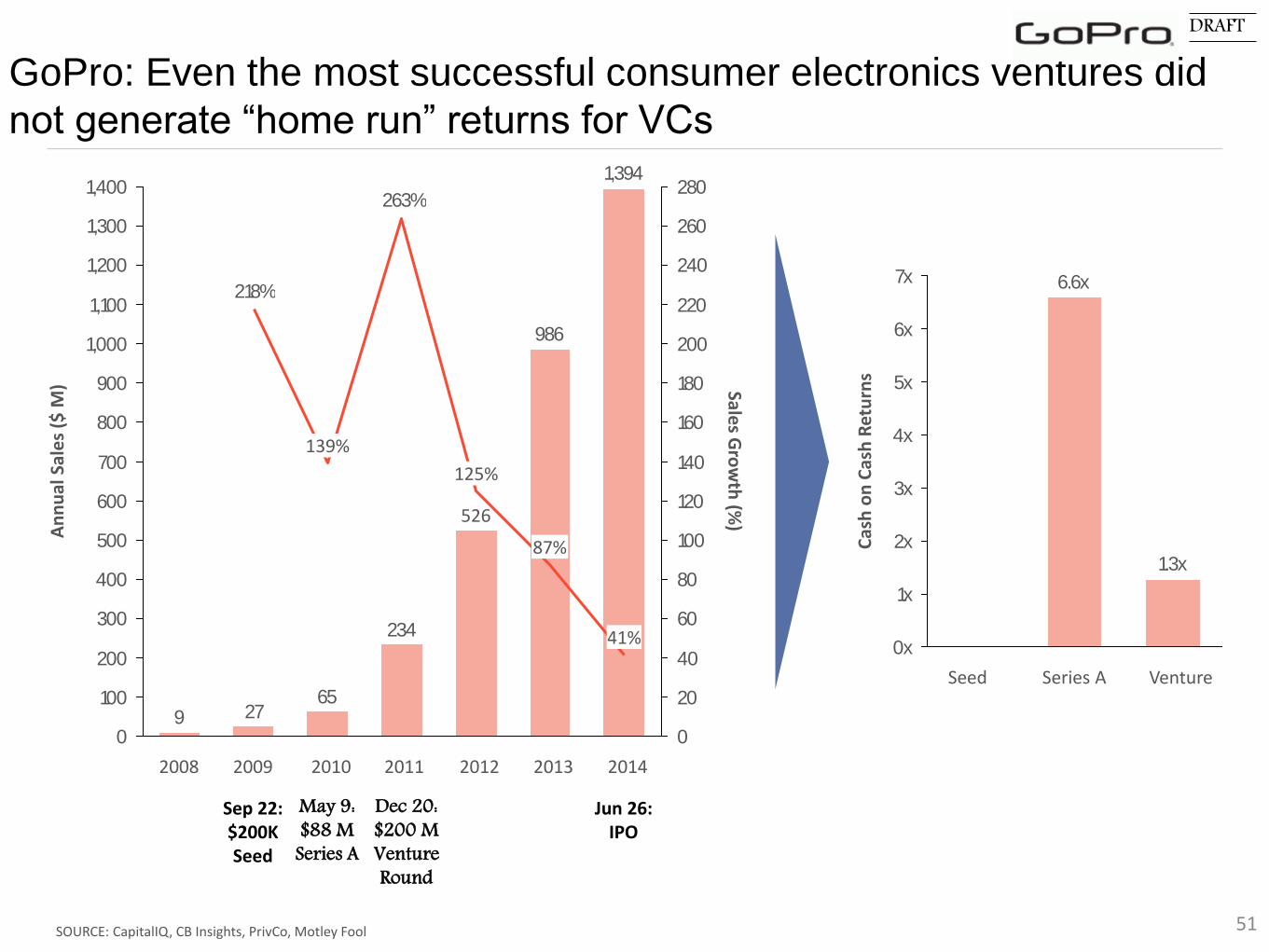

GoPro: Even the most successful consumer electronics ventures did

not generate “home run” returns for VCs

SOURCE: CapitalIQ, CB Insights, PrivCo, Motley Fool 51

1,394

986

234

65279

263%

218%

0

100

200

300

400

500

600

700

800

900

1,000

1,100

1,200

1,300

1,400

0

20

40

60

80

100

120

140

160

180

200

220

240

260

280

Sales G

row

th (%

)

An

nu

al S

ale

s ($

M)

20092008

41%

125%

201320112010 2014

87%

2012

526

139%

1.3x

6.6x

0x

1x

2x

3x

4x

5x

6x

7x

VentureSeries ASeed

Cas

h o

n C

ash

Ret

urn

s

May 9: $88 M

Series A

Sep 22: $200K Seed

Dec 20:$200 M Venture Round

DRAFT

Jun 26: IPO

Fitbit success demonstrates that consumer electronics

can exhibit exponential growth trajectories

SOURCE: Forbes 52

DRAFT

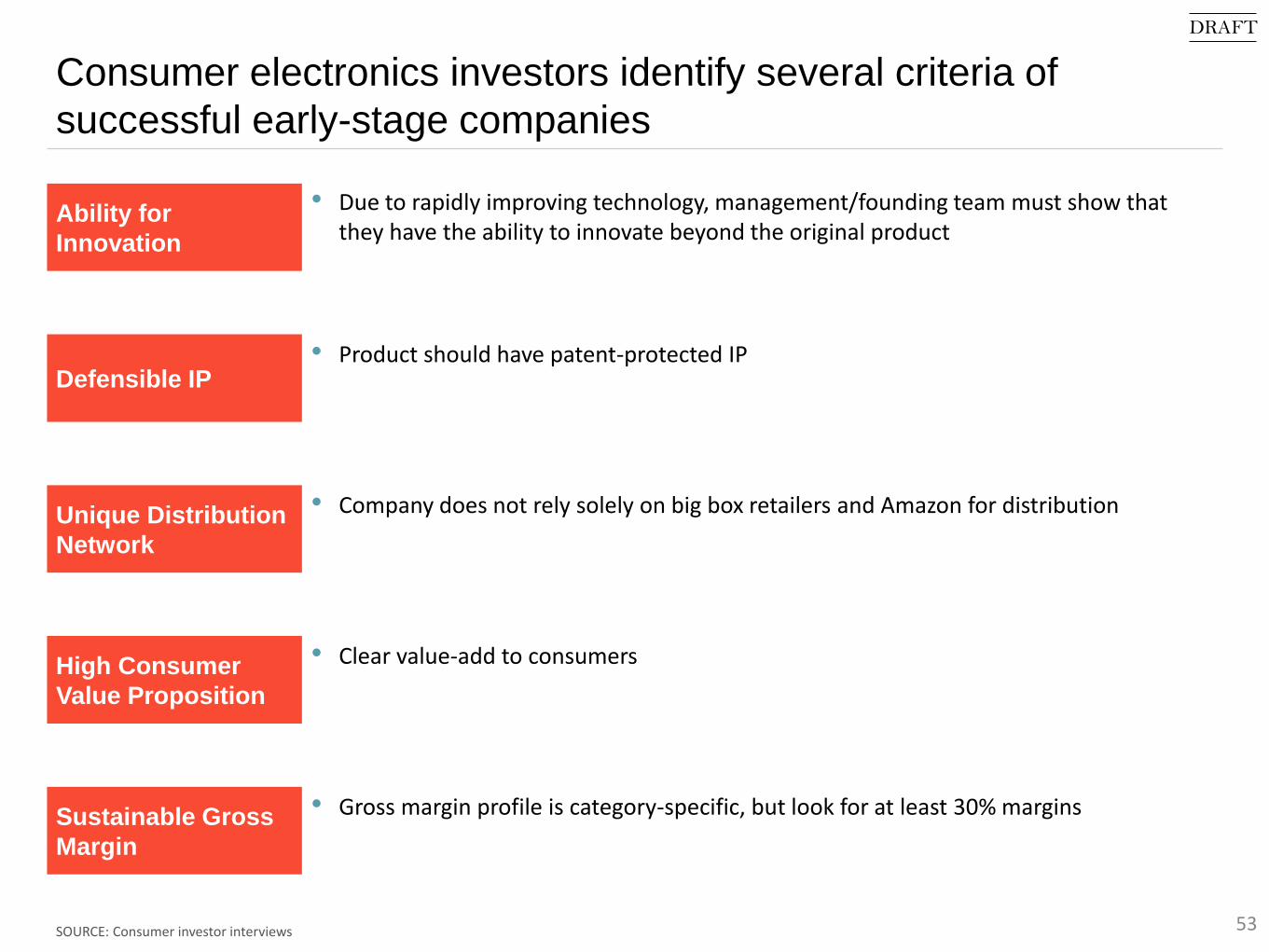

Consumer electronics investors identify several criteria of

successful early-stage companies

SOURCE: Consumer investor interviews 53

Ability for

Innovation

• Due to rapidly improving technology, management/founding team must show that they have the ability to innovate beyond the original product

Defensible IP• Product should have patent-protected IP

Unique Distribution

Network

• Company does not rely solely on big box retailers and Amazon for distribution

High Consumer

Value Proposition

• Clear value-add to consumers

Sustainable Gross

Margin

• Gross margin profile is category-specific, but look for at least 30% margins

DRAFT

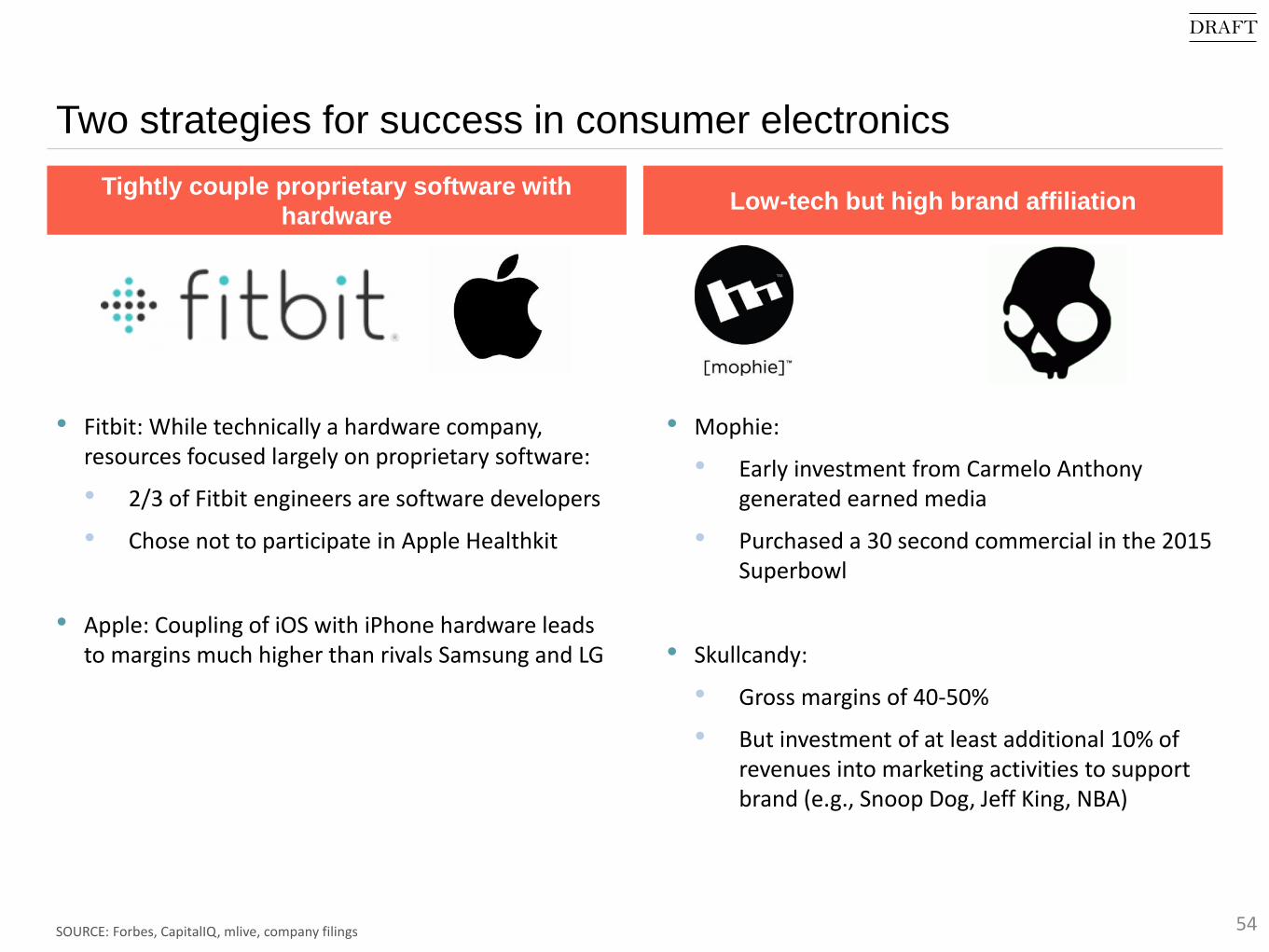

Two strategies for success in consumer electronics

SOURCE: Forbes, CapitalIQ, mlive, company filings 54

Tightly couple proprietary software with

hardwareLow-tech but high brand affiliation

• Fitbit: While technically a hardware company, resources focused largely on proprietary software:

• 2/3 of Fitbit engineers are software developers

• Chose not to participate in Apple Healthkit

• Apple: Coupling of iOS with iPhone hardware leads to margins much higher than rivals Samsung and LG

• Mophie:

• Early investment from Carmelo Anthony generated earned media

• Purchased a 30 second commercial in the 2015 Superbowl

• Skullcandy:

• Gross margins of 40-50%

• But investment of at least additional 10% of revenues into marketing activities to support brand (e.g., Snoop Dog, Jeff King, NBA)

DRAFT