revenue & receipts cycle – internal controls & test of controls

TRANSCRIPT

Revenue & Receipts Cycle –Internal Controls &

Test of Controls

REFERENCES

• Internal control knowledge

• International Standard on Auditing (ISA) 315 &330“Identifying and assessing the risks of material misstatement through understanding the entity and its environment” and responding thereto – selected paragraphs

LEARNING OUTCOMES

Revenue & receipts system; controls readdressed (Revision)Mostly self study1. Understand the internal control structure of the cycle including major

classes of transactions and affected accounts2. Understand and describe the cycles functional areas3. Design a system of controls for the revenue and receipt cycle4. Identify and explain weaknesses in the control systems and make

recommendations for improvementAuditors application 5. Understand the decision tree for deciding on when to follow a “test of

control” approach6. Identify and describe the “key internal controls” on which to place

reliance7. Understand the direction of testing when performing tests on the key

internal controls8. Describe the test of control procedures9. Understand the consequences of exceptions found during the testing of

internal controls

• Classes of transactions affected:

SALES and SALES RETURNS (revenue) RECEIPT transactions (movements in cash & bank balances)

• Account balances affected:

ACCOUNTS RECEIVABLE (Including trade debtors and allowances for doubtful debts)

CASH and BANK

INTRODUCTION TO THE CYCLE

Consider: 2.1 Variation amongst entities2.2 Cash sales2.3 Credit sales2.4 Legislation

BASIC FUNCTIONSIN THE CYCLE

AN 10/2-10/3

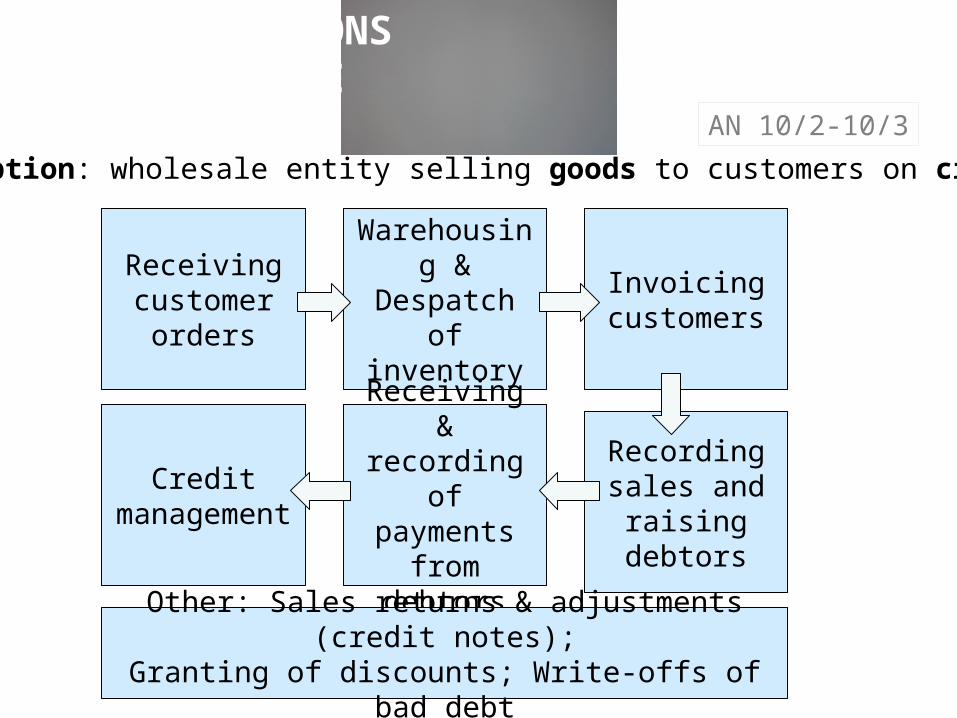

Assumption: wholesale entity selling goods to customers on credit:

Receiving customer

orders

Warehousing & Despatch of

inventory

Invoicing customers

Recording sales and

raising debtors

Receiving & recording of payments

from debtors

Credit management

Other: Sales returns & adjustments (credit notes);Granting of discounts; Write-offs of bad debt

Approval and authorisation What level of staff should

approve/authorize?

Segregation of dutiesBetween execution, authorization,

custody of asset, recording.

Isolation of responsibilityEmployee acknowledges performing duty

Access and custody controls (security) Protecting assets and information

Comparisons and reconciliations Between what? Who performs it?

CONTROL ACTIVITIES IN THE CYCLE

Categories of control activities

INFORMATION FLOW IN THE CYCLE

Credit management• Credit application form

None

Order department• Customer order• Internal sales order

None

Warehouse/despatch• Picking slip• Delivery note

[Inventory items removed from inventory register. G/L entries depend on periodic vs. perpetual].

Functional area and documents/records prepared

Accounting entries in general ledger

INFORMATION FLOW IN THE CYCLE

Invoicing• Customer invoice

Functional area and documents/records prepared

Accounting entries in general ledger

None

Recording of sales• Sales journal• Debtors ledger

Debit Trade debtors Credit Sales

Receiving cash• Receipt• Deposit slip• Remittance register

None

INFORMATION FLOW IN THE CYCLE

Recording of receipts• Cash book• Debtors ledger

Debit Bank Credit Trade debtors

Functional area and documents/records prepared

Accounting entries in financial records\

Sales returns and adjustments• Goods returned voucher (GRV)• Credit note

Debit (Returns)/sales Credit Trade debtors

BOOKKEEPING IN THE CYCLE

• ISO• DN

Sales journal

Debtors ledger

General ledger

• Remitt adv.• Bank stmt.• Dep. slip• Receipt

Cash book

Debtors ledger

INV

General ledger

Financial statements

Trial balanceReconciliations:Bank recon: Bank statement & GL (cash book)Debtors recon: Debtors ledger & GL debtors control a/c

OBJECTIVES OF INTERNAL CONTROLS (REVISION)

Validity

AccuracyCompleteness

= V, A, C

of reco

rded

financia

l inform

ation!

A proper accounting system and related internal controlswill achieve the “control objectives” of Validity, Accuracy and

Completeness of financial information.

• Why does management want V, A and C of financial information?• Why is an auditor interested in whether controls achieve V, A, C?

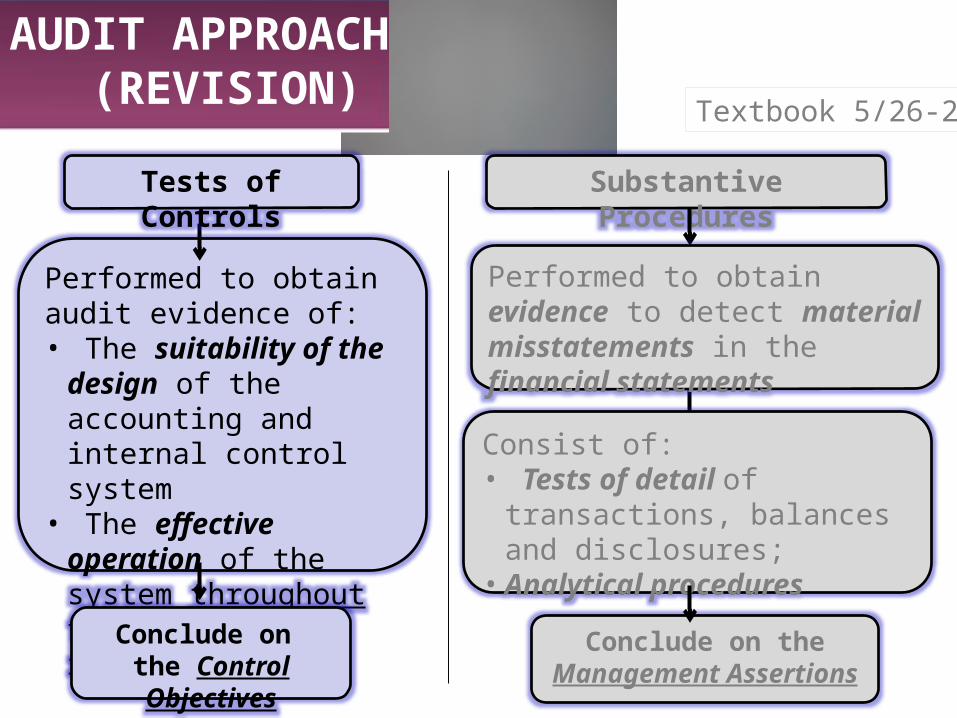

Performed to obtain audit evidence of:• The suitability of the

design of the accounting and internal control system

• The effective operation of the system throughout the period of reliance.

Tests of Controls

AUDIT APPROACH (REVISION)

Substantive Procedures

Textbook 5/26-27

Performed to obtain evidence to detect material misstatements in the financial statements

Conclude on the Control Objectives

Conclude on the Management Assertions

Consist of:• Tests of detail of transactions,

balances and disclosures;• Analytical procedures

Tests of controls must be performed when (ISA 315, para. 08):

• Risk assessment includes an expectation that controls are operating effectively

• Risks identified for which substantive procedures alone do not provide sufficient appropriate evidence

TESTS OF CONTROLS- INTRODUCTION

However, even if test of control approach followed, substantive procedures are compulsory for each material class of

transactions, account balance and disclosure (ISA 330, para. 18)

TESTS OF CONTROLS - NATURE

Purpose of audit procedures (including tests of controls): Are the financial statements fairly presented?

:: Focus is thus on the recorded financial information ::

Are there controls in place that can achieve fair presentation through Validity, Accuracy and Completeness

of recorded financial information?

If so, perform test procedures on those controls to determine whether: there is evidence of the control having taken place; the control operated effectively as intended.

TESTS OF CONTROLS - NATURE

Perform tests of controls by applying the following procedures:

Inquiry Observation Inspection

Reperformance

Evidence control took place

Evidence control operated effectively

Example:Manager’s signature on bank recon as evidence of review: Really reviewed? Reviewed it appropriately?

Therefore, reperform to obtain evidence on operating effectiveness of the control.

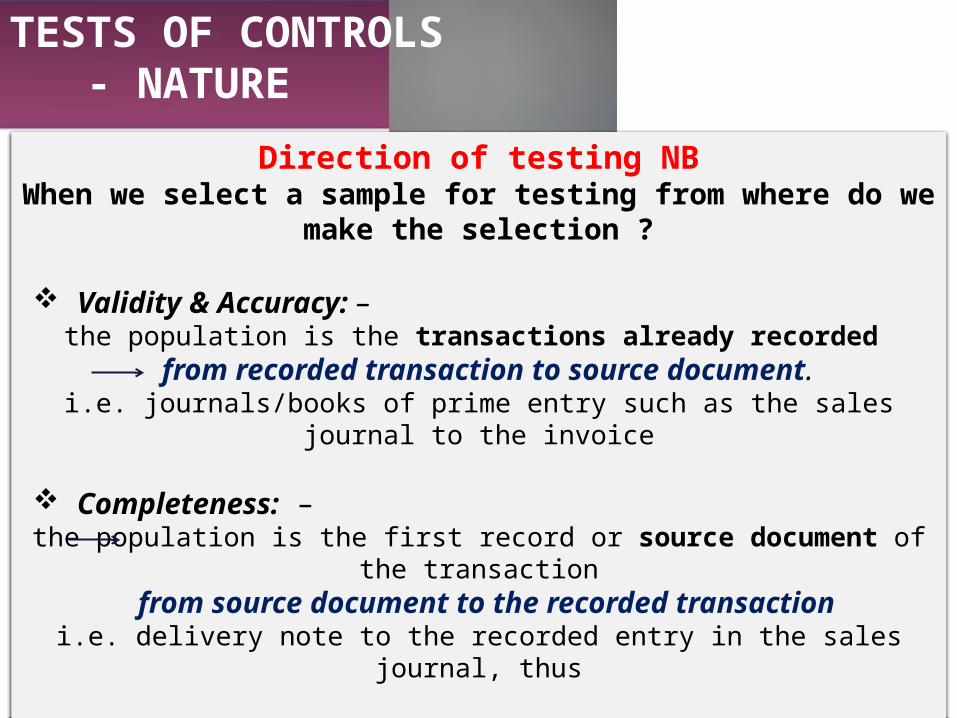

TESTS OF CONTROLS - NATURE

Direction of testing NBWhen we select a sample for testing from where do we make the

selection ?

Validity & Accuracy: – the population is the transactions already recorded

from recorded transaction to source document.i.e. journals/books of prime entry such as the sales journal to the invoice

Completeness: – the population is the first record or source document of the transaction

from source document to the recorded transactioni.e. delivery note to the recorded entry in the sales journal, thus

Applying an incorrect direction of testing when answering a question will lead to an irrelevant/incorrect answer.

• However, not test ALL controls (impractical and costly) • Test only KEY controls (those wish to place reliance on)

• ISA 315, para. A60: “Not all … controls are relevant to the auditor’s risk assessment.”

• Which controls are “KEY”? “Key” = measure of extent to which the control addresses the risk

involved.

TESTS OF CONTROLS - EXTENT

“Extent” = “How much to test”The more reliance placed on controls, the more tests of

controls to perform on those controls in order to JUSTIFY the reliance.

Which controls are “KEY”?

Example: consider RISK OF INCOMPLETE recording of sales transactions in sales journal:

Control 1: “Invoices are pre-printed and sequentially numbered”

vs.Control 2: “The senior bookkeeper reviews the sequential

numbering of invoices recorded in the sales journal and follows up on missing entries”.

Which is “KEY” control?

TESTS OF CONTROLS - EXTENT

Distinguish between key controls and mere supporting (indirect) controls!

• Tests of control can be performed several months before year end (“interim audit”).

• Advantages of this include:

Time & opportunity to amend the substantive audit program (in case exceptions found and reliance not justified);

Reduce time pressure during final audit.

• However, the auditor needs evidence about the operation of controls throughout the year (ISA 330 para 12).

• Thus also test intervening months between interim and year-end.

TESTS OF CONTROLS - TIMING

“Timing” = “When to test”

Exceptions occur when a internal control procedure is:

• not applied• not applied correctly and consistently• applied by an unauthorised person

NOTE: An exception in a transaction of R 1 million carries the same weight as an exception in a transaction of R 1. Why?

Accordingly, tests of controls are NOT value orientated! The control is tested, and not the underlying financial value.

TESTS OF CONTROLS - EXCEPTIONS

What if exceptions in internal controls are found by auditor?I.e. impact on audit approach?

ANSWERING “TEST OF CONTROL” QUESTIONS IN THE CYCLE

1. Identify key control in scenario (i.e. controls you’d rely on for purpose of concluding on fair presentation of financial information)

2. Identify control objective applicable (V, A and/or C)

3. Determine direction of testing (recorded financial information to supporting doc or supporting doc to recorded financial information)

4. State selection and source of sample (e.g. sales journal / invoices)

5. Consider hierarchy of audit evidence reliability (source, nature)

6. Formulate and describe test of control procedure inquire, observe, inspect: evidence that control took place reperform: test operating effectiveness of control.

[Audit verb] [Party/Process/Document] [Purpose]

SYSTEM You are the senior in charge of the audit of Office Space (Pty) Ltd, a wholesale company which sells office furniture. During the planning phase of the current audit you established that the system for the processing of sales is as follows: Sales OrdersOrders are received from retailers across the country. The majority of orders are faxed to the company, while some are received by phone. A sales order clerk writes out a sequentially numbered internal sales order (ISO) for both the fax and telephone orders. A second sales order clerk checks the calculations on the ISO back to the faxes received.

Credit ControlThe sequentially numbered ISOs are, from time to time, passed to the credit controller during the day who confirms that the customer is still within his/her credit limit and authorizes the sale by signing the order. The ISOs are given back to the sales order clerk who transfers a copy of the ISO to the head of stores.

EXAMPLEYOU ARE REQUIRED TO: Identify internal control procedures present in the system that you would wish to place reliance on, and describe test of control procedures you would perform to obtain reliable evidence about the performance of each control identified.

Internal control procedure

Test of control

1. Credit control:Credit controller assesses the credit-worthiness of each customer and authorizes each sale by signing the ISO.

(Validity of sales : Authorization)

1.1.

1.2.

1.3.

1.4.

Select a sample of sales transactions recorded in sales journal, follow through to the supporting invoice and:1.1.1 Inspect the corresponding ISO for

the approval signature of the credit controller.

(Note: direction of testing)

Enquire of management regarding the reliability of the credit control function.

Enquire of the credit controller regarding his function and the likelihood of fictitious/invalid orders getting past him/her.

Reperform the creditworthiness check to confirm the check was properly performed by the credit controller (operating effectiveness).

Suggested solution: Office Space (Pty) Ltd

Warehousing and Dispatch

The head of stores, on the authority of the signed ISO, requests a store man to pick the goods from the store and authorizes the store man to transfer the goods to the dispatch clerk. The head of stores agrees the ISO to the goods actually picked, then stamps the order "filled" and signs it.

The dispatch clerk prepare a sequentially pre-numbered delivery note for each order. The delivery note and the ISO are cross-referenced. The fast copy remains in the delivery note book and the two top copies are torn out and packed, with the boxed goods, into the delivery truck. Gate control personnel conduct checks on the trucks leaving the premises by checking that all goods in the truck appears on the delivery note accompanying the goods.

The top copy of the delivery note is left with the customer and the second copy is signed by the customer to be returned to the invoicing section.

2. Gate controlGate personnel conduct checks on goods leaving the premises.

(Completeness of sales)

2.1

2.2

2.3

2.4

Observe the checking of trucks and goods by gate control personnel.By reperformance, select trucks leaving the premises and compare the content with the accompanying delivery note.Enquire of management as to the reliability of the gate control and any problems which may have occurred.Enquire of the gate control personnel regarding their function to ensure they understand what is expected of them.

Internal control procedure Test of control

3. Customers are required to sign delivery notes as acknowledgement of receipt of goods.

(Validity of sales : Authenticity)

3.1 For the sample of sales invoices selected in 1.1 above: agree by inspection of the invoice

the corresponding customer signed delivery note to confirm evidence of the customer ‘s acknowledgement of receipt.

(Note: direction of testing)

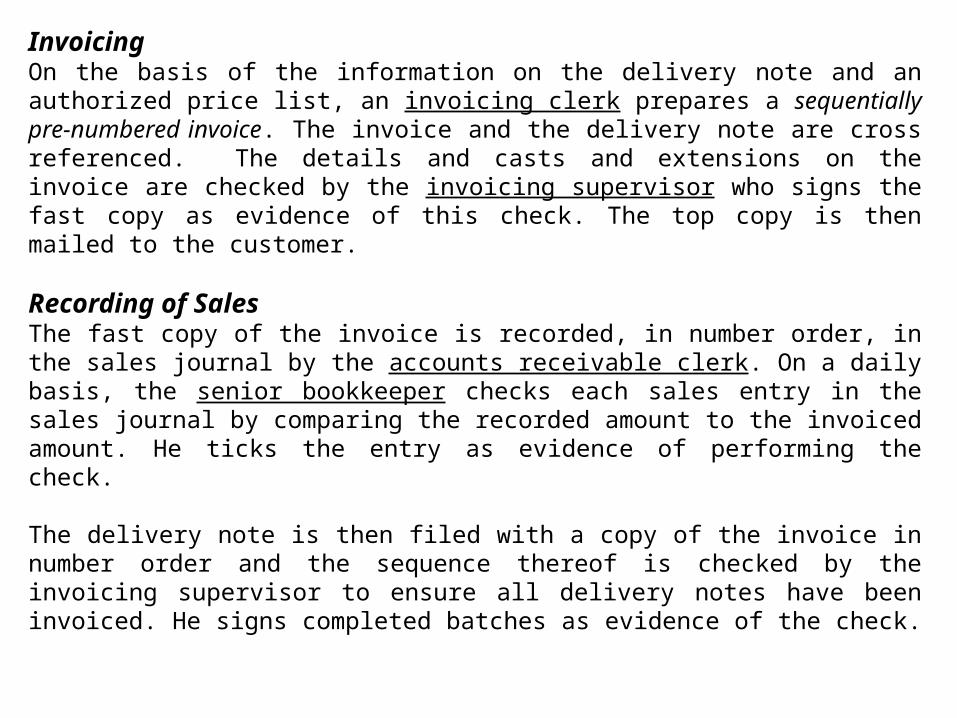

InvoicingOn the basis of the information on the delivery note and an authorized price list, an invoicing clerk prepares a sequentially pre-numbered invoice. The invoice and the delivery note are cross referenced. The details and casts and extensions on the invoice are checked by the invoicing supervisor who signs the fast copy as evidence of this check. The top copy is then mailed to the customer.

Recording of SalesThe fast copy of the invoice is recorded, in number order, in the sales journal by the accounts receivable clerk. On a daily basis, the senior bookkeeper checks each sales entry in the sales journal by comparing the recorded amount to the invoiced amount. He ticks the entry as evidence of performing the check.

The delivery note is then filed with a copy of the invoice in number order and the sequence thereof is checked by the invoicing supervisor to ensure all delivery notes have been invoiced. He signs completed batches as evidence of the check.

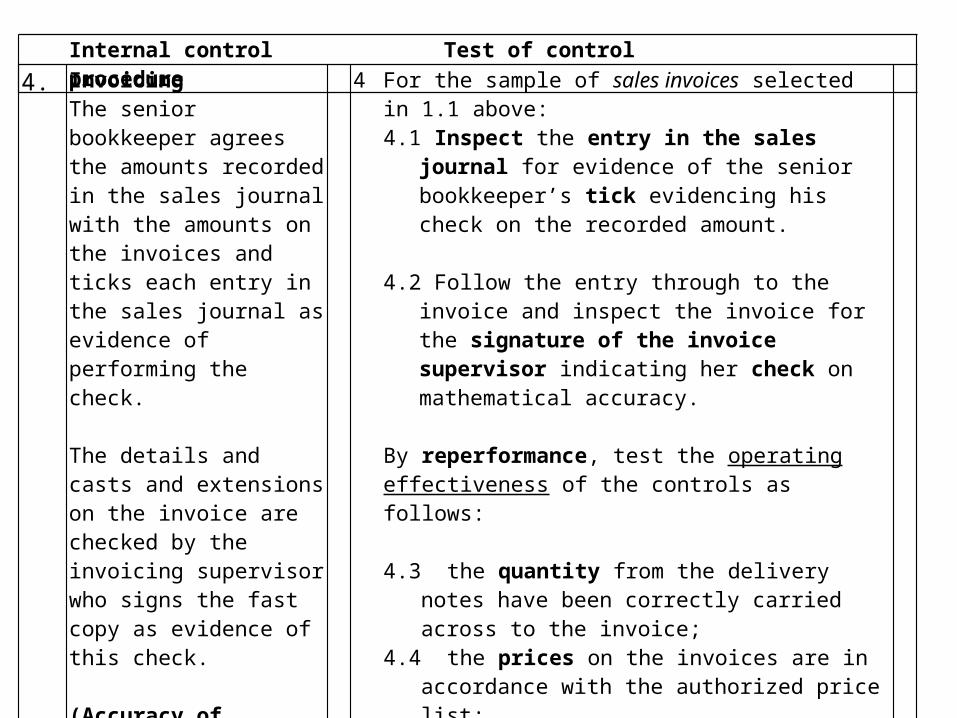

4. InvoicingThe senior bookkeeper agrees the amounts recorded in the sales journal with the amounts on the invoices and ticks each entry in the sales journal as evidence of performing the check.

The details and casts and extensions on the invoice are checked by the invoicing supervisor who signs the fast copy as evidence of this check.

(Accuracy of revenue)

4 For the sample of sales invoices selected in 1.1 above:4.1 Inspect the entry in the sales journal for

evidence of the senior bookkeeper’s tick evidencing his check on the recorded amount.

4.2 Follow the entry through to the invoice and inspect the invoice for the signature of the invoice supervisor indicating her check on mathematical accuracy.

By reperformance, test the operating effectiveness of the controls as follows:

4.3 the quantity from the delivery notes have been correctly carried across to the invoice;

4.4 the prices on the invoices are in accordance with the authorized price list;

4.5 each invoiced amount has been correctly recorded in the sales journal;

4.6 casts and extensions are correct on invoice and in the sales journal.

Internal control procedure Test of control

5. Invoicing:The delivery note is filed in number order with the invoice and the sequence thereof is checked by the invoicing supervisor, who signs completed batches as evidence of the check.

(Completeness of revenue)

5.1

5.2

Inspect the batches of the delivery notes in the invoicing section for signature of the invoicing supervisor indicating the sequence check for completeness of invoiced delivery notes.

Reperform the sequence check on delivery notes.

Select a sample of delivery notes and, using the cross-referencing, inspect the corresponding fast copy invoice, and trace the invoice to the sales journal. (Note: direction of testing)

Internal control procedure Test of control

Thank you! Dankie! Enkosi Kakhulu!!

END

When answering “weakness” questions, remember the following:

Read the scenario and the ‘required’ very carefully!

Know the difference between ‘identify’, ‘explain’ and ‘recommend’.

‘Weakness’ should be in detail and must be relevant to the scenario and required.

‘Explanation’ should explain “what can go wrong/what are the risks involved”.

Recommendation must be in detail : specify the actual control procedure and not simply the control objective:

e.g. “All sales should be recorded” (control objective) vs.

“Sequential numbering of recorded invoices in the sales journal should be reviewed by Mr A Countant on a regular basis for missing numbers (control procedure)

ANSWER TECHNIQUE

The following is not acceptable when answering weakness questions:

Stating the control activity category as a weakness (e.g. “No division of duties”) rather than the control weakness in the activity itself (e.g. “Person receiving orders from customers also ships inventory items to customers”).

Making vague references to responsibility levels, e.g. stating a control procedure should be performed by a “second clerk” or “a senior staff member” if the scenario clearly indicates the titles of the positions in the entity and the staff members’ names. (e.g. “financial accountant”/Mr A Countant).

Making assumptions that are not relevant to the scenario or the type of business.

Allocating tasks to incorrect levels of authority, e.g. “financial manager should perform the bank reconciliation” while there clearly is a bookkeeping clerk available to do so. Clerks are the staff performing most functions and executing most controls! Senior staff and management approve, authorize and review etc.

ANSWER TECHNIQUE (CONTINUED)