review of retail floorspace demand

TRANSCRIPT

Directions for Bay Street Review of Retail Floorspace Demand

City of Port Phillip December 2008

This Report has been prepared for:

This report has been prepared by: SGS Economics and Planning Pty. Ltd.

ACN 007 437 729

5th Floor, 171 Latrobe Street,

Melbourne Victoria 3000

phone: 61 3 8616 0331

fax: 61 3 8616 0332

email: [email protected]

web: www.sgsep.com.au

Offices in Melbourne, Sydney, Brisbane, Hobart, Canberra

Table of Contents

20082125 Future Directions for Bay Street_04_Final.doc

Table of Contents

Executive Summary ..................................................................... 1

1 Introduction ........................................................................ 3

1.1 Background ............................................................................................................ 3 1.2 Task ...................................................................................................................... 4 1.3 Study Area ............................................................................................................. 5

2 Retail Floor Space Demand Analysis ....................................... 7

2.1 Available Retail Expenditure ...................................................................................... 7 2.2 Bay Street Activity Centre Turnover ............................................................................ 9 2.3 Bay Street Floorspace Demand ................................................................................ 10 2.4 Impact Assessment ............................................................................................... 13

2.4.1 Scenario 1 ............................................................................................... 14 2.4.2 Scenario 2 ............................................................................................... 14 2.4.3 Impact Analysis Results ............................................................................. 14 2.4.4 Comparison of Results ............................................................................... 17

3 The Strategic Context for Bay Street .................................... 18

3.1 'City to Bay Boulevard' Plan in 1980s ........................................................................ 18 3.2 Inner Melbourne Action Plan (IMAP).......................................................................... 21 3.3 International Interest in Public Transport Boulevards ................................................... 26 3.4 Prospects for a Bay Street Boulevard Today ............................................................... 27

3.4.1 Urban Form of Boulevard ........................................................................... 30 3.5 Planning and Design of Bay Street, Port Melbourne ..................................................... 32

3.5.1 Niches for Bay Street................................................................................. 32

Appendix .................................................................................. 36

Economic and Social Order in Retailing and Shopping .................................................. 36

Tables

Table 1: National Retail Expenditure Per Capita (2006$) ......................................................... 8 Table 2: Bay Street Household Expenditure Variation by Income (2003 $) ................................. 8 Table 3: Retail Expenditure in Bay Street by residents in Bay Street and surrounding areas 2006 to

2021 ............................................................................................................... 9 Table 4: Retail Turnover of Bay Street Activity Centre 2006 to 2021 ......................................... 9 Table 5: Business as Usual Forecast RTD ........................................................................... 10 Table 6: Bay Street Retail Floorspace 2008 ........................................................................ 10 Table 7: Standard RTD (2006$) ....................................................................................... 11

Table of Contents

20082125 Future Directions for Bay Street_04_Final.doc

Table 8: Bay Street Floorspace Demand ............................................................................ 12 Table 9: Williamstown Road Development Assumptions (Zone 80) ......................................... 14 Table 10: Impact Assessment for Bay Street - Summary ...................................................... 16 Table 11: Future Directions Strategy Paper January 2006 Results Vs. 2008 Retail Forecasts ....... 17

Figures

Figure 1: Bay Street Context ............................................................................................. 5 Figure 2: National Retail Spending per Capita ....................................................................... 7 Figure 3: Competing Centre for Impact Assessment. ............................................................ 13 Figure 4: Impact on Turnover in Bay Street ........................................................................ 15 Figure 5: Physical Framework (Fig.15) ............................................................................... 19 Figure 6: Development Proposals (Fig.16) .......................................................................... 20 Figure 7: Multiple Links (neither fig number cited nor key provided) ....................................... 21 Figure 8: Portland Metro Corridor Concept Diagram ............................................................. 26 Figure 9: Portland Metro Corridor Map ............................................................................... 27 Figure 10: Bay Street – North View ................................................................................... 28 Figure 11: Bay Street – South View .................................................................................. 28 Figure 12: Southbank to the Bay Link................................................................................ 29 Figure 13: Typical Boulevard Profile ................................................................................... 30 Figure 14: City of Melbourne: Swanston Street profile with tram tracks and ‘Copenhagen’ bicycle

lanes ............................................................................................................ 31 Figure 15: Profile of Typical Boulevard in Portland (Oregon) .................................................. 31

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 1

Executive Summary

Bay Street is a designated ‘major’ activity centre under Melbourne 2030 and subsequently in

planning must be consistent with the metropolitan strategy. The Inner Melbourne Action Plan

(IMAP) is a joint venture of the municipalities of Melbourne, Port Phillip, Yarra and Stonnington to

achieve cooperation and plan coordination between themselves in implementing Melbourne 2030.

Given the rapid growth of residential development over the last 10 years in Port Melbourne, in and

around Bay Street, the retail growth potential is quite significant. SGS estimates show Bay Street

will have a retail turnover of $142.4 million by 2021 (a 3.3% growth from 2006), led by the

Supermarkets commodity sector, Hospitality and Services and Other Food. The growth in turnover

is translated into a demand for retail floorspace of 10,343 sqm. With respect to

accommodating the floorspace demand in Bay Street, it is important to look at the overall strategic

direction as SGS’s conclusion is that Bay Street should be recognised and planned as one of

Melbourne’s strategic boulevards that combined with its extension along City Road radiate from the

City to the Bay.

Currently the model of a boulevard that serves as a major transportation conduit is popular

internationally for restructuring established urban areas to be more pedestrian and public transport

friendly. These boulevards are commonly planned and developed as transport conduits with higher

density housing along them, rather like what is already being developed along Bay Street.

An appropriate way of identifying the niches to be introduced or strengthened along Bay Street is

to identify existing magnet destinations around which complementary dependent businesses can be

clustered. Bay Street has several magnet facilities with varying degrees of drawing power and

potential:

• Beach destination and scene: foreshore of Port Philip Bay. The iconic entertainment

venue of Circus Oz is part of this

• Food-for-the-home: supermarkets

• Government services: especially local government such as public library, community

centre.

The precinct between Rouse Street and Beach Street (and along Beach Street) has special

potential because of its proximity to the foreshore and the Bay. This precinct could and should be

developed as a tourist/day tripping destination to rival Acland Street. There is a need for some

urban design branding that could and should be used to make this south precinct distinctive from

the remainder of Bay Street.

The waterfront around Station Pier is already evolving into a substantial tourist destination and

this could be reinforced by creative redevelopment of the south end of Bay Street and the

foreshore area between the two along Beach Street. This could be provided in the form of

entertainment venues to complement the pubs in the south end, and establishing more prominent

hospitality and services to entice visitors from the Pier, to venture to Bay Street.

‘Food for the home' is a very important and very large niche: the basic essentials in any

community. Most of the food-for-the-home businesses are located between Rouse Street and

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 2

Bridge Street. This is the core retailing in the Bay Street activity centre and it should be planned

for it to remain so. Demand for Other Food, should be accommodated in and around this precinct.

Recently in Melbourne there has emerged a network of farmer’s markets. There is already a

farmers’ market held in the Gasworks Park once per month and it is a popular shopping destination

that draws in customers from across the immediate sub-region. It is again recommended that a

farmers’ market be established along Bay Street, preferably in the vicinity of the other food-for-

the-home shopping facilities so as to exploit potential synergy and to absorb some of the Other

Food commodity demand. This should function on alternative days to Gasworks Park.

There may be a prospect for reinforcing the food-for-the-home niche by attracting an additional

supermarket such as Aldi or Safeway. With appropriate positioning this could help reinvigorate the

north end of the precinct as has previously been suggested by SGS.

Bay Street is fortunate in that it has an active library at the north end: in the block between

Spring Street North and Spring Street South. The Port Melbourne public library at the north

end of Bay Street could and should be made an anchor for a business niche and spatial precinct

that includes not only the library itself but other ancillary retail uses. Libraries are the most

frequented cultural facilities in any community and they offer a basis for a range of small business

that can exploit this drawing power. Shops retailing computers, computer services, books, music,

stationary, coffee/ wine, and the like, can benefit from exposure to people who use the library.

The suggestions made above, compare quite strongly in their nature to the ‘Future Directions Paper

January 2006’. Recurring themes include a demand for another supermarket in the established

core or in the north, strengthening the retail offer around the library, and providing a stronger

Hospitality and Services/Tourism offer near beach end of Bay Street.

Bay Street, as mentioned has some key core strengths, it is predominantly a Hospitality and

Services centre, with Supermarkets and Other Food as the highest contributors to turnover. The

development of a centre in the Business 3 Zone on Williamstown Road will not have a substantial

impact on Turnover in Bay Street. The only impact would be a reduction in the demand for

Household goods and Other Retail on Bay Street, by a maximum of 2,000 sqm.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 3

1 Introduction

Given the growth in residential apartment development over the last 10 years and limited potential

development sites in Bay Street, City of Port Phillip has commissioned SGS to update the

information, statistics and estimates of the Activity Centres Review – Future Directions Strategy

Paper January 2006 to inform the background research for a structure plan for Bay Street.

1.1 Background

As identified in Future Directions Paper January 2006, Bay Street’s:

Strengths include:

• Coles supermarket providing a major retail anchor in the street.

• Heritage buildings providing character to an attractive streetscape.

• A diverse range of retail tenants.

• Day and night activity contributed to by Bay Street’s proximity to Station Pier and the

foreshore.

• A variety of residential accommodation and housing forms.

Weaknesses include:

• Insufficient retail along parts of the south side of Bay Street.

• Public transport along Bay Street, no train and no foreshore transit based connection to

St.Kilda.

• New development impacting on heritage built form.

• Use of lanes to link pedestrians to Bay Street.

As a designated major activity centre, Bay Street needs to position itself to respond to:

• A 64.6% increase in residential population over the last 10 years in Port Melbourne

(Census data 2006).

• An increase in the mix and diversity of retail opportunities.

• Providing a connectedness between Station Pier and the foreshore and the retail corridor.

• Improving the pedestrian experience into and out of the street by utilising existing lanes

and encouraging “through block” access in new developments. The key strategic directions for Bay Street Port Melbourne aim to:

• Strengthen the physical, visual and active connections between the waterfront, Bay Street

and Station Pier

• Increase visitor shopping activity and visitor facilities and services in Waterfront Place and

Beach Street

• Maintain and extend the mix and integration of land uses and activity in Bay Street

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 4

• Protect the local urban character and townscape image

• Reinforce the current supermarket complex as the retail core

• Encourage pedestrian movement in surrounding streets

1.2 Task

• Use 2006 census data to review statistics and document findings in relation to:

-Retail turnover

-Projected turnover (to 2021)

-Projected net retail growth (to 2021)

-Retail floor space demand

• As it is not clear if there are any potential development sites available in Bay Street and/or

located in the Business 1 Zone and given the rapid growth of residential development over

the last 10 years in Port Melbourne, in and around Bay Street, where will the projected

total floor space demand of 21,727sqm (Jan 2006) or a revised projection as per above, be

accommodated?

• Highlight any changes in business/retail type and/or use that are documented in the Future

Directions Paper January 2006 for different precincts.

• Investigate the impact of a retail centre in the Business 3 Zone on Williamstown Road to

the north west of Bay Street. (Eg. Bunnings has now established on Williamstown Road.

This is not an activity centre and relies on car based visitation).

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 5

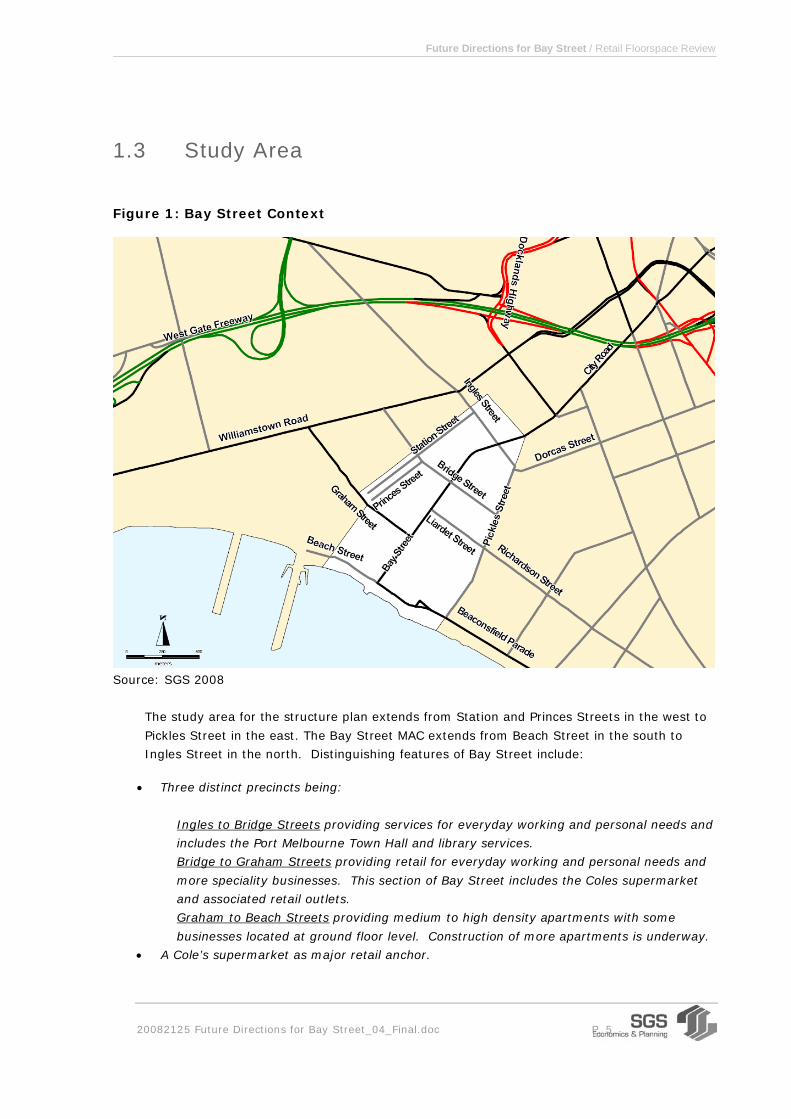

1.3 Study Area

Figure 1: Bay Street Context

Source: SGS 2008

The study area for the structure plan extends from Station and Princes Streets in the west to

Pickles Street in the east. The Bay Street MAC extends from Beach Street in the south to

Ingles Street in the north. Distinguishing features of Bay Street include:

• Three distinct precincts being:

Ingles to Bridge Streets providing services for everyday working and personal needs and

includes the Port Melbourne Town Hall and library services.

Bridge to Graham Streets providing retail for everyday working and personal needs and

more speciality businesses. This section of Bay Street includes the Coles supermarket

and associated retail outlets.

Graham to Beach Streets providing medium to high density apartments with some

businesses located at ground floor level. Construction of more apartments is underway.

• A Cole’s supermarket as major retail anchor.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 6

• A proliferation of businesses between Ingles and Beach Streets with an increased number

of beauty salons, hairdressers, real estate and travel agents indicating an increased

affluence in the area.

• An attractive streetscape.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 7

2 Retail Floor Space Demand Analysis

2.1 Available Retail Expenditure

The latest population projections were obtained from the DSE on an SLA basis across Victoria.

These projections are based on the 2001 ABS Census, and take into account policies such as

Melbourne 2030. These population projections were then adapted to Journey to Work Travel Zone

(2001) based on land availability (as published in the 2006 Urban Development Program by the

DSE) and ABS ERP figures for 2006, for use in retail modeling.

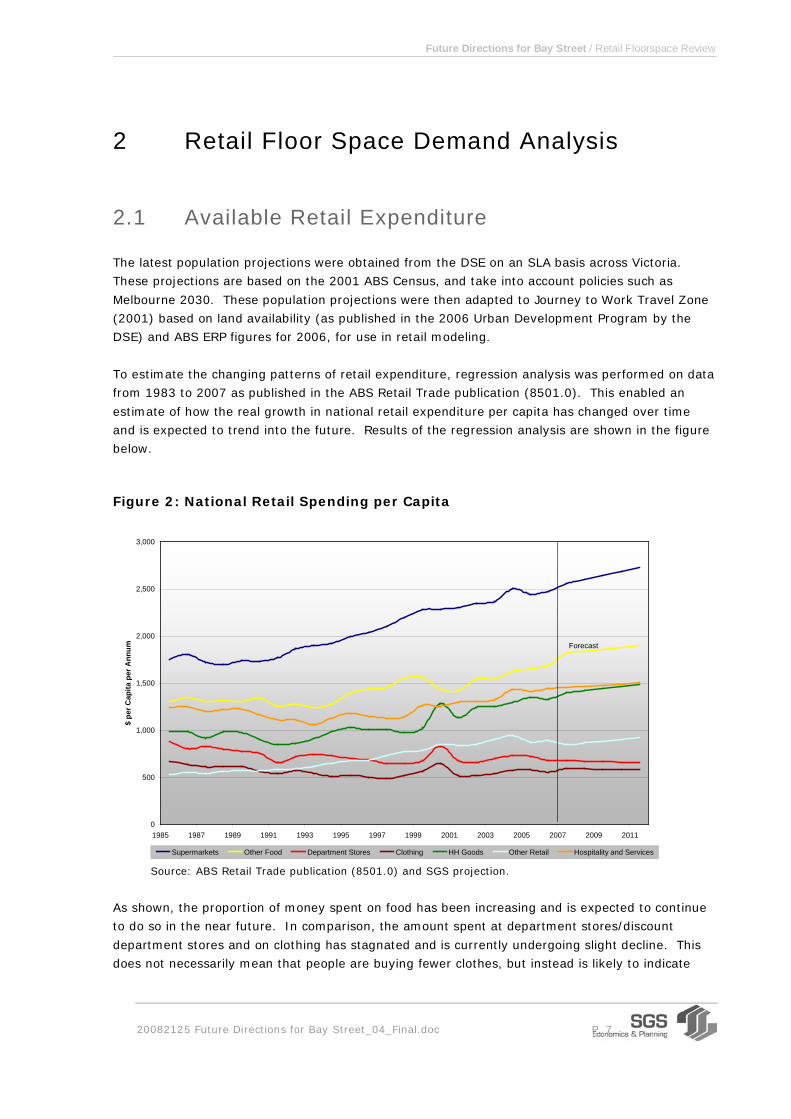

To estimate the changing patterns of retail expenditure, regression analysis was performed on data

from 1983 to 2007 as published in the ABS Retail Trade publication (8501.0). This enabled an

estimate of how the real growth in national retail expenditure per capita has changed over time

and is expected to trend into the future. Results of the regression analysis are shown in the figure

below.

Figure 2: National Retail Spending per Capita

0

500

1,000

1,500

2,000

2,500

3,000

1985 1987 1989 1991 1993 1995 1997 1999 2001 2003 2005 2007 2009 2011

$ pe

r Cap

ita p

er A

nnum

Supermarkets Other Food Department Stores Clothing HH Goods Other Retail Hospitality and Services

Forecast

Source: ABS Retail Trade publication (8501.0) and SGS projection.

As shown, the proportion of money spent on food has been increasing and is expected to continue

to do so in the near future. In comparison, the amount spent at department stores/discount

department stores and on clothing has stagnated and is currently undergoing slight decline. This

does not necessarily mean that people are buying fewer clothes, but instead is likely to indicate

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 8

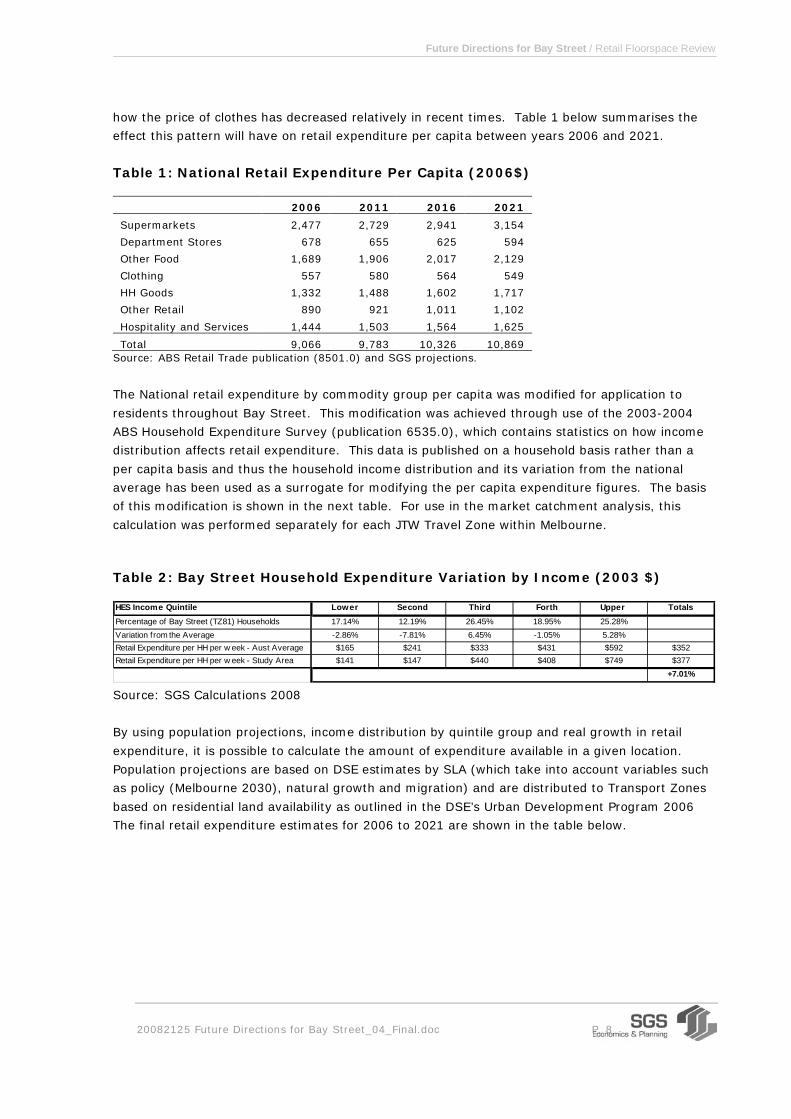

how the price of clothes has decreased relatively in recent times. Table 1 below summarises the

effect this pattern will have on retail expenditure per capita between years 2006 and 2021.

Table 1: National Retail Expenditure Per Capita (2006$)

2006 2011 2016 2021

Supermarkets 2,477 2,729 2,941 3,154

Department Stores 678 655 625 594

Other Food 1,689 1,906 2,017 2,129

Clothing 557 580 564 549

HH Goods 1,332 1,488 1,602 1,717

Other Retail 890 921 1,011 1,102

Hospitality and Services 1,444 1,503 1,564 1,625

Total 9,066 9,783 10,326 10,869 Source: ABS Retail Trade publication (8501.0) and SGS projections.

The National retail expenditure by commodity group per capita was modified for application to

residents throughout Bay Street. This modification was achieved through use of the 2003-2004

ABS Household Expenditure Survey (publication 6535.0), which contains statistics on how income

distribution affects retail expenditure. This data is published on a household basis rather than a

per capita basis and thus the household income distribution and its variation from the national

average has been used as a surrogate for modifying the per capita expenditure figures. The basis

of this modification is shown in the next table. For use in the market catchment analysis, this

calculation was performed separately for each JTW Travel Zone within Melbourne.

Table 2: Bay Street Household Expenditure Variation by Income (2003 $)

HES Income Quintile Lower Second Third Forth Upper TotalsPercentage of Bay Street (TZ81) Households 17.14% 12.19% 26.45% 18.95% 25.28%Variation from the Average -2.86% -7.81% 6.45% -1.05% 5.28%Retail Expenditure per HH per w eek - Aust Average $165 $241 $333 $431 $592 $352Retail Expenditure per HH per w eek - Study Area $141 $147 $440 $408 $749 $377

+7.01% Source: SGS Calculations 2008

By using population projections, income distribution by quintile group and real growth in retail

expenditure, it is possible to calculate the amount of expenditure available in a given location.

Population projections are based on DSE estimates by SLA (which take into account variables such

as policy (Melbourne 2030), natural growth and migration) and are distributed to Transport Zones

based on residential land availability as outlined in the DSE’s Urban Development Program 2006

The final retail expenditure estimates for 2006 to 2021 are shown in the table below.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 9

Table 3: Retail Expenditure in Bay Street by residents in Bay Street and surrounding areas 2006 to 2021

Expenditure 2006 2011 2016 2021Net Retail Growth

Annual Avg Growth (2006-

2021) Supermarkets $23.3m $28.3m $34.7m $43.5m $20.2m 4.2%Department Stores $6.6m $8.0m $8.5m $9.5m $2.9m 2.5%Other Food $15.9m $19.3m $24.2m $29.8m $13.9m 4.3%Clothing $5.4m $6.6m $7.7m $8.7m $3.2m 3.1%HH Goods $12.8m $15.5m $19.3m $24.1m $11.4m 4.3%Other Retail $8.6m $10.5m $12.0m $15.4m $6.8m 3.9%Hospitality and Services $14.3m $17.4m $20.1m $24.3m $10.0m 3.6%Total $86.9m $105.6m $126.5m $155.3m $68.4m 3.9% Source: SGS 2008

To calculate required retail floorspace in the future, it is assumed that Bay Street would maintain

its current market share within Melbourne, as the population grows and the retail offer in Bay

Street naturally adapts to accommodate extra demand. The combination of growth in population,

growth in average retail spends per capita and income distribution for residence in the Bay Street

and the surrounding areas will determine the predicted future demand for retail expansion along

Bay Street.

2.2 Bay Street Activity Centre Turnover

Retail Employment for each 2001 Journey-to-Work Travel Zone (a geographic term used to define

a small area) in Victoria was calculated using ABS Census Journey-to-Work Data, 2006. The

number of retail jobs was then used to estimate the size of retail centres within each Travel Zone

and thus the total turnover for each Zone across Metropolitan Melbourne. This information was

then supplemented by known floorspace and turnover data as published by the various reports

such as the Victorian Shopping Centres directory as published by the Property Council of Australia.

The SGS retail model was then used to approximate the market shares for these Travel Zones

based on their estimated turnover. The table below summarises the initial and forecast turnover of

the Bay Street centre as defined by Travel Zone 81 (see Figure 1).

Table 4: Retail Turnover of Bay Street Activity Centre 2006 to 2021

Turnover 2006 2011 2016 2021Net Retail Growth

Annual Avg Growth (2006-

2021) Supermarkets $28.4m $33.5m $40.3m $49.2m $20.8m 3.7%Department Stores $0.4m $0.5m $0.5m $0.5m $0.1m 2.1%Other Food $13.7m $16.1m $19.8m $23.7m $10.0m 3.7%Clothing and Soft Goods $2.8m $3.3m $3.8m $4.1m $1.3m 2.5%Household Goods $4.2m $5.0m $6.1m $7.4m $3.1m 3.8%Other Retail $9.4m $11.1m $12.5m $15.4m $5.9m 3.3%Hospitality and Services $28.4m $32.7m $36.6m $42.1m $13.7m 2.7%Total $87.3m $102.3m $119.4m $142.4m $55.1m 3.3%

In order to estimate the required floor space within an activity centre it is first necessary to

determine the amount of turnover a shopping centre generates per sqm of floor space (known as

the retail turnover density or RTD). It should be noted that the RTDs can vary substantially from

centre to centre; for example, past studies have shown that the RTDs achieved by a supermarket

in a regional shopping centre may be as high as $9,500 whereas specialty shops in minor shopping

strips can survive on an RTD of $2,500 due to the lower rents that prevail in such locations. An

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 10

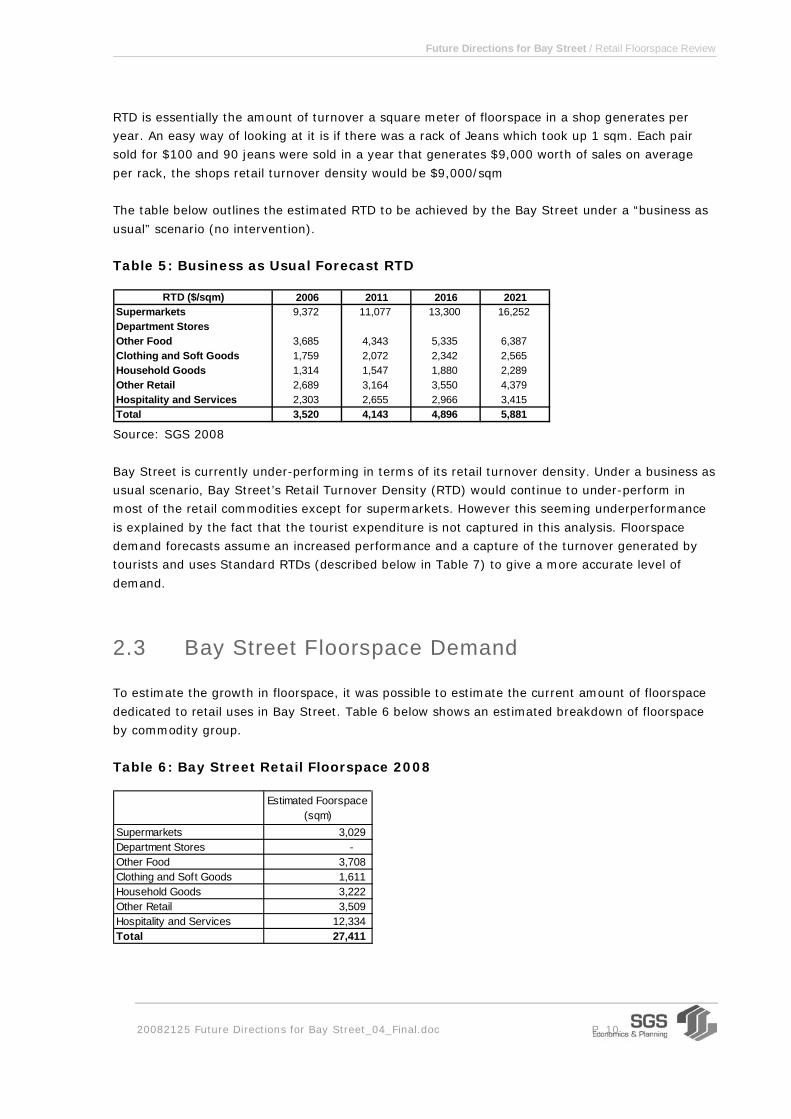

RTD is essentially the amount of turnover a square meter of floorspace in a shop generates per

year. An easy way of looking at it is if there was a rack of Jeans which took up 1 sqm. Each pair

sold for $100 and 90 jeans were sold in a year that generates $9,000 worth of sales on average

per rack, the shops retail turnover density would be $9,000/sqm

The table below outlines the estimated RTD to be achieved by the Bay Street under a “business as

usual” scenario (no intervention).

Table 5: Business as Usual Forecast RTD

RTD ($/sqm) 2006 2011 2016 2021Supermarkets 9,372 11,077 13,300 16,252Department StoresOther Food 3,685 4,343 5,335 6,387Clothing and Soft Goods 1,759 2,072 2,342 2,565Household Goods 1,314 1,547 1,880 2,289Other Retail 2,689 3,164 3,550 4,379Hospitality and Services 2,303 2,655 2,966 3,415Total 3,520 4,143 4,896 5,881 Source: SGS 2008

Bay Street is currently under-performing in terms of its retail turnover density. Under a business as

usual scenario, Bay Street’s Retail Turnover Density (RTD) would continue to under-perform in

most of the retail commodities except for supermarkets. However this seeming underperformance

is explained by the fact that the tourist expenditure is not captured in this analysis. Floorspace

demand forecasts assume an increased performance and a capture of the turnover generated by

tourists and uses Standard RTDs (described below in Table 7) to give a more accurate level of

demand.

2.3 Bay Street Floorspace Demand

To estimate the growth in floorspace, it was possible to estimate the current amount of floorspace

dedicated to retail uses in Bay Street. Table 6 below shows an estimated breakdown of floorspace

by commodity group.

Table 6: Bay Street Retail Floorspace 2008

Estimated Foorspace (sqm)

Supermarkets 3,029 Department Stores - Other Food 3,708 Clothing and Soft Goods 1,611 Household Goods 3,222 Other Retail 3,509 Hospitality and Services 12,334 Total 27,411

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 11

Bay Street has approximately 27,000 square meters of retail floorspace. A high proportion (45%)

is in Hospitality and Services.

The demand for floorspace calculation takes into account an increase in the performance of shops

currently in Bay Street to absorb the growth in expenditure and also captures the tourist

expenditure. The forecast turnover of the centre by commodity group is shown in Table 8 overleaf.

By using the standard RTD values Table 7, the demand for future floorspace can be determined.

Table 7: Standard RTD (2006$)

RTD ($/sqm)Supermarkets 9,180Department Stores 2,869Other Food 6,885Clothing and Soft Goods 3,443Household Goods 3,443Other Retail 4,590Hospitality and Services 3,443Total 4,836

Table 8 below, shows the calculation of floorspace demand based on the Standard RTDs and the

net retail growth (growth in turnover) of the centre.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 12

Table 8: Bay Street Floorspace Demand

Commodity 2006 Turnover 2011 Turnover 2016 Turnover 2021 Turnover Estimated Foorspace 2006

Growth In Turnover (2006-2021)

Standard RTD (2006$/sqm)

Floorspace Demand (2006 - 2021)

Supermarkets $28.4m $33.5m $40.3m $49.2m 3029 sqm $20.8m $9,180 2270 sqm

Department Stores $0.4m $0.5m $0.5m $0.5m 0 sqm $0.1m $2,869 51 sqm

Other Food $13.7m $16.1m $19.8m $23.7m 3708 sqm $10.0m $6,885 1455 sqm

Clothes and Soft Goods $2.8m $3.3m $3.8m $4.1m 1611 sqm $1.3m $3,443 377 sqm

Household goods and Hardw are (Bulky Goods) $4.2m $5.0m $6.1m $7.4m 3222 sqm $3.1m $3,443 912 sqm

Other Retail $9.4m $11.1m $12.5m $15.4m 3509 sqm $5.9m $4,590 1292 sqm

Hospitality and Services $28.4m $32.7m $36.6m $42.1m 12334 sqm $13.7m $3,443 3986 sqm

Total Turnover $87.3m $102.3m $119.4m $142.4m 27411 sqm $55.1m $4,836 10343 sqm

The demand for floorspace in Bay Street is estimated to be 10,343 square meters. Hospitality and Services represents about 38% of total demand.

Other Food is also in strong demand, followed by other retail (not including supermarkets).

The following section looks at the impacts on floorspace demand in Bay Street, if a competing centre is developed in a Business 3 Zone off

Williamstown Road, north-west of Bay Street.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 13

2.4 Impact Assessment

Given that a Bunnings has recently located on Williamstown Road near Bay Street, there is a

potential for a complementary retail offer in the same location. Figure 3 below presents a context

map of the location of the ‘competing centre’ located in the geographic definition Travel Zone 80

(TZ 80). Bay Street shopping precinct is in (TZ 81).

Figure 3: Competing Centre for Impact Assessment.

Source: SGS 2008

As the location of the Bunnings is within a Business 3 Zone (B3Z), there are several restrictions

regarding the development of retail in such zones. Namely retail premises are restricted to large

floorspace areas that are much greater than a “normal shop”. In the B3Z, a premises needs to

have a floor area of at least 1000sqm. This can include things such as camping equipment,

electric light fittings, equestrian supplies, floor coverings, furnishings, furniture, swimming pools,

etc. Places like Harvey Norman, Rays Outdoor/ Tent City. A supermarket use falls within a “shop”

definition and by definition is a prohibited use in a B3Z.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 14

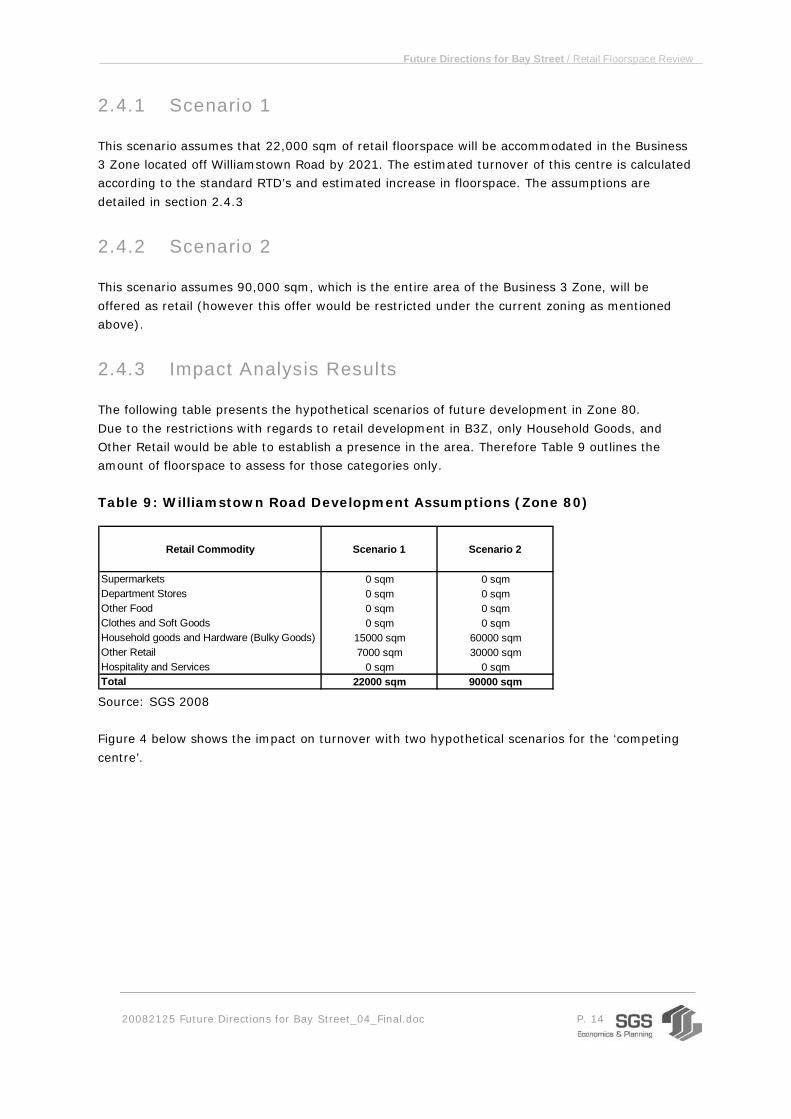

2.4.1 Scenario 1

This scenario assumes that 22,000 sqm of retail floorspace will be accommodated in the Business

3 Zone located off Williamstown Road by 2021. The estimated turnover of this centre is calculated

according to the standard RTD’s and estimated increase in floorspace. The assumptions are

detailed in section 2.4.3

2.4.2 Scenario 2

This scenario assumes 90,000 sqm, which is the entire area of the Business 3 Zone, will be

offered as retail (however this offer would be restricted under the current zoning as mentioned

above).

2.4.3 Impact Analysis Results

The following table presents the hypothetical scenarios of future development in Zone 80.

Due to the restrictions with regards to retail development in B3Z, only Household Goods, and

Other Retail would be able to establish a presence in the area. Therefore Table 9 outlines the

amount of floorspace to assess for those categories only.

Table 9: Williamstown Road Development Assumptions (Zone 80)

Retail Commodity Scenario 1 Scenario 2

Supermarkets 0 sqm 0 sqmDepartment Stores 0 sqm 0 sqmOther Food 0 sqm 0 sqmClothes and Soft Goods 0 sqm 0 sqmHousehold goods and Hardware (Bulky Goods) 15000 sqm 60000 sqmOther Retail 7000 sqm 30000 sqmHospitality and Services 0 sqm 0 sqmTotal 22000 sqm 90000 sqm Source: SGS 2008

Figure 4 below shows the impact on turnover with two hypothetical scenarios for the ‘competing

centre’.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 15

Figure 4: Impact on Turnover in Bay Street

$0.0m

$20.0m

$40.0m

$60.0m

$80.0m

$100.0m

$120.0m

$140.0m

$160.0m

Supermarkets Department Stores

Other Food Clothes and Soft Goods

Household goods and Hardware

(Bulky Goods)

Other Retail Hospitality and Services

Total

2021Turnover - Base 2021 Turnover -Scenario 1 2021 Turnover -Scenario 2

Source: SGS 2008

The development of a centre in the Business 3 Zone on Williamstown Road, will not have a

substantial impact on Turnover in Bay Street. This is because Bay Street is predominantly a

Hospitality and Services centre, with Supermarkets and Other Food as the highest contributors to

turnover.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 16

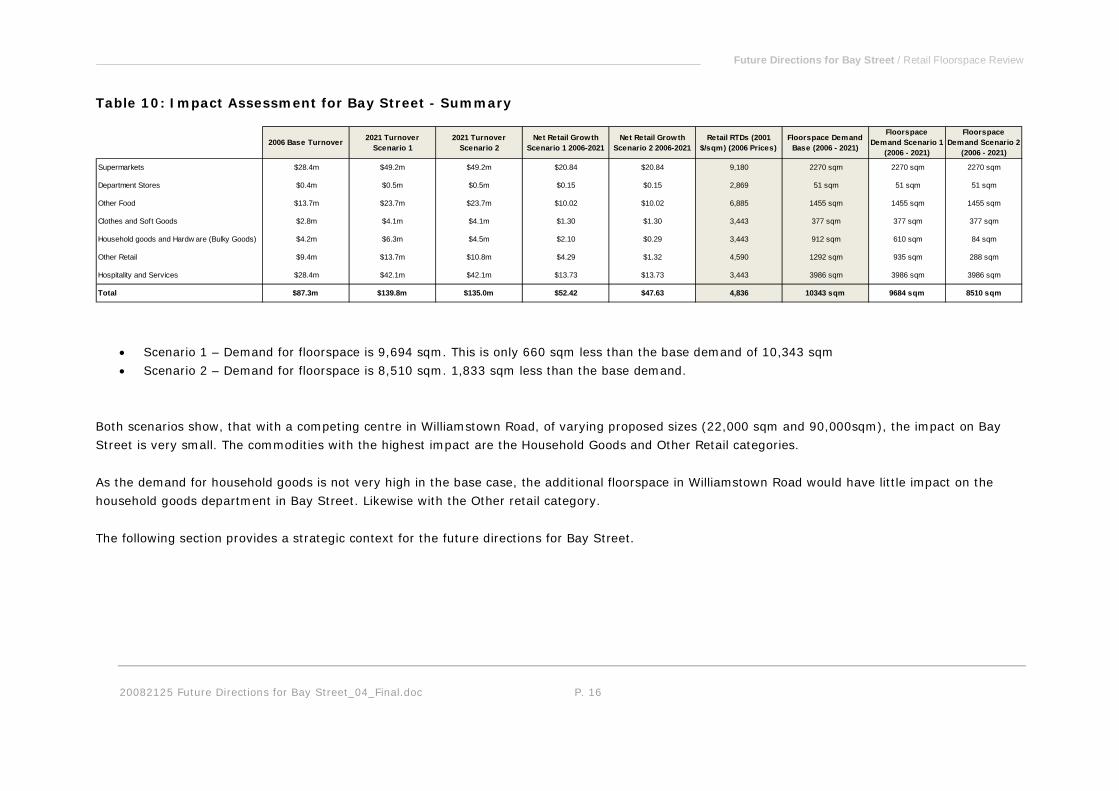

Table 10: Impact Assessment for Bay Street - Summary

2006 Base Turnover 2021 Turnover Scenario 1

2021 Turnover Scenario 2

Net Retail Growth Scenario 1 2006-2021

Net Retail Growth Scenario 2 2006-2021

Retail RTDs (2001 $/sqm) (2006 Prices)

Floorspace Demand Base (2006 - 2021)

Floorspace Demand Scenario 1

(2006 - 2021)

Floorspace Demand Scenario 2

(2006 - 2021)

Supermarkets $28.4m $49.2m $49.2m $20.84 $20.84 9,180 2270 sqm 2270 sqm 2270 sqm

Department Stores $0.4m $0.5m $0.5m $0.15 $0.15 2,869 51 sqm 51 sqm 51 sqm

Other Food $13.7m $23.7m $23.7m $10.02 $10.02 6,885 1455 sqm 1455 sqm 1455 sqm

Clothes and Soft Goods $2.8m $4.1m $4.1m $1.30 $1.30 3,443 377 sqm 377 sqm 377 sqm

Household goods and Hardw are (Bulky Goods) $4.2m $6.3m $4.5m $2.10 $0.29 3,443 912 sqm 610 sqm 84 sqm

Other Retail $9.4m $13.7m $10.8m $4.29 $1.32 4,590 1292 sqm 935 sqm 288 sqm

Hospitality and Services $28.4m $42.1m $42.1m $13.73 $13.73 3,443 3986 sqm 3986 sqm 3986 sqm

Total $87.3m $139.8m $135.0m $52.42 $47.63 4,836 10343 sqm 9684 sqm 8510 sqm

• Scenario 1 – Demand for floorspace is 9,694 sqm. This is only 660 sqm less than the base demand of 10,343 sqm

• Scenario 2 – Demand for floorspace is 8,510 sqm. 1,833 sqm less than the base demand.

Both scenarios show, that with a competing centre in Williamstown Road, of varying proposed sizes (22,000 sqm and 90,000sqm), the impact on Bay

Street is very small. The commodities with the highest impact are the Household Goods and Other Retail categories.

As the demand for household goods is not very high in the base case, the additional floorspace in Williamstown Road would have little impact on the

household goods department in Bay Street. Likewise with the Other retail category.

The following section provides a strategic context for the future directions for Bay Street.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 17

2.4.4 Comparison of Results

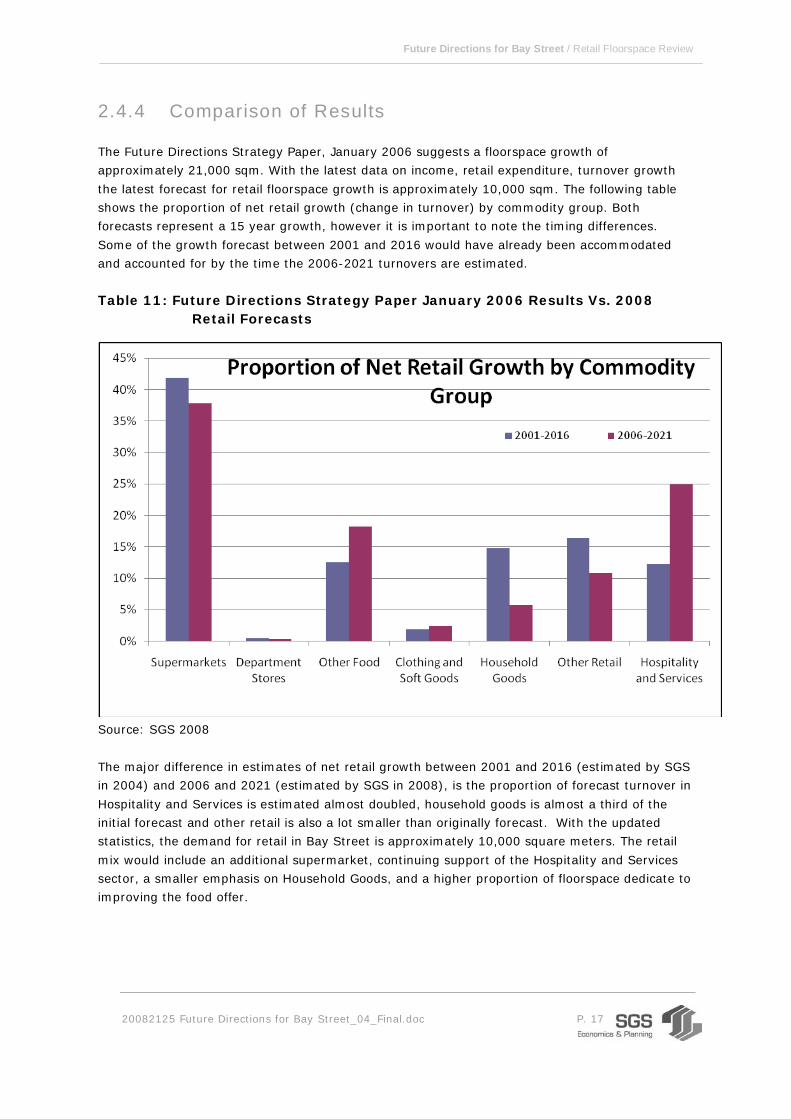

The Future Directions Strategy Paper, January 2006 suggests a floorspace growth of

approximately 21,000 sqm. With the latest data on income, retail expenditure, turnover growth

the latest forecast for retail floorspace growth is approximately 10,000 sqm. The following table

shows the proportion of net retail growth (change in turnover) by commodity group. Both

forecasts represent a 15 year growth, however it is important to note the timing differences.

Some of the growth forecast between 2001 and 2016 would have already been accommodated

and accounted for by the time the 2006-2021 turnovers are estimated.

Table 11: Future Directions Strategy Paper January 2006 Results Vs. 2008 Retail Forecasts

Source: SGS 2008

The major difference in estimates of net retail growth between 2001 and 2016 (estimated by SGS

in 2004) and 2006 and 2021 (estimated by SGS in 2008), is the proportion of forecast turnover in

Hospitality and Services is estimated almost doubled, household goods is almost a third of the

initial forecast and other retail is also a lot smaller than originally forecast. With the updated

statistics, the demand for retail in Bay Street is approximately 10,000 square meters. The retail

mix would include an additional supermarket, continuing support of the Hospitality and Services

sector, a smaller emphasis on Household Goods, and a higher proportion of floorspace dedicate to

improving the food offer.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 18

3 The Strategic Context for Bay Street

Bay Street is a designated ‘major’ activity centre under Melbourne 2030 and subsequently its

planning must be consistent with the metropolitan strategy. IMAP is a joint venture of the

municipalities of Melbourne, Port Phillip, Yarra and Stonnington to achieve cooperation and plan

coordination between themselves in implementing Melbourne 2030.

It is important that the Bay Street Activity Centre is based on a strongly supported context plan

so as to fully exploit its potential to service its immediate Port Melbourne trade area, that of the

wider Port Phillip Municipality and even Metropolitan Melbourne.

The following section suggests a strategic context for the planning and development of Bay Street

based on a previous plans for the area and on trends in cities overseas.

Since this study was first commenced it has come to the notice of SGS that the Inner Melbourne

Action Plan (IMAP) has been adopted by Council. Clearly any structure plan for Bay Street should

be consistent with that plan. Although detailed analysis of the content of IMAP has not been

undertaken as part of this project IMAP does suggest a context that is in line with that suggested

herein. A brief understand of the thrust of IMAP that affects Bay Street can be obtained from

IMAP maps 1, 2, 3 and 7 in particular.

SGS’s conclusion is that Bay Street should be recognised and planned as one of Melbourne’s

major boulevards that combined with its extension along City Road radiate from the City to the

Bay. This would put it in the same category as St Kilda Road, Royal Parade, Flemington Road,

and the likes.

3.1 'City to Bay Boulevard' Plan in 1980s

Creation of such a boulevard was the official policy and plan of the Cain Labor Government in the

1980s: Central Melbourne, Framework for the Future - No 6. Land Use and Development Strategy

(Department of Planning & Environment, 1984). That plan was also the subject of a video that

explains the concepts of the City to Bay Boulevard (Melbourne’s Best, DVD – available from SGS

or DPCD).

The plan was implemented substantially and it changed the fundamental function and form of

Southbank for the better. However, it did not deliver on the concept for an iconic boulevard from

St Kilda Road to the Bay (along City Road). This plan should be re-examined with the intention of

up-dating it and using it as Bay Street’s sub-regional strategy. Note that the following diagrams are synoptic only and the original document should be read for

any detail required.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 19

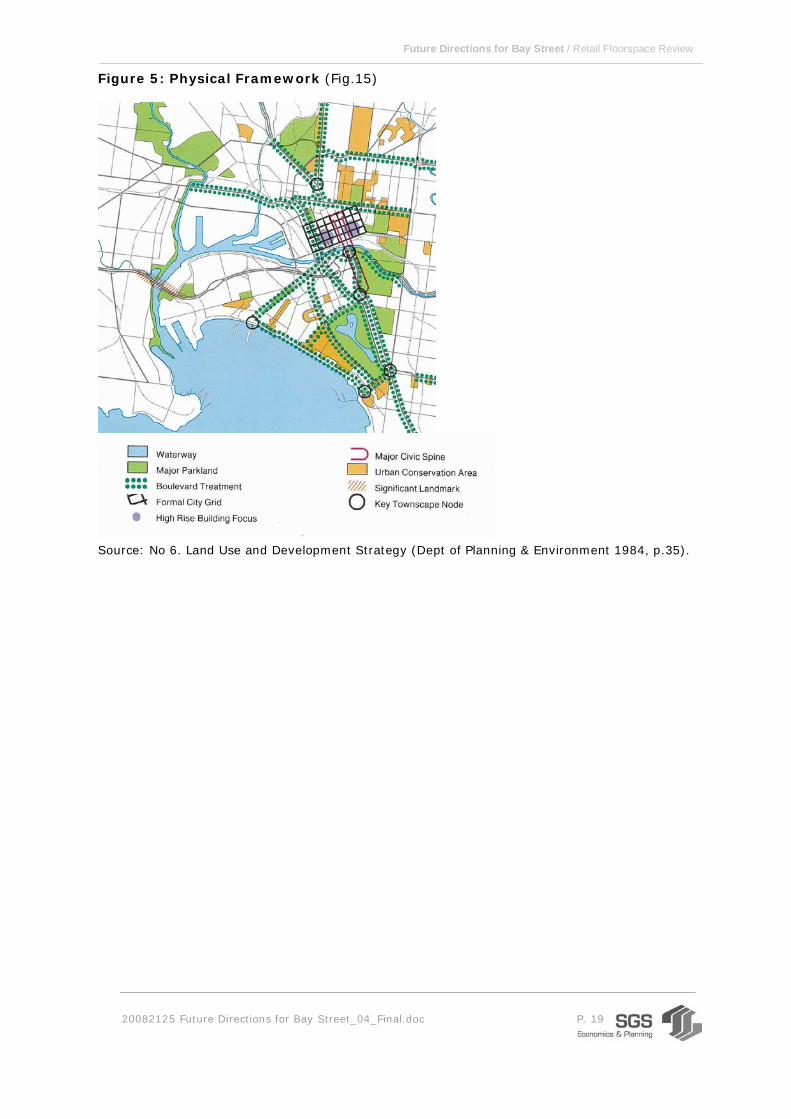

Figure 5: Physical Framework (Fig.15)

Source: No 6. Land Use and Development Strategy (Dept of Planning & Environment 1984, p.35).

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 20

Figure 6: Development Proposals (Fig.16)

Source: No 6. Land Use and Development Strategy (Dept of Planning & Environment 1984).

Note that Bay Street is not the actual subject of the boulevard in the Cain Government plan; it is

the Beacon Cove tramway line. It did make sense to activate the Beacon Cove railway track as a

dedicated light rail; as it does to maintain it. However, under the circumstances there was never

a prospect of using it as a stimulus for major renewal and rejuvenation of the retail and

commercial infrastructure of the area, as the situation is with Bay Street.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 21

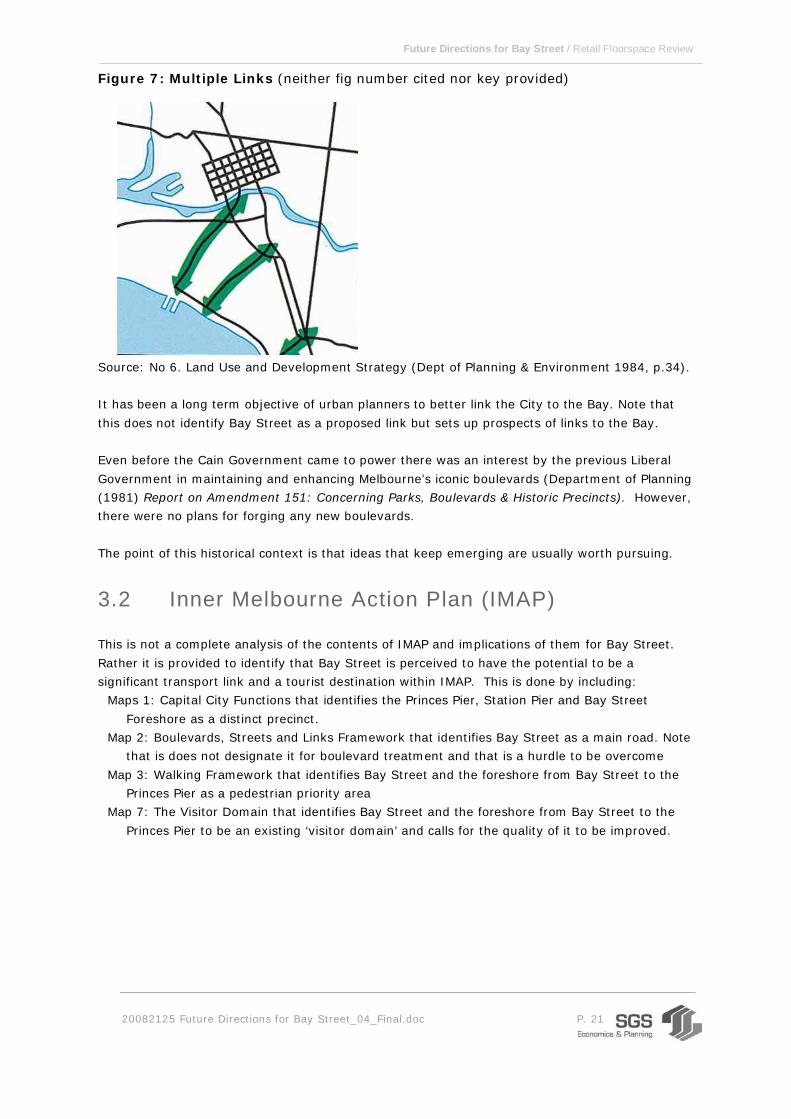

Figure 7: Multiple Links (neither fig number cited nor key provided)

Source: No 6. Land Use and Development Strategy (Dept of Planning & Environment 1984, p.34). It has been a long term objective of urban planners to better link the City to the Bay. Note that

this does not identify Bay Street as a proposed link but sets up prospects of links to the Bay. Even before the Cain Government came to power there was an interest by the previous Liberal

Government in maintaining and enhancing Melbourne’s iconic boulevards (Department of Planning

(1981) Report on Amendment 151: Concerning Parks, Boulevards & Historic Precincts). However,

there were no plans for forging any new boulevards.

The point of this historical context is that ideas that keep emerging are usually worth pursuing.

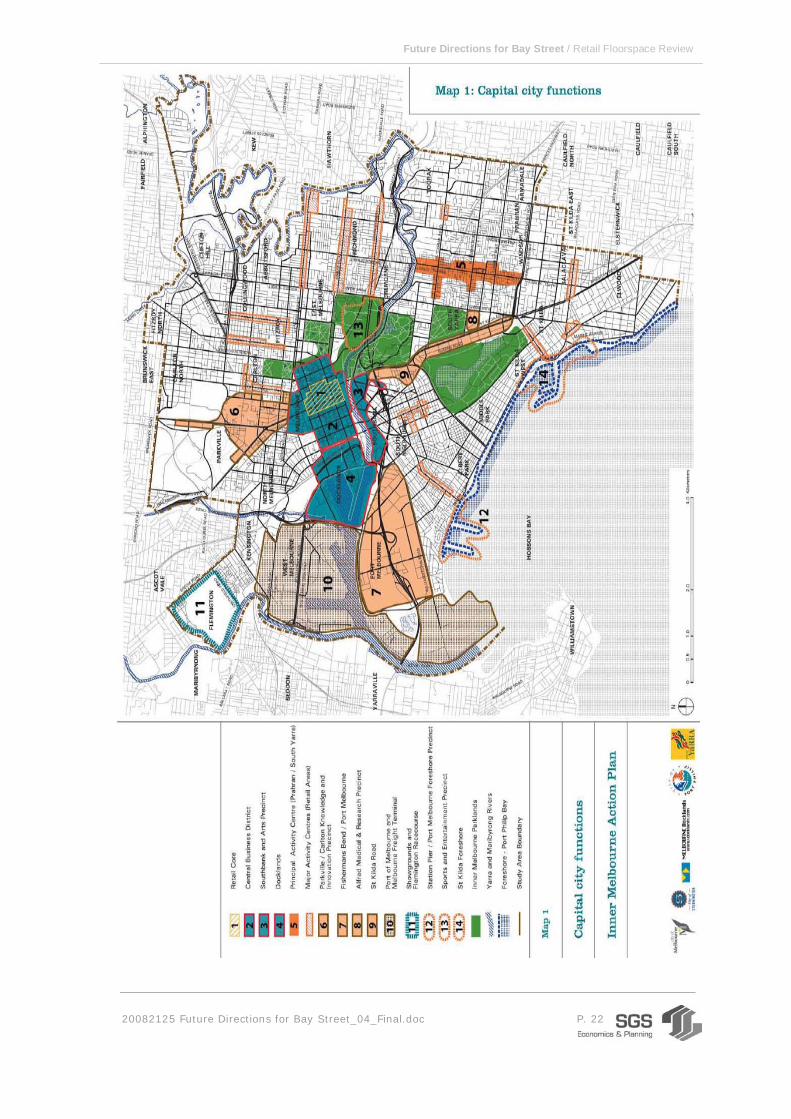

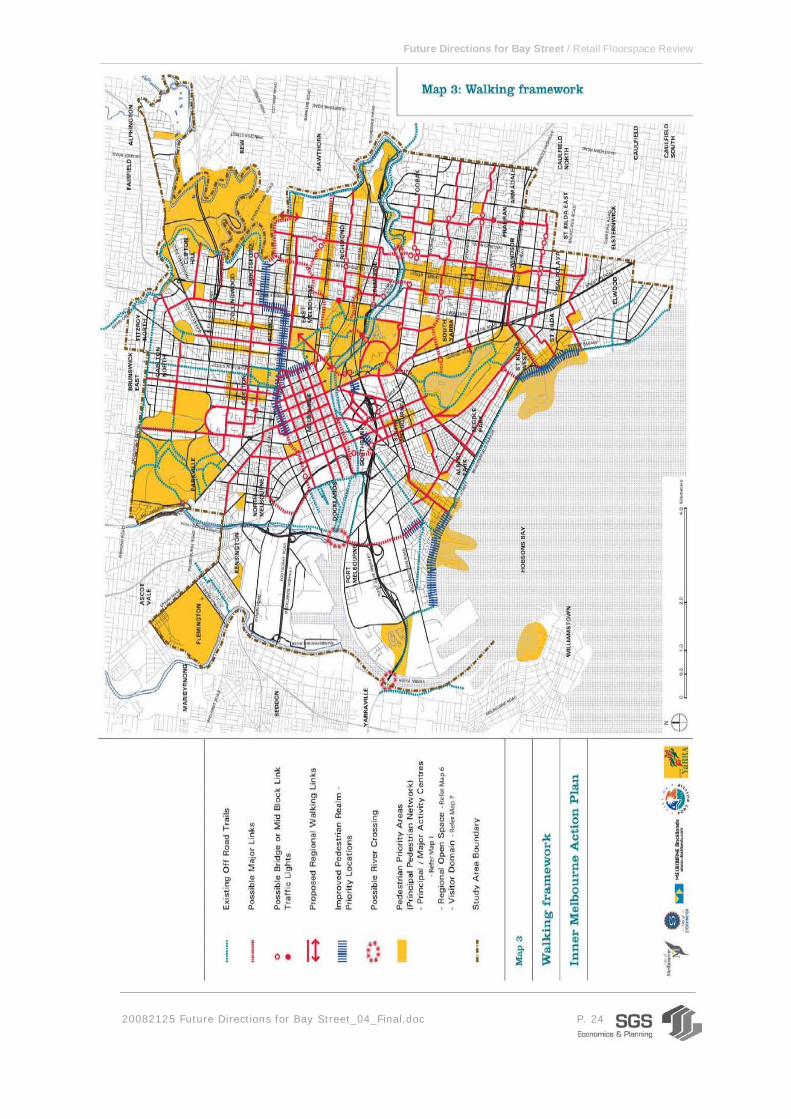

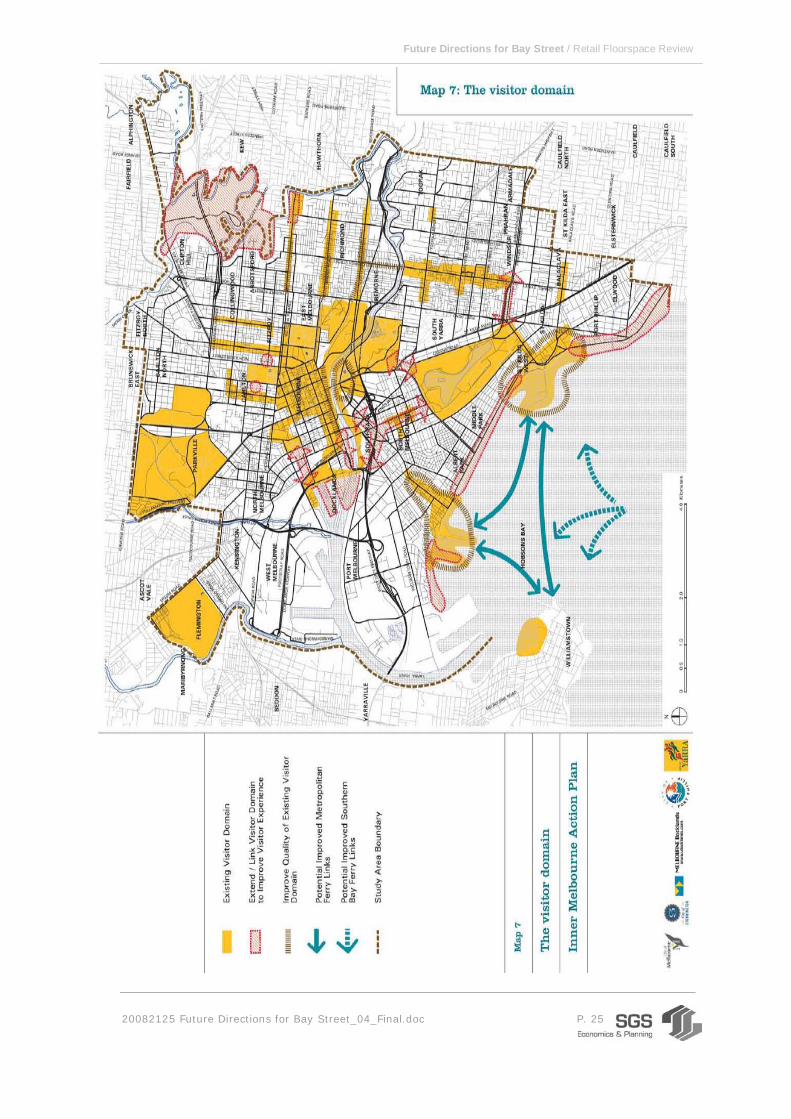

3.2 Inner Melbourne Action Plan (IMAP)

This is not a complete analysis of the contents of IMAP and implications of them for Bay Street.

Rather it is provided to identify that Bay Street is perceived to have the potential to be a

significant transport link and a tourist destination within IMAP. This is done by including:

Maps 1: Capital City Functions that identifies the Princes Pier, Station Pier and Bay Street

Foreshore as a distinct precinct.

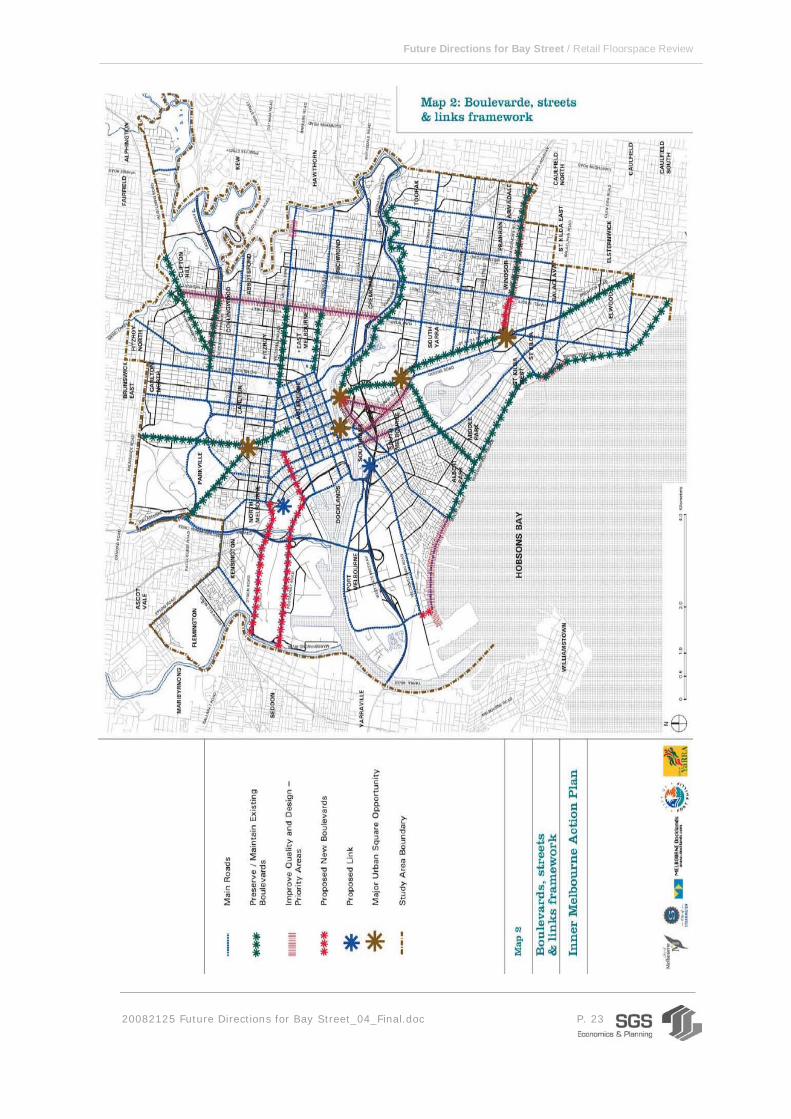

Map 2: Boulevards, Streets and Links Framework that identifies Bay Street as a main road. Note

that is does not designate it for boulevard treatment and that is a hurdle to be overcome

Map 3: Walking Framework that identifies Bay Street and the foreshore from Bay Street to the

Princes Pier as a pedestrian priority area

Map 7: The Visitor Domain that identifies Bay Street and the foreshore from Bay Street to the

Princes Pier to be an existing ‘visitor domain’ and calls for the quality of it to be improved.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 22

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 23

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 24

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 25

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 26

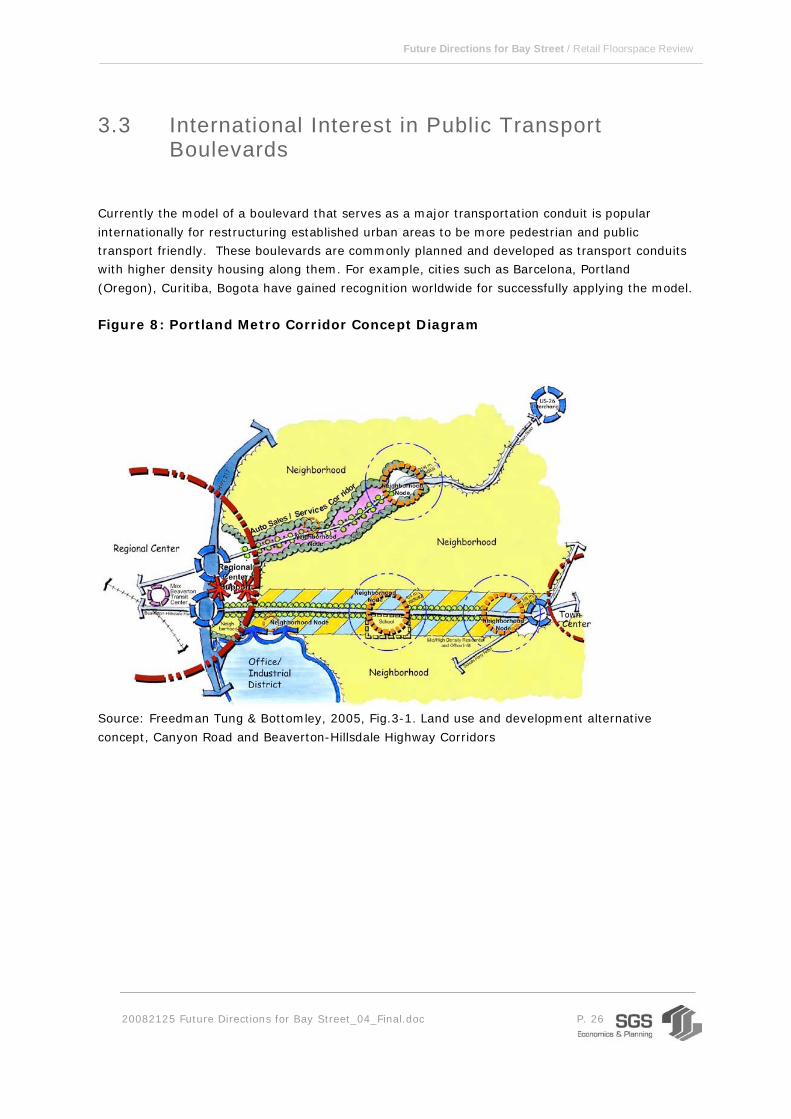

3.3 International Interest in Public Transport Boulevards

Currently the model of a boulevard that serves as a major transportation conduit is popular

internationally for restructuring established urban areas to be more pedestrian and public

transport friendly. These boulevards are commonly planned and developed as transport conduits

with higher density housing along them. For example, cities such as Barcelona, Portland

(Oregon), Curitiba, Bogota have gained recognition worldwide for successfully applying the model.

Figure 8: Portland Metro Corridor Concept Diagram

Source: Freedman Tung & Bottomley, 2005, Fig.3-1. Land use and development alternative

concept, Canyon Road and Beaverton-Hillsdale Highway Corridors

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 27

Figure 9: Portland Metro Corridor Map

Source: Metro Data Resource Centre (DRC) 2004. Fig.1: Corridor case study area, Beaverton-

Hillsdale Highway & Canyon Road.

Part of the dividend from the application of the model is that it creates potential for increasing

residential density along major arterial roads, especially those that also serve as public transport

routes.

The model is now being talked about in Australia. Rob Adams, MCC, recently gave a presentation

in the Department of Transport on the preparation of a concept plan to increase housing density

along main arterial roads within the City of Melbourne.

3.4 Prospects for a Bay Street Boulevard Today

Bay Street would be a good test case for such a model of development. As indicated previously,

Bay Street already has many of the characteristics of a boulevard by virtue of it having had a

cable tram line in an earlier era of its development. Note that in Central Melbourne: Framework

for the Future (1984) Bay Street was not identified for Boulevard treatment but rather Pickles

Street was.

It is recommended that City of Port Phillip makes contact with the City of Melbourne to see how

they can co-operate on such concepts to their mutual advantage.

Within the area surrounding Bay Street the housing market is already implementing such

concepts, if not to a formal plan, with housing already intensifying at both ends of the Bay Street/

City Road link:

• At Beach Road end of bay street there are Bayview Apartments, Westpoint Apartments,

and the Atlantis Apartments

• At the City Road end (Southbank) there are several residential and commercial complexes

that includes the Eureka Tower

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 28

Figure 10: Bay Street – North View

Figure 11: Bay Street – South View

Source: SGS 2008

There are numerous older poor quality industrial/ showroom buildings along City Road in the

Southbank area that are ripe for renewal. These could be developed as mixed use complexes

with residential and commercial above retail and commercial uses that are pedestrian friendly and

celebrate the linear form of the new boulevard.

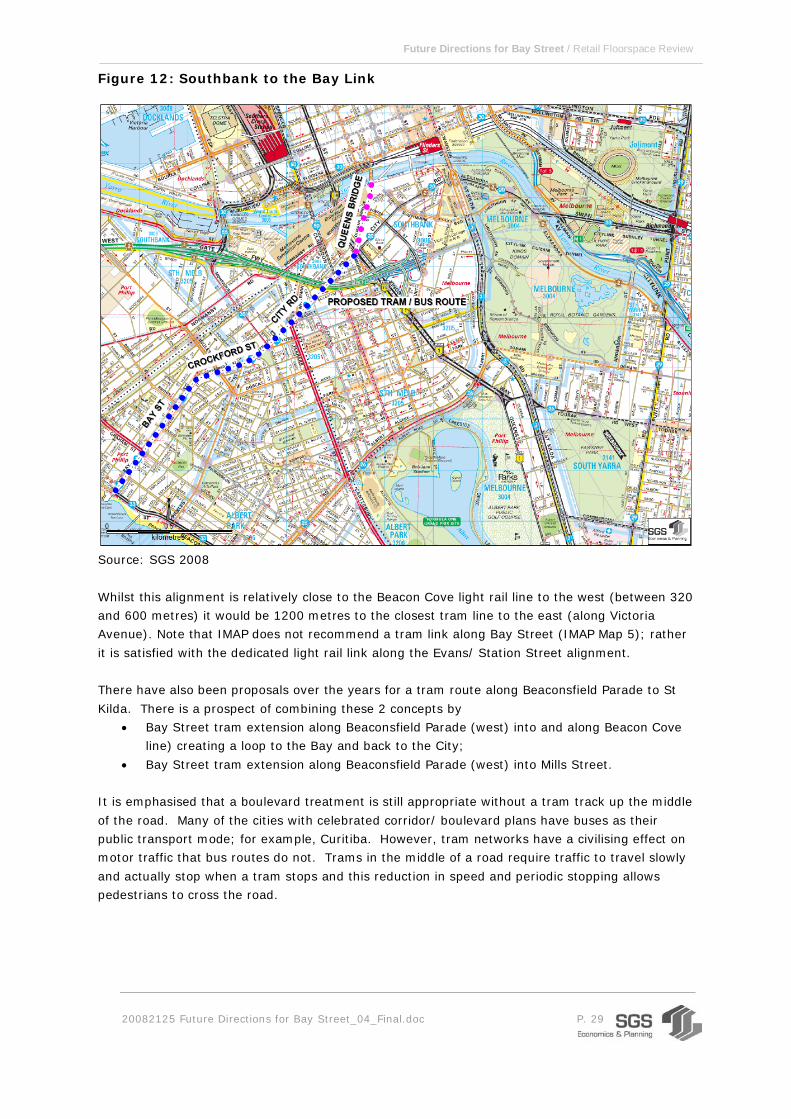

The prospect of a new tram line being developed along Bay Street/ City Road should be explored

as part of a City to Bay Boulevard.

It would be exciting if there could be a tram line put back along Bay Street/ City Road to

Queensbridge Street, through the proposed new public square at Southbank and into Market/

William Streets.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 29

Figure 12: Southbank to the Bay Link

Source: SGS 2008

Whilst this alignment is relatively close to the Beacon Cove light rail line to the west (between 320

and 600 metres) it would be 1200 metres to the closest tram line to the east (along Victoria

Avenue). Note that IMAP does not recommend a tram link along Bay Street (IMAP Map 5); rather

it is satisfied with the dedicated light rail link along the Evans/ Station Street alignment.

There have also been proposals over the years for a tram route along Beaconsfield Parade to St

Kilda. There is a prospect of combining these 2 concepts by

• Bay Street tram extension along Beaconsfield Parade (west) into and along Beacon Cove

line) creating a loop to the Bay and back to the City;

• Bay Street tram extension along Beaconsfield Parade (west) into Mills Street.

It is emphasised that a boulevard treatment is still appropriate without a tram track up the middle

of the road. Many of the cities with celebrated corridor/ boulevard plans have buses as their

public transport mode; for example, Curitiba. However, tram networks have a civilising effect on

motor traffic that bus routes do not. Trams in the middle of a road require traffic to travel slowly

and actually stop when a tram stops and this reduction in speed and periodic stopping allows

pedestrians to cross the road.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 30

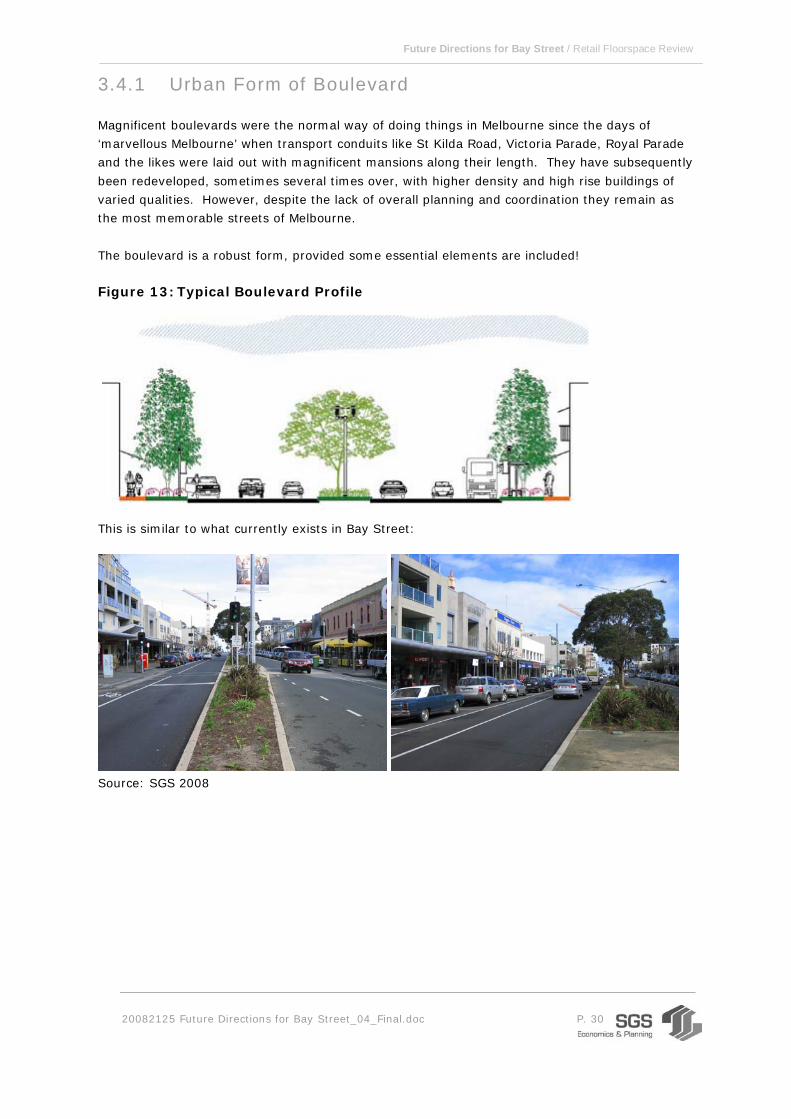

3.4.1 Urban Form of Boulevard

Magnificent boulevards were the normal way of doing things in Melbourne since the days of

‘marvellous Melbourne’ when transport conduits like St Kilda Road, Victoria Parade, Royal Parade

and the likes were laid out with magnificent mansions along their length. They have subsequently

been redeveloped, sometimes several times over, with higher density and high rise buildings of

varied qualities. However, despite the lack of overall planning and coordination they remain as

the most memorable streets of Melbourne.

The boulevard is a robust form, provided some essential elements are included! Figure 13: Typical Boulevard Profile

This is similar to what currently exists in Bay Street:

Source: SGS 2008

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 31

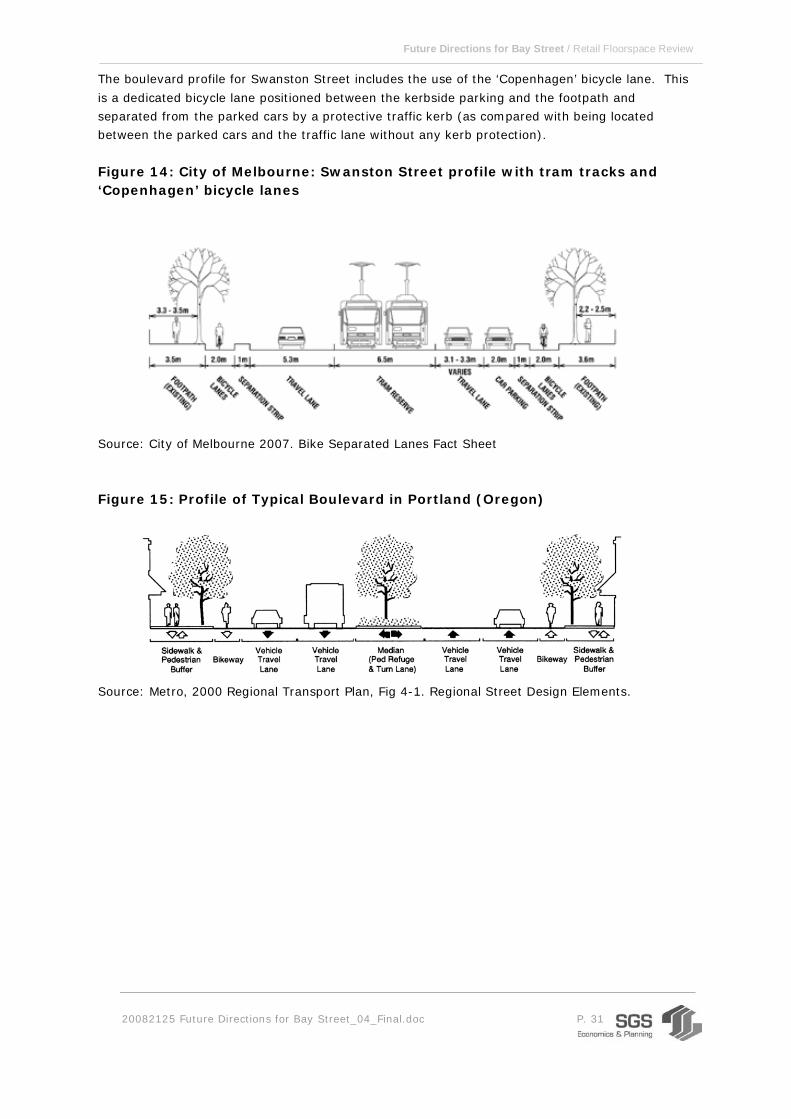

The boulevard profile for Swanston Street includes the use of the ‘Copenhagen’ bicycle lane. This

is a dedicated bicycle lane positioned between the kerbside parking and the footpath and

separated from the parked cars by a protective traffic kerb (as compared with being located

between the parked cars and the traffic lane without any kerb protection).

Figure 14: City of Melbourne: Swanston Street profile with tram tracks and ‘Copenhagen’ bicycle lanes

Source: City of Melbourne 2007. Bike Separated Lanes Fact Sheet

Figure 15: Profile of Typical Boulevard in Portland (Oregon)

Source: Metro, 2000 Regional Transport Plan, Fig 4-1. Regional Street Design Elements.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 32

3.5 Planning and Design of Bay Street, Port Melbourne

3.5.1 Niches for Bay Street

An appropriate way of identifying the niches to be introduced or strengthened along Bay Street is

to identify existing magnet destinations around which complementary dependent businesses can

be clustered.

Bay Street has several magnet facilities with varying degrees of drawing power and potential:

• Food-for-the-home: supermarkets

• Beach destination and scene: foreshore of Port Philip bay

• Iconic entertainment venue: Circus Oz

• Government services: especially local government such as public library, community

centre.

There are other possible niches that do exist along Bay Street but not to any great extent. The

population profile of the immediate area suggests that these could be supported.

• Health, fitness, well-being: gymnasiums, youth clubs, community centres

• Medical services: general practitioners, dentists, opticians, physiotherapists

• Popular entertainment: reception/ entertainment centres, night clubs

Although these niches do not necessarily need to be set in specific precincts along Bay Street it is

likely that they will be identifiable particular locations and areas of the street. (Please refer to

Appendix for the contextual description of each of the following)

Food-for-the-Home Niche

This is the most important niche to pursue in strengthening the overall shopping district, for the

reasons expressed below.

‘Food for the home' is a very important and very large niche. Overwhelming evidence indicates

that shopping is done as two consecutive food and non-food expeditions even when occurring in

the same shopping destination.

There are numerous social and economic reasons for retaining food shopping. First, food shops

generally, and supermarkets in particular, are major attractors of shoppers and there are

prospects for flow-on expenditure to any specialty shops nearby, including specialist food.

Second, food shopping is a frequently repeated activity, commonly at least weekly, so that it

helps community development. Third, there are usually some remnants of resident population

that need servicing and it is important to overall street vitality that they be encouraged to remain

as residents.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 33

The effect of a supermarket is similar to a cluster of individual shops selling complementary food

commodities and can be recreated with an equivalent mix of individual shops. However, within a

supermarket, shoppers are assured that the different products will be conveniently clustered

within easy sight and walking distance and this is difficult to recreate in shopping districts.

A full-line supermarket in a shopping district inevitably results in competition for traders on the

street selling vegetable/ fruit produce, meat and delicatessen items. A smaller range

supermarket such as Aldi may be preferred, since it leaves opportunities for small independent

traders; however, it will be successfully as a collective only if the small traders are located

nearby.

The 'food-for-the-home' Niche is already a major strength of the Bay Street shopping district.

There are 4 major supermarket brands in Victoria: Coles, Safeway, IGA and Aldi, and Bay Street

already has 2 of them: Coles, located on the corner of Liardet Street and Bay Street and IGA,

located near the corner of Rouse Street and Bay Street.. It makes sense to encourage clustering

most of the food-for-the-home outlets in the blocks between Rouse Street and Liardet Street.

It is unlikely that there is the market demand in the area of Bay Street to support all 4 types of

Australian supermarkets at this time. However, with the redevelopment of higher density housing

along Bay Street it may only be a matter of time before there is sufficient demand.

The major advantage of a linear form for a shopping district (as opposed to a point centre) is that

a new shopping destination can be developed anywhere along its length so that it serves an

adjacent primary trade area but is still readily accessible to residents along the length of Bay

Street/ City Road. Aldi operates a different retailing model from the other three, provides a

different offering and would be a valuable addition. An Aldi supermarket as an anchor north of

Liardet Street may well be a possibility and that could stimulate development of more

independent food-for-the-home outlets. Whilst government has difficulty controlling retailing activities on privately owned land it has

virtually absolute control over what happens on public land within shopping districts: streets,

parks and the likes. Trading on publically owned land is an old and honourable retailing form that

can be an effective means of introducing specific merchandise or tenants. Street trading can

provide a service not offered in shops; for example, for 'shopping on the run'. Ironically, it can

also help the trading in adjacent shops by slowing pedestrians to a browsing pace, and initial

stops at stalls can result in sales for adjacent shops. Traders also perform simple janitorial tasks

in going about their business. In these ways, street trading can be an effective means of

influencing the vitality and viability of a shopping district. Recently in Melbourne there has emerged a network of farmer’s markets. Farmers markets, a USA concept, enable farmers to sell their produce direct to consumers. The tendency in Australia is to locate

farmer’s markets away from a major activity centre, out-of-centre, in a park or sports oval

setting. This means that any potential synergy between the farmers market and the nearest

activity centre is almost certainly irrelevant because it need a car trip to move from one to the

other. In-centre locations enable the farmer’s markets to act as major draw-cards (anchors or

magnet) for the more conventional shopping in the adjacent business district.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 34

There is already a farmers’ market held in the Gasworks Park once per month and it is a popular

shopping destination that draws in customers from across the immediate sub-region.

It is recommended that a farmers’ market be established along Bay Street, preferably in the

vicinity of the other food-for-the-home shopping facilities so as to exploit potential synergy.

Initially this should be on a monthly basis with the intention of holding it more frequently,

possibly even 3-4 weeks a month (on the weeks that the Gasworks Farmers Market is not

operating). There are several locations that could be considered. There may be a prospect of

locating a farmers’ market in and around the small public park in Liardet Street (Olives Corner),

the Liardet Community Centre and the Neighbourhood House complex that extends back to Nott

Street.

Beach Destination and Scene

The precinct between Rouse Street and Beach Street (and along Beach Street) has special

potential because of its proximity to the foreshore and the Bay. Water frontage of any type is

especially appealing for locals, tourists and day trippers. However, unlike streets in a similar

situation such as Acland Street it has not managed to forge a role as a tourist destination.

This precinct could and should be developed as a tourist/day tripping destination to rival Acland

Street. It already has the basis of a tourism destination: Circus Oz headquarters, a couple of

historic pubs, several heritage buildings with prospects for creative reuse, and views to the

foreshore and Port Phillip Bay. There is a need for some urban design branding that could and

should be used to make this south precinct distinctive from the remainder of Bay Street.

The waterfront around Station Pier is already evolving into a substantial tourist destination and

this could be reinforced by creative redevelopment of the south end of Bay Street and the

foreshore area between the two along Beach Street. Note that IMAP map 7 suggest that the area

from Princes Pier to Bay Street (including all of the Bay Street shopping street) be developed as a

major ‘Visitor Domain’.

Currently the War Memorial and the Port Melbourne Yacht Club are located on the foreshore

immediately across from the end of Bay Street (at the junction of Beach Street and Bay Street).

There is some benefit in creating a better sense of place at this junction. This should make a

better connection between Bay Street and the Bay, visual and physical, and attract more people

across from Bay Street onto the foreshore, and vice versa.

Public Community Hub

Government is limited in its influence on the business mix of shopping districts unless it owns

business premises to lease to preferred businesses on conditions to attract them. However,

government does own buildings for the delivery of a large number of services that are virtual

monopolies, such as libraries, health centres. Many of these are accessed in a similar way as

shops and have similar location requirements. Although they do not make sales in the

conventional manner they can be effective anchors for concomitant shopping destinations. Public libraries are particularly popular and inclusive destinations: there are effective anchors for a

shopping district. Bay Street is fortunate in that it has an active library at the north end: in the

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 35

block between Spring Street North and Spring Street South. Libraries increase the cultural

opportunities for local residents and are important community facilities for that reason alone.

However, they are also used by the widest cross section of society: by all ages, by both genders,

by all education levels and by all ethnic groups. More importantly a large percentage of the

Australian population use libraries: Australia has a participation rate of over 30% and on average

Australians access a library 5 times per year (Australian Bureau of Statistics).

A library can be a compelling reason for shoppers to go to a shopping district and a point of

difference from other shopping destinations without a library. Local governments often overlook

the significance of libraries to the economic viability and social vitality of shopping districts. They

often prefer out-of-centre locations surrounded with car parking because of the cost saving. This

removes an important magnet for the shopping district but also may reduce library usage.

Ironically, corporate shopping centres recognise the importance of libraries as magnets and are

prepared to provide space for them at peppercorn rents. For example, the City of Maribyrnong

(Metropolitan Melbourne) has a branch library in Highpoint City, Melbourne’s largest shopping

centre, for a rent of $50/ annum on a 30 year lease. The City of Knox has a library in Knox City

Shopping Centre for $1/ annum.

The Port Melbourne public library at the north end of Bay Street could and should be made an

anchor for a business niche and spatial precinct that includes not only the library itself but other retail uses. Libraries appropriately located within a shopping district can serve an anchor role that is only surpassed in drawing power by the supermarkets. A good library can stimulate the establishment of

commercial businesses selling: books and magazines, stationary goods, computers, coffee and

other refreshments, travel products and the likes. This precinct of Bay Street is not very vital and

it is in need of a major injection of public funds to stimulate private sector investment and

business change. Note that if the existing library is deemed unsuitable there may be prospects

for developing a bigger and better one at the south end of Bay Street as part of the tourist,

entertainment precinct.

Libraries are becoming increasingly wide in the scope of their services. Some libraries have

meeting rooms, theatres, exhibition spaces, coffee shops, cafes, telephones and public notice

boards all of which draw in potential shoppers to the district. Some are organisers of community

events such as art exhibitions, talks, demonstrations and public meetings. As such, they make a

significant contribution to community building.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 36

Appendix

Economic and Social Order in Retailing and Shopping

Behind the apparent haphazard mixture and location of shops and services on traditional shopping

streets, there is an underlying economic and social order that is analysable.

Agglomeration Forces in the Clustering of Shops

Shopping is commonly multi-purpose: several commodities are purchased on one shopping trip.

Consumers choose a shopping destination from competing destinations according to the likelihood

of obtaining all required goods and the attractiveness of any shopping destination is largely a

function of the range of goods on offer at competitive prices.

Consumer choice of goods tends to increase directly with the number of shops clustered and

agglomeration provides a greater probability of getting needs satisfied. The agglomeration gives

customers a greater opportunity for choosing their requirements within a given expenditure of

time and money: it reduces the travel and search costs of shopping.

Furthermore, purchase of some goods creates demand for other goods with which they have an

affinity. For example, a purchase of a new shirt induces demand for a tie or a new dress induces

demand for shoes and purchase of meat induces demand for vegetables to complete a menu.

In this there are major advantages in retail businesses clustering together (rather than

dispersing), even with those with which they are in direct competition and business entrepreneurs

respond appropriately. Most empirical studies on the location of shopping outlets indicate strong

propensity to agglomerate. However, this tendency appears to vary with the particular functions

and the extent to which it occurs remains a contentious issue.

Although retailing is primarily an economic phenomenon, it is also a social one. Shopping

destinations commonly offer more than standard commodities: they offer a range of opportunities

such as personal services, entertainment and cultural activities. In making choices about a

shopping destination, shoppers are influenced by the availability of facilities such as libraries,

coffee shops, entertainment complexes and health centres.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 37

Synergy, Externalities and Critical Mass in Retail Clustering.

There is an observable phenomenon in shopping in which the drawing power and trading

performance of a group of shops is greater than that of the sum of the individual shops. This

accumulative effect is referred to as synergy

Synergy is a medical term, which refers to coordination in the action of muscles, organs or drugs.

The term is used in retail planning in reference to the coexistence of two, or more, shopping/

business activities that are mutually supportive.

Critical mass, another jargon term, is the size and functional composition at which synergy or

symbiosis occurs, usually measured as floorspace.

Synergy and critical mass are concepts not only of interdependence and size of uses but also of

their placement and compactness. Synergy and shoppers' perception of critical mass tend to be

fostered by agglomeration of uses and to be nullified by their dispersion. The terms are used

conceptually rather than empirically and few planners or researchers are able to define them

specifically. They serve to emphasise that shopping centres and streets function as accumulative

entities and the importance of choosing merchandise/ tenants to complement and reinforce the

whole entity.

The fundamental principle in the planning of corporate shopping centres is to provide and locate a

mix of merchandise/ tenants to maximise synergy. It is much easier to generate synergy in

shopping centres than in shopping streets because of the ability to achieve a more precise

functional composition. However, the same economic forces are in place and the same principles

apply.

Some retail businesses have characteristics of use or built form that has an effect on the

efficiency and attractiveness of adjacent businesses. Synergy is created, or destroyed, by such

characteristics and they have an economic effect on neighbouring businesses and the whole

business district. This is the externality effect, so called.

An externality is an economics term referring to the effect of one business on the economic

performance of another without any monetary transaction occurring between them. An

externality can be positive: conferring benefits and appreciating synergy. For example, the

operation of a noted department store increasing the trading potential of a fashion boutique next

door. Alternatively, an externality can be negative: imposing costs and depreciating synergy. For

example, the operations of an adult sex aid shop decreasing the trading potential of a fashion

boutique next door.

Fundamentally, it is advantageous to minimise negative externalities and to maximise positive

externalities. This can be done by separating those uses and built forms which cause negative

externalities and clustering together those which provide positive externality effects.

It is inherently desirable for shopping centres and streets to make decisions that increase positive

externalities and reduce negative externalities so that synergy in the shopping environment is

maximised.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 38

Magnet and Dependent Relationships in Clustered Shops

Distinction can be made in shopping destinations between shops with a high profile and drawing

power and those with a low profile and drawing power.

High profile shops are those that are highly recognised in their retail environment, are major

shopping destination and draw customers to themselves in their own right. These magnet or

anchor shops develop their high public profile and drawing power from consistent advertising,

record of quality goods and service, and the likes. Department stores, such as Myer or Target are

the ultimate magnets in Melbourne.

At the other extreme, there are dependent shops that have a low profile in their retail

environment, have a small drawing power and depend on passing custom attracted by the

magnet shops. Dependent shops make different degrees of contribution, according to their type,

quality and public profile. For example, many of the chains of small shops such as Country Road

and Body Shop, have a high public profile generated over an extensive period of service and

advertising and are minor attractions in their own right. Others are almost totally dependent on

the drawing power of the magnets; for example, confectionary shops.

The planning and design of corporately owned shopping centres is based on such principles with

small shops subsidising the rents of their larger magnet shops. For example, department stores

pay less rent per sq metre than the small shops clustered around them. This same retail affinity

between magnet and dependent shops exists along shopping streets. However, it is not so

formalised nor are there any means of collecting revenue for externalities bestowed and using it

to subsidise the establishment of the magnets.

The overall status and drawing power of any shopping entity is determined largely by the quality

of its magnets. The distinction between magnet and dependent shops is not absolute: there are

degrees in the profile level and drawing power of shops. For example large supermarkets also

have a high profile and acknowledged drawing power but not as large as that of a major

department store.

It is unlikely that Bay Street can ever attract a major department store when other major

shopping destinations such as High Street, Armadale and Chapel Street cannot. A supermarket is

likely to be that best that can be achieved as a primary magnet. However, there may be

prospects for also attracting second string discount department stores such as Dimmeys selling

general personal goods.

Application of retail principles to drive and appropriate business mix

The most significant component in the appeal of any shopping destination: corporate shopping

centre or traditional shopping district is the range of goods on offer at competitive prices: the

business mix.

The function/ tenancy mix component of a business plan sets out a preferred and proposed

functional composition for a shopping district. It is an identification of appropriate businesses to

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 39

be targeted for modification, expansion, contraction, recruitment, and the like. The end result

should be a schedule of existing and proposed functions together with a statement of their future

state. For example:

• ‘food: organic fresh food business to be developed or recruited’; or

• ‘restaurants/ cafes: one of existing restaurants/ cafes to be encouraged to increase its

status and service to cater for a higher quality and cost niche’.

It is acknowledged that under current planning legislation it is simply not possible to regulate the

actual business or tenancy mix within Business1 zones: a shop= a shop, of whatever type.

However, in subsequent recruitment efforts it is important to have a clear understanding of what

is and is not sought and favoured.

The importance of having complementary non-retail uses is acknowledged and consequently the

schedule should include any non-retail uses to be developed.

It is important that any list of optimum functions and tenants be tempered with pragmatism

because it needs to be implementable. Consequently, it should propose an optimum, not in the

‘ideal’ sense, but the ‘best possible’ in recognition of constraints identified in audits done

previously.

The SWOT concept and terminology is used widely in planning for the revitalisation of shopping

districts. For example, it pervades much of the literature of the UK’s Association of Town Centre

Management. It is common in literature on marketing where it is applied to the analysis of the

competitiveness of individual companies. It is an acronym of the four components of the

analysis:

• strengths;

• weaknesses;

• opportunities;

• threats. The intention of a business function/ tenancy audit is to identify the strengths and weaknesses in

the performance of an existing function/ tenancy mix to assist in deriving a better functional

composition. In turn, this is a means to the identification of functions to be introduced, deleted,

expanded and reduced from a shopping district; which is part of a business plan. Consequently, it

is particularly useful to identify those functions and tenancies that are lacking in a shopping

district or in competing shopping destinations.

Economic Clusters or Niches

Whilst it is clearly advantageous to have a major new injection of a generative business or

magnet complex to ‘kick start’ any shopping district revitalisation, the opportunity does not

emerge often. Fortunately, it is possible to generate considerable drawing power by creating a

critical mass of small shops directed at a particular customer segment or niche.

In devising a function/ tenancy plan it is important not only to specify commodities individually

but also as clusters based on economic themes or niches. For example, appropriate clothing,

shoes, cosmetics, jewellery, hair dressings are economically linked in a 'ladies’ fashion' niche.

Future Directions for Bay Street / Retail Floorspace Review

20082125 Future Directions for Bay Street_04_Final.doc P. 40

There are examples in Melbourne where revitalisation of shopping districts has happened with

clusters of specialist shops. Bridge Road, Richmond, was once a dilapidated shopping district

today it is a major shopping destination for ladies fashion: a niche serving the metropolitan-wide

role. Similarly, Victoria Street Collingwood is a revitalised strip centre based on the needs of

ethnic Vietnamese customers.

The purpose of auditing, discussed previously, is to assist with identification of niches that are

particular significant in a trade area and that need to be given additional support. Any commodity

gaps in existing niches represent a prospect for recruitment and business success since there is

already an established customer base.

The end result of any business plan is the improvement of the business turnover of a shopping

district as an entity. Increased shopper expenditure has to be accommodated by targeting

businesses to improve the performance of shopping districts, achievable through:

• restructuring existing businesses in existing, expanded or relocated businesses;

• attraction of new businesses and premises.

Generally the revitalisation of a shopping district involves attracting new traders and new real

estate and plans should acknowledge this. However, change and growth can also occur with

existing traders and real estate. Revitalisation policies and programs based on improvement to

the existing business environment are often more appropriate, easier to implement and more cost

effective. In particular, it is more difficult to mount opposition against policies and programs to

improve business efficiency than it is to do so against those promoting new development.

Business targeting decisions tend to include a measure of both new and existing businesses.