revision on the uk economy as and a2 economics may 2009

TRANSCRIPT

Revision on the UK Economy

AS and A2 Economics

May 2009

Annual percentage change in GDP at constant pricesThe Economic Cycle - Growth in UK National Output

Source: UK Statistics Commission

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

Pe

rce

nt

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

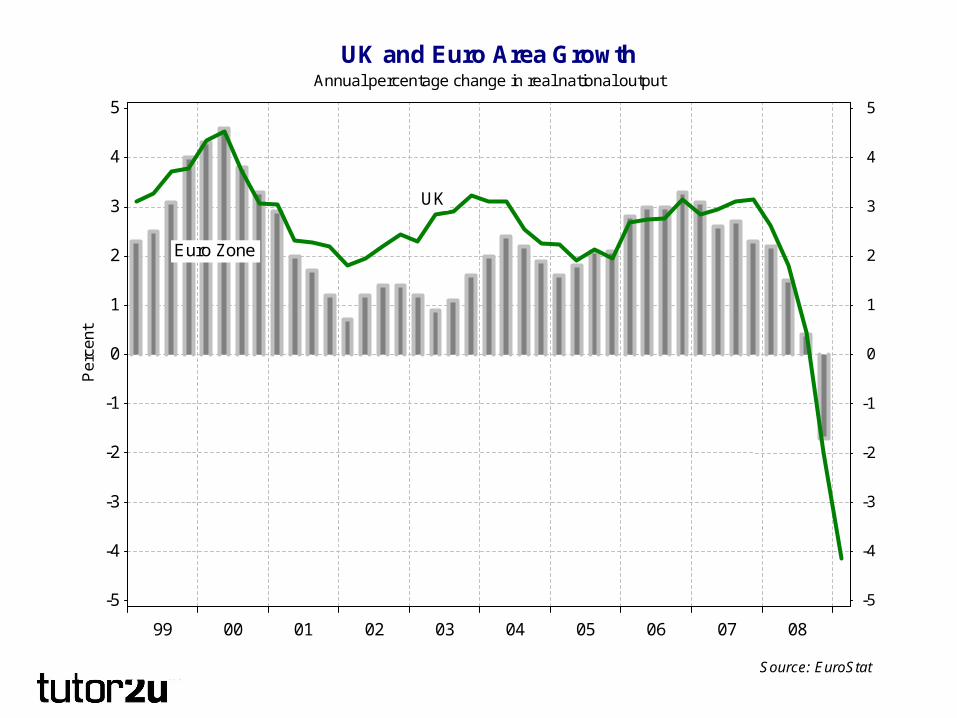

Annual percentage change in real national output

UK and Euro Area Growth

Source: EuroStat

99 00 01 02 03 04 05 06 07 08

-5

-4

-3

-2

-1

0

1

2

3

4

5P

erc

en

t

-5

-4

-3

-2

-1

0

1

2

3

4

5

Euro Zone

UK

Percentage rate of growth year on year at constant prices

United States - Growth and Unemployment

Source: Reuters EcoWin

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

3.5

4.0

4.5

5.0

5.5

6.0

6.5

7.0

7.5

8.0

8.5

Pe

rce

nt

3.54.04.55.05.56.06.57.07.58.08.5

Unemployment Rate (% of labour force)

-1

0

1

2

3

4

5P

erc

en

t

-1

0

1

2

3

4

5

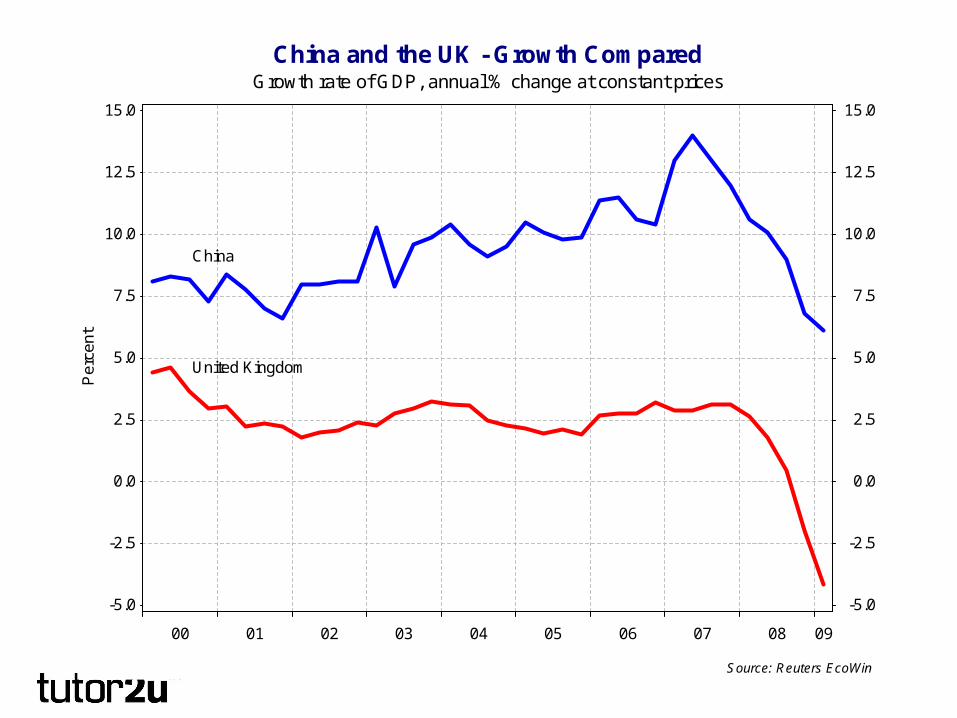

Economic Growth

Growth rate of GDP, annual % change at constant pricesChina and the UK - Growth Compared

Source: Reuters EcoWin

00 01 02 03 04 05 06 07 08 09

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0P

erc

en

t

-5.0

-2.5

0.0

2.5

5.0

7.5

10.0

12.5

15.0

China

United Kingdom

Evidence for the stock cycle in the UK

Changes in stocks and the UK economic cycle

Source: Reuters EcoWin

00 01 02 03 04 05 06 07 08 09

bill

ion

s

-5

-4

-3

-2

-1

0

1

2

3

4

£ (

bill

ion

s)

-5

-4

-3

-2

-1

0

1

2

3

4

Changes in stocks (a negative figure indicators that businesses were reducing their stock levels)Change in the value of stocks

-5-4-3-2-1012345

Pe

rce

nt

-5-4-3-2-1012345

GDP growth Real GDP Growth

Economics Blog

Recession - causation

• Global credit crisis• Asset price deflation• Rising food and oil prices• Cuts in real disposable income• Collapse of consumer and business sentiment• De-globalisation• Falling profits, investment• Labour shedding• Financial crisis has spread to the real economy

Index of Prices 2000=100

The Economist Commodity Price Index

Source: Economist Commodity Price Index

05 06 07 08 09

100

125

150

175

200

225

250

275

300

325In

de

x

100

125

150

175

200

225

250

275

300

325

All Commodities

Industrial Metals

Food

FTSE 100 index (bottom pane) Average UK house price (top pane)

FTSE 100 and Average UK House Prices

Source: Reuters EcoWin

00 01 02 03 04 05 06 07 08 09

3000

4000

5000

6000

7000

Ind

ex

3000

4000

5000

6000

7000

FTSE 100

80000

100000

120000

140000

160000

180000

200000

£s

80000

100000

120000

140000

160000

180000

200000House Prices

Expectations over next 12 months, % balance of optimists over pessimists

Confidence will need to improve before recovery arrives

Source: Reuters EcoWin

01 02 03 04 05 06 07 08 09

-60

-50

-40

-30

-20

-10

0

10

20N

et b

ala

nce

-60

-50

-40

-30

-20

-10

0

10

20

General state of the economy

Likely to make major purchases

People's Own Financial Situation

Net % balance of people expecting higher unemployment in the next yearUnemployment Expectations

Source: Reuters EcoWin

86 88 90 92 94 96 98 00 02 04 06 08

-20

-10

0

10

20

30

40

50

60

70

80

Ne

t ba

lan

ce

-20

-10

0

10

20

30

40

50

60

70

80

Percentage of disposable income that is saved, quarterly data

Household Savings Ratio

Source: UK Statistics Commission

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0P

erc

en

t

-2.0

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

£ billion per month, seasonally adjusted dataUnited Kingdom Exports to Euro Zone Countries

Source: Reuters EcoWin

03 04 05 06 07 08 09

bill

ion

s

7

8

9

10

11

12

13

14

GB

P (

bill

ion

s)

7

8

9

10

11

12

13

14Figures for 2006 affected by MTIC VAT fraud, also known as 'carousel fraud'

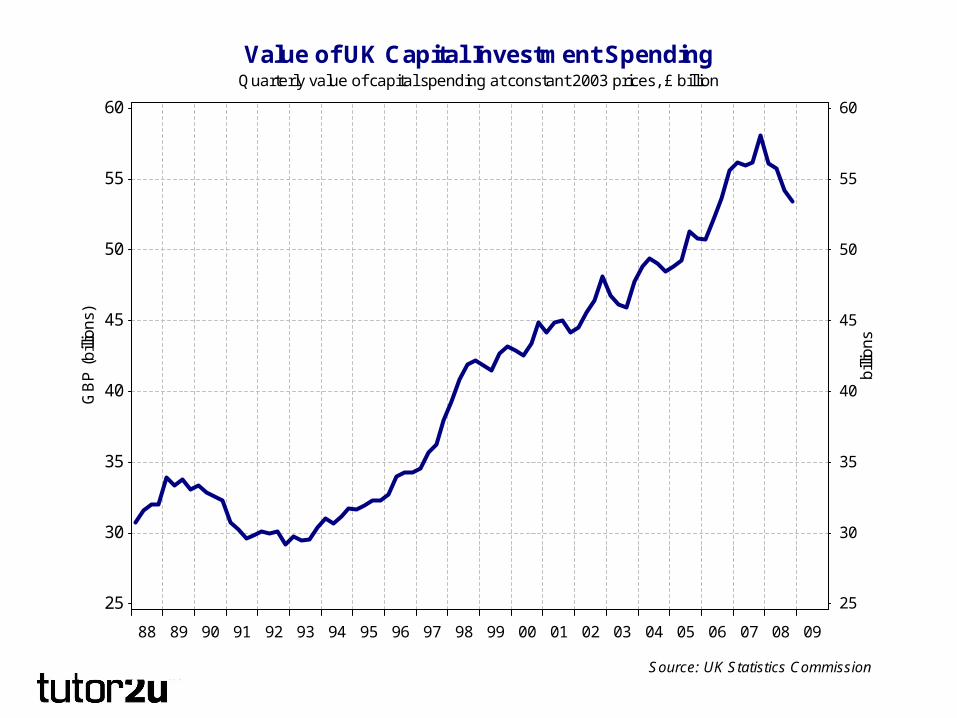

Quarterly value of capital spending at constant 2003 prices, £ billion

Value of UK Capital Investment Spending

Source: UK Statistics Commission

88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

bill

ion

s

25

30

35

40

45

50

55

60G

BP

(b

illio

ns)

25

30

35

40

45

50

55

60

Recession Fallout

Actual GDP - Potential GDP, measured as a percentage of potential GDP source: OECD

United Kingdom, Output gap of the total economy

Source: OECD World Economic Outlook

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10

-4

-3

-2

-1

0

1

2

3

4

5P

erc

en

tag

e o

f p

ote

ntia

l GD

P

-4

-3

-2

-1

0

1

2

3

4

5

Annual percentage change in GDP at constant prices and Short Term unemployment

Unemployment and the Economic Cycle

Source: Reuters EcoWin

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08

-5

-4

-3

-2

-1

0

1

2

3

4

5

Pe

rce

nt

-5

-4

-3

-2

-1

0

1

2

3

4

5

Annual growth of real GDP

mill

ion

s

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25P

ers

on

(m

illio

ns)

0.85

0.90

0.95

1.00

1.05

1.10

1.15

1.20

1.25

People out of work for up to six months (LFS measure)

UK Real GDP Growth and Consumer Price Inflation. annual percentage change

UK Growth, Inflation and Policy Interest Rates

Source: Reuters EcoWin

02 03 04 05 06 07 08 09

-5

-4

-3

-2

-1

0

1

2

3

4

5

6

Pe

rce

nt

-5-4-3-2-10123456

Base interest rates

Real GDP growth

Consumer price inflation

0

1

2

3

4

5

6P

erc

en

t

0

1

2

3

4

5

6

Base Interest Rates

Policy Interest Rates

Annual percentage change in the retail price index and CPI

Retail Price and Consumer Price Inflation in the UK

Source: UK Statistics Commission

97 98 99 00 01 02 03 04 05 06 07 08 09

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0P

erc

en

t

-2.0

-1.0

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Consumer price index

All items retail price index (RPI)

Bank of England/NOP, how do you expect prices to change over the next 12 months?

Inflation Expectations

How do you expect prices to change over the next 12 months? How has prices changed over the past 12 months?

Source: Bank of England

99 00 01 02 03 04 05 06 07 08 09

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5P

erc

en

t

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

Annual percentage change in consumer prices, unemployment rate (%)

UK Unemployment and Consumer Price Inflation

Source: Reuters EcoWin

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

-2

-1

0

1

2

3

4

5

6

7

8

9

10P

erc

en

t

-2

-1

0

1

2

3

4

5

6

7

8

9

10

Unemployment

Inflation

Source: OECD World Economic Outlook

UK - Potential GDP and Trend Growth

Source: OECD World Economic Outlook

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

tho

usa

nd

bill

ion

s

0.750.800.850.900.951.001.051.101.151.201.251.30

Re

al G

DP

(th

ou

san

d b

illio

ns)

0.750.800.850.900.951.001.051.101.151.201.251.30

Potential GDP

Potential GDP for the UK

1.50

1.75

2.00

2.25

2.50

2.75

3.00P

erc

en

t

1.50

1.75

2.00

2.25

2.50

2.75

3.00Estimated UK Trend Growth Rate

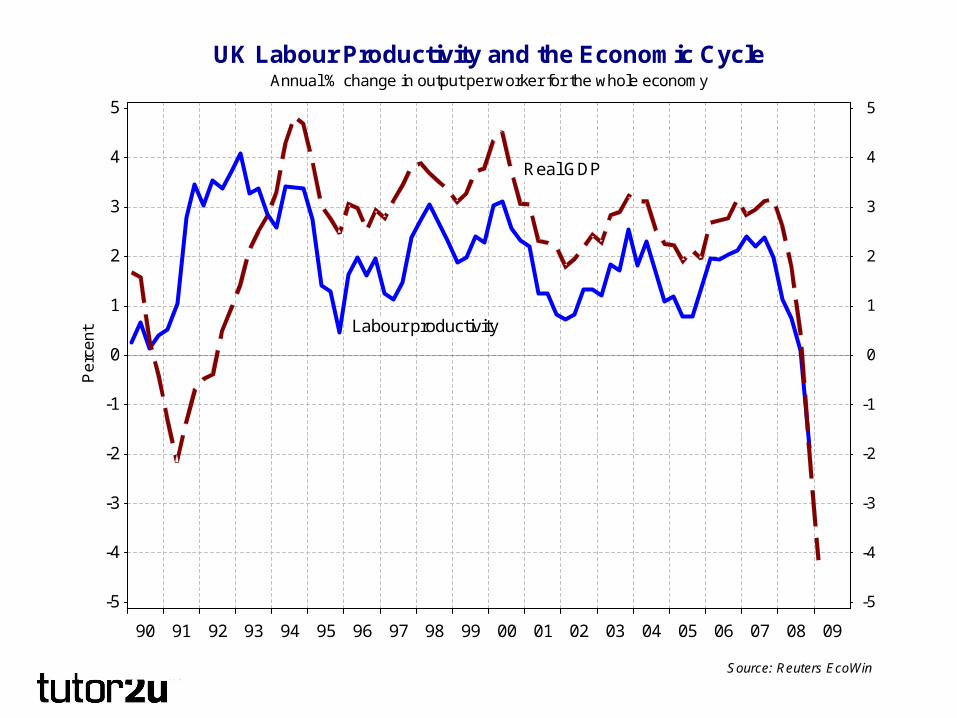

Annual % change in output per worker for the whole economy

UK Labour Productivity and the Economic Cycle

Source: Reuters EcoWin

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09

-5

-4

-3

-2

-1

0

1

2

3

4

5P

erc

en

t

-5

-4

-3

-2

-1

0

1

2

3

4

5

Labour productivity

Real GDP

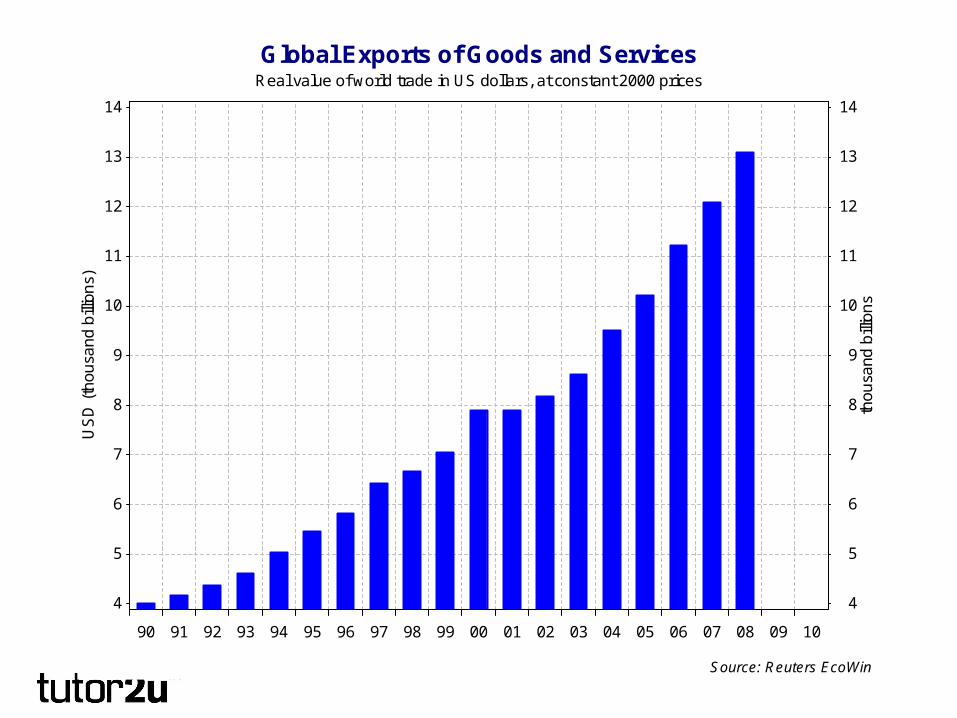

Real value of world trade in US dollars, at constant 2000 prices

Global Exports of Goods and Services

Source: Reuters EcoWin

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

tho

usa

nd

bill

ion

s

4

5

6

7

8

9

10

11

12

13

14U

SD

(th

ou

san

d b

illio

ns)

4

5

6

7

8

9

10

11

12

13

14

Economics Blog

Recession Fallout – Key Points

• Cyclical consequences– Unemployment– Rising budget deficit– Falling business investment– Inflationary pressures easing / wage cuts?

• Possible semi-permanent effects– Rising structural unemployment– Other hysteresis effects including business failures– Changes to financial system – tougher regulation of

banking and other financial services– Will the UK’s trend growth suffer? LRAS impact?

Policy Responses

Economics Blog

Pulling every lever

• Policy rates have moved to the floor (0.5%)• £75bn quantitative easing (March 2009)• 25% depreciation of sterling over last 12 months• Injection of capital into the banking system• Government borrowing of more than 12% of

GDP (annual fiscal deficit > £175bn)• National debt that > 80% of GDP within 2 years

Percentage - set by the Bank of England Monetary Policy Committee

Monetary Policy Interest Rates in the UK

Source: Bank of England

00 01 02 03 04 05 06 07 08 090

1

2

3

4

5

6P

erc

en

t

0

1

2

3

4

5

6

Per Cent

Interest Rates for the Euro Zone, the UK and the USA

Euro Zone Interest Rate United States Interest Rate United Kingdom Base RateSource: Reuters EcoWin

03 04 05 06 07 08 090.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0P

erc

en

t

0.0

0.5

1.0

1.5

2.0

2.5

3.0

3.5

4.0

4.5

5.0

5.5

6.0

USA Interest Rates

Bank of England Rates

Euro Zone Interest Rates

Per cent, source: Bank of England

The Cost of Borrowing

Source: Bank of England

04 05 06 07 08 090.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0P

erc

en

t

0.0

2.0

4.0

6.0

8.0

10.0

12.0

14.0

16.0

18.0

20.0

Mortgage rates

Base Interest Rates (set by BoE)

Overdrafts

Credit cards

Trade-weighted index value for sterling in the foreign exchange market, daily value

United Kingdom Effective Exchange Rate Index

Source: Reuters EcoWin

04 05 06 07 08 09

70

75

80

85

90

95

100

105

110In

de

x

70

75

80

85

90

95

100

105

110

Trade-weighted index value for sterling in the foreign exchange market, daily valueSterling and Base Interest Rates

Source: Reuters EcoWin

Jan07

Mar May Jul Sep Nov Jan08

Mar May Jul Sep Nov Jan09

Mar May

70

75

80

85

90

95

100

105

110

Ind

ex

70

75

80

85

90

95

100

105

110

Sterling Exchange Rate Index (trade-weighted)

0.0

1.0

2.0

3.0

4.0

5.0

6.0P

erc

en

t

0.0

1.0

2.0

3.0

4.0

5.0

6.0

Base Interest Rates

US dollars per £1, daily closing exchange rateDollar-Sterling Exchange Rate

Source: Reuters EcoWin

Jan06

Apr Jul Oct Jan07

Apr Jul Oct Jan08

Apr Jul Oct Jan09

Apr Jul Oct

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

GB

P/U

SD

1.3

1.4

1.5

1.6

1.7

1.8

1.9

2.0

2.1

2.2

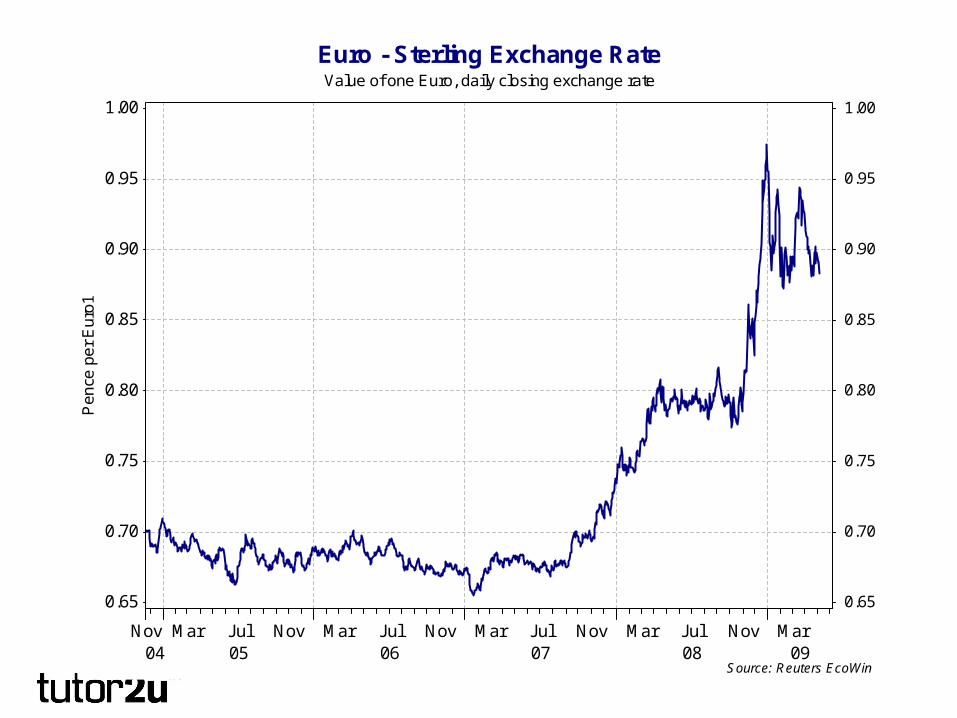

Value of one Euro, daily closing exchange rate

Euro - Sterling Exchange Rate

Source: Reuters EcoWin

Nov04 05

Mar Jul Nov06

Mar Jul Nov07

Mar Jul Nov08

Mar Jul Nov09

Mar

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00P

en

ce p

er

Eu

ro1

0.65

0.70

0.75

0.80

0.85

0.90

0.95

1.00

Economics Blog

Bank of England – From Independence to Impotence?

1. Nowhere to go on policy interest rates – liquidity trap reached?

2. Inflation target is being ignored for now (will there be a change?)

3. The key rate now is on government bonds - not the base rate

4. Government committed to HUGE borrowing £175bn in 2010

5. Will the Bank buy as many bonds as the government needs? Or will the bank say enough is enough?

6. For most people the base rate of interest is an irrelevance 1. Look at the cost of unsecured credit

2. Even if borrowing costs are low, can you actually get a loan?

Budget Balance = Tax revenues - Total Government Spending, £ billionUK Government Budget Balance

Source: Reuters EcoWin

80 82 84 86 88 90 92 94 96 98 00 02 04 06 08 10 12

bill

ion

s

-170

-160

-150

-140

-130

-120

-110

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

£ (

bill

ion

s)

-170

-160

-150

-140

-130

-120

-110

-100

-90

-80

-70

-60

-50

-40

-30

-20

-10

0

10

20

Measured as a percentage of national income (09-10 is a forecast from the OECD)

UK Government Spending and Taxation

Source: OECD World Economic Outlook

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10

36

37

38

39

40

41

42

43

44

45

46

47

48

49P

er

cen

t of G

DP

36

37

38

39

40

41

42

43

44

45

46

47

48

49

Total Tax Revenue

Government Spending Budget deficit where G>T

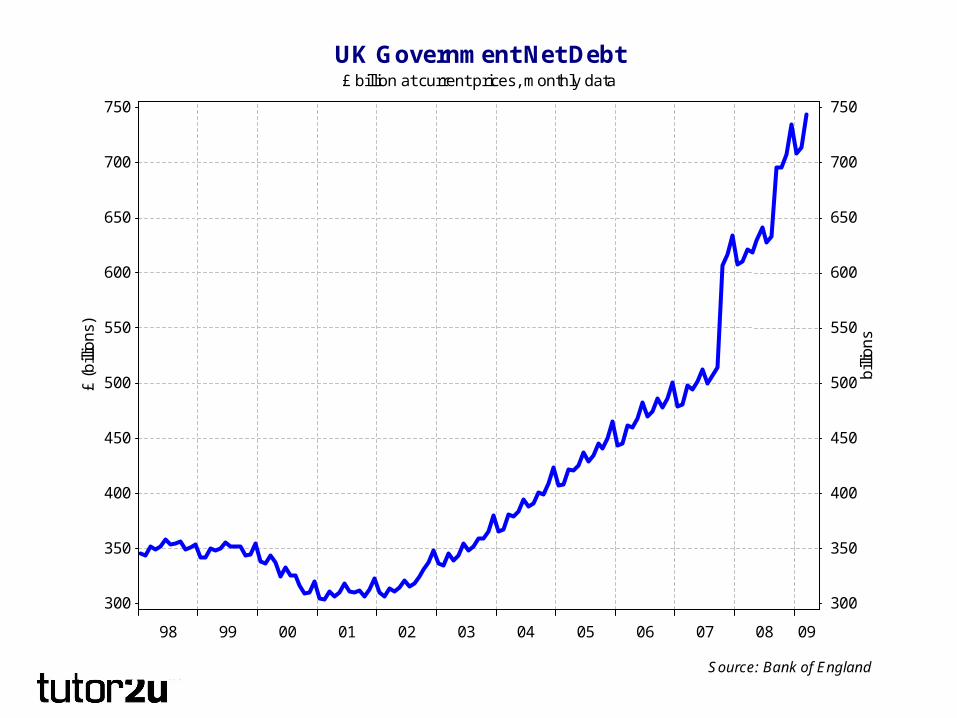

£ billion at current prices, monthly data

UK Government Net Debt

Source: Bank of England

98 99 00 01 02 03 04 05 06 07 08 09

bill

ion

s

300

350

400

450

500

550

600

650

700

750£

(b

illio

ns)

300

350

400

450

500

550

600

650

700

750

Economics Blog

Evaluation

• Monetary and fiscal policy are now joined at the hip• Short term – appetite (demand) for bonds eases the

problems of financing an eye-wateringly large fiscal deficit

• Good fiscal stimuli are timely, targeted, and temporary• But there is no such thing as a free lunch• Fiscal policy will need to be tightened • There will be some crowding out of the private sector• We cannot ignore the risk of resurgent inflation in a

recovery – whenever that comes• Weak sterling poses a major credit (solvency) risk for the

UK government – even if we are not (quite) an Iceland

For essential last minute revision on Economics, don’t forget to visit

the Economics Blog everyday