risk management and indian banking: opportunities and challenges · risk management and indian...

TRANSCRIPT

Risk managementand Indian Banking:

Opportunities and ChallengesSusan Thomas

http://www.igidr.ac.in/˜susant

IGIDR

Bombay

Risk managementand Indian Banking:Opportunities and Challenges – p. 1

Background

Risk managementand Indian Banking:Opportunities and Challenges – p. 2

The problem

Banking is risky business!

1. Very high leverage:India: Food 1.1, Machinery 0.6, Automobiles 1.1, Auto

Ancillaries 1.19, Banking 17.6.

US: Manufacturing 0.25-0.35, Utilities 1.4-1.5, Trade 0.3-0.4,

Banking 15.

2. Opaque assets: Loans, OTC derivatives. Non-transparent OTC

trading.

3. Moral hazard: Deposit insurance.

Nobel Laureate Merton Miller: “Banking is a disasterprone 19th century industry”.

Risk managementand Indian Banking:Opportunities and Challenges – p. 3

The goals of Basel norms

In the late eighties, there was a lot of cross-borderlending particularly by the Japanese banks.Japanese banks grew enormously and gatheredmarket share; Western banks complained aboutJapanese banks being regulated badly.

Basel I was an attempt to standardise the regulationgoverning the global banking industry.

The heart of the Basel I norms defined minimumrequired equity capital, i.e. an attempt to containleverage.

Risk managementand Indian Banking:Opportunities and Challenges – p. 4

Basel I, contd.

Required equity capital was a single numbercalculated as a fraction of the risk weighted assets(RWA).

RWA = w1x1 + w2x2 + . . ., where x1 was corporateexposure, and w1 = 1.The weights for all the other classes of assets was setat less than 1.

The main focus appeared to be on addressing creditrisk.

The minimum equity requirement was set through aminimum Capital Adequacy Ratio (CAR), attypically 8% of RWA.

Risk managementand Indian Banking:Opportunities and Challenges – p. 5

What was right about the Basel Cap-ital Accord

The CAR requirement did reduce the extremely highlevels of leverage in the banking industry.

Risk managementand Indian Banking:Opportunities and Challenges – p. 6

What was wrong about the BaselCapital Accord

The calculation of RWA is incorrect.Risks in the banking portfolio are not linear.

Assets were classified on very broad lines.(Eg. OECD government bonds.)

The focus on credit risk gave banks incentives tofind new ways of bearing risk.(Eg. higher exposure in interest rate risk, OTC derivatives.)

Ignored the problem of opacity - loans, OTCderivatives, OTC trading.

Ignored differences between countries.(If 8% works for the OECD, what is correct for India?)

Risk managementand Indian Banking:Opportunities and Challenges – p. 7

Negative consequences

Even though these were broad recommendations,they became rigid in the hands of weak bankingregulators.This became especially problematic countries wherethe regulatory framework was not strong enough todevelop their own risk management rules.

The focus shifted from taking risks with a clearunderstanding of the returns, to blindly using BISrules.

Risk managementand Indian Banking:Opportunities and Challenges – p. 8

Basel II

An attempt to move away from linear rules of thumb.

Some of the implementation involvesTrying to improve upon the linear formula.

Reliance on credit ratings.

Exploit “internal models” of risk measurement in banks.

Taking more interest in incentives - of banks, of securities

markets.

This is still ‘playing the game of Basel I’ - but trying tofind a better formula for equity capital.

Risk managementand Indian Banking:Opportunities and Challenges – p. 9

What India should do with Basel-II

We should not repeat the mistakes about Basel-I –that of blindly adopting some externally supplied setof rules.

We should treat Basel-II as a set of interesting ideas,and craft a new framework of banking regulationbased on genuine understanding of risk.

Risk managementand Indian Banking:Opportunities and Challenges – p. 10

Improving Indian banking regula-tion

Need to develop models for interest rate VaR.

Need to develop models of credit risk.

Banks must be given incentives to create such models

internally. One proposal:

The bank must present their internal risk models to the

regulator, and if they are good enough, be used for the

calculation of CAR.

Need to move towards more transparent assets – bonds, not

loans; exchange traded, not OTC derivatives.

These require sound market design.

Importance of market discipline; models of bank failure

probability based on the stock price.

Importance of correct pricing of deposit insurance.

Risk managementand Indian Banking:Opportunities and Challenges – p. 11

Progress in India oninterest rate risk modelling

Risk managementand Indian Banking:Opportunities and Challenges – p. 12

Importance of fixed income risk

There is some evidence that banks in Indiasubstituted credit risk by interest rate risk when RBIlay down a common risk management frameworkfor the Indian banking sector based on Basel-I.

Patnaik & Shah (2002): Roughly two-thirds ofbanks in India would lose more than 25% of equitycapital when faced with a 99% shock.

Existing rules about interest rate risk regulation arewrong: i.e. 2.5% risk weightage, and IFR.

Risk managementand Indian Banking:Opportunities and Challenges – p. 13

Fixed income VaR

The yield curve fluctuates - this generates price riskfor every fixed income portfolio.

We seek statements like “VaR for the portfolio at a99% level on a one-day horizon”.

This is the rupee loss which will be exceededtomorrow with a 1% probability.

Risk managementand Indian Banking:Opportunities and Challenges – p. 14

Fixed income VaR

faces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.

This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Fixed income VaR

faces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.

This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.

This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Fixed income VaR

faces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.

This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.

This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.

This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Fixed income VaRfaces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.

This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.

This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.

This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Fixed income VaRfaces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.

This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.

This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Fixed income VaRfaces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.

This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Fixed income VaRfaces serious hurdles

Make a model about fluctuations of the yield curve.Simulate 10,000 draws from it.This requires a good model telling us how the entireyield curve fluctuates.

Reprice the full portfolio at each of these draws.This requires a sound pricing technology wherebythe impact of alternative yield curves is clearlyknown.

So we get 10,000 outcomes for the profit/loss on theportfolio on a one-day horizon.Read off the 100th worst loss after sorting these10,000 numbers.This is easy.

Risk managementand Indian Banking:Opportunities and Challenges – p. 15

Difficulties in testing

VaR methodologies must be backed by testing.

Banking applications require VaR over longhorizons.

Here the tests of VaR are particularly weak.

Data in India is weak.

We should be careful in knowing what we do notknow.

Risk managementand Indian Banking:Opportunities and Challenges – p. 16

Fixed income derivatives

So far we have only talked about bonds.What about interest rate futures, interest rateoptions?

Jayanth Varma’s Risk Management Committee hasworked on models for computing VaR on a one-dayhorizon.(The committee report is on the SEBI website.)

This is fundamentally easier, since we seek only aone-day horizon, not a one-year horizon.

Committee observes lack of scientific knowledge,but is confident about conservative approximations.

This work will drive collateral requirements forinterest rate futures and options.

RBI’s guidelines for OTC interest rate derivatives(1999) are not based on analysis of risk.

Risk managementand Indian Banking:Opportunities and Challenges – p. 17

Progress in India oncredit risk modelling

Risk managementand Indian Banking:Opportunities and Challenges – p. 18

Credit risk requires three steps

What is the failure probability of a bond?This is about predicting default.

What is the loss given default?This is about creditors rights.

The above two give how much risk premium tocharge for a loan.This has logic like the CAPM - betas, systematicrisk.

How do we put the pieces together to think aboutportfolio VaR?What you can’t diversify has to be priced over andabove simple risk-neutral reasoning.

Risk managementand Indian Banking:Opportunities and Challenges – p. 19

Credit risk requires three steps

What is the failure probability of a bond?This is about predicting default.

What is the loss given default?This is about creditors rights.

The above two give how much risk premium tocharge for a loan.This has logic like the CAPM - betas, systematicrisk.

How do we put the pieces together to think aboutportfolio VaR?What you can’t diversify has to be priced over andabove simple risk-neutral reasoning.

Risk managementand Indian Banking:Opportunities and Challenges – p. 19

Credit risk requires three steps

What is the failure probability of a bond?This is about predicting default.

What is the loss given default?This is about creditors rights.

The above two give how much risk premium tocharge for a loan.This has logic like the CAPM - betas, systematicrisk.

How do we put the pieces together to think aboutportfolio VaR?What you can’t diversify has to be priced over andabove simple risk-neutral reasoning.

Risk managementand Indian Banking:Opportunities and Challenges – p. 19

Credit risk requires three steps

What is the failure probability of a bond?This is about predicting default.

What is the loss given default?This is about creditors rights.

The above two give how much risk premium tocharge for a loan.This has logic like the CAPM - betas, systematicrisk.

How do we put the pieces together to think aboutportfolio VaR?What you can’t diversify has to be priced over andabove simple risk-neutral reasoning.

Risk managementand Indian Banking:Opportunities and Challenges – p. 19

Situation in India

Problem What we know

Failure of a bond Quite a bitLoss given default Little.Portfolio credit risk Very little.

Risk managementand Indian Banking:Opportunities and Challenges – p. 20

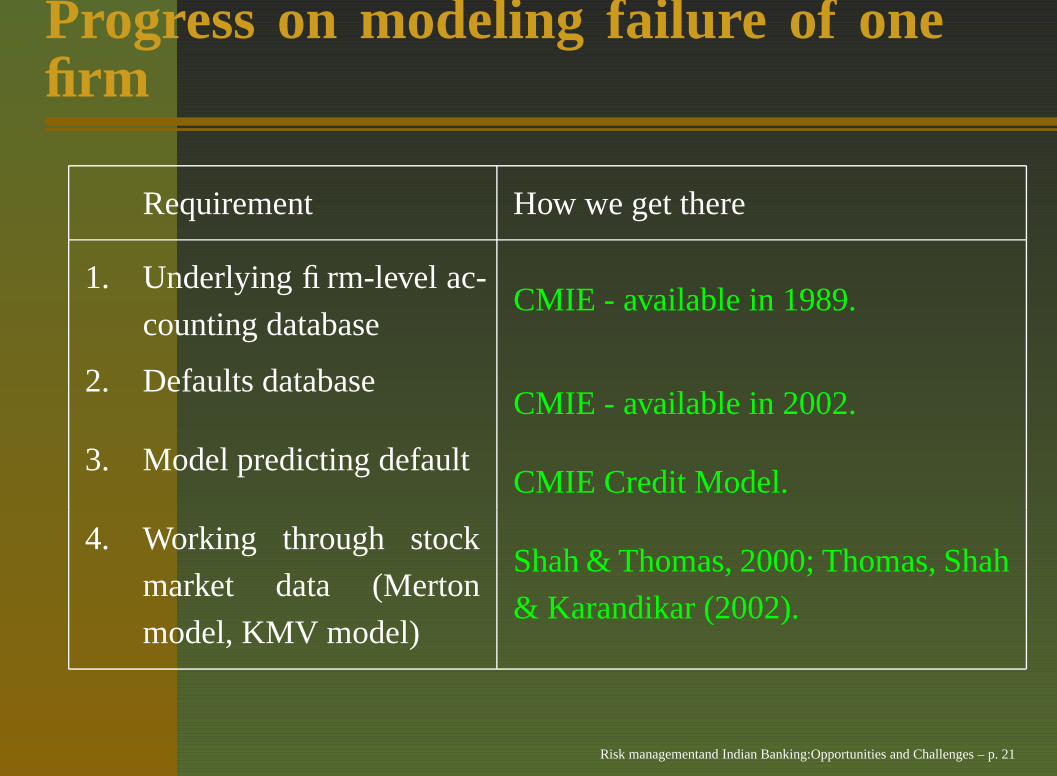

Progress on modeling failure of onefirm

Requirement

How we get there

1. Underlying firm-level ac-

counting database

CMIE - available in 1989.

2. Defaults database

CMIE - available in 2002.

3. Model predicting default

CMIE Credit Model.

4. Working through stock

market data (Merton

model, KMV model)

Shah & Thomas, 2000; Thomas, Shah

& Karandikar (2002).

Risk managementand Indian Banking:Opportunities and Challenges – p. 21

Progress on modeling failure of onefirm

Requirement How we get there

1. Underlying firm-level ac-

counting database

CMIE - available in 1989.

2. Defaults database

CMIE - available in 2002.

3. Model predicting default

CMIE Credit Model.

4. Working through stock

market data (Merton

model, KMV model)

Shah & Thomas, 2000; Thomas, Shah

& Karandikar (2002).

Risk managementand Indian Banking:Opportunities and Challenges – p. 21

Progress on modeling failure of onefirm

Requirement How we get there

1. Underlying firm-level ac-

counting databaseCMIE - available in 1989.

2. Defaults database

CMIE - available in 2002.

3. Model predicting default

CMIE Credit Model.

4. Working through stock

market data (Merton

model, KMV model)

Shah & Thomas, 2000; Thomas, Shah

& Karandikar (2002).

Risk managementand Indian Banking:Opportunities and Challenges – p. 21

Progress on modeling failure of onefirm

Requirement How we get there

1. Underlying firm-level ac-

counting databaseCMIE - available in 1989.

2. Defaults databaseCMIE - available in 2002.

3. Model predicting default

CMIE Credit Model.

4. Working through stock

market data (Merton

model, KMV model)

Shah & Thomas, 2000; Thomas, Shah

& Karandikar (2002).

Risk managementand Indian Banking:Opportunities and Challenges – p. 21

Progress on modeling failure of onefirm

Requirement How we get there

1. Underlying firm-level ac-

counting databaseCMIE - available in 1989.

2. Defaults databaseCMIE - available in 2002.

3. Model predicting defaultCMIE Credit Model.

4. Working through stock

market data (Merton

model, KMV model)

Shah & Thomas, 2000; Thomas, Shah

& Karandikar (2002).

Risk managementand Indian Banking:Opportunities and Challenges – p. 21

Progress on modeling failure of onefirm

Requirement How we get there

1. Underlying firm-level ac-

counting databaseCMIE - available in 1989.

2. Defaults databaseCMIE - available in 2002.

3. Model predicting defaultCMIE Credit Model.

4. Working through stock

market data (Merton

model, KMV model)

Shah & Thomas, 2000; Thomas, Shah

& Karandikar (2002).

Risk managementand Indian Banking:Opportunities and Challenges – p. 21

From the CMIE Credit Model:

0.0 0.2 0.4 0.6 0.8 1.0

0.0

0.2

0.4

0.6

0.8

1.0

CMIE Credit ModelMoodys Altman Z-Score 1Altman Z-Score 2Model with no prediction capabilityModel with perfect prediction capability

Risk managementand Indian Banking:Opportunities and Challenges – p. 22

From Thomas, Shah & Karandikar,2002:

-200 0 200

Number of days

1.0

1.5

2.0

Avg

. DfD

DowngradesUpgrades Reaffirmations

Risk managementand Indian Banking:Opportunities and Challenges – p. 23

Further reading

Risk managementand Indian Banking:Opportunities and Challenges – p. 24

VaR

SUSAN THOMAS and AJAY SHAH. “Risk and theIndian economy.” In: “India Development Report1999-2000,” (editor) KIRIT S. PARIKH, chapter 16,pages 231–242. Oxford University Press, 1999

AJAY SHAH and SUSAN THOMAS. “Rethinkingprudential regulation.” In: “India DevelopmentReport 1999-2000,” (editor) KIRIT S. PARIKH,chapter 17, pages 243–255. Oxford University Press,1999

MANDIRA SARMA, SUSAN THOMAS, and AJAYSHAH. “Selection of Value at Risk models.” Journalof Forecasting, 22(4):pages 337–358 (2003)

Risk managementand Indian Banking:Opportunities and Challenges – p. 25

Recent work on fixed income VaR

ILA PATNAIK and AJAY SHAH. “Interest-rate risk inthe Indian banking system.” Technical report,ICRIER, New Delhi (December 2002)

Jayanth Varma’s committee report on interest ratederivatives - came up on SEBI website on 19/3/2003.

Gangadhar Darbha has done work on extreme valuetheory for interest rate VaR.

Risk managementand Indian Banking:Opportunities and Challenges – p. 26

Credit risk

CMIE Prowess manuals.

SUBRATA SARKAR and SUSAN THOMAS.“Assessing default probabilities using accountingdata: a case of firms in india.” Technical report,IGIDR (2003)

AJAY SHAH and SUSAN THOMAS. “Systemicfragility in Indian banking: Harnessing informationfrom the equity market.” Technical report, IGIDR,Bombay, India (December 2000)

SUSAN THOMAS, AJAY SHAH, and RAJEEVA L.KARANDIKAR. “Does the stock market get it beforethe rating agencies? Some evidence on the Mertonmodel.” Technical report, IGIDR and ISI, Delhi(June 2002) Risk managementand Indian Banking:Opportunities and Challenges – p. 27