royal vopak roadshow presentation fy2011.ppt

TRANSCRIPT

Roadshow presentationAnnual Results 2011

Forward-looking statement

This presentation contains statements of a forward-looking nature, based on currently available plans

and forecasts. Given the dynamics of the markets and the environments of the 31 countries in which

Vopak provides logistics services, the company cannot guarantee the accuracy and completeness of

such statements.

Unforeseen circumstances include, but are not limited to, exceptional income and expense items,

unexpected economic, political and foreign exchange developments, and possible changes to IFRS

reporting rules.

Statements of a forward-looking nature issued by the company must always be assessed in the

context of the events, risks and uncertainties of the markets and environments in which Vopak

operates. These factors could lead to actual results being materially different from those expected.

Roadshow presentation FY 2011 2

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 3

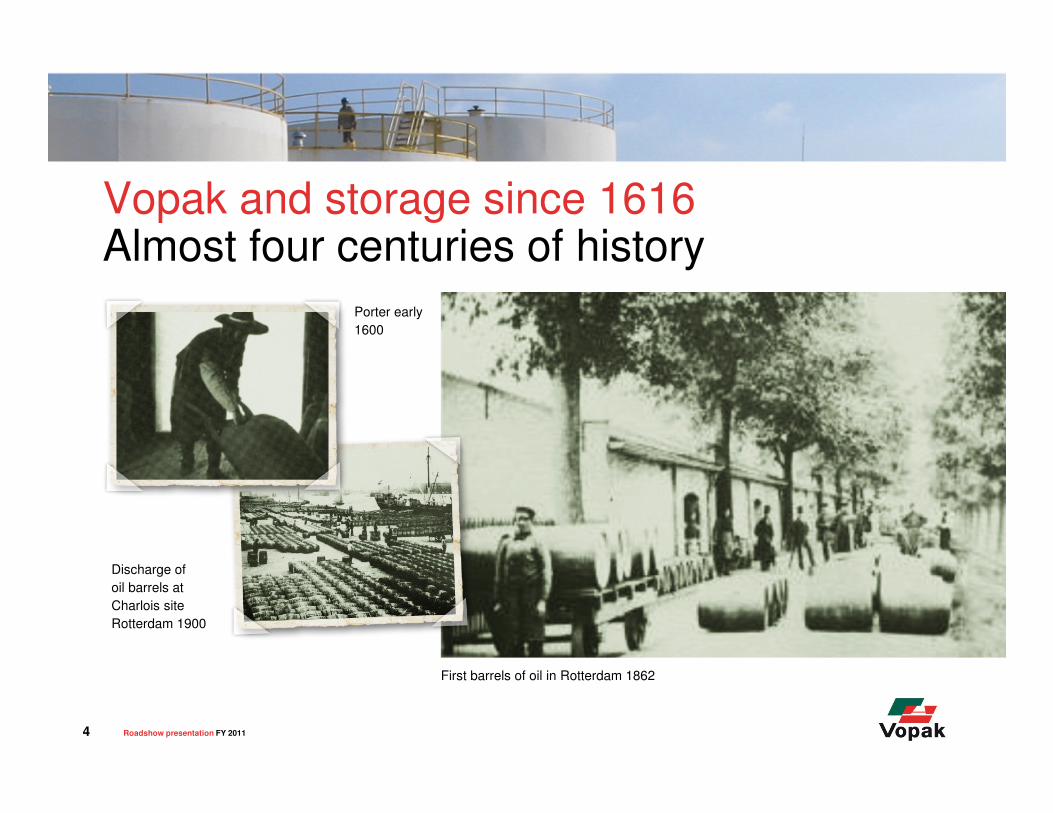

Vopak and storage since 1616Almost four centuries of history

Discharge of

oil barrels at

Charlois site

Rotterdam 1900

Porter early

1600

First barrels of oil in Rotterdam 1862

Roadshow presentation FY 2011 4

84 Terminals in 31 countries

And a number of terminals under construction.

Roadshow presentation FY 2011 5

Key figures and some of our customers

Employees

Terminals

Countries

Capacity

Net Revenues ‘11

EBIT* ‘11

Market capitalization**

5,901 (incl. JVs)

84

31

27.9 Million cbm

€ 1,172 Million

€ 469 Million

€ 5.2 Billion

Roadshow presentation FY 2011

* Excluding exceptional items.** At year-end 2011.

6

Tank terminalKey role in oil and chemical supply chain

Customers

Oil, Gas and

Chemicals companies

Governments

Trading companies

Services

Storage

Blending

Break bulk

Make bulk

Drumming

Heating / cooling

Weighing

Products

Oil (derivatives)

Chemicals

Vegetable oils

Biofuels

Supply and transport

Vessels

Barges

Pipelines

Tank trucks

Rail wagons

Drums

LNG

LPG

Chemical

gases

Roadshow presentation FY 2011 7

Vopak’s role in the supply chain

Feedstock Production

FeedstockGathering

Production &Refining

ProductsTransmission

Independent Storage &Transshipment

Mid-Stream& End-userDistribution

Oil, Gas and Chemical supply chain

Roadshow presentation FY 2011 8

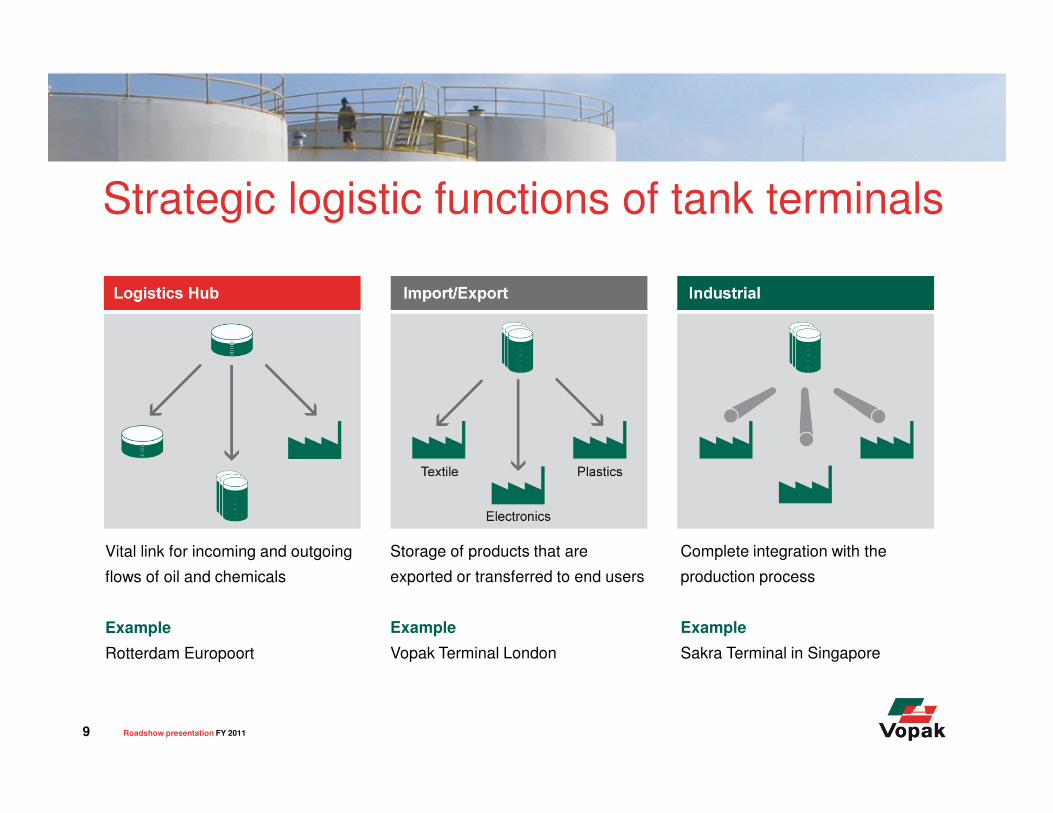

Strategic logistic functions of tank terminals

Vital link for incoming and outgoing

flows of oil and chemicals

Example

Rotterdam Europoort

Storage of products that are

exported or transferred to end users

Example

Vopak Terminal London

Complete integration with the

production process

Example

Sakra Terminal in Singapore

Roadshow presentation FY 2011 9

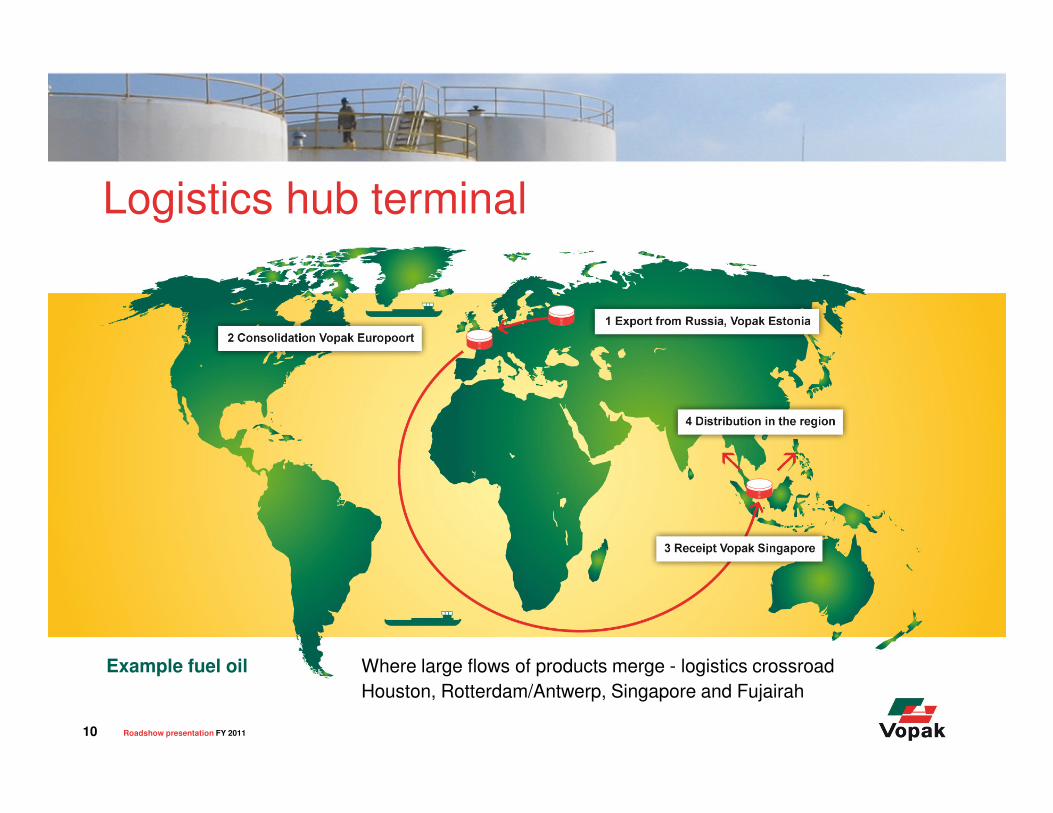

Logistics hub terminal

Example fuel oil Where large flows of products merge - logistics crossroad

Houston, Rotterdam/Antwerp, Singapore and Fujairah

Roadshow presentation FY 2011 10

Import/Export terminal

� Break or make bulk

� Local distribution

Roadshow presentation FY 2011 11

Industrial terminalStorage facilities integrated at chemical park

Vopak Terminals Singapore - Sakra Terminal

Exxon Mobil

Perstorp

Sumitomo Chemical

Mitsui Chemicals

Air Products

Chevron

Asahi Kasei Chemicals

SembCorp Utilities

Celanese

Kuraray

Dupont

Roadshow presentation FY 2011 12

Global mega trends drive Vopak’s markets

� GDP growth in

non-OECD� Increasing need

transport and

mobility

� Increasing

(sustainable)

energy need

� Population

growth, mainly

non-OECD

Roadshow presentation FY 2011 13

Non-OECD economies drive energy consumption growth,fossil fuels will remain the dominant energy provider until 2035

OECD China Rest of world

World primary energy demand by region in IEA New Policies ScenarioIn Mtoe

Source: IEA WEO 2010

World primary energy demand by fuel in IEA New Policies ScenarioIn Mtoe

Roadshow presentation FY 2011 14

Strengthening Vopak’s competitive position in a period of worldwide challenges

� Socio-economic unrests

(e.g. ‘Arab-spring’) � Geopolitical challenges� Financial turmoil and

economic uncertainties

Roadshow presentation FY 2011 15

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 16

Robust results in 2011

2011

93.0

2010

93.0

2009

94.0

2008

95.0

2007

96.0

2006

94.0

Occupancy rate

In percent

90-95%-1.0

2011

27.8

2010

28.8

2009

28.3

2008

27.1

2007

21.8

2006

21.2

Storage capacity

In mln cbm

+6%

2011

636.0

2010

598.2

2009

513.4

2008

429.3

2007

369.5

2006

314.1

EBITDA Development*

In mln EUR

* Excluding exceptional items; including net result from Joint VenturesRoadshow presentation FY 2011 17

Personal and process safety

-15%

2011

1.1

2010

1.3

2009

1.4

2008

1.7

2007

1.4

2006

1.9

The lost time injury rate (LTIR) Total injuries leading to lost time per million hours worked

by own employees and contractors

-6%

2011

3.0

2010

3.2

2009

6.5

2008

5.8

2007

6.2

2006

7.1

Process Incidents

# incidents

Total Injury RateTotal injuries per million hours worked by own employees

+16%

2011

154.0

2010

133.0

2009

141.0

Roadshow presentation FY 2011 18

Focused strategy to execute

Customer LeadershipOperational Excellence

Our Foundation

• Safety, Health and Environment

• Our People

Our ability to construct,

operate and maintain

our terminals to

deliver our service at

competitive costs

Our ability to create

a relationship

with our customers

Our ability to find or

identify the right location

for our terminals

Growth LeadershipA B C

Roadshow presentation FY 2011 19

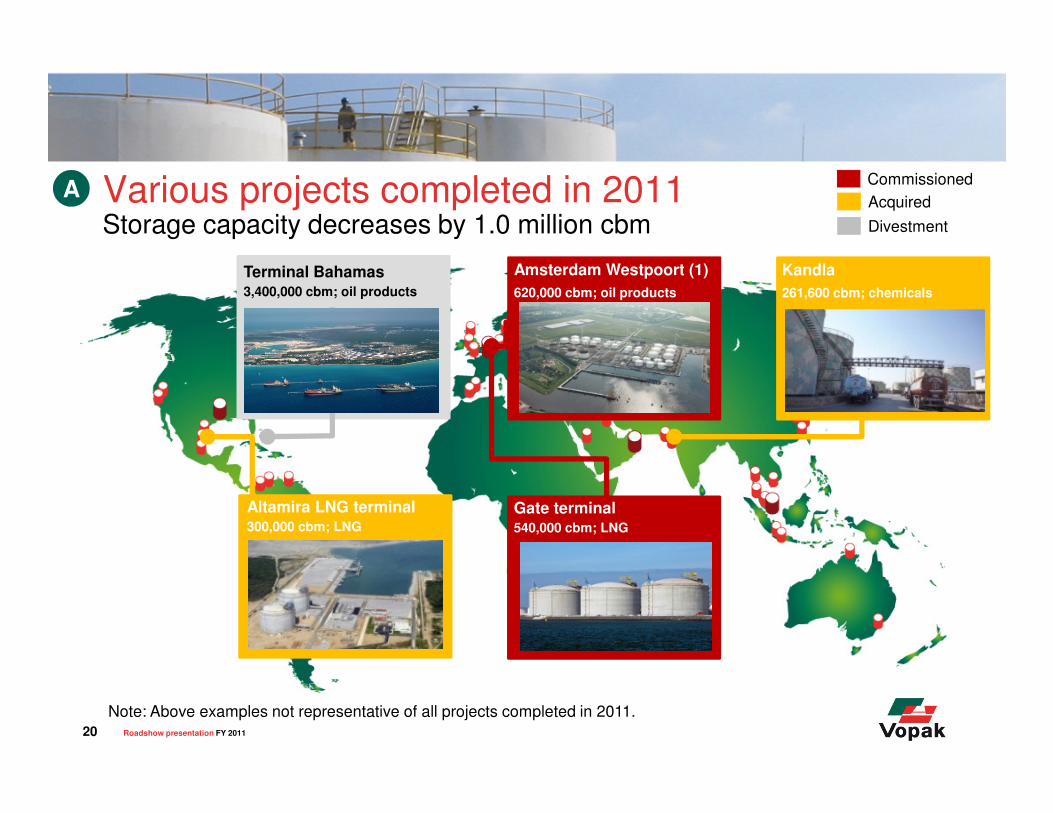

Various projects completed in 2011Storage capacity decreases by 1.0 million cbm

ACommissioned

Acquired

Divestment

Amsterdam Westpoort (1)

620,000 cbm; oil products

Kandla

261,600 cbm; chemicals

Altamira

Altamira LNG terminal 300,000 cbm; LNG

Terminal Bahamas 3,400,000 cbm; oil products

Gate terminal 540,000 cbm; LNG

Note: Above examples not representative of all projects completed in 2011.Roadshow presentation FY 2011 20

Strengthening competitive position: improve safety performance and efficiency

� Operational efficiency improvements

� Focus on master plans

EfficiencySafety

� Improving safety performance

� Reinforce our Vopak Fundamentals

on Safety

B

Roadshow presentation FY 2011 21

Serving markets from a product perspective C

� Customer segmentation

� Access to the right people

� Understand customer’s strategy

Account Management

� Port Attractiveness

� Relevance for Network

� Pro-active approach

Portfolio of Terminals

� Understand basic technology

� Understand imbalances

� Understand trade flow dynamics

Product strategy

Winning

clients and

ports

Roadshow presentation FY 2011 22

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 23

Global energy product trends drive Vopak’s market

Oil products Chemical products Biofuels & Vegoils LNG

�Global Crude oil

trade business

�Europe’s gasoline

surplus

�Europe’s deficit for

middle distillates

�Asia’s deficit for

Fuel Oil

�Feedstock

advantage in ME

�Renewed Gulf

re-emerges due to

shale gas

�Rationalization in

Europe

�Politics, annual

harvest and

demand growth will

lead to increased

flows between US-

Brazil-Europe-Asia

�A globalizing

natural gas market

with new business

models

�LNG growth due to

imbalances,

security of supply

and environmental

push

Roadshow presentation FY 2011 24

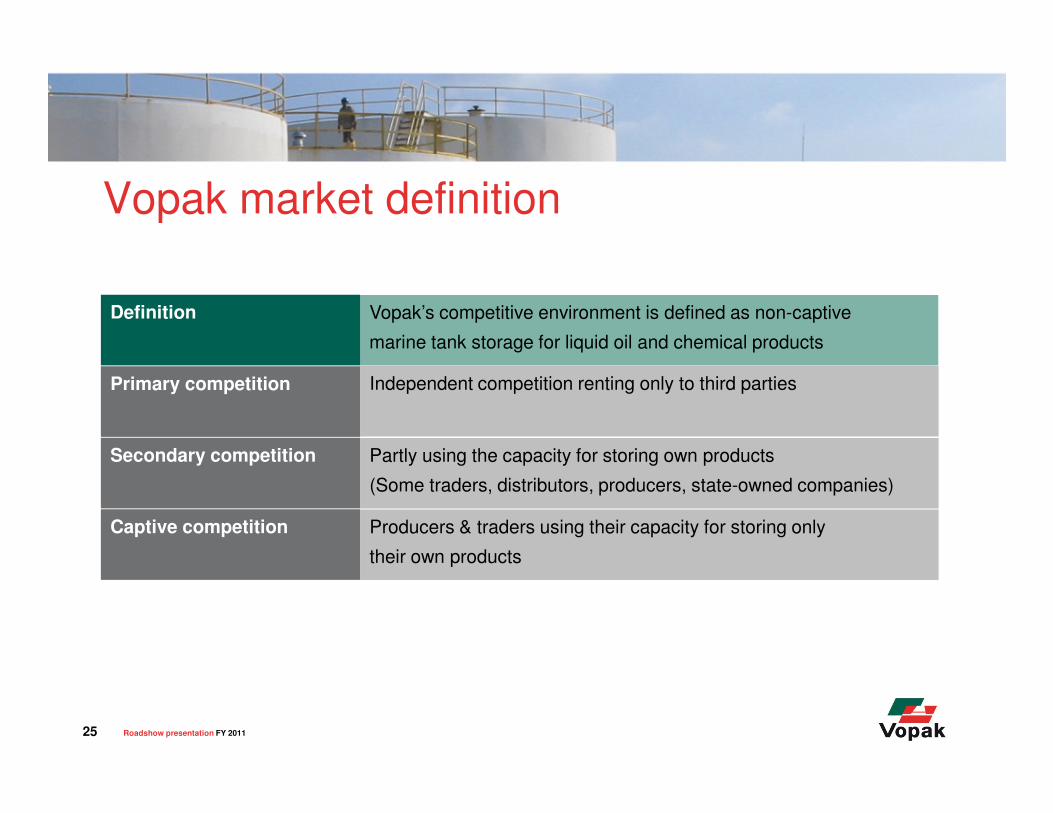

Vopak market definition

Vopak’s competitive environment is defined as non-captive

marine tank storage for liquid oil and chemical products

Definition

Primary competition Independent competition renting only to third parties

Secondary competition Partly using the capacity for storing own products

(Some traders, distributors, producers, state-owned companies)

Captive competition Producers & traders using their capacity for storing only

their own products

Roadshow presentation FY 2011 25

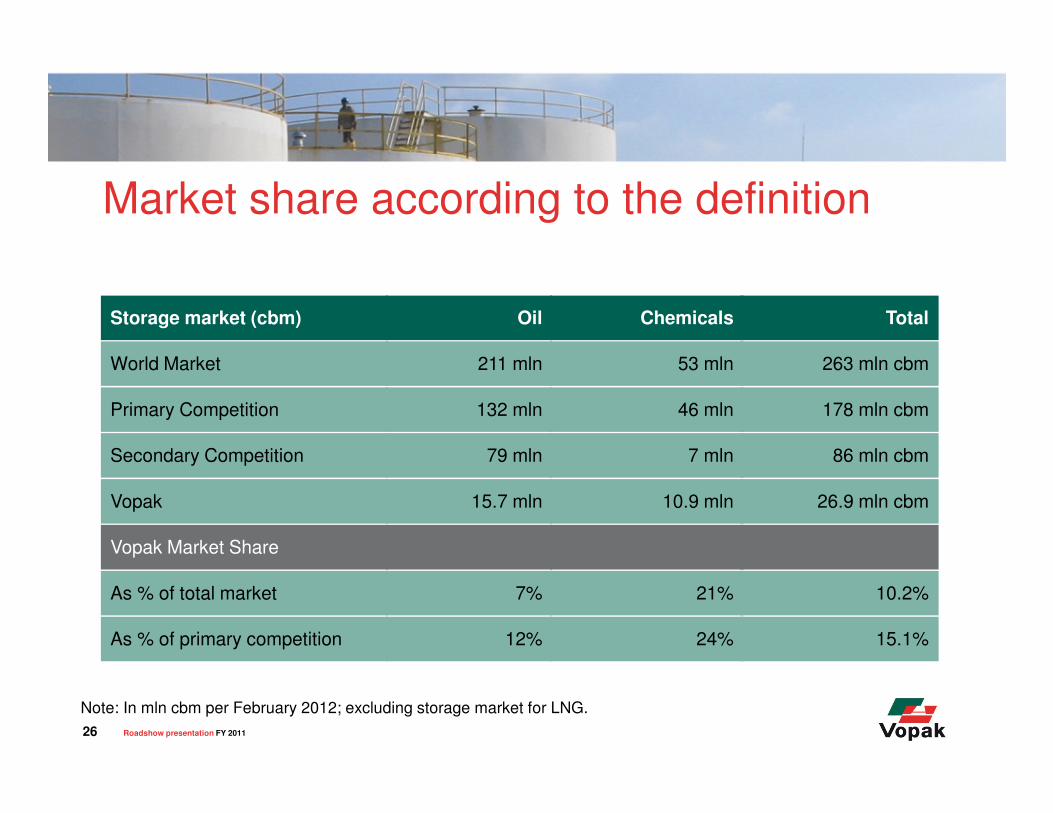

Market share according to the definition

Storage market (cbm) Oil Chemicals Total

World Market 211 mln 53 mln 263 mln cbm

Primary Competition 132 mln 46 mln 178 mln cbm

Secondary Competition 79 mln 7 mln 86 mln cbm

Vopak Market Share

As % of total market 7% 21% 10.2%

As % of primary competition 12% 24% 15.1%

Vopak 15.7 mln 10.9 mln 26.9 mln cbm

Note: In mln cbm per February 2012; excluding storage market for LNG.

Roadshow presentation FY 2011 26

Demand growth in storage marketto support international trade flows

Additional Worldwide Storage Capacity Total

World Market, incl. Vopak 28.2 mln cbm

Growth % 10.7 %

Vopak 6.0 mln cbm

Growth as % of Vopak capacity 21.6 %*

Roadshow presentation FY 2011

* Based on current storage capacity of 27.8 million cbm.

27

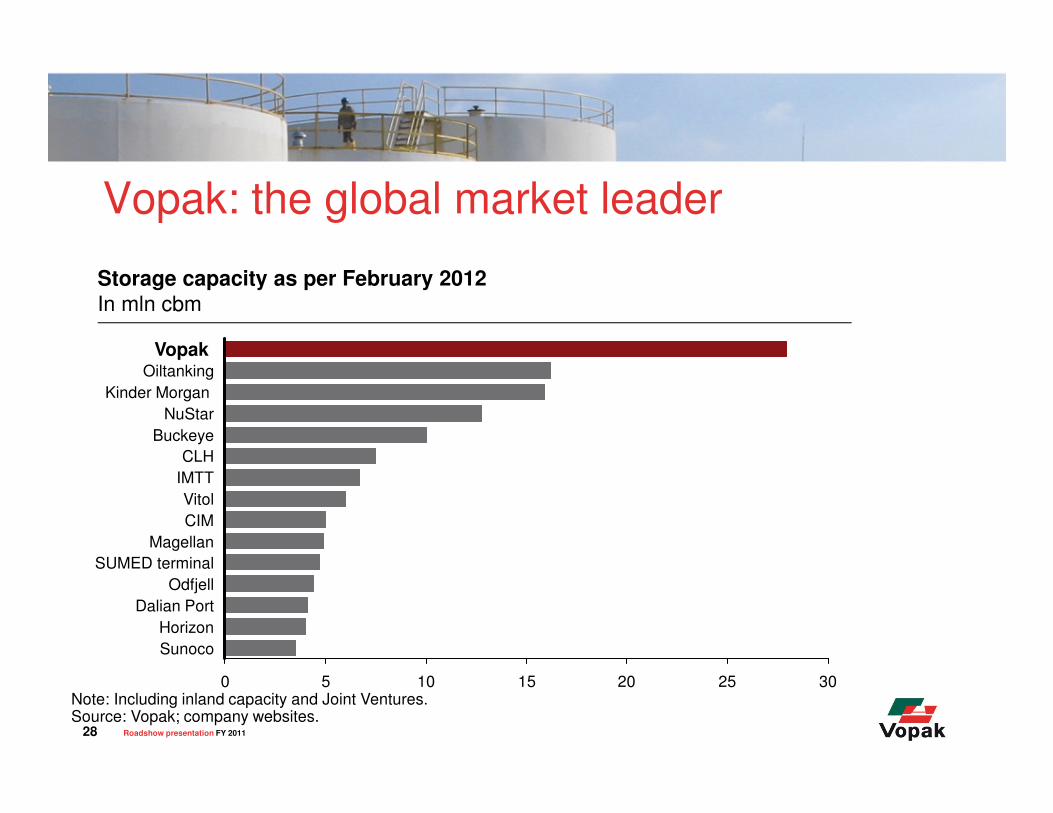

Vopak: the global market leader

0 5 10 15 20 25 30

Vitol

CLH

IMTT

Buckeye

Magellan

SUMED terminal

Odfjell

Dalian Port

Horizon

Sunoco

CIM

VopakOiltanking

Kinder Morgan

NuStar

Storage capacity as per February 2012

In mln cbm

Note: Including inland capacity and Joint Ventures.Source: Vopak; company websites.

Roadshow presentation FY 2011 28

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 29

Capacity developments 2010-2014

In mln cbm

Global products trends resulting in company growth through healthy demand for storage capacity

2011

93.0

2010

93.0

2009

94.0

2008

95.0

2007

96.0

2006

94.0

Occupancy rate

In percent

90-95%

+6.0

-1.0

31-12-2014

33.8

New terminals

4.2

Expansions

1.8

31-12-2011

27.8

New terminals

1.7

Expansions

0.8

Divest-ments

3.5

31-12-2010

28.8

Roadshow presentation FY 2011 30

Various projects under constructionTotal storage capacity under construction 6.0 million cbm

Under construction

Amsterdam Westpoort (2)

570,000 cbm; oil products

Pengerang

1,278,000 cbm; oil products

Fujairah

606,000 cbm; oil products

Europoort

400,000 cbm; oil products

Eemshaven

660,000 cbm; oil products

Hainan

1,350,000 cbm; oil products

Algeciras

403,000 cbm; oil products

Note: Above examples not representative of all projects under construction.Roadshow presentation FY 2011 31

Storage capacity under construction (1)

Location Ownership Product cbm 2010 2011 2012 2013 2014

Netherlands,

Westpoort (2)100% O 570,000

Mexico, Altamira 100% C 15,800

China, Tianjin (2) 50% LPG 240,000

China,

Zhangjiagang100% C 55,600

Thailand,

Map Ta Phut49% C 15,000

Belgium, Antwerp 100% C 7,500

UAE, Fujairah 33.3% O 606,000

China, Coajing 50% C 16,000

Netherlands,

Eemshaven50% O 660,000

Roadshow presentation FY 2011 32

Storage capacity under construction (2)Location Ownership Product cbm 2010 2011 2012 2013 2014

Spain, Algeciras 80% O 403,000

Netherlands,

Rotterdam100% C 20,000

China,

Dongguan50% C 153,000

Singapore,

Banyan69.5% C 100,200

China, Hainan 49% O 1,350,000

Malaysia,

Pengerang44% O 1,278,000

Netherlands,

Europoort100% O 400,000

Total additional storage capacity (in million cbm) 2.1 2.2 1.7

Accumulated storage capacity (in million cbm) 27.8 29.9 32.1 33.8

Roadshow presentation FY 2011 33

Various projects under study Under study

Fos-sur-Mer

LNG

West-Java

LPG

Bioko Island

Oil products

Bahia Las Minas

Oil products

Perth Amboy

Oil products

Roadshow presentation FY 2011 34

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 35

Contribution of Vopak value drivers in the past and present

Occupancy improvements

2003-06 2007-09 2010-2011 2012 >

Operational efficiency gains

Capacity expansion

PresentPresentPast Future

Playing field between 90 - 95%

Roadshow presentation FY 2011 36

Focused strategy delivers results

EBITDA Development 2006-2011*

In mln EUR

* Excluding exceptional items; including net result from Joint Ventures

+102%

2011

636.0

EBITDA

improvements

FX resultDivestments2006

314.1

� Healthy occupancy rate

� Improved revenue per cubic

meter

� Effective cost management

� Storage capacity growth

Roadshow presentation FY 2011 37

Contract duration portfolio did not change significantly since 2008

Contract position 2008

In percent of revenues

Contract position 2011

In percent of revenues

> 3 year 44%

1-3 year

37%

< 1 year

19%

> 3 year39%

1-3 year

41%

< 1 year

20%

Roadshow presentation FY 2011 38

Transition year 2011 in line with outlook

EBIT*

In million EUR1,171.9

+6%

20112010

1,106.3

Revenues

In million EUR

* Including net result from Joint Ventures.Note: Excluding exceptional items.

469.4

+5%

20112010

445.3

Earnings per share*

In EUR275.4

+4%

20112010

264.8

Net profit*

In million EUR2.16

+4%

20112010

2.08

Roadshow presentation FY 2011 39

+6.0

-1.0+7.6

2014

33.8

21.2

12.6

2013

32.1

11.3

2011

27.8

19.6

8.2

20.8

2010

28.8

18.3

10.5

2009

28.3

18.1

10.2

2008

27.1

17.5

9.6

2007

21.8

16.7

5.1

2006

21.2

15.8

5.4

2012

29.9

9.6

20.3

Storage capacityIn mln cbm

Revenue developments supported by robust demand for storage capacity

Subsidiaries

Joint ventures

Roadshow presentation FY 2011 40

Healthy occupancy rates between 90-95%

95

Q4

2008

95

Q3

2008

94

Q2

2008

95

Q1

2008

96

Q4

2011

94

Q3

2011

93

Q2

2011

93

Q1

2011

92

Q4

2010

92

Q3

2010

92

Q2

2010

93

Q1

2010

93

Q4

2009

93

Q3

2009

93

Q2

2009

95

Q1

2009

Occupancy rate

In percent

90-95%

Roadshow presentation FY 2011 41

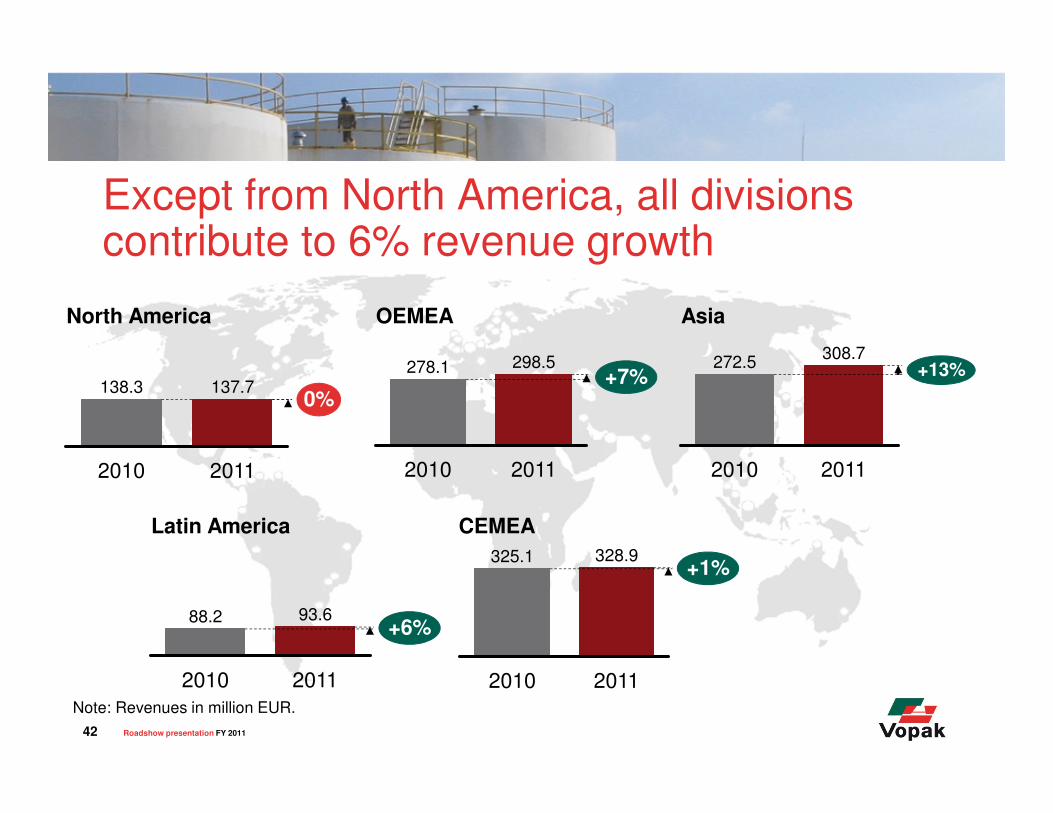

Except from North America, all divisions contribute to 6% revenue growth

137.70%

20112010

138.3

North America

Note: Revenues in million EUR.

298.5+7%

20112010

278.1

OEMEA

308.7+13%

20112010

272.5

Asia

93.6+6%

20112010

88.2

Latin America

328.9+1%

20112010

325.1

CEMEA

Roadshow presentation FY 2011 42

EBIT excluding exceptional items increased by 5% to EUR 469.4 million

445.3EBIT excl. exceptional items

442.0

Operating profit

Net result Joint Ventures

(3.3)

358.6

83.4

Exceptional gain (loss)

EBIT incl. exceptional items

220.4

585.5

365.1

469.4

116.1

2010

In mln EUR

2011

In mln EUR

Delta

In percent

2%

164%

32%

5%

Net profit 264.8 275.4 4%

Roadshow presentation FY 2011 43

63% of EBIT generated in non-euro currencies

Total 2.6

Non allocated 0.1

Latin America 0.7

North America 1.6

Asia 5.4

CEMEA 0.4

OEMEA 0.2

FX translation-effect on EBITIn mln EUR

EBIT transactional currenciesIn percent

Other

24%

EUR37%

SGD28%

USD

11%

� Transactional currency exchange risks are

limited

� As a rule revenues, costs and financing are

denominated in the same currency

Note: Excluding exceptional items.Roadshow presentation FY 2011 44

5% EBIT increase mainly driven by Asia, Global LNG, OEMEA, and Latin America

33.8 -27%

20112010

46.0

North America

Note: EBIT in million EUR; Excluding exceptional items; including net result from Joint Ventures

161.4+3%

20112010

156.4

OEMEA

185.3+12%

20112010

165.7

Asia

28.2+10%

20112010

25.7

Latin America

87.8-3%

20112010

90.6

CEMEA Global LNG

2011

4.4

2010

-5.9

Roadshow presentation FY 2011 45

1.2 -86%*

20112010

8.6

48.1+4%

20112010

46.129.6

0%

20112010

29.7

0.8

20112010

1.1-27%

2.1

2011

+40%

2010

1.5

2011

9.9

2010

-2,0

Net result from Joint Ventures increases with 8%

North America OEMEA Asia

Latin America CEMEA Global LNG

* Due to the sale of Vopak’s 20% equity stake in BORCO (Bahamas).Note: Results JVs in million EUR; Excluding exceptional items.

Roadshow presentation FY 2011 46

Revenues Incl. proportionate consolidation JVs tank storage

1,171.9

+6%

20112010

1,106.3

Revenues

Subsidiaries (Equity method)1,452.0

+6%

20112010

1,365.3

EBITDAIncl. proportionate consolidation JVs tank storage

EBITDA

Subsidiaries* (Equity method)

IFRS equity accounting versus proportionate consolidation

* Including net result from Joint Ventures.Note: In million EUR; Excluding exceptional items.

636.0+6%

20112010

598.2701.4

+5%

20112010

665.2

Roadshow presentation FY 2011 47

Former situation

CE

ME

A

Th

e N

eth

erl

an

ds

OE

ME

ACurrent situation

� The former divisions Vopak Chemicals

EMEA and Vopak Oil EMEA

� The current divisions Vopak Netherlands

and Vopak EMEA as of 1 January 2012

Further optimizing the organization structure

EM

EA

Roadshow presentation FY 2011 48

‘Pro forma’ results new division structure Netherlands and EMEA

400.8+4%

20112010

386.4

Revenues Netherlands

* Including net result from Joint Ventures.Note: In million EUR; Excluding exceptional items.

156.3-1%

20112010

157.2

EBIT Netherlands*

1.5-35%

20112010

2.3

Results JVs Netherlands

226.6+5%

20112010

216.8

Revenues EMEA

92.9+3%

20112010

89.8

EBIT EMEA* Results JVs EMEA

2011

48.7+8%

2010

45.3

Roadshow presentation FY 2011 49

Vopak is well positioned to maintain healthy EBIT(DA) margins

EBIT(DA) Margin*In percent

0

10

20

30

40

50

2004 2005 2006 2007 2008 2009 2010 2011

Focus on logistic efficiency improvements for our clients

has led to increased EBIT(DA) margins

* Excluding exceptional items; excluding Net result from Joint Ventures.

EBIT Margin

EBITDA Margin

Roadshow presentation FY 2011 50

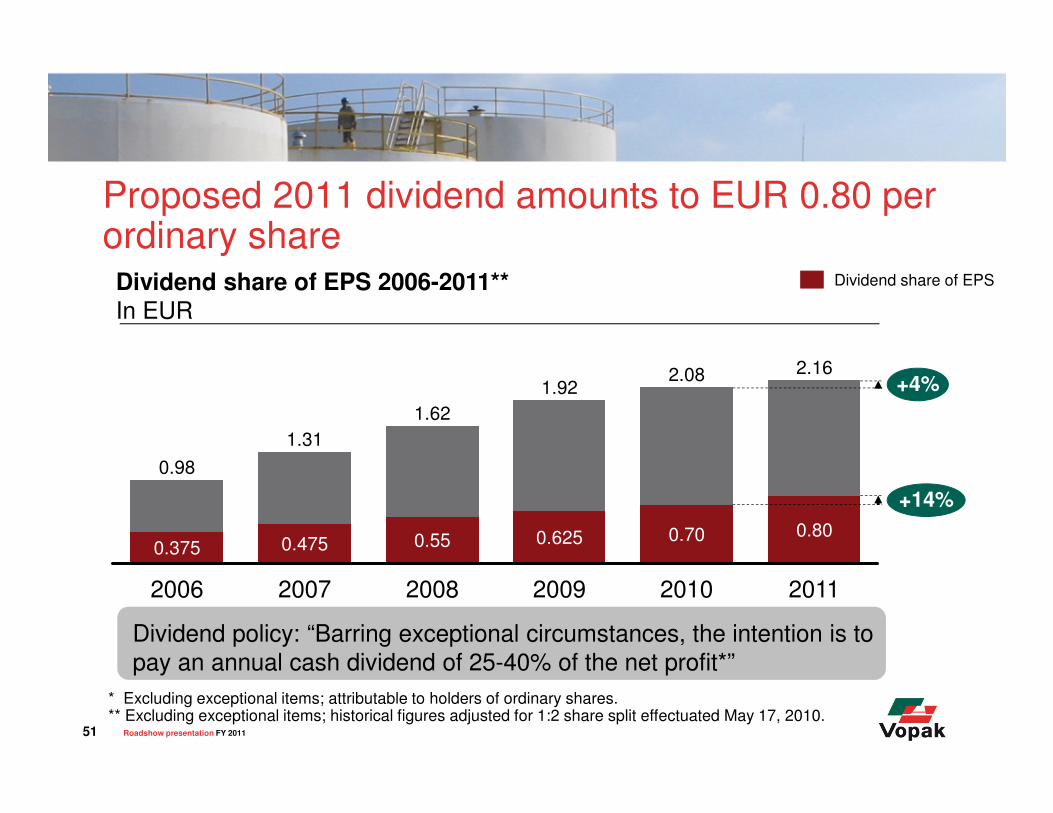

Proposed 2011 dividend amounts to EUR 0.80 per ordinary share

+4%

1.62

0.55

2.16

2007

+14%

2011

1.31

0.80

2010

0.475

2.08

0.70

2006 2009

1.92

0.98

0.625

2008

0.375

Dividend share of EPS 2006-2011**In EUR

* Excluding exceptional items; attributable to holders of ordinary shares.** Excluding exceptional items; historical figures adjusted for 1:2 share split effectuated May 17, 2010.

Dividend share of EPS

Dividend policy: “Barring exceptional circumstances, the intention is to

pay an annual cash dividend of 25-40% of the net profit*”

Roadshow presentation FY 2011 51

Various other topics

“Net Finance costs aligned with expansion program.”

“Effective tax rate 2011.”

“Accounting consequences:

IAS 19 Employee Benefits

effective for 2013.”

“Sources and uses of cash in

2011.”

II

I

III

III

V

“Vopak’s Pensions.”

See appendix for further details

Roadshow presentation FY 2011 52

Quarterly EBIT development“Solid year-on-year growth”

EBIT development per Quarter*

In mln EUR

108.4113.398.6

Q1

109.5

+21%+6%

-4%0%

Q4

130.0

107.596.9

Q3

121.3114.8

104.2

Q2

109.7

85.6

EBIT 2011

EBIT 2010

EBIT 2009

* Excluding exceptional items.

Roadshow presentation FY 2011 53

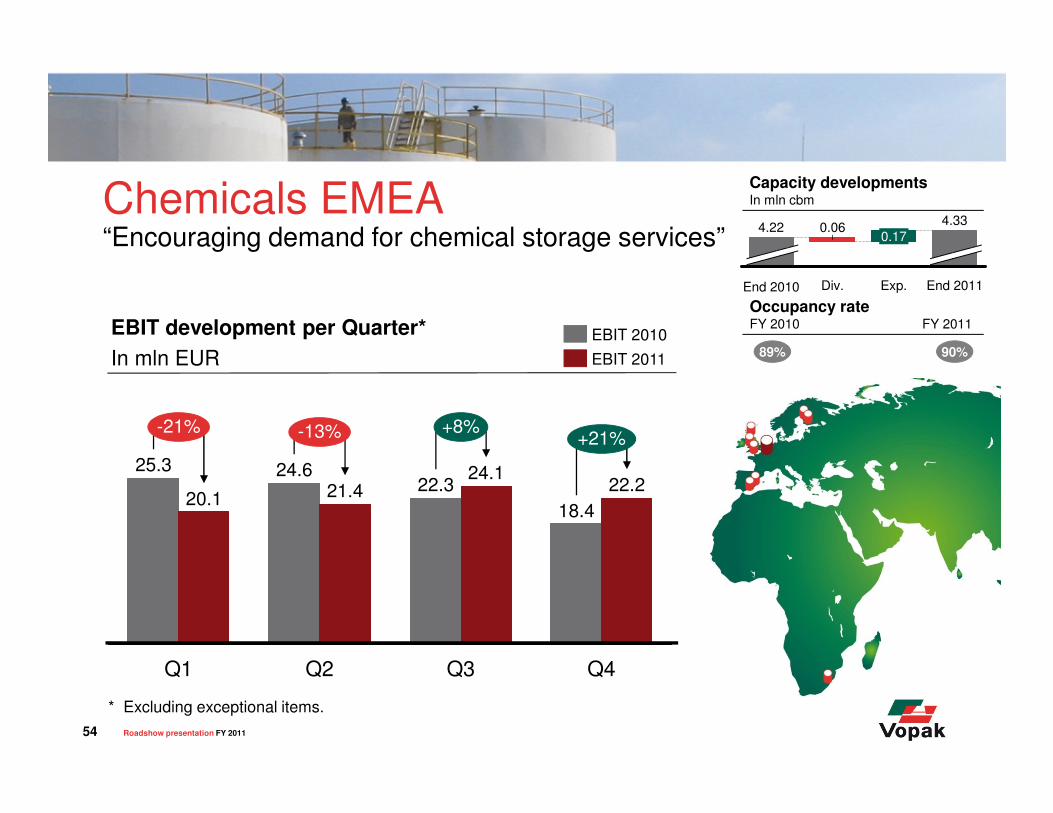

Chemicals EMEA“Encouraging demand for chemical storage services”

EBIT development per Quarter*

In mln EUR

20.1

25.3

+8%

22.222.3

Q1

+21%-13%-21%

Q4

18.4

Q3

24.1

Q2

21.424.6

EBIT 2011

EBIT 2010

* Excluding exceptional items.

Capacity developmentsIn mln cbm

End 2011

4.33

Exp.End 2010

0.174.22

Div.

0.06

89% 90%

Occupancy rate FY 2010 FY 2011

Roadshow presentation FY 2011 54

Oil EMEA“Robust market conditions in the storage and handling of oil products”

EBIT development per Quarter*

In mln EUR

+27%

-1%-8%-5%

Q4

47.3

37.1

Q3

41.742.0

Q2

36.639.7

Q1

35.837.6

EBIT 2011

EBIT 2010

* Excluding exceptional items.

Capacity developmentsIn mln cbm

End 2011

12.28

Exp.

1.16

Div.

0.00

End 2010

11.12

95% 94%

Occupancy rate FY 2010 FY 2011

Roadshow presentation FY 2011 55

Asia“Continuous growth in Asia”

EBIT development per Quarter*

In mln EUR

+1%+5%+15%+29%

Q4

46.746.2

Q3

45.042.7

Q2

46.2

40.1

Q1

47.4

36.7

EBIT 2011

EBIT 2010

* Excluding exceptional items.

Capacity developmentsIn mln cbm

End 2011

7.09

Exp.

0.31

Div.

0.00

End 2010

6.78

92% 94%

Occupancy rate FY 2010 FY 2011

Roadshow presentation FY 2011 56

North America“Encouraging finish in a transition year”

EBIT development per Quarter*

In mln EUR

-26%

Q4

8.910.6

Q3

8.010.1

Q2

7.1

12.0

Q1

9.8

13.3-16%-21%

-41%

EBIT 2011

EBIT 2010

* Excluding exceptional items.

Capacity developmentsIn mln cbm

End 2011

2.32

Exp.

0.00

Div.

3.41

End 2010

5.73

94% 93%

Occupancy rate FY 2010 FY 2011

Roadshow presentation FY 2011 57

Latin America“Healthy demand for chemicals and palm oil”

EBIT development per Quarter*

In mln EUR

+60%+6%-10%0%

Q4

7.5

4.7

Q3

7.06.6

Q2

6.47.1

Q1

7.37.3

EBIT 2011

EBIT 2010

* Excluding exceptional items.

Capacity developmentsIn mln cbm

End 2011

0.99

Exp.

0.02

Div.

0.00

End 2010

0.97

90% 89%

Occupancy rate FY 2010 FY 2011

Roadshow presentation FY 2011 58

Results in HY2 2011 fuelled by expansions

610.8

+9%

HY2 2011HY2 2010

562.4

251.5

222.3 +13%

HY2 2011HY2 2010

HY2 2010

151.9

HY2 2011

+15%132.4 +14%

HY2 2011HY2 2010

1.041.19

* Including net result from Joint Ventures.Note: Excluding exceptional items.

EBIT*

In million EUR

Revenues

In million EUR

Earnings per share*

In EUR

Net profit*

In million EUR

Roadshow presentation FY 2011 59

Total investments

565535

800

446

268

711

201120102009200820072006

Total investments 2006-2011

In mln EUR

Total expansion CAPEX Group companies and JVs

In mln EUR

~1400

~500

Average yearly Sustaining Capex ~EUR150-200 mln

Total Capex(6.0 mln cbm under construction)

~1,900

Other Capex* ~1,400

Remaining Vopak share in Capex(Group Capex / equity share in JVs)

~500

* Group Capex spend; contributed Vopak equity share in JVs; total partners’ equity share in JVs; total non recourse financing in JVs.

Roadshow presentation FY 2011 60

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 61

Strategic finance

0

1

2

3

4

5

2.63

2009

2.23

2008

2.54

2007

1.71

2006

1.61

2005

1.76

2004

2.20

2003*

2.42

3.75

2010

2.65

2011

Net senior debt : EBITDA ratio

* Based on Dutch GAAP.

Maximum Ratio under current US PP program

Maximum Ratio under other PP programs and syndicated revolving credit facility

Roadshow presentation FY 2011 62

Various other financing topics

“Debt funding program further strengthened during 2011.” “Maturity of debt

funding further enhanced.”

“Balanced debt

repayment schedule.”

VII

VI

VIII

See appendix for

further details

Roadshow presentation FY 2011 63

Contents

General Introduction

Achievements 2011

Business environment

Growth projects

Business performance

Financing

Outlook

Roadshow presentation FY 2011 64

Contribution of Vopak value drivers in the future

Occupancy improvements

2003-06 2007-09 2010-2011 2012 >

Operational efficiency gains

Capacity expansion

PresentPresentPast Future

Playing field between 90 - 95%

Roadshow presentation FY 2011 65

Solid

Outlook assumptions

Oil products Chemicals Biofuels & Vegoils LNG

Robust

~60%

Encouraging Solid

<1%

Mixed

~17.5-20%

Industrial terminals

~12.5% ~7.5-10%

2011

~60-65% ~2.5-5%~17.5-20% ~7.5-10% ~5-7.5%

2013

Note: width of the boxes do not represent actual percentages.

~x% Share of EBIT

Roadshow presentation FY 2011 66

Vopak expects to realize an EBITDA of between EUR 725-800 million in 2013

262.5

2004

231.8

2013

725-800

2011

636.0

2010

598.2

2009

513.4

2008

429.3

2007

369.5

2006

314.1

2005

EBITDA Development and guidanceIn EUR mln

Note: Excluding exceptional items; including Net result from Joint Ventures

Historical results

Guidance/Outlook

� Long-term

guidance

ROCE

average 16%

Roadshow presentation FY 2011 67

Note: Excluding exceptional items; including net result from Joint Ventures

Vopak expects to realize an EBITDA of between EUR 725-800 million in 2013

6% EBITDA growth

5% EBIT growth

4% EPS growth

Proposal cash dividend of EUR 0.80 per share (+14%)

Adequate funding of growth strategy secured

Roadshow presentation FY 2011 68

Forward-looking statement

This document contains statements of a forward-looking nature, based on currently available plans

and forecasts. Given the dynamics of the markets and the environments of the 31 countries in which

Vopak renders logistics services, the company cannot guarantee the accuracy and completeness of

forward-looking statements.

Unforeseen circumstances include, but are not limited to, exceptional income and expense items,

unexpected economic, political and foreign exchange developments, and possible changes to IFRS

reporting rules.

Statements of a forward-looking nature issued by the company must always be assessed in the

context of the events, risks and uncertainties of the markets and environments in which Vopak

operates. These factors could lead to actual results being materially different from those expected.

Roadshow presentation FY 2011 69

Royal Vopak

Westerlaan 10 Tel: +31 10 4002911

3016 CK Rotterdam Fax: +31 10 4139829

The Netherlands www.vopak.com

Net Finance costs aligned with expansion program

Net finance costs -68.4

Finance costs 73.0

Interest and

dividend income 4.6

Net finance costs 2010

In mln EUR

-78.6

85.9

7.3

2006

7.0

2011

4.7

2010

5.2

2009

5.4

2008

5.4

2007

6.3

Average interest rate

In percent

1,017.7

2008

996.7

2007

561.9

2006

425.7

2011

1,605.6

2010

1,431.4

2009

Net interest bearing debt

In mln EUR

Net finance costs 2011*

In mln EUR

* The increase is mainly attributable to the exceptional loss of EUR 5.0 million related to the sale of Vopak’s 20% equity stake in BORCO (Bahamas).

I

Roadshow presentation FY 2011 71

Effective tax rate 2011

Effective Tax Rate

In percent

-2%72.8 71.3

20112010

TaxIn mln EUR

0.05.4

19.5

2010

19.5

2011

14.1

� EUR 108.5 million of book gain on the

sale of our 20% equity stake in BORCO

(Bahamas) is exempted for tax purposes

� Excluding exceptional items, the effective

tax rate for 2011 amounted to 19.5%

II

Roadshow presentation FY 2011 72

Sources and uses of cash in 2011

Net Cash position

31/12/2011*

13.1

Divest-

ments

281.3

Invest-

ments

710.9

Tax paid

28.1

Net finance

costs

61.3

Gross

operating

cash flow

495.8

Net Cash position 1/1/2011*

147.8

FX /

(de)con-

solidation

2.9

-67.0

Financing

activities

181.4

Derivative

Settlement

Consolidated Statement of Cash Flows

In mln EUR

* Including bank overdrafts.

III

Roadshow presentation FY 2011 73

Vopak’s Pensions

Dutch 83%

Other 17%

� Cover ratio ultimo 2011

is 106%

� Return was 5% in 2011

� Pension contribution to

remain at the same,

maximum level of 30%

� An additional contribution

of EUR 50 million in 2011

Vopak’s Pension obligations

In percentDutch Pension Fund

Highlights

Other

20%

Dutch

80%

IV

Roadshow presentation FY 2011 74

Accounting consequences: IAS 19 Employee Benefits effective for 2013

� Higher volatility in net pension liabilityRemoval

10% corridor

approach

Only service

and net finance

cost in P&L

� Rest of changes (i.e. remeasurements)

in other comprehensive income,

including the first time recognition of the

10% corridor (EUR 107.4 million)

Discount rate

expected return

plan assets

� The discount rate used to measure the defined benefit obligation will

also be used for the expected returns on plan assets, which

generally is a lower rate than used under current IAS 19

� Immediate recognition of

the unrecognized actuarial

gains and losses through

equity, which amounted to

EUR 107.4 million at

1 January 2012 for the

financial statements 2013

(comparable figures 2012)*

V

* See page 90 Annual Report 2011.Note: Effectively at 1 January 2012

Roadshow presentation FY 2011 75

Renewal RCF – 2 February 2012EUR 1.1 bln revolving credit facility (RCF)

Maturity 5 + 1 years

Debt funding program further strengthened during 2011

Renewal RCF – 2 February 2011EUR 1.2 bln revolving credit facility (RCF)

Maturity 5 + 1 + 1 years

Extension with 1 year

VI

Roadshow presentation FY 2011 76

Maturity of debt funding further enhanced

Maximum

Net Senior Debt/

EBITDA

3.75 3.75 3.75

Additional headroom

when financed with

subordinated debt

> 3.75 > 3.75

Minimum EBITDA /

Net Interest Payable3.5 3.5

Amount outstanding

Redemption

payment

- Up to 4.25 > 3.75

Term

Asian PPUS PP RCFCovenant

2001 2007 2009 SGD2009 SGD2010 JPY PP EUR 1.2 bln

4.0 3.5 3.5

65 mln 375 mln 674 mln

USD USD USD

2011-2016 2015-2022 2017-2029

210 mln 225 mln 20 bln

SGD SGD JPY

2014 2018 2040 2016*

* On 2 February 2012, extension of the facility with one additional year (EUR 1.1 billion).Note: PP = Private Placement and RCF = Revolving Credit Facility

EUR

100 mln

VII

Roadshow presentation FY 2011 77

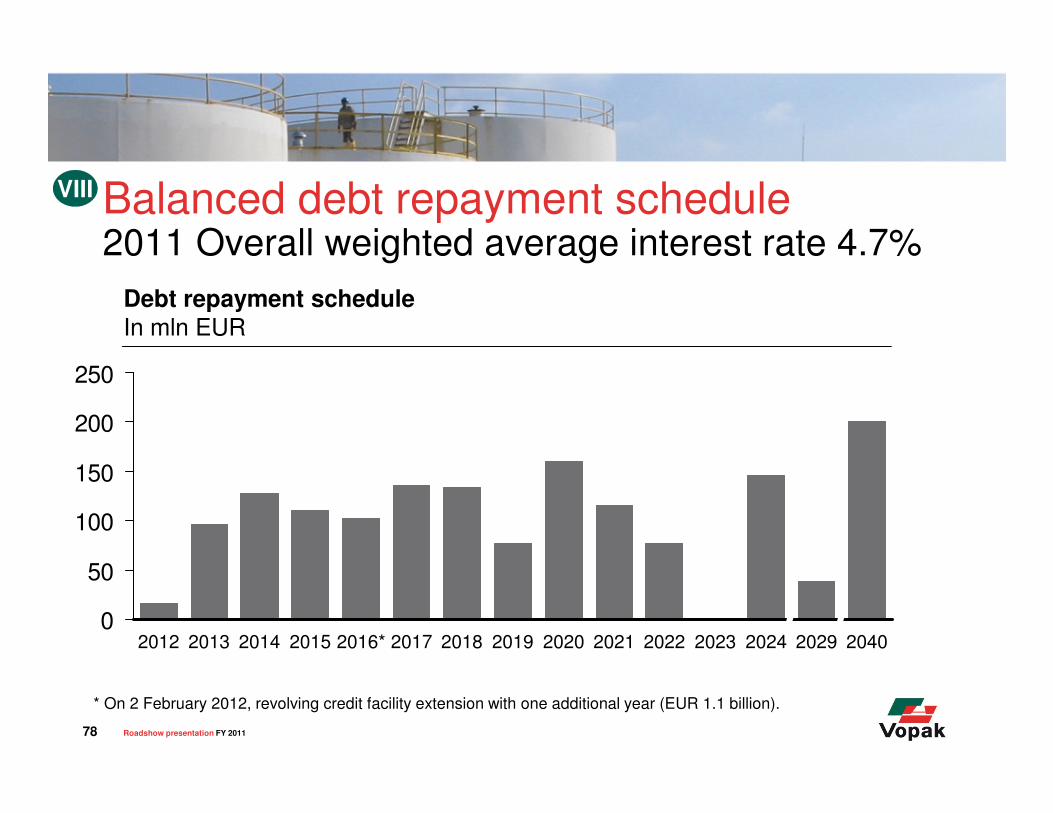

Balanced debt repayment schedule2011 Overall weighted average interest rate 4.7%

Debt repayment schedule

In mln EUR

0

50

100

150

200

250

20132012 2022 2024 2029 2040202320202019 2021201820172016*20152014

* On 2 February 2012, revolving credit facility extension with one additional year (EUR 1.1 billion).

VIII

Roadshow presentation FY 2011 78

The world of Vopak

Roadshow presentation FY 2011 79