rumo logística operadora multimodal s.a.ri.rumolog.com/ptb/7275/rumo - itr e release 3t15.pdf · 3...

TRANSCRIPT

Rumo Logística Operadora Multimodal S.A.

Interim Financial Statements

September 30, 2015

and review report of the independent auditors thereon

(A free translation of the original in Portuguese)

Rumo Logística Operadora Multimodal S.A.

Interim Financial Statements

September 30, 2015

Contents

Independent auditor’s report on review of interim financial

statements 3

Balance sheets 5

Statements of income 8

Statements of comprehensive income 10

Statements of changes in equity 11

Statements of cash flows – indirect method 14

Statements of value added 17

Notes to the interim financial statements 19

3

Independent auditor's report on review of interim financial statements

To the Board of Directors and Shareholders Rumo Logística Operadora Multimodal S.A.

Santos-SP

Introduction

We have reviewed the accompanying individual and consolidated interim financial statements of

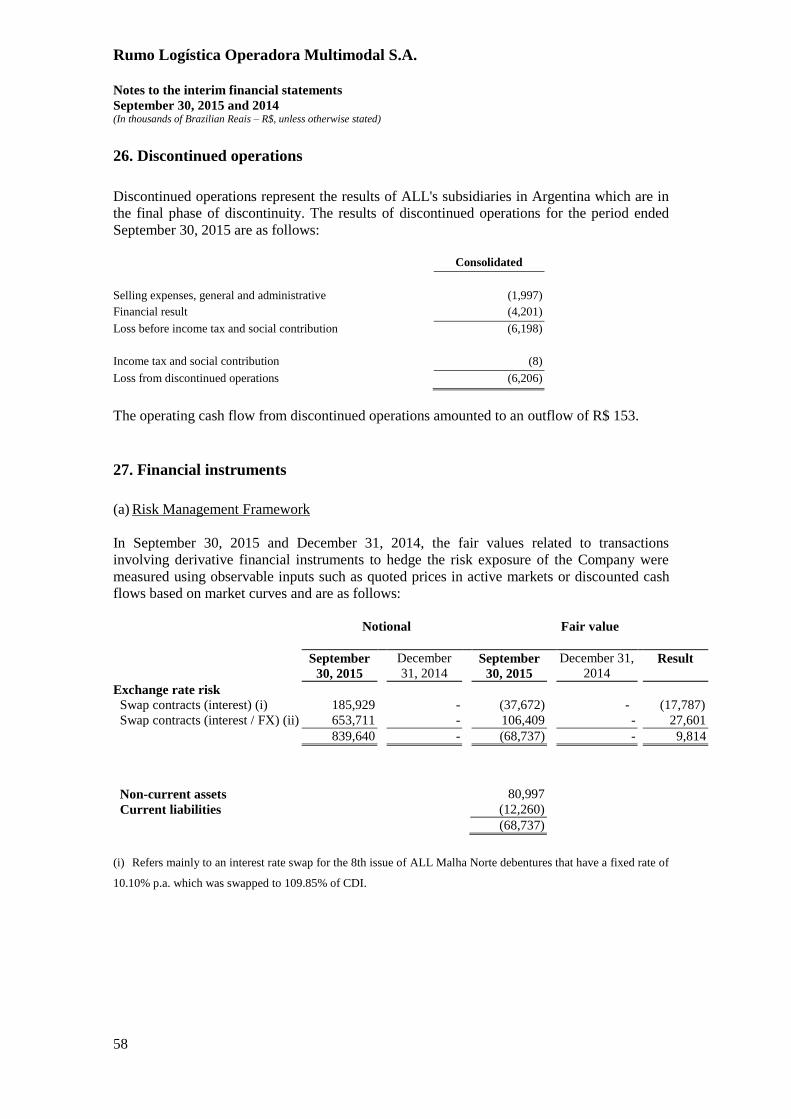

Rumo Logística Operadora Multimodal S.A. (“the Company”) in the Quarterly Information Form

– ITR for the quarter ended September 30, 2015, which comprise the balance sheet as at

September 30, 2015 and the related statements of income and other comprehensive income for the

3- and 9-month periods then ended and the changes in equity and cash flows for the 9-month

period then ended, and explanatory notes.

Management is responsible for the preparation and fair presentation of these interim financial

statements in accordance with Technical Pronouncement CPC 21(R1) and IAS 34, ‘Interim

Financial Reporting’ as issued by the International Accounting Standards Board – IASB, as well

as the presentation of the information in accordance with Comissão de Valores Mobiliários

(“CVM”) regulations applicable to the Quarterly Information Form – ITR. Our responsibility is to

express a conclusion on these interim financial statements based on our review.

Scope of Review

We conducted our review in accordance with the Brazilian and International Standard on Review

Engagements 2410, “Review of Interim Financial Information Performed by the Independent

Auditor of the Entity”. A review of interim financial statements consists of making inquiries,

primarily of persons responsible for financial and accounting matters, and applying analytical and

other review procedures. A review is substantially less in scope than an audit conducted in

accordance with auditing standards and consequently does not enable us to obtain assurance that

we would become aware of all significant matters that might be identified in an audit.

Accordingly, we do not express an audit opinion.

Conclusion on the interim financial statements

Based on our review, nothing has come to our attention that causes us to believe that the

accompanying interim financial statements included in the Quarterly Information Form – ITR

referred above were not prepared, in all material respects, in accordance with CPC21 (R1) and

IAS 34 applicable to the preparation of the Quarterly Information Form – ITR and presented in

accordance with the CVM regulations.

4

Other matters

Statement of value added

We have also reviewed the Statements of value added (DVA), individual and consolidated, for

the 9-month period ended September 30, 2015, prepared by Management, whose presentation in

interim financial information is required by CVM regulation applicable to the Quarterly

Information Form – ITR and is considered supplementary information by IFRS, that does not

required the DVA presentation. These statements were subject to the same review procedures

previously described and, based on our review, nothing has come to our attention that causes us to

believe that they were not prepared, in all material respects, consistently with the individual and

consolidated interim financial statements as a whole.

Corresponding figures

The corresponding figures, individual and consolidated, for the balance sheet as at December 31,

2014 were audited by another auditor who issued an unmodified report on March 3, 2015 and the

statements, individual and consolidated, of income and other comprehensive income for the 3-

and 9-month periods ended September 30, 2014 and changes in equity and cash flows for the 9-

month period ended September 30, 2014 were reviewed by another auditor who issued an

unmodified report on November 5, 2014. The corresponding figures related to the statement of

value added (DVA), individual and consolidated, for the 9-month period ended September 30,

2014, were subject to the same review procedures by those auditors and, based on their review,

those auditors issued a report stating that nothing has come to their attention that causes them to

believe that the DVA were not prepared, in all material respects, consistently with the individual

and consolidated interim financial statements as a whole.

Curitiba, November 5, 2015.

KPMG Auditores Independentes

CRC SP-014428/O-6

Original in Portuguese signed by

João Alberto Dias Panceri

Accountant CRC PR048555/O-2

5

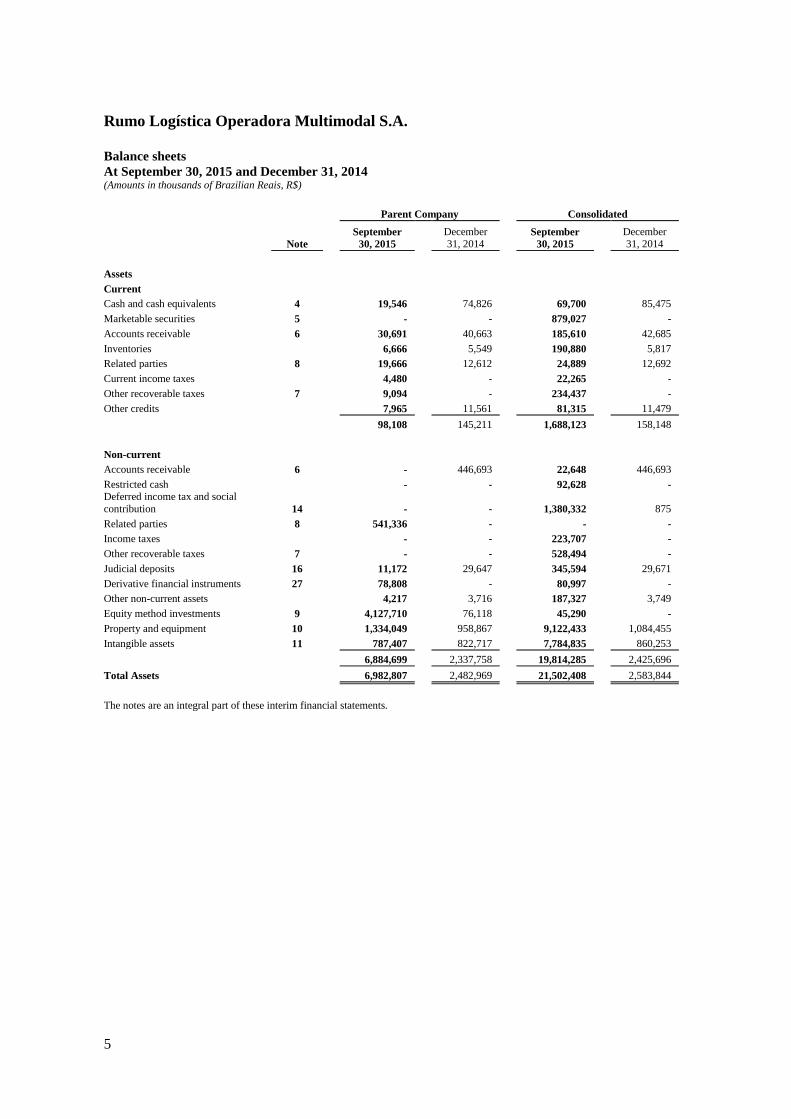

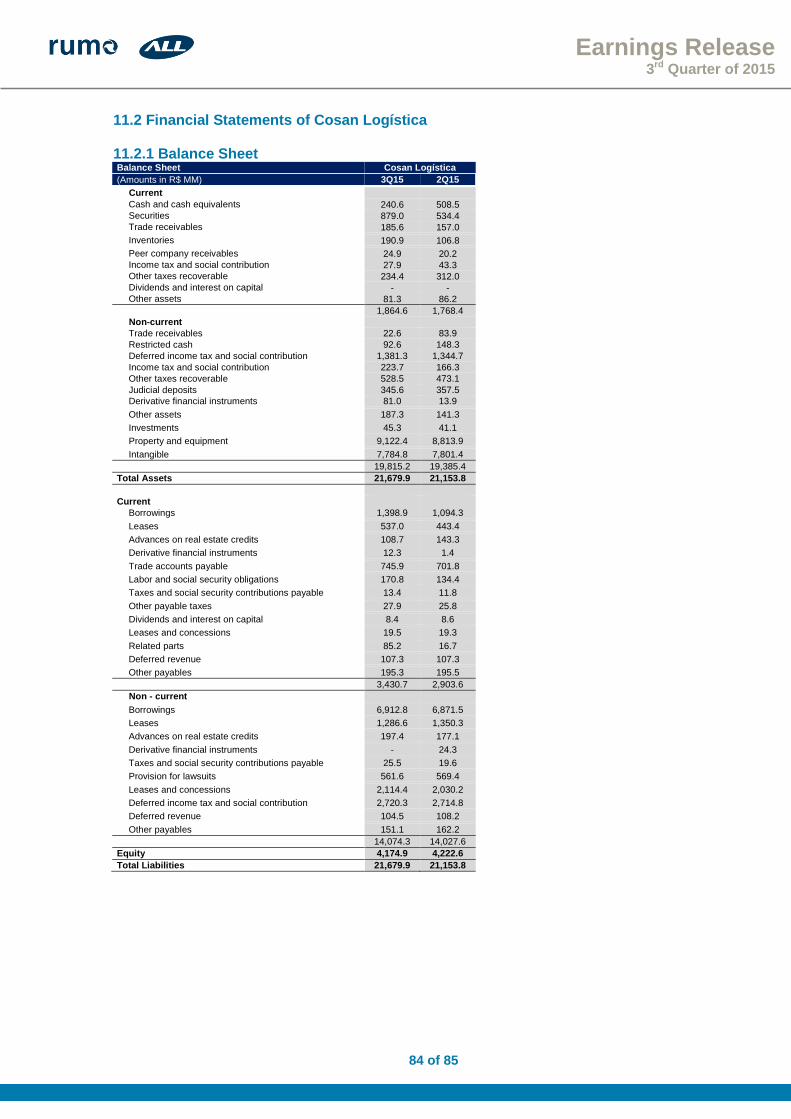

Rumo Logística Operadora Multimodal S.A.

Balance sheets

At September 30, 2015 and December 31, 2014 (Amounts in thousands of Brazilian Reais, R$)

Parent Company Consolidated

Note

September

30, 2015

December 31, 2014

September

30, 2015

December 31, 2014

Assets

Current

Cash and cash equivalents 4 19,546 74,826 69,700 85,475

Marketable securities 5 - - 879,027 -

Accounts receivable 6 30,691 40,663 185,610 42,685

Inventories 6,666 5,549 190,880 5,817

Related parties 8 19,666 12,612 24,889 12,692

Current income taxes 4,480 - 22,265 -

Other recoverable taxes 7 9,094 - 234,437 -

Other credits 7,965 11,561 81,315 11,479

98,108 145,211 1,688,123 158,148

Non-current

Accounts receivable 6 - 446,693 22,648 446,693

Restricted cash - - 92,628 - Deferred income tax and social

contribution 14 - - 1,380,332 875

Related parties 8 541,336 - - -

Income taxes - - 223,707 -

Other recoverable taxes 7 - - 528,494 -

Judicial deposits 16 11,172 29,647 345,594 29,671

Derivative financial instruments 27 78,808 - 80,997 -

Other non-current assets 4,217 3,716 187,327 3,749

Equity method investments 9 4,127,710 76,118 45,290 -

Property and equipment 10 1,334,049 958,867 9,122,433 1,084,455

Intangible assets 11 787,407 822,717 7,784,835 860,253

6,884,699 2,337,758 19,814,285 2,425,696

Total Assets 6,982,807 2,482,969 21,502,408 2,583,844

The notes are an integral part of these interim financial statements.

6

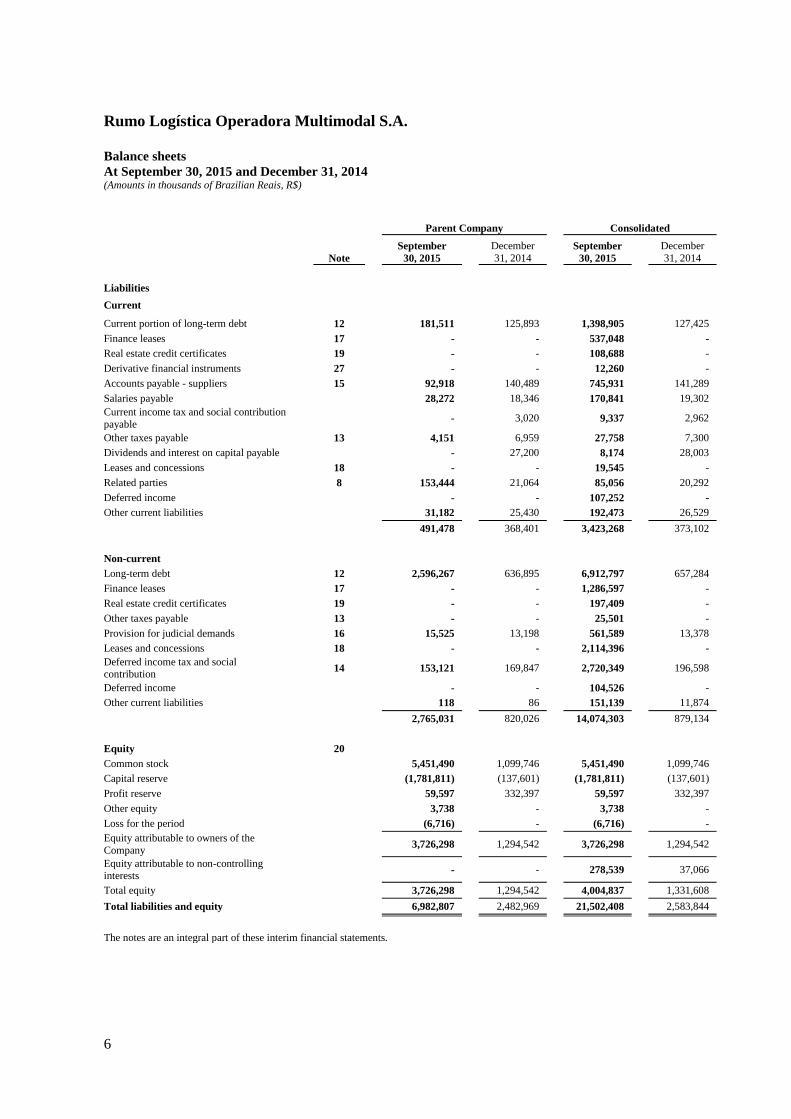

Rumo Logística Operadora Multimodal S.A.

Balance sheets

At September 30, 2015 and December 31, 2014 (Amounts in thousands of Brazilian Reais, R$)

Parent Company Consolidated

Note

September

30, 2015

December

31, 2014 September

30, 2015

December

31, 2014

Liabilities

Current

Current portion of long-term debt 12 181,511 125,893 1,398,905 127,425

Finance leases 17 - - 537,048 -

Real estate credit certificates 19 - - 108,688 -

Derivative financial instruments 27 - - 12,260 -

Accounts payable - suppliers 15 92,918 140,489 745,931 141,289

Salaries payable 28,272 18,346 170,841 19,302

Current income tax and social contribution

payable - 3,020 9,337 2,962

Other taxes payable 13 4,151 6,959 27,758 7,300

Dividends and interest on capital payable - 27,200 8,174 28,003

Leases and concessions 18 - - 19,545 -

Related parties 8 153,444 21,064 85,056 20,292

Deferred income - - 107,252 -

Other current liabilities 31,182 25,430 192,473 26,529

491,478 368,401 3,423,268 373,102

Non-current

Long-term debt 12 2,596,267 636,895 6,912,797 657,284

Finance leases 17 - - 1,286,597 -

Real estate credit certificates 19 - - 197,409 -

Other taxes payable 13 - - 25,501 -

Provision for judicial demands 16 15,525 13,198 561,589 13,378

Leases and concessions 18 - - 2,114,396 -

Deferred income tax and social contribution

14 153,121 169,847 2,720,349 196,598

Deferred income - - 104,526 -

Other current liabilities 118 86 151,139 11,874

2,765,031 820,026 14,074,303 879,134

Equity 20

Common stock 5,451,490 1,099,746 5,451,490 1,099,746

Capital reserve (1,781,811) (137,601) (1,781,811) (137,601)

Profit reserve 59,597 332,397 59,597 332,397

Other equity 3,738 - 3,738 -

Loss for the period (6,716) - (6,716) -

Equity attributable to owners of the

Company 3,726,298 1,294,542 3,726,298 1,294,542

Equity attributable to non-controlling interests

- - 278,539 37,066

Total equity 3,726,298 1,294,542 4,004,837 1,331,608

Total liabilities and equity 6,982,807 2,482,969 21,502,408 2,583,844

The notes are an integral part of these interim financial statements.

7

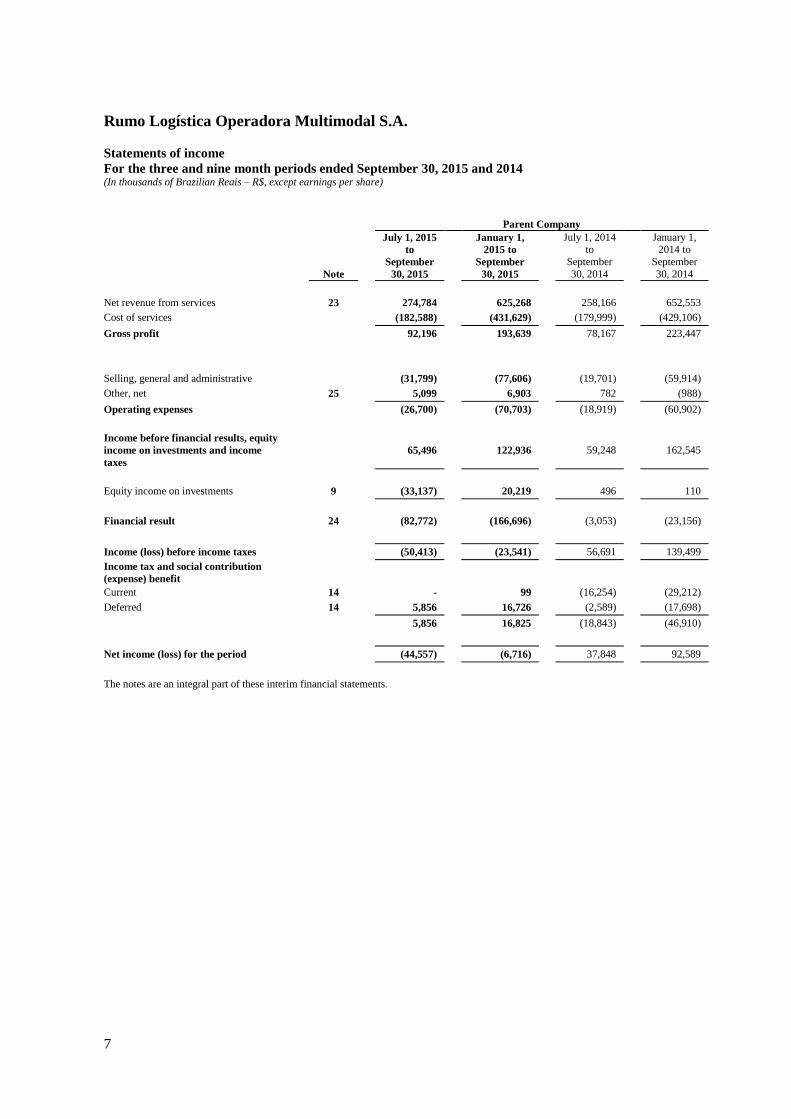

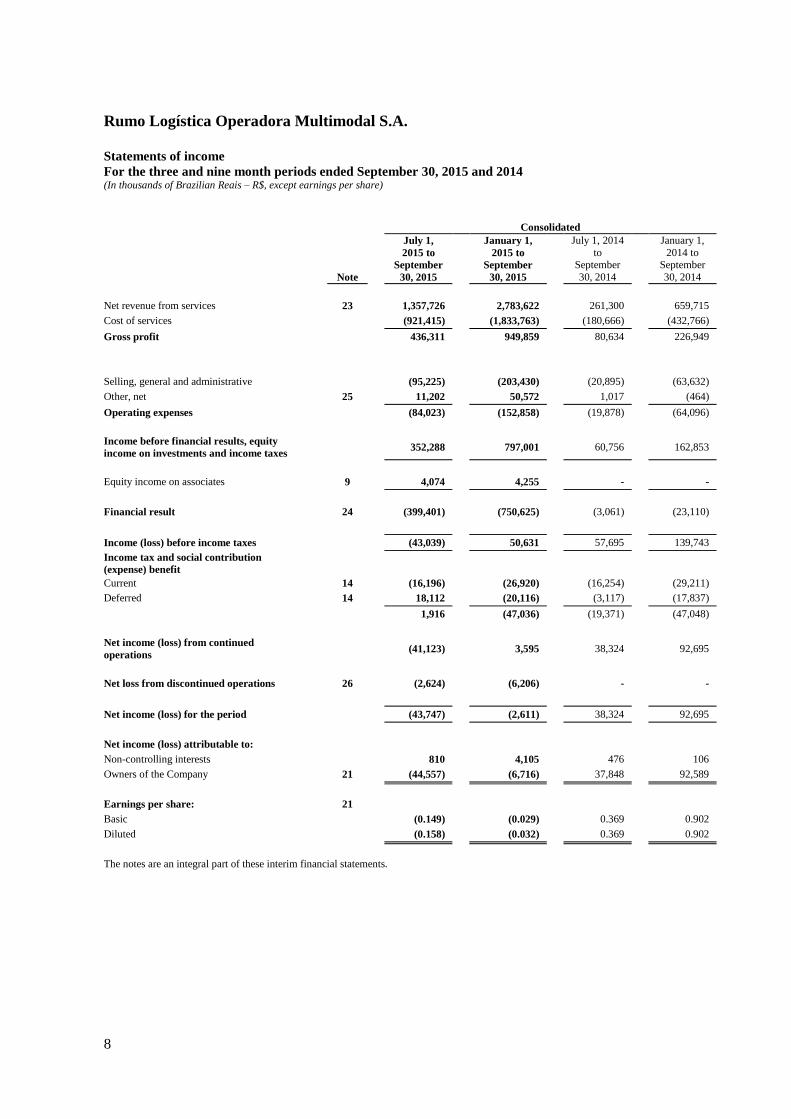

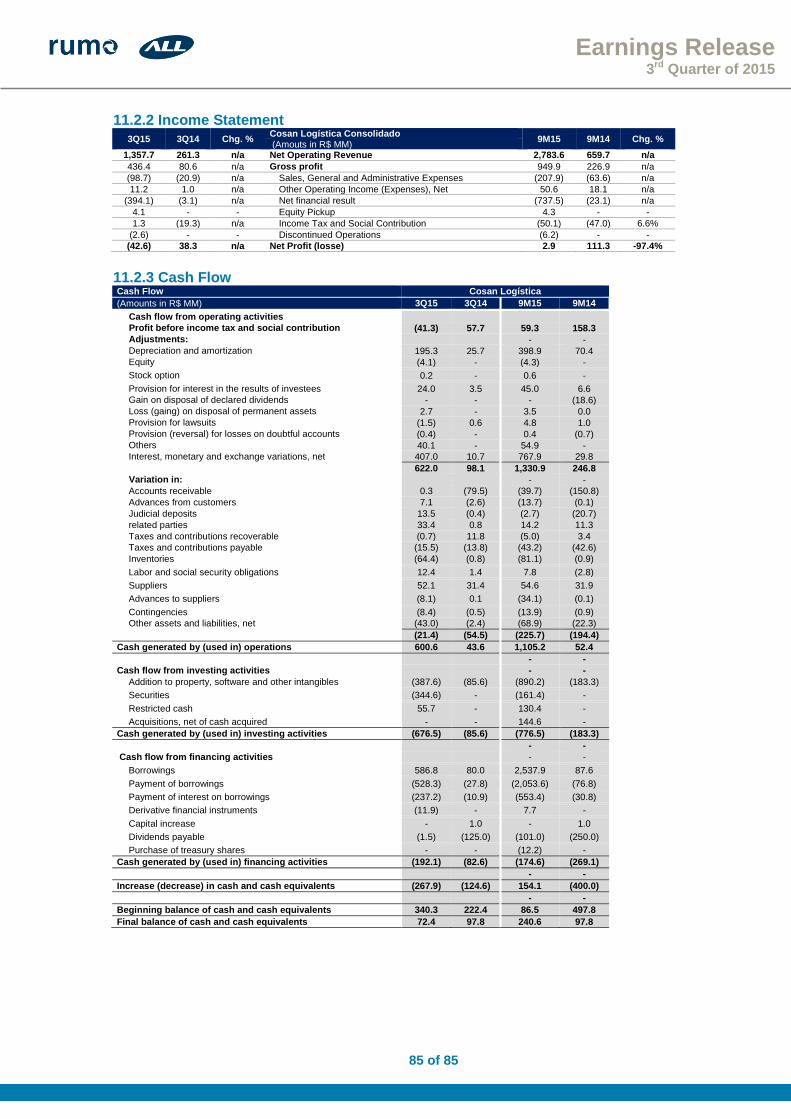

Rumo Logística Operadora Multimodal S.A.

Statements of income

For the three and nine month periods ended September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, except earnings per share)

Parent Company

Note

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1, 2014 to

September

30, 2014

January 1, 2014 to

September

30, 2014

Net revenue from services 23 274,784 625,268 258,166 652,553

Cost of services (182,588) (431,629) (179,999) (429,106)

Gross profit 92,196 193,639 78,167 223,447

Selling, general and administrative (31,799) (77,606) (19,701) (59,914)

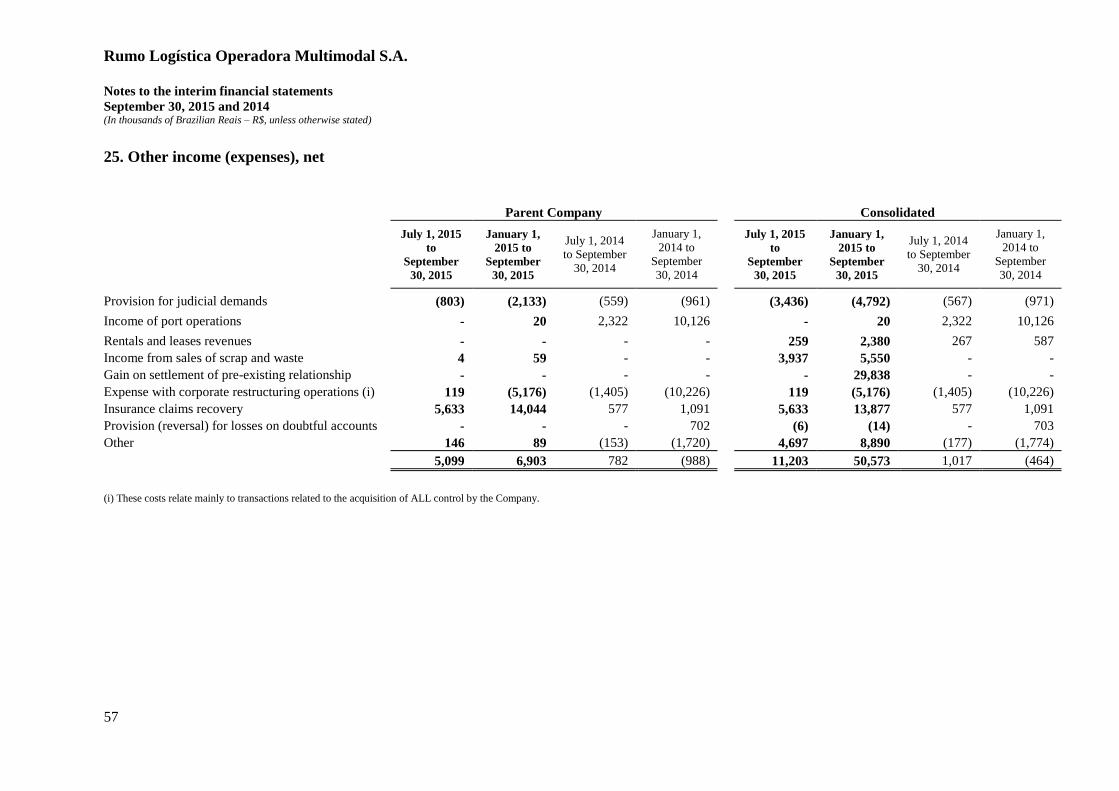

Other, net 25 5,099 6,903 782 (988)

Operating expenses (26,700) (70,703) (18,919) (60,902)

Income before financial results, equity

income on investments and income

taxes

65,496 122,936 59,248 162,545

Equity income on investments 9 (33,137) 20,219 496 110

Financial result 24 (82,772) (166,696) (3,053) (23,156)

Income (loss) before income taxes (50,413) (23,541) 56,691 139,499

Income tax and social contribution

(expense) benefit

Current 14 - 99 (16,254) (29,212)

Deferred 14 5,856 16,726 (2,589) (17,698)

5,856 16,825 (18,843) (46,910)

Net income (loss) for the period (44,557) (6,716) 37,848 92,589

The notes are an integral part of these interim financial statements.

8

Rumo Logística Operadora Multimodal S.A.

Statements of income

For the three and nine month periods ended September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, except earnings per share)

Consolidated

Note

July 1,

2015 to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1, 2014

to September

30, 2014

January 1,

2014 to September

30, 2014

Net revenue from services 23 1,357,726 2,783,622 261,300 659,715

Cost of services (921,415) (1,833,763) (180,666) (432,766)

Gross profit 436,311 949,859 80,634 226,949

Selling, general and administrative (95,225) (203,430) (20,895) (63,632)

Other, net 25 11,202 50,572 1,017 (464)

Operating expenses (84,023) (152,858) (19,878) (64,096)

Income before financial results, equity

income on investments and income taxes 352,288 797,001 60,756 162,853

Equity income on associates 9 4,074 4,255 - -

Financial result 24 (399,401) (750,625) (3,061) (23,110)

Income (loss) before income taxes (43,039) 50,631 57,695 139,743

Income tax and social contribution

(expense) benefit

Current 14 (16,196) (26,920) (16,254) (29,211)

Deferred 14 18,112 (20,116) (3,117) (17,837)

1,916 (47,036) (19,371) (47,048)

Net income (loss) from continued

operations (41,123) 3,595 38,324 92,695

Net loss from discontinued operations 26 (2,624) (6,206) - -

Net income (loss) for the period (43,747) (2,611) 38,324 92,695

Net income (loss) attributable to:

Non-controlling interests 810 4,105 476 106

Owners of the Company 21 (44,557) (6,716) 37,848 92,589

Earnings per share: 21

Basic (0.149) (0.029) 0.369 0.902

Diluted (0.158) (0.032) 0.369 0.902

The notes are an integral part of these interim financial statements.

9

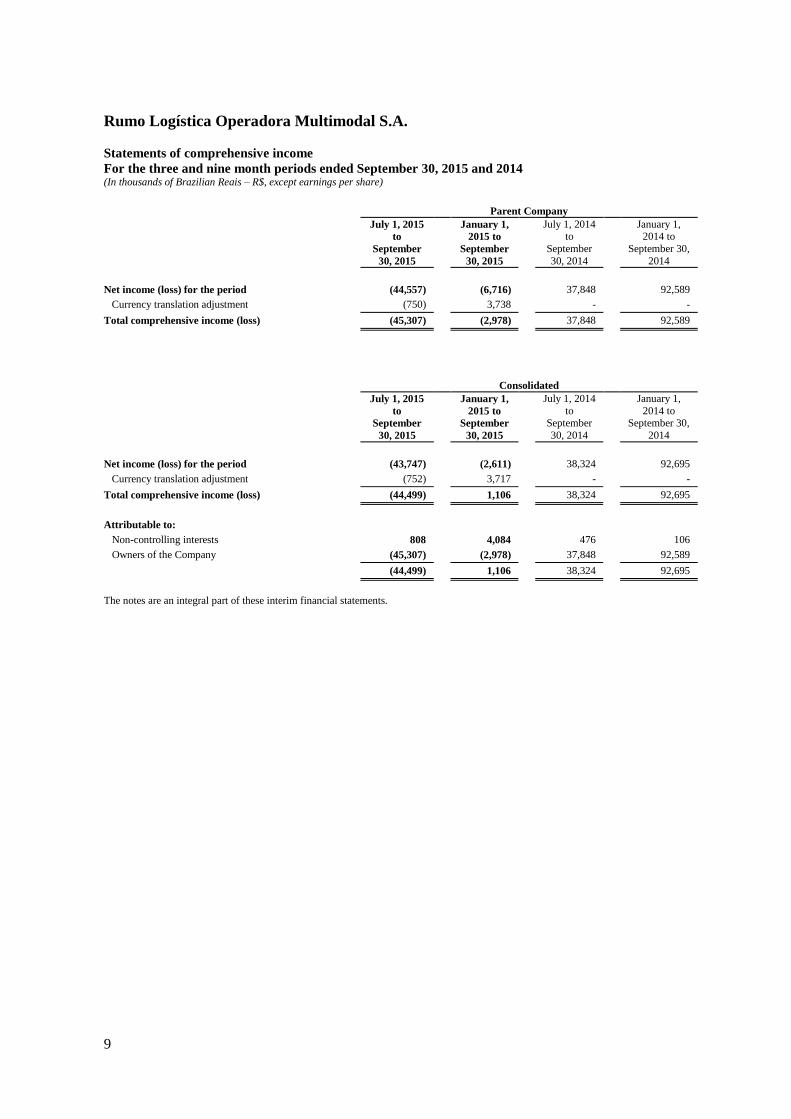

Rumo Logística Operadora Multimodal S.A.

Statements of comprehensive income

For the three and nine month periods ended September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, except earnings per share)

Parent Company

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1, 2014 to

September

30, 2014

January 1, 2014 to

September 30,

2014

Net income (loss) for the period (44,557) (6,716) 37,848 92,589

Currency translation adjustment (750) 3,738 - -

Total comprehensive income (loss) (45,307) (2,978) 37,848 92,589

Consolidated

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1, 2014

to September

30, 2014

January 1,

2014 to September 30,

2014

Net income (loss) for the period (43,747) (2,611) 38,324 92,695

Currency translation adjustment (752) 3,717 - -

Total comprehensive income (loss) (44,499) 1,106 38,324 92,695

Attributable to:

Non-controlling interests 808 4,084 476 106

Owners of the Company (45,307) (2,978) 37,848 92,589

(44,499) 1,106 38,324 92,695

The notes are an integral part of these interim financial statements.

10

Rumo Logística Operadora Multimodal S.A.

Statements of changes in equity

For the nine month periods ended September 30, 2015 and 2014

(Amounts in thousands of Brazilian Reais, R$)

Attributable to shareholders of Company

Profit reserve

Common

stock

Capital

reserve Legal

Retained

earnings

Profit for the

period Total

Non-

controlling

interest Total equity

Balance at January 1, 2014 1,099,746

(137,601) 24,486 372,250 - 1,358,881 37,013 1,395,894

Income for the period - - - - 92,589 92,589 106 92,695

Total comprehensive income for the

period - - - - 92,589 92,589 106 92,695

Reserve from write-off of dividends - - - 98,334 - 98,334 - 98,334

Interim dividends - - - (250,000) - (250,000) 65 (249,935)

Total contributions or distributions

to shareholders, recognized directly

in equity - - - (151,666) - (151,666) 65 (151,601)

Balance at September 30, 2014 1,099,746 (137,601) 24,486 220,584 92,589 1,299,804 37,184 1,336,988

The notes are an integral part of these interim financial statements.

11

Rumo Logística Operadora Multimodal S.A.

Statements of changes in equity

For the nine month periods ended September 30, 2015 and 2014

(Amounts in thousands of Brazilian Reais, R$)

Attributable to shareholders of Company

Profit reserve

Common

stock

Capital

reserve Legal

Retained

earnings

Loss for the

period Other equity Total

Non-

controlling

interest Total equity

Balance at January 1,

2015 1,099,746 (137,601) 30,212 302,185 - - 1,294,542 37,066 1,331,608

Loss for the period - - - - (6,716) - (6,716) 4,105 (2,611)

Currency translation

adjustment - - - - - 3,738 3,738 (21) 3,717

Total comprehensive

income for the period - - - - (6,716) 3,738 (2,978) 4,084 1,106

Capital increase (ALL

acquisition) 4,351,744 (1,644,210) - - - - 2,707,534 240,900 2,948,434

Dividends (Note 20 c) - - - (272,800) - - (272,800) (3,511) (276,311)

Total contributions or

distributions to

shareholders,

recognized directly in

equity 4,351,744 (1,644,210) - (272,800) - - 2,434,734 237,389 2,672,123

Balance at September

30, 2015 5,451,490 (1,781,811) 30,212 29,385 (6,716) 3,738 3,726,298 278,539 4,004,837

The notes are an integral part of these interim financial statements.

12

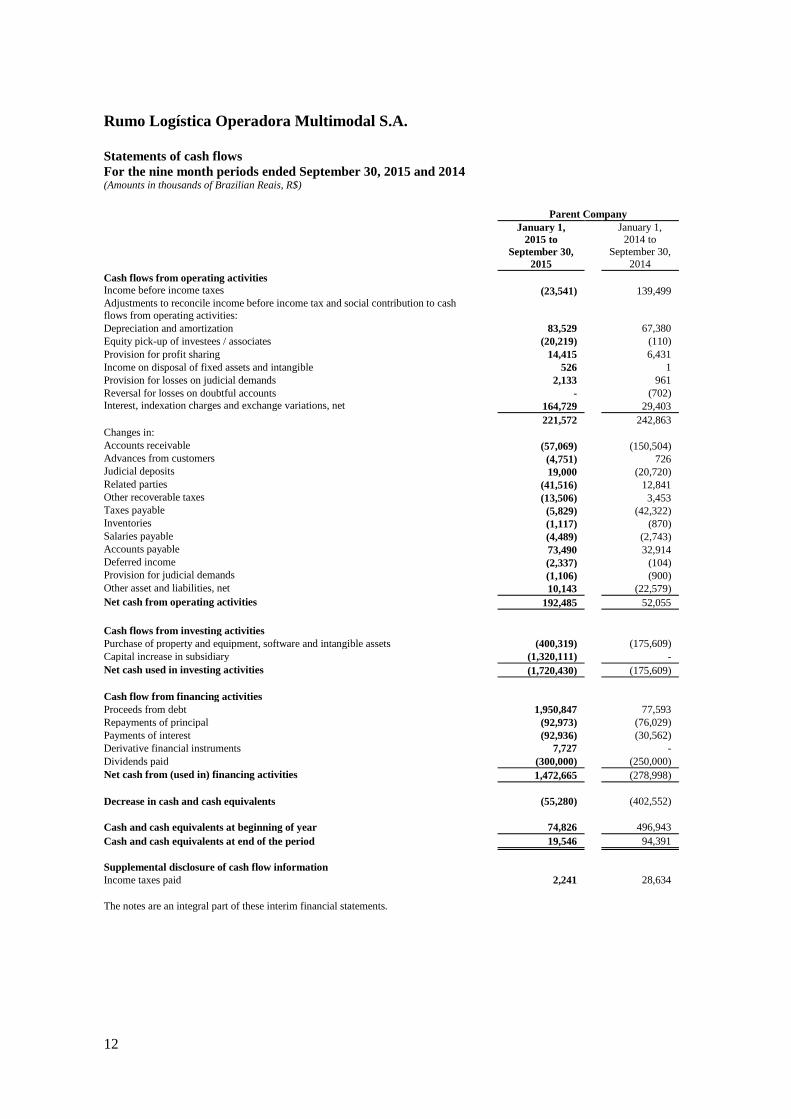

Rumo Logística Operadora Multimodal S.A.

Statements of cash flows

For the nine month periods ended September 30, 2015 and 2014 (Amounts in thousands of Brazilian Reais, R$)

Parent Company

January 1,

2015 to

September 30,

2015

January 1, 2014 to

September 30,

2014

Cash flows from operating activities

Income before income taxes (23,541) 139,499 Adjustments to reconcile income before income tax and social contribution to cash

flows from operating activities:

Depreciation and amortization 83,529 67,380

Equity pick-up of investees / associates (20,219) (110)

Provision for profit sharing 14,415 6,431

Income on disposal of fixed assets and intangible 526 1

Provision for losses on judicial demands 2,133 961

Reversal for losses on doubtful accounts - (702)

Interest, indexation charges and exchange variations, net 164,729 29,403

221,572 242,863

Changes in: Accounts receivable (57,069) (150,504) Advances from customers (4,751) 726 Judicial deposits 19,000 (20,720)

Related parties (41,516) 12,841

Other recoverable taxes (13,506) 3,453 Taxes payable (5,829) (42,322) Inventories (1,117) (870)

Salaries payable (4,489) (2,743)

Accounts payable 73,490 32,914 Deferred income (2,337) (104) Provision for judicial demands (1,106) (900)

Other asset and liabilities, net 10,143 (22,579)

Net cash from operating activities 192,485 52,055

Cash flows from investing activities

Purchase of property and equipment, software and intangible assets (400,319) (175,609)

Capital increase in subsidiary (1,320,111) -

Net cash used in investing activities (1,720,430) (175,609)

Cash flow from financing activities

Proceeds from debt 1,950,847 77,593

Repayments of principal (92,973) (76,029)

Payments of interest (92,936) (30,562)

Derivative financial instruments 7,727 -

Dividends paid (300,000) (250,000)

Net cash from (used in) financing activities 1,472,665 (278,998)

Decrease in cash and cash equivalents (55,280) (402,552)

Cash and cash equivalents at beginning of year 74,826 496,943

Cash and cash equivalents at end of the period 19,546 94,391

Supplemental disclosure of cash flow information

Income taxes paid 2,241 28,634

The notes are an integral part of these interim financial statements.

13

Rumo Logística Operadora Multimodal S.A.

Statements of cash flows

For the nine month periods ended September 30, 2015 and 2014 (Amounts in thousands of Brazilian Reais, R$)

Consolidated

January 1,

2015 to

September

30, 2015

January 1, 2014 to

September 30,

2014

Cash flow from operating activities

Income before income taxes 50,631 139,743 Adjustments to reconcile net income before income tax and social contribution to cash flows

from operating activities:

Depreciation and amortization 398,871 70,378

Equity pick-up of investees / associates (4,255) -

Provision for profit sharing 44,993 6,631

Income on disposal of fixed assets and intangible 3,463 1

Provision for losses on judicial demands 4,801 971

Provision (reversal) for losses on doubtful accounts 386 (702)

Other 52,102 - Interest, indexation charges and exchange variations, net 767,889 29,810

1,318,881 246,832

Changes in: Accounts receivable (39,676) (150,804) Advances from customers (13,745) (89)

Judicial deposits (2,687) (20,736)

Related parties 14,029 11,349 Other recoverable taxes 656 3,428 Taxes payable (43,309) (42,614)

Inventories (81,068) (862)

Salaries payable 7,817 (2,785) Accounts payable 54,568 31,908 Deferred income (34,116) (80)

Judicial demands (13,855) (892)

Other asset and liabilities, net (68,948) (22,261)

Net cash from operating activities 1,098,547 52,394

Cash flow from investing activities

Purchase of property, plant and equipment, software and intangible assets (890,184) (183,280)

Marketable securities (161,405) -

Restricted cash 130,440 -

Net cash acquired in business acquisition 169,703 -

Net cash used in investing activities (751,446) (183,280)

Cash flow from financing activities

Proceeds from debt 2,537,908 87,576

Repayments of principal (2,053,608) (76,840)

Payments of interest (553,403) (30,839)

Derivative financial instruments 7,727 -

Dividends paid (301,500) (250,000)

Net cash used in financing activities (362,876) (270,103)

Decrease in cash and cash equivalents (15,775) (400,989)

Cash and cash equivalents at beginning of year 85,475 497,753

Cash and cash equivalents at end of the period 69,700 96,764

Supplemental disclosure of cash flow information

Income taxes paid 6,431 28,922

The notes are an integral part of these interim financial statements.

14

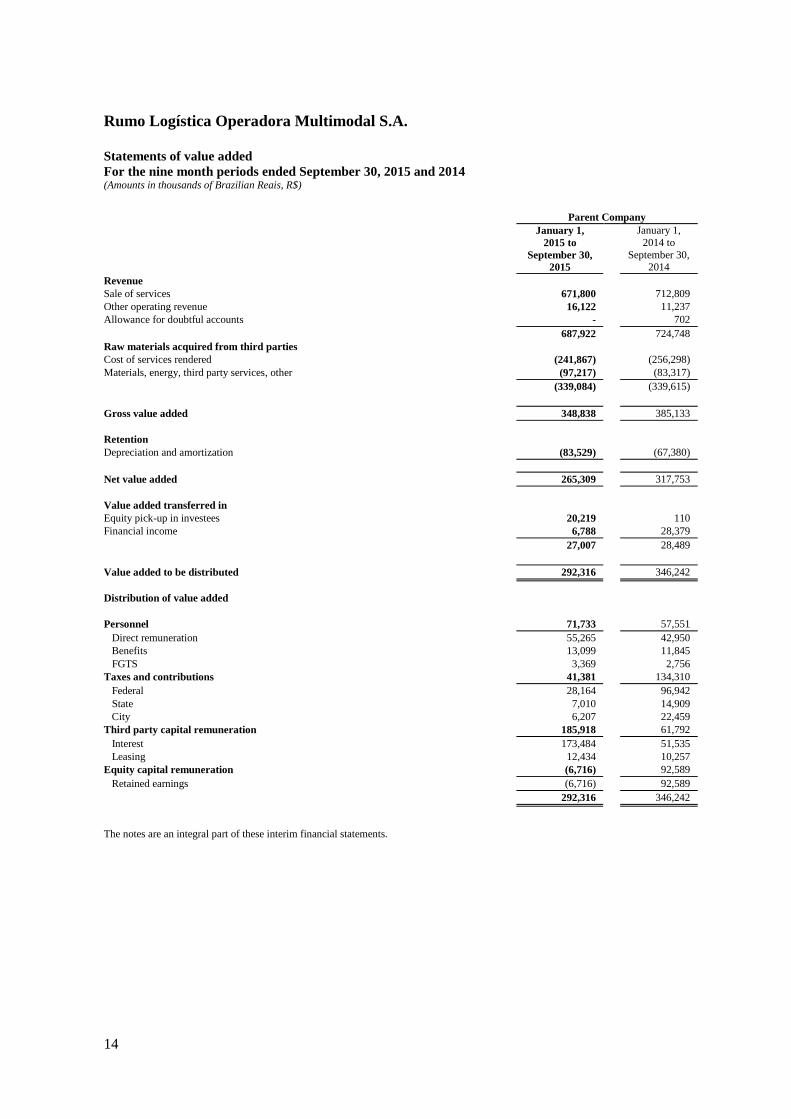

Rumo Logística Operadora Multimodal S.A.

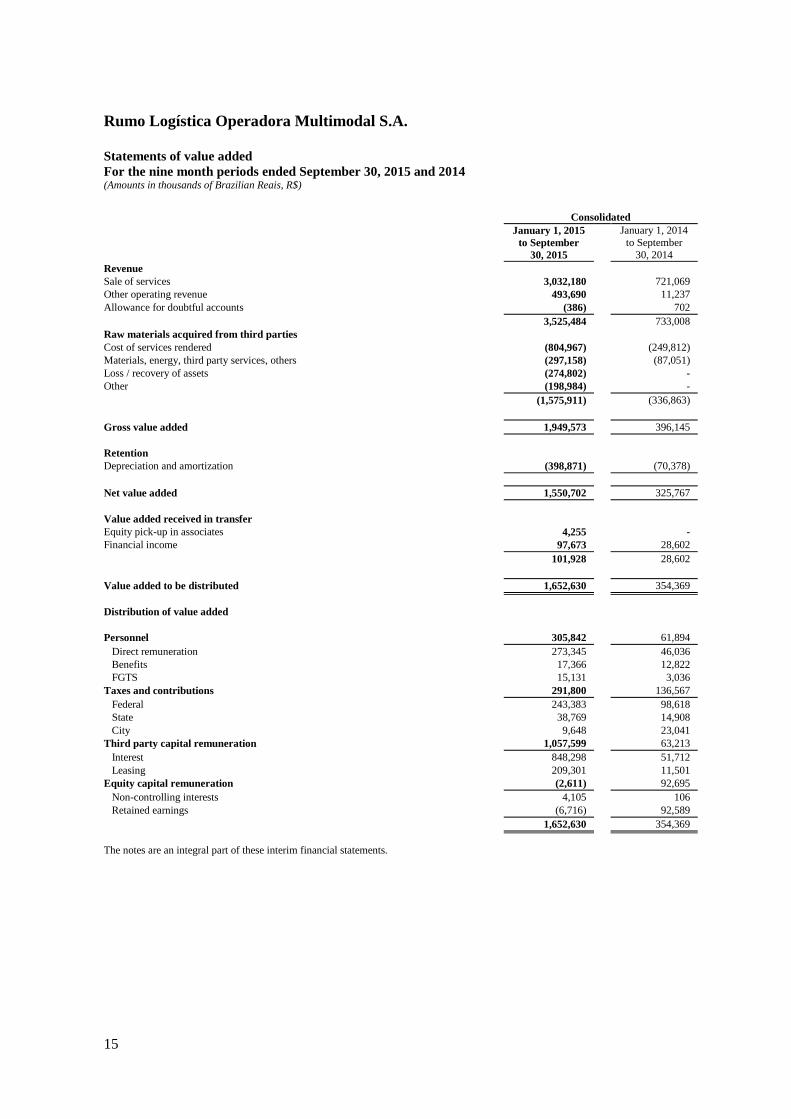

Statements of value added

For the nine month periods ended September 30, 2015 and 2014 (Amounts in thousands of Brazilian Reais, R$)

Parent Company

January 1,

2015 to

September 30,

2015

January 1,

2014 to

September 30, 2014

Revenue

Sale of services 671,800 712,809

Other operating revenue 16,122 11,237

Allowance for doubtful accounts - 702

687,922 724,748

Raw materials acquired from third parties

Cost of services rendered (241,867) (256,298)

Materials, energy, third party services, other (97,217) (83,317)

(339,084) (339,615)

Gross value added 348,838 385,133

Retention

Depreciation and amortization (83,529) (67,380)

Net value added 265,309 317,753

Value added transferred in

Equity pick-up in investees 20,219 110

Financial income 6,788 28,379

27,007 28,489

Value added to be distributed 292,316 346,242

Distribution of value added

Personnel 71,733 57,551

Direct remuneration 55,265 42,950

Benefits 13,099 11,845

FGTS 3,369 2,756

Taxes and contributions 41,381 134,310

Federal 28,164 96,942

State 7,010 14,909

City 6,207 22,459

Third party capital remuneration 185,918 61,792

Interest 173,484 51,535

Leasing 12,434 10,257

Equity capital remuneration (6,716) 92,589

Retained earnings (6,716) 92,589

292,316 346,242

The notes are an integral part of these interim financial statements.

15

Rumo Logística Operadora Multimodal S.A.

Statements of value added

For the nine month periods ended September 30, 2015 and 2014 (Amounts in thousands of Brazilian Reais, R$)

Consolidated

January 1, 2015

to September

30, 2015

January 1, 2014

to September

30, 2014

Revenue

Sale of services 3,032,180 721,069

Other operating revenue 493,690 11,237

Allowance for doubtful accounts (386) 702

3,525,484 733,008

Raw materials acquired from third parties

Cost of services rendered (804,967) (249,812)

Materials, energy, third party services, others (297,158) (87,051)

Loss / recovery of assets (274,802) -

Other (198,984) -

(1,575,911) (336,863)

Gross value added 1,949,573 396,145

Retention

Depreciation and amortization (398,871) (70,378)

Net value added 1,550,702 325,767

Value added received in transfer

Equity pick-up in associates 4,255 -

Financial income 97,673 28,602

101,928 28,602

Value added to be distributed 1,652,630 354,369

Distribution of value added

Personnel 305,842 61,894

Direct remuneration 273,345 46,036

Benefits 17,366 12,822

FGTS 15,131 3,036

Taxes and contributions 291,800 136,567

Federal 243,383 98,618

State 38,769 14,908

City 9,648 23,041

Third party capital remuneration 1,057,599 63,213

Interest 848,298 51,712

Leasing 209,301 11,501

Equity capital remuneration (2,611) 92,695

Non-controlling interests 4,105 106

Retained earnings (6,716) 92,589

1,652,630 354,369

The notes are an integral part of these interim financial statements.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

16

1. Operations

Rumo Logística Operadora Multimodal S.A. ("The Company" or "Rumo"), is a publicly traded

company with its shares traded on the São Paulo stock exchange (“BM&FBOVESPA) under

the ticker RUMO3, and has its headquarters in the city of Santos, State of São Paulo, Brazil. The

Company is a direct subsidiary of Cosan Logística S.A. ("Cosan Logística") which owns 26.26%

of its capital, and its Parent Company is Cosan Ltd. ("CZZ"). On April 1, 2015 the Company

acquired full control over the capital of ALL - América Latina Logística S.A. ("ALL").

The Company is a service provider in the logistics sector (transport and elevation), principally for

export commodities, providing an integrated transport solution, handling, storage and shipment

from the production centers to the main southern and southeast ports, and also holds interests in

other companies, ventures and consortia related to infrastructure.

The Company also operates in the rail transportation segment in Southern Brazil through its

subsidiary ALL - América Latina Logística Malha Sul S.A. ("ALL Malha Sul"), and the Central

West region and State of São Paulo through subsidiaries ALL - América Latina Logística Malha

Paulista S.A. ("ALL Malha Paulista"), ALL - America Latina Logística Malha Norte S.A. ("ALL

Malha Norte") and ALL - América Latina Logística Malha Oeste S.A. ("ALL Malha Oeste"). In

addition, the subsidiary Brado Logística e Participações S.A. ("Brado") operates in the container

segment.

Additionally, the Company has terminals for transshipment and terminals for export of sugar and

grains at the Port of Santos.

On September 30, 2015, the Company had a negative consolidated working capital of R$

1,735,145. On the other hand, it generated consolidated operating cash flows of R$ 1,098,547 and

made investments in modernizing its rolling stock and improving the railway network in the

amount of R$ 890,184, in line with its business plan. Management has been working on measures

that will enable the Company to present a balanced structure of debt, in order to fully meet its

business plan. Thus, management believes the use of the going concern assumption in the

preparation of these interim financial statements is appropriate.

a) ALL Acquisition

On May 8, 2014, the shareholders approved at the Extraordinary General Meeting the

acquisition of ALL’s shares by the Company, effectively suspended until obtaining the approval

of the Merger of Shares by Conselho Administrativo de Defesa Econômica ("CADE"), by

Agência Nacional de Transportes Terrestres ("ANTT") as well as from any other public

administration bodies from which prior authorizations are necessary and verification (or waiver

by the applicable part) of any other conditions precedent set forth in the proposal sent by the

Company to ALL on 24 February, 2014, to the effectiveness of the acquisition.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

17

On February 11, 2015, in response to the provisions of article 2 of CVM Instruction 358/2002,

the Company announced the unanimous approval by CADE, pursuant to art. 61 of Law No.

12,529 / 2011, the concentration acts on the merger of ALL shares issued by the Company upon

the conclusion of an Agreement in concentration control ("ACC").

As required by ACC, the new company started to adopt certain behaviors aimed to eliminate the

competition concerns identified in the opinion of the General Superintendence of the CADE.

These behavioral obligations remain in force for a period of seven (7) years (from the publication

of its approval in the Diário Oficial da União) and are meant primarily to ensure isonomic

attendance by the users of railway services charges, primarily through strengthening the

governance rules, the adoption of transparent mechanisms in pricing parameters, service

attendance control and limitation of the use of rail transport by related parties.

On March 19, 2015 Agência Nacional de Transportes Aquaviários ("ANTAQ") approved the

change of control, which was the last condition precedent to the effectiveness of the merger.

On March 23, 2015 ALL's Board of Directors approved the merger, and from April 1, 2015, the

Company's shares, already reflecting the effects of the Share Exchange, began trading on the

BM&FBOVESPA. As a result of this process the ALL's shares (Bovespa: ALLL3) ceased to be

traded on the BM&FBOVESPA on March 31, 2015. As a result, on April 1, 2015, ALL has

become a wholly owned subsidiary of the Company.

The accounting effects of the acquisition of ALL are presented in note 3 and the financial position

and consolidated results of operations for the periods subsequent to the acquisition are not

necessarily comparable with information presented in prior periods.

b) The concession of railway operation and port terminal

The Company holds, through subsidiaries or affiliates, concessions of railway services and port

terminals, whose scope and completion are as follows:

Companies Concession end Coverage area

Subsidiaries

Terminais Portuários Rumo e Teaçú December 2036 Port of Santos-SP

ALL Malha Sul February 2027 Southern Brazil and Sao Paulo State

ALL Malha Paulista December 2028 Sao Paulo State

ALL Malha Oeste June 2026 Midwest and State of São Paulo

ALL Malha Norte May 2079 Midwest and State of São Paulo

Portofer June 2025 Port of Santos-SP

Associates

Terminal XXXIX October 2025 Port of Santos-SP

TGG - Terminal de Granéis do Guarujá August 2027 Port of Santos-SP

Termag - Terminal Marítimo de Guarujá August 2027 Port of Santos-SP

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

18

The subsidiaries and associates above are subject to compliance with certain conditions set out in

the privatization bids and the concession contracts for railway networks and port terminals.

The concession agreements of these subsidiaries and associates shall be terminated by: expiration

of the contractual term; expropriation; forfeiture; termination; annulment and bankruptcy; or

termination of the dealership.

In the event of the termination of any of the concessions, the main effects would be as follows:

Return to the government all the rights and privileges transferred to the subsidiaries,

together with leased assets and those resulting from investments that are considered

reversible by the Federal Government as being necessary to the continuous provision of

the granted service.

The reversible assets would be indemnified by the Federal Government at the residual

cost, calculated based on the accounting records of the subsidiaries, considering

depreciation; such costs would be subject to technical and financial analysis by the

Federal Government. Any and all improvements made to the permanent track

superstructure would not be considered as investments for indemnification purposes.

c) Liquidity rights exercised at Brado

On June 3, 2015 the Company, through its direct subsidiary ALL, informed that Brado’s non-

controlling shareholders exercised their liquidity right provided in the shareholders’ agreement,

which enables the exit of Brado’s original shareholders via a share exchange. As a result, the

Company and the Brado’s original shareholders prepared appraisal reports, based on the

economic value of the companies, to establish an exchange ratio, which has not yet been

concluded.

2. Presentation of interim financial statements and significant accounting policies

2.1. Basis of preparation

The interim financial statements have been prepared in accordance with CPC 21 (R1) and IAS 34

- Interim Financial Reporting issued by the International Accounting Standards Board (IASB),

and presented in accordance with the standards issued by the Brazilian Securities and Exchange

Commission (CVM) applicable to the Quarterly Information (ITR) and do not include all of the

information required in complete, annual financial statements.

These interim financial statements were prepared following the basis of preparation and

accounting policies consistent with those adopted in preparing the financial statements as of

December 31, 2014 and should be read together. New applicable accounting policies due to the

acquisition of ALL are described below. The notes that have not changed significantly or had

irrelevant changes compared to December 31, 2014 were not repeated in full in these interim

financial statements.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

19

However, selected information has been included to explain the main events and transactions that

occurred to enable the understanding of changes in financial position and performance of

operations since the issuance of the annual financial statements for the year ended December 31,

2014.

In preparing these interim financial statements, management used judgments, estimates and

assumptions that affect the application of the Company's accounting policies and the reported

amounts of assets, liabilities, income and expenses. Actual results may differ from these

estimates. Estimates and assumptions are reviewed on an ongoing basis and have not changed in

relation to the financial statements of December 31, 2014.

The presentation of the Statement of Value Added (“DVA”) is required by Brazilian corporate

law and the accounting practices adopted in Brazil applicable to publicly traded companies. IFRS

does not require the presentation of such statement. As a result, under IFRS, such statement is

presented as supplementary information.

On November 5, 2015, the Company’s management approved and authorized the issuance of

these interim financial statements.

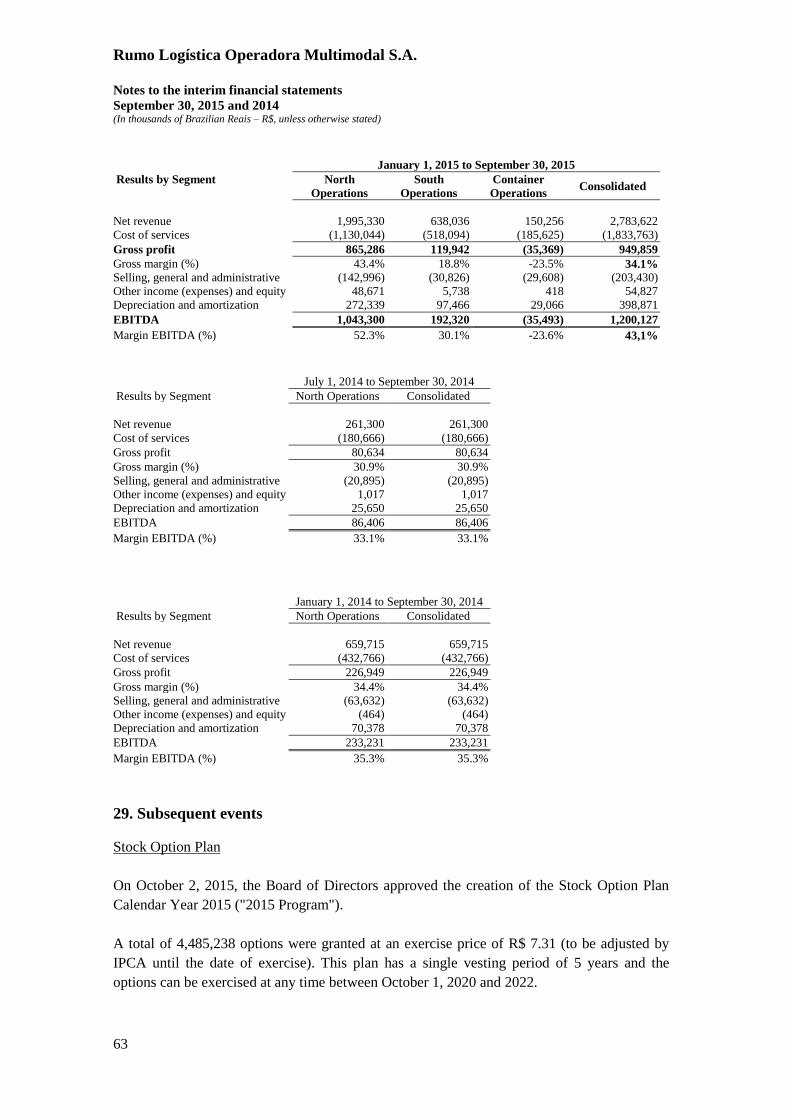

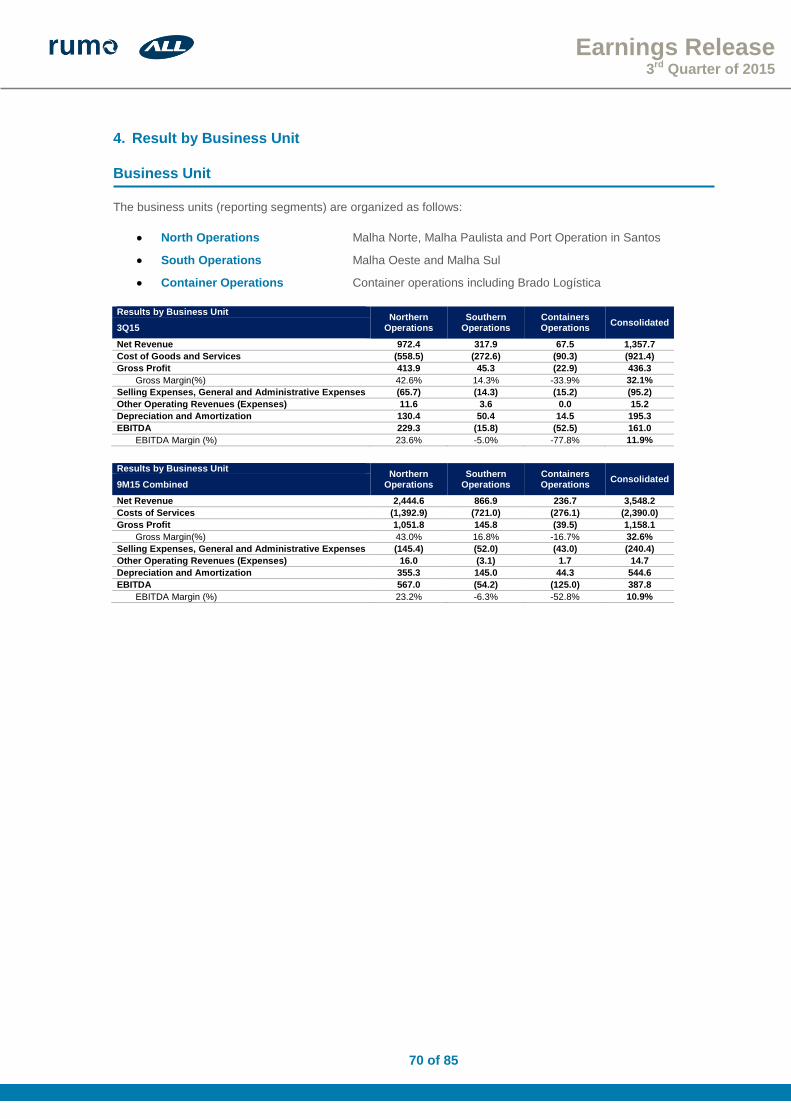

Presentation of segment information

Operating segment information is presented consistently with the internal reporting provided to

the chief operating decision maker. The chief operating decision maker, responsible for allocating

resources and assessing performance of the operating segments is the Executive Board, also

responsible for making the strategic decisions of the Company and its subsidiaries.

With the acquisition of ALL, management initiated an internal restructuring that led to the

creation of two vice-presidencies, the first focused on South operations (comprised of railway and

transshipment in the concession area of ALL Malha Sul and ALL Malha Oeste) and the second

focused on the North Operations (composed by railway operations, transshipment and port

elevation in the areas of the Company's concession, ALL Malha Norte and ALL Malha Paulista).

A third segment includes Brado, the Company's indirect subsidiary focused on container

operations and the container operations of other group companies. Therefore, the Company now

discloses three segments: (i) North Operations, (ii) South Operations, and (iii) Container

Operations.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

20

2.2. Basis of consolidation

The consolidated interim financial statements include the financial statements of the Company

and its subsidiaries, listed below:

Directly and indirectly controlled

September 30, 2015 December 31, 2014

Subsidiaries

Direct

Logispot Armazéns Gerais S.A. 51.00% 51.00%

Rumo Um S.A. - 100.00%

Rumo Dois S.A. - 100.00%

ALL – América Latina Logística S.A. 100.00% -

Indirect

ALL Intermodal S.A. 100.00% - ALL Malha Oeste S.A. 100.00% - ALL Malha Paulista S.A. 100.00% - ALL Malha Sul S.A. 100.00% - ALL Malha Norte S.A. 99.24% - ALL Participações S.A. 100.00% - ALL Armazéns Gerais Ltda. 100.00% - Portofer Ltda. 100.00% - Boswells S.A. 100.00% - Brado Holding S.A. 100.00% - Brado Logística e Participações S.A. 62.22% - Brado Logística S.A. 62.22% - Tezza Consultoria de Negócios Ltda. 99.99% - ALL Equipamentos Ltda. 99.99% - ALL Argentina S.A. 90.96% - ALL Mesopotâmica S.A. 70.56% -

ALL Central S.A. 73.55% -

Paranaguá S.A. 99.83% - ALL Rail Management Ltda. 50.01% - PGT S.A. 100.00% -

Associates (Equity)

Rhall Terminais Ltda. 30.00% -

Termag S.A. 19.85% -

TGG S.A. 9.92% -

Terminal XXXIX S.A. 49.62% -

2.3. Hedge

The Company entered into bilateral loans denominated in US Dollars through Resolution

4,131/62 denominated in US$ equivalent to R$ 409,271. The currency exposure in US$ of these

operations was protected with SWAP transactions exchanging indexes and eliminating the risk of

currency fluctuations. The fair value changes of the contracted derivative are recognized through

profit or loss.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

21

The Company has designated these loan agreements as liabilities measured at fair value through

profit or loss in order to eliminate or at least significantly reduce the measurement inconsistency

that would otherwise arise from measurement and recognition of gains and losses on loans and

derivatives on different bases. As a result, the fair value fluctuations on these loans are recognized

through profit or loss.

2.4. Business combination

Business combinations are recognized using the acquisition method. The transferred

consideration for the acquisition is generally measured at fair value, as well as the identifiable net

assets acquired and liabilities assumed. Any resulting goodwill is tested annually for impairment.

Transaction costs are charged to income as incurred, except costs related to the issuance of debt

instruments or equity.

The consideration transferred does not include amounts related to pre-existing relationships

payments. These amounts are generally recognized in the income statement.

2.5. Non-current assets held for sale and discontinued operations

The Company classifies non-current assets as held for sale if their carrying amounts are

recoverable mainly through sale rather than through continued use. Non-current assets classified

as held for sale are measured at the lower of their carrying amount and fair value less selling

costs.

Classification criteria as held for sale are considered met only when the sale is highly probable

and the asset is available for immediate sale. Management must be committed to the completion

of the sale within one year from the date of classification.

Discontinued operations are excluded from the results from continuing operations and are

presented as a single line item in the income statement.

Additional disclosures are presented in note 26. All other notes to the financial statements include

amounts for continuing operations, unless otherwise stated.

2.6. Deferred income

Substantially comprised of amounts received from clients for investment in fixed assets in return

of a rail service contract requiring future performance of services by the Company.

2.7. New standards and interpretations not yet adopted

The following new standards and interpretations were issued by the IASB but are not effective for

the year 2015. Early adoption of standards, although encouraged by the IASB, is not permitted in

Brazil by the Brazilian Accounting Pronouncements Committee (CPC), which has not yet issued

its version of these standards.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

22

IFRS 9 - "Financial instruments" addresses the classification, measurement and recognition of

financial assets and liabilities. The full version of IFRS 9 was published in July 2014, effective as

of January 1, 2018. Management is evaluating the full impact of its adoption.

IFRS 15 - "Contract Revenue from Customers" - This new standard provides the principles that

an entity applies to determine the measurement of revenue and when it is recognized. It is

effective on January 1, 2018 and supersedes IAS 11 - "Construction Contracts", IAS 18 -

"Income" and their related interpretations. Management is evaluating the impact of its adoption.

There are no other IFRS or IFRIC interpretations that are not yet effective and that are expected

to have a significant impact on the Company.

2.8. Cash flow – non cash transactions

During the nine-month period ended September 30, 2015, the Company made the following non

cash transactions that are not reflected in the statement of consolidated cash flows:

Acquisition of net assets of ALL in the amount of R$ 2,567,669 through the issuance of

equity instruments, except for the cash acquired in the transaction of R$ 169,703 (Note

3).

Finance lease of locomotives and rail cars in the amount of R$ 262,759.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

23

3. Business combination

As described in note 1, on April 1, 2015, after the necessary approvals of the competent bodies,

the Company acquired 100% of the common shares of ALL and through the shareholders'

agreement, obtained its control and consolidated its results.

The acquisition took place by an exchange of shares, with the issuance by the Company of

1,963,670,770 registered common shares with no par value, representing 65.67% of its equity in

exchange for 100% of the share capital of ALL, represented by 681,995,165 common shares.

As a result of the acquisition, the Company consolidates its participation strategy in the logistics

and infrastructure business in Brazil, by adding approximately 12,000 km of existing rail tracks in

ALL concessions.

a) Consideration transferred

As a basis for measuring the fair value of the consideration transferred, the share price of ALL

("ALLL3") on the BM&FBOVESPA at the close of business on March 31, 2015 was used, at the

price of R$ 3.97 per share. Additionally, the value was adjusted for the settlement of pre-existing

relationship, as follows:

Acquired common shares (681,995,165) at R$ 3.97 2,707,534

Pre-existing relationship settlement 29,838

Total consideration transferred 2,737,372

Settlement of pre-existing relationship

In March 2009, the Company and ALL signed an operating agreement (pre-existing relationship)

for the supply of sugar and other grains transportation logistics from the western state of São

Paulo to the Port of Santos, in which the Company has port concessions for elevation services.

According to the terms of the existing agreement, the Company invested in the construction and

improvement of permanent tracks under concession of ALL and acquired rolling stock for use in

the transport of products in ALL’s rail network, in order to increase ALL’s rail freight transport

capacity. In exchange for the Company's investments, the agreement stipulated that ALL would

provide a certain capacity of rail transport services, as well as compensate the Company through

the payment of a contractually fixed fee per ton of product transported by ALL using the rail

network and / or by the use of the rolling stock provided by the Company to ALL.

This preexisting relationship was settled when the Company acquired ALL. The Company

recognized a gain of R$ 29,838 as a result of this settlement and this amount was recognized in

the income statement as "other operating income".

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

24

The fair value measurement of the pre-existing relationship was based on the difference between

the value of the investment made by the Company and the discounted cash flow return on this

investment, considering the contractually agreed volume and rate.

b) Identifiable assets acquired and liabilities assumed

The preliminary fair value of assets acquired and liabilities assumed is as follows: Fair value of identifiable assets acquired and liabilities assumed

Cash and cash equivalents 169,703

Marketable securities 940,689

Accounts receivable 385,367

Inventories 84,326

Other assets 1,617,232

Property and plant 7,225,047

Intangible assets 7,500,080

Loans and financing (3,782,919)

Debentures (2,856,304)

Finance lease (1,857,947)

Real estate credit certificates (340,255)

Suppliers payable (890,153)

Lease and concession (1,974,280)

Provision for judicial demands (553,094)

Other liabilities (1,563,425)

Deferred income and social contribution taxes (1,125,795)

Non-controlling interest (240,900)

Total net identifiable assets 2,737,372

Measurement of fair values

In measuring fair values management used valuation techniques considering market prices for

similar items, replacement costs, discounted cash flow, among others.

Since this is a preliminary measure of fair value, if new information obtained within one year

from the date of purchase, on facts and circumstances that existed at the acquisition date, indicate

adjustments to the amounts mentioned above, or any additional liability that existed at the

acquisition date, the purchase price allocation will be revised.

The Company has elected to measure the non-controlling interest on Brado – indirect subsidiary

controlled by ALL - based on the proportionate interest in the recognized amount of fair value of

identifiable net assets of Brado.

Accounts receivable fair value of R$ 385,367 is net of an allowance of R$ 51,495.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

25

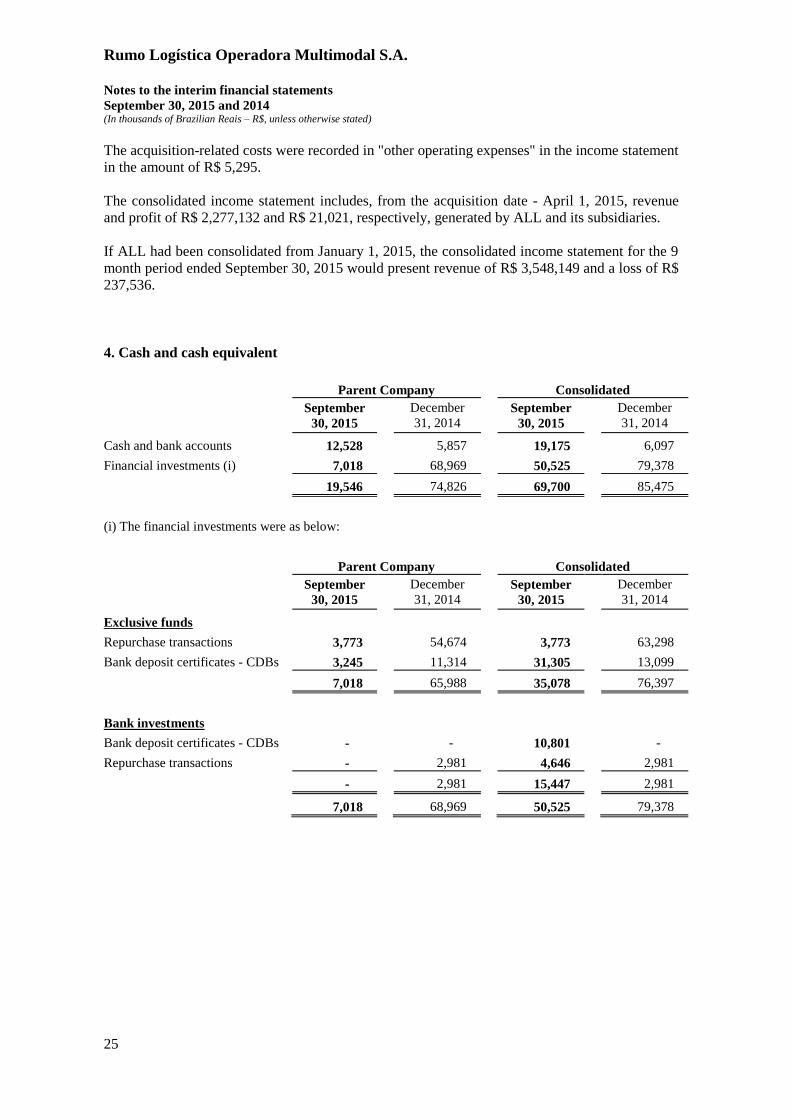

The acquisition-related costs were recorded in "other operating expenses" in the income statement

in the amount of R$ 5,295.

The consolidated income statement includes, from the acquisition date - April 1, 2015, revenue

and profit of R$ 2,277,132 and R$ 21,021, respectively, generated by ALL and its subsidiaries.

If ALL had been consolidated from January 1, 2015, the consolidated income statement for the 9

month period ended September 30, 2015 would present revenue of R$ 3,548,149 and a loss of R$

237,536.

4. Cash and cash equivalent

Parent Company Consolidated

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Cash and bank accounts 12,528 5,857 19,175 6,097

Financial investments (i) 7,018 68,969 50,525 79,378

19,546 74,826 69,700 85,475

(i) The financial investments were as below:

Parent Company Consolidated

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Exclusive funds

Repurchase transactions 3,773 54,674 3,773 63,298

Bank deposit certificates - CDBs 3,245 11,314 31,305 13,099

7,018 65,988 35,078 76,397

Bank investments

Bank deposit certificates - CDBs - - 10,801 -

Repurchase transactions - 2,981 4,646 2,981

- 2,981 15,447 2,981

7,018 68,969 50,525 79,378

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

26

5. Marketable securities

Consolidated

September 30,

2015

December 31,

2014

Current assets

CDB investments linked to BNDES loans 196,059 -

Government bonds 682,968 -

879,027 -

6. Accounts receivable

Parent Company Consolidated

September 30,

2015

December 31,

2014

September 30,

2015

December 31,

2014

Domestic and foreign 31,806 509,421 238,023 511,500

Allowance for doubtful

accounts (1,115) (22,065) (29,765) (22,122)

30,691 487,356 208,258 489,378

Current 30,691 40,663 185,610 42,685

Non-current - 446,693 22,648 446,693

The reduction in the consolidated balance refers mainly to the elimination of accounts receivable from ALL due to its

consolidation with the acquisition of control on April 1, 2015. Regarding the Parent Company, balances receivable

from ALL were reclassified to related parties.

7. Other recoverable taxes Parent Company Consolidated

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Contribution to social security financing

(“COFINS”) 7,469 - 238,383 -

Social integration program (“PIS”) 1,625 - 71,303 -

Tax on circulation of goods, transport services

and communication (“ICMS”) (i) - - 217,062 -

ICMS - CIAP (ii) - - 222,569 -

Other - - 13,614 -

9,094 - 762,931 -

Current 9,094 - 234,437 -

Non-current - - 528,494 -

(i) ICMS credit on the acquisition of inputs and diesel used in transport services.

(ii) ICMS credit arising from acquisitions of fixed assets.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

27

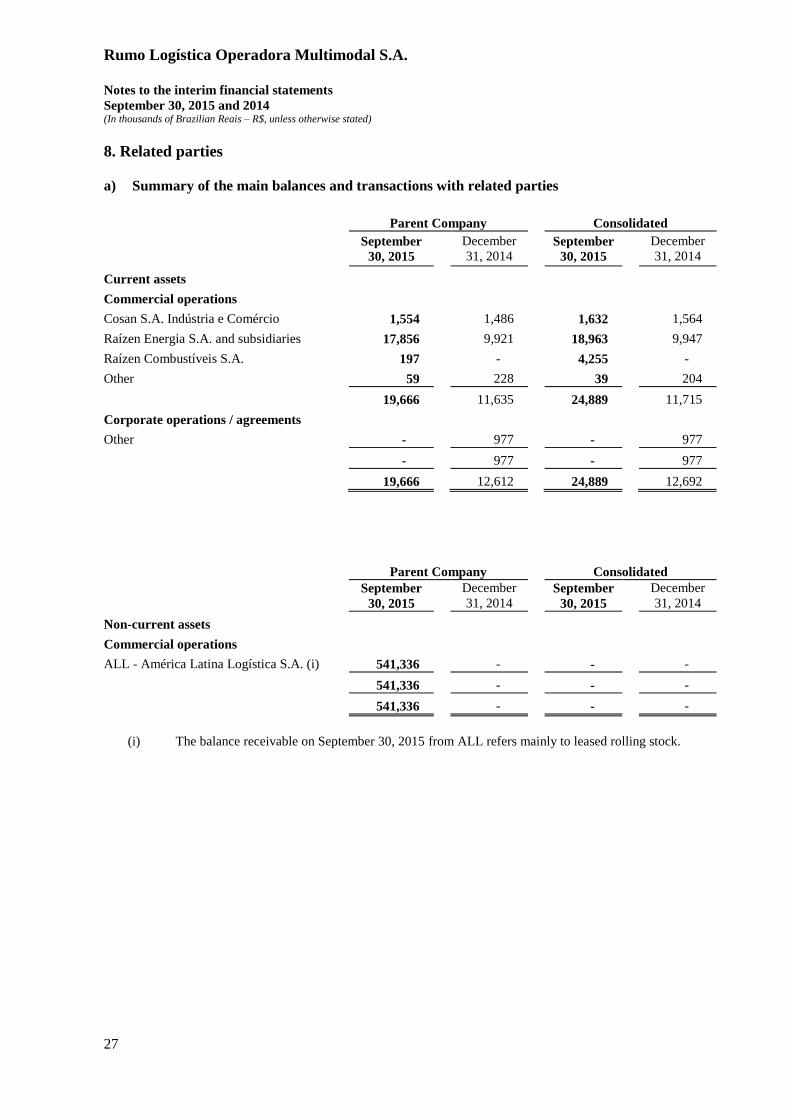

8. Related parties

a) Summary of the main balances and transactions with related parties

Parent Company Consolidated

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Current assets

Commercial operations

Cosan S.A. Indústria e Comércio 1,554 1,486 1,632 1,564

Raízen Energia S.A. and subsidiaries 17,856 9,921 18,963 9,947

Raízen Combustíveis S.A. 197 - 4,255 -

Other 59 228 39 204

19,666 11,635 24,889 11,715

Corporate operations / agreements

Other - 977 - 977

- 977 - 977

19,666 12,612 24,889 12,692

Parent Company Consolidated

September

30, 2015

December

31, 2014 September

30, 2015

December

31, 2014

Non-current assets

Commercial operations

ALL - América Latina Logística S.A. (i) 541,336 - - -

541,336 - - -

541,336 - - -

(i) The balance receivable on September 30, 2015 from ALL refers mainly to leased rolling stock.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

28

Parent Company Consolidated

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Current liabilities

Commercial operations

Cosan S.A. Indústria e Comércio 5,049 3,342 5,049 3,342

ALL - América Latina Logística S.A. (i) 134,791 - - -

Raízen Energia S.A. and subsidiaries 12,116 16,441 12,406 16,542

Cosan Lubrificantes e Especialidades S.A. 377 363 4,983 363

Raízen Combustíveis S.A. (ii) 1 - 62,618 -

Logispot Armazéns Gerais S.A. 1,110 - - -

Other - 918 - 45

153,444 21,064 85,056 20,292

(i) The balance payable on September 30, 2015 to ALL refers to rail transport services provided.

(ii) The balance payable on September 30, 2015 to Raízen Combustíveis refers to purchases of fuel.

b) Summary of transactions with related parties

Parent Company

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1,

2014 to

September

30, 2014

January 1,

2014 to

September

30, 2014

Services

Raízen Energia S.A. and subsidiaries (i) 98,094 224,140 75,037 208,899

ALL - América Latina Logística S.A. 67,441 110,578 - -

Other - - 315 1,387

165,535 334,718 75,352 210,286

Shared expenses

Cosan S.A. Indústria e Comércio (3,908) (6,621) (2,440) (7,221)

Raízen Energia S.A. (1,229) (3,571) (1,090) (3,869)

(5,137) (10,192) (3,530) (11,090)

Purchases

Raízen Combustíveis S.A. - (12) (11) (729)

Logispot Armazéns Gerais S.A. (1,572) (6,444) (4,861) (10,650)

ALL - América Latina Logística S.A. (59,342) (63,318) - -

Brado Logística S.A - (14,682) - -

Cosan Cayman Finance Lim (3) (3) - -

Cosan Lubrificantes e Especialidades (51) (154) - -

(60,968) (84,613) (4,872) (11,379)

Financial result

Rezende Barbosa S.A. Administração e

Participações - 10 85 378

Other - (9) 15 15

- 1 100 393

(i) The balances in the three- and nine-month periods ended September 30, 2015 with Raizen Energia and its

subsidiaries refer mainly to transport storage and port elevation services.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

29

Consolidated

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1,

2014 to

September

30, 2014

January 1,

2014 to

September

30, 2014

Services

Raízen Energia S.A. and subsidiaries (i) 99,658 229,998 77,617 211,478

Raízen Combustíveis S.A. (ii) 28,155 55,518 - -

Other - - 315 1,387

127,813 285,516 77,932 212,865

Shared expenses

Cosan S.A. Indústria e Comércio (3,908) (6,621) (2,440) (7,221)

Raízen Energia S.A. (2,313) (4,857) (1,189) (4,190)

(6,221) (11,478) (3,629) (11,411)

Purchases

Raízen Combustíveis S.A. (iii) (200,570) (202,334) (11) (729)

Cosan Cayman Finance Lim (3) (3) - -

Cosan Lubrificantes e Especialidades (11,793) (20,546) - -

(212,366) (222,883) (11) (729)

Financial result

Rezende Barbosa S.A. Administração e

Participações - 10 85 378

Raízen Energia S.A. (9) (9) - -

Outros - - 15 15

(9) 1 100 393

(i) The balances in the three- and nine-month periods ended September 30, 2015 with Raizen Energia and its

subsidiaries refer mainly to transport, storage and port elevation services.

(ii) The balances in the three-and nine-month periods ended September 30, 2015 with Raizen Combustíveis refer

to fuel transportation services.

(iii) The balances in the three- and nine-month periods ended September 30, 2015 with Raizen Combustíveis

refer to acquisition of fuel.

Officers and directors remuneration

Fixed and variable remuneration of the statutory officers, board of directors and fiscal board

amounts to R$ 5,546 during the nine-month period ended September 30, 2015 (2014: R$ 2,282),

and the entire amount is classified as short-term benefits.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

30

9. Equity method investments (Parent Company)

Direct

subsidiaries

Total

shares of

the investee

Shares held

by the

Company

Percentage

of interest

(%)

Balance at

December

31, 2014

Equity

pick-up

Business

Combination

Capital

increase

Comprehensive

income Other

Balance at

September

30, 2015

Logispot

Armazéns

Gerais S.A.

("Logispot") 2,040,816 1,040,816 51% 76,108 (650) - - - - 75,458

ALL 681,995,165 681,995,165 100% - 20,869 2,707,534 1,320,111 3,738 - 4,052,252

Rumo Um

S.A. - - - 5 - - - - (5) -

Rumo Dois

S.A. - - - 5 - - - - (5) -

76,118 20,219 2,707,534 1,320,111 3,738 (10) 4,127,710

(Consolidated)

Indirect associates

Total

shares of

the

investee

Shares

held by

the

Company

Percentage

of interest

(%)

Balance at

December

31, 2014

Equity

pick-

up

Business

combination Other

Balance at

September

30, 2015

Rhall Terminais 28,580 8,574 30.00% - 122 3,492 - 3,614

Termag S.A. 500,000 99,246 19.85% - (1,732) 6,175 - 4,443

TGG S.A. 79,747,000 7,914,609 9.92% - 3,256 16,275 - 19,531

Terminal XXXIX 200,000 99,246 49.62% - 2,609 15,343 (250) 17,702

- 4,255 41,285 (250) 45,290

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

31

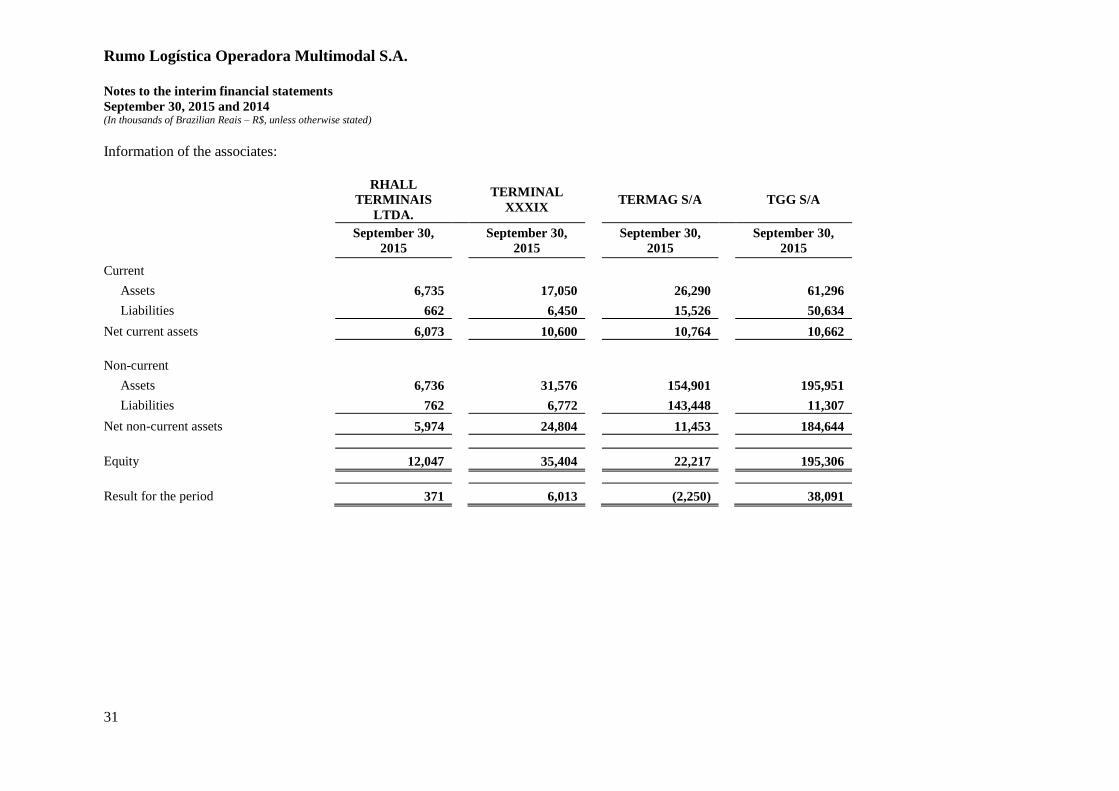

Information of the associates:

RHALL

TERMINAIS

LTDA.

TERMINAL

XXXIX

TERMAG S/A TGG S/A

September 30,

2015

September 30,

2015

September 30,

2015

September 30,

2015

Current

Assets 6,735 17,050 26,290 61,296

Liabilities 662 6,450 15,526 50,634

Net current assets 6,073 10,600 10,764 10,662

Non-current

Assets 6,736 31,576 154,901 195,951

Liabilities 762 6,772 143,448 11,307

Net non-current assets 5,974 24,804 11,453 184,644

Equity 12,047 35,404 22,217 195,306

Result for the period 371 6,013 (2,250) 38,091

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

32

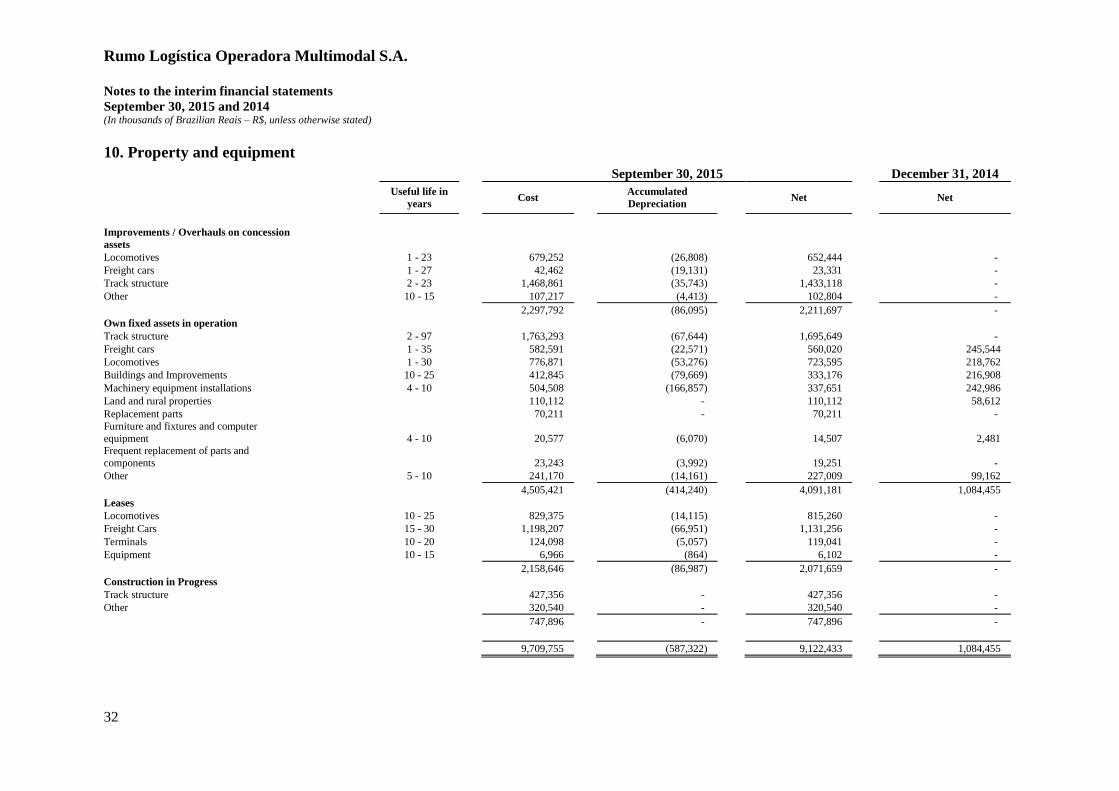

10. Property and equipment

September 30, 2015 December 31, 2014

Useful life in

years Cost

Accumulated

Depreciation Net Net

Improvements / Overhauls on concession

assets

Locomotives 1 - 23 679,252 (26,808) 652,444 -

Freight cars 1 - 27 42,462 (19,131) 23,331 -

Track structure 2 - 23 1,468,861 (35,743) 1,433,118 -

Other 10 - 15 107,217 (4,413) 102,804 -

2,297,792 (86,095) 2,211,697 -

Own fixed assets in operation

Track structure 2 - 97 1,763,293 (67,644) 1,695,649 -

Freight cars 1 - 35 582,591 (22,571) 560,020 245,544

Locomotives 1 - 30 776,871 (53,276) 723,595 218,762

Buildings and Improvements 10 - 25 412,845 (79,669) 333,176 216,908

Machinery equipment installations 4 - 10 504,508 (166,857) 337,651 242,986

Land and rural properties 110,112 - 110,112 58,612

Replacement parts 70,211 - 70,211 -

Furniture and fixtures and computer

equipment 4 - 10 20,577 (6,070) 14,507 2,481 Frequent replacement of parts and

components 23,243 (3,992) 19,251 -

Other 5 - 10 241,170 (14,161) 227,009 99,162

4,505,421 (414,240) 4,091,181 1,084,455

Leases

Locomotives 10 - 25 829,375 (14,115) 815,260 -

Freight Cars 15 - 30 1,198,207 (66,951) 1,131,256 -

Terminals 10 - 20 124,098 (5,057) 119,041 -

Equipment 10 - 15 6,966 (864) 6,102 -

2,158,646 (86,987) 2,071,659 -

Construction in Progress

Track structure 427,356 - 427,356 -

Other 320,540 - 320,540 -

747,896 - 747,896 -

9,709,755 (587,322) 9,122,433 1,084,455

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

33

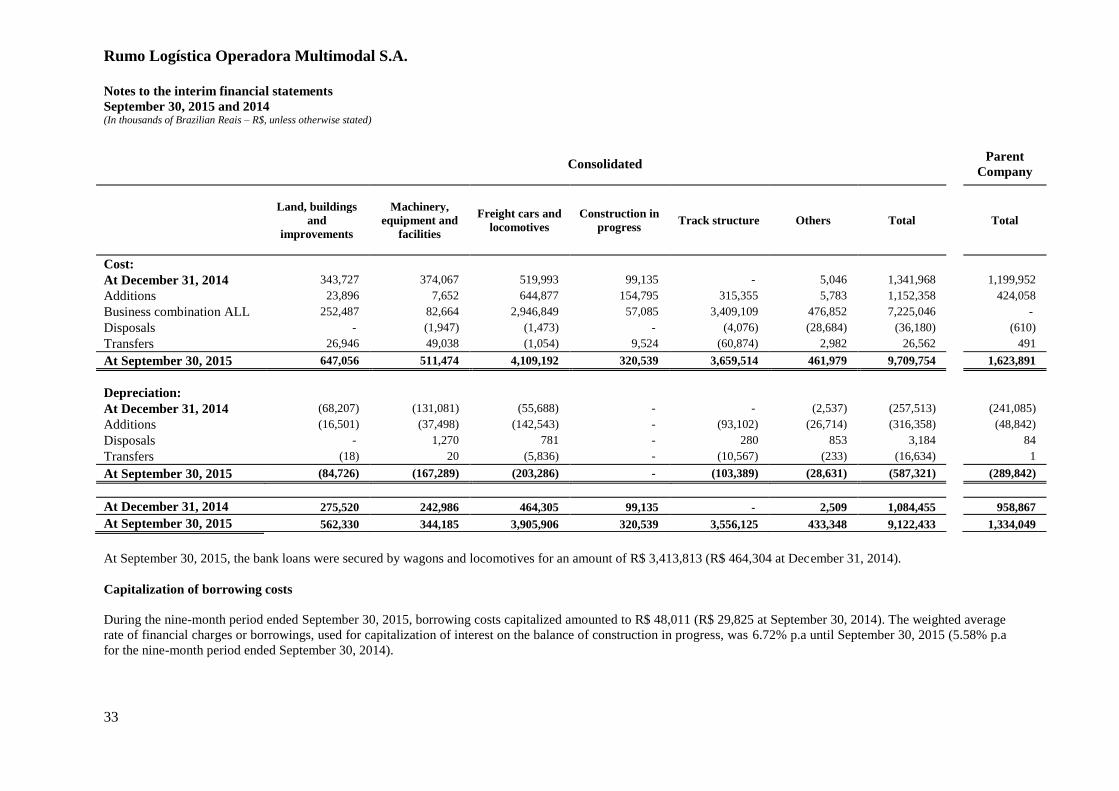

Consolidated

Parent

Company

Land, buildings

and

improvements

Machinery,

equipment and

facilities

Freight cars and

locomotives

Construction in

progress Track structure Others Total Total

Cost:

At December 31, 2014 343,727 374,067 519,993 99,135 - 5,046 1,341,968 1,199,952

Additions 23,896 7,652 644,877 154,795 315,355 5,783 1,152,358 424,058

Business combination ALL 252,487 82,664 2,946,849 57,085 3,409,109 476,852 7,225,046 -

Disposals - (1,947) (1,473) - (4,076) (28,684) (36,180) (610)

Transfers 26,946 49,038 (1,054) 9,524 (60,874) 2,982 26,562 491

At September 30, 2015 647,056 511,474 4,109,192 320,539 3,659,514 461,979 9,709,754 1,623,891

Depreciation:

At December 31, 2014 (68,207) (131,081) (55,688) - - (2,537) (257,513) (241,085)

Additions (16,501) (37,498) (142,543) - (93,102) (26,714) (316,358) (48,842)

Disposals - 1,270 781 - 280 853 3,184 84

Transfers (18) 20 (5,836) - (10,567) (233) (16,634) 1

At September 30, 2015 (84,726) (167,289) (203,286) - (103,389) (28,631) (587,321) (289,842)

At December 31, 2014 275,520 242,986 464,305 99,135 - 2,509 1,084,455 958,867

At September 30, 2015 562,330 344,185 3,905,906 320,539 3,556,125 433,348 9,122,433 1,334,049

At September 30, 2015, the bank loans were secured by wagons and locomotives for an amount of R$ 3,413,813 (R$ 464,304 at December 31, 2014).

Capitalization of borrowing costs

During the nine-month period ended September 30, 2015, borrowing costs capitalized amounted to R$ 48,011 (R$ 29,825 at September 30, 2014). The weighted average

rate of financial charges or borrowings, used for capitalization of interest on the balance of construction in progress, was 6.72% p.a until September 30, 2015 (5.58% p.a

for the nine-month period ended September 30, 2014).

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

34

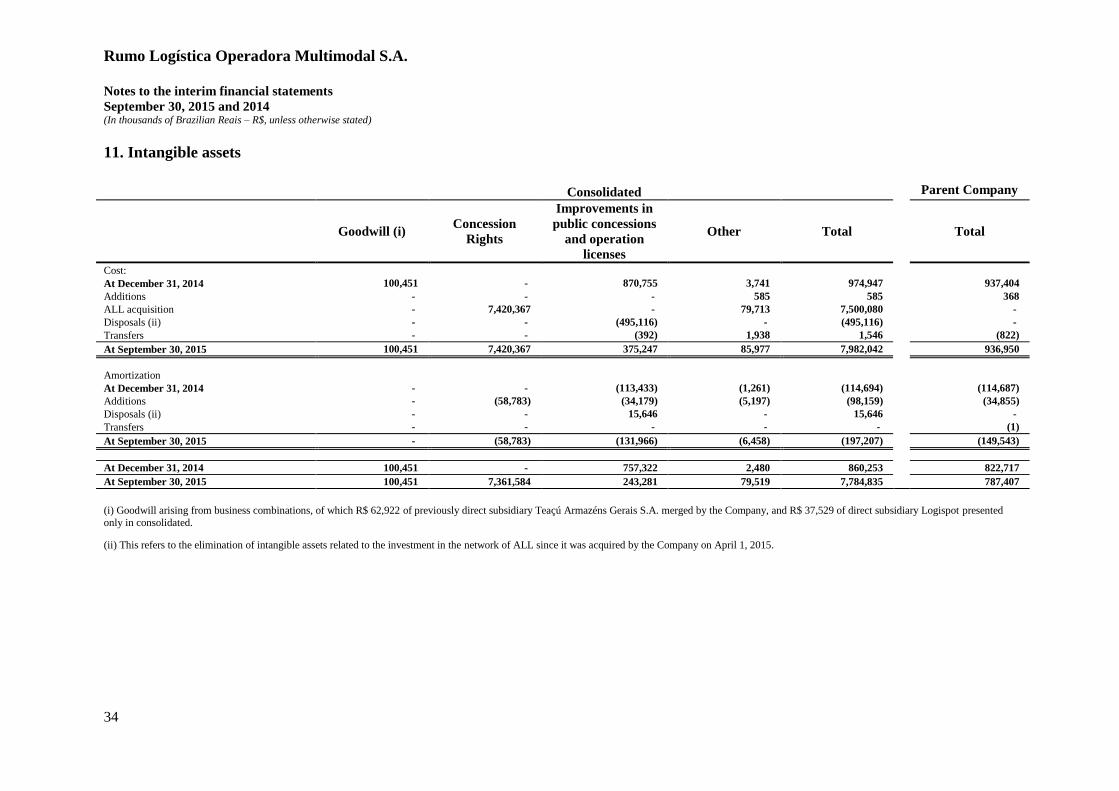

11. Intangible assets

Consolidated Parent Company

Goodwill (i) Concession

Rights

Improvements in

public concessions

and operation

licenses

Other Total Total

Cost:

At December 31, 2014 100,451 - 870,755 3,741 974,947 937,404

Additions - - - 585 585 368

ALL acquisition - 7,420,367 - 79,713 7,500,080 -

Disposals (ii) - - (495,116) - (495,116) -

Transfers - - (392) 1,938 1,546 (822)

At September 30, 2015 100,451 7,420,367 375,247 85,977 7,982,042 936,950

Amortization

At December 31, 2014 - - (113,433) (1,261) (114,694) (114,687)

Additions - (58,783) (34,179) (5,197) (98,159) (34,855)

Disposals (ii) - - 15,646 - 15,646 -

Transfers - - - - - (1)

At September 30, 2015 - (58,783) (131,966) (6,458) (197,207) (149,543)

At December 31, 2014 100,451 - 757,322 2,480 860,253 822,717

At September 30, 2015 100,451 7,361,584 243,281 79,519 7,784,835 787,407

(i) Goodwill arising from business combinations, of which R$ 62,922 of previously direct subsidiary Teaçú Armazéns Gerais S.A. merged by the Company, and R$ 37,529 of direct subsidiary Logispot presented

only in consolidated.

(ii) This refers to the elimination of intangible assets related to the investment in the network of ALL since it was acquired by the Company on April 1, 2015.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

35

Intangibles (other than goodwill) Annual rate of

amortization September 30, 2015 December 31, 2014

Software (a) 20% 14,623 2,480

Operating license and customer base (b) 3.7% 243,281 250,825

Right of way on public concessions (c ) 5.93% - 506,497

Public concession rights (d) 1.56% 7,361,584 -

Other 64,896 -

Total 7,684,384 759,802

a) Refers mainly to the business management system - ERP of the Company

b) Port operation license and relationships with the Company's customers, from the Teaçú business combination.

c) Refers to the improvements made to the railways under concession and operated by ALL until March 31, 2015, when ALL was acquired by the Company.

d) Refers to the concession rights acquired, allocated to Malha Norte concession upon the business combination of ALL, which will be amortized the term of this concession

by 2079.

The Company annually tests the recoverable amount of goodwill arising from expected future results of business combinations. The assets subject to

depreciation and amortization are tested only if there are indicators that the carrying amount is not recoverable.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

36

12. Loans and borrowings

Financial charges (a) Parent Company Consolidated

Description Index Average

interest

rate

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Maturity

date

Finame Pré-fixed 4.27% 504,125 305,218 843,788 307,005 2025

Long-term

interest rate

reference

unit(“URTJ

LP”)

8.47%

432,846 457,570 433,112 457,570 2022

Finem Pré-fixed 4.02% - - 4,717 3,420 2024

URTJLP 8.25% - - 2,404,349 13,231 2029

Consumer

price index

(“IPCA”)

17.95%

- - 3,965 3,483 2021

SELIC 15.85% - - 5,984 - 2020

UMBNDES 10.16% - - 1,189 - 2022

FRN Dollar (US$) 2.63% 200,439 - 200,439 - 2017

Loan 4131 Dollar (US$) 3.13% 208,832 - 300,538 - 2017

Commercial

banks % of CDI 14.13% - - 1,450 - 2015

CDI +

spread 17.87% - - 304,711 - 2016

Pré-fixed 20.98% - - 4,860 - 2016

Debentures URTJLP 8,00% - - 2,539 - 2016

Non-

convertible

debentures % of CDI 15.26% - - 506,980 - 2018

Pré-fixed 10.1% - - 164,909 - 2020

% Net

revenue - - - 27,488 - 2016

CDI +

spread 16.16% 1,431,536 - 2,233,286 - 2018

FCO Pré-fixed 4.12% - - 3,010 - 2024

NCE Dollar (US$) 3.4% - - 127,800 - 2016

% of CDI 15.70% - - 736,588 - 2019

2,777,778 762,788 8,311,702 784,709

Current 181,511 125,893 1,398,905 127,425

Non-current 2,596,267 636,895 6,912,797 657,284

a) Financial charges at September 30, 2015, unless otherwise indicated.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

37

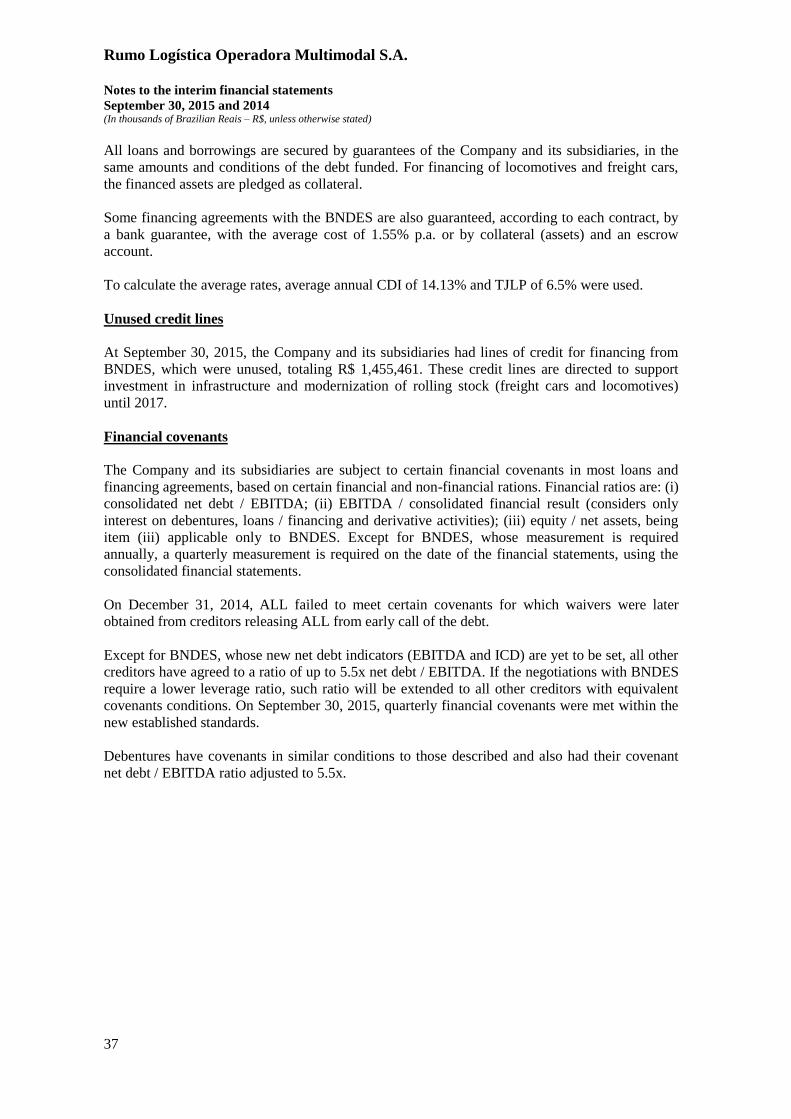

All loans and borrowings are secured by guarantees of the Company and its subsidiaries, in the

same amounts and conditions of the debt funded. For financing of locomotives and freight cars,

the financed assets are pledged as collateral.

Some financing agreements with the BNDES are also guaranteed, according to each contract, by

a bank guarantee, with the average cost of 1.55% p.a. or by collateral (assets) and an escrow

account.

To calculate the average rates, average annual CDI of 14.13% and TJLP of 6.5% were used.

Unused credit lines

At September 30, 2015, the Company and its subsidiaries had lines of credit for financing from

BNDES, which were unused, totaling R$ 1,455,461. These credit lines are directed to support

investment in infrastructure and modernization of rolling stock (freight cars and locomotives)

until 2017.

Financial covenants

The Company and its subsidiaries are subject to certain financial covenants in most loans and

financing agreements, based on certain financial and non-financial rations. Financial ratios are: (i)

consolidated net debt / EBITDA; (ii) EBITDA / consolidated financial result (considers only

interest on debentures, loans / financing and derivative activities); (iii) equity / net assets, being

item (iii) applicable only to BNDES. Except for BNDES, whose measurement is required

annually, a quarterly measurement is required on the date of the financial statements, using the

consolidated financial statements.

On December 31, 2014, ALL failed to meet certain covenants for which waivers were later

obtained from creditors releasing ALL from early call of the debt.

Except for BNDES, whose new net debt indicators (EBITDA and ICD) are yet to be set, all other

creditors have agreed to a ratio of up to 5.5x net debt / EBITDA. If the negotiations with BNDES

require a lower leverage ratio, such ratio will be extended to all other creditors with equivalent

covenants conditions. On September 30, 2015, quarterly financial covenants were met within the

new established standards.

Debentures have covenants in similar conditions to those described and also had their covenant

net debt / EBITDA ratio adjusted to 5.5x.

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

38

The installments on long-term, net of amortization of issuing costs have the following scheduled

maturities:

Parent Company Consolidated

September 30,

2015

December 31,

2014 September 30,

2015

December 31,

2014

13 to 24 months 561,268 136,234 1,429,839 140,050

25 to 36 months 1,555,033 136,234 3,082,251 139,336

37 to 48 months 157,961 136,224 824,239 139,326

49 to 60 months 111,333 125,531 468,845 128,633

61 to 72 months 83,587 60,520 515,877 63,622

73 to 84 months 50,459 35,505 179,773 38,607

85 to 96 months 37,970 6,647 96,491 7,247

Thereafter 38,656 - 315,482 463

2,596,267 636,895 6,912,797 657,284

On September 30, 2015 and December 31, 2014, carrying value approximates fair value of debt.

13. Other taxes payable

Parent Company Consolidated

September

30, 2015

December

31, 2014

September

30, 2015

December

31, 2014

Description

Contribution to social security financing

(“COFINS”) - 1,846 1,901 1,919

Social integration program (“PIS”) - 375 408 390

National social security institute (“INSS”) 1,635 1,508 4,460 1,687

Tax on circulation of goods, transport services

and communication (“ICMS”) 53 1,025 4,134 1,025

Recovery program (“Refis”) 902 902 30,899 902

Other 1,561 1,303 11,457 1,377

4,151 6,959 53,259 7,300

Current 4,151 6,959 27,758 7,300

Non-current - - 25,501 -

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

39

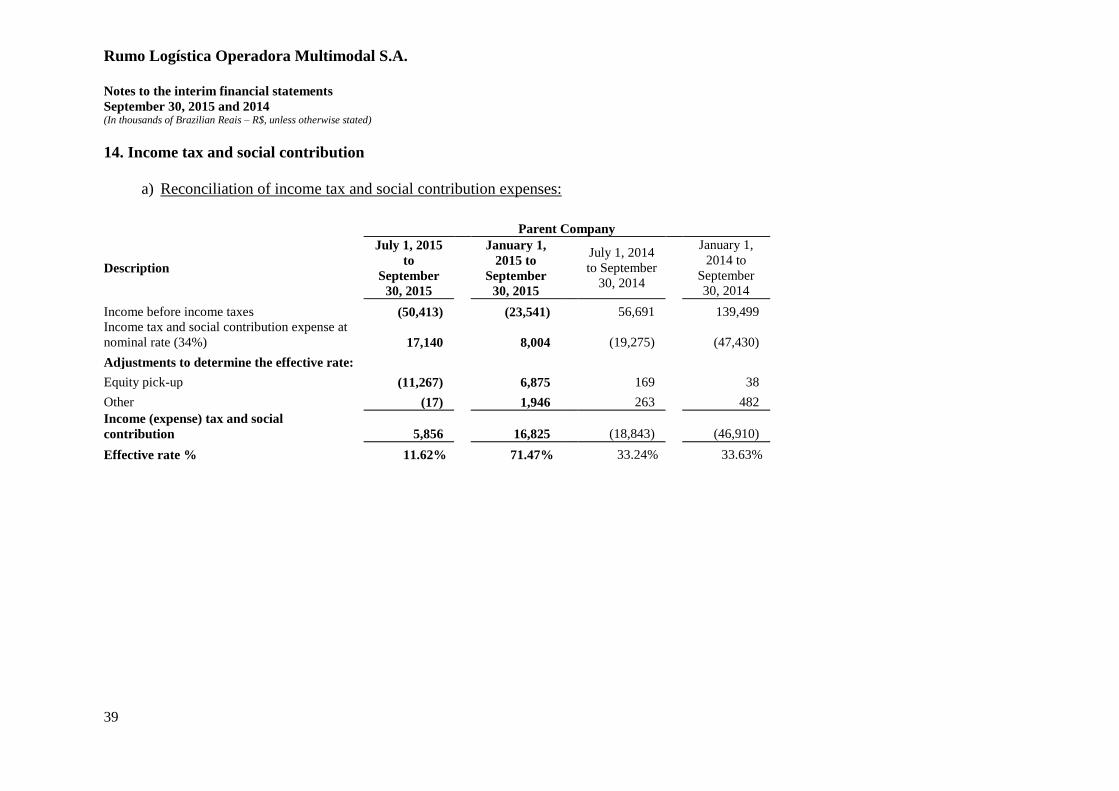

14. Income tax and social contribution

a) Reconciliation of income tax and social contribution expenses:

Parent Company

Description

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1, 2014

to September

30, 2014

January 1,

2014 to

September

30, 2014

Income before income taxes (50,413) (23,541) 56,691 139,499

Income tax and social contribution expense at

nominal rate (34%) 17,140 8,004 (19,275) (47,430)

Adjustments to determine the effective rate:

Equity pick-up (11,267) 6,875 169 38

Other (17) 1,946 263 482

Income (expense) tax and social

contribution 5,856 16,825 (18,843) (46,910)

Effective rate % 11.62% 71.47% 33.24% 33.63%

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

40

Consolidated

Description

July 1, 2015

to

September

30, 2015

January 1,

2015 to

September

30, 2015

July 1, 2014

to September

30, 2014

January 1,

2014 to

September

30, 2014

Income before income taxes (43,039) 50,631 57,695 139,743

Income tax and social contribution expense at nominal rate (34%) 14,633 (17,215) (19,616) (47,513)

Adjustments to determine the effective rate:

Equity pick-up 1,385 1,446 - -

Rate difference on deemed profit taxation method (156) 383 - -

Goodwill amortization tax (realization) 463 927 - -

Unrecognized NOLs and temporary differences (26,618) (53,903) - -

Exploration profit - tax incentive 11,850 20,946 - -

Other 359 380 245 465

Income (expense) tax and social contribution 1,916 (47,036) (19,371) (47,048)

Effective rate % 4.45% 92.90% 33.58% 33.67%

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

41

b) Deferred corporate income tax (IRPJ) and social contribution (CSLL) assets and liabilities:

Parent Company

Description September 30, 2015

December 31,

2014

Basis IRPJ 25% CSLL 9% Total

Tax losses:

Tax losses carry forwards – income tax 78,952 19,738 - 19,738 -

Tax losses of social contribution 104,035 - 9,363 9,363 -

Temporary differences:

Exchange variation - Cash basis 140,382 35,096 12,634 47,730 -

Derivatives (78,809) (19,702) (7,093) (26,795) -

Accelerated depreciation (234,995) (58,749) - (58,749) (65,020)

Tax goodwill amortized (13,786) (3,447) (1,241) (4,688) 8,398

Review of useful life (161,986) (40,497) (14,579) (55,076) (41,669)

Business combination - Fixed assets (137) (34) (12) (46) (405)

Business combination - Intangible assets (241,645) (60,411) (21,748) (82,159) (85,154)

Provision for judicial demands 15,525 3,881 1,397 5,278 4,488

Provision for profit sharing 14,517 3,629 1,307 4,936 3,348

Allowance for doubtful accounts 1,115 279 100 379 7,502

Other (38,332) (9,583) (3,449) (13,032) (1,335)

Total (129,800) (23,321) (153,121) (169,847)

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

42

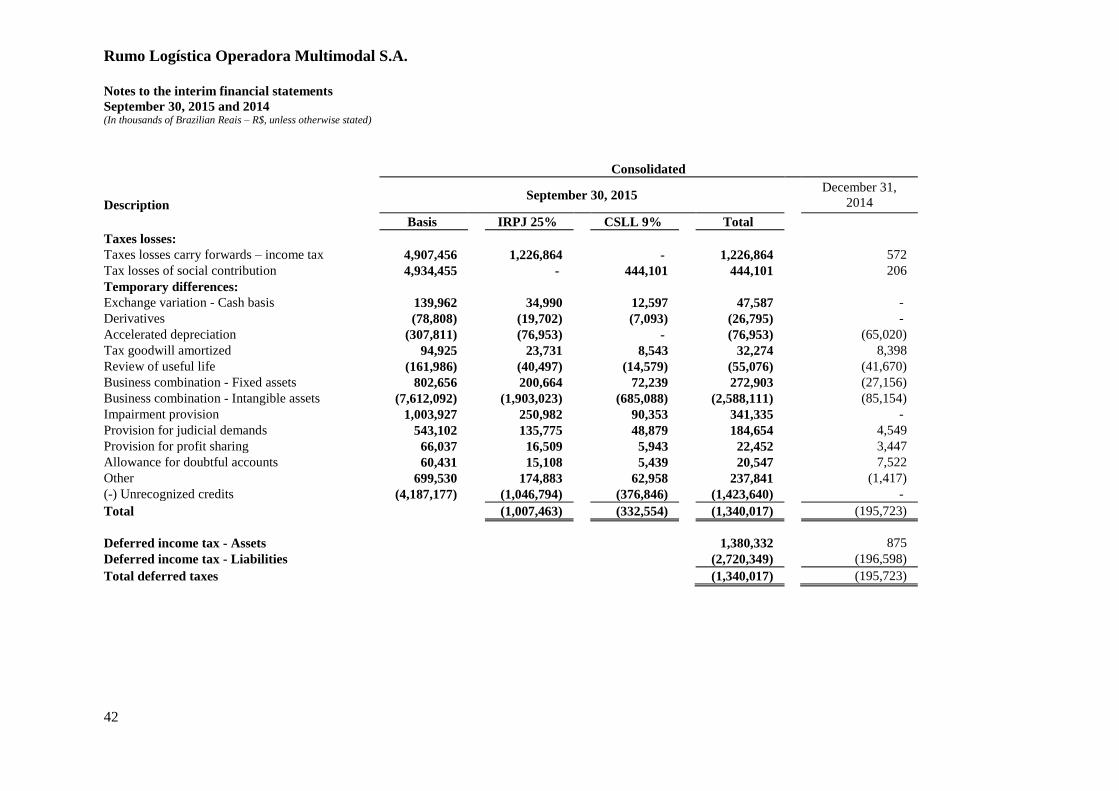

Consolidated

Description September 30, 2015

December 31,

2014

Basis IRPJ 25% CSLL 9% Total

Taxes losses:

Taxes losses carry forwards – income tax 4,907,456 1,226,864 - 1,226,864 572

Tax losses of social contribution 4,934,455 - 444,101 444,101 206

Temporary differences:

Exchange variation - Cash basis 139,962 34,990 12,597 47,587 -

Derivatives (78,808) (19,702) (7,093) (26,795) -

Accelerated depreciation (307,811) (76,953) - (76,953) (65,020)

Tax goodwill amortized 94,925 23,731 8,543 32,274 8,398

Review of useful life (161,986) (40,497) (14,579) (55,076) (41,670)

Business combination - Fixed assets 802,656 200,664 72,239 272,903 (27,156)

Business combination - Intangible assets (7,612,092) (1,903,023) (685,088) (2,588,111) (85,154)

Impairment provision 1,003,927 250,982 90,353 341,335 -

Provision for judicial demands 543,102 135,775 48,879 184,654 4,549

Provision for profit sharing 66,037 16,509 5,943 22,452 3,447

Allowance for doubtful accounts 60,431 15,108 5,439 20,547 7,522

Other 699,530 174,883 62,958 237,841 (1,417)

(-) Unrecognized credits (4,187,177) (1,046,794) (376,846) (1,423,640) -

Total (1,007,463) (332,554) (1,340,017) (195,723)

Deferred income tax - Assets 1,380,332 875

Deferred income tax - Liabilities (2,720,349) (196,598)

Total deferred taxes (1,340,017) (195,723)

Rumo Logística Operadora Multimodal S.A.

Notes to the interim financial statements

September 30, 2015 and 2014 (In thousands of Brazilian Reais – R$, unless otherwise stated)

43

c) Changes in deferred taxes (net):

Parent Company Consolidated