saija final reportsaija.in/wp-content/uploads/2016/01/crisil_2013.pdf · the mfi grading report and...

TRANSCRIPT

CRISIL MFIGrading

mfR4

Saija Finance Private Limited

(SFPL)

Date Assigned June 4, 2013

1

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

DISCLAIMER

CRISIL's microfinance institution (MFI) Grading reflects CRISIL’s current opinion on the ability of an

MFI to conduct its operations in a scalable and sustainable manner. In the case of NGO-MFIs and

entities with multiple businesses, CRISIL’s MFI Gradings apply only to their microfinance programmes.

The MFI Grading is a one-time exercise and the Grading will not be kept under surveillance. This

grading is valid for a period of one year from the date of assignment. However, CRISIL reserves the

right to suspend, withdraw, or revise the MFI grading at any time, on the basis of any new information

or unavailability of information or any other circumstances brought to CRISIL’s notice, which CRISIL

believes may have an impact on the grading. CRISIL recommends that the user of the Grading seeks a

review of the Grading if the graded institution/microfinance programme experiences significant

changes/events during this period which could impact the graded institution/its grading.

CRISIL MFI Gradings are based on the information provided by the Institution, or obtained by CRISIL

from sources it considers reliable. CRISIL does not guarantee the completeness or accuracy of the

information on which the MFI Grading is based. CRISIL MFI Grading is not a recommendation to

purchase, sell or hold any financial instrument issued by the graded MFI, or to make loans and

donations / grants to the institution. The MFI Grading does not constitute an audit of the graded MFI by

CRISIL.

The MFI Grading Report and the information contained therein are the intellectual property of CRISIL.

The MFI Grading Report should not be reproduced or distributed or communicated directly or indirectly

in any form to any other person or published or copied in whole or in part, for any purpose or by any

means without the prior written permission of CRISIL. The MFI Grading should not be used for

mobilising deposits/savings/thrift/insurance funds/other funds (including equity) from their

members/clients or general public and should not be used in its external communications, promotional

materials or member/client passbooks. CRISIL is not responsible for any errors and especially states

that it has no financial liability, whatsoever, to the subscribers/ users/transmitters/distributors of its MFI

Gradings. For the latest information on any outstanding CRISIL MFI Gradings, please contact CRISIL

RATING DESK at [email protected] or at (+91-22)-3342 3047/3064.

2

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

MICROFINANCE INSTITUTION (MFI) GRADING

MFI GRADING HISTORY

mfR1 CRISIL’s microfinance institution (MFI) Grading is a current opinion

on the ability of an MFI to conduct its operations in a scalable and

sustainable manner. The MFI Grading is assigned on an eight-point

scale, with ‘mfR1’ being the highest, and ‘mfR8’ the lowest. The MFI

Grading is a measure of the overall performance of an MFI on a

broad range of parameters under CRISIL’s MICROS framework. It

includes a traditional creditworthiness analysis using the CRAMEL

approach, modified to be applicable to the microfinance sector. The

acronym MICROS stands for Management, Institutional

arrangement, Capital adequacy and asset quality, Resources and

asset-liability management, Operational effectiveness, and

Scalability and sustainability.

MFI Grading scale: mfR1 - highest; mfR8 – lowest

mfR2

mfR3

mfR4

mfR5

mfR6

mfR7

mfR8

MFI Grading Assigned in mfR5 April 18, 2012 mfR5 January, 2011 mfR5 July, 2009

3

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

FACT SHEET

Name of the MFI : Saija Finance Private Limited (previously known as

Regards Finance Private Limited)

Year of Incorporation : September 1997

Year of commencement of microfinance programme

: November 2007

Legal status : Private limited company registered as a non-banking

finance company (NBFC) with the RBI and classified

as a non-deposit taking NBFC (NBFC-ND)

Managing Director : Mr. SR Sinha

Office address : 3rd floor, Uma Complex, Frazer Road

Patna - 800 001, Bihar

Tel: +91 612 2216 009

Email: [email protected], [email protected]

Web: www.saija.in

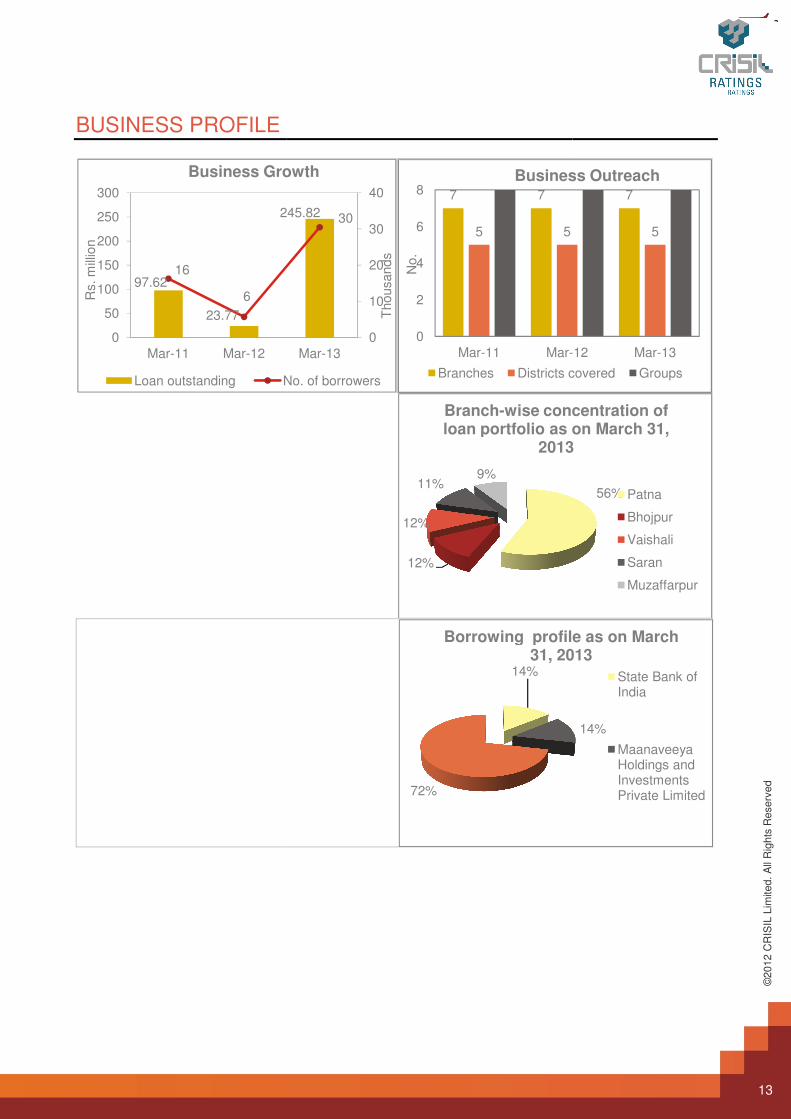

Bankers and lenders : State Bank of India, Maanaveeya Holdings and

Investments Private Limited, IFMR Capital Finance

Private Limited, and Small Industries Development

Bank of India

Statutory Auditors : BSSR and Company, Gurgaon

4

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

ABOUT THE MICROFINANCE PROGRAMME As on March 31, 2013

Lending model : Lends to joint-liability groups (JLGs)

Products : • Microfinance loans: The MFI extends 46 weeks, 12

months, 24 months and 12 months loans of Rs.5,000 to

Rs.50,000 at an interest of 26.00 per cent (on a

reducing-balance basis). Processing fee is one per cent

of the loan amount. Loans include:

o Saija Karobar Rin (SKR): Business loan for self-

employed men and women organised in groups of 4

to 6 members

o Saija Mahila Rin (SMR): Household loan for

income-generating activities, extended to women

organised in groups of 10 to 15

• Loan insurance: The MFI has a tie-up with Life

Insurance Corporation of India (LIC) and India First Life

Insurance Company to offer life insurance to borrowers

(and spouse). It collects an insurance fee of Rs.102 for

loan size of Rs.10,000 and provides life insurance cover

for an assurance of Rs.10,000.

Borrower base : 30,489 (5,702 as on March 31, 2012)

Employees : 120 (77 credit officers)

Number of branches : 7

Loan outstanding : Rs.245.82 million (Rs.23.77 million as on March 31, 2012)

Loans disbursed : Rs.408.87 million (Rs.73.03 million as on March 31, 2012)

Geographical reach : 5 districts of Bihar

5

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

SOCIAL AND TRANSPARENCY INDICATORS As on March 31, 2013 in per cent

Average loan outstanding/per capita gross national income (GNI), 2012 12

Percentage of women staff 10

Percentage of women borrowers 88

Effective IRR (including interest, processing fees, and any other fees) 26.00

Client dropout rate 8

Is interest rate (on declining basis) communicated to clients in writing? Yes

Are processing charges communicated to clients in writing? Yes

Does the MFI provide an official receipt to clients after repayment collections? Yes

Is access to loan of other MFIs a parameter to select/screen clients? Yes

Is access to loan of other MFIs/residual income factored in appraising the client’s repayment capacity?

Yes

Does the MFI appraise the client’s income/poverty/asset level and use this data to target other low-income clients?

Yes

Does the MFI capture and analyse reasons for client dropout rate? Partial**

Are clients provided head office contact details as part of the grievance redressal mechanism?

Yes

*Source: Based on Central Statistical Organisation (CSO) data

GNI is based on current prices and is a quick estimate for financial year 2012-13 **Dropout rates are recorded but not analysed.

6

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

GRADING RATIONALE CRISIL’s microfinance institution (MFI) grading on Saija Finance Private Limited (SFPL) reflects

the following strengths:

• Experienced board and senior management

• Strong financial and managerial support from Accion International and PI International

• Adequate capitalisation to support midterm growth

• Above-average asset quality

The listed grading strengths are offset by the following weaknesses:

• Moderate resource profile

• Concentration of operation in a few districts of Bihar

• High operating expenses and weak earnings profile

Profile

SFPL is a Bihar-based NBFC-ND, registered in New Delhi. It was incorporated in 1997 and

acquired by its current management in 2007. In the same year, it started its microfinance

programme by taking over a small loan portfolio from Saija Vikas, its associate non-profit

organisation. Saija Vikas was registered in July 2007 under the Societies Registration Act No. 21

of 1860.

SFPL’s microfinance programme seeks to facilitate small income-generation ventures, such as

green-groceries, embroidery shops, eateries, tailoring establishments, and agriculture-related

activities. It currently operates through seven branches across five districts of Bihar, namely Patna,

Bhojpur, Vaishali, Saran, and Muzaffarpur. The MFI plans to expand its operations across Bihar

and to Jharkhand and Uttar Pradesh as well. SFPL had 30,489 borrowers and loans outstanding of

Rs.245.82 million as on March 31, 2013.

SFPL offers two types of JLG loans — Saija Karobar Rin for business purposes and Saija Mahila

Rin for household purposes. The former is extended to groups of 4–6 men and women and the

latter to groups of 10–15 women. The loan size varies from Rs.5,000 to Rs.50,000, as per the

client’s repayment capacity, number of loan cycles, and type of activity. The loans are extended for

tenure of 46 weeks, 12 months, 24 months and 12 months at a reducing interest rate of 26.00 per

7

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

cent per annum. The loans are repayable in weekly, fortnightly, and monthly instalments and carry

a one-time processing fee of one per cent of the loan amount.

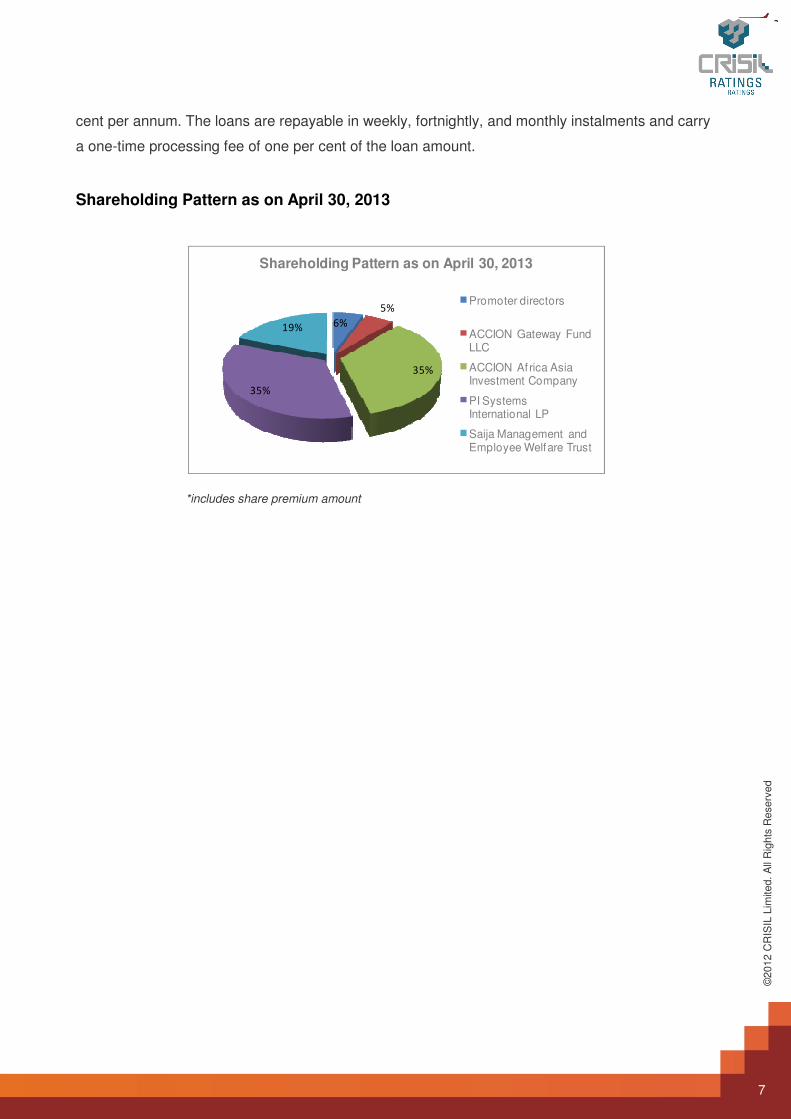

Shareholding Pattern as on April 30, 2013

*includes share premium amount

6%

5%

35%

35%

19%

Shareholding Pattern as on April 30, 2013

Promoter directors

ACCION Gateway Fund LLC

ACCION Af rica Asia Investment Company

PI Systems International LP

Saija Management and Employee Welfare Trust

8

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

MANAGEMENT

Extensive microfinance experience in area of operations

• SFPL’s founders has over 25 years of experience in banking,

finance, insurance, and providing microfinance services in the

organisation’s area of operations. CRISIL believes that the

founder’s prior experience in a high degree of operational expertise

will help the organisation to expand in new areas, while also

maintaining its portfolio quality.

Adequate credit-approval mechanisms

• The MFI has adequate client selection and credit-approval

mechanisms, as loans are sanctioned only after due diligence is

conducted by the assistant branch manager (ABM) and BM.

• The MFI’s loan sanction process is decentralised at the branch

level. It has tie-ups with two credit bureaus—High Mark and

Equifax—to identify instances of multiple lending.

Continues to receive support from its international partner-Accion International

• SFPL has partnered with the global organisation Accion

International (AI), which has partnerships with more than 60 MFIs

in Latin America, Asia, and Africa. AI provides Saija Finance with

technical support, including the development of loan products,

delivery models, MIS, internal control systems and operations

processes. AI has also deputed two professionals to manage

SFPL’s operations.

Adequate systems and processes

• The MFI’s systems and processes have improved significantly

since the previous grading as it starts using a loan tracking

software called ‘Omni Enterprises’ at the head office (HO) and

branch levels to generate demand and collection statements.

• The software is integrated with the accounting package and can

generate various other reports as on daily basis, including portfolio

at risk (PAR) statement, documentation on loan processing and

disbursements, and progress reports at the field and branch levels.

Adequate internal audit system for current scale of operations

• SFPL has an internal audit team of four personnel to verify demand

and collection sheets and other documents at the branches. The

internal audit is conducted on a monthly basis on Ho and branch

level, and the findings are shared with the respective BMs. The

9

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

branches are required to send the compliance document to the

HO. CRISIL believes that the MFI’s internal audit process is

adequate for its current scale of operations.

Moderate cash management practices

• SFPL has a separate bank account for each branch, which helps

the HO track financial transactions on field. Each branch deposits

its daily collections at its bank and updates the system on the same

day. The HO conducts monthly reconciliation. SFPL has also

availed cash-in-transit and a cash-in-safe insurance. However,

CRISIL identified a few instances where the branches were

maintaining excess cash balance.

Good social impact • In 2011, SFPL launched an entrepreneurial development program

(EDP) and a financial literacy program (FLP) for its members. EDP

provides skill training on general business and basic accounting,

while FLP creates awareness on how savings can be used to

create assets and working capital. CRISIL believes that the MFI

can significantly improve its social impact by scaling up these

programs. About 200 members have enrolled already.

INSTITUTIONAL ARRANGEMENT

Experienced board and senior management

• SFPL has a six-member board, comprising one promoter, two AI-

nominated directors, two Pragati International nominated directors,

and one independent director. The board members have extensive

experience in financial services, banking, development, and

microfinance.

• SFPL’s senior management comprises professionals with

experience in finance, HR, IT, and strategic planning. The team’s

significant microfinance experience is expected to help the

organisation steer its programme.

• SFPL has formed a five-year technical agreement with AI, under

which the latter provides technical assistance and deputes two full-

time professionals to manage SFPL’s operations.

10

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

CAPITAL ADEQUACY AND ASSET QUALITY

Adequate capitalisation

• SFPL’s net worth improved to Rs.252.74 million (as on March 31,

2013) from Rs.6.80 million (as on March 31, 2012) due to equity

infusion in May 2012 from its partners Accion International and

Pragati International.

• Following capital infusion:

o Its capital adequacy ratio (CAR) improved significantly to 97.28

per cent as on March 31, 2013 from 33.83 per cent as on March

31, 2012. Similarly, its debt-equity ratio declined to 0.03 times

from 6.45 times in the same period.

o Moreover, its portfolio increased to Rs.245.82 million as on March

31, 2013 from Rs.23.77 million as on March 31, 2012.

• SFPL has aggressive growth plans for the next two years and

envisages a loan outstanding of Rs.1063.85 million for March 2014.

CRISIL believes its present capital will be sufficient to support growth

over the medium term.

Above average asset quality

• SFPL has maintained above-average asset quality with an on-time

repayment rate of 99.98 per cent as on March 31, 2013 and portfolio

at risk greater than 90 days (PAR>90 days) of 0.02 per cent.

• CRISIL believes that SFPL’s ability to extend repeat loans and meet

the credit demand on a timely basis will be an important grading

factor.

Significant geographic concentration

• SFPL’s entire loan portfolio is concentrated in five districts of Bihar,

thus making it vulnerable to high credit and operational risks.

• As operations are expected to remain concentrated over the near

term, any adverse credit event in area of operations could affect the

MFI’s capitalisation levels. Its ability to maintain delinquency at

acceptable levels while also pursuing growth remains a key grading

sensitivity factor.

RESOURCES AND ASSET LIABILITY MANAGEMENT

Moderate resource profile and high cost of borrowings

• SFPL is extensively dependent on a few lenders including banks,

and financial institutions (FIs). As on September 30, 2012, it had

outstanding borrowings of Rs.671.72 million, sourced from more

11

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

than six lenders. Though the MFI raised Rs.460 million during the

last quarter of 2011-12 (refers to financial year, April 1 to March 31),

it was unable to raise any incremental borrowings in the last six

months of the year.

• SFPL’s weighted average cost of borrowings for the year ended

March 31, 2011, was 15.00 per cent. Its weighted average cost is

similar when compared to other similar MFIs due to constrained

funding from banks to the MFI sector.

• CRISIL believes SFPL’s inability to raise adequate resources on

time will not only impact its business growth but also its asset

quality. Hence, the MFI’s poor borrower to member ratio was 40.00

per cent as on September 30, 2012. Continuous transfer of SHGs

from HIH resulting in incremental demand and dependence on a few

lenders could create liquidity pressures on the MFI.

OPERATIONAL EFFECTIVENESS

Pressure on earnings profile

• Improved income following increase in asset size enabled SFPL to

reduce its net loss to Rs.3.48 million in 2012-13 from Rs.17.35

million in 2011-12. The loss in 2012-13 occurred due to intangibles

written off (Rs.8.00 million).

• Following increase in asset size:

o SFPL’s operational self-sufficiency (OSS) improved to 110.88

per cent as on March 31, 2013 from 54.20 per cent as on March

31, 2012.

o Field productivity indicators have also improved, with loan

outstanding per credit officer increasing to Rs.3.19 million as on

March 31, 2013 from Rs.0.52 million as on March 31, 2012.

Loan outstanding per branch increased to Rs.35.12 million as on

March 31, 2013 from Rs.3.40 million as on March 31, 2012.

o Operating expense (opex) declined to 23.75 per cent in 2012-13

from 30.12 per cent in the previous year. However, as the MFI’s

opex is still higher than its similar-sized peers, it has decided to

increase the productivity of existing staff and branches.

• CRISIL expects SFPL’s earnings profile to remain modest despite

12

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

an increase in disbursements and productivity levels.

SCALABILITY AND SUSTAINABILITY

Adequate management’s experience to sustain operations

• CRISIL believes SFPL has adequate managerial experience,

processes and systems in place to scale and sustain its operations

over the long-term. It benefits from the financial and technical

support it receives from its international partner (Accion Gateway

Fund).

• SFPL expects its advances to increase to Rs.1,063.85 million in

2013-14 from Rs.245.82 million in 2012-13. Given its current size,

these projections may be ambitious but CRISIL expects the MFI to

be able to scale up its operations due to support from Accion as well

as its ability to raise fresh borrowings.

BUSINESS PROFILE

97.62

23.77

245.82

16

6

0

50

100

150

200

250

300

Mar-11 Mar-12

Rs. m

illio

n

Business Growth

Loan outstanding No. of borrowers

245.82 30

0

10

20

30

40

Mar-13

Thousands

Business Growth

No. of borrowers

7 7

5 5

0

2

4

6

8

Mar-11 Mar-

No.

Business Outreach

Branches Districts covered

12%

12%

11%9%

Branch-wise concentration of loan portfolio as on March 31,

2013

14%

72%

Borrowing profile as on March 31, 2013

13

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

7

5

-12 Mar-13

Business Outreach

Districts covered Groups

56%

wise concentration of loan portfolio as on March 31,

2013

Patna

Bhojpur

Vaishali

Saran

Muzaffarpur

14%

Borrowing profile as on March 31, 2013

State Bank of India

Maanaveeya Holdings and Investments Private Limited

14

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

FINANCIAL INDICATORS Income and expenditure statement Rs. million

For the year ended 2015 2014 2013 2012 2011

MFI’s Projections Provisional Audited

Fund based income 362.09 208.30 45.72 20.63 21.68

Interest and finance charges 147.80 70.52 4.36 15.62 8.18

Gross spread 214.29 137.77 41.36 5.01 13.50

Fee based income - - 3.64 0.89 4.19

Total income 362.09 208.30 49.36 21.52 25.86

Gross surplus 214.29 137.77 45.00 5.90 17.68

Personnel expenses - - 19.76 13.12 15.14

Administrative expenses 120.65 98.29 17.08 8.98 6.97

Total expenses 120.65 98.29 36.84 22.10 22.11

Provision for loan loss 9.93 17.83 0.03

0.26

Write-off of bad debts - - 0.05 0.13 -

Write-off of intangible assets - - 8.00* - -

Total write-offs and provisions 9.93 17.83 8.46 0.13 0.26

Depreciation 6.35 5.98 2.86 1.86 2.07

Profit/loss before tax 77.37 15.66 -3.16 -18.19 -6.75

Tax 25.53 5.17 0.32 -0.83 0.51

Net surplus 51.84 10.49 -3.48 -17.35 -7.26

*Intangible assets (trademark) written-off

15

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

Balance sheet Rs. million

As on March 31, 2015 2014 2013 2012 2011

Liabilities MFI’s Projections Provisional Audited

Net worth 388.45 336.61 252.74 6.80 23.84

Borrowings 1,260.28 828.06 7.20 43.84 100.21

Provision for loan loss 31.21 21.28 0.63 0.26 -

Other liabilities and provisions 6.94 6.94 24.72 4.37 5.50

Total current liabilities 38.14 28.22 31.46 8.06 5.50

Total liabilities 1,686.87 1192.88 291.40 58.69 129.56

Assets

Loans and advances 1,560.28 1,063.85 245.82 23.77 97.62

Cash & bank balances 2.38 1.02 31.26 5.76 14.70

Security deposit - - 0.14 0.12 -

Total funds deployed 1,562.66 1,064.87 277.42 32.82 113.92

Other current assets & advances 114.53 114.53 8.33 15.27 3.29

Net fixed assets 9.68 13.48 5.66 10.60 12.35

Total assets 1,686.87 1,192.88 291.40 58.70 129.56

16

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

Key Financial Ratios in per cent

For the period ended March 31, 2015 2014 2013 2012 2011

Yield MFI’s Projections Provisional Audited

Fund based yield 27.56 31.04 26.55 23.61 24.78

Portfolio Yield 27.60 31.81 30.55 28.55 28.60

Fee based income/Avg. funds deployed - - 2.35 1.21 5.06

Total income/Avg. funds deployed 27.56 31.04 28.90 24.82 29.84

Cost of funds

Interest paid/Avg. funds deployed 11.25 10.51 2.81 21.29 9.89

Interest paid/Avg. borrowings 14.15 16.89 17.07 21.69 12.37

Interest spread

Spreads on lending 13.41 14.15 9.48 1.93 12.41

Overheads

Operating expense ratio 9.18 14.65 23.75 30.12 26.73

Personnel expense ratio - - 12.74 17.88 18.30

Administrative expense ratio 9.18 14.65 11.01 12.23 8.43

Profitability

Net surplus/Avg. net worth 14.30 3.56 -2.68 -113.28 -25.84

Net profit/Avg. funds deployed 3.95 1.56 -2.24 -23.65 -8.78

Operational self sufficiency 127.17 108.13 110.88 54.20 79.31

Asset quality

Provisioning/Avg. loan outstanding 0.76 2.72 5.96 - 0.36

Capitalisation

Total debt/net worth (times) 3.24 2.46 0.03 6.45 4.20

Capital adequacy 23.06 28.24 97.28 33.83 29.88

17

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

Annexure

1.1 Outreach summary ........................................................................................................ 18

1.2 Human resource and productivity summary ................................................................. 18

1.3 Asset quality.................................................................................................................. 19

18

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

1.1 Outreach summary

As on/For the period ended Unit Mar-13 Mar-12 Mar-11

Borrowers No. 30,489 5,702 16,270

Groups No. 3,220 754 1,889

Branches No. 7 7 7

Villages covered No. 2477 580 1453

Districts No. 5 5 5

Women borrowers % 88 68 84

Disbursements Rs. mn 408.87 73.03 202.98

Loan outstanding Rs. mn 245.82 23.77 97.62

1.2 Human resource and productivity summary

As on/For the period ended Unit Mar-13 Mar-12 Mar-11

Total employees No. 120 75 101

Credit officers No. 77 46 62

Women employees No. 13 9 13

Borrowers/branch No. 4,356 815 2,324

Loan outstanding/branch Rs. mn 35.12 3.40 13.95

Borrowers/credit officer No. 396 124 262

Loan outstanding/credit officer Rs. mn 3.19 0.52 1.57

Average loan outstanding/borrower Rs. mn 8,063 4,169 6,000

19

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

1.3 Asset quality Rs. million

Mar-13 Mar-12 Mar-11

Total outstanding balance associated with loans that are

Amt % of PAR Amt % of PAR Amt % of PAR

Portfolio being current 245.76 99.98 23.74 99.86 97.66 99.79

Late (at least one payment) - - - - -

1-30 days 0.01 -

- 0.04 0.04

31-90 days 0.01 -

- 0.01 0.01

91-180 days

- 0.01 0.03 0.05 0.05

181-365 days 0.01 - 0.03 0.13 0.11 0.11

1 year or more - -

- - -

Total portfolio 245.82 100.00 23.77 100.00 97.87 100.00

Portfolio at risk > 30 days 0.01 0.15 0.17

Portfolio at risk > 90 days - 0.15 0.16

20

©2012 C

RIS

IL L

imited. A

ll R

ights

Reserv

ed

CRISIL MFIGrading

This page is intentionally left blank

Contact Us

Analytical Contacts

Mr. Yogesh Dixit Director

[email protected] +91 22 3342 3037

Mr. T Raj Sekhar Associate Director

[email protected] +91 44 4226 3614

CRISIL House, Central Avenue, Hiranandani Business Park Powai, Mumbai 400 076 Phone: + 91 22 3342 3000 Fax: + 91 22 3342 3001 Email: [email protected] www.crisil.com