salada foods jamaica limited buy - homepage - …€¦ · · 2017-11-26salada foods (buy 1) 2 | p...

TRANSCRIPT

Salada Foods (Buy 1) 1 | P a g e

Company Name: Salada Foods Jamaica Limited

Sector: Manufacturing – Food, Tobacco & Beverages

Location: Kingston

Country: Jamaica

Competitors:

JSE Ticker: SALF JSE Segment: Manufacturing & Retail Majority Stakeholder: Donovan Lewis

Date: Friday, April 29, 2011

Salada Foods Jamaica Limited BUY

JSE: SALF Bloomberg: SALF Ja

52 Week Range

$7.50 – 14.00

Market Price $9.00

Valuation $11.76

Key Metrics – September 2010

Gross Margin 38%

Operating Margin 16%

Net Margin 14%

Debt-to-Equity 0.00%

Current Ratio 12.73

ROE 15.00%

ROA 13.00%

Book Value $7.48

EPS (Last 4Q) $0.73

Trailing PE 12.31

PBV 1.44X

Salada Foods (Buy 1) 2 | P a g e

Executive Summary

Salada Foods Jamaica Limited (SALF) is the largest producer of instant (non-blue mountain) coffee in Jamaica. For the 2007-2009 period of the recession they demonstrated resilience and recorded record operating profits and elevated interest income which translated to record net profits. In 2010, the reduction in consumer demand took its toll and forced the company to absorb additional production costs associated with the volatility in global commodity prices. Additionally, the implementation of the JDX resulted in a noticeable drop in interest income and therefore net profit. By analysing historical performance using quantitative and qualitative metrics, we look deduce insights on the company to arrive at a recommendation.

Company Overview

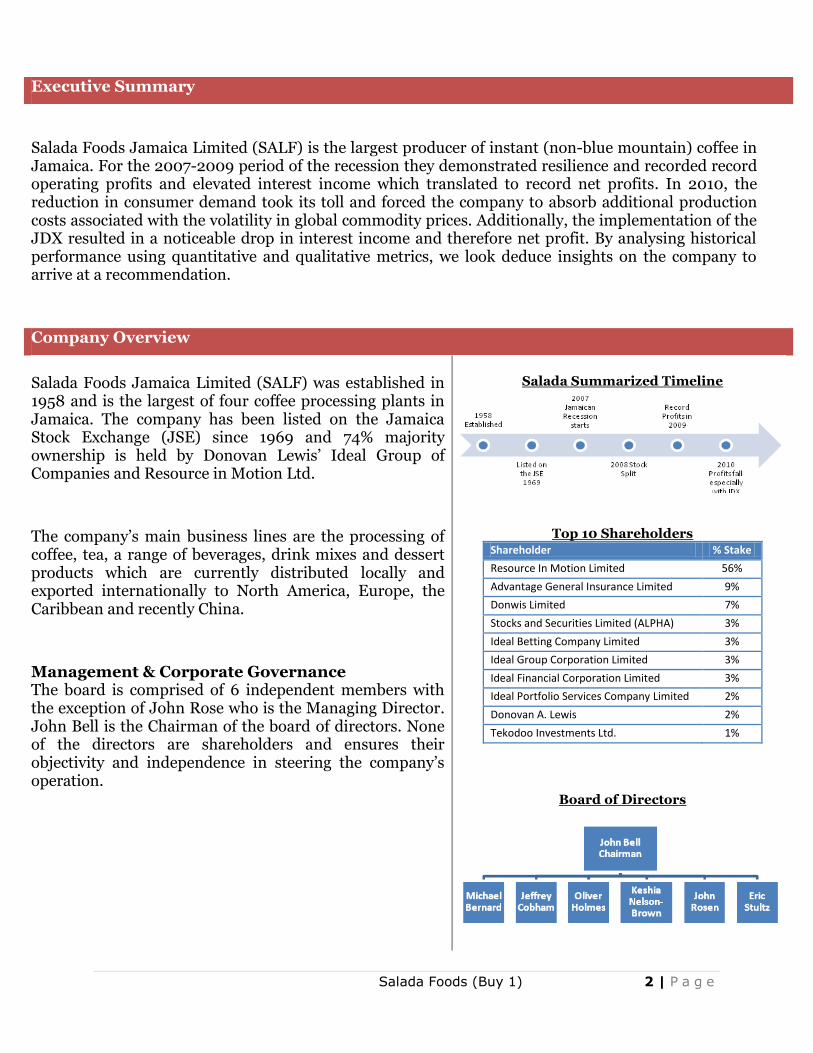

Salada Foods Jamaica Limited (SALF) was established in 1958 and is the largest of four coffee processing plants in Jamaica. The company has been listed on the Jamaica Stock Exchange (JSE) since 1969 and 74% majority ownership is held by Donovan Lewis’ Ideal Group of Companies and Resource in Motion Ltd.

The company’s main business lines are the processing of coffee, tea, a range of beverages, drink mixes and dessert products which are currently distributed locally and exported internationally to North America, Europe, the Caribbean and recently China.

Management & Corporate Governance The board is comprised of 6 independent members with the exception of John Rose who is the Managing Director. John Bell is the Chairman of the board of directors. None of the directors are shareholders and ensures their objectivity and independence in steering the company’s operation.

Salada Summarized Timeline

Top 10 Shareholders

Shareholder % Stake

Resource In Motion Limited 56%

Advantage General Insurance Limited 9%

Donwis Limited 7%

Stocks and Securities Limited (ALPHA) 3%

Ideal Betting Company Limited 3%

Ideal Group Corporation Limited 3%

Ideal Financial Corporation Limited 3%

Ideal Portfolio Services Company Limited 2%

Donovan A. Lewis 2%

Tekodoo Investments Ltd. 1%

Board of Directors

Salada Foods (Buy 1) 3 | P a g e

Industry Experience

Board Mem bers

Dir

ec

tor

ship

s*

Ma

nu

fac

turi

ng

Dis

trib

uti

on

Insu

ra

nc

e

Inv

Ba

nk

ing

Ba

nk

ing

Board Mem bers

John Rosen 1 √

Michael Bernard 2 √ √

Jeffrey Cobham 3 √ √ √ √ √

Oliv er Holmes 1 √ √ √

Keshia Nelson-Brown 2 √ √

Eric Stultz 1 √

John Bell 1 √

Economic Analysis

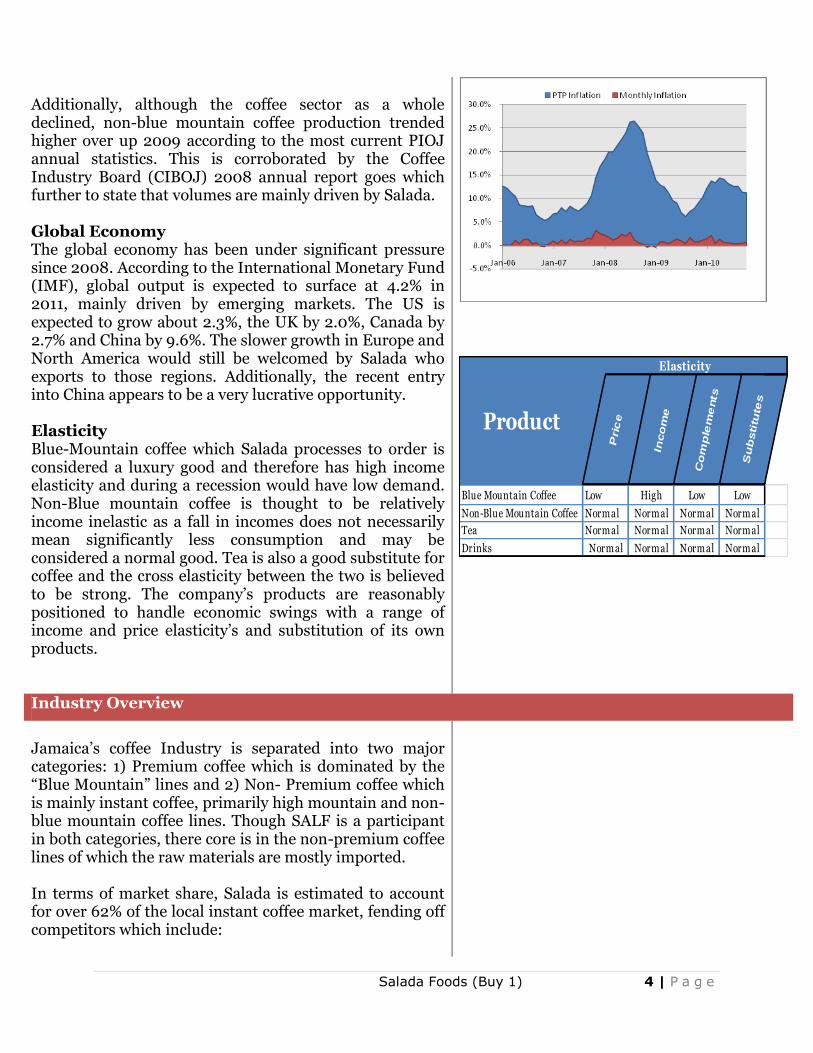

Local Economy The spillover effect of the global downturn has had a severe impact on the Jamaican economy especially due to structural deficiencies including: inefficiencies in the public sector, high energy costs, crime and politics. The Jamaican economic downturn has therefore been characterized by: weakened consumer demand, exchange rate devaluation (stabilized now), elevated inflation levels (moderating) and negative GDP growth. For the quarter ended December 2010, the Jamaican economy continued its decline from 2007, with year-on-year real GDP dropping 0.9%. A closer look at the data showed that the manufacturing sector was one of the major contributors with a 2.6% y-o-y decline for the quarter. Specifically, the subsector, Food, Beverages & Tobacco (which includes Salada) declined 0.7% for the period which was better than the manufacturing sector and overall economy. In nominal terms, this equates to a 1.6% decline in the subsector while the company was able to generate a 6.9% increase in revenues for the December quarter. This was a creditable performance by the company compare to both the sector and economy. Salada’s remarkable growth (especially under the circumstances) suggests that either: 1) The company from the economic downturn, possibly due to its lower priced products being substituted for premium lines or 2) The company’s increased promotional activities successfully stimulated demand. We supect a combination of both.

Salada Foods (Buy 1) 4 | P a g e

Additionally, although the coffee sector as a whole declined, non-blue mountain coffee production trended higher over up 2009 according to the most current PIOJ annual statistics. This is corroborated by the Coffee Industry Board (CIBOJ) 2008 annual report goes which further to state that volumes are mainly driven by Salada. Global Economy The global economy has been under significant pressure since 2008. According to the International Monetary Fund (IMF), global output is expected to surface at 4.2% in 2011, mainly driven by emerging markets. The US is expected to grow about 2.3%, the UK by 2.0%, Canada by 2.7% and China by 9.6%. The slower growth in Europe and North America would still be welcomed by Salada who exports to those regions. Additionally, the recent entry into China appears to be a very lucrative opportunity. Elasticity Blue-Mountain coffee which Salada processes to order is considered a luxury good and therefore has high income elasticity and during a recession would have low demand. Non-Blue mountain coffee is thought to be relatively income inelastic as a fall in incomes does not necessarily mean significantly less consumption and may be considered a normal good. Tea is also a good substitute for coffee and the cross elasticity between the two is believed to be strong. The company’s products are reasonably positioned to handle economic swings with a range of income and price elasticity’s and substitution of its own products.

Product

Elasticity

Pri

ce

Inco

me

Co

mp

lem

ents

Su

bsti

tute

s

Product

Blue Mountain Coffee Low High Low Low

Non-Blue Mountain Coffee Normal Normal Normal Normal

Tea Normal Normal Normal Normal

Drinks Normal Normal Normal Normal

Industry Overview

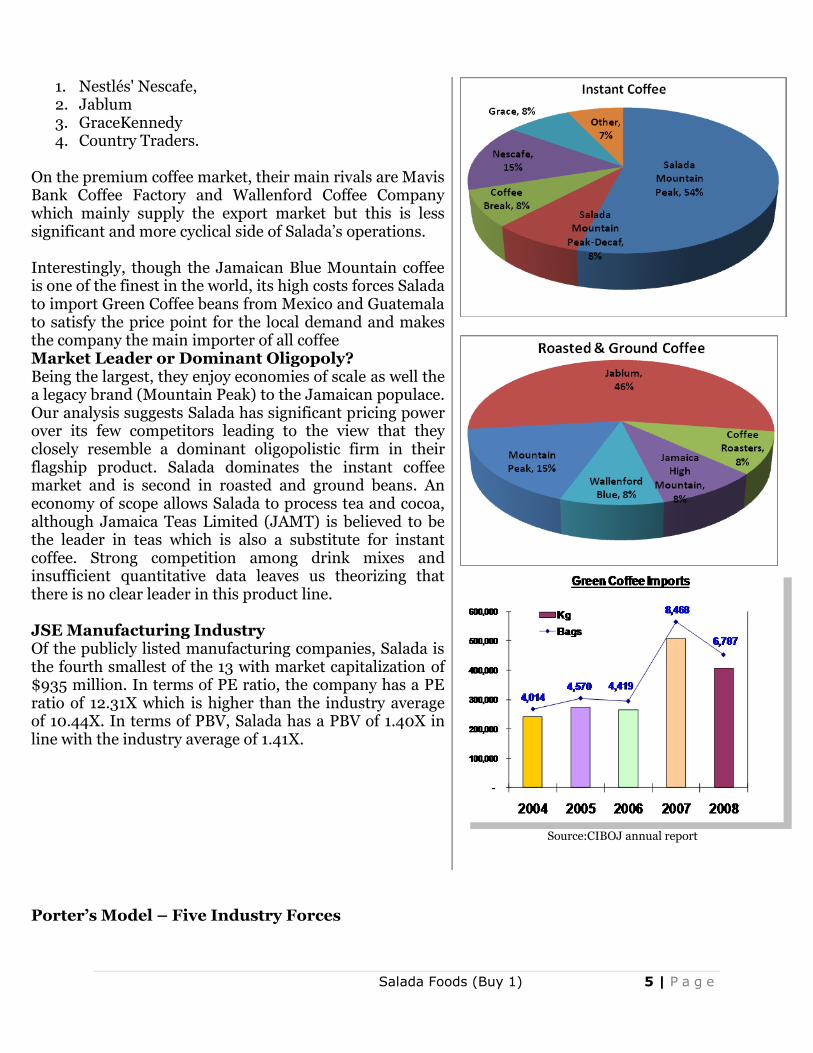

Jamaica’s coffee Industry is separated into two major categories: 1) Premium coffee which is dominated by the “Blue Mountain” lines and 2) Non- Premium coffee which is mainly instant coffee, primarily high mountain and non-blue mountain coffee lines. Though SALF is a participant in both categories, there core is in the non-premium coffee lines of which the raw materials are mostly imported. In terms of market share, Salada is estimated to account for over 62% of the local instant coffee market, fending off competitors which include:

Salada Foods (Buy 1) 5 | P a g e

1. Nestlés' Nescafe, 2. Jablum 3. GraceKennedy 4. Country Traders.

On the premium coffee market, their main rivals are Mavis Bank Coffee Factory and Wallenford Coffee Company which mainly supply the export market but this is less significant and more cyclical side of Salada’s operations. Interestingly, though the Jamaican Blue Mountain coffee is one of the finest in the world, its high costs forces Salada to import Green Coffee beans from Mexico and Guatemala to satisfy the price point for the local demand and makes the company the main importer of all coffee Market Leader or Dominant Oligopoly? Being the largest, they enjoy economies of scale as well the a legacy brand (Mountain Peak) to the Jamaican populace. Our analysis suggests Salada has significant pricing power over its few competitors leading to the view that they closely resemble a dominant oligopolistic firm in their flagship product. Salada dominates the instant coffee market and is second in roasted and ground beans. An economy of scope allows Salada to process tea and cocoa, although Jamaica Teas Limited (JAMT) is believed to be the leader in teas which is also a substitute for instant coffee. Strong competition among drink mixes and insufficient quantitative data leaves us theorizing that there is no clear leader in this product line. JSE Manufacturing Industry Of the publicly listed manufacturing companies, Salada is the fourth smallest of the 13 with market capitalization of $935 million. In terms of PE ratio, the company has a PE ratio of 12.31X which is higher than the industry average of 10.44X. In terms of PBV, Salada has a PBV of 1.40X in line with the industry average of 1.41X.

Source:CIBOJ annual report

Porter’s Model – Five Industry Forces

Salada Foods (Buy 1) 6 | P a g e

Competitive Force Ranking Rationale

Threat of New

Entrants Low

The Coffee Industry Board of Jamaica regulates all coffee production, importation and exportation. The high cost of local coffee due to its premium quality makes it unattractive for the local market. Importation of cheaper coffee requires special permission from the regulator

Bargaining Power of

Suppliers Low

There is no single supplier of raw materials locally.

Bargaining Power of

Buyers Low

There is no single buyer such as the government which is

able to influence the company’s accommodation or ability

to generate revenues

Availability of

Substitutes Moderate

Tea is a good substitute for coffee

Rivalry Among

Competitors

Moderate -

High

Moderate for coffee and Tea Products. High for drink

mixes

Salada Foods (Buy 1) 7 | P a g e

Porter’s Model – Five Forces of Industry Competition

INDUSTRY COMPETITORS

Rivalry Among Grace

Country Traders Nescafe Jablum

SUBSTITUTES – MODERATE

Teas

Energy drinks

POTENTIAL ENTRANTS - LOW

CIBOJ regulates all coffee activity

Jamaican grown coffee is very expensive

SUPPLIERS – LOW

Mexico

Guatemala

India

Jamaica

BUYERS - LOW

Salada Foods (Buy 1) 8 | P a g e

SWOT Analysis

STRENGTHS WEAKNESSES

Mountain Peak brand have a decades long

legacy with the Jamaican populace, although

below Blue Mountain quality.

Relatively lower prices due to premium lines

Largest coffee processor in Jamaica

Concentration in a single type of product

(coffee based)

Spraying-drying method not the most

efficient production process.

OPPORTUNITIES THREATS

Expansion of product distribution

internationally

Introduction of value added products

Fairly untapped export market

Weak economic backdrop locally and

internationally

Impact of natural disasters (hurricanes) on

coffee farms

Salada Foods (Buy 1) 9 | P a g e

Financial Statement Analysis – December 2010 (See Appendix 1)

Growth & Profitability Revenues – grew at a compounded annual growth rate (CAGR) of 10% from 2005 to 2010, a commendable achievement considering the downturn in the local economy since 2007. Peak volumes were achieved in 2009 and the company is steadily approaching those levels again. The growth in revenue followed through to the first quarter ended December 2010 with a 6.9% improvement to $110 million. Margins – Gross, Operating and Net Margins showed steady improvements from 2005 until 2009, but the protracted recession impacted consumer demand in 2010 and forced the company to absorb increased production costs while intensifying promotional activities. Operating margins were also likely affected by increased exportation which was used to balance the falloff in local demand. The reduction in margins is likely to be short-lived as the company is expected to pass on increased production costs to consumers with an improving economic backdrop. Net Profit – Rapid growth slowed once the local recession started in late 2007 and then declined from its peak in 2009 as the company absorbed additional costs. Looking ahead, the company is better positioned to pass on costs to consumers, with demand expected to be less price elastic with time elapsed. DuPont Analysis (ROE Decomposition) Asset Turnover has steadily trended down over the period while Financial Leverage was flat. Therefore, ROE was driven by the movement in Net Profit Margin which rapidly improved from 2005 – 2009, but fell in 2010 due to higher production and marketing costs as well lower interest income post JDX.

ROE – Dupont Analysis

2005 2006 2007 2008 2009 2010

Last 12M

Asset Turnover 1.15 1.25 1.17 1.08 0.93 0.75 0.72

xFinancial Leverage

1.32 1.25 1.20 1.15 1.15 1.19 1.14

xNet Profit Margin

10% 12% 20% 19% 25% 19% 18%

=ROE 15% 19% 28% 24% 27% 17% 14%

Salada Foods (Buy 1) 10 | P a g e

Solvency Long-Term-Debt to Equity – The Company utilizes minimal long term debt in its balance sheet and its debt-to-equity ratio has averaged less than 2% over the last 5 years. Financial Leverage – the company has utilized very little leverage to grow their operations. In 2005, leverage was 1.25X and has steadily declined to 1.15X Interest Coverage – has been excellent due to very little debt on the balance which allows operating profit to comfortably cover interest costs. Conclusion: SALF holds virtually zero long-term debt while having strong cash balances relative to the company’s size. These can be channeled to driving future growth such as in the company’s recent attempt to acquire the government controlled Mavis Bank Coffee Factory. The company’s capacities to expand operations are very favorable. Liquidity Current Ratio – As mentioned in the solvency measures above, the company maintains significant cash balances and short term deposits which result in a high current ratio of 12X up to December 2010 compared to 4.21 in 2005. Undoubtedly this is highest of the JSE companies and speaks to their financial strength as a small player. Cash Conversion Cycle – has progressively increased over the last 5 years from 77 days in 2005 to 205 days as at December 2010. The table below and graph to the right shows the trend, and also shows the main driver to be Days of Inventory on Hand. It suggests the company has is utilizing too much working capital by increasing inventory levels.

Cash Conversion Cycle

Days 2005 2006 2007 2008 2009 2010 Last 12 M

Days of Inventory on Hand

94 117 109 122 162 187 218

Days Sales Outstanding

43 32 42 57 65 60 51

Number of Days of Payables

60 47 42 50 58 71 64

Cash Conversion Cycle

77 102 109 130 169 176 205

Conclusion: SALF’s strong liquidity position shows they may be overly invested in working capital and should consider reducing inventory levels as well looking for expansion opportunities or paying dividends.

Salada Foods (Buy 1) 11 | P a g e

Outlook

Salada Foods Jamaica Limited, the largest producers of coffee and coffee based products in Jamaica has

consistently recorded improved revenue and profitability over the past 10 years. Revenues grew at a

compounded annual growth rate (CAGR) of 10% while profits climbed by a CAGR of 28% in the same

period. This was an impressive feat.

As the global recession unwound in 2008, Salada was proactive in reengineering its distribution and

marketing operations to increase productivity while limiting the exposure to volatility in raw material

costs although they were still affected. The company assigned Musson Jamaica limited as the exclusive

distributor of coffee on the domestic market and this allowed better focus of their marketing and

distribution, leading to revenue growth.

In recent years, the company has improved its internal infrastructure and broadened the distribution of

its products particularly in the overseas markets. Recently, Salada commenced distribution in China,

while maintaining exports to other markets within the Caribbean, North America and Europe.

Nevertheless, Salada Foods still maintains a strong reliance on the domestic market which is the primary

contributor to revenues and profits. According to the company’s management, the export market

accounts for about 12% of revenues and may be an avenue for growth in future periods. In fact, the

company attributes top line growth in its latest nine months results to December 2010 to increased

exportation.

The outlook on the instant coffee business remains fairly strong both locally and internationally. This is

especially true since premium brands are likely to continue facing downward pressure due to the

sensitivity to consumer spending both locally and internationally. Salada demonstrated strong revenue

growth amidst the economic headwinds and we believe as conditions improve, the company will reap

further benefits. In the short to medium term, we expect Salada to continue growing its revenue base and

profitability through: continued penetration of the international markets, introduction of value added

products and more focused marketing. Net profit is expected to grow approximately 16% over the next 10

years, with Salada possessing significant growth potential.

Salada Foods (Buy 1) 12 | P a g e

Projections & Valuations

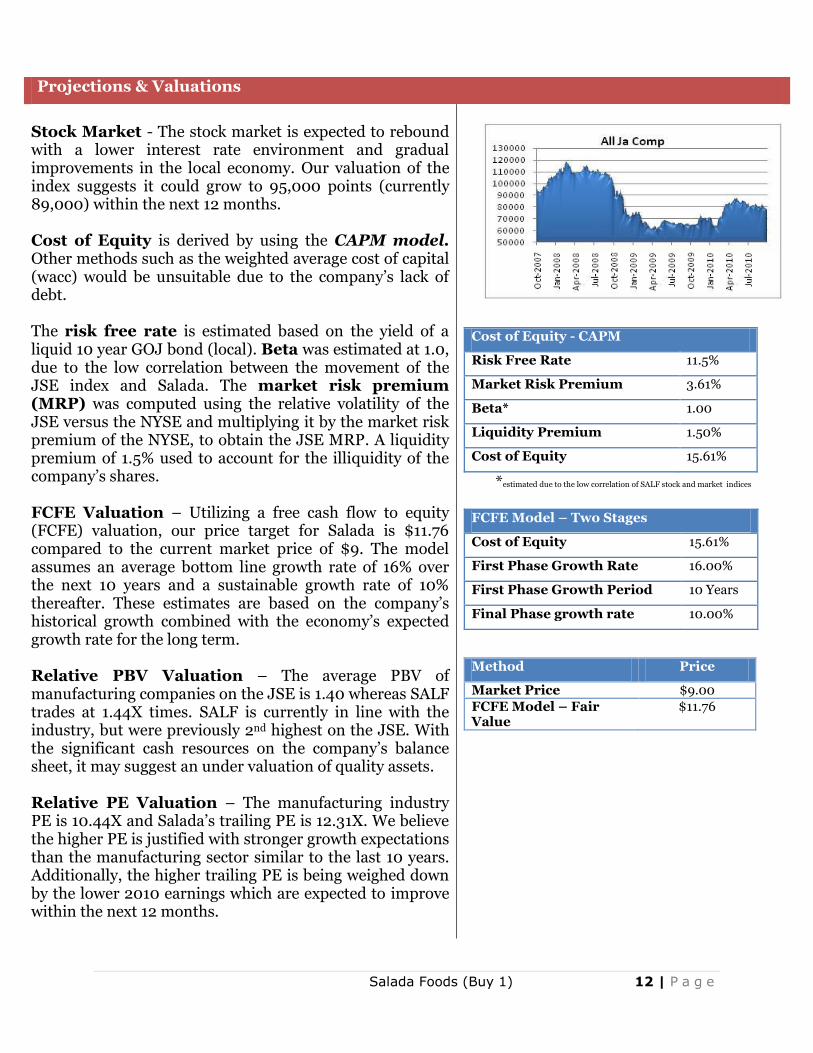

Stock Market - The stock market is expected to rebound with a lower interest rate environment and gradual improvements in the local economy. Our valuation of the index suggests it could grow to 95,000 points (currently 89,000) within the next 12 months. Cost of Equity is derived by using the CAPM model. Other methods such as the weighted average cost of capital (wacc) would be unsuitable due to the company’s lack of debt. The risk free rate is estimated based on the yield of a liquid 10 year GOJ bond (local). Beta was estimated at 1.0, due to the low correlation between the movement of the JSE index and Salada. The market risk premium (MRP) was computed using the relative volatility of the JSE versus the NYSE and multiplying it by the market risk premium of the NYSE, to obtain the JSE MRP. A liquidity premium of 1.5% used to account for the illiquidity of the company’s shares. FCFE Valuation – Utilizing a free cash flow to equity (FCFE) valuation, our price target for Salada is $11.76 compared to the current market price of $9. The model assumes an average bottom line growth rate of 16% over the next 10 years and a sustainable growth rate of 10% thereafter. These estimates are based on the company’s historical growth combined with the economy’s expected growth rate for the long term. Relative PBV Valuation – The average PBV of manufacturing companies on the JSE is 1.40 whereas SALF trades at 1.44X times. SALF is currently in line with the industry, but were previously 2nd highest on the JSE. With the significant cash resources on the company’s balance sheet, it may suggest an under valuation of quality assets. Relative PE Valuation – The manufacturing industry PE is 10.44X and Salada’s trailing PE is 12.31X. We believe the higher PE is justified with stronger growth expectations than the manufacturing sector similar to the last 10 years. Additionally, the higher trailing PE is being weighed down by the lower 2010 earnings which are expected to improve within the next 12 months.

Cost of Equity - CAPM

Risk Free Rate 11.5%

Market Risk Premium 3.61%

Beta* 1.00

Liquidity Premium 1.50%

Cost of Equity 15.61%

*estimated due to the low correlation of SALF stock and market indices

FCFE Model – Two Stages

Cost of Equity 15.61%

First Phase Growth Rate 16.00%

First Phase Growth Period 10 Years

Final Phase growth rate 10.00%

Method Price

Market Price $9.00

FCFE Model – Fair Value

$11.76

Salada Foods (Buy 1) 13 | P a g e

Technical Analysis

Momentum Indicators

Based on the low trading activity of the stock, momentum

indicators below could give misreading signals but are still

used as a guide.

Relative Strength Index (RSI) – The RSI is a

momentum indicator which suggests a buy reading when

below the 30 mark and sells above the 7o mark. At 41.73,

the indicator is in the hold zone.

Commodity Channel Index (CCI or CMCI) – Similar

to the RSI indicator, a buy rating is generated below -100

and a sell rating above 100. The signal is currently

between and suggests a hold.

RSI

CMCI

Salada Foods (Buy 1) 14 | P a g e

Recommendation

Salada has had a challenging 2010, stifled by weak consumer demand, increased production

costs and lower investment income after the JDX. Notwithstanding, our recommendation is

based on the following:

1. We expect the economy to resume growth within 12 months and the measures taken by

Salada should result in greater returns.

2. They are a dominant player in the instant coffee business and we believe they can

continue to grow their market and improving margins through the introduction of value

added products.

3. The company’s high cash balance and the attempt to buy Mavis Bank suggests the

company is looking for growth and expansion opportunities.

4. Our FCFE valuation model suggests the stock is valued 31% higher at $11.76.

5. PE and PBV relative valuations show that the stock is trading above the market (PE) and

in line with the market PBV respectively. We believe both valuations are justified and we

also expect that Salada’s profit growth will outpace the industry.

6. High cash resources suggest there could be a capital distribution i

With most factors being favourable for Salada and fair value which suggests the stock is

underpriced, at a market price of $9 which is 30% below the fair value of $11.76, we recommend

Salada as a BUY.

Salada Foods (Buy 1) 15 | P a g e

Appendix 1 – Financial Summary

J$ Millions 2005 2006 2007 2008 2009 2010 Last 12 M Q1 2010 Q1 2011 SEP 2011E SEP 2012E

Income Statement

Revenues 268.74 302.93 342.75 393.80 432.43 426.38 433.54 103.63 110.80 484.92 512.80

Cost of Revenue 185.30 192.53 201.11 230.98 234.78 260.15 266.80 62.51 69.16 303.07 320.50

Gross Profit 83.44 110.40 141.64 162.82 197.65 166.22 166.74 41.13 41.64 181.84 192.30

Other Operating Revenue 0.90 1.80 2.67 2.32 2.77 2.56 1.74 0.92 0.10 0.37 2.59

Selling, General & Admin Expense

69.49 63.68 55.88 72.27 75.18 77.38 80.53 20.71 23.86 78.94 81.39

Operating profit 14.84 48.52 88.44 92.87 125.24 91.40 87.96 21.33 17.89 103.28 113.50

Interest Expense 0.35 0.16 0.26 0.37 2.59 2.62 2.62 0.00 0.00

Interest Income 14.66 21.54 39.18 34.30 29.56 10.94 6.20 34.46 30.00

Pretax Income 5.57 56.09 102.83 114.03 161.84 123.09 114.90 32.27 24.09 137.73 143.50

Taxation 2.82 19.17 34.67 38.71 53.64 41.68 38.95 10.76 8.03 45.91 47.83

Net profit 27.45 36.93 68.17 75.33 108.20 81.41 75.95 21.52 16.06 91.82 95.66

Balance Sheet

Cash and Short Term Investments

68.279 96.405 162.833 163.827 275.675 303.411 291.207 273.117 291.207

Total Assets 228.016 255.788 327.661 401.082 526.89 604.953 595.414 523.099 595.414

Total Current Liabilities 37.486 34.11 41.458 42.538 57.676 68.519 42.561 63.527 42.561

Long Term Loans 22.412 17.266 12.262 7.211 1.311 0 0 0 0

Total Liabilities 54.752 50.339 54.046 52.139 69.752 97.551 71.955 75.603 71.955

Total Shareholders' Equity 173.264 205.449 273.615 348.943 457.138 507.402 523.459 447.496 523.459

Ratios

Gross Margin 31% 36% 41% 41% 46% 39% 38% 40% 38% 38% 38%

Operating Margin 6% 16% 26% 24% 29% 21% 20% 21% 16%

Net Margin 10% 12% 20% 19% 25% 19% 18% 21% 14%

ROA 12% 14% 21% 19% 21% 13% 13% 4% 3%

ROE 16% 20% 28% 24% 27% 17% 15% 5% 3%

Debt-to-Equity 13% 8% 4% 2% 0% 0% 0% 0% 0%

Interest Coverage 42.41 299.50 340.13 249.64 48.43 34.94 33.62

Financial Leverage 1.32 1.25 1.20 1.15 1.15 1.19 1.14 0.00 0.00

Current Ratio 4.21 5.61 6.44 7.93 8.04 7.62 12.03 7.23 12.03

Per Share Data

Book Value per Share 1.67 1.98 2.63 3.36 4.40 5.40 6.40 6.40 7.40 4.50

Revenue Per Share 2.59 2.92 3.30 3.79 4.16 4.10 4.17 1.00 1.07 1.03

Earnings Per Share 0.26 0.36 0.66 0.73 1.04 0.78 0.73 0.21 0.15 0.76 0.92

Free Cash Flow Per Share -0.15 0.21 0.51 -0.18 0.76 0.00 0.00 0.00 0.00 10.00

Price 22 26 67 92 10.75 11.75 9 12.75 9

Valuation Metrics

Price To Book Value 0.13 1.31 2.54 2.74 2.44 2.18 1.41 1.99 1.22 2.22

Price to Revenue Per Share

0.85 0.89 2.03 2.43 2.58 2.86 2.16 12.78 8.44

Price to Earnings per Share

8.33 7.31 10.21 12.69 10.32 14.99 12.31 61.56 14.56

Salada Foods (Buy 1) 16 | P a g e

Bibliography

Author Website

Jamaica Stock Exchange www.jamstockex.com

International Monetary Fund (IMF) www.imf.org

Bank of Jamaica www.boj.org.jm

Planning Institute of Jamaica www.pioj.gov.jm

Statistical Institute of Jamaica www.statinja.com

Business Monitor International www.businessmonitor.com

Bloomberg (Terminal) www.bloomberg.com

Investopedia www.investopedia.com

Coffee Industry Board www.ciboj.org

Salada Foods Jamaica Limited www.saladafoods.com