santander brazil credit conference 2016

TRANSCRIPT

Santander Brazil Credit Conference April, 2016

2

The information contained in this presentation may include statements whichconstitute forward-looking statements, within the meaning of Section 27A of the U.S.Securities Act of 1933, as amended, and Section 21E of the U.S. Securities ExchangeAct of 1934, as amended. Such forward-looking statements involve a certain degree ofrisk and uncertainty with respect to business, financial, trend, strategy and otherforecasts, and are based on assumptions, data or methods that, although consideredreasonable by the company at the time, may turn out to be incorrect or imprecise, ormay not be possible to realize. The company gives no assurance that expectationsdisclosed in this presentation will be confirmed. Prospective investors are cautionedthat any such forward-looking statements are not guarantees of future performanceand involve risks and uncertainties, and that actual results may differ materially fromthose in the forward-looking statements, due to a variety of factors, including, but notlimited to, the risks of international business and other risks referred to in thecompany’s filings with the CVM and SEC. The company does not undertake, andspecifically disclaims any obligation to update any forward-looking statements, whichspeak only for the date on which they are made.

Disclaimer

3

Pulp and Paper Market2Financial and Operational Highlights3

Agenda

Company Overview1

Expansion Project – Horizonte 24Dividends5Cost reduction initiatives and industry statistics 6

4

Company Overview

5

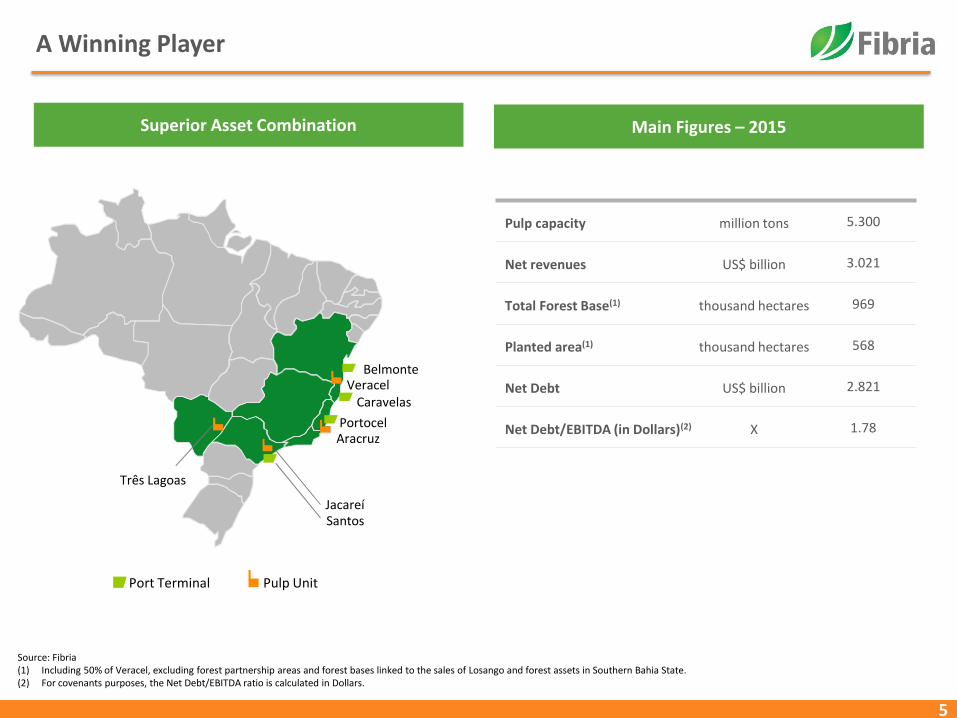

A Winning Player

Port Terminal Pulp Unit

Três Lagoas

Santos

AracruzPortocel

Caravelas

BelmonteVeracel

Jacareí

Superior Asset Combination Main Figures – 2015

Pulp capacity million tons 5.300

Net revenues US$ billion 3.021

Total Forest Base(1) thousand hectares 969

Planted area(1) thousand hectares 568

Net Debt US$ billion 2.821

Net Debt/EBITDA (in Dollars)(2) X 1.78

Source: Fibria(1) Including 50% of Veracel, excluding forest partnership areas and forest bases linked to the sales of Losango and forest assets in Southern Bahia State. (2) For covenants purposes, the Net Debt/EBITDA ratio is calculated in Dollars.

6

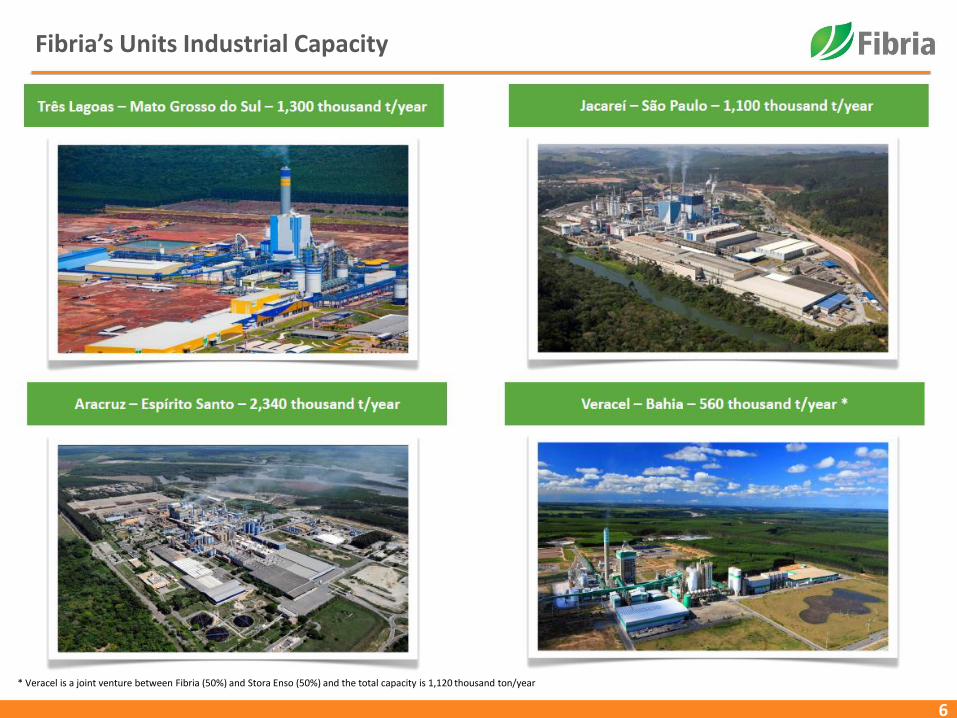

Fibria’s Units Industrial Capacity

* Veracel is a joint venture between Fibria (50%) and Stora Enso (50%) and the total capacity is 1,120 thousand ton/year

7

Worldwide presence

Strong global customer base

Long-term relationships

Focus on customers with stable business

Customized pulp products and services

Sound forestry and industrial R&D

Focus on less volatile end-use markets such as tissue

Efficient logistics set up

Low dependence on volatile markets such as China

Low credit risk

100% certified pulp (FSC and PEFC/Cerflor)

Sales Mix by End Use - Fibria Highlights

Fibria’s Commercial Strategy

Net Revenues by Region - Fibria

Region - 4Q15 End Use - 4Q15

42% 37%43% 43%

35% 36%46% 42% 39% 40%

47% 42% 42% 42%

26%30% 22%

29%31% 31%

19% 23% 27% 27% 17% 24% 25% 29%

22% 25% 26%21%

25% 26% 26% 27% 24% 23% 26% 26% 25% 20%

10% 9% 10% 8% 9% 8% 10% 9% 10% 10% 10% 9% 8% 9%

3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Europe North America Asia Other

50%

35%

15%

Printing & Writing

Specialties

TissueEurope

42%

N. America

29%

Asia20%LatAm

9%

8

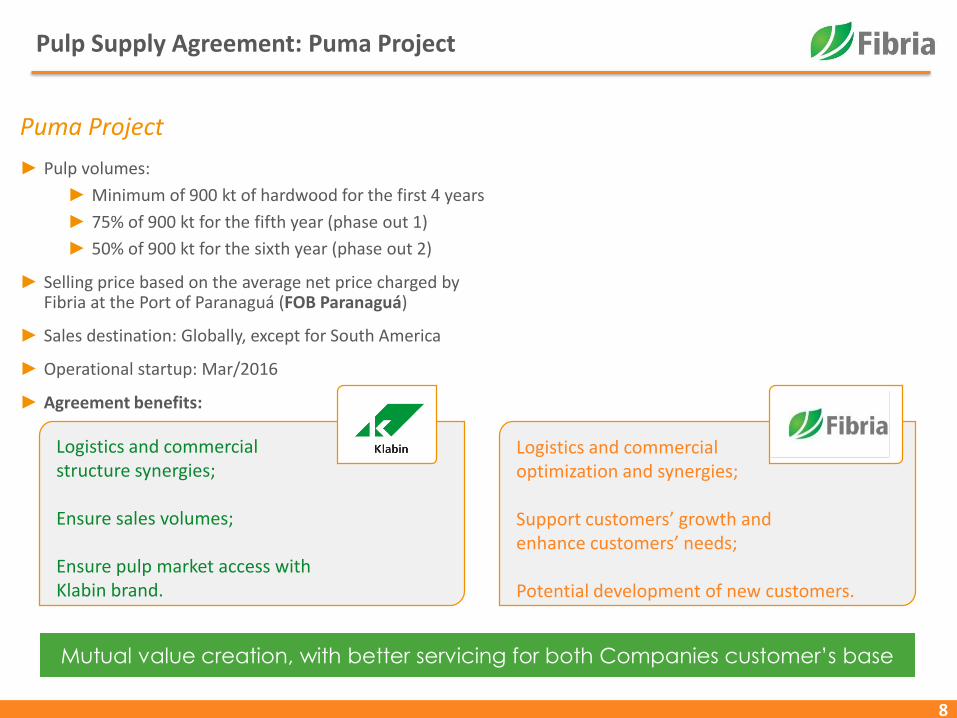

Pulp Supply Agreement: Puma Project

► Pulp volumes:

► Minimum of 900 kt of hardwood for the first 4 years

► 75% of 900 kt for the fifth year (phase out 1)

► 50% of 900 kt for the sixth year (phase out 2)

► Selling price based on the average net price charged by Fibria at the Port of Paranaguá (FOB Paranaguá)

► Sales destination: Globally, except for South America

► Operational startup: Mar/2016

► Agreement benefits:

Puma Project

Mutual value creation, with better servicing for both Companies customer’s base

Logistics and commercial structure synergies;

Ensure sales volumes;

Ensure pulp market access with Klabin brand.

Logistics and commercial optimization and synergies;

Support customers’ growth and enhance customers’ needs;

Potential development of new customers.

9

Pulp and Paper Market

10

The “better than expected scenario” has become a reality again in 2015…

BHKP CAPACITY CHANGES

EXPECTED SCENARIO FOR 2015 IN DEC’14 REALIZED SCENARIO IN 2015

1,095

-315

-65

115

85

30

200

750

265

750

400

BEKP demand growth**

Net

Possible closures*

Ence Huelva

April Rizhao

Sappi Cloquet

Old Town (Expera)

Portucel Cacia

Eldorado

CMPC Guaiba II

Oji Nantong

Montes del Plata

Suzano Maranhão

-400 to -800

1,415 to 1,815

*Based on annual closures average (400,000 to 800,000 t/yr)

**Source: PPPC Outlook for Eucalyptus Market Pulp December 2014

1,232

1,450

-400

-315

-190

115

40

40

30

200

500

265

750

400

BEKP demand growth**

Net

Unexpected Downtimes

Ence Huelva

April Rizhao

Sappi Cloquet

Ence Navia

Old Town (Expera)

Portucel Cacia

Eldorado

CMPC Guaiba II

Oji Nantong

Montes del Plata

Suzano Maranhão

Indonesia, China,

Uruguay and Brazil

**Source: PPPC Market Pulp World 20

11

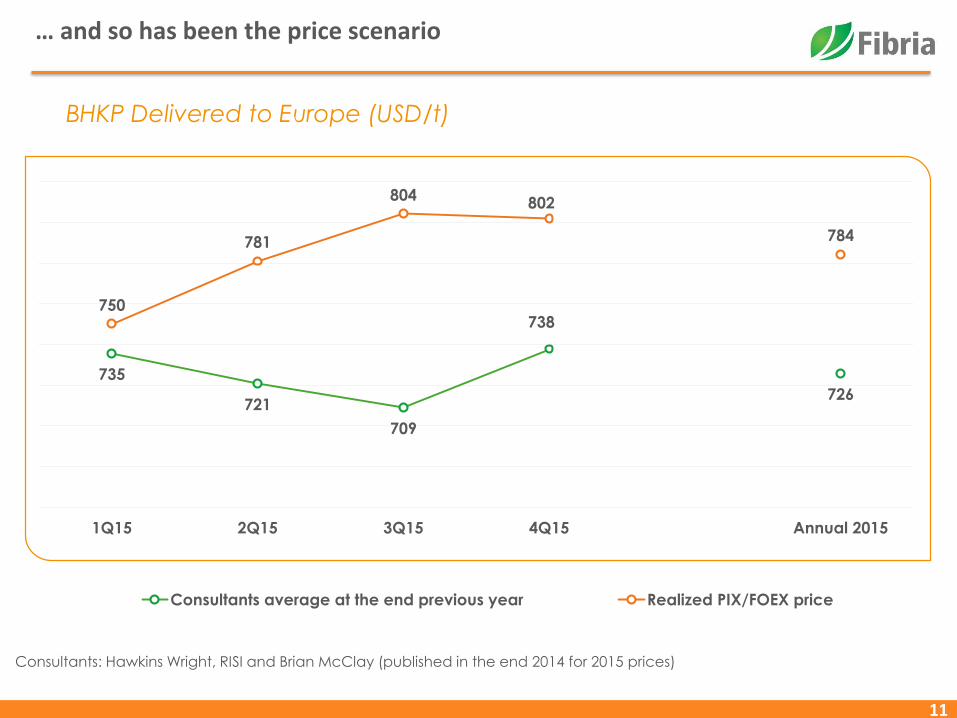

… and so has been the price scenario

BHKP Delivered to Europe (USD/t)

735

721

709

738

726

750

781

804802

784

1Q15 2Q15 3Q15 4Q15 Annual 2015

Consultants average at the end previous year Realized PIX/FOEX price

Consultants: Hawkins Wright, RISI and Brian McClay (published in the end 2014 for 2015 prices)

12

Better worldwide macroeconomics are the key drivers… But the special focus is on Europe

Real GDP % Annual Growth

Source: International Monetary Fund, World Economic Outlook Database, January 2016

3.4

-0.8

2.2

7.7

3.3

-0,3

1.5

7.7

3.4

0.9

2.4

7.3

3.1

1.5

2.4

6.9

3.5

1.7

2.4

6.3

World Euro Area USA China

2012 2013 2014 2015 2016

13

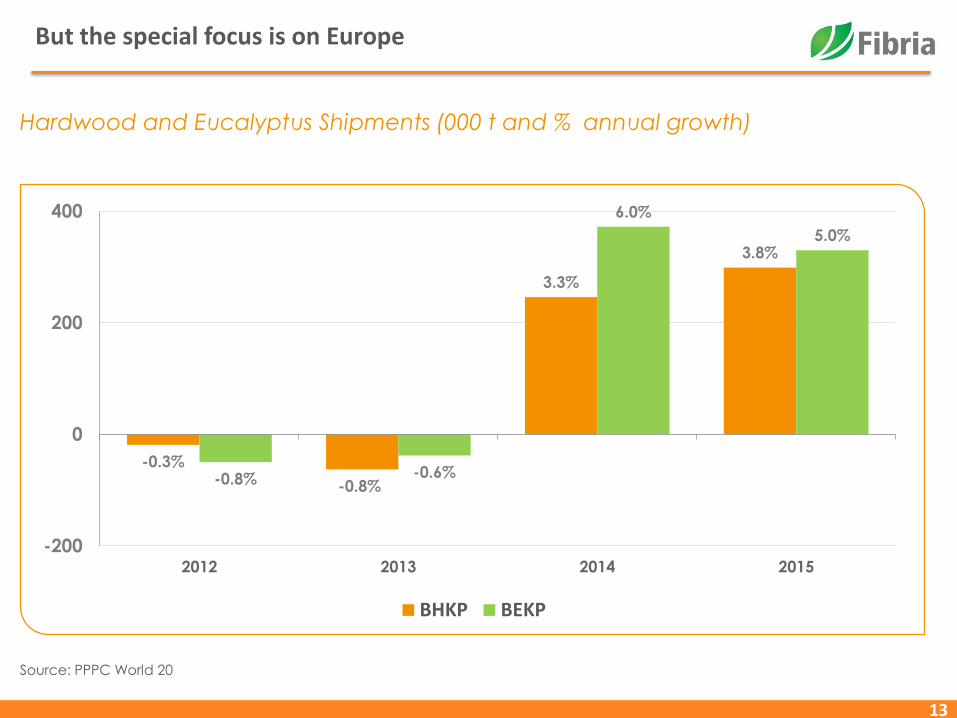

But the special focus is on Europe

Hardwood and Eucalyptus Shipments (000 t and % annual growth)

Source: PPPC World 20

-0.3%

-0.8%

3.3%

3.8%

-0.8% -0.6%

6.0%

5.0%

-200

0

200

400

2012 2013 2014 2015

BHKP BEKP

14

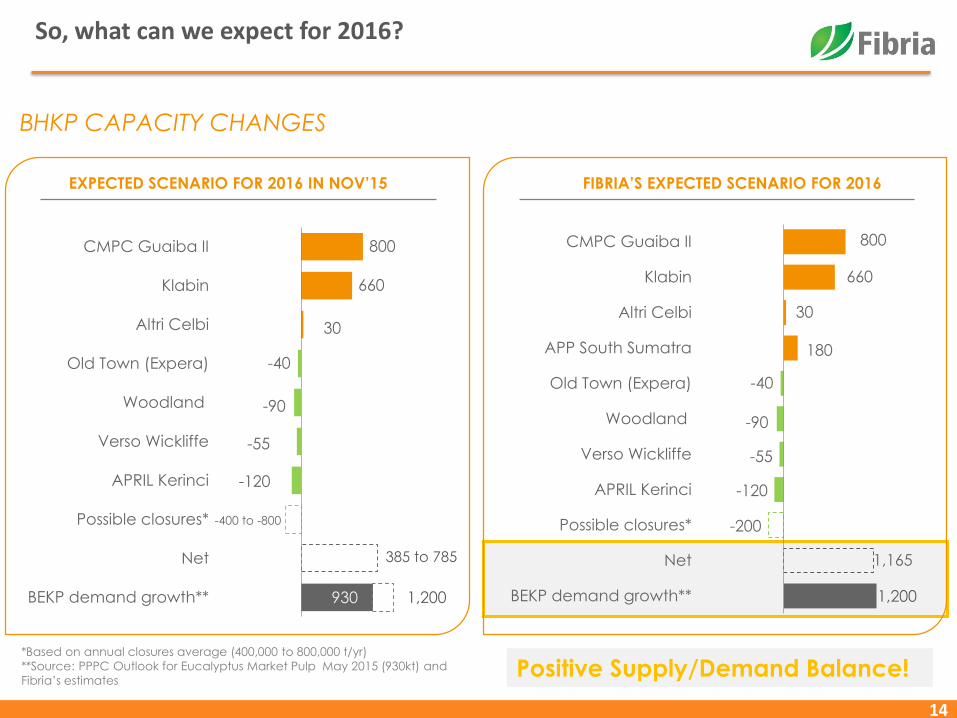

So, what can we expect for 2016?

BHKP CAPACITY CHANGES

EXPECTED SCENARIO FOR 2016 IN NOV’15 FIBRIA’S EXPECTED SCENARIO FOR 2016

930

-120

-55

-90

-40

30

660

800

BEKP demand growth**

Net

Possible closures*

APRIL Kerinci

Verso Wickliffe

Woodland

Old Town (Expera)

Altri Celbi

Klabin

CMPC Guaiba II

-400 to -800

385 to 785

1,200

*Based on annual closures average (400,000 to 800,000 t/yr)

**Source: PPPC Outlook for Eucalyptus Market Pulp May 2015 (930kt) and

Fibria’s estimates

1,200

1,165

-200

-120

-55

-90

-40

180

30

660

800

BEKP demand growth**

Net

Possible closures*

APRIL Kerinci

Verso Wickliffe

Woodland

Old Town (Expera)

APP South Sumatra

Altri Celbi

Klabin

CMPC Guaiba II

Positive Supply/Demand Balance!

15

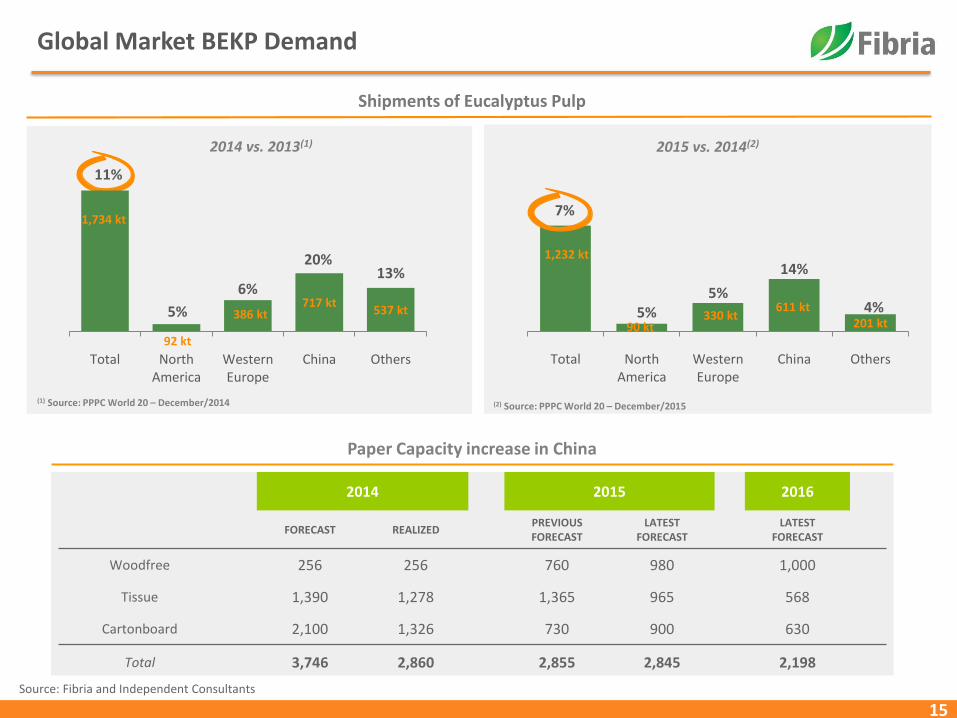

1,232 kt

90 kt330 kt

611 kt201 kt

7%

5%5%

14%

4%

Total NorthAmerica

WesternEurope

China Others

Shipments of Eucalyptus Pulp

(1) Source: PPPC World 20 – January/2015

Global Market BEKP Demand

Paper Capacity increase in China

2014 2015 2016

FORECAST REALIZEDPREVIOUS FORECAST

LATEST FORECAST

LATEST FORECAST

Woodfree 256 256 760 980 1,000

Tissue 1,390 1,278 1,365 965 568

Cartonboard 2,100 1,326 730 900 630

Total 3,746 2,860 2,855 2,845 2,198

Source: Fibria and Independent Consultants

2015 vs. 2014(2)

(1) Source: PPPC World 20 – December/2014 (2) Source: PPPC World 20 – December/2015

1,734 kt

92 kt

386 kt717 kt

537 kt

11%

5%

6%

20%13%

Total NorthAmerica

WesternEurope

China Others

2014 vs. 2013(1)

16

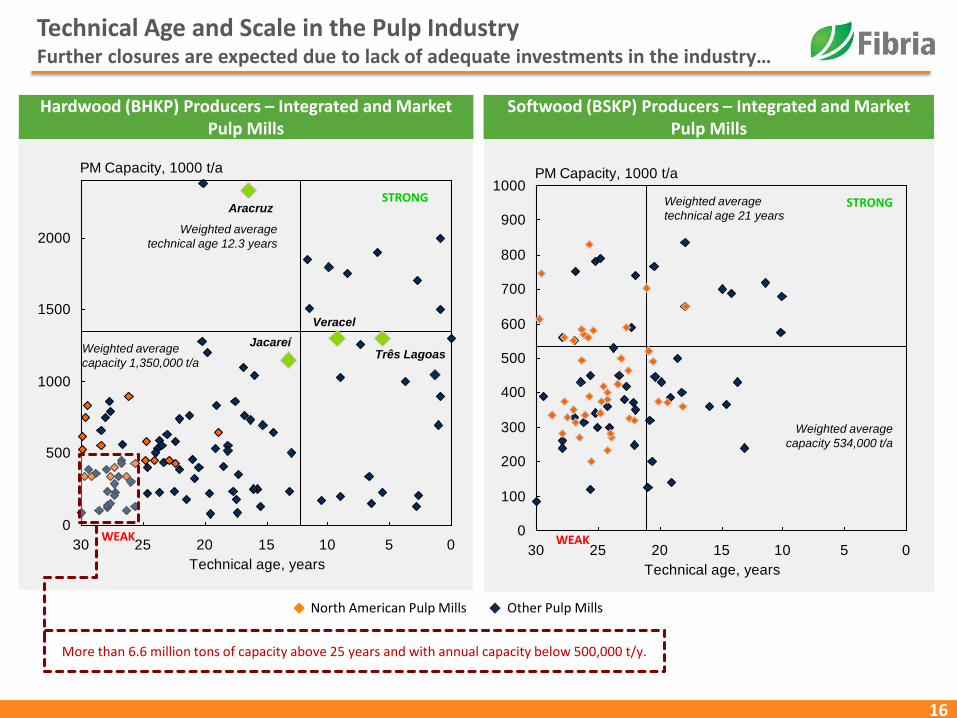

Technical Age and Scale in the Pulp IndustryFurther closures are expected due to lack of adequate investments in the industry…

Hardwood (BHKP) Producers – Integrated and Market Pulp Mills

Softwood (BSKP) Producers – Integrated and Market Pulp Mills

STRONG

Weighted average

technical age 12.3 years

Weighted average

capacity 1,350,000 t/a

Aracruz

Três Lagoas

Veracel

Jacareí

WEAK

STRONGWeighted average

technical age 21 years

Weighted average

capacity 534,000 t/a

North American Pulp Mills Other Pulp Mills

WEAK

More than 6.6 million tons of capacity above 25 years and with annual capacity below 500,000 t/y.

PM Capacity, 1000 t/a

0

500

1000

1500

2000

051015202530

Technical age, years

PM Capacity, 1000 t/a

0

100

200

300

400

500

600

700

800

900

1000

051015202530

Technical age, years

17

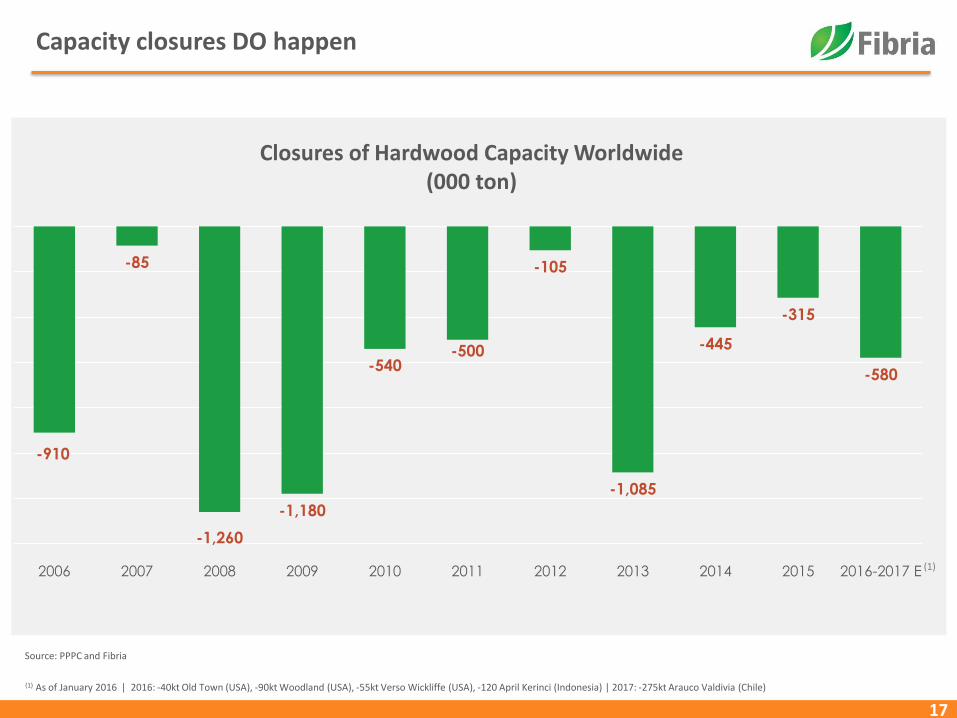

Source: PPPC and Fibria

Closures of Hardwood Capacity Worldwide(000 ton)

Capacity closures DO happen

-910

-85

-1,260

-1,180

-540-500

-105

-1,085

-445

-315

-580

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016-2017 E (1)

(1) As of January 2016 | 2016: -40kt Old Town (USA), -90kt Woodland (USA), -55kt Verso Wickliffe (USA), -120 April Kerinci (Indonesia) | 2017: -275kt Arauco Valdivia (Chile)

18

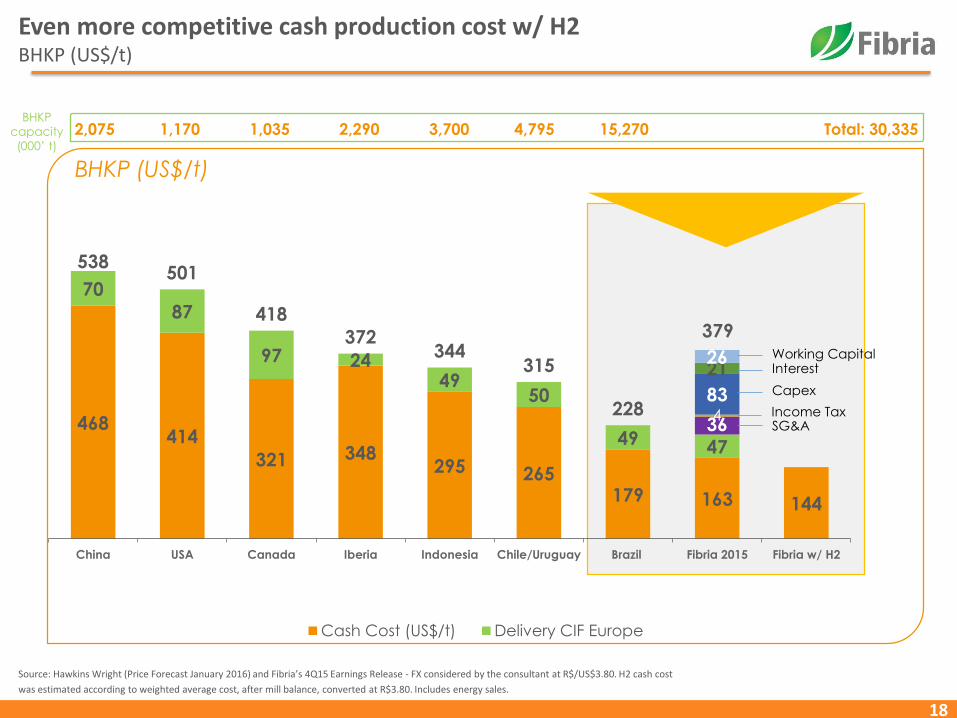

Even more competitive cash production cost w/ H2 BHKP (US$/t)

Source: Hawkins Wright (Price Forecast January 2016) and Fibria’s 4Q15 Earnings Release - FX considered by the consultant at R$/US$3.80. H2 cash cost

was estimated according to weighted average cost, after mill balance, converted at R$3.80. Includes energy sales.

468414

321 348295 265

179 163 144

70

87

97 2449

50

49 47

538501

418

372344

315

228364

83

2126

379

China USA Canada Iberia Indonesia Chile/Uruguay Brazil Fibria 2015 Fibria w/ H2

Cash Cost (US$/t) Delivery CIF Europe

BHKP (US$/t)

Interest

Capex

SG&AIncome Tax

2,075 1,170 1,035 2,290 3,700 4,795 15,270 Total: 30,335BHKP

capacity

(000’ t)

Working Capital

19

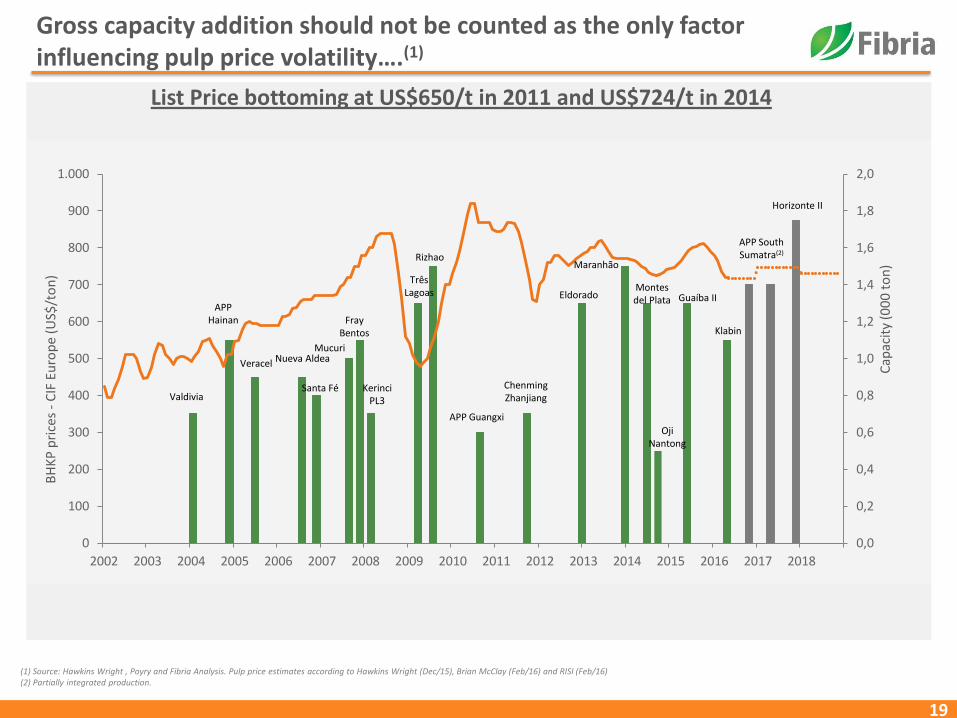

Gross capacity addition should not be counted as the only factorinfluencing pulp price volatility….(1)

List Price bottoming at US$650/t in 2011 and US$724/t in 2014

Cap

acit

y (0

00

to

n)

0,0

0,2

0,4

0,6

0,8

1,0

1,2

1,4

1,6

1,8

2,0

0

100

200

300

400

500

600

700

800

900

1.000

2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018

Valdivia

APP Hainan

Veracel Nueva Aldea

Santa Fé

Mucuri

FrayBentos

KerinciPL3

Três Lagoas

Rizhao

APP Guangxi

ChenmingZhanjiang

EldoradoMontes del Plata

Maranhão

Guaíba II

APP South Sumatra(2)

Klabin

OjiNantong

Horizonte II

BH

KP

pri

ces

-C

IF E

uro

pe

(U

S$/t

on

)

(1) Source: Hawkins Wright , Poyry and Fibria Analysis. Pulp price estimates according to Hawkins Wright (Dec/15), Brian McClay (Feb/16) and RISI (Feb/16)(2) Partially integrated production.

In the last 15 years, pulp volatility has been just 8%...why?

20

► Market price closer to producer’s marginal cost

► The marginal cost producers are based in Europe and North America

► Flattish industry cost curve

► Higher flexibility to adjust supply side during imbalanced market

► Lower dependency on Asian market (~25%) compared to hard commodities (70%+)

► Market end users are linked to consumer goods, such as tissue

► Incipient pulp price futures market and low liquidity

Source: Bloomberg – March 22th, 2016

0

40

80

120

160

De

c-9

9

May

-00

Oct

-00

Mar

-01

Au

g-0

1

Jan

-02

Jun

-02

No

v-0

2

Ap

r-0

3

Sep

-03

Feb

-04

Jul-

04

De

c-0

4

May

-05

Oct

-05

Mar

-06

Au

g-0

6

Jan

-07

Jun

-07

No

v-0

7

Ap

r-0

8

Sep

-08

Feb

-09

Jul-

09

De

c-0

9

May

-10

Oct

-10

Mar

-11

Au

g-1

1

Jan

-12

Jun

-12

No

v-1

2

Ap

r-1

3

Sep

-13

Feb

-14

Jul-

14

De

c-1

4

May

-15

Oct

-15

Mar

-16

BHKP - FOEX Europe (base 100) CPI (base 100)

21

Lowest volatility among commodities

Source: Bloomberg – March 31, 2016

Low volatility of hardwood pulp price, even though

new capacities have come on stream during the period.

2535455565758595

105115125135145155165175185195205215225

Jan

-12

Ma

r-1

2

Ma

y-1

2

Jul-1

2

Se

p-1

2

No

v-1

2

Jan

-13

Ma

r-1

3

Ma

y-1

3

Jul-1

3

Se

p-1

3

No

v-1

3

Jan

-14

Ma

r-1

4

Ma

y-1

4

Jul-1

4

Se

p-1

4

No

v-1

4

Jan

-15

Ma

r-1

5

Ma

y-1

5

Jul-1

5

Se

p-1

5

No

v-1

5

Jan

-16

Ma

r-1

6

Iron Ore Soy Bean Crude Oil Sugar BHKP - FOEX Europe Exchange Rate (R$/US$)

113

190

76

66

3939

100 = January 1, 2012

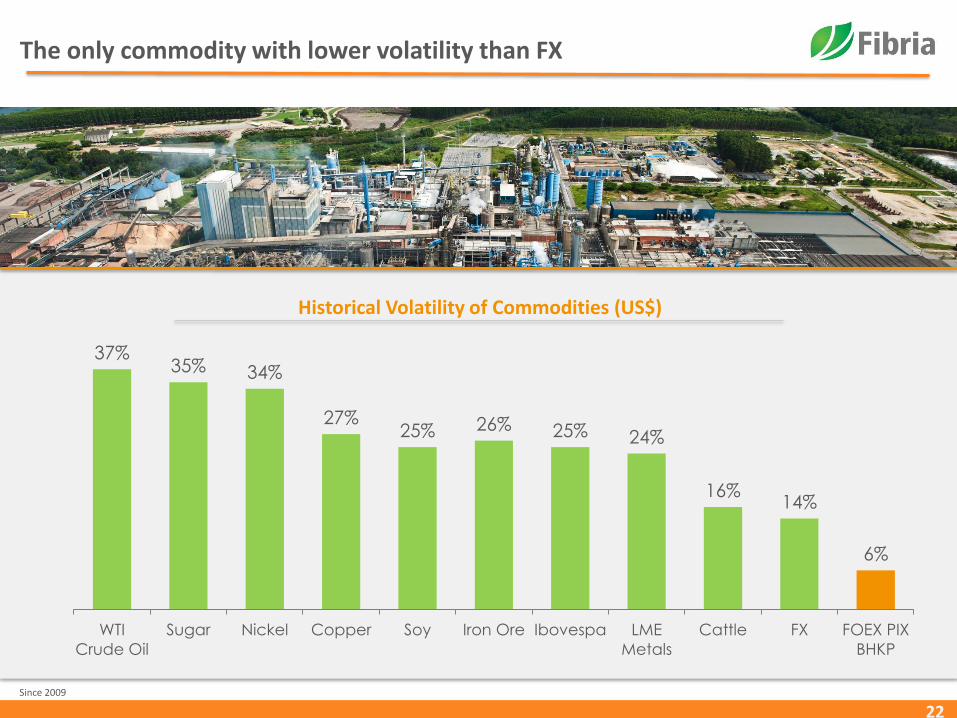

The only commodity with lower volatility than FX

Historical Volatility of Commodities (US$)

Since 2009

22

37%35% 34%

27%25% 26% 25% 24%

16%14%

6%

WTI

Crude Oil

Sugar Nickel Copper Soy Iron Ore Ibovespa LME

Metals

Cattle FX FOEX PIX

BHKP

23

Financial and Operational Highlights

24

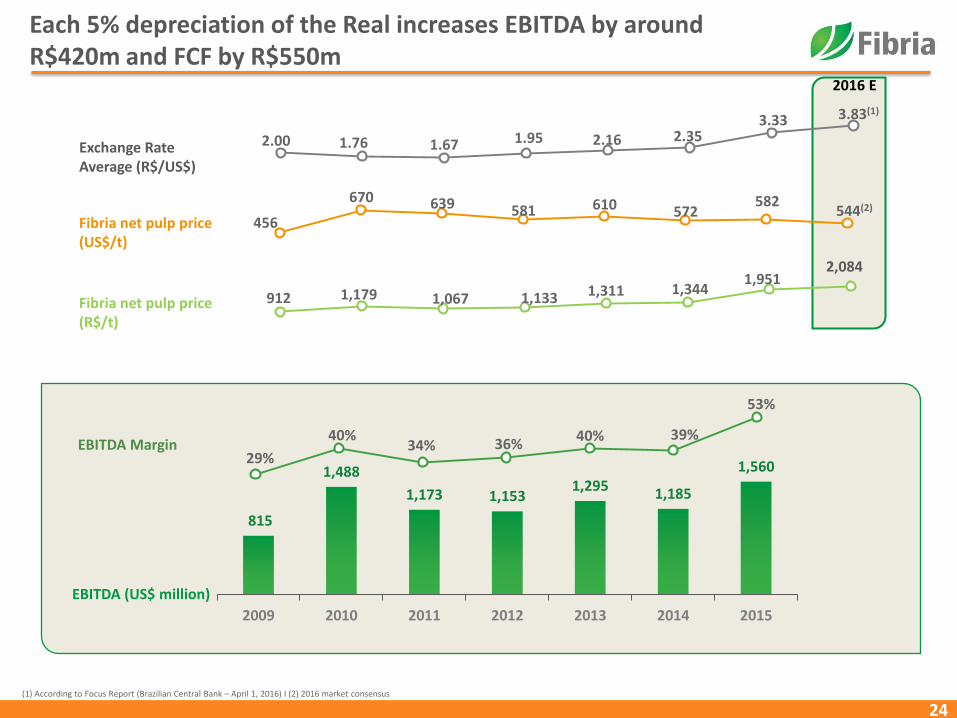

Each 5% depreciation of the Real increases EBITDA by aroundR$420m and FCF by R$550m

815

1,488

1,173 1,1531,295 1,185

1,560

2009 2010 2011 2012 2013 2014 2015

Exchange Rate Average (R$/US$)

EBITDA Margin

EBITDA (US$ million)

Fibria net pulp price(US$/t)

Fibria net pulp price(R$/t)

2.00 1.76 1.67 1.95 2.16 2.35 3.33 3.83(1)

456

670 639 581 610 572 582

544(2)

29%

40%34% 36%

40% 39%

53%

912 1,179 1,067 1,133 1,311 1,3441,951

2,084

(1) According to Focus Report (Brazilian Central Bank – April 1, 2016) I (2) 2016 market consensus

2016 E

25

Cash Production Cost (US$/t) – 4Q15

186171

148

11

(56) 610

113

(14)(10)

4Q14 Inflation FX Lowerenergy price

Maintenancedowntime

Non recurringwood

Non recurringenergy

consumption

Cash cost4Q15

Total nonrecurring

Maintenancedowntime

4Q15 recurringcash cost

ex-downtime

Management initiatives gains partially offset the inflation impact

Fibria Cash Production Cost(1) (US$/ton)

Consistently controlling the

cash production

cost

26

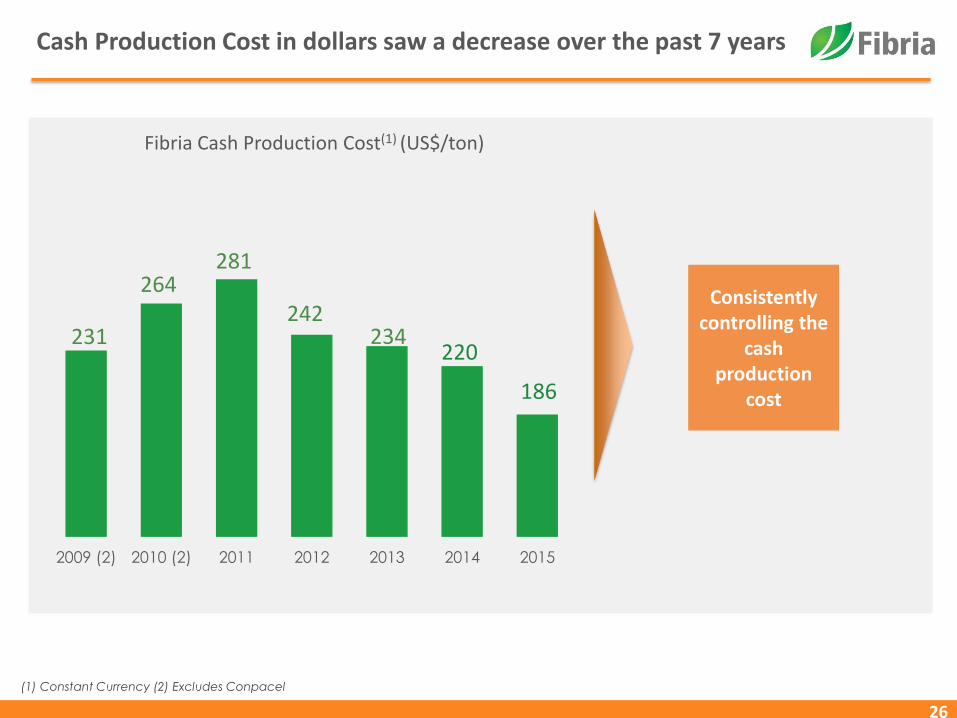

Cash Production Cost in dollars saw a decrease over the past 7 years

231

264281

242234

220

186

2009 (2) 2010 (2) 2011 2012 2013 2014 2015

(1) Constant Currency (2) Excludes Conpacel

27

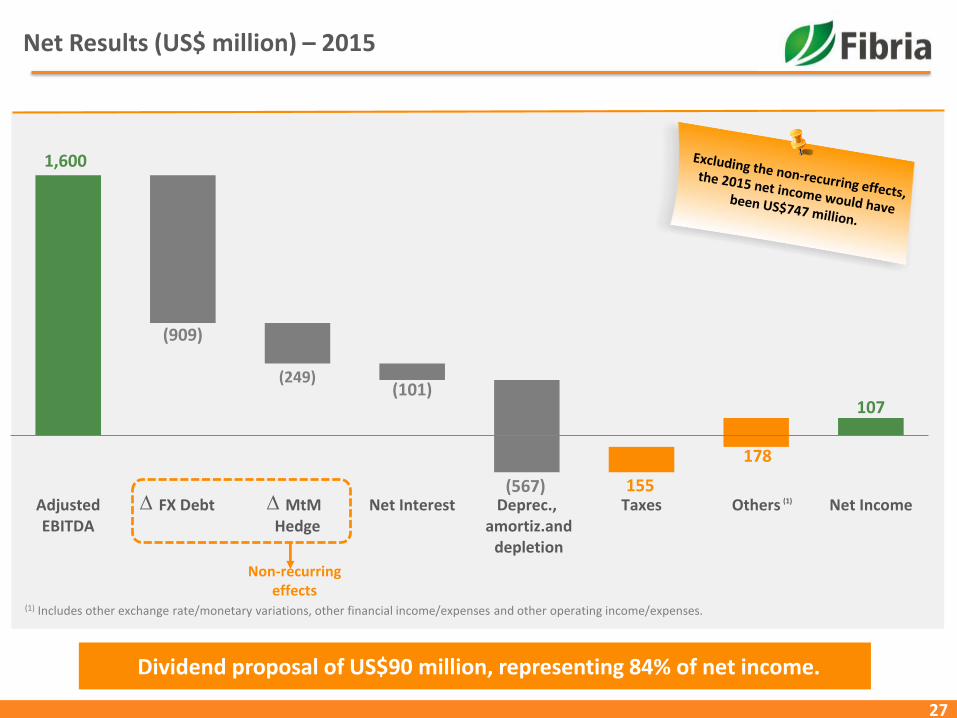

Net Results (US$ million) – 2015

1,600

107

(909)

(249)(101)

-0,227

155

-

(567)

178

AdjustedEBITDA

FX Debt MtMHedge

Net Interest Deprec., amortiz.and

depletion

Taxes Others Net Income

Non-recurringeffects

(1) Includes other exchange rate/monetary variations, other financial income/expenses and other operating income/expenses.

∆∆ (1)

Dividend proposal of US$90 million, representing 84% of net income.

Free Cash Flow

28(1) Before expansion capex

US$ million

EBITDA Margin

Average FX

-256

-77

-7

125

2977

194

84113

53

329

4

11151

103130

112

317

225

2Q11 3Q11 4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

34% 33% 28% 30% 37% 37% 41% 39% 39% 41% 42% 41% 35% 35% 45% 50% 50% 56%

1.60 1.63 1.80 1.77 1.96 2.03 2.06 2.00 2.07 2.29 2.27 2.37 2.23 2.27 2.55 2.87 3.07 3.54

54%

3.84

29

Free Cash Flow(1) – 2015

US$ million

1,600

859

636

(484) (89)(151) (23) 6

( 223 )

AdjustedEBITDA

Capex(ex-H2 project &

land deal)

NetInterest

WorkingCapital

Taxes Others FCF(ex-H2 project &

land deal)

CapexH2 &

land deal

FCF

(3)

(1) Not considering dividend payments, capex related to the Horizonte 2 Project and the land acquisition in December 2015.(2) Not considering dividend payments.(3) Includes other financial results.

30

ROE and ROIC (US$)

30

ROE = Adjusted EBIT(1)/ Equity before IAS 41(2)

4.8%3.4%

5.7% 6.2%

25.1%

32.0%

2011 2012 2013 2014 2015 Annualized4Q15 US$

ROIC = Adjusted EBIT(3)/ Invested Capital before IAS 41(2)

(1) Adjusted EBITDA – CAPEX – Net Interest – Taxes (2) International accounting standards for biological assets.(3) Adjusted EBITDA – CAPEX – Taxes

3.9%

6.9%9.2%

8.0%

22.8%

29.2%

2011 2012 2013 2014 2015 Annualized4Q15 US$

1.67 1.95 2.16 2.35 3.34 3.84 1.67 1.95 2.16 2.35 3.34AverageFX

3.84AverageFX

31

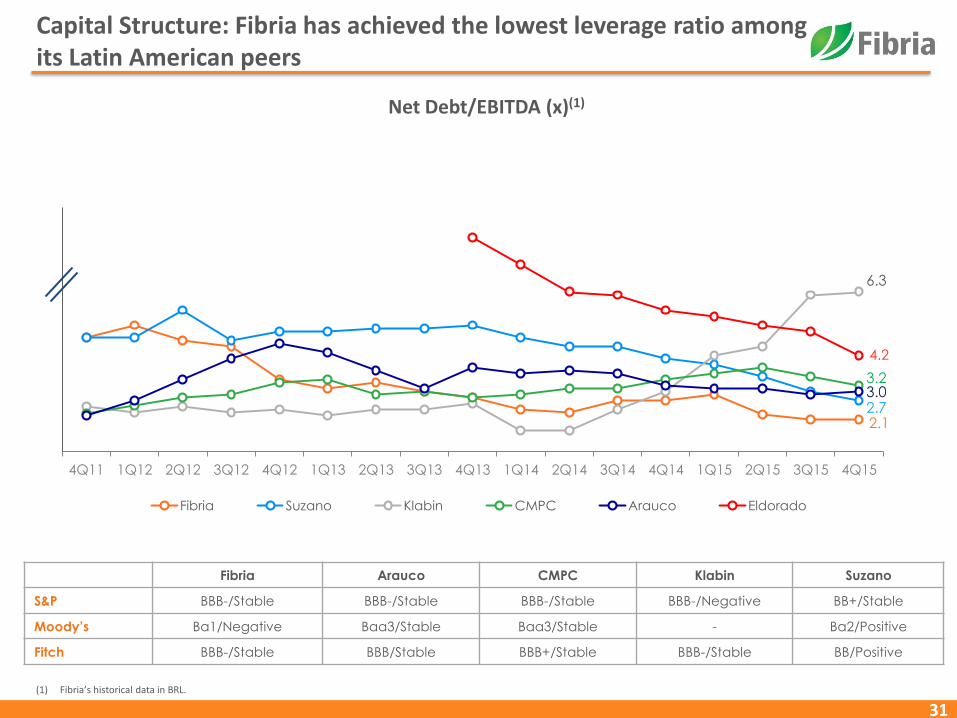

Capital Structure: Fibria has achieved the lowest leverage ratio among its Latin American peers

Net Debt/EBITDA (x)(1)

Fibria Arauco CMPC Klabin Suzano

S&P BBB-/Stable BBB-/Stable BBB-/Stable BBB-/Negative BB+/Stable

Moody’s Ba1/Negative Baa3/Stable Baa3/Stable - Ba2/Positive

Fitch BBB-/Stable BBB/Stable BBB+/Stable BBB-/Stable BB/Positive

(1) Fibria’s historical data in BRL.

2.12.7

6.3

3.23.0

4.2

4Q11 1Q12 2Q12 3Q12 4Q12 1Q13 2Q13 3Q13 4Q13 1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15

Fibria Suzano Klabin CMPC Arauco Eldorado

32

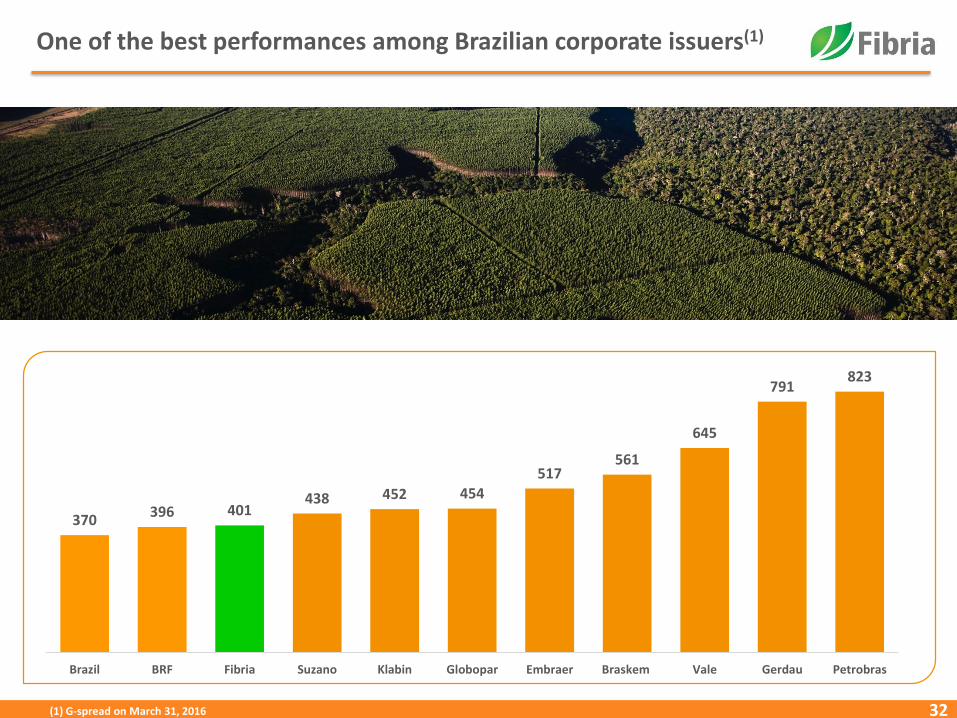

One of the best performances among Brazilian corporate issuers(1)

(1) G-spread on March 31, 2016

370396 401

438 452 454

517561

645

791823

Brazil BRF Fibria Suzano Klabin Globopar Embraer Braskem Vale Gerdau Petrobras

33

200

400

600

800

1.000

1.200

1.400

2010 2011 2012 2013 2014 2015

Fibria 2020 Fibria 2021 Fibria 2024

Interest expense, leverage and average cost of debt in US$ Historical G-spread (bps)

Strong credit quality

7.29

4.11 4.25

3.32

2.602.41

1.78

Leverage(x)

6.3 5.95.5

5.24.6

3.4 3.3(1)

6.3 5.95.5

5.24.6

3.4 3.3(1)

Cost of debt

473414 408

350

268200

141

2009 2010 2011 2012 2013 2014 2015

Interest Expense

(US$ million)Cost of debt (%)

BBB- BBB- Ba1

34

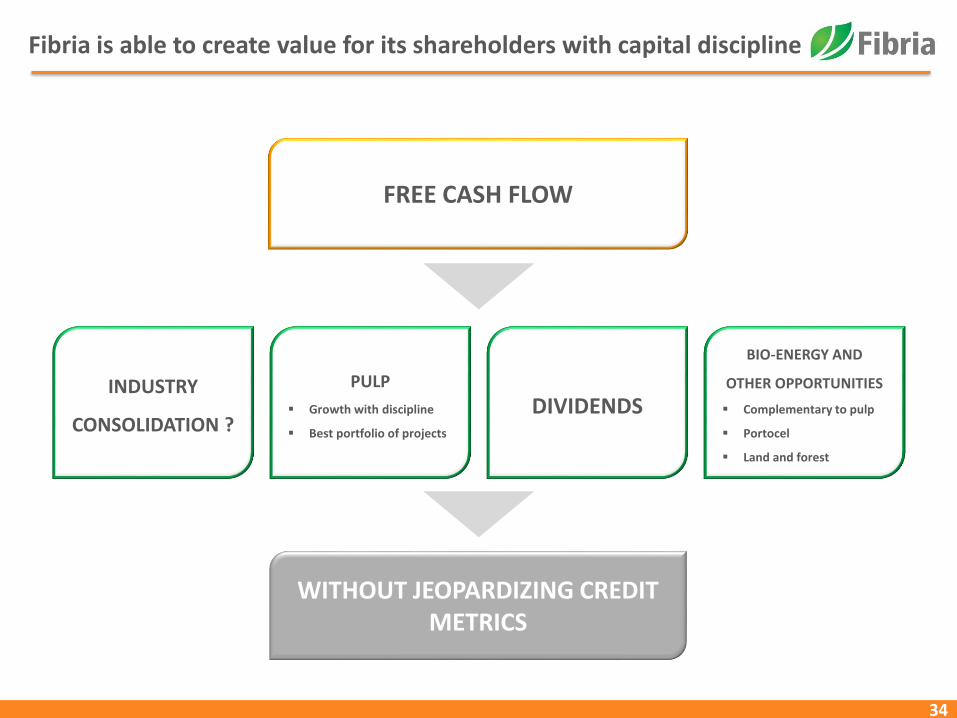

Fibria is able to create value for its shareholders with capital discipline

INDUSTRY

CONSOLIDATION ?

PULP

Growth with discipline

Best portfolio of projects

DIVIDENDS

BIO-ENERGY AND

OTHER OPPORTUNITIES

Complementary to pulp

Portocel

Land and forest

FREE CASH FLOW

WITHOUT JEOPARDIZING CREDIT METRICS

35

BACK UP

36

Expansion Project – Horizonte 2

37

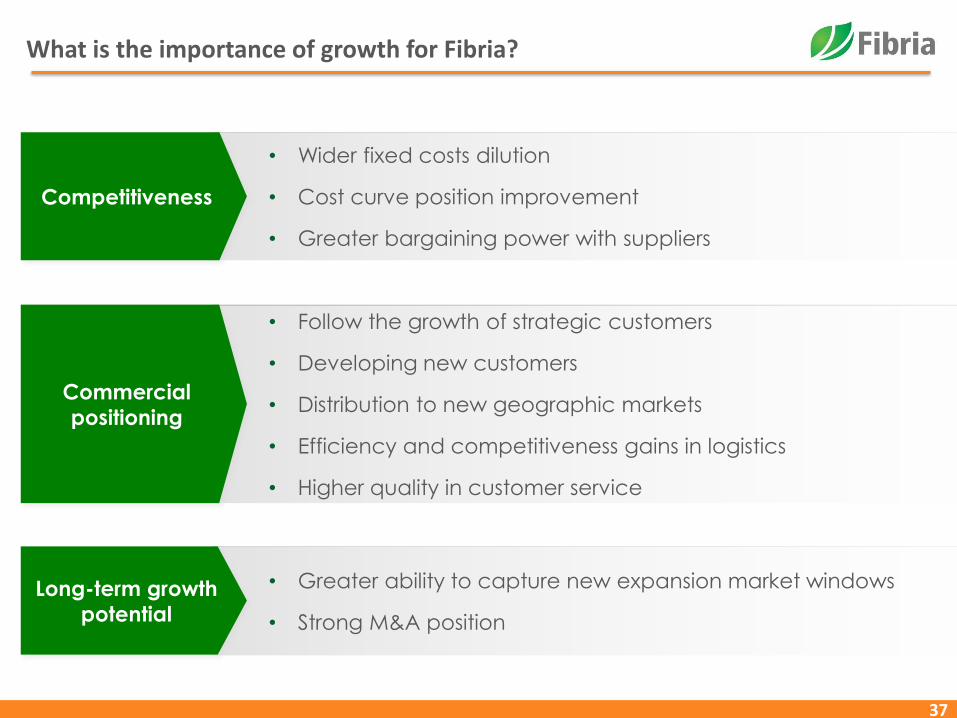

• Follow the growth of strategic customers

• Developing new customers

• Distribution to new geographic markets

• Efficiency and competitiveness gains in logistics

• Higher quality in customer service

• Greater ability to capture new expansion market windows

• Strong M&A position

Competitiveness

Commercial

positioning

Long-term growth

potential

What is the importance of growth for Fibria?

• Wider fixed costs dilution

• Cost curve position improvement

• Greater bargaining power with suppliers

38

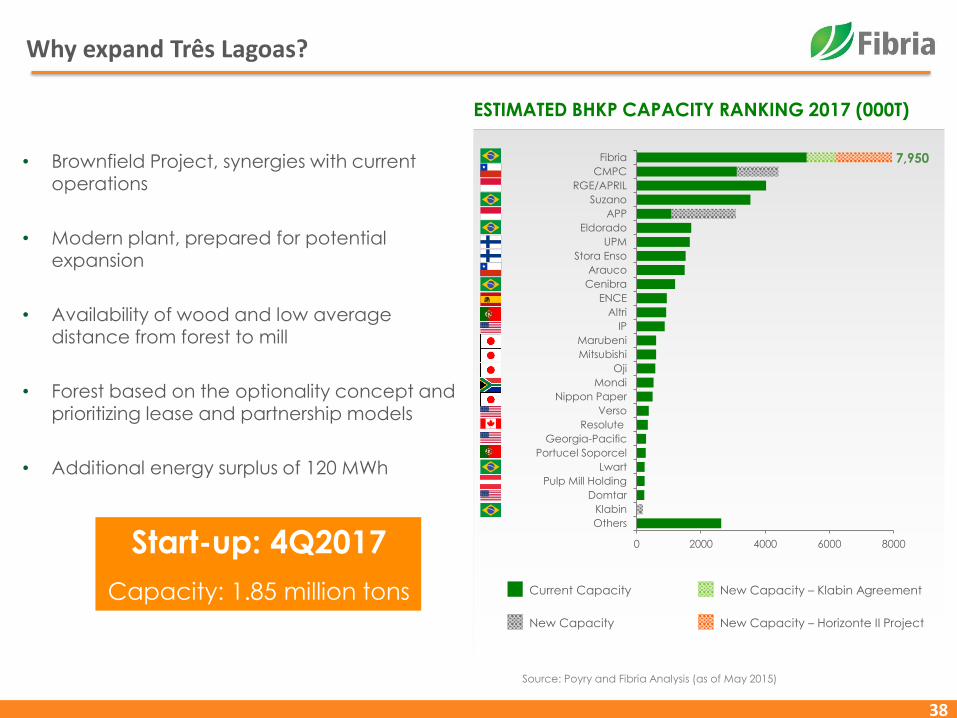

Why expand Três Lagoas?

• Brownfield Project, synergies with current operations

• Modern plant, prepared for potential expansion

• Availability of wood and low average distance from forest to mill

• Forest based on the optionality concept and prioritizing lease and partnership models

• Additional energy surplus of 120 MWh

Start-up: 4Q2017

Capacity: 1.85 million tons

ESTIMATED BHKP CAPACITY RANKING 2017 (000T)

Source: Poyry and Fibria Analysis (as of May 2015)

0 2000 4000 6000 8000

Others

Klabin

Domtar

Pulp Mill Holding

Lwart

Portucel Soporcel

Georgia-Pacific

Resolute

Verso

Nippon Paper

Mondi

Oji

Mitsubishi

Marubeni

IP

Altri

ENCE

Cenibra

Arauco

Stora Enso

UPM

Eldorado

APP

Suzano

RGE/APRIL

CMPC

Fibria 7,950

Current Capacity

New Capacity

New Capacity – Klabin Agreement

New Capacity – Horizonte II Project

39

Pulp sales destination: Fibria growing where the market grows

(1) Considers 4Q15 last twelve months. | (2) Includes Klabin’s sales volume

37%

36%

43%

24%

19%25%

8%8%

Total sales volume distribution

after H2 start up(2)

Current net revenue distribution(1)

40

Schedule

Startup

Utilities clearance and commissioningL1 interconnections

during maintenancedowntime

Initial hiring of harvest workers

Hiring of operational team

Negotiations with concession holders and

Port of Santos tendering

2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17

2015 2016 2017

Beginning of infrastructure and

purchase of the TGs

Purchase of theindustrial plants

Beginning ofconstruction

Beginning ofassembly

Beginning of forest machinery deliveries

Beginning of harvest

Definition of outbound logistics formats

Updated video

41

H2 Project will have the forest base ready for the start-up

Forestry base required:

H1: 120,000 ha

H2: 174,000 ha

Total: 294,000 ha

42

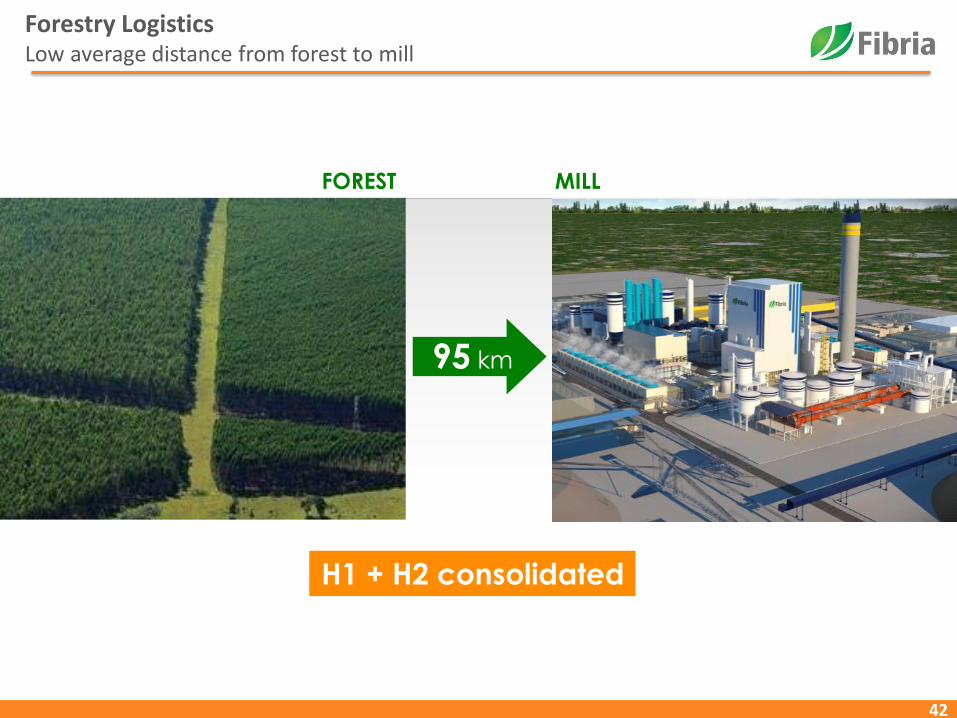

Forestry LogisticsLow average distance from forest to mill

FOREST MILL

95 km

H1 + H2 consolidated

43

Outbound logisticsFibria has logistical alternatives on a competitive basis

Ports

Highways

Railroads

Waterways

Data Collection / Preliminary Analysis

Logistics Costs

Opex - Rates

Capex

Qualitative

Modal conditions

Analysis

Mato Grosso

Mato Grosso do

Sul

Goiás

Brasilia

44

Expansion CAPEX updateFrom US$2.5 bi to US$2.2 bi

0.65

0.32

0.05

0.20

2.5

2.2

Original Revised

BRL EUR USD and others

72%

26%

2%

72%

19%

9%

FX and inflation partially offset by the negotiation with suppliers

CAPEX (US$ billion)

3%

60%

33%

3%1%

2015 2016 2017 2018 2019 and

thereafter

Timetable

45

Funding

Amortization Schedule – 4Q15 Proforma with TLS II – US$ million

Cost and maturity:

4Q15 4Q15 + H2

Average Cost (US$ p.a)

Average Maturity (years)

3.3%

4.3

2.8%

5.0

H2

2.0%

6.3

(1) Considering swap transactions. | (2) Debt FX 3Q15: 3.9729 / FX considering new funding for the TLS II Project: 3.90

275 274

581

1.113

482

668

140 126

721

115 10345 13

2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 2026 2027 2028

BNDES Bond PPE NCE ACC/ACE CRA ECA Outros FDCO Total

Capex H2: 1,350 668

46

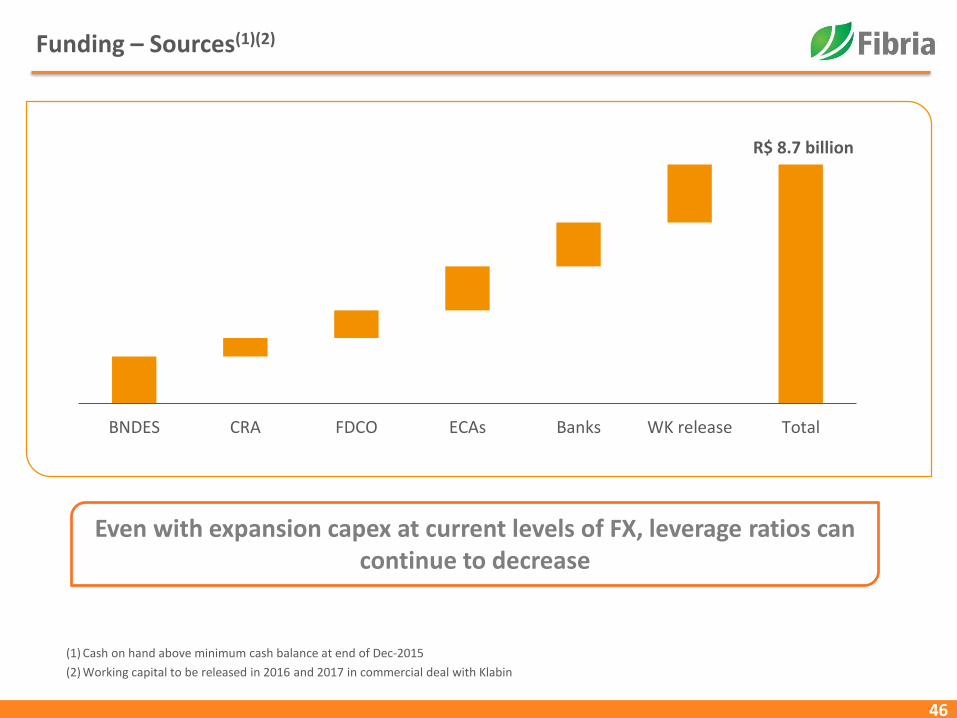

Funding – Sources(1)(2)

(1) Cash on hand above minimum cash balance at end of Dec-2015

(2) Working capital to be released in 2016 and 2017 in commercial deal with Klabin

Even with expansion capex at current levels of FX, leverage ratios cancontinue to decrease

R$ 8.7 billion

BNDES CRA FDCO ECAs Banks WK release Total

47

Rating agencies understand that the Project will not jeopardize Fibria’s credit metrics

“We expect Fibria to continue benefiting from higher operating cash flows which

would allow it to enlarge its Três Lagoas industrial complex while keeping its debt at

reasonable levels for a low investment-grade rating”

“Fitch’s base case, which assumes that the company builds a new pulp mill (Três

Lagoas II) starting in 2015 and uses net pulp prices of between USD575 and USD675

per ton during the construction period, results in net leverage reaching 3.5x(1). Net

leverage would quickly decline to around 2.5x(1) once the mill becomes operationalin the second half of 2017”

(1) According to rating agency methodology

48

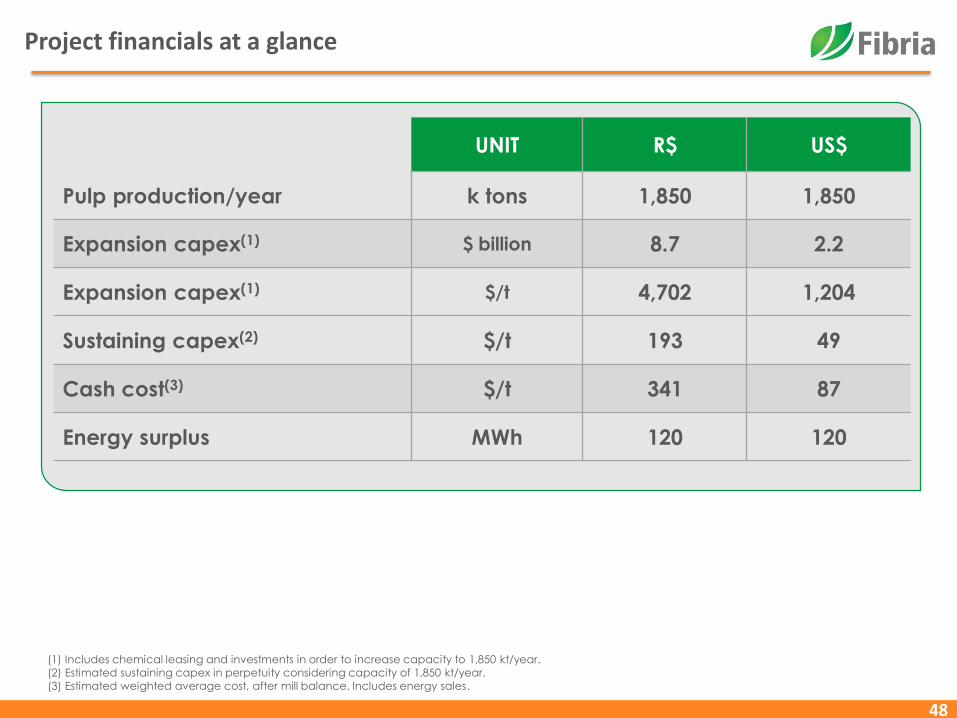

Project financials at a glance

UNIT R$ US$

Pulp production/year k tons 1,850 1,850

Expansion capex(1) $ billion 8.7 2.2

Expansion capex(1) $/t 4,702 1,204

Sustaining capex(2) $/t 193 49

Cash cost(3) $/t 341 87

Energy surplus MWh 120 120

(1) Includes chemical leasing and investments in order to increase capacity to 1,850 kt/year.

(2) Estimated sustaining capex in perpetuity considering capacity of 1,850 kt/year.

(3) Estimated weighted average cost, after mill balance. Includes energy sales.

Although some potential brownfields are listed,

there are significant challenges.

We don’t think that such competitiveness is easily replicable, since the scenario is becoming more complex…

Land

Infrastructure/Logistics

Certified wood availability

Environmental requirements

Public funding constraints

Governance standards

Cost of capital

Credit rating

50

Dividends

51

►Indebtedness and Liquidity ►Market Risk Management►Risk Management►Corporate Governance►Related Parties Transactions►Anti-Corruption►Information Disclosure►Securities Trading►Antitrust►Genetically Modified Eucalyptus►Dividend Policy►Sustainability

Policies approved by the Board of Directors

52

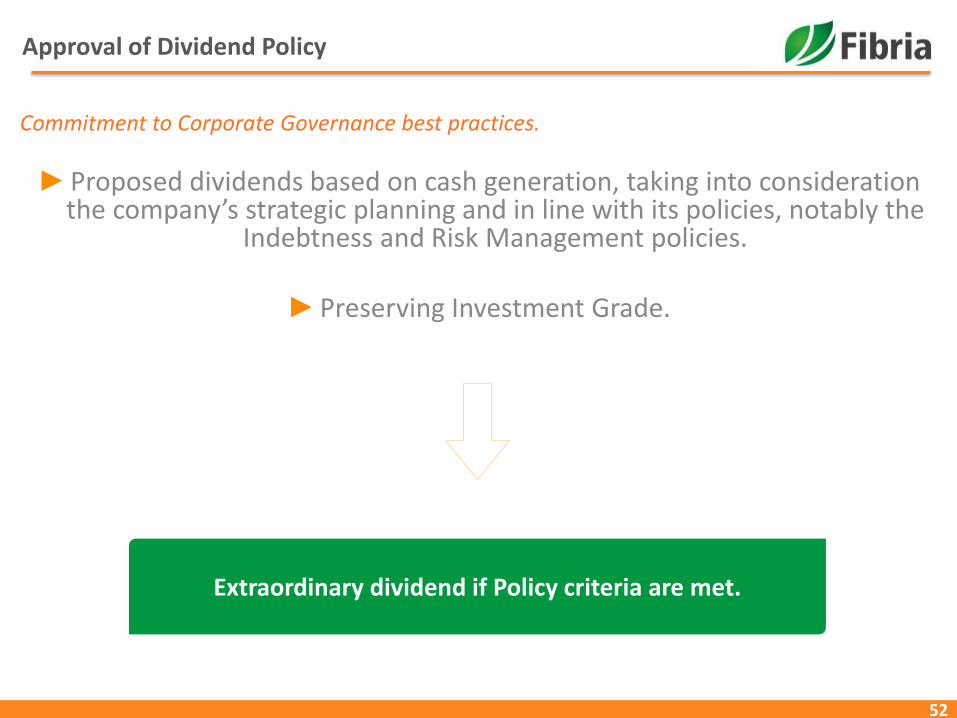

Approval of Dividend Policy

►Proposed dividends based on cash generation, taking into considerationthe company’s strategic planning and in line with its policies, notably the

Indebtness and Risk Management policies.

►Preserving Investment Grade.

Commitment to Corporate Governance best practices.

Extraordinary dividend if Policy criteria are met.

53

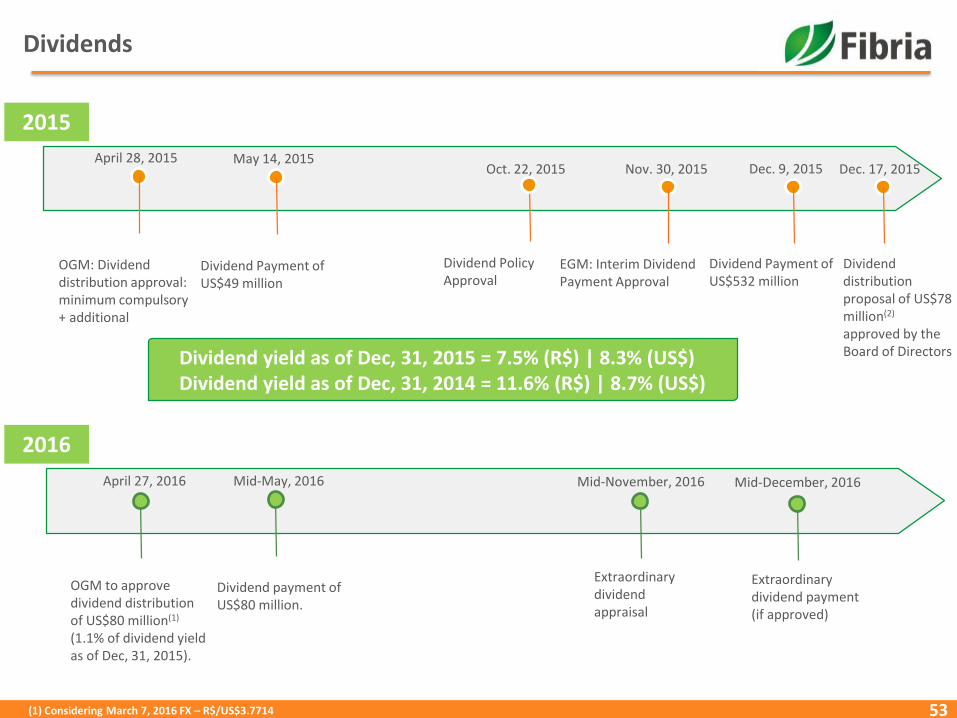

Dividends

Dividend yield as of Dec, 31, 2015 = 7.5% (R$) | 8.3% (US$)Dividend yield as of Dec, 31, 2014 = 11.6% (R$) | 8.7% (US$)

OGM: Dividenddistribution approval: minimum compulsory + additional

April 28, 2015 May 14, 2015

Dividend Payment ofUS$49 million

EGM: Interim DividendPayment Approval

Nov. 30, 2015 Dec. 9, 2015

Dividend Payment ofUS$532 million

Oct. 22, 2015

Dividend PolicyApproval

April 27, 2016

Dec. 17, 2015

Dividenddistribution proposal of US$78 million(2)

approved by the Board of Directors

OGM to approvedividend distributionof US$80 million(1)

(1.1% of dividend yieldas of Dec, 31, 2015).

Mid-May, 2016

Dividend payment ofUS$80 million.

2015

2016

Mid-November, 2016

Extraordinarydividendappraisal

Mid-December, 2016

Extraordinarydividend payment(if approved)

(1) Considering March 7, 2016 FX – R$/US$3.7714

54

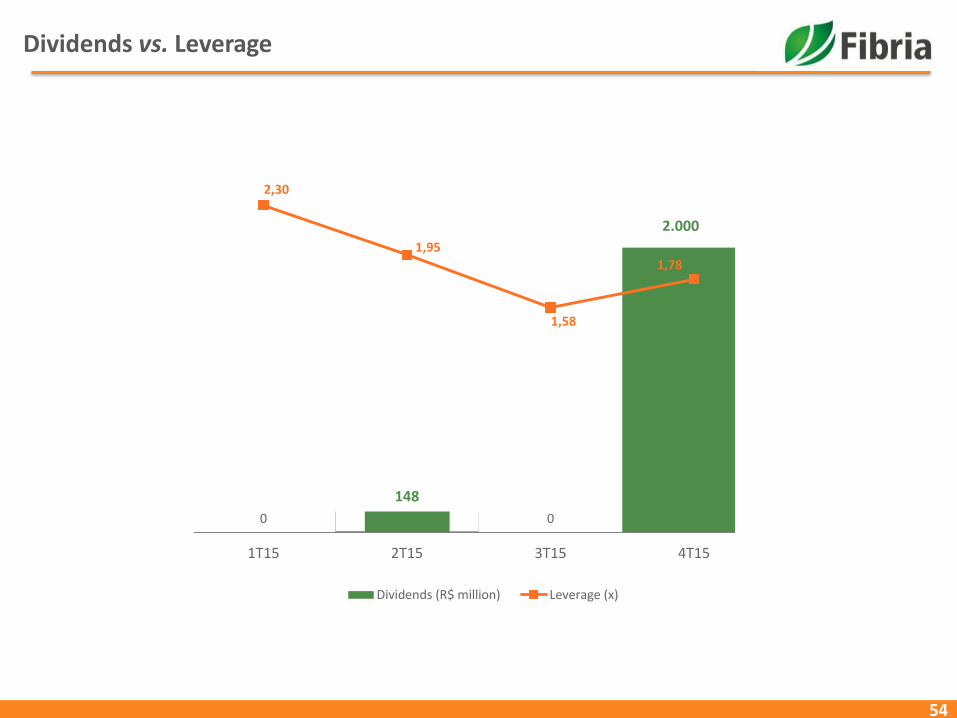

Dividends vs. Leverage

0

148

0

2.000

2,30

1,95

1,58

1,78

0,00

0,50

1,00

1,50

2,00

2,50

1T15 2T15 3T15 4T15

0,0

500,0

1.000,0

1.500,0

2.000,0

2.500,0

Dividends (R$ million) Leverage (x)

55

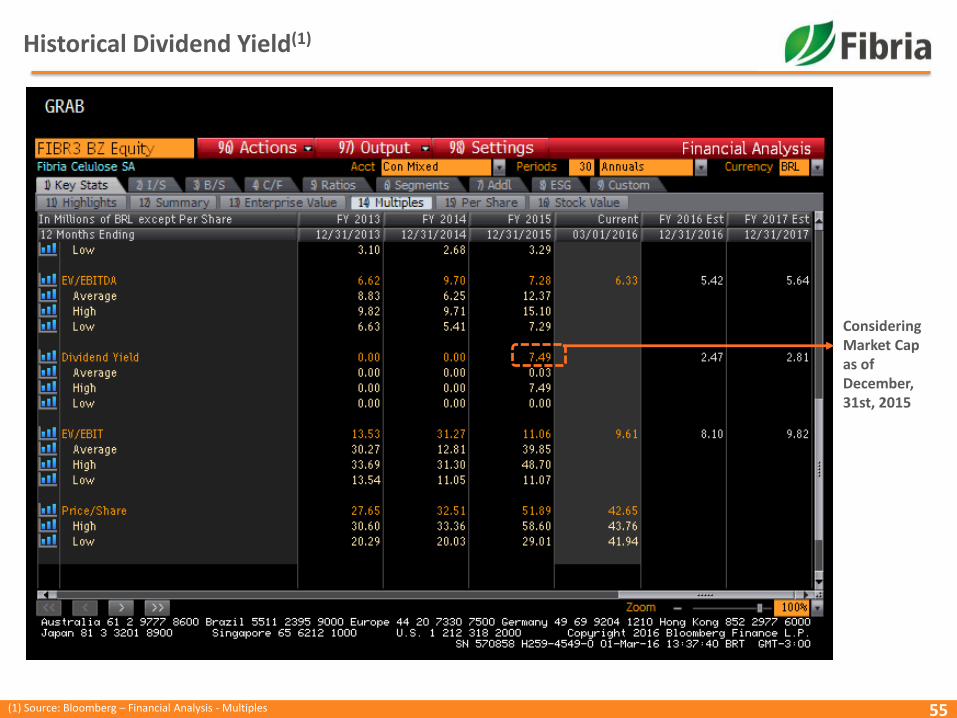

Historical Dividend Yield(1)

(1) Source: Bloomberg – Financial Analysis - Multiples

ConsideringMarket Capas ofDecember, 31st, 2015

56

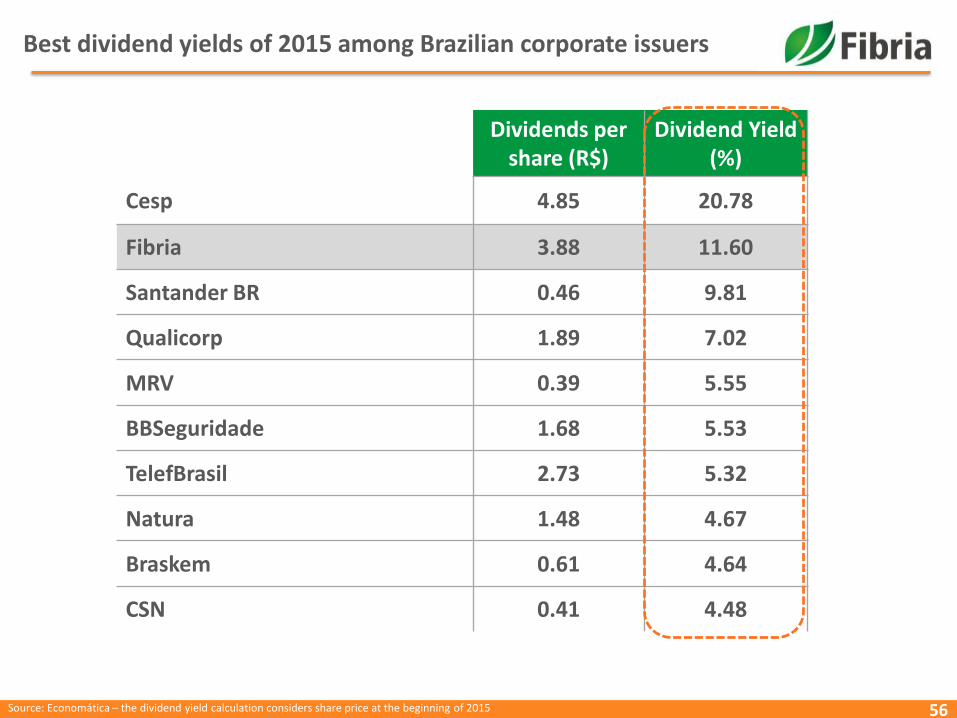

Best dividend yields of 2015 among Brazilian corporate issuers

Source: Economática – the dividend yield calculation considers share price at the beginning of 2015

Dividends per share (R$)

Dividend Yield(%)

Cesp 4.85 20.78

Fibria 3.88 11.60

Santander BR 0.46 9.81

Qualicorp 1.89 7.02

MRV 0.39 5.55

BBSeguridade 1.68 5.53

TelefBrasil 2.73 5.32

Natura 1.48 4.67

Braskem 0.61 4.64

CSN 0.41 4.48

57

Cost reduction initiatives and industry statistics

58

Structural Competitiveness

1. Third-party wood reduction

2. Forestry operations productivity

3. Industrial

NPV: US$0.4 billion

NPV: US$0.6 billion

NPV: US$0.1 billion

Total : US$1.1 billion

0%

20%

40%

60%

80%

100%

2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025

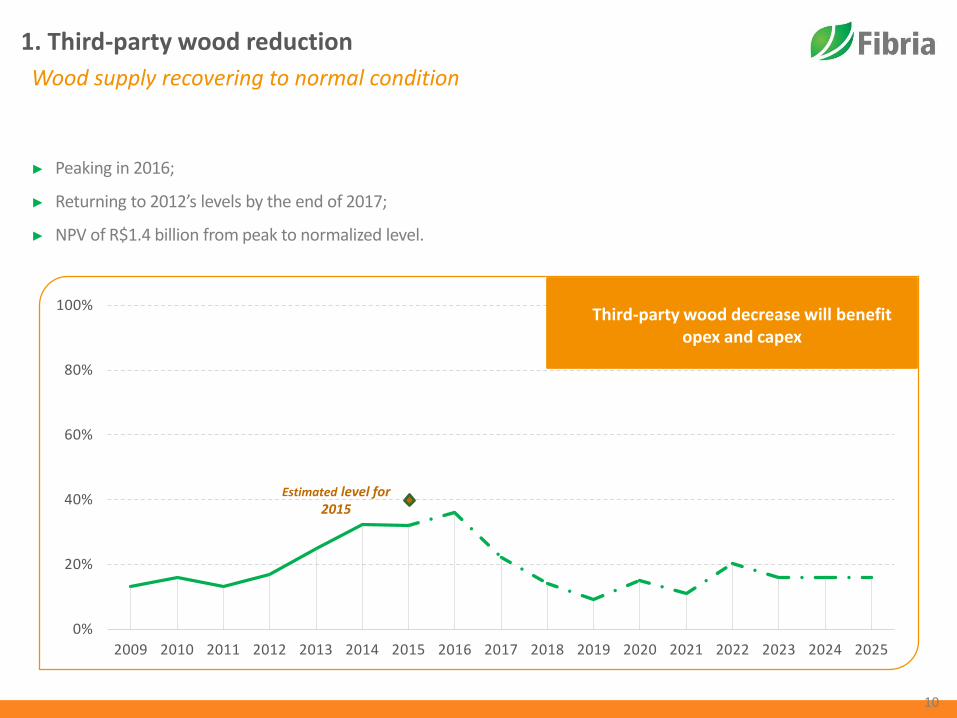

1. Third-party wood reduction

Wood supply recovering to normal condition

► Peaking in 2016;

► Returning to 2012’s levels by the end of 2017;

► NPV of R$1.4 billion from peak to normalized level.

Estimated level for 2015

Third-party wood decrease will benefitopex and capex

10

► Most part of the standing wood was already paid

► Despite the higher forest to mill distance, the wood from Losango is less expensive than the

available wood from around Espírito Santo and Bahia States

► Positive impact over industrial costs due to better productivity

11

1. Third-party wood reduction

Losango

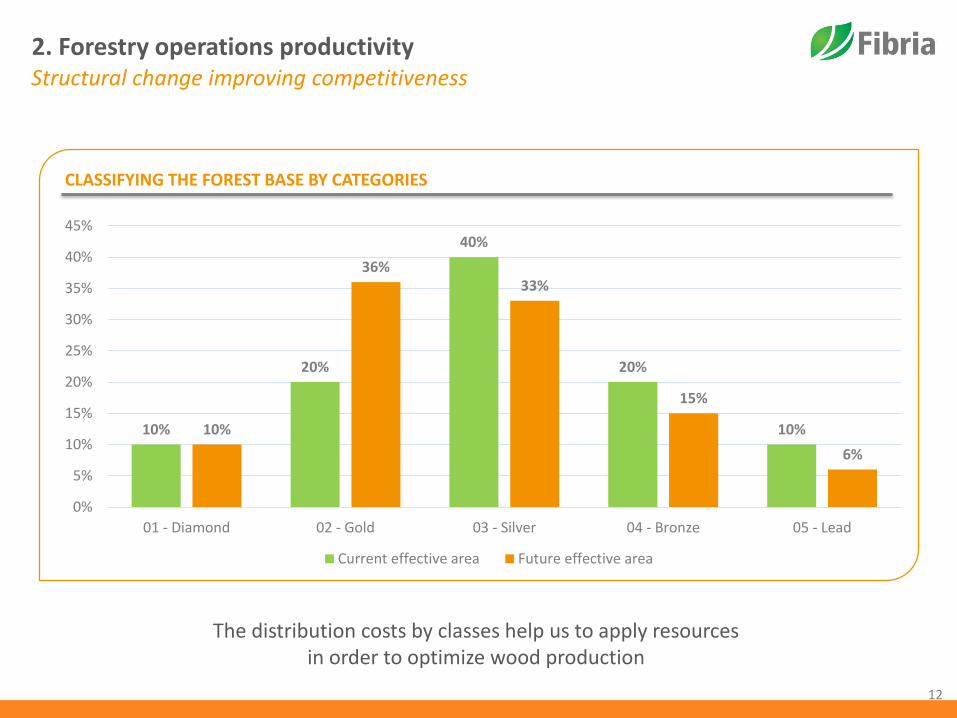

The distribution costs by classes help us to apply resources in order to optimize wood production

10%

20%

40%

20%

10%10%

36%33%

15%

6%

0%

5%

10%

15%

20%

25%

30%

35%

40%

45%

01 - Diamond 02 - Gold 03 - Silver 04 - Bronze 05 - Lead

Current effective area Future effective area

2. Forestry operations productivity

CLASSIFYING THE FOREST BASE BY CATEGORIES

12

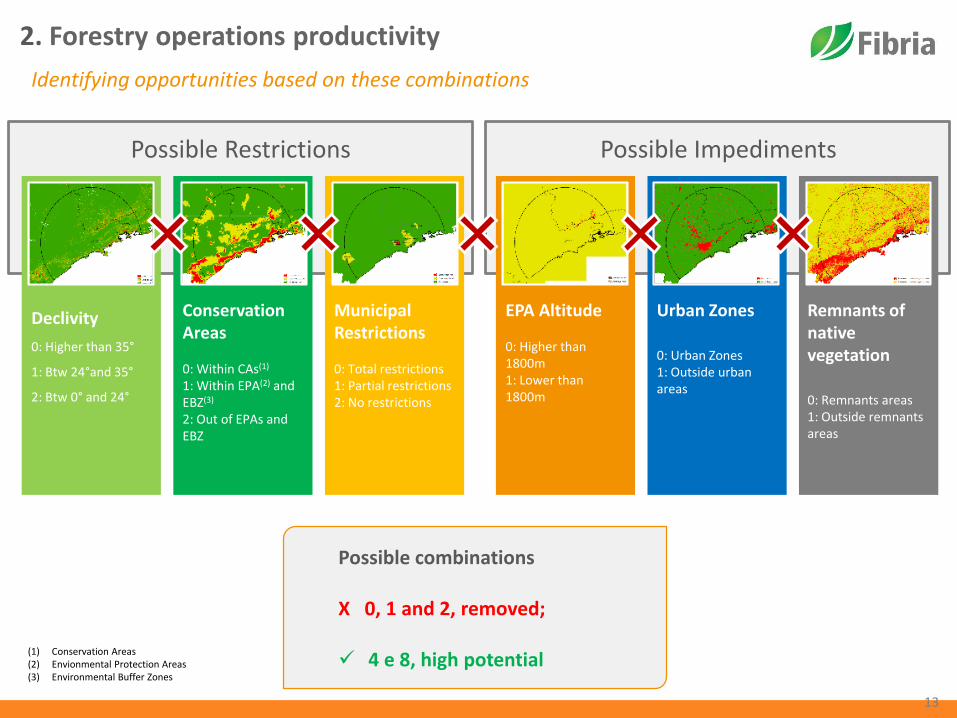

Structural change improving competitiveness

Possible Restrictions

Declivity

0: Higher than 35°

1: Btw 24°and 35°

2: Btw 0° and 24°

ConservationAreas

0: Within CAs(1)

1: Within EPA(2) andEBZ(3)

2: Out of EPAs andEBZ

Municipal Restrictions

0: Total restrictions1: Partial restrictions2: No restrictions

EPA Altitude

0: Higher than1800m1: Lower than1800m

Urban Zones

0: Urban Zones1: Outside urbanareas

Remnants ofnativevegetation

0: Remnants areas1: Outside remnantsareas

Possible Impediments

Possible combinations

X 0, 1 and 2, removed;

4 e 8, high potential(1) Conservation Areas(2) Envionmental Protection Areas(3) Environmental Buffer Zones

13

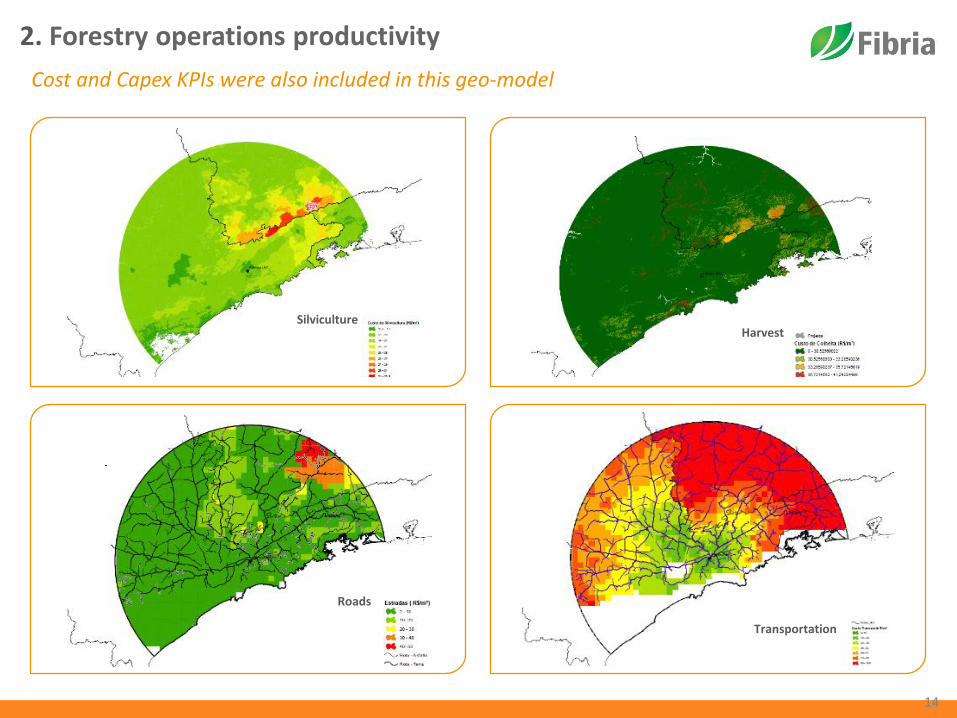

2. Forestry operations productivity

Identifying opportunities based on these combinations

Roads

Transportation

SilvicultureHarvest

14

2. Forestry operations productivity

Cost and Capex KPIs were also included in this geo-model

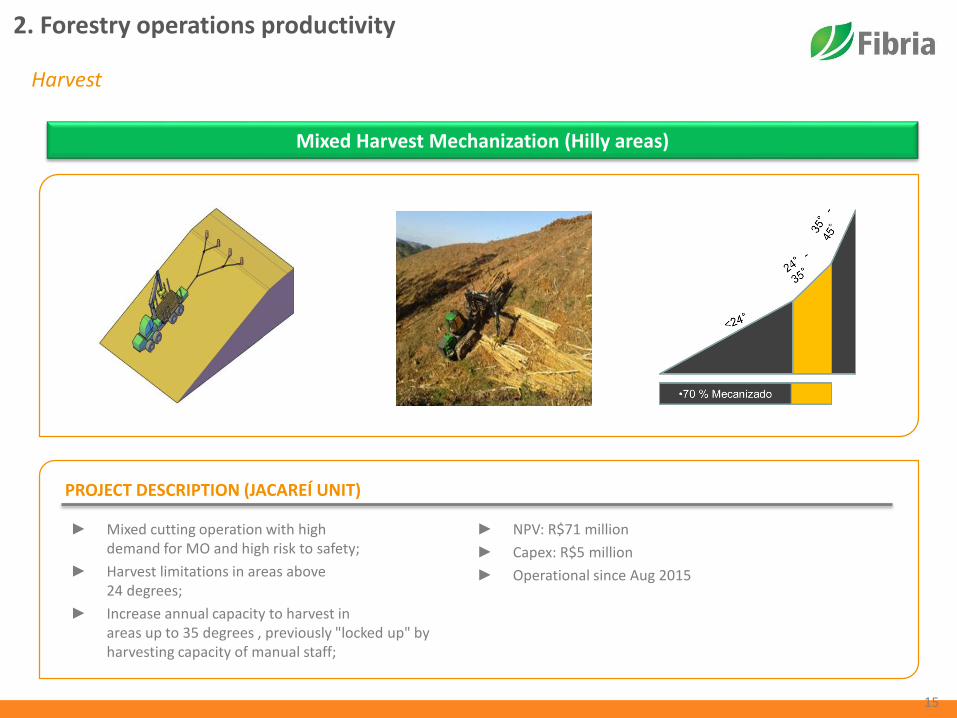

Mixed Harvest Mechanization (Hilly areas)

2. Forestry operations productivity

► Mixed cutting operation with high demand for MO and high risk to safety;

► Harvest limitations in areas above 24 degrees;

► Increase annual capacity to harvest in areas up to 35 degrees , previously "locked up" by harvesting capacity of manual staff;

► NPV: R$71 million

► Capex: R$5 million

► Operational since Aug 2015

PROJECT DESCRIPTION (JACAREÍ UNIT)

15

Harvest

PIFF

► Freight cost reduction;

► Increased load box for timber/woodchip transport

► Use of lightweight steel;

► Operational risk reduction (flipping);

► Investment: R$33 million

► NPV: R$139 million

► Startup: 2015 / 2016

PROJECT DESCRIPTION (ARACRUZ, JACAREÍ AND TRÊS LAGOAS UNITS)

Timber transportation Woodchip transportation

16

2. Forestry operations productivity

Transportation

Maritime Wood Shipping Project

► Capex and Opex reduction;

► Increase in cargo handling due to increase in

stack height volume

► Reduction in heavy truck road traffic

► Capex: R$38 million

► NPV: R$95 million

► Startup: Jan/2017

PROJECT DESCRIPTION (ARACRUZ UNIT)

17

2. Forestry operations productivity

Transportation

10%

30%

50%

70%

90%

100%

0%

20%

40%

60%

80%

100%

2015 2016 2017 2018 2019 2020

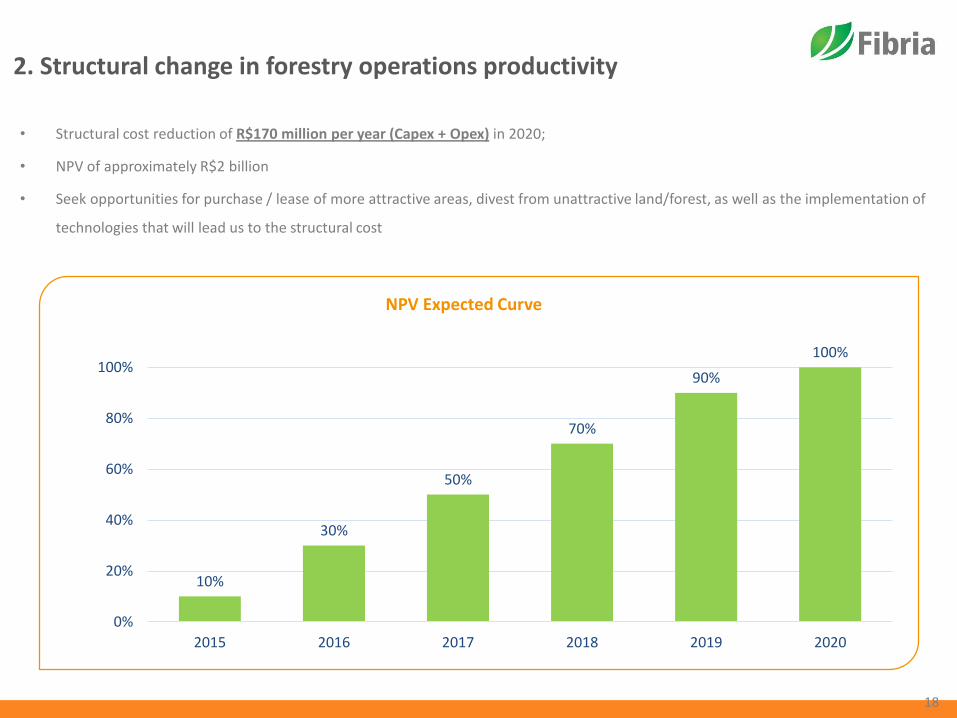

2. Structural change in forestry operations productivity

• Structural cost reduction of R$170 million per year (Capex + Opex) in 2020;

• NPV of approximately R$2 billion

• Seek opportunities for purchase / lease of more attractive areas, divest from unattractive land/forest, as well as the implementation of

technologies that will lead us to the structural cost

NPV Expected Curve

18

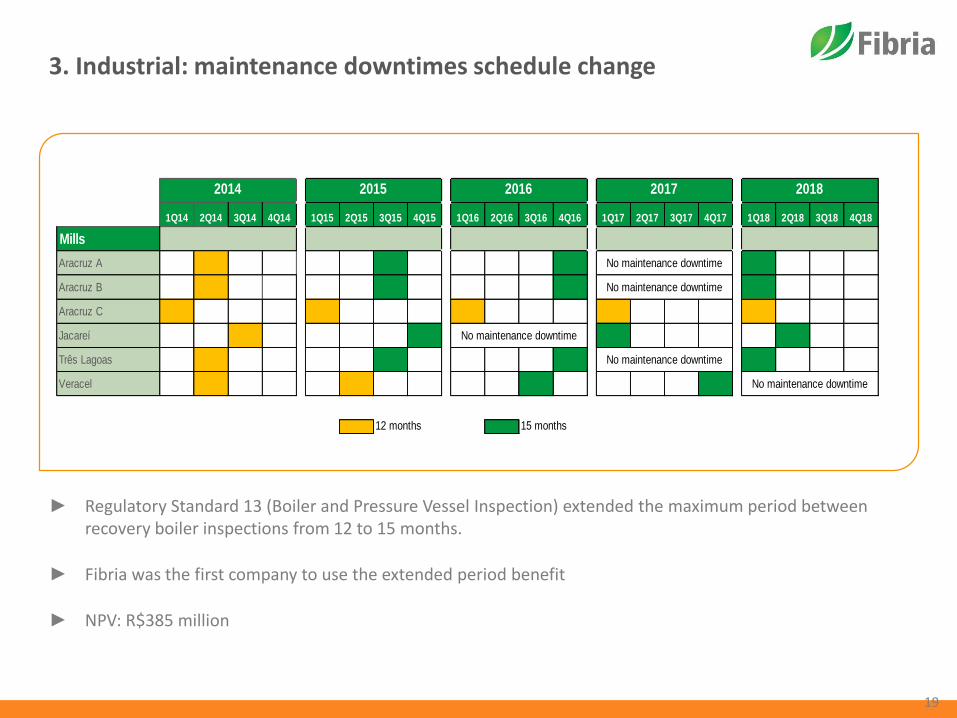

3. Industrial: maintenance downtimes schedule change

► Regulatory Standard 13 (Boiler and Pressure Vessel Inspection) extended the maximum period between recovery boiler inspections from 12 to 15 months.

► Fibria was the first company to use the extended period benefit

► NPV: R$385 million

19

1Q14 2Q14 3Q14 4Q14 1Q15 2Q15 3Q15 4Q15 1Q16 2Q16 3Q16 4Q16 1Q17 2Q17 3Q17 4Q17 1Q18 2Q18 3Q18 4Q18

Mills

Aracruz A

Aracruz B

Aracruz C

Jacareí

Três Lagoas

Veracel

12 months 15 months

No maintenance downtime

No maintenance downtime

No maintenance downtime

No maintenance downtime

No maintenance downtime

2014 2015 2016 2017 2018

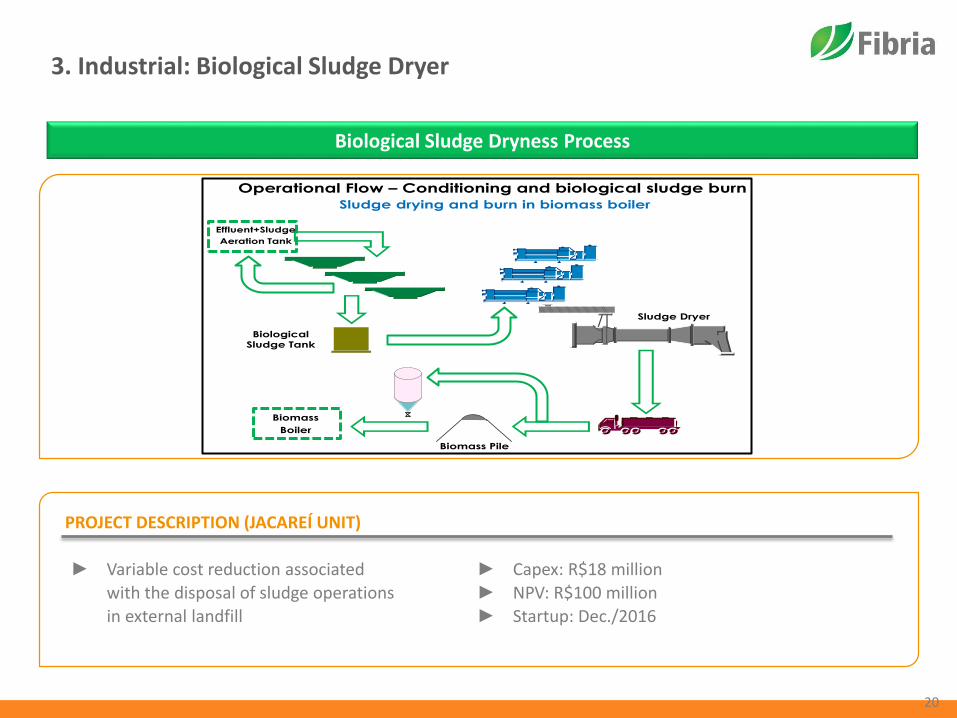

Biological Sludge Dryness Process

3. Industrial: Biological Sludge Dryer

► Variable cost reduction associated

with the disposal of sludge operations

in external landfill

► Capex: R$18 million

► NPV: R$100 million

► Startup: Dec./2016

PROJECT DESCRIPTION (JACAREÍ UNIT)

Operational Flow – Conditioning and biological sludge burn

•00Effluent+Sludge

Aeration Tank

Biological

Sludge Tank

•00Biomass Pile

Sludge Dryer

Biomass

Boiler

Sludge drying and burn in biomass boiler

20

70

Fibria’s tax structure

Fiscal - annual adjustment

Benefit Amount Maturity

Goodwill

(Aracruz

acquisition)

Annual tax deduction:

US$23 million (tax)

Remaining Balance Dec/15:

US$ 0.213 billion (base)

2018

Forestry Capex

in Mato Grosso

do Sul state

2015 tax deduction related

to depletion: US$9.4 millionUndefined

Tax loss carryforward and tax credits

Benefit Amount

Tax loss

carryforward

Balance up to Dec./15: US$33

million (base)

Accumulated tax

credits

Balance Dec./15:

- PIS/COFINS: US$186 million

- Withholding tax (IR and CSLL):

R$195 million

- Befiex: US$91 million

- Reintegra: US$23 million

2010 2011 2012 2013 2014 2015

US$ 9 million US$ 2 million US$ 8 million US$ 14 million US$ 12 million US$ 23 million

TAX BENEFITS

TAX PAYMENT (cash basis)

(1)

(2)

(1) Considering FX 3.9048 | (2) Considering average FX for the period.

71

Leadership Position

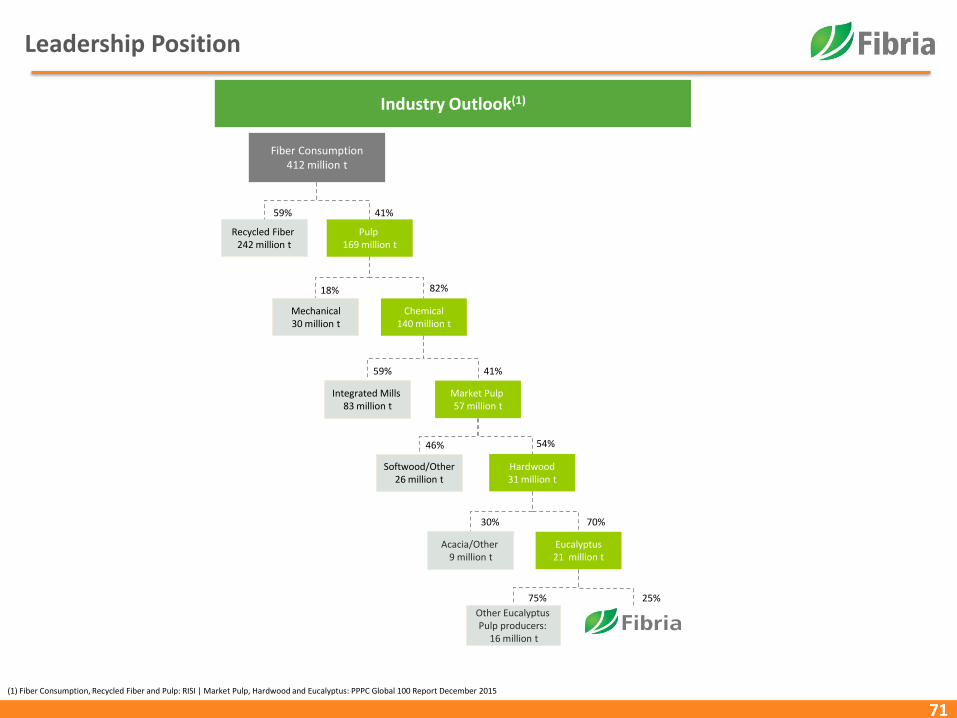

(1) Fiber Consumption, Recycled Fiber and Pulp: RISI | Market Pulp, Hardwood and Eucalyptus: PPPC Global 100 Report December 2015

Recycled Fiber 242 million t

46% 54%

59%

18% 82%

59% 41%

41%

30% 70%

25%75%

Fiber Consumption412 million t

Pulp 169 million t

Chemical140 million t

Mechanical30 million t

Integrated Mills 83 million t

Market Pulp 57 million t

Hardwood31 million t

Other Eucalyptus Pulp producers:

16 million t

Softwood/Other 26 million t

Acacia/Other 9 million t

Eucalyptus21 million t

Industry Outlook(1)

72

Global Market Pulp Demand

Demand growth rateHardwood (BHKP) vs. Softwood (BSKP) (000 ton)

Hardwood demand will continue to increase at a faster pace than Softwood

Source: PPPC report (Sept. 2015) Source: PPPC reports. Excludes Sulphite and UKP market pulp (Sept./15)

0

5.000

10.000

15.000

20.000

25.000

30.000

35.000

40.000

19

98

19

99

20

00

20

01

20

02

20

03

20

04

20

05

20

06

20

07

20

08

20

09

20

10

20

11

20

12

20

13

20

14

20

15

20

16

20

17

20

18

20

19

Hardwood Softwood

2014 - 2019 CAGR:Hardwood: +2.5%Softwood: +0.8%

000 ton 1999 2009 2019

Growth

1999-

2009

Growth

2009-

2019

Hardwood 16.3 24.8 33.8 52% 36%

Eucalyptus 6.0 15.9 24.1 165% 52%

Softwood 19.0 21.4 24.9 13% 16%

Market Pulp 35.3 46.2 58.7 30% 27%

Paper Production – Runnability with BHKP

Source: RISI conference, August 2014.

73

World Tissue Consumption, 1991-2013 (3)

Per Capita Consumption of Tissue by World Region (3)China's Share of Market Pulp (2)

24

15 15

12

7 65

1

N.America

WestEurope

Japan Oceania EastEurope

LatAm China Africa

10% 10%12% 14%

21%

17%

22%23% 23% 24%

25%

0

2

4

6

8

10

12

14

0%

5%

10%

15%

20%

25%

30%

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

Eucalyptus Hardwood Total % Compared to the global Market Pulp

(Kg/capita/year)

(million t) (kg/person/year)

Between 2005 and 2015, the Chinese market share of eucalyptus shipments increased by 20 p.p. (total market pulp: + p.p.)

0

5

10

15

20

25

30

35

1991 1996 2001 2006 2009 2010 2011 2012 2013N.America W.Europe E.Europe L.AmericaMiddle East Japan China Asia FEOceania Africa

LTM Growth Rate +4.2%

Benefiting From China’s Growth

(1) PPPC – Pulp China – Flash Report – December 2015(2) PPPC – W20. Coverage for chemical market pulp is 80% of world capacity (3) RISI

(million t)

8.724

4.301

2.154 2.029

166 59 15

9.185

4.898

2.041 1.849

201 189 8

BHKP Total LatinAmerica (1)

Indonesia Others(2) USA Canada WesternEurope

2014 2015

Latin America is the leading exporter of BHKP to China, accounting to approximately 53% of China's total imports in 2015.

(‘000s t)

(1) includes South Africa and New Zealand. | (2) Includes China, Japan, Malaysia, Russia, Thailand and Vietnam.

China’s Hardwood Imports of BHKP by Country (1)

74

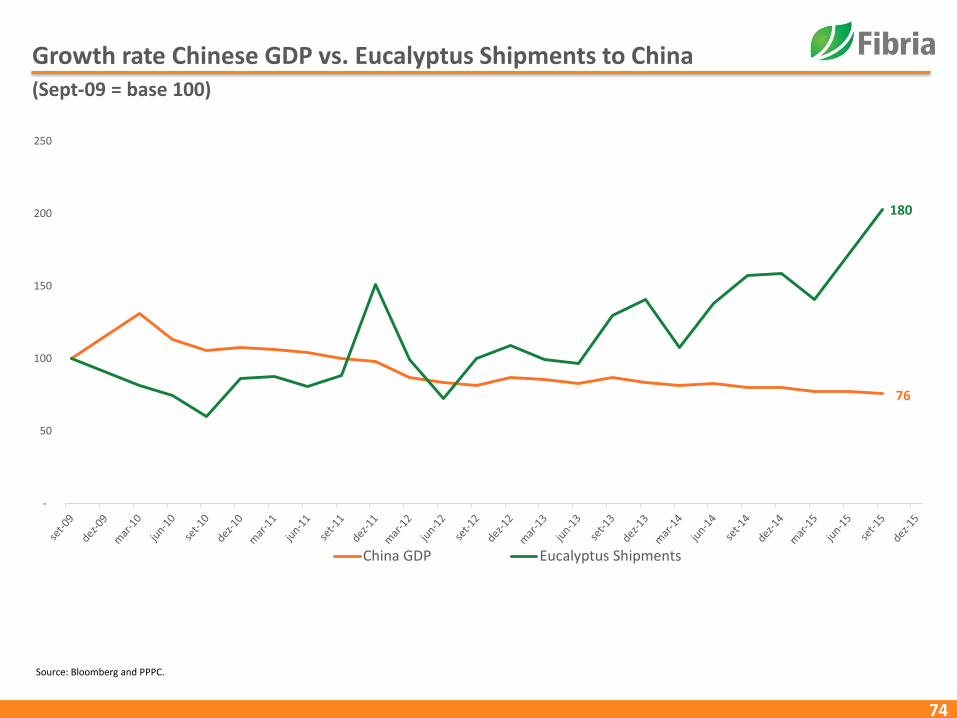

Growth rate Chinese GDP vs. Eucalyptus Shipments to China (Sept-09 = base 100)

Source: Bloomberg and PPPC.

180

-

50

100

150

200

250

China GDP Eucalyptus Shipments

76

75

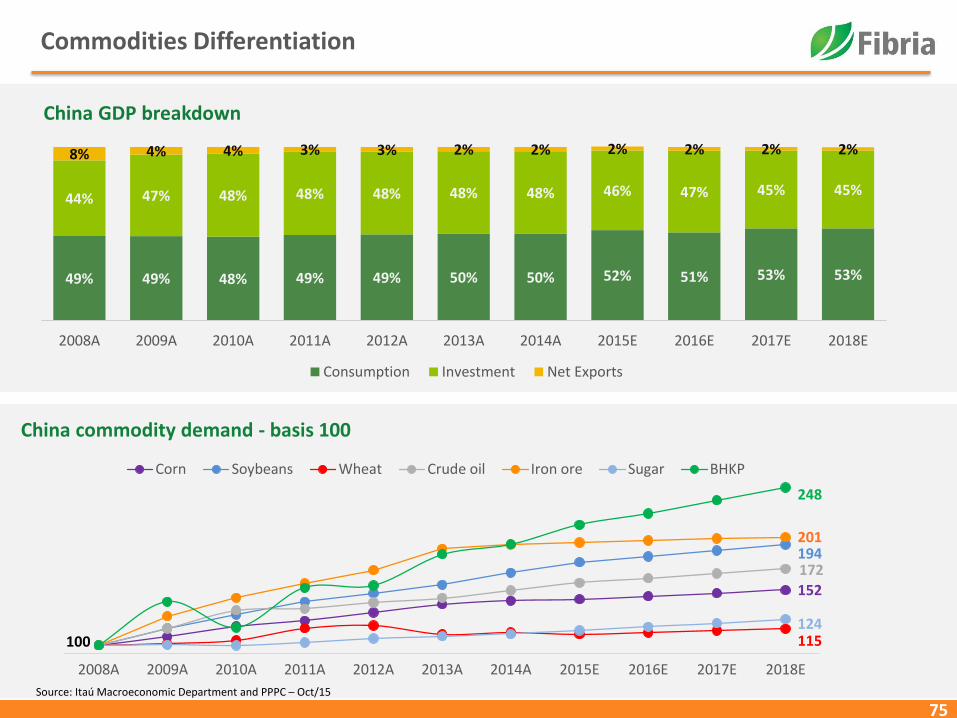

Commodities Differentiation

China GDP breakdown

China commodity demand - basis 100

49% 49% 48% 49% 49% 50% 50% 52% 51% 53% 53%

44% 47% 48% 48% 48% 48% 48% 46% 47% 45% 45%

8% 4% 4% 3% 3% 2% 2% 2% 2% 2% 2%

2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015E 2016E 2017E 2018E

Consumption Investment Net Exports

2008A 2009A 2010A 2011A 2012A 2013A 2014A 2015E 2016E 2017E 2018E

Corn Soybeans Wheat Crude oil Iron ore Sugar BHKP

100

248

201194172

152

124115

Source: Itaú Macroeconomic Department and PPPC – Oct/15

76

Global Paper Consumption

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

Developed Markets Emerging Markets

CAGR 1996 – 2006Developed Markets: + 1.7%Emerging Markets : + 6.0%

85,291

117,611

15,548

37,474

P&W Consumption (000 tons)(1)

Tissue Consumption (000 tons)(1)

114,507

CAGR 2007 – 2016Developed Markets: - 4.0%Emerging Markets : + 4.1%

CAGR 1996 – 2006Developed Markets: + 2.4%Emerging Markets : + 6.9%

CAGR 2007 – 2016Developed Markets: + 1.4%Emerging Markets : + 6.7%

26,877

Source: RISI

77

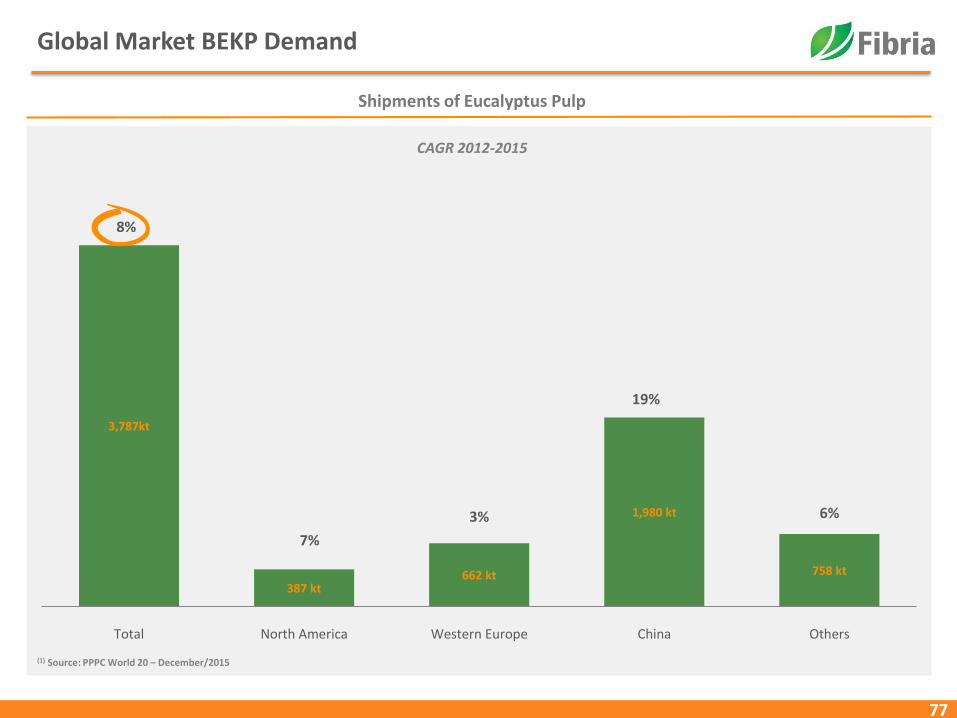

Shipments of Eucalyptus Pulp

Global Market BEKP Demand

(1) Source: PPPC World 20 – January/2015

(1) Source: PPPC World 20 – December/2015

CAGR 2012-2015

3,787kt

387 kt662 kt

1,980 kt

758 kt

8%

7%

3%

19%

6%

Total North America Western Europe China Others