savillsresearch insight key australian retail transactions february 2014

TRANSCRIPT

Insight Key Australian Transactions

InsightKey Australian Retail Transactions

Savills ResearchFebruary 2014

savills.com.au/research

Savills Research

OverviewThe calendar year 2013 marked a significant recovery for investment markets with property sales turnover at record levels and strong gains made on local and global sharemarkets – interest rates have stayed low, the search for yield and security remained strong however there has been more capital allocated for higher risk property including development. The S&P500 index rose 25 percent to a record high reflecting cheap capital and a sense of economic recovery in the United States. The Australian ASX200 Index rose 13 percent and the Australian dollar fell 15 percent against the US dollar. Nationally, over $22 billion of commercial property has been transacted and over 3 million square metres of industrial and office space has been reported leased which gives us confidence that the markets are operating normally.

Commercial property yields in particular continue to look attractive. The Australian economy is being rebalanced as growth in mining softens. This means housing and retail should continue to lift with positive knock on effects to industrial and office markets. As consumer confidence continues to rise, so should business confidence. As profit margins are restored, business decision making should gain momentum. Some State governments will move into election mode and could be expected to provide some stimulus to parts of the economy providing further momentum to investment markets. China and the United States are forecast to contribute positively to Australia’s economic outlook whilst Europe could be on the cusp of a subdued recovery.

2

Insight Key Australian Transactions

savills.com.au/research 3

Australian Retail PropertyThe retail sector faces both cyclical and structural issues. Some cyclical issues are starting to move in its favour. Consumer confidence is improving, certainly not deteriorating and the cyclical falls in interest rates are certainly helping. Employment is growing strongly in four or five sectors and shrinking in four or five sectors and the jobs gained and lost are not necessarily in the same physical place. This means certain catchment areas are doing it tough and some are doing well.

The size and shape of the workforce has a profound impact on retail property because wages determine spending and jobs define catchment areas. Australia is almost unique in the world as being one of very few countries that have expanded their workforce during the global financial crisis. The Australian workforce has grown by almost a million people from 10.7 million to 11.6 million from November 2007 to November 2013. Over the past year we have shed jobs in Agriculture, Real Estate, Manufacturing, Mining and IT. However, we have created twice as many jobs as we have lost – Retail, Healthcare, Government and Transport. Over the six years of the global financial crisis we have shed jobs in Manufacturing and Agriculture but we have created five times as many jobs elsewhere. These same trends have been present for 30 years (with some bumps along the way). Agriculture and Manufacturing have been in the doldrums for 30 years – an entire generation – this is not new news. Whilst we have lost 256,000 jobs in these two sectors, we have created 21 times the same number of jobs in other sectors – a total of 5.3 million jobs. How much more is earned in these newly created jobs? If workers are paid more, they put more into superannuation, they pay more tax, they spend more and they pay more for a house – a virtuous property cycle.

The newly arrived population have a profound impact on property because they need somewhere to live and goods to put in it. Instant housing and bulky goods demand. Less people leaving the country means fewer houses freed up for those arriving.

With the size of the workforce growing and more people coming into the country (and less leaving) it is little wonder that a recovery in housing is underway. It may not feel like a boom, but it is starting. Credit growth has been rising for a year and prices for dwellings are starting to rise again.

Changes in consumer spending patterns since 2007 appear to have had an adverse effect on department store, apparel and discretionary retailing turnover generally. This has impacted tenants in Regional and some Sub-Regional shopping centres. Lower turnover combined with increasing rents has led to specialty occupancy costs rising to an average of 18 percent in Regional Shopping Centres. This is a level that could generally be described as unsustainable and any one or combinations of three things are likely to happen from here. One, occupancy costs fall to a more sustainable level; two, incentives are provided by the landlord to mitigate

the high occupancy costs; three, turnover increases as consumers return. In any case, the returns from this sector of retail appear to be constrained for the foreseeable future.

The structural issues facing retail are more formidable but not insurmountable. Savills expect the retail sector to evolve to take advantage of the structural issues rather than be over-run by them. The ageing of the population will continue to create challenges for retailers as they jockey for the dollars of retirees. Retirees can be expected to prefer services over goods and will not necessarily continue to dwell in their traditional catchment areas. Internet retailing has already changed the face of retailing for certain categories of goods and will no doubt continue to evolve and challenge more categories over time. New business models are establishing themselves.

<$10m $50 - $100m$10-$50m >$100m

Source: Savills Research

Australian Retail Property Sales by Price Range ($m)Dec-03 to Dec-13

$0

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

Dec-0

4

Dec-0

3

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3

4

Savills Research

Retail Investment MarketSavills recorded approximately $6.8 billion worth of retail property transactions nationally in the 12 months to December 2013, up from $4.4 billion in the previous year, and up on the five year average, which was $4.3 billion. In the 12 months to December 2013, 158 properties were sold, up from the previous year of 133, and up on the five year average of 136.

In the 12 months to December 2013, $2.9 billion worth of transactions were reported in the > $100m price range, accounting for 43 percent of total retail property sales activity. Over the same period, sales in the $10m - $50m price range had the greatest number of transactions (91 or 58 percent).

In the 12 months to December 2013, $2.1 billion worth of transactions occurred in the 'Sub Regional' retail centre category, accounting for 31 percent of total retail property transactions. During the same period the 'Neighbourhood' centre category had the greatest number of transactions (58 or 37 percent).

The 'Trust' purchaser category was the most active in the investment market for the year ended December 2013, purchasing 35 percent of stock sold. However, the 'Private Investor' category recorded the most transactions (59).

Retail bulky goods property sales within Australia have increased in volume in the 12 months to December 2013. Savills recorded 24 property sales. These sales amounted to $807 million worth of retail bulky good property transactions. This was up from the previous year of $787 million worth of sales in 29 transactions and up from the five year average of $573 million worth of sales in 22 transactions.

Australian institutional investors (Funds, Trusts and Syndicates) are increasingly active as flows to superannuation continue unabated.

“Retail bulky goods property sales within Australia have increased in volume” Savills Research

Foreign investors have been purchasing part shares of shopping centres as passive investments whilst private investors continue to be attracted to high street retailing, CBD retailing and freestanding supermarkets.

If the RBA are successful in stimulating growth in the non-resources side of the economy then the retail sector nationally should be a beneficiary of stronger retail turnover growth. Very early signs of this were seen in the last six months of 2013.

City Centre Sub Regional

Freestanding Regional

Bulky Goods Other

Neighbourhood Shops

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3

Australian Retail Retail Property Transactions by Centre Type ($m)Dec-03 to Dec-13

$1,000

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

$8,000

$0

Source: Savills Research

Insight Key Australian Transactions

savills.com.au/research 5

“Savills recorded approximately $6.8 billion worth of retail property transactions nationally” Savills Research

Demand for short term accommodation near hospitals, medical centres and aged care facilities appear obvious.

Demand for appropriate amounts and styles of residential property at appropriate pricing to cater for demand from over 65 year olds is another enormous opportunity in property markets. A ‘one size fits all’ strategy is unlikely to be successful – location, amenity, transport and other lifestyle considerations will play their part. House swapping (popular in Europe), time share (popular in America), retirement living, aged care, ‘granny flats’, tree change and sea change all present opportunities for those providing services to property.

Finally, the way you spend money when you are retired is different to the way you spend it when you are working. We should expect to see some profound changes to the retail landscape as demand for goods and services change. This is an evolution in the retail landscape – not a death knell – though certain categories will struggle, others will thrive and new ones will be born.

Special Insight: The Ageing Of The PopulationBecause there is no fountain of youth, one thing we can rely on is the ageing of the population. For most of human existence on the planet only 10 percent of the population were considered old. Today we are moving from around 10 percent to around 30 percent. This is not an Australian phenomenon but a global phenomenon. The effect on property can be expected to be profound. Demand for lifestyle property, retirement property, aged care, health care and peripheral health services is expected to triple over coming decades.

The number of people aged greater than 65 in Australia is expected to rise from approximately 3 million today to 4.5 million in a decade and peak at 8 million in the years that follow. As sure as night follows day, this trend in population is unavoidable. So, what property trends may we expect to see? An increase in demand for healthcare and health services is to be expected. In the United States, health services are moving into shopping centres – we should expect to see that here too.

Australian RetailRetail Property Buyer Profile12 months to Dec-13

Source: Savills Research

Dec-0

3

Dec-0

4

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

30

5

10

15

20

25

30

35$900

$800

$700

$600

$500

$400

$300

$200

$100

$0

Source: Savills Research

Australian Retail Bulky Goods Property Sales ($m and number)Dec-03 to Dec-13Sales >$5m (LHS) No (RHS)

Private Investor17%

Developer1%

Foreign Investor20%

Syndicate2%

Undisclosed2%

Trust36%

Fund22%

6

Savills Research

Insight Key Australian Transactions

savills.com.au/research 7

New South WalesSavills recorded approximately $2.4 billion worth of retail property transactions in the 12 months to December 2013, up from $1.4 billion in the previous year, and up on the five year average, which was $1.3 billion. In the 12 months to December 2013, 44 properties were sold, down from the previous year of 50, and up on the five year average of 43.

The 'Fund' purchaser category was the most active in the investment market for the year ended December 2013, purchasing 39 percent of stock sold. Similarly, the 'Fund' category recorded the most transactions (16).

Retail bulky goods property sales within Australia have increased in volume in the 12 months to December 2013. Savills recorded 9 property sales. These sales amounted to $352 million worth of retail bulky good property transactions. This was up from the previous year of $322 million worth of sales in 10 transactions and up from the five year average of $247 million worth of sales in 8 transactions.

New South Wales RetailRetail Property Sales by Price Range ($m)Dec-03 to Dec-13

Dec-0

4

Dec-0

3

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3

Source: Savills Research

“The retail sector faces both cyclical and structural issues. Some cyclical issues are starting to move in its favour.” Tony Crabb, Savills Research

$2,500

$3,000

$3,500

$2,000

$1,500

$1,000

$500

$0

< $10m $50 - $100m$10m - $50m > $100m

Erina Fair, Erina 1

8

Savills Research

Carlingford Court, Corner Pennant Hills and Carlingford Rds, Carlingford

Price: $175.50 million

Date: December 2013

Initial Yield: 7.25%

Market Yield: na

Rate/sq m: $6,187

Vendor: GPT

Purchaser: Federation Centres

Comment: The centre is anchored by Coles, Woolworths, Target and approximately 100 specialty stores. Carlingford Court is located approximately 20 kilometres north west of the Sydney CBD.

Centro Roseland (50%), Roselands Dr, Roselands

Price: $166.90 million

Date: June 2013

Initial Yield: 7.00%

Market Yield: na

Rate/sq m: $5,577

Vendor: Federation Centres

Purchaser: Challenger

Comment: The centre offers over 170 specialty stores anchored by Myer, Target, Coles and Food for Less, along with Best & Less, Priceline Pharmacy and Dick Smith.

NSW Key Retail Transactions 2013

Erina Fair (50%), Terrigal Drive, Erina

Price: $397.10 million

Date: May 2013

Initial Yield: na

Market Yield: 6-6.15%

Rate/sq m: $7,764

Vendor: GPT

Purchaser: National Pension Service (via APPF)

Comment: Erina Fair is the largest shopping centre on the Central Coast. The centre is anchored by Myer, Kmart, Target, Big W, Best & Less, Woolworths, Coles and Aldi plus over 300 specialty stores.

Centro Bankstown (50%), 12 North Tce, Bankstown

Price: $287.50 million

Date: June 2013

Initial Yield: 6.80%

Market Yield: na

Rate/sq m: $7,223

Vendor: Federation Centres

Purchaser: Challenger

Comment: The centre is anchored by Myer, Big W, Target, Kmart, Woolworths, Supa IGA and over 310 specialty stores. There are two fresh food precincts (Grand Market, Fresh Life), a food court and numerous cafes serving delicious food at extremely competitive prices.

Top Ryde City, Corner Delvin and Pope St, Ryde

Price: $341.00 million

Date: November 2012

Initial Yield: 7.77%

Market Yield: 6.97%

Rate/sq m: $4,428

Vendor: John Beville Trust

Purchaser: Blackstone Group

Comment: Top Ryde City is a predominantly four level, Regional shopping centre with a total GLA of 77,009 square metres (excluding ‘pad’ sites/external tenancies). The centre commenced trading in its current form in August 2010. The centre comprises a Myer, Big W, Woolworths, Franklins and Aldi, Fitness First Gym, Event Cinema, 18 Mini-Major tenancies, 168 specialty tenancies, 31 kiosks, 9 ATMs, four ‘pad’ sites/external tenancies and 46 vacancies.

225 George Street, Sydney

1

2

4

53

Carlingford Court, Carlingford

Centro Roselands, Roselands

3

4

Insight Key Australian Transactions

savills.com.au/research 9

Supa Centre Belrose, Mona Vale Rd, Terrey Hills

Price: $88.00 million

Date: November 2013

Initial Yield: 8.26%

Market Yield: 8.22%

Rate/sq m: $2,745

Vendor: Terrace Tower Group

Purchaser: BB Retail Capital

Comment: Supa Centre Belrose comprises a fully enclosed Bulky Goods centre that opened for trade in October 2006. The centre is laid out over 3 retail levels with a GLA of approximately 31,692 square metres (excluding the car wash). The centre comprises several national retailers including Domayne, JB Hi-Fi, Spotlight, Anaconda, Nick Scali, Plush and Freedom Furniture together with 12 Mini-Major tenants (including 2 vacancies), 19 specialties, two ATMs, one Kiosk and one Pad site (car wash). The centre also provides car parking for 1,185 vehicles on a site of 4.023 hectares.

Centro Warriewood (50%), Jacksons Rd, Warriewood

Price: $72.23 million

Date: March 2013

Initial Yield: 7.50%

Market Yield: na

Rate/sq m: $6,521

Vendor: Federation Centres

Purchaser: ISPT

Centro Toormina (50%), 5 Toormina Rd, Toormina

Price: $65.50 million

Date: June 2013

Initial Yield: 8.80%

Market Yield: na

Rate/sq m: $6,288

Vendor: Federation Centres

Purchaser: Challenger

Comment: Centro Toormina is the only centre in Coffs Harbour to house both a Coles and Woolworths supermarket under the one roof and also boasts the only Kmart within a 200km radius. Located in the developing Southern urban area of Coffs Harbour, Centro Toormina underwent a major re-development in November 2008 expanding the centre to over 21,694 square metres.

Auburn Home Mega Mall, Auburn

Price: $55.00 million

Date: July 2013

Initial Yield: 7.50%

Market Yield: 10.50%

Rate/sq m: $1,722

Vendor: AMP Capital Investors / Unisuper

Purchaser: Primewest Management

Comment: Homemaker Megamall Auburn comprises a fully enclosed Bulky Goods centre that opened for trade in October 1999 and was refurbished in 2004. The centre is predominantly laid out over two retail levels with an additional upper mezzanine level and has a GLA of approximately 32,341 square metres (excluding ‘pad site’). The centre has a strong presence of national retailers including Freedom, Deco Rug, The Good Guys, Snooze, The Sleeping Giant and Fantastic Furniture.

Oxford Square, 63 Oxford St, Darlinghurst

Price: $62.70 million

Date: February 2013

Initial Yield: 8.00%

Market Yield: 11.30%

Rate/sq m: $5,187

Vendor: Local Private Investor

Purchaser: Australian Property Opportunities Fund

Comment: Oxford Square comprises a convenient fully leased retail/commercial complex (extensively refurbished 2005) prominently located on major thoroughfare Oxford Street within one of Sydney's most densely populated areas. The mixed use asset is situated below the residential building known as The Monument.

9

10

76

8

Oxford Square, Darlinghurst

Top Ryde City, Ryde5

10

10

Savills Research

Insight Key Australian Transactions

QueenslandSavills has recorded approximately $930 billion worth of retail property transactions in the 12 months to December 2013, down from $2.46 billion in the previous year, and down on the five year average, which was $1.15 billion. In the 12 months to December 2013, 31 properties were sold, down from the previous year of 48, and down on the five year average of 39.

The 'Trust' purchaser category was the most active in the Queensland investment market for the year ended December 2013, purchasing 31 percent of stock sold. However, the 'Private Investor' category had the most transactions (11).

Bulky goods property sales in Queensland have increased in volume in the 12 months to December 2013. Savills have recorded $371 million worth of retail bulky good property transactions within the state, up from the previous year of $258 million and up on the five year average of $214 million.

Queensland Retail Retail Property Sales by Price Range ($m)Dec-03 to Dec-13

< $10m $50 - $100m$10m - $50m > $100m

Dec-0

4

Dec-0

3

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3

$0

$500

$2000

$1500

$2000

$2500

$3000

Source: Savills Research

Beenleigh Marketplace2

savills.com.au/research 11

12

Savills Research

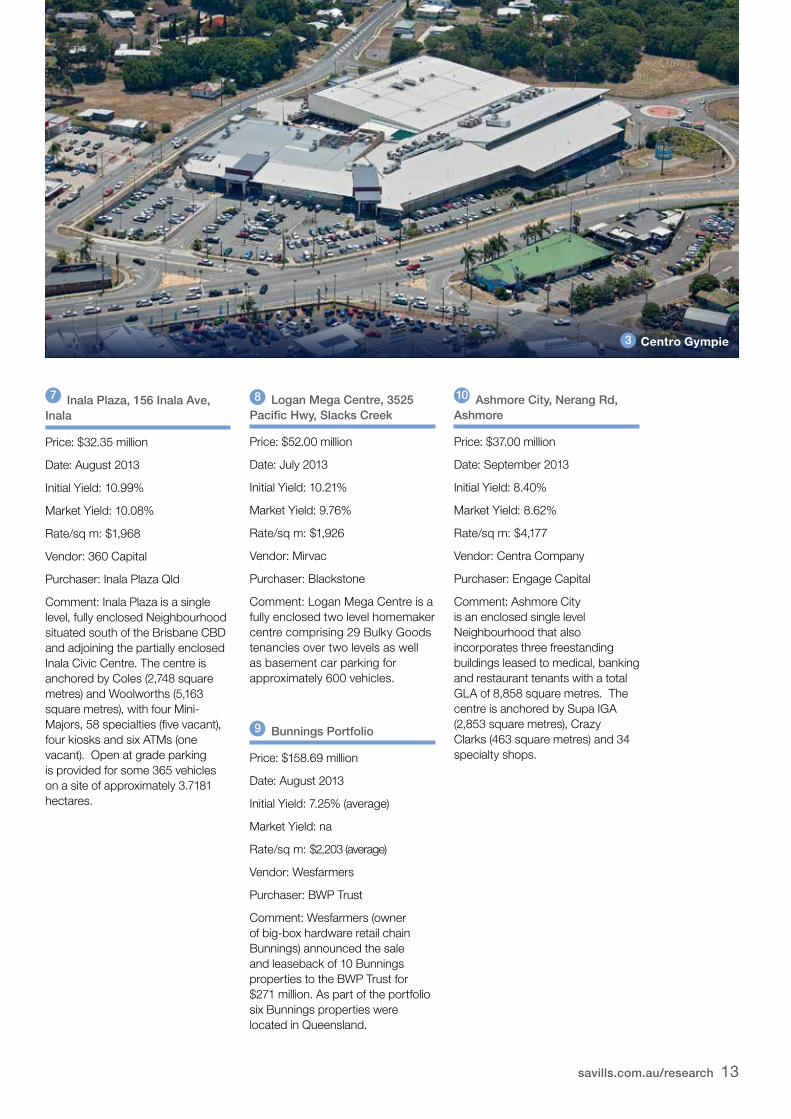

Centro Gympie, Bruce Hwy, Gympie

Price: $63.80 million

Date: April 2013

Initial Yield: 7.55%

Market Yield: 7.50%

Rate/sq m: $4,540

Vendor: Centro

Purchaser: Federation Centres

Comment: Centro Gympie is a single level enclosed Sub Regional with a total GLA of 14,054 square metres. The centre was constructed in 1979 with major redevelopment completed in March 2007. The centre comprises a Woolworths (3,534 square metres), Big W (5,574 square metres) one Mini-Major tenancy and some 46 specialty stores.

Kmart Plaza, 878 Ruthven St, Toowoomba

Price: $57.00 million (including land)

Date: July 2013

Initial Yield: 7.04%

Market Yield: 6.97%

Rate/sq m: $4,216

Vendor: ISPT

Purchaser: McConaghy

Comment: Toowoomba Plaza is a single level enclosed Sub Regional with a GLA of 13,045 square metres. The centre commenced trading in 1977 and was last refurbished in 2009. The anchor tenant comprises of a Coles (3,314 square metres) and a Kmart (7,324 square metres) with 24 specialities, 6 ATM’s and 2 kiosks.

QLD Key Retail Transactions 2013

Homemaker City, Wickham Street, Fortitude Valley

Price: $103.77 million

Date: July 2013

Initial Yield: 9.35%

Market Yield: 8.95%

Rate/sq m: $2,711

Vendor: GPT

Purchaser: Altis Property Partners

Comment: Homemaker City, Fortitude Valley comprises a three stage enclosed Bulky Goods development completed between 2002 (Stage 1 and 2) and 2004 (Stage 3). Stage 1 is anchored by first level Harvey Norman / Domayne (7,384 square metres) as well as 13 specialties to the ground level.

Beenleigh Marketplace, 114 Beenleigh St, Beenleigh

Price: $88.40 million

Date: October 2013

Initial Yield: 7.67%

Market Yield: 7.48%

Rate/sq m: $4,881

Vendor: Colonial

Purchaser: Dexus

Comment: Beenleigh Marketplace is an enclosed single level Sub Regional with a total GLA of 17,128 square metres. The centre commenced trading in March 1999 and comprises a Big W, Woolworths, one Mini-Major tenancy and 54 specialty tenancies.

Bluewater Square, 20 Anzac Avenue, Redcliffe

Price: $41.75 million

Date: March 2013

Initial Yield: 9.84%

Market Yield: 8.51%

Rate/sq m: $4,147

Vendor: Syndicate

Purchaser: CP Retail & Alceon Group

Comment: Bluewater Square Shopping Centre is a two-level, fully enclosed neighbourhood centre. Anchored by a Woolworths (3,941 square metres) and some 27 speciality shops, five kiosks, four ATMS and nine first level office/other tenancies. Car parking provided for some 625 vehicles.

Great Western Super Centre, 1028 Samford Rd, Keperra

Price: $62.90 million

Date: May 2013

Initial Yield: 7.57%

Market Yield: 7.50%

Rate/sq m: $4,088

Vendor: Brookfield

Purchaser: Charter Hall

Comment: A single level partially enclosed Neighbourhood incorporating some bulky goods tenancies. The centre is anchored by Woolworths (3,173 square metres) and Aldi (1,296 square metres).

1

2

3

46

5

Insight Key Australian Transactions

savills.com.au/research 13

Logan Mega Centre, 3525 Pacific Hwy, Slacks Creek

Price: $52.00 million

Date: July 2013

Initial Yield: 10.21%

Market Yield: 9.76%

Rate/sq m: $1,926

Vendor: Mirvac

Purchaser: Blackstone

Comment: Logan Mega Centre is a fully enclosed two level homemaker centre comprising 29 Bulky Goods tenancies over two levels as well as basement car parking for approximately 600 vehicles.

Bunnings Portfolio

Price: $158.69 million

Date: August 2013

Initial Yield: 7.25% (average)

Market Yield: na

Rate/sq m: $2,203 (average)

Vendor: Wesfarmers

Purchaser: BWP Trust

Comment: Wesfarmers (owner of big-box hardware retail chain Bunnings) announced the sale and leaseback of 10 Bunnings properties to the BWP Trust for $271 million. As part of the portfolio six Bunnings properties were located in Queensland.

Ashmore City, Nerang Rd, Ashmore

Price: $37.00 million

Date: September 2013

Initial Yield: 8.40%

Market Yield: 8.62%

Rate/sq m: $4,177

Vendor: Centra Company

Purchaser: Engage Capital

Comment: Ashmore City is an enclosed single level Neighbourhood that also incorporates three freestanding buildings leased to medical, banking and restaurant tenants with a total GLA of 8,858 square metres. The centre is anchored by Supa IGA (2,853 square metres), Crazy Clarks (463 square metres) and 34 specialty shops.

Inala Plaza, 156 Inala Ave, Inala

Price: $32.35 million

Date: August 2013

Initial Yield: 10.99%

Market Yield: 10.08%

Rate/sq m: $1,968

Vendor: 360 Capital

Purchaser: Inala Plaza Qld

Comment: Inala Plaza is a single level, fully enclosed Neighbourhood situated south of the Brisbane CBD and adjoining the partially enclosed Inala Civic Centre. The centre is anchored by Coles (2,748 square metres) and Woolworths (5,163 square metres), with four Mini-Majors, 58 specialties (five vacant), four kiosks and six ATMs (one vacant). Open at grade parking is provided for some 365 vehicles on a site of approximately 3.7181 hectares.

7 8

9

10

Centro Gympie3

14

Savills Research

Insight Key Australian Transactions

South AustraliaSavills has recorded approximately $205 million worth of retail property transactions in the year to December 2013, down from $431 million in the previous year, and down on the five year average, which was $302 million. In the year to December 2013, 29 properties were sold, down from the previous year of 37, and down on the five year average of 39.

The 'Trust' purchaser category was the most active in the South Australian investment market for the year ended December 2013, purchasing 43 percent of stock sold. However, the 'Private Investor' category had the most transactions (22).

Bulky goods property sales in South Australia have decreased in volume in the 12 months to December 2013. Savills have recorded $24 million worth of retail bulky good property transactions within the state, down from the previous year of $134 million and down on the five year average of $54 million.

South Australian Retail Retail Property Sales by Price Range ($m)Dec-07 to Dec-13

< $10m $50 - $100m$10m - $50m > $100m

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3$0

$50

$100

$150

$200

$250

$300

$350

$400

$450

$500

Source: Savills Research

Southgate Plaza, Morphett Vale1

savills.com.au/research 15

16

Savills Research

Fairview Green Shopping, Centre, 325-339 Hancock Rd, Fairview Park

Price: $24.75 million

Date: August 2013

Initial Yield: 9.12%

Market Yield: 8.30%

Rate/sq m: $3,725

Vendor: Akrotiri Property Corp

Purchaser: Primewest Funds

Comment: A Neighbourhood which opened in 2009 comprising a Foodland (4,756 square metres GLA which includes a mezzanine office area of 920 square metres), 14 specialty shops (including one vacancy), kiosk, and two ATM’s. The centre comprises an internal mall while six of the specialty tenancies have external access. The property provides some 398 car parking spaces, the majority (approximately 305 spaces) of which are situated on a lower level with retail area accessed via a travelator. There is also an upper level car parking area (approximately 75 spaces) together with 18 spaces at ground level. Located within a strong retail trade area.

SA Key Retail Transactions 2013

Southgate Plaza, 90-108 Sherriffs Rd, Morphett Vale

Price: $60.00 million

Date: October 2013

Initial Yield: 7.47%

Market Yield: 7.97%

Rate/sq m: $3,787

Vendor: ISPT

Purchaser: Charter Hall

Comment: Southgate Plaza is a single level partially enclosed Sub Regional originally constructed in 1968 and last extended/refurbished in 2012. The centre comprises a Coles (3,696 square metres), Target (7,035 square metres), 39 specialty shops (including three vacancies), 16 ATMs and one pad site. Open air at grade car parking is provided for 767 vehicles on a large site of 4.613 hectares.

Bunnings Warehouse, 933-945 North East Rd, Modbury

Price: $16.30 million

Date: November 2013

Initial Yield: 7.75%

Market Yield: 7.75%

Rate/sq m: $2,642

Vendor: National Mutual Life Nominees (AMP)

Purchaser: Local Private Investor

Comment: Improvements comprise a modern (2004) purpose built hardware and building supplies store, providing open plan showroom for hardware sales, office, fenced garden centre and rear timber storage yard. On-grade car parking is provided for approximately 87 vehicles together with under-croft car parking for approximately 203 vehicles. Leased to Bunnings for an initial 12 year term commencing 1 October 2013 (lease was recently renegotiated) with a further four option terms of five years each. Net passing income is assessed at $1,263,000 per annum. The property was originally purpose built for Mitre 10 Mega Hardware, with Bunnings taking over the site in 2007.

Fairview Green, Fairview Park

“The 'Trust' purchaser category was the most active in the South Australian investment market.” Savills Research

1

2 3

2

Insight Key Australian Transactions

savills.com.au/research 17

71 Rundle Mall, Adelaide

Price: $7.53 million

Date: October 2013

Initial Yield: 5.50%

Market Yield: 5.50%

Rate/sq m: $43,029 (ground floor retail area)

Vendor: Local Private Investor

Purchaser: Private Investor

Comment: Improvements comprise a 2 storey building currently disposed as ground floor retail tenancy and first floor offices. The property is located on the southern side of Rundle Mall to the corner of Francis Street, and west of the newly established Rundle Place retail development. The property is leased to QJ Finance Pty Ltd (trading as Mazzucchelli’s Jewellers) for a term of 5 years commencing 2 April 2012 (lease extension) and expiring 1 April 2017 with a current passing rental of $587,663 per annum gross. Rent is reviewed to CPI annually, with a market review having been implemented as at 2 April 2012 at which time the lease was extended.

Burbridge Shopping Centre, 693-709a Burbridge Rd, West Beach

Price: $6.54 million

Date: November 2013

Initial Yield: 6.38%

Market Yield: 6.38%

Rate/sq m: $2,835

Vendor: Local Private Investor

Purchaser: Local Private Investor

Comment: Burbridge Shopping Centre is a Neighbourhood anchored by a Drake Foodland, together with 12 specialty shops and one ATM. Passing income of the centre is advised as $425,883 per annum net. The property is located approximately 9 kilometres west of the Adelaide CBD, and approximately 500 metres from the Adelaide coastline. The property is situated in a well established catchment area, with the surrounding residential population and seasonal tourism as well as limited competition providing for strong trade in the Centre.

Fairview Green, Fairview Park

71 Rundle Mall, Adelaide

4 5

Bunnings Warehouse, Modbury3

4

Burbridge Shopping Centre, West Beach5

18

Savills Research

Insight Key Australian Transactions

savills.com.au/research 19

VictoriaSavills has recorded approximately $1.9 billion worth of retail property transactions in the year to December 2013, up from $560 million in the previous year, and up on the five year average, which was $1.22 billion. In the year to December 2013, 97 properties were sold, up from the previous year of 75, and up on the five year average of 75.

The 'Fund' purchaser category was the most active in the Victorian investment market for the year ended December 2013, purchasing 27 percent of stock sold. However, the 'Private Investor' category had the most transactions (64).

Bulky goods property sales in Victoria have increased in volume in the 12 months to December 2013. Savills have recorded $98 million worth of retail bulky good property transactions within the state, up from the previous year of $68 million and up on the five year average of $85 million.

Victoria RetailRetail Property Sales by Price Range ($m)Dec-03 to Dec-13

< $10m $50 - $100m$10m - $50m > $100m

Dec-0

4

Dec-0

3

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3

$2,500

$2,000

$1,500

$1,000

$500

$0

Source: Savills Research

“Savills has recorded approximately $1.9 billion worth of retail property transactions in Victoria.Savills Research

206 Bourke Street, Melbourne2

20

Savills Research

Rosebud Plaza, Boneo Rd, Rosebud

Price: $100.00 million

Date: October 2013

Initial Yield: 7.80%

Market Yield: n/a

Rate/sq m: $4,193

Vendor: Colonial

Purchaser: Charter Hall

Comment: Sub Regional with three majors and 53 specialties.

Karingal Shopping Centre, Cranbourne Shopping Centre

Price: Part of $371.00 million portfolio sale

Date: February 2013

Initial Yield: circa 7.25% & 7.50% respectively

Market Yield: n/a

Rate/sq m: $4,485 & $3,706 respectively

Vendor: Federation Centres

Purchaser: ISPT

Comment: Part of $371m shopping centre portfolio sale involving 50% interest in four sub regional centres and a convenience centre. Two centres located in Victoria.

VIC Key Retail Transactions 2013

Greensborough Plaza, Main St, Greensborough

Price: $360.00 million

Date March: 2013

Initial Yield: n/a

Market Yield: n/a

Rate/sq m: $6,223

Vendor: Lend Lease: APPF

Purchaser: Blackstone Group

Comment: Eight majors including Target, Kmart, Coles, Rebel Sport, Harvey Norman & JB HiFi, with 160 specialties.

206 Bourke St, Melbourne

Price: $105.00 million

Date: September 2013

Initial Yield: 7.74%

Market Yield: n/a

Rate/sq m: $8,865

Vendor: Private investor

Purchaser: Hiap Hoe (Singapore)

Comment: City centre arcade including tenants such as G Star, Quicksilver, JB Hi Fi, Regent Club, Shanghai Dynasty and Dragon Boat Restaurant.

Showground Village, Taylors Hill Village, Lilydale Village and Tarneit West Village

Price: Part of $532.00 million portfolio sale

Date: May 2013

Initial Yield: n/a

Market Yield: n/a

Rate/sq m: n/a

Vendor: Coles

Purchaser: ISPT

Comment: ISPT purchased 75% interest in 19 neighbourhood centres owned by Coles for $532 million. Four of these centres were in Victoria. ISPT expected to place centres into newly created trust ISPT Retail Australia Property Trust of which ISPT will be 75% owner and Coles 25%.

Keilor Downs Plaza, 80 Taylors Road, Keilor Downs

Price: $67.00 million

Date: March 2013

Initial Yield: 8.80%

Market Yield: n/a

Rate/sq m: $3,567

Vendor: Centro MCS 33

Purchaser: Colonial

Comment: Anchored by Coles, Aldi and Kmart, including 57 specialties and more than 50,000 square metres vacant land.

1

4

5

6

2

3

Keilor Downs Plaza6

Insight Key Australian Transactions

savills.com.au/research 21

Home HQ, Whitehorse Rd, Nunawading

Price: $48.00 million

Date: July 2013

Initial Yield: 10.70%

Market Yield: 9.79%

Rate/sq m: $2,099

Vendor: Charter Hall

Purchaser: Arkadia

Comment: Bulky Goods centre with three anchor tenants of Nick Scali, The Good Guys and Bev Marks Beds with seventeen other outlets.

Kookai, 254 Collins St, Melbourne

Price: $14.21 million

Date: November 2013

Initial Yield: 4.42%

Market Yield: n/a

Rate/sq m: $35,704

Vendor: Victorian Private Investor

Purchaser: Foreign Investor

Comment: Recently refurbished three level retail building fully leased to international fashion label 'Kookai' on a new long term lease.

Langwarrin Plaza, Alfred Square, Drouin Central, Ocean Grove Marketplace, Target Centre & Wyndham Vale Square

Price: $135.80 million portfolio sale

Date: June 2013

Initial Yield: 7.70%

Market Yield: n/a

Rate/sq m: n/a

Vendor: Lascorp

Purchaser: SCA Property Group

Comment: SCA Property Group acquired a portfolio of seven neighbourhood centres, six in Victoria.

Neighbourhood & Freestanding centres in Bright, Maffra, Mildura and Warrnambool

Price: $53.60 million portfolio sale

Date: November 2013

Initial Yield: n/a

Market Yield: n/a

Rate/sq m: n/a

Vendor: SCA Property Group

Purchaser: Private Investment Consortium

Comment: Five properties (four in Victoria) sold as a portfolio for $53.6 million.

7 9

8

10

Home HQ Nunawading 9

22

Savills Research

254 Collins Street, Melbourne10

Insight Key Australian Transactions

savills.com.au/research 23

Western AustraliaSavills has recorded approximately $1,276.43 million worth of retail property transactions in the year to December 2013, up from $716.88 million in the previous year, and up on the five year average, which was $683.78 million. In the year to December 2013, 27 properties were sold, up from the previous year of 18, and up on the five year average of 17.

The 'Fund' purchaser category was the most active in the Western Australian investment market for the year ended December 2013, purchasing 30 percent of stock sold. However, the 'Private Investor' category had the most transactions (8).

Bulky goods property sales in Western Australia have increased in volume in the 12 months to December 2013. Savills have recorded $20 million worth of retail bulky good property transactions within the state, down from the previous year of $43 million and down on the five year average of $23 million.

West Australia Retail Retail Property Sales by Price Range ($m)Dec-03 to Dec-13

Dec-0

4

Dec-0

3

Dec-0

5

Dec-0

6

Dec-0

7

Dec-0

8

Dec-0

9

Dec-1

0

Dec-11

Dec-1

2

Dec-1

3

Source: Savills Research

$1,000

$1,200

$1,400

$800

$600

$400

$200

$0

254 Collins Street, Melbourne

< $10m $50 - $100m$10m - $50m > $100m

Claremont Quarter, Claremont3

24

Savills Research

WA Key Retail Transactions 2013

Bunbury Forum, Sandridge Rd, Bunbury

Price: $143.28 million

Date: September 2013

Initial Yield: 6.65%

Market Yield: 6.65%

Rate/sq m: $6,410

Vendor: Atlas Point

Purchaser: Challenger

Comment: The centre was sold to Challenger Life after an off market Expressions of Interest campaign closing August 2013. The passing gross rentals within the centre are considered sustainable with the average specialty GOC ratio below industry benchmarks. There is a Development Approval to expand the centre up to 30,942 square metres.

Phoenix Park, 254 Rockingham Rd, Spearwood

Price: $75.80 million

Date: February 2013

Initial Yield: 8.06%

Market Yield: 8.03%

Rate/sq m: $3,690

Vendor: Volley Investments

Purchaser: Rockworth Asset Management

Comment: All three major tenancies trading poorly, below the Urbis average. Subject property sold to a Singaporean investor after a prolonged sales campaign.

Claremont Quarter (50%), Claremont

Price: $171.50 million

Date: February 2013

Initial Yield: 6.17%

Market Yield: 6.22%

Rate/sq m: $11,433

Vendor: Brookfield

Purchaser: QIC

Comment: Remaining 50% interest and management rights retained by Hawaiian. 5.76 year WALE. The centre is currently held within a strata title and as such any future redevelopment potential is very limited.

Melville Plaza, Canning Hwy, Bicton

Price: $29.00 million

Date: April 2013

Initial Yield: 6.83%

Market Yield: 7.36%

Rate/sq m: $3,821

Vendor: Federation Centres

Purchaser: Hawaiian Investments

Comment: The short term lease expiry to Coles (three years) was considered a deterrent to some prospective buyers however most were actively encouraged by this given the outgoings recovery which was considered to provide some leverage at the pending option.

Kelmscott Plaza, Albany Hwy, Kelmscott

Price: $15.00 million

Date: April 2013

Initial Yield: 8.71%

Market Yield: na

Rate/sq m: $2,953

Vendor: CK Properties

Purchaser: Singaporean Investor

Comment: Located on busy Albany Highway, Kelmscott, this centre is anchored by a Woolworths and Wizard Pharmacy, with other national tenants such as Subway.

Secret Harbour, Beard St, Secret Harbour

Price: $33.20 million

Date: June 2013

Initial Yield: 7.80%

Market Yield: 7.81%

Rate/sq m: $4,432

Vendor: Secret Harbour Shopping Centre

Purchaser: Charter Hall

Comment: Transaction includes adjoining 3.1 ha development site for possible future expansion. Sold via an Expressions of Interest campaign.

1

3

4

4

6

5

2

Bunbury Forum, Bunbury

Pheonix Park Shopping Centre, Spearwood Melville Plaza, Bicton

1

2

Insight Key Australian Transactions

savills.com.au/research 25

Centro Mandurah (50%), 330 Pinjara Rd, Mandurah

Price: $131.71 million

Date: June 2013

Initial Yield: 7.25%

Market Yield: 7.18%

Rate/sq m: $7,835

Vendor: Coles

Purchaser: ISPT

Comment: The Centre formed part of the 50% interest acquisition by ISPT in a portfolio of five shopping centres owned and managed by Federation Centres that also included Halls Head in WA, Cranbourne and Karringal in VIC and Warriewood in NSW. The portfolio sale collectively transacted for $371.4 million.

Karrinyup (33%), 200 Karrinyup Rd, Karrinyup

Price: $246.70 million

Date: September 2013

Initial Yield: 5.75%

Market Yield: na

Rate/sq m: $13,504

Vendor: Westfield Group & Westfield REIT

Purchaser: UniSuper

Comment: UniSuper is now the sole owner of this property. Management has been retained by AMP.

Harbour Town (50%), 840 Wellington St, West Perth

Price: $205.00 million

Date: October 2013

Initial Yield: 6.52%

Market Yield: 6.52

Rate/sq m: $9,653

Vendor: Lend Lease

Purchaser: Far East Organisation

Comment: The only dedicated DFO retail asset in Perth and Western Australia. Central Perth location fronting Wellington, Sutherland and Market Streets, West Perth, within 1km of CBD. Located within 200 metres of City West Railway station, and adjacent to Perth’s main north/south freeway’s. Significant landholding of over 1.98 hectares.

Brighton Village, 5 Kingsbridge Rd, Butler

Price: $21.00 million

Date: November 2013

Initial Yield: 7.90%

Market Yield: na

Rate/sq m: $5,460

Vendor: Primewest

Purchaser: Coles / ISPT

Comment: Purchased by the centres anchor tenant Coles in partnership with ISPT. This centre is surrounded by recently developed residential estate in a thriving northern coastal Perth suburb between the Neerabup National Park and the Indian Ocean coast line. Regarded as one of Australia’s fastest selling coastal communities and the fastest growing residential area in the City of Wanneroo.

5

7

8

8

10

10

9

Bunbury Forum, Bunbury

Kelmscott Plaza, Kelmscott

Karrinyup Shopping Centre, Karrinyup

Harbour Town, West Perth

Savills Research

26

Dominic LongManaging Director VIC+61 (0) 402 441 074+61 (0) 3 8686 [email protected]

Glenn LampardDivisional Director, Research+61 (0) 419 008 742+61 (0) 3 8686 [email protected]

QLD

SA

WA

Paul McLeanCEO & Managing Director QLD+61 (0) 7 3221 [email protected]

Rino CarpinelliManaging Director SA+61 (0) 414 842 673+61 (0) 8 8237 [email protected]

Steven LercheDivisional Director, Retail Sales+61 (0) 414 467 216+61 (0) 2 8215 [email protected]

Paul CraigManaging Director WA+61 (0) 422 235 519+61 (0) 8 9488 [email protected]

Tony CrabbNational Head, ResearchResearch+61 (0) 422 221 604+61 (0) 3 8686 [email protected]

Peter TysonDivisional Director, Retail Sales+61 (0) 418 725 155+61 (0) 7 3002 [email protected]

Paul DayDivisional Director, Research+61 (0) 403 324 737+61 (0) 7 3002 [email protected]

Pat De MariaExecutive, Investment Sales+61 (0) 421 569 984+61 (0) 3 8686 [email protected]

Hamish JohnstonAnalyst, Research+61 (0) 439 833 808+61 (0) 8 8237 5029 [email protected]

Gemma AlexanderAssociate Director, Research+61 (0) 437 051 397+61 (0) 8 9488 4140 [email protected]

Miles RoweDivisional Director, City Sales+61 (0) 422 236 311+61 (0) 8 9488 4116 [email protected]

Simon FennManaging Director NSW+61 (0) 438 573 431+61 (0) 2 8215 [email protected]

Phil HardingManaging Director ACT+61 (0) 408 868 206+61 (0) 2 6221 [email protected]

Simon HemphillDivisional Director, Research+61 (0) 466 775 680+61 (0) 2 8215 [email protected]

NSW / ACTKey Contacts

VIC

Insight Key Australian Transactions

savills.com.au/research 27

This information is general information only and is subject to change without notice. No representations or warranties of any nature whatsoever are given, intended or implied. Savills will not be liable for any omissions or errors. Savills will not be liable, including for negligence, for any direct, indirect, special, incidental or consequential losses or damages arising out of our in any way connected with use of any of this information. This information does not form part of or constitute an offer or contract. You should rely on your own enquiries about the accuracy of any information or materials. All images are only for illustrative purposes. This information must not be copied, reproduced or distributed without the prior written consent of Savills.

Savills Research Queensland

Spotlight Brisbane CBD Retail March 2013

Highlights International retailers such as Zara,

Abercombie & Fitch continue to look for prime retail space in Brisbane’s CBD.

Brisbane’s CBD Retail vacancy has declined from 6.30% at August 2011 to 6.01% as at March 2013.

Department stores and services dominated the tenancy mix comprising each 23% of total (sq m) retail space in the CBD.

Retail rents in the CBD should

remain relatively steady in the short term as the effects of the economy hold back further increases.

Overall the future looks bright for Brisbane’s CBD retail market and should be supported by strong population growth and demand from leading international retailers.

Download the Savills Appfor insights at your fingertips

Savills Research TeamOur highly regarded research division are dedicated to understanding and giving in-depth insight into the commercial, industrial & retail markets throughout Australia.

We also provide in-depth consultancy services, ranging from tenant representation to property site selection for multinational businesses.

Our research teams are highly qualified real estate professionals with comprehensive knowledge of property markets across Australia. The Savills Research & Consultancy team has years of experience, and supported by our extensive agency, property management and valuation professionals, are highly regarded and respected along with Savills Research teams across the globe.

Savills provide free research reports on all major property markets, and some example papers include:

� Office Markets � Retail Markets � Residential Trends � Industrial Markets � International Markets

For our latest reports, contact one of the team or visit savills.com.au/research

Adelaide

Brisbane

Canberra

Gold Coast

Melbourne

Notting Hill

Parramatta

Perth

Sunshine Coast

Sydney

+61 (0) 8 8237 5000

+61 (0) 7 3221 8355

+61 (0) 2 6221 8200

+61 (0) 7 5509 1700

+61 (0) 3 8686 8000

+61 (0) 3 9947 5100

+61 (0) 2 9761 1333

+61 (0) 8 9488 4111

+61 (0) 7 5313 7500

+61 (0) 2 8215 8888

savills.com.au

Savills is a leading global real estate service provider listed on the London Stock Exchange.

The company, established in 1855, has a rich heritage with unrivalled growth and has been ranked No.1 by turnover in the UK by the Estates Gazette for ten consecutive years. Savills is a company that leads rather than follows and now has over 500 offices and associates throughout the Americas, Europe, Asia Pacific, Africa and the Middle East.

Across the Asia Pacific, Savills have over 45 offices in Australia, New Zealand, Singapore, Malaysia, Thailand, Vietnam, Hong Kong, Macao, China, Taiwan, Korea and Japan.

Savills Australia specialises in the provision of industrial, commercial, retail and residential property services across the country. We are recognised as established leaders within the Australian property markets and deliver a seamless service both locally and throughout our global network of offices.

A unique combination of sector knowledge and entrepreneurial flair gives clients access to real estate expertise of the highest calibre. We are regarded as an innovative, thinking organisation cemented by the best people with excellent negotiation skills. Savills focus on a defined set of clients, offering a premium service to organisations and individuals with whom we share a common goal.

Contact Savills for advice on all aspects of property:

Sales and Leasing Corporate Advisory Asset Management Property Accounting Valuations Residential Services Project Management Research