sbd achievements in the first two years of … 4_marlene... · 4,9 million in poverty 1 million not...

TRANSCRIPT

SBD ACHIEVEMENTS IN THE FIRST TWO YEARS OF EFFECTIVE

IMPLEMENTATIONRESULTADOS DEL I SEMESTRE DEL 2017

6 | SETIEMBRE | 2017

Costa Rica | Cifras

Total Population4,9 million

In Poverty

1 million

Not Poor3,9

million

Women50%

Female Householders

40%

Average IncomePer household: $1737.34Per capita: $642.8243% of the population

Earns less than $800.67 a month

Fuente: Datos obtenidos del INEC.

Costa Rica | Parque Empresarial Mipyme

Fuente: ENAHOPRO - INEC - 2015

The SME business park, accordingto data from the National Survey ofProducing Households (ENAHOPRO)of INEC, in 2015, registered a totalof 460,368 independent employeesand entrepreneurs.

460.368Independent employees or

entrepreneurs

Costa Rica | Cifras

SME Business Park20.243

4.0724.563

Central RegionConcentrates 75% of the country’s economic activity

SMEsGenerate 30% of employment.

Fuente: Estado situación de la Pyme en CR 2016 - MEIC

MicroSmall

Medium

28.878 SMEs

Costa Rica |SME Business Park

Fuente: Estado situación de la Pyme en CR 2016 - MEIC

Small14.1%

Medium15.8%

Micro70.1%

Industry12%

IT5%

Commerce40%

Services43%

In 2016, SMEs accounted for 93.3% of companies in the country.

The Service and Trade sectors grouped83% of SME companies.

¿What is the BSD?

It is a public policy oriented to promote thedevelopment of SMEs of all sectors andentrepreneurships; through financing and businessdevelopment services.

It is financial inclusion and promotion.

BSD | Strategic Partners

53Operations

19Regulated SUGEF

33Non regulated

43

Public Banks

Private Banks

9 Savings and CreditCooperatives

2 Financecompanies

1 Mutual Funds

14 ServiceCooperatives

12 Microfinancing

14 Placement agents

•BSD conducts training for operators to improvemarket service abilities.

• Overall, 800 points of customer service in thecountry.

• Greater access to micro, small and mediumproducers.

• Times for appointments have been reduced.

• More expedited procedures for credits.

• Different market niches are dealt with byspecialized personnel.

Products from BSDProducts

Financial

Capital Seed

Credits•Emergency Credits

•Direct credits•Credit lines

•Production Chains

Guarantees• individual

•Portfolio Guarantess

Support for Companies:

Technical Assistance

Financial Education

Capacity building for BSD operators

¿What is the BSD?

We will be the strategic ally of SMEs in the countryfor its growth and development through financialsolutions adapted to their needs.

We promote the creation, innovation, productivityand competitiveness of SMEs in the country, throughfinancial and business support solutions.

VISION

MISSION

The work of BSD in Policies and Actions for Financial Inclusion and

Education.

Technical SecretarySeptember 2017

gOB

Areas

Legal ProductOperators

Rules &Regulations Placing Impact

Actions

BSD | Legal Framework

• Development of specialized regulations.• Reduction in funding costs.• More financial operators.• Portfolio of products according to economic activities.• Dynamism in meeting the needs of the producer.• Support for entrepreneurship and seed capital of high

value generation.

Benefits of the Reform to the Law 9274

gOBLegal Legal Framework Improved

Reform of Law 8634 of the SBD through the approval of Law 9274 (November 2014)and regulated on March 9, 2015.

"The development of financial products under Law 8634 focused on loans and guarantees, with little progress in new products to support entrepreneurship." The reform of the Law gives a boost to products through the new categorization of beneficiaries (associative models, microcredit and entrepreneurs) as well as new tools.(Evaluation Committee, 2nd report, October 2016)

Topic Law 8634 and its Regulations Ley 9274 and its Regulations

Beneficiaries SMEsMediim enterprise that ahs no access to public banks.

Defines the beneficiary: micro and small enterprises, small micro agricultural producers, associative groups, microcredit beneficiaries, entrepreneurs,Medium-sized company by a reasoned exception from the Rector's Council

Priority Zones Zones outside of the main cities. Areas with less social development

Formality Requires formality of the beneficiary companies after two years

This access barrier is eliminated

Scope of the funding

Viable feasible projects technically, economically and financially

Financing and promotion of productive projects

Concept of Banking for Development

Banking for development as an obligation of public and private banks

Development Banking as a line of business with different characteristics to commercial banking

Guarantees Individual guarantees for beneficiaries with insufficient guarantees

Explicit authority for portfolio guarantees and counter-guaranteesAcknowledgment of Guarantee as unconditional and irrevocableLeverage of the guarantee fund greater than 1Guarantee for beneficiaries with insufficient guarantees

Non financialservices

Inoperability of business support services provided by INA

Powers to dictate policies to the Governing Council on the use of resources in relation to the needs of the beneficiaries of the Law.Result: Practical implementation PYMES INA.

OrientationFundamentals

Access to credit,Access to guaranteesAccess to business support servicesFinancial sustainability of resourcesDifferentiated regulation

Financial and economic inclusionReal access to financingReal access to guaranteesReal access to business support servicesEffective monitoring of resources

Perspective of Support to the Beneficiary

Topic Law 8634 and its Regulations Law 9274 and its Regulations

Financial Operators Only the SFN regulated by the General Superintendency of Financial Entities (SUGEF)

Incorporates microfinance institutions as channelers of financial resources

Structure Complex bureaucratic structure Simplifies the structure. More efficient. The Technical Secretary assumes a central role of supervision, control, coordination and follow-up of the guidelines of the Governing Council.

Fiancial Resources Inoperancia de los principales recursos de fondeo (FCD)Recursos de Bancos Privados a Públicos en calidad de préstamo. Poca posibilidad práctica de bancos privados operen sus propios recursos

Financial cost reasonablenessPublic transfer of funds for the "BriefcaseTax" for FINADEPossibility of borrowing of FINADE (trust)

Normative Diferentiated normative Minimum conditions for a prudential regulation and creation of the BSD Credit Information System

Sancitions to the SFN

Not defined Penalties of up to 1% of the equity due to negligence or fraud, coordination scheme SBD-SUGEF-CONASSIF

Control and Supervision

Scheme supervision and control: Comptroller, SUGEF; Central bank; Internal and External Audit of the participating banks in the SBD and the Technical Secretary of the BSD.Policy Recommendations and evaluation of system performance and impact: Evaluation Commission, every 4 yearsAccountability: Legislative AssemblyOthers: Joint Advisory Commission with Advice, Policy Recommendations and Impact Measurement to the Governing Board.

Supervision and Control Scheme: Comptroller, SUGEF, Internal and External Audit of the banks participating in the BSD and the Internal Audit of the BSD.BSD performance evaluation and policy recommendations and best banking and prudential practices: BCCR and Evaluation Commission (c / 4 years)Annual Accountability: Legislative AssemblyNon-regulated entities: Monitoring unit of the Technical Secretariat of the Governing Council.

Structural Perspective

Topic Law 8634 and its Regulations Law 9274 and its Regulations

Limits At least 40% to the Agricultural SectorGuarantee up to 75% of the amount of credit

At least 40% to the agricultural sectorAt least 25% to FOFIDE Microfinance; CDF; development credits of Private BanksGuarantee up to 75% of the amount of credit

Microfinance N/A Possibility of channeling resources from SBD FundsRecognition as beneficiary of the lawAccess to the Guarantee FundPossibility of securitization of your credit portfolios according to rules established by SUGEVAL (not yet implemented

Structural Perspective

Areas

Rules and Regulations

Actions

Rules and Regulations

SUGEF Special Regulation and supplementary

regulations issued by BSD

The Conassif issued a special Regulation, which runs from October 2016, for themanagement and evaluation of credit risk for the Development Bank System (SUGEF15‐16), which, among other things, offers a differentiation technique according toparticular characteristics of the line of development banking business.

Operating regulations on the first and second floor credit activity of banksparticipating in the Banking System for Development (AG‐1583‐197‐2016, in effectsince January 2017)

SUGEF Agreement 15-16

The main scope of this regulation, derived from Law 9274, is as follows:

• Development banking as a line of business: second-tier banking and other development debtors.

• Methodologies backed by credit policies, corporate governance and a risk-based supervision approach.

• Look for consistency with international practices or standards.

• Simplified framework and requirements for minimum information needed in credit files.

• Consideration of the funds of guarantees and guarantees as mitigation, and the technical definition of the level of coverage (number of times) of the guarantee fund.

• Disclosure of credit information of the BSD in support of credit management.

• Microcredit risk rating according to the nature of development operations

• Consideration of security interests as risk mitigation.

• Development of CIC BSD, debtor central.

• Weighting of microcredits in 75% in solvency ratio.

• Recognition of group credits as a form of financing.

BSD Agreement AG-1583-197-2016

It develops the figure of Correspondents banking under two modalities:

Bank Correspondents

Placement Agents (1st floor

bank)

Correspondent Agents (assumes only part of the credit process)

The following aspects are regulated:FormalityResponsibilitiesInfrastructureIts functions vis-à-vis the beneficiaryControl and Transparency

•Second floor bank•1rst and 2nd floor operation

•Placement agent and correspondent

•Beneficiary and operator profile

Definitions

•Operator’s accreditation•Program Authorization• Correspondent’s Registry

Authorization Process

•About beneficiaries of law•About goals and limits•Selection of agents (contracts)

Corp. Governance Responsibilities

•Program Risks•Credit Process•Case file

Management of risks and credit process.

•Plans•Effective rate.

Release of information

•Responsability.•Capture, verification, remission

Information

•Responsabiilities•Prohibitions

Agents

BSD Agreement AG-1583-197-2016: Structure of the Regulations

Area

Product Operators

Actions

CAR: Banking opportunities tailored for the rural sector

Products

– They are Rural Support Councils (CARs) that emulate the former figure of rural credit boards of the National Bank (no longer active).

– The new BNCR Program with BSD support includes:• Microcredit with a threshold of ₵ 5million• Portfolio guarantees• Business Development Resources

– Scheme for Bank Correspondents in areas of low financial penetration:– First C.A.R .: Agricultural Centers of Nandayure and Tarrazú, Azada Cariari,

Bijagua Association– It is based on: Customer knowledge, small division of operations and

simplified procedures

CAR: Synergy of Participantsand Products

PARTICIPANTS BENEFITSDebtor (Beneficiary) Access to credit with simple processing and business

support serviceslFinancial Operator BNCR Liquid guarantees

Credit Divisibility Penetration in areas where the bank has no presence Reduces costs associated with risk assets (estimates and

capital)

Correspondent Agent Progress in your Community Access to SBD Resources (financial and non-financial) You can charge commission to your customers

FINADE Increases Leverage of the Guarantee Fund Higher profits Reduces operating costs

Area

Placement

Action

Costa Rica in numbers and the importanceof SMEs

Portfolio of BSD on 30/6/17

Portfolio of BSD on 30/6/17

AREA

Impacts

Action

BSD | Placements

350.422

261.14525%

78% Micro enterprise

35.711 operations

30% Zones with “Very low” and “low” social developmentindex.Millions in Costa Rican colones

TOTAL CREDIT BSD

I Semester of 2017

Total Placement Total

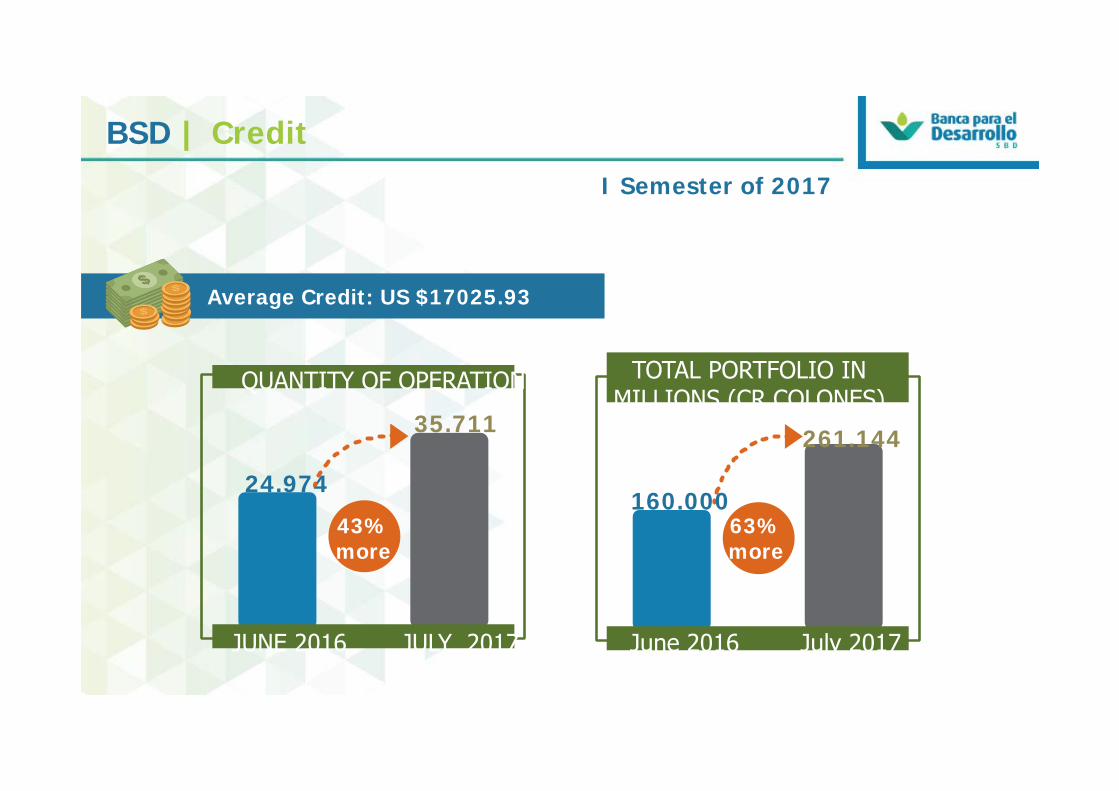

BSD | CreditI Semester of 2017

Average Credit: US $17025.93

QUANTITY OF OPERATIONS

24.974

43%more

35.711

JUNE 2016 JULY 2017

TOTAL PORTFOLIO IN MILLIONS (CR COLONES)

160.000

261.144

63%more

June 2016 July 2017

BSD | CreditI Semestre del 2017

Credit Portfolio by RegionCR Colon

172.697

177.725

Central Rural

HUETAR ATLANTIC

3%

HUETAR NORTH

20%

CHOROTEGA12%

BRUNCA

12%

CENTRAL

49%

CENTRAL PACIFIC

4%

COLOCACIÓN POR REGIÓN

51% Resources in Rural Areas

More resources to zones with low banking

SBD | CreditI Semester of 2017

53% in Agricultural Sector

PLACEMENT BY ACTIVITY

Transport5%

Tourism1%

Agriculture53%

Trade16%

Industry5%

Services20%

2%

20%

78%

MediumSmallMicro

BSD | Access by Genre

25%

57%

18%

BDS | Inclusion

626 New Clients per month

SBD | Inclusion

35 711Operations

112Entrepreneurs

30.677Micro

3.858Small size

103Medium size

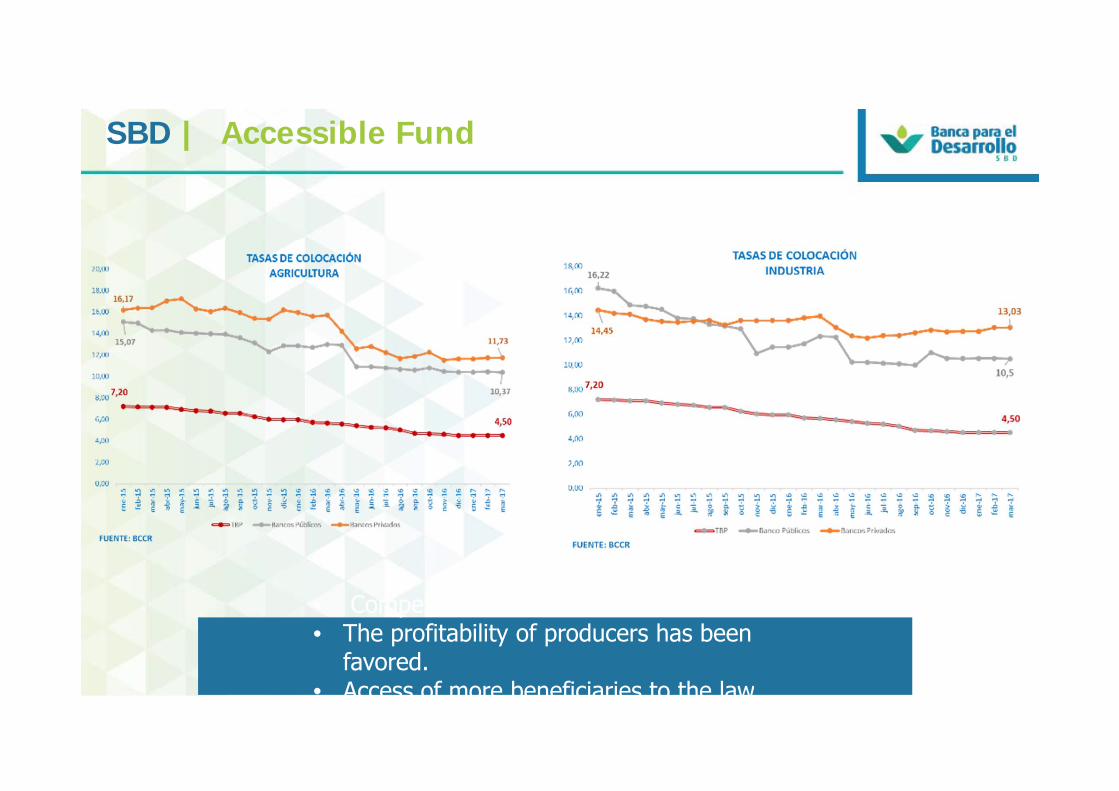

SBD | Accessible Fund

• Competition of rates in the market.• The profitability of producers has been

favored.• Access of more beneficiaries to the law

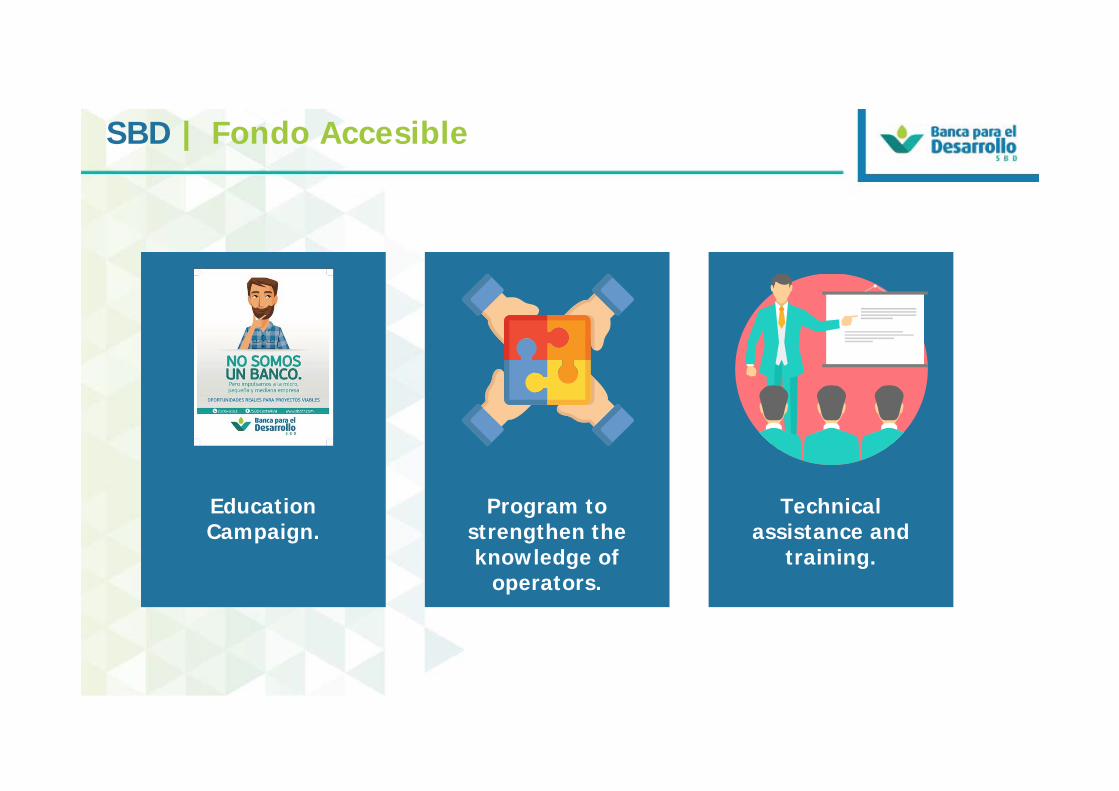

SBD | Fondo Accesible

Fomento de la innovación

y tecnologías limpias

EducationCampaign.

Program tostrengthen theknowledge of

operators.

Technicalassistance and

training.

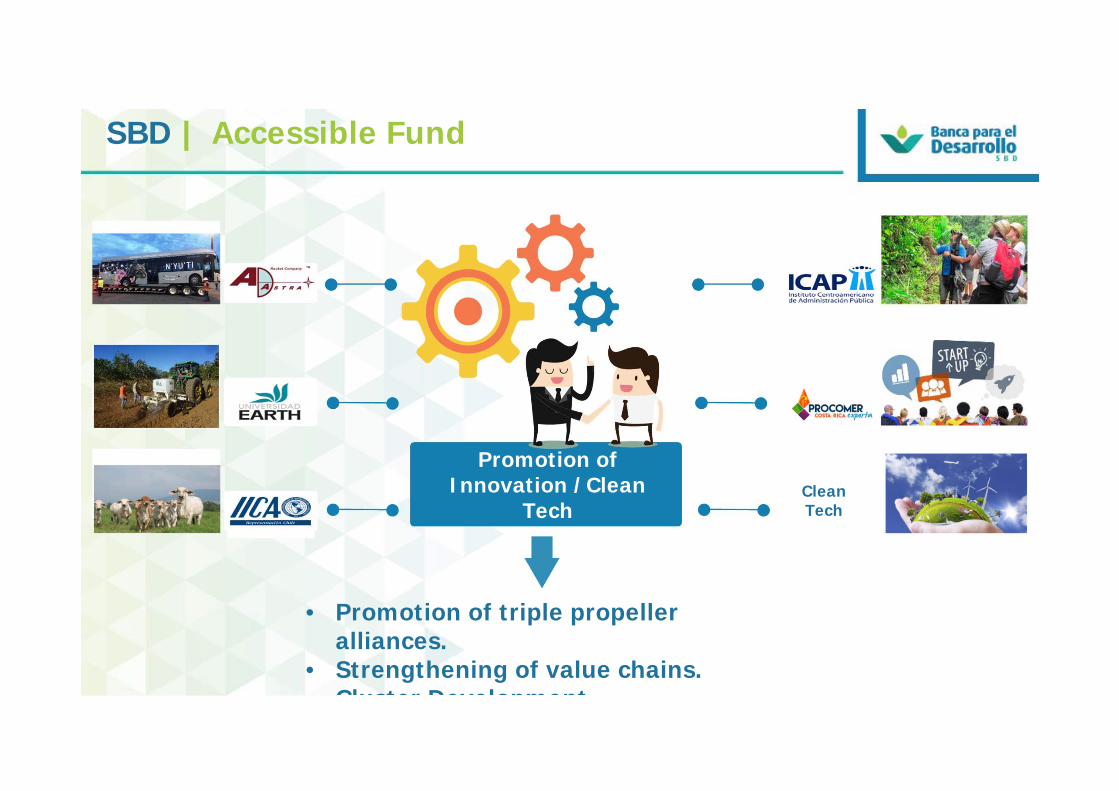

SBD | Accessible Fund

CleanTech

Promotion of Innovation /Clean

Tech

• Promotion of triple propelleralliances.

• Strengthening of value chains.Cluster Development

Projects under development towards Financial Inclusion

• CIC SBD –SUGEF: Credit information of the SBD beneficiary. Joint project with the Superintendency of Financial Institutions..

• PSBD Client Protection Protocol: joint project with the Central Bank of Costa Rica (BCCR).

• Self-regulation and Market Discipline for Microfinance Institutions: Jointly with REDCOM (Microfinance Network)