scholarship project paper 2014 market's responses to ... · necessarily represent the capital...

TRANSCRIPT

www.set.or.th/setresearch

Disclaimer: The views expressed in this working paper are those of the author(s) and do not necessarily represent the Capital Market Research Institute or the Stock Exchange of Thailand. Capital Market Research Institute Scholarship Papers are research in progress by the author(s) and are published to elicit comments and stimulate discussion.

Scholarship Project Paper 2014

Market's Responses to Deferred Taxes: Evidence from Early Adoption and Effective Periods

Preeyanan Chotikasilp Management Accounting Staff

PTT Global Chemical Public Company Limited Bangkok, Thailand 10900

E-mail: [email protected]

Pailin Trongmateerut, PhD* Lecturer in Accounting Thammasat University

Department of Accounting Thammasat Business School

Bangkok, Thailand 10200 E-mail: [email protected]

*Corresponding author

www.set.or.th/setresearch

Disclaimer: The views expressed in this working paper are those of the author(s) and do not necessarily represent the Capital Market Research Institute or the Stock Exchange of Thailand. Capital Market Research Institute Scholarship Papers are research in progress by the author(s) and are published to elicit comments and stimulate discussion.

Chaiyuth Padungsaksawasdi, PhD Lecturer in Finance

Thammasat University Department of Finance

Thammasat Business School Bangkok, Thailand 10200

E-mail: [email protected]

20 February 2015

Abstract

This study examines how the market perceives the relevance of deferred tax assets and liabilities and

current period tax deferrals that reported by Thai companies under the balance sheet method of IAS 12 over the

period 2010 – 2013. Our results suggest that net deferred taxes are viewed as future tax saving. The market seems

to weigh deferred tax liabilities as liabilities but does not price deferred tax assets as assets. Furthermore, we finds

that the market values deferred tax assets reported by loss-making financial firms that early adopted IAS 12.

JEL Classification: Preeyanan was a graduate student, Master of Science in Finance (MIF), Thammasat Business

School when conducting this research. We thank Pornchai Chunhachinda, Anutchanat Jaroenjitrkam, for very helpful

comments and discussions. The opinions/suggestions/comments conveyed in this study are those of the authors,

and do not necessarily reflect that of PTT Global Chemical Public Company Limited. All remaining errors are owns. Keywords: Deferred Tax, Current Tax Deferral, TAS12, Value Relevance, Market Perception.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

Content

Page

Chapter 1 Introduction 2

Chapter 2 Li terature Review 5

Chapter 3 Practices of Early Adoption 9

Chapter 4 IAS No. 12 and accounting environment 10

Chapter 5 Data and Methodology 11

5.1 Data

5.2 Regression Models

Chapter 6 Empirical Results 15

6.1 Descriptive statistics

6.2 Net deferred tax assets and net deferred tax liabilities

6.3 Net current tax deferrals

6.4 Deferred tax assets and deferred tax liabilities

6.5 Evidence in financial sector during early adoption period

Chapter 7 Conclusion, Limitation, and Future Research 21

References 23

Table

1. Industry classification 26

2. Descriptive Statistics 26

3. Pearson correlation metrics 29

4. Levels regression using unbalanced panel data and GLS 30

5. Returns regression using unbalanced panel data and GLS 31

6. Levels regression using unbalanced panel data and GLS 32

7. Levels regression: Financial sector versus other sectors in early adoption period 34

2014 Capital Market Research Institute, The Stock Exchange of Thailand

2

Chapter1 Introduction

Accounting for income tax has been mandatory practice worldwide. However, the

usefulness of deferred tax accounting remains inconclusive. IAS 12 requires deferred tax assets

and deferred tax liabilities be recognized under the balance sheet method. The deferred tax

assets are the amounts of income taxes recoverable in future period in respect of the

deductible temporary difference1 and the carryforwards of unused tax losses and tax credits.

The deferred tax liabilities are the amounts of income taxes payable in future periods in respect

of taxable temporary differences.2 Moreover, firms are required to disclose the major

components of deferred tax expense (income) relating to the origination and reversal of

temporary differences, for example, depreciation and amortization, loss carried forward and

provision of employee benefit.

Prior studies examine the market perception of the relevance of deferred tax

assets and liabilities by Australian companies under the income statement method3 specified by

the Australian Accounting Standards Board in 1020 (AASB 1020) (Chang, Herbohn and Tutticci,

2009) and by U.S. companies under the balance sheets method4 specified by Statement of

1 Temporary difference is the difference between the carrying amount of an asset or liability in the statement of financial position and its tax base. Deductible temporary difference is temporary difference that will result in amounts that are deductible in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled. 2 Taxable temporary differences is temporary difference that will result in amounts that are deductible in determining taxable profit (tax loss) of future periods when the carrying amount of the asset or liability is recovered or settled. 3 The income statement method recognizes timing differences between taxable income or loss and accounting profit or loss as deferred tax assets or liabilities. 4 The balance sheet method of tax accounting recognizes temporary differences between the carrying amount of an asset or liability and its tax base as deferred tax accruals. The balance sheet method results in an increase in components giving rise to deferred tax assets and liabilities.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

3

Financial Accounting Standards No.109, Accounting for Income Taxes (SFAS 109) (Amir, 1997;

Miller and Skinner 1998) and under the income statement method specified by Accounting

Principles Board Opinion No.11, Accounting for Income taxes (APB 11) ( Givoly and

Hayn,1992; Chaney and Jeter, 1994). In general, the result of studies suggest that the market

views the deferred tax liabilities as other reported liabilities, although the relation may be

tempered by recurring items that have little reversal and views the deferred tax assets as future

tax saving, although the relation may be reduced since the market could be interpreted as a

signal of future losses.

Research Objective:

We aim to investigate how the market views deferred tax assets and deferred tax

liabilities surrounding the IFRS environment. Though prior research does not substantiate

enough evidence to formulate directional hypotheses, the required disclosure under IAS 12

guides our propositions as follows. Our main research question is whether deferred taxes are

priced by the market. To gain more insight, we conjecture that the market accounts for the net

change of deferred tax balance. The loss reporting firms are of our interest as well, since the

way the market processes the information content of loss is different from that of net income

(Hayn, 1995). More importantly, loss firms usually report the loss carryforwards as a

component of their deferred tax assets that will reverse in the short run according to IAS 12.

Furthermore, Thai market offers a unique way to explore the impact of early and mandatory

adoption of IAS 12.5 We also investigate how market perceives components of deferred

taxes disclosed by early adopters and mandatory adopters. The industry effect appears to play

roles in how market processes deferred tax information (Chang et al., 2009); we thus

5 The Federation of Accounting Profession (FAP), the sole Thai accounting standard setting body, mandates the adoption of the Thai Accounting Standard No. 12 Income Taxes (TAS No. 12) by January 1, 2013. TAS No. 12 is directly translated from IAS No. 12. FAP explicitly encourages listed firms to early adopt the standard.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

4

separately examine the financial sector due to its distinct business characteristics and highly

regulatory requirements (Skinner, 2008).

Expected outcomes

Our findings contribute to the body of income taxes literature in a number of ways.

1. We examine the information content of deferred taxes in the IFRS regime using

rigorous statistical analytical method.

2. We find the early adoption effect on how market prices deferred tax balance.

Timing of adoption is a significant factor in deferred tax content.

3. We include the loss firms in our study to gain more insight how the market

differentially perceives deferred taxes of loss firms.

4. The financial industry variable in our analysis helps explain the market

perception and deferred tax balance reversal expectation.

The results offer practical implications.

1. Our study informs standard setting bodies how presentation and disclosure of

deferred taxes are viewed. Deferred tax assets and deferred tax liabilities are asymmetrically

valued.

2. Regulatory monitoring of the deferred tax balances and movement is

quintessential for the financial industry because our evidence suggests the market prices the

information content of deferred tax assets disclosed by early adopters in the financial sector.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

5

Chapter 2 Literature Review

The particular purpose of accounting for deferred taxes is to report tax information

useful to stakeholders. Importantly, accounting for income taxes serves as a linkage between financial

statements and tax returns (Graham et al., 2012). Deferred tax disclosure is the only source of

information about current and future taxes for investors. However, deferred tax accounting is a

complex, debatable issue in financial reporting. The differences between accounting principles and

revenue codes result in book-tax differences, namely the temporary and the permanent differences.

Temporary differences are the differences between the book value of an asset (a

liability) and its tax base resulting in taxable amount. The differences must be accounted for and

presented on financial statements. These differences in bases result in taxable or deductible amounts

in future years, when the asset is recovered or the liability is settled.6 Permanent differences, another

type of book-tax differences, will never reverse due to tax law. Certain expenses are never allowed as

tax deductions, such as entertainment expenses; and certain revenues are never taxed, such as

research grant for educational purpose. Permanent differences hence are not a concern for financial

reporting. Accounting for income taxes technically affects every transaction in which a firm engages

and causes the complex as well as costly accounting process of deferred tax allocation. In sum, the

benefits of deferred tax disclosures remain controversial.

Although accounting for income taxes was first prescribed in 1942 in the U.S. and has

long been evolved from the income statement approach to the balance sheet approach, prevailing

6 As an illustration of temporary differences, if the market price of merchandise inventory declines permanently, the inventory must be marked down to the market price and the loss is recognized immediately for financial reporting. For tax purpose, this write-down will be deductible through the actual sales of the inventory. Thus, tax benefit will arise until the loss is realized under tax law. To further explain the timing difference, the book and tax treatments of property, plant, and equipment are diverged. Given faster depreciation under tax law, the amount of tax depreciation is higher than that of book depreciation. Consequently, the tax amount of property, plant, and equipment is lower than the book amount resulting in the deferred tax liability.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

6

research in the value relevance of deferred taxes is scant.7 Given the non-extensivity of the numbers

of studies and the limitations of prior research designs, past research in the incremental information

content of the income taxes reveal inconclusive evidence. Hence, we group prior evidence into two

categories; the U.S. and the rest of the world, due to the fact of large empirical evidence emphasizing

in the U.S. capital markets.

First, we group deferred tax studies in the U.S. into two parts based on the accounting

standards, namely the income statement and the balance sheet approaches.8 Up to date, the findings

on price-deferred tax relation remain mixed. Early empirical works conducted under the income

statement approach according to APB No. 11 establish that deferred tax liabilities are value relevant

(Beaver and Dukes, 1972; Givoly and Hayn, 1992; Amir et al., 1997; and Ayres, 1998). Givoly and

Hayn (1992) document that the market perceives deferred tax liabilities as future tax costs, since the

enactment of the Tax Reform Act of 1986 reduced the corporate tax rate from 46 percent to 34

percent.9 Particularly, abnormal stock returns positively associate with the amount of deferred tax

liabilities. In different findings, Chaney and Jeter (1994) find a negative relation between deferred tax

liabilities and stock returns. They conclude that the market views deferred tax liabilities as future tax

payment and provides information about level of manipulation in reported earnings.

7 Graham et al. (2012) provide the background and an excellent review of pertinent research of accounting for income taxes. 8 The income statement approach recognizes timing differences between taxable income and accounting income as deferred tax assets or deferred tax liabilities. This approach compares revenues and expenses recognized for book and tax purposes, eliminates permanent differences, and computes income tax expenses based on book income before taxes (excluding permanent differences). The difference between the income tax expense based on book income and the current income tax to be paid to the tax authority is either deferred tax asset or deferred tax liabilities. APB No. 11 requires firms to report only the net deferred tax liabilities without separate disclosure of deferred tax assets. The balance sheet approach recognizes timing differences between the carrying amount of an asset (a liability) and its tax base as deferred tax accruals. The balance sheet method results in an increase in components giving rise to deferred tax assets and deferred liabilities. The recognition of deferred taxes reflects that it is probable that the recovery or settlement of the carrying amount will make future tax payment smaller (or larger) than they would be if such recovery or settlement were to have no tax consequences. 9 The decrease in tax rate causes the decrease in cash outlays. The DTL as future tax payment would decrease at lower tax rate. Subsequently, the smaller the DTL, the larger the firm value.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

7

The balance sheet method, consequently prescribed in SFAS No. 10910 superseding

APB No. 11 in 1992, instigates further empirical studies in the incremental value relevance of deferred

tax accounts. Using a price levels approach, Amir et al. (1997) examine the market valuation of

various deferred tax components. They document that the market prices the components of deferred

tax accounts differently, depending on the likelihood of the reversal in these accounts.11 This means

that the deferred tax liabilities from depreciation and amortization are not priced significantly because

of continuing investment in depreciable assets and low probability of reversal. Differently, the market

significantly prices the deferred taxes from restructuring charges as this component is expected to

reverse in the near future. Interestingly, the loss carryforwards component is not value relevant,

implying that investors do not expect the loss carryforwards to be utilized. Ayers (1998) indicates that

the separate recognition of deferred tax assets, the valuation allowance, and the adjustments for tax

law changes are associated with firm value. SFAS No. 109 indeed provides value relevant information

beyond APB No. 11. Amir and Sougiannis (1999) find a strong positive relation between deferred

taxes from loss carryforwards and share prices, since it represents as future tax saving. Chen and

Schoderbek (2000) find no evidence that financial analysts accounted for a higher tax rate alter their

earnings forecasts. Lev and Nissim (2004) find no significant relation between deferred tax expense

and annual stock returns, suggesting the value irrelevance of deferred taxes.

Second, in addition to the evidence in the U.S. discussed above, Zeng (2003)

examines the valuation of loss carryforwards (one of deferred tax components) in Canadian market

and finds that loss carryforwards enhance firms' market values. Chang, Herbohn, and Tutticci (2009),

who study the roles of deferred tax in Australia, consider the value relevance of deferred tax assets

and liabilities under the income statement approach specified by AASB No. 1020. They conclude that

10 SFAS No. 109 requires firms to disclose deferred tax assets and deferred tax liabilities, as well as to classify them either as current or noncurrent, which is based on the classification of the related nontax assets or nontax liabilities for financial reporting. Tax assets or liabilities that are not associated with a respective underlying asset or liability are classified based on the expected reversal period. 11 DTA and DTL will reverse when the transaction settlements incur following the tax code. For example, warranty expense must be estimated and booked since the sale transaction occurs in the first year. Thus, warranty expense and liability are recognized. This give rises of DTA and tax deductible. In the following year, warranty claim is made. Then, the reversal of DTA occurs.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

8

the market perceives deferred tax assets as future tax saving and deferred tax liabilities as future tax

payment. They elaborate that an increase in deferred tax assets from loss carryforwards is viewed as

future cash saving when firms make profits. Chludek (2011) examines the value relevance of deferred

taxes based on German firms surrounding with the IFRS environment. In general, investors in German

market do not consider deferred tax as important information. However, large net deferred tax assets

are most likely to translate into actual cash flow and considered value relevance.

A few studies in deferred taxes are conducted in Thailand. Toommanon (2007)

investigates the change of tax accounting policies from tax payable method to deferred tax method

during the period of 1995 to 2006. The results indicate that the market does not react positively to a

possible upward in future earnings, which the deferred tax asset causes such an increase. This

means that the market does not perceive deferred tax assets as a signal of future tax saving.

From a practical viewpoint, accounting professional and regulatory bodies agree that

mandating IAS No. 12 enhances the quality and usefulness of financial reporting for users. The body

of income tax research seems to advocate the value relevance of the deferred taxes. Nevertheless,

growing academic literature provide inconclusive support. Under the income statement approach, later

research on the components of deferred taxes, assets, and liabilities, provides mixed results, since the

components are not easily disentangled. Then, the balance sheet approach superseding the income

statement approach appears to provide the transparency of deferred tax components as advocated by

practitioners. Academic works based on the balance sheet method, particularly under the IFRS

environment, are quite limited and provides inconsistent evidence with research under the income

statement approach (Chludek, 2011). To bridge this research gap, our study aims to examine the net

deferred tax balance and the components under the IFRS context. Our data provides a unique way to

additionally investigate the effect of the IFRS early adoption.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

9

Chapter 3 Practices of Early Adoption

Morris (1987) posits that higher quality firms would adopt the best accounting policy to

signal higher quality, which is in line with the signaling theory. Superior performing firms, in particular,

would choose to early adopt an accounting standard advocated by accounting professional bodies to

make their high qualities publicly visible. In other words, firms early adopt a certain accounting

standard because they attempt to communicate their positive prospects resulted from the adoption to

the market. Cassidy, Urbancic, Sylvestre, and Ralston (1993) argue that the reason of early adopting

accounting standard(s) is a beneficial effect on the financial statement, especially the likelihood of an

increase in reported earnings.

Eakin and Gramlich (2000) examine the insider trading and the early adoption of SFAS No.

96 during the period of 1987 to 1988. The pooled regressions suggest that regardless of the

magnitude of the income effect, managers of adopting firms have unfavorable outlooks in their

performances. The finding of partitioned sample demonstrates that managers of firms with large

increasing net income from early adopting SFAS No. 96 signal their positive outlooks by purchasing

their own firms’ stocks. Using 394 firm-years in the Stock Exchange of Thailand during the period of

2004 to 2008, Acaranupong (2010) examines the equity valuation and the voluntary adoption of the

accounting for deferred taxes under the balance sheet approach. The market prices deferred tax

assets and deferred tax liabilities disclosed by early adopters. Surprisingly, the market prices deferred

tax assets for non-adopters. The result should be interpreted with care because of the

operationalization of non-adopters and the small sample size.12 These issues are fairly common in

past accounting research for income taxes (see the discussion of econometric issues in Graham, et

al., 2012 and Holthausen and Watts, 2001).

12 Acaranupong (2010) defines non-adopters as firms that do not adopt the deferred tax policies or use the deferral method. The sample includes 394 firm-years from the SET100, which is relatively small.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

10

Chapter 4 IAS No. 12 and accounting environment

Because our study is performed under the Stock Exchange of Thailand, we are obliged to

provide the background of the IAS No. 12 adoption and relevant contextual information. IAS No. 12 as

in 2009 bound volume was adopted and titled as Thai Accounting Standard No. 12 (TAS No. 12).13

This standard was mandated to be effective by January 1, 2013. The implementation of IAS No. 12 in

Thailand exhibits some distinctive characteristics. First, deferred tax assets can be recognized if it is

probable that the tax benefits can be utilized in the near future. As the restriction of probability for

reversal and the timing of IAS No. 12 adoption, we can disregard the valuation allowance account,

which was a concern in prior studies (e.g., Miller and Skinner, 1998). Second, both deferred tax

assets and deferred tax liabilities are classified as net balance as noncurrent on the balance sheet with

supplemental note disclosure. This presentation requirement of IAS 12 facilitates our research design

to further investigate the effect of loss versus profit firms. Third, a constant effective tax rate in

Thailand during the time period in this study helps us rule out the effect of tax rate changes as

studied by Chen and Schoderbek (2000) and Givolyn and Hayn (1992) that might confound our

results. Last and practically, there is a single tax authority in the country, the Revenue Department,

eliminating any potential effect of multiple jurisdictions, which do not allow for netting the deferred tax

asset and deferred tax liability balances.

13 The Federation of Accounting Profession (FAP), the sole Thai accounting standard setting body, announced the IFRS compliance and adoption phases commencing in 2011. The IAS and IFRS are translated to Thai language and named as Thai Accounting Standard (TAS) and Thai Financial Reporting Standard (TFRS). A set of IAS and IFRS was approved and announced in the Government Gazette on May 26, 2010. The FAP and the SEC aim for full compliance by 2013 for all Thai listed companies. Particularly, listed firms are mandated to adopt Thai Accounting Standard No. 12 Income Taxes (TAS No. 12) by January 1, 2013. TAS No. 12 is directly translated from IAS No. 12 (2009 Bounded Volume). The FAP explicitly encourages listed firms to early adopt the standard. By the end of 2013, all listed companies must report and provide full disclosure of income taxes.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

11

Chapter 5 Data and Methodology

5.1 Data

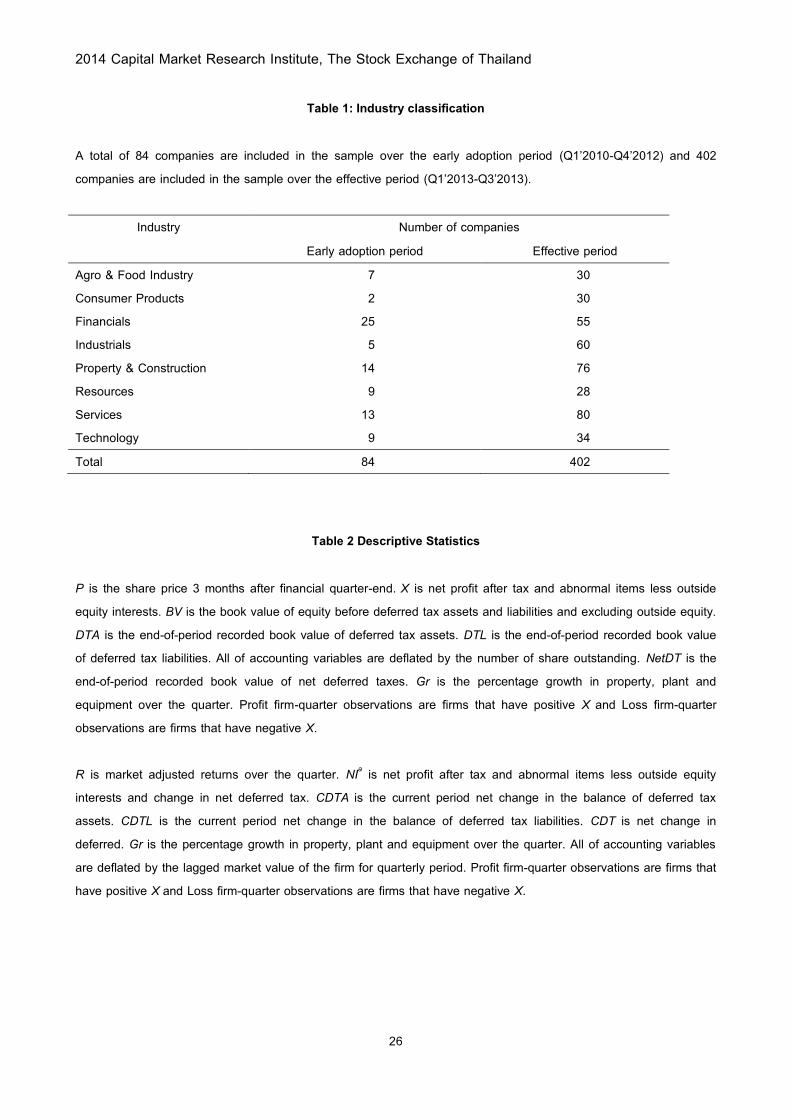

We begin with 534 companies listed in the Stock Exchange of Thailand during the period of

March 2010 to September 2013. We winsorize the data following these criteria. First, 45 property

funds and 19 companies under rehabilitation are excluded. Second, 25 companies are excluded

because the fiscal year does not start at January 1st. Third, 20 companies had no record of deferred

tax asset or deferred tax liability in any of sample quarters. Last, 23 companies are removed due to

substantial incomplete data. The final sample consists of 402 listed companies. The data is

unbalanced panel set of 2,028 firm-quarters. We hand-collect data for profits, book values, assets,

and liabilities from financial statements and notes (Form 56-1) filed at the Securities and Exchange

Commission (SEC). Stock prices are from DataStream.

Table 1 shows the sample classified by the types of industry and the time period of

deferred tax adoption. The data consist of eight sectors, namely the Agro & Food Industry, Consumer

Products, Financials, Industrials, Property & Construction, Resources, Services, and Technology. We

also separate the data into two time period intervals, the early adoption period (Quarter 1, 2010 to

Quarter 4, 2012) and the effective period (Quarter 1, 2013 to Quarter 3, 2013). There are 84

companies over the early adoption period and 402 companies over the effective period, respectively.

More specifically, companies in Financial and Property & Construction sectors are dominant over both

periods and may confound the results. We take these two sectors into consideration as the industry

effect (as presented in regression models in section 5.2.

5.2 Regression Models

We employ both price levels and returns models to validate the market’s response on

deferred taxes. The price levels model presented in equation (1) is based on the Ohlson (1995)

valuation framework that the market value or share price equals the book value adjusted for the

2014 Capital Market Research Institute, The Stock Exchange of Thailand

12

current profitability and other information, including the net deferred tax variable. We start our analysis

on the net deferred taxes account, which TAS No. 12 requires listed firms to classify both deferred tax

assets and deferred tax liabilities as noncurrent net deferred taxes balance on the balance sheets.

This feature is unique and allows us an excellent opportunity to investigate the role of net deferred

taxes on the markets' perception. The price levels model is as follows.

𝑃𝑖𝑡 = 𝛽0 + 𝛽1𝑋𝑖𝑡 + 𝛽2𝐵𝑉𝑖𝑡 + 𝛽3𝑁𝐷𝑇𝑖𝑡 + 𝛽4𝐺𝑟𝑖𝑡 + 𝛽5𝑃𝑅𝑂𝑃𝑖𝑡 + 𝛽6𝐹𝐼𝑁𝑖𝑡 + 𝛽7𝐿𝑂𝑆𝑆𝑖𝑡 + 𝛽8𝐿𝑂𝑆𝑆

× 𝑋𝑖𝑡 + 𝛽9𝐿𝑂𝑆𝑆 × 𝐵𝑉𝑖𝑡 + 𝛽10𝐿𝑂𝑆𝑆 × 𝑁𝐷𝑇𝑖𝑡 + 𝜀𝑖𝑡

(1)

where

𝑃𝑖𝑡 is the share price of company i 3 months after quarterly financial statement end t.

𝑋𝑖𝑡 is the net profit after tax and abnormal items less outside equity interests for

company i during the quarter t.

𝐵𝑉𝑖𝑡 is the book value of equity before deferred tax assets and liabilities and excluding

outside equity for company i at the end of quarter t.

𝑁𝐷𝑇𝑖𝑡 is the end-of-period recorded book value of net deferred taxes for company i by

coding net deferred tax assets as positive numbers and net deferred tax liabilities as

negative numbers. All of accounting variables are deflated by the number of share outstanding.

Control variables:

𝐺𝑟𝑖𝑡 is the percentage growth in property, plant, and equipment for company i at the over

the quarter t.14

𝑃𝑅𝑂𝑃𝑖𝑡 is a dummy variable for companies listed in property & construction industry sector

with a value of 1, otherwise 0.15

14 Chaney and Jeter (1994) show that growth in assets is highly correlated with timing differences on depreciation and leads to increasing DTL. If firm's growth is viewed as a positive signal of expected future cash flows, a positive relation between stock prices and firm's growth variable would be expected.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

13

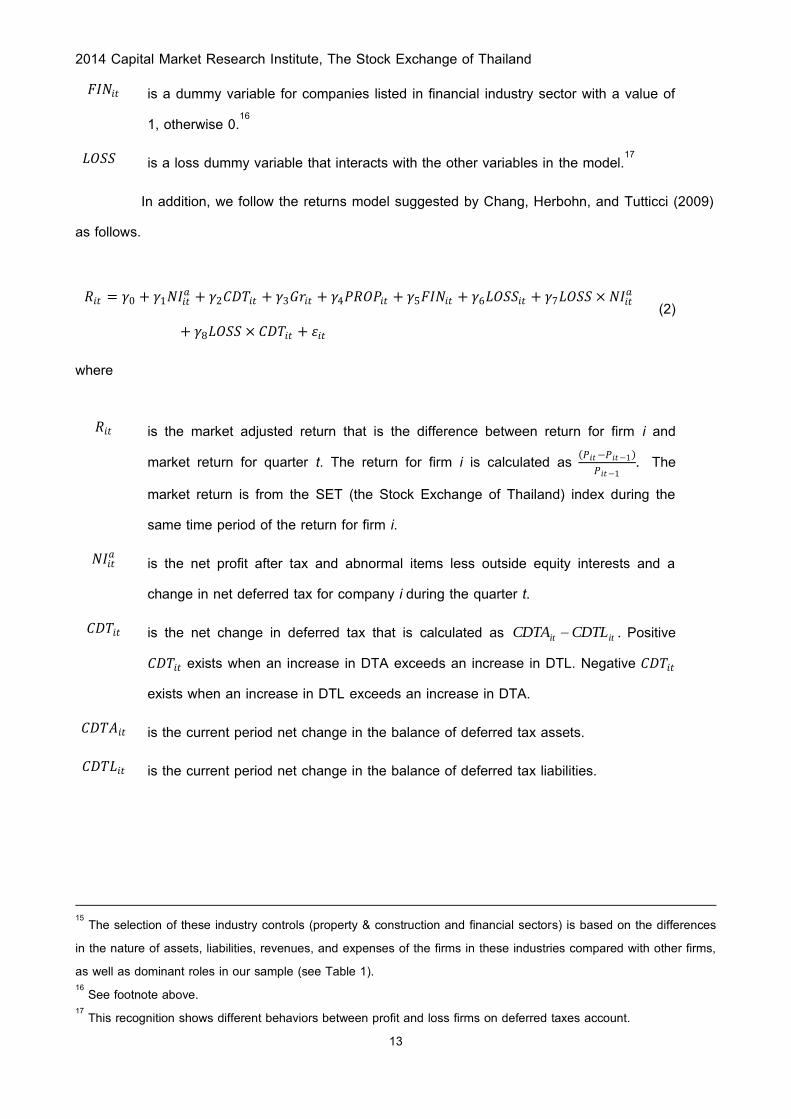

𝐹𝐼𝑁𝑖𝑡 is a dummy variable for companies listed in financial industry sector with a value of

1, otherwise 0.16

𝐿𝑂𝑆𝑆 is a loss dummy variable that interacts with the other variables in the model.17

In addition, we follow the returns model suggested by Chang, Herbohn, and Tutticci (2009)

as follows.

𝑅𝑖𝑡 = 𝛾0 + 𝛾1𝑁𝐼𝑖𝑡

𝑎 + 𝛾2𝐶𝐷𝑇𝑖𝑡 + 𝛾3𝐺𝑟𝑖𝑡 + 𝛾4𝑃𝑅𝑂𝑃𝑖𝑡 + 𝛾5𝐹𝐼𝑁𝑖𝑡 + 𝛾6𝐿𝑂𝑆𝑆𝑖𝑡 + 𝛾7𝐿𝑂𝑆𝑆 × 𝑁𝐼𝑖𝑡𝑎

+ 𝛾8𝐿𝑂𝑆𝑆 × 𝐶𝐷𝑇𝑖𝑡 + 𝜀𝑖𝑡

(2)

where

𝑅𝑖𝑡 is the market adjusted return that is the difference between return for firm i and

market return for quarter t. The return for firm i is calculated as 𝑃𝑖𝑡−𝑃𝑖𝑡−1

𝑃𝑖𝑡−1. The

market return is from the SET (the Stock Exchange of Thailand) index during the

same time period of the return for firm i.

𝑁𝐼𝑖𝑡𝑎 is the net profit after tax and abnormal items less outside equity interests and a

change in net deferred tax for company i during the quarter t.

𝐶𝐷𝑇𝑖𝑡 is the net change in deferred tax that is calculated as itit CDTLCDTA . Positive

𝐶𝐷𝑇𝑖𝑡 exists when an increase in DTA exceeds an increase in DTL. Negative 𝐶𝐷𝑇𝑖𝑡

exists when an increase in DTL exceeds an increase in DTA.

𝐶𝐷𝑇𝐴𝑖𝑡 is the current period net change in the balance of deferred tax assets.

𝐶𝐷𝑇𝐿𝑖𝑡 is the current period net change in the balance of deferred tax liabilities.

15 The selection of these industry controls (property & construction and financial sectors) is based on the differences in the nature of assets, liabilities, revenues, and expenses of the firms in these industries compared with other firms, as well as dominant roles in our sample (see Table 1). 16 See footnote above. 17 This recognition shows different behaviors between profit and loss firms on deferred taxes account.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

14

Note that the control variables for growth, industry, and loss in the returns model are

identical to the price levels model. All accounting variables are deflated by the lagged market value of

the firm for quarterly period.

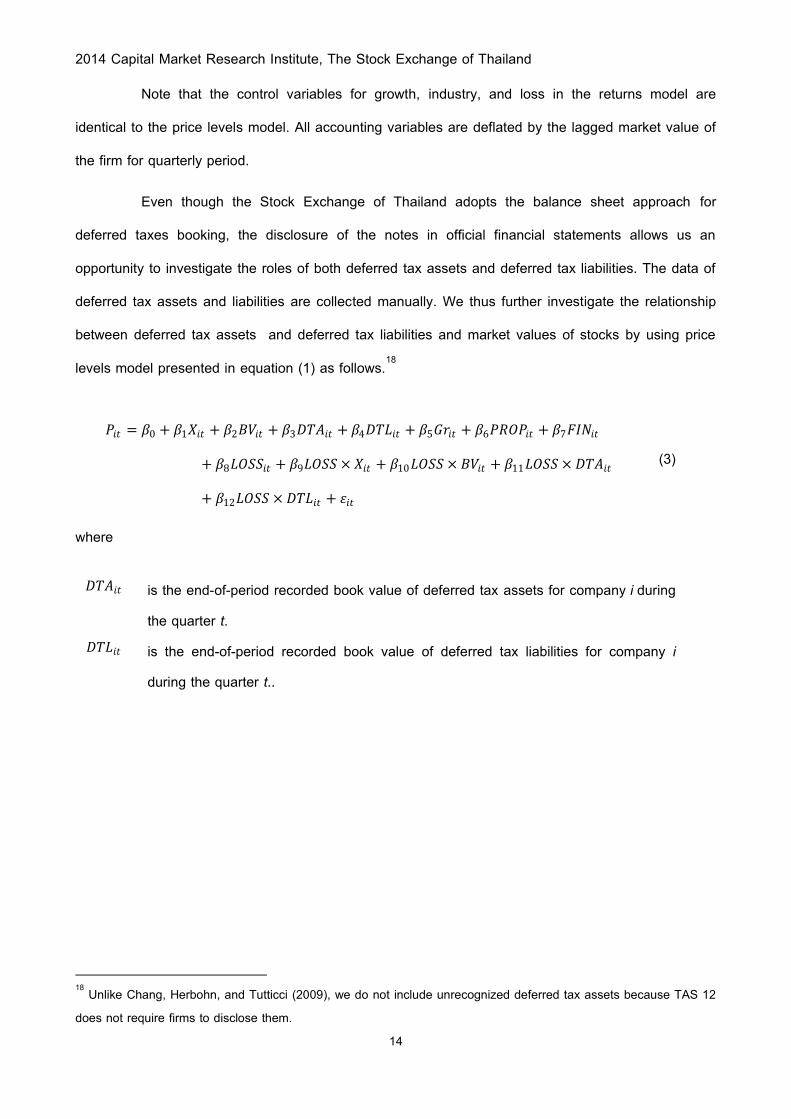

Even though the Stock Exchange of Thailand adopts the balance sheet approach for

deferred taxes booking, the disclosure of the notes in official financial statements allows us an

opportunity to investigate the roles of both deferred tax assets and deferred tax liabilities. The data of

deferred tax assets and liabilities are collected manually. We thus further investigate the relationship

between deferred tax assets and deferred tax liabilities and market values of stocks by using price

levels model presented in equation (1) as follows.18

𝑃𝑖𝑡 = 𝛽0 + 𝛽1𝑋𝑖𝑡 + 𝛽2𝐵𝑉𝑖𝑡 + 𝛽3𝐷𝑇𝐴𝑖𝑡 + 𝛽4𝐷𝑇𝐿𝑖𝑡 + 𝛽5𝐺𝑟𝑖𝑡 + 𝛽6𝑃𝑅𝑂𝑃𝑖𝑡 + 𝛽7𝐹𝐼𝑁𝑖𝑡

+ 𝛽8𝐿𝑂𝑆𝑆𝑖𝑡 + 𝛽9𝐿𝑂𝑆𝑆 × 𝑋𝑖𝑡 + 𝛽10𝐿𝑂𝑆𝑆× 𝐵𝑉𝑖𝑡 + 𝛽11𝐿𝑂𝑆𝑆 × 𝐷𝑇𝐴𝑖𝑡

+ 𝛽12𝐿𝑂𝑆𝑆 × 𝐷𝑇𝐿𝑖𝑡 + 𝜀𝑖𝑡

(3)

where

𝐷𝑇𝐴𝑖𝑡 is the end-of-period recorded book value of deferred tax assets for company i during

the quarter t. 𝐷𝑇𝐿𝑖𝑡 is the end-of-period recorded book value of deferred tax liabilities for company i

during the quarter t..

18 Unlike Chang, Herbohn, and Tutticci (2009), we do not include unrecognized deferred tax assets because TAS 12 does not require firms to disclose them.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

15

Chapter 6 Empirical Results

6.1 Descriptive statistics

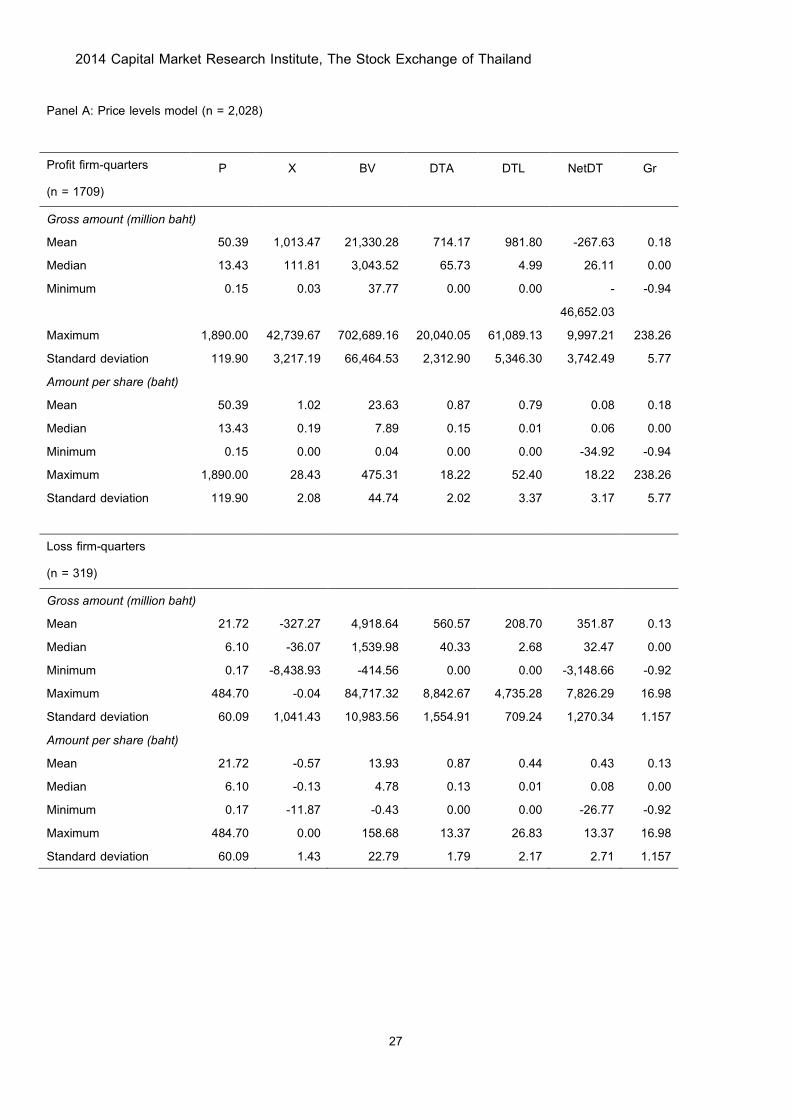

Table 2 presents the summary statistics of key variables for quarterly samples data. We

categorize data into profit and loss firms. This confirms fundamental differences between profit and

loss firms. Panel A presents the summary statistics in terms of gross amount and amount per share

for the 2,028 firm-quarter in the price levels model, which separates into the 1,709 profit firm-quarter

and the 319 loss firm-quarter.19 The stock price, profit, book value, and deferred taxed assets and

deferred tax liabilities are, on average, higher for profit firms than loss firms. The average growth in

property, plant, and equipment is not much difference for profit firms (18%) and loss firms (13%). The

mean deferred tax liabilities of 981.80 million baht are higher than the mean deferred tax asset of

714.17 million baht. This indicates income-decreasing manipulation for tax benefit by recording more

deferred tax liabilities (Chaney and Jeter, 1994). Loss firms show that the mean deferred tax assets of

560.57 million baht are higher than the mean deferred tax liabilities of 208.70 million baht. This

indicates the manipulation on reported increasing earnings by recording more deferred tax assets

(Chaney and Jeter, 1994). The means net deferred tax assets/liabilities per share have positive sign

for both profit and loss firms at 0.08 and 0.43, respectively, which indicates that more firms have net

deferred tax assets rather than net deferred tax liabilities.

Panel B of Table 2 presents the summary statistics in terms of gross amount and amount

per share for the 2,019 firm-quarter in the returns model, which separates into the 1,701 profit firm-

quarter and the 318 loss firm-quarter. The reduction in the samples of returns model is due to missing

data for calculating lagged market values. The average return for profit firm is 2% and loss firm is - 19 Profit firm-quarter observations are firms that have positive net profit after tax and abnormal items less outside equity interest (positive X) during the quarter t. Loss firm-quarter observations are firms that have negative net profit after tax and abnormal items less outside equity interest (negative X) during the quarter t.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

16

3%. The average net amount of deferred tax recognized each quarter (CDT) is small with the median

level around zero and presents in positive value for both profit firms (0.84) and loss firm (1.44). It

means that an increase in deferred tax assets (CDTA) is larger than increase in deferred tax liabilities

(CDTL).

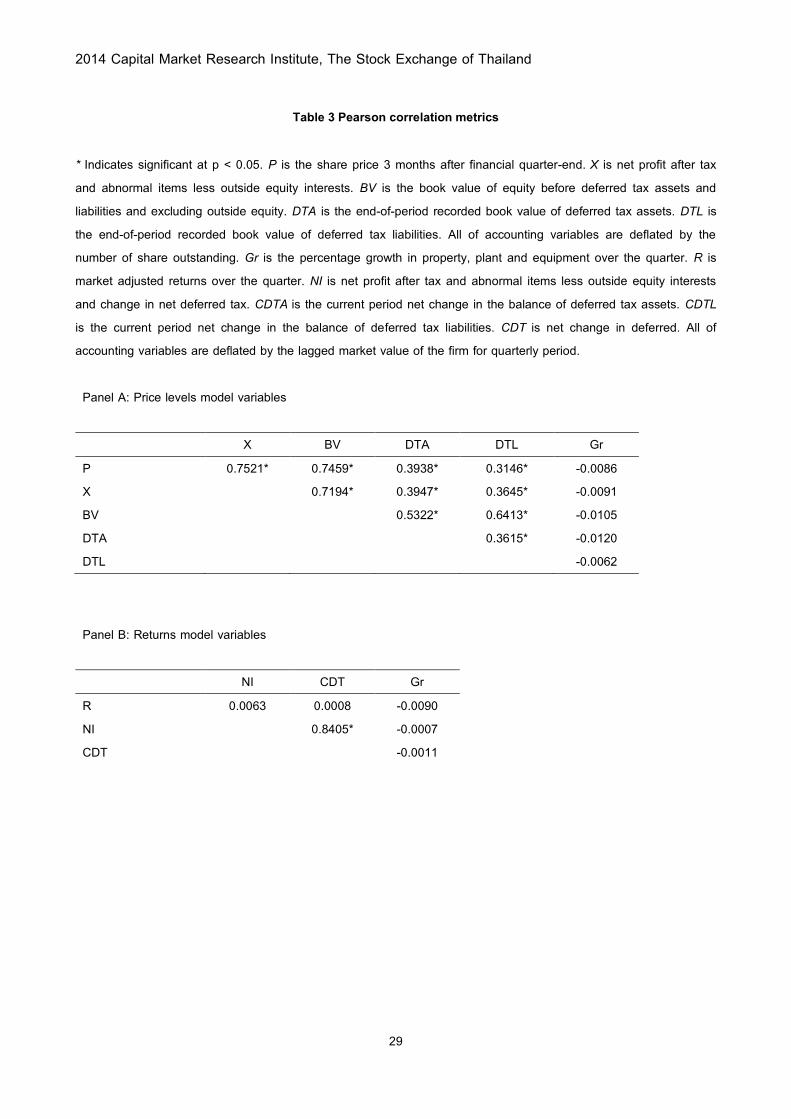

Panels A and B of Table 3 report the Pearson correlation coefficients between variables

used in price levels and returns models, respectively. For the price levels model, the variables

including profit, book value, deferred tax assets, and deferred tax liabilities are correlated significantly

as expected. For the returns model, CDT correlates with NI (0.8405), implying that firms in general are

able to generate sufficient profit in the future to offset net deferred tax assets. The correlation

coefficients for price levels model and returns model suggests that the multicollinearity is not a

concern.

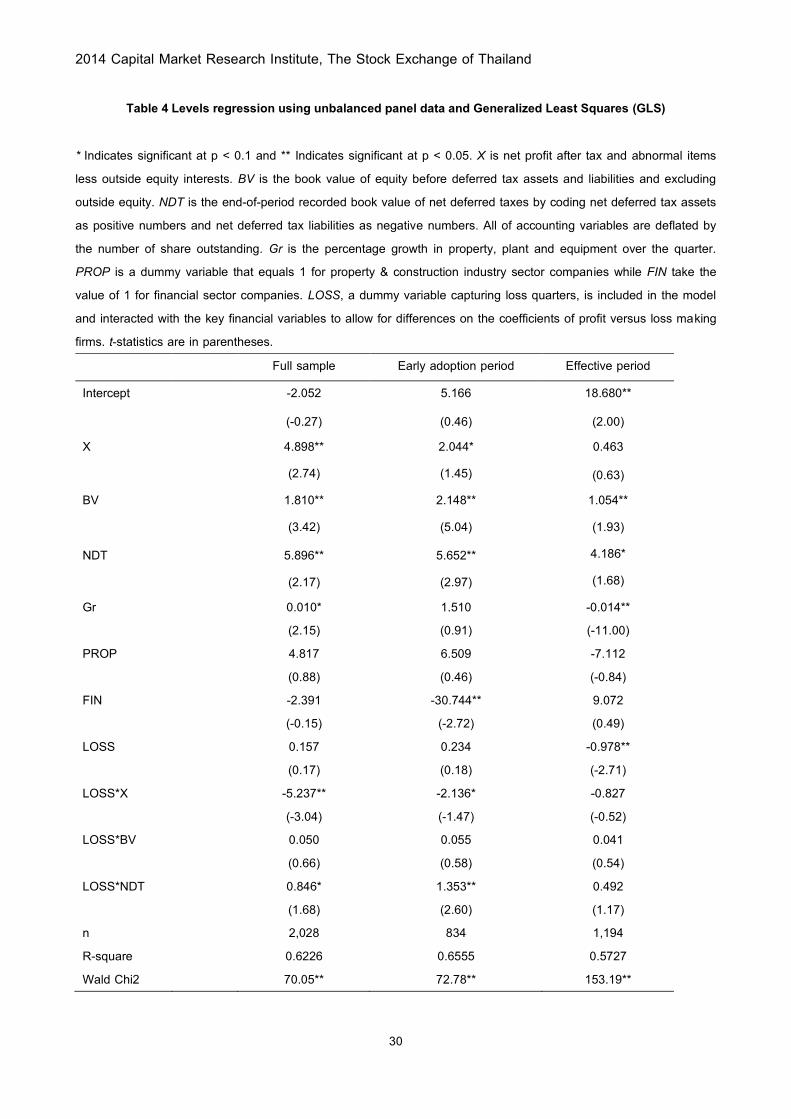

6.2 Net deferred tax assets and net deferred tax liabilities

In these two following sections we investigate the role of the net effect of deferred taxes.

We argue that investors utilize and analyze financial information from the entire balance sheet and

TAS No. 12 requires to disclose as noncurrent net deferred tax on the balance sheet. Thus one-side

of deferred taxes is not an appropriate measure to show the relation between deferred taxes and the

perception of the market. Table 4 shows the results of the price levels model in net deferred tax

account. Our levels model incorporates random effects with White’s (1980) robust standard errors and

covariance to control heteroscedasticity problem and uses Swamy and Arora (1972) estimate of

component variances, which is suitable for unbalanced panel data and small sample (Baltagi and

Chang, 1994). Our techniques employed in this study are superior to most prior studies, which takes

issues of unbalanced data, small samples size, heteroscedasticity, and serial correlation arising from

the samples data into consideration. The regression result for the full sample is in the first column. We

re-run the regressions separately for early adoption period (Quarter 1, 2010 - Quarter 4, 2012) in the

second column and effective period (Quarter 1, 2013 - Quarter 3, 2013) in the last column. For profit-

reporting firms, importantly, the coefficients on net deferred tax (NDT) are positive and statistically

significant in all periods, indicating that the market perceives net deferred tax assets as future tax

saving and net deferred tax liabilities as future tax payment. This finding is consistent with Amir et al.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

17

(1997). Moreover, the results show that earnings (X) and book value (BV) are positively associated

with stock price and statistically significant, promising the efficacy of the Ohlson's (1995) model and

being consistent with previous findings.20 It is worth to note that the financial industry plays an

important role only during early adoption period.

It is logical to document that markets expect the persistence in future positive

performance, but it is not true for negative performance (Hayn, 1995). Thus, the impact of net profit

firms is greater than that of net loss firms. The coefficient of profit firms should be greater than one

and statistically significant, while that of loss firms should not be statistically significant. To take this

issue into consideration, we investigate the interactive roles of profit and loss firms on other

accounting variables in our models. The interaction between earnings and a loss dummy variable

shows when firms are not able to generate profits, the reduction in earnings coefficient is noticeable

(Chang, Herbohn, and Tutticci, 2009). This is confirmed by the reduction in coefficients of the

interaction terms.21 This could be interpreted that an increase in earnings of loss-reporting firms

causes a decrease in stock prices by 0.339 and 0.092 over the full sample and early adoption

periods, respectively.22 This is also logical to say that markets react negatively to poor performing

firms, causing the reduction in stock prices. The same phenomenon appears in book values, though it

is not negative and not significant. Our prime interest is the sign of the net deferred taxes on loss-

reporting firms, which are the same as those of on profit-reporting firms, meaning that markets are

likely to perceive the benefit of less negative net deferred taxes. Due to the same positive signs of

these two variables, the magnitude effect of deferred tax on loss making firms is amplified, showing

that investors expect that loss-reporting firms can use the benefit of the future tax saving from loss

carryforwards in the near future, otherwise overoptimistic. We conclude that investors do understand

the role of net positive deferred taxes in saving future cash of companies. The evidence during early

20 With the exception of the insignificance of earnings during effective period. A potential reason is a small sample size. 21 The coefficients of earnings (the interaction between a loss dummy varible and earnings) in full sample, early adoption, and effective periods are 4.898 (-5.237), 2.044 (-2.136), and 0.463 (-0.827), respectively. 22 The magnitude effect of an interaction term (dummy and main accounting variables) is the summation between the coefficient of the interaction term and its respective main accounting variable

2014 Capital Market Research Institute, The Stock Exchange of Thailand

18

adoption period is stronger than the other sample periods, implying that deferred taxes account is

value relevant and signals important information to the market.

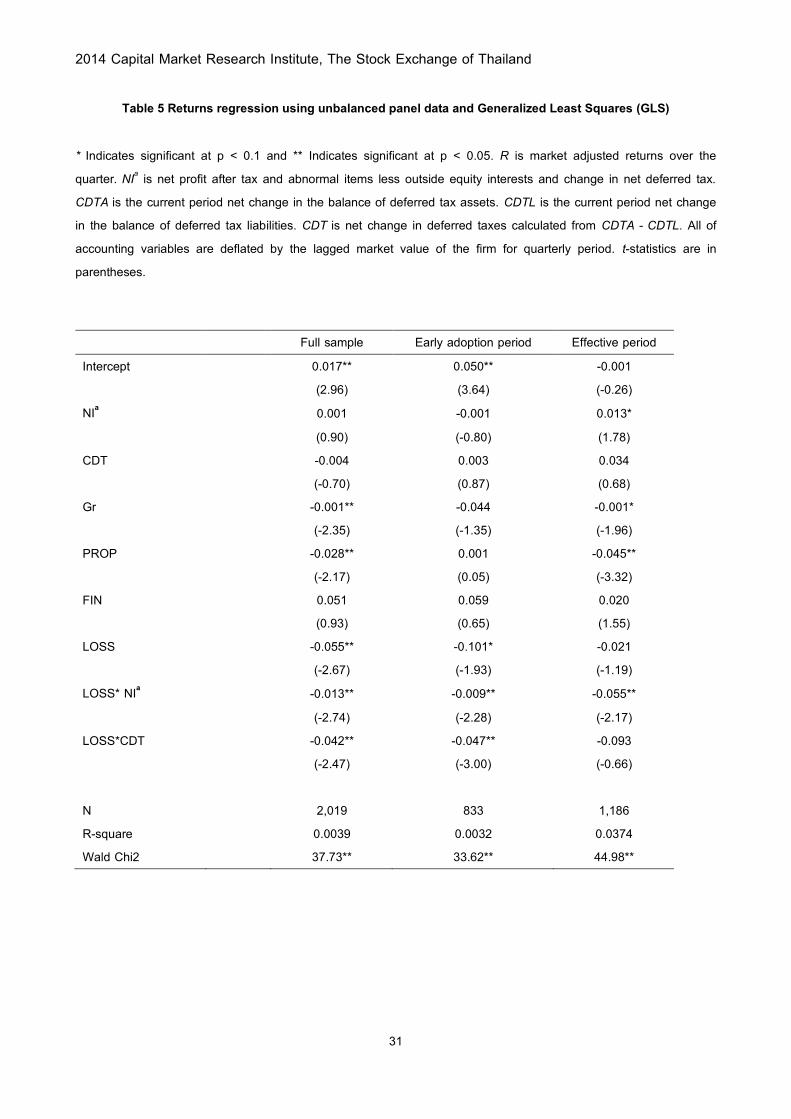

6.3 Net current tax deferrals

We further analyze the net change of current period deferred tax (CDT) accruals by using

the returns model as presented in equation (2).23 The most striking and surprising result is the

insignificance of the CDT for profit firms in all periods studied. However, it is not true for loss-

reporting firms. They do play more important roles in this experiment. Net increase in DTA is inversely

related to the return. To gain further insight, the two sub-period models are executed. Our early

adoption model highlights the effect of early adoption on the market's response. The interaction

between LOSS and CDT is significant (-0.047). This can be interpreted that the increase in CDT is

viewed as future tax payment for loss-reporting early adopter firms. We obtain the explanation from

the notes to financial statements of loss firms and find that the major component of deferred tax

assets is loss carryforwards. The increase in net change of deferred taxes therefore conveys the

lower probability of reversing loss carryforwards to the market. Market interprets the larger net change

of DTA relative to the change of DTL as the persistent loss and the questionable reversal of loss

carryforwards.

Taken together, the findings suggest the asymmetric market responses to deferred taxes

reported under IAS No. 12. In the big picture, the market seems to weight DTL as liabilities, but does

not price DTA. Interestingly, the information content of NDT is confirmed in our study. The market

prices net deferred taxes as required by IAS No. 12. The net change in deferred taxes for the early

adopters is negatively associated with the market price. Our statistical analyses illuminate the effect of

early adoption in the accounting for income taxes literature. Early adoption of IAS No. 12 plays a

significant role in signaling the components of deferred taxes to the market. Among early adopters,

the DTA of loss-reporting financial firms is priced positively. In contrast, the DTL of loss-reporting

mandatory adopters is viewed as future tax liabilities.

23

The results of price levels model is available upon request.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

19

6.4 Deferred tax assets and deferred tax liabilities

Our full sample shows that earnings (X) and book value (BV) are positively associated with

stock price and statistically significant for profit firms, while the interaction of earnings and loss dummy

(LOSS*X) shows that the coefficient on earnings decrease when firm makes a loss that consistent

with expectations. Growth in property, plant and equipment is positively significant with a coefficient of

0.008 (p < 0.05).

Focusing on the full sample, the coefficient on DTA for profit firms is not statistically

significant, meaning that the market does not view DTA as future tax benefits (e.g., Amir et al., 1997;

Toommanon, 2007; and Chludek, 2011). Possible explanations are the uncertain cash flow

implications and reversal of deferred tax asset components including post-retirement benefit liabilities,

depreciation, and amortization. For the loss firms in early adoption period, the coefficient on deferred

tax assets (LOSS*DTA) is positive and statistically significant (2.503), which is consistent with Amir

and Sougiannis (1999) and Chang et al. (2009). The market perceives the DTA reported by loss firms

early adopting IAS No. 12 would reverse and save future cash flow for the firms. Contrarily, for the

firms adopting IAS No. 12 as mandated, the market does not perceive DTA as assets but views DTL

as liabilities. We conclude that only loss firms with early adopting IAS No. 12 successfully signal the

market about their potential future tax savings. Since the coefficient of FIN during early adoption

period is large and significantly negative (-26.696), this provides an opportunity to further investigate

financial industry as a control variable in the early adoption period by comparing with the other

industries in later analysis.24 The DTL is viewed as future tax liabilities as the coefficients of DTL in

the full sample (-8.217), early adoption (-9.864), and effective period (-4.246) are negative and

significant as presented in Table 6. This suggests that the market discounts DTL when pricing the

security (Ayers, 1998; Tse and Holtzman, 1995). The DTL reported by loss-reporting mandatory

adopters is viewed as liabilities as the coefficient of LOSS*DTL is negative and significant (-0.991),

while DTL reported by the early adopters that also report loss is not value relevant. Confirming the

industry effect, the coefficient of DTL in Table 6 suggests the market discount the price of early

24 Though property & construction sector are dominant in our analyses, it does not play an important role in the regression models.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

20

adopters in other sectors. Taken together, the market responds to the DTL because the components

of DTL are expected to reverse in the short run.

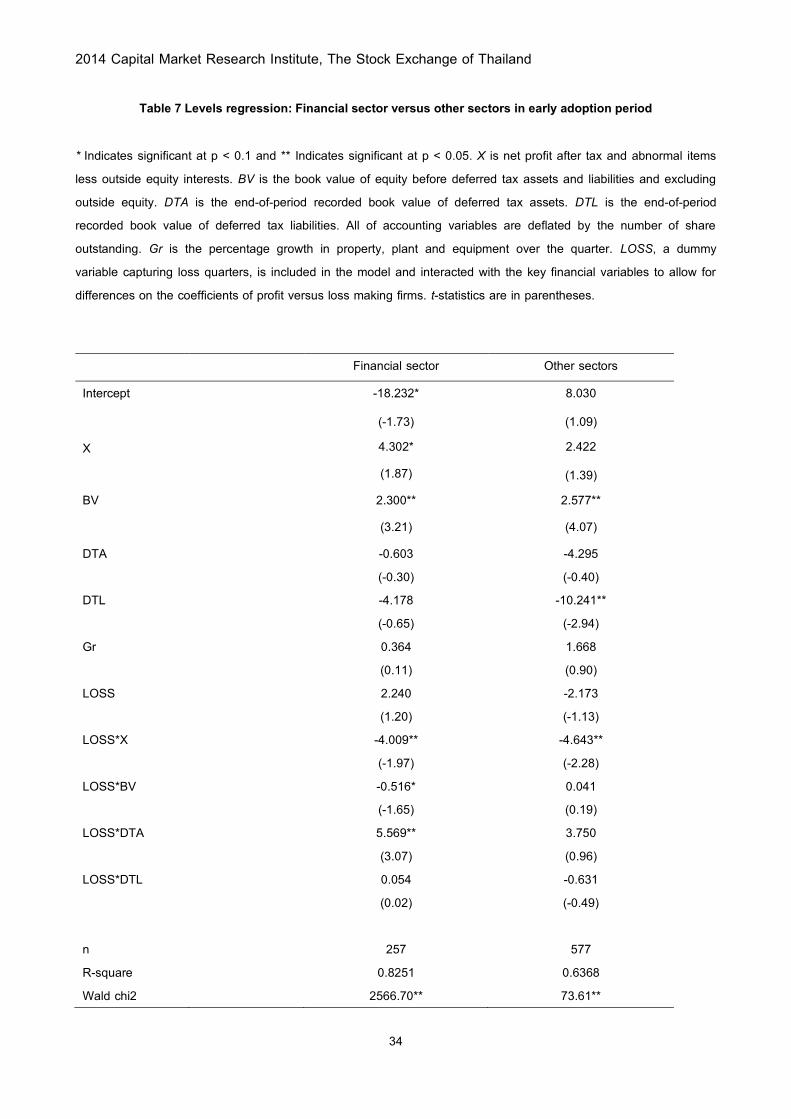

6.5 Evidence in financial sector during early adoption period

The results in Table 7 show that the coefficient of LOSS*DTA of the financial firms is large,

positive, and statistically significant (5.569). While the coefficient of LOSS*DTA of the other sectors is

positive but not significant (3.750), the DTL is negative and significant (-10.241). Thus, the market

values only DTA reported by loss firms in financial industry during early adoption period but not DTA

reported by early adopters in the other sectors. This market's response may be attributed to that the

main components of deferred tax assets for loss firms in financial sector are from provision of doubtful

debt and outstanding claim reserve. For insurance companies, outstanding claim reserve represents

estimate of ultimate obligations in respect of actual claim or known incidents expected to give rise to

claims. This reserve is expected to reverse as tax expense when actual claim happens. Alternatively,

Skinner (2008) reports that bank management in Japan uses DTA to manage reported levels of

regulatory capital to avoid falling below the minimum capital thresholds. Therefore, it indicates that

market perceives deferred tax assets from these components as future tax saving.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

21

Chapter 7 Conclusion, Limitation, and Future Research

This study examines how the market perceives the relevance of deferred tax assets and

liabilities reported by companies listed on the Stock Exchange of Thailand under IAS No. 12 and

whether current period tax deferrals have any value relevance. Our analysis uses the price levels and

returns models. The levels model of full sample suggests that the market does not perceive future

benefits from deferred tax assets. Nonetheless, our further investigation reveals intriguing

observations that the loss-reporting early adopters effectively convey the future tax saving to the

market. The market views deferred tax assets of loss firms in financial industry as assets because the

main components of deferred tax assets are provision of doubtful debt and outstanding claim reserve

that are expected to reverse in the short run. For deferred taxed liabilities, the market views as future

tax payment because main components of deferred taxed liabilities are from unrealized gain on

available-for-sale financial assets and revaluation surplus on assets that investors expect to reverse

as taxable income in the short run. For the offsetting balance, market perceives net deferred tax

assets as future tax saving and net deferred tax liabilities as deferred tax payment. This may indicate

that net deferred tax assets provide more value relevance to investors than separate deferred tax

assets. This confirms that the net balance disclosure requirement under IAS No. 12 is warranted.

The returns model centralizes on the market perception of net current tax deferrals. We do

not find enough support for the relation between net current tax deferrals and returns for profit firms.

Specifically to the case of loss firms, the net current tax deferrals are negatively correlated with

returns. Investors interpret the larger increasing deferred tax assets over the increasing deferred tax

liabilities as a signal of higher future losses and the less likely reversal of loss carryforwards.

In conclusion, our results suggest that the market perception of deferred tax assets and

liabilities under the balance sheet method depend on the deferred tax accounts, the adoption period,

as well as the likelihood of reversal. The timing of deferred tax balance reversal and cash flow

2014 Capital Market Research Institute, The Stock Exchange of Thailand

22

implications are differentially perceived depending on the characteristics of deferred tax components

and the financial performance.

We acknowledge that small sample size may compromise our statistical power. We address

this issue by using quarterly data and panel regression models. Subsequent research may expand the

time interval to detect the changes in the deferred taxes and market perception.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

23

References

Amir, E., M. Kirschenheiter, and K. Willard (1997), “The valuation of deferred taxes”, Contemporary

Accounting Research 14, 597–622.

Amir, E., and T. Sougiannis (1999), “Analysts’ interpretation and investors’ valuation of tax

carryforwards”, Contemporary Accounting Research 16, 1–33.

Ayres, B. C. (1998), “Deferred tax accounting under SFAS, 109: An empirical investigation of its

incremental value-relevance relative to APB No.11”, Accounting Review 73, 195–212.

Baltagi, B. H., and Y.-J. Chang. 1994. Incomplete panels: A comparative study of alternative estimators

for the unbalanced one-way error component regression model. Journal of Econometrics 62: 67–89.

Cassidy, J., F. R. Urbancic, J. Sylvestre, and F. Ralston (2011), “Accounting for income taxes: A study of

early vs. postponed adoption decisions for controversial accounting standards”, Journal of Applied Business

Research 9, 52-57

Chaney, P. K., and D. C. Jeter (1994), “The effect of deferred taxes on security prices”, Journal of

Accounting, Auditing and Finance 9, 91–116.

Chandra, U. and B. T. Ro (1997), “The association between deferred taxes and common stock risk”,

Journal of Accounting and Public Policy 16, 311-333.

Chang, C., K. Herbohn and I. Tutticci (2009), “Market's perception of deferred tax accruals”, Accounting

and Finance 49, 645-643.

Chludek, A. K. (2011), “Perceived versus actual cash flow implications of deferred taxes—An analysis of

value relevance and reversal under IFRS”, Journal of International Accounting Research 10(1), 1-25.

Dhaliwal, D., R. Trezevant, and M. Wilkins (2000), “Tests of deferred tax explanation of the negative

association between the LIFO reserve and firm value”, Contemporary Accounting Research 17, 41-59.

Eakin, C. F. and J. D. Gramlich (2000), “Insider trading and the early adoption of SFAS 96: A test of the

signaling hypothesis”, Advances in Accounting 17, 111-133.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

24

Graham, J. R., J. S. Raedy, and D. A. Shackelford (2012), “Research in accounting for income taxes”,

Journal of Accounting and Economics 53, 412-434.

Guenther, D. and R. Sansing (2004), “The valuation relevance of reversing deferred tax liabilities”, The

Accounting Review 79, 437-451.

Federation of Accounting Professions (2009), “Draft Thai accounting standard No.56 Income Taxes”,

http://www.fap.or.th

Federation of Accounting Professions (2010), “Thai accounting standard No.12 Income Taxes”,

http://www.fap.or.th

Givoly, D. and C. Hayn (1992), “The valuation of the deferred tax liability: Evidence from the stock

market”, The Accounting Review 67, 394-410.

Graham, J. R., J. S. Raedy, and D. A. Shackelford (2012), “Research in accounting for income taxes”,

Journal of Accounting and Economics 53, 412-434.

Holthausen, R. and R. Watts (2001). “The relevance of value-relevance literature for financial accounting

standard setting”, Journal of Accounting and Economics 31, 3-75.

International Accounting Standards Board (2009), “International accounting standard No.12 Income

Taxes”, http://www.ifrs.org

Lev, B. and D. Nissim (2004), “Taxable income, future earnings, and equity values”, The Accounting

Review 79(4), 1039-1074.

Miller, G. S. and D. J. Skinner (1998), “Determinants of the valuation allowance for deferred tax assets

under SFAS No.109”, The Accounting Review 73, 213-233

Ohlson, J. (1995), “Earnings, book values and dividends in security valuation”, Contemporary Accounting

Research 11, 661–687.

Porteba, J., N. Rao, and J. Seidman (2011) “Deferred tax positions and incentives for corporate

behavior around corporate tax changes”, National Tax Journal 64(1), 27-58.

Sansing, R. (1998) “The deferred tax liability”, Journal of Accounting Research 36, 357-363.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

25

Skinner, D. J. (2008) “The rise of deferred tax assets in Japan: The role of deferred tax accounting in

the Japanese banking crisis”, Journal of Accounting and Economics 46, 218-239.

Swamy, P. A. V. B. and S. S. Arora (1972), “The exact finite sample properties of estimators of

coefficients in the error components regression models”, Econometrica, Vol. 40, pp. 253-260.

Tse, S. and M. Holtzman (1995), “The cross-sectional valuation of deferred income taxes: Effects of

industry-specific tax policies”, Working paper, University of Texas at Austin.

Tummanon, V. (2007), “The effects of the adoption of deferred taxes accounting policy during B.E. 2538-

2549”, Journal of Accounting Professions 7, 27-47

White, H. (1980), A heteroskedasticity-consistent covariance matrix estimator and a direct test for

heteroskedasticity", Econometrica 48 (4): 817–838.

Zeng, T. (2003), “The valuation of loss carryforwards”, Canadian Journal of Administrative Sciences 20,

166–176.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

26

Table 1: Industry classification

A total of 84 companies are included in the sample over the early adoption period (Q1’2010-Q4’2012) and 402 companies are included in the sample over the effective period (Q1’2013-Q3’2013).

Industry Number of companies Early adoption period Effective period

Agro & Food Industry 7 30 Consumer Products 2 30 Financials 25 55 Industrials 5 60 Property & Construction 14 76 Resources 9 28 Services 13 80 Technology 9 34 Total 84 402

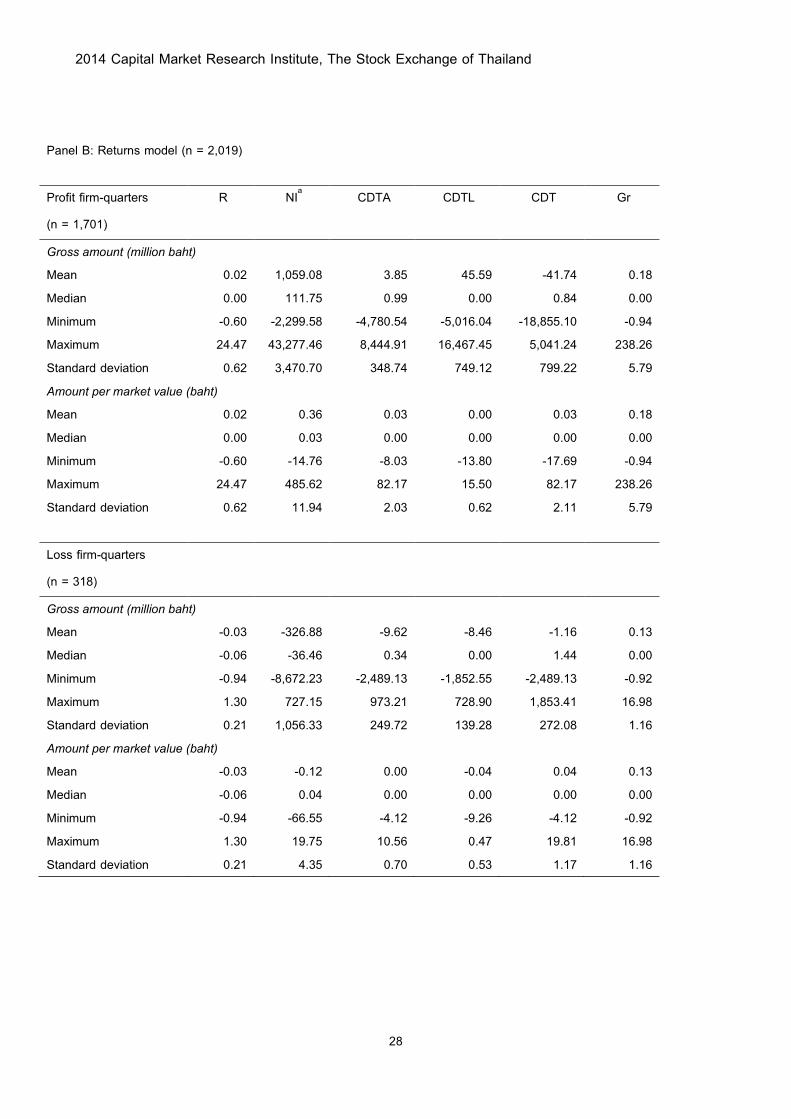

Table 2 Descriptive Statistics P is the share price 3 months after financial quarter-end. X is net profit after tax and abnormal items less outside equity interests. BV is the book value of equity before deferred tax assets and liabilities and excluding outside equity. DTA is the end-of-period recorded book value of deferred tax assets. DTL is the end-of-period recorded book value of deferred tax liabilities. All of accounting variables are deflated by the number of share outstanding. NetDT is the end-of-period recorded book value of net deferred taxes. Gr is the percentage growth in property, plant and equipment over the quarter. Profit firm-quarter observations are firms that have positive X and Loss firm-quarter observations are firms that have negative X. R is market adjusted returns over the quarter. NIa is net profit after tax and abnormal items less outside equity interests and change in net deferred tax. CDTA is the current period net change in the balance of deferred tax assets. CDTL is the current period net change in the balance of deferred tax liabilities. CDT is net change in deferred. Gr is the percentage growth in property, plant and equipment over the quarter. All of accounting variables are deflated by the lagged market value of the firm for quarterly period. Profit firm-quarter observations are firms that have positive X and Loss firm-quarter observations are firms that have negative X.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

27

Panel A: Price levels model (n = 2,028)

Profit firm-quarters

(n = 1709) P X BV DTA DTL NetDT Gr

Gross amount (million baht) Mean 50.39 1,013.47 21,330.28 714.17 981.80 -267.63 0.18 Median 13.43 111.81 3,043.52 65.73 4.99 26.11 0.00 Minimum 0.15 0.03 37.77 0.00 0.00 -

46,652.03 -0.94

Maximum 1,890.00 42,739.67 702,689.16 20,040.05 61,089.13 9,997.21 238.26 Standard deviation 119.90 3,217.19 66,464.53 2,312.90 5,346.30 3,742.49 5.77 Amount per share (baht) Mean 50.39 1.02 23.63 0.87 0.79 0.08 0.18 Median 13.43 0.19 7.89 0.15 0.01 0.06 0.00 Minimum 0.15 0.00 0.04 0.00 0.00 -34.92 -0.94 Maximum 1,890.00 28.43 475.31 18.22 52.40 18.22 238.26 Standard deviation 119.90 2.08 44.74 2.02 3.37 3.17 5.77

Loss firm-quarters

(n = 319)

Gross amount (million baht) Mean 21.72 -327.27 4,918.64 560.57 208.70 351.87 0.13 Median 6.10 -36.07 1,539.98 40.33 2.68 32.47 0.00 Minimum 0.17 -8,438.93 -414.56 0.00 0.00 -3,148.66 -0.92 Maximum 484.70 -0.04 84,717.32 8,842.67 4,735.28 7,826.29 16.98 Standard deviation 60.09 1,041.43 10,983.56 1,554.91 709.24 1,270.34 1.157 Amount per share (baht) Mean 21.72 -0.57 13.93 0.87 0.44 0.43 0.13 Median 6.10 -0.13 4.78 0.13 0.01 0.08 0.00 Minimum 0.17 -11.87 -0.43 0.00 0.00 -26.77 -0.92 Maximum 484.70 0.00 158.68 13.37 26.83 13.37 16.98 Standard deviation 60.09 1.43 22.79 1.79 2.17 2.71 1.157

2014 Capital Market Research Institute, The Stock Exchange of Thailand

28

Panel B: Returns model (n = 2,019) Profit firm-quarters

(n = 1,701)

R NIa CDTA CDTL CDT Gr

Gross amount (million baht) Mean 0.02 1,059.08 3.85 45.59 -41.74 0.18 Median 0.00 111.75 0.99 0.00 0.84 0.00 Minimum -0.60 -2,299.58 -4,780.54 -5,016.04 -18,855.10 -0.94 Maximum 24.47 43,277.46 8,444.91 16,467.45 5,041.24 238.26 Standard deviation 0.62 3,470.70 348.74 749.12 799.22 5.79 Amount per market value (baht) Mean 0.02 0.36 0.03 0.00 0.03 0.18 Median 0.00 0.03 0.00 0.00 0.00 0.00 Minimum -0.60 -14.76 -8.03 -13.80 -17.69 -0.94 Maximum 24.47 485.62 82.17 15.50 82.17 238.26 Standard deviation 0.62 11.94 2.03 0.62 2.11 5.79

Loss firm-quarters

(n = 318)

Gross amount (million baht) Mean -0.03 -326.88 -9.62 -8.46 -1.16 0.13 Median -0.06 -36.46 0.34 0.00 1.44 0.00 Minimum -0.94 -8,672.23 -2,489.13 -1,852.55 -2,489.13 -0.92 Maximum 1.30 727.15 973.21 728.90 1,853.41 16.98 Standard deviation 0.21 1,056.33 249.72 139.28 272.08 1.16 Amount per market value (baht) Mean -0.03 -0.12 0.00 -0.04 0.04 0.13 Median -0.06 0.04 0.00 0.00 0.00 0.00 Minimum -0.94 -66.55 -4.12 -9.26 -4.12 -0.92 Maximum 1.30 19.75 10.56 0.47 19.81 16.98 Standard deviation 0.21 4.35 0.70 0.53 1.17 1.16

2014 Capital Market Research Institute, The Stock Exchange of Thailand

29

Table 3 Pearson correlation metrics

* Indicates significant at p < 0.05. P is the share price 3 months after financial quarter-end. X is net profit after tax and abnormal items less outside equity interests. BV is the book value of equity before deferred tax assets and liabilities and excluding outside equity. DTA is the end-of-period recorded book value of deferred tax assets. DTL is the end-of-period recorded book value of deferred tax liabilities. All of accounting variables are deflated by the number of share outstanding. Gr is the percentage growth in property, plant and equipment over the quarter. R is market adjusted returns over the quarter. NI is net profit after tax and abnormal items less outside equity interests and change in net deferred tax. CDTA is the current period net change in the balance of deferred tax assets. CDTL is the current period net change in the balance of deferred tax liabilities. CDT is net change in deferred. All of accounting variables are deflated by the lagged market value of the firm for quarterly period. Panel A: Price levels model variables X BV DTA DTL Gr P 0.7521* 0.7459* 0.3938* 0.3146* -0.0086 X 0.7194* 0.3947* 0.3645* -0.0091 BV 0.5322* 0.6413* -0.0105 DTA 0.3615* -0.0120 DTL -0.0062

Panel B: Returns model variables

NI CDT Gr R 0.0063 0.0008 -0.0090 NI 0.8405* -0.0007 CDT -0.0011

2014 Capital Market Research Institute, The Stock Exchange of Thailand

30

Table 4 Levels regression using unbalanced panel data and Generalized Least Squares (GLS)

* Indicates significant at p < 0.1 and ** Indicates significant at p < 0.05. X is net profit after tax and abnormal items less outside equity interests. BV is the book value of equity before deferred tax assets and liabilities and excluding outside equity. NDT is the end-of-period recorded book value of net deferred taxes by coding net deferred tax assets as positive numbers and net deferred tax liabilities as negative numbers. All of accounting variables are deflated by the number of share outstanding. Gr is the percentage growth in property, plant and equipment over the quarter. PROP is a dummy variable that equals 1 for property & construction industry sector companies while FIN take the value of 1 for financial sector companies. LOSS, a dummy variable capturing loss quarters, is included in the model and interacted with the key financial variables to allow for differences on the coefficients of profit versus loss making firms. t-statistics are in parentheses.

Full sample Early adoption period Effective period

Intercept -2.052 5.166 18.680**

(-0.27) (0.46) (2.00) X 4.898** 2.044* 0.463

(2.74) (1.45) (0.63) BV 1.810** 2.148** 1.054**

(3.42) (5.04) (1.93)

NDT 5.896** 5.652** 4.186*

(2.17) (2.97) (1.68)

Gr 0.010* 1.510 -0.014** (2.15) (0.91) (-11.00) PROP 4.817 6.509 -7.112 (0.88) (0.46) (-0.84) FIN -2.391 -30.744** 9.072 (-0.15) (-2.72) (0.49) LOSS 0.157 0.234 -0.978** (0.17) (0.18) (-2.71) LOSS*X -5.237** -2.136* -0.827 (-3.04) (-1.47) (-0.52) LOSS*BV 0.050 0.055 0.041 (0.66) (0.58) (0.54) LOSS*NDT 0.846* 1.353** 0.492 (1.68) (2.60) (1.17) n 2,028 834 1,194 R-square 0.6226 0.6555 0.5727 Wald Chi2 70.05** 72.78** 153.19**

2014 Capital Market Research Institute, The Stock Exchange of Thailand

31

Table 5 Returns regression using unbalanced panel data and Generalized Least Squares (GLS)

* Indicates significant at p < 0.1 and ** Indicates significant at p < 0.05. R is market adjusted returns over the quarter. NIa is net profit after tax and abnormal items less outside equity interests and change in net deferred tax. CDTA is the current period net change in the balance of deferred tax assets. CDTL is the current period net change in the balance of deferred tax liabilities. CDT is net change in deferred taxes calculated from CDTA - CDTL. All of accounting variables are deflated by the lagged market value of the firm for quarterly period. t-statistics are in parentheses.

Full sample Early adoption period Effective period Intercept 0.017** 0.050** -0.001 (2.96) (3.64) (-0.26) NIa 0.001 -0.001 0.013* (0.90) (-0.80) (1.78) CDT -0.004 0.003 0.034 (-0.70) (0.87) (0.68) Gr -0.001** -0.044 -0.001* (-2.35) (-1.35) (-1.96) PROP -0.028** 0.001 -0.045** (-2.17) (0.05) (-3.32) FIN 0.051 0.059 0.020 (0.93) (0.65) (1.55) LOSS -0.055** -0.101* -0.021 (-2.67) (-1.93) (-1.19) LOSS* NIa -0.013** -0.009** -0.055** (-2.74) (-2.28) (-2.17) LOSS*CDT -0.042** -0.047** -0.093 (-2.47) (-3.00) (-0.66) N 2,019 833 1,186 R-square 0.0039 0.0032 0.0374 Wald Chi2 37.73** 33.62** 44.98**

2014 Capital Market Research Institute, The Stock Exchange of Thailand

32

Table 6 Levels regression using unbalanced panel data and Generalized Least Squares (GLS)

* Indicates significant at p < 0.1 and ** Indicates significant at p < 0.05. X is net profit after tax and abnormal items less outside equity interests. BV is the book value of equity before deferred tax assets and liabilities and excluding outside equity. DTA is the end-of-period recorded book value of deferred tax assets. DTL is the end-of-period recorded book value of deferred tax liabilities. All of accounting variables are deflated by the number of share outstanding. Gr is the percentage growth in property, plant and equipment over the quarter. PROP is a dummy variable that equals 1 for property & construction industry sector companies while FIN take the value of 1 for financial sector companies. LOSS, a dummy variable capturing loss quarters, is included in the model and interacted with the key financial variables to allow for differences on the coefficients of profit versus loss making firms. t-statistics are in parentheses.

2014 Capital Market Research Institute, The Stock Exchange of Thailand

33

Full sample Early adoption period Effective period

Intercept -2.373 3.563 18.278**

(-0.30) (0.33) (2.02)

X 5.095** 2.389* 0.443

(2.71) (1.69) (0.59)

BV 2.022** 2.523** 1.073**

(3.37) (5.18) (1.75)

DTA -1.372 1.094 4.227 (-0.34) (0.41) (1.02) DTL -8.217** -9.864** -4.246* (-2.44) (-3.83) (-1.57) Gr 0.008** 1.622 -0.013** (1.99) (0.94) (-9.55) PROP 5.195 4.982 -6.868 (0.92) (0.39) (-0.82) FIN 7.035 -26.696** 9.127 (0.48) (-2.33) (0.50) LOSS 0.235 0.684 -0.808** (0.23) (0.40) (-2.86) LOSS*X -5.990** -2.855* -0.570 (-3.05) (-1.87) (-0.33) LOSS*BV 0.026 -0.032 0.112 (0.25) (-0.16) (1.15) LOSS*DTA 1.717 2.503** -1.121 (1.51) (2.48) (-0.98) LOSS*DTL -0.488 -0.222 -0.991* (-0.72) (-0.18) (-1.67) n 2,028 834 1,194 R-square 0.6353 0.6714 0.5732 Wald chi2 67.09** 85.45** 157.57**

2014 Capital Market Research Institute, The Stock Exchange of Thailand

34

Table 7 Levels regression: Financial sector versus other sectors in early adoption period

* Indicates significant at p < 0.1 and ** Indicates significant at p < 0.05. X is net profit after tax and abnormal items less outside equity interests. BV is the book value of equity before deferred tax assets and liabilities and excluding outside equity. DTA is the end-of-period recorded book value of deferred tax assets. DTL is the end-of-period recorded book value of deferred tax liabilities. All of accounting variables are deflated by the number of share outstanding. Gr is the percentage growth in property, plant and equipment over the quarter. LOSS, a dummy variable capturing loss quarters, is included in the model and interacted with the key financial variables to allow for differences on the coefficients of profit versus loss making firms. t-statistics are in parentheses.

Financial sector Other sectors

Intercept -18.232* 8.030

(-1.73) (1.09)

X 4.302* 2.422

(1.87) (1.39) BV 2.300** 2.577**

(3.21) (4.07)

DTA -0.603 -4.295 (-0.30) (-0.40) DTL -4.178 -10.241** (-0.65) (-2.94) Gr 0.364 1.668 (0.11) (0.90) LOSS 2.240 -2.173 (1.20) (-1.13) LOSS*X -4.009** -4.643** (-1.97) (-2.28) LOSS*BV -0.516* 0.041 (-1.65) (0.19) LOSS*DTA 5.569** 3.750 (3.07) (0.96) LOSS*DTL 0.054 -0.631 (0.02) (-0.49) n 257 577 R-square 0.8251 0.6368 Wald chi2 2566.70** 73.61**