second quarter 2016 earnings conference...

TRANSCRIPT

Second Quarter 2016 Earnings

Conference Call

July 27, 2016

Cautionary Note Regarding Forward-Looking Statements

2

Certain information contained in this presentation is forward‐looking information based on current expectations and plans that involve risks and uncertainties. Forward‐looking information includes, among other

things, statements concerning the expected completion of the Southern Natural Gas strategic venture, projected costs and schedules for the completion and start-up of ongoing construction projects, earnings per

share guidance, expected economic development, expected capital expenditures and financing plans. Southern Company cautions that there are certain factors that can cause actual results to differ materially

from the forward‐looking information that has been provided. The reader is cautioned not to put undue reliance on this forward‐looking information, which is not a guarantee of future performance and is subject to

a number of uncertainties and other factors, many of which are outside the control of Southern Company; accordingly, there can be no assurance that such suggested results will be realized. The following

factors, in addition to those discussed in Southern Company’s Annual Report on Form 10‐K for the year ended December 31, 2015, and subsequent securities filings, could cause actual results to differ materially

from management expectations as suggested by such forward‐looking information: the impact of recent and future federal and state regulatory changes, including legislative and regulatory initiatives regarding

deregulation and restructuring of the electric utility industry, environmental laws regulating emissions, discharges, and disposal to air, water, and land, and also changes in tax and other laws and regulations to

which Southern Company and its subsidiaries are subject, as well as changes in application of existing laws and regulations; current and future litigation, regulatory investigations, proceedings, or inquiries,

including, without limitation, Internal Revenue Service and state tax audits; the effects, extent, and timing of the entry of additional competition in the markets in which Southern Company’s subsidiaries operate;

variations in demand for electricity and natural gas, including those relating to weather, the general economy and recovery from the last recession, population and business growth (and declines), the effects of

energy conservation and efficiency measures, including from the development and deployment of alternative energy sources such as self-generation and distributed generation technologies, and any potential

economic impacts resulting from federal fiscal decisions; available sources and costs of natural gas and other fuels; effects of inflation; the ability to control costs and avoid cost overruns during the development

and construction of facilities, which include the development and construction of generating facilities with designs that have not been finalized or previously constructed, including changes in labor costs and

productivity, adverse weather conditions, shortages and inconsistent quality of equipment, materials, and labor, contractor or supplier delay, non-performance under construction, operating, or other agreements,

operational readiness, including specialized operator training and required site safety programs, unforeseen engineering or design problems, start-up activities (including major equipment failure and system

integration), and/or operational performance (including additional costs to satisfy any operational parameters ultimately adopted by any Public Service Commission (“PSC”)); the ability to construct facilities in

accordance with the requirements of permits and licenses, to satisfy any environmental performance standards and the requirements of tax credits and other incentives, and to integrate facilities into the Southern

Company system upon completion of construction; investment performance of Southern Company’s employee and retiree benefit plans and the Southern Company system’s nuclear decommissioning trust funds;

advances in technology; state and federal rate regulations and the impact of pending and future rate cases and negotiations, including rate actions relating to fuel and other cost recovery mechanisms; legal

proceedings and regulatory approvals and actions related to Plant Vogtle Units 3 and 4, including Georgia PSC approvals and Nuclear Regulatory Commission actions; actions related to cost recovery for the

integrated coal gasification combined cycle facility under construction in Kemper County Mississippi (the “Kemper IGCC”), including the ultimate impact of the 2015 decision of the Mississippi Supreme Court, the

Mississippi PSC’s December 2015 rate order, and related legal or regulatory proceedings, Mississippi PSC review of the prudence of Kemper IGCC costs and approval of further permanent rate recovery plans,

actions relating to proposed securitization, satisfaction of requirements to utilize grants, and the ultimate impact of the termination of the proposed sale of an interest in the Kemper IGCC to South Mississippi

Electric Power Association; the ability to successfully operate the electric utilities’ generating, transmission, and distribution facilities and Southern Company Gas’ natural gas distribution and storage facilities and

the successful performance of necessary corporate functions; the inherent risks involved in operating and constructing nuclear generating facilities, including environmental, health, regulatory, natural disaster,

terrorism, and financial risks; the inherent risks involved in transporting and storing natural gas; the performance of projects undertaken by the non-utility businesses and the success of efforts to invest in and

develop new opportunities; internal restructuring or other restructuring options that may be pursued; potential business strategies, including acquisitions or dispositions of assets or businesses, which cannot be

assured to be completed or beneficial to Southern Company or its subsidiaries; the possibility that the anticipated benefits from the acquisition of Southern Company Gas cannot be fully realized or may take

longer to realize than expected, the possibility that costs related to the integration of Southern Company and Southern Company Gas will be greater than expected, the ability to retain and hire key personnel and

maintain relationships with customers, suppliers, or other business partners, and the diversion of management time on integration-related issues; the ability of counterparties of Southern Company and its

subsidiaries to make payments as and when due and to perform as required; the ability to obtain new short- and long-term contracts with wholesale customers; the direct or indirect effect on the Southern

Company system’s business or Southern Company Gas’ business resulting from cyber intrusion or terrorist incidents and the threat of terrorist incidents; interest rate fluctuations and financial market conditions

and the results of financing efforts; changes in Southern Company’s and any of its subsidiaries’ credit ratings, including impacts on interest rates, access to capital markets, and collateral requirements; the

impacts of any sovereign financial issues, including impacts on interest rates, access to capital markets, impacts on currency exchange rates, counterparty performance, and the economy in general, as well as

potential impacts on the benefits of the Department of Energy loan guarantees; the ability of Southern Company’s subsidiaries to obtain additional generating capacity (or sell excess generating capacity) at

competitive prices; catastrophic events such as fires, earthquakes, explosions, floods, hurricanes and other storms, droughts, pandemic health events such as influenzas, or other similar occurrences; the direct

or indirect effects on the Southern Company system’s business or Southern Company Gas’ business resulting from incidents affecting the U.S. electric grid, natural gas pipeline infrastructure, or operation of

generating or storage resources; and the effect of accounting pronouncements issued periodically by standard-setting bodies. Southern Company expressly disclaims any obligation to update any

forward‐looking information.

Major Accomplishments

Vogtle 4

First Syngas

*Subject to closing

3

• First syngas using Gasifier ‘B’

• Heavy level of activity in the coming days

• Next milestone: initial syngas power production

Kemper Project Update

4

Vogtle 3&4 Construction Update

5

Recent Progress

Unit 3Set generator stator, deaerator, and

first low pressure turbine lower casing

Set all “Big 6” modules

Set all four step-up transformers

All four Reactor Coolant Pumps received onsite

Unit 4Completed Cooling Tower Veil

Set first mechanical module

Near Term

Unit 3• Set Containment Vessel Ring 2

Unit 4• Set CA20 module in the auxiliary building

On the Horizon• Set Reactor Vessel (Unit 3)

• Set Steam Generator ‘B’ (Unit 3)

• Initial energization

Unit 3All “Big 6” Modules set

6

CA03

CA02

CA01

CA20

*CA04 is located below CA01 and is not pictured

CA05

Q2 YTD

2015 2016 2015 2016

Earnings Per Share As Reported $0.69 $0.68 $1.25 $1.21

Impact of increase in Kemper cost estimate $0.02 $0.03 $0.02 $0.06

Acquisition costs - $0.03 - $0.05

MCAR Settlement costs - - $0.01 -

Earnings Per Share x-items $0.71 $0.74 $1.28 $1.32

Acquisition Debt Financing Cost* - $0.03 - $0.03

Earnings Per Share Comparable to Guidance $0.71 $0.77 $1.28 $1.35

2016 Earnings Results

7

Note: Please reference the Financial Highlights pages of the earnings package for a full reconciliation.

*For comparison purposes, these costs have been removed as they were not included in the 2016 earnings guidance presented in the first quarter of 2016.

Q2 2016 vs. Q2 2015 Adjusted EPS Drivers

Note: Please reference the Financial Highlights pages of the earnings package for a full reconciliation.

Q2 2015 Q2 2016

$0.71$0.77+13¢ -1¢ +1¢-1¢

Other

Revenue

Impacts

Wholesale

Electric

Operations

Interest

Expense

Traditional Electric

Operating Companies +7¢

-4¢+4¢

Shares-2¢

Retail Sales

Non-fuel

O&M

AFUDC

-4¢

Parent & Other

(Excluding

Acquisition

Financing Debt

Cost)

-2¢

Southern

Power

Depreciation

& AmortizationTaxes

Other

+5¢-3¢

8

2016 Earnings Per Share

9

Excluding• Southern Company Gas and acquisition debt financing cost

• Southern Company Gas, PowerSecure and SONAT acquisition costs

• SONAT and related financing costs

Q3 Estimate = $1.16 per share

2016 Guidance = $2.76 - $2.88*

* 2016 guidance provided as of February 3, 2016 on the 4Q 2015 earnings conference call

Capex

Alabama Power 1.3 0.7 0.6 1.3

Georgia Power 2.5 1.2 1.3 2.5

Gulf Power 0.2 0.1 0.1 0.2

Mississippi Power 0.8 0.3 0.5 0.8

Southern Power* 2.4 1.5 3.0 4.5

Southern Company Gas n/a 0.0 0.8 0.8

Total Capex 7.3 3.9 6.3 10.2

Acquisitions:

Southern Company Gas 8.0 8.0 0.0 8.0

SONAT Pipeline n/a 0.0 1.5 1.5

PowerSecure n/a 0.4 0.0 0.4

Total Acquisitions 8.0 8.4 1.5

Projected 2016 Capital Investments = $20.1B$ in billions

10

Updated ForecastFebruary

Forecast

*Excludes partnership interest

Jan-Jun Jul-Dec Total

Note: totals may not foot due to rounding

112016 2016

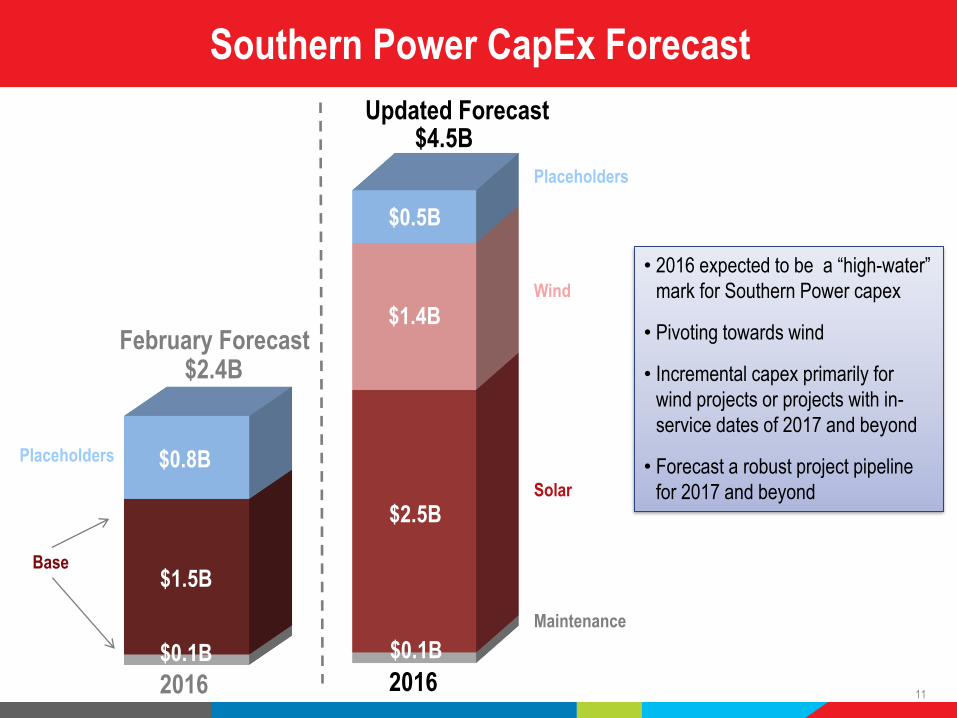

Southern Power CapEx Forecast

$0.8B

$0.5B

$2.5B

$2.4B

$4.5B

February Forecast

$1.5B

$0.1B

Updated Forecast

$0.1B

Wind

Placeholders

Solar

Maintenance

$1.4B

Placeholders

Base

• 2016 expected to be a “high-water”

mark for Southern Power capex

• Pivoting towards wind

• Incremental capex primarily for

wind projects or projects with in-

service dates of 2017 and beyond

• Forecast a robust project pipeline

for 2017 and beyond

2016 Financing Plan$12 billion of debt issued or drawn to date at an average coupon of 2.94% and average maturity of 12 years

$0.5B

$1.0B

$1.5B

$2.0B

$2.5B

$3.0B

$3.5B

$8.0B

$9.0B

Alabama

Power

Georgia

Power

Gulf

Power

Mississippi

Power

Southern

Power

Southern

Company

Gas

Debt for

Investment

In SONAT

Sr. Debt Jr. Subordinated

Debt

Common

Equity

$275M$550M $400M(3)

Parent Company

$400M

$950M$1.2B(1) $1.2B(2)

$8.5B

$1.4B

(1) Syndicated bank loans. Currently drawn $900 million with the remaining $300 million to be drawn in October 2016

(2) Issued amount of $1.2B represents the USD equivalent of €1.1 billion issued in June

(3) Debt to be issued by a Southern Company subsidiary

$300Mfor

placeholders

$750M

$2.0B

$150M

YTD financing activity thru June

Projected Jr. Subordinated Debt

Projected Common Equity

Projected Sr. Debt

Projected DOE Loan

$8.5B

12

$900M

Appendix

Generation Portfolio Diversity

14

Capacity Factors Q2 YTD

2015 2016 2015 2016

Coal - PRB 64% 58% 61% 54%

Coal - Non-PRB 41% 33% 35% 29%

Gas - Combined Cycle 65% 73% 69% 73%

Energy Mix Q2 YTD

2015 2016 2015 2016

Natural Gas 44% 50% 46% 50%

Coal 37% 30% 34% 27%

Nuclear 15% 16% 16% 16%

Hydro/Other 4% 4% 4% 7%

AssetSize

(MW)SPC Ownership

(MW)Location

Original PPA Term

CustomerCODDate

Technology

Cimarron 31 28 Colfax Co., NM 25 years Tri State Dec-2010 First Solar Thin Film (Fixed)

Apex 20 18 N. Las Vegas, NV 25 years NVE Jul-2012 Trina Crystalline (ATI Trackers)

Granville 3 2 Oxford, NC 20 years Duke Energy Oct-2012 MEMC Crystalline (ATI Trackers)

Spectrum 30 27 N. Las Vegas, NV 25 years NVE Sep-2013 MEMC Crystalline (ATI Trackers)

Campo Verde 147 133 Imperial Co., CA 20 years SDG&E Oct-2013 First Solar Thin Film (Fixed)

Adobe 20 18 Kern Co., CA 20 years SCE May-2014 MEMC Crystalline (Gestamp Trackers)

Macho Springs 55 50 Luna Co., NM 20 years El Paso Electric May-2014 First Solar Thin Film (FS trackers)

Imperial Valley (Solar Gen 2)

163 83 Imperial Co., CA 25 years SDG&E Nov-2014 First Solar Thin Film (FS trackers)

Lost Hills-Blackwell 33 17 Kern Co., CA 29 years 4 yr. Roseville/25 yr. PG&E Apr-2015 FS Series 3 Black Plus (FS Trackers)

North Star 62 31 Fresno Co., CA 20 years PG&E Jun-2015 First Solar Thin Film (FS Trackers)

Nacogdoches 116 116 Sacul, TX 20 years Austin Energy Jun-2012 Biomass

Decatur Parkway 84 84 Decatur Co., GA 25 years Georgia Power Dec-2015 First Solar Thin Film (FS Trackers)

Decatur County 20 20 Decatur Co., GA 20 years Georgia Power Dec-2015 Jinko Crystalline (Tracker)

Pawpaw 30 30 Taylor Co., GA 30 years Georgia Power Mar-2016 Trina Crystalline

Butler (Strata) 22 22 Taylor Co., GA 20 years Georgia Power Feb-2016 FS Series 3 Black Plus Fixed

Morelos del Sol 15 14 Kern Co., CA 20 years PG&E Nov-2015 Solar Frontier Thin Film (Clavijo)

Calipatria 20 18 Imperial Co. CA 20 years SDG&E Feb-2016 Solar Frontier Thin Film (Clavijo)

Kay Wind 299 299 Kay Co., OK 20 years Westar (199 MW) GRDA (100 MW) Dec-2015 130WT’s Siemens

Grant Wind 152 152 Grant Co., OK 20 years E. TX EC/NE. TX EC/W. Farmers EC Apr-2016 66 WT’s Siemens

Passadumkeag 43 43 Penobscot Co., ME 15 years Eversource Energy (WMECO) Jul-2016 13 WT’s Vestas

Subtotal –Operating Assets

1,365 1,205

Southern Power Renewable Portfolio – Operational Assets

15

AssetSize

(MW)SPC Ownership

(MW)Location

Original PPA Term

CustomerCODDate

Technology

Sandhills - Taylor County (EMCs)

147 147 Taylor Co., GA 25 yearsCobb, Flint, Irwin, Middle Georgia

and Sawnee EMC’sQ4-2016 First Solar Thin Film (FS Trackers)

Butler (Community) 104 104 Taylor Co., GA 30 years Georgia Power Q4-2016 First Solar Thin Film (FS Trackers)

Desert Stateline 300 198 San Bernardino, CA 20 years SCE Q3-2016 First Solar Thin Film (Fixed)

Tranquillity 205 105 Fresno Co., CA 18 years Shell Energy & SCE Q4-2016 Polycrystalline (Tracking)

Garland & Garland A 205 105 Kern Co., CA 15 & 20 years SCE Q4-2016 Multicrystalline (Tracking)

Roserock 160 82 Pecos Co., TX 20 years Austin Energy Q4-2016 Multicrystalline (Tracking)

East Pecos 120 120 Pecos Co., TX 15 years Austin Energy Q4-2016 First Solar Thin Film (FS Trackers)

Henrietta 102 52 Kings Co., CA 20 years PG&E Q3-2016 SunPower modular power block

Rutherford 75 67 Rutherford Co., NC Confidential Confidential Q4-2016 Trina Monocrystalline (Fixed)

Lamesa 102 102 Dawson Co., TX 15 years City of Garland Q2-2017 Trina Polycrystalline (Tracking)

Subtotal - Under Construction

1,520 1,082

Grand Total 2,885 2,287

Southern Power Renewable Portfolio – Projects Under Construction

16

Southern Company and Subsidiary Ratings

17

Senior Unsecured (Moody’s/S&P/Fitch)

Southern Company Baa2/BBB+/A-

(S/N/S)

AlabamaPower

A1/A-/A+(S/N/S)

GeorgiaPower

A3/A-/A+(S/N/S)

GulfPower

A2/A-/A(S/N/S)

MississippiPower

Baa3/BBB+/BBB+(N/N/S)

SouthernPower

Baa1/BBB+/BBB+(S/N/S)

Southern Company Gas

Nicor GasAa3/A/AA-

(S/N/S)

Southern Company Gas Capital

Baa1/A-/BBB+(S/N/S)

Note: Ratings, other than Nicor Gas, are Senior Unsecured (Moody’s/S&P/Fitch). Nicor Gas Ratings are Sr. Secured. A securities rating is not a recommendation to buy,

sell or hold securities and may be subject to revision or withdrawal at any time. The graphic above represents a simplified diagram highlighting major SO issuing entities.

P – Positive Outlook, S – Stable outlook, N – Negative Outlook, NR – Not Rated

Long-term Debt Maturity Schedule$ in millions - as of June 30, 2016

18

SO Pro-Forma Long-Term

Debt Maturities 2016-2020

$13,290

2016

YTD Remaining Total 2017 2018 2019 2020 5Y Total

Alabama Power 200 - 200 561 - 200 250 1,211

Georgia Power 504 200 704 450 750 500 42 2,446

Gulf Power 125 110 235 85 - - 175 495

Mississippi Power 900 300 1,200 586 900 125 7 2,818

Southern Power - 400 400 500 350 - 300 1,550

Parent - 500 500 800 1,000 1,350 600 4,250

SO Standalone 1,729 1,510 3,239 2,431 3,000 2,175 1,373 12,218

Southern Company Gas 125 420 545 22 155 350 - 1,072

SO Pro-Forma(1) 1,854 1,930 3,784 2,453 3,155 2,525 1,373 13,290

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

$4,000

2016 2017 2018 2019 2020

SO Pro-Forma Long-Term Debt Maturity Profile

SO Standalone Southern Company Gas(1) Gives pro-forma effect to the acquisition of Southern Company Gas

Southern Company Liquidity and Credit $ in millions - as of 6/30/2016

19

Post-acquisition of Southern Company Gas, Southern Company will have nearly

$8.5 billion in committed credit facilities

(1) Other reflects non-SEC reporting subsidiaries including PowerSecure, SEGCO, Southern Nuclear, SouthernLINC and others(2) Includes Cash and Cash Equivalents, Parent cash excludes approximately $8 billion of restricted cash as of 6/30/2016; subject to revision prior to filing Southern Company second quarter 2016 10-Q(3) PCB Floaters include all variable rate pollution control revenue bonds outstanding

* Gives pro-forma effect to the acquisition of SO Gas

Note: totals may not foot due to rounding

2016 2017 2018 2019 2020 Total

SO Consolidated Credit Facilities Expirations $ 353 $ 63 $ 1,665 $ - $ 4,400 $ 6,480

Southern Company Gas Facility Expirations $ - $ 75 $ 1,925 $ - $ - $ 2,000

SO Pro-Forma Facility Expirations* $ 353 $ 138 $ 3,590 $ - $ 4,400 $ 8,480

Alabama

Power

Georgia

Power

Gulf

Power

Mississippi

Power Parent

Southern

Power Other(1)

SO

Consolidated

Southern

Company Gas

SO Pro-

Forma

Unused Credit Lines 1,335 1,732 280 150 2,250 560 80 6,386 1,943 8,329

Cash(2)

343$ 121$ 46$ 137$ 122$ 1,023$ 104$ 1,897$ 15$ 1,912$

Total 1,678 1,853 326 287 2,372 1,583 184 8,283 1,959 10,241

Less: Outstanding CP - 197 88 - 95 62 41 478 114 592

Less: PCBs Floaters(3)

890 868 82 40 - - - 1,880 - 1,880

Net Available Liquidity 788$ 788$ 156$ 247$ 2,277$ 1,521$ 144$ 5,924$ 1,845$ 7,769$

*