segmental bridge+i. - pci.org · (fhwa). these unpublished ... cast prestressed i-girder spans and...

TRANSCRIPT

+°• Segmental Bridge+I.

Construction—Thev Wave of the Future

♦*r r^

♦fit

.. W. Jack Wilkes*++^ Vice President

• Figg and Muller Engineers, Inc.'++ Washington, D C.

There is today a resurgence in high-way bridge construction across North

America spurred on by the demand fornew bridges and a pressing need for therehabilitation and replacement of exist-ing bridges. It would appear then thatthe members of the Prestressed Con-crete Institute, both individually and col-lectively, are interested in expandingtheir businesses by taking advantage ofthis burgeoning bridge market.

If we are to properly assess the pros-pects for growth, however, we need toexamine past performance.

In a 1976 report, W. Burr Bennett, Jr.,at the time PCI executive director, statedthat the precast prestressed concreteindustry started with no producers in1949, exceeded $10 million production

'Formerly. Chief, Bridge Division, Federat HighwayAdministration, U.S. Department of Transportation,Washington, D.C.

in 1959, and had reached a total volumeof $1.4 billion in 1975 from 350 man-ufacturers. Unfortunately, since then, theindustry's exponential growth of the past2 1/2 decades has slowed down to atrickle. For an example of what has hap-pened to transportation structures, andparticularly highway bridges, let us lookat some statistical data obtained fromthe Federal Highway Administration(FHWA).

These unpublished annual reportsshow the number, costs, and percentageof bridges constructed each calendaryear since 1966 with federal highwayfunds for the three major categories ofstructure, namely, reinforced concrete,structural steel. and prestressed con-crete. These data are summarized inTable 1. Similar data are not availablefor bridges built without federal funds,but the trends and percentages wouldnot vary appreciably.

24

Based on federal statistical data and his many

years of experience in the bridge field, the authorcontends that the time is ripe for producers to make

the quantum jump to precast concrete segmentalconstruction.

1600

1400 11

1200 rI

W 1000 ^--^ VSTEEL1^/

q Boo '

\ ^7

oJ 600 \^

N, PRESTRESSED

::::T

E

REINFORCED400

CONCRETE ^^

200 ^ ---, --^ ---

69 70 71 72 73 74 75 76 77 78 79 80CALENDAR YEARS

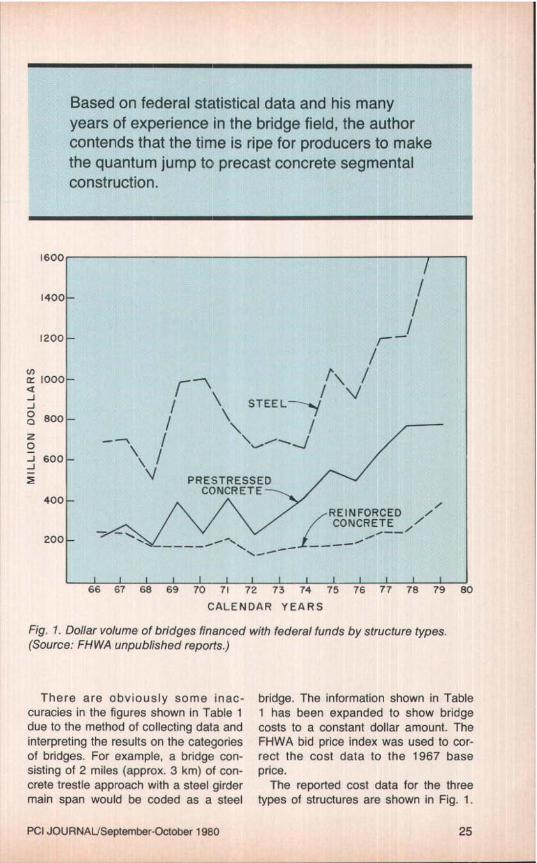

Fig. 1. Dollar volume of bridges financed with federal funds by structure types.(Source: FHWA unpublished reports.)

There are obviously some inac-curacies in the figures shown in Table 1due to the method of collecting data andinterpreting the results on the categoriesof bridges. For example, a bridge con-sisting of 2 mires (approx. 3 km) of con-crete trestle approach with a steel girdermain span would be coded as a steel

bridge. The information shown in Table1 has been expanded to show bridgecosts to a constant dollar amount. TheFHWA bid price index was used to cor-rect the cost data to the 1967 baseprice.

The reported cost data for the threetypes of structures are shown in Fig. 1.

PCI JOURNAL.1September-October 1980 25

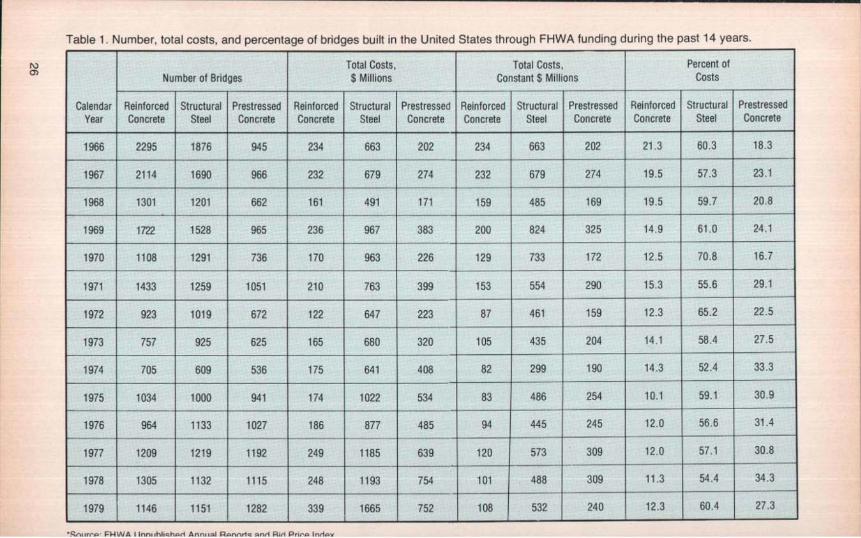

Table 1 Number, total costs, and percentage of bridges built in the United States through FHWA funding during the past 14 years.

Number of BridgesTotal Costs,$ Millions

Total Costs,Constant $ Millions

Percent ofCosts

CalendarYear

ReinforcedConcrete

StructuralSteel

PrestressedConcrete

ReinforcedConcrete

StructuralSteel

PrestressedConcrete

ReinforcedConcrete

StructuralSteel

PrestressedConcrete

ReinforcedConcrete

StructuralSteel

PrestressedConcrete

1966 2295 1876 945 234 663 202 234 663 202 21.3 60.3 18.3

1967 2114 1690 966 232 679 274 232 679 274 19.5 57.3 23.1

1968 1301 1201 662 161 491 171 159 485 169 19.5 59.7 20.8

1969 1722 1528 965 236 967 383 200 824 325 14.9 61.0 24.1

1970 1108 1291 736 170 963 226 129 733 172 12.5 70.8 16.7

1971 1433 1259 1051 210 763 399 153 554 290 15.3 55.6 29.1

1972 923 1019 672 122 647 223 87 461 159 12.3 65.2 22.5

1973 757 925 625 165 680 320 105 435 204 14.1 58.4 27.5

1974 705 609 536 175 641 408 82 299 190 14.3 52.4 33.3

1975 1034 1000 941 174 1022 534 83 486 254 10.1 59.1 30.9

1976 964 1133 1027 186 877 485 94 445 245 12.0 56.6 31.4

1977 1209 1219 1192 249 1185 639 120 573 309 12.0 57.1 30.8

1978 1305 1132 1115 248 1193 754 101 488 309 11.3 54.4 34.3

1979 1146 1151 1282 339 1665 752 108 532 240 12.3 60.4 27.3

Sniirrn FI4WA I Innnhlichnrl Annual Pnnnrtc and Pir Prnnn lnrica

The constant dollar value for the threetypes is shown in Fig. 2. The curves tellus that what appeared to be a continualgrowth for prestressed concrete bridges(see Fig. 1) is in reality no growth at allfor the last 10 years. This is despite thefact that the funding for the Federal As-sisted Bridge Replacement Programshould have produced almost a one bil-lion dollar increase in bridge construc-tion for 1979. Perhaps this growth willshow up in the 1980 results, but I doubtit.

Each of us can form our own opinion forthis lack of growth, but let me give youmy thoughts on the subject.

Until recently, prestressed concretebridges in North America could becategorized into two general types: pre-cast prestressed I-girder spans andpost-tensioned box girder spans. Theprestressed I-girder designs or thefamiliar AASHTO-PCI standard sectionsare simple substitutions for conventional

reinforced concrete or steel beams. Theprestressed i-girder designs have domi-nated short-span bridge construction inmost parts of the United States, How-ever, in California, the most commonstructure for moderate span lengths hasbeen cast-in-place concrete box girderdesigns.

In both the I-girder (although to amuch less degree) and box girder con-structions, extensive on-site labor, mate-rials, and equipment are required. Con-ventional construction methods areutilized: falsework, forms, steel placingand tying, concrete batching, mixing,placing, and finishing. These are essen-tially the methods and techniques thathave been used for the last 100 years.

If we are to make significant progressin the bridge market, we have to find abetter way to perform these operations.It should be no surprise that thepioneers in this field have not only founda better way but they have found thebest way! The better way is cast-in-

800 r•

U)

o soo \, !I STEEL ^\ \'C 1

-J 400 PRESTRESSED

JCONCRETE `\^

^^ '^` REIN FORCED2O0-CONCRETE

66 67 68 69 70 71 72 73 74 75 76 77 78 79 80

CALENDAR YEARS

Fig. 2. Constant dollar volume of bridges financed with federal funds. (Source:

FHWA bid price index.)

PCI JOURNAL September-October 1980 27

place segmental concrete box girderswhich is still necessary for very longspan construction but the best way isprecast segmental concrete box girders.

The principal disadvantage of cast-in-place construction is that it is subjectto the same difficulties that the otheron-site construction methods sufferfrom. The most obvious advantages ofprecast segmental construction are:speed of construction, quality control offactory production, reduction of on-sitelabor and operations, maximum reduc-tion of materials and as a result is muchmore economical where multiple spansare required. These benefits are in addi-tion to the vastly improved aesthetic ap-pearance and elimination of futuremaintenance costs which are commonfor all concrete box girder structures.

Let us now take a quick look at thetrack record of recent precast andcast-in-place segmental concrete boxgirder bridges built in the United States.When alternate designs are offered, the

segmental designs have been 10 to 20percent lower than conventional designswhich sometimes included precast pre-stressed girders. The span lengths varyfrom 100 to 400 ft (30 to 122 m) for pre-cast segmental designs and up to 750 ft(229 m) for cast-in-place segmental de-signs. If we look into designs that havebeen prepared and studies that are al-ready underway, we can anticipate thatprecast segmental designs areeconomical for spans as short as 40 ft(12 m) and for cast-in-place segmentalspans up to 850 ft (259 m).

The examples for the above citedspan lengths are the Long Key Bridge inFlorida with 118-ft (36 m) spans and theDauphin Island Bridge in Alabama withthe 400-ft (122 m) span using precastsegmental construction. The longestspan cast-in-place segmental bridge inNorth America is the Houston ShipChannel Bridge [750 ft (229 m) 1.

Span ranges for segmental concreteconstruction have been expanded to truly

One of the 9 ft (2.75 m) deep precast segments for Linn Cove Viaduct beingtrucked to construction site. The segments were cast inside a building about a mile(1.6 km) from bridge. Indoor casting was necessary due to severe weather of theBlue Ridge Mountain region of North Carolina.

1

monumental proportions by usircable-stayed designs. Bridges wi1050-ft (320 m) center spans have beiconstructed and designs have be(completed for a 1300-ft (397 m) centspan for the Dames Point BridgeJacksonville, Florida. There seems to tno limit to the future of segmental coCrete concepts.

At one time bridge engineers weable to estimate at the preliminary dsign stage what structural type and mterial would be the most economical.today's inflationary period of materiprices, it is almost impossible for brideengineers to determine with any degrtof certainty the most economical desicuntil actual bids are received. The biding documents must provide many otions of materials, construction methodand designs. "Value Engineering" dorduring the design stage pays off mu(more than that done during constructioi

What can now be done to take avantage of this new technology? Finwe should advocate as national poll,,,the concept of alternate designs. TheFHWA has issued instructions to theirfield offices that all "major bridges" mustprovide for alternate designs. The defini-tion for "major bridge" is somewhatflexible, but a bridge costing as much as$5 million should in my opinion have al-ternate designs prepared. The wisdomof this policy has been proven time aftertime. When alternate designs are offeredfor bridge projects, not only is competi-tion between materials offered, but addi-tional contractors are attracted to bid oneach type of structure. Competition isthe name of the game to reduce costs!

On the subject of competition, I do notunderstand why so few prestressedconcrete producers have been involvedin segmental concrete bridge projects inthe United States. In practically everysegmental project to date, the success-ful contractor has had to set up his ownprecast operation. When this occurs it

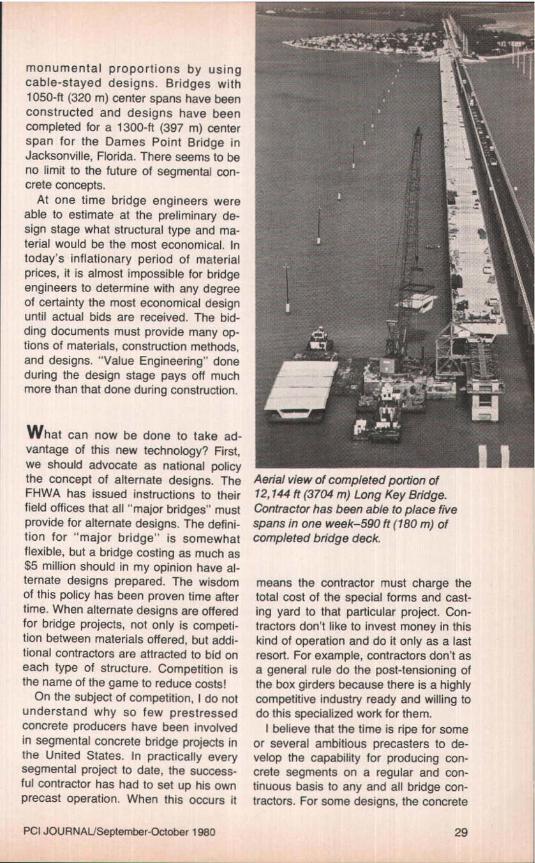

Aerial view of completed portion of12,144 ft (3704 m) Long Key Bridge.Contractor has been able to place fivespans in one week-590 ft (180 m) ofcompleted bridge deck.

means the contractor must charge thetotal cost of the special forms and cast-ing yard to that particular project. Con-tractors don't like to invest money in thiskind of operation and do it only as a lastresort. For example, contractors don't asa general rule do the post-tensioning ofthe box girders because there is a highlycompetitive industry ready and willing todo this specialized work for them.

f believe that the time is ripe for someor several ambitious precasters to de-velop the capability for producing con-crete segments on a regular and con-tinuous basis to any and alt bridge con-tractors. For some designs, the concrete

PCI JOURNAL/September-October 1980 29

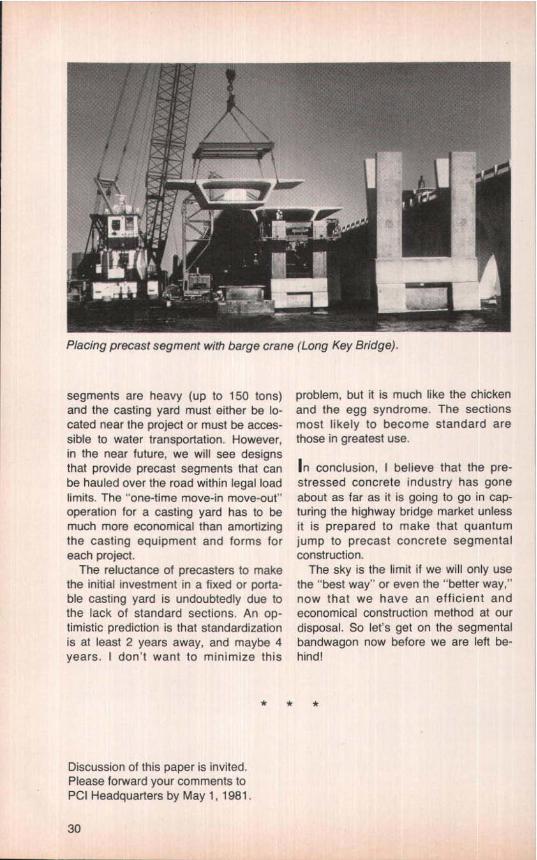

Placing precast segment with barge crane (Long Key Bridge).

segments are heavy (up to 150 tons)and the casting yard must either be lo-cated near the project or must be acces-sible to water transportation. However,in the near future, we will see designsthat provide precast segments that canbe hauled over the road within legal loadlimits. The "one-time move-in move-out"operation for a casting yard has to bemuch more economical than amortizingthe casting equipment and forms foreach project.

The reluctance of precasters to makethe initial investment in a fixed or porta-ble casting yard is undoubtedly due tothe lack of standard sections. An op-timistic prediction is that standardizationis at least 2 years away, and maybe 4years. I don't want to minimize this

problem, but it is much like the chickenand the egg syndrome. The sectionsmost likely to become standard arethose in greatest use.

In conclusion, I believe that the pre-stressed concrete industry has goneabout as far as it is going to go in cap-turing the highway bridge market unlessit is prepared to make that quantumjump to precast concrete segmentalconstruction.

The sky is the limit if we will only usethe "best way" or even the "better way,"now that we have an efficient andeconomical construction method at ourdisposal. So let's get on the segmentalbandwagon now before we are left be-hind!

Discussion of this paper is invited.Please forward your comments toPCI Headquarters by May 1, 1981,

30