segura j., braun c. (eds.) an eponymous dictionary of economics (elgar, 2004)(isbn...

TRANSCRIPT

An Eponymous Dictionary of Economics

An Eponymous Dictionaryof EconomicsA Guide to Laws and Theorems Named after Economists

Edited by

Julio SeguraProfessor of Economic Theory, Universidad Complutense, Madrid, Spain,

and

Carlos Rodríguez BraunProfessor of History of Economic Thought, Universidad Complutense,Madrid, Spain

Edward ElgarCheltenham, UK • Northampton, MA, USA

© Carlos Rodríguez Braun and Julio Segura 2004

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical or photocopying, recording, or otherwise without the prior permission of the publisher.

Published byEdward Elgar Publishing LimitedGlensanda HouseMontpellier ParadeCheltenhamGlos GL50 1UAUK

Edward Elgar Publishing, Inc.136 West StreetSuite 202NorthamptonMassachusetts 01060USA

A catalogue record for this bookis available from the British Library

ISBN 1 84376 029 0 (cased)

Typeset by Cambrian Typesetters, Frimley, SurreyPrinted and bound in Great Britain by MPG Books Ltd, Bodmin, Cornwall

Contents

List of contributors and their entries xiiiPreface xxvii

Adam Smith problem 1Adam Smith’s invisible hand 1Aitken’s theorem 3Akerlof’s ‘lemons’ 3Allais paradox 4Areeda–Turner predation rule 4Arrow’s impossibility theorem 6Arrow’s learning by doing 8Arrow–Debreu general equilibrium model 9Arrow–Pratt’s measure of risk aversion 10Atkinson’s index 11Averch–Johnson effect 12

Babbage’s principle 13Bagehot’s principle 13Balassa–Samuelson effect 14Banach’s contractive mapping principle 14Baumol’s contestable markets 15Baumol’s disease 16Baumol–Tobin transactions demand for cash 17Bayes’s theorem 18Bayesian–Nash equilibrium 19Becher’s principle 20Becker’s time allocation model 21Bellman’s principle of optimality and equations 23Bergson’s social indifference curve 23Bernoulli’s paradox 24Berry–Levinsohn–Pakes algorithm 25Bertrand competition model 25Beveridge–Nelson decomposition 27Black–Scholes model 28Bonferroni bound 29Boolean algebras 30Borda’s rule 30Bowley’s law 31Box–Cox transformation 31Box–Jenkins analysis 32Brouwer fixed point theorem 34

v

Buchanan’s clubs theory 34Buridan’s ass 35

Cagan’s hyperinflation model 36Cairnes–Haberler model 36Cantillon effect 37Cantor’s nested intervals theorem 38Cass–Koopmans criterion 38Cauchy distribution 39Cauchy’s sequence 39Cauchy–Schwarz inequality 40Chamberlin’s oligopoly model 41Chipman–Moore–Samuelson compensation criterion 42Chow’s test 43Clark problem 43Clark–Fisher hypothesis 44Clark–Knight paradigm 44Coase conjecture 45Coase theorem 46Cobb–Douglas function 47Cochrane–Orcutt procedure 48Condorcet’s criterion 49Cournot aggregation condition 50Cournot’s oligopoly model 51Cowles Commission 52Cox’s test 53

Davenant–King law of demand 54Díaz–Alejandro effect 54Dickey–Fuller test 55Director’s law 56Divisia index 57Dixit–Stiglitz monopolistic competition model 58Dorfman–Steiner condition 60Duesenberry demonstration effect 60Durbin–Watson statistic 61Durbin–Wu–Hausman test 62

Edgeworth box 63Edgeworth expansion 65Edgeworth oligopoly model 66Edgeworth taxation paradox 67Ellsberg paradox 68Engel aggregation condition 68Engel curve 69Engel’s law 71

vi Contents

Engle–Granger method 72Euclidean spaces 72Euler’s theorem and equations 73

Farrell’s technical efficiency measurement 75Faustmann–Ohlin theorem 75Fisher effect 76Fisher–Shiller expectations hypothesis 77Fourier transform 77Friedman’s rule for monetary policy 79Friedman–Savage hypothesis 80Fullarton’s principle 81Fullerton–King’s effective marginal tax rate 82

Gale–Nikaido theorem 83Gaussian distribution 84Gauss–Markov theorem 86Genberg–Zecher criterion 87Gerschenkron’s growth hypothesis 87Gibbard–Satterthwaite theorem 88Gibbs sampling 89Gibrat’s law 90Gibson’s paradox 90Giffen goods 91Gini’s coefficient 91Goodhart’s law 92Gorman’s polar form 92Gossen’s laws 93Graham’s demand 94Graham’s paradox 95Granger’s causality test 96Gresham’s law 97Gresham’s law in politics 98

Haavelmo balanced budget theorem 99Hamiltonian function and Hamilton–Jacobi equations 100Hansen–Perlof effect 101Harberger’s triangle 101Harris–Todaro model 102Harrod’s technical progress 103Harrod–Domar model 104Harsanyi’s equiprobability model 105Hausman’s test 105Hawkins–Simon theorem 106Hayekian triangle 107Heckman’s two-step method 108

Contents vii

Heckscher–Ohlin theorem 109Herfindahl–Hirschman index 111Hermann–Schmoller definition 111Hessian matrix and determinant 112Hicks compensation criterion 113Hicks composite commodities 113Hicks’s technical progress 113Hicksian demand 114Hicksian perfect stability 115Hicks–Hansen model 116Hodrick–Prescott decomposition 118Hotelling’s model of spatial competition 118Hotelling’s T2 statistic 119Hotelling’s theorem 120Hume’s fork 121Hume’s law 121

Itô’s lemma 123

Jarque–Bera test 125Johansen’s procedure 125Jones’s magnification effect 126Juglar cycle 126

Kakutani’s fixed point theorem 128Kakwani index 128Kalai–Smorodinsky bargaining solution 129Kaldor compensation criterion 129Kaldor paradox 130Kaldor’s growth laws 131Kaldor–Meade expenditure tax 131Kalman filter 132Kelvin’s dictum 133Keynes effect 134Keynes’s demand for money 134Keynes’s plan 136Kitchin cycle 137Kolmogorov’s large numbers law 137Kolmogorov–Smirnov test 138Kondratieff long waves 139Koopman’s efficiency criterion 140Kuhn–Tucker theorem 140Kuznets’s curve 141Kuznets’s swings 142

Laffer’s curve 143Lagrange multipliers 143

viii Contents

Lagrange multiplier test 144Lancaster’s characteristics 146Lancaster–Lipsey’s second best 146Lange–Lerner mechanism 147Laspeyres index 148Lauderdale’s paradox 148Learned Hand formula 149Lebesgue’s measure and integral 149LeChatelier principle 150Ledyard–Clark–Groves mechanism 151Leontief model 152Leontief paradox 153Lerner index 154Lindahl–Samuelson public goods 155Ljung–Box statistics 156Longfield paradox 157Lorenz’s curve 158Lucas critique 158Lyapunov’s central limit theorem 159Lyapunov stability 159

Mann–Wald’s theorem 161Markov chain model 161Markov switching autoregressive model 162Markowitz portfolio selection model 163Marshall’s external economies 164Marshall’s stability 165Marshall’s symmetallism 166Marshallian demand 166Marshall–Lerner condition 167Maskin mechanism 168Minkowski’s theorem 169Modigliani–Miller theorem 170Montaigne dogma 171Moore’s law 172Mundell–Fleming model 172Musgrave’s three branches of the budget 173Muth’s rational expectations 175Myerson revelation principle 176

Nash bargaining solution 178Nash equilibrium 179Negishi’s stability without recontracting 181von Neumann’s growth model 182von Neumann–Morgenstern expected utility theorem 183von Neumann–Morgenstern stable set 185

Contents ix

Newton–Raphson method 185Neyman–Fisher theorem 186Neyman–Pearson test 187

Occam’s razor 189Okun’s law and gap 189

Paasche index 192Palgrave’s dictionaries 192Palmer’s rule 193Pareto distribution 194Pareto efficiency 194Pasinetti’s paradox 195Patman effect 197Peacock–Wiseman’s displacement effect 197Pearson chi-squared statistics 198Peel’s law 199Perron–Frobenius theorem 199Phillips curve 200Phillips–Perron test 201Pigou effect 203Pigou tax 204Pigou–Dalton progressive transfers 204Poisson’s distribution 205Poisson process 206Pontryagin’s maximun principle 206Ponzi schemes 207Prebisch–Singer hypothesis 208

Radner’s turnpike property 210Ramsey model and rule 211Ramsey’s inverse elasticity rule 212Rao–Blackwell’s theorem 213Rawls’s justice criterion 213Reynolds–Smolensky index 214Ricardian equivalence 215Ricardian vice 216Ricardo effect 217Ricardo’s comparative costs 218Ricardo–Viner model 219Robinson–Metzler condition 220Rostow’s model 220Roy’s identity 222Rubinstein’s model 222Rybczynski theorem 223

x Contents

Samuelson condition 225Sard’s theorem 225Sargan test 226Sargant effect 227Say’s law 227Schmeidler’s lemma 229Schumpeter’s vision 230Schumpeterian entrepreneur 230Schwarz criterion 231Scitovsky’s community indifference curve 232Scitovsky’s compensation criterion 232Selten paradox 233Senior’s last hour 234Shapley value 235Shapley–Folkman theorem 236Sharpe’s ratio 236Shephard’s lemma 237Simon’s income tax base 238Slutksky equation 238Slutsky–Yule effect 240Snedecor F-distribution 241Solow’s growth model and residual 242Sonnenschein–Mantel–Debreu theorem 244Spencer’s law 244Sperner’s lemma 245Sraffa’s model 245Stackelberg’s oligopoly model 246Stigler’s law of eponymy 247Stolper–Samuelson theorem 248Student t-distribution 248Suits index 250Swan’s model 251

Tanzi–Olivera effect 252Taylor rule 252Taylor’s theorem 253Tchébichef’s inequality 254Theil index 254Thünen’s formula 255Tiebout’s voting with the feet process 256Tinbergen’s rule 257Tobin’s q 257Tobin’s tax 258Tocqueville’s cross 260Tullock’s trapezoid 261Turgot–Smith theorem 262

Contents xi

Veblen effect good 264Verdoorn’s law 264Vickrey auction 265

Wagner’s law 266Wald test 266Walras’s auctioneer and tâtonnement 268Walras’s law 268Weber–Fechner law 269Weibull distribution 270Weierstrass extreme value theorem 270White test 271Wicksell effect 271Wicksell’s benefit principle for the distribution of tax burden 273Wicksell’s cumulative process 274Wiener process 275Wiener–Khintchine theorem 276Wieser’s law 276Williams’s fair innings argument 277Wold’s decomposition 277

Zellner estimator 279

xii Contents

Contributors and their entries

Albarrán, Pedro, Universidad Carlos III, Madrid, SpainPigou tax

Albert López-Ibor, Rocío, Universidad Complutense, Madrid, SpainLearned Hand formula

Albi, Emilio, Universidad Complutense, Madrid, SpainSimons’s income tax base

Almenar, Salvador, Universidad de Valencia, Valencia, SpainEngel’s law

Almodovar, António, Universidade do Porto, Porto, PortugalWeber–Fechner law

Alonso, Aurora, Universidad del País Vasco-EHU, Bilbao, SpainLucas critique

Alonso Neira, Miguel Ángel, Universidad Rey Juan Carlos, Madrid, SpainHayekian triangle

Andrés, Javier, Universidad de Valencia, Valencia, SpainPigou effect

Aparicio-Acosta, Felipe M., Universidad Carlos III, Madrid, SpainFourier transform

Aragonés, Enriqueta, Universitat Autònoma de Barcelona, Barcelona, SpainRawls justice criterion

Arellano, Manuel, CEMFI, Madrid, SpainLagrange multiplier test

Argemí, Lluís, Universitat de Barcelona, Barcelona, SpainGossen’s laws

Arruñada, Benito, Universitat Pompeu Fabra, Barcelona, SpainBaumol’s disease

Artés Caselles, Joaquín, Universidad Complutense, Madrid, SpainLeontief paradox

Astigarraga, Jesús, Universidad de Deusto, Bilbao, SpainPalgrave’s dictionaries

Avedillo, Milagros, Comisión Nacional de Energía, Madrid, SpainDivisia index

Ayala, Luis, Universidad Rey Juan Carlos, Madrid, SpainAtkinson index

xiii

Ayuso, Juan, Banco de España, Madrid, SpainAllais paradox; Ellsberg paradox

Aznar, Antonio, Universidad de Zaragoza, Zaragoza, SpainDurbin–Wu–Hausman test

Bacaria, Jordi, Universitat Autònoma de Barcelona, Barcelona, SpainBuchanan’s clubs theory

Badenes Plá, Nuria, Universidad Complutense, Madrid, SpainKaldor–Meade expenditure tax; Tiebout’s voting with the feet process; Tullock’s trapezoid

Barberá, Salvador, Universitat Autònoma de Barcelona, Barcelona, SpainArrow’s impossibility theorem

Bel, Germà, Universitat de Barcelona, Barcelona, SpainClark problem; Clark–Knight paradigm

Bentolila, Samuel, CEMFI, Madrid, SpainHicks–Hansen model

Bergantiños, Gustavo, Universidad de Vigo, Vigo, Pontevedra, SpainBrouwer fixed point theorem; Kakutani’s fixed point theorem

Berganza, Juan Carlos, Banco de España, Madrid, SpainLerner index

Berrendero, José R., Universidad Autónoma, Madrid, SpainKolmogorov–Smirnov test

Blanco González, María, Universidad San Pablo CEU, Madrid, SpainCowles Commission

Bobadilla, Gabriel F., Omega-Capital, Madrid, SpainMarkowitz portfolio selection model; Fisher–Shiller expectations hypothesis

Bolado, Elsa, Universitat de Barcelona, Barcelona, SpainKeynes effect

Borrell, Joan-Ramon, Universitat de Barcelona, Barcelona, SpainBerry–Levinsohn–Pakes algorithm

Bover, Olympia, Banco de España, Madrid, SpainGaussian distribution

Bru, Segundo, Universidad de Valencia, Valencia, SpainSenior’s last hour

Burguet, Roberto, Universitat Autònoma de Barcelona, Barcelona, SpainWalras’s auctioneer and tâtonnement

Cabrillo, Francisco, Universidad Complutense, Madrid, SpainCoase theorem

Calderón Cuadrado, Reyes, Universidad de Navarra, Pamplona, SpainHermann–Schmoller definition

xiv Contributors and their entries

Callealta, Francisco J., Universidad de Alcalá de Henares, Alcalá de Henares, Madrid,SpainNeyman–Fisher theorem

Calsamiglia, Xavier, Universitat Pompeu Fabra, Barcelona, SpainGale–Nikaido theorem

Calzada, Joan, Universitat de Barcelona, Barcelona, SpainStolper–Samuelson theorem

Candeal, Jan Carlos, Universidad de Zaragoza, Zaragoza, SpainCantor’s nested intervals theorem; Cauchy’s sequence

Carbajo, Alfonso, Confederación Española de Cajas de Ahorro, Madrid, SpainDirector’s law

Cardoso, José Luís, Universidad Técnica de Lisboa, Lisboa, PortugalGresham’s law

Carnero, M. Angeles, Universidad Carlos III, Madrid, SpainMann–Wald’s theorem

Carrasco, Nicolás, Universidad Carlos III, Madrid, SpainCox’s test; White test

Carrasco, Raquel, Universidad Carlos III, Madrid, SpainCournot aggregation condition; Engel aggregation condition

Carrera, Carmen, Universidad Complutense, Madrid, SpainSlutsky equation

Caruana, Guillermo, CEMFI, Madrid, SpainHicks composite commodities

Castillo, Ignacio del, Ministerio de Hacienda, Madrid, SpainFullarton’s principle

Castillo Franquet, Joan, Universitat Autònoma de Barcelona, Barcelona, SpainTchébichef’s inequality

Castro, Ana Esther, Universidad de Vigo, Vigo, Pontevedra, SpainPonzi schemes

Cerdá, Emilio, Universidad Complutense, Madrid, SpainBellman’s principle of optimality and equations; Euler’s theorem and equations

Comín, Diego, New York University, New York, USAHarrod–Domar model

Corchón, Luis, Universidad Carlos III, Madrid, SpainMaskin mechanism

Costas, Antón, Universitat de Barcelona, Barcelona, SpainPalmer’s Rule; Peel’s Law

Contributors and their entries xv

Díaz-Emparanza, Ignacio, Instituto de Economía Aplicada, Universidad del País Vasco-EHU, Bilbao, SpainCochrane–Orcutt procedure

Dolado, Juan J., Universidad Carlos III, Madrid, SpainBonferroni bound; Markov switching autoregressive model

Domenech, Rafael, Universidad de Valencia, Valencia, SpainSolow’s growth model and residual

Echevarría, Cruz Angel, Universidad del País Vasco-EHU, Bilbao, SpainOkun’s law and gap

Escribano, Alvaro, Universidad Carlos III, Madrid, SpainEngle–Granger method; Hodrick–Prescott decomposition

Espasa, Antoni, Universidad Carlos III, Madrid, SpainBox–Jenkins analysis

Espiga, David, La Caixa-S.I. Gestión Global de Riesgos, Barcelona, SpainEdgeworth oligopoly model

Esteban, Joan M., Universitat Autònoma de Barcelona, Barcelona, SpainPigou–Dalton progressive transfers

Estrada, Angel, Banco de España, Madrid, SpainHarrod’s technical progress; Hicks’s technical progress

Etxebarria Zubeldía, Gorka, Deloitte & Touche, Madrid, SpainMontaigne dogma

Fariñas, José C., Universidad Complutense, Madrid, SpainDorfman–Steiner condition

Febrero, Ramón, Universidad Complutense, Madrid, SpainBecker’s time allocation model

Fernández, José L., Universidad Autónoma, Madrid, SpainCauchy–Schwarz inequality; Itô’s lemma

Fernández Delgado, Rogelio, Universidad Rey Juan Carlos, Madrid, SpainPatman effect

Fernández-Macho, F. Javier, Universidad del País Vasco-EHU, Bilbao, SpainSlutsky–Yule effect

Ferreira, Eva, Universidad del País Vasco-EHU, Bilbao, SpainBlack–Scholes model; Pareto distribution; Sharpe’s ratio

Flores Parra, Jordi, Servicio de Estudios de Caja Madrid, Madrid, Spain and UniversidadCarlos III, Madrid, SpainSamuelson’s condition

Franco, Yanna G., Universidad Complutense, Madrid, SpainCairnes–Haberler model; Ricardo–Viner model

xvi Contributors and their entries

Freire Rubio, Mª Teresa, Escuela Superior de Gestión Comercial y Marketing, Madrid,SpainLange–Lerner mechanism

Freixas, Xavier, Universitat Pompeu Fabra, Barcelona, Spain and CEPRFriedman-Savage hypothesis

Frutos de, M. Angeles, Universidad Carlos III, Madrid, SpainHotelling’s model of spatial competition

Fuente de la, Angel, Universitat Autònoma de Barcelona, Barcelona, SpainSwan’s model

Gallastegui, Carmen, Universidad del País Vasco-EHU, Bilbao, SpainPhillip’s curve

Gallego, Elena, Universidad Complutense, Madrid, SpainRobinson-Metzler condition

García, Jaume, Universitat Pompeu Fabra, Barcelona, SpainHeckman’s two-step method

García-Bermejo, Juan C., Universidad Autónoma, Madrid, SpainHarsanyi’s equiprobability model

García-Jurado, Ignacio, Universidad de Santiago de Compostela, Santiago de Compostela,A Coruña, SpainSelten paradox

García Ferrer, Antonio, Universidad Autónoma, Madrid, SpainZellner estimator

García Lapresta, José Luis, Universidad de Valladolid, Valladolid, SpainBolean algebras; Taylor’s theorem

García Pérez, José Ignacio, Fundación CENTRA, Sevilla, SpainScitovsky’s compensation criterion

García-Ruiz, José L., Universidad Complutense, Madrid, SpainHarris–Todaro model; Prebisch–Singer hypothesis

Gimeno, Juan A., Universidad Nacional de Educación a Distancia, Madrid, SpainPeacock–Wiseman’s displacement effect; Wagner’s law

Girón, F. Javier, Universidad de Málaga, Málaga, SpainGauss–Markov theorem

Gómez Rivas, Léon, Universidad Europea, Madrid, SpainLongfield’s paradox

Graffe, Fritz, Universidad del País Vasco-EHU, Bilbao, SpainLeontief model

Grifell-Tatjé, E., Universitat Autònoma de Barcelona, Barcelona, SpainFarrell’s technical efficiency measurement

Contributors and their entries xvii

Guisán, M. Cármen, Universidad de Santiago de Compostela, Santiago de Compostela, ACoruña, SpainChow’s test; Granger’s causality test

Herce, José A., Universidad Complutense, Madrid, SpainCass–Koopmans criterion; Koopmans’s efficiency criterion

Herguera, Iñigo, Universidad Complutense, Madrid, SpainGorman’s polar form

Hernández Andreu, Juan, Universidad Complutense, Madrid, SpainJuglar cycle; Kitchin cycle; Kondratieff long waves

Herrero, Cármen, Universidad de Alicante, Alicante, SpainPerron–Frobenius theorem

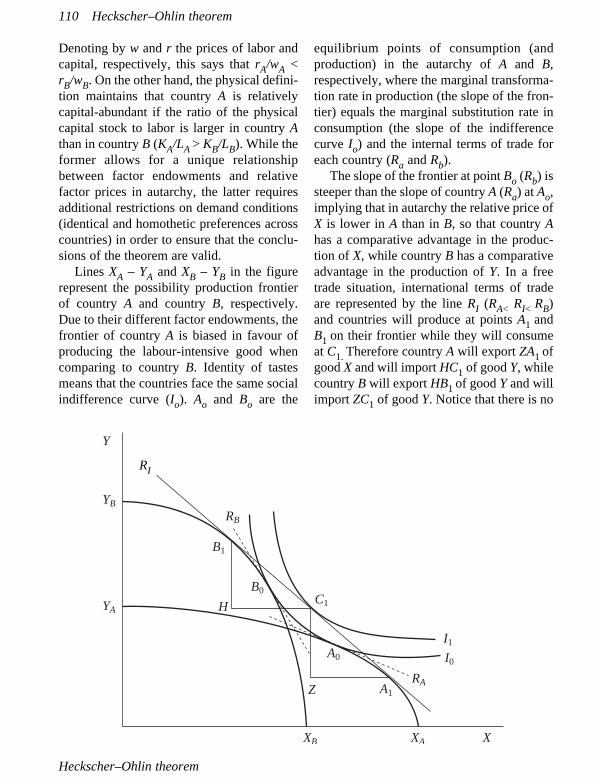

Herrero, Teresa, Confederación Española de Cajas de Ahorro, Madrid, SpainHeckscher–Ohlin theorem; Rybczynski theorem

Hervés-Beloso, Carlos, Universidad de Vigo, Vigo, Pontevedra, SpainSard’s theorem

Hoyo, Juan del, Universidad Autónoma, Madrid, SpainBox–Cox transformation

Huergo, Elena, Universidad Complutense, Madrid, SpainStackelberg’s oligopoly model

Huerta de Soto, Jesús, Universidad Rey Juan Carlos, Madrid, SpainRicardo effect

Ibarrola, Pilar, Universidad Complutense, Madrid, SpainLjung–Box statistics

Iglesia, Jesús de la, Universidad Complutense, Madrid, SpainTocqueville’s cross

de la Iglesia Villasol, Mª Covadonga, Universidad Complutense, Madrid, SpainHotelling’s theorem

Iñarra, Elena, Universidad deli País Vasco-EHU, Bilbao, Spainvon Neumann–Morgenstern stable set

Induraín, Esteban, Universidad Pública de Navarra, Pamplona, SpainHawkins–Simon theorem; Weierstrass extreme value theorem

Jimeno, Juan F., Universidad de Alcalá de Henares, Alcalá de Henares, Madrid, SpainRamsey model and rule

Justel, Ana, Universidad Autónoma, Madrid, SpainGibbs sampling

Lafuente, Alberto, Universidad de Zaragoza, Zaragoza, SpainHerfindahl–Hirschman index

xviii Contributors and their entries

Lasheras, Miguel A., Grupo CIM, Madrid, SpainBaumol’s contestable markets; Ramsey’s inverse elasticity rule

Llobet, Gerard, CEMFI, Madrid, SpainBertrand competition model; Cournot’s oligopoly model

Llombart, Vicent, Universidad de Valencia, Valencia, SpainTurgot–Smith theorem

Llorente Alvarez, J. Guillermo, Universidad Autónoma, Madrid, SpainSchwarz criterion

López, Salvador, Universitat Autònoma de Barcelona, Barcelona, SpainAverch–Johnson effect

López Laborda, Julio, Universidad de Zaragoza, Zaragoza, SpainKakwani index

Lorences, Joaquín, Universidad de Oviedo, Oviedo, SpainCobb–Douglas function

Loscos Fernández, Javier, Universidad Complutense, Madrid, SpainHansen–Perloff effect

Lovell, C.A.K., The University of Georgia, Georgia, USAFarrell’s technical efficiency measurement

Lozano Vivas, Ana, Universidad de Málaga, Málaga, SpainWalras’s law

Lucena, Maurici, CDTI, Madrid, SpainLaffer’s curve; Tobin’s tax

Macho-Stadler, Inés, Universitat Autònoma de Barcelona, Barcelona, SpainAkerlof’s ‘lemons’

Malo de Molina, José Luis, Banco de España, Madrid, SpainFriedman’s rule for monetary policy

Manresa, Antonio, Universitat de Barcelona, Barcelona, SpainBergson’s social indifference curve

Maravall, Agustín, Banco de España, Madrid, SpainKalman filter

Marhuenda, Francisco, Universidad Carlos III, Madrid, SpainHamiltonian function and Hamilton–Jacobi equations; Lyapunov stability

Martín, Carmela, Universidad Complutense, Madrid, SpainArrow’s learning by doing

Martín Marcos, Ana, Universidad Nacional de Educación de Distancia, Madrid, SpainScitovsky’s community indifference curve

Martín Martín, Victoriano, Universidad Rey Juan Carlos, Madrid, SpainBuridan’s ass; Occam’s razor

Contributors and their entries xix

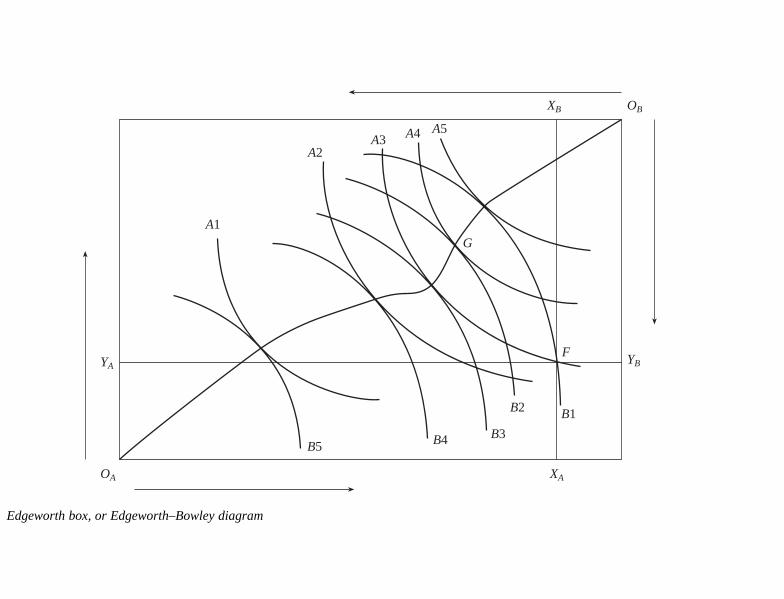

Martín-Román, Angel, Universidad de Valladolid, Segovia, SpainEdgeworth box

Martínez, Diego, Fundación CENTRA, Sevilla, SpainLindahl–Samuelson public goods

Martinez Giralt, Xavier, Universitat Autònoma de Barcelona, Barcelona, SpainSchmeidler’s lemma; Sperner’s lemma

Martínez-Legaz, Juan E., Universitat Autònoma de Barcelona, Barcelona, SpainLagrange multipliers; Banach’s contractive mapping principle

Martínez Parera, Montserrat, Servicio de Estudios del BBVA, Madrid, SpainFisher effect

Martínez Turégano, David, AFI, Madrid, SpainBowley’s law

Mas-Colell, Andreu, Universitat Pompeu Fabra, Barcelona, SpainArrow–Debreu general equilibrium model

Mazón, Cristina, Universidad Complutense, Madrid, SpainRoy’s identity; Shephard’s lemma

Méndez-Ibisate, Fernando, Universidad Complutense, Madrid, SpainCantillon effect; Marshall’s symmetallism; Marshall–Lerner condition

Mira, Pedro, CEMFI, Madrid, SpainCauchy distribution; Sargan test

Molina, José Alberto, Universidad de Zaragoza, Zaragoza, SpainLancaster’s characteristics

Monasterio, Carlos, Universidad de Oviedo, Oviedo, SpainWicksell’s benefit principle for the distribution of tax burden

Morán, Manuel, Universidad Complutense, Madrid, SpainEuclidean spaces; Hessian matrix and determinant

Moreira dos Santos, Pedro, Universidad Complutense, Madrid, SpainGresham’s law in politics

Moreno, Diego, Universidad Carlos III, Madrid, SpainGibbard–Satterthwaite theorem

Moreno García, Emma, Universidad de Salamanca, Salamanca, SpainMinkowski’s theorem

Moreno Martín, Lourdes, Universidad Complutense, Madrid, SpainChamberlin’s oligopoly model

Mulas Granados, Carlos, Universidad Complutense, Madrid, SpainLedyard–Clark–Groves mechanism

Naveira, Manuel, BBVA, Madrid, SpainGibrat’s law; Marshall’s external economies

xx Contributors and their entries

Novales, Alfonso, Universidad Complutense, Madrid, SpainRadner’s turnpike property

Núñez, Carmelo, Universidad Carlos III, Madrid, SpainLebesgue’s measure and integral

Núñez, José J., Universitat Autònoma de Barcelona, Barcelona, SpainMarkov chain model; Poisson process

Núñez, Oliver, Universidad Carlos III, Madrid, SpainKolmogorov’s large numbers law; Wiener process

Olcina, Gonzalo, Universidad de Valencia, Valencia, SpainRubinstein’s model

Ontiveros, Emilio, AFI, Madrid, SpainDíaz–Alejandro effect; Tanzi-Olivera effect

Ortiz-Villajos, José M., Universidad Complutense, Madrid, SpainKaldor paradox; Kaldor’s growth laws; Ricardo’s comparative costs; Verdoorn’s law

Padilla, Jorge Atilano, Nera and CEPRAreeda–Turner predation rule; Coase conjecture

Pardo, Leandro, Universidad Complutense, Madrid, SpainPearson’s chi-squared statistic; Rao–Blackwell’s theorem

Pascual, Jordi, Universitat de Barcelona, Barcelona, SpainBabbage’s principle; Bagehot’s principle

Pazó, Consuelo, Universidad de Vigo, Vigo, Pontevedra, SpainDixit–Stiglitz monopolistic competition model

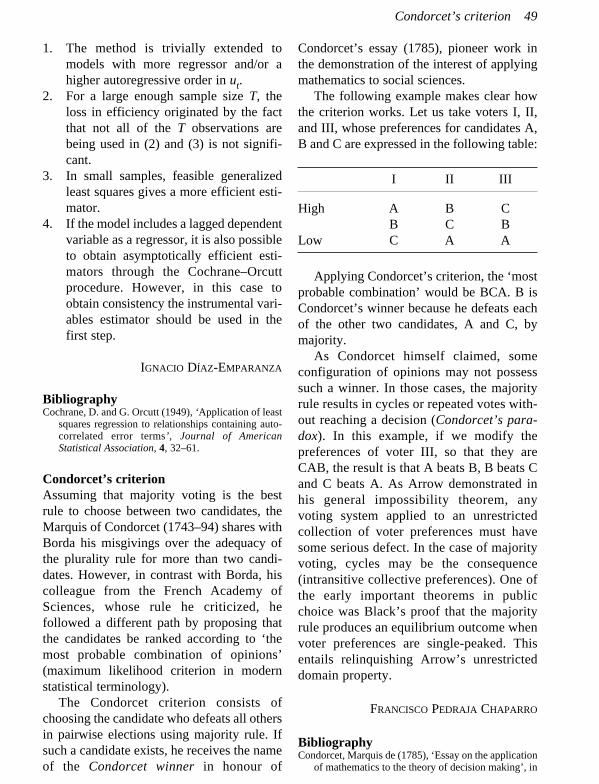

Pedraja Chaparro, Francisco, Universidad de Extremadura, Badajoz, SpainBorda’s rule; Condorcet’s criterion

Peña, Daniel, Universidad Carlos III, Madrid, SpainBayes’s theorem

Pena Trapero, J.B., Universidad de Alcalá de Henares, Alcalá de Henares, Madrid, SpainBeveridge–Nelson decomposition

Perdices de Blas, Luis, Universidad Complutense, Madrid, SpainBecher’s principle; Davenant–King law of demand

Pérez Quirós, Gabriel, Banco de España, Madrid, SpainSuits index

Pérez Villareal, J., Universidad de Cantabria, Santander, SpainHaavelmo balanced budget theorem

Pérez-Castrillo, David, Universidad Autònoma de Barcelona, Barcelona, SpainVickrey auction

Pires Jiménez, Luis Eduardo, Universidad Rey Juan Carlos, Madrid, SpainGibson paradox

Contributors and their entries xxi

Polo, Clemente, Universitat Autònoma de Barcelona, Barcelona, SpainLancaster–Lipsey’s second best

Poncela, Pilar, Universidad Autónoma, Madrid, SpainJohansen’s procedure

Pons, Aleix, CEMFI, Madrid, SpainGraham’s demand

Ponsati, Clara, Institut d’Anàlisi Econòmica, CSIC, Barcelona, SpainKalai–Smorodinsky bargaining solution

Prat, Albert, Universidad Politécnica de Cataluña, Barcelona, SpainHotelling’s T2 statistics; Student t-distribution

Prieto, Francisco Javier, Universidad Carlos III, Madrid, SpainNewton–Raphson method; Pontryagin’s maximum principle

Puch, Luis A., Universidad Complutense, Madrid, SpainChipman–Moore–Samuelson compensation criterion; Hicks compensation criterion; Kaldorcompensation criterion

Puig, Pedro, Universitat Autònoma de Barcelona, Barcelona, SpainPoisson’s distribution

Quesada Paloma, Vicente, Universidad Complutense, Madrid, SpainEdgeworth expansion

Ramos Gorostiza, José Luis, Universidad Complutense, Madrid, SpainFaustmann–Ohlin theorem

Reeder, John, Universidad Complutense, Madrid, SpainAdam Smith problem; Adam Smith’s invisible hand

Regúlez Castillo, Marta, Universidad del País Vasco-EHU, Bilbao, SpainHausman’s test

Repullo, Rafael, CEMFI, Madrid, SpainPareto efficiency; Sonnenschein–Mantel–Debreu theorem

Restoy, Fernando, Banco de España, Madrid, SpainRicardian equivalence

Rey, José Manuel, Universidad Complutense, Madrid, SpainNegishi’s stability without recontracting

Ricoy, Carlos J., Universidad de Santiago de Compostela, Santiago de Compostela, ACoruña, SpainWicksell effect

Rodero-Cosano, Javier, Fundación CENTRA, Sevilla, SpainMyerson revelation principle

Rodrigo Fernández, Antonio, Universidad Complutense, Madrid, SpainArrow–Pratt’s measure of risk aversion

xxii Contributors and their entries

Rodríguez Braun, Carlos, Universidad Complutense, Madrid, SpainClark–Fisher hypothesis; Genberg-Zecher criterion; Hume’s fork; Kelvin’s dictum; Moore’slaw; Spencer’s law; Stigler’s law of eponymy; Wieser’s law

Rodríguez Romero, Luis, Universidad Carlos III, Madrid, SpainEngel curve

Rodríguez-Gutíerrez, Cesar, Universidad de Oviedo, Oviedo, SpainLaspeyres index; Paasche index

Rojo, Luis Ángel, Universidad Complutense, Madrid, SpainKeynes’s demand for money

Romera, Rosario, Universidad Carlos III, Madrid, SpainWiener–Khintchine theorem

Rosado, Ana, Universidad Complutense, Madrid, SpainTinbergen’s rule

Rosés, Joan R., Universitat Pompeu Fabra, Barcelona, Spain and Universidad Carlos III,Madrid, SpainGerschenkron’s growth hypothesis; Kuznets’s curve; Kuznets’s swings

Ruíz Huerta, Jesús, Universidad Rey Juan Carlos, Madrid, SpainEdgeworth taxation paradox

Salas, Rafael, Universidad Complutense, Madrid, SpainGini’s coefficient; Lorenz’s curve

Salas, Vicente, Universidad de Zaragoza, Zaragoza, SpainModigliani–Miller theorem; Tobin’s q

San Emeterio Martín, Nieves, Universidad Rey Juan Carlos, Madrid, SpainLauderdale’s paradox

San Julián, Javier, Universitat de Barcelona, Barcelona, SpainGraham’s paradox; Sargant effect

Sánchez, Ismael, Universidad Carlos III, Madrid, SpainNeyman–Pearson test

Sánchez Chóliz, Julio, Universidad de Zaragoza, Zaragoza, SpainSraffa’s model

Sánchez Hormigo, Alfonso, Universidad de Zaragoza, Zaragoza, SpainKeynes’s plan

Sánchez Maldonado, José, Universidad de Málaga, Málaga, SpainMusgrave’s three branches of the budget

Sancho, Amparo, Universidad de Valencia, Valencia, SpainJarque–Bera test

Santacoloma, Jon, Universidad de Deusto, Bilbao, SpainDuesenberry demonstration effect

Contributors and their entries xxiii

Santos-Redondo, Manuel, Universidad Complutense, Madrid, SpainSchumpeterian entrepeneur; Schumpeter’s vision; Veblen effect good

Sanz, José F., Instituto de Estudios Fiscales, Ministerio de Hacienda, Madrid, SpainFullerton-King’s effective marginal tax rate

Sastre, Mercedes, Universidad Complutense, Madrid, SpainReynolds–Smolensky index

Satorra, Albert, Universitat Pompeu Fabra, Barcelona, SpainWald test

Saurina Salas, Jesús, Banco de España, Madrid, SpainBernoulli’s paradox

Schwartz, Pedro, Universidad San Pablo CEU, Madrid, SpainSay’s law

Sebastián, Carlos, Universidad Complutense, Madrid, SpainMuth’s rational expectations

Sebastián, Miguel, Universidad Complutense, Madrid, SpainMundell–Fleming model

Segura, Julio, Universidad Complutense, Madrid, SpainBaumol–Tobin transactions demand for cash; Hicksian perfect stability; LeChatelier principle; Marshall’s stability; Shapley–Folkman theorem; Snedecor F-distribution

Senra, Eva, Universidad Carlos III, Madrid, SpainWold’s decomposition

Sosvilla-Rivero, Simón, Universidad Complutense, Madrid, Spain and FEDEA, Madrid,SpainDickey–Fuller test; Phillips–Perron test

Suarez, Javier, CEMFI, Madrid, Spainvon Neumann–Morgenstern expected utility theorem

Suriñach, Jordi, Universitat de Barcelona, Barcelona, SpainAitken’s theorem; Durbin–Watson statistics

Teixeira, José Francisco, Universidad de Vigo, Vigo, Pontevedra, SpainWicksell’s cumulative process

Torres, Xavier, Banco de España, Madrid, SpainHicksian demand; Marshallian demand

Tortella, Gabriel, Universidad de Alcalá de Henares, Alcalá de Henares, Madrid, SpainRostow’s model

Trincado, Estrella, Universidad Complutense, Madrid, SpainHume’s law; Ricardian vice

Urbano Salvador, Amparo, Universidad de Valencia, Valencia, SpainBayesian–Nash equilibrium

xxiv Contributors and their entries

Urbanos Garrido, Rosa María, Universidad Complutense, Madrid, SpainWilliams’s fair innings argument

Valenciano, Federico, Universidad del País Vasco-EHU, Bilbao, SpainNash bargaining solution

Vallés, Javier, Banco de España, Madrid, SpainGiffen goods

Varela, Juán, Ministerio de Hacienda, Madrid, SpainJones’s magnification effect

Vázquez, Jesús, Universidad del País Vasco-EHU, Bilbao, SpainCagan’s hyperinflation model

Vázquez Furelos, Mercedes, Universidad Complutense, Madrid, SpainLyapunov’s central limit theorem

Vega, Juan, Universidad de Extremadura, Badajoz, SpainHarberger’s triangle

Vega-Redondo, Fernando, Universidad de Alicante, Alicante, SpainNash equilibrium

Vegara, David, Ministerio de Economià y Hacienda, Madrid, SpainGoodhart’s law; Taylor rule

Vegara-Carrió, Josep Ma, Universitat Autònoma de Barcelona, Barcelona, Spainvon Neumann’s growth model; Pasinetti’s paradox

Villagarcía, Teresa, Universidad Carlos III, Madrid, SpainWeibull distribution

Viñals, José, Banco de España, Madrid, SpainBalassa–Samuelson effect

Zaratiegui, Jesús M., Universidad de Navarra, Pamplona, SpainThünen’s formula

Zarzuelo, José Manuel, Universidad del País Vasco-EHU, Bilbao, SpainKuhn–Tucker theorem; Shapley value

Zubiri, Ignacio, Universidad del País Vasco-EHU, Bilbao, SpainTheil index

Contributors and their entries xxv

Preface

Robert K. Merton defined eponymy as ‘the practice of affixing the name of the scientist to allor part of what he has found’. Eponymy has fascinating features and can be approached fromseveral different angles, but only a few attempts have been made to tackle the subject lexico-graphically in science and art, and the present is the first Eponymous Dictionary ofEconomics.

The reader must be warned that this is a modest book, aiming at helpfulness more thanerudition. We realized that economics has expanded in this sense too: there are hundreds ofeponyms, and the average economist will probably be acquainted with, let alone be able tomaster, just a number of them. This is the void that the Dictionary is expected to fill, and ina manageable volume: delving into the problems of the sociology of science, dispelling allMertonian multiple discoveries, and tracing the origins, on so many occasions spurious, ofeach eponym (cf. ‘Stigler’s Law of Eponymy’ infra), would have meant editing another book,or rather books.

A dictionary is by definition not complete, and arguably not completable. Perhaps this iseven more so in our case. We fancy that we have listed most of the economic eponyms, andalso some non-economic, albeit used in our profession, but we are aware of the risk of includ-ing non-material or rare entries; in these cases we have tried to select interesting eponyms, oreponyms coined by or referring to interesting thinkers. We hope that the reader will spot fewmistakes in the opposite sense; that is, the exclusion of important and widely used eponyms.

The selection has been especially hard in mathematics and econometrics, much moreeponymy-prone than any other field connected with economics. The low risk-aversion readerwho wishes to uphold the conjecture that eponymy has numerically something to do withscientific relevance will find that the number of eponyms tends to dwindle after the 1960s;whether this means that seminal results have dwindled too is a highly debatable and, owingto the critical time dimension of eponymy, a likely unanswerable question.

In any case, we hasten to invite criticisms and suggestions in order to improve eventualfuture editions of the dictionary (please find below our e-mail addresses for contacts).

We would like particularly to thank all the contributors, and also other colleagues that havehelped us: Emilio Albi, José María Capapé, Toni Espasa, María del Carmen Gallastegui,Cecilia Garcés, Carlos Hervés, Elena Iñarra, Emilio Lamo de Espinosa, Jaime de Salas,Rafael Salas, Vicente Salas Fumás, Cristóbal Torres and Juan Urrutia. We are grateful for thehelp received from Edward Elgar’s staff in all the stages of the book, and especially for BobPickens’ outstanding job as editor.

Madrid, December 2003J.S. [[email protected]]

C.R.B. [[email protected]]

xxvii

Mathematical notation

A vector is usually denoted by a lower case italic letter such as x or y, and sometimes is repre-sented with an arrow on top of the letter such as x→ or y→. Sometimes a vector is described byenumeration of its elements; in these cases subscripts are used to denote individual elementsof a vector and superscripts to denote a specific one: x = (x1, . . ., xn) means a generic n-dimensional vector and x0 = (x0

1, . . ., x0n) a specific n-dimensional vector. As it is usual, x >>

y means xi > yi (i = 1, . . ., n) and x > y means xi ≥ yi for all i and, for at least one i, xi > yi.A set is denoted by a capital italic letter such as X or Y. If a set is defined by some prop-

erty of its members, it is written with brackets which contain in the first place the typicalelement followed by a vertical line and the property: X = (x/x >> 0) is the set of vectors x withpositive elements. In particular, R is the set of real numbers, R+ the set of non-negative realnumbers, R++ the set of positive real numbers and a superscript denotes the dimension of theset. Rn

+ is the set of n-dimensional vectors whose elements are all real non-negative numbers.Matrices are denoted by capital italic letters such as A or B, or by squared brackets

surrounding their typical element [aij] or [bij]. When necessary, A(qxm) indicates that matrixA has q rows and m columns (is of order qxm).

In equations systems expressed in matricial form it is supposed that dimensions of matri-ces and vectors are the right ones, therefore we do not use transposition symbols. For exam-ple, in the system y = Ax + u, with A(nxn), all the three vectors must have n rows and 1 columnbut they are represented ini the text as y = (y1, . . ., yn), x = (x1, . . ., xn) and u = (u1, . . ., un).The only exceptions are when expressing a quadratic form such as xAx� or a matricial prod-uct such as (X� X)–1.

The remaining notation is the standard use for mathematics, and when more specific nota-tion is used it is explained in the text.

xxviii

Adam Smith problemIn the third quarter of the nineteenth century,a series of economists writing in German(Karl Knies, 1853, Lujo Brentano, 1877 andthe Polish aristocrat Witold von Skarzynski,1878) put forward a hypothesis known as theUmschwungstheorie. This suggested thatAdam Smith’s ideas had undergone a turn-around between the publication of his philo-sophical work, the Theory of Moral Senti-ments in 1759 and the writing of the Wealth ofNations, a turnaround (umschwung) whichhad resulted in the theory of sympathy set outin the first work being replaced by a new‘selfish’ approach in his later economicstudy. Knies, Brentano and Skarzynskiargued that this turnaround was to be attrib-uted to the influence of French materialistthinkers, above all Helvétius, with whomSmith had come into contact during his longstay in France (1763–66). Smith was some-thing of a bête noire for the new Germannationalist economists: previously anti-freetrade German economists from List toHildebrand, defenders of Nationalökonomie,had attacked Smith (and smithianismus) asan unoriginal prophet of free trade orthodox-ies, which constituted in reality a defence ofBritish industrial supremacy.

Thus was born what came to be calledDas Adam Smith Problem, in its moresophisticated version, the idea that the theoryof sympathy set out in the Theory of MoralSentiments is in some way incompatible withthe self-interested, profit-maximizing ethicwhich supposedly underlies the Wealth ofNations. Since then there have been repeateddenials of this incompatibility, on the part ofupholders of the consistency thesis, such asAugustus Oncken in 1897 and the majorityof twentieth-century interpreters of Smith’s

work. More recent readings maintain that theAdam Smith problem is a false one, hingeingon a misinterpretation of such key terms as‘selfishness’ and ‘self-interest’, that is, thatself-interest is not the same as selfishnessand does not exclude the possibility of altru-istic behaviour. Nagging doubts, however,resurface from time to time – Viner, forexample, expressed in 1927 the view that‘there are divergences between them [MoralSentiments and Wealth of Nations] which areimpossible of reconciliation’ – and althoughthe Umschwungstheorie is highly implaus-ible, one cannot fail to be impressed by thedifferences in tone and emphasis between thetwo books.

JOHN REEDER

BibliographyMontes, Leonidas (2003), ‘Das Adam Smith Problem:

its origins, the stages of the current debate and oneimplication for our understanding of sympathy’,Journal of the History of Economic Thought, 25 (1),63–90.

Nieli, Russell (1986), ‘Spheres of intimacy and theAdam Smith problem’, Journal of the History ofIdeas, 47 (4), 611–24.

Adam Smith’s invisible handOn three separate occasions in his writings,Adam Smith uses the metaphor of the invis-ible hand, twice to describe how a sponta-neously evolved institution, the competitivemarket, both coordinates the various interestsof the individual economic agents who go tomake up society and allocates optimally thedifferent resources in the economy.

The first use of the metaphor by Smith,however, does not refer to the market mech-anism. It occurs in the context of Smith’searly unfinished philosophical essay on TheHistory of Astronomy (1795, III.2, p. 49) in a

1

A

discussion of the origins of polytheism: ‘inall Polytheistic religions, among savages, aswell as in the early ages of Heathen antiquity,it is the irregular events of nature only thatare ascribed to the agency and power of theirgods. Fire burns, and water refreshes; heavybodies descend and lighter substances flyupwards, by the necessity of their ownnature; nor was the invisible hand of Jupiterever apprehended to be employed in thosematters’.

The second reference to the invisible handis to be found in Smith’s major philosophicalwork, The Theory of Moral Sentiments(1759, IV.i.10, p. 184), where, in a passageredolent of a philosopher’s distaste forconsumerism, Smith stresses the unintendedconsequences of human actions:

The produce of the soil maintains at all timesnearly that number of inhabitants which it iscapable of maintaining. The rich only selectfrom the heap what is most precious and agree-able. They consume little more than the poor,and in spite of their natural selfishness andrapacity, though they mean only their ownconveniency, though the sole end which theypropose from the labours of all the thousandswhom they employ, be the gratification oftheir own vain and insatiable desires, theydivide with the poor the produce of all theirimprovements. They are led by an invisiblehand to make nearly the same distribution ofthe necessaries of life, which would have beenmade, had the earth been divided into equalportions among all its inhabitants, and thuswithout intending it, without knowing it,advance the interests of the society, and affordmeans to the multiplication of the species.

Finally, in the Wealth of Nations (1776,IV.ii.9, p. 456), Smith returns to his invisiblehand metaphor to describe explicitly how themarket mechanism recycles the pursuit ofindividual self-interest to the benefit of soci-ety as a whole, and en passant expresses adeep-rooted scepticism concerning thosepeople (generally not merchants) who affectto ‘trade for the publick good’:

As every individual, therefore, endeavours asmuch as he can both to employ his capital inthe support of domestick industry, and so todirect that industry that its produce may be ofthe greatest value; every individual necessarilylabours to render the annual revenue of thesociety as great as he can. He generally,indeed, neither intends to promote the publickinterest, nor knows how much he is promotingit. . . . by directing that industry in such amanner as its produce may be of the greatestvalue, he intends only his own gain, and he isin this, as in many other cases, led by an invis-ible hand to promote an end which was no partof his intention. Nor is it always the worse forthe society that it was no part of it. By pursu-ing his own interest he frequently promotesthat of the society more effectually than whenhe really intends to promote it. I have neverknown much good done by those who affect totrade for the publick good. It is an affectation,indeed, not very common among merchants,and very few words need be employed indissuading them from it.

More recently, interest in Adam Smith’sinvisible hand metaphor has enjoyed arevival, thanks in part to the resurfacing ofphilosophical problems concerning the unin-tended social outcomes of conscious andintentional human actions as discussed, forexample, in the works of Karl Popper andFriedrich von Hayek, and in part to the fasci-nation with the concept of the competitivemarket as the most efficient means of allo-cating resources expressed by a new genera-tion of free-market economists.

JOHN REEDER

BibliographyMacfie, A.L. (1971), ‘The invisible hand of Jupiter’,

Journal of the History of Ideas, 32 (4), 593–9.Smith, Adam (1759), The Theory of Moral Sentiments,

reprinted in D.D. Raphael and A.L. Macfie (eds)(1982), The Glasgow Edition of the Works andCorrespondence of Adam Smith, Indianapolis:Liberty Classics.

Smith, Adam (1776), An Inquiry into the Nature andCauses of the Wealth of Nations, reprinted in W.B.Todd (ed.) (1981), The Glasgow Edition of theWorks and Correspondence of Adam Smith,Indianapolis: Liberty Classics.

2 Adam Smith’s invisible hand

Smith, Adam (1795), Essays on Philosophical Subjects,reprinted in W.P.D. Wightman and J.C. Bryce (eds)(1982), The Glasgow Edition of the Works andCorrespondence of Adam Smith, Indianapolis:Liberty Classics.

Aitken’s theoremNamed after New Zealander mathematicianAlexander Craig Aitken (1895–1967), thetheorem that shows that the method thatprovides estimators that are efficient as wellas linear and unbiased (that is, of all themethods that provide linear unbiased estima-tors, the one that presents the least variance)when the disturbance term of the regressionmodel is non-spherical, is a generalized leastsquares estimation (GLSE). This theoryconsiders as a particular case the Gauss–Markov theorem for the case of regressionmodels with spherical disturbance term andis derived from the definition of a linearunbiased estimator other than that providedby GLSE (b = ((X�WX)–1 X�W–1 + C)Y, Cbeing a matrix with (at least) one of itselements other than zero) and demonstratesthat its variance is given by VAR(b) =VAR(b flGLSE) + s2CWC�, where s2CWC� is apositive defined matrix, and therefore thatthe variances of the b estimators are greaterthan those of the b flGLSE estimators.

JORDI SURINACH

BibliographyAitken, A. (1935), ‘On least squares and linear combi-

nations of observations’, Proceedings of the RoyalStatistical Society, 55, 42–8.

See also: Gauss–Markov theorem.

Akerlof’s ‘lemons’George A. Akerlof (b.1940) got his B.A. atYale University, graduated at MIT in 1966and obtained an assistant professorship atUniversity of California at Berkeley. In hisfirst year at Berkeley he wrote the ‘Marketfor “lemons” ’, the work for which he wascited for the Nobel Prize that he obtained in

2001 (jointly with A. Michael Spence andJoseph E. Stiglitz). His main research interesthas been (and still is) the consequences formacroeconomic problems of different micro-economic structures such as asymmetricinformation or staggered contracts. Recentlyhe has been working on the effects of differ-ent assumptions regarding fairness and socialcustoms on unemployment.

The used car market captures the essenceof the ‘Market for “lemons” ’ problem. Carscan be good or bad. When a person buys anew car, he/she has an expectation regardingits quality. After using the car for a certaintime, the owner has more accurate informa-tion on its quality. Owners of bad cars(‘lemons’) will tend to replace them, whilethe owners of good cars will more often keepthem (this is an argument similar to the oneunderlying the statement: bad money drivesout the good). In addition, in the second-handmarket, all sellers will claim that the car theysell is of good quality, while the buyerscannot distinguish good from bad second-hand cars. Hence the price of cars will reflecttheir expected quality (the average quality) inthe second-hand market. However, at thisprice high-quality cars would be underpricedand the seller might prefer not to sell. Thisleads to the fact that only lemons will betraded.

In this paper Akerlof demonstrates howadverse selection problems may arise whensellers have more information than buyersabout the quality of the product. When thecontract includes a single parameter (theprice) the problem cannot be avoided andmarkets cannot work. Many goods may notbe traded. In order to address an adverseselection problem (to separate the good fromthe bad quality items) it is necessary to addingredients to the contract. For example, theinclusion of guarantees or certifications onthe quality may reduce the informationalproblem in the second-hand cars market.

The approach pioneered by Akerlof has

Akerlof’s ‘lemons’ 3

been extensively applied to the study ofmany other economic subjects such as finan-cial markets (how asymmetric informationbetween borrowers and lenders may explainvery high borrowing rates), public econom-ics (the difficulty for the elderly of contract-ing private medical insurance), laboreconomics (the discrimination of minorities)and so on.

INÉS MACHO-STADLER

BibliographyAkerlof, G.A. (1970), ‘The market for “lemons”: quality

uncertainty and the market mechanism’, QuarterlyJournal of Economics, 89, 488–500.

Allais paradoxOne of the axioms underlying expected util-ity theory requires that, if A is preferred to B,a lottery assigning a probability p to winningA and (1 – p) to C will be preferred to anotherlottery assigning probability p to B and (1 –p) to C, irrespective of what C is. The Allaisparadox, due to French economist MauriceAllais (1911–2001, Nobel Prize 1988) chal-lenges this axiom.

Given a choice between one million euroand a gamble offering a 10 per cent chance ofreceiving five million, an 89 per cent chanceof obtaining one million and a 1 per centchance of receiving nothing, you are likely topick the former. Nevertheless, you are alsolikely to prefer a lottery offering a 10 percent probability of obtaining five million(and 90 per cent of gaining nothing) toanother with 11 per cent probability ofobtaining one million and 89 per cent ofwinning nothing.

Now write the outcomes of those gamblesas a 4 × 3 table with probabilities 10 per cent,89 per cent and 1 per cent heading eachcolumn and the corresponding prizes in eachrow (that is, 1, 1 and 1; 5, 1 and 0; 5, 0 and0; and 1, 0 and 1, respectively). If the centralcolumn, which plays the role of C, is

dropped, your choices above (as mostpeople’s) are perceptibly inconsistent: if thefirst row was preferred to the second, thefourth should have been preferred to thethird.

For some authors, this paradox illustratesthat agents tend to neglect small reductionsin risk (in the second gamble above, the riskof nothing is only marginally higher in thefirst option) unless they completely eliminateit: in the first option of the first gamble youare offered one million for sure. For others,however, it reveals only a sort of ‘opticalillusion’ without any serious implication foreconomic theory.

JUAN AYUSO

BibliographyAllais, M. (1953), ‘Le Comportement de l’homme

rationnel devant la risque: critique des postulats etaxioms de l’ecole américaine’, Econometrica, 21,269–90.

See also: Ellsberg paradox, von Neumann–Morgenstern expected utility theorem.

Areeda–Turner predation ruleIn 1975, Phillip Areeda (1930–95) andDonald Turner (1921–94), at the time profes-sors at Harvard Law School, published whatnow everybody regards as a seminal paper,‘Predatory pricing and related practicesunder Section 2 of the Sherman Act’. In thatpaper, they provided a rigorous definition ofpredation and considered how to identifyprices that should be condemned under theSherman Act. For Areeda and Turner, preda-tion is ‘the deliberate sacrifice of presentrevenues for the purpose of driving rivals outof the market and then recouping the lossesthrough higher profits earned in the absenceof competition’.

Areeda and Turner advocated the adop-tion of a per se prohibition on pricing belowmarginal costs, and robustly defended thissuggestion against possible alternatives. The

4 Allais paradox

basis of their claim was that companies thatwere maximizing short-run profits would, bydefinition, not be predating. Those compa-nies would not price below marginal cost.Given the difficulties of estimating marginalcosts, Areeda and Turner suggested usingaverage variable costs as a proxy.

The Areeda–Turner rule was quicklyadopted by the US courts as early as 1975, inInternational Air Industries v. AmericanExcelsior Co. The application of the rule haddramatic effects on success rates for plain-tiffs in predatory pricing cases: after thepublication of the article, success ratesdropped to 8 per cent of cases reported,compared to 77 per cent in preceding years.The number of predatory pricing cases alsodropped as a result of the widespread adop-tion of the Areeda–Turner rule by the courts(Bolton et al. 2000).

In Europe, the Areeda–Turner rulebecomes firmly established as a central testfor predation in 1991, in AKZO v.Commission. In this case, the court statedthat prices below average variable costshould be presumed predatory. However thecourt added an important second limb to therule. Areeda and Turner had argued thatprices above marginal cost were higher thanprofit-maximizing ones and so should beconsidered legal, ‘even if they were belowaverage total costs’. The European Court ofJustice (ECJ) took a different view. It foundAKZO guilty of predatory pricing when itsprices were between average variable andaverage total costs. The court emphasized,however, that such prices could only befound predatory if there was independentevidence that they formed part of a plan toexclude rivals, that is, evidence of exclu-sionary intent. This is consistent with theemphasis of Areeda and Turner that preda-tory prices are different from those that thecompany would set if it were maximizingshort-run profits without exclusionaryintent.

The adequacy of average variable costsas a proxy for marginal costs has receivedconsiderable attention (Williamson, 1977;Joskow and Klevorick, 1979). In 1996,William Baumol made a decisive contribu-tion on this subject in a paper in which heagreed that the two measures may be differ-ent, but argued that average variable costswas the more appropriate one. His conclu-sion was based on reformulating theAreeda–Turner rule. The original rule wasbased on identifying prices below profit-maximizing ones. Baumol developedinstead a rule based on whether pricescould exclude equally efficient rivals. Heargued that the rule which implementedthis was to compare prices to average vari-able costs or, more generally, to averageavoidable costs: if a company’s price isabove its average avoidable cost, an equallyefficient rival that remains in the marketwill earn a price per unit that exceeds theaverage costs per unit it would avoid if itceased production.

There has also been debate aboutwhether the price–cost test in theAreeda–Turner rule is sufficient. On the onehand, the United States Supreme Court hasstated in several cases that plaintiffs mustalso demonstrate that the predator has areasonable prospect of recouping the costsof predation through market power after theexit of the prey. This is the so-called‘recoupment test’. In Europe, on the otherhand, the ECJ explicitly rejected the needfor a showing of recoupment in Tetra Pak I(1996 and 1997).

None of these debates, however, over-shadows Areeda and Turner’s achievement.They brought discipline to the legal analysisof predation, and the comparison of priceswith some measure of costs, which theyintroduced, remains the cornerstone of prac-tice on both sides of the Atlantic.

JORGE ATILANO PADILLA

Areeda–Turner predation rule 5

BibliographyAreeda, Phillip and Donald F. Turner (1975), ‘Predatory

pricing and related practices under Section 2 of theSherman Act’, Harvard Law Review, 88, 697–733.

Baumol, William J. (1996), ‘Predation and the logic ofthe average variable cost test’, Journal of Law andEconomics, 39, 49–72.

Bolton, Patrick, Joseph F. Brodley and Michael H.Riordan (2000), ‘Predatory pricing: strategic theoryand legal policy’, Georgetown Law Journal, 88,2239–330.

Joskow, A. and Alvin Klevorick (1979): ‘A frameworkfor analyzing predatory pricing policy’, Yale LawJournal, 89, 213.

Williamson, Oliver (1977), ‘Predatory pricing: a stra-tegic and welfare analysis’, Yale Law Journal, 87,384.

Arrow’s impossibility theoremKenneth J. Arrow (b.1921, Nobel Prize inEconomics 1972) is the author of this cele-brated result which first appeared in ChapterV of Social Choice and Individual Values(1951). Paradoxically, Arrow called itinitially the ‘general possibility theorem’, butit is always referred to as an impossibilitytheorem, given its essentially negative char-acter. The theorem establishes the incompati-bility among several axioms that might besatisfied (or not) by methods to aggregateindividual preferences into social prefer-ences. I will express it in formal terms, andwill then comment on its interpretations andon its impact in the development of econom-ics and other disciplines.

In fact, the best known and most repro-duced version of the theorem is not the one inthe original version, but the one that Arrowformulated in Chapter VIII of the 1963second edition of Social Choice andIndividual Values. This chapter, entitled‘Notes on the theory of social choice’, wasadded to the original text and constitutes theonly change between the two editions. Thereformulation of the theorem was partlyjustified by the simplicity of the new version,and also because Julian Blau (1957) hadpointed out that there was a difficulty withthe expression of the original result.

Both formulations start from the same

formal framework. Consider a society of nagents, which has to express preferencesregarding the alternatives in a set A. Thepreferences of agents are given by complete,reflexive, transitive binary relations on A.Each list of n such relations can be inter-preted as the expression of a state of opinionwithin society. Rules that assign a complete,reflexive, transitive binary relation (a socialpreference) to each admissible state of opin-ion are called ‘social welfare functions’.

Specifically, Arrow proposes a list ofproperties, in the form of axioms, anddiscusses whether or not they may be satis-fied by a social welfare function. In his 1963edition, he puts forward the followingaxioms:

• Universal domain (U): the domain ofthe function must include all possiblecombinations of individual prefer-ences;

• Pareto (P): whenever all agents agreethat an alternative x is better thananother alternative y, at a given state ofopinion, then the corresponding socialpreference must rank x as better than y;

• Independence of irrelevant alternatives(I): the social ordering of any two alter-natives, for any state of opinion, mustonly depend on the ordering of thesetwo alternatives by individuals;

• Non-dictatorship (D): no single agentmust be able to determine the strictsocial preference at all states of opin-ion.

Arrow’s impossibility theorem (1963)tells that, when society faces three or morealternatives, no social welfare function cansimultaneously meet U, P, I and D.

By Arrow’s own account, the need toformulate a result in this vein arose whentrying to answer a candid question, posed by aresearcher at RAND Corporation: does itmake sense to speak about social preferences?

6 Arrow’s impossibility theorem

A first quick answer would be to say that thepreferences of society are those of the major-ity of its members. But this is not goodenough, since the majority relation generatedby a society of n voters may be cyclical, assoon as there are more than two alternatives,and thus different from individual prefer-ences, which are usually assumed to be tran-sitive. The majority rule (which otherwisesatisfies all of Arrow’s requirements), is nota social welfare function, when society facesmore than two alternatives. Arrow’s theoremgeneralizes this remark to any other rule: nosocial welfare function can meet his require-ments, and no aggregation method meetingthem can be a social welfare function.

Indeed, some of the essential assumptionsunderlying the theorem are not explicitlystated as axioms. For example, the requiredtransitivity of the social preference, whichrules out the majority method, is included inthe very definition of a social welfare func-tion. Testing the robustness of Arrow’s the-orem to alternative versions of its implicitand explicit conditions has been a majoractivity of social choice theory for more thanhalf a century. Kelly’s updated bibliographycontains thousands of references inspired byArrow’s impossibility theorem.

The impact of the theorem is due to therichness and variety of its possible interpre-tations, and the consequences it has on eachof its possible readings.

A first interpretation of Arrow’s formalframework is as a representation of votingmethods. Though he was not fully aware of itin 1951, Arrow’s analysis of voting systemsfalls within a centuries-old tradition ofauthors who discussed the properties ofvoting systems, including Plinius the Young,Ramón Llull, Borda, Condorcet, Laplace andDodgson, among others. Arrow added histori-cal notes on some of these authors in his1963 edition, and the interested reader canfind more details on this tradition in McLeanand Urken (1995). Each of these authors

studied and proposed different methods ofvoting, but none of them fully acknowledgedthe pervasive barriers that are so wellexpressed by Arrow’s theorem: that nomethod at all can be perfect, because anypossible one must violate some of the reason-able requirements imposed by the impossi-bility theorem. This changes the perspectivein voting theory: if a voting method must beselected over others, it must be on the meritsand its defects, taken together; none can bepresented as an ideal.

Another important reading of Arrow’stheorem is the object of Chapter IV in hismonograph. Arrow’s framework allows us toput into perspective the debate among econ-omists of the first part of the twentiethcentury, regarding the possibility of a theoryof economic welfare that would be devoid ofinterpersonal comparisons of utility and ofany interpretation of utility as a cardinalmagnitude. Kaldor, Hicks, Scitovsky,Bergson and Samuelson, among other greateconomists of the period, were involved in adiscussion regarding this possibility, whileusing conventional tools of economic analy-sis. Arrow provided a general frameworkwithin which he could identify the sharedvalues of these economists as partial require-ments on the characteristics of a method toaggregate individual preferences into socialorderings. By showing the impossibility ofmeeting all these requirements simultane-ously, Arrow’s theorem provided a newfocus to the controversies: no one was closerto success than anyone else. Everyone waslooking for the impossible. No perfect aggre-gation method was worth looking for, as itdid not exist. Trade-offs between the proper-ties of possible methods had to be the mainconcern.

Arrow’s theorem received immediateattention, both as a methodological criticismof the ‘new welfare economics’ and becauseof its voting theory interpretation. But noteveryone accepted that it was relevant. In

Arrow’s impossibility theorem 7

particular, the condition of independence ofirrelevant alternatives was not easilyaccepted as expressing the desiderata of thenew welfare economics. Even now, it is adebated axiom. Yet Arrow’s theorem hasshown a remarkable robustness over morethan 50 years, and has been a paradigm formany other results regarding the generaldifficulties in aggregating preferences, andthe importance of concentrating on trade-offs, rather than setting absolute standards.

Arrow left some interesting topics out ofhis monograph, including issues of aggrega-tion and mechanism design. He mentioned,but did not elaborate on, the possibility thatvoters might strategically misrepresent theirpreferences. He did not discuss the reasonswhy some alternatives are on the table, andothers are not, at the time a social decisionmust be taken. He did not provide a generalframework where the possibility of usingcardinal information and of performing inter-personal comparisons of utility could beexplicitly discussed. These were routes thatlater authors were to take. But his impossi-bility theorem, in all its specificity, provideda new way to analyze normative issues andestablished a research program for genera-tions.

SALVADOR BARBERÀ

BibliographyArrow, K.J. (1951), Social Choice and Individual

Values, New York: John Wiley; 2nd definitive edn1963.

Blau, Julian H. (1957), ‘The existence of social welfarefunctions’, Econometrica, 25, 302–13.

Kelly, Jerry S., ‘Social choice theory: a bibliography’,http://www.maxwell.syr.edu/maxpages/faculty/jskelly/A.htm.

McLean, Ian and Arnold B. Urken (1995), Classics ofSocial Choice, The University of Michigan Press.

See also: Bergson’s social indifference curve, Borda’srule, Chipman–Moore–Samuelson compensationcriterion, Condorcet’s criterion, Hicks compensationcriterion, Kaldor compensation criterion, Scitovski’scompensation criterion.

Arrow’s learning by doingThis is the key concept in the model developedby Kenneth J. Arrow (b.1921, Nobel Prize1972) in 1962 with the purpose of explainingthe changes in technological knowledge whichunderlie intertemporal and international shiftsin production functions. In this respect, Arrowsuggests that, according to many psycholo-gists, the acquisition of knowledge, what isusually termed ‘learning’, is the product ofexperience (‘doing’). More specifically, headvances the hypothesis that technical changedepends upon experience in the activity ofproduction, which he approaches by cumula-tive gross investment, assuming that new capi-tal goods are better than old ones; that is to say,if we compare a unit of capital goods producedin the time t1 with one produced at time t2, thefirst requires the cooperation of at least asmuch labour as the second, and produces nomore product. Capital equipment comes inunits of equal (infinitesimal) size, and theproductivity achievable using any unit ofequipment depends on how much investmenthad already occurred when this particular unitwas produced.

Arrow’s view is, therefore, that at leastpart of technological progress does notdepend on the passage of time as such, butgrows out of ‘experience’ caught by cumula-tive gross investment; that is, a vehicle forimprovements in skill and technical knowl-edge. His model may be considered as aprecursor to the further new or endogenousgrowth theory. Thus the last paragraph ofArrow’s paper reads as follows: ‘It has beenassumed that learning takes place only as aby-product of ordinary production. In fact,society has created institutions, education andresearch, whose purpose is to enable learningto take place more rapidly. A fuller modelwould take account of these as additionalvariables.’ Indeed, this is precisely what morerecent growth literature has been doing.

CARMELA MARTÍN

8 Arrow’s learning by doing

BibliographyArrow, K.J. (1962), ‘The economics implications of

learning by doing’, Review of Economic Studies, 29(3), 155–73.

Arrow–Debreu general equilibriummodelNamed after K.J. Arrow (b.1921, NobelPrize 1972) and G. Debreu (b. 1921, NobelPrize 1983) the model (1954) constitutes amilestone in the path of formalization andgeneralization of the general equilibriummodel of Léon Walras (see Arrow and Hahn,1971, for both models). An aspect which ischaracteristic of the contribution of Arrow–Debreu is the introduction of the concept ofcontingent commodity.

The fundamentals of Walras’s generalequilibrium theory (McKenzie, 2002) areconsumers, consumers’ preferences andresources, and the technologies available tosociety. From this the theory offers anaccount of firms and of the allocation, bymeans of markets, of consumers’ resourcesamong firms and of final produced commod-ities among consumers.

Every Walrasian model distinguishesitself by a basic parametric prices hypothe-sis: ‘Prices are fixed parameters for everyindividual, consumer or firm decision prob-lem.’ That is, the terms of trade amongcommodities are taken as fixed by everyindividual decision maker (‘absence ofmonopoly power’). There is a variety ofcircumstances that justify the hypothesis,perhaps approximately: (a) every individualdecision maker is an insignificant part of theoverall market, (b) some trader – an auction-eer, a possible entrant, a regulator – guaran-tees by its potential actions the terms oftrade in the market.

The Arrow–Debreu model emphasizes asecond, market completeness, hypothesis:‘There is a market, hence a price, for everyconceivable commodity.’ In particular, thisholds for contingent commodities, promising

to deliver amounts of a (physical) good if acertain state of the world occurs. Of course,for this to be possible, information has to be‘symmetric’. The complete markets hypothe-sis does, in essence, imply that there is nocost in opening markets (including those thatat equilibrium will be inactive).

In any Walrasian model an equilibrium isspecified by two components. The firstassigns a price to each market. The secondattributes an input–output vector to each firmand a vector of demands and supplies toevery consumer. Input–output vectors shouldbe profit-maximizing, given the technology,and each vector of demands–supplies mustbe affordable and preference-maximizinggiven the budget restriction of the consumer.

Note that, since some of the commoditiesare contingent, an Arrow–Debreu equilib-rium determines a pattern of final risk bear-ing among consumers.

In a context of convexity hypothesis, or inone with many (bounded) decision makers,an equilibrium is guaranteed to exist. Muchmore restrictive are the conditions for itsuniqueness.

The Arrow–Debreu equilibrium enjoys akey property, called the first welfare the-orem: under a minor technical condition (localnonsatiation of preferences) equilibriumallocations are Pareto optimal: it is impossi-ble to reassign inputs, outputs and commodi-ties so that, in the end, no consumer is worseoff and at least one is better off. To attempt apurely verbal justification of this, consider aweaker claim: it is impossible to reassigninputs, outputs and commodities so that, inthe end, all consumers are better off (for thislocal non-satiation is not required). Definethe concept of gross national product (GNP)at equilibrium as the sum of the aggregatevalue (for the equilibrium prices) of initialendowments of society plus the aggregateprofits of the firms in the economy (that is,the sum over firms of the maximum profitsfor the equilibrium prices). The GNP is the

Arrow–Debreu general equilibrium model 9

aggregate amount of income distributedamong the different consumers.

Consider now any rearrangement ofinputs, outputs and commodities. Evaluatedat equilibrium prices, the aggregate value ofthe rearrangement cannot be higher than theGNP because the total endowments are thesame and the individual profits at therearrangement have to be smaller than orequal to the profit-maximizing value.Therefore the aggregate value (at equilibriumprices) of the consumptions at the rearrange-ment is not larger than the GNP. Hence thereis at least one consumer for which the valueof consumption at the rearrangement is nothigher than income at equilibrium. Becausethe equilibrium consumption for thisconsumer is no worse than any other afford-able consumption we conclude that therearrangement is not an improvement for her.

Under convexity assumptions there is aconverse result, known as the second welfaretheorem: every Pareto optimum can besustained as a competitive equilibrium after alump-sum transfer of income.

The theoretical significance of theArrow–Debreu model is as a benchmark. Itoffers, succinctly and elegantly, a structureof markets that guarantees the fundamentalproperty of Pareto optimality. Incidentally,in particular contexts it may suffice todispose of a ‘spanning’ set of markets. Thus,in an intertemporal context, it typicallysuffices that in each period there are spotmarkets and markets for the exchange ofcontingent money at the next date. In themodern theory of finance a sufficient marketstructure to guarantee optimality obtains,under some conditions, if there are a fewfinancial assets that can be traded (possiblyshort) without any special limit.

Yet it should be recognized that realism isnot the strong point of the theory. For exam-ple, much relevant information in economicsis asymmetric, hence not all contingentmarkets can exist. The advantage of the

theory is that it constitutes a classificationtool for the causes according to which aspecific market structure may not guaranteefinal optimality. The causes will fall into twocategories: those related to the incomplete-ness of markets (externalities, insufficientinsurance opportunities and so on) and thoserelated to the possession of market power bysome decision makers.

ANDREU MAS-COLELL

BibliographyArrow K. and G. Debreu (1954), ‘Existence of an equi-

librium for a competitive economy’, Econometrica,22, 265–90.

Arrow K. and F. Hahn (1971), General CompetitiveAnalysis, San Francisco, CA: Holden-Day.

McKenzie, L. (2002), Classical General EquilibriumTheory, Cambridge, MA: The MIT Press.

See also: Pareto efficiency, Walras’s auctioneer andtâtonnement.

Arrow–Pratt’s measure of risk aversionThe extensively used measure of risk aver-sion, known as the Arrow–Pratt coefficient,was developed simultaneously and inde-pendently by K.J. Arrow (see Arrow, 1970)and J.W. Pratt (see Pratt, 1964) in the1960s. They consider a decision maker,endowed with wealth x and an increasingutility function u, facing a risky choicerepresented by a random variable z withdistribution F. A risk-averse individual ischaracterized by a concave utility function.The extent of his risk aversion is closelyrelated to the degree of concavity of u.Since u�(x) and the curvature of u are notinvariant under positive lineal transforma-tions of u, they are not meaningfulmeasures of concavity in utility theory.They propose instead what is generallyknown as the Arrow–Pratt measure of riskaversion, namely r(x) = –u�(x)/u�(x).

Assume without loss of generality thatEz = 0 and s2

z = Ez2 < ∞. Pratt defines therisk premium p by the equation u(x – p) =

10 Arrow–Pratt’s measure of risk aversion

E(u(x + z)), which indicates that the indi-vidual is indifferent between receiving z andgetting the non-random amount –p. Thegreater is p the more risk-averse the indi-vidual is. However, p depends not only on xand u but also on F, which complicatesmatters. Assuming that u has a third deriva-tive, which is continuous and bounded overthe range of z, and using first and secondorder expansions of u around x, we canwrite p(x, F) ≅ r(x)s2

z/2 for s2z small enough.

Then p is proportional to r(x) and thus r(x)can be used to measure risk aversion ‘in thesmall’. In fact r(x) has global properties andis also valid ‘in the large’. Pratt proves that,if a utility function u1 exhibits everywheregreater local risk aversion than anotherfunction u2, that is, if r1(x) > r2(x) for all x,then p1(x, F) > p2(x, F) for every x and F.Hence, u1 is globally more risk-averse thanu2. The function r(x) is called the absolutemeasure of risk aversion in contrast to itsrelative counterpart, r*(x) = xr(x), definedusing the relative risk premium p*(x, F) =p(x, F)/x.

Arrow uses basically the same approachbut, instead of p, he defines the probabilityp(x, h) which makes the individual indiffer-ent between accepting or rejecting a bet withoutcomes +h and –h, and probabilities p and1 – p, respectively. For h small enough, heproves that

1p(x, h) ≅ — + r(x)h/4.

2

The behaviour of the Arrow–Prattmeasures as x changes can be used to findutility functions associated with any behav-iour towards risk, and this is, in Arrow’swords, ‘of the greatest importance for theprediction of economic reactions in the pres-ence of uncertainty.’

ANTONIO RODRIGO FERNÁNDEZ

BibliographyArrow, K.J. (1970), Essays in the Theory of Risk-

Bearing, Essay 3, Amsterdam: North-Holland/American Elsevier, pp. 90–120.

Pratt, J.W. (1964), ‘Risk aversion in the small and in thelarge’, Econometrica, 32, 122–36.

See also: von Neumann–Morgenstern expected utilitytheorem.

Atkinson’s indexOne of the most popular inequalitymeasures, named after the Welsh economistAnthony Barnes Atkinson (b.1944), theindex has been extensively used in thenormative measurement of inequality.Atkinson (1970) set out the approach toconstructing social inequality indices basedon the loss of equivalent income. In aninitial contribution, another Welsh econo-mist, Edward Hugh Dalton (1887–1962),used a simple utilitarian social welfare func-tion to derive an inequality measure. Thesame utility function was taken to apply toall individuals, with diminishing marginalutility from income. An equal distributionshould maximize social welfare. Inequalityshould be estimated as the shortfall of thesum-total of utilities from the maximalvalue. In an extended way, the Atkinsonindex measures the social loss resulting fromunequal income distribution by shortfalls ofequivalent incomes. Inequality is measuredby the percentage reduction of total incomethat can be sustained without reducing socialwelfare, by distributing the new reducedtotal exactly. The difference of the equallydistributed equivalent income with theactual income gives Atkinson’s measure ofinequality.

The social welfare function considered byAtkinson has the form

y l–e

U(y) = A + B —— , e ≠ 1l – e

U(y) = loge (y), e = 1

Atkinson’s index 11

and the index takes the form

1——

l n yi l – el – e

Ae = 1 – [— ∑ (—) ] e ≥ 0, e ≠ 1n i=l m

l n yiA1 = 1 – exp[ — ∑ Ln (—)]n i=l me = 1

where e is a measure of the degree ofinequality aversion or the relative sensitiv-ity of transfers at different income levels.As e rises, we attach more weight to trans-fers at the lower end of the distribution andless weight to transfers at the top. Thelimiting cases at both extremes are e →∞,which only takes account of transfers to thevery lowest income group and e → 0,giving the linear utility function whichranks distribution solely according to totalincome.

LUÍS AYALA

BibliographyAtkinson, A.B. (1970), ‘On the measurement of inequal-

ity’, Journal of Economic Theory, 2, 244–63.Dalton, H. (1920), ‘The measurement of the inequality

of incomes’, Economic Journal, 30, 348–61.

See also: Gini’s coefficient, Theil index.