senior or younger doctor: what you need to know about ... · senior or younger doctor: what you...

TRANSCRIPT

Senior or Younger Doctor:

What You Need to Know

About Transition Activities

Roger K. Hill, M.S.A., A.S.A.

Transition Alternatives:

The Five Fundamentals

Transition Alternatives:

Prototypical Sale

▪ Full Sale

▪ Control

▪ Least Secure

▪ Cash / Note Ratio

▪ Practice Size Limitation

▪ Time Frame 0-2 Years

▪ Asset Sale

Transition Alternatives:

Delayed Sale

▪ Variation on a Theme

▪ Full Sale

▪ Control and Compromise for Security

▪ Cash / Note Ratio

▪ Time Frame 1-3 Years

▪ Asset Sale

Transition Alternatives:

Fractional Sale

▪ Portion of Practice

▪ More Complex

▪ Emotional Aspects

▪ Larger Practices or Time Frame

of More than 5 Years

Transition Alternatives:

Hybrid (Fractional to Full Sale)

▪ Begins as Fractional Sale

▪ Predetermined Buy-Out Date

▪ Purchaser Owns 100.0% At End

▪ “Golden Handcuffs” (Security)

▪ Can Progress to New Fractional Sale

Transition Alternatives:

Mergers

▪ Most Complex

▪ Single Survivor Entity

▪ Longest Time Frame

(Generally 8-10 Years)

▪ Slow Down Merger

What About the

Transition Process?

I Have Found

A Practice:

Now What?

The 10,000-Foot View

(Or, What Do I Need to Know?)

1. Practice Valuation

2. Cash Flow Projections (Proforma)

3. Financing Considerations

4. Legal Documents

5. Managing Your New Practice

Practice Valuation:

Fair Market Value

Appropriate Valuation Methodology

1. Fair Market Value (FMV) Is the Sum of:

A. Tangible Assets

• Equipment

• Furnishings

• Leasehold Improvements

• Office Equipment

• Supplies

B. Intangible Assets

• Goodwill

• Covenant Not to Compete

• Patient Records

• Telephone Number(s)

Appropriate Valuation Methodology

• Intangible Value Indices

• Practice Growth Rate

• Profitability

• Location

• Procedure Mix

• New Patient Flow

• Related Factors (10-12)

1. Establish Intangibles Value

2. Add Tangible Value

3. Could Be More or Less Than Static Percentage

4. Key is Value of the Intangibles

5. Database on Intangible Value

1. Mean

2. First Standard Deviation

Appropriate Valuation Methodology

Cash Flow Projections (Proforma)

The Fulcrum

(On Which the Lever Turns)

Limitations of Fair Market Value

• Fair Market Value (FMV) Does Not Define

Financial Benefit

• FMV Defines:

• Value of Tangibles

• Value of Intangibles

• Normalized Overhead Rate

“Beans and Weenies”

• You Need to Know:

• Pre-Tax Income

• Estimated Income Taxes

• After-Tax Cash Flow, or

Will I Have Enough for

Beans and Weenies?

Cash Flow Projections (Full Sale)

• Illustrate All of the Above

• Test Value

• Increase Confidence

• Enhances Financing Request

Proforma: Previewing Financial Outcome

3rd Year 4th Year 5th Year

Proj. Prof. Income $1,111,980 $1,134,220 $1,156,904

Practice Overhead (764,929) (779,708) (794,782)

Distributable Profit $347,051 $354,512 $362,122

Dr. New's Coll. Alloc. $0 $741,104 $954,823

Associate Collections 0 194,997 0

Hygiene Allocation 0 198,119 202,082

Total Allocation $0 $1,134,220 $1,156,904

Overhead Allocation $0 ($779,708) ($794,782)

Pre-Tax Profit $0 $354,512 $362,122

Compensation as Associate $160,620

Practice Purchase Interest (43,209) (39,985)

Depreciation & Amortization (60,921) (56,874)

Equipment Purchase Interest (2,874) (2,520)

Depreciation on Equip. Purch. (5,769) (5,769)

Working Capital Interest (5,189) (4,192)

Payable to Dr. Seller (58,499) 0

Personal Deductions (22,700) (22,700) (22,700)

Pre-Tax Income $137,920 $155,350 $230,081

Estimated Taxes (41,837) (47,180) (71,161)

After Tax Income $96,083 $108,170 $158,920

Practice Purchase Principal (41,530) (44,754)

Depreciation & Amortization 60,921 56,874

Equipment Purchase Principal (4,559) (4,913)

Depreciation on Equip. Purch. 5,769 5,769

Working Capital Principal (12,845) (13,842)

Non-Financed Capital Exp. (10,000) (10,000)

Personal Deductions 22,700 22,700 22,700

After Tax Cash Flow $118,783 $128,627 $170,755

Cash Flow Projections (Partnership)

A. Trigger Point

B. Financial Structure

C. Income Distribution Formula

1st Year 2nd Year

Proj. Prof. Income $1,311,251 $1,507,123

Practice Overhead (607,311) (742,631)

Distributable Profit $703,940 $764,493

Dr. New's Alloc. Coll. $433,559 $524,833

Hygiene Allocation 0 228,729

Total Allocation $433,559 $753,562

Overhead Allocation (200,805) (371,315)

Pre-Tax Profit $232,754 $382,246

Assoc. Compensation 150,000

Management Fee Paid (19,240)

Existing Debt Interest (1,605)

Line of Credit Interest (2,391)

New CapEx Interest (21,695)

Personal Items (6,028)

Personal Deductions (20,200) (11,841)

Pre-Tax Income $129,800 $319,447

Estimated Taxes (41,000) (106,433)

After Tax Income $88,800 $213,014

Stock Pmts.Buyin (5,219)

Existing Debt Principal (16,083)

Line of Credit Principal (6,842)

New CapEx Principal (25,594)

Non-Financed Capital Exp. 0

Personal Deductions 20,200 11,841

After Tax Cash Flow $109,000 $171,117

Proforma: Previewing Financial Outcome

Financing:

How Do I Get the Money?

Lender Information Items

• Practice Information

• Valuation Study

• Cash Flow Projections

• Operational Information

• Tax Returns

• Interim Financials

Lender Information Items

• Purchaser Information

• Curriculum Vitae (Resume)

• Production History

• Brief Business Plan

• Telephone Interview

Minimum Lender Requirements

• Credit Score ≥ 680

• Production History

• Zero Years Experience (Orthodontic only)

• Practice Size / Years of Experience /

Seller’s Post-Sale Tenure

• Relaxed Standards

• “What if My Net Worth Is Negative?”

Not All Lenders Created Equally

• Asset-Based Lenders

• “Bricks and Sticks”

• Cash Flow Lenders

• Specialized Group

• National and Local

• Bank and Non-Bank Lenders

Legal Documents for Closing

(Full Sale)

Fundamental Documents

for the Purchase

• Letter of Intent (LOI)

• Asset Purchase Agreement

• Lease Agreement for Office

• Employment Agreement for Seller

Letter of Intent (LOI)

• Defines the Agreement in Principle

• May Be Binding or Non-Binding

• Summary of Deal Points

• Superseded at Closing

Asset Purchase Agreement

• Conveys Ownership

• Typical Sections:

• Closing Date

• Purchase Price / Manner of Payment

• Allocation of Purchase Price

• Indemnification

• Covenant Not to Compete (Seller)

Asset Purchase Agreement (cont’)

• Representations / Warranties

• Rework / Work in Progress

• Covenant Not to Compete

• Seller’s Post-Sale Transition

• General Provisions

Lease Agreement

• Can Take Several Forms:

• New Lease

• Assumption

• Sub-Lease

Lease Agreement

• New Lease Most Common

• Lender Requirements

• Length of Loan

• Base and Extensions

• Landlord Waiver

Seller Post-Sale Employment Agreement

• Typically Paid a Per Diem

• Usually No Benefits

• Can Be Independent Contractor

• Flexible Schedule / Front-End Loaded

Legal Documents for Partnerships

• Initial Documents – Associateship

• Employment Agreement

• Non-Transactional

• Compensation, Benefits, Covenant, etc.

• Letter of Intent

• Sets Out Transactional Details of Buy-In

• Daily Partnership Operations

• Income Division, Death, Disability, Retirement, etc.

Legal Documents for Partnerships

• Partnership Documents – Initiate Buy-In

• Doctors Jointly Owning Corporation

(Cardboard Box)

• Stock Sale Agreement

• Shareholder Agreement

• Employment Agreement

Legal Documents for Partnerships

• Partnership Documents – Initiate Buy-In

• Doctors Own Separate Corporation

(Triangle)

• Asset Sale Agreement

• Partnership Agreement

• Employment Agreement

Financing Options:

Where Will I Get the Money?

Financing Options

• You Are Wealthy…Not Really

• Outside Lenders (Banks, etc.)

• Owner Financing (Seller Acts As Bank)

• Family Members – Really Complicated

• Robbing Convenience Stores –

Not Recommended

Financing Options

• Outside Financing

• Most Common

• Relaxed Borrowing Schedule

• Common Term Lengths

• 84 Months

• 120 Months

• Longer Term (120) and Paying Extra

Financing Options

• Seller Financing

• Seller Essentially Bank

• Usually Only Small Portion

• Same Rates / Terms as Primary Note

• Total of Payments Same as All Bank

Financing Options

• Seller Financing (con’t)

• For the Seller

• Risk Factor

• Need Insurance

• Second Lien Position

• No Tax Advantage

• Need For Continued Financial Oversight

Financing Options

• “Steppin’ Over Dollars to Pick Up Pennies”

• First Get Best Deal You Can, But…

• Sale Price $1.0 Million

• Payment On 10-Year Term

• 5.0% or 5.5%

• Different Over Term of Loan: $29,500

Financing Options

• “Steppin’ Over Dollars to Pick Up Pennies”

• Took a Month to Negotiate 5.0% Rate

• Practice Income = $100,000 per Month

• Overhead 55.0% = $55,000

• Pre-Tax Profit 45.0% = $45,000

• Net Result – Lost $15,500

The Purpose of a Valuation

and Proforma

The Purpose of a Valuation and Proforma

• In the Beginning…

• Establishes Value for Transaction

• Static Percentages (e.g., 80.0%) Inaccurate

/ Misleading

• First Standard Deviation 56.95% to 96.32%

• Range Is 39.37% - Not a Good Place to

Guess

The Purpose of a Valuation and Proforma

• Location in Range Established With:• Spreadsheet Analysis (Financial X-Ray)

• Due Diligence Visit

• Valuation Algorithms

• Typically Done by Valuation Professional

The Purpose of a Valuation and Proforma

• Valuation Is Only the Beginning

• Limitations of a Valuation Study

• Segue to Proforma (Cash Flow

Projections)

The Purpose of a Valuation and Proforma

• Proforma (PF) Establishes Financial

Outcome(s)

• (1) Full Sale

• (2) Fractional Sale

• Tests ABCs:

• A. Trigger Point

• B. Financial Structure

• C. Income Distribution Formula

The Purpose of a Valuation and Proforma

• Timing For Valuation / Proforma

• Full Sale at Outset of Process

• Fractional Sale

• Before Associateship Begins

• Update at End of Associateship

• Update Is Tangible Net Worth Only

The Purpose of a Valuation and Proforma

• The Update Protocol• Each Doctor’s Legitimate Agenda

• Baseline Fair Market Value Includes Senior’s Solo

Growth Rate

• Growth Beyond This Attributable to Associate

• Updated Fair Market Value =

$ Original Intangible Value

Then-Current Tangible Value

$ Updated Value for Buy-In

The Purpose of a Valuation and Proforma

• Proforma (PF) Establishes Financial

Outcome(s), con’t

• (3) Delayed Sale

• Baseline For Letter of Intent

• Triggering Events

• Reaching Agreed-Upon Date

• Seller’s Death – Immediate

• Seller’s Disability – Immediate

• Mutually Agreed Acceleration

The Purpose of a Valuation and Proforma

• Proforma (PF) Establishes Financial

Outcome(s), con’t

• (3) Delayed Sale

• Update at Triggering Event

• Update Protocol

• Intangible Value +/- 5.0% - No Change

• Intangible Value >5.0% - New Value

• Then-Current Tangible Value

The Purpose of a Valuation and Proforma

• Proforma (PF) Establishes Financial

Outcome(s), con’t

• (4) Letter of Intent for:

• Death

• Disability

• Retirement

• No Agreed-Upon Date – Contingency

Agreement

• Baseline Fair Market Value in LOI

• Update Protocol Same As Delayed Sale

Factors Affecting Value

Factors Affecting Value

• Fair Market Value (FMV), Sum of:

• Tangible Net Worth

• Intangible Value

• FMV = (Intangible + TNW)

• Intangible Value Larger / More Critical

Factors Affecting Value

• Factors Affecting Value of Intangibles

• Profitability

• The Big Four:

• Salaries / Wages (Staff) – 18.0% - 22.0%

• Rent / Occupancy Expenses – 5.0% - 7.0%

• Dental Supplies – 6.0% - 10.0%

• Laboratory Charges (Aligners, etc.) – 6.0% - 8.0%

Factors Affecting Value

• Factors Affecting Value of Intangibles

• Growth Rate

• Location

• Production / Collection Ratio

• Service Mix (Brackets vs. Aligners)

Factors Affecting Value

• Factors Affecting Value of Intangibles

• Effectiveness of Marketing Protocol

• Ratio of Doctor / Direct Referrals

• Range

• Depth

Factors Affecting Value

• Factors Affecting Value of Tangibles

• Age of Fixed Assets (F/As)

• Dental Equipment

• Office Equipment

• Furnishings

• Leasehold Improvements

• Current State of Technology

Factors Affecting Value

• Factors Affecting Value of Tangibles

• Orthodontic Receivables

• (+) Contracts Receivable (C/R)

• (+) Accounts Receivable (A/R)

• (-) Prepaid Treatment

• C/R Value Less Than Face Amount

Typical Valuation Methodologies

• Science Says “Two Particles / Same

Space / Same Time”

• All the Same, It’s Happening with

Valuations

• Individual / Traditional Market

• Income Approaches

• $Financial Reward

%Risk = $FMV

• Comparable Sales (Market)

Typical Valuation Methodologies

Typical Valuation Methodologies

• Individual / Traditional Market (cont’d)

• Average (Currently) ~80.0% of Revenue

• BUT, It Varies Widely

• One Foot in Boiling Water; the Other in

Freezing Water

• First Standard Deviation Is

56.95% to 96.82%

Typical Valuation Methodologies

• Corporate Valuation Metric

• Typical Value Range: 4.0 to 7.0 x EBITDA

• Translated: 100.0% to 150.0% of Revenue

• Corporate Buyers Focused on Numbers

• An Income Stream Is an Income Stream

Typical Valuation Methodologies

• Corporate Valuation Metric

• EBITDA – What Is This?

• $ Practice Revenue

(Normalized Overhead)

(Reasonable Doctor Compensation)

$ EBITDA

Allocation of the Purchase Price

Allocation of the Purchase Price

• Assigns Portion of Price to Each Asset Class

• Seller and Buyer Must Use Same Allocation

• Push / Pull in Tax Code

• Not As Difficult As It Sounds

• Tax-Driven Process

Allocation of the Purchase Price

• Order of Allocation• Receivables

• Consumable Supplies

• Fixed Assets

• Patient Records

• Covenant Not to Compete

• Personal Goodwill

Corporation Sells

Doctor Sells

Allocation of Purchase Price

Asset Seller Purchaser

Supplies* Ordinary Income Expensed in First Year

Fixed Assets* Generally Ordinary Depreciable Over 5-7 Years

Patient

Records*

Capital Gain Depreciable Over 15 Years

Contracts

Receivable

Included in Goodwill Depreciable Over 15 Years

Covenant Ordinary if Isolated;

Capital if Combined

with Goodwill

Depreciable Over 15 Years

Personal

Goodwill

Capital Gain Depreciable Over 15 Years

* If the practice is incorporated these items must be sold by the corporation. Gain from these may be subject to both corporate and personal taxation.

Allocation of the Purchase Price

• What Is Goodwill?

• Goodwill Is Only an Expectation

• Expectation Financial Benefit

Continues After Change of Owners

• That Is, the Patients / Referrers Will Stay

Legal Entities and Tax Implications

Legal Entities and Tax Implications

• Sole Proprietorship (Not Incorporated)

• No Separation Between You and the Practice

• No Protection from General Liability

• Limited Tax Reduction Flexibility

Legal Entities and Tax Implications

• Incorporating Your Practice

• Corporation Distinct From Individual (You)

• Limits Exposure to General Liability

• Increased Tax Reduction Strategy

• Tax Planning

• Discretionary Expenses

Legal Entities and Tax Implications

• Two Types of Corporations

• (1) C (or Closed) Corporation

• Original Type

• Less Tax Flexibility Than S Corporation

• Can Be Tax-Paying Entity

Legal Entities and Tax Implications

• Two Types of Corporations

• (2) Subchapter S Corporation

• Sub S

• More Recent Development

• Greater Tax Planning Flexibility

• A “Flow Through” Entity

• Not a Tax-Paying Entity

Legal Entities and Tax Implications

• What Is the Difference?

• C Corp – Money in Checking Account at

Year’s End Subject to Corporate Tax

• S Corp – Money in Checking Account Not

Subject to Corporate Tax

• Money “Flows Through” to Personal Return

• Not Tax-Paying Entity

Legal Entities and Tax Implications

• $100.0m in Bank Account Year End

• (21.0m) Corporate Income Tax

• (19.0m) Individual Income Tax

• $60.0m After-Tax Income

• C (Closed) Corporation

Legal Entities and Tax Implications

• C Corporations

• Can Be Tax-Paying Entity

• Inattention = Corporate Income Tax

• Doctor Incurred 40.0% Total Tax

Legal Entities and Tax Implications

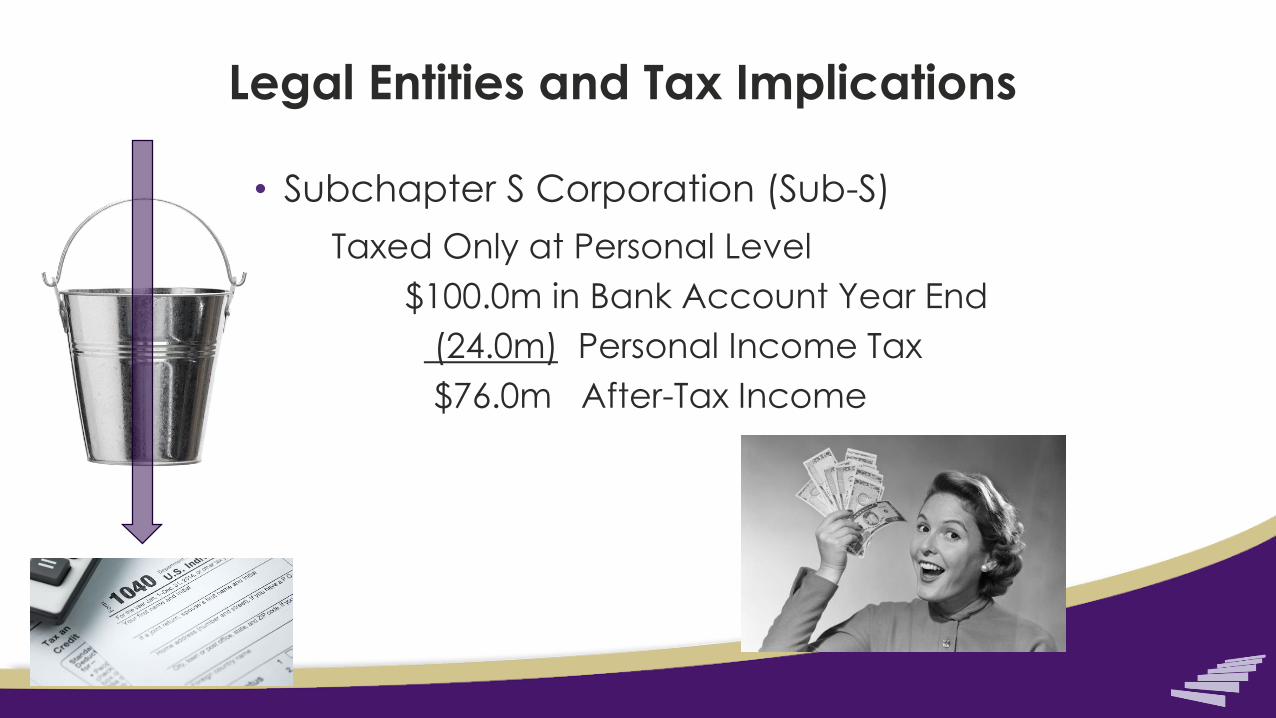

• Subchapter S Corporation (Sub-S)

• $100.0m Still in Bank Account

• Called a “Flow-Through” Entity

• Flows Through to Doctor’s 1040

Legal Entities and Tax Implications

• Subchapter S Corporation (Sub-S)

• Taxed Only at Personal Level

• $100.0m in Bank Account Year End

• (24.0m) Personal Income Tax

• $76.0m After-Tax Income

Legal Entities and Tax Implications

• Limited Liability Company (LLC)

• Professional Limited Liability Company (PLLC)

• Blend of Subchapter S and Sole Proprietorship

• Can Be Advantageous in States That Tax Sub S

• PLLC in a Few States, Same as LLC

Legal Entities and Tax Implications

• General Partnership

• Requires Multiple Owners, Corporations Do Not

• Older Type Entity, Rarely Used

• Distinct From Individual (You)

• Joint and Several Liability

Advisors for Transitions – and Beyond

• CPAs

• Attorneys• Dental / Orthodontic Experience

• Tax Attorneys

• Consultants

• Wide-Spectrum Financial / Legal Groups

• Specific to Dentistry and Orthodontics

8816 Red Oak Blvd.

Charlotte, NC 28217

(877) 306-9780

www.mcgillhillgroup.com

Senior or Younger Doctor: What You Need to Know About Transition Activities

Roger K. Hill, MSA, ASA

• Transition Alternatives: The Five Fundamentals

• What About the Transition Process?

• Practice Valuation: Fair Market Value

• Cash Flow Projections

• Financing: How Do I Get the Money?

• Legal Documents for Closing

• Financing Options

• The Purpose of a Valuation and Proforma

• Factors Affecting Value

• Typical Valuation Methodologies

• Allocation of the Purchase Price

• Legal Entities and Tax Implications

Terms & Definitions

Tangible Assets - A tangible asset is an asset that has a physical form. Tangible assets include

both fixed assets, such as machinery, buildings and land, and current assets, such as inventory.

Intangible Assets - Nonphysical assets, including, but not limited to: known location, trained

staff, assigned telephone numbers, patient records, web site(s), and personal goodwill.

EBITDA - Earnings before interest, tax, depreciation and amortization (EBITDA) is a measure

of a company's operating performance. Essentially, it's a way to evaluate a company's

performance without having to factor in financing decisions, accounting decisions or tax

environments.