september kpn deck (md banks) (3) - mdfinbank.com · registration with the sec or with any state...

TRANSCRIPT

Today’s Ground Rules for Community Banks in Accessing Middle Market C&I and Consumer Lending

September 2015

2

FORWARD‐LOOKING STATEMENT AND OTHER IMPORTANT DISCLOSURES

AP Commercial LLC, is a wholly owned subsidiary of Alliance Partners and is the SEC‐registered investment adviser referred to herein as “Alliance Partners.” Registration with the SEC or with any state securities authority does not imply a certain level of skill or training.

Information contained herein may include information with respect to prior investment performance. Information with respect to prior performance, while a useful tool in evaluating Alliance Partners’ investment activities, is not necessarily indicative of actual results that may be achieved for unrealized investments.

This presentation is for informational purposes only and does not constitute an offer to sell, or the solicitation of an offer to buy, any security, product, or service of Alliance Partners.

Unless otherwise noted, information included herein is presented as of December 31, 2014. This presentation is not complete, and the information contained herein may change at any time without notice. Alliance Partners does not have any responsibility to update the presentation to account for such changes. Alliance Partners makes no representation or warranty, express or implied, with respect to the accuracy, reasonableness or completeness of any of the information contained herein, including, but not limited to, information obtained from third parties. Past performance is no guarantee of future returns.

The information contained herein is not intended to provide, and should not be relied upon for, accounting, legal or tax advice or investment recommendations.

Note 1: Sample loans were selected from all loans presented to BancAlliance members through September 30, 2014, and one loan from each of thethree current lending platforms was selected. Sample loans are presented for illustrative purposes only to provide examples of the types of loansavailable through the BancAlliance network. BancAlliance members may or may not own these sample loans at this time. The specific loans identifieddo not represent all of the loans recommended to BancAlliance members. To request a complete list of all recommendations made within the past year,contact [email protected].

Note 2: The portfolio summary represents the portfolio of loans offered by Alliance Partners to BancAlliance members, which is generally representative of the portfolio held by BancAlliance members in aggregate as of March 16, 2015. Each loan in the portfolio is given equal weight, irrespective of size of the loan.

3

Presented By

BancAlliance.comWashington, D.C. Office | 4445 Willard Avenue Suite 1100 | Chevy Chase, MD 20815

Main:(301) 232‐5440 | Email: [email protected]

301.232.5416 | [email protected]

Wayne GoreDirector, Alliance Partners

Wayne is a Director at Alliance Partners. Prior to joining Alliance Partners, Wayne held

leadership roles in the Financial Institutions Group with McKinsey & Co. and served as

Managing Director at the Corporate Executive Board. Previously, Wayne was an investment

banker with Merrill Lynch and Goldman Sachs as a member of the Mergers & Acquisitions

teams. He has also served on the Board of a non‐U.S. community bank during its growth

from $200 million to $1.1 billion in assets. Wayne received his B.A. from Princeton University

and his J.D. and M.B.A. from Columbia University.

4

MEMBERSHIP DEMOGRAPHICS

Members typically range in size from $200MM to $10B in assets

BancAlliance is an exclusive network with

200+ MEMBERS

AL1

AZ2

CA13

CT6

FL11

GA5

IL17

IN6

IA2

KS1

LA6

DE1

MA20MI

3

MO6

NJ7

NY4

OH3

OK4

PA10

RI1

TX9

WI1

KY2

ME1MN

4

MT1

NE11NV

1

NH2

NC10

OR3

SC3

TN1

UT1

VA11

WA3

WV1 DC

2

ID1

MD4

WY

ND

SD

CO

NM ARMS

VT

5

1. The Business Case for Middle Market C&I in Community Banking

2. Reclaiming Market-share in Consumer Lending

3. An Overview of the BancAlliance Platform– Credit Selectivity Priorities and Approval Process

– Credit Management and Loan Portfolio Objectives

New Lending Platforms for Community Banks

6

Business Drivers for Prudent Diversification

Return on Average Equity

Real Estate Concentration

Cash & Securities as % of Assets

Assets in 5+year Maturities

National medians represent banks with $200MM‐$10BN in total assets1Represents banks registered as of May 10, 2015.Source: SNL. Represents medians for Q4 data.

Trends:‐ Decreased Return on Average Equity

‐ High real estate concentrations, even post crisis

‐ Excess liquidity‐ Long‐dated assets

Some Community Banks Have Chosen to Diversify into Corporate C&I via Leveraged Loans

11%

8%

10%

7%

0

2

4

6

8

10

12

2004 2014(%

) National Avg. Attendees Avg.

74%

79%79%

86%

65

70

75

80

85

90

2004 2014

(%) National Avg. Attendees Avg.

5%

15%16%

26%

‐

5

10

15

20

25

30

2004 2014

(%) National Avg. Attendees Avg.

28% 27%27%

26%

20

22

24

26

28

30

2004 2014

(%) National Avg. Attendees Avg.

7

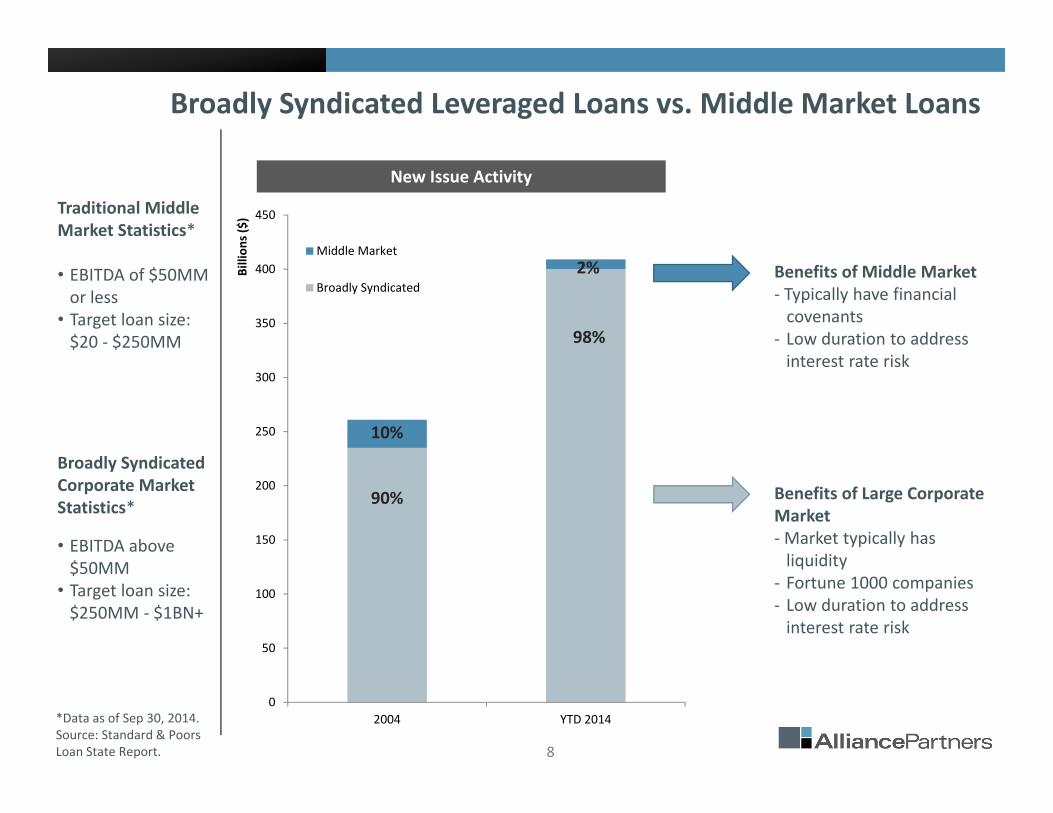

Definitions will vary, but there are typically a few common themes:– Proceeds used to purchase companies outright, acquire additional companies to be merged with an existing company, or for capital distributions

– Total Debt divided by EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization) exceeds 4X; or Senior Debt divided by EBITDA exceeds 3X; or other defined measure appropriate for a particular industry

– Not a uniform market Essentially two categories:• Broadly Syndicated Leveraged Loans• Middle Market Leveraged Loans

What is a Leveraged Loan?

Why are Community Banks Attracted to this Market?– Access to diversified pool of C&I loans– Can provide better risk‐adjusted return versus in‐market C&I– Typically floating rate, priced off Prime or LIBOR (“L”)

8

0

50

100

150

200

250

300

350

400

450

2004 YTD 2014

Billion

s ($)

Middle Market

Broadly Syndicated

Broadly Syndicated Leveraged Loans vs. Middle Market Loans

Benefits of Middle Market‐ Typically have financial covenants

‐ Low duration to address interest rate risk

Benefits of Large Corporate Market‐Market typically has liquidity

‐ Fortune 1000 companies‐ Low duration to address interest rate risk

Broadly Syndicated Corporate Market Statistics*

• EBITDA above $50MM

• Target loan size: $250MM ‐ $1BN+

Traditional Middle Market Statistics*

• EBITDA of $50MM or less

• Target loan size: $20 ‐ $250MM

*Data as of Sep 30, 2014. Source: Standard & PoorsLoan State Report.

98%

90%

10%

2%

New Issue Activity

9

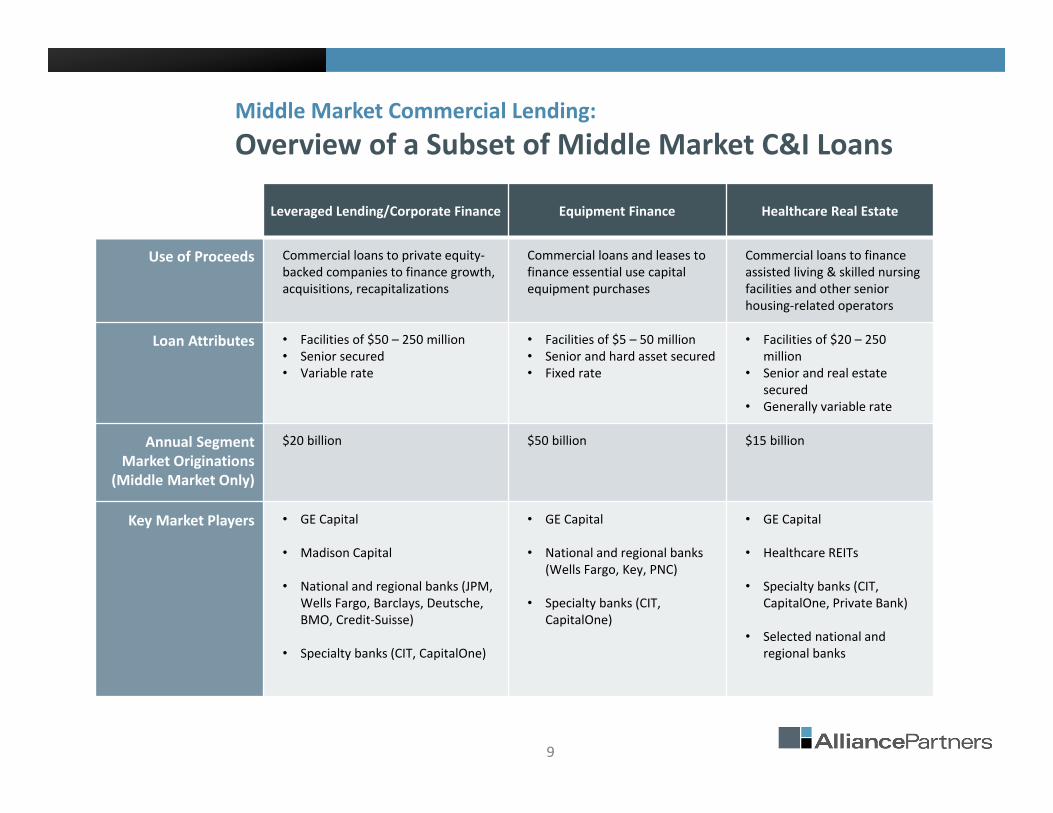

Middle Market Commercial Lending: Overview of a Subset of Middle Market C&I Loans

Leveraged Lending/Corporate Finance Equipment Finance Healthcare Real Estate

Use of Proceeds Commercial loans to private equity‐backed companies to finance growth, acquisitions, recapitalizations

Commercial loans and leases to finance essential use capital equipment purchases

Commercial loans to finance assisted living & skilled nursing facilities and other senior housing‐related operators

Loan Attributes • Facilities of $50 – 250 million• Senior secured• Variable rate

• Facilities of $5 – 50 million• Senior and hard asset secured• Fixed rate

• Facilities of $20 – 250 million

• Senior and real estate secured

• Generally variable rate

Annual Segment Market Originations

(Middle Market Only)

$20 billion $50 billion $15 billion

Key Market Players • GE Capital

• Madison Capital

• National and regional banks (JPM, Wells Fargo, Barclays, Deutsche, BMO, Credit‐Suisse)

• Specialty banks (CIT, CapitalOne)

• GE Capital

• National and regional banks (Wells Fargo, Key, PNC)

• Specialty banks (CIT, CapitalOne)

• GE Capital

• Healthcare REITs

• Specialty banks (CIT, CapitalOne, Private Bank)

• Selected national and regional banks

10

Anatomy of a Middle Market C&I Loan1

What does Company do?Provides outsourced janitorial services to retail and grocery customers at more than 14,000 stores across all 50 states and Canada.

Credit Snapshot*:• Senior Secured Term Loan• 7 Years• 4.77%, with 1% L Floor

Opportunity: Lend to a market leader with

customer relationships avg. 10+ years

What does Company do?One of the largest crane rental companies in North America with a diverse fleet of over 3,000 units of lift equipment capable of serving a broad range of market sectors.

Credit Snapshot*:• Equipment Secured TL• 47 months• 3.09%

Opportunity:One of largest crane rental

companies in the US with strong collateral and amortization

What does Company do?159‐unit assisted living and memory care facility that recently completed an expansion project, increasing units from 126.

Credit Snapshot*:• Secured by 1st Mortgage• 5 years• 3.32%, with 0.75% L Floor

Opportunity:Solid operating history in a

strong market with real estate collateral

Many middle market C&I companies offer a product with a national footprint

Corporate Finance Equipment Finance Healthcare Real Estate

*This yield is net of advisory fees and expenses paid to Alliance Partners, which can range from 50‐150 basis points.

11

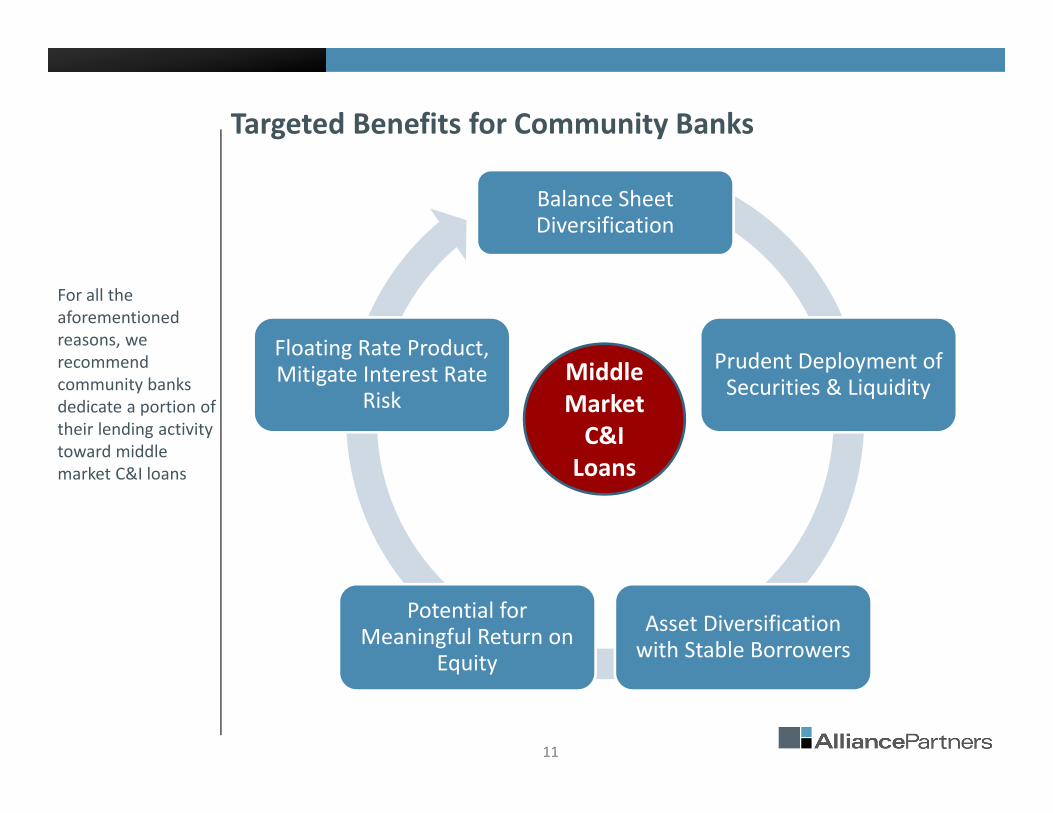

Targeted Benefits for Community Banks

For all the aforementioned reasons, we recommend community banks dedicate a portion of their lending activity toward middle market C&I loans

Balance Sheet Diversification

Prudent Deployment of Securities & Liquidity

Asset Diversification with Stable Borrowers

Potential for Meaningful Return on

Equity

Floating Rate Product, Mitigate Interest Rate

RiskMiddle Market C&I Loans

12

The Consumer Finance Challenge and Opportunity

Due to lack of independent scale to compete with the largest banks in consumer lending, community banks have lost market share in a $1.3 trillion marketplace they once dominated.

Source: Wall Street Journal

13

Real Estate

Merchant Cash Advance

Pay Day

Education Financing

Explosion of New Lenders: Marketplace Lending

Marketplace Lending Developments and Opportunities_vFinal.pptx\31 AUG 2014\3:25 PM\2

Marketplace Lenders

SMB Credit

Consumer

Purchase Financing

All Shapes, All Sizes

14

Drivers of the ShiftMost community banks are unable to compete independently due to economies of scale across the business including risk analytics, advertising, ops, compliance, and servicing

The Consumer Finance Challenge and Opportunity

Implications for Community BankersNarrower customer relationships (implicitly inviting the big banks in)

Loss of earning assetsLoss of diversification:

However,…Community banks enjoy superior customer relationships (consumers would much prefer to do business with them over bigger banks)

Community banks enjoy superior cost and stability of capital

Source: SNL data, Banks between $200MM and $10BN in total assets. As of September 30, 2014.

15

The Opportunity

Generate Loan Growth and DiversificationHold a diversified portfolio of high FICO score consumer whole loans consistent with strict underwriting guidelines.

Deliver a First Rate Customer ExperienceProvide access to a borrower‐friendly, pre‐approved loan with competitive rates.

Trusted Compliance Management Oversight With expertise in regulatory and compliance issues, BancAlliance provides comprehensive program oversight.

Limited Investment RequiredLending Club provides marketing, services loans and creates the technology customer‐interface.

Potential for Attractive Risk‐adjusted Returns

Consumer Loan Program in Partnership with Lending Club

Independent RISK Analysis*

Average Borrower FICO 704 ‐ 731

Average Borrower Debt‐to‐Income 16.0% ‐ 18.0%

Average Borrower Income 75,000 ‐ 87,000

Gross Rates 7.0% ‐ 13.4%

Charge Off / Prepay Impact 2.1% ‐ 4.8%

Lending Club Servicing Fee 0.8% ‐ 1.0%

BancAlliance Servicing Fee 0.4% ‐ 0.6%

Weighted Average Estimated Net Yield 4.9% ‐ 7.0%

* Performed by MTG Risk, LLC using Lending Club data.

16

An Overview of the BancAlliance Platform

17

Executive Overview

The BancAlliance network is a shared lending platform that provides its community bank members with a broad array of loan programs and services, including sourcing, underwriting and managing loans that might otherwise be inaccessible.

Our mission is to enable our members, the banks that direct our activities, to prudently diversify into high‐quality commercial, consumer and other loans in a manner consistent with the

highest commercial and regulatory standards –without changing the nature or mission of the

traditional community bank.

3

18

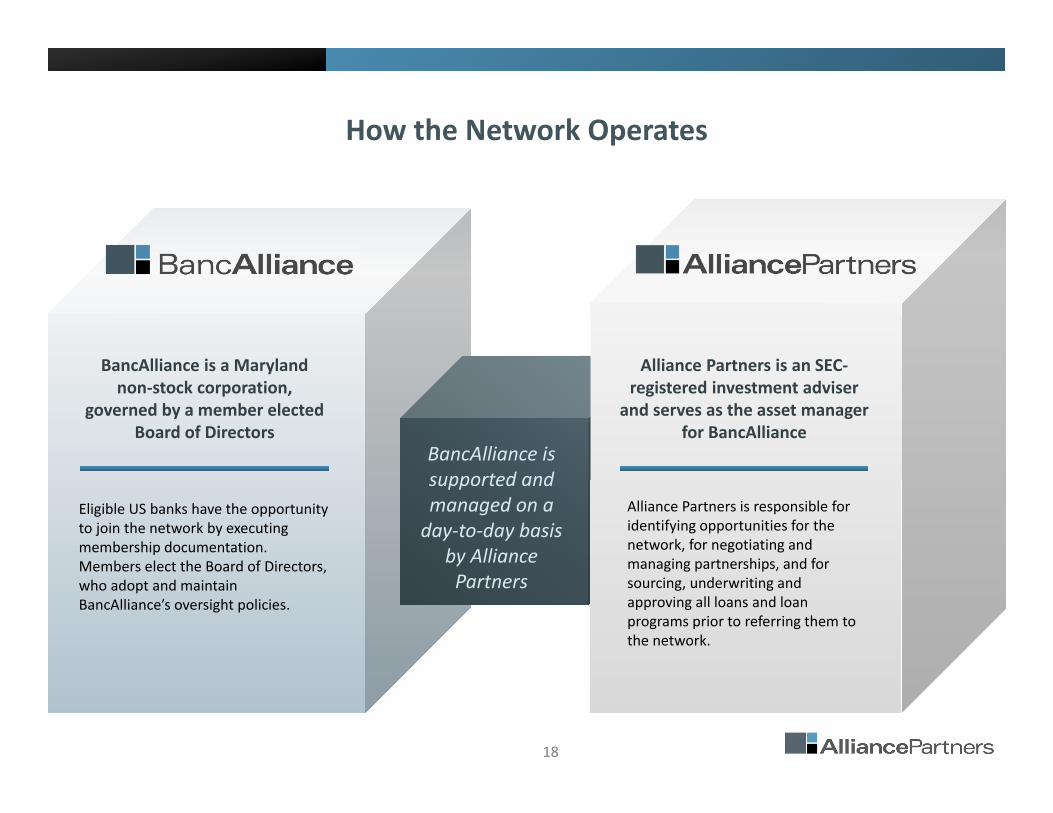

How the Network Operates

BancAlliance is a Maryland non‐stock corporation,

governed by a member elected Board of Directors

Eligible US banks have the opportunity to join the network by executing membership documentation. Members elect the Board of Directors, who adopt and maintain BancAlliance’s oversight policies.

Alliance Partners is an SEC‐registered investment adviser

and serves as the asset manager for BancAlliance

Alliance Partners is responsible for identifying opportunities for the network, for negotiating and managing partnerships, and for sourcing, underwriting and approving all loans and loan programs prior to referring them to the network.

BancAlliance is supported and managed on a day‐to‐day basis

by Alliance Partners

19

Deep Expertise Alliance Partners offers a strong team drawn from industry leading firms with expertise specific to BancAllianceloan programs. In addition, members of the Alliance Partners management team have had decades of experience managing lending businesses through a variety of credit cycles. The team is in service to BancAlliance members.

Specialized Focus Alliance Partners focuses on identifying the specific challenges facing community banks and developing innovative solutions that advance the interests of BancAlliance members.

Strong Compliance Framework Alliance Partners recognizes the critical importance of regulatory compliance and designs the BancAlliance loan programs and services to operate in a manner consistent with regulatory expectations. To the extent possible, Alliance Partners seeks to minimize the regulatory challenges and costs imposed on members.

Alignment of Interests The BancAlliance Board of Directors ensures that the interests of members and Alliance Partners are aligned.

Fiduciary Duties and Oversight Alliance Partners is a registered investment advisor subject to oversight and examination by the SEC.

The Asset Manager

Alliance Partners is the investment advisor to BancAlliance members. Alliance Partners deploys a specialized orientation and set of resources to help members meet their asset and return objectives.

20

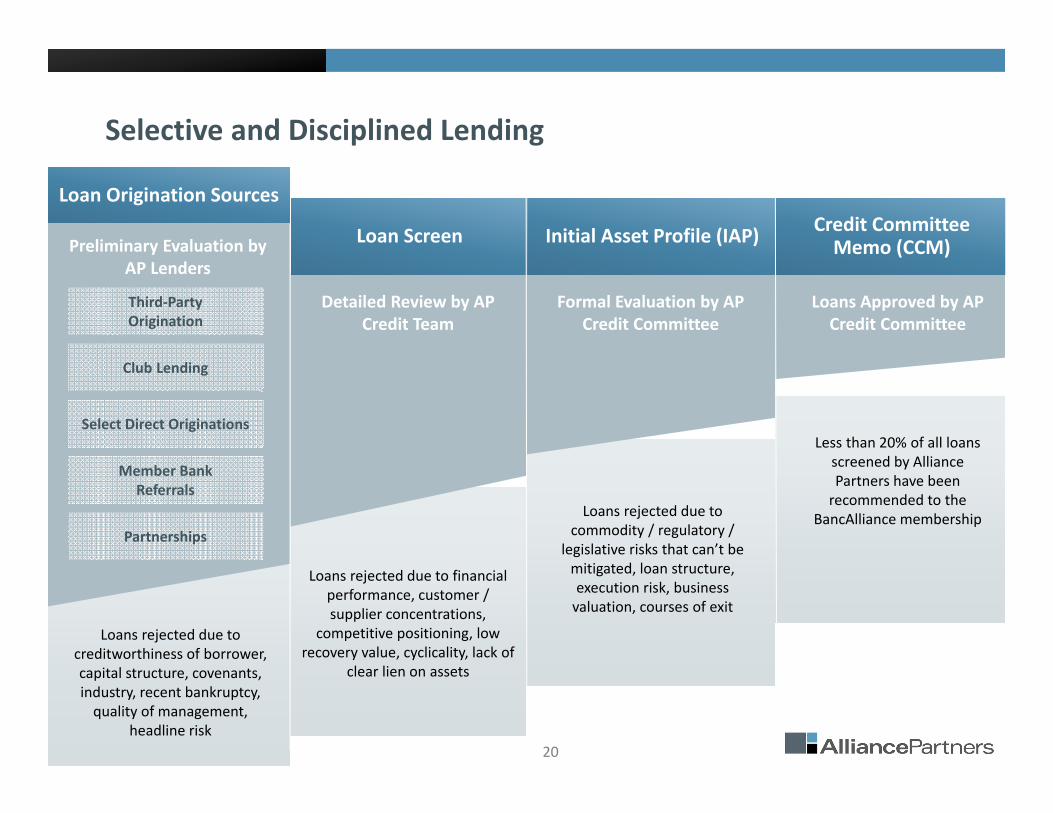

Loan Screen Initial Asset Profile (IAP) Credit CommitteeMemo (CCM)Preliminary Evaluation by

AP Lenders

Detailed Review by AP Credit Team

Formal Evaluation by AP Credit Committee

Loans Approved by AP Credit Committee

Loans rejected due to creditworthiness of borrower, capital structure, covenants, industry, recent bankruptcy, quality of management,

headline risk

Loans rejected due to financial performance, customer / supplier concentrations,

competitive positioning, low recovery value, cyclicality, lack of

clear lien on assets

Loans rejected due to commodity / regulatory /

legislative risks that can’t be mitigated, loan structure, execution risk, business valuation, courses of exit

Less than 20% of all loans screened by Alliance Partners have been recommended to the

BancAlliance membership

Selective and Disciplined Lending

Loan Origination Sources

Third‐Party Origination

Select Direct Originations

Partnerships

Club Lending

Member Bank Referrals

21

Commercial Loan Program: Portfolio Summary

Business Services, 11.8%Capital

Equipment, 3.2%

Consumer Goods, 5.4%

Consumer Services, 2.2%

Education, 2.2%

Environmental, 1.1%

Financial Services, 4.3%

Food & Beverage, 8.6%

Healthcare, 8.6%Logistics, 6.5%

Manufacturing, 33.3%

Media, 3.2%

Mining, 1.1%

Packaging, 1.1%

Software, 5.4%

Technology, 1.1%Automotive, 1.1%

By Industry

Corporate Finance

Our Corporate Finance Team provides cash flow‐based financing alongside experienced private equity sponsors to fund growth, acquisitions, expansion, or recapitalizations of middle‐market businesses with $10‐75 million in EBITDA. Our Corporate Finance Team typically sources senior term and revolving debt facilities ranging in size from $40‐250 million and secured by all of the assets and stock of the business. These loans generally have variable interest rates.

Healthcare Real Estate Finance

Our Healthcare Real Estate Finance Team provides first mortgage loans to dedicated healthcare facilities alongside operators with demonstrated successful track records with similar facilities. We focus on financing skilled nursing and senior housing properties, often where the operator is enhancing or repositioning the facility. Our Healthcare Real Estate Finance Team typically sources senior term debt facilities ranging in size from $10‐50 million and secured by a mortgage on the real estate as well as a pledge of any contractual lease payments related to the underlying property. These loans may have either fixed or variable interest rates.

Equipment Finance

Our Equipment Finance Team provides equipment‐secured loans to middle‐market businesses. We focus on financing the acquisition of essential use equipment collateral that is tied to the growth and profitability of the business. Our Equipment Finance Team typically sources senior term debt facilities and capital leases ranging in size from $5‐50 million, secured by specific equipment collateral. These loans generally have fixed interest rates.

Asset‐based Finance

Our Asset‐based Finance Team provides asset‐based loans to non‐bank finance companies and similar businesses. We focus on financing financial assets and contracted streams of cash flows. Our Asset‐based Finance Team typically sources senior term debt facilities ranging in size from $5‐100 million and secured by the specified assets.

2

22

BancAlliance has teamed up with Lending Club, one of the world’s largest marketplace lenders, to create a model that empowers community banks to compete in consumer lending.

Consumer Loan Program

BankCustomer

Community Bank

BancAlliance

Lending Club

Proven origination and servicing technology High‐quality, validated underwriting models Superior customer service/experience All loans originated through regulated bank

Strengthens customer relationships Low marginal costs Portfolio diversification Increased interest and fee income

Program design, oversight and due diligence Compliance management Performance analytics Portfolio reporting

Lower debt burden and cost savings Improved FICO score Ability to obtain consumer loan through trusted community bank User‐friendly online experience

Washington, D.C.4445 Willard Avenue, Suite 1100

Chevy Chase, MD 20815

Telephone: (301) 232‐5400www.bancalliance.com // www.alliancepartners.com