shares and taxation taxation implications of owning shares

TRANSCRIPT

Shares and Taxation

Taxation implications of owning shares

Income Tax• Any income that you make is able to

be taxed.• Everyone is entitled to the first

$18200 of income being tax free – Tax Free Threshold.

• With shares returns from dividends and capital gains are both classed as income and as such are both able to be taxed.

• Capital Gains Tax (GCT) is a tax levied on any capital gain (profit) made on an investment.

• Laws relating to capital gains seem to continually change. Some of the general changes are:

• Shares purchased pre 1985 are not subject to CGT.

• Shares purchased pre September 1999 the Capital Gain can be calculated using the indexation model or the discount model.

Capital Gains Tax

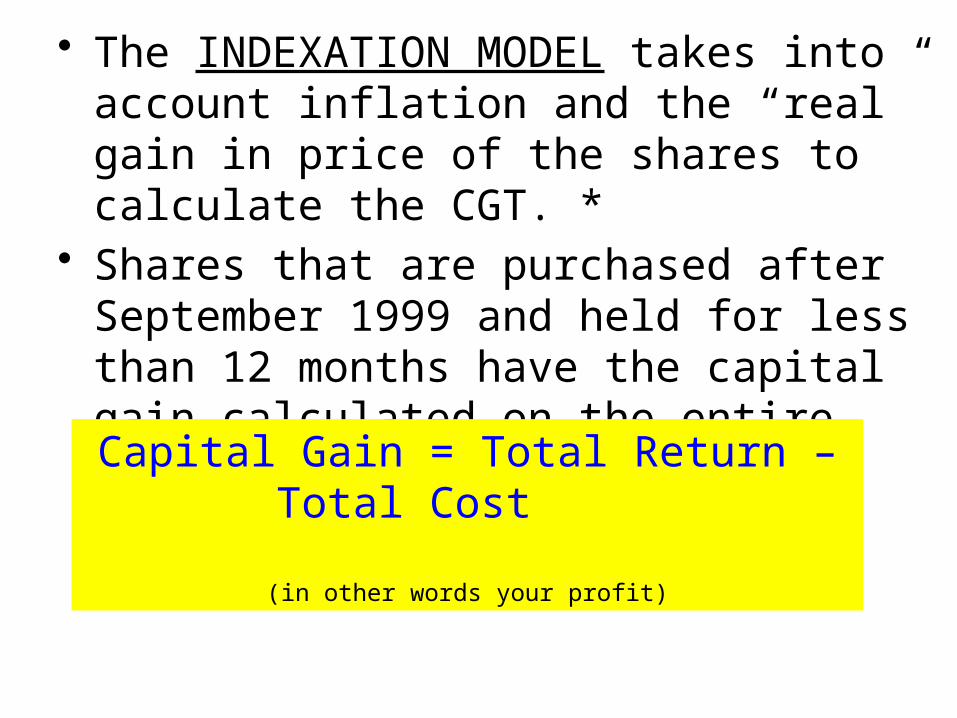

• The INDEXATION MODEL takes into account inflation and the “real” gain in price of the shares to calculate the CGT. *

• Shares that are purchased after September 1999 and held for less than 12 months have the capital gain calculated on the entire gain.Capital Gain = Total Return – Total Cost

(in other words your profit)

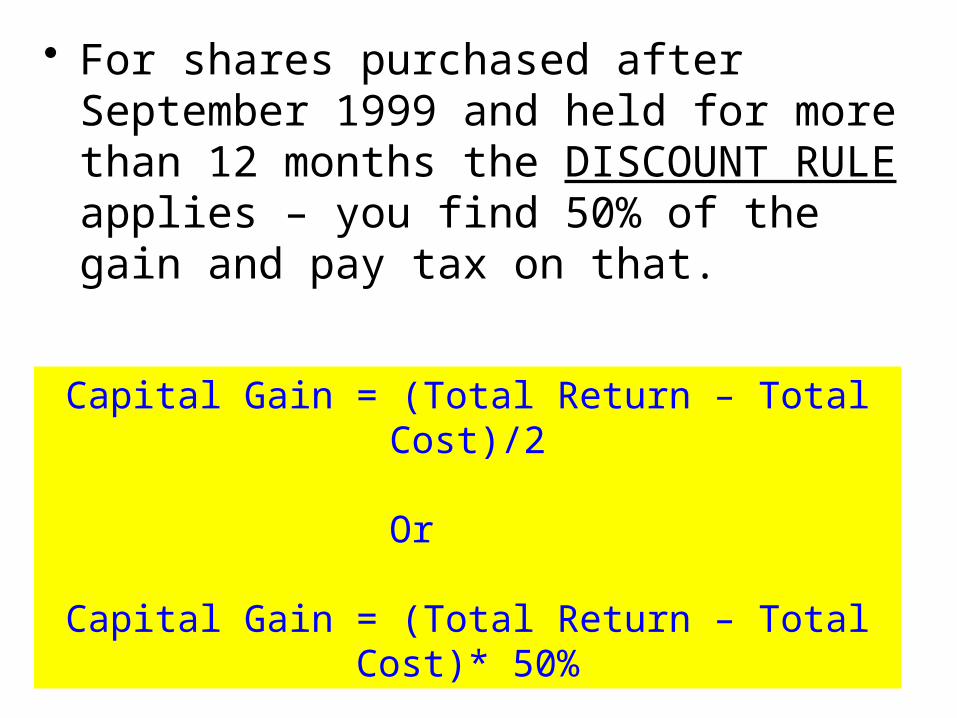

• For shares purchased after September 1999 and held for more than 12 months the DISCOUNT RULE applies – you find 50% of the gain and pay tax on that.

Capital Gain = (Total Return – Total Cost)/2

Or

Capital Gain = (Total Return – Total Cost)* 50%

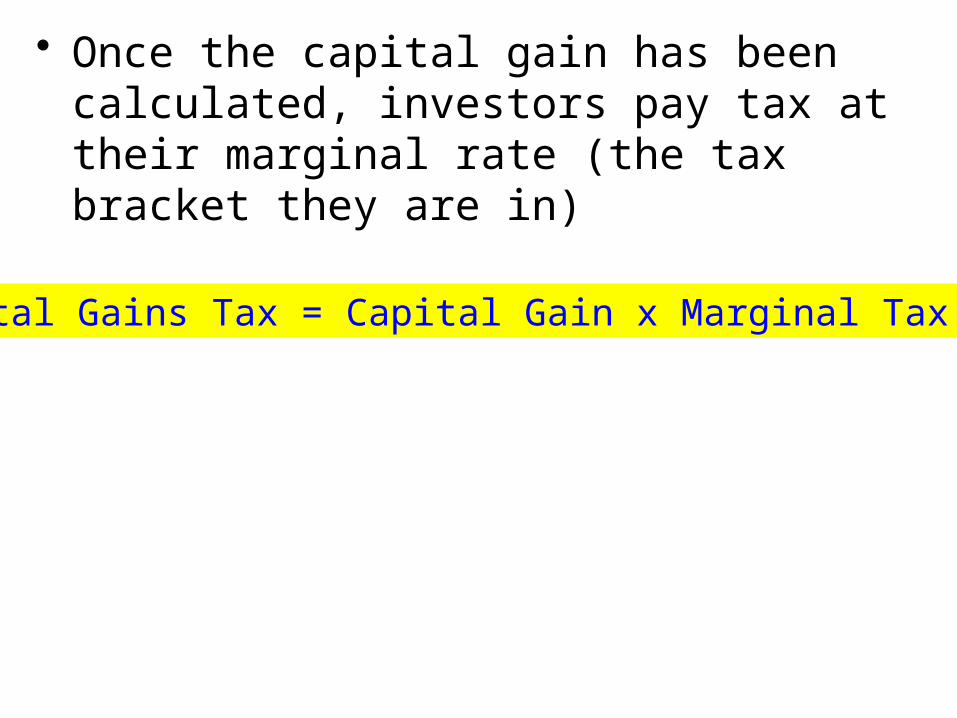

• Once the capital gain has been calculated, investors pay tax at their marginal rate (the tax bracket they are in)

Capital Gains Tax = Capital Gain x Marginal Tax Rate

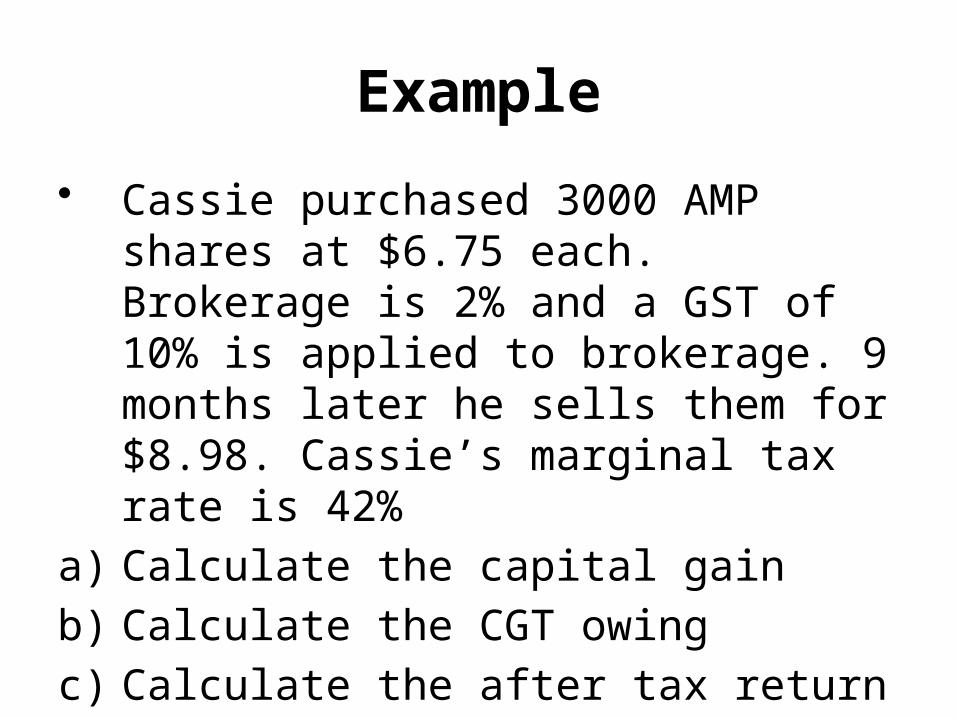

Example

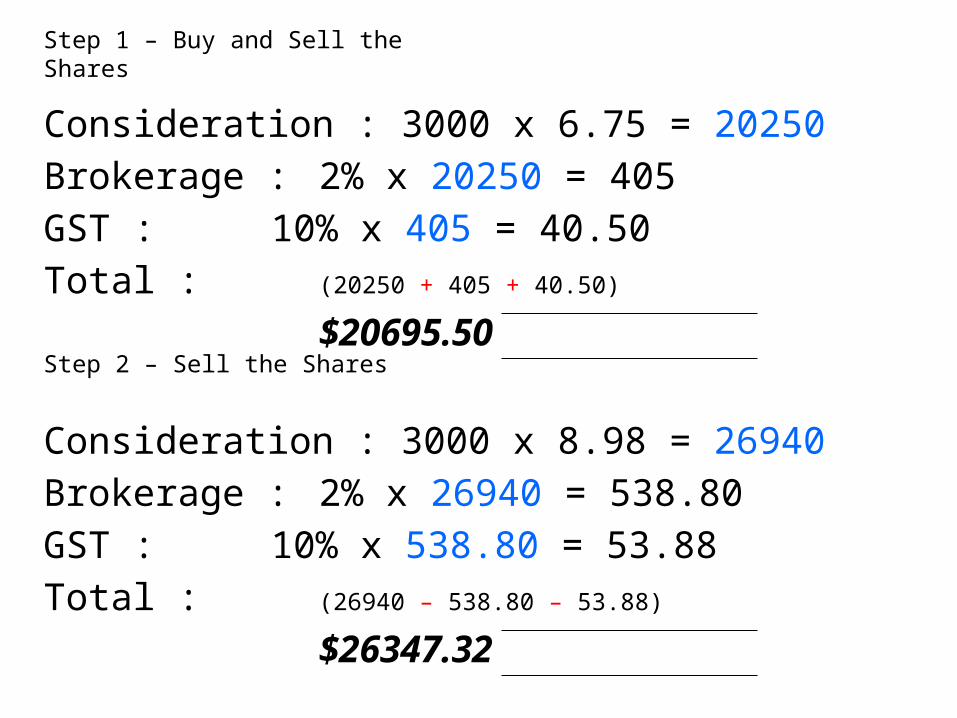

• Cassie purchased 3000 AMP shares at $6.75 each. Brokerage is 2% and a GST of 10% is applied to brokerage. 9 months later he sells them for $8.98. Cassie’s marginal tax rate is 42%

a) Calculate the capital gain

b) Calculate the CGT owing

c) Calculate the after tax return

Consideration : 3000 x 6.75 = 20250

Brokerage : 2% x 20250 = 405

GST : 10% x 405 = 40.50

Total : (20250 + 405 + 40.50)

$20695.50

Step 1 – Buy and Sell the Shares

Consideration : 3000 x 8.98 = 26940

Brokerage : 2% x 26940 = 538.80

GST : 10% x 538.80 = 53.88

Total : (26940 – 538.80 – 53.88)

$26347.32

Step 2 – Sell the Shares

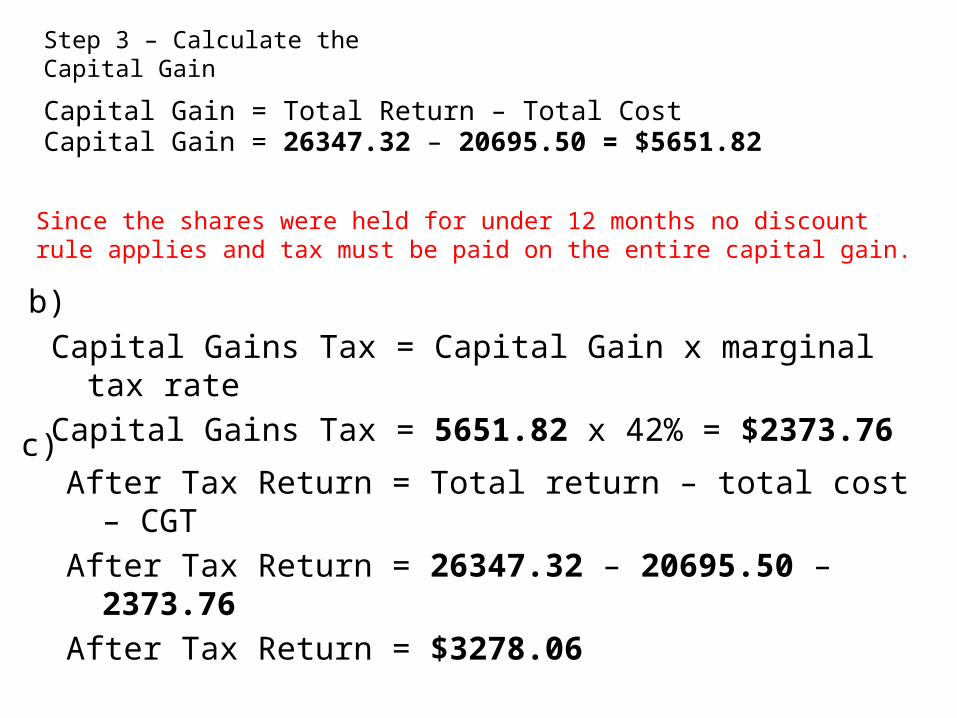

Capital Gain = Total Return – Total CostCapital Gain = 26347.32 – 20695.50 = $5651.82

Step 3 – Calculate the Capital Gain

Capital Gains Tax = Capital Gain x marginal tax rate

Capital Gains Tax = 5651.82 x 42% = $2373.76

Since the shares were held for under 12 months no discount rule applies and tax must be paid on the entire capital gain.

b)

c)After Tax Return = Total return – total cost – CGT

After Tax Return = 26347.32 – 20695.50 – 2373.76

After Tax Return = $3278.06

Capital Losses• Most investors at some point make

poor decisions regarding investments and make a loss.

• The decision needs to be made to hold on to them and hopefully they will rise in value or sell them.

• If you sell them for less than you bought them for it is called a CAPITAL LOSS.

• A capital loss can be used to offset any capital gains – this reduces the amount of CGT payable.

• Capital losses are offset against the full value of any discountable capital gains. (i.e. before the 50% rule is applied)

• If your capital losses exceed your capital gains in a year – then the net capital loss (the amount left over) will be carried into the next financial year.

• It is best to offset the loss against any gain that the 50% rule doesn’t apply to.

Tax on Dividends

• Before 1987 a company would pay tax on their profits (dividends) and then you as a shareholder would pay tax on your income – so the Government was kind of getting 2 lots of tax out of one payment.

• DIVIDEND IMPUTATION - is a method that gives tax advantages to shareholders who receive dividends.

• FULLY FRANKED Dividends have the tax paid on them by the company at the company rate 30%.

• This means when you get the dividend tax has already been paid – giving you the possibility of :– not paying tax on the dividends– Paying reduced tax on the dividends– Getting money back in the form of a tax

return– Depending on your marginal tax rate

• If your marginal tax rate is below the company tax rate you will get a refund!

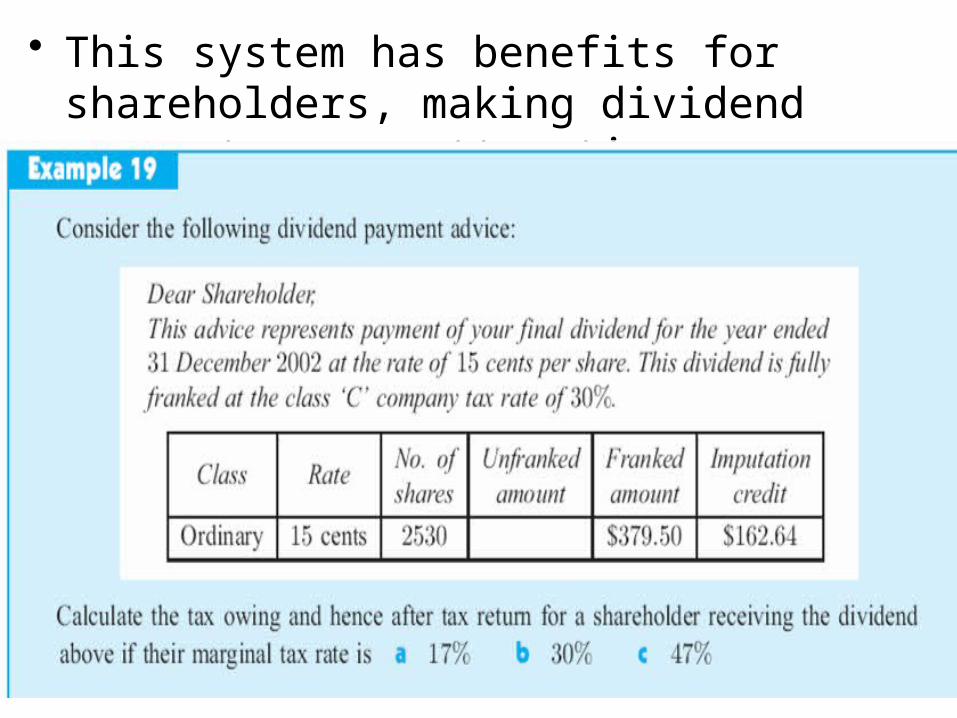

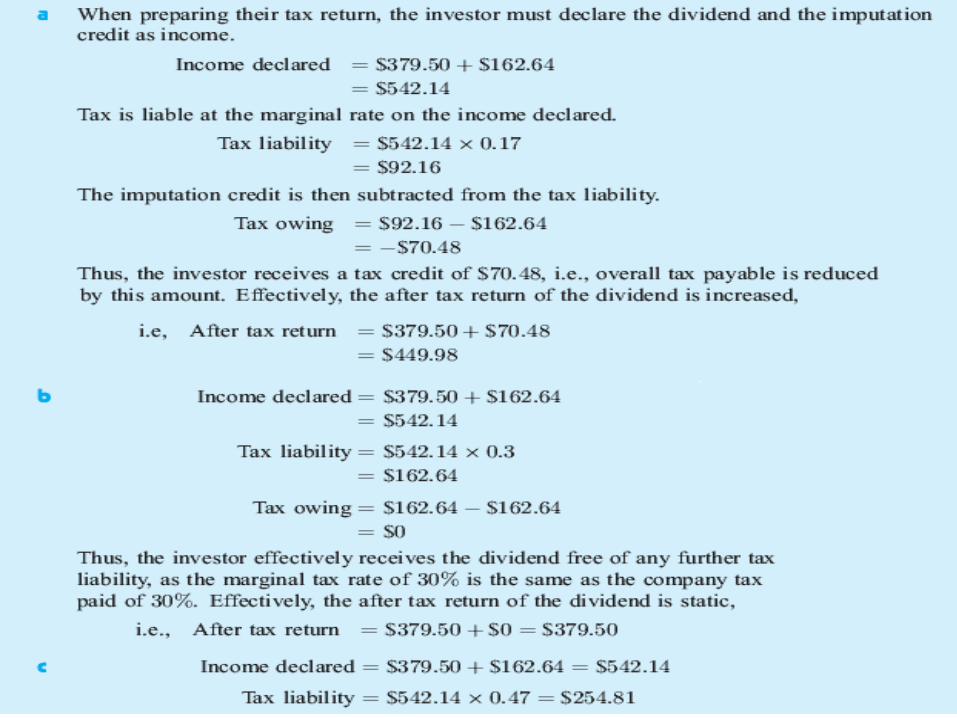

• This system has benefits for shareholders, making dividend payments more attractive.

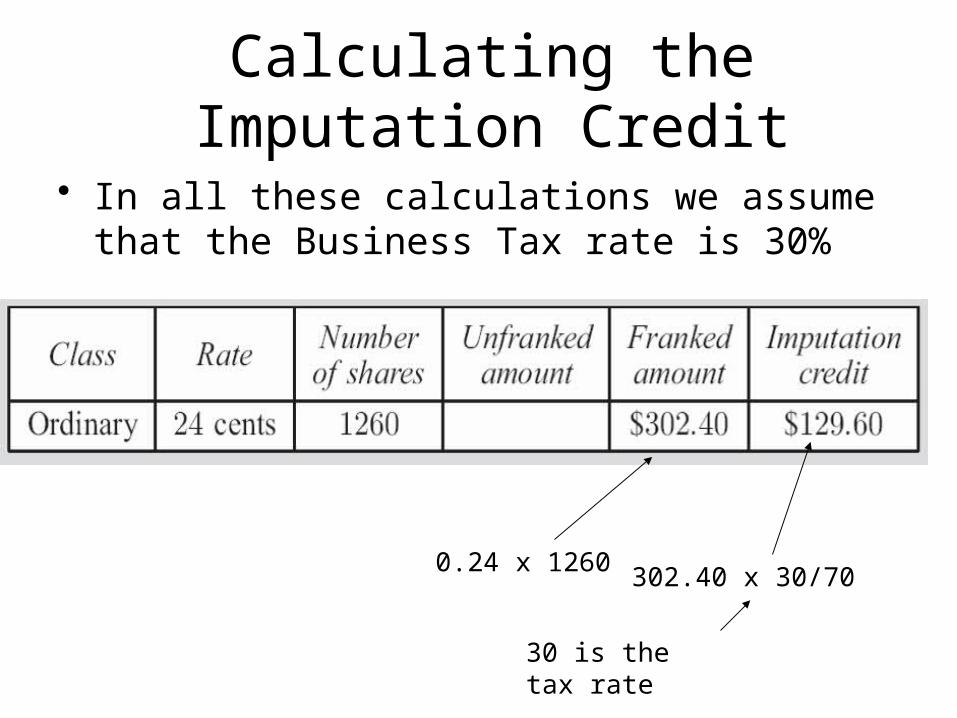

Calculating the Imputation Credit

• In all these calculations we assume that the Business Tax rate is 30%

0.24 x 1260 302.40 x 30/70

30 is the tax rate

Questions to Do• Page 12

–Exercise 7D.5• Q 1,2

• Page 12–Exercise 7D.6

• Q 1,2,3,5