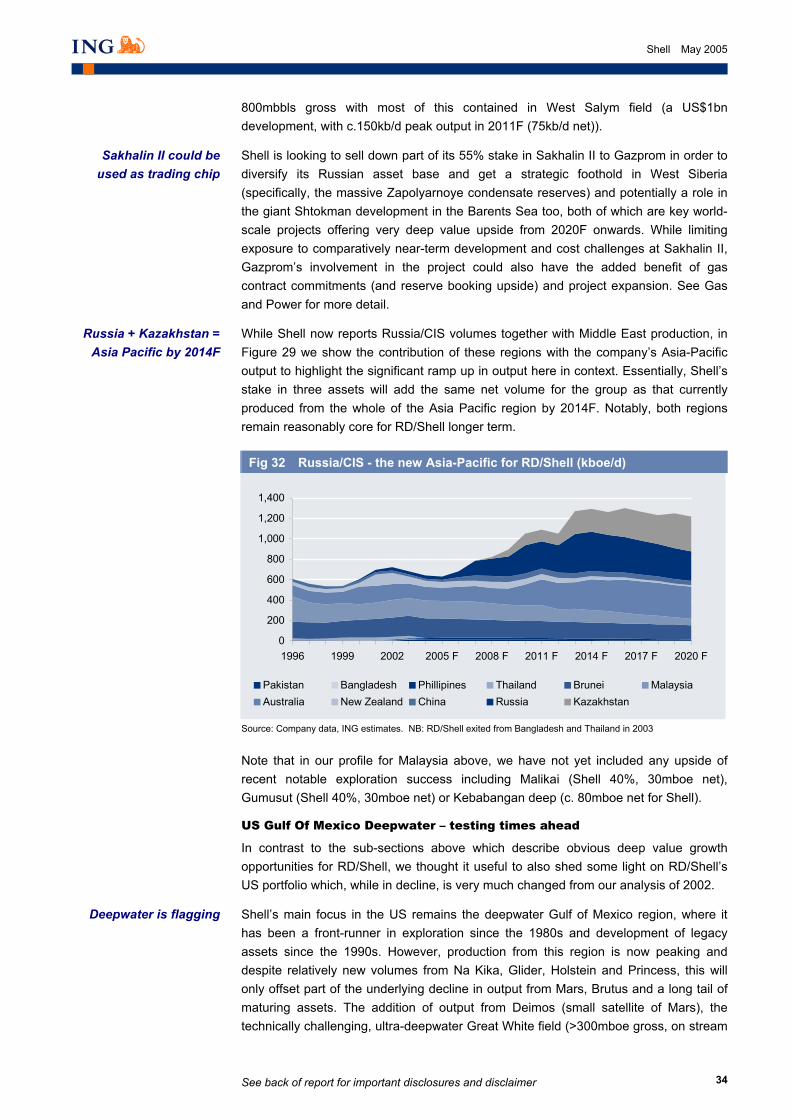

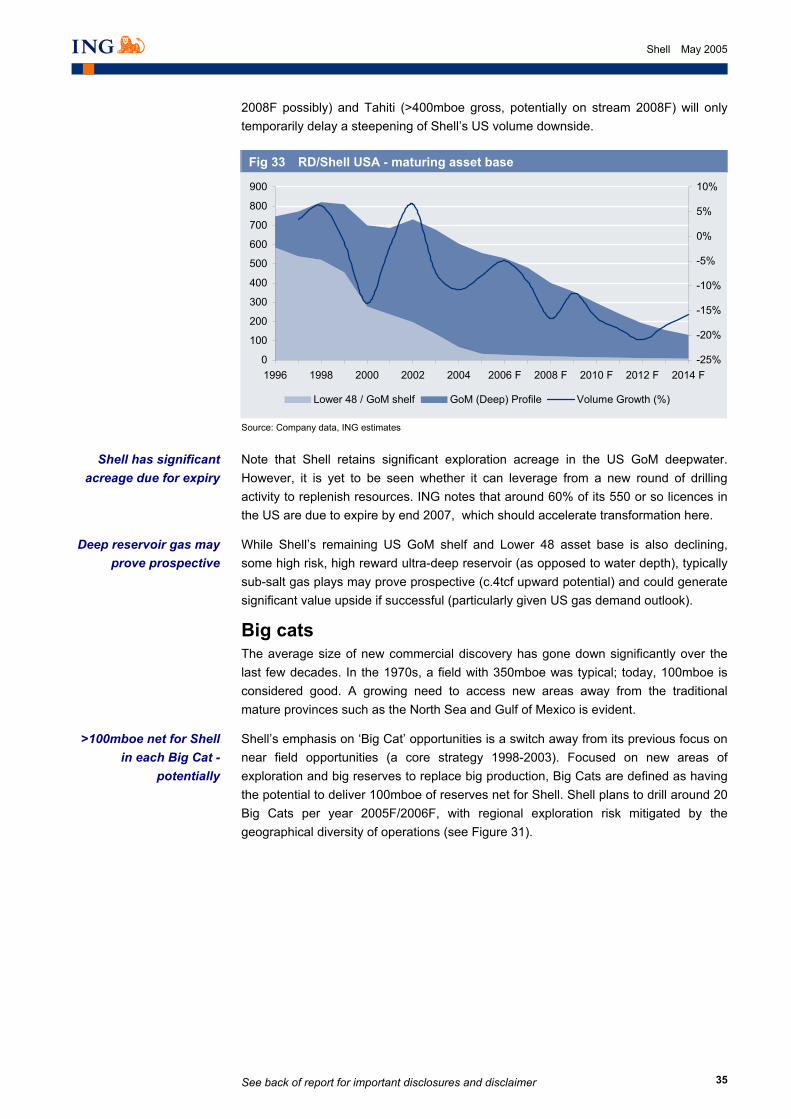

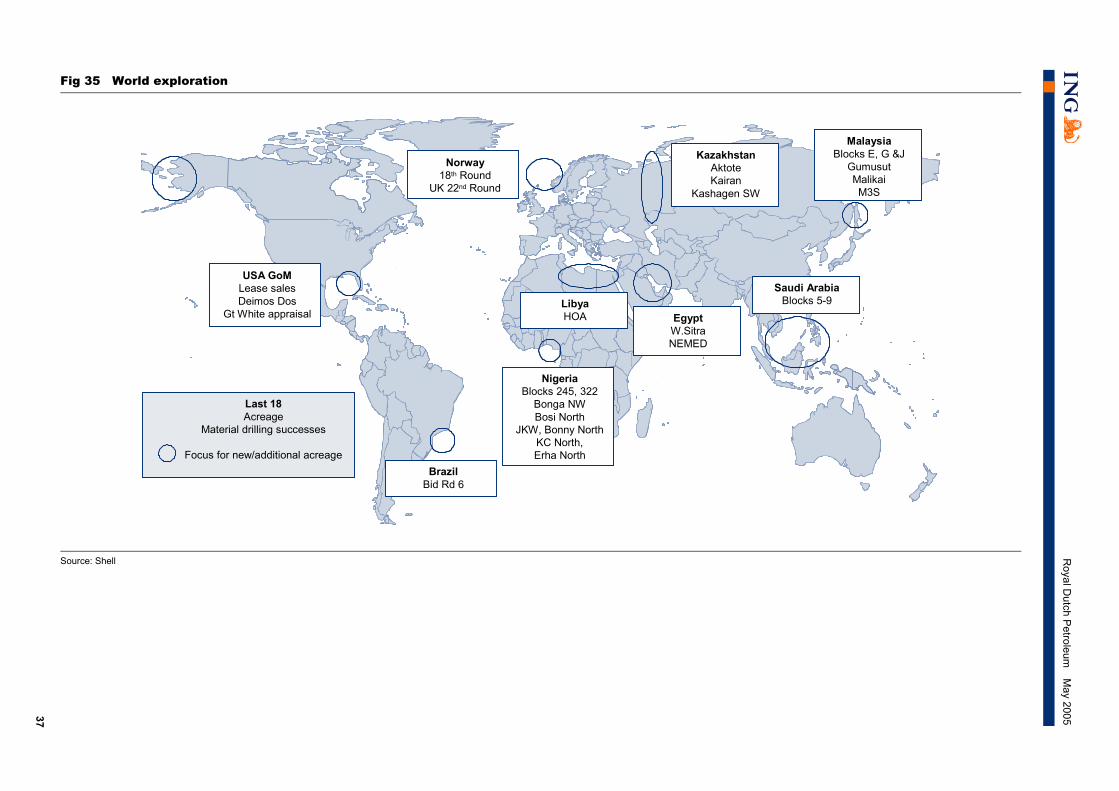

shell report

TRANSCRIPT

iiiiil EQUITY MARKETS

Oil & Gas Western Europe

Reserves no longer an issue but volumes modest ◆

Return to fundamental valuation expected post unification ◆

No real catalysts for growth until 2007/2008 ◆

Angus McPhail(44 131) 527 [email protected]

Jason Kenney(44 131) 527 [email protected]

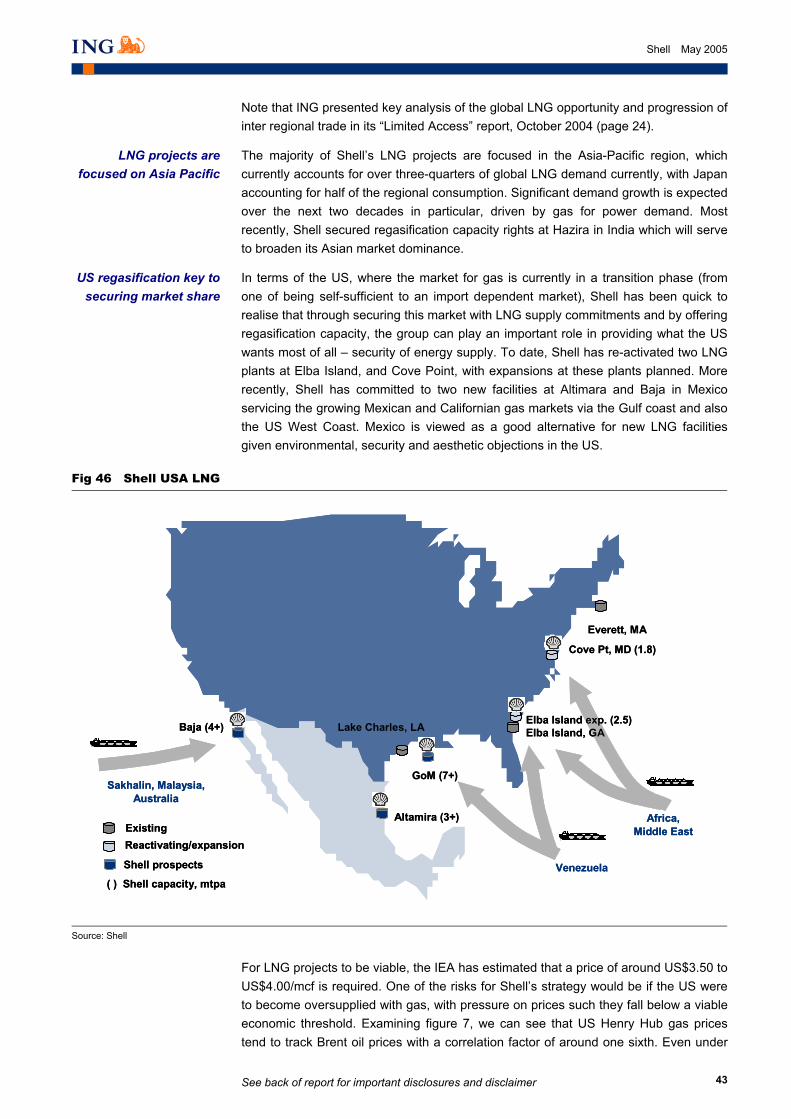

ShellThe long journey

May 2005

Sh

ell

May 2005

SEE THE DISCLOSURES APPENDIX FOR IMPORTANT DISCLOSURES AND ANALYST CERTIFICATION

AMSTERDAM BRUSSELS LONDON NEW YORK SINGAPORE Foppingadreef 7 Amsterdam Netherlands 1102BD

Avenue Marnix 24 Brussels Belgium B-1000

60 London Wall London United Kingdom EC2M 5TQ

1325 Avenue of the Americas New York USA 10019

19/F Republic Plaza, 9 Raffles Place, #19-02, Singapore 048619

Tel: 31 20 563 87 98 Tel: 32 2 557 10 26 Tel: 44 20 7767 1000 Tel: 1 646 424 6000 Tel: 65 6535 3688

BRATISLAVA

Tel: 421 2 5934 61 11

BUCHAREST

Tel: 40 21 222 1600

BUDAPEST

Tel: 36 1 268 0140

BUENOS AIRES

Tel: 54 11 4310 4700

DUBLIN

Tel: 353 1 638 4000

EDINBURGH

Tel: 44 131 527 3000

GENEVA

Tel: 41 22 593 8050

HONG KONG

Tel: 852 2848 8488

ISTANBUL

Tel: 90 212 258 8770

KIEV

Tel: 380 44 230 3030

MADRID

Tel: 34 91 789 8880

MANILA

Tel: 632 840 8888

MEXICO CITY

Tel: 52 55 5258 2000

MILAN

Tel: 39 02 89629 3660

MOSCOW

Tel: 7095 755 5400

PARIS

Tel: 33 1 56 39 31 41

PRAGUE

Tel: 420 2 5747 1111

SANTIAGO

Tel: 562 452 2700

SAO PAULO

Tel: 55 11 4504 6000

SEOUL

Tel: 822 317 1500

SHANGHAI

Tel: 86 21 6841 3355

SOFIA

Tel: 359 2 917 6400

TAIPEI

Tel: 886 2 2734 7500

TOKYO

Tel: 813 5210 1500

WARSAW

Tel: 48 22 820 5018

Disclaimer This publication has been prepared on behalf of ING (being for this purpose the wholesale and investment banking business of ING Bank NV and certain of its subsidiary companies) solely for the information of its clients. ING forms part of ING Group (being for this purpose ING Groep NV and its subsidiary and affiliated companies). It is not investment advice or an offer or solicitation for the purchase or sale of any financial instrument. While reasonable care has been taken to ensure that the information contained herein is not untrue or misleading at the time of publication, ING makes no representation that it is accurate or complete. The information contained herein is subject to change without notice. ING Group and any of its officers, employees, related and discretionary accounts may, to the extent not disclosed above and to the extent permitted by law, have long or short positions or may otherwise be interested in any transactions or investments (including derivatives) referred to in this publication. In addition, ING Group may provide banking, insurance or asset management services for, or solicit such business from, any company referred to in this publication. Neither ING nor any of its officers or employees accepts any liability for any direct or consequential loss arising from any use of this publication or its contents. Copyright and database rights protection exists in this publication and it may not be reproduced, distributed or published by any person for any purpose without the prior express consent of ING. All rights are reserved.

Any investments referred to herein may involve significant risk, are not necessarily available in all jurisdictions, may be illiquid and may not be suitable for all investors. The value of, or income from, any investments referred to herein may fluctuate and/or be affected by changes in exchange rates. Past performance is not indicative of future results. Investors should make their own investment decisions without relying on this publication. Only investors with sufficient knowledge and experience in financial matters to evaluate the merits and risks should consider an investment in any issuer or market discussed herein and other persons should not take any action on the basis of this publication. This publication is issued:1) in the United Kingdom only to persons described in Articles 19, 47 and 49 of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2001 and is not intended to be distributed, directly or indirectly, to any other class of persons (including private investors); 2) in Italy only to persons described in Article No. 31 of Consob Regulation No. 11522/98.Clients should contact analysts at, and execute transactions through, an ING entity in their home jurisdiction unless governing law permits otherwise.

ING Bank N.V., London branch is authorised by the Dutch Central Bank and regulated by the Financial Services Authority for the conduct of UK business. It is incorporated in the Netherlands and its London branch is registered in the UK (number BR000341) at 60 London Wall, London EC2M 5TQ. ING Financial Markets LLC, which is a member of the NYSE, NASD and SIPC and part of ING, has accepted responsibility for the distribution of this report in the United States under applicable requirements.

This document is classified as UK Independent Research as defined in the ING Bank London Branch Research policy drawn up in accordance with FSA Rule COB 7.16.5R (2).

EQ_UK IND Additional information is available on request

See back of report for important disclosures and disclaimer

1

Shell May 2005

Contents Summary 2

Indexation & valuation 3

Pros & cons 22

Exploration & production 24

Gas & power 41

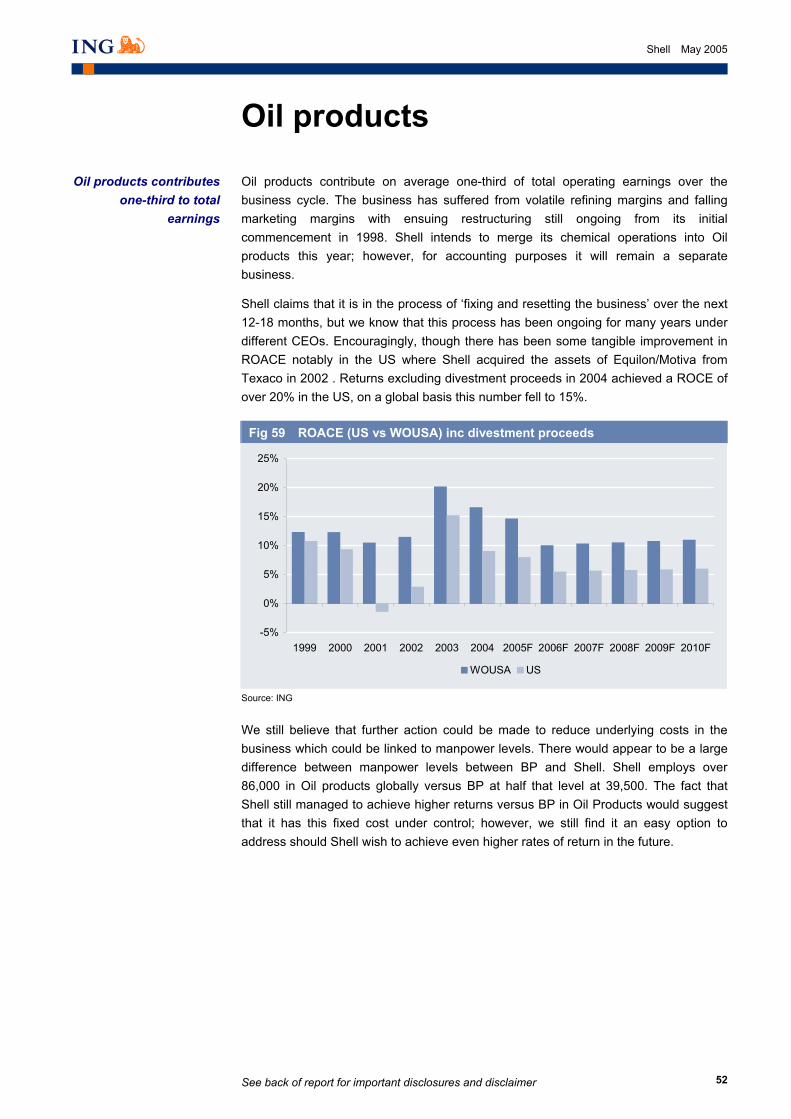

Oil products 52

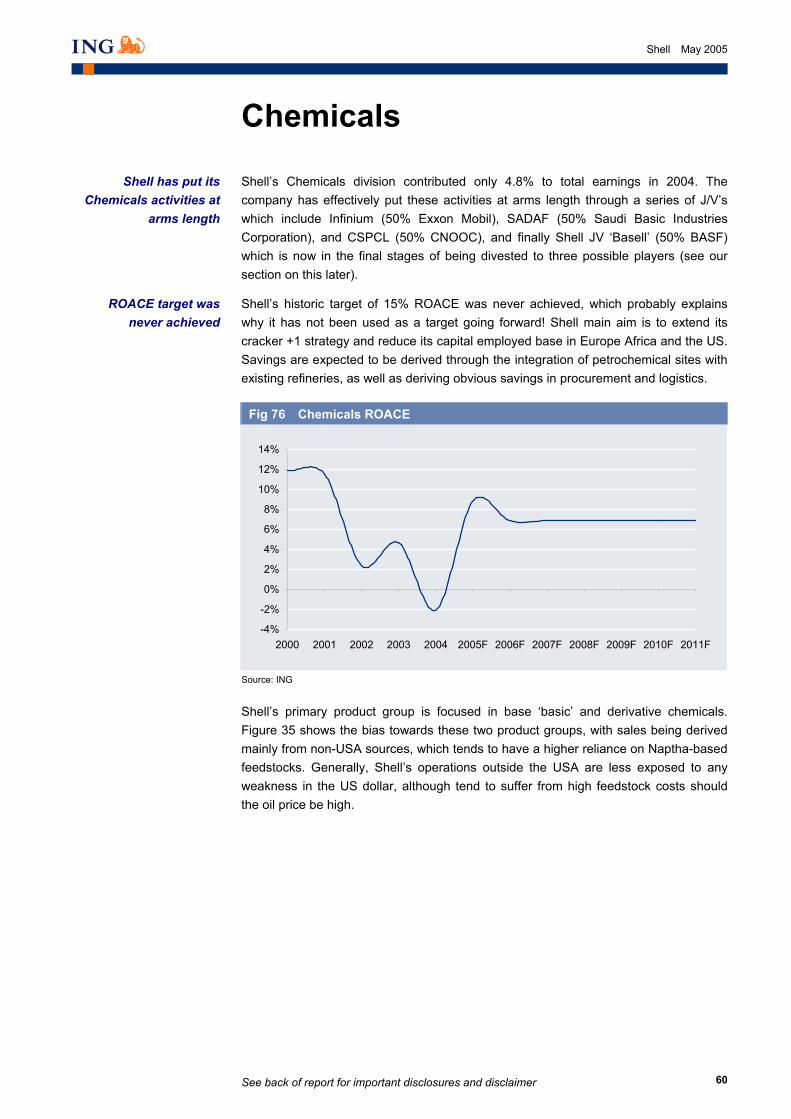

Chemicals 60

Others 62

Financials 66

Glossary 72

Conversion factors 73

Disclosures Appendix 74

Oil & Gas

Angus McPhail Edinburgh +44 (0)131 527 3029 [email protected]

Cover photo courtesy of NASA, Apollo 8 December 1968

Acknowledgement: Nadia Kappou, Doctoral Researcher, ISMA Centre, University of Reading.

See back of report for important disclosures and disclaimer 2

Shell May 2005

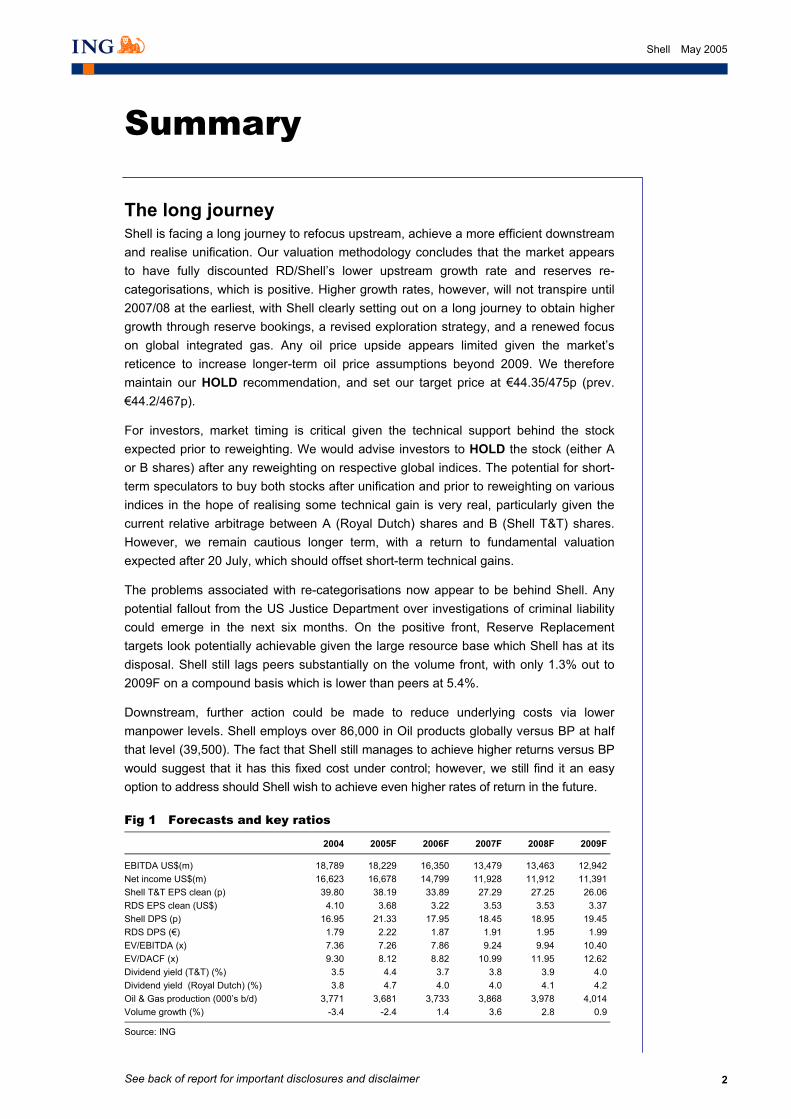

Summary

The long journey Shell is facing a long journey to refocus upstream, achieve a more efficient downstream and realise unification. Our valuation methodology concludes that the market appears to have fully discounted RD/Shell’s lower upstream growth rate and reserves re-categorisations, which is positive. Higher growth rates, however, will not transpire until 2007/08 at the earliest, with Shell clearly setting out on a long journey to obtain higher growth through reserve bookings, a revised exploration strategy, and a renewed focus on global integrated gas. Any oil price upside appears limited given the market’s reticence to increase longer-term oil price assumptions beyond 2009. We therefore maintain our HOLD recommendation, and set our target price at €44.35/475p (prev. €44.2/467p).

For investors, market timing is critical given the technical support behind the stock expected prior to reweighting. We would advise investors to HOLD the stock (either A or B shares) after any reweighting on respective global indices. The potential for short-term speculators to buy both stocks after unification and prior to reweighting on various indices in the hope of realising some technical gain is very real, particularly given the current relative arbitrage between A (Royal Dutch) shares and B (Shell T&T) shares. However, we remain cautious longer term, with a return to fundamental valuation expected after 20 July, which should offset short-term technical gains.

The problems associated with re-categorisations now appear to be behind Shell. Any potential fallout from the US Justice Department over investigations of criminal liability could emerge in the next six months. On the positive front, Reserve Replacement targets look potentially achievable given the large resource base which Shell has at its disposal. Shell still lags peers substantially on the volume front, with only 1.3% out to 2009F on a compound basis which is lower than peers at 5.4%.

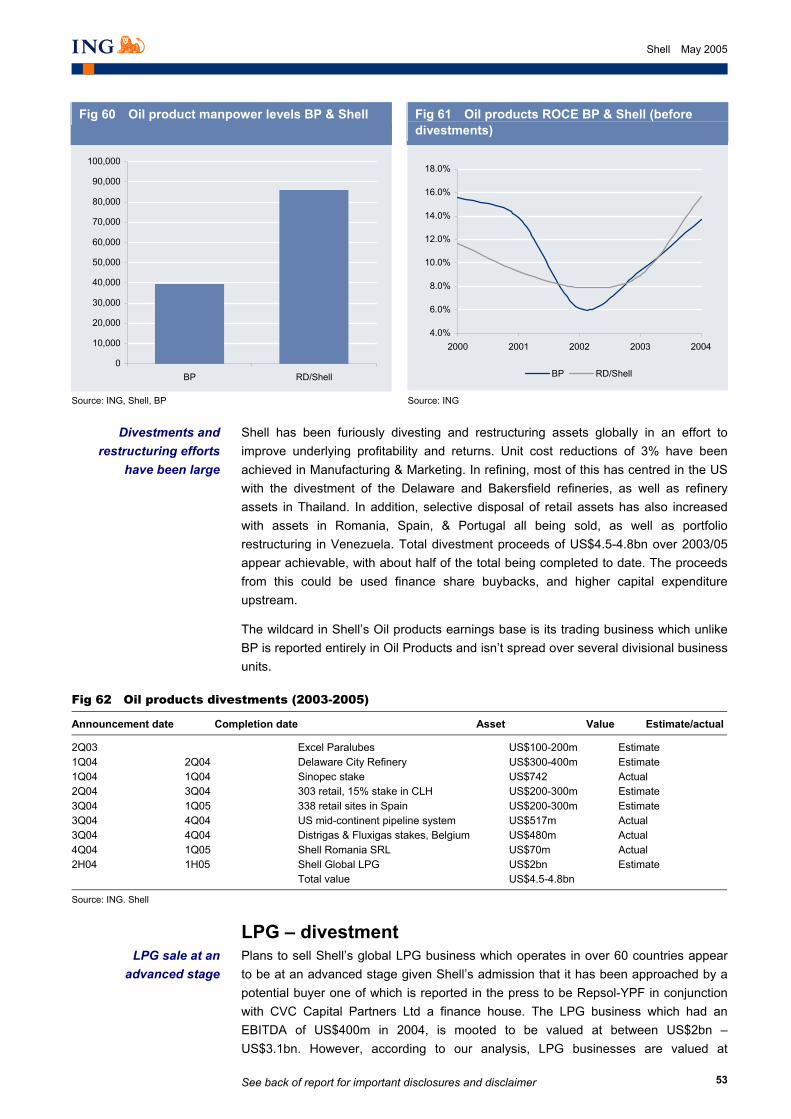

Downstream, further action could be made to reduce underlying costs via lower manpower levels. Shell employs over 86,000 in Oil products globally versus BP at half that level (39,500). The fact that Shell still manages to achieve higher returns versus BP would suggest that it has this fixed cost under control; however, we still find it an easy option to address should Shell wish to achieve even higher rates of return in the future.

Fig 1 Forecasts and key ratios

2004 2005F 2006F 2007F 2008F 2009F

EBITDA US$(m) 18,789 18,229 16,350 13,479 13,463 12,942 Net income US$(m) 16,623 16,678 14,799 11,928 11,912 11,391 Shell T&T EPS clean (p) 39.80 38.19 33.89 27.29 27.25 26.06 RDS EPS clean (US$) 4.10 3.68 3.22 3.53 3.53 3.37 Shell DPS (p) 16.95 21.33 17.95 18.45 18.95 19.45 RDS DPS (€) 1.79 2.22 1.87 1.91 1.95 1.99 EV/EBITDA (x) 7.36 7.26 7.86 9.24 9.94 10.40 EV/DACF (x) 9.30 8.12 8.82 10.99 11.95 12.62 Dividend yield (T&T) (%) 3.5 4.4 3.7 3.8 3.9 4.0 Dividend yield (Royal Dutch) (%) 3.8 4.7 4.0 4.0 4.1 4.2 Oil & Gas production (000’s b/d) 3,771 3,681 3,733 3,868 3,978 4,014 Volume growth (%) -3.4 -2.4 1.4 3.6 2.8 0.9

Source: ING

See back of report for important disclosures and disclaimer

3

Shell May 2005

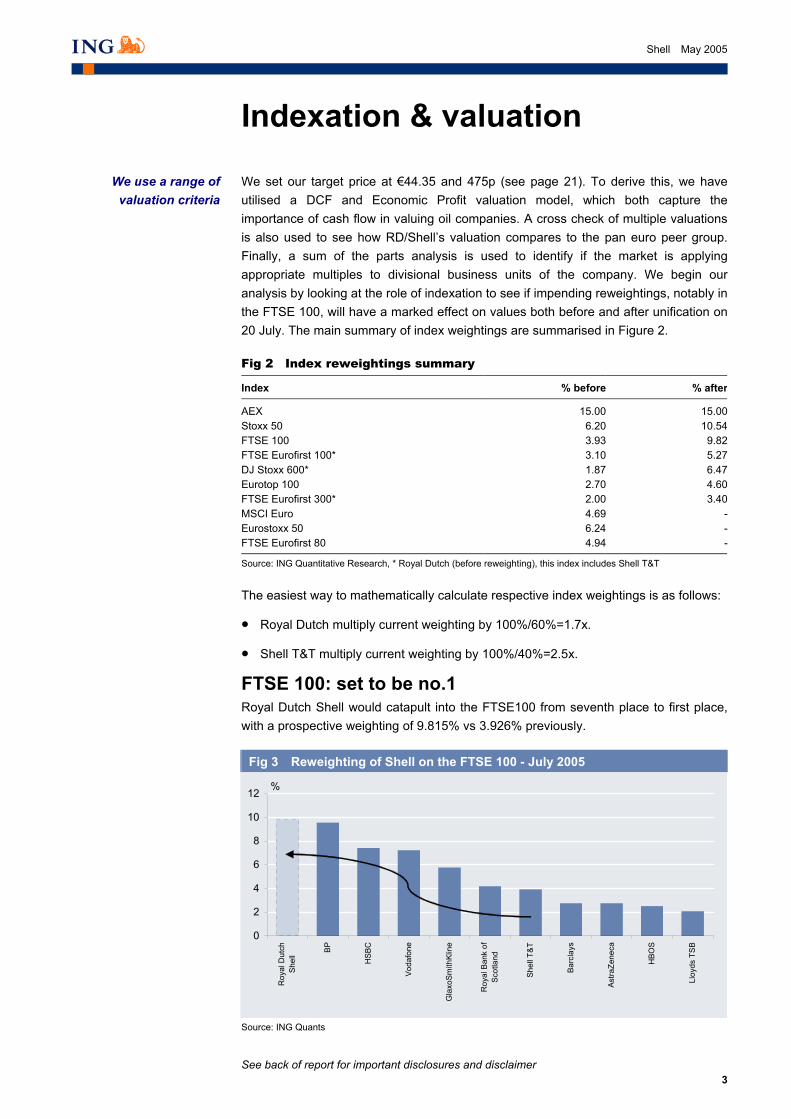

Indexation & valuation

We set our target price at €44.35 and 475p (see page 21). To derive this, we have utilised a DCF and Economic Profit valuation model, which both capture the importance of cash flow in valuing oil companies. A cross check of multiple valuations is also used to see how RD/Shell’s valuation compares to the pan euro peer group. Finally, a sum of the parts analysis is used to identify if the market is applying appropriate multiples to divisional business units of the company. We begin our analysis by looking at the role of indexation to see if impending reweightings, notably in the FTSE 100, will have a marked effect on values both before and after unification on 20 July. The main summary of index weightings are summarised in Figure 2.

Fig 2 Index reweightings summary

Index % before % after

AEX 15.00 15.00Stoxx 50 6.20 10.54FTSE 100 3.93 9.82FTSE Eurofirst 100* 3.10 5.27DJ Stoxx 600* 1.87 6.47Eurotop 100 2.70 4.60FTSE Eurofirst 300* 2.00 3.40MSCI Euro 4.69 -Eurostoxx 50 6.24 -FTSE Eurofirst 80 4.94 -

Source: ING Quantitative Research, * Royal Dutch (before reweighting), this index includes Shell T&T

_

The easiest way to mathematically calculate respective index weightings is as follows:

• Royal Dutch multiply current weighting by 100%/60%=1.7x.

• Shell T&T multiply current weighting by 100%/40%=2.5x.

FTSE 100: set to be no.1 Royal Dutch Shell would catapult into the FTSE100 from seventh place to first place, with a prospective weighting of 9.815% vs 3.926% previously.

Fig 3 Reweighting of Shell on the FTSE 100 - July 2005

0

2

4

6

8

10

12

Roy

al D

utch

Shel

l BP

HSB

C

Voda

fone

Gla

xoSm

ithKl

ine

Roy

al B

ank

ofSc

otla

nd

Shel

l T&T

Barc

lays

Astra

Zene

ca

HBO

S

Lloy

ds T

SB

%

Source: ING Quants

_

We use a range of valuation criteria

See back of report for important disclosures and disclaimer

4

Shell May 2005

Four central questions are crucial to understanding what may follow Shell’s reweighting on the FTSE100:

• Has the indexation effect been fully factored into current valuations?

The full effect on the FTSE has yet to be factored in. Index tracking funds have a legal requirement to wait until the effective date. There has been some evidence of hedge funds buying options ahead of the re-weighting last October, which may have accounted for the rally in the stock. Academic studies1 have shown that stock liquidity implies speculators may trade in advance of the announcement, while index trackers trade between the announcement and effective dates. There is strong evidence to suggest that stocks exhibit cumulative abnormal returns (CAR) 17 days prior to the effective date, or around 3 July given the effective date is 20 July. This equates to 4.7% CAR after adjusting for market returns.

• What may happen to the new entities valuation after 20 July?

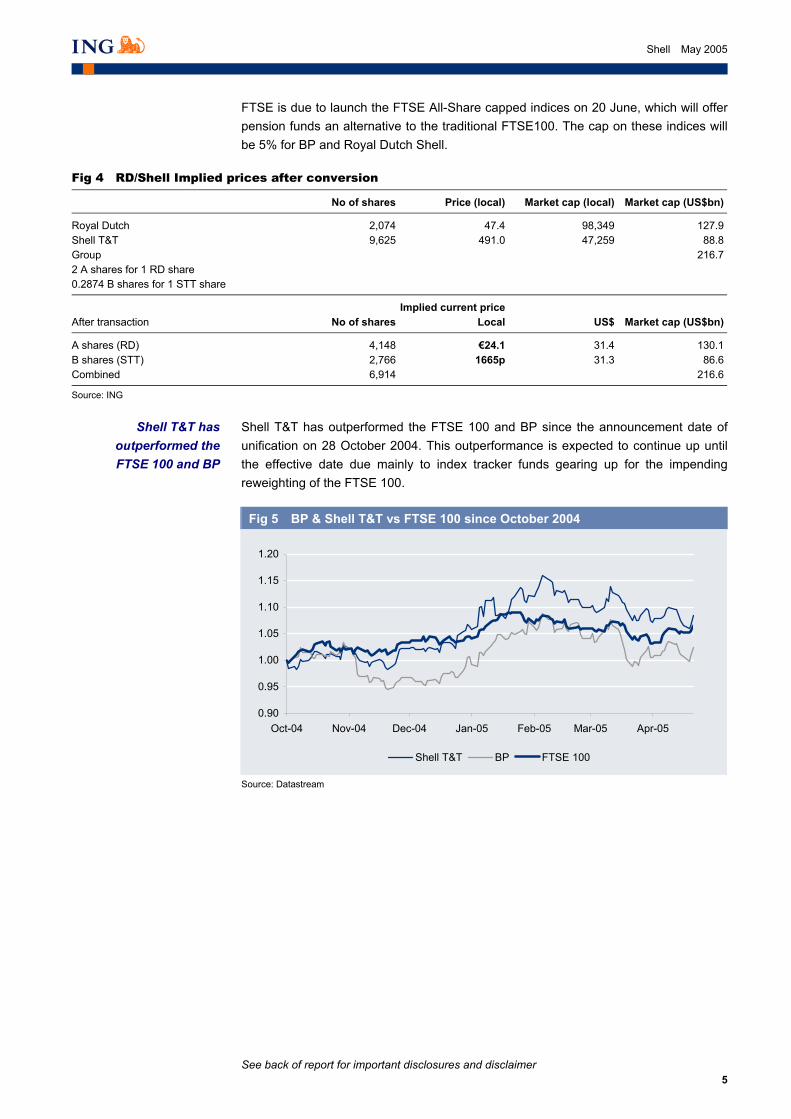

Figure 4 shows that the prospective price of Royal Dutch Shell in London and Amsterdam is 1665p and €24.1 respectively. The UK’s lower equity risk premium relative to the European market should help stabilise Royal Dutch Shell’s stock price longer term.

Recent academic research on the FTSE1002 points towards insignificant returns between the announcement date, and 120 days after the effective date (AD+120), or in this case 17 November 2005. A recent academic study by Brunel University indicated that AD+120 a CAR of 1.63% was achieved. After adjusting for information and press coverage effects, as well as financial (EPS changes), the firm age and other adjustments, this return falls to 0.81%. These studies only analysed for inclusion and exclusion from the index, but do not examine the effect on current index constituents. Given the fact that Shell T&T is currently a large market constituent of the FTSE 100, with a high stock liquidity inferred by low transaction costs and a high degree of publicly-available information, the CAR could be higher given the size and liquidity of Shell T&T.

ING consider fundamental rather than technical effects to be paramount after the effective date – the ongoing legal risks through the US Justice department and other legal authorities, the low growth profile, rising cost base upstream, and obvious unit cost restructuring potential downstream. We advise investors to exercise caution and not be carried way with what amounts to a short-term technical rally.

• Will the FTSE 100 automatically be re-weighted on 20 July?

FTSE 100 Index reviews have occurred in the second weeks of March, June, September and December with changes being applied on the Monday after the third Friday of the same month. This means that there are seven days from the review date through to the effective date, being 20 July. FTSE have confirmed that given the size of the re-weighting, changes will be implemented automatically and not subjected to the usual time schedule.

• How can investors in the FTSE limit their risk given the large weighting of Royal Dutch Shell?

1 Dr Bryan Mase, Brunel University, ‘The Impact of Changes in the FTSE 100 Index’ 2 Jay Dahya, Baruch College, City University of New York ‘Playing Footsy with the FTSE 100 Index’, March 2005

Cumulative abnormal returns expected ahead

of unification

ING cautious after unification

See back of report for important disclosures and disclaimer

5

Shell May 2005

FTSE is due to launch the FTSE All-Share capped indices on 20 June, which will offer pension funds an alternative to the traditional FTSE100. The cap on these indices will be 5% for BP and Royal Dutch Shell.

Fig 4 RD/Shell Implied prices after conversion

No of shares Price (local) Market cap (local) Market cap (US$bn)

Royal Dutch 2,074 47.4 98,349 127.9Shell T&T 9,625 491.0 47,259 88.8Group 216.72 A shares for 1 RD share 0.2874 B shares for 1 STT share

Implied current price After transaction No of shares Local US$ Market cap (US$bn)

A shares (RD) 4,148 €24.1 31.4 130.1B shares (STT) 2,766 1665p 31.3 86.6Combined 6,914 216.6

Source: ING

_

Shell T&T has outperformed the FTSE 100 and BP since the announcement date of unification on 28 October 2004. This outperformance is expected to continue up until the effective date due mainly to index tracker funds gearing up for the impending reweighting of the FTSE 100.

Fig 5 BP & Shell T&T vs FTSE 100 since October 2004

0.90

0.95

1.00

1.05

1.10

1.15

1.20

Oct-04 Nov-04 Dec-04 Jan-05 Feb-05 Mar-05 Apr-05

Shell T&T BP FTSE 100

Source: Datastream

_

Shell T&T has outperformed the FTSE 100 and BP

See back of report for important disclosures and disclaimer

6

Shell May 2005

AEX: implications Royal Dutch Shell’s weighting moved on 2 March from 10% to 15%. No change in this is expected after the new entity is formed. Under the scenario of A shares being predominantly traded in London as opposed to Amsterdam, under AEX listing rules at least 10% of total turnover in a stock should be executed on the exchange. If we were to suppose that the majority of trades were executed in London, then this could potentially lead to Royal Dutch Shell being excluded form the AEX.

In addition, the AEX also specifies that at least 25% of the issued shares of a security should be freely available for trading (“free float”) at Euronext Amsterdam. However, a security may nevertheless be included in the index if its free float, although less than 25%, ‘equals, or is greater than, the free float of the security which ranks 25th on Euronext Amsterdam in terms of free float market capitalisation.’

Under either scenario, ING consider it likely that the AEX inclusion rules would probably change. In addition, some European investors may be unwilling to trade in London given the stamp duty levy.

Other indices RD Shell will be deleted from the MSCI NL and MSCI EMU indices. As the MSCI uses so-called 'building blocks', all individual indices can be added to form a larger index. As RD Shell will be a constituent of the UK indices for the full market cap weight, it cannot be a constituent anymore for the Dutch or Euroland indices, otherwise it would be counted twice. It will also be deleted from the DJ EuroStoxx 50 index which does not include UK-based stocks, although will remain in the Stoxx 50 index which does. Examining the FTSE Eurotop 100, Shell’s weighting will increase from 2.7% to 4.6%.

The AEX will remain the same

Some deletions will occur by virtue of the

UK primary listing

See back of report for important disclosures and disclaimer

7

Shell May 2005

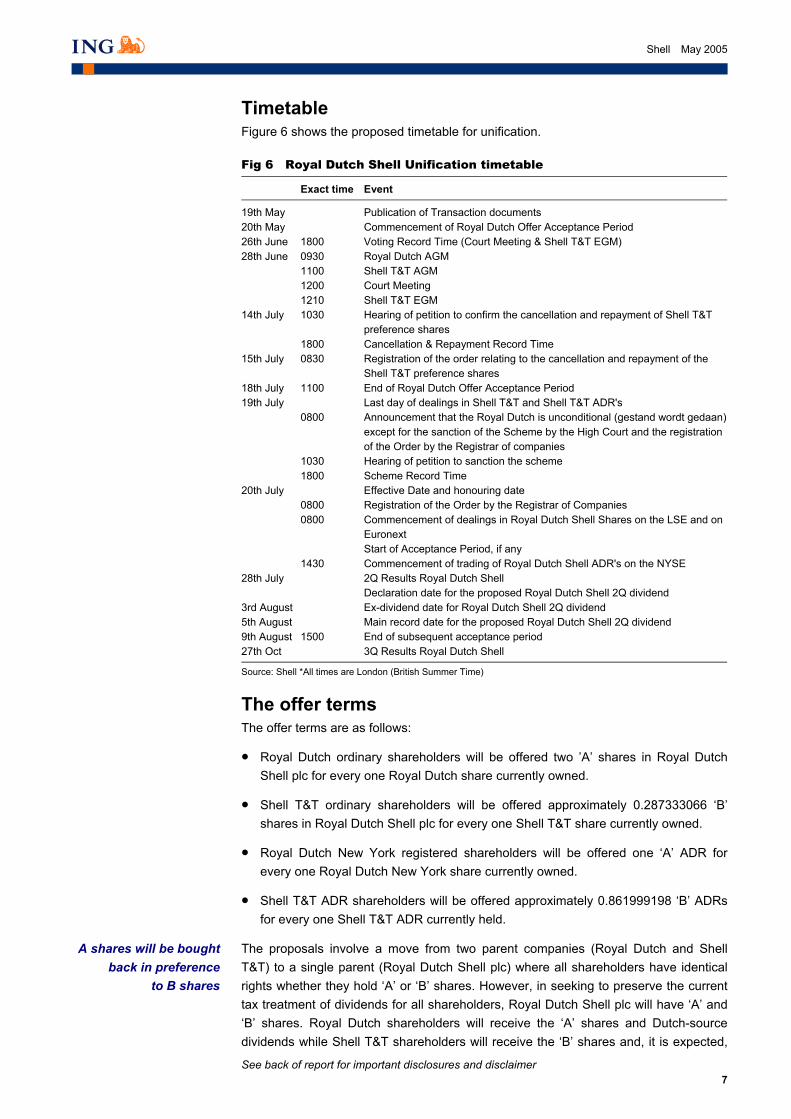

Timetable Figure 6 shows the proposed timetable for unification.

Fig 6 Royal Dutch Shell Unification timetable

Exact time Event

19th May Publication of Transaction documents 20th May Commencement of Royal Dutch Offer Acceptance Period 26th June 1800 Voting Record Time (Court Meeting & Shell T&T EGM) 28th June 0930 Royal Dutch AGM 1100 Shell T&T AGM 1200 Court Meeting 1210 Shell T&T EGM 14th July 1030 Hearing of petition to confirm the cancellation and repayment of Shell T&T

preference shares 1800 Cancellation & Repayment Record Time 15th July 0830 Registration of the order relating to the cancellation and repayment of the

Shell T&T preference shares 18th July 1100 End of Royal Dutch Offer Acceptance Period 19th July Last day of dealings in Shell T&T and Shell T&T ADR's 0800 Announcement that the Royal Dutch is unconditional (gestand wordt gedaan)

except for the sanction of the Scheme by the High Court and the registration of the Order by the Registrar of companies

1030 Hearing of petition to sanction the scheme 1800 Scheme Record Time 20th July Effective Date and honouring date 0800 Registration of the Order by the Registrar of Companies 0800 Commencement of dealings in Royal Dutch Shell Shares on the LSE and on

Euronext Start of Acceptance Period, if any 1430 Commencement of trading of Royal Dutch Shell ADR's on the NYSE 28th July 2Q Results Royal Dutch Shell Declaration date for the proposed Royal Dutch Shell 2Q dividend 3rd August Ex-dividend date for Royal Dutch Shell 2Q dividend 5th August Main record date for the proposed Royal Dutch Shell 2Q dividend 9th August 1500 End of subsequent acceptance period 27th Oct 3Q Results Royal Dutch Shell

Source: Shell *All times are London (British Summer Time)

_

The offer terms The offer terms are as follows:

• Royal Dutch ordinary shareholders will be offered two ’A’ shares in Royal Dutch Shell plc for every one Royal Dutch share currently owned.

• Shell T&T ordinary shareholders will be offered approximately 0.287333066 ‘B’ shares in Royal Dutch Shell plc for every one Shell T&T share currently owned.

• Royal Dutch New York registered shareholders will be offered one ‘A’ ADR for every one Royal Dutch New York share currently owned.

• Shell T&T ADR shareholders will be offered approximately 0.861999198 ‘B’ ADRs for every one Shell T&T ADR currently held.

The proposals involve a move from two parent companies (Royal Dutch and Shell T&T) to a single parent (Royal Dutch Shell plc) where all shareholders have identical rights whether they hold ‘A’ or ‘B’ shares. However, in seeking to preserve the current tax treatment of dividends for all shareholders, Royal Dutch Shell plc will have ‘A’ and ‘B’ shares. Royal Dutch shareholders will receive the ‘A’ shares and Dutch-source dividends while Shell T&T shareholders will receive the ‘B’ shares and, it is expected,

A shares will be bought back in preference

to B shares

See back of report for important disclosures and disclaimer

8

Shell May 2005

UK source dividends. This has been done to reflect the different tax treatment in the two countries, with A shares being subject to Dutch withholding tax, and B shares to UK base stamp duty.

Both ‘A’ and ‘B’ shares will be listed on the London Stock Exchange and the Euronext Amsterdam Exchange as well as the New York Stock Exchange (in ADR form). The shares are not fungible/interchangeable. Although they are not interchangeable, they have identical rights. The only difference between the ‘A’ and ‘B’ shares is that holders of the ‘A’ shares will receive Dutch sourced dividends which are paid in euros and Holders of the ‘B’ shares are expected to receive UK-sourced dividends paid in Pounds Sterling.

The company has stated clearly that it intends to buy back A shares over B shares depending on ‘prevailing market prices and the relative tax treatment’, although recently there did appear to be some speculation that B shares would not be subjected to UK taxes which would put both classes of share on a level playing field for share buybacks. The upper limits on Shell's ability to buy back A (RD) shares under Dutch tax law are governed by Article 4c ‘Wet op Dividendbelasting' which allows companies to buy back shares if the company increases dividends, and secondly does not buy back more than 10 times the average cash dividend payment over a specified five-year period. Shell can easily satisfy both criteria, given the fact that its dividend policy has achieved consistent growth in dividends, and secondly total dividends paid amount to around US$36bn over the last five years, some seven-12 times higher than the proposed dividend.

The 95% acceptance level for Royal Dutch shareholders looks ambitious. Although given the wording in the Royal Dutch offer document under 'Other Risk factors' one could draw the opinion that Shell is banking on shareholders taking fright and converting anyway. An extended offer period for those classes of shareholders not converting does look a very real possibility.

With the euphoria over the new entity ‘Royal Dutch Shell’, the company may aim to scrap A shares at some stage in the future, which in our view could be linked to the European taxation convergence which could see Dutch withholding taxes applied in the UK instead of the current stamp duty. This issue is of course highly speculative and any convergence appears unlikely, particularly given the UK stance over the adoption of the euro.

One point of concern involves UK-based retail investors who will not qualify for UK rollover tax relief, with the Inland Revenue treating the transfer of shares as a disposal. This means that for retail investors in Shell T&T the transaction will be treated as a capital gains tax liability. Shell has clearly opted for the greater good principle whereby only certain classes of UK funds will be exempt such as Pension Funds, Investment Trusts, and OEICs. Retail investors account for only about 18% of Shell T&T current shareholder base.

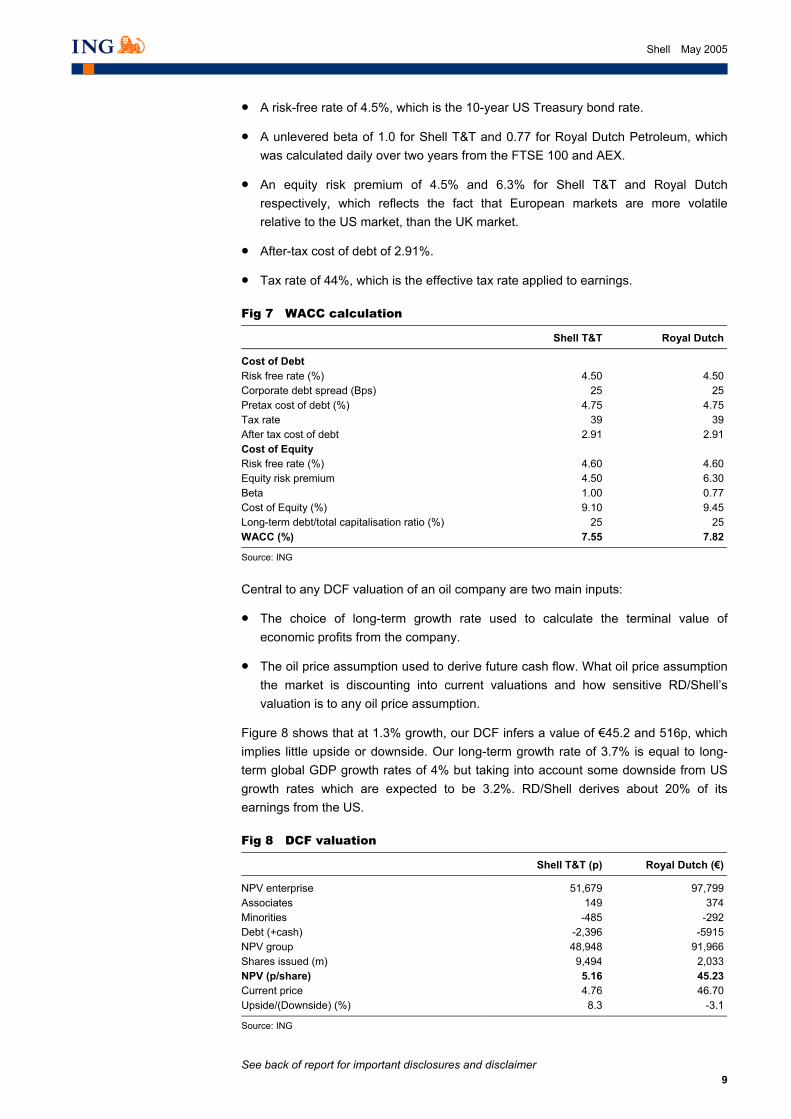

DCF Our DCF model utilises the weighted average cost of capital (WACC) over 50 years in order to capture the time value of money. Shell has low levels of gearing; in fact, it is sub-optimal since net debt is now negative given the high excess cash base. This means that the WACC is effectively the cost of equity.

In calculating our WACC of 6.8%, we assumed the following:

A shares may be scrapped at some point

in the future

We have utilised a DCF model over 50 years

UK retail investors will not qualify for tax relief

The 95% acceptance level looks ambitious

A shares may be bought back in preference

to B shares

There will be A shares and B shares

See back of report for important disclosures and disclaimer

9

Shell May 2005

• A risk-free rate of 4.5%, which is the 10-year US Treasury bond rate.

• A unlevered beta of 1.0 for Shell T&T and 0.77 for Royal Dutch Petroleum, which was calculated daily over two years from the FTSE 100 and AEX.

• An equity risk premium of 4.5% and 6.3% for Shell T&T and Royal Dutch respectively, which reflects the fact that European markets are more volatile relative to the US market, than the UK market.

• After-tax cost of debt of 2.91%.

• Tax rate of 44%, which is the effective tax rate applied to earnings.

Fig 7 WACC calculation

Shell T&T Royal Dutch

Cost of Debt Risk free rate (%) 4.50 4.50Corporate debt spread (Bps) 25 25Pretax cost of debt (%) 4.75 4.75Tax rate 39 39After tax cost of debt 2.91 2.91Cost of Equity Risk free rate (%) 4.60 4.60Equity risk premium 4.50 6.30Beta 1.00 0.77Cost of Equity (%) 9.10 9.45Long-term debt/total capitalisation ratio (%) 25 25WACC (%) 7.55 7.82

Source: ING

_

Central to any DCF valuation of an oil company are two main inputs:

• The choice of long-term growth rate used to calculate the terminal value of economic profits from the company.

• The oil price assumption used to derive future cash flow. What oil price assumption the market is discounting into current valuations and how sensitive RD/Shell’s valuation is to any oil price assumption.

Figure 8 shows that at 1.3% growth, our DCF infers a value of €45.2 and 516p, which implies little upside or downside. Our long-term growth rate of 3.7% is equal to long-term global GDP growth rates of 4% but taking into account some downside from US growth rates which are expected to be 3.2%. RD/Shell derives about 20% of its earnings from the US.

Fig 8 DCF valuation

Shell T&T (p) Royal Dutch (€)

NPV enterprise 51,679 97,799 Associates 149 374Minorities -485 -292Debt (+cash) -2,396 -5915NPV group 48,948 91,966 Shares issued (m) 9,494 2,033NPV (p/share) 5.16 45.23Current price 4.76 46.70Upside/(Downside) (%) 8.3 -3.1

Source: ING

_

See back of report for important disclosures and disclaimer

10

Shell May 2005

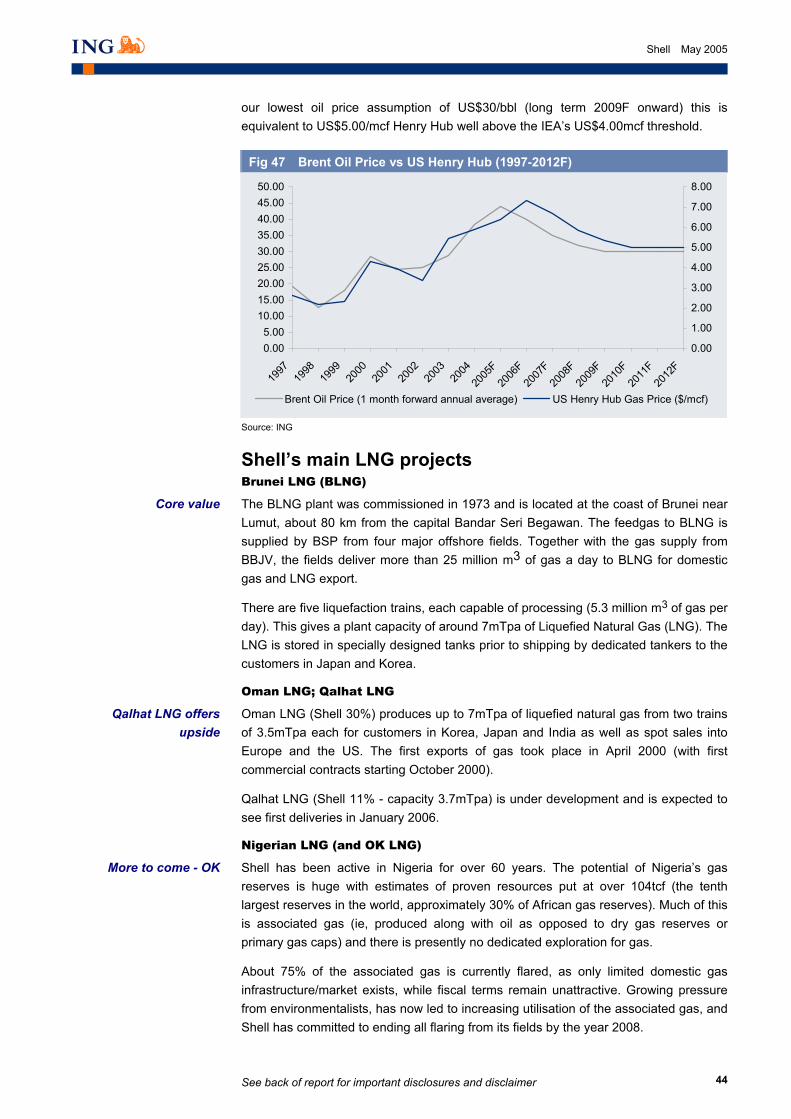

While resilient to low oil prices because of Shell’s high gas exposure and downstream earnings base, in valuation terms the implications of higher long-term oil prices (post 2008) remain important for underlying valuations on a sector and stock-specific basis.

Current valuations would appear to be factoring in US$30/bbl. Any paradigm shift to increase this cannot come from any short-term supply shocks alone or through the influences of inventory hedging, which has introduced its own premium into current oil prices; but from low global exploration success rates, faster demand for oil in key regions such as China and India, and the slower development of the new global LNG infrastructure, which is acting as a valuable substitution resource to traditional crude supplies.

The implications of higher longer-term oil prices remain

important for valuations

11

Royal D

utch Petroleum

May 2005

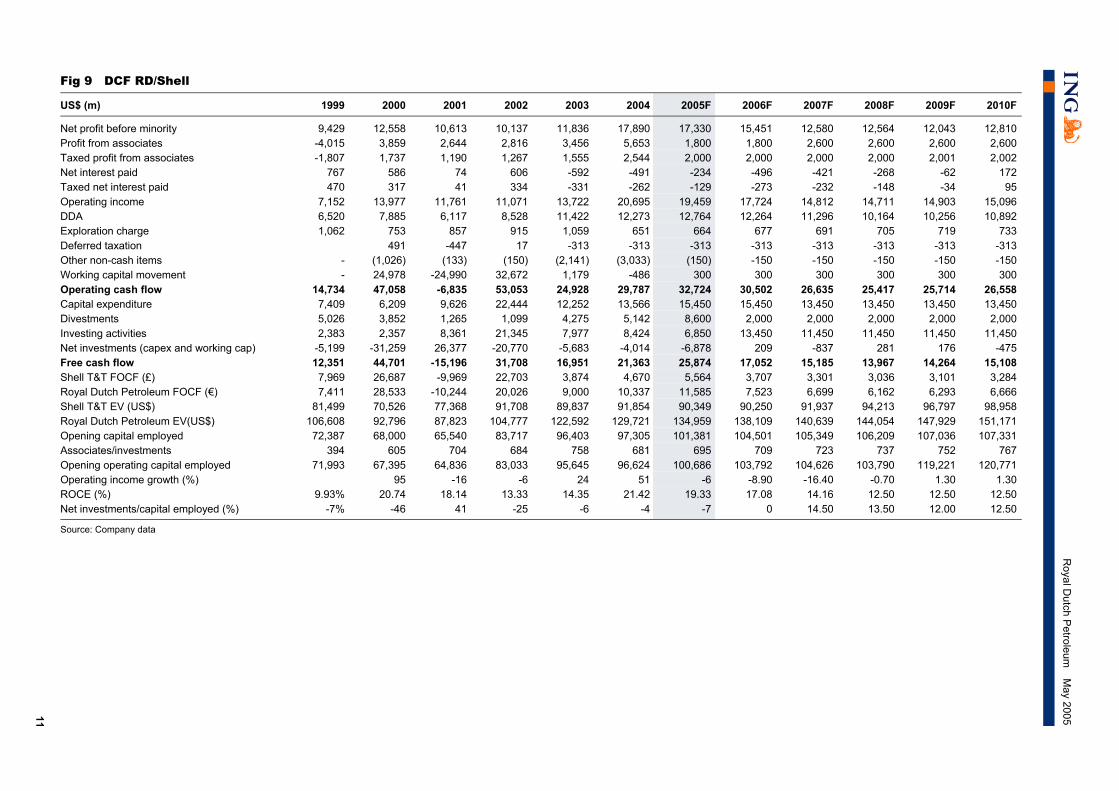

Fig 9 DCF RD/Shell

US$ (m) 1999 2000 2001 2002 2003 2004 2005F 2006F 2007F 2008F 2009F 2010F

Net profit before minority 9,429 12,558 10,613 10,137 11,836 17,890 17,330 15,451 12,580 12,564 12,043 12,810 Profit from associates -4,015 3,859 2,644 2,816 3,456 5,653 1,800 1,800 2,600 2,600 2,600 2,600 Taxed profit from associates -1,807 1,737 1,190 1,267 1,555 2,544 2,000 2,000 2,000 2,000 2,001 2,002 Net interest paid 767 586 74 606 -592 -491 -234 -496 -421 -268 -62 172 Taxed net interest paid 470 317 41 334 -331 -262 -129 -273 -232 -148 -34 95 Operating income 7,152 13,977 11,761 11,071 13,722 20,695 19,459 17,724 14,812 14,711 14,903 15,096 DDA 6,520 7,885 6,117 8,528 11,422 12,273 12,764 12,264 11,296 10,164 10,256 10,892 Exploration charge 1,062 753 857 915 1,059 651 664 677 691 705 719 733 Deferred taxation 491 -447 17 -313 -313 -313 -313 -313 -313 -313 -313 Other non-cash items - (1,026) (133) (150) (2,141) (3,033) (150) -150 -150 -150 -150 -150 Working capital movement - 24,978 -24,990 32,672 1,179 -486 300 300 300 300 300 300 Operating cash flow 14,734 47,058 -6,835 53,053 24,928 29,787 32,724 30,502 26,635 25,417 25,714 26,558 Capital expenditure 7,409 6,209 9,626 22,444 12,252 13,566 15,450 15,450 13,450 13,450 13,450 13,450 Divestments 5,026 3,852 1,265 1,099 4,275 5,142 8,600 2,000 2,000 2,000 2,000 2,000 Investing activities 2,383 2,357 8,361 21,345 7,977 8,424 6,850 13,450 11,450 11,450 11,450 11,450 Net investments (capex and working cap) -5,199 -31,259 26,377 -20,770 -5,683 -4,014 -6,878 209 -837 281 176 -475 Free cash flow 12,351 44,701 -15,196 31,708 16,951 21,363 25,874 17,052 15,185 13,967 14,264 15,108 Shell T&T FOCF (£) 7,969 26,687 -9,969 22,703 3,874 4,670 5,564 3,707 3,301 3,036 3,101 3,284 Royal Dutch Petroleum FOCF (€) 7,411 28,533 -10,244 20,026 9,000 10,337 11,585 7,523 6,699 6,162 6,293 6,666 Shell T&T EV (US$) 81,499 70,526 77,368 91,708 89,837 91,854 90,349 90,250 91,937 94,213 96,797 98,958 Royal Dutch Petroleum EV(US$) 106,608 92,796 87,823 104,777 122,592 129,721 134,959 138,109 140,639 144,054 147,929 151,171 Opening capital employed 72,387 68,000 65,540 83,717 96,403 97,305 101,381 104,501 105,349 106,209 107,036 107,331 Associates/investments 394 605 704 684 758 681 695 709 723 737 752 767 Opening operating capital employed 71,993 67,395 64,836 83,033 95,645 96,624 100,686 103,792 104,626 103,790 119,221 120,771 Operating income growth (%) 95 -16 -6 24 51 -6 -8.90 -16.40 -0.70 1.30 1.30 ROCE (%) 9.93% 20.74 18.14 13.33 14.35 21.42 19.33 17.08 14.16 12.50 12.50 12.50 Net investments/capital employed (%) -7% -46 41 -25 -6 -4 -7 0 14.50 13.50 12.00 12.50

Source: Company data

_

See back of report for important disclosures and disclaimer

12

Shell May 2005

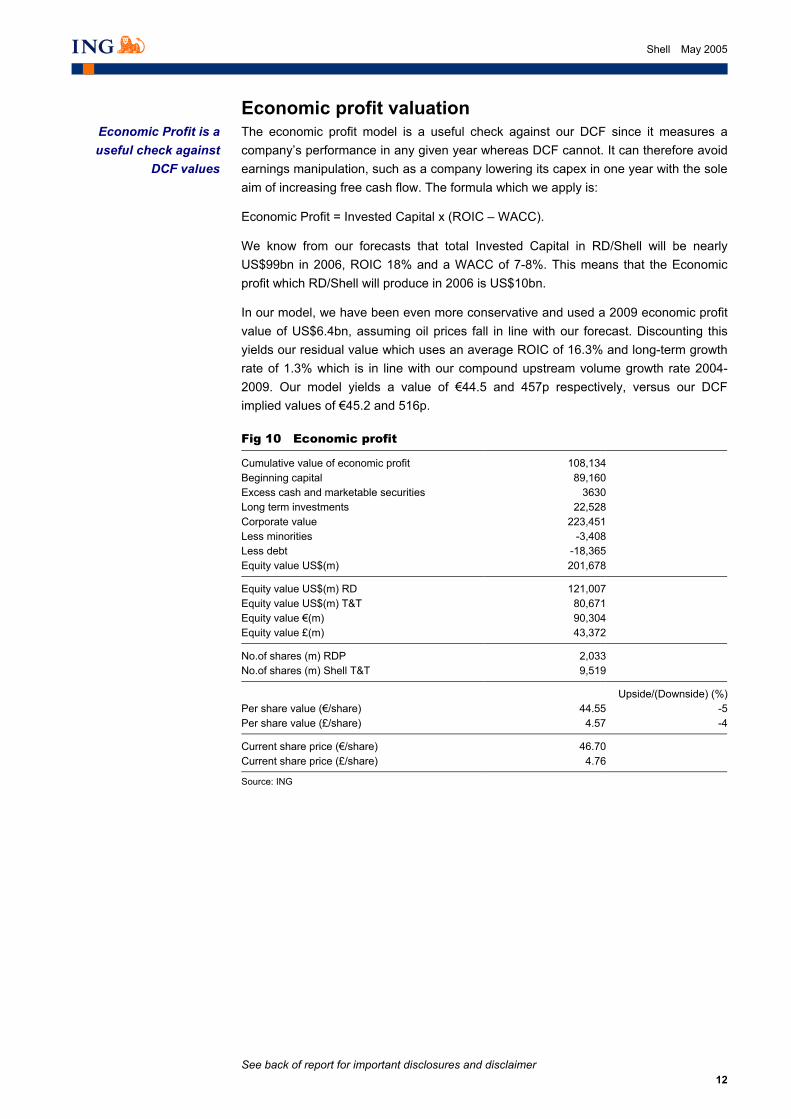

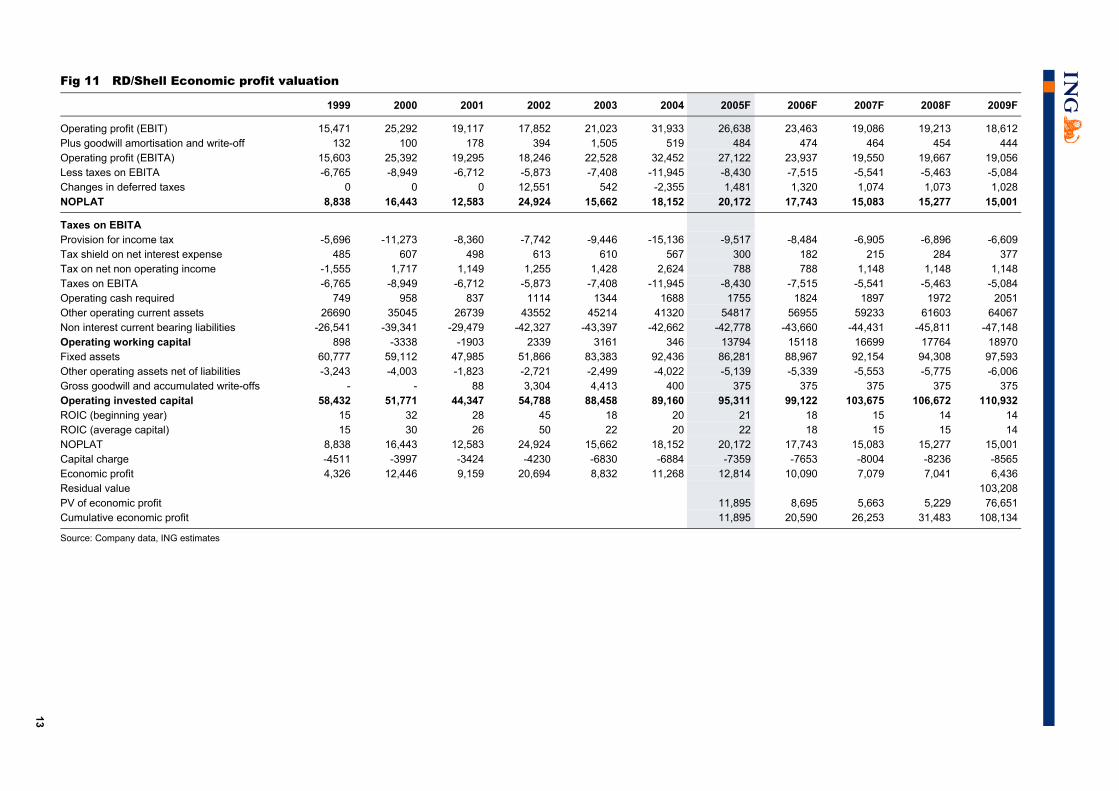

Economic profit valuation The economic profit model is a useful check against our DCF since it measures a company’s performance in any given year whereas DCF cannot. It can therefore avoid earnings manipulation, such as a company lowering its capex in one year with the sole aim of increasing free cash flow. The formula which we apply is:

Economic Profit = Invested Capital x (ROIC – WACC).

We know from our forecasts that total Invested Capital in RD/Shell will be nearly US$99bn in 2006, ROIC 18% and a WACC of 7-8%. This means that the Economic profit which RD/Shell will produce in 2006 is US$10bn.

In our model, we have been even more conservative and used a 2009 economic profit value of US$6.4bn, assuming oil prices fall in line with our forecast. Discounting this yields our residual value which uses an average ROIC of 16.3% and long-term growth rate of 1.3% which is in line with our compound upstream volume growth rate 2004-2009. Our model yields a value of €44.5 and 457p respectively, versus our DCF implied values of €45.2 and 516p.

Fig 10 Economic profit

Cumulative value of economic profit 108,134 Beginning capital 89,160 Excess cash and marketable securities 3630Long term investments 22,528Corporate value 223,451 Less minorities -3,408Less debt -18,365Equity value US$(m) 201,678

Equity value US$(m) RD 121,007 Equity value US$(m) T&T 80,671 Equity value €(m) 90,304 Equity value £(m) 43,372

No.of shares (m) RDP 2,033No.of shares (m) Shell T&T 9,519

Upside/(Downside) (%)Per share value (€/share) 44.55 -5Per share value (£/share) 4.57 -4

Current share price (€/share) 46.70Current share price (£/share) 4.76

Source: ING _

Economic Profit is a useful check against

DCF values

13

Fig 11 RD/Shell Economic profit valuation

1999 2000 2001 2002 2003 2004 2005F 2006F 2007F 2008F 2009F

Operating profit (EBIT) 15,471 25,292 19,117 17,852 21,023 31,933 26,638 23,463 19,086 19,213 18,612 Plus goodwill amortisation and write-off 132 100 178 394 1,505 519 484 474 464 454 444 Operating profit (EBITA) 15,603 25,392 19,295 18,246 22,528 32,452 27,122 23,937 19,550 19,667 19,056 Less taxes on EBITA -6,765 -8,949 -6,712 -5,873 -7,408 -11,945 -8,430 -7,515 -5,541 -5,463 -5,084 Changes in deferred taxes 0 0 0 12,551 542 -2,355 1,481 1,320 1,074 1,073 1,028 NOPLAT 8,838 16,443 12,583 24,924 15,662 18,152 20,172 17,743 15,083 15,277 15,001

Taxes on EBITA Provision for income tax -5,696 -11,273 -8,360 -7,742 -9,446 -15,136 -9,517 -8,484 -6,905 -6,896 -6,609 Tax shield on net interest expense 485 607 498 613 610 567 300 182 215 284 377 Tax on net non operating income -1,555 1,717 1,149 1,255 1,428 2,624 788 788 1,148 1,148 1,148 Taxes on EBITA -6,765 -8,949 -6,712 -5,873 -7,408 -11,945 -8,430 -7,515 -5,541 -5,463 -5,084 Operating cash required 749 958 837 1114 1344 1688 1755 1824 1897 1972 2051 Other operating current assets 26690 35045 26739 43552 45214 41320 54817 56955 59233 61603 64067 Non interest current bearing liabilities -26,541 -39,341 -29,479 -42,327 -43,397 -42,662 -42,778 -43,660 -44,431 -45,811 -47,148 Operating working capital 898 -3338 -1903 2339 3161 346 13794 15118 16699 17764 18970 Fixed assets 60,777 59,112 47,985 51,866 83,383 92,436 86,281 88,967 92,154 94,308 97,593 Other operating assets net of liabilities -3,243 -4,003 -1,823 -2,721 -2,499 -4,022 -5,139 -5,339 -5,553 -5,775 -6,006 Gross goodwill and accumulated write-offs - - 88 3,304 4,413 400 375 375 375 375 375 Operating invested capital 58,432 51,771 44,347 54,788 88,458 89,160 95,311 99,122 103,675 106,672 110,932 ROIC (beginning year) 15 32 28 45 18 20 21 18 15 14 14 ROIC (average capital) 15 30 26 50 22 20 22 18 15 15 14 NOPLAT 8,838 16,443 12,583 24,924 15,662 18,152 20,172 17,743 15,083 15,277 15,001 Capital charge -4511 -3997 -3424 -4230 -6830 -6884 -7359 -7653 -8004 -8236 -8565 Economic profit 4,326 12,446 9,159 20,694 8,832 11,268 12,814 10,090 7,079 7,041 6,436 Residual value 103,208 PV of economic profit 11,895 8,695 5,663 5,229 76,651 Cumulative economic profit 11,895 20,590 26,253 31,483 108,134

Source: Company data, ING estimates

_

See back of report for important disclosures and disclaimer

14

Shell May 2005

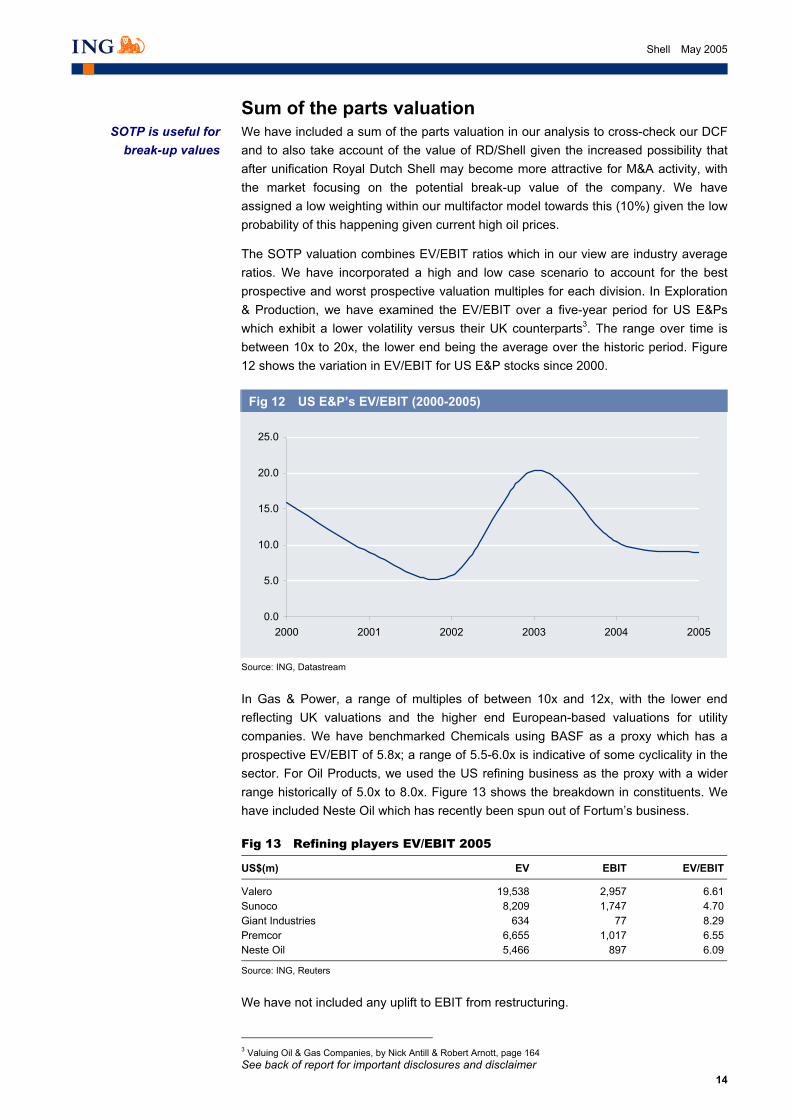

Sum of the parts valuation We have included a sum of the parts valuation in our analysis to cross-check our DCF and to also take account of the value of RD/Shell given the increased possibility that after unification Royal Dutch Shell may become more attractive for M&A activity, with the market focusing on the potential break-up value of the company. We have assigned a low weighting within our multifactor model towards this (10%) given the low probability of this happening given current high oil prices.

The SOTP valuation combines EV/EBIT ratios which in our view are industry average ratios. We have incorporated a high and low case scenario to account for the best prospective and worst prospective valuation multiples for each division. In Exploration & Production, we have examined the EV/EBIT over a five-year period for US E&Ps which exhibit a lower volatility versus their UK counterparts3. The range over time is between 10x to 20x, the lower end being the average over the historic period. Figure 12 shows the variation in EV/EBIT for US E&P stocks since 2000.

Fig 12 US E&P’s EV/EBIT (2000-2005)

0.0

5.0

10.0

15.0

20.0

25.0

2000 2001 2002 2003 2004 2005

Source: ING, Datastream

_

In Gas & Power, a range of multiples of between 10x and 12x, with the lower end reflecting UK valuations and the higher end European-based valuations for utility companies. We have benchmarked Chemicals using BASF as a proxy which has a prospective EV/EBIT of 5.8x; a range of 5.5-6.0x is indicative of some cyclicality in the sector. For Oil Products, we used the US refining business as the proxy with a wider range historically of 5.0x to 8.0x. Figure 13 shows the breakdown in constituents. We have included Neste Oil which has recently been spun out of Fortum’s business.

Fig 13 Refining players EV/EBIT 2005

US$(m) EV EBIT EV/EBIT

Valero 19,538 2,957 6.61Sunoco 8,209 1,747 4.70Giant Industries 634 77 8.29Premcor 6,655 1,017 6.55Neste Oil 5,466 897 6.09

Source: ING, Reuters

_

We have not included any uplift to EBIT from restructuring.

3 Valuing Oil & Gas Companies, by Nick Antill & Robert Arnott, page 164

SOTP is useful for break-up values

See back of report for important disclosures and disclaimer

15

Shell May 2005

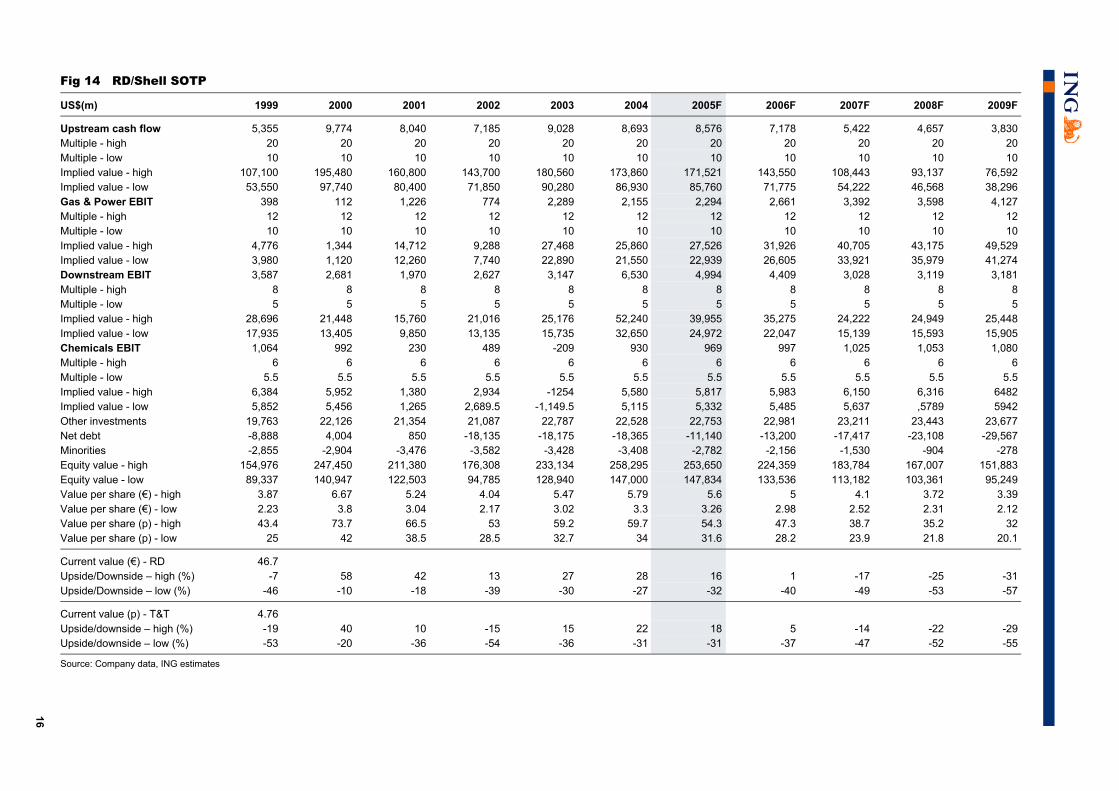

From our analysis, RD/Shell has a range in valuations which are between 298p and 500p for Shell T&T, and €28 to €47 for Royal Dutch for the next three years. The top end of the valuation indicates limited upside.

16

Fig 14 RD/Shell SOTP

US$(m) 1999 2000 2001 2002 2003 2004 2005F 2006F 2007F 2008F 2009F

Upstream cash flow 5,355 9,774 8,040 7,185 9,028 8,693 8,576 7,178 5,422 4,657 3,830 Multiple - high 20 20 20 20 20 20 20 20 20 20 20 Multiple - low 10 10 10 10 10 10 10 10 10 10 10 Implied value - high 107,100 195,480 160,800 143,700 180,560 173,860 171,521 143,550 108,443 93,137 76,592 Implied value - low 53,550 97,740 80,400 71,850 90,280 86,930 85,760 71,775 54,222 46,568 38,296 Gas & Power EBIT 398 112 1,226 774 2,289 2,155 2,294 2,661 3,392 3,598 4,127 Multiple - high 12 12 12 12 12 12 12 12 12 12 12 Multiple - low 10 10 10 10 10 10 10 10 10 10 10 Implied value - high 4,776 1,344 14,712 9,288 27,468 25,860 27,526 31,926 40,705 43,175 49,529 Implied value - low 3,980 1,120 12,260 7,740 22,890 21,550 22,939 26,605 33,921 35,979 41,274 Downstream EBIT 3,587 2,681 1,970 2,627 3,147 6,530 4,994 4,409 3,028 3,119 3,181 Multiple - high 8 8 8 8 8 8 8 8 8 8 8 Multiple - low 5 5 5 5 5 5 5 5 5 5 5 Implied value - high 28,696 21,448 15,760 21,016 25,176 52,240 39,955 35,275 24,222 24,949 25,448 Implied value - low 17,935 13,405 9,850 13,135 15,735 32,650 24,972 22,047 15,139 15,593 15,905 Chemicals EBIT 1,064 992 230 489 -209 930 969 997 1,025 1,053 1,080 Multiple - high 6 6 6 6 6 6 6 6 6 6 6 Multiple - low 5.5 5.5 5.5 5.5 5.5 5.5 5.5 5.5 5.5 5.5 5.5 Implied value - high 6,384 5,952 1,380 2,934 -1254 5,580 5,817 5,983 6,150 6,316 6482 Implied value - low 5,852 5,456 1,265 2,689.5 -1,149.5 5,115 5,332 5,485 5,637 ,5789 5942 Other investments 19,763 22,126 21,354 21,087 22,787 22,528 22,753 22,981 23,211 23,443 23,677 Net debt -8,888 4,004 850 -18,135 -18,175 -18,365 -11,140 -13,200 -17,417 -23,108 -29,567 Minorities -2,855 -2,904 -3,476 -3,582 -3,428 -3,408 -2,782 -2,156 -1,530 -904 -278 Equity value - high 154,976 247,450 211,380 176,308 233,134 258,295 253,650 224,359 183,784 167,007 151,883 Equity value - low 89,337 140,947 122,503 94,785 128,940 147,000 147,834 133,536 113,182 103,361 95,249 Value per share (€) - high 3.87 6.67 5.24 4.04 5.47 5.79 5.6 5 4.1 3.72 3.39 Value per share (€) - low 2.23 3.8 3.04 2.17 3.02 3.3 3.26 2.98 2.52 2.31 2.12 Value per share (p) - high 43.4 73.7 66.5 53 59.2 59.7 54.3 47.3 38.7 35.2 32 Value per share (p) - low 25 42 38.5 28.5 32.7 34 31.6 28.2 23.9 21.8 20.1

Current value (€) - RD 46.7 Upside/Downside – high (%) -7 58 42 13 27 28 16 1 -17 -25 -31 Upside/Downside – low (%) -46 -10 -18 -39 -30 -27 -32 -40 -49 -53 -57

Current value (p) - T&T 4.76 Upside/downside – high (%) -19 40 10 -15 15 22 18 5 -14 -22 -29 Upside/downside – low (%) -53 -20 -36 -54 -36 -31 -31 -37 -47 -52 -55

Source: Company data, ING estimates

_

See back of report for important disclosures and disclaimer

17

Shell May 2005

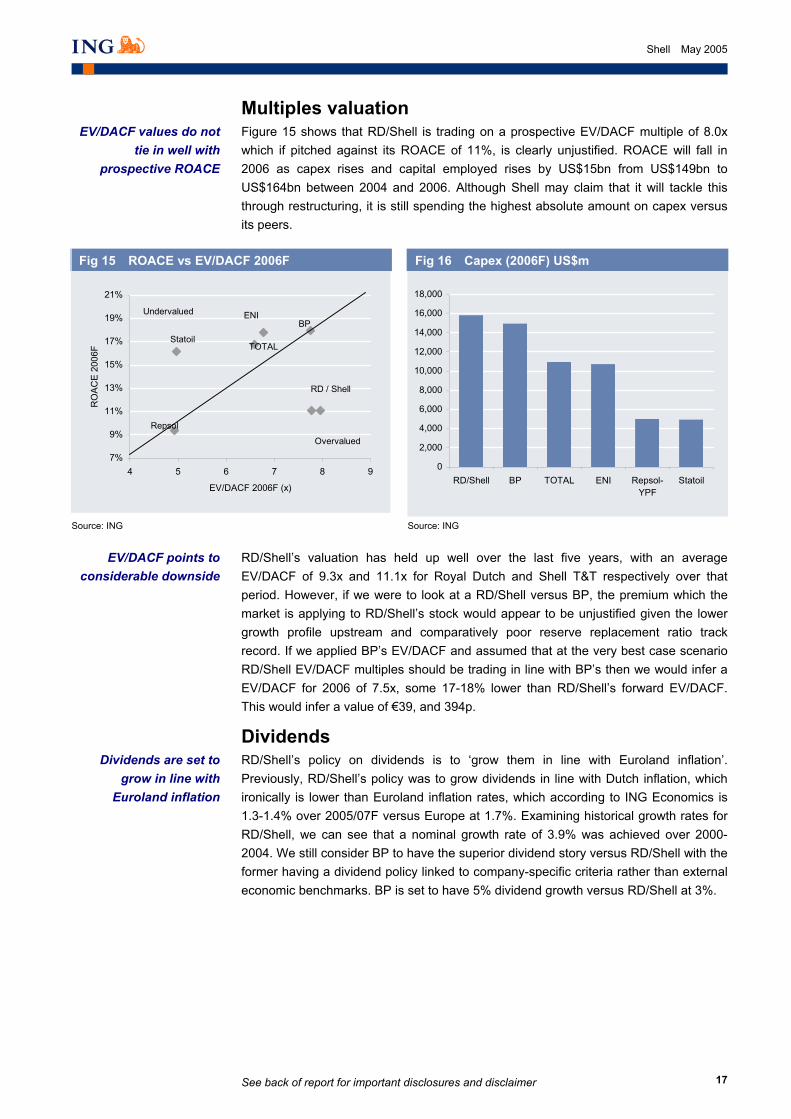

Multiples valuation Figure 15 shows that RD/Shell is trading on a prospective EV/DACF multiple of 8.0x which if pitched against its ROACE of 11%, is clearly unjustified. ROACE will fall in 2006 as capex rises and capital employed rises by US$15bn from US$149bn to US$164bn between 2004 and 2006. Although Shell may claim that it will tackle this through restructuring, it is still spending the highest absolute amount on capex versus its peers.

Fig 15 ROACE vs EV/DACF 2006F

Fig 16 Capex (2006F) US$m

7%

9%

11%

13%

15%

17%

19%

21%

4 5 6 7 8 9

EV/DACF 2006F (x)

RO

AC

E 2

006F

Repsol

ENI

TOTAL

BP

RD / Shell

Statoil

Undervalued

Overvalued

0

2,000

4,000

6,000

8,000

10,000

12,000

14,000

16,000

18,000

RD/Shell BP TOTAL ENI Repsol-YPF

Statoil

Source: ING Source: ING

_

RD/Shell’s valuation has held up well over the last five years, with an average EV/DACF of 9.3x and 11.1x for Royal Dutch and Shell T&T respectively over that period. However, if we were to look at a RD/Shell versus BP, the premium which the market is applying to RD/Shell’s stock would appear to be unjustified given the lower growth profile upstream and comparatively poor reserve replacement ratio track record. If we applied BP’s EV/DACF and assumed that at the very best case scenario RD/Shell EV/DACF multiples should be trading in line with BP’s then we would infer a EV/DACF for 2006 of 7.5x, some 17-18% lower than RD/Shell’s forward EV/DACF. This would infer a value of €39, and 394p.

Dividends RD/Shell’s policy on dividends is to ‘grow them in line with Euroland inflation’. Previously, RD/Shell’s policy was to grow dividends in line with Dutch inflation, which ironically is lower than Euroland inflation rates, which according to ING Economics is 1.3-1.4% over 2005/07F versus Europe at 1.7%. Examining historical growth rates for RD/Shell, we can see that a nominal growth rate of 3.9% was achieved over 2000-2004. We still consider BP to have the superior dividend story versus RD/Shell with the former having a dividend policy linked to company-specific criteria rather than external economic benchmarks. BP is set to have 5% dividend growth versus RD/Shell at 3%.

EV/DACF points to considerable downside

Dividends are set to grow in line with

Euroland inflation

EV/DACF values do not tie in well with

prospective ROACE

See back of report for important disclosures and disclaimer

18

Shell May 2005

Fig 17 Dividend growth (2000-2009)

-2.0%0.0%2.0%4.0%6.0%8.0%

10.0%12.0%14.0%16.0%

2000 2001 2002 2003 2004 2005F 2006F 2007F 2008F 2009F

Shell T&T BP

Source: ING

_

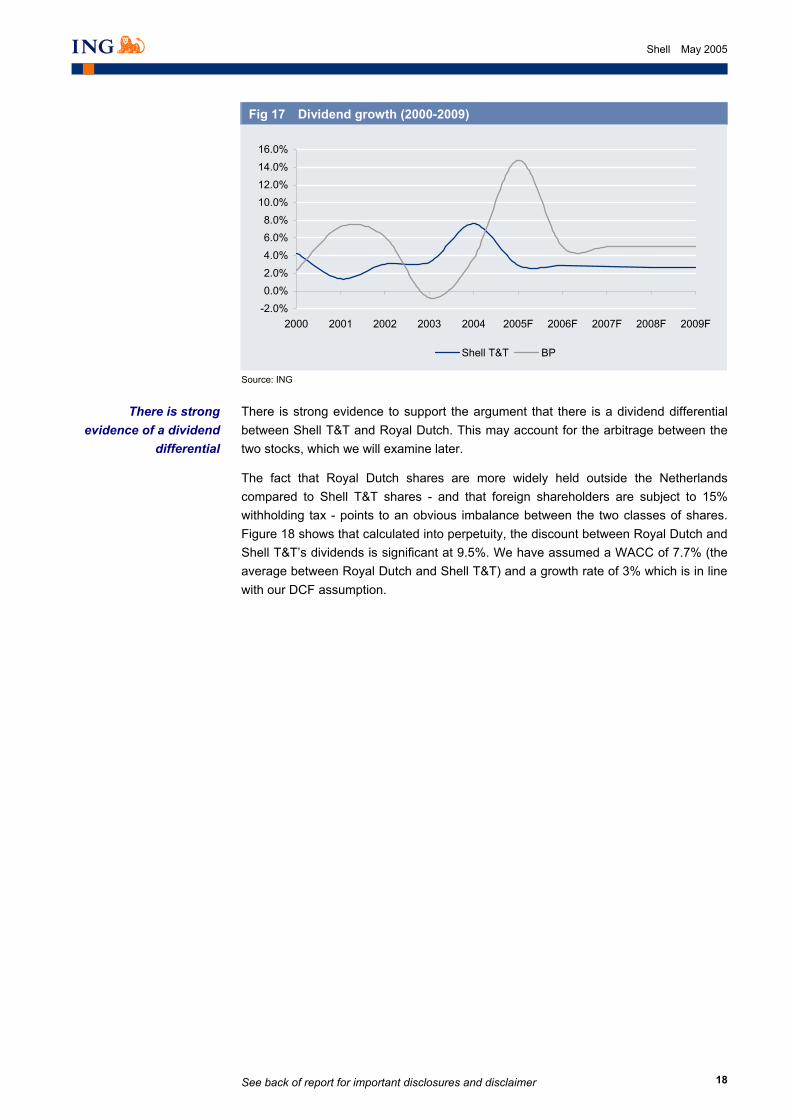

There is strong evidence to support the argument that there is a dividend differential between Shell T&T and Royal Dutch. This may account for the arbitrage between the two stocks, which we will examine later.

The fact that Royal Dutch shares are more widely held outside the Netherlands compared to Shell T&T shares - and that foreign shareholders are subject to 15% withholding tax - points to an obvious imbalance between the two classes of shares. Figure 18 shows that calculated into perpetuity, the discount between Royal Dutch and Shell T&T’s dividends is significant at 9.5%. We have assumed a WACC of 7.7% (the average between Royal Dutch and Shell T&T) and a growth rate of 3% which is in line with our DCF assumption.

There is strong evidence of a dividend

differential

See back of report for important disclosures and disclaimer

19

Shell May 2005

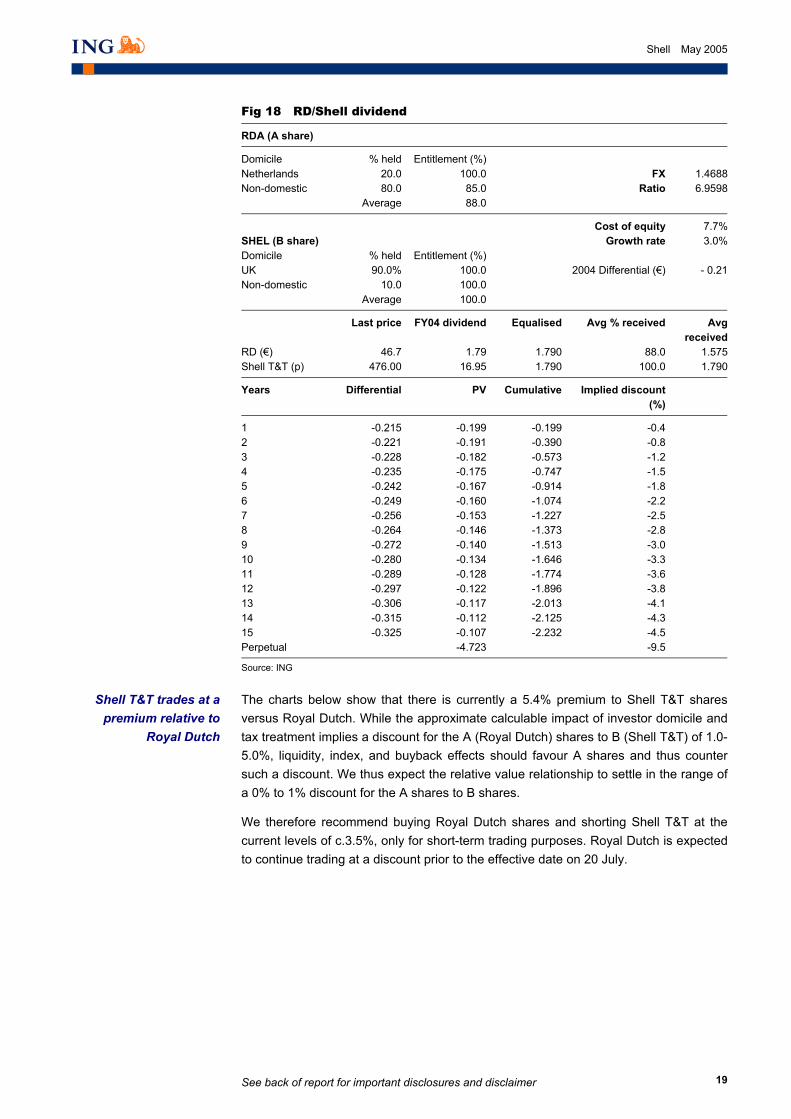

Fig 18 RD/Shell dividend

RDA (A share)

Domicile % held Entitlement (%)Netherlands 20.0 100.0 FX 1.4688 Non-domestic 80.0 85.0 Ratio 6.9598 Average 88.0

Cost of equity 7.7%SHEL (B share) Growth rate 3.0%Domicile % held Entitlement (%)UK 90.0% 100.0 2004 Differential (€) - 0.21 Non-domestic 10.0 100.0 Average 100.0

Last price FY04 dividend Equalised Avg % received Avg received

RD (€) 46.7 1.79 1.790 88.0 1.575 Shell T&T (p) 476.00 16.95 1.790 100.0 1.790

Years Differential PV Cumulative Implied discount(%)

1 -0.215 -0.199 -0.199 -0.42 -0.221 -0.191 -0.390 -0.83 -0.228 -0.182 -0.573 -1.24 -0.235 -0.175 -0.747 -1.55 -0.242 -0.167 -0.914 -1.86 -0.249 -0.160 -1.074 -2.27 -0.256 -0.153 -1.227 -2.58 -0.264 -0.146 -1.373 -2.89 -0.272 -0.140 -1.513 -3.010 -0.280 -0.134 -1.646 -3.311 -0.289 -0.128 -1.774 -3.612 -0.297 -0.122 -1.896 -3.813 -0.306 -0.117 -2.013 -4.114 -0.315 -0.112 -2.125 -4.315 -0.325 -0.107 -2.232 -4.5Perpetual -4.723 -9.5

Source: ING

_

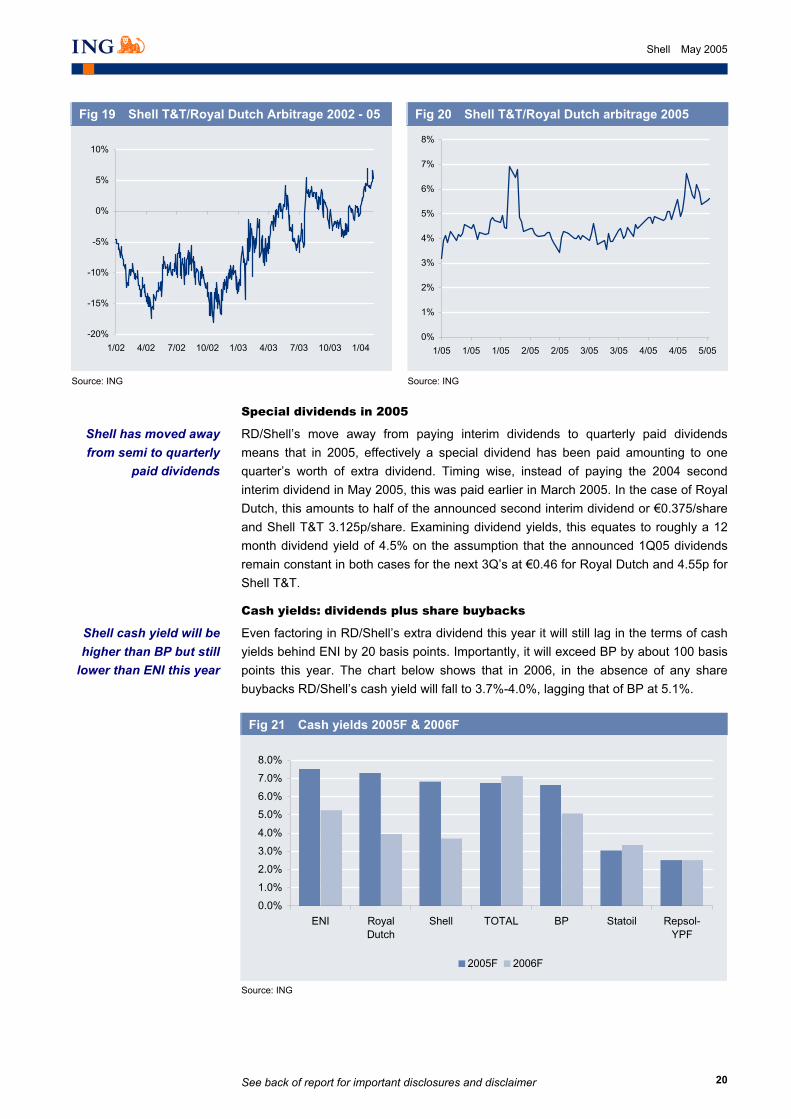

The charts below show that there is currently a 5.4% premium to Shell T&T shares versus Royal Dutch. While the approximate calculable impact of investor domicile and tax treatment implies a discount for the A (Royal Dutch) shares to B (Shell T&T) of 1.0-5.0%, liquidity, index, and buyback effects should favour A shares and thus counter such a discount. We thus expect the relative value relationship to settle in the range of a 0% to 1% discount for the A shares to B shares.

We therefore recommend buying Royal Dutch shares and shorting Shell T&T at the current levels of c.3.5%, only for short-term trading purposes. Royal Dutch is expected to continue trading at a discount prior to the effective date on 20 July.

Shell T&T trades at a premium relative to

Royal Dutch

See back of report for important disclosures and disclaimer

20

Shell May 2005

Fig 19 Shell T&T/Royal Dutch Arbitrage 2002 - 05

Fig 20 Shell T&T/Royal Dutch arbitrage 2005

-20%

-15%

-10%

-5%

0%

5%

10%

1/02 4/02 7/02 10/02 1/03 4/03 7/03 10/03 1/04

0%

1%

2%

3%

4%

5%

6%

7%

8%

1/05 1/05 1/05 2/05 2/05 3/05 3/05 4/05 4/05 5/05

Source: ING Source: ING

_

Special dividends in 2005

RD/Shell’s move away from paying interim dividends to quarterly paid dividends means that in 2005, effectively a special dividend has been paid amounting to one quarter’s worth of extra dividend. Timing wise, instead of paying the 2004 second interim dividend in May 2005, this was paid earlier in March 2005. In the case of Royal Dutch, this amounts to half of the announced second interim dividend or €0.375/share and Shell T&T 3.125p/share. Examining dividend yields, this equates to roughly a 12 month dividend yield of 4.5% on the assumption that the announced 1Q05 dividends remain constant in both cases for the next 3Q’s at €0.46 for Royal Dutch and 4.55p for Shell T&T.

Cash yields: dividends plus share buybacks

Even factoring in RD/Shell’s extra dividend this year it will still lag in the terms of cash yields behind ENI by 20 basis points. Importantly, it will exceed BP by about 100 basis points this year. The chart below shows that in 2006, in the absence of any share buybacks RD/Shell’s cash yield will fall to 3.7%-4.0%, lagging that of BP at 5.1%.

Fig 21 Cash yields 2005F & 2006F

0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

ENI RoyalDutch

Shell TOTAL BP Statoil Repsol-YPF

2005F 2006F

Source: ING

Shell has moved away from semi to quarterly

paid dividends

Shell cash yield will be higher than BP but still

lower than ENI this year

See back of report for important disclosures and disclaimer

21

Shell May 2005

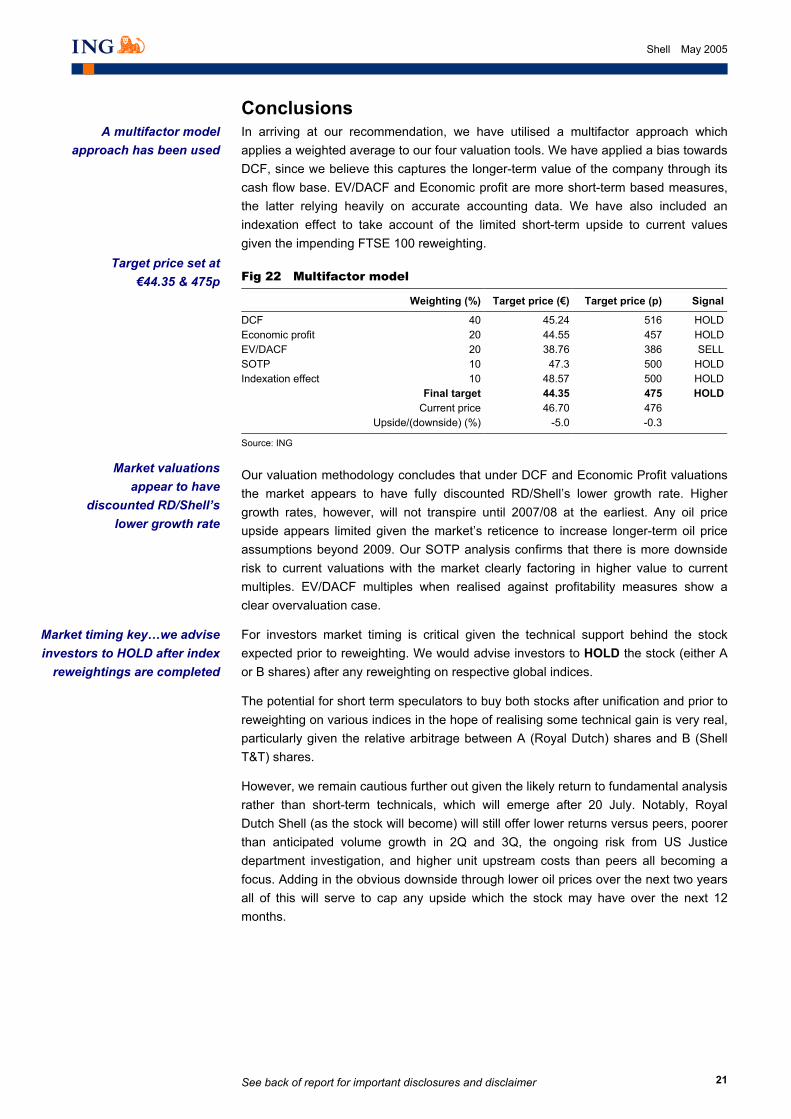

Conclusions In arriving at our recommendation, we have utilised a multifactor approach which applies a weighted average to our four valuation tools. We have applied a bias towards DCF, since we believe this captures the longer-term value of the company through its cash flow base. EV/DACF and Economic profit are more short-term based measures, the latter relying heavily on accurate accounting data. We have also included an indexation effect to take account of the limited short-term upside to current values given the impending FTSE 100 reweighting.

Fig 22 Multifactor model

Weighting (%) Target price (€) Target price (p) Signal

DCF 40 45.24 516 HOLDEconomic profit 20 44.55 457 HOLD EV/DACF 20 38.76 386 SELLSOTP 10 47.3 500 HOLDIndexation effect 10 48.57 500 HOLD Final target 44.35 475 HOLD Current price 46.70 476 Upside/(downside) (%) -5.0 -0.3

Source: ING

_

Our valuation methodology concludes that under DCF and Economic Profit valuations the market appears to have fully discounted RD/Shell’s lower growth rate. Higher growth rates, however, will not transpire until 2007/08 at the earliest. Any oil price upside appears limited given the market’s reticence to increase longer-term oil price assumptions beyond 2009. Our SOTP analysis confirms that there is more downside risk to current valuations with the market clearly factoring in higher value to current multiples. EV/DACF multiples when realised against profitability measures show a clear overvaluation case.

For investors market timing is critical given the technical support behind the stock expected prior to reweighting. We would advise investors to HOLD the stock (either A or B shares) after any reweighting on respective global indices.

The potential for short term speculators to buy both stocks after unification and prior to reweighting on various indices in the hope of realising some technical gain is very real, particularly given the relative arbitrage between A (Royal Dutch) shares and B (Shell T&T) shares.

However, we remain cautious further out given the likely return to fundamental analysis rather than short-term technicals, which will emerge after 20 July. Notably, Royal Dutch Shell (as the stock will become) will still offer lower returns versus peers, poorer than anticipated volume growth in 2Q and 3Q, the ongoing risk from US Justice department investigation, and higher unit upstream costs than peers all becoming a focus. Adding in the obvious downside through lower oil prices over the next two years all of this will serve to cap any upside which the stock may have over the next 12 months.

Market timing key…we advise investors to HOLD after index

reweightings are completed

A multifactor model approach has been used

Target price set at €44.35 & 475p

Market valuations appear to have

discounted RD/Shell’s lower growth rate

See back of report for important disclosures and disclaimer

22

Shell May 2005

Pros & cons

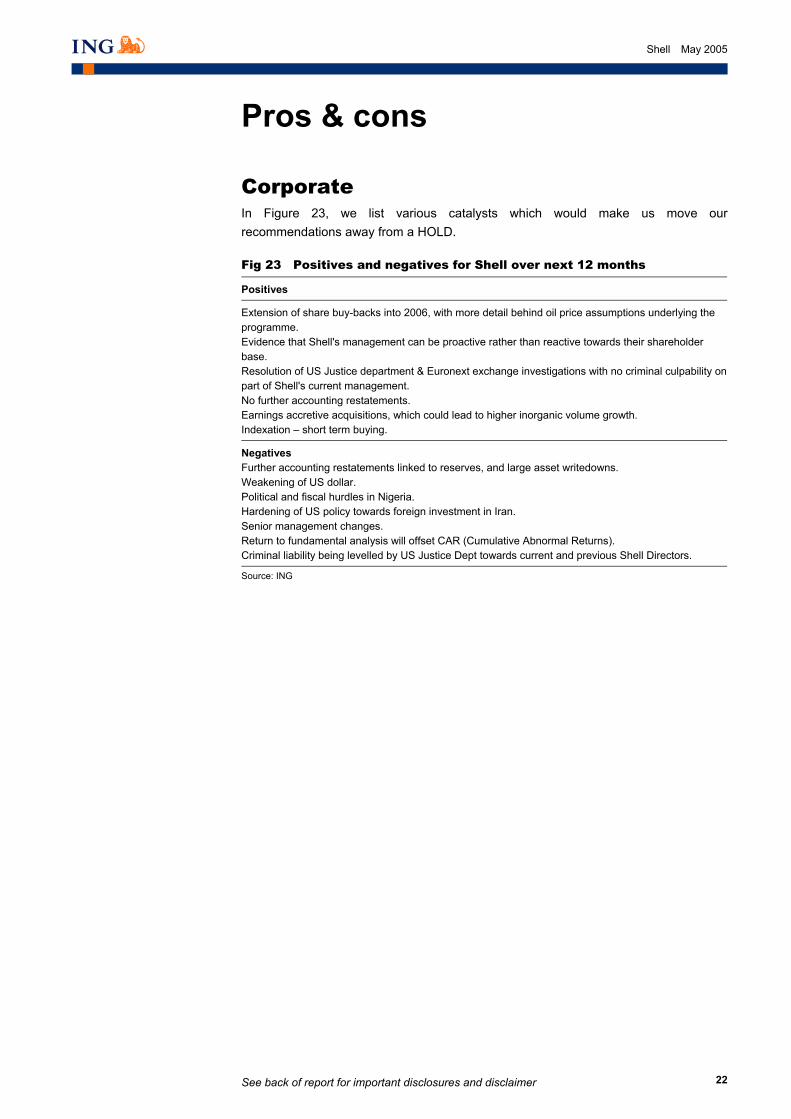

Corporate In Figure 23, we list various catalysts which would make us move our recommendations away from a HOLD.

Fig 23 Positives and negatives for Shell over next 12 months

Positives

Extension of share buy-backs into 2006, with more detail behind oil price assumptions underlying the programme. Evidence that Shell's management can be proactive rather than reactive towards their shareholder base. Resolution of US Justice department & Euronext exchange investigations with no criminal culpability on part of Shell's current management. No further accounting restatements. Earnings accretive acquisitions, which could lead to higher inorganic volume growth. Indexation – short term buying.

Negatives Further accounting restatements linked to reserves, and large asset writedowns. Weakening of US dollar. Political and fiscal hurdles in Nigeria. Hardening of US policy towards foreign investment in Iran. Senior management changes. Return to fundamental analysis will offset CAR (Cumulative Abnormal Returns). Criminal liability being levelled by US Justice Dept towards current and previous Shell Directors.

Source: ING

_

See back of report for important disclosures and disclaimer

23

Shell May 2005

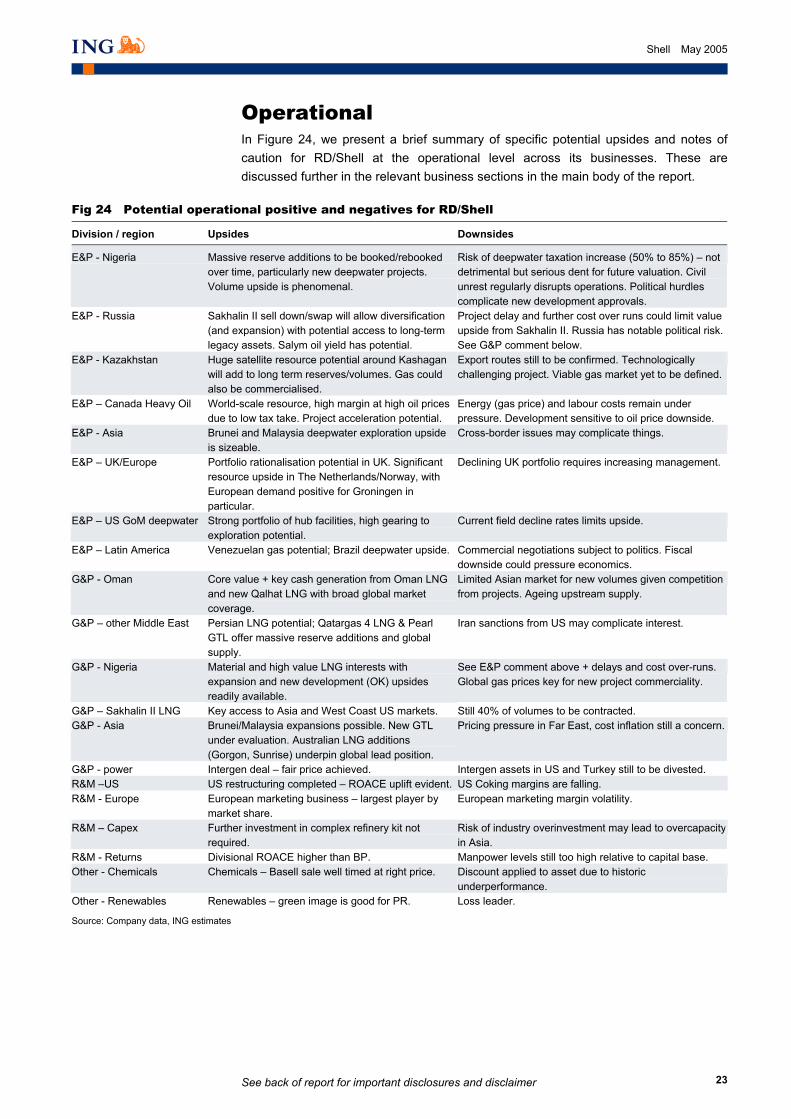

Operational In Figure 24, we present a brief summary of specific potential upsides and notes of caution for RD/Shell at the operational level across its businesses. These are discussed further in the relevant business sections in the main body of the report.

Fig 24 Potential operational positive and negatives for RD/Shell

Division / region Upsides Downsides

E&P - Nigeria Massive reserve additions to be booked/rebooked over time, particularly new deepwater projects. Volume upside is phenomenal.

Risk of deepwater taxation increase (50% to 85%) – not detrimental but serious dent for future valuation. Civil unrest regularly disrupts operations. Political hurdles complicate new development approvals.

E&P - Russia Sakhalin II sell down/swap will allow diversification (and expansion) with potential access to long-term legacy assets. Salym oil yield has potential.

Project delay and further cost over runs could limit value upside from Sakhalin II. Russia has notable political risk. See G&P comment below.

E&P - Kazakhstan Huge satellite resource potential around Kashagan will add to long term reserves/volumes. Gas could also be commercialised.

Export routes still to be confirmed. Technologically challenging project. Viable gas market yet to be defined.

E&P – Canada Heavy Oil World-scale resource, high margin at high oil prices due to low tax take. Project acceleration potential.

Energy (gas price) and labour costs remain under pressure. Development sensitive to oil price downside.

E&P - Asia Brunei and Malaysia deepwater exploration upside is sizeable.

Cross-border issues may complicate things.

E&P – UK/Europe Portfolio rationalisation potential in UK. Significant resource upside in The Netherlands/Norway, with European demand positive for Groningen in particular.

Declining UK portfolio requires increasing management.

E&P – US GoM deepwater Strong portfolio of hub facilities, high gearing to exploration potential.

Current field decline rates limits upside.

E&P – Latin America Venezuelan gas potential; Brazil deepwater upside. Commercial negotiations subject to politics. Fiscal downside could pressure economics.

G&P - Oman Core value + key cash generation from Oman LNG and new Qalhat LNG with broad global market coverage.

Limited Asian market for new volumes given competition from projects. Ageing upstream supply.

G&P – other Middle East Persian LNG potential; Qatargas 4 LNG & Pearl GTL offer massive reserve additions and global supply.

Iran sanctions from US may complicate interest.

G&P - Nigeria Material and high value LNG interests with expansion and new development (OK) upsides readily available.

See E&P comment above + delays and cost over-runs. Global gas prices key for new project commerciality.

G&P – Sakhalin II LNG Key access to Asia and West Coast US markets. Still 40% of volumes to be contracted. G&P - Asia Brunei/Malaysia expansions possible. New GTL

under evaluation. Australian LNG additions (Gorgon, Sunrise) underpin global lead position.

Pricing pressure in Far East, cost inflation still a concern.

G&P - power Intergen deal – fair price achieved. Intergen assets in US and Turkey still to be divested. R&M –US US restructuring completed – ROACE uplift evident. US Coking margins are falling. R&M - Europe European marketing business – largest player by

market share. European marketing margin volatility.

R&M – Capex Further investment in complex refinery kit not required.

Risk of industry overinvestment may lead to overcapacity in Asia.

R&M - Returns Divisional ROACE higher than BP. Manpower levels still too high relative to capital base. Other - Chemicals Chemicals – Basell sale well timed at right price. Discount applied to asset due to historic

underperformance. Other - Renewables Renewables – green image is good for PR. Loss leader.

Source: Company data, ING estimates

_

See back of report for important disclosures and disclaimer

24

Shell May 2005

Exploration & production

Introduction The wide range of group ROACEs for the pan-Euro majors (12% to 22%) reflects the integrated structure of the majors and company’s bias toward the upstream business. The upstream division remains core to returns for oil majors providing a ROACE in excess of 25% currently, and even above 30% for the most efficient operators and those able to provide for growth. This compares to only 15% to 20% ROACE downstream and barely double-digit ROACE from Chemicals despite recent cycle upturn.

The key factors supporting a sound performance upstream include an ability to find and replace produced volumes, a disciplined focus on efficient recovery and costs, and foresight to gain access to new resources with which to underpin the longer-term sustainability of a group’s operations. Obviously, volume growth helps differentiate performance, particularly when combined with a robust macro environment in the short term.

For RD/Shell, reserves (and more explicitly the hydrocarbon accounting of reserves) have dogged the company of late. While the company technically still has resources in the ground, the long-term sustainability of the group’s upstream division has been brought into question, with the company’s ability to progress the development of new projects and commercialise its resource base effectively in dispute.

While admitting underinvestment in its upstream division 1998 to 2003, and having spent most of 2004 reassessing it options, RD/Shell is embarking on a new phase of investment for growth across its portfolio. Unfortunately, there will be a lead time for this to make a credible and obvious impact for long-term earnings and valuation and we remain cautious at this stage as to the company’s outlook upstream on this basis.

In the following section, we analyse briefly the key issues for RD/Shell in the short term (namely reserves replacement, production growth and rising costs). As part of our production review, we also look at some of the current and future focus for activity across the company’s portfolio in order to better understand the potential this offers.

Upstream issues There are three main issues currently affecting RD/Shell’s upstream business:

• Reserves replacement – surprisingly, not a problem.

• Production growth – poor to 2007 but deep value potential from new regions and a new focus on material oil, integrated gas and unconventional energy.

• Rising costs – an industry wide issue.

Reserves replacement – potential upside The problems associated with re-categorisations (or historic hydrocarbon accounting) now appear to be behind Shell, although we note that any potential fallout from the US Justice Department over allegations of criminal liability could emerge in the next six months. This may weigh on the stock once implications are disclosed.

The reserve problems of Shell now appear to be

behind them

A credible upstream division will underpin

group returns

Reserves issues bring sustainable growth into

question

New investment commitment has a lead

time to reinvigorate performance

ING cautious of new drivers and timing of upstream turnaround

See back of report for important disclosures and disclaimer

25

Shell May 2005

A more pressing concern which remains is how Shell will achieve what at first looks like an ambitious Reserves Replacement (RRR) target of 100% for the period 2005-09.

The high degree of scepticism in the market is understandable given Shell’s organic RRR averaged only 61% over 1999 to 2003, and (eventually) was only 38% in 2004. However, RD/Shell had some 60bnboe in its proven and probable reserves base end 2003. This compares to 14bnboe barrels of proven resources booked at the end of 2004, which leaves 46bnboe of reserves still to be booked over the next few decades.

According to Shell, the company could book another 14bnboe of this resource in total by the end of 2009 even under “conservative” assumptions (and potentially a total of 19 bnboe by 2014). The bulk of the potential reserves in addition to 2009 includes large projects such as Bonga, Erha, Ormen Lange, Sakhalin, Qatar GTL, Kashaghan, and Gorgon (and this before Heavy Oil projects) –which so far appear to be making credible headway in terms of development progress and commercial negotiation.

Based on our production forecast (see later) we see a total of some 7bnboe output 2005 to 2009 (or an average 3.85mboe/d for the period). This is roughly half the level of the reserves that could potentially be booked over the period implying an average 200% replacement (ie, twice the expected production).

Even if we were more optimistic for production, and Shell were to become more conservative on reserve bookings (or we assume some delays to bookings given the technically and commercially challenging nature of the projects involved) it would still be plausible to see Shell achieving an RRR in excess of 150% over 2005-2009.

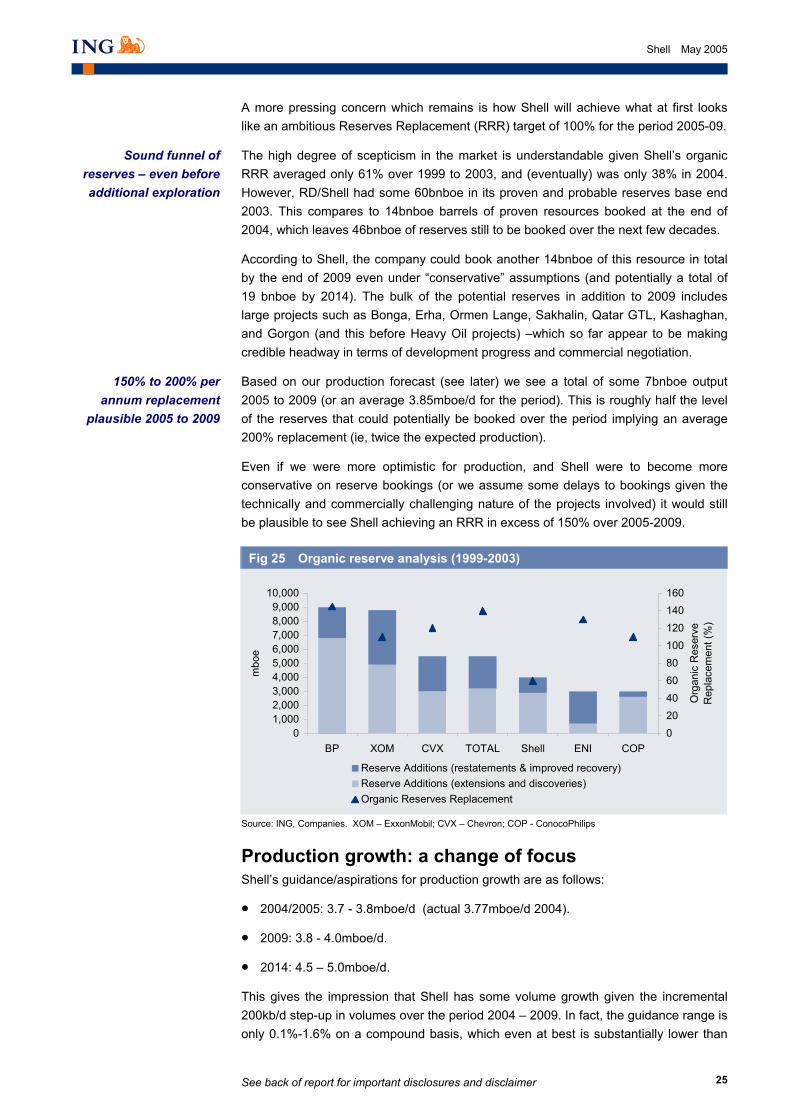

Fig 25 Organic reserve analysis (1999-2003)

01,0002,0003,0004,0005,0006,0007,0008,0009,000

10,000

BP XOM CVX TOTAL Shell ENI COP

mbo

e

020406080100120140160

Org

anic

Res

erve

R

epla

cem

ent (

%)

Reserve Additions (restatements & improved recovery)Reserve Additions (extensions and discoveries)Organic Reserves Replacement

Source: ING, Companies. XOM – ExxonMobil; CVX – Chevron; COP - ConocoPhilips

_

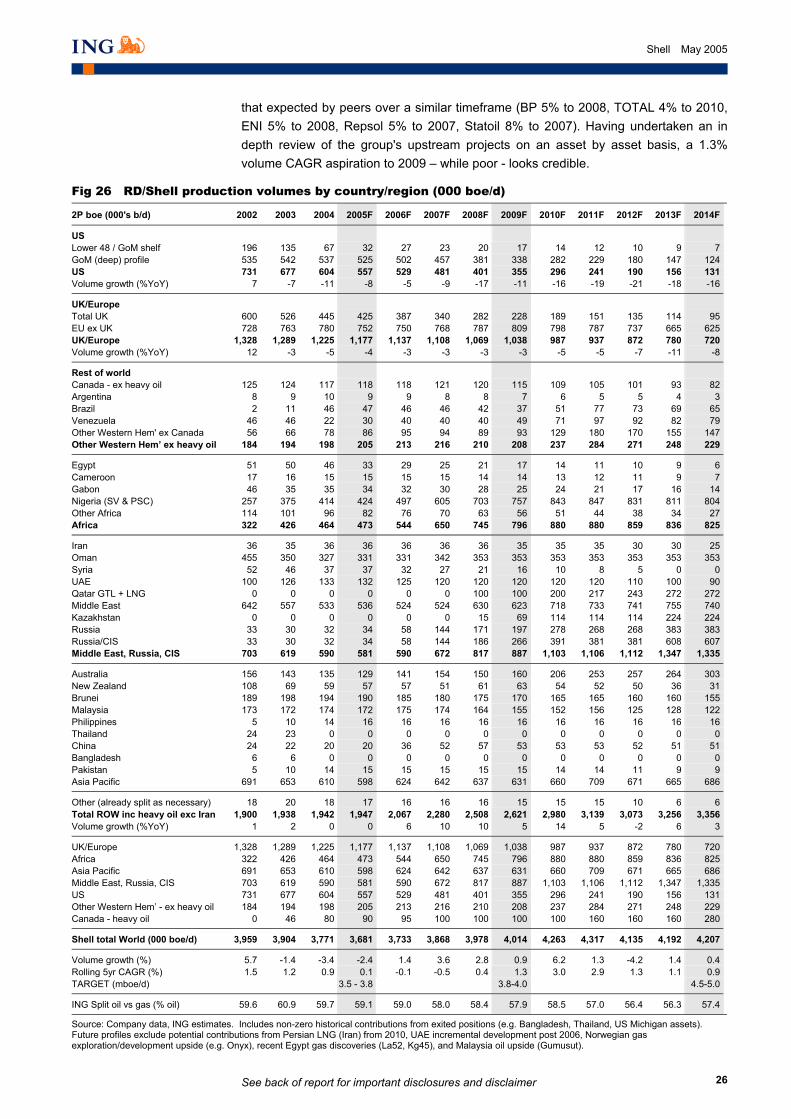

Production growth: a change of focus Shell’s guidance/aspirations for production growth are as follows:

• 2004/2005: 3.7 - 3.8mboe/d (actual 3.77mboe/d 2004).

• 2009: 3.8 - 4.0mboe/d.

• 2014: 4.5 – 5.0mboe/d.

This gives the impression that Shell has some volume growth given the incremental 200kb/d step-up in volumes over the period 2004 – 2009. In fact, the guidance range is only 0.1%-1.6% on a compound basis, which even at best is substantially lower than

150% to 200% per annum replacement

plausible 2005 to 2009

Sound funnel of reserves – even before additional exploration

See back of report for important disclosures and disclaimer

26

Shell May 2005

that expected by peers over a similar timeframe (BP 5% to 2008, TOTAL 4% to 2010, ENI 5% to 2008, Repsol 5% to 2007, Statoil 8% to 2007). Having undertaken an in depth review of the group's upstream projects on an asset by asset basis, a 1.3% volume CAGR aspiration to 2009 – while poor - looks credible.

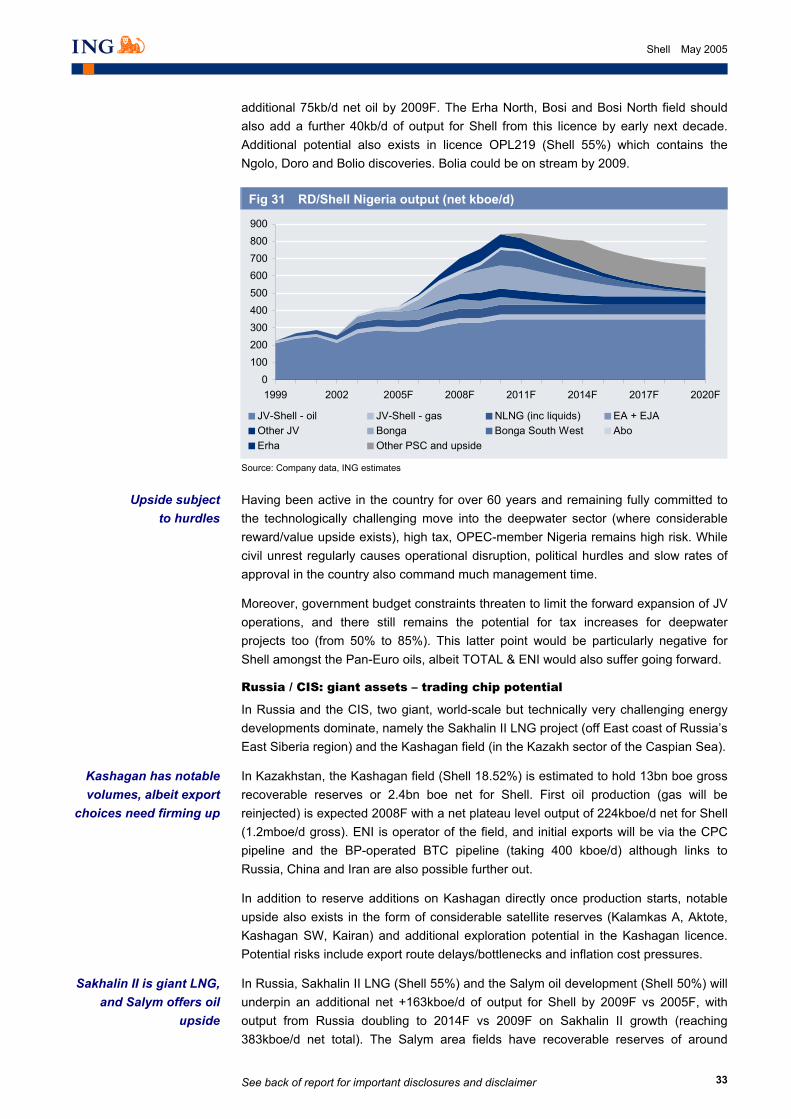

Fig 26 RD/Shell production volumes by country/region (000 boe/d)

2P boe (000's b/d) 2002 2003 2004 2005F 2006F 2007F 2008F 2009F 2010F 2011F 2012F 2013F 2014F

US Lower 48 / GoM shelf 196 135 67 32 27 23 20 17 14 12 10 9 7GoM (deep) profile 535 542 537 525 502 457 381 338 282 229 180 147 124US 731 677 604 557 529 481 401 355 296 241 190 156 131Volume growth (%YoY) 7 -7 -11 -8 -5 -9 -17 -11 -16 -19 -21 -18 -16

UK/Europe Total UK 600 526 445 425 387 340 282 228 189 151 135 114 95EU ex UK 728 763 780 752 750 768 787 809 798 787 737 665 625UK/Europe 1,328 1,289 1,225 1,177 1,137 1,108 1,069 1,038 987 937 872 780 720Volume growth (%YoY) 12 -3 -5 -4 -3 -3 -3 -3 -5 -5 -7 -11 -8

Rest of world Canada - ex heavy oil 125 124 117 118 118 121 120 115 109 105 101 93 82Argentina 8 9 10 9 9 8 8 7 6 5 5 4 3Brazil 2 11 46 47 46 46 42 37 51 77 73 69 65Venezuela 46 46 22 30 40 40 40 49 71 97 92 82 79Other Western Hem' ex Canada 56 66 78 86 95 94 89 93 129 180 170 155 147Other Western Hem’ ex heavy oil 184 194 198 205 213 216 210 208 237 284 271 248 229

Egypt 51 50 46 33 29 25 21 17 14 11 10 9 6Cameroon 17 16 15 15 15 15 14 14 13 12 11 9 7Gabon 46 35 35 34 32 30 28 25 24 21 17 16 14Nigeria (SV & PSC) 257 375 414 424 497 605 703 757 843 847 831 811 804Other Africa 114 101 96 82 76 70 63 56 51 44 38 34 27Africa 322 426 464 473 544 650 745 796 880 880 859 836 825

Iran 36 35 36 36 36 36 36 35 35 35 30 30 25Oman 455 350 327 331 331 342 353 353 353 353 353 353 353Syria 52 46 37 37 32 27 21 16 10 8 5 0 0UAE 100 126 133 132 125 120 120 120 120 120 110 100 90Qatar GTL + LNG 0 0 0 0 0 0 100 100 200 217 243 272 272Middle East 642 557 533 536 524 524 630 623 718 733 741 755 740Kazakhstan 0 0 0 0 0 0 15 69 114 114 114 224 224Russia 33 30 32 34 58 144 171 197 278 268 268 383 383Russia/CIS 33 30 32 34 58 144 186 266 391 381 381 608 607Middle East, Russia, CIS 703 619 590 581 590 672 817 887 1,103 1,106 1,112 1,347 1,335

Australia 156 143 135 129 141 154 150 160 206 253 257 264 303New Zealand 108 69 59 57 57 51 61 63 54 52 50 36 31Brunei 189 198 194 190 185 180 175 170 165 165 160 160 155Malaysia 173 172 174 172 175 174 164 155 152 156 125 128 122Philippines 5 10 14 16 16 16 16 16 16 16 16 16 16Thailand 24 23 0 0 0 0 0 0 0 0 0 0 0China 24 22 20 20 36 52 57 53 53 53 52 51 51Bangladesh 6 6 0 0 0 0 0 0 0 0 0 0 0Pakistan 5 10 14 15 15 15 15 15 14 14 11 9 9Asia Pacific 691 653 610 598 624 642 637 631 660 709 671 665 686

Other (already split as necessary) 18 20 18 17 16 16 16 15 15 15 10 6 6Total ROW inc heavy oil exc Iran 1,900 1,938 1,942 1,947 2,067 2,280 2,508 2,621 2,980 3,139 3,073 3,256 3,356Volume growth (%YoY) 1 2 0 0 6 10 10 5 14 5 -2 6 3

UK/Europe 1,328 1,289 1,225 1,177 1,137 1,108 1,069 1,038 987 937 872 780 720Africa 322 426 464 473 544 650 745 796 880 880 859 836 825Asia Pacific 691 653 610 598 624 642 637 631 660 709 671 665 686Middle East, Russia, CIS 703 619 590 581 590 672 817 887 1,103 1,106 1,112 1,347 1,335US 731 677 604 557 529 481 401 355 296 241 190 156 131Other Western Hem’ - ex heavy oil 184 194 198 205 213 216 210 208 237 284 271 248 229Canada - heavy oil 0 46 80 90 95 100 100 100 100 160 160 160 280

Shell total World (000 boe/d) 3,959 3,904 3,771 3,681 3,733 3,868 3,978 4,014 4,263 4,317 4,135 4,192 4,207

Volume growth (%) 5.7 -1.4 -3.4 -2.4 1.4 3.6 2.8 0.9 6.2 1.3 -4.2 1.4 0.4Rolling 5yr CAGR (%) 1.5 1.2 0.9 0.1 -0.1 -0.5 0.4 1.3 3.0 2.9 1.3 1.1 0.9TARGET (mboe/d) 3.5 - 3.8 3.8-4.0 4.5-5.0

ING Split oil vs gas (% oil) 59.6 60.9 59.7 59.1 59.0 58.0 58.4 57.9 58.5 57.0 56.4 56.3 57.4

Source: Company data, ING estimates. Includes non-zero historical contributions from exited positions (e.g. Bangladesh, Thailand, US Michigan assets). Future profiles exclude potential contributions from Persian LNG (Iran) from 2010, UAE incremental development post 2006, Norwegian gas exploration/development upside (e.g. Onyx), recent Egypt gas discoveries (La52, Kg45), and Malaysia oil upside (Gumusut).

_

See back of report for important disclosures and disclaimer

27

Shell May 2005

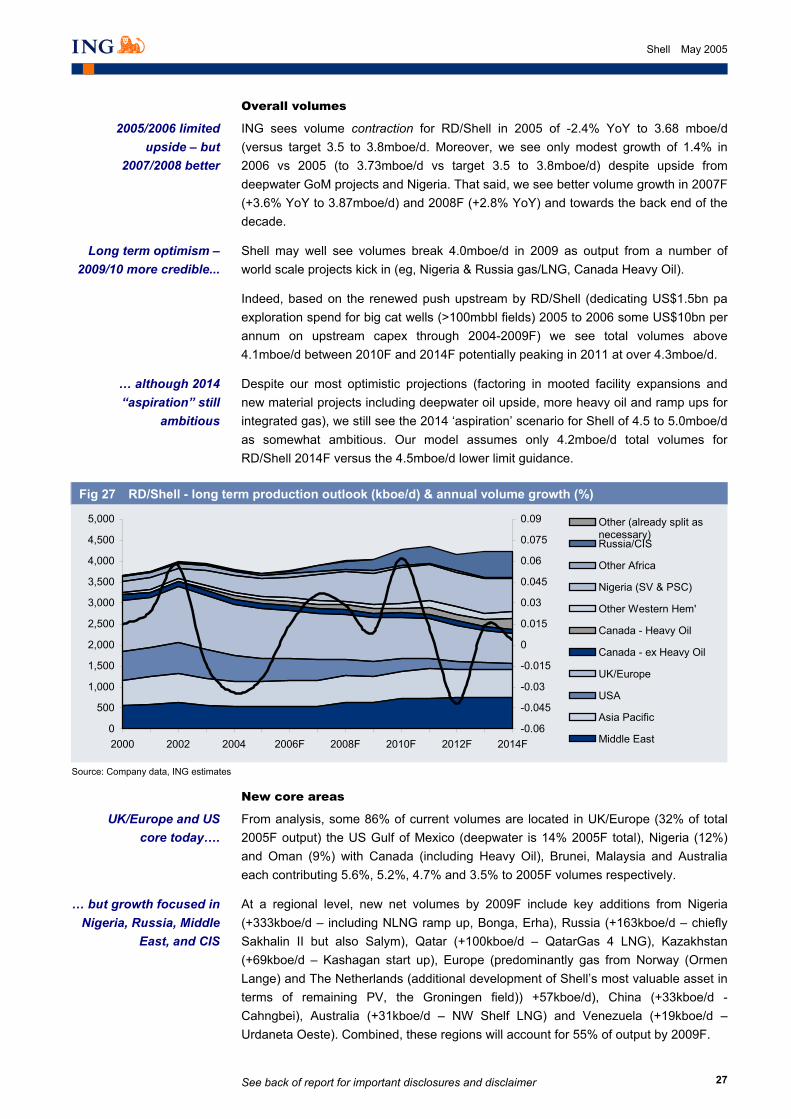

Overall volumes

ING sees volume contraction for RD/Shell in 2005 of -2.4% YoY to 3.68 mboe/d (versus target 3.5 to 3.8mboe/d. Moreover, we see only modest growth of 1.4% in 2006 vs 2005 (to 3.73mboe/d vs target 3.5 to 3.8mboe/d) despite upside from deepwater GoM projects and Nigeria. That said, we see better volume growth in 2007F (+3.6% YoY to 3.87mboe/d) and 2008F (+2.8% YoY) and towards the back end of the decade.

Shell may well see volumes break 4.0mboe/d in 2009 as output from a number of world scale projects kick in (eg, Nigeria & Russia gas/LNG, Canada Heavy Oil).

Indeed, based on the renewed push upstream by RD/Shell (dedicating US$1.5bn pa exploration spend for big cat wells (>100mbbl fields) 2005 to 2006 some US$10bn per annum on upstream capex through 2004-2009F) we see total volumes above 4.1mboe/d between 2010F and 2014F potentially peaking in 2011 at over 4.3mboe/d.

Despite our most optimistic projections (factoring in mooted facility expansions and new material projects including deepwater oil upside, more heavy oil and ramp ups for integrated gas), we still see the 2014 ‘aspiration’ scenario for Shell of 4.5 to 5.0mboe/d as somewhat ambitious. Our model assumes only 4.2mboe/d total volumes for RD/Shell 2014F versus the 4.5mboe/d lower limit guidance.

Fig 27 RD/Shell - long term production outlook (kboe/d) & annual volume growth (%)

0

500

1,000

1,500

2,000

2,500

3,000

3,500

4,000

4,500

5,000

2000 2002 2004 2006F 2008F 2010F 2012F 2014F-0.06

-0.045

-0.03

-0.015

0

0.015

0.03

0.045

0.06

0.075

0.09 Other (already split asnecessary)Russia/CIS

Other Africa

Nigeria (SV & PSC)

Other Western Hem'

Canada - Heavy Oil

Canada - ex Heavy Oil

UK/Europe

USA

Asia Pacific

Middle East

Source: Company data, ING estimates _

New core areas

From analysis, some 86% of current volumes are located in UK/Europe (32% of total 2005F output) the US Gulf of Mexico (deepwater is 14% 2005F total), Nigeria (12%) and Oman (9%) with Canada (including Heavy Oil), Brunei, Malaysia and Australia each contributing 5.6%, 5.2%, 4.7% and 3.5% to 2005F volumes respectively.

At a regional level, new net volumes by 2009F include key additions from Nigeria (+333kboe/d – including NLNG ramp up, Bonga, Erha), Russia (+163kboe/d – chiefly Sakhalin II but also Salym), Qatar (+100kboe/d – QatarGas 4 LNG), Kazakhstan (+69kboe/d – Kashagan start up), Europe (predominantly gas from Norway (Ormen Lange) and The Netherlands (additional development of Shell’s most valuable asset in terms of remaining PV, the Groningen field)) +57kboe/d), China (+33kboe/d - Cahngbei), Australia (+31kboe/d – NW Shelf LNG) and Venezuela (+19kboe/d – Urdaneta Oeste). Combined, these regions will account for 55% of output by 2009F.

2005/2006 limited upside – but

2007/2008 better

Long term optimism – 2009/10 more credible...

… although 2014 “aspiration” still

ambitious

UK/Europe and US core today….

… but growth focused in Nigeria, Russia, Middle

East, and CIS

See back of report for important disclosures and disclaimer

28

Shell May 2005

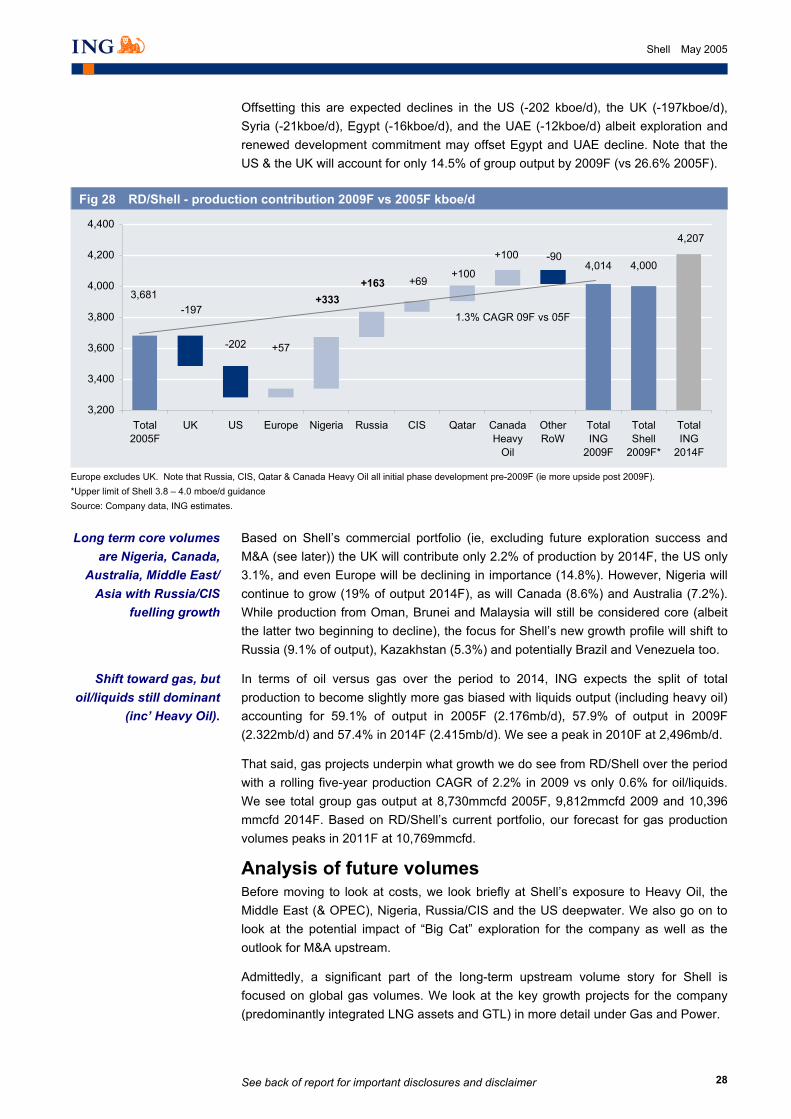

Offsetting this are expected declines in the US (-202 kboe/d), the UK (-197kboe/d), Syria (-21kboe/d), Egypt (-16kboe/d), and the UAE (-12kboe/d) albeit exploration and renewed development commitment may offset Egypt and UAE decline. Note that the US & the UK will account for only 14.5% of group output by 2009F (vs 26.6% 2005F).

Fig 28 RD/Shell - production contribution 2009F vs 2005F kboe/d

4,207

4,0004,014

3,681

+100

+100 -90

+57-202

+69+163+333

-197

3,200

3,400

3,600

3,800

4,000

4,200

4,400

Total2005F

UK US Europe Nigeria Russia CIS Qatar CanadaHeavy

Oil

OtherRoW

TotalING

2009F

TotalShell

2009F*

TotalING

2014F

1.3% CAGR 09F vs 05F

Europe excludes UK. Note that Russia, CIS, Qatar & Canada Heavy Oil all initial phase development pre-2009F (ie more upside post 2009F). *Upper limit of Shell 3.8 – 4.0 mboe/d guidance Source: Company data, ING estimates.

_

Based on Shell’s commercial portfolio (ie, excluding future exploration success and M&A (see later)) the UK will contribute only 2.2% of production by 2014F, the US only 3.1%, and even Europe will be declining in importance (14.8%). However, Nigeria will continue to grow (19% of output 2014F), as will Canada (8.6%) and Australia (7.2%). While production from Oman, Brunei and Malaysia will still be considered core (albeit the latter two beginning to decline), the focus for Shell’s new growth profile will shift to Russia (9.1% of output), Kazakhstan (5.3%) and potentially Brazil and Venezuela too.

In terms of oil versus gas over the period to 2014, ING expects the split of total production to become slightly more gas biased with liquids output (including heavy oil) accounting for 59.1% of output in 2005F (2.176mb/d), 57.9% of output in 2009F (2.322mb/d) and 57.4% in 2014F (2.415mb/d). We see a peak in 2010F at 2,496mb/d.

That said, gas projects underpin what growth we do see from RD/Shell over the period with a rolling five-year production CAGR of 2.2% in 2009 vs only 0.6% for oil/liquids. We see total group gas output at 8,730mmcfd 2005F, 9,812mmcfd 2009 and 10,396 mmcfd 2014F. Based on RD/Shell’s current portfolio, our forecast for gas production volumes peaks in 2011F at 10,769mmcfd.

Analysis of future volumes Before moving to look at costs, we look briefly at Shell’s exposure to Heavy Oil, the Middle East (& OPEC), Nigeria, Russia/CIS and the US deepwater. We also go on to look at the potential impact of “Big Cat” exploration for the company as well as the outlook for M&A upstream.

Admittedly, a significant part of the long-term upstream volume story for Shell is focused on global gas volumes. We look at the key growth projects for the company (predominantly integrated LNG assets and GTL) in more detail under Gas and Power.

Long term core volumes are Nigeria, Canada,

Australia, Middle East/ Asia with Russia/CIS

fuelling growth

Shift toward gas, but oil/liquids still dominant

(inc’ Heavy Oil).

See back of report for important disclosures and disclaimer

29

Shell May 2005

Heavy oil - resource upside

Part of Shell’s long-term growth strategy is based on non-conventional energy including heavy oil (essentially viscous Bitumen - high specific gravity, low hydrogen to carbon ratio) with the company’s efforts focused on the mining of Canadian oil sands. Why? In terms of remaining resources, it is estimated that Canada has some 320 billion barrels of recoverable bitumen contained in its oil sands (20% mineable; 80% In Situ recovery) or around 300bn barrels synthetic crude once upgraded. This compares to estimates of Saudi Arabia’s remaining oil reserves of around 260bn barrels. So, Canada truly offers a world-scale opportunity albeit deep value.

On a global scale, non-conventional oil production (including Gas-To-Liquids (GTL) – see Gas and Power section) is projected to grow from 1.6mb/d in 2002 to 3.8mb/d 2010 and potentially 10.1mb/d in 2030, at which stage it will account for around 8% of global oil supply. The majority (76%) of the non-conventional production gains will come primarily from upgraded Bitumen/synthetic crudes from Canada and also the Orinoco extra-heavy crude oil belt in Venezuela.

In particular, with some US$75bn of investment possible (CN$60bn), Alberta alone is expected to be producing some 700kboe/d of synthetic crude by around 2018-2020 with output of this level sustainable for decades thereafter. Around 50% of this will be upgraded crude from the Athabasca region. Note that while Heavy Oil has comparatively higher operating costs, it offers high margin at high prices due to low government take. Moreover, oil sand assets carry virtually zero exploration risk too.

The overall contribution of heavy oil to Shell’s global portfolio is relatively low at only 2.4% currently, or about 90kboe/d synthetic crude (net 2005F). This is predominantly AOSP1 output (Athabasca Oil Sands Project - Phase 1) which is focused on the Muskeg River resources (approximately 1.6bn boe recoverable reserves gross). although there is a small contribution from the Peace River development too. Shell Canada (owned 78% by Shell) has a net 60% stake in AOSP which is a fully integrated project and includes the Scotford Upgrader located next to Shell’s Scotford Refinery.

Fig 29 Shell net heavy oil output (kboe/d) and % of total production

0

50

100

150

200

250

300

2003 2005F 2007F 2009F 2011F 2013F 2015F 2017F 2019F0.0%

1.0%

2.0%

3.0%

4.0%

5.0%

6.0%

7.0%

8.0%

9.0%

Total Heavy Oil Production (kboe/d) Heavy Oil Prod as % of total production

Source: ING, Company Estimates

_

As new projects come on stream in subsequent AOSP phases (including the Muskeg River Expansion (2006/2007), Jackpine Mine Phase 1 (2011), and Jackpine Mine Phase 2 (2014) the percentage contribution of Heavy Oil production for Shell could reach 7% or around 280kb/d net for Shell by 2014.

Canadian oil sands – a world-scale resource

Increasing importance for RD/Shell - long term

Large investment, sustainable plateau

output, and high margins under robust

oil prices

Huge potential for upside in reserves

bookings

See back of report for important disclosures and disclaimer

30

Shell May 2005

This plateau level of output is considered plausible for 30 years thereafter – with upside from additional development very possible given the giant resource availability and expansion opportunities. ING estimates that so far only around 0.9bn boe of the potential 3.9bn boe net (6.5bn boe gross) recoverable resource exposure has been booked by Shell, which in itself offers upside for reserve replacement to 2010F (see earlier). Moreover, gross reserves in place are estimated at 9bn to 10bn boe in place offering room for recovery upside.

Mining and upgrading projects in Canada have become much more competitive these days with a total cost for recovery/upgrading estimated at around US$12/bbl today (versus >US$20/bbl in the early 1990s). This is now in line with the more energy-intensive in situ projects which usually incorporate steam-assisted gravity drainage (SAGD) or the injection of heat (as steam) to allow bitumen to flow and be recovered.

While both types of recovery are attractive at today’s oil price (returns of 20% plus under a US$20/bbl base case obviously vastly increased under the current US$45/bbl oil price, with the value of projects also increasing directly in proportion to oil price moves in percent terms), we note that the cost of steam production remains particularly sensitive to gas prices, which remain high. This provides added pressure for in-situ heavy oil recovery over mining projects, albeit higher energy costs affect both. Labour remains a key cost concern in Canada too given limited manpower availability.

Note that heavy oil and synthetic crude by its nature requires refineries with a higher complexity to refine it into oil products such as gasoline or jet fuel. Obviously the integrated nature of AOSP and Scotford in Canada offers particular synergies for Shell. In addition though, Shell’s higher Nelson’s complexity in Canada and the US also offers upside for the medium-term at least given the fact that Heavy/Light crude differentials have increased and a greater margin on refining heavy crude is possible. This is looked at further in the Oil Products section later.