sÍntese - inglês · prospectiva e estratégia 2000 – 2020”, verbo, lisbon, ... marques, p....

TRANSCRIPT

ENGINEERING AND TECHNOLOGY FOR THE DEVELOPMENT OF PORTUGAL:

Technology Foresight, 2000 – 2020

- SYNTHESIS -

L. Valadares Tavares

CESUR – Centre of Urban and Regional Systems – Dept. of Civil Engineering and Architecture – Instituto Superior Técnico (IST), LISBON - PORTUGAL http:\\www.civil.ist.utl.pt/~et2000

Abstract

The Project Engineering and Technology 2000 (ET 2000) was launched by three institutions, the Academy of Engineering (AE), the Society of Engineers (OE) and the Portuguese Industrial Association (AIP) on late 1999 and was completed on the end of 2000. A foresight project is always a process of analysis, conception and development searching for a more clear perspective about problems, tensions or woes, and oriented to design and to propose better approaches and strategies. ET 2000 was no exception. Still, as a Technology Foresight Project, specific questions were raised before being launched: A – Does Portugal, as a small economy, need a Technology Foresight Project? B – Should it be a Top-Down project or a Bottom-Up process? C – Which goals? D – Which approach? The developed project was based on clear answers to these questions: A – Yes, but not to “rediscover”, once again, the most promising key technologies. That has been already studied, several times, from US to France, and the frontiers of knowledge are universal. The answer to this question is yes, but to produce an updated diagnosis of the use of our Engineering and Technology (E&T) know-how, for a more sustainable and competitive economy, during coming decades, and to develop a strategic vision about our future. B – A major challenge is the integration of experiences, opinions and know-how distributed through many professionals and institutions and therefore the basic “infra-structure” of this project should be a network based on an initial group and developed by diversified bottom-up processes. C – Major goals are the identification of strong and weak points of our E&T system, to build up scenarios for the next 10-20 years and to propose strategies to improve its contribution to the sustainability and competitiveness of portuguese society. D – Therefore, the adopted approach was demand-driven, starting from needs and trends of the studied economic sectors and looking for the major potential contribution of knowledge to achieve a better performance. The main results were published in a book presented and discussed by 400 participants, last November, during a Conference carried out at INETI (27-28 November 2000), and major contributions are included in this synthetic description. They cover: a) the adopted process and methodology including some new instruments like the model of impact matrices

applied to the 17 economic sectors; b) a diagnostic perspective about how Portugal can meet the challenges of a knowledge-based society

emphasizing six major “horizontal” issues: c) major scenarios and strategic proposals. Finally, specific initiatives are discussed and presented herein.

L. Valadares Tavares

NOTE This book presents major analyses and proposals developed by the FORESIGHT PROJECT “ENGINEERING AND TECHNOLOGY 2000 (ET 2000)” promoted by Academia de Engenharia (Academy of Engineering), Ordem dos Engenheiros (Society of Engineers) and Associação Industrial Portuguesa (Portuguese Industrial Association) during 1999 and 2000. The final report of this project was published as a book, Tavares, L. V., “A Engenharia e a Tecnologia ao Serviço do Desenvolvimento em Portugal: Prospectiva e Estratégia 2000 – 2020”, VERBO, Lisbon, 2000 (in portuguese). This synthetic presentation is based on that book and on the specialized reports written by several colleagues from firms and universities: Abel Mateus, António Antunes e Maria Filomena Medes Paulo Ferrão, Ascenso Pires e Ângela Canas Manuel Heitor e Pedro Conceição Amado Silva e Francisco Mendes Palma José Paulo Esperança Maria da Conceição Santos Gaspar Nero e Silvia Nereu Fernando Branco e Adriana Garcia Jaime Melo Baptista e Eduarda Beja Neves Alberto Moreno e Francisco Mendes Palma Xavier Malcata e F. Gomes Silva Epifânio da Franca Ruy Mesquita, Paulo Peças e Sales Gomes Rui Felizardo, Alexandre Videira e Luís Palma Féria Luís Almeida Joaquim Leandro de Melo e Fortunato Frederico Ramôa Ribeiro e Clemente Pedro Nunes José Manuel Viegas José Filipe Rafael e António M. Beja Altamiro Machado e Eduardo Beira João Bento, Rui Gonçalves Henriques, Cristina Gouveia e Beatriz Condessa Manuel João Pereira Ricardo Oliveira e Luís Maltez Carlos Henggeler Antunes, Carla Oliveira, Luís Lapão. The participation of several colleagues during the November Conference was also particularly important, namely: António Alfaiate, Luís Mira Amaral, F. Nunes Correia, Sousa Gomes, Mário Lino, M. Athayde Marques, P. Norton de Matos, Maximiano Martins, Carlos Campos Morais, Manuel Norton, Maria João Rodrigues, João Salgueiro, J. Gomes Simão, Sérgio Trindade, Special thanks are due to the cooperation of Manuel Heitor, João Bártolo, C. Henggeler Antunes and Luís Lapão. Our foreign colleagues were a source of useful inspiration but special thanks are due to Prof. James Kahan from RAND Europe for his innovative and friendly suggestions. The project ET 2000 was carried out by CESUR – Centre of Urban and Regional Systems of the Department of Civil Engineering and Architecthure (DEC) of IST (Instituto Superior Técnico) under a contract with the Portuguese Industrial Association. Thanks are due to Patrícia Nunes for processing this document. The author is responsible for any deficiency or limitation of this book.

L. Valadares Tavares

iii

INDEX

1 THE PROJECT: ET 2000....................................................................................................................... 2

1.1 OBJECTIVES ................................................................................................................................... 2 1.2 METHODOLOGY............................................................................................................................ 2 1.3 THE PROCESS................................................................................................................................. 6

2 PORTUGAL 2000: WHAT ECONOMIC, BUSINESS, TECHNOLOGICAL AND ENVIRONMENTAL DIAGNOSIS? ............................................................................................................ 10

2.1 DEVELOPMENT AND KNOWLEDGE ......................................................................................... 10 2.2 DEVELOPMENT AND ENVIRONMENT...................................................................................... 14

2.2.1 Environment and Industrial Ecology ........................................................................................ 14 2.2.2 Thematic Challenges................................................................................................................ 15 2.2.3 Growth with more pollution and consumption of materials ....................................................... 16

2.3 ECONOMIC DEVELOPMENT AND INNOVATION .................................................................... 17 2.4 DEVELOPMENT, INTERNATIONALIZATION AND TECHNOLOGICAL MARKETING.......... 19 2.5 DEVELOPMENT AND HUMAN CAPITAL .................................................................................. 20

2.5.1 Higher Education..................................................................................................................... 21 2.5.2 Research and Development (RD).............................................................................................. 22

2.6 PORTUGAL BENCHMARKING ................................................................................................... 24

3 WHICH FUTURE SCENARIOS?........................................................................................................ 31

3.1 EUROPE......................................................................................................................................... 31 3.2 TECHNOLOGICAL FUTURE........................................................................................................ 33 3.3 THE PORTUGUESE SOCIETY ..................................................................................................... 34 3.4 STUDIED SECTORS...................................................................................................................... 35

3.4.1 Building Materials ................................................................................................................... 35 3.4.2 Construction............................................................................................................................ 36 3.4.3 Environment ............................................................................................................................ 36 3.4.4 Energy..................................................................................................................................... 36 3.4.5 Food and Beverages ................................................................................................................ 37 3.4.6 Electronics............................................................................................................................... 37 3.4.7 Metal and Plastic Production ................................................................................................... 38 3.4.8 Automobile Industry................................................................................................................. 38 3.4.9 Textiles and Clothes................................................................................................................. 39 3.4.10 Shoes ....................................................................................................................................... 39 3.4.11 Chemical Industry.................................................................................................................... 40 3.4.12 Transportation......................................................................................................................... 41 3.4.13 Telecommunications ................................................................................................................ 41 3.4.14 Information Technologies......................................................................................................... 42 3.4.15 Geographical Information Systems (GIS) ................................................................................. 43 3.4.16 Financial Services.................................................................................................................... 43 3.4.17 Engineering Services................................................................................................................ 44

4 STRATEGIES AND POLICIES........................................................................................................... 46

4.1 ENVIRONMENT AND INNOVATION.......................................................................................... 46 4.2 COMPETITIVENESS AND KNOWLEDGE................................................................................... 46 4.3 KNOWLEDGE AND COMPETITIVENESS FOR THE 17 STUDIED SECTORS .......................... 49 4.4 A STRATEGIC VISION FOR ENGINEERING AND TECHNOLOGY IN PORTUGAL ................ 52

4.4.1 Conditions ............................................................................................................................... 52 4.4.2 Guidelines ............................................................................................................................... 53

4.5 PROPOSALS.................................................................................................................................. 55 4.6 FINAL WORDS.............................................................................................................................. 60

5 REFERENCES...................................................................................................................................... 61

ANNEX: The network of the Human Capital

iv

“A NEW STRATEGIC GOAL FOR THE NEXT DECADE: TO BECOME THE MOST COMPETITIVE AND DYNAMIC KNOWLEDGE – BASED ECONOMY IN THE WORLD”

Lisbon Council of the European Union 23-24 March 2000

“IN MY VILLAGE, WE WERE POOR, EVEN THE RICH PEOPLE, BECAUSE WE HAD NO SENSE OF FUTURE”

Salvador Caetano, CEO of the automobile sector Portugal, June 2000

“THE MISSION OF FORESIGHT IS NOT PLANNING THE FUTURE BUT RATHER PLANNING FOR THE FUTURE AS IT IS BECOMING MORE UNCERTAIN AND UNPREDICTABLE”

L. Valadares Tavares November 2000

v

INSTITUTIONAL PERSPECTIVES: “… we have to boost technology and innovation with the purpose of increasing competitiveness and productivity of portuguese firms. I have accepted to be the Chairman of the Honour Committee of ET 2000 to underline the merits of its objectives and methodology. We have to share experiences, woes and expectations in order that easy turnkey solutions will be rejected and a new more promising future will be invented”

Jorge Sampaio, Presidente da República “… We hope that the results of ET 2000 will contribute to the mission of Academia de Engenharia: “PRO HOMINIS DIGNITATE INGENIUM”

Armando Lencastre, Presidente da Academia de Engenharia “… Engineering and technological qualifications are essential to cope with economic growth and increasing societal complexity. Therefore, Engineering and Technology are key factors for a development model towards the Knowledge Society”

Francisco Sousa Soares, Bastonário da Ordem dos Engenheiros “… The main reason to launch this project stems from the awareness about the nature of the key challenges for the future of Portugal: strategic development and use of Engineering and Technology know-how to improve sustainability and competitiveness of our firms”

João Bártolo, Presidente do Conselho Orientador

1

1. THE PROJECT: ET 2000

“The void o’th’ world must with an arch be spanned The ways of Nature must be read aright That there may be a wise and friendly hand To make this dark world better and more bright Oh, with what joy and love I understand These master-souls that ache for truth and light” Fernando Pessoa*, 1907

* Fernando Pessoa is a portuguese poet born in South Africa and considered as one of the most important european poets of the 20th century. He has a complex heteronymic structure and a vast collection of poems, written in portuguese, french and english with deep insights about the identity and the future of Portugal and of Europe.

2

1 THE PROJECT: ET 2000 1.1 OBJECTIVES The challenges of economic development are requiring a new conception of corporation, opening wider perspectives on strategy, market relationship, reengineering, benchmarking and human capital. However, during the last years, the crucial role of the engineer or of the technologist in many portuguese firms is being faded gradually and is been replaced by more attractive and popular profiles based on Management, Business, Commerce. An well known portuguese CEO when asked about technology gave a clear answer: if required, we will buy it! Therefore, a central and open question to be examined is: what is the role of Engineering and Technology (E&T) to increase the competitiveness of our firms and to improve the pace of development for Portugal. This is the research question of ET 2000 aiming to propose specific actions to boost the contribution of Engineering and Technology for the development of our country. The specific goals of ET 2000 are: A – Discussion of major scenarios for portuguese firms B – Competitiveness analysis C – Diagnosis of human capital D – Study of knowledge and innovation networks E – Enhancing the contribution of E&T role for major value chains F – Design of E&T profiles and evaluation of strategic options G –Strategic analysis about the role of Research and Development (RD), Education and Training H – Promotion of debates. 1.2 METHODOLOGY ET 2000 concerns Engineering Technology and Competitiveness and hence basic definitions have been proposed: Engineering: Conception, design and implementation of systems or the production of goods or services devoted to the fulfilment of society’s needs, founded on scientific and technological knowledge and developed according to paradigms of ethics, effectiveness and efficiency as well as environmental sustainability and equilibrium. Technology: Capacity to develop artefacts through operational applications of scientific knowledge with the same paradigms of Engineering. Competitiveness: ability to promote sustainable and profitable sales in markets with strict requirements. The adopted methodology has been based on several scientific contributions and on original interdisciplinary models. Such contributions include proposals by (Godet, 1991), OECD (OECD, 1977) and Rand (Kahan and Cave, 2000). They emphasize the open and process oriented nature of Foresight, the belief that we can construct a better future and the commitment to support a strategic vision about the role of E&T. The proposed models include:

3

I – A cross-disciplinary networking based on ISSUES and SECTORS: ISSUES: Macro-Societal Scenarios, Macro-Economic Scenarios, Business Dynamics, Environment, Innovation, Technological Marketing, Internationalization SECTORS: Building Materials, Construction, Environment, Energy, Food Industry, Electronics, Metal and Plastic Products and Manufacturing, Automobile Industry, Textiles and Fashion, Shoes Industry, Chemical Industry, Transports and Distribution, Telecommunications, Information Technologies, Geographic Information Systems, Financial Services, Engineering Services. II – A specification of major Areas of Knowledge for ET 2000 After several debates, the following list was selected (each area is subdivided in 4 to 6 sub-areas): • Process Technologies (PR) • Biotechnology (BT) • Materials (MT) • Discrete Production (DP) • Energy (EN) • Opto – Electronics (OE) • Information and Communication • Systems Engineering (SE) • Infra-Structuring and Construction (ICT) • Environmental Technologies (ET) • Transportation Technologies (TT) III – a taxonomy of knowledge This classification has a key role in ET 2000 as it is not based on traditional schemes but rather on the strategic functionality of each type of knowledge: A – Planning and Evaluation B – Procurement C – Conception and Design D – Production E – Integration and Management F – Maintenance G – Rehabilitation H – Use and Operation I – Training IV – A firm’s value chain for knowledge The adopted model is presented in Fig. 1.1.

4

Value Chain for Knowledge Fig. 1.1

Policies Strategic

Development Tactical and Operational

Management

Driving and Leadership

Process Supply Products

Technological Infra-structure

RD Skills (Human Resources) Equipments

Materials

Equipment Patents And Rights

X X X

Channels Competitors

Markets

X X X

5

V – Impact Matrices These matrices describe the impact of each area of knowledge (i = 1, …, M = 11) I on each type product (j=1, …, Nk) of each economic sector of activity (k=1, …, K=17). Thus, for each sector k, a survey was carried out to estimate the impact level of i on j:

)k(Xij

where )k(Xij is a measure of the relevance of area i for j in sector k

The following indicators can be computed in terms of Xij: Average Relevance of Area i for Sector k

)k(J)k(X)k(Y)k(J

1jiji

∑==

where J(k) is the number of products for sector k. Technological Intensity of Sector k

)k(I

)k(Y)k(YS

)k(I

1ii∑

= =

where I (k) is the number of areas with Yi (k)>0. Technological Dispersion of Sector k

( )[ ]11M

2kYN)k(DS i

=≥

=o

Areas i=1, …, M

0 – No impact 1 – Small impact 2 – High impact 3 – Very high impact

Products

j = 1, …, Nj

)k(Xij

for each k

6

Global Relevance of Area i

K

)k(YZ

K

1ki

i

∑= =

Construction of Scenarios The construction of Scenarios was based on the combination of different types of evolution for key morphological features of Europe and of Portugal. The following features were identified: a) Europe: Competitiveness Social Protection Integration Fragmentation b) Portugal: Civil Society State Transformation Stagnation International Openness Closeness Sustainability Unstability

1.3 THE PROCESS The development of a Foresight Project is useful not just for its results but also for the developed process. The ET 2000 process was based on a rich and diversified system of networks involving multiple actors with different motivations: A – Coordinators and Co-coordinators of specialized groups: LEADERS – NETWORK Each issue or analysed sector had a specialized group which was chaired by a coordinator (“pilot”) and co-coordinator (“co-pilot”). The former was an academic and the latter coming from a related business. This network brought to the project a vast and diversified ground of experiences and knowledge. In Fig. 1.2 the main academic and business institutions are represented.

7

Leaders - Network Fig. 1.2

AUL – Autonomous University of Lisbon

IST – Higher Technical Institute (Technical

University of Lisbon)

LNEC – National Laboratory of Civil

Engineering

UNL – New University of

Lisbon

ISCTE – Higher Institute for Sciences of Labour

and Administration

Minho University

UC – Coimbra University

UCP – Portuguese Catholic University

IST (Coordination)

FEUP – Faculty of Engineering of Oporto University (INESC)

CNIG COBA

CHIPIDEA

EFACEC

IPE

ITEC

Luís Simões

Papelaco

PT - Inovação Quimigal Renault

Somague

Agência para o investimento

no Norte

AD-TRANS

BANIF

CAP-Gemini

8

B – Representatives of public and private institutions: Academic – Business Council: ADVISORY NETWORK This council met in important moments of the project to give strategic advises about the development of the project. Furthermore, additional meetings were organized by AIP by AEP (Portugal Business Association) and by OE. C – International methodologic group: INTERNATIONAL PANEL This group includes Mr. Barry Stevens, OECD International Futures Programme, Prof. David Gibson, IC2 Institute, The University of Texas at Austin, USA, Prof. Giorgio Sirilli, Inst. Of Studies of Scientific Research, ISRDS, IT, Prof. H. Muller-Merbach, Kaiserslautern University, Germany, Prof. J. P. Contzen, Scientific Advisor of the Minister of Science and technology during the Portuguese Presidency of the EU, Prof. James Gavigan, IPTS, European Commission, Dr. James Kahan, Rand Europe, Dr. Jonathan Cave, Rand Europe, Prof. Keith White-Hunt, Hong-Kong Science and Technology University, PRC, Prof. Konstandinos Goulias, The Pennsylvania State University, USA, Prof. Peter Idenburg, Delft Univ. Technology, NL, Prof. Leo Jansen, Interdept. Research Programme Netherlands, Prof. Robert Wilson, LBJ School of Public Affairs, The University of Texas at Austin, USA, Dr. Thomas Haeringer, Baden-Wurttemberg, DE, Prof. Wolfgang Michalski, OECD, International Futures Programme (Director). Three meetings about international cooperation and methodological issues have taken place in Lisbon. The general structure of the project is represented in Fig. 1.3:

ET 2000 Structure

Fig. 1.3

HONORARY CHAIRMAN OF ET 2000: HIS EXCELLENCY THE PRESIDENT OF REPUBLIC

CHAIRMANSHIP OF THE PROJECT Prof. Armando Lencastre (AE), Comendador Jorge Rocha de Matos (AIP), Eng.º Sousa Soares (OE), Eng.º João Bártolo, Prof. Luís Valadares Tavares, Eng.º Pereira do Vale

ADVISORY COMMITTEE

Eng.º João Bártolo (presidente), Eng.º Marques Videira (AE), Eng.º António Alfaiate (AIP), Eng.º Viana

Baptista (OE), Prof. Luís Valadares Tavares (Director), Eng.º Pereira do Vale (General Secretary)

CONFERENCE COMMITTEE

Prof. L. Valadares Tavares (president), Prof. Ricardo Oliveira (AE), Prof.ª Graça Carvalho (OE), Eng.º

Luís Lapão (IST), Dr. Pereira Bastos (AIP)

DIRECTOR OF THE PROJECT Prof. Luís Valadares Tavares

PROJECT TEAM - CESUR

ACADEMIC – BUSINESS COUNCIL

Prof. Luís Valente de Oliveira

LEADERS NETWORK and SPECIALIZED GROUPS

9

2. Portugal 2000: What Economic, Business, Technological and Environmental Diagnosis?

“This is a country, measureless – but real More than the life the world appears to have And more the Nature itself natural To the frightening truth of being alive Fernando Pessoa , 1910

10

2 PORTUGAL 2000: WHAT ECONOMIC, BUSINESS, TECHNOLOGICAL AND

ENVIRONMENTAL DIAGNOSIS? 2.1 DEVELOPMENT AND KNOWLEDGE Portugal is experiencing a process of growth, increasing income and consumption, changing values and uses, moving from primary and manufacturing activities to a more open and services oriented economy. Portuguese GDP expressed in PPP (Purchased Parity Power) is presented in terms of EU average in next figure.

Real Convergence to European Union

30

40

50

60

70

80

90

100

110

120

19601961

1962196

31964

19651966

19671968

1969

19701971

19721973

1974197

51976

19771978

19791980

198119

82198

31984

19851986

198719

881989

19901991

19921993

1994

19951996

19971998

1999

Espanha Irlanda Portugal

Real Convergence to European Union

Fig. 2.1 This growth can be explained by the usual factors – Labour (L), Human Capital (H), Physical Capital (F) using Cobb-Douglas methodology and the average annual growth rates of these magnitudes are presented on Table 2.1.

Table 2.1 Average Rates of Annual Growth for Portuguese Economy

Period L

H F Residuals (Total

productivity, P) GDP

50-60 0.20 1.14 2.44 0.51 4.29 60-70 0.26 0.42 2.37 2.80 5.85 70-80 -0.29 1.69 2.36 1.47 5.24 80-90 0.03 1.43 1.49 1.26 4.21 90-00 0.15 1.50 1.42 -0.22 2.84

The following conclusions can be drawn up: - growth has slowed down last decade;

Ireland

Spain

Portugal

%

11

- during eighties, H and P have a similar growth, near 1/3 of the total; - during the nineties, the total productivity growth is negative and the growth of L and F is similar This analysis is consistent with the low productivity existing in Portugal (1997) around 58% of OECD average:

Country GDP for working hour

(% of OECD average) Australia 96 Austria 102 Belgium 128 Canada 97 Denmark 92 Finland 93 France 123 Germany 105 Greece 75 Ireland 108 Italy 106 Japan 82 Netherlands 121 New Zealand 69 Norway 126 Portugal 56 Spain 84 Sweden 93 Switzerland 94 Turkey 36 UK 100 US 120 EU=14 103

Obviously, there results are also correlated with the Gross Added Value sectoral structure as it is shown in Fig. 2.2 where the small contribution of “knowledge sectors” for Portugal is quite clear:

0

10

20

30

40

50

60

% T

otal

Icel

and

Portu

gal

Nor

way

Spa

in

Spai

n

New

Zea

land

Cor

ea

Italy

Mex

ico

Den

mar

k

Finl

and

Aus

tria

Bel

gium

Aus

tralia EU

Fran

ce

Net

herla

nds

Swed

en

OC

DE

Can

ada

Uni

ted

King

dom

Japa

n

EUA

Ger

man

y

1: High Technology Industry 2: Medium Technology Industry 3: 1 + 24: Communications 5: Banking and Insurance Community Services and Others7: 5 + 6

Knowledge Sectors

Fig. 2.2

3

1

2

4

5

7

6

12

35

55

75

95

115

135

155

30.00 35.00 40.00 45.00 50.00 55.00 60.00 65.00

% of knowledge sectors in total GAV (1997)

GD

P (P

PP) a

s % o

f UE

aver

age

(199

7)

Portugal

NorwayDenmark

FinlandItaly

SpainNew Zealand

Mexico

Hungary

Belgium

AustraliaFrance

U. K.Sweden

Netherlands

GreeceCorea

JapanCanada

EUA

Germany

Relationship between GDP and “Know ledge sectors”

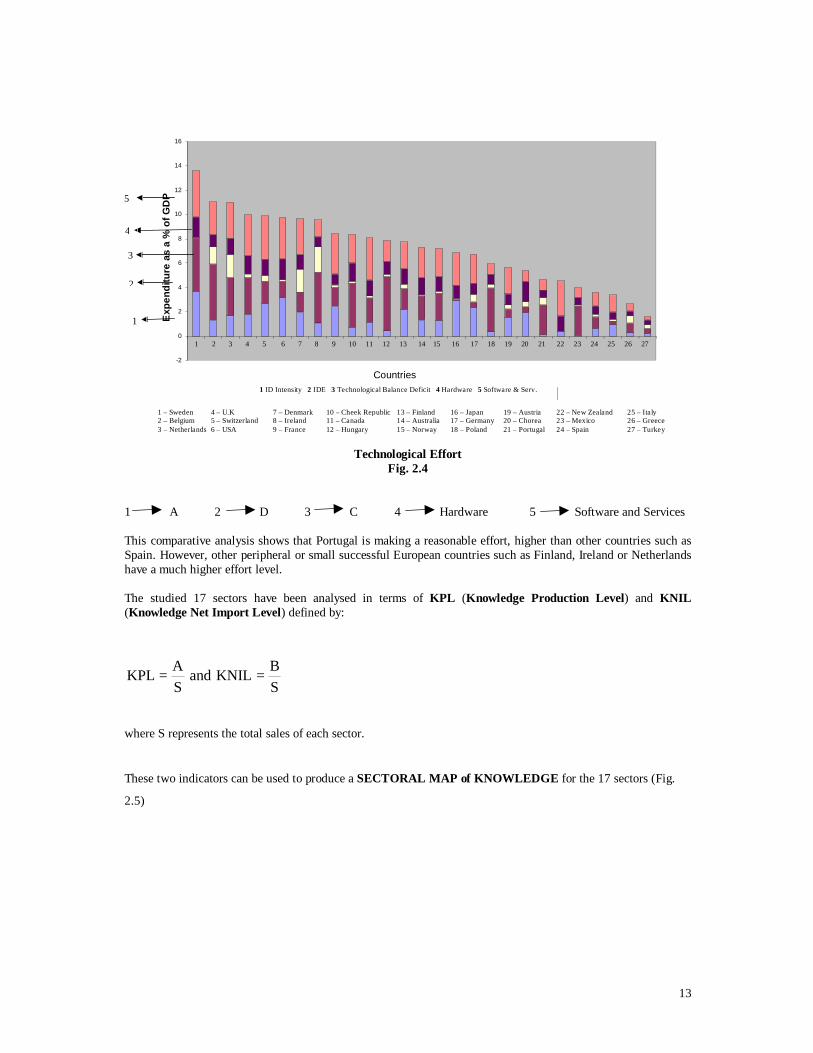

Fig. 2.3 These results are important because GDP tends to be correlated with the percentage of the “knowledge sectors” in total GAV (Fig. 2.3). Therefore, special attention should be given to the diagnostic analysis of the technological effort carried out by Portugal and such analysis is based on a new indicator proposed by ET2000 and called, Technological Effort – TE defined by the sum of: A – RD expenses B – Net Deficit of the National Technological Balance (just for non-incorporated technology) C – Acquisition of computer systems (hardware, software, services) D – Foreign Direct Investment A is measure of the production of knowledge, B describes the net import of knowledge, C includes the investment on Information Technology and D measures an important inflow assuming that it is associated to a higher level of knowledge or technology. All these indicators are expressed as a percentage of GDP. The estimated TE for Portugal is compared to other OECD countries (Fig. 2.4):

13

-2

0

2

4

6

8

10

12

14

16

Exp

endi

ture

as

a %

of G

DP

I&D Intensity IDE Débitos Balança Tecnológica Hardware Software & Serv.

Countries

1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 25 26 27

Technological Effort Fig. 2.4

1 A 2 D 3 C 4 Hardware 5 Software and Services This comparative analysis shows that Portugal is making a reasonable effort, higher than other countries such as Spain. However, other peripheral or small successful European countries such as Finland, Ireland or Netherlands have a much higher effort level. The studied 17 sectors have been analysed in terms of KPL (Knowledge Production Level) and KNIL (Knowledge Net Import Level) defined by:

SBKNILand

SAKPL ==

where S represents the total sales of each sector.

These two indicators can be used to produce a SECTORAL MAP of KNOWLEDGE for the 17 sectors (Fig.

2.5)

5

4

3

2

1

1 ID Intensity 2 IDE 3 Technological Balance Deficit 4 Hardware 5 Software & Serv.

1 – Sweden 4 – U.K 7 – Denmark 10 – Cheek Republic 13 – Finland 16 – Japan 19 – Austria 22 – New Zealand 25 – Italy 2 – Belgium 5 – Switzerland 8 – Ireland 11 – Canada 14 – Australia 17 – Germany 20 – Chorea 23 – Mexico 26 – Greece 3 – Netherlands 6 – USA 9 – France 12 – Hungary 15 – Norway 18 – Poland 21 – Portugal 24 – Spain 27 – Turkey

14

0.000%

0.100%

0.200%

0.300%

0.400%

0.500%

0.600%

0.700%

0.800%

-0.01 -0.005 0 0.005 0.01 0.015 0.02Knowledge Net Import Level

Kno

wle

dge

Prod

uctio

nLe

vel (

KPL)

EL

IT

FS

CHMP

TLEV

EN

TDFI

ES

TX

SI

CT

BM

AI

Building Materials (BM), Construction (CT), Environment (EV), Energy (EN), Food Industry (FI), Electronics (EL), Metal and Plastic Products and Manufacturing (MP), Automobile Industry (AI), Textiles (TX), Shoes Industry (SI), Chemistry (CH), Transportation and Distribution (TD), Telecommunications (TL), Information Technologies (IT), GIS, Financial Services (FS), Engineering Services (ES)

Sectoral Map of Knowledge Fig. 2.5

It should be noted that KPL may be underestimated for Engineering Services and Environment as they rely also on significant RD carried out by universities and other public institutions. This figure shows that: - there is a group of sectors with reasonably high level of knowledge production: Chemistry, Technology

Information, GIS, Electronics, Metal and Plastic Products and Manufacturing and Engineering Services. - Engineering Services are, by far, the most relevant exporter of knowledge - The Automobile industry is an exceptional case where there is a high level of imports of knowledge but

negligible production - The curve suggests different stages of an evolution towards an export stage - There is a cluster of sectors with very little activity either producing or important knowledge. 2.2 DEVELOPMENT AND ENVIRONMENT

2.2.1 Environment and Industrial Ecology Sustainable development implies keeping harmony between the environmental equilibrium and the pressure generated by growing consumption as well as by a more intensive use of resources. This is the main motivation for the development of Industrial Ecology (Graedel and Allenby, 1995). This approach implies considering the integrated life cycle of any product as a closed cycle of any product minimizing wastage and discovering new ways to recycle, to reuse, to recover, to rehabilitate whatever has to be extracted or produced to fulfil needs and demand. All externalities have to be identified and different schemes can be suggested to implement this new approach such as: - recycling systems within industry - exchange systems for residuals creating a market between different industries and sectors - industrial eco-parks developing a regional framework to optimize all processes required by Industrial

Ecology.

- NPC

15

This new domain is a source of business innovation creating new opportunities for the “green” business and for SMEs (Small and Medium Enterprises) as it is shown by (Esty and Porter, 1998).

2.2.2 Thematic Challenges Several organizations have focused major thematic challenges for environment, namely: - Environment European Agency, (EEA, 1999) - Direcção – Geral do Ambiente, (DGA, 1999) and the following list can be quoted: I → Greenhouse effect II → Ozone decay III → Air quality IV → Water resources scarcity V → Soils VI → Waste VII → Natural and technological risks VIII → Biodiversity IX → Genetical modified organisms The study of these 9 issues requires appropriate indicators and they can be classified according to their meaning to understand environmental processes: DF → Driving forces P → Pressure S → State I → Impact R → Response The present situation of these indicators for Portugal can be described in terms of three different alternative situations: A → Availability of Indicators and Data B → Availability of Indicators but Unavailability Data C → Unavailability of Indicators and of Data.

1 2 3 4 5 6

Building Materials Construction Environment Energy Food Industry Electronics

DF P S I R DF P S I R DF P S I R DF P S I R DF P S I R DF P S I R

I C A B C B C A B C C A A B C A C C B C C

II C B B C B C C B C C

III C C B C B C C B C B A A B B B C B B C C

IV A A B C B C C B C B

V A C B C B

VI C A C C C C A C B B B B C C C A A C B B C C C C C C A C C B

VII A B C C C

VIII A B A C B

16

7 8 9 10 11 12 Metal and Plastic

Products and Manufacturing

Automobile Industry Textiles Shoes Industry Chemistry Transportation and Distribution

DF P S I R DF P S I R DF P S I R DF P S I R DF P S I R DF P S I R

I C B C C C A A B C A A A B C A

II

III C A B C C A A B C A C A B C B A A B B B

IV C C C B C C B C B C C B B B C

V C B B C C A A B C C C C B C B C B B C B A A C C C

VI C A C C C A A C C C C A C C C C

VII C C B C C C B C C C

VIII A A A C C

2.2.3 Growth with more pollution and consumption of materials The overall level of pollution per inhabitant is lower in Portugal than the EU average as we have a lower industrial production. However, the analysis of the pollution load generated in each GDP unit shown that its level is increasing. In Table 2.2, the production of gases (greenhouse effect) per GDP unit (106 PTE) is presented for 1990 and 1995.

Table 2.2 CO2 CH4 N2O NOx CO NMVOC*

1990 1995 1990 1995 1990 1995 1990 1995 1990 1995 1990 1995

Energy 12.78 22.49 0.0021 0.005 0.0002 0.0003 0.05 0.08 0.003 0.006 0.020 0.07

Metal and Plastic Products

and Manufacturing 0.50 0.81 37 34 14 19 0.00001 0.00001 0.01 - 1.8E-05 2.2E-05

Food Industry 0.48 0.51 240 277 34 33 - - - - - -

Textiles 0.74 0.82 78 73 25 24 - - - - - -

Shoes Industry - - - - - - - - - - - -

Building Materials 3.43 2.96 399 366 47 40 - - - - - -

Construction - - - - - - - - - - - -

Electronics - - - - - - - - - - - -

Chemistry 0.92 1.47 0.0004 0.0004 3.2E-05 3.1E-05 0.0006 0.0006 0 0 0.002 0.002

Transportation and

Distribution 10.53 13.70 0.0049 0.0052 4.2E-04 7.4E-04 0.17 0.21 0.56 0.82 0.06 0.08

Automobile Industry - - - - - - - - - - - -

Financial Services 0.0003 0.010 8.8E-09 2.1E-07 1.8E-08 3.9E-07 1.4E-06 2.3E-05 0 0 1.1E-07 1.9E-06

Environment 0.0330 0.002 7.3E-07 4.5E-08 3.2E-07 9.8E-08 8.2E-05 2.7E-05 0 0 2.6E-06 2.2E-06

Telecommunications 0.0250 0.043 5.3E-07 9.3E-07 1.1E-06 1.8E-06 0.0003 2.7E-04 0 0 2.1E-05 2.3E-05 * Non methane volatile organic compounds showing that our economic growth is increasing the pollution effect except for the building materials sector, probably due to additional filtering in the cement industry and fuel substitution.

17

Another important perspective concerns the relationship between the direct consumption of materials (Direct Materials Input) and GDP. Unfortunately, DMI is increasing quite significantly as it is shown in next figure.

DMI, Direct Material Input per capita (1988-1995)

Fig. 2.6 2.3 ECONOMIC DEVELOPMENT AND INNOVATION Innovation is a main source of value generation in modern business and two major types have been defined: product innovation and process innovation. Both have a key importance for Portugal: - Product innovation is required to design and to launch new products. Actually, a main problem of

portuguese firms is the lack of “final products” either in Industry or in Services - Process innovation is essential to improve efficiency and as it was pointed out portuguese productivity is a

long way behind OECD average. - A third type of innovation may be proposed: channel innovation concerning the adopted systems to reach

the consumers markets. The new revolution of E-Business allows a new range of channels globalizing markets and firms.

However, innovation requires build up effective networks of partners and such behaviour implies a good deal of trust between multiple actors. Such level is quite low in countries like Portugal as it is shown in Figure where it is presented the percentage of positive answers to the question “can we trust other people?” (World Values Survey)

18

Fig. 2.7 Social Trust

0 10 20 30 40 50 60 70

Turkey

Mexico

Portugal

France

Italy

Germany

Belgium

Austria

Spain

Korea

Ireland

Japan

Iceland

Switzerland

UK

US

Netherlands

Australia

Canada

Denmark

Sweden

Finland

Norway

A Measure of Trust

Also, the contribution given by foreign corporations active in Portugal is rather limited to the objective of innovation and research:

Table 2.3 RD of American corporations in European countries

Country RD/employee (103 US dol/empl.)

Royalties and licences / RD expenses

Ireland 3,8 3% Germany 3,5 1% Spain 0,6 5% France 1,5 4% U. K. 2,3 0,5% Portugal 0,1 33% Greece 0,1 6%

The studies on innovation carried but by ET2000 allow the following conclusions: • Major limitations are due to the so called “intensity effect” correlated with low educational levels, low RD

and low synergies between institutions (universities, firms, etc.) • The so-called “structural effect” due to an economic structure including traditional sectors is important,

too. Despite the increasing importance of Services, traditional manufacturing industries like textiles, shoes and some food industries are quite important. Shoes have started more innovative processes than the others and results are promising.

• There is an obvious need to integrate policies for Science, Technology and Innovation, requiring more effective links between universities, other public institutions and corporations.

• The potential offered by digital technologies has a vital importance despite debatable results about its impact on productivity. The delays on liberalization of communications and on disseminating E-Business are not favourable to explore these new opportunities.

• portuguese labour legal framework is comparatively more rigid that the regulation existing in most OECD countries, even in southern Europe, and this is not a positive contribution to innovation as it implies and it

19

generates changes. After all, the words of Schumpeter can be quoted: “Innovation is a process of creative destruction”.

• Finally, an analysis of innovation would remain incomplete without looking at its major contributor: the entrepreneur.

However, the process of decision making of the entrepreneur or manager to overcome problems and difficulties tends to look for innovation just after several other attempts as it is presented in the following “staircase” of decision stages:

Fig. 2.8

The “staircase” of the portuguese manager

Innovation?

Cost reduction

Market “protection” to increase revenues

Demand for State subsidies

2.4 DEVELOPMENT, INTERNATIONALIZATION AND TECHNOLOGICAL MARKETING The process of progressive international openness of portuguese economy has been crucial to the increase of our national income despite obvious problems for the less competitive economic sectors (namely, primary sector). New digital and communication technologies are globalizing markets allowing not just the distribution and sales of products, far way from their production sites, but also a similar trend for personal and commercial services. The small size of our economy has been partially overcome through processes of merging and concentration ignoring alternative strategies based on cooperation, partnership and networking. Internationalization tends to be inevitable for small economies as it is the case of Portugal and benchmarking for competitiveness is urgent within a globalized market framework. Globalized markets imply intensive use of technology and, particularly, of technologic marketing tools. The concept of technologic marketing applies either to the sales of technologic products such as computers or mobile phones or to the use of technology to market any product or service (ATM, Internet, etc.). Assuming that portuguese economy is focusing on services, technological marketing becomes crucially important. However, data about computers (just 11% of families have a PC against an average of 18% in EU) and, even more, about E-Business show a clear delay. Fortunately, the reduced use of computers at home is compensated by an wider access at workplaces or universities.

Table 2.4 Access to computers and internet

% of individuals (≥ 15 years)

1997 (Sept. – Dec.) 1999 (Apr. – Jun) - having access to a computer 47.8% 51.4% - having access to internet 13.0% 21.6% (4.3%)* (9%)* *in Spain

The comparison of internet use with Spain is favourable to Portugal and the place selected for that use is quite different: in Portugal, 20% of users do it from home and 40% from work or from study places but in Spain 40% of users do it from home, 40% form the work place and 20% from study place.

Decisional Options

20

In Portugal, e-shopping is still rather small (about 106 contos around 1999) and more peripheral regions like Azores and Madeira lead this business. B2B is in an infant stage but several leading economic groups are now heavily investing on this new area (Trade.com, Forum B to B, etc.). The activity to interconnect these market places with portuguese firms, namely SMEs will be a key condition for success. Of course, all this new age of technology in E-Business is an excellent opportunity for Engineering and Technology in Portugal . Several priority areas include computer and communication systems, management information systems (namely to interconnect SMEs with marketplaces), datamining and CRS (customer relationship systems), website engineering, decision systems, etc. A less developed know-how on Engineering and Technology for these new areas will condemn Portugal to be an economy oriented for low added value services, loosing competitiveness in international markets. 2.5 DEVELOPMENT AND HUMAN CAPITAL The educational qualification of portuguese population (25 à 64 years old) has a much lower level than most OECD countries as it is shown in next Figure: just around 20% have completed upper secondary education or higher, against about 30%, 50%, 60% or 65% for Spain, Ireland, Netherlands and Finland, respectively. The evolution of the population having completed upper secondary education (level ≥ 3 according to ISCED and in Portugal ≥ 12th grade) can be simulated for the horizon of 2020 in terms of the educational achievement for age group:

1577 1397 1238 908 Population (103 inhab)

Year 2000: % level ≥ 3 → 18%

30 %

20%

10%

5%

% ≥ level 3

25

35

45

55

65

Age group (years)

1497 (present age group 15-25)

Year 2010: % level ≥ 3→ 30%

55%

30%

20%

10%

1198 (present age group 5-14) Year 2020: 39% % level ≥3 → 48%

X

55%

30%

20%

X

Fig. 2.9

Simulation of the evolution of portuguese population with level ≥ 3 This model shows that Portugal will not exceed 40% if there is no significant jump in the achievements from present rate

60%* Nowadays X is around 50% 100%

21

2.5.1 Higher Education a) Trends The improvement of Higher Education in quantitative and qualitative terms is essential to develop Engineering and Technology. In Portugal, the percentage of the active population with higher education is around 10% (1996) against an average of 23% in OECD (OECD, 1998) and levels of 18%m 23%, 21% and 23% for Spain, Ireland, Finland and Netherlands, respectively. During the last decade the inflow of Portugal students to Higher Education had an huge increase reaching a population of around 351 000 students on 1996/7 but since then the inflow has been decreasing due to the decrease of birth rate (since 1978) and also due to the stagnation (or even reduction) of participation rates above 21 years old:

Table 2.5 Participation Rate (ME, 1999)

Age Year 96/97 97/98 16 83% 85% 19 63% 66% 21 35% 33% 23 26% 23% 25 15% 14%

Therefore, the forecast of 229000 students for 2005/6 can be even an overestimation of the population of students in Higher Education.

b) Comparative analysis The graduation rate (number of students completing higher education in terms of their population group) for Portugal has increased but is lower than in other reference countries (OECD, 1998):

Table 2.6

Country Graduation rate (%) - 1996 -

Portugal 16% Spain 27% Ireland 26% Netherlands 20% Finland 24%

showing that we still have a deficit between 5 and 10%. The percentage of portuguese students completing long programs (“licenciatura”, 4-5 years) has increased as the percentage of those completing a B. Sc has fallen down from 40% to 26% between 1992 and 1996. This is quite negative for Engineering and Technology as the increasing scarcity of technologists qualified with an intermediate level is a very serious shortcoming to the competitiveness of our Economy. The distribution of graduates per subject can be compared also with other countries

22

Table 2.7 % candidates % graduates Portugal

98 Portugal

96 Ireland

96 Netherlands

96 Finland

96 Sciences, Mathematics, Computers, Engineering and Architecture

23% 21% 30% 25% 38%

Law, Social Sciences, Education, Humanities, Economics, Management and Arts

56%

72%

65%

62%

50%

Health 19% 7% 5% 13% 12% The case of Ireland is a very interesting example as there has been during last decade a strong commitment to increase the education in Science and Technology, jumping the previous rate of candidates to more than 50%. (information received from the F. Kauppinen, European Foundation for the Improvement of Living and Working Conditions, Dublin, 2001, March). This Table shows the obvious strong deficit of Health and a small one in Sciences and Technology if compared to Finland and Ireland (Recently, Ireland has increased significantly the 30% share). Unfortunately, present trends are not very favourable: - the renewal of active population is around 2% per year and the number of annual graduates is around 20000.

Therefore, even if the rate of graduation for present cohort reaches 60%, this means that the percentage of active population with this level will be around 18% on still below present average for OECD.

- Increasing that graduation rate would imply a significant reduction of present drop out which is quite high (≈40% - 50%) but this rate seems rather stable.

- The percentage of students choosing Science or Technology in Secondary Education is decreasing: 63% à 52% from 1990 to 1997.

Summing up, it seems that: - Higher Education has a rather low level of efficiency due to high dropping-out and retention levels. This

means that Portugal will not reach the average level of qualification of OECD – 1996 on the target year of 2020, unless radical changes will be pursued.

- There is a growing scarcity of graduates in Engineering and Technology, particularly for the intermediate level (B Sc or certificate level)

- This scarcity will spread over most Engineering and Technology areas but it is already quite high for domains like Computers, Systems, Communication, Multimedia, Environmental, Services, Infra-structures (Civil Engineering)

2.5.2 Research and Development (RD) RD effort of the portuguese State has increased significantly during last years:

Table 2.8 Public RD as % of GDP

1988 1997 Portugal 0.29% 0.54% Spain 0.42% 0.50% Finland 0.75% 1.16% Netherlands 0.94% 0.76% Ireland 0.36% 0.32%

becoming higher than in other countries like Ireland or Spain.

23

However, private RD is still very low (about 22% of total) compared to the others: 69% (Ireland), 47% (Spain) and average EU 64%.

Obviously, the total RD effort (as % of GDP), q, is given by f1

pq

−= where p is the public RD (also as % of

GDP) and f the fraction due to private RD. Thus, one has q = 2.8 p for average EU but for Portugal just q = 1.25p, obtaining q ≈ 0.7%, quite below the target of 1% often praised by politicians. The distribution of RD per subject areas was studied by Contzen (Contzen, 2000):

Table 2.9 Distribution of RD per subject areas

Agro-Sciences Humanities Technologies Others Portugal 13% 20% 14% 53% E.U 4% 13% 20% 63% Ireland 21% 14% 39% 36%

showing that technologies deserve in Portugal much less attention. The number of scholarships to support PhD students had a very positive growth but those for MSc have been reduced (OCT, 1999)

Table 2.10 Distribution of scholarships

Scholarships 1994 1998 PhD 520 677 MSc 776 186

The distribution of PhDs per subjects has been lead by students’ choice (Bonfim, 2000):

Table 2.11

Distribution of scholarships per domain Subject %

Electrical and Computer Engineering 27 Chemistry 25 Civil Engineering 15 Chemical Engineering and Biotechnology 13 Mechanical Engineering 13 Materials 7

and the area of Information and Communication Technologies is quite below reasonable levels. Unfortunately, around 95% of PhDs stay at the university system and the example of Chemical Engineering can be quoted: between 70 and 97, 290 PhDs were produced but just about 20 or 25 PhDs were found in industry. Other indicators can be used but the following conclusions seem quite obvious: - the strong public effort during last decade has developed a basic public RD infrastructure, although more

oriented for Sciences than for Technologies. - Most of public RD effort has been allocated in terms of demand without considering specific policy

priorities; - Most of the existing public RD system is based on traditional classification of subjects and it is not oriented

to support the new RD paradigm: the so-called “Mode 2 research” (Gibbons et al, 1994).

24

- New challenges will require substantial changes, namely:

- Higher Education cannot go on absorbing more than 90% of new PhDs; - The EU contribution to our RD effort is quite substantial but it will be much smaller after 2006; - Setting up priorities and major options for our Science and Technology policy should be not delayed; - RD effort in Defence should be increased developing synergies with other civilian areas making a better

use of compensation policies for important procurement decisions; - The urgent development of private RD requires not just priorities but a new “problem oriented” approach

supporting networks and innovative programs. EU is also moving in this direction through the “Key Actions” approach and the new ERA (European Research Area).

2.6 PORTUGAL BENCHMARKING This diagnostic analysis would be incomplete if Portugal (PT) is not compared with other reference countries. The usual approach of comparing Portugal with EU average seems less attractive as this is a sliding reference. Thus, four other European countries were selected: - Spain (SP): the most important neighbour experiencing significant development - Ireland (IR): a peripheral european country belonging to the first priority within the Community Support

framework and achieving substantial economic success. - Finland (FL): a very peripheral country having succeeded to overcome economic troubles after the end of

Soviet Union. - Netherlands (NL): small country with a very aggressive economy giving a high priority to human capital

and technology. The following benchmarking was estimated for the end of nineties:

Fig. 2.10 Expected life and birth rate

Population and Health

7071727374757677787980

9 10 11 12 13 14

(nº births/103 hab.)

(yea

rs)

PT

NL

FLIR

SP

25

Fig. 2.11

Tuberculosis and HIV

Population and Health

0

10

20

30

40

50

60

0 20 40 60 80 100 120Nº HIV new infected cases/ year

Tube

rcul

osis

(n.º

of c

ases

/ 10

5 inha

b.)

PT

FL

IRNL

SP

Fig. 2.12 GDP growth and employment

Economy

-2

-1

0

1

2

3

4

0 2 4 6 8

Average annual growth rate of GDP (88-98)

Ave

rage

ann

ual g

row

th r

ate

of

empl

oym

ent (

88 -

98)

PT

NL

FL

IR

SP

Fig. 2.13

Economy

0

10

20

30

40

50

60

70

80

0 10 20 30 40 50Competitiveness indicatir (according to IMD 2000,

considering 47 countries starting with the worst one)

GD

P/in

hab.

as

% o

f US

leve

l

PT

NL

FLIR

SP

26

Fig. 2.14 Participation Rate and Educational Achievement

Knowledge

0

5

10

15

20

25

30

35

0 20 40 60 80% of population (15-64 years) with level >=3 (1996)

Part

icip

atio

n R

ate

(Hig

her E

d.) f

or

18-2

1 ye

ars

(199

6)

PT

PB

FL

IR

ES

Fig. 2.15

Study of English and Mathematics

Knowledge

440450460470480490500510520530540550

0 20 40 60 80 100 120% of students studying english in Basic/Secondary Education

Scor

e ac

hiev

ed in

Inte

rnat

iona

l M

athe

mat

ics

Test

(TIM

S, 1

3 ye

ars,

19

95)

PT

NL

FL

IR

SP

*

* In this case, the foreign language is French

Fig. 2.16 RD Structure

Knowledge

0

10

20

30

40

50

60

70

80

0 0,5 1 1,5 2 2,5 3 3,5RD as % of GDP

Priv

ate

% o

f RD

PT

PBFL

IRES

27

Fig. 2.17 Patents and Publications

Knowledge

0

20

40

60

80

100

120

140

0 10 20 30 40 50 60

Annual nº of patent request / 105 hab.

N.º

of s

cien

tific

pub

licat

ions

/ 10

5 hab

.PT

NLFL

IRSP

Fig. 2.18

Computers and E-Business

Knowledge

0

0,2

0,4

0,6

0,8

1

1,2

1,4

1,6

1,8

0 2 4 6 8

Expenditure in Information and Communication Technologies (as % of GDP)

Nº o

f ser

vers

with

sec

urity

pro

tect

ion

for E

-B

usin

ess/

105 h

ab.

PT

NL

FLIR

SP

Fig. 2.19

Internet and Mobile Phones

Knowledge

0

20

40

60

80

100

120

0 10 20 30 40 50 60N.º mobile phones / 100 inhab.

Nº o

f int

erne

t ser

vice

s / 1

000

inha

.

PT

NL

FL

IRSP

28

Fig. 2.20 Investment on Technology and Infra-Structures (according to Schwab et al, 1999)

Knowledge

0102030405060708090

100

0 10 20 30 40 50 60

Infra-Structure

Tecn

olog

yPT

NL

FLIR

SP

Fig. 2.21 COx and NOx

Environment

0

20

40

60

80

100

120

140

0 10 20 30 40 50 60

Nox (kg/inhab.)

Co x

kg/

inha

b.

PT

PB

FLIR

ES

Fig. 2.22 Regional Development

0

10

20

30

40

50

60

70

80

90

100

0 0,2 0,4 0,6 0,8 1

Nº of Regions (A+B)* / Total of Regions

% P

opul

atio

n in

Reg

ions

(A+B

)

PT

NLFL

IRSP

* according to the classification by the European Commission, 1998.

29

All these analysis and the study of recent trends of these indicators can be synthetized by the following graph displaying the areas where Portugal has achieved stronger advances but also those with an weaker position:

Expected life Communications Income per capita Participation Rate and public RD Qualification of Active Population Productivity Pollution impact of economic activity

Educational achievements Competitiveness and technological effort (Private RD and exports of High-Tec industries)

Economic use of new technologies (E-Business, etc)

Higher Advance

Weaker situation

Improvement

Stagnation

30

3. Which Future Scenarios?

“Men to to-day, to-morrow’s dust when years have past where shall ye go? What vulgar daub or hurried lust Shall chronicle your joy and woe? Wave on the crest of life’s swift sea After to-day who’ll think of ye?” Fernando Pessoa, 1904

31

3 WHICH FUTURE SCENARIOS? 3.1 EUROPE The fast development of Portugal during last decades is strongly linked to the process of integration in the European Union and therefore debating future scenarios for Portugal leads us inevitably to discuss the future of Europe. And Europe is in a process of fast change, too. During last decade, the treaties of Maastricht and of Amsterdam have consolidated our common european institutions and it seems that the depth achieved along multiple societal dimension can be represented as follows:

Fig. 3.1 The domain of Research and Technological Development (RDI) has become a competence of the Union by the Single Act (1987) and acquired higher importance by the Maastrich Treaty (1993). The challenges faced by Europe and announced by J.J. Schreiber through his famous “Le Défit American” thirty years ago are more real than ever. Therefore, a main question is what are the major dimensions of change for the European Union during coming decades? ET 2000 formulates these dimensions into 9 perspectives. A – Demography and Environment European population is becoming older and by 2025 the age group ≥ 65 years will include 85 Million inhabitants, about 22% of the population against 15.4% (in 1995). The demographic evolution for Portugal is similar with 20% in 2016 against 14% in 1991. These forecasts can be significantly changed by specific immigration policies, probably associated to overcoming shortage of professional profiles. This is well illustrated by the recent announcement by the chancellor of Germany to start a massive import of computers’ technologists. European environment has been under growing pressure during the last decades and this trend cannot be kept. The increase of pollution emissions (NOx, SO2, NH4 and volatile organic products), the need to take care of adequate and of waste treatment systems, the decontamination of soils, the reduction of greenhouse factors

Social Dimension (Social support, Labour mobility, Social exclusion)

Knowledge and Environment Dimensions (Education,

Training, RD, Environment) Political Dimension (Foreign policy, Defence, Citizenship)

Development Dimension (Sectoral and Regional Disparities, CSF)

Commercial Dimension (Internal Market)

32

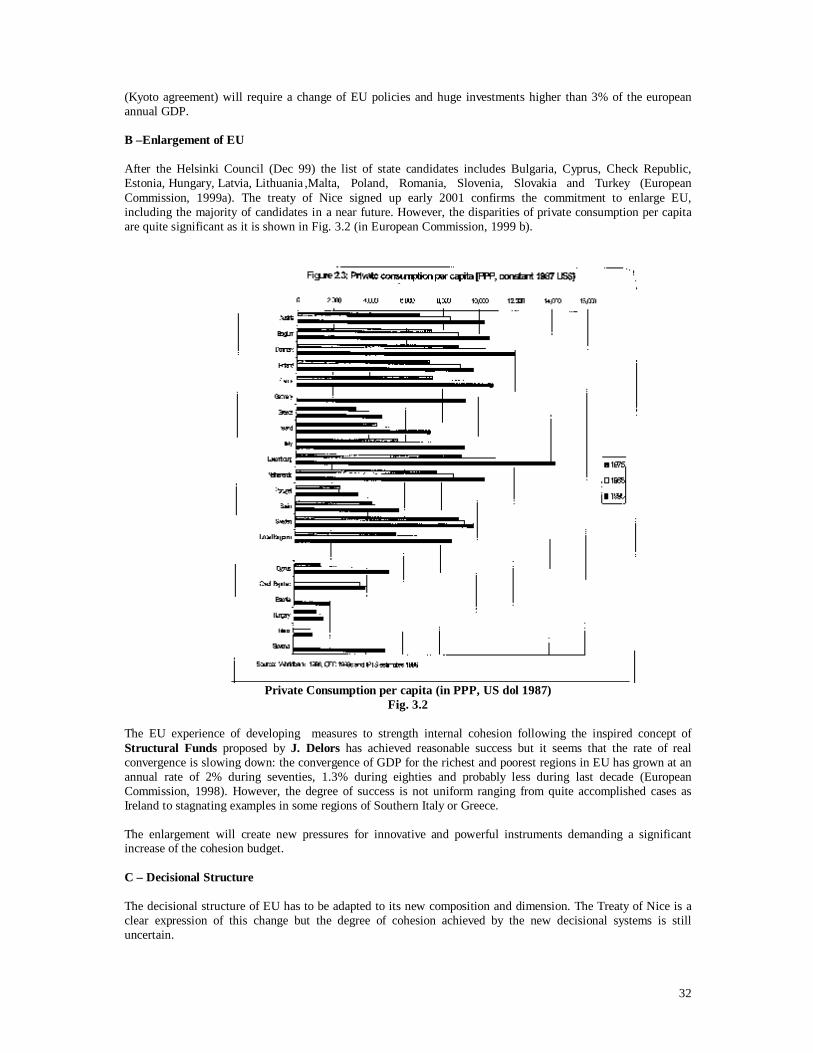

(Kyoto agreement) will require a change of EU policies and huge investments higher than 3% of the european annual GDP. B –Enlargement of EU After the Helsinki Council (Dec 99) the list of state candidates includes Bulgaria, Cyprus, Check Republic, Estonia, Hungary, Latvia, Lithuania ,Malta, Poland, Romania, Slovenia, Slovakia and Turkey (European Commission, 1999a). The treaty of Nice signed up early 2001 confirms the commitment to enlarge EU, including the majority of candidates in a near future. However, the disparities of private consumption per capita are quite significant as it is shown in Fig. 3.2 (in European Commission, 1999 b).

Private Consumption per capita (in PPP, US dol 1987)

Fig. 3.2 The EU experience of developing measures to strength internal cohesion following the inspired concept of Structural Funds proposed by J. Delors has achieved reasonable success but it seems that the rate of real convergence is slowing down: the convergence of GDP for the richest and poorest regions in EU has grown at an annual rate of 2% during seventies, 1.3% during eighties and probably less during last decade (European Commission, 1998). However, the degree of success is not uniform ranging from quite accomplished cases as Ireland to stagnating examples in some regions of Southern Italy or Greece. The enlargement will create new pressures for innovative and powerful instruments demanding a significant increase of the cohesion budget. C – Decisional Structure The decisional structure of EU has to be adapted to its new composition and dimension. The Treaty of Nice is a clear expression of this change but the degree of cohesion achieved by the new decisional systems is still uncertain.

33

D – Global Competitiveness The growing liberalization of the world trade, namely after the Seattle Conference of WTO, last year, will require new policies in Europe which will be difficult to implement with a large fraction of the national income allocated to the State (in Portugal, this percentage is already around 50%). Within EU, the acceptance of new members (outside Euro region) will attract for these new regions low-salary industries and more traditional activities. Therefore, countries at an intermediate level of development as it is the case of Portugal have to speed up their commitment to focus on more advanced services and industries E – Internal Tensions and Conflicts Previsions analysis suggest a more vast and heterogeneous Europe (Europe – Mosaic) close to the sustainability limits and with multiple local tension nodes. The ability to cope with these new problems will be a crucial factor for the success of EU. Major scenarios for EU can be drawn up in terms of two basic lines: a) Cohesion or Fragmentation b) Competition or Social Protection The resulting 4 cases are presented in Fig. 3.3

III

I

IV

II

Fig. 3.3

These four scenarios will shape our future and also the role of Engineering and Technology (ET) to improve sustainable development. Demand for ET will be higher with cohesion and the clients will be more connected to public authorities (“public markets”) or to wider and private markets if the trends emphasize more competition or more social protection, respectively. 3.2 TECHNOLOGICAL FUTURE Several institutions are looking for the scientific and technologic areas of knowledge that seem more promising in coming years. The Institute Battelle (USA) has selected seven key topics: BQG – New engineering solutions based on Biochemistry and Genetics to develop new tools for Health, Food and Environment (genetic treatments and functional food) NMAT – New material, with innovative properties (joint elements, memory, ultra-light materials, concrete with carbon fibbers, etc) ENP – New powerful and small sources of power (new generation of batteries)

Competitiveness

Fragmentation Cohesion

Cohesion

Social Protection

Competition

34

INF – New information and communication systems distributing computational power by common commodities and networks (home systems, transportation controls, E-urban areas, etc.) TRA – New cableless transmission systems (infra-red for industries, etc) and superconductors working at room temperature ERT – New integrated systems for environmental control and natural resources management (Sewage treatment systems, water purification, industrial ecology, etc.) NAN - Nanomachines (molecular tools) The duration of the innovation cycles associated to these new achievements will condition strongly the technological “landscape” of the next two decades. 3.3 THE PORTUGUESE SOCIETY The process of change of the portuguese society is particularly important for the development of Engineering and Technology (E&T) and 4 major perspectives were considered in terms of key societal paradigms: + Paradigm of Civil Society + Paradigm of Change + Paradigm of International Openness + Paradigm of Sustainability Each perspective has a pole favouring E&T contribution to society and an anti-pole as it is represented in next figure:

Four Major Societal Perspectives Fig. 3.4

The first direction is essential to develop innovation and dynamic business networks requiring more E&T knowledge but the second one is no less important as the future challenges require flexible and fast processes of adaptation and evolution. Portugal is a small country and international links are a source of opportunities and also a way of avoiding national limitations. The last issue concerns sustainability and all work done at ET 2000 has emphasized clearly the importance of integrating this paradigm in modern E&T in order that this key objective will be tackled by E&T and also because of the new markets to be supplied.

Favourable Directions to integrate E&T in Portuguese Society

Civil Society Initiative

State Dominance

Prone to Change

Against Change

International Openness

International Closeness

Sustainability

Volatility

35

Two alternative evolutions have been drawn and of course I will be much more favorable than II (Fig. 3.5).

Scenarios for Portugal Fig. 3.5

Scenario I requires a strong effort to transfer to civil society a good deal of power and resources managed by the State (First Paradigm) and this radical burst will have strong impacts on other dimensions. The author has no doubts on the vital importance about these societal scenarios to shape the future of our country and the use of E&T to boost competitiveness and development. 3.4 STUDIED SECTORS

3.4.1 Building Materials This sector includes a very diversified spectrum of industries belonging to different groups: Ceramics, (including stones, glasses, cement, concrete), Polymers (wood, cork, plastics, bitumen, paints and varnishes, glues), Metals (steel, cast iron, aluminium, ironwork, taps) and other materials (precasted cement products, etc). This sector is responding to the growth of housing and infra-structures construction but its technological level is quite heterogeneous: • Skills and qualification Sub-sectors such as those of stones or traditional ceramics have much lower levels than others like those of dyes and glues. • International Openness and Competitiveness Several products are heavily exported like stones and cork but imports are growing in other sub-sectors, such as furniture or even ceramics, showing a lower competitiveness of our industry compared to other countries like France, Italy or even Spain. This sector is also quite fragmented including many “worlds” with different culture and associations based on affinities of raw materials and production processes but less oriented to promote synergies to develop integrated final products and marketing strategies.

Civil Society Initiative

State Dominance

Prone to Change

Against Change

International Openness

International Closeness

Sustainability

Volatility

Scenario I

Scenario II

Existing situation Scenario

36

The foresight analysis recommends the following strategies: - priority to increase competitiveness within EU - development of product innovation integrating contributions from sub-sectors: from a “materials” culture

towards a “building solution” approach - improvement of design and quality standards. This requires intensive training and new qualification

structures and centres - reorientation of professional and business associations to stimulate new product and marketing cultures.

3.4.2 Construction This is a major sector of portuguese economy accounting for about 7% of our GNP and a high multiplier effects as it is estimated than each unit of revenue of this sector generates another 0.75 of revenues in other sectors. Unfortunately, the level of qualification of most workforces is rather low and its actual size is undetermined as it includes a significant number of illegal immigrants. The following strategies can be recommended from the developed analysis: - increasing the market segmentation for products and services; - complementing major products with related services; - achieving a significant increase of quality should be assessed by the final client rather than by the producers

themselves; - hence, clients’ surveys and quality panels should be generalized, which is also a requirement of the new

standards for quality control; - developing an integrated strategy to improve qualification and productivity not just in terms of technological

solutions but also using other contributions from Psychology and Industrial Sociology; - supporting joint international developments associated to portuguese investment abroad (Environment,

Telecommunications, etc); - promoting new markets like rehabilitation of housing and of structures; - stimulating product and process innovation; - contributing to the identity and dynamics of real estate sector;

3.4.3 Environment This sector includes an wide variety is sub-systems such as water, soil, ecosystems, waste, urban environment and noise. These sub-sectors require a long list of skills and problem areas to be studied such as coastal or estuarine protection, water supply and treatment, water or waste recycling, air quality control, emission reduction, biodiversity and natural areas conservation, urban planning, green areas and urban equipment, noise monitoring and control. Several strategies were proposed: - priority to the training of middle level technologists and specialized experts; - development of management information systems to monitor environmental systems - promotion of innovation, stimulating new clusters of SMEs developing synergies with other technologies

such as ICT, GIS, etc. - partnerships between the State and private sector to coordinate the regional development of better solutions

without disturbing the development of nature markets - strong investment in specific “niches” to achieve international competitiveness and to develop synergies

with portuguese investment in foreign countries

3.4.4 Energy Portugal has a low final energy consumption per inhabitant (≈ 2 toes, tones of oil equivalent, 1996) against an European average of 3.8. Our country has no oil or gas but hydroelectricity is a valuable resources and other sources like wind can have a significant development in the future. Natural gas and mini-hydropower stations are improving our national balance.

37

Three major strategic objectives should be considered: I – Reduction of foreign dependency, increasing security and reliability II – Increasing sectoral competitiveness III – Improving environmental standards and fulfilling Kyoto objectives. Several areas of development have to be pursued to achieve these objectives:

a) management of resources, I, III b) rational use of energy, I, II, III c) efficiency of the energy systems, I d) competition and regulation, II e) pollution emission, III

The following guidelines can be suggested: - Promotion of a culture of competition and regulation - Development of technological education and training for the most relevant areas - Promotion of a culture of energy conservation, namely for designers and managers - Monitoring prices and differentiating those technologies avoiding externalities related to pollution effects

(water, wind, etc). - Promoting of RD oriented to increase the efficiency of energy use - Promotion of co-generation and other clean technologies - Supporting the use of natural gas in specific industries - Supporting SMEs for better energy options - Promotion of better energy options for large national projects

3.4.5 Food and Beverages This sector accounts for about 3% of the total value of national industrial output and it is quite important not just because this sector fulfils essential needs but also because it is rather stable across highs and lows of economic cycles. The following groups of products have to be considered: - groceries - dairy products - frozen food - canned - hot beverages - biscuits and sweets - “charcuteries” Four major strategies are proposed:

a) focusing products with a higher growth rate such as functional products and pre-prepared food b) promotion of products innovation as a key condition for success through partnerships between

universities and corporations c) developing horizontal and vertical integration of firms within the main processes of internationalisation d) improvement of supply chains and other logistic conditions developing partnerships with agricultural

production

3.4.6 Electronics The production of this sector corresponds to about 3.5% of GDP on 1998, employing 1% of the active population. Major sub-sectors include machinery and industrial equipment, wires and cables, measuring equipment, automation and control, telecommunication computers, electronic components, batteries, lamps and other equipment, consumer electronics.

38

Most of the recent portuguese development was based on cables, electronic components and consumer electronics using low qualified labour and suffering the challenge of other regions with lower salaries. Several strategies should be pursued: - transfer of technological know-how to improve our knowledge bases; - increase of applied RD; - searching for new market “niches” with promising trends in international markets; - acquisitions or mergers increasing competitiveness; - modernization of production processes; - clustering of technological SMEs; - Stimulation of innovation.

3.4.7 Metal and Plastic Production This is a main component of portuguese industry accounting for ¼ of its firms and generating 15% of its GAV (about 18% of total industrial employment). This sector includes basic metallurgy, metal products, machinery and non-electric equipment, transportation equipment. Unfortunately, the qualification level is low and competitiveness is limited. The following strategies are suggested: - Focusing four critical issues: environment, quality, security and maintenance - Globalization and “crashing” supply chains - Improving intangible factors for competitiveness such as innovation design, flexibility and post-sale services - Priority to the training of technologist in the areas of measurement, digital operation and control.

3.4.8 Automobile Industry This industry has grown recently through the development of the new VW factory, Auto Europa, and has increased the total sales from 85 x 109 to 736 x 109 PTEs (1986 à 1998). This last development had a very strong and positive impact on a large “palette” of industries due to a very well structured process of procurement. The evaluation of sales is presented in the following graph.

Fig. 3.6

Facturação por Grupos de Actividade (milhões de contos)

0

50

100

150

200

250

1992 1993 1994 1995 1996 1997 1998

Interiors

Engines

Electric Components

Structure

Buses

Pneumatics

Others (moulds, tools, etc.)

39

Major recommendations are: 1. Development of new assembly lines. Attracting another OEM (“Original Equipment Manufacturer”) can

have a very positive effect 2. Capturing “systems integration” to have new development centres in Portugal (such as Delphi) 3. Promotion of a culture of “product engineering” increasing RD and innovation 4. Development of partnerships to achieve vertical integration and scale economies 5. Internationalization of human resources

3.4.9 Textiles and Clothes The sales per employee have been growing (fig. 3.5) but they are below the European average (42% or 30% for textiles and clothes, respectively).

0

1

2

3

4

5

6

7

8

9

1994 1995 1996 1997

10 P

TE