society of industrial and office realtors® 1 sior new mexico chapter industrial & office update

TRANSCRIPT

Society of Industrial and Office REALTORS®

Society of Industrial and Office REALTORS®1

SIOR New Mexico ChapterIndustrial & Office Update

Society of Industrial and Office REALTORS®

SIOR Market Update

SIOR is the leading industrial and office real estate brokerage association.

SIOR confers the SIOR designation to only the most knowledgeable, experienced, ethical, and successful commercial real estate brokerage specialists.

Society of Industrial and Office REALTORS®

SIOR NM Chapter Members

Society of Industrial and Office REALTORS®

THANK YOU SPONSORS!

Society of Industrial and Office REALTORS®

AGENDA

• Overall local Industrial and Office Statistics

• Comparison to Regional Markets

• Jim Smith – Discuss Industrial Sector

• Tom Jenkins – Discuss Office Sector

• Questions

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

Recession

Low Point - 5%Low Point - 5%

Current- 9%Current- 9%Peak - 11%Peak - 11%

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

Recession

Low Point - 11%Low Point - 11%

Peak/Current – 20%Peak/Current – 20%

WHY??

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

Society of Industrial and Office REALTORS®

LOCAL STATISTICS

• Annual Absorption & Construction for past 10 years

• In peak years, the Industrial market absorbs 750K-1 million SF per year

• In 2006, there was more product built than the next 7 years combined!

Society of Industrial and Office REALTORS®

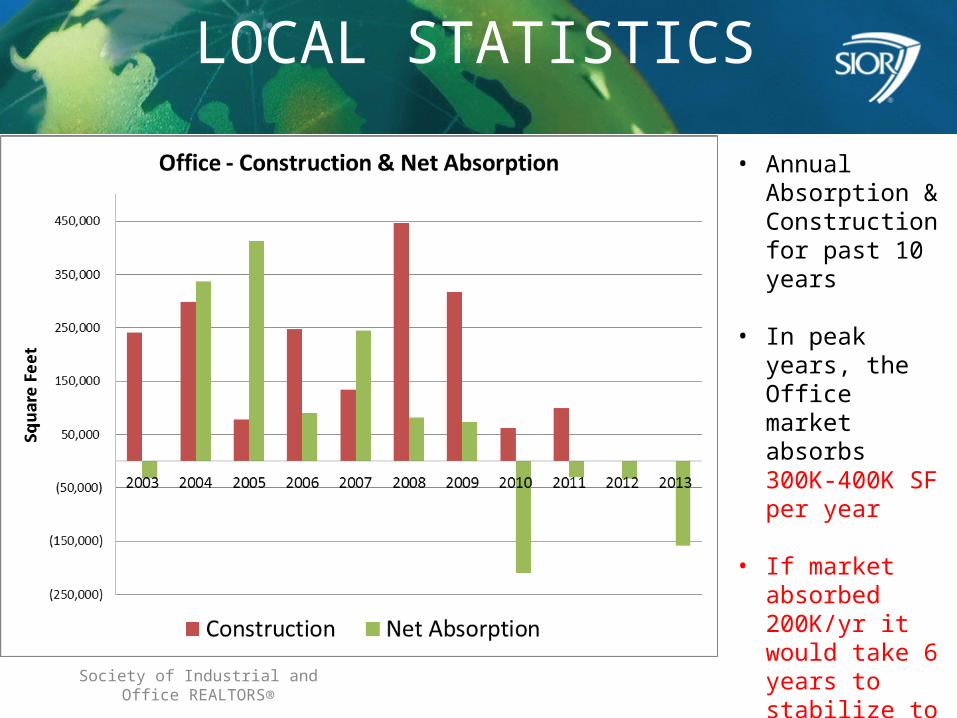

LOCAL STATISTICS

• Annual Absorption & Construction for past 10 years

• In peak years, the Office market absorbs 300K-400K SF per year

• If market absorbed 200K/yr it would take 6 years to stabilize to 12% Vacancy

Society of Industrial and Office REALTORS®

Regional Comparison(Industrial)

• ABQ’s industrial vacancy stacks up well to competing regional markets

• ABQ has less SF per capita than many competing cities.

• Denver and Salt Lake City are larger distribution hubs

Society of Industrial and Office REALTORS®

Regional Comparison(Office)

•Although ABQ’s vacancy is high, it is comparable to PHX and Las Vegas.

•PHX currently has 26 million SF of vacant space

•ABQ has let SF per capita than competing markets likely due to high govt influence.

Society of Industrial and Office REALTORS®

Society of Industrial and Office REALTORS®16

Industrial Overview

Jim Smith, SIORCBRE

Society of Industrial and Office REALTORS®

Albuquerque Industrial Market

• National versus local trends• Largest industrial transactions over the last 8

quarters• Market activity by industry and decision

drivers• Forecast

Society of Industrial and Office REALTORS®

National versus Local Trends (Tenant perspective)

National Trends Albuquerque Trends

Concessions tighten Ditto

Less available space Varies by submarket, development type and age

Multiple offers on same space Sometimes, but infrequent

e-commerce activity up Not here

Spec development returns, but limited to top 5 markets

Ha!

Port volume up – retail sales remain strong

Albuquerque has seen some consumer goods warehousing activity

Society of Industrial and Office REALTORS®

National versus Local Trends(Landlord perspective)

National Trends Albuquerque Trends

Leasing volume to prerecession levels in most major markets

Not yet

Beginning to see rent growth Maybe in some cases

Capital available for spec construction Not yet

Competition for space increasing Infrequently

Landlords closely tracking housing market

Yes

Developers contemplate additional high cube space 36’+

Not here

Society of Industrial and Office REALTORS®

Largest Industrial TransactionsQ4 2011 – Q3 2013

SF Occupier Address Date occupied

219,000 Admiral Beverage 3980 Prince St SE Q3 2013

133,000 US Foods 3700 Prince St SE Q4 2011

114,000 Fidelitone Logistics 801 Comanche Rd NE Q1 2012

109,000 Vitality Works 8500 Bluewater Rd NW Q1 2012

87,000 Friedman Recycling 5049 Edith Blvd. NE Q2 2013

45,901 Bruckner Truck Sales 8101 Daytona NW Q4 2013

41,000 SAMS Academy 4100 Aerospace Pkwy Q3 2012

40,800 Durham School 2401 Menaul Blvd NE Q1 2013

40,000 Fed Ex Ground 4525 Paseo del Norte NE Q4 2011

39,000 Air Gas 2929 Vassar Dr. NE Q4 2011

Society of Industrial and Office REALTORS®

Locations of largest industrial transactions

SOUTH I-25

2

NORTH I-25

5WEST MESA

3

Society of Industrial and Office REALTORS®

What sort of activity is driving Albuquerque industrial market?

Society of Industrial and Office REALTORS®

Market Activity

Warehousing of retail and consumer goods•Retail third party logistics providers, Pepsi

Bottling, Admiral Beverage, US Food

•What drives location decisions?– 24’+ ceiling height– ESFR (Early Suppression, Fast Response) fire sprinklers– trailer parking– Two of three user built new facilities

Society of Industrial and Office REALTORS®

16’ clear height, not sprinkled

Society of Industrial and Office REALTORS®

28’ clear height withESFR fire sprinklers

Society of Industrial and Office REALTORS®

Trailer parking

Society of Industrial and Office REALTORS®

Market Activity

Oil and gas• Transportation – pipeline

• Pipeline companies have generated construction work.

• Some engineering company activity related to oil and gas industry

• Opportunity is related new technologies (fracking) which have made extraction of resources viable.

• What drives location decision? – Storage requirement and term

Society of Industrial and Office REALTORS®

Market Activity

Cell tower construction: •Activity driven by new technologies and required hardware/infrastructure upgrade.

•Construction work of limited duration.

•What drives location decisions? – Storage requirement and term

Society of Industrial and Office REALTORS®

Forecast

• Owner user activity has been positively affected by low interest rates, but as interest rates uncertainty continues will users become less optimistic about purchasing?

• There is limited and shrinking availability of class A inventory (constructed post-2000, 24’+ clear height with ESFR fire sprinkler systems).– Cost of new class A facilities will likely see asking lease rates 20% above

current market asking rates?

• Construction activity to remain below 10-year average for the next 18 months

• Annual rent growth 3-4% - above inflation

Society of Industrial and Office REALTORS®

What might disrupt the path forward?

• Availability of adequate wet utilities in south I-25 corridor and far west side may limit options for quick development.

• Will there be downward pressure on land prices to make development affordable?

• Lack of rail service in Albuquerque.

Society of Industrial and Office REALTORS®

Society of Industrial and Office REALTORS®31

Office Market Overview

Tom Jenkins, SIORReal Estate Advisors

Society of Industrial and Office REALTORS®

Society of Industrial and Office REALTORS®

Triplicate

DocuSign

CONTRACT

Society of Industrial and Office REALTORS®HP12C Calculator

Excel Spreadsheet

Society of Industrial and Office REALTORS®

Pager

Pocket full of quarters..

Payphone

Society of Industrial and Office REALTORS®

WattsLine

Skype, Face Time, WebEx, Go-To-Meeting

Society of Industrial and Office REALTORS®

Society of Industrial and Office REALTORS®

Quality Pre-1985

• Multi-Story Atrium Lobbies• Granite Flooring and Counters in Common

Areas• Water Features• Substantial Window Lines and Views• Large Offices

Society of Industrial and Office REALTORS®

Quality Today

• Function• Efficient use of space• Infrastructure• Lower operating costs• Higher density

Society of Industrial and Office REALTORS®

300 People 500 People

Impact of Higher Density

Society of Industrial and Office REALTORS®PRIVATE OFFICES OPEN FLOOR PLAN

Society of Industrial and Office REALTORS®

Total Office Inventory14.1 Million Square Feet

Quality Office InventoryGreater Density & After 1985

3.6 Million Square Feet

Society of Industrial and Office REALTORS®

Largest Office TransactionsQ4 2011 – Q3 2013

Square Footage

Occupier Address Date of Transaction

133,090 Presbyterian (sale) 9521 San Mateo Q4 2011

84,724 Blue Cross Blue Shield 4411 The 25 Way Q3 2013

63,000 Lowes 6301 Jefferson Q4 2011

47,000 Molina Health Care 7401 Snaproll Q2 2013

37,478 State of NM HSD 1474 Rodeo Road Q2 2013

33,682 Canon 4041 Jefferson Place Q3 2013

30,898 Lowes Expansion 6401 Jefferson Q2 2012

28,726 Molina Health Care 8801 Horizon Way Q1 2013

21,856 Lovelace Healthcare 7850 Jefferson Q1 2012

18,762 Moss Adams 6565 Americas Parkway Q2 2013

Society of Industrial and Office REALTORS®

Vacancy and Rental Rate (Smoothed)

Society of Industrial and Office REALTORS®

Time on Market

Society of Industrial and Office REALTORS®

Selection of ABQ

Society of Industrial and Office REALTORS®

CANON’S SEARCH FOR “QUALITY” OFFICE BUILDINGS

7401 Snaproll

4400 Masthead

5700 W University

4411 The 25 Way

4041 Jefferson Plz

4500 Alexander Blvd

Society of Industrial and Office REALTORS®

CANONGAP

MOLINA HEALTHCARE

UNIVERSITY OF NM

AVAILABLE

BLUE CROSS BLUE SHIELD

Society of Industrial and Office REALTORS®

What Could Be?

“The new office will offer improved infrastructure to better accommodate the

needs of our employees and business,” Gap spokeswoman Avery Vaught.

Society of Industrial and Office REALTORS®

What Could Be?

Society of Industrial and Office REALTORS®

Summary of Flight to Quality

• Office users will continue to migrate to “quality” office buildings

• Vacancy rates will continue to decrease in “quality” buildings

• Rental Rate Gap will increase between “quality” office buildings and Class C buildings.

• Redevelopment and repurposing of existing buildings

• There will be new substantial office buildings breaking ground

Society of Industrial and Office REALTORS®

Society of Industrial and Office REALTORS®52

Thank You & Happy Thanksgiving!