solar markets update - amazon web services market... · thai solar slated to rejuvenate from...

TRANSCRIPT

financeasia.solarenergyevents.com

4-5 JULY 2017 | SINGAPORE

SOLAR MARKETS UPDATE

2

CONTENTSAsia PacificWhy 2016’s drop in renewables investment was good news in disguise 32017 global PV demand forecasts as high as 85GW 4Thailand and Vietnam become lead countries for OEM solar module supply 5

AustraliaLyon Group to build world’s largest solar-plus-storage project in South Australia 7Australian rooftop solar financier issues another AU$50 million climate bond 8First Solar closes financing for 48.5MW solar project in New South Wales 9Enel to acquire 137MW phase of Bungala Solar project in Australia 10

ChinaPrice of Chinese module imports to India dropped 8% in Q1 2017 11

IndiaIndia added 5.5GW solar in FY2016/17 12UK-India trade ties deepen with £240 million energy investment 13Fortum proves low solar tariffs viable in India 14India’s Greenko raises US$155 million equity from GIC and Abu Dhabi investors 15ADB approves US$175 million to Powergrid for solar park transmission 16

IndonesiaEngie partnerships to invest US$1.25 billion in Indonesian renewables, agreements in Singapore 17Indonesia’s new rural electrification regulation 18

JapanCanadian Solar secures US$35 million credit facility with Sumitomo Mitsui Finance 19Streamlined: Japan’s PV market future 20GSSG Solar to acquire 350MW portfolio of solar in Japan 21International PV players ready for Japan’s large-scale tenders 22Japan’s big PV names targeting self-consumption and rooftop market 23Japan to lower tariffs, cancel projects after paying ¥2.3tr last year for FiTs 24

PhilippinesPhilippines hits 903MW of solar PV under RE law, ground-breaking on 150MW plant 26

MalaysiaEdra plans to develop 50MW solar project in Malaysia 27Malaysia to auction 460MW of large-scale solar PV 27ENGIE enters partnership to develop solar in Malaysia 28

PakistanPakistan to adopt competitive bidding for new solar PV projects 29Canada MoU with Pakistani province for 1GW of solar 30

Sri LankaSri Lanka to tender 100MW floating solar plant, funds module R&D 31

ThailandThai solar slated to rejuvenate from mid-2017 but long dry spells expected 32

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

3

ASIA PACIFIC

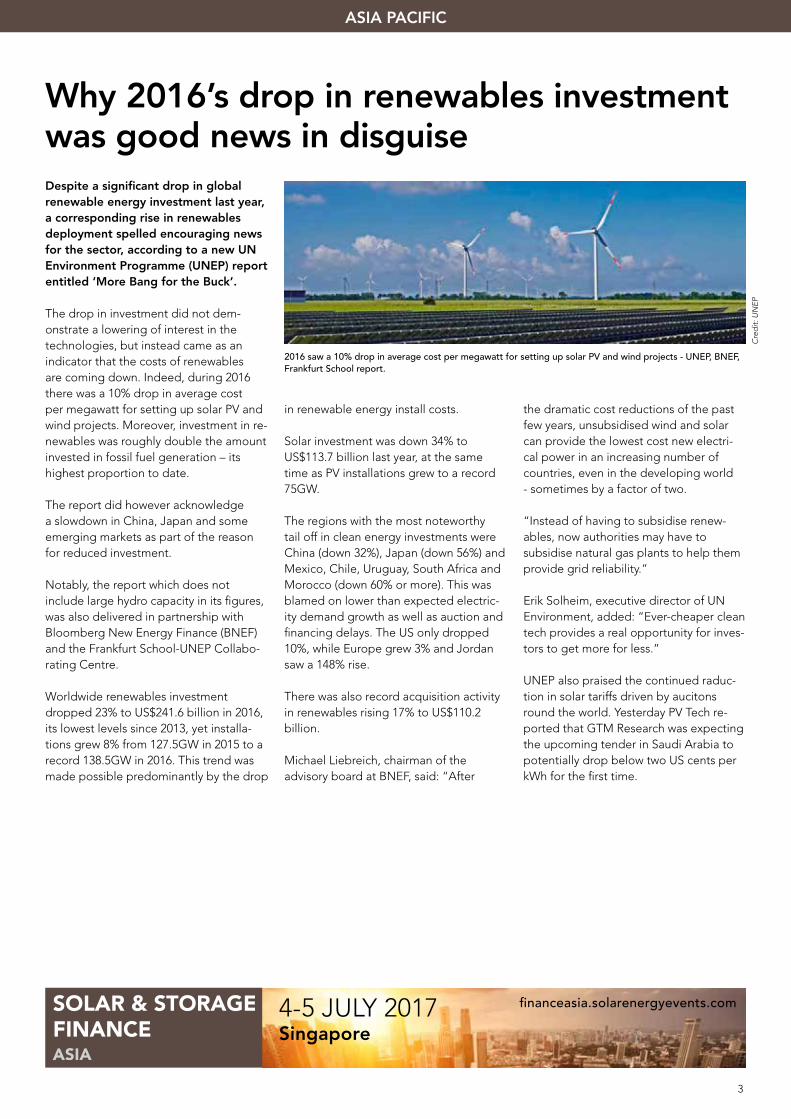

Why 2016’s drop in renewables investment was good news in disguiseDespite a significant drop in global renewable energy investment last year, a corresponding rise in renewables deployment spelled encouraging news for the sector, according to a new UN Environment Programme (UNEP) report entitled ‘More Bang for the Buck’.

The drop in investment did not dem-onstrate a lowering of interest in the technologies, but instead came as an indicator that the costs of renewables are coming down. Indeed, during 2016 there was a 10% drop in average cost per megawatt for setting up solar PV and wind projects. Moreover, investment in re-newables was roughly double the amount invested in fossil fuel generation – its highest proportion to date.

The report did however acknowledge a slowdown in China, Japan and some emerging markets as part of the reason for reduced investment.

Notably, the report which does not include large hydro capacity in its figures, was also delivered in partnership with Bloomberg New Energy Finance (BNEF) and the Frankfurt School-UNEP Collabo-rating Centre.

Worldwide renewables investment dropped 23% to US$241.6 billion in 2016, its lowest levels since 2013, yet installa-tions grew 8% from 127.5GW in 2015 to a record 138.5GW in 2016. This trend was made possible predominantly by the drop

in renewable energy install costs.

Solar investment was down 34% to US$113.7 billion last year, at the same time as PV installations grew to a record 75GW.

The regions with the most noteworthy tail off in clean energy investments were China (down 32%), Japan (down 56%) and Mexico, Chile, Uruguay, South Africa and Morocco (down 60% or more). This was blamed on lower than expected electric-ity demand growth as well as auction and financing delays. The US only dropped 10%, while Europe grew 3% and Jordan saw a 148% rise.

There was also record acquisition activity in renewables rising 17% to US$110.2 billion.

Michael Liebreich, chairman of the advisory board at BNEF, said: “After

the dramatic cost reductions of the past few years, unsubsidised wind and solar can provide the lowest cost new electri-cal power in an increasing number of countries, even in the developing world - sometimes by a factor of two.

“Instead of having to subsidise renew-ables, now authorities may have to subsidise natural gas plants to help them provide grid reliability.”

Erik Solheim, executive director of UN Environment, added: “Ever-cheaper clean tech provides a real opportunity for inves-tors to get more for less.”

UNEP also praised the continued raduc-tion in solar tariffs driven by aucitons round the world. Yesterday PV Tech re-ported that GTM Research was expecting the upcoming tender in Saudi Arabia to potentially drop below two US cents per kWh for the first time.

Cre

dit:

UN

EP

2016 saw a 10% drop in average cost per megawatt for setting up solar PV and wind projects - UNEP, BNEF, Frankfurt School report.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

4

ASIA PACIFIC

2017 global PV demand forecasts as high as 85GWGlobal PV demand for 2017 could be as high as 85GW according to market research firm GTM.

The figures published on Tuesday coincid-ed with that of rival firm IHS Markit, which has predicted a lower tally of 79GW.

The latter’s prediction of negligible growth on its 2016 figure of 78GW is at-tributed to poor performance in the three largest markets of China, the US and Japan.

GTM Research has forecast that by the end of 2017, India will have overtaken Japan to become the third-largest PV end-market demonstrating that India can hardly be considered an emerging market.

“In some senses, characterizing what we expect to be a nearly 10 GW market with a refined national tender program, domestic content capacity, and a consoli-dated base of large players as ‘emerg-ing’ seems pretty crude. On the whole, I would disagree with that characteriza-tion,” Ben Attia, research associate at GTM Research and lead author of the report told PV Tech.

“But in another sense, India is still an emerging market because the market potential is still significantly limited by capital squeezes, effective rooftop policy, grid balancing and utility bankability risks, component quality risks, and huge,

untapped segments including residential rooftop and rural mini-grids, problems that mature markets typically do not face,” he added.

Great unknownChina has proven to be a difficult market to forecast with state-level proclamations capable of shifting the industry on its axis.

Both firms expect recent deployment growth in China to tail off with IHS going further and betting on a fall in installa-tions during 2017.

The bumper +34GW witnessed in China

last year was partly attributed to a large volume of projects completed prior to 2016 finally being recognised in Beijing’s official register.

Bloomberg New Energy Finance told PV Tech that its rolling forecast for 2017 is currently at a range of 76-81GW with the mid-point figure 79GW.

Figures released last month by Taiwan-based firm EnergyTrend predicted just 73.9GW. It echoed the expectation of reduced rollout in China and also expects to see India leapfrog Japan into the num-ber three spot.

Cre

dit:

Wel

spun

Ren

ewab

les.

India is expected to overtake Japan as the third-largest market globally.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

5

ASIA PACIFIC

Thailand and Vietnam become lead countries for OEM solar module supplyWhile third-party outsourcing of solar PV module assembly has been a con-stant feature of the PV industry for many years, the landscape of suppliers and the country of manufacturing has changed radically in the past two years, and will continue to do so out to the end of 2018.

This article shows clearly how third-party module supply by original equipment manufacturers (OEMs) has moved firmly to Thailand and Vietnam, with continued market-share gains expected from these countries going forward.

We explain why these changes have oc-curred and what the implications of this shift are expected to be.

The analysis is taken from the January 2017 release of our PV Manufacturing & Technology Quarterly report. The themes are set to be discussed at the forthcom-ing PV CellTech 2017 event in Penang, Malaysia, 14-15 March 2017.

What is the role of OEM suppliers in solar?Firstly, it is worth reviewing what we mean by OEM supply, and why many suppliers and OEMs themselves choose to stay off the radar in terms of promoting this supply-to-market tactic.

In contrast to the semiconductor industry that has different definitions of contract manufacturing and roles for OEMs in the supply-chain, solar module manufacturing is relatively simple and simply assembling cells into a module ranks is a one-stop shop with virtually no technical barriers-to-entry.

Therefore, the role of the dedicated OEM for solar module production is somewhat synonymous with module contract sup-ply, and the terms are used in this article interchangeably. The main term that is

different in outsourcing for solar cells and modules comes from tolling, something that is different from the role of dedicated OEMs and is touched on below when we talk about the China issue.

Contract manufacturing is prevalent across almost every adjacent technology market, not simply the solar industry. The drivers tend to be somewhat industry-specific, but are mainly stimulated by cost and route-to-market. It is a theme that has reshaped global manufacturing in the whole for the past four decades, has often been characterized by chasing the next cheap labour region, and could not be a more pertinent topic to consider in global economics, with President Trump and Mexico forming the lead case-study.

Again, China forms a unique case for third-party sourcing

Before we dive into the discussion and analysis of global OEM module supply for solar, the first thing we need to do is

remove mainland China from the picture. This is done because third-party outsourc-ing in China is rather the norm for solar, all across ingot, wafer, cell and module production.

In fact, tolling is rife in China, where com-panies effectively sublet time on under-utilized factories to produce product for other competitors. Even polysilicon plants are used on a tolling basis in China.

Tolling is radically different from OEM supply. OEM suppliers’ model is to oper-ate as a dedicated third-party assembly route, with a brand, such as Flextronics, Celestica and Jabil Circuits. Often OEM suppliers shift to a dual OEM/direct-mar-ket approach, generally driven by lack of business or a hunger to increase margins.

There are likely hundreds of companies in China today that operate in a quasi-OEM, partial-tolling, and on/off direct-sell-to-market approach. There is no parallel in the solar industry, and nor should

Imag

e: C

eles

tric

a

Contract manufacturing is prevalent across almost every adjacent technology market, not simply the solar industry.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

6

ASIA PACIFIC

one expect to see this change in China anytime in the near future.

Therefore, in our graphic below, we remove all China-based third-party activ-ity, that also happens to be impossible for anyone to come close to tracking with accuracy, and look at the main OEM production trends outside China. This is shown in the graphic below.

Of all the updated and new analysis of PV manufacturing done by our in-house research team, this is one of the most striking visuals. We have chosen to group data across certain countries and regions to show the trend most clearly. This means putting OEM module production in Europe, Canada, Korea, Indonesia, Taiwan, India and some others into the Rest-of-the-World group. This allows us to track everything outside Latin America, Malaysia, and the dual Southeast Asia countries of Vietnam and Thailand, as one group that operates differently to the aforementioned countries.

We make a clear distinction also be-tween Malaysia and Vietnam/Thailand, with OEM operations in Malaysia again differentiated, in a similar way to how the country as a whole is placed for high-tech

manufacturing. Moreover, within Vietnam and Thailand, it is important to define clearly who is operating the sites. In this regard, the separation of Malaysia from Vietnam and Thailand is again justified, with Vietnam and Thailand having a greater number of OEM players whose business model has more of a sub-contract element to it, with the custom-ers often being Chinese companies who bankroll the efforts.

The OEM landscape post SunEdison restructuringThe other factor that has come into play in the past 12 months comes from the fallout of the SunEdison supply arrange-ments, with SunEdison just a few years ago being highly vocal and proud of running a fab-lite approach. Virtually overnight – at the end of 2015 – module and cell suppliers that were reliant on a constant supply of product being shipped to SunEdison’s downstream projects had to quickly find new customers, or even decide if the timing was right to move from OEM supply to a branded offering to the end-market.

It appears most have managed this, albeit with related impairment and write-off costs. Ultimately, at the start of 2016,

there were still many Chinese companies that needed fully-operational third-party supply routes to feed the US market. During 2016 however, this has changed due to the increased availability of new cell and module capacity set up across Southeast Asia by Chinese and Taiwanese companies, under their own brand.

PV CellTech to address prospects for OEM suppliers going forwardAs we set up the agenda for the PV CellTech 2017 event in Penang, Malay-sia, 14-15 March 2017, we specifically invited some of the companies that were behind the above market shifts, as OEM operations had previously been incred-ibly stealth within the solar industry. The other driving factor is our continued focus on really knowing who is making the cells and modules being shipped to the end-market today.

To view the latest PV CellTech agenda, please follow this link. To register for the event, click here.

We will also be hosting free webinars in February, discussing PV manufacturing and technology trends and the impact of global market drivers. You can register for these webinars through this link.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

7

AUSTRALIA

Lyon Group to build world’s largest solar-plus-storage project in South AustraliaBrisbane-based renewable energy investor Lyon Group will soon start building a AU$1 billion (US$767 mil-lion) solar-plus-storage farm in South Australia - the world’s largest.

The Riverland project will include 330MW of solar PV requiring AU$700 million investment alongside a 100MW/400MWh lithium-ion battery system costing be-tween AU$200-300 million. This will also be Australia’s largest PV farm.

Various news outlets including the Aus-tralian Broadcasting Corporation have cited Lyon Group founding partner David Green speaking to reporters in Adelaide about the record-breaking project.

Green said the project would include 3.4 million solar panels and 1.1 million bat-teries. Lyon Group has secured land with construction set to kick off in June, requir-ing 270 workers, and commissioning due in December. It was reported that grid connection negotiations are at advanced stages.

The storage element of the project comes at an auspicious time given the multiple blackout issues that hit South Australia over the last few months, causing a fierce national debate about whether renew-ables were to blame. Even Tesla chief Elon Musk weighed in by offering to build a 100MW battery to solve the crisis, which he would provide free of cost if not com-missioned within 100 days of being asked. Just a few days later the South Australian government announced plans to tender for a 100MW battery, emphasizing that there will be an open, competitive tender

process. Lyon Group has reportedly al-ready shown interest in participating.

Moreover, as more renewables come online all over the country, Australia’ s energy industry faces the impact of im-minent closures of multiple old, coal-fired plants. For example, the Clean Energy Council today called for renewables and storage to replace the 1.6GW Hazelwood coal station in Victoria, which was closed this week.

Now Lyon Group, which is backed by Japanese giant Mitsubishi and Blackstone via US hedge fund Magnetar Capital, has announced its own separate storage plan for South Australia.

Green told reporters that the solar power generation will qualify for renewable energy subsidies of AU$84/MWh, addi-tional to the wholesale market price. The project is also 100% equity financed.

Another 100MW battery at KingfisherLyon Group had already announced last year another major solar-plus-storage project at Roxby Downs in South Austra-lia.

The Kingfisher Project will include 120MW of solar costing AU$250 million and a 100MW/200MWh lithium-ion battery system requiring between AU$100-150 million investment. This will include 1.3 million PV panels and 1.1 million batteries again.

The battery will be connected to a grid that will power nearby mining activity. The project will also be connected to Australia’s wholesale market, the National Electricity Market (NEM). It is due to come into full operation by mid-2018.

Engineering firm Downer will carry out EPC, while US-based firm First Solar will carry out O&M activities.

Cre

dit:

Lyo

n G

roup

Another solar-plus-storage project from Lyon Solar.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

8

AUSTRALIA

Australian rooftop solar financier issues another AU$50 million climate bondFinancial services group FlexiGroup, whose subsidiary Certegy Ezi-Pay finances rooftop solar, has issued a AU$50 million (US$38 million) climate bond, which has been certified by the global Climate Bonds Initiative (CBI).

The Clean Energy Finance Corporation (CEFC) made a cornerstone commitment of AU$20 million to the bond.

This is only the second climate-certified issue of a bond backed by securitised as-sets in Australia, with FlexiGroup issuing a very similar bond back in April 2016.

CEFC debt markets lead Richard Lovell said: “FlexiGroup achieved tighter pric-ing on this climate bond, which shows investors were prepared to pay a ‘green premium’. This is a strong market signal which will assist in accelerating the de-velopment of a more varied and flexible green bond market in Australia.”

The bond is backed by consumer receiv-ables originated through FlexiGroup’s wholly-owned subsidiary Certegy Ezi-Pay, which has financed more than 120,000 solar PV rooftop installations.

Lovell added: “There is clearly a global trend toward investment in green

bonds. Our investment support for the FlexiGroup climate bond is part of our strategy to ensure that Australia’s clean energy sector can tap into this burgeon-ing source of capital, and that investors with a socially responsible mandate have the opportunity to participate.”

Cre

dit:

CEF

C

The Clean Energy Finance Corporation (CEFC) made a cornerstone commitment of AU$20 million to the bond.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

9

AUSTRALIA

First Solar closes financing for 48.5MW solar project in New South WalesUS integrated PV firm First Solar has reached financial close on a 48.5MW(ac) solar project in New South Wales, Australia.

The Manildra Solar Farm has received AU$9.8 million (US$7.5 million) of grant funding from the Australian Renew-able Energy Agency (ARENA) under its large-scale solar funding round. A 13-year power purchase agreement (PPA) has also been signed with EnergyAustralia, a major utility that is set to sign PPAs for 500MW of wind and solar projects across eastern Australia.

The project will use 466,000 First Solar thin-film modules and single-axis trackers to produce more than 120GWh per year for the equivalent of 14,000 households.

Jack Curtis, First Solar regional manager for Asia Pacific, said: “We have witnessed unprecedented cost reductions in large-scale solar in recent years. As the appetite for this asset class continues to grow, timely and reliable project delivery will be the strongest driver of future cost reduc-tions, cementing solar as a competitive energy source in Australia.”

First Solar has also appointed local engi-neering firm O’Donnell Griffin to provide EPC services for the project. Construction is scheduled to commence in the first half of 2017 and once complete in 2018, First Solar will have more than 400MW(ac) of solar PV installed in Australia.

ARENA chief executive Ivor Frischknecht said: “By supporting innovators like First Solar, ARENA has fast-tracked the development of substantial new Austra-lian industries like the large-scale solar sector, which is now on the cusp of being commercial.”

Cre

dit:

Firs

t Sol

ar

The Manildra Solar Farm has received AU$9.8 million (US$7.5 million) of grant funding from ARENA.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

10

AUSTRALIA

Enel to acquire 137MW phase of Bungala Solar project in AustraliaEnel announced Monday that it has closed an agreement to acquire Bunga-la Solar One — the 137.5MW phase of the 275 MW Bungala Solar PV project — from Bungala Solar Holding Pty Ltd., a subsidiary of Australian developer Reach Solar Energy Pty Ltd.

The project is currently tabbed as the largest ready-to-build solar project in Aus-tralia. The transaction was conducted by Enel through a joint venture between Enel Green Power and the Dutch Infrastructure Fund (DIF).

The purchase of the phase is expected to be closed in the third quarter of 2017. The Bungala Solar project is located near Port Augusta in South Australia.

Francesco Starace, Enel CEO and gen-eral manager, said: “The acquisition of Australia’s largest PV project, which takes us onto a new continent, is an important step forward for the Enel Group. The Australian renewable energy market is characterised by abundant resources and growing demand. Enel will work to harness these resources and contribute to the Australian economy, generating shared value for all our stakeholders through a strategy that delivers industrial growth built upon a foundation of sustain-able development.”

The joint venture’s total investment in the 275MW installation is around US$315 million dollars — which entails project construction, with Enel providing around

US$157 million dollars.

The total investment will be financed through a combination of equity and project finance with a consortium of local and international banks. The project is fully contracted with a long-term power purchase agreement with Australian utility Origin Energy.

Construction at Bungala Solar One is expected to begin by mid-2017, followed by Bungala Solar Two — with construc-tion slated to start by the end of 2017.

The total installation is expected to be completed and operational by the third quarter of 2018.

The Bungala Solar project is expected to produce around 570 GWh annually, equivalent to the consumption needs of approximately 82,000 Australian homes.There are already plans for larger solar projects to be developed in Australia, as the Kidston Solar project is expected to feature a 270MW second phase that will be paired alongside the initial 50MW phase.

Imag

e: E

nel

The 275MW project is expected to be completed by the third quarter of 2018.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

11

CHINA

Price of Chinese module imports to India dropped 8% in Q1 2017The price of Chinese module imports to India has dropped 8% over the last quarter and 29% year-on-year, according to new price indices calculated by consul-tancy firm Bridge to India.

The consultancy has analysed import prices for modules and inverters, as well as costs of utility-scale and rooftop EPC, by interviewing up to 10 leading project developers, EPC firms and module sup-pliers.

ModulesLooking specifically at multi-crystalline PV module imports from China for orders of minimum 50MW in size, Bridge to India calculated cost, insurance and freight (CIF) to India, not including any further port or inland transportation costs. Mod-ule prices have been falling steeply due to oversupply combined with quarterly demand fluctuations in China.

InvertersInverter prices were shown to have fallen 21% year-on-year and 5% over the last quarter, mainly due to increasing compe-tition and new players such as TBEA, Hua-wei and Sungrow entering the market.

Utility-scale EPCFor utility scale solar projects of 50MW

in size, EPC prices declined 22% year-on-year, and 8% over Q1 2017.

Rooftop EPCMeanwhile, for 500kW rooftop solar proj-ects on an industrial pre-fabricated metal structure, EPC prices have declined 21%

year-on-year and 6% over the last quarter.

Bridge to India, associate director, con-sulting at Bridge to India, wrote a blog on PV Tech today discussing the new tender process paradigm in India following recent record low solar tariffs.

Bridge to India has analysed import prices for modules and inverters, as well as costs of utility-scale and rooftop EPC.

Cre

dit:

Alp

ex S

olar

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

12

INDIA

India added 5.5GW solar in FY2016/17India added 5,526MW of solar PV capacity in the fiscal year 2016/17, up 83% on the previous year, according to new figures from the Ministry of New and Renewable Energy (MNRE).

Consultancy firm Bridge to India said the numbers were “impressive”, but still 50% below the annual target of 12GW. On the other hand, wind additions of 5.4GW in the same period were 35% over the annual target.

The consultancy noted a downward trend in renewable energy allocation during the financial year making the 20,450MW target for 2017/18 “impos-sible” to meet.

India did install a “blockbuster” 5.8GW of renewables in March in the lead up to the financial year end, which was more than the previous 11 months combined. Bridge to India noted that this rush was likely to have been driven by a widely expected phase out of incentives from this month onwards. Incentives under

threat include accelerated depreciation and 10-year tax holidays.

Noting the downward trend in solar tenders over the year, the consultancy expects this trend to continue for up

to six months. Despite just “modest” renewables growth expected in 2017/18, Bridge to India forecasts that deploy-ment will still be well ahead of thermal capacity additions.

Cre

dit:

IBC

Sol

ar

India installed a blockbuster 5.8GW or renewables in March in the lead up to the financial year end.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

13

INDIA

UK-India trade ties deepen with £240 million energy investmentA joint investment of £240 million has been unveiled by the UK and Indian governments to encourage investment into India’s rapidly growing energy and renewables market and deepen trading ties between the two countries.

UK chancellor Philip Hammond visited Delhi and Mumbai on Tuesday as part of the 9th UK-India Economic and Financial Dialogue (EFD), hosted by Indian Finance Minister Arun Jaitley. As the UK prepares to leave the European Union, Hammond was expected to engage in high level talks aimed at expanding the UK’s eco-nomic and trading relationship with India.

As part of these efforts, investment from the City of London is to be encouraged into India’s energy sector through a UK-India sub-fund of India’s National Invest-ment and Infrastructure Fund. With a core investment of £120 million from each gov-ernment, this will aim to raise £500 million for Indian infrastructure projects.

The fund will focus initial investments on India’s rapidly growing energy and renewables market and a fund manager is expected to be selected by the autumn.

Hammond said: “As we prepare to leave the European Union, it is more important than ever that we strengthen our relation-ship with India, one of the world’s leading economies and one of our oldest friends and allies.”

The UK’s secretary of state for business, energy and industrial strategy (BEIS) has also landed in India to take part in the first talks between the two countries dedi-cated to deepening energy cooperation between the two countries.

Greg Clark will meet with his ministerial counterparts over the two day visit (6-7 April) as part of the inaugural India-UK Energy for Growth Dialogue, which will

seek to agree priority areas for bilateral collaboration and a business delegation of over 40 companies will explore com-mercial opportunities.

Representatives from across power, renewables, oil and gas will discuss future direction for the energy sector, infra-structure financing, and opportunities for wider collaboration.

In addition to energy, Clark will also engage in discussions on climate change and wider UK-India ties supporting re-search and innovation as part of the UK’s emerging industrial strategy.

Speaking ahead of the visit, the minister said: “On my second visit to India since taking office, I look forward to discussing our shared priorities of providing secure, affordable and sustainable energy. It is clear that building greater collaboration between the UK and India in the energy sector has the potential to increase pros-perity and growth in both our nations.

“As we deliver on the shared commit-ment to provide sustainable, secure and affordable energy in both our countries, the India-UK Energy for Growth Dialogue will enable us to explore the immense shared economic opportunities lying ahead.

“India invests more in the UK than in the rest of the EU combined, while the UK is the biggest G20 investor in India. I look forward to discussing how the UK govern-ment’s Industrial Strategy will increase the prospects for shared trade, investment and energy innovation between our two great countries.”

According to BEIS, the Energy for Growth Dialogue takes forward a commitment made by Prime Ministers Narendra Modi and Theresa May during the latter’s visit to India in November last year when plans were unveiled for a £10 million joint research and development centre to sup-port solar innovations.

Chancellor Philip Hammond visited Delhi and Mumbai earlier this week for the 9th UK-India Economic and Financial Dialogue.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

14

INDIA

Fortum proves low solar tariffs viable in IndiaFinnish firm Fortum has commissioned a 70MW solar PV plant in the Indian state of Rajasthan, which it won last year at what was then a record low tariff of INR4.34/kWh (US$0.067).

Critics had said that even higher tariffs in other states were unworkable, although irradiation and solar park costs do vary in each location.

Prices hovered above this 4.34 rupee level for some time, but they dropped signifi-cantly lower in February this year with the likes of Acme Solar hitting a levelized tariff of INR3.29/kWh at the Rewa park in Madhya Pradesh. Jaws dropped in the industry, followed by the usual to and fro between doubters and those convinced that market conditions genuinely make such low tariffs feasible.

Fortum’s plant completion will be wel-comed by the Indian government, which despite aiming to push prices down will want to see through a sustainable industry. Nonetheless it is well known that Fortum has a rock solid balance sheet and Bridge to India has cited poor risk pricing in the business plans of Fortum’s Indian rivals.

The firm’s 70MW commissioning at the Bhadla Solar Park came on schedule, having secured a 25-year power purchase agreement with major Indian utility NTPC.

Fortum entered India by announcing plans to invest €200-400 million. The Bhadla project is the company’s third and

largest solar plant to date, with a total 85MW installed across Rajasthan and Madhya Pradesh. The company is also building a 100MW solar plant at Pavaga-da in Karnataka, which is due for comple-tion in the next few months, with a tariff of INR 4.79/kWh.

Cre

dit:

For

tum

Cor

por

atio

n

Fortum has commissioned a 70MW solar PV plant in the Indian state of Rajasthan with what was once a record low tariff.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

15

INDIA

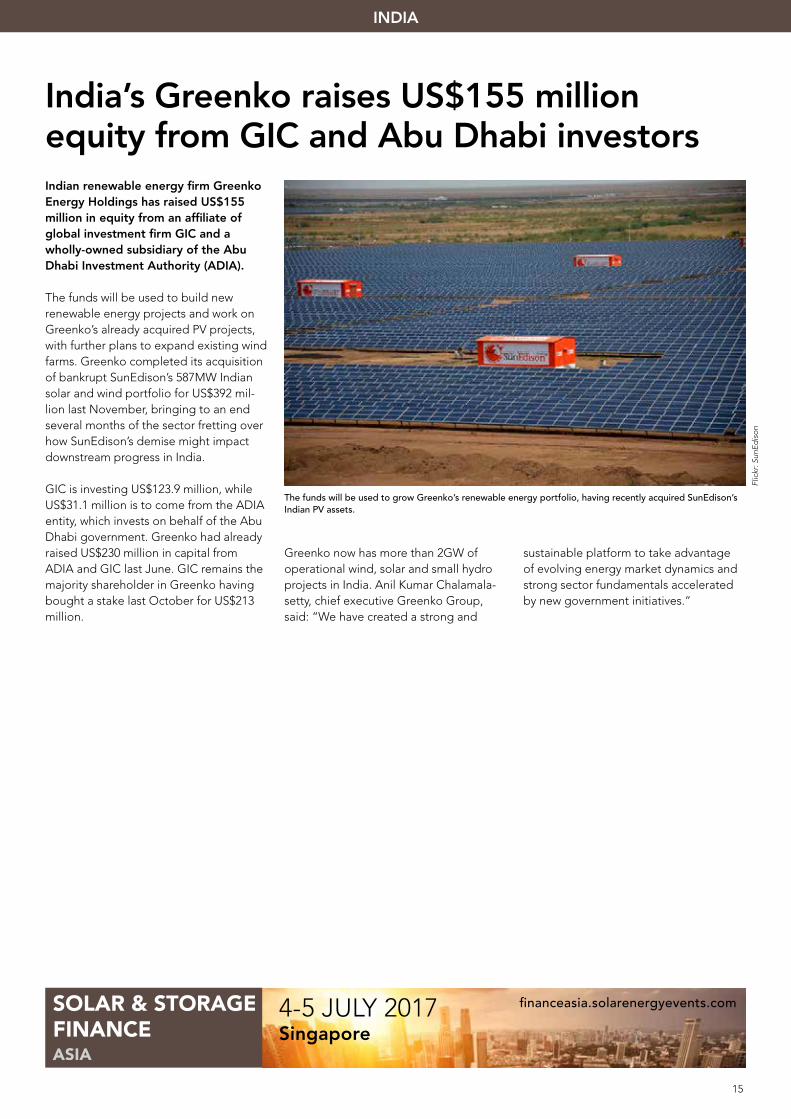

India’s Greenko raises US$155 million equity from GIC and Abu Dhabi investorsIndian renewable energy firm Greenko Energy Holdings has raised US$155 million in equity from an affiliate of global investment firm GIC and a wholly-owned subsidiary of the Abu Dhabi Investment Authority (ADIA).

The funds will be used to build new renewable energy projects and work on Greenko’s already acquired PV projects, with further plans to expand existing wind farms. Greenko completed its acquisition of bankrupt SunEdison’s 587MW Indian solar and wind portfolio for US$392 mil-lion last November, bringing to an end several months of the sector fretting over how SunEdison’s demise might impact downstream progress in India.

GIC is investing US$123.9 million, while US$31.1 million is to come from the ADIA entity, which invests on behalf of the Abu Dhabi government. Greenko had already raised US$230 million in capital from ADIA and GIC last June. GIC remains the majority shareholder in Greenko having bought a stake last October for US$213 million.

Greenko now has more than 2GW of operational wind, solar and small hydro projects in India. Anil Kumar Chalamala-setty, chief executive Greenko Group, said: “We have created a strong and

sustainable platform to take advantage of evolving energy market dynamics and strong sector fundamentals accelerated by new government initiatives.”

Flic

kr: S

unEd

ison

The funds will be used to grow Greenko’s renewable energy portfolio, having recently acquired SunEdison’s Indian PV assets.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

16

INDIA

ADB approves US$175 million to Powergrid for solar park transmissionThe Asian Development Bank (ADB) has approved a US$175 million loan to India’s major network operator and utility Power Grid Corporation of India (Powergrid) relating to solar park trans-mission.

ADB will also administer a US$50 million co-financing loan equivalent from the Clean Technology Fund (CTF) – a US$5.8 billion component of the Climate Invest-ment Funds.

India recently doubled its solar park capacity target to 40GW, and Powergrid is working on projects to improve transmis-sion.

Specifically it is working on transmission infrastructure for 2.5GW of power from parks in Bhadla in the state of Rajasthan as well as 700MW from Banaskantha, Gujarat. Furthermore it is working on two subprojects aiming to increase solar power generation by 4.2GW.

In related news, this week Indian state-run utility NTPC also completed commission-ing of its 260MW project at the Bhadla Solar Park.

Transmission is one of a number of issues affecting solar parks, including retender-ing of solar park capacity of late due to various infrastructure delays putting off potential bidders.

“India, with its mandate of achieving a more sustainable future, is leading the lines in achieving energy security while increasing energy capacity and supply through renewable sources such as solar

energy,” said Kaoru Ogino, an ADB prin-cipal Eenergy specialist. “We are looking forward to the benefits of this partnership with Powergrid to continue helping India achieve a more inclusive and sustainable future.”

An ADB loan agreement of up to US$500 million was announced last month relat-ing to Green Energy Corridor projects.

Flic

kr:A

DB

ADB will also administer a US$50 million co-financing loan equivalent from the Clean Technology Fund (CTF).

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

17

INDONESIA

Engie partnerships to invest US$1.25 billion in Indonesian renewables, agreements in SingaporeFrench power giant Engie Group is partnering with three firms to develop various solar-related projects in Indo-nesia requiring US$1.25 billion invest-ment.

The largest partnership agreement is with sugar producer Sugar Group for a joint US$1 billion investment in 500MW of solar PV and biomass projects in Sumatra and Eastern Indonesia over five years. Of this, 300MW will be dedicated to solar parks, including a 140MW park in Lampung.

The second partnership is with micro-grid developer Electric Vine Industries to invest US$240 million in building and operating smart PV microgrids for 3,000 villages in the province of Papua over five years. The projects are set to power around 2.5 million people during a 20-year period.

The third is with PT Arya Watala Capital to invest US$15 million in up to 10MW of solar plants in East Nusa Tenggara, the southernmost province, over three years. The projects will be located in 10 differ-ent areas in the province on major islands such as West Timor, Flores and Sumba.

Didier Holleaux, executive vice president of Engie Group, said: “Our strategy is to work through an ecosystem of partners to co-develop and scale renewable energy and innovative low-carbon technology solutions to meet the country’s unique energy challenges.”

The three partnership agreements come as part of the Terrawatt Initiative, a non-

profit organization that was launched by Engie during COP21, and were signed as part of French President Francois Hollande’s visit to Southeast Asia in late March.

Singapore and Malaysia partnershipsAs part of Hollande’s visit, Engie has also signed a partnership agreement in Malay-sia with Sime Darby on renewable energy.

It has also partnered with utility Senoko Energy and electricity storage group Bolloré to co-develop smart city solutions including energy storage in Singapore and the Asia Pacific region.

Finally, Engie has signed agreements with its R&D arm Engie lab, Nanyang

Technological University Singapore and Schneider Electric to work on micro-grid technologies for the region.

Yeoh Keat Chuan, managing director of Singapore Economic Development Board, which will support the projects, said: “The rapid urbanisation in Asia is accelerating the need for smart and sus-tainable urban solutions. We are pleased that Engie is leveraging Singapore’s strong ecosystem of industry and research partners to develop and commercialise new urban solutions in Singapore to serve this region. These efforts also build on the capabilities of the new Engie Lab Singapore, which was launched last year, and reflects Engie’s growing presence in Singapore.”

Flic

kr: B

art S

pie

lman

The largest partnership agreement is with Sugar Group for a joint US$1 billion investment in 500MW of solar PV and biomass projects.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

18

INDONESIA

Indonesia’s new rural electrification regulationIn an unprecedented move, the Direc-torate General of Electricity under the Indonesian Ministry of Energy and Min-eral Resources has pushed through a rural electrification regulation recently signed by the new minister, Ignasius Jonan. This regulation provides the framework on how a private business entity can provide electricity to current-ly un-electrified regions through busi-ness area concessions. It also provide ways to calculate and receive electricity subsidies from the government.

This regulation opens the flood gates to businesses currently providing electrifica-tion technologies and business models to rural areas. The exact requirements on how to become an appointed electricity provider is not defined within the regula-tion. Today there is an abundance of technologies and business models avail-able. Without a complete and responsible feasibility study, there is a huge risk to the communities that they will receive elec-tricity in ways that are neither appropriate nor adequate. Indonesia’s diversity means that the energy use needs and growth potential between the communities vary widely.

Who will be performing a complete and responsible energy needs assessment, geophysical survey of the area, studies for social behavior, and economic activity and growth potential compiled as a useful

feasibility study? Without knowing these variables, any business model that relies on household tariff collection can fail before it even starts. Farming communi-ties only have cash a few months within their harvest payments. Fishing communi-ties and day labourers at nearby mines or fields typically have daily income. Will the businesses pay attention to these facts and apply the right payment scheme? Or will they assume everyone will pay for all of the electricity produced for the dura-tion of the project?

Even more worrying is that there is no standard of service defined in the regulation. A solar lantern or an inad-equate small home system given to each household may be counted as providing electricity service to the community. This means that distributors of these products will be able to get approval to dissemi-nate their wares and get paid through the subsidy fund. What if the community needs more than lanterns or individual systems? What about productive use of energy? What about communities that are better served with mini-grids?

The reverse can also happen where mini-grid providers will be able to install their systems in locations where there is no need. A huge amount of subsidies will be required to build the mini grids in these locations. Unless they are also bringing additional economic activity, the available

energy will be wasted.

Rural electrification and its financial viability is a complex issue. It involves engaging with the communities and understanding their needs, both physi-cally and culturally. Understanding their requirements, their potential for growth, and acknowledging their way of living is required for a sustainable electrification program.

Our team members and myself are still learning new things despite having visited over 300 rural communities and engaging with them and listening to their stories. We inspected over 200 solar PV microgrid systems and continue to find opportuni-ties to learn more about how to acknowl-edge each community as unique social constructs. Only then we can develop and design an appropriate electrification plan using the right technologies and payment schemes that meet their needs.

Despite all of this, the new regulation provides an opportunity for the private sector to engage in electrifying Indone-sia’s 12,000 villages currently without any access to electricity. If the right compa-nies can take advantage of the regulation, this will create mutually beneficial rela-tionships between them, the Indonesian government and more importantly the community members and households.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

19

JAPAN

Canadian Solar secures US$35 million credit facility with Sumitomo Mitsui FinanceSolar power company Canadian Solar announced Thursday that its wholly-owned subsidiary Canadian Solar Proj-ects K.K. has entered into a three-year credit agreement with Sumitomo Mitsui Finance for US$35 million.

Sumitomo Mitsui Finance stands as one of Japan’s largest leasing companies in the world — boasting a presence across the globe. The facility earned commit-ments from five finance leasing institu-tions.

Canadian Solar intends to use the pro-ceeds from the facility in order to spur the development of PV projects in Japan. This stands as Canadian Solar’s second financ-ing with the Sumitomo Mitsui Finance group.

Dr. Shawn Qu, chairman and chief execu-tive officer of Canadian Solar, said: “We are pleased to secure strong support

from a leading group of finance leasing institutions. We value our partnership with SMFL. This is our second financing with the broader Sumitomo Mitsui Financial Group. We have successfully raised in

excess of JPY13 billion of credit lines with them. We look forward to expanding our banking relationship in Japan and other important markets.”

Imag

e: C

anad

ian

Sola

r

Canadian Solar intends to use the proceeds from the facility in order to spur the development of PV projects in Japan.

20

JAPAN

Streamlined: Japan’s PV market futureIn every maturing market for solar PV, thoughts start to turn away from generating raw kilowatt-hours and be-ing paid handsomely through feed-in tariffs (FiTs) for them. Instead, sensible thinking focuses on generating power where and when it is actually needed, whether that be through on-site self-consumption or injecting it into the grid at the times of day when it is most needed, using batteries. In Japan how-ever, this trajectory has been transpar-ent and accelerated over the past five years that the FiT has been in existence (since July 2012).

“When we had ¥42 (US$0.37) /kWh FiT, the business was so easy, people who knew nothing about PV could run PV busi-nesses, but now those amateurs are not able to control the situation. Those who can manage the situation correctly can run business. Others have already left the PV industry,” Yoshio Sekiguchi, a technical expert at local, vertically integrated PV company Looop, says.

Over and over again, at last week’s PV Expo trade show in Tokyo, PV Tech heard that those that will survive in Japan’s PV market will be the ones in it for the long haul.

On a product level, you could see this in the fact that the domestic likes of Looop and China’s Trina Solar were offering glass-glass modules, boasting ever-tougher materials and longer lifespans. In Looop’s case they were offering the in-dustry’s longest warranties – 30 years – for their ‘Nextough’ modules, while Trina So-lar was promoting the maximum yield fac-tor of their bifacial modules at the show. Indeed, there were several domestic and international makers showcasing bifacial modules, showing that squeezing out every drop of power from limited space is getting more and more important.

Overall trendsMarket analysis expert Izumi Kaizuka of research firm RTS PV says this year’s PV

market in Japan is likely to total around 8.6GW. Although figures released of module shipments by the Japan Photo-voltaic Energy Association (JPEA) only come up to around 6.4GW, Kaizuka says the JPEA statistics do not include Tier 3, Tier 4 makers, or many instances of large conglomerates like Marubeni buying directly from Chinese makers.

Kaizuka says that despite the absence of precise data, some trends become appar-ent from looking at the market: market volumes are down from the 10GW+ early years of the FiT, and manufacturing volumes are down for Japanese module makers.

In all, the mass market for PV in Japan could have peaked in 2015, especially where ‘megasolar’ was concerned, on which RTS’ Kaizuka and Trina Solar Japan’s director Ye Chen were in agree-ment.

Two of Japan’s largest module manufac-turers, Kyocera – with around 1.4GW of capacity - and thin-film stalwarts Solar

Frontier, were this year not even repre-sented with stands at the show, although their products were on display on the booths of distributors. The pair have elected to focus on their overseas activi-ties for the time being, Kaizuka explained.

“In Japan, based on historical records, the peak of the solar industry was 2015 and 2016. Everybody says the same thing, it’s going to slow down a little bit until 2020 to absorb all those projects that have already registered and keep stable market size after that,” Trina Solar’s Ye Chen says.

“[The] market majority after that will come from commercial and residential roof-tops.”

RTS PV’s Kaizuka believes that going forward, Japan’s market will streamline down to around 5GW of new demand per year, even if as much as half of a 50GW+ pipeline of already-approved projects is cancelled, as has been widely reported.

This year’s first tenders for large-scale

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

Imag

e: A

ndy

Col

thor

pe.

Trina Solar Japan director Ye Chen with the company's latest bifacial modules, at the PV Expo show in Tokyo.

21

JAPAN

GSSG Solar to acquire 350MW portfolio of solar in JapanSolar investment firm GSSG Solar an-nounced Monday that it will provide over US$120 million in additional com-mitments to the firm’s investments in Japanese solar projects.

As a result of this increased capacity, GSSG will invest in the acquisition and financing of an incremental US$1 billion of Japanese mega-solar plants over a three-year investment period.

GSSG raised its first fund in 2014, which focused primarily on Japanese solar with select exposure to the US utility solar mar-ket. This new commitment is exclusively tabbed for the Japanese market and will allow the firm to acquire another 350MW of solar projects within the country.

GSSG is an investment manager that overviews the technical, financial, and ex-ecution risk of each potential solar project investment. It focuses on aligned and col-

laborative structures with its development partners and stakeholders.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

Imag

e: M

arti

n A

beg

gle

n /

Flic

kr

GSSG will invest in the acquisition and financing of an incremental US$1 billion of Japanese mega-solar plants over a three-year investment period.

solar (projects over 2MW) could be a ‘wait-and-see’ process for many develop-ers, who may choose not to get involved just yet, nonetheless an existing backlog of higher FiT projects will sustain the market for some time to come, Kaizuka says. Furthermore, while the FiT drops this year to ¥21, this is still much higher than in comparable markets like Germany (US$0.06/kWh). According to Looop sales representative Rihan Kimura, system prices have fallen so much in Japan that the IRR’s for projects have actually slightly risen from around 5%-6% to 6%-8%.

Self-consumption future and batteriesAs we already explored in a news item

last week, Japan’s move towards a self-consumption based solar market has lead to the likes of Toshiba, Sharp and Panasonic focusing firmly on the Zero Energy House (ZEH) concept, with higher efficiency modules taking pride of place. Foreign players like LG and SunPower who also make high efficiency modules will continue to aggressively target this market too, Izumi Kaizuka says, while it will be “harder to sell high volumes of cheap modules into the megasolar (2MW+) market”.

Masaaki Shibata, a 20-year veteran of the Japanese renewables industry and president of consulting group and de-

veloper Eiwat, says batteries are another next logical step, for large-scale as well as rooftop solar. His company is involved with deploying US-made Aquion non-tox-ic, non-flammable ‘saltwater electrolyte’ batteries into Japan and according to Shi-bata, if Aquion’s initial tranche of 10 proj-ects in Japan this year go well, regional power companies, which also govern Japan’s grid network, could give the ok for a further wave of batteries. As well as allowing for greater self-consumption, the batteries could also remove the curtail-ment risk from PV plant output, which has been seen as a barrier to investment in some of the more saturated grid areas.

22

JAPAN

International PV players ready for Japan’s large-scale tendersThe prospect of Japan introducing a ten-der system for large-scale solar project rights from this year does not phase in-ternational companies doing PV business in Japan, who have said they are ready for the new policy.

Dr Shawn Qu, CEO of Canadian Solar, and Terry Zhao, CEO of Chinese inverter com-pany Sungrow’s Japanese subsidiary both told PV Tech that the prospect of annual 500MW auctions for PV projects over 2MW is not an obstacle to their ambitions in the region. “We are prepared. We are ready to participate in the tenders under the new rules,” Qu said. “Competition is always there,” he added when asked if the new auction system would lead to aggressive price competition across the industry.

“Even with the FiT, it has already dropped several times and now the tenders will allow some market elements into this process. But there have been tendering mechanisms in many other countries where Canadian Solar participates, so we are not surprised at all, we will be fully prepared and will par-ticipate.” Ontario-headquartered Canadian Solar recently connected a 24MWp PV plant in Yamaguchi Prefecture, bringing its total portfolio in operation in Japan to 46MWp. That project was awarded the feed-in tariff (FiT) rate of ¥40 (US$0.35)/kWh, applicable in 2013, the second year of Japan’s large-scale FiT scheme.

Although the FiT rate has since fallen drasti-cally, this year dropping to just ¥21/kWh for projects to be awarded under the tender, Canadian Solar has a further pipeline in Ja-pan of 167MWp of projects under construc-tion and 66MWp of projects ready to go, all at higher FiT rates than this year’s reduced rate. “We still have a good inventory of high FiT projects that will take a few more years to build out. [Furthermore], we’ve been in this business for 16 years. We know that grid parity is the ultimate goal and we think we can beat conventional energy sources

on price, so [the lowering of the FiT rate] was not a surprise to us at all,” Qu said.

Inverter maker welcomes increased competition through tendersMeanwhile, Sungrow Japan, which has a target to supply 200MW of inverters in the country this year, wants to be in the country long-term, CEO Terry Zhao said. “Unlike some other Chinese companies, we want to be in business in Japan for 20, 30 years from now,” Zhao said.

The company has introduced two inverters to the Japanese market, including a central inverter solution specifically for 2MW+ PV plants, meaning it has a lot at stake in Japan’s megasolar (local term for large-scale) market. Zhao said that Japan’s falling FiT would not deter the company. “The FiT will drop to ¥21 next month, but even that is dearer than in other countries. In the Japanese market, costs are very high so we and panel makers need to bring whole system costs down. The FiT could still drop to ¥20 or ¥18 and we would still be ok [as an industry],” Zhao said.

Sungrow welcomes the introduction of tenders, according to Zhao. “It is good news for us, because [to be successful] in auctions, you have to lower costs. For lower costs, if the inverter is cheaper, it’s not enough. But we can make the whole system cheaper, with 10% payback [in Japan]. For our inverters, the transformer will be cheap-er in some cases. With some other inverter makers you need two transformers for just 1MW of PV. With ours, for a 2MW system you can use just one transformer instead of two. These technical aspects will make our customers win the auctions [we hope]. We see it as a positive step,” Zhao said.

What may make the process more com-plex and difficult for some are new rules governing the right to connect to Japan’s regional grid network, Izumi Kaizuka, a mar-ket research expert at Tokyo-based RTS PV, told PV Tech. In addition to securing rights through auctions, project developers must also enter what could be lengthy discus-sions with whichever of Japan’s 10 regional utilities – which are also the country’s grid operators – to get their PV plants grid-tied, which is a necessity to receive the FiT.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

Imag

e: A

ndy

Col

thor

pe.

Canadian Solar's stand at PV Expo, Tokyo. The company was showcasing its vertically integrated strengths from high-efficiency modules to EPC services and everything inbetween including residential energy storage solutions.

23

JAPAN

Japan’s big PV names targeting self-consumption and rooftop marketThe Japanese PV market’s switch from a feed-in tariff (FiT) driven, mostly utility-scale phenomenon to one based on rooftops and self-consump-tion was in evidence at the PV Expo trade show in Tokyo this week.

PV Tech visited the booths of major manufacturers and international house-hold names Panasonic, Toshiba and Sharp during the exhibition. It was clear that while utility-scale PV (known as ‘mega solar’) in Japan is set to dimin-ish in market size, with the government now confirming the introduction of an-nual 500MW tenders, each of the three big names was preparing to see the already strong residential market take off further and commercial PV continue to grow. The Japanese government has confirmed that FiT prices will fall to ¥21 (US$0.18)/kW this year with further drops expected next year, meaning that from then it will be as economical to self-consume onsite generated power as to sell it back to power companies.

Panasonic’s booth included its latest high-efficiency ‘HIT’ branded modules for the residential market boasting conversion efficiencies as high as 19.3%. They are also branded ‘P&S’, or ‘push and slide’, which means the modules can be easily snapped into place on rooftop installations. Streamlining labour costs and installation times have been a key area where improvements have been cited as needed in Japan’s market.

While residential rooftop PV is still be-ing installed on a feed-in tariff basis for the most part in Japan, Panasonic was marketing inverter solutions for house-holds that are ‘battery-ready’, so that when economics dictate, system owners will be able to simply add lithium-ion batteries to their existing PV systems. Panasonic as well as Sharp was also sell-

ing so-called ‘hybrid’ inverters, which incorporate solar PV inverters and bat-tery inverters into one package.

Also of interest on the Panasonic stand was a new set of square modules for the commercial market, specifically designed to be placed in narrow spaces on flat roofs at high altitude, including the many skyscrapers that dominate the skylines of Tokyo and other major Japa-nese cities. The modules are capable of withstanding strong winds and are considered suitable even for buildings more than 200 metres tall.

Zero Energy Houses and Zero Energy BuildingsJapan has introduced new Zero Energy House (ZEH) and Zero Energy Building (ZEB) standards. While last year industry sources at the show had expressed a belief that ZEH would be mandatory for all new houses built by 2020, it appears the government has scaled back its ambitions on receiving feedback from housebuilders. Instead there is a target that by that year 50% of new dwellings and new commercial buildings will be net zero energy, which still represents a sizeable opportunity in a country which builds close to one million new houses a year.

In addition to the big three profiled, many companies were presenting kits and solutions for ZEH, incorporating heating and insulation, PV and energy storage. Perhaps the most sophisti-cated looking was Sharp’s (pictured). Companies like Panasonic, Sharp and Toshiba, which are involved in a number of different business areas related to electronics already have many of the necessary technologies within their production and marketing capabilities and the focus on ZEH and ZEB seemed a natural fit.

Sharp business strategy manager Hideo Miki said that from his company’s point of view it was important to make ZEH kits that were not just capable of gener-ating more power than they consumed in nominal terms, but also by using bat-teries making practical good use of that generated power.

Miki said that while there are some incentives available from the govern-ment for ZEH, the support scheme seems somewhat complex and requires homeowners to present evidence of the house being net zero energy before funds can be received. Sharp has also launched its own range of batteries for houses in several configurations with up to 6.5kWh of storage available in the basic models.

Toshiba’s latest ranges of products for the rooftop market included a pro-totype solar roofing tile, which while more conspicuous than Tesla-SolarCity’s much-hyped solar shingles, still ap-peared to fit neatly into rows of normal roofing tiles. Unfortunately as the tiles were not yet available to buy, Toshiba representatives also demanded that PV Tech refrain from photographing them, so we cannot show them to you.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

Sharp's Zero Energy House solution, utilising the company's own-brand 'Blacksolar' high-efficiency modules.

Imag

e: A

ndy

Col

thor

pe.

24

JAPAN

Japan to lower tariffs, cancel projects after paying ¥2.3tr last year for FiTsJapan is set to lower its levels of feed-in tariff (FiT) payments once again, while a multi-gigawatt pipeline of unbuilt large-scale PV projects will be “cancelled” at the beginning of April.

On the opening day of World Smart Energy Week, incorporating the PV Expo show in Tokyo, Toshimitsu Fujiki, a director at Japan’s government Ministry of Economy, Trade and Industry (METI), confirmed that a “new FiT system” will be in effect from the beginning of the new financial year, 1 April.

While Fujiki did not allude to how much would now be payable for the power generated at various scales, drops of 10% and 11% have not been uncommon in the past couple of years, with the average FiT payment currently standing at around ¥21 (US$0.19)/kWh. Japan’s renewable energy FiT has primarily fostered solar development rather than other forms of generation such as wind and biomass and Fujiki said that in 2016, the Japanese government paid out ¥2.3 trillion in tariffs.

“There are great possibilities [for renew-able energy] but we must reduce costs,” Fujiki said, referencing recent tenders in Abu Dhabi that secured project development at just US$0.03/kWh as an example of what might be achieved.

METI will hold briefing seminars around Japan in order to educate and discuss with stakeholders how to introduce more renewables into the energy mix while reducing the taxpayer burden. The METI official said repeatedly that one important aspect of this was the concept of “local production and lo-cal consumption”. This could refer to self-consumption of PV, particularly in non-grid connected systems, as well as local consumption of PV. Fujiki ruled out

the prospect of widespread build-out of more transmission lines to carry the power, emphasising the “local” dimen-sion of the idea.

“We have to think of better ways to utilise existing [transmission] lines. We have to study this,” Fujiki said, add-ing that METI was likely to create new agencies to support self-consumption policies and sector coupling.

Confirmation of tenders and cancellation of unbuilt projectsSome 57GW of large-scale PV projects were registered for the FiT in the first two or three years of the scheme’s introduction after 2012, with would-be developers taking advantage of rela-tively relaxed rules on what constituted a project’s planning documents.

PV-Tech has reported extensively on this ‘pipeline’, with many non-PV firms jumping into the industry and putting

forward plans to build facilities. In some cases it has been suspected that after taking the rights to build solar farms at FiT rates of as much as ¥42 per kilowatt, developers have intentionally waited for equipment prices to keep dropping to maximise their profits.

Following much speculation on the fate of these several dozen gigawatts of projects, Fujiki of METI confirmed today in a keynote address at the expo’s conference that as of 1 April, projects unbuilt or without concrete plans to go ahead in place will lose their rights to the FiT and will be cancelled. In the most recent edition of PV Tech Power, Solar Media’s technical journal for the downstream solar industry, Japanese industry analyst Dr Hiroshi Matsukawa of research group RTS PV estimated that as much as half to two-thirds of that 57GW pipeline is likely to be axed.

Fujiki also confirmed that as part of the

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

Imag

e: A

ndy

Col

thor

pe.

The opening ceremony for PV Expo in Tokyo this morning. An estimated 70,000 people attend the whole World Smart Energy Week event, which also includes expos on fuel cells, batteries and other technologies.

25

JAPAN

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

ongoing streamlining of renewable en-ergy policy, Japan will introduce tenders and auctions for PV projects over 2MW in size as of this year. RTS’ Matsukawa also said in that PV Tech Power article that he believed these would be annual auctions of 500MW at a time.

Energy efficiency, Zero Energy Homes, hydrogen and negawattsFujiki’s keynote address focused also on energy efficiency measures in Japan, stating that huge strides have been taken in improving energy efficiency in factories and service industries, with Japan’s economy still reliant on heavy industries such as chemical processing and steel.

Of immediate interest to the PV industry is the increasing focus on residential energy efficiency, most notably in the creation of Zero Energy Home (ZEH) standards. These net-zero energy houses would as a matter of course in-clude PV and energy storage as well as double-glazed windows and other forms of insulation.

Fujiki said many housebuilders had de-scribed ZEH as a difficult goal to attain, but he said it was “critical” that such steps were taken, with the government expected to make all new homes net-zero energy dwellings by 2020.

Also being put forward are “negawatt trading schemes”, including demand re-

sponse and the aggregation of distrib-uted energy resources into virtual power plants (VPPs), which Fujiki said detailed regulations have been in the process of drafting at METI since last October.

Finally, Japan is also betting big on hydrogen fuel cells, with the country’s car manufacturers being the world’s first to produce commercial hydrogen vehicles including Toyota’s Mirai, with several hundred miles’ fuel range. Only 92 hydrogen refuelling stations so far are in operation in Japan, but they have already become commercialised, Fujiki said. In addition, over 170,000 hydrogen fuel cells for households were installed last year at private residences in Japan, Fujiki said.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

26

PHILIPPINES

Philippines hits 903MW of solar PV under RE law, ground-breaking on 150MW plantThe Philippines had 903MW of installed solar PV capacity under its Renewable Energy Law at the end of 2016, accord-ing to Department of Energy (DOE) figures.

The majority of this (900MW) was grid-connected, with the rest (3.2MW) in the self-consumption category. The figures do not include 55 renewable energy-based projects installed under different laws.

Overall a total of 150 grid-connected projects and 16 self-consumption projects have been awarded, with a total potential capacity of nearly 4,082MW.

Nearly 95MW PV due to start operation in Philippines in MarchThe Philippines is also expected to bring 94.2MW of solar PV projects into com-mercial operation this month, according to more DOE figures.

Of the three principal geographical divi-sions of the Philippines, Mindanao will not see any projects commissioned although it does have 338MW of projects going through feasibility studies or at various stages of development.

Project developers with capacities ex-pected to reach commercial operation in the division of Visayas include:• Cosmo Solar Energy - 5.67MW• SunAsia Energy - 60MW

Visayas has 465MW of projects under consideration or at various stages of development.

Meanwhile, expected additions at the division of Luzon include:• Next Generation Power Technology -

18MW• CW Marketing & Development -

1.675MW• SPARC Solar Powered Agri-Rural Com-

munities - 3.82MW• SPARC Solar Power Agri-Rural Commu-

nities - 5.02MW

Luzon has 1,179MW of projects under consideration or at various stages of development.

The DOE has also released figures show-ing that as of 31 December 2016, there were 201 solar energy projects, totalling nearly 2,131MW, which have pending ap-plications across the three divisions.

Solar Philippines breaks ground on 150MW PV plant in TalacIn related news, Filipino renewable energy firm Solar Philippines has started construction on a 150MW PV plant in at Concepcion, Tarlac, in the Philippines, ac-cording to another release from the DOE.

The project will use locally sourced mod-ules and is set to power the equivalent of 300,000 households once completed by

the end of 2017.

At the ground-breaking ceremony, energy secretary Alfonso Cusi said: “Currently, the country’s power demand is at 13,000MW and our supply is barely 14,000MW, hence we need more power as well as reserve power.”

The release suggests that energy storage will be installed alongside the plant, but no further details were given and the firm has not responded to requests.

Cusi added: “Solar power plants with reliable storage capability can be most useful in island countries like the Philip-pines.”

In an interview with PV Tech, Pete Maniego, senior policy adviser of the Institute for Climate & Sustainable Cities and of Counsel of Dime & Eviota Law, has discussed the need for price-based competition in the Philippines.

Cre

dit:

Con

erg

y

The Philippines is also expected to bring 94.2MW of solar PV projects into commercial operation this month.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

27

MALAYSIA

Edra plans to develop 50MW solar project in MalaysiaIndependent power producer Edra is planning to develop a new 50MW solar project in the Malaysian state of Kedah, according to the Malaysian state news agency, Bernama.

The project, which Edra plans to develop by early 2018, would be led by Edra’s wholly-owned unit, Edra Solar.

Datuk Mark Ling, president and executive director of Edra Power, said: “The Kedah solar plant is expected to generate ap-proximately 80,000 MWh of electricity per year and would be developed over 104 hectares at Bandar Kuala Ketil in Baling, Kedah.”

Project Kedah Solar would stand as the first of many utility-scale solar PV power plants with an aggregate capacity of up to 500MW to be developed by Edra pursuant to the conditional award from the Ministry of Energy, Green Technology and Water.

Edra Solar Entered into a land sales and purchase (SPA) agreement in August 2015 with BDB Land Sdn Bhd, a subsid-iary of Bina Darulaman Bhd (BDB) for the

acquisition of the land that the project will be developed on. Edra plans to create skilled jobs for Malaysians through Project Kedah Solar during the construction, operations and maintenance phases of the project — with engineers, operational

and management team comprised mostly of a local staff.

Once completed, the PV project is ex-pected to cut down on 36,000 tonnes of carbon emissions per year.

Imag

e: R

ober

t Sco

ble

/ F

lickr

The 50MW PV project would generate 80,000 MWh of electricity per year.

Malaysia to auction 460MW of large-scale solar PVThe Energy Commission of Malaysia (EC) has issued a Request for Proposla (RfP) document hoping to auction up to 460MWac of large-scale solar capacity.

Under EC’s second competitive bidding programme, it hopes to awards projects of 1-30MW capacity to make up a total of 360MW in Peninsular Malaysia and

100MW in Sabah and Labuan in the East.

All solar plants will be connected to the grid, with power purchase agreements to be signed with the main utilities Tenaga Nasional Berhad (TNB) or Sabah Electric-ity Sdn. Bhd. (SESB).

The RfP document was made available

last week and the deadline for submis-sions is 1 August 2017.

Last November PV Tech caught up with Catherine Ridu, chief executive officer of the Malaysia Sustainable Development Authority (SEDA) to discuss the policies needed to drive solar in the Southeast Asian country.

28

MALAYSIA

ENGIE enters partnership to develop solar in MalaysiaFrench energy group ENGIE has signed a partnership agreement with Sime Darby, a Malaysian multinational for the co-development of solar and integrated facilities management services.

Malaysia is one of France’s major eco-nomic partners in Southeast Asia.

“We are pleased to form this strategic partnership with Sime Darby, a most respected and successful multinational corporation with a strong local foothold. Our aligned vision on sustainability and performance offers many opportunities to combine our strengths to positively impact the lives of our many stakehold-ers,” said Didier Holleaux, executive vice president of ENGIE.

ENGIE and Sime Darby will be provid-ing low-cost solar PV, aiding Malaysia in its renewable energy goals. The country has a target to procure 2GW of clean energy by 2020 – 10% of its overall

energy mix, 3.5GW by 2030 (13%) and 11.5GW by 2050 (34%).

“Our partnership will pave the way for greater collaboration in the solar and integrated facilities management space. With a combination of technical exper-tise and a deep understanding of the Malaysian market, we believe this part-

nership will enable us to significantly expand into these sectors,” said Tan Sri Data Mohd Bakke Salleh, president and group chief executive of Sime Darby.

In other ENGIE news, the company an-nounced earlier this month that it has issued its second green bond, worth approximately US$1.6 billion

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

Sour

ce: E

NG

IE G

roup

(From left to right) Sime Darby’s Tan Sri Samsudin Osman, Scott Cameron, Malaysia’s Minister of Internation-al Trade and Industry Dato’ Sri Mustapa Mohamed, President of France Francois Hollande, Executive Vice President of ENGIE Didier Holleaux, Chairman of ENGIE Gérard Mestrallet.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

29

PAKISTAN

Pakistan to adopt competitive bidding for new solar PV projectsPakistan is set to adopt competitive bidding for new solar PV projects, ac-cording to an order published by the National Electric Power Regulatory Authority (NEPRA).

Since June last year the Authority has been gathering views from stakeholders on whether to shift towards a competitive bidding methodology, hoping to move on from the previous policy of upfront tariffs for solar, of which there have been three to date.

A total of eight organisations intervened on the proposals. Most believed a sudden change in policy to reverse bidding would hinder investment in the sector, given that the country is in the midst of a PV development cycle. Such bidding should only be brought in once the current cycle is over, they said. Another argument was that creating the framework for competi-tive auctions would take substantial time, while interveners also pointed to several global examples of countries reverting back from auctions after they damaged the market.

NEPRA has now rejected these argu-ments, citing central government support for the adoption of competitive auctions for renewable energy in general.

In its order, NEPRA stated: “The Author-ity feels that the procurement of power under transparent competitive process is most appropriate as it can fetch realistic

prices based on the prevailing conditions of the market. It has also been observed that competitive bidding mode has been the most successful and preferred mode for arriving at fair and judicious prices and after announcing three upfront tariffs for solar PV technology, this is the appropri-ate time for a logical shift towards [a] competitive regime.”

The authority also noted consistently im-proving efficiencies and declining prices for PV equipment over recent years, a trend expected to continue for some

time. For this reason, it has also decided to adopt the auction model without a benchmark levelized tariff.

To carry out tenders, relevant agencies will prepare Request for Proposal docu-ments for approval by NEPRA. State-run utility National Transmission and Despatch Company (NTDC) will offtake power from auctioned projects.

NEPRA has recommended the Federal Government to notify its decision in the official Gazette.

Flic

kr: N

icol

as R

aym

on

Eight organisations intervened on the proposals but NEPRA has gone ahead with competitive bidding for solar.

4-5 JULY 2017Singapore

financeasia.solarenergyevents.com

30

PAKISTAN

Canada MoU with Pakistani province for 1GW of solarA Canadian government entity has signed a memorandum of understand-ing (MoU) with the government of Pakistani province Khyber Pakhtunkh-wa (KP) to cooperate on up to 1GW of solar energy projects in the region.

The Canadian Commercial Corporation (CCC) will help facilitate private compa-nies to come in and contract with the KP government to set up renewable energy projects, a source at the trade depart-ment at the High Commission of Canada in Pakistan told PV Tech.

Location, project numbers and sizes have not been specified in the three-year MoU.

Discussing the purpose of the agreement, the source said: “The primary reason is that Pakistan is an energy deficient country. Because of that, they introduced policies which are attractive to foreign in-vestors and foreign companies that want to invest in renewable energy.”

He also cited “attractive” upfront tariffs as a reason for various companies from