spring 2014 corporate presentation mark thompson chief executive officer

TRANSCRIPT

Spring 2014Corporate Presentation

Mark Thompson Chief Executive Officer

2

Disclaimer

Certain information in this presentation and oral statements made during this meeting are forward-looking and relate to Concordia’s anticipated financial position, business strategy, events and courses of action. Words or phrases such as “anticipate,” “objective,” “may,” “will,” “might,” “should,” “could,” “can,” “intend,” “expect,” “believe,” “estimate,” “predict,” “potential,” “plan,” “is designed to” or similar expressions suggest future outcomes. Forward-looking statements include, among other things, statements about: our expectations regarding our expenses, sales and operations; our future customer concentration; our anticipated cash needs and our estimates regarding our capital requirements and our need for additional financing; our ability to anticipate the future needs of our customers; our ability to achieve new design wins; our plans for future products and enhancements of existing products; our future growth strategy and growth rate; our future intellectual property; and our anticipated trends and challenges in the markets in which we operate. Such statements reflect our current views with respect to future events and are based on assumptions and subject to significant risks and uncertainties. Although we believe that the assumptions underlying these statements are reasonable, they may prove to be incorrect. Given these risks, uncertainties and assumptions, you should not place undue reliance on these forward-looking statements. Our actual results, performance or achievements could differ materially from those contemplated, expressed or implied in our statements as a result of various risk factors, including, but not limited to, business, economic and capital market conditions; market conditions and the demand and pricing for our products; our relationships with our customers, distributors and business partners; our ability to successfully define, design and release new products in a timely manner that meet our customers’ needs; our ability to attract, retain and motivate qualified personnel; competition in our industry; our ability to maintain technological leadership; our manufacturing supply chain, including pricing of goods and availability of adequate manufacturing capacity from our manufacturing suppliers; our ability to transition to new wafer fabrication process technologies and achieve higher levels of design integration; our ability to manage risks inherent in foreign operations; our ability to successfully maintain and enforce our intellectual property rights and defend third-party claims of infringement of their intellectual property rights; our ability to manage cash flow, foreign exchange risk and working capital; our ability to manage our growth; fluctuation in our quarterly operating results; and our dependence on key personnel. Except as required by law, we undertake no obligation to update or revise publicly any forward‑looking statements, whether as a result of new information, future events or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. Neither we nor any of our representatives make any representation or warranty, express or implied, as to the accuracy, sufficiency or completeness of the information in this presentation. Neither we nor any of our representatives shall have any liability whatsoever, under contract, tort, trust or otherwise, to you or any person resulting from the use of the information in this presentation by you or any of your representatives or for omissions from the information in this presentation. T his presentation also contains statistical data, estimates and forecasts that are based on independent industry publications or other publicly available information, while other information is based on Concordia’s internal sources. Although Concordia believes that these third-party sources referred to in this presentation are reliable, Concordia has not independently verified the information provided by these third parties. While Concordia is not aware of any misstatements regarding any third-party information presented in this presentation, their estimates, in particular, as they relate to projections, involve numerous assumptions, are subject to risks and uncertainties, and are subject to change based on various factors, including the risk factors discussed above.

Non-IFRS Measures This presentation makes reference to certain non-IFRS measures. These non-IFRS measures are not recognized measures under IFRS and do not have a standardized meaning prescribed by IFRS, and are therefore unlikely to be comparable to similar measures presented by other companies. When used, these measures are defined in such terms as to allow the reconciliation to the closest IFRS measure. These measures are provided as additional information to complement those IFRS measures by providing further understanding of the Company’s results of operations from management’s perspective. Accordingly, they should not be considered in isolation nor as a substitute for analyses of the Company’s financial information reported under IFRS. Management uses non-IFRS measures such as EBITDA and Adjusted EBITDA to provide investors with a supplemental measure of the Company’s operating performance and thus highlight trends in the Company’s core business that may not otherwise be apparent when relying solely on IFRS financial measures. Management also believes that securities analysts, investors and other interested parties frequently use non-IFRS measures in the evaluation of issuers. Management also uses non-IFRS measures in order to facilitate operating performance comparisons from period to period, prepare annual operating budgets, and to assess its ability to meet future debt service, capital expenditure, and working capital requirements.

1EBITDAAs used herein, EBITDA is defined as net income adjusted for net interest expense, income tax expense, depreciation and amortization. Management uses EBITDA to assess the Company’s operating performance. A reconciliation of net income to EBITDA is provided below.

2ADJUSTED EBITDAAs used herein, adjusted EBITDA is defined as EBITDA adjusted for one-time charges associated with acquisitions, one-time charges associated with the Company’s listing on the TSX, non-cash items such as unrealized gains / losses on derivative instruments, and realized / unrealized gains/losses related to foreign exchange revaluation. Management uses adjusted EBITDA as a key metric in assessing business performance when comparing actual results to budgets and forecasts. Management believes adjusted EBITDA is an important measure of operating performance and cash flow, and provides useful information to investors because it highlights trends in the underlying business that may not otherwise be apparent when relying solely on IFRS measures.

3

Executive Experience

Mark Thompson Founder, CEO & Director

Biovail Corporation (currently Valeant): VP Business Development and Associate General Counsel Trimel Pharmaceuticals: Co-Founder Tribute Pharmaceuticals: Co-Founder Lawyer at Oslers and Davies Completed over $2.0 billion in transactions

Leith TessyCFO

25 years of international experience as a finance and operations executive LG-Nortel (JV between Nortel Networks & LG Electronics): CFO and COO Nortel Networks: CFO of Carrier Networks Division Nuance Communications: SVP, Finance

Wayne KreppnerCOO

15 years of global experience in pharmaceutical R&D, Manufacturing and Operations Trimel Pharmaceuticals: Vice President, Product Development Biovail Corporation: Vice President of Technology Transfer Executive experience in Product Registration and Quality

John McCleeryMD and CFO of Concordia Barbados

30 years of international experience as a senior financial and operational executive Trimel BioPharma: VP, General Manager, CFO Biovail Laboratories International (currently Valeant Laboratories International): VP and General

Manager Biovail Corporation (currently Valeant): developed and managed enterprise risk management and

compliance

Robert AltmanPresident, Pinnacle Biologics

25 years of pharmaceuticals operations experience Pinnacle Biologics: Chief Commercial Officer Marathon Pharmaceuticals: Founder and CEO Astellas Pharma: Senior Vice-President Abbott Laboratories: Vice-President, General Manager, Pharmaceutical Product Division

Management Team

4

Concordia’s Strategy

Orphan Drugs1) Specialized regulatory protection

2) Limited competition

3) Pricing power

4) Too small for big pharma

Funding

Distribution Control

Specialty Healthcare Distribution1) Niche distribution

2) Cash flow from diabetic product distribution

Legacy Drugs1) Strong cash flow

2) Limited sales and marketing expenses

3) Attractive acquisition metrics

4) Sold directly to wholesalers

Concordia is a specialty pharmaceutical company focused on legacy and orphan pharmaceutical products

5

ConcordiaHealthcare Corp.

Parent Co. – Canada

Concordia Pharmaceuticals

Legacy Drugs – Barbados

Pinnacle Biologics

Orphan Drugs – US

Complete Medical Homecare

Specialty Distribution – US

Owner of Legacy Drugs and IP

Sells Products into U.S. Directs development for new

indications Supply chain management

Development and Sales of Orphan Drugs

Distribution of diabetic products

Fully licensed pharmacy

Distribution capabilities across the U.S.

Concordia Overview

6

Attention Deficit Hyperactivity Disorder (ADHD)

Asthma and severe allergic conditions

Head lice infestation (prescription)

Irritable Bowel Syndrome (IBS)

Product Portfolio

Legacy Drugs

Medical Equipment &Other Healthcare Products

Distribution of diabetic products

Licensed pharmacy

Specialty distribution capabilities across the U.S.

Specialty Healthcare Distribution (Complete Medical Homecare)

Photodynamic Therapy with Photofrin®

Approved legacy drug treatment for three rare forms of cancer

Upside from potential new orphan drug indications – CCA and Meso

To be sold via Concordia’s specialty healthcare distribution arm

Pinnacle Biologics

Product Description

7

Donnatal ®

70-year history of safety, excellent brand equity All competitors removed from market during 2012-

13, market exclusivity expected for foreseeable future

Promotional activities instituted in 2012, ramping through 2014-15

2013 revenue of US$49.1 mm and EBITDA of US$40.2 mm

Promotio

n Initiated

Generic Withdraw

alBegan

Promotion

Escalated

8

Photodynamic Therapy: Overview

Non-thermallaser light

Tissueuptake

and clearance

Photosensitizing Agent(IV Administration)

Relatively SelectiveRetention in Tumor

Tumor Tissue Destruction

ResidentOxygen

9

Cholangiocarcinoma – U.S. Phase III Registration Study

Prospective, open label, randomized, multicenter study

Design is consistent with Ortner ME et al.*

SPA approved by FDA 200 patients; 2 arms (stent + chemo versus stent +

PDT with Photofrin + chemo) Only 1 registration trial needed Interim analysis at 45 events

First patient expected: Q2 2014

*Gastroenterology. 2003 November; 125(5): 1355-63.

10

Successful Swiss Clinical Trial

Randomized Prospectus Study

70 patients: 39 randomized; 31 excluded/nonrandomized (open PDT)

Stenting & PDT

Stenting Alone

Open PDT

Patients 20 19 31

Primary endpoint:Survival 493 days 98 days 426 days

P-value P < 0.0001 P < 0.0001

PDT significantly improves survival in patients with NCC

Study stopped early due to impressive results

Severely ill patients eligible for PDT

11

25% Palliative

U.S. Cholangiocarcinoma Market Estimate

Incid

ence

of

Cholan

gioca

rcino

ma

Less

Intra

hepa

tic C

holan

gioca

rcino

ma

Patien

ts w

ith

no J

aund

ice (5

%)

Patien

ts U

nder

going

Res

ectio

n

Resec

ted

patie

nt fa

cing

recu

rrent

, obs

truct

ive tu

mor

s

Photo

frin

Targe

ts

4,380

1,756 1,756 2,0692,640

627 314

1,740

132

125

Source: SEER data, Physician Interviews; Cerenti analysis.

Photofrin Market Potential – Cholangiocarcinoma Patients

Non-Resectable

Extrahepatic & Hilar

Cholangiocarcinoma

(60%)

(5% Curative)5%

12.5%

47%

40%

Dosage : 2 mg/Kg per treatment Approximately 2 vials/patient /treatment at $19K

per vial On average 2 to 5 treatments per patient

12

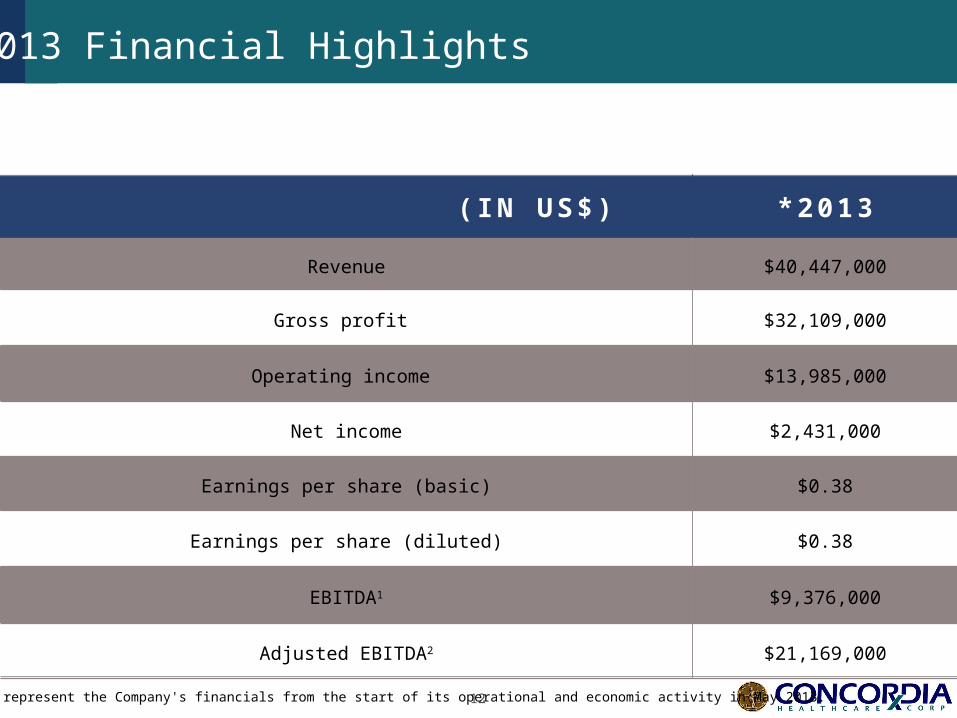

( IN US$) *2013

Revenue $40,447,000

Gross profit $32,109,000

Operating income $13,985,000

Net income $2,431,000

Earnings per share (basic) $0.38

Earnings per share (diluted) $0.38

EBITDA1 $9,376,000

Adjusted EBITDA2 $21,169,000

2013 Financial Highlights

* 2013 results represent the Company's financials from the start of its operational and economic activity in May 2013.

13

( IN US$) Q1 2014

Revenue $16,810,000

Gross profit $12,956,000

Operating income $4,939,000

Net loss ($1,836,000)

Earnings per share basic ($0.09)

Earnings per share diluted ($0.09)

EBITDA1 $3,546,000

Adjusted EBITDA2 $5,903,000

First Quarter, 2014 Financial Highlights

14

*Cap Structure

Ticker TSX: CXR, OTC QX: CHEHF

Common shares outstanding 28.5 mm

Recent share price $35.64

Market capitalization (Cdn) $1,013 mm

52 week High/Low $35.64/$7.60

**Average Daily Volume 217,981

Analyst Coverage Beacon Securities, Cormark Securities, GMP Securities,

TD Securities

Shareholders AEGON Capital Management, Fidelity, Fiera Capital, Janus Capital Management, Pyramis Global Advisors,

Visium

Mgmt and Board ownership Approximately 25%

*as of June 9, 2014**Jan.1, 2014- May, 20 2014

Spring 2014Corporate Presentation

Mark Thompson Chief Executive Officer