state of the canadian oilfield services industry and 2015 outlook webinar

TRANSCRIPT

Presented by:

Date:

David Yager, National Leader Oilfield Services

February 2015

Strategies Produced for

Today and Tomorrow

State of the Canadian Oilfield

Services Industry and 2015

Outlook

Rig photos courtesy of Beaver Drilling Ltd.

Page 3

Program

1. About MNP.

2. What is Oilfield Services?

3. Where have we been?

4. Where are we going?

5. How should a client manage

its company in a challenging

market environment.

Page 4

OUR PEOPLE

The MNP Advantage:

• Fifth largest tax, accounting and business advisory services firm in Canada.

• Offices in strategic locations throughout all the major producing areas of the Western Canadian Sedimentary Basin.

• Experience with over 5,500 oilfield services clients.

• Over 150 dedicated OFS professionals.

• Member of the major OFS industry associations.

• Only professional services firm with an on-hands industry specialist.

• Corporate restructuring specialists in all major Canadian centres.

• Alberta based corporate recovery specialists experienced in the major Alberta industries.

Page 5

OUR PEOPLE

“Think Global, Act Local”

• Over 75 offices from Montreal to Vancouver Island.

• Member of Praxity Global Alliance of Independent Firms giving us

worldwide presence.

• We have specialists located in the areas necessary to meet the local

needs of our OFS clients.

Page 6

Where We Operate

Western Canadian

Sedimentary Basin

We work where you work

Page 7

1 - What is Oilfield Service?

E&P company seeks to

develop an oil or gas

reservoir

Delivery of oil or gas to refinery

terminal or pipeline access

facility

1. Exploration

2. Engineering & Consulting

3. Construction

4. Transportation

5. Drilling & Service Rigs

6. Wellhead Services

7. Downhole Tools

8. Equipment Rentals

9. Equipment Supply

10.Logistics

11.Fabrication & Manufacturing

12.Production

All the products and

services an oil company

does not supply itself

Page 8

1 Exploration

2 Engineering

3 Construction

4 Transportation

5 Drilling & Service Rigs

6 Wellhead Services7 Downhole Tools

8 Equipment Rentals

9 Equipment Supply

10 Logistics

11 Fabrication,

Manufacturing

12 Production

OILFIELD SERVICES

Major subsectors in

the Exploration &

Production process

from early stage

investment to

commercial

development

MNP Oilfield Services Subsectors Through

Oil and Gas Development Investment Cycle

Page 9

Sources of Revenue for OFS

WHERE DO PRODUCERS GET THEIR MONEY

• Cashflow from oil and gas production sales (net of operating expenses)

• E&P capital inflows (debt, equity)

WHERE DO OFS COMPANIES GETS THEIR MONEY

• E&P Capital Expenditures (CAPEX)

• E&P operating costs

• Service sector CAPEX

Page 10

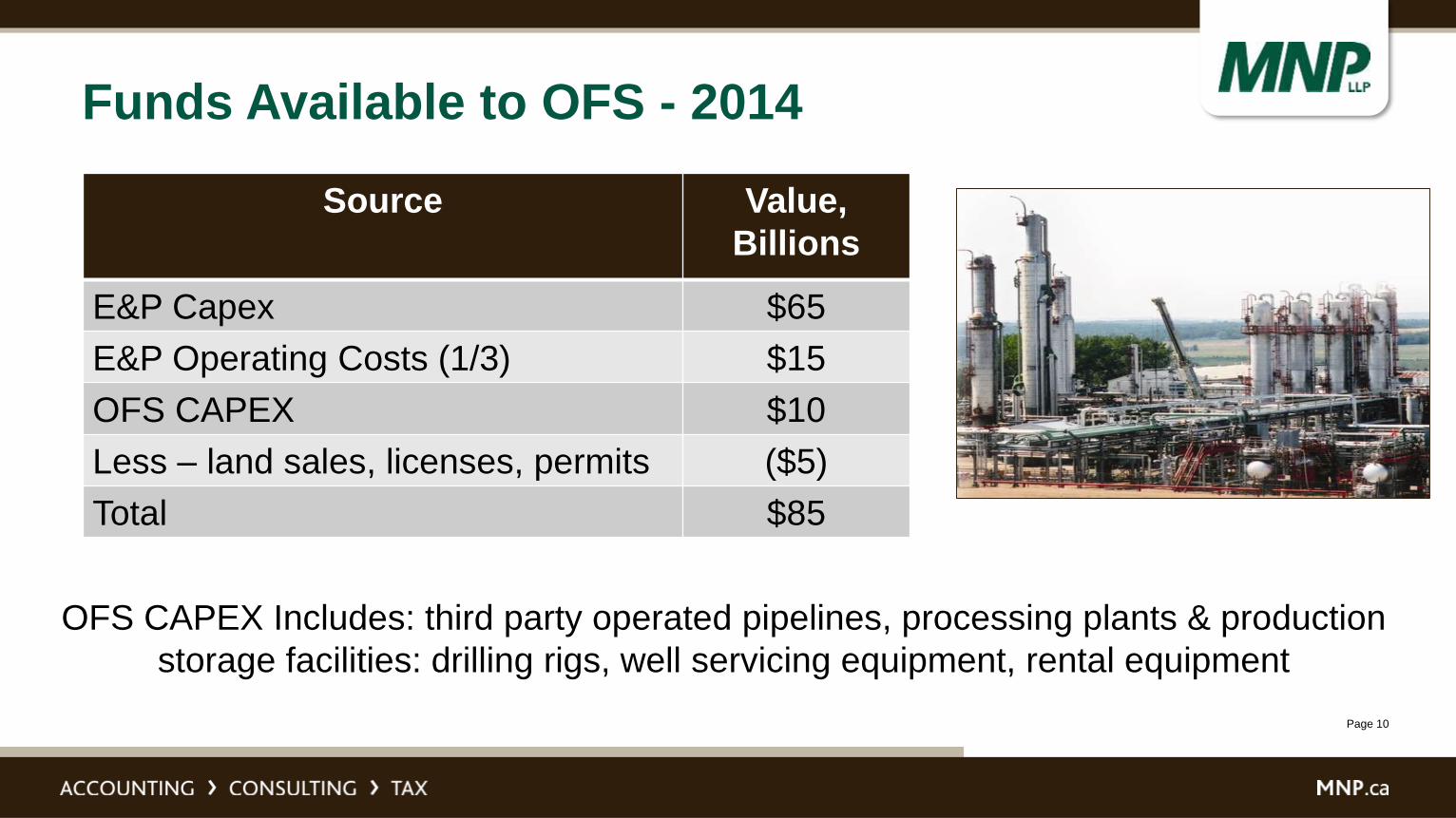

Funds Available to OFS - 2014

Source Value,

Billions

E&P Capex $65

E&P Operating Costs (1/3) $15

OFS CAPEX $10

Less – land sales, licenses, permits ($5)

Total $85

OFS CAPEX Includes: third party operated pipelines, processing plants & production

storage facilities: drilling rigs, well servicing equipment, rental equipment

Page 11

2 – Where Have We Been?

• Summary of upstream oil industry

macro-economic drivers

–Production

–Revenue and cashflow

–Capital expenditures – conventional

and oilsands

–The gas boom

–The oilsands boom

–Upstream operating expenditures –

conventional and oilsands

Page 12

Production Volumes

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

20

11

2012

2013

2014

Oil/Liquids

Bitumen

Gas

Total

SOURCE: ARC Financial

Millions of Barrels of Oil or Natural Gas Liquids

Millions of Barrels of Oil Equivalent of Gas (@ 6:1) Per Day

Page 13

Revenue/Cashflow 1998 - 2015

$0.0

$20.0

$40.0

$60.0

$80.0

$100.0

$120.0

$140.0

$160.0

1998

1999

2000

20

01

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Billions of $ Cdn – (Estimates 2014 & 2015)

SOURCE: ARC Financial Jan 27/15

Record Year

Page 14

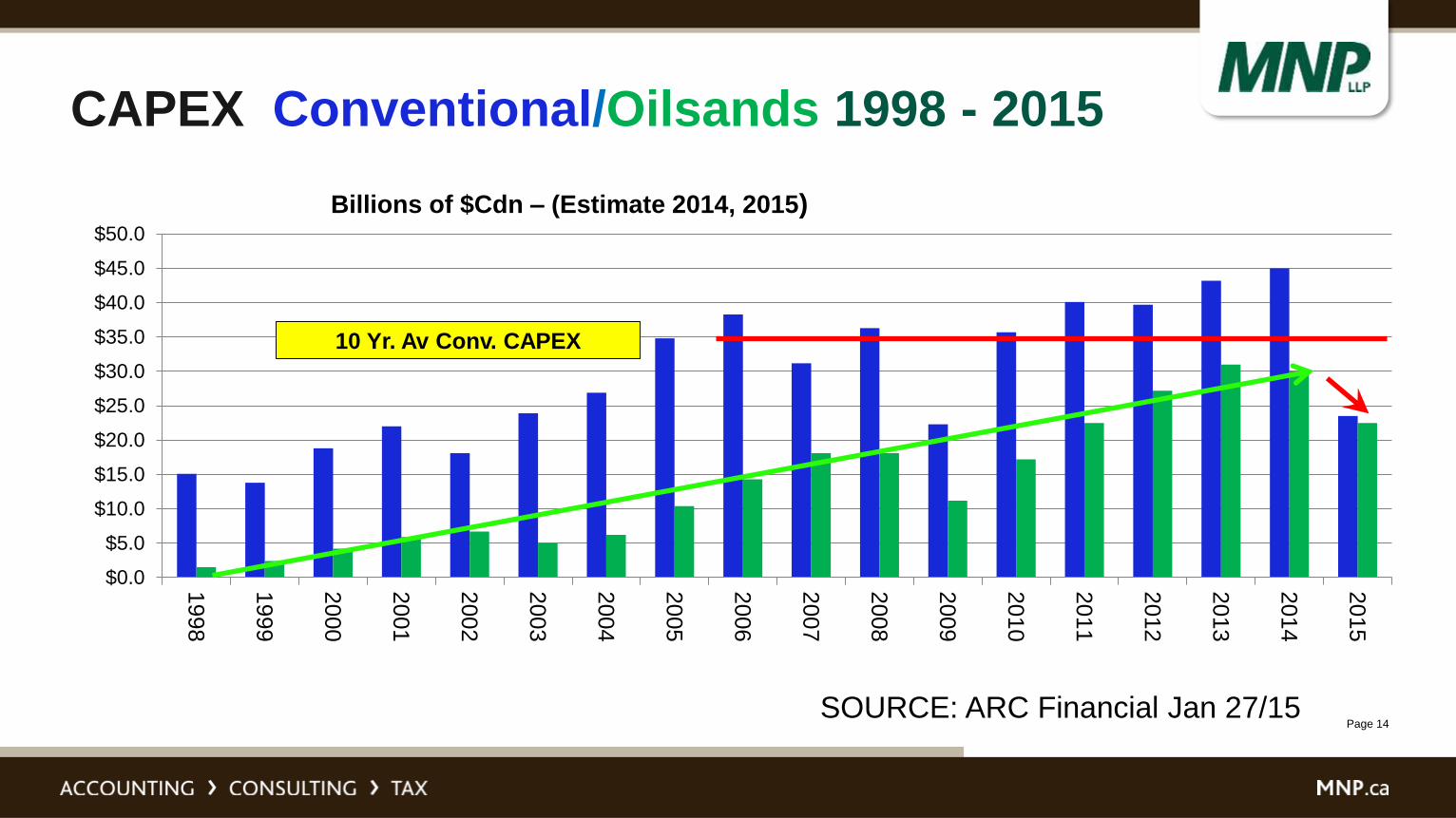

CAPEX Conventional/Oilsands 1998 - 2015

$0.0

$5.0

$10.0

$15.0

$20.0

$25.0

$30.0

$35.0

$40.0

$45.0

$50.0

1998

1999

2000

20

01

2002

2003

2004

20

05

2006

2007

2008

2009

2010

2011

2012

2013

2014

2015

Billions of $Cdn – (Estimate 2014, 2015)

SOURCE: ARC Financial Jan 27/15

10 Yr. Av Conv. CAPEX

Page 15

$0

$10

$20

$30

$40

$50

$60

199

1

199

2

199

3

199

4

19

95

199

6

199

7

199

8

199

9

200

0

200

1

200

2

200

3

20

04

200

5

200

6

200

7

200

8

200

9

201

0

201

1

201

2

20

13

201

4

Production

Value

SOURCE: CAPP, ARC

YAHOO!

The Gas Boom – 2000 to 2008

Billions of dollars of revenue

Billions of cubic feet per day

Page 16

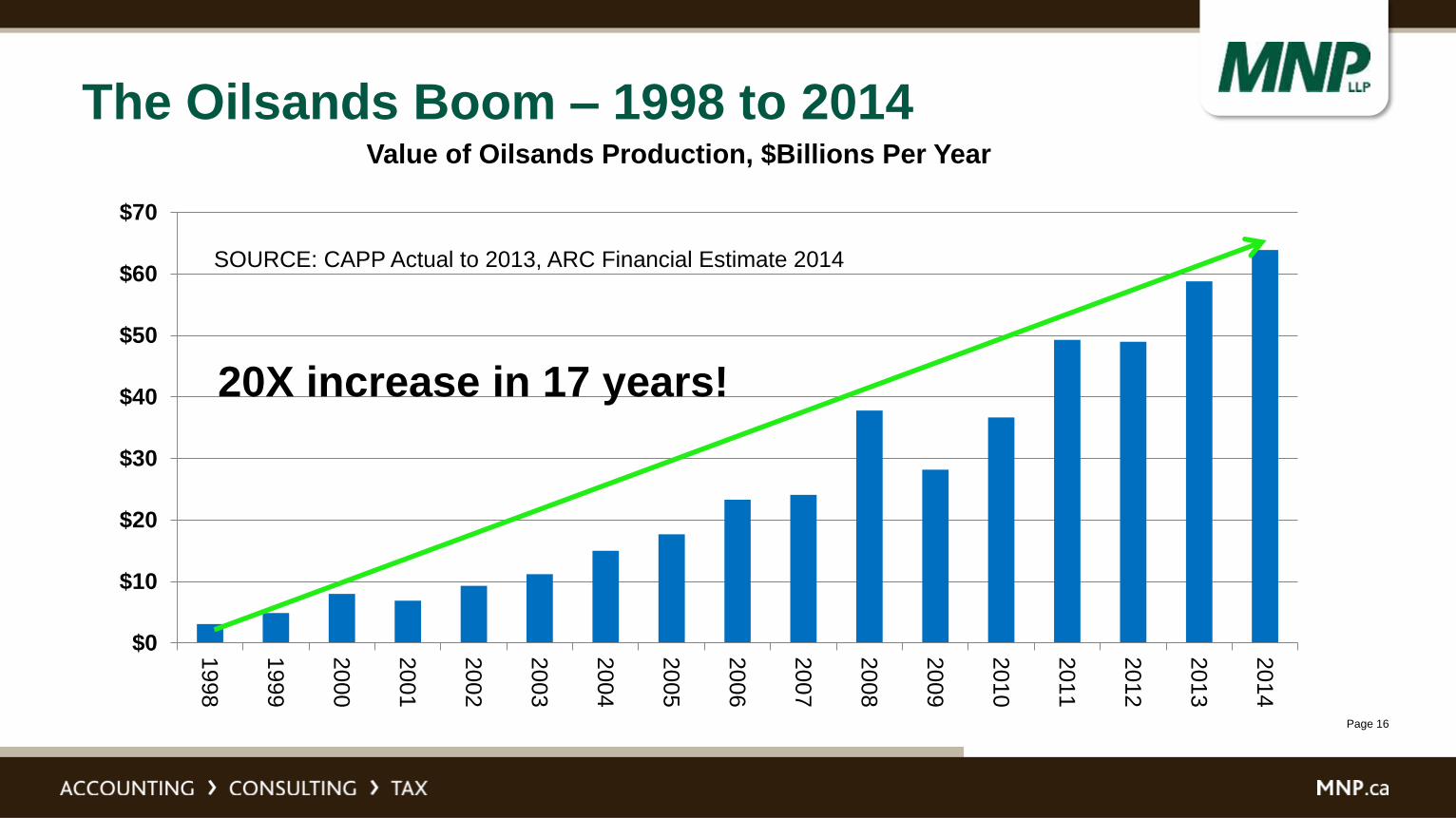

The Oilsands Boom – 1998 to 2014

$0

$10

$20

$30

$40

$50

$60

$70

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

20

14

Value of Oilsands Production, $Billions Per Year

20X increase in 17 years!

SOURCE: CAPP Actual to 2013, ARC Financial Estimate 2014

Page 17

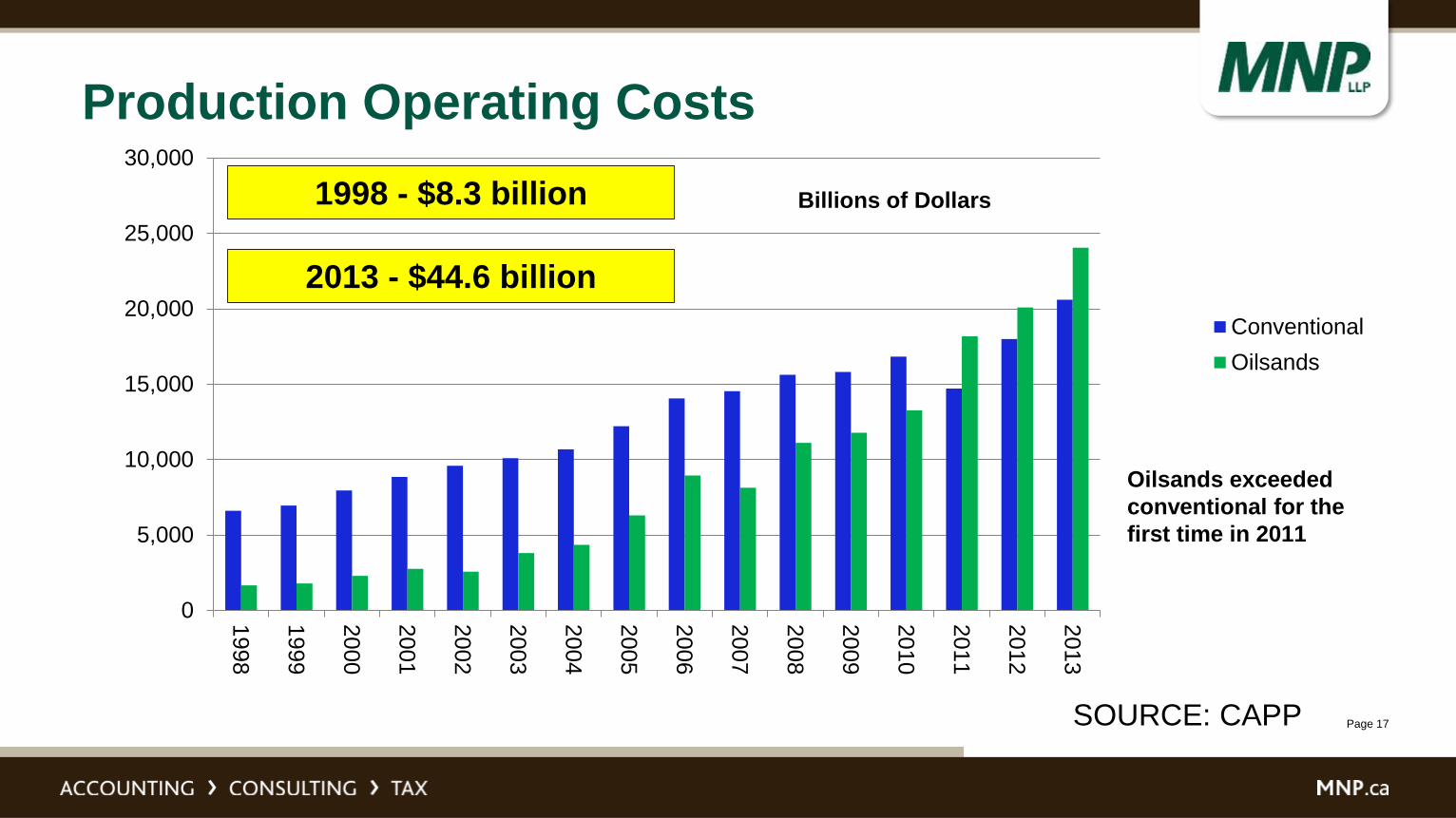

Production Operating Costs

0

5,000

10,000

15,000

20,000

25,000

30,000

1998

1999

20

00

2001

2002

2003

2004

2005

2006

2007

2008

2009

2010

2011

2012

2013

Conventional

Oilsands

Billions of Dollars

Oilsands exceeded

conventional for the

first time in 2011

SOURCE: CAPP

1998 - $8.3 billion

2013 - $44.6 billion

Page 18

0.0%

20.0%

40.0%

60.0%

80.0%

100.0%

120.0%

140.0%

160.0%

1998

1999

2000

2001

2002

2003

2004

2005

2006

2007

20

08

2009

20

10

2011

2012

2013

2014

2015

Equity/Debt Inflows

Oil Price Collapses

Royalty Trust Era

Oil hits $147/bbl

Reinvestment Ratio: CAPEX/After-Tax Cashflow

(Estimates 2014, 2015)

SOURCE: ARC Financial Jan 20/15

Page 19

3 - Where Are We Going?

• Oil prices – recent versus current

• Gas prices – recent versus current

• Current oil and gas pricing environment

• PSAC drilling forecast – wells

• PSAC drilling forecast – meters drilled

• PSAC drilling forecast – rig operating days

• CAPEX – CAPP

• CAPEX – Peters & Company & Woods Mackenzie

• Outlook by sector – MNP classification system

• Winners and losers by service line

• Three major positive outlook drivers

• How it looks today – major revenue contraction

Page 20

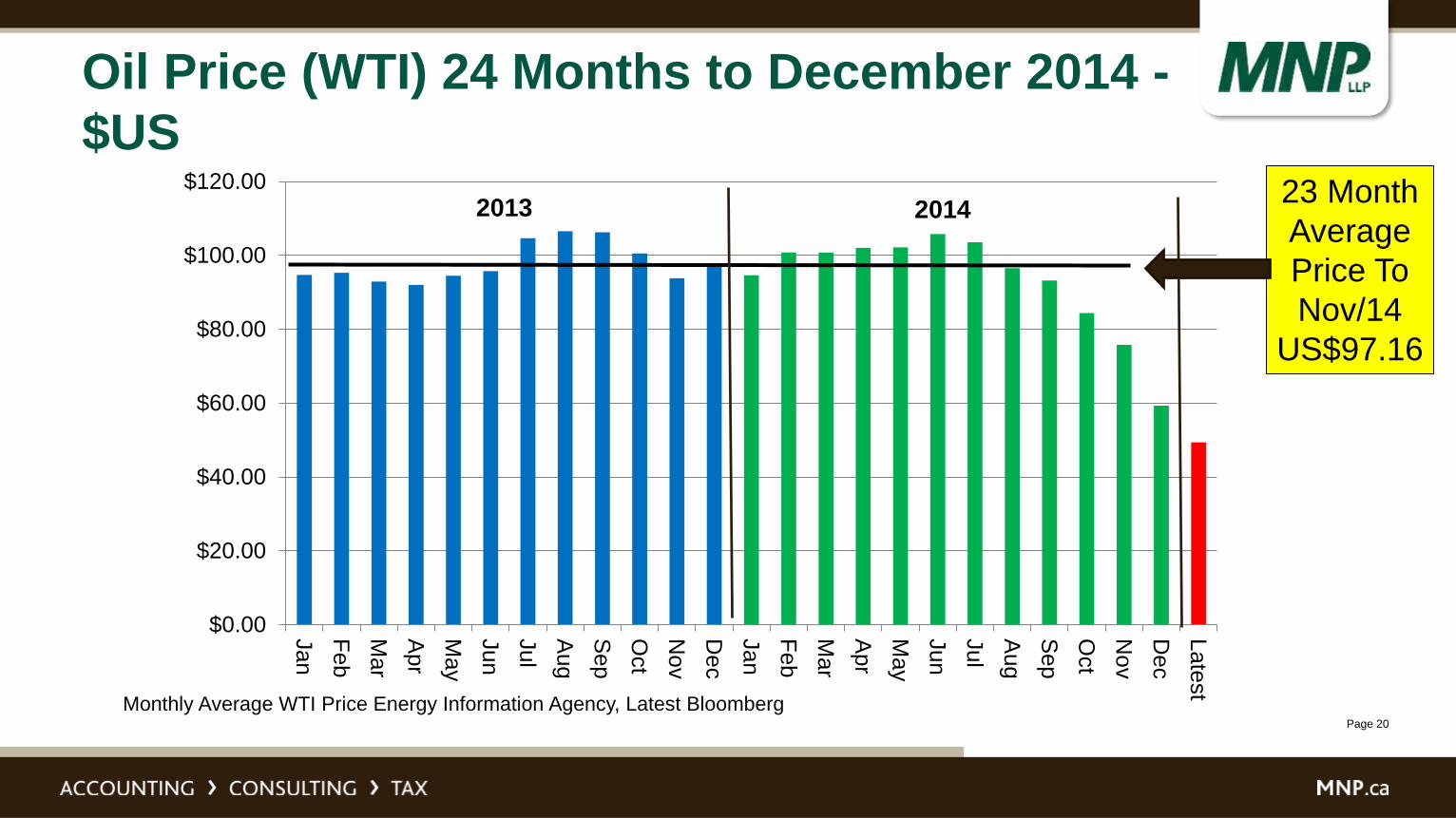

Oil Price (WTI) 24 Months to December 2014 -

$US

$0.00

$20.00

$40.00

$60.00

$80.00

$100.00

$120.00

Jan

Feb

Mar

Ap

r

May

Ju

n

Jul

Au

g

Se

p

Oct

No

v

De

c

Jan

Feb

Mar

Ap

r

May

Jun

Jul

Au

g

Se

p

Oct

No

v

De

c

La

test

20142013

Monthly Average WTI Price Energy Information Agency, Latest Bloomberg

23 Month

Average

Price To

Nov/14

US$97.16

Page 21

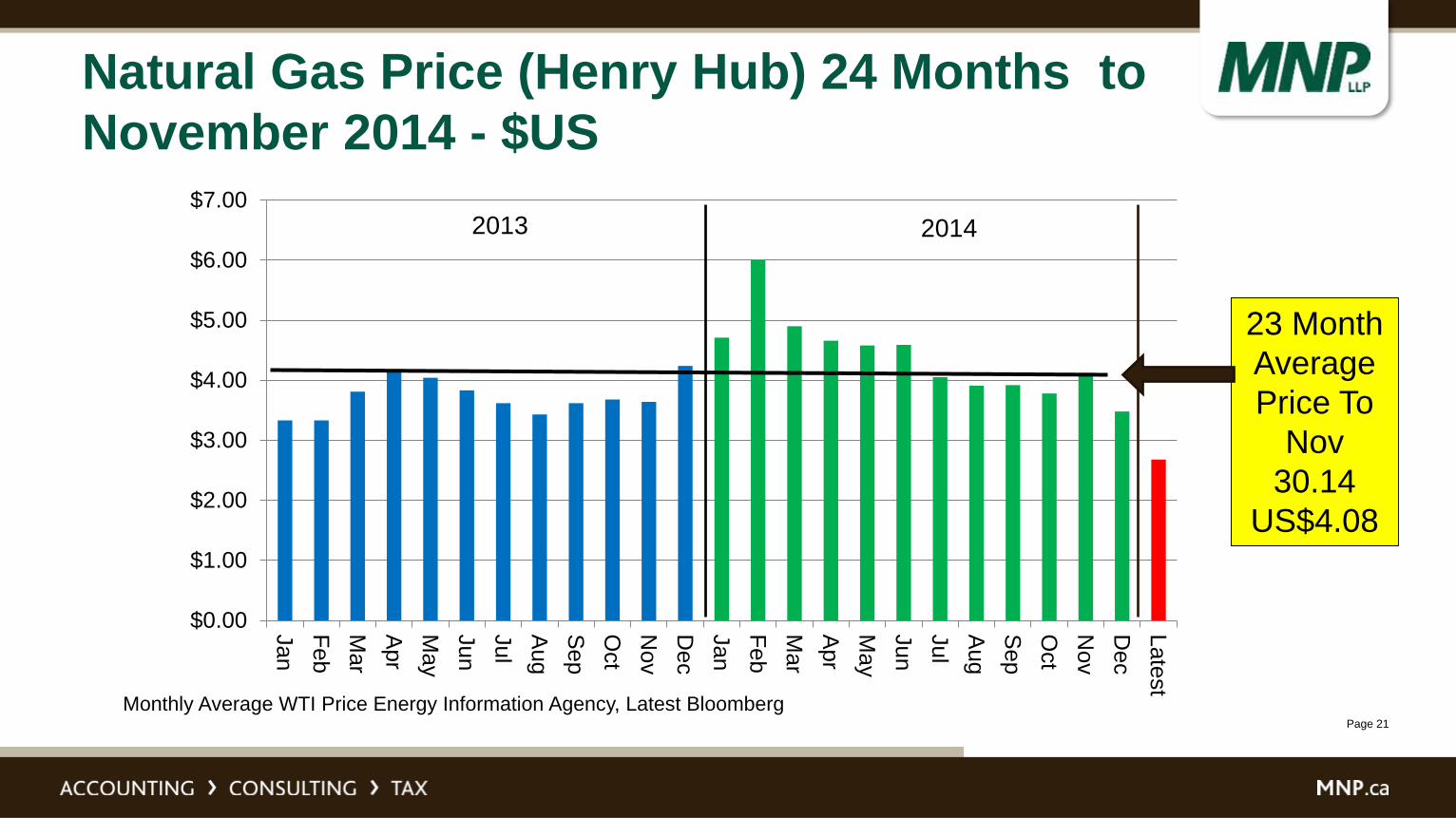

Natural Gas Price (Henry Hub) 24 Months to

November 2014 - $US

$0.00

$1.00

$2.00

$3.00

$4.00

$5.00

$6.00

$7.00

Jan

Fe

b

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Jan

Feb

Mar

Apr

May

Jun

Jul

Aug

Sep

Oct

Nov

Dec

Late

st

2013 2014

23 Month

Average

Price To

Nov

30.14

US$4.08

Monthly Average WTI Price Energy Information Agency, Latest Bloomberg

Page 22

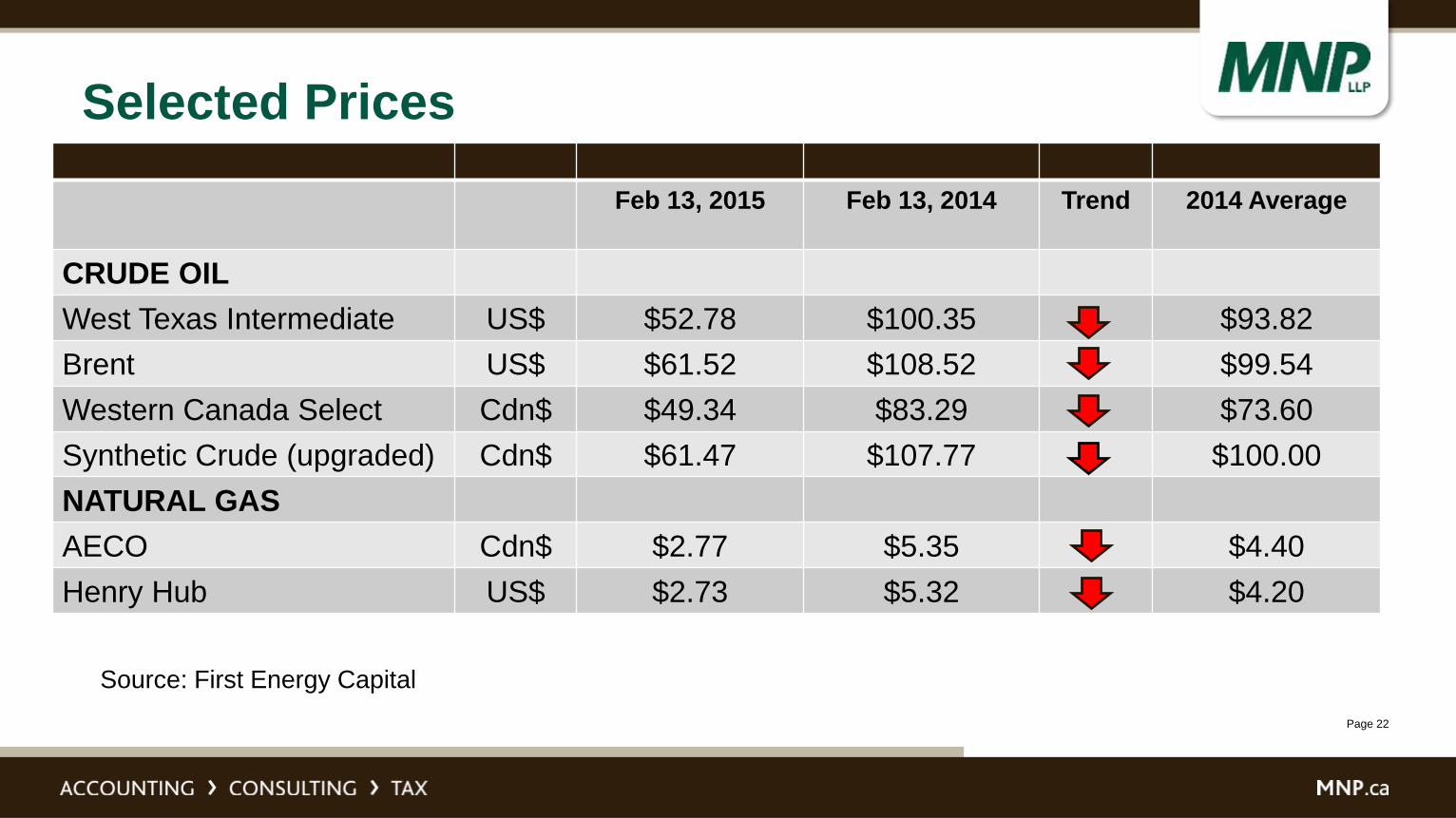

Selected Prices

Feb 13, 2015 Feb 13, 2014 Trend 2014 Average

CRUDE OIL

West Texas Intermediate US$ $52.78 $100.35 $93.82

Brent US$ $61.52 $108.52 $99.54

Western Canada Select Cdn$ $49.34 $83.29 $73.60

Synthetic Crude (upgraded) Cdn$ $61.47 $107.77 $100.00

NATURAL GAS

AECO Cdn$ $2.77 $5.35 $4.40

Henry Hub US$ $2.73 $5.32 $4.20

Source: First Energy Capital

Page 23

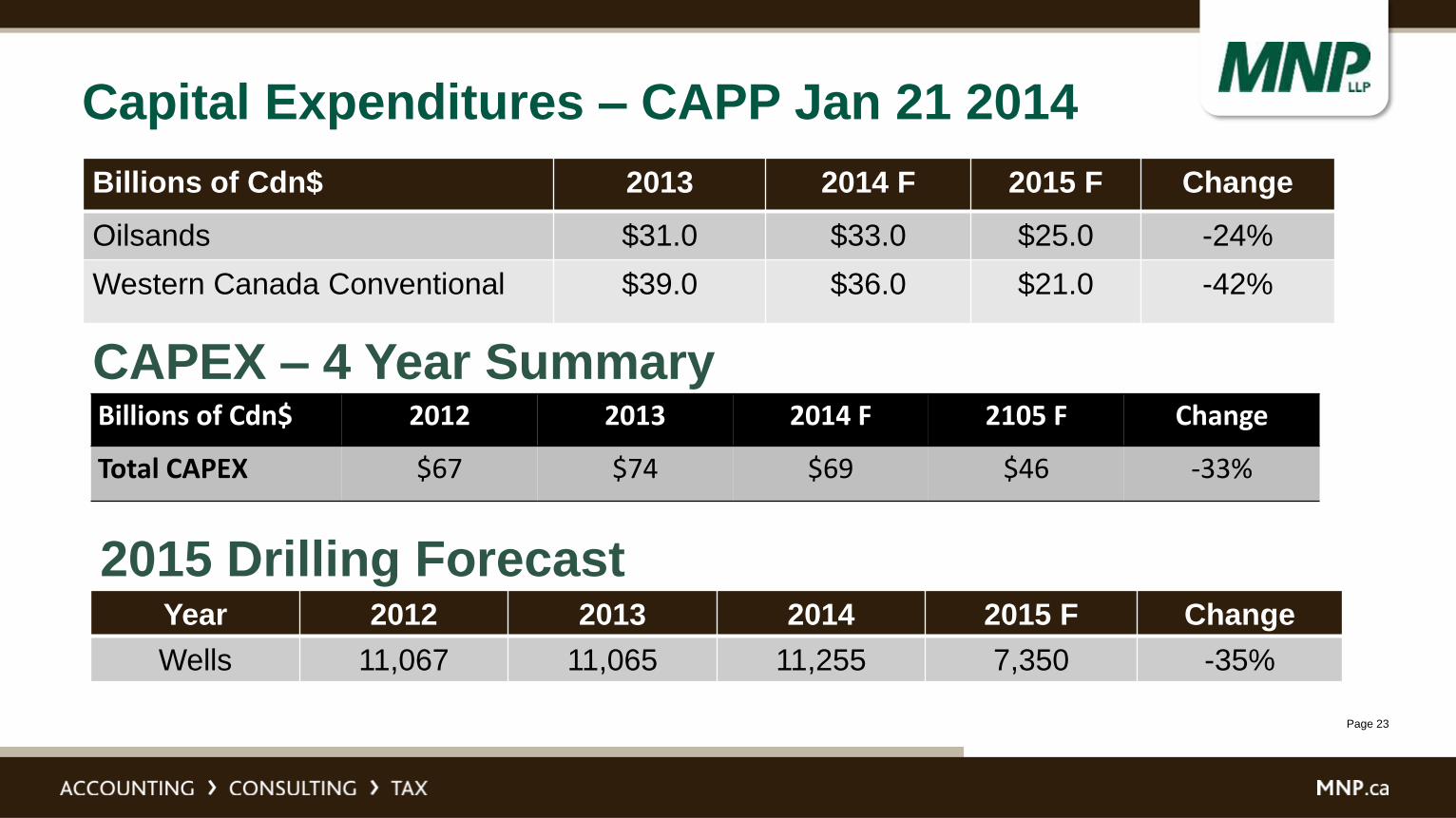

Capital Expenditures – CAPP Jan 21 2014

Billions of Cdn$ 2013 2014 F 2015 F Change

Oilsands $31.0 $33.0 $25.0 -24%

Western Canada Conventional $39.0 $36.0 $21.0 -42%

Billions of Cdn$ 2012 2013 2014 F 2105 F Change

Total CAPEX $67 $74 $69 $46 -33%

CAPEX – 4 Year Summary

Year 2012 2013 2014 2015 F Change

Wells 11,067 11,065 11,255 7,350 -35%

2015 Drilling Forecast

Page 24

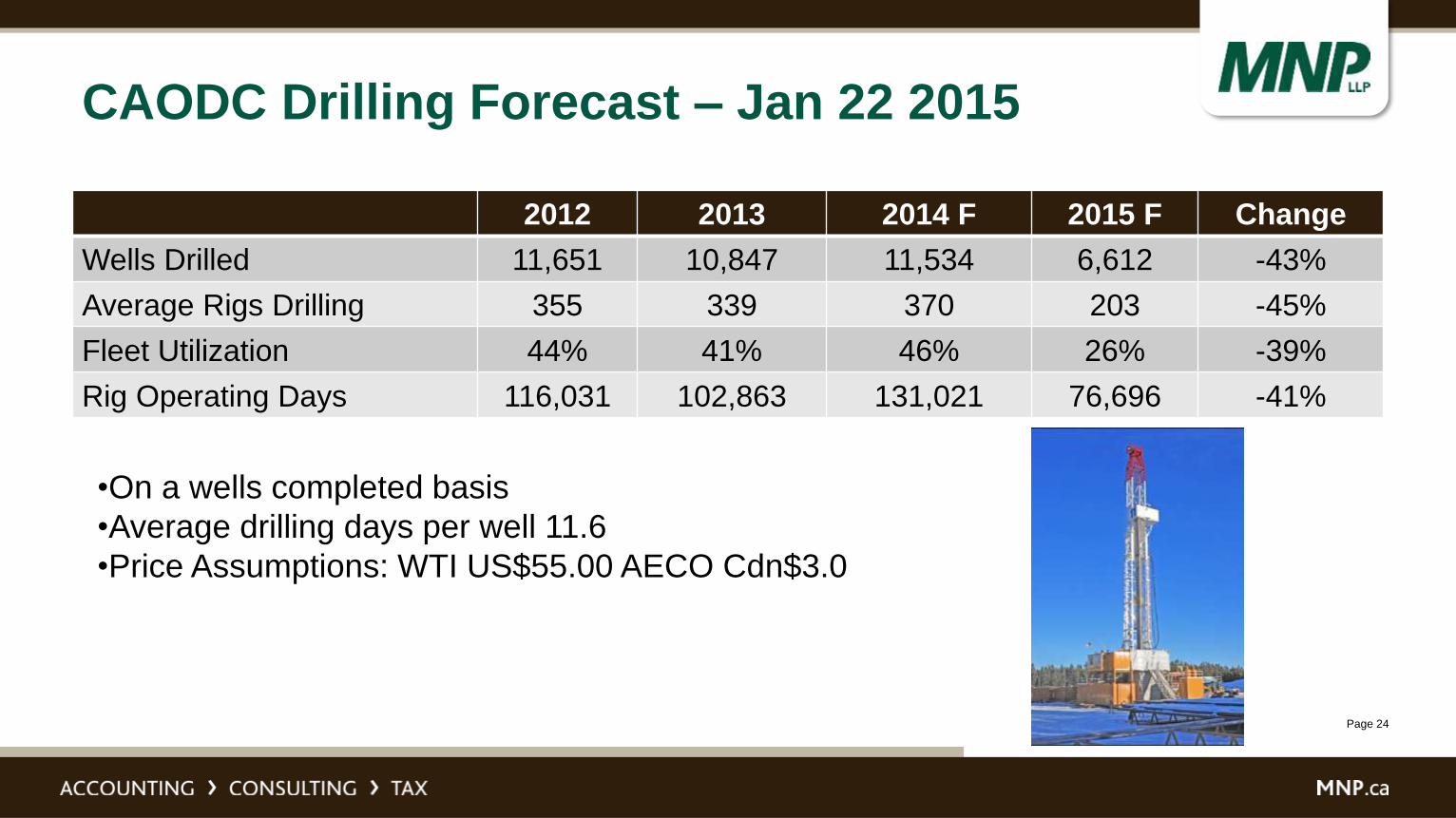

CAODC Drilling Forecast – Jan 22 2015

2012 2013 2014 F 2015 F Change

Wells Drilled 11,651 10,847 11,534 6,612 -43%

Average Rigs Drilling 355 339 370 203 -45%

Fleet Utilization 44% 41% 46% 26% -39%

Rig Operating Days 116,031 102,863 131,021 76,696 -41%

•On a wells completed basis

•Average drilling days per well 11.6

•Price Assumptions: WTI US$55.00 AECO Cdn$3.0

Page 25

2015 Trends By MNP Sector

Exploration Downhole Tools

Engineering & Consulting Equipment Rentals

Construction Supply

Transportation Logistics

Drilling & Service Rigs Manufacturing & Fabrication

Wellbore Services Production

Page 26

Rebound By Sector

OFS Activity Sector Outlook

Production Services – keep the cash

flowing

Continuing, pricing main challenge

Facilities & Pipelines – processing plants

and gathering systems

Expanding with production volume, pricing

pressure main problem

Shale Oil Drilling Down for now but first to recover with oil

prices

Oilsands sustaining CAPEX Ongoing because of harsh operating

conditions, pricing main challenge

Oilsands growth CAPEX Winding down as construction finishes, no

new projects, no recovery imminent

Page 27

Major Positive Potential Changes

• LNG Project Announced – B.C. tax

changes in place: will somebody

commit?

• Keystone XL Approval – will

Republicans overpower President

Obama?

• Supply/Demand Balance Oil Price

Recovery in mid-2015 – lower prices

drive demand, lower prices reduce

North American shale oil output

Page 28

How It Looks Today

• Producer cashflow in 2015 forecast to fall by

50%, all E&P CAPEX budgets reduced

• Overall reduction in demand for goods and

services with the exception of production

infrastructure

• Pricing pressure will follow

• Capital markets have contracted

• Over-leverage (too much debt) will be difficult

to manage

• The 2011 – 2014 business plan will not work in

2015

Page 29

2015 Drilling Starts Slowly

Date Active Drilling Rigs Change

February 10, 2015 359 -43%

February 11, 2014 632 -1%

February 12, 2013 624

Source: June-Warren Nickles Rig Locator Feb 10, 2015

Page 30

U.S. Oil Drilling Rig Count Declining

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

Feb

14/1

5

Feb

6/1

5

Jan 3

0/1

5

Jan 2

3/1

5

Jan 1

6/1

5

Jan 9

/15

Jan 2

/15

De

c 2

6/1

4

De

c 1

9/1

4

De

c 1

2/1

4

De

c 5

/14

No

v 2

6/1

4

No

v 2

1/1

4

No

v 1

4/1

4

No

v 7

/14

Oct 31

/14

Oct 24

/14

Oct 17

/14

Oct 10

/14

Oct 3/1

4

Sep 2

6/1

4

Sep 1

9/1

4

Sep 1

2/1

4

Sep 5

/14

Aug 2

9/1

4

Aug 2

2/1

4

Aug 1

5/1

4

Aug 8

/14

Aug 1

/14

Jul 25/1

4

Jul 18/1

4

Jul 11/1

4

July

3/1

4

Rigs Drilling For Oil in the United States, Baker Hughes July 3, 2014 - February 13, 2015

Down 35% from October 2014 peak

Page 31

4 – What Should Clients Do?

• Understand where they make

their money

• Understand operational

considerations

• Have a cash management system

• Have financial flexibility

• Have a risk management system

Page 32

Does Clients Know Where They Make (or

Lose) Money?

• Pricing, job costs, and field margins

• Variable expenses versus fixed

expenses – do they know what they

are?

• Do they have monthly internal

financial reports per station, division,

product line so they can detect

problems?

• Are they paying too much tax in

Canada or internationally?

Page 33

Operations Considerations

• Do our clients understand

the implications of a more

challenging business

environment?

• Is everyone in the

company going in the

same direction?

• Are they using the lowest

cost suppliers and vendors

(without compromising

quality)?

Page 34

Collections

• Do they undertake credit checks on

their customers?

• Do they get their field tickets signed

and processed to the invoice stage

in a timely manner?

• Does their operations team know a)

how important this is and b) the best

practices for faster payment

• Do they know what late payments

cost?

Page 35

Financial Flexibility

• Are they employing the cheapest

possible sources of capital?

• Do they have the financial reports

necessary to secure lower cost

capital?

• If they wanted to sell, buy or merge

with a competitor, do they have the

financial information required to

actually do a deal?

Page 36

Risk Management

• Are they taking on excessive credit risk in the event of a significant

downturn?

• Are they experiencing “leakage”? Are tools going out the back door?

Is all the fuel going into company vehicles?

Page 37

CONTACTS

Oilfield Services LeaderDavid Yager

Direct: 403 461 8566

Corporate Recovery

CalgaryVictor Kroeger Verne Wood

Direct: 403 298 8479 Direct: 403 537 1621

[email protected] [email protected]

EdmontonEric Sirrs

Direct: 780 969 1491