steelmint indian steel weekly report as on 27 june 11

TRANSCRIPT

8/6/2019 SteelMint Indian Steel Weekly Report as on 27 June 11

http://slidepdf.com/reader/full/steelmint-indian-steel-weekly-report-as-on-27-june-11 1/4

1

www.steelmint.com

Weekly Highlights

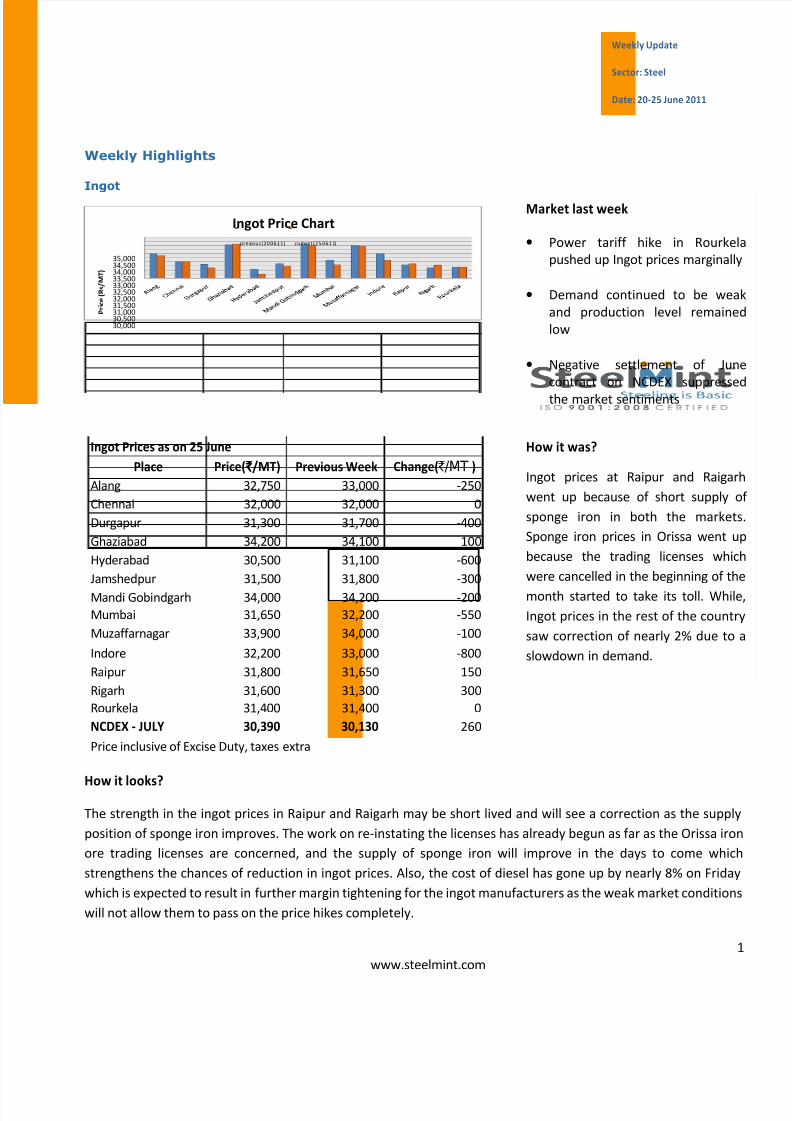

Ingot

30,00030,50031,00031,50032,00032,50033,00033,50034,00034,50035,000

P r i c e ( R s / M T )

Ingot Price Chart

previous (20.06.11) current (25.06.11)

Place Price(`̀̀̀/MT) Previous Week Change(`/MT )

Alang 32,750 33,000 -250

Chennai 32,000 32,000 0

Durgapur 31,300 31,700 -400

Ghaziabad 34,200 34,100 100

Hyderabad 30,500 31,100 -600

Jamshedpur 31,500 31,800 -300

Mandi Gobindgarh 34,000 34,200 -200

Mumbai 31,650 32,200 -550

Muzaffarnagar 33,900 34,000 -100

Indore 32,200 33,000 -800

Raipur 31,800 31,650 150

Rigarh 31,600 31,300 300

Rourkela 31,400 31,400 0

NCDEX - JULY 30,390 30,130 260

Ingot Prices as on 25 June

Price inclusive of Excise Duty, taxes extra

How it looks?

The strength in the ingot prices in Raipur and Raigarh may be short lived and will see a correction as the supply

position of sponge iron improves. The work on re-instating the licenses has already begun as far as the Orissa iron

ore trading licenses are concerned, and the supply of sponge iron will improve in the days to come which

strengthens the chances of reduction in ingot prices. Also, the cost of diesel has gone up by nearly 8% on Friday

which is expected to result in further margin tightening for the ingot manufacturers as the weak market conditions

will not allow them to pass on the price hikes completely.

Weekly Update

Sector: Steel

Date: 20-25 June 2011

Market last week

• Power tariff hike in Rourkel

pushed up Ingot prices marginally

• Demand continued to be wea

and production level remained

low

• Negative settlement of Jun

contract on NCDEX suppresse

the market sentiments

How it was?

Ingot prices at Raipur and Raigarh

went up because of short supply o

sponge iron in both the markets

Sponge iron prices in Orissa went u

because the trading licenses whic

were cancelled in the beginning of the

month started to take its toll. While

Ingot prices in the rest of the country

saw correction of nearly 2% due to

slowdown in demand.

8/6/2019 SteelMint Indian Steel Weekly Report as on 27 June 11

http://slidepdf.com/reader/full/steelmint-indian-steel-weekly-report-as-on-27-june-11 2/4

2

www.steelmint.com

Scrap

15,000

20,000

25,000

30,000

P r i c e ( R

s / M T )

Scrap Price Chart

previous (20.06.11) current (25.06.11)

Place Price( `̀̀̀/MT) Previous Week Change (in ` )

Alang 22,900 23,150 -250

Chennai 24,500 24,500 0

Goa 23,000 23,500 -500

Hyderabad 24,000 24,000 0

Indore 23,000 24,100 -1100

Jamshedpur 24,500 24,500 0

Mandi Gobindgarh 26,500 26,500 0

Mumbai 24,000 24,000 0Raipur 25,200 25,300 -100

Excise Duty & taxes extra as applicable

HMS Scrap Prices as on 25 June

How it looks?

Currently, imported scrap is available at a lower rate which is expected to keep prices of domestic scrap in chec

Due to monsoons ahead, Ingot manufacturers may also keep production low and thus may not build their stock f

scrap.

Further, increase in diesel prices will make transportation dearer too, resulting in low margins for scrap trad

(anyone holding stock) and thus limiting chances for a price rise.

Market last week

• Advent of monsoons pulled down

scrap prices at few mandis’

•

Cheap Imported scrap affected thedomestic scrap price in Mumbai

Local scarp was offered at R

24,000/MT

• Imported Scrap prices went down

by $10; now offered at $465

470/MT in the internationa

Market (Turkey)

How it was?

It was a steady week for steel scr

market. Domestic Scrap pric

remained unchanged at most of t

mandis’. Steel manufacturers are no

keeping their production low due

monsoon season which has also ke

the prices in check.

Indore market remained the wo

performing market where pric

corrected by Rs 1,100/MT.

8/6/2019 SteelMint Indian Steel Weekly Report as on 27 June 11

http://slidepdf.com/reader/full/steelmint-indian-steel-weekly-report-as-on-27-june-11 3/4

3

www.steelmint.com

TMT

30,000

32,00034,000

36,000

38,00040,000

P r i c e ( R

s / M T )

TMT Price Chart

previous (20.06.11) current (25.06.11)

Place Price(`̀̀̀/MT) Previous Week Change (in ` )

Chennai 37,300 37,000 300

Durgapur 36,400 37,000 -600

Hyderabad 34,200 34,700 -500

Indore 37,800 39,300 -1500

Jamshedpur 37,000 37,000 0

Mumbai 36,300 36,400 -100

Nagpur 37,400 37,500 -100

Raipur 34,850 34,850 0

TMT (12MM) Prices as on 25 June

Price inclusive of Excise Duty, taxes as applicable

How it looks?

Activity in the market remains low as buyers have held their purchases. Prices will only pick up once demand for

finished products improves. Domestic steel prices are unlikely to go up in the coming days due to a possible

correction in raw material costs and lower production figures. The outlook for the market is not very encouraging

and is expected to remain dismal during monsoons. To an extent, it will depend on how monsoon turns out.

Market last week

• Re-bar prices moved down sharply

at major mandis’.

• Construction activities slowdown amonsoon arrives earlier

• Interest rates and fuel cost move u

• Demand remains weak

How it was?

A sharp downward correction in Ingot

prices and weak demand has forced

Re-bar manufacturers to reduce their

prices. Re-bar prices at most of the

mandis’ went down by Rs 100-

1,500/MT. Whereas, Re-bar prices at

Chennai move up by Rs 300/MT. The

demand for finished goods was stil

uncertain as buyers held their

purchase. Also, they are not willing to

pay much.

8/6/2019 SteelMint Indian Steel Weekly Report as on 27 June 11

http://slidepdf.com/reader/full/steelmint-indian-steel-weekly-report-as-on-27-june-11 4/4

4

www.steelmint.com

201-C Rishabh Complex,

M.G Road,

Raipur (C.G)

Phone: +91 90092 22344

Fax: 0771-4048884

E-mail: [email protected]

ABOUT US:

SteelMint Info Services is an ISO 9001:2008 certified Steel Research Company which

provides current prices, news & logistical updates on Steel raw materials (domestic and

international), semi-finished and finished products covering almost all major mandis' in

India along with Steel Long on NCDEX. It helps people take informed decisions, who are

in the business of Steel. The organization’s motive is to provide current prices, market

view, steel news and demand - supply situations at various locations across country; of

iron ore, semi-finished and finished Steel products. The idea is to keep people aware of

what is happening in the world of Steel.

Services offered are:

· Steel Prices

· Steel Reports

· Iron ore prices and related updates /sentiments India /China

· Shipping and Logistics Reports (Freight, Vessel line up, Railway freight)

· Stock levels at different ports of India

Disclaimer

Additional information is available upon request. Information has been obtained from sources believed to be

reliable but SteelMint Info Services or its affiliates do not warrant its completeness or accuracy except with

respect to any disclosures relative to SteelMint and/or its affiliates and the analyst’s involvement with the

issuer that is the subject of the research. Opinions and estimates constitute our judgment as of the date of this

material and are subject to change without notice. Past performance is not indicative of future results. This

material is not intended as an offer or solicitation for the purchase or sale of any item. The opinions and

recommendations herein do not take into account individual client circumstances, objectives, or needs and are

not intended as recommendations of particular products or strategies to particular clients. The recipient of this

report must make its own independent decisions regarding any product or items mentioned herein. Periodic

updates may be provided on industry specific developments or announcements, market conditions or any other

publicly available information.

Use of the information presented here is at your sole risk, and any content, material and/or data presented or

otherwise obtained through your use of the information in the document is at your own risk and you will be

solely responsible for any damage to you personally or your company or organization or business associates

whatsoever which in anyway results from the use, reliance or application on such content material and/or data

and/or information.