strategic analysis of samsung's smartphone product portfolio

TRANSCRIPT

Strategic analysis of Samsung's smartphone product portfolio:Countering the challenge from Chinese competitors A

By

Soo Jin Go

Bachelor of Political Science, Korea University, 2006MBA, Sungkyunkwan University, 2015

MASSACHUSETT" INSTITuTEOF FECHNOL0LGY

JUN 2 4 2015

LIBRARIES

SUBMITTED TO THE MIT SLOAN SCHOOL OF MANAGEMENT IN PARTIAL FULFILLMENT OF THEREQUIREMENTS FOR THE DEGREE OF

MASTER OF SCIENCE IN MANAGEMENT STUDIESAT THE

MASSACHUSETTS INSTITUTE OF TECHNOLOGY

JUNE 2015

@2015 Soo Jin Go. All rights reserved.

The author hereby grants to MIT permission to reproduceand to distribute publicly paper and electronic

copies of this thesis document in whole or in partin any medium now known or hereafter created.

Signature of Author:

Certified by:

Accepted by:

Signature redactedMIT Sloan School of Management

Signature redacted May 8,2015

(I Michael A. CusumanoSMR Distinguished Professor of Management

Thesis Supervisor

Signature redactedU Michael A. Cusumano

SMR Distinguished Professor of ManagementProgram Director, M.S. in Management Studies Program

MIT Sloan School of Management

[Page intentionally left blank]

2

Strategic analysis of Samsung's smartphone product portfolio:Countering the challenge from Chinese competitors

By

Soo Jin Go

Submitted to MIT Sloan School of Managementon May 8, 2015 in Partial Fulfillment of the

requirements for the Degree of Master of Science inManagement Studies.

ABSTRACT

After entering the smartphone era, Samsung has recorded enormous growth in sales

and profits. It developed state of the art hardware technology and introduced innovative

features with its flagship models, the Galaxy S series. While it emphasized high-end product

development to compete with global vendors such as Apple, Samsung expanded its product

portfolio to the affordable segment. In the early stages, this strategy succeeded in increasing

revenues and market share. However, as Chinese vendors emerge in the global mobile device

market, Samsung has struggled to keep its market share in the low-end device markets.

Relatively cheap Chinese devices have attacked Samsung's affordable segment. Samsung's

strategy of utilizing economies of scale and the halo effect from flagship models was not

effective to compete against the price competitiveness of Chinese. Since the dynamic aspects of

competition and the importance of platform are increasing, Samsung needs to build a new

sustainable portfolio strategy integrating its platform service and hardware portfolio.

Thesis Supervisor: Michael A. Cusumano

Title: SMR Distinguished Professor of Management

3

[Page intentionally left blank]

4

Table of Contents

A BSTRACTT ................................................................................................................................................................ 3

Chapter 1: Introduction ...................................................................................................................................... 8

1.1. M otivation................................................................................................................................................8

1.2. Objectives and m ethodology ...................................................................................................... 9

1.3. Sam sung Electronics overview ................................................................................................. 10

Chapter 2: A nalysis of the early sm artphone m arket...................................................................... 11

2.1. M obile devices m arket trend.................................................................................................... 11

2.2. The advent of Chinese vendors................................................................................................. 14

2.3. Sam sung's early sm artphone portfolio strategy................................................................. 15

Chapter 3: Analysis of mid and low-end segments in the smartphone market......................19

3.1. M obile devices m arket trend.................................................................................................... 19

3.2. A scending Chinese com petitors.............................................................................................. 23

3.3. Samsung's portfolio strategy for the mid-end segment................................................. 32

Chapter 4: Recom m endations....................................................................................................................... 38

4.1. N ew challenges in the m id and low -end segm ents............................................................... 38

4.2. Case study - Benchmarking Xiaomi's successful case ..................................................... 39

4.3. Sam sung's lim itations ...................................................................................................................... 41

4.4. Recommendation for Samsung's product portfolio strategy........................................ 42

Chapter 5: Conclusion....................................................................................................................................... 44

References............................................................................................................................................................. 46

5

List of Figures

Figure 1. IT & Mobile Communications Division Revenue and Profit in Samsung.......9

Figure 2. Global Mobile Phone Sales: Smartphone vs Feature Phone 2008-2013 .... 12

Figure 3. Global Mobile Phone Market Share 2007 - 2013............................................. 13

Figure 4. Galaxy S Series Sales Units...................................................................................... 15

Figure 5. Regional Smartphone ASP and Chinese Average Manufacturing Cost........16

Figure 6. Worldwide Smartphone Vendor Market Share 2011.Q1 - 2012.Q1........18

Figure 7. Sales of Smartphones by Region 2013-2018 .................................................. 20

Figure 8. Sales of Smartphones - Developed vs Emerging World .............................. 20

Figure 9. Smartphone Sales Units and ASP Trend ............................................................. 22

Figure 10. Smartphone Priceband Forecast Chart - Units ............................................. 22

Figure 11. Worldwide Smartphone Vendor Market Share 2011.Q3 - 2014.Q4 ......... 24

Figure 12. Smartphone Sales Units of Chinese Manufacturers..................................... 27

Figure 13. Smartphone Market Share in the Mid-end Segment - below $200 ........... 28

Figure 14. Smartphone Market Share in China 2012 - 2014....................................... 29

Figure 15. Mobile Phone Market Share in China 2007 - 2013 .................................... 29

Figure 16. Product Portfolio by Price - Huawei ................................................................ 31

Figure 17. Product Portfolio by Price - ZTE........................................................................ 31

Figure 18. Samsung's Smartphone Market Share by Regions....................................... 35

Figure 19. Operating Margin of Smartphone Manufacturers ........................................ 37

6

List of Tables

Table 1. Worldwide Top Five Smartphone Vendors Shipments, Market Share and

Year-Over-Year Growth 2011-2012............................................................................. 13

Table 2. Samsung and Huawei Low-end Smartphone in 2011....................................17

Table 3. Smartphone ASP Forecast in Region..................................................................... 23

Table 4. Worldwide Top Five Smartphone Vendors Shipments, Market Share and

Year-Over-Year Grow th...................................................................................................... 25

Table 5. Mobile Phone Shipments by Region, 2012 and 2013 ..................................... 26

Table 6. Smartphone Main Components from Chinese Vendors................................. 27

Table 7. Samsung Galaxy S3 Mini, Galaxy S3 and Xiaomi Mi3....................................... 34

Table 8. Samsung Mid-end Smartphone Line-up ............................................................. 36

Table 9. Chinese Mid-end Smartphone Line-up................................................................ 36

7

Chapter 1: Introduction

1.1. Motivation

Samsung Electronics announced an earnings shock in 2014. Its revenue generated

is 206 trillion Korean won and profit is 25 trillion won. This result is called "earnings shock"

because its revenue decreased 9.8% from the previous year and profit decreased almost 32%

from the previous year. Most of the profit decreases are caused by a huge drop of revenues

and profits of the IT & Mobile Communications division. Due to low demand for new

products in the mobile market and keen competition from rivals like Apple's iPhone6, the

IM division recorded a 15 trillion Korean won profit, half of its previous profits. Until this

year, the mobile device business has been in a leading position to make most profits in the

corporation and to raise brand image as a global leading technology company. After

launching Galaxy S in 2010, mobile devices have increased their share of revenue and profit

in Samsung internally (up to 60.7% and 67.8% of revenue and profit, respectively), as well

as in absolute money amounts. The strategy of Samsung to expand its smartphone portfolio

to the low and mid-end range also contributed to increasing its market share as well as

revenues and profits. However, as consumer electronics such as mobile devices are

becoming commodities, price competition increases and the margin is getting lower.

Chinese competitors have diversified the aspect of competition in the past few years. Rising

Chinese companies in the market are intensifying this price war in the entry-level devices

market. In addition, major manufacturers in China have developed mobile communication

technology in order to keep up with multinational players such as Samsung and Apple.

Samsung has struggled to keep its market share in the market, faced with challenges from

8

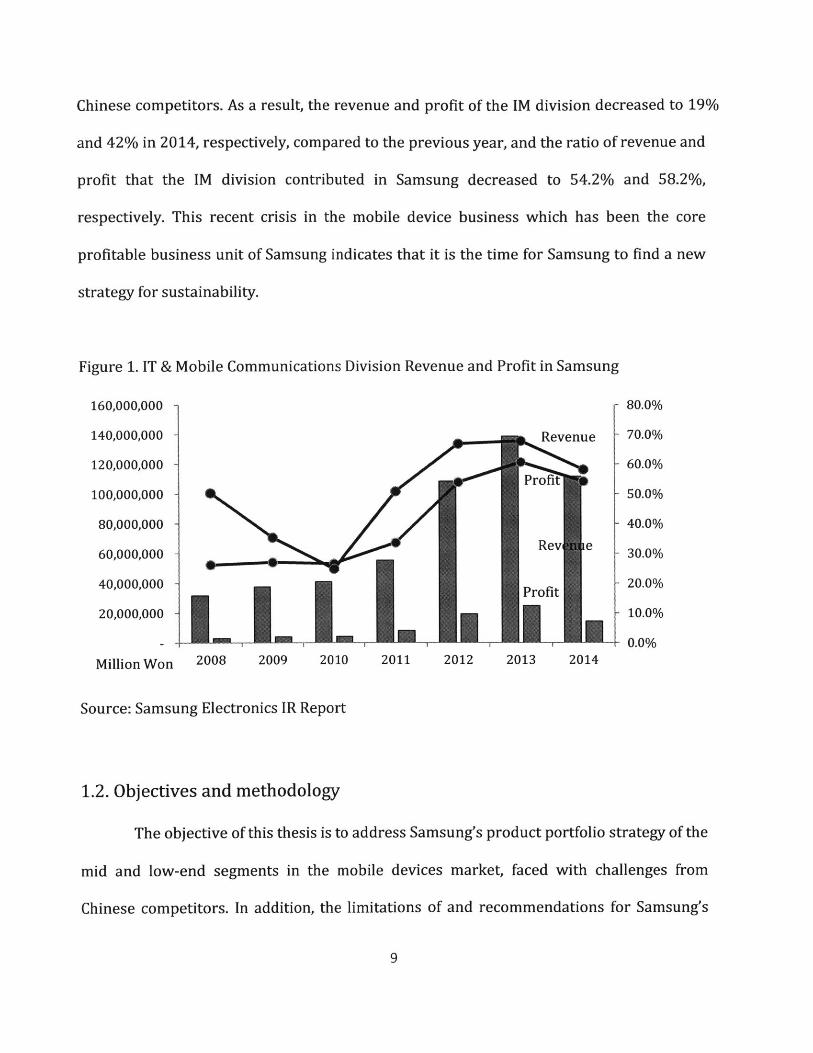

Chinese competitors. As a result, the revenue and profit of the IM division decreased to 19%

and 42% in 2014, respectively, compared to the previous year, and the ratio of revenue and

profit that the IM division contributed in Samsung decreased to 54.2% and 58.2%,

respectively. This recent crisis in the mobile device business which has been the core

profitable business unit of Samsung indicates that it is the time for Samsung to find a new

strategy for sustainability.

Figure 1. IT & Mobile Communications Division Revenue and Profit in Samsung

160,000,000 80.0%

140,000,000 Revenue 70.0%

120,000,000 60.0%

100,000,000 50.0%

80,000,000 40.0%

60,000,000 30.0%

40,000,000 Profit 20.0%

20,000,000 10.0%

- r0.0%

Million Won 2008 2009 2010 2011 2012 2013 2014

Source: Samsung Electronics IR Report

1.2. Objectives and methodology

The objective of this thesis is to address Samsung's product portfolio strategy of the

mid and low-end segments in the mobile devices market, faced with challenges from

Chinese competitors. In addition, the limitations of and recommendations for Samsung's

9

strategy is derived from that analysis. In this research, the change of market trends in this

segment will be reviewed in Chapter 2 and 3. According to the market trends, the case

study includes not only the strategy of Chinese competitors but also the strategies Samsung

has deployed to counter these threats. Finally, the limitations and recommendations for

Samsung's portfolio strategy will be described in the conclusion.

1.3. Samsung Electronics overview

Samsung Electronics Co., Ltd. is a South Korean multinational electronics company.

(Samsung, 2013) It is the world's largest information technology company. The company

achieved a record consolidated net income of US$26.2B on sales of US$ $268.8B in 2013. Its

main products are consumer electronics, IT & Mobile Communications, and device

solutions. It has manufacturing plants and sales networks in 80 countries and more than

370,000 employees around the world. Samsung has a unique organizational structure,

operating 10 independent business units. They are coordinated under three divisions.

Consumer Electronics (CE) consists of visual display, digital appliances, printing solutions,

and health and medical equipment business units. IT & Mobile Communications (IM)

encompasses the mobile communications, networks, and digital imaging business units.

Device Solutions (DS) includes memory, system LSI, and LED. Through relentless

innovations and research, the company has continued its successful growth and enhanced

its brand image in the global market, ranked 7th in Interbrand's best global brands 2014.

Samsung Electronics aspires to create new technologies that inspire the world. To fuel this

innovation, the company operates more than 30 R&D centers around the globe. In 2012, it

10

invested US$10.8B in R&D, with more than 60,000 employees worldwide dedicated to

developing future technologies.

Chapter 2: Analysis of the early smartphone market

2.1. Mobile devices market trend

Before the smartphone era, Nokia occupied a dominant place in the mobile devices

market for over 10 years. Nokia succeeded in transiting to 2G digital technology while

Motorola was clinging to 1G analog technology. (Kim, 2011) By having a strong cost-

efficient platform strategy, SCM, and distribution channel structure all around the world,

Nokia sold various products from high-end PDAs to low-end black and white display

cellphones in huge volumes. However, with the popularization of smartphones in 2009, the

center of gravity of the mobile phone market began to move into the smartphone business.

Steve Jobs announced the first iPhone in 2007 at MacWorld Expo Keynote. Smartphones

had already existed in the mobile phone market like the Nokia Symbian or Blackberry but

the iPhone was the first device offering easy and diversified applications. Apple provided

not only hardware with an operating system but also software with diversified applications.

Consumers could utilize their mobile phones as personal computers with various

applications such as the Safari web browser, E-mail, and navigations. Apple has developed

a digital platform to distribute mobile apps on iOS, allowing third parties to develop

applications with the iOS SDK. Apple opened the App Store on July 10, 2008, and now more

than 1,400,000 applications are available in the app store. (January, 2015) Apple has

recorded tremendous sales and profits every year. Over 500 million units of the iPhone

11

series were sold on March, 2014. This accomplishment took only 7 years after Steve Jobs

announced the first iPhone in 2007. At the same time, Nokia, Motorola, and LG that were

feature phone central firms fell sharply in market share. Nokia failed to transit to a

successful smartphone OS in the global market after the iPhone came out. Apple brought

out a new form of competition, based on software (operating system) as well as hardware

(devices). The two prominent OSs, Android and iOS, are expanding market share drastically

whereas Symbian that was almost the only smartphone OS before is shrinking. Nokia stuck

to the Symbian OS that was less convenient and innovative than iOS or Android.

In 2011, Samsung took the No.1 position from Nokia in the mobile devices market.

According to Gartner data, feature phone sales have decreased rapidly while smartphone

sales started to ramp up at a rapid pace from 2011. The traditional champions who were

stuck in the existing product portfolio lost sales and shares except for Apple and Samsung

who started to expand the smartphone portfolios.

Figure 2. Global Mobile Phone Sales: Smartphone vs Feature Phone 2008-2013

400,000 - -

350,000

300,000Feature Phone

250,000

200,000

Smartphone150.000

100,000

50,000-

1Qo8 4QO8 3Q09 2010 1Q11 4Q11 3Q12 2Q13

Source: Gartner

12

Table 1. Worldwide Top Five Smartphone Vendors Shipments, Market Share and Year-Over-

Year Growth 2011-2012

(Units in Millions)

2012 2012 2011 2011 Year-Over-Vendor Shipment Market Shipment Market Year Change

Volumes Share Volumes Share

Samsung 215.8 39.6% 94.2 19.0% 129.1%

Apple 136.8 25.1% 93.1 18.8% 46.9%

Nokia 35.1 6.4% 77.3 15.6% -54.6%

HTC 32.6 6.0% 43.6 8.8% -25.2%

RIM 32.5 6.0% 51.1 10.3% -36.4%

Others 92.4 16.9% 136 27.5% -32.1%

Total 545.20 100.0% 495.30 100.0% 10.1%

Source: IDC Worldwide Quarterly Mobile Phone Tracker

Figure 3. Global Mobile Phone Market Share 2007 - 2013

40% -36% 36%

35% -2%

30% -

25% -6% % 8% Samsung

20% - 2% 0%

15% - % 6% 1 Nokia

10% - 0 Apple0

5% 0 0 7% % LG0 1%20/ %3% Lenovo

0%

2007 2008 2009 2010 2011 2012 2013

Source: Euromonitor from Trade Sources/National Statistics

13

i MWW- -M-

2.2. The advent of Chinese vendors

The technology to manufacture smartphones in China was developed from a gray-

market (named "Shan-Zhai) in 2007. After the Chinese government removed the policy of

the approbation for mobile phone manufacturing, small-sized vendors started to imitate

well-known smartphones such as iPhone. In addition, these manufacturers provided

unique functions such as mobile TV or dual SIM mode. According to a survey by iSuppli in

2009, they sold 145 million units in 2009, which accounted for 35% of market share in

China. (Liao and Hsieh, 2012)

Big IT companies and OEM vendors in China started to pay attention to the

smartphone market and entered the market in 2011. Huawei and ZTE are global

telecommunications equipment manufacturers, and Lenovo is a global PC maker. Hisense

and TCL are LCD TV production companies in China. They had already built competitive

technology related with the IT and communication fields. In addition, OEM manufacturers

such as Tyenwi, Gionee and OPPO have grown their manufacturing capacity and experience.

Huawei and ZTE built strong relationships with operators, supplying communication

equipment. They possessed technology enough to provide quad-core devices with high

R&D investment as global suppliers of communication equipment. However, weak brand

awareness in the global market made it difficult for them to enter developed countries.

They provided "white box" handsets that Chinese vendors manufactured with operators'

brand names to carriers using strong relationship with operators in order to easily enter

the mobile devices market.

14

2.3. Samsung's early smartphone portfolio strategy

Launching the Galaxy S (19000) in June 2010, Samsung started to develop its

Android smartphone portfolio in earnest. Before Android, Samsung also had Symbian-

based PDAs and smartphone lines. In addition, Windows messaging phones such as the

Black Jack series (i607 and i617) were sold in the business market segment against

Blackberry products. These early smartphone products were positioned in the niche

product segment in Samsung's portfolio at that time. However, the Galaxy S was launched

as a flagship model in 2010. Before the Galaxy S, Samsung launched Omnia I and II,

Windows mobile OS based smartphones in 2008 and 2009, but it failed with customers

harshly criticizing its technical malfunctions.

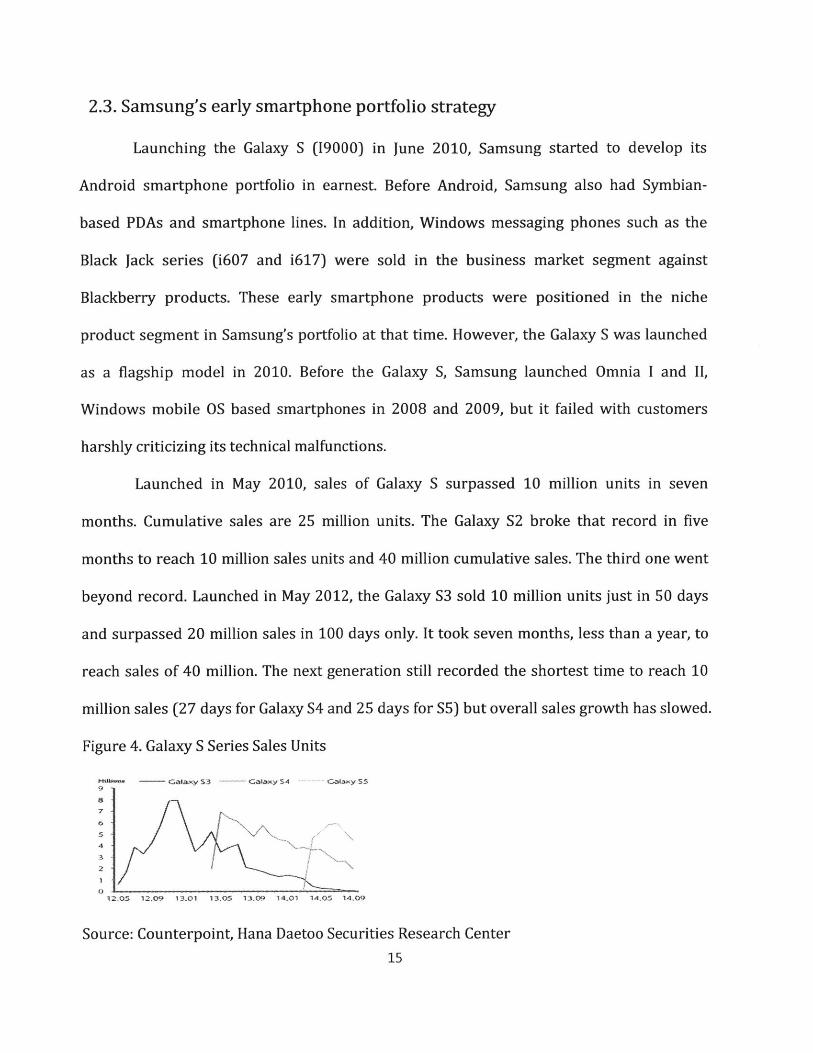

Launched in May 2010, sales of Galaxy S surpassed 10 million units in seven

months. Cumulative sales are 25 million units. The Galaxy S2 broke that record in five

months to reach 10 million sales units and 40 million cumulative sales. The third one went

beyond record. Launched in May 2012, the Galaxy S3 sold 10 million units just in 50 days

and surpassed 20 million sales in 100 days only. It took seven months, less than a year, to

reach sales of 40 million. The next generation still recorded the shortest time to reach 10

million sales (27 days for Galaxy S4 and 25 days for S5) but overall sales growth has slowed.

Figure 4. Galaxy S Series Sales Units

Hikh. G~a~ $3 Galaxy $4 Galaky SS

Source: Counterpoint, Hana Daetoo Securities Research Center

15

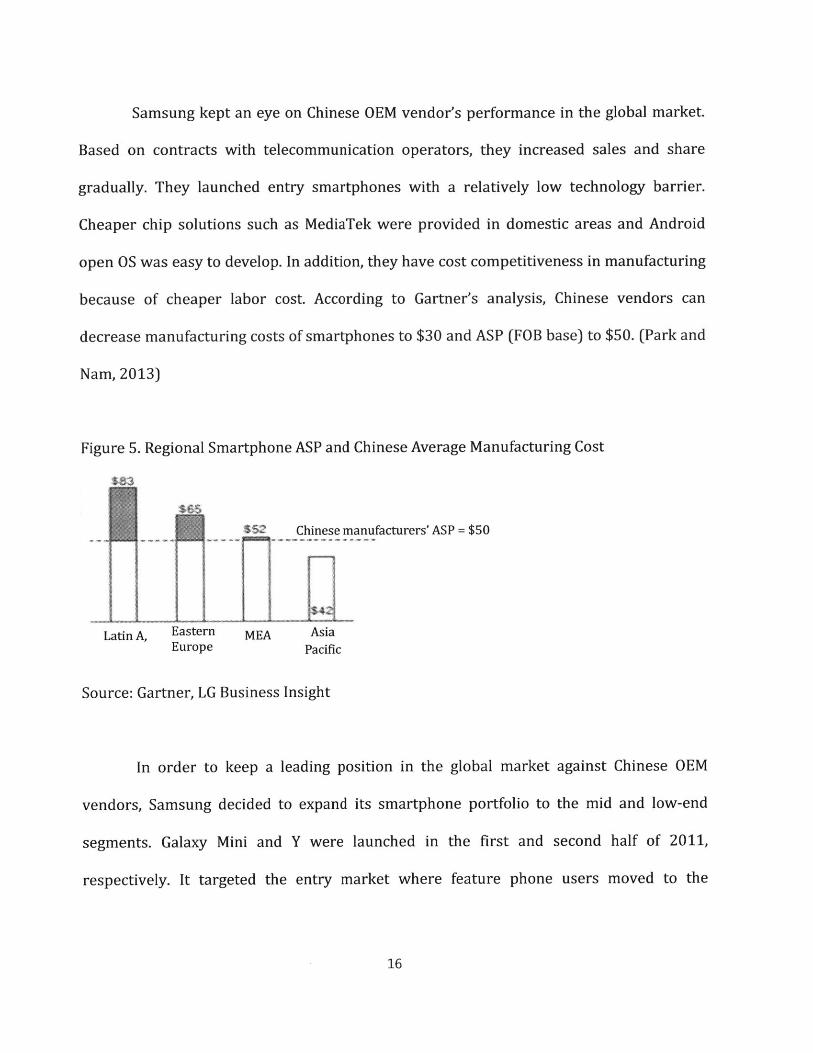

Samsung kept an eye on Chinese OEM vendor's performance in the global market.

Based on contracts with telecommunication operators, they increased sales and share

gradually. They launched entry smartphones with a relatively low technology barrier.

Cheaper chip solutions such as MediaTek were provided in domestic areas and Android

open OS was easy to develop. In addition, they have cost competitiveness in manufacturing

because of cheaper labor cost. According to Gartner's analysis, Chinese vendors can

decrease manufacturing costs of smartphones to $30 and ASP (FOB base) to $50. (Park and

Nam, 2013)

Figure 5. Regional Smartphone ASP and Chinese Average Manufacturing Cost

$ Chinese manufacturers' ASP = $50

Latin A, Eastern MEA AsiaEurope Pacific

Source: Gartner, LG Business Insight

In order to keep a leading position in the global market against Chinese OEM

vendors, Samsung decided to expand its smartphone portfolio to the mid and low-end

segments. Galaxy Mini and Y were launched in the first and second half of 2011,

respectively. It targeted the entry market where feature phone users moved to the

16

smartphone segment for the first time. These products had a smaller display size around

3.0" and basic features for Android OS to match its affordable price.

Table 2. Samsung and Huawei Low-end Smartphone in 2011

Samsung Galaxy Mini Samsung Galaxy Y Huawei U8650 SonicS5570 S5360

Image

Price* $150 $120 $145

Launch 2011.02 2011.10 2011.07

Network HSDPA7.2 HSDPA7.2 HSDPA7.2

3.14" 240x320 pixels 3.0" 240x320 pixels 3.5" 320x480 pixels

Display TFT TFT TFT

Android OS, v2.2OS(FroO), pg l Android OS, v2.3.5 Android OS, v2.3.3

OS (Froyo), upgradable .Gnebed Gnebedto 2. (inerred) (Gingerbread) (Gingerbread)to v2.3 (Gingerbread)

160 MB, 384 MB RAM, 180 MB, 290 MB RAM, 160 MB, 256 MB RAM,Memory microSD microSD microSD

Camera 3.15 MP 2MP 3.15 MP

Battery Li-Ion 1200 mAh Li-Ion 1200 mAh Li-Ion 1400 mAh

Bluetooth, A-GPS, Bluetooth, A-GPS, Bluetooth, A-GPS,microUSB, microUSB, microUSB,

Accelerometer, Accelerometer, Accelerometer,

Etc., Proximity, Compass, Proximity, Compass, Proximity, Compass,

Document Document Document

viewer/editor, viewer/editor, viewer/editor,

Photo/video editor Photo/video editor Photo/video editor

* Price: Retail Price in India and Pakistan

17

This strategy of expanding its portfolio was so successful that Samsung took the

first position in the smartphone market against Apple from 2011. While Apple sold its

iPhone series only in the premium product segment, Samsung provided various products

with a wide range of prices and specifications. With this product portfolio strategy of

providing a wide range of models, Samsung could keep its momentum in the mobile

devices market from the second half of 2011.

Figure 6. Worldwide Smartphone Vendor Market Share 2011.Q1 - 2012.Q1

35 %

30 % 29.1% Samsung

27.0- Others25 %% 24.2% Apple

20 % 18.3

15 % 1&.6%

10% - 8.2% Nokia6.7% RIM

5% 4.8% HTC

0%fo1l 2011 3011 4011

Source: IDC Worldwide Quarterly Mobile Phone Tracker

18

Chapter 3: Analysis of mid and low-end segments in the smartphone

market

3.1. Mobile devices market trend

As the matured market is saturated in developed countries, the emerging market is

becoming a target group for higher margins and volumes. Mobile device manufacturers

have paid attention to the emerging market with more potential customers as a new target

group because demand in developed countries is becoming more restrictive to grow.

According to Counterpoint and Hana Daetoo Securities Research Center, the penetration of

smartphones in developed countries is reaching to almost 88% while the penetration in

developing countries is below 70% of the global average. (Kim, 2014) The developed

market is depending on replacement demand for sales. Therefore, the emerging market is

becoming the main driver in smartphone sales growth. Even though the Chinese market is

expected to show slower sales growth in the long run, the country's vast population will

generate volume growth. (Golovko, 2014) In China and in India, mainly with a younger

generation, a significant number of feature phone users are trying to upgrade to the

smartphone segment. Several vendors are targeting this consumer group who are

interested in the latest technology but with a low budget by providing various models at a

cheaper price. (Pandey and Nakra, 2014)

19

Figure 7. Sales of Smartphones by Region 2013-2018

20

1 8

1 6

1 4

1

1

0

2

6

2013 2014 2015 2016

m Northfka Arnierac3

-u fv1ddl1. East anrd A.truca

2017 2018

mVV4sterrn EjrCope

FotRes-t cpl Ass.

St Rest <>I t"*- WVorsc1

Source: Euromonitor International Passport Consumer Electronics Outlook, Trends and

Analysis (2014, September)

Figure 8. Sales of Smartphones - Developed vs Emerging World

Million

1.8001.600

1.400

1.20

1.000

600

400

200

0

]Devloped.cou

Emer. n

-. -. The ratio of emerging cuntries

Lnutries Countries

80%

70%

60%

50%

40%

30%

20%

10%

0%2008 2000 2010 2011 2012 2013E 2014E 2015E

Source: Strategy Analytics, Hanwha Investment and Securities Co., Ltd Research Center

20

0 4

02

0,0

Therefore, companies are expanding the mid and low-end smartphone lineups for

the consumers with lower purchasing power in the emerging market. According to Strategy

Analytics and Hanwha Investment and Securities Co., Ltd Research Center, with growing

demand in the emerging market, the affordable smartphone market is expecting high

growth. More than 70% of smartphones are expected to be sold in the emerging market

after 2015. According to IDC research, the sales proportion of low-priced smartphones -

below 300 USD - will be about 60% in 2016. Consumers in the mid/low-end segments are

more price-sensitive and have less brand loyalty than premium segment consumers. Until

2011, ASP increased around 5% because hardware was enhanced with higher features in

the developed market. However, from 2011, ASP started to go down with limitations of

hardware innovation. According to Gartner and Hana Daetoo Securities Research Center,

the average selling price of smartphones reached $270 in 2014, down 8% from $293 in

2013. It expects that ASP will be $237 by 2016 with this trend. (Kim, 2014) The research of

Strategy Analytics and Hanwha Research Center expected a similar trend that indicates a

drop in smartphone ASP from 2011.

21

Figure 9. Smartphone Sales Units and ASP Trend

- Sales Unit

2008 2009

"*e ASP

million1.600

1.400

1.200

1.000

600

400

200

02012 2013E 201AE

Source: Strategy Analytics, Hanwha Investment and Securities Co., Ltd Research Center

Figure 10. Smartphone Priceband Forecast Chart - Units

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

$700+

$650 - <$700

$600 - <$650

=$sso-<$600SSOO- <$550

* $4SO- <$500

a S400 -<$450

*$350-<$400

*$300-<$3SO

*$250- <$300

N$200 -<$250

N$150-<$200E $100 - 4150

E$50-<$100

N$0- <$50

2008 2009 2010 2011 2012 2013 2014 2015 2016

Source: IDC Market Analysis Perspective: Worldwide Mobile Phone Market, Dec. 2013

22

2010 2011

360

-340

- 320

-300

- 280

- 260

- 240

- 220

-200ZOSE

0. Ev-

Table 3. Smartphone ASP Forecast in Region

'10 '11 '12 '13 '14(F) '15(F) '16(F)North $402 $411 $435 $424 $399 $375 $346

AmericaWestern $345 $362 $362 $363 $330 $302 $280Europe

Asia $287 $301 $279 $248 $228 $216 $204

Latin $287 $296 $271 $243 $234 $226 $220AmericaEastern $283 $281 $287 $275 $264 $245 $230Europe

MEA $277 $274 $252 $246 $237 $230 $224

Global $329 $334 $319 $293 $270 $253 $237

Source: Gartner, Hana Daetoo Securities Research Center

3.2. Ascending Chinese competitors

From 2012, the global smartphone market has been deployed with competition

between Samsung and Apple, and Chinese vendors are in hot pursuit. Sales and profits of

earlier champions such as Nokia or HTC are slumped while Chinese vendors show a steady

growth trend. Huawei, ZTE, Lenovo, and Xiaomi have come to the front in the global market.

The rapid increase in low-end smartphone sales has driven the growth of these players.

According to Gartner's findings in 2014, Samsung sold 73.2 million smartphones

worldwide during the third quarter of 2014; shipments were down from the 80.4 million in

the third quarter of 2013. While Samsung is struggling, Xiaomi's sales record has risen to

15.8 million units from 3.6 million during the same period. They secured fourth place with

5.2% market share worldwide in the fourth quarter of 2014. (Reisinger, 2014) Chinese

23

vendors, Huawei, Lenovo, and Xiaomi have expanded global market share at around 5%

which is a similar level as LG.

However, this expansion is based on the growth of the Chinese domestic market.

According to CCS Insight, in 2013, the Chinese market increased 76% than in 2012, from

168 million to 296 million. The Chinese smartphone market occupied around 29% of the

global market in 2013, increasing from 23% in 2012.

Figure 11. Worldwide Smartphone Vendor Market Share 2011.Q3 - 2014.Q4

35.0% -

30.0% -

25.0% Samsung

20.0% Apple

15.0% -

10.0% LenovoHuawei

5.0% omi

0.0% -tL11.Q311.Q412.Q112.Q212.Q312.Q413.Q113.Q213.Q313.Q414.Q114.Q214.Q314.Q4

Source: IDC Worldwide Quarterly Mobile Phone Tracker

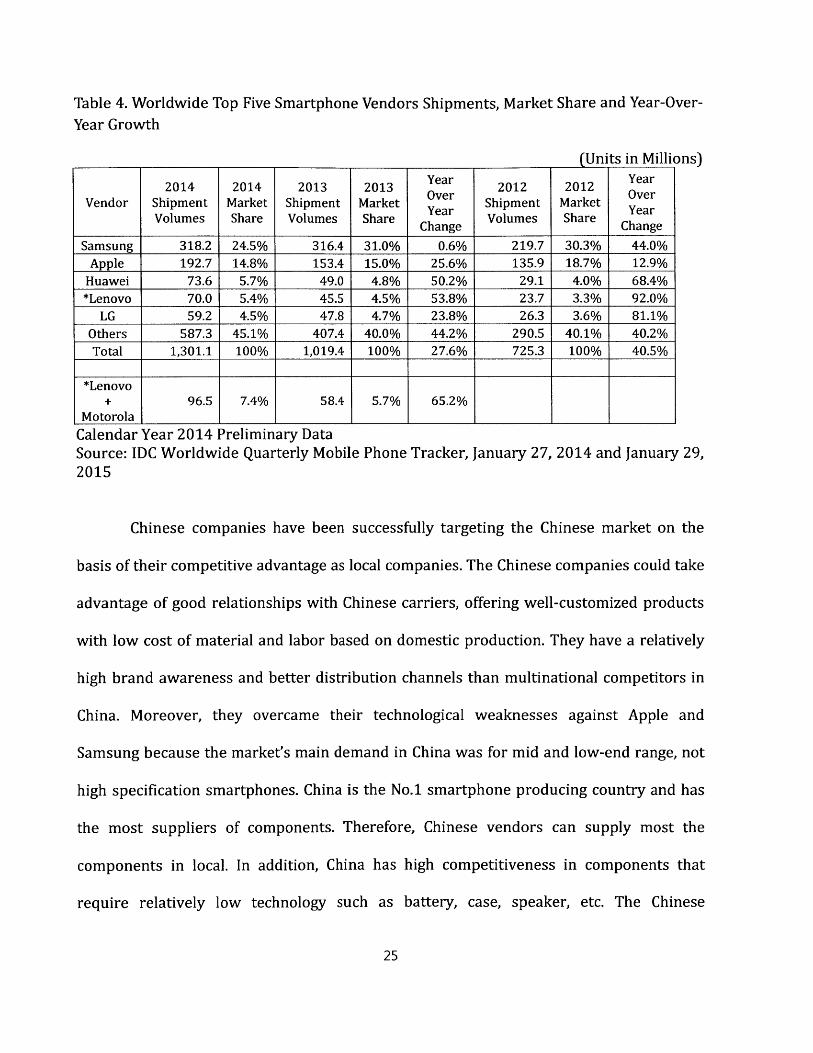

24

Table 4. Worldwide Top Five Smartphone Vendors Shipments, Market Share and Year-Over-

Year Growth

(Units in Millions)

2014 2014 2013 2013 Year 2012 2012 YearVendor Shipment Market Shipment Market Over Shipment Market Over

Volumes Share Volumes Share Year Volumes Share Chag_____Change Change

Samsung 318.2 24.5% 316.4 31.0% 0.6% 219.7 30.3% 44.0%Apple 192.7 14.8% 153.4 15.0% 25.6% 135.9 18.7% 12.9%

Huawei 73.6 5.7% 49.0 4.8% 50.2% 29.1 4.0% 68.4%*Lenovo 70.0 5.4% 45.5 4.5% 53.8% 23.7 3.3% 92.0%

LG 59.2 4.5% 47.8 4.7% 23.8% 26.3 3.6% 81.1%Others 587.3 45.1% 407.4 40.0% 44.2% 290.5 40.1% 40.2%Total 1,301.1 100% 1,019.4 100% 27.6% 725.3 100% 40.5%

*Lenovo+ 96.5 7.4% 58.4 5.7% 65.2%

Motorola 1 1Calendar Year 2014 Preliminary DataSource: IDC Worldwide Quarterly Mobile Phone Tracker, January 27, 2014 and January 29,2015

Chinese companies have been successfully targeting the Chinese market on the

basis of their competitive advantage as local companies. The Chinese companies could take

advantage of good relationships with Chinese carriers, offering well-customized products

with low cost of material and labor based on domestic production. They have a relatively

high brand awareness and better distribution channels than multinational competitors in

China. Moreover, they overcame their technological weaknesses against Apple and

Samsung because the market's main demand in China was for mid and low-end range, not

high specification smartphones. China is the No.1 smartphone producing country and has

the most suppliers of components. Therefore, Chinese vendors can supply most the

components in local. In addition, China has high competitiveness in components that

require relatively low technology such as battery, case, speaker, etc. The Chinese

25

government has expanded its supporting policies and investment for the mobile device

business and communication technology. China has decided telecommunication and

information industry as the main industry to enhance competitiveness in the global market.

It organized the "IMT-2020 Promotion Group" in February 2012 in order to develop 5G

technology. (Kim, 2014)

Table 5. Mobile Phone Shipments by Region, 2012 and 2013

Total Smartphones

FeaturePhones

Total Smartphones(%)

FeaturePhones

(Units in Millions)Growth in 2013 1

Smartphones

North 201 127 74 201 157 44 0% 24% -41%America (15%)Latin 174 68 106 180 90 90 3% 32% -15%America (9%)Western 183 119 64 184 144 40 1% 21% -38%Europe (14%)Eastern 111 44 67 114 57 57 3% 30% -15%Europe (6%)MEA 279 76 203 297 107 190 6% 41% -6%

(10%)Asia Pacific 776 301 475 859 472 387 11% 57% -19%

(46%)China 337 168 168 385 296 89 14% 76% -47%

(29%)India 213 43 170 240 65 175 13% 51% 3%

(6%)Developed 92 63 29 94 73 21 2% 16% -28%markets (7%)Emerging 135 27 108 140 38 102 4% 41% -6%markets (4%)

Total 1724 735 989 1835 1027 808 6% 40% -18%

Source: CCS Insight

26

2012 Shipments 2013 Shipments

Total FeaturePhones

Figure 12. Smartphone Sales Units of Chinese Manufacturers

800

Units (millios)

600

0

Source: Gartner

Table 6. Smartphone Main Components from Chinese Vendors

China/Taiwan SuppliersMemory

Semi-Conductor RA/RF

System on Chip MediaTek, Spreadtrum, Hisilicon,System___nChipLeadcore, RockchipCamera Module Sunny Optical, Truly, BYD, Lite-on Tech

Display Truly, Tianma, BYDE, BOETouch Panel 0-film tech, Truly, TPK, Wuhu token

Components PCB Kingboard, Goworld, CompegAcoustic AAC, GoerTek, GettopBatteries BAK, BYD, Scud

Source: Morgan Stanley

27

Figure 13. Smartphone Market Share in the Mid-end Segment - below $200

2013.09 2014.09

Huawei,6%

Nokia, LG, 6%Nokia, Alcatel, Lenovo, Nokia, Lenovo,7% 7% 4% 7%

Source: Gartner

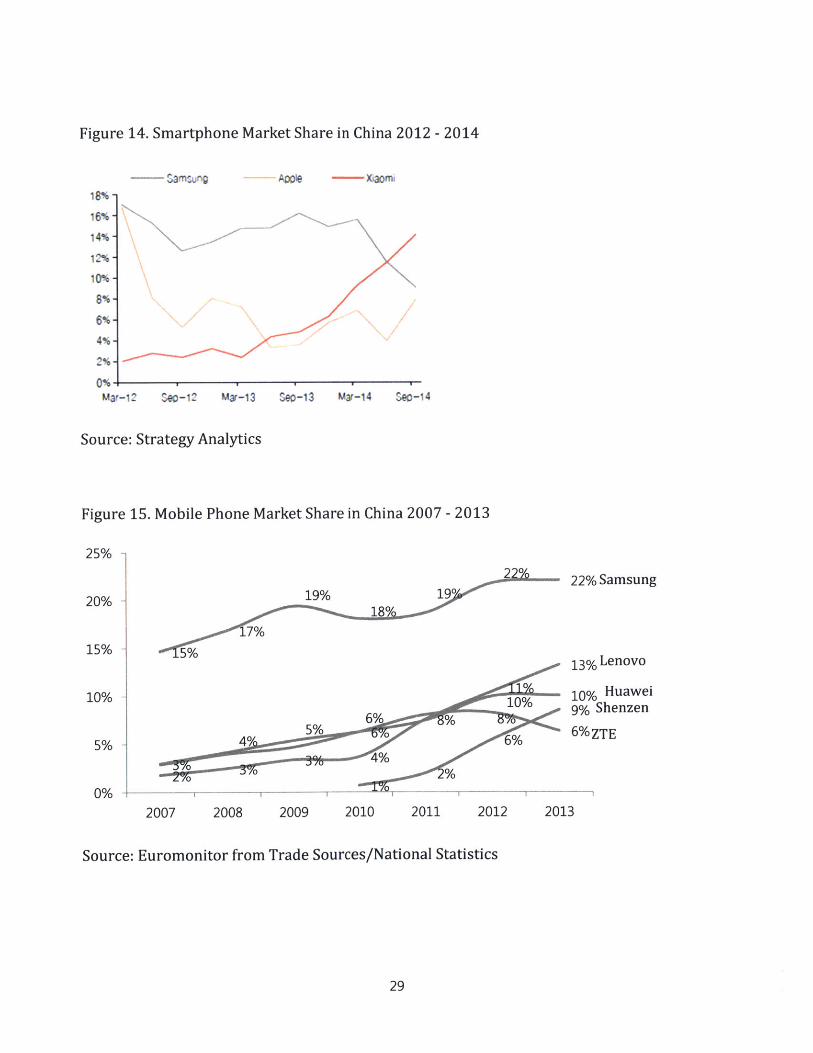

In the third quarter of 2014, Samsung's market share in China plunged to 9%,

compared to 16% in 2013. Top Chinese brands such as Xiaomi, Lenovo, and Huawei

increased sales with aggressive promotion of high-end smartphones at low-price. The

average selling price of Chinese vendors is $ 100, whereas ASP of Samsung is $393 and

Apple's is $688. Looking at the Chinese market and Chinese companies, Chinese

manufacturers occupied 76% of market share in the Chinese smartphone market in the

first half of 2014 whereas multinational companies including Samsung, Apple and Nokia

took 57.3% of market share in 2011. Eight out of the top 10 companies are Chinese ones.

These companies are rapidly taking into the market share of foreign companies. (Kim, 2014)

28

Figure 14. Smartphone Market Share in China 2012 - 2014

SSamseur Axile - aomi

x

N

Mar-14 Seo-14

Source: Strategy Analytics

Figure 15. Mobile Phone Market Share in China 2007 - 2013

25% -

29% 1922% Samsung

20% -198 9

15% 1 5%

2007

13% ~1%Lenovo

10% Huawei9% Shenzen

6%ZTE10/o

6%%5% Vc

40 4%* %O

2008 2009 2010 2011 2012 2013

Source: Euromonitor from Trade Sources/National Statistics

29

18%-

16%-

14%-

12%-

10%-

8%-

6%-4%-

2% -

Mar-12 seo-12 Mar-13 Seo-13

10% ~

5% -

U0O +-----

Qualitative innovation for smartphones is almost reaching the limit while

quantitative growth of devices and services continues. Chinese followers are closing the

technology gap with leaders such as Samsung and Apple since smartphone technology is

becoming standardized. Even Apple launched a lower cost model, the iPhone 5C, because of

market pressure. In addition, Chinese vendors have grown in technology innovation at a

rapid pace while Samsung and Apple have gone through a slowdown. For example, Huawei

developed its own AP (application processor). OPPO had the first smartphone with a 50

million pixels camera and Xiaomi launched the thinnest smartphone (5.5mm). By

developing their own technology, they started to expand their product portfolio from low-

end to mid-range models. Huawei established a production plant for premium products

and expanded M&A with European semi-conductor companies in order to secure high-end

technology. It has invested 14.2% of revenues in R&D in 2014 which was twice as much

as Samsung's R&D spending ratio of 6.4%. Even though Samsung spent more than twice

Huawei did on R&D ($13.4B, $6.6B, respectively), the relative numbers to overall revenue

implies that Huawei is focusing on developing technology first. Huawei's investment in

R&D even exceeds Apple's R&D spending, which was recorded at $6B in 2014, 3% of

annual revenue. Lenovo acquired Motorola in 2014 and expanded R&D and production in

Wuhan. It also bought the NFC patent from NEC Japan.

30

Figure 16. Product Portfolio by Price - Huawei

2013.10

$400- S500

1300-1400

$200 -$300

$100 -$200

$100 uxder

0% 10% 20% 30% 40%. 50% 60%

Source: Counterpoint, Hana Daetoo Securities

Figure 17. Product Portfolio by Price - ZTE

2013.10

5400-S500

$300 -$400

$200-S300

$100 -200

Sl00 under

1400- $500

1300-5400

1200-$300

1100-1200

S100 under

0% 10%

Research Center

1400-S500

5300-S400

1200-S300

1100-1200

$100 under

2014.09

0% 10% 20% 30% 40%

Source: Counterpoint, Hana

50% 6M% 7ft 0% 10% 20% 30% 40% 50% 60%

Daetoo Securities Research Center

Xiaomi reduced its prices through direct online distribution to end consumers.

Xiaomi provided high-end smartphones at half the price of Apple and Samsung at around

300-400 USD. Therefore, its amount of sales in China increased 15.8 million units in the

third quarter of 2014, from 3.6 million units of the same quarter in 2013. Xiaomi became

31

2014.09

20% 30% 40%

M

the best smartphone seller in China with 14% market share. It has captured the attention of

early adaptors using its distinguished marketing strategy and unique operating system,

imitating Apple's.

The commoditization of smartphone is leading the high volume growth in an

emerging market. The next target countries are India, Middle Asia, and Africa as China has

led market growth for a couple of years. These are the lowest income countries so price

competition would be fiercer causing worse profit for the whole industry. (Song, 2014)

Samsung's profit has decreased from the third quarter in 2014 and Chinese high-end

brands such as Lenovo and Huawei started to go through a slowdown in volume growth.

Even though sales units increased overall, operating profit of most main players decreased

significantly because of dropping ASP and increasing marketing costs. In order to expand

market share and secure enough profit, Chinese manufacturers are starting to pay

attention to potential in other regions.

3.3. Samsung's portfolio strategy for the mid-end segment

Given the more intense competition in the mid and low-end segments, cost

competitiveness is determined to be a more important issue. 60% of smartphone

components in Samsung are provided by internal production. This vertical integration in

production costs can be taken advantage of via aggressive pricing. One of the Samsung's

strengths is large and diverse manufacturing base. (Loo, 2015) Samsung occupies several

affiliates related to components of mobile devices unlike competitors who outsource most

components to third parties. It has 6 manufacturing plants only for mobile devices around

the world, including Korea, China, Vietnam, India and Brazil. These factors allow to

32

Samsung establish economies of scale and control costs. Samsung outperformed with good

quality and price competitiveness by R&D investment and mass production system at

product maturity stage rather than leading innovation at the early stage. It provided a wide

range of smartphones with various specifications and prices.

Samsung launched the "Mini Series" in 2012. Galaxy III Mini was a sub brand of

Galaxy S III. It had a similar platform and design identity as the flagship model, but had

lower specifications such as smaller display and lower camera resolution. It was aimed to

take a halo effect from the flagship model. This strategy that utilized derived products

applied a strong brand image and power of expansive products to less expensive items.

This lower price product was targeted to make consumers have same image and

expectations as the Galaxy S III by utilizing a powerful brand image. It was aimed at

satisfying two consumers' expectations: price and product functions.

33

Table 7. Samsung Galaxy S3 Mini, Galaxy S3 and Xiaomi Mi3

Samsung 18190 Samsung 19300 XiaomiGalaxy III Mini Galaxy S III Mi3

Image

Price $341 $699 $327

Launch 2012.11 2012.05 2013.12Network HSPA14.4/5.76Mbps HSPA21.1/5.76Mbps HSPA42.2/5.76Mbps

4.0" 480x800 pixels 4.8" 720x1280pixels 5.0" 1080x1920pixelsDisplay sAMOLED sAMOLED IPS LCD

Android OS, v4.0.4(Ice Android OS,OS OS, Cream Sandwich), v4.3(JellyBean),

4.3(JellyBean) 4.4.2 (KitKat)

Memory 8/16GB, 1GB RAM, 16/32/64GB, 1GB 16/64GB, 2GB RAMmicroSD RAM, microSD

Camera 5MP+VGA 8MP+1.9MP 13MP+2MP

Battery Li-Ion 1500 mAh Li-Ion 2100 mAh Li-Ion 3050 mAh

1.4GHz Quad-core 2.3GHz Quad-core Krait

1GHz Dual-core Cortex-A9, 400, Accelerometer,Cortex-A9, Accelerometer, Gyro, Gyro, Proximity,

Etc., Accelerometer, Gyro, Proximity, Compass, S Compass, Fast battery

Proximity, Compass Voice language charging: 60% in 30commands and min (Quick Charge 2.0)

dictation

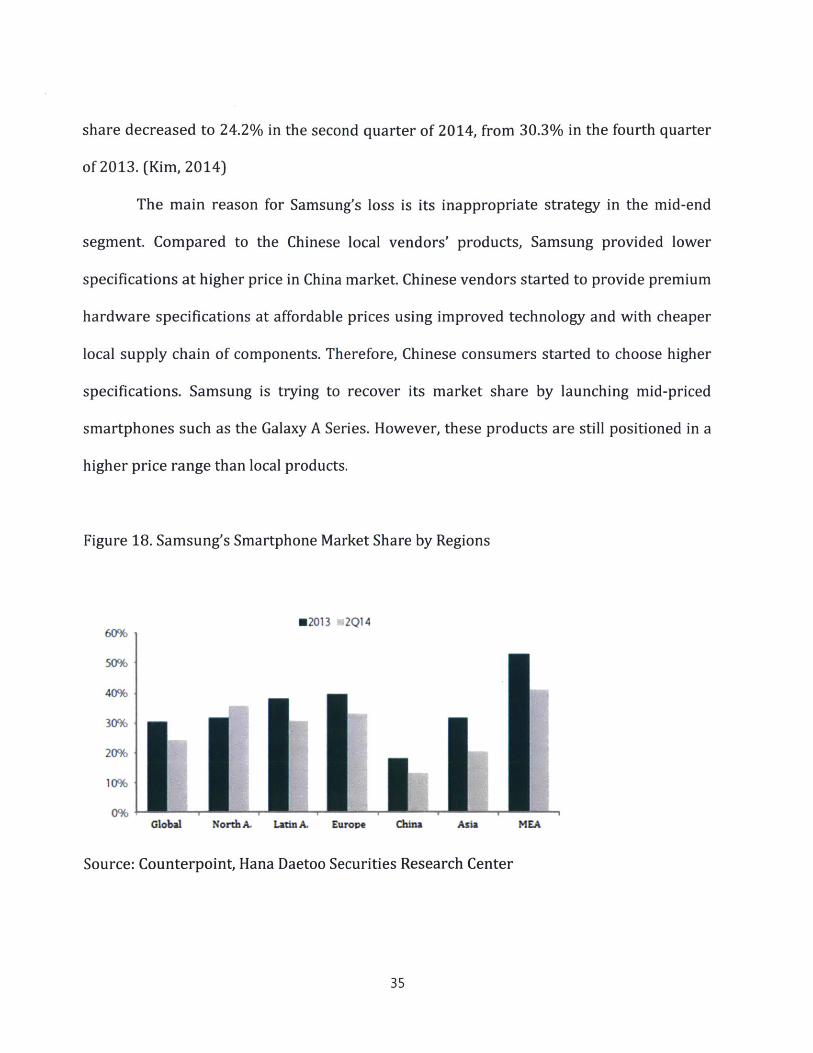

However, Samsung lost significant market share in 2014. Samsung was a solid No.1

player in every region except North America. Furthermore, it had more than a 20% point

gap with the second player except in China. However, it dropped to the second position in

China with 0.1% point gap with Xiaomi and the market share decreased in every region,

especially more than 10% points in the emerging markets. Therefore, its global market

34

share decreased to 24.2% in the second quarter of 2014, from 30.3% in the fourth quarter

of 2013. (Kim, 2014)

The main reason for Samsung's loss is its inappropriate strategy in the mid-end

segment. Compared to the Chinese local vendors' products, Samsung provided lower

specifications at higher price in China market. Chinese vendors started to provide premium

hardware specifications at affordable prices using improved technology and with cheaper

local supply chain of components. Therefore, Chinese consumers started to choose higher

specifications. Samsung is trying to recover its market share by launching mid-priced

smartphones such as the Galaxy A Series. However, these products are still positioned in a

higher price range than local products.

Figure 18. Samsung's Smartphone Market Share by Regions

*2013 %2Q1460%

50%

40%

30%

20%

10%

0%Global NorthA. Latin A. Europm China Asia MEA

Source: Counterpoint, Hana Daetoo Securities Research Center

35

Table 8. Samsung Mid-end Smartphone Line-up

Galasy S Duos 3 Galaxy Ace 4 Galaxy Core 2 Galaxy Young 2

Image

Price $140 $270 $215 $120. 121.4x62.9x10.8 121.4x62.9x10x9.109.8x59.9x11.8Dimension 130.3x68x9.8 mm

mm mm mmWeight 124g 123.8g 138g 108g

AP 1200 MHz 1000 MHz 1200 MHz 1000 MHzCore/ Dual Core Quad Core Single Core

Chipset DulCrRAM 512MB 512MB 768MB 512MB

Display 4.0", 480x800 4.0", 480x800 4.5", 480x800 3.5", 320x480Camera 5M + VGA 5M + VGA 5M + VGA 3.15MBattery 1500mAh 1500 mAh 2000mAh 1300 mAh

Source: Hana Daetoo Securities Research Center

Table 9. Chinese Mid-end Smartphone Line-up

ZTE Blade L2 Huawei Honor 3C Xiaomi Mi 1S Lenovo A850+Play

Image

Price $140 $95 $130 $150

Dimension 142.5x72.2x9mm 142.2x72.3x9.4m 137x69x9.9mm 150x77x8.9mmm

Weight 166g 156g 158g 161gAP 1300 MHz 1300 MHz 1600 MHz 1400 MHz

Choset Quad Core Quad Core Quad Core Octa Core

RAM 1GB 1GB 1GB 1GBDisplay 5.0", 480x854 5.0", 720x1280 4.7", 720x1280 5.5", 540x960Camera 8M or SM +VGA 8M + 2M 8M +1.6M SM + VGABattery 2000 mAh 2000 mAh 2000 mAh 2500 mAh

Source: Hana Daetoo Securities Research Center

36

The fierce competition in the mid and low-end smartphone segment would be

expected to lead Samsung to a chicken game of losing its own profit, like in the semi-

conductor industry. Therefore, the success of lower price range smartphones depends on

creating other added values besides prices. (Song, 2014) Samsung's operating margin of

the IM division in 2014 dropped significantly to 13%, compared to 18% in 2013. The main

reason was lower sales records of the Galaxy S5 and the rise of mid-priced smartphones in

China. (Song, 2014) The Mini Series was also affected by poor reputation of the flagship

model. It showed that losing the leading position in mid-priced segment brings about a loss

of profits.

Figure 19. Operating Margin of Smartphone Manufacturers

30%

20%

0%

-10%-

-20%-Mar-

Samsung -A00e - Huawei

- Lenv - ZE- C0010ad

TCL

08 Mar-09 Mar-10 Mar-11 Mar-12 Mar-13 Mar-14

Source: Strategy Analytics

37

I

Chapter 4: Recommendations

4.1. New challenges in the mid and low-end segments

Recently, Chinese vendors are turning their attention to other markets out of China.

Xiaomi started to sell products in Singapore from 2014 and announced its launch in the

Indian market. In 2014, 6 Chinese players entered the Indian market. Lenovo launched 12

models in India from 2013, providing a wide price range of products from 4,000 to 36,000

rupees. The Middle East and Africa is another big emerging market for these vendors.

According to IDC research, the number of smartphones sold in Q3 2014 was up 300% year

on year. 40% of total handset shipments which reached 64 million units in Q2 2014 are in

the smartphones category. The leading countries are mostly GCC (Gulf Cooperation Council)

members such as UAE, Saudi Arabia, Turkey, and Kuwait but more developing countries in

sub-Saharan Africa are following the smartphone market growth at a rapid pace. The

primary factor is the extremely low-cost of devices from Chinese vendors. The main

Chinese vendors such as Huawei and Lenovo already entered this market and offered more

affordable devices than Apple and Samsung. According to IDC research, Huawei recorded

second place in the smartphone market, jumping its market share from 2% to 10% in Q2

2014. Samsung still remains the concrete leader with 45% market share but is struggling to

keep its position with 8% points market share drop from a year ago. (Shetty, 2014) In

addition, local brands outsourcing their phones from the production catalogues of

independent manufacturers in China have worked well with better functions but at much

lower prices than the main players. Tecno in Nigeria and Kenya is an example whose

smartphone shipments were up 269% year on year in Q3 2014. (Shetty, 2015)

38

Besides aggressive Chinese competitors, traditional players are preparing to start

over in the market. Nokia with Microsoft announced three mid-range segment devices on

September 4, 2014: Lumia 830, Lumia 730 Dual SIM, and Lumia 735. With high-end

specifications, 5" display, 10 megapixel camera, and LTE connectivity, Lumia 830 was

positioned in the mid-range price range, -E330/US$430. The others are clearly more

affordable than Lumia 830: Lumia 730 Dual SIM retailing at E199/US$257 and the Lumia

735 at E219/US$283D. (Llamas, 2014) For the entry market, Nokia launched the X series in

2014. The Nokia X retails at 89 euros and features a 4" touchscreen and a 3MP camera. The

Nokia X+ increases the memory and storage and raises the price to 99 euros. Finally, the

Nokia XL brings a 5" touchscreen and a front-facing 2MP camera for 109 euros. (Llamas,

2014) Surprisingly, Nokia utilized Android OS for lower specification and price. Nokia

targets the below $150 smartphone market, where 322.6 million units were sold

worldwide in 2013.

4.2. Case study - Benchmarking Xiaomi's successful case

Xiaomi's strategy is distinctive from other Chinese vendors. It gives up profit from

hardware, so provides well-featured smartphones at significantly low prices. Instead of

hardware sales, Xiaomi pursues profit from content and services. Its ultimate goal is

becoming a contents and services provider like Amazon, Google, or Facebook. Xiaomi has a

plan to expand its product portfolio to TV and home appliances in order to lock in more

users to its own eco system. Xiaomi's smartphones are still under the Android platform, but

Xiaomi created a unique and attractive user experience. Lei Jun, the founder and CEO of

39

Xiaomi, created a custom ROM in open source Android, named MiUI. MiUI has MiCloud, a

web storage service and MiTalk, a cross platform web-based messaging system. (Golovko,

2014) Xiaomi's user experience through MiUI, MI, aims at consolidating software,

hardware and services of all home appliances. By active discussion with Xiaomi product

users, Xiaomi has developed user-friendly features on its platform. After achieving

popularity with MiUI, he made a bet on a low-price and high-volume strategy in the market.

The price range is almost half of Samsung and Apple with similar specifications, so it could

capture first time smartphone users in China. As soon as they experienced Xiaomi's UX,

consumers became big fans of Xiaomi smartphones. Xiaomi spent little money for

marketing activities, depending on word of mouth and online direct distribution. Xiaomi

provides added value for consumers besides price. Therefore, Xiaomi has quickly emerged

as one of the largest smartphone manufacturers in 2014. This success comes from an

integrated strategy between hardware and platform. Xiaomi created a user friendly

platform which was transformed from Android and attracted consumers by affordably

priced high feature hardware. Although it has achieved most of the current success in China

where the government restricts Google and Android and supports Chinese platforms, the

next movement to foreign markets is expected by confirmed platform and product strategy

from millions of customers.

40

4.3. Samsung's limitations

Samsung has made an attempt to enhance its software competitiveness. However,

Samsung is evaluated as a hardware manufacturer, experiencing the failure of launching its

own operating system, Bada. Bada was an operating system based on Linux, mainly

developed by Samsung and Intel. Samsung initiated this development to target the

integration of a wide range of devices including smartphones, tablets, TVs, PCs, and other

consumer electronic appliances. This project started as LiMo (Linux Mobile) Foundation in

2007 and changed its name to Tizen Association in 2012. Samsung launched the Wave

series based on the Bada OS from 2009. However, it failed to expand its share in the

smartphone OS category and was absorbed into the Tizen project in 2013. Samsung

launched only two wearable smart watches with Tizen. However, without launching

hardware devices which is the core of mobile eco system, application developers cannot

help leaving the system, and vice versa.

In addition, Samsung established the MSC (Mobile Solution Center) in 2008 to

encourage development of content and services. It opened the "Samsung Mobile Innovator"

website for third parties to develop mobile software in October 2008. (Kim and Rhee, 2011)

In this website, application developers around the world shared ideas and were supported

to commercialize applications in "Samsung Apps". Furthermore, Samsung tried to secure

contents by strategic cooperation with contents providers such as Warner Brothers and

Universal Studios. The early strategy was to provide cross device contents to differentiate

products from Nokia. Samsung tried to expand its consumer range by providing compatible

contents to mobile, TV, laptop, and so on. However, Samsung considers software as

complementary to selling more hardware devices. The management level in Samsung

41

evaluated that content and services business can play a supporting role for making

hardware business as well as software business sustainable. Apple created a business

model of value added virtuous circle where device and content supports dramatic growth

in the market for each other. Looking at Apple's case, Samsung defined that the

sustainability of contents and services business had the capability to influence growth of its

core business continuously and repetitively. However, as a traditional hardware

manufacturer it faced high risk in jumping into a new business with high fluctuations.

Therefore, Samsung obtained contents by cooperation with contents providers instead of

developing them itself. Therefore, Samsung made an alliance with Google and became the

best contributor of Android's success.

4.4. Recommendation for Samsung's product portfolio strategy

Currently, more than hardware sales, contents and services are becoming the main

source of big revenue and profit. (Loo, 2015) As in Apple's success, controlling software is a

key factor of the company's success these days. Many successful companies in the IT

industry possess platforms in the eco systems like Google and Apple. Apple has established

a concrete ecosystem to seize power over content and services in the applications market.

Apple provides convenient SKD, a Software Development Kit and 70% of revenue per share

for application developers to lure them to join iOS spontaneously. (Kim and Rhee, 2011)

Apple succeeded in securing 1.4 million kinds of unique application software, two practical

online shops (iTunes music store and Apple App store) and simple operating systems (OS X

for Mac and iOS for iPhone and iPad) for customers.

42

There is an opportunity for Samsung to develop another OS in order to provide

more value for consumers. Xiaomi's success (MiUI) shows a good example of how to

circumvent the Android OS. Samsung has accumulated enough technology development

and experience of trial and error in the software business. Samsung can offer a distinctive

value using its core competency: convergence. Samsung needs to develop Tizen as an

operating system to unify multiple devices including mobile, TV, home appliances, and so

on. Samsung is perhaps the only manufacturer that is able to build this convergence eco-

system because it has all business divisions including consumer electronics, IT & mobile

communications, and device solutions. It has already settled mass production sites, R&D,

and distribution channels around the world. Using massive resources, Samsung can

develop a convergence OS easier than other competitors. This economy of scale also

supports its strong hardware strategy integrating price and marketing. Established high-

end technology and mass production can elaborate its marketing strategy to attract more

consumers in the ecosystem. Therefore, Samsung can create its own eco system and retain

its leadership in the fierce competition.

43

Chapter 5: Conclusion

Samsung has occupied the No.1 position in the global market just after its transition

to the smartphone portfolio. Apple is the only rival in this specific segment and its

distinguished product portfolio strategy which offers a wide range of products and has

succeeded in increasing sales units and revenues. However, the smartphone market

saturation is causing a shift towards low cost competition. Samsung needs to find a new

strategy to sustain its revenue growth. The war in the mid and low-end segments against

Chinese competitors is totally different from the war with Apple. Upon the same operating

system which is open for everyone, Samsung should attract more customers by very

limited differentiating points. What is worse, competitors have strength in price

competitiveness, which is the most important point for consumers of this segment.

Furthermore, as soon as they dominate the low-end market, Chinese competitors started to

encroach on premium segments with competitive prices, which is Samsung's main source

of share and profits. They aim to increase profits by securing a strong market position and

expanding product sales in the premium segment which has a higher operating margin. In

the premium segment, Samsung has led market growth using its own advanced technology

and alliance with Google against Apple. In this competition, Samsung should not offer just a

cheaper version of flagship models to low-end segment consumers like the Mini Series

because other competitors are providing smartphones with premium specifications at

relatively affordable prices. The key for Samsung is to find added value for consumers

besides price. How to build a strong power over platform and software is a key strategy for

the new competition. From the recent successful case of Xiaomi, Samsung needs to spread

44

its own ecosystem to consumers to confirm its competitive edge with attractive product

marketing strategies.

Faced with new challenges from various competitors, Samsung is showing that it

focuses on the original core competency. Galaxy S6 and S6 Edge emphasize the state of the

art technology of Samsung. The launching show in Barcelona pointed to strong competition

with Apple directly. However, it cannot ignore the enormous potential of the emerging

market and the mid and low-end segments. It is certain that Samsung is preparing for a

new takeoff in the smartphone market. Samsung is expected to show another success by

making the right strategic decision.

45

References

Danova, Tony (2013, August 20), Smartphones finally outsold feature phones in the global

market, Business Insider Australia

Golovko, Mykola (2014, September), Consumer electronics: outlook, trends and analysis,

Euromonitor International passport

Golovko, Mykola (2014, October), Beijing Xiaomi Co Ltd., in consumer electronics (world),

Euromonitor International passport

iSuppli. (2009), Cell phone industry's dirty little secret: China' 145 million unit gray market,

Retrieved from http://www.isuppli.com/china-electronicssupply-

chain/news/pages/cell-phone-industrys-dirty-little-secretchinas-145-million-unit-

gray-market.aspx

Kim, Dongwoo (2011, September 2), Changes and implications of the mobile phone market

competition, KB financial group Inc., industry report

Kim, Heesung, Oh, Jusik, Jeong, Hongsik, Seo, Younghi (2013, July 30), The golden age of

mid-low end smartphone and tablet PC's, Hanwha investment and securities Co., Ltd

research center, Hanwha morning brief

Kim, Jiyeon and Rhee, Dongkee (2011, April 20), The strategy of Samsung Electronics'

smartphone business: with managements' consideration for sustainability, The

journal of professional management

Kim, Jongki (2014, May 15), Global prospects and implications of Chinese smartphone

industry, Korea Institute for industrial economics & trade

Kim, Roko (2014, November 4), The trend and outlook of mobile device industry analysis in

2015, Hana Daetoo research center

46

Liao, Chun-Hsiung and Hsieh (2012, May), Determinants of consumer's willingness to

purchase gray-market smartphones

Llamas, Ramon T. (2014, February 24), Storming the Beach: Nokia Brings Open Source

Android to Entry-Level Smartphones, IDC Press Release

Llamas, Ramon T. (2014, May 28), Smartphone Momentum Still Evident with Shipments

Expected to Reach 1.2 Billion in 2014 and Growing 23.1% Over 2013, IDC Press

Release

Llamas, Ramon T. (2014, September 4), Microsoft Attacks the Mid-Range Smartphone

Market with Affordability and Capability, IDC Press Release

Loo, Wee Teck (2015, January), Passport: Samsung Corp in consumer electronics (world),

Euromonitor International

Pandey and Nakra (2014, November), Consumer preference towards smartphone brands,

with special reference to Android operating system

Park, R and Nam, H (2013, June 5), Analysis of Chinese mobile device manufacturers: from

local market to global market, LGERI LG Business insight

Reisinger, Don (2014, December 16), Xiaomi soars while Samsung sinks in Gartner

Smartphone Market Study, eWeek

Samsung in coordination with Cheil Worldwide and ICGroup (2013), Samsung profile 2013

Shetty, Anulekha (2014, October 13), Smartphones set the pace as MEA handset sales top

64 million units in Q2 2014, IDC Press Release

Shetty, Anulekha (2015, January 19), MEA smartphone market booms as 4G LTE shipments

to GCC grow 400%, IDC Press Release

Song, Eunjung (2014, November 11), The prospect of mobile device industry in 2015 - the

47

industry impact analysis of low-end smartphone below 100 USD, Hi investment &

securities research center industry report

48