stubbornly persistent factor migrations with rapid international economic convergence*

TRANSCRIPT

STUBBORNLY PERSISTENT FACTOR MIGRATIONS WITH RAPID INTERNATIONAL ECONOMIC CONVERGENCE*

HARRY CLARKE

La Trobe University

A model of persisting labour and capital migrations is proposed which relies on capital installation adjustment costs. Labour and capital markets are supposed internationally integrated with free factor movements imposing a ‘law of one price’ on the gross return to each factor. The development of infrastructure and other capital projects however is accompanied by adjustment costs that create a divergence between the gross and net returns to capital. This makes it optimal to accumulate capital only gradually. Thus, although there is rapid international economic convergence because returns on traded assets and labour are internationally determined, labour and capital immigrations persist. The consistency of this model with some stylised facts of experience is examined using data for four high factor immigration economies from 1870-1991.

I. INTRODUCTION

This paper examines the influence of capital adjustment costs on labour and capital market factor trades and economic development in an optimising, open economy growth model. Because of liberal labour immigration laws it is supposed that wages in this economy are kept pegged at international levels through endogenous adjustments in immigration. However, concerning capital inputs, even though there is perfect capital mobility so gross rental costs of capital (costs inclusive of adjustment costs) are similarly equated to international capital costs, capital installatioris are supposed to involve substantial installation and adjustment costs. Therefore the capital installations, which determine labour demands, proceed only gradually through time so that flow demands for both labour immigrants and capital imports remain finite.

At the same time it is the returns to internationally-traded inputs that dominate aggregate factor incomes. Since these returns are internationally determined, convergence in living standards between factor source and factor destination economies is rapid. In short, even though factor migrations persist in the longer term, international income convergence is observed to be rapid and factor price convergence instantaneous.

These broad features of development experience are consistent with some ‘broad brush’ characteristics of the development experience of high factor immigration countries and particularly Australia. For example, in his revisionist economic history of Australia. Sinclair (1976) argued that, from the 1820s to the 1920s, two capital market characteristics had a dominant influence on economic development:

First, there were capital adjustment costs associated with installing capital, developing infrastructure, transportation networks and so on in newly emerging Australia. Sinclair stressed the way adjustment costs constrained the development of an internal transportation system which in turn limited growth possibilities by creating obstacles to the installation of other new capital.

* I thank Rodney Maddock, Peter Stemp and an anonymous referee for their helpful comments. The views expressed however are mine.

236

1996 PERSISTENT FACTOR MIGRATIONS WITH RAPID INTERNATIONAL ECONOMIC CONVERGENCE 237

Second, there were capital supply restrictions amounting to supply inelasticity. Such inelasticity can be accounted for similarly to adjustment costs since their primary effect was to delay capital installations so as not to bid up capital’s effective supply price.

Sinclair argued it was capital supply limitations reflecting adjustment costs - not restrictions on labour supply as conventionally supposed - which conditioned Australian development. A detailed historical argument provided by Sinclair backs a primary emphasis on the role of capital adjustment costs in conditioning Australian development experience.

Apart from the primary role of capital constraints, there is evidence supporting the view that factor price and real per capita income convergence have been more rapid in high factor migration countries than commonly supposed. Some of this evidence is reviewed below in Section 111 but it is important to understand that the general argument here is not inconsistent with earlier research as well. Thus Pope and Withers (1993) show that labour immigration to Australia did not depress real wages from 1861 to 1913 and, at the same time, emphasise the close links between UK and Australian wages. These findings are consistent both with rapid wage convergence and the view that immigration would exert no discernible effects on wages because of labour market integration. Labour immigration would not depress Australian wages if flows merely endogenously adjusted to equate wages in Australia with those in the ‘Old World’.

Regarding capital markets there is now persuasive evidence of extensive long-term capital market integration even in the 1880s: see Zevin (1992).

Other empirical evidence (Clarke and Martin, 1995) suggests that dependence on foreign savings has had extraordinary persistence in Australian, Canadian and US settings. This evidence shows the various current account deficits and nominal GNPs were cointegrated from 1861-1992 suggesting gradualism in capital inflows as development unfolded. These authors also showed that GNP per head in Australia and the UK were cointegrated over the satne period suggesting rapid overall economic convergence. Both of these empirical findings are primary consequences of the present theoretical modeling. Some of this latter evidence is reviewed below in more detail as well as other indirect evidence. Moreover, evidence is reviewed not only for Australia but other high labour immigration countries (and one high emigration country) as well.

The model presented clearly contrasts with alternative views of historical experience whereby gradual factor market integration lead to gradual economic convergence. There are of course many reasons advanced in the literature for ongoing factor immigrations. Maasey el (I/. (1993) discuss networkmg, institutional, cumulative causation and system theories all of which can rationalise the perpetuation of immigration. None of these explanations however simultaneously imply that labour will accompany capital flows and that there will be rupid international economic convergence.’

For the most part the present analysis considers net capital and labour imniigrcltions rather than net capital and labour emigratioris. However. this is to make the exposition as simple as possible. It is easy to account for emigrations and in several places (and particularly in a penultimate empirical section where UK experience is referred to) this is done explicitly.

I One argument for continuing labour migrations is that one country has a more rapid population growth rate than another. This is a dubious theory since labour destination countries have typically experienced high natural population growth rates than emigration countries. This material is reviewed in Clarke ( 1996b). Clarke and Smith (1996, forthcoming).

238 AUSTRALIAN ECONOMIC PAPERS DECEMBER

A disclaimer is appropriate here. The present paper is exploratory and broad brush - more work is needed to firm up the framework’s usefulness. Formal testing of the adjustment cost model is izof attempted in this paper - only indirect evidence is provided showing model consistency with stylised facts. No attention is paid to the way the composition of migration has evolved or to the role for the major demand fluctuations that seem inconsistent with simple neoclassical theorising. If economic historians are led to scrutinise the facts more carefully and economists are encouraged to entertain the possible interpretative relevance of the model then the paper’s main objective will have been achieved.

11. THE MODEL

An initial population of L ( 0 ) worker-shareholders (‘the initial settlers’) in a small open economy own equity in an economy-wide firm. The firm uses internationally traded capital and labour and some non-internationally traded fixed factors such as land. The population of worker- shareholders lives forever and does not increase by natural population growth.2 The total available workforce changes endogenously (and monotonically) through time either (i) through labour immigrations to be L ( t ) > L(0) at time t or (ii) through labour emigrations to be L ( t ) < L ( 0 ) at t . International labour migrations clear international labour markets at each time 2.

The worker-shareholders appoint managers to operate the firm to maximise profits in a competitive international market. The manager’s tasks are to arrange capital installations and labour employment to maximise the market value of the firm.

Investment I adds to capital stocks at a constant cost q per unit. Alternatively disinvestment of existing capital stocks can be achieved by selling off stocks at their per unit value q. Capital installations or the sale of installed capital assets at rate I are supposed to incur capital adjustment costs C ( I ) that take the form of an ‘evaporative’ diminution of output. Following Eisner and Stroltz (1963), Could (1968) and Lucas (1967) it is supposed that such costs are increasing and convex with

C ” ( I ) > 0 and C”’(0) = 0 (Ib)

The supply of labour is assumed perfectly elastic at the going real international wage with additional required workers arriving costlessly as immigrants.

The firm manager then selects investment and labour supply time paths to maximise the present value of output accruing to shareholder-workers. Assuming (as we do) that domestic saving is small relative to capital inflows, positive net investment can be identified as a capital imports so. with the assumption of fixed local labour supplies. all additional factors of production are supplied in international markets. The task of the manager is to

2 This assumption is convenient. It could be replaced by the equivalent assumption that agents have finite lives with replacement fertility and perfect intergenerational altruism. This latter would need to be coupled with the assumption that assets are traded at correctly anticipated market values. Allowing for exogenous growth in the domestic labour force would complicate the story marginally because labour shortages would then not be met entirely from immigration as we now assume.

1996 PERSISTENT FACTOR MIGRATIONS WITH RAPID INTERNATIONAL ECONOMIC CONVERGENCE 239

max)'exp(-Gt){F(L.K)- w ( L - L (0 ) ) -q l -C( I )dr ] 0

with d K l d t = 1. K ( 0 ) = KO ( 3 1 )

Here 6 is the discount rate (taken as the international interest rate) and the value of traded final output is unity. F is the production function which is implicitly dependent on fixed natural resource stocks and \+J is the exogenous international wage (assumed constanl).

(PI) here is the discounted value of output accruing to the initial settlers. (?a) are the capital stock dynamics while (2b) expresses the condition for labour market equilibrium: the marginal product of labour must equal the real international wage. Since labour inputs can be changed with zero adjustment costs (2b) defines the equilibrium level of employment i n labour markets given capital stocks: It means that wages locally will be at pegged international levels via equilibrating international factor movements.

Solving (2b) for L yields

where G ' = dC1dK = -FLKIFLL > 0 and G,, = dG1dw = llFL, < 0

if. a\ is always assumed, labour and capital are complementary input&.'

Then the Hamiltoninn relevant to problem (P1) can be written

where capital's shadow price. Z. is a continuous costate for which

and where (2a) holds. Taking the time derivative of (6) and ,ubxtituting from ( 5 ) and (6) to eliminate Z

With labour market clearing at the exogenous international wage

1 This relation formalixs Sinclair's view of labour supply as a function of capital inflow: w e Sinclair ( 1 976, p. 9).

240 AUSTRALIAN ECONOMIC PAPERS DECEMBER

In the steady state where I = 0 and hence where there are no capital installation costs

where K' is the Golden-Rule capital intensify. Taking a first-order Taylor series approximation to (7) and coupling it with (2a) we have

dKldt

where p = (FLLFKK - FLK2)/FLLC" is negative if, as conventionally assumed, FLL < 0 and the numerator of this expression is positive.

The eigenvalues 1 of the linearised system are

6 f $ 2 - 4p a = 2

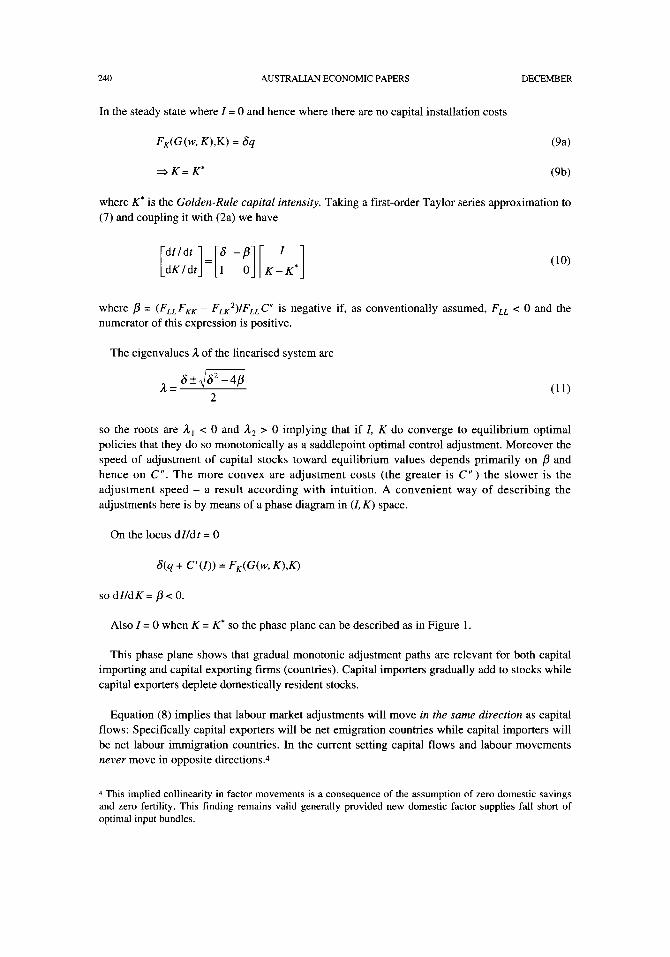

so the roots are A , < 0 and A2 > 0 implying that if I, K do converge to equilibrium optimal policies that they do so monotonically as a saddlepoint optimal control adjustment. Moreover the speed of adjustment of capital stocks toward equilibrium values depends primarily on p and hence on C". The more convex are adjustment costs (the greater is C " ) the slower is the adjustment speed - a result according with intuition. A convenient way of describing the adjustments here is by means of a phase diagram in ( I , K) space.

On the locus d Ild t = 0

so dlld K = p < 0.

Also I = 0 when K = K' so the phase plane can be described as in Figure 1.

This phase plane shows that gradual monotonic adjustment paths are relevant for both capital importing and capital exporting firms (countries). Capital importers gradually add to stocks while capital exporters deplete domestically resident stocks.

Equation (8) implies that labour market adjustments will move in rhe same direction as capital flows: Specifically capital exporters will be net emigration countries while capital importers will be net labour immigration countries. In the current setting capital flows and labour movements never move in opposite directions.''

4 This implied collinearity in factor movements is a consequence of the assumption of zero domestic savings and zero fertility. This finding remains valid generally provided new domestic factor supplies fall short of optimal input bundles.

1996 PERSlSTENT FACTOR MIGRATIONS WlTH RAPID 1NTERNATlONAL ECONOMIC CONVERGENCE 231

L

FIGURE 1 Phase plane in I, K space

For the case of a net immigration country the long-run comparative static effects of increased real source country wages are easy to sort out. Such increased wages drive up wages in the labour migration destination country reducing long-run equilibrium capital demands there. With capital market equilibrium

From (2b) and (3) we have

and increased wages (indicating higher labour productivity) imply higher capital intensities.

Therefore, at each time wages are determined internationally and domestic capital return5 (net of capital adjustment costs) are equal to the shadow price of capital (via (6)). In the steady state wages and capital returns (FK/q ) remain at international levels so, with factor price equalisation and equivalent production possibilities in source and destination countries, provided that returns to non-traded factors are a minor part of aggregate incorne.5 per worker incomes will also converge to international levels.

5 In a diversified multiproduct world even returns to the non-internationally traded factor will be equalised if trade substitutes for factor mobility via Hecksher-Ohlin-Snmuelson ‘factor price equalisation’ : see e . ~ . Woodland (1982). The assumption made can be thought of as an approximation to this result.

242 AUSTRALIAN ECONOMIC PAPERS DECEMBER

Take as an example the specific instance of a Cobb-Douglas production technology with a fixed resource asset (e.g. land) R

where lower case letters denote parameters between zero and unity. From (8)

d L l d t - b dKldt L 1 - u K

so proportional labour force growth is some constant fraction of proportional growth in capital stocks. The latter grows at a finite rate so rates of labour force change are also bounded.

While the model presented is simple its implications capture several important features of some factor source and factor destination economies over the last hundred years or so, namely:

Long-term evidence of substantial (if imperfect) labour market integration; Long-term evidence of substantial per capita income convergence; The persistence of capital and labour immigrations in the face of factor and income

A tendency for positive correlation between capital and labour immigrations through time. convergence;

This last feature is not an inevitable consequence of the joint mobility of capital and labour. For a high wage country with production specialised in a single capital intensive output, capital and labour inputs can achieve international factor price equalisation via a labour inflow or via a capital outflow. Then factor movements are substitutes with movements in one type of input reducing incentives for the other input to migrate in the opposite direction. In our formulation however the factor flows inevitab[y move in the same direction and hence act as complements.

We now examine evidence for high factor immigration countries concerning these stylised facts.

111. EVIDENCE

Are major stylised factor migration facts consistent with the theoretical model analysed? Direct tests of the model are impossible since direct evidence on adjustment costs is unavailable. Indirect tests can be devised by proxying the role of adjustment costs. This merely involves inserting rates ofchange of inputs into production functions6 although in the present context this would call for an intractable reformulation of the core model. Moreover such a reformulation raises in itself a host of identification problems relating to the source of lagged effects of investment demands. This is a task beyond the present scope and is not attempted.

For the most part instead we draw on data bases compiled in Clarke (1996b), Clarke and Smith (1996) and Williamson (1991). The high labour immigration countries considered are Australia, Canada and the United States. The single high emigration country considered is the United Kingdom. The period of investigation is from about 1870 to 1991.

6 A recent set of estimated investment demands using this approach is Shapiro (1986). This includes an extensive bibliography.

I W 6 PERSISTENT FACTOR h l l G R A T l O N S WITH RAPID INTERNATIONAL EC0NC)hllC CONVERGENCt 243

There are two stylised facts relevant to these economies that are not consistent with the niodel presented and hence which require comnient.

I . While real international wages are constant in the model the evidence drawn on shows wages exhibiting secular increase. This can be understood using an extended model where international wages are exogenously driven by technical progress. resource discoveries and the aggregate effects of global labour immigrations on source country labour niarheth. The previous multi- period optimisation task then is interpreted as determining current capital and labour demands period-by-period given static international wage expectations. Wligc c ~ u r i ~ r ~ y c ~ r i c c is then defined to mean wages in different countries show converging trends. Rtrpicl wci,ge cor i i~crg~~ricc~ is interpreted strictly to mean wages in different countries are highly contemporaneously correlated. /rzco/iie co/icer-gcrzce (and mpid i//co/rie c~uii~~rgerrc~~) is defined analogously.

Accounting e.qdicit/j for technological change and so on generates ;I messier and less tractable model but with identical qualitative conclusions with respect to international factor flows.

7. As mentioned the model downplays natural population increase and the role of' domestic savings. In examining relations between capital inflows and immigration. this does not matter provided that domestic savings and natural population growth do not exceed domestic input requirements. This has typically been the case for countries like Australia m d Canada but. for the United States. domestic savings has sometimes exceeded requirements. Then the strict relation we forecast between capital and labour imports can break down ~ capital c;ui be exported at the same time that immigration is proceding because of labour market shortages. This qualification - important as i t is -does not impinge directly o n the results to follow.

a) Wtrge c'oril'ergc~fzce

Figures 2-4 show trend$ i n real wages i n Australia. Canada and the US compared to those i n the UK from 1870-1991. Here the Williamson (1991) data is used. Wage levels in different countries are not expressed in comparable units s o we can only assess relaiive long-term trend behaviour. There are fairly close contemporaneous correlations in a11 cases up to the 1920~7 and fcx Canada this high correlation continues through to 1950. For Australia i t per. through to about 1975.

While these correlations are consistent with yc,nvis t in,g wage differentials the more plausible explanation i s that r q d r\~r ,yc ' c.oriver-ger/w occui~ed over the indicated subperiods. Williamson ( 1991) describes the interval 1870-1913 as 'four decades of clrumatic convergence' that accords with this view.

That convergence was not rapid 1920 in some cases (for Canada and the UK. the US and the CJK some wage diwrge/icie.s developed) is consistent with the idea that European migration to the New World decreased rapidly in importance after this time: see Clarke ( l996b). Clarke and Smith (19%). Also UK wages after 1975 seem to increase too rapidly - th i s may reflect an overvalued UK currency rather than persistent real (purchasing power parity adjusted) wage divergence.

244 AUSTRALIAN ECONOMIC PAPERS

500

g 400

300 a 2 200 100 w- -

FIGURE 2 Real wages in Australia and the UK 1870-1991

DECEMBER

FIGURE 3 Real wages in Canada and the UK 1870-1991

1996 PERSISTENT FACTOR MIGRATIONS WITH RAPID INTERNATIONAL ECONOMIC CONVERGENCb 245

FIGURE 4 Real wages in the US and the UK 1870-1991

b) Income convergence

Figures 4-6 show trends in real per cupitu incomes in Australia. Canada and the US relative to the UK using data prepared for Clarke (1996b). Clarke and Smith (1996). The period covered is 1870-1991. No attempt was made to standardise units so levels are not internationally comparable. The evidence for simple convergence however is strong for most of the entire

The only significant divergence observed is during the period 1570- 1890 when per. cupita incomes in Australia grew significantly out of trend with UK figures. It is often argued that Australian per capita incomes were very high over this period because of the effects of the gold discoveries in the 1850s: see Butlin (1962). Sometimes Australia’s economic performance over the subsequent century is criticised because its relative advantage over this period has diminished. The chart suggests that even if this view is correct must of the convergence back to UK per capita income levels had occurred before 1895. Subsequently Australia has simply followed income trends elsewhere.

These findings, while consistent with the theoretical analysis, have stronger implications. Efficiency in international labour markets implies strong wage convergence but only income convergence in the longer term. The empirical results above supported the hypothesis of strong wage convergence over the long term but empirically income convergence is observed to obtain not only in the steady state but also instantaneously. Thus there is evidence of strong income (as well as factor price) convergence.

The simple correlations over the entire 122 year period 1870-1991 were: 0.97 (Australia-UK). 0.99 (Canada and UK) and 0.99 (US-UK).

246 AUSTRALIAN ECONOMIC PAPERS DECEMBER

12 500 ?c

9 400 5 300 8 a 8

2

a ol

u

a

+.’ .3

42 .3

200 g 100 5 !&

FIGURE 5 Real GNP per capita in Australia and the UK 1870-1991

FIGURE 6 Real GNP per capita in the US and the UK 1870-1991

FIGURE 7 Real GNP per capita in the US and the UK 1870-1991

19Yh PERSISTENT FACTOR MIGRATIONS WITH RAPID INTERNATIONAL ECONOhlIC C O N V E R G E N C L 217

By not correcting for exchange rate differences the implicit assumption is purchasing power parity and the ‘law of one price’ - this is likely an appropriate assumption i n the v e n long-run. However. even after correcting the income series above for exchange rate movements much the same conclusions resulted. Movements in income estimates then however displayed implausibly high short-run variation so results are not discussed here.

O n e possible contr ibut ion to s t rong income conve rgence resul ts is the obse rved pseitdocorii’eI‘Yeri(.C in living stiundards which occurs when measured GDP per head is used to describe welfare change in a competitive economy subject to labour immigrations: see Clarke ( 1996a).9

c) Pcwisterice of jactor. tnove/iitvits

That labour immigration movements tend to persist i s widely analysed i n the literature: For a survey of theoretical explanations not relying on adjustment costs see Mnssey et c r l . ( 1993. pp.448-454). Very rapid periods of labour immigration hcrve occurred (Australia in the 1850s and Canada after 1900) but for most countries labour immigration has an extended history. The substantial U S and UK labour immigrations persisted from 1850 to 1920 while the substantial Australian and Canadian immigrations have (except for the inter-war period) continued through to the present time. Much the same observation can be made regurdinp capital outflows: the UK remained a significant international supplier of capital for much of the period 183-0-1913. Australia and Canada have remained significant capital importers throughout most of their recorded histories.

These facts while consistent with various other explanations are also not inconsistent with an adjustment cost explanation.

c ) CLlpitiil-luDoitr.J[~~~, corri~~ler~ic.rittii-ir?.

The positive association between capital flows and labour immigrations suggesting factor flow complementarity has been analysed at length in Clarke ( 199613). Clarke and Smith (1996) and Clarke and Martin (1995). It is unnecessary to replicate the details of these arguments here. The main features of the indicated association are that:

For Australia there is a close positive association between capital inflows and immigration over the entire period 1861-1991. The simple correlation between the variables from 1870- 1991 is r = 0.32 that is reasonably high given the vast period covercd. data inadequacies and massive structural change.

For Canada the association is positive and dramatically close. From 1870-1991 the simple correlation between capital inflow rates and immigration rates is I’ = 0.72.

Y Labour immigrations are associated with welfare gains for hoth prrrvisting residrnts and nrwcomers alike i n competitive economies for ‘gains-from-trade‘ rciisons. Thus welfare rise with lahour immigrations occur. However since not all inputs are increased hy lahour immigration per c . q > i / u GDP wi l l fall wrongly suggesting a welfare hll. For further discussion see Clarke (1996~).

DECEMBER 248 AUSTRALIAN ECONOMIC PAPERS

For the US over the entire period 1870-1991 there is a relatively weak positive relationship between the respective inflow rates.

For the UK there is a very close positive association between capital oufjlows and emigrations from 1870-1913 ( r = 0.46) when very large factor outflows occurred.

For each of Australia, Canada and the UK there is causality evidence that ‘capital chased labour’ over the period 1870- 199 1.

To sum up, with the possible exception of the US there is considerable evidence of a sustained positive relation between capital flows and international labour movements as predicted by the adjustment cost model.

IV. CONCLUSIONS

The model of capital and labour migrations presented is simple. In many ways it is little more than a restatement of basic adjustment cost models used in analysing investment decisions within competitive firms. Yet the model is consistent with some stylised facts of history. The model is also consistent with a dynamic, episodic view of immigration history that reflects the facts.

In brief, the analysis supports the view that labour and capital migrations persisted for very long periods because of adjustment costs associated with installing capital. These factor migrations ensured rapid wage and income convergence between countries.

Not all immigration and convergence history can be explained in such a simple framework. The change in immigration composition to countries like Australia from traditional ‘old world’ sources toward newly industrialising Asian countries is something calling for a richer theory. Also while short-term variability of immigration flows due to business cycle fluctuations can be rationalised as due to technological shocks this is a strained explanation because of its neglect of aggregate demand. These deficiencies ernphasise the provisional and exploratory nature of the present framework.

Further work along the lines suggested could deal explicitly with natural population growth and with the contribution of domestic savings to investment supply. The role of technical progress could also be modelled to rationalise secular wage and income increase. Endogenising technical progress by making it depend on capital stock or learning-by-doing could produce steady state growth even in per capita variables thereby generating results which are both more theoretically satisfying and empirically relevant.

1996 PERSISTENT FACTOR MIGRATIONS WITH RAPID INTEIWATIONAL ECONOMIC CONVERGENCE 219

REFERENCES

Butlin, N.G. ( 1962). Austrulitrrr Domestic Product, Irrivstrnerrr ( i d Foreign Borrovting (London: Cambridge University Press).

Clarke. H.R. ( 1996a), ‘Labour Immigrations and the Pseudoconvergence of National Living Standards’, mimeograph.

Clarke, H.R. ( 1996b). ‘UK Labour Emigrations and Capital Exports 1816-1991’, Orterriutional Migration, forthcoming.

Clarke, H.R. and Martin. V. (1995). ‘Does Capital Chase Labour Internationally’?’ Papers and Proceedings of the AicstrnlidNevv Zeulnrid Economic History Society Conference, University of Melbourne. 31 March 31-2 April.

Clarke. H.R. and Smith. L. ( 1996). ’Labour Immigration and Capital Flows: Long-Term Australian, Canadian and United States Experience‘. Inrernutionul Migration Rt7iieit.. forthcoming.

Eisner. R. and Stroltz. R.H. ( 1963). ‘Determinants of Business Investment’. bizpacrs o fMone tav Policy (New Jersey: Englewood Cliffs).

Could, J.P. ( 1968). ‘Adjustment Costs in the Theory of Investment of the Firm’, ReiBiew of Economic Studies, vol. 35, January.

Lucas, R.E. (1 967). ‘Optimal Investment Policy and the Flexible Accelerator’, Internccrional Economic Reiie~t , vol. 8, February.

Massey, D.S., Arungo, J., Hugo, G., Kouaouci. A., Pellegrino, A. and Taylor, J.E. (1993). ‘Theories of International Migration: A Review and Appraisal’, Poptclatron arid Development Review, vol. 19. no. 3, September.

Pope, D. and Withers, G. (1993). ‘Wage Effects of International Migration in the Late Nineteenth Century: The Australian Case’. mimeo.

Shapiro, M.D. (1986), ‘The Dynamic Demand for Capital and Labour’. Quarterly Journal of

Economics. vol. 101, no. 3.

Sinclair, W.A. ( 1976). The P roccss of Econornic Development in Australia (Melbourne: Cheshire).

Williamson, J.G. (1991). ‘The Evolution of Global Labour Markets in the First and Second World Since 1830: Background Evidence and Hypotheses’. Hurvard Institute of Economic Research Discussion Paper Number 157 1. Harvard University, Cambridge. Massachusetts.

Woodland, A.D. ( 1982), Intertiutional Trcidc. and Resource Allocrrtion (Amsterdam: North Holland, Publishing Co.).

Zevin, R.B. (1992), ‘Are World Financial Markets More Open’? If So Why and With What Effects?’ in T. Banuri and J. Schor (eds). Firzariciul 0ptvine.s.~ und National Autonomy (London: Oxford University Press).